Integration

Sept. 4, 2024

What is “integration” and why does it matter?

What is integration?

Many businesses raise capital by selling securities in registered offerings or in exempt offerings. Many offerings have limitations and conditions on their use, such as the amount a company may raise over a 12-month period or how and when the company may reach out to investors.

If a company offers or sells securities in reliance on different offering pathways in parallel or in close time proximity to one another, questions can arise as to whether the offerings should be viewed as one “integrated” offering for purposes of analyzing whether the offering complied with securities laws.

Why does integration matter?

If a company attempts to structure multiple offerings with different limitations and conditions, but those offerings are assessed as one integrated offering, the integrated offering may fail to meet all the applicable limitations and conditions. If that happens, the offering may not have been conducted in compliance with federal securities laws. Companies and their leadership can face penalties and other consequences if they do not comply with securities laws.

How can you prevent your offerings from being integrated?

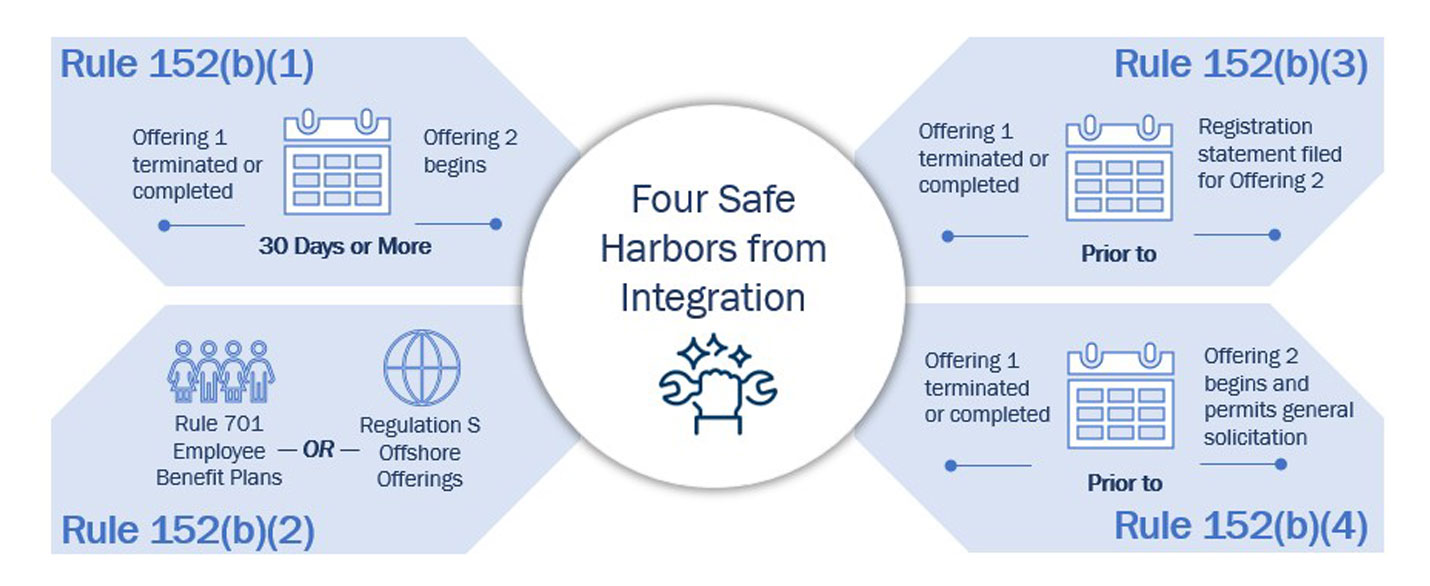

Determining whether multiple offerings may be considered integrated depends on the particular facts and circumstances of those offerings. Companies should carefully consider whether each offering complies with the registration requirements of the Securities Act, or that an exemption from registration is available for the particular offering. In addition, there are four non-exclusive safe harbors from integration that, if satisfied, will generally result in the offerings not being integrated:

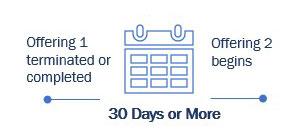

Rule 152(b)(1) Safe Harbor

A safe harbor from integration exists if Offering 1 terminates or completes 30 days or more before Offering 2 begins. However, if Offering 1 allows general solicitation, the company must reasonably believe that either:

- the company did not solicit any investor in Offering 2 via the general solicitation used in Offering 1 or

- the company established a substantive relationship with each such investor prior to Offering 2

Rule 152(b)(2) Safe Harbor

A safe harbor from integration exists if offerings are made in compliance with the Rule 701 for employee benefits plan OR Regulation S offshore offerings.

Rule 152(b)(3) Safe Harbor

A safe harbor from integration exists If Offering 1:

- did not permit general solicitation

- permitted general solicitation but was only made to qualified institutional buyers or institutional accredited investors or

- was terminated or completed 30 days or more prior to Offering 2

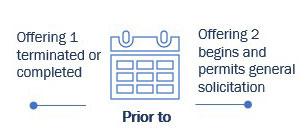

Rule 152(b)(4) Safe Harbor

A safe harbor from integration exists If Offering 1 terminates or completes before Offering 2 begins and permits general solicitation.

Learn more about the integration safe harbors.

Have suggestions on additional educational resources? Email smallbusiness@sec.gov.

Print this Building Block.

Last Reviewed or Updated: Aug. 8, 2025