Data Highlight

Order Book Reporting Methods and Their Impact on Some Market Activity Measures

June 29, 2022

DATA HIGHLIGHT 2014-03

March 19, 2014

This Data Highlight explores the impact of different order book reporting mechanisms on the interpretation of three common market activity measures: cancel-to-trade ratio, odd lot trade ratio and odd lot volume ratio. To account for the disparate nature of the feeds, we have made some modifications (discussed in detail below) to a number of the exchange-specific metrics published on the Market Structure web site. Details of these changes are also in the Market Activity Methodology document.

Two Order Book Methods

The two dominant formats used by the exchanges to report trade and order activities on their direct feeds are “order-based” and “level-book.” The order-based method prints a message for every displayed quote or order (i.e., orders that are not immediately executable and not denoted as hidden). Each displayed order receives an order identification number (“order id”) that permits the matching of subsequent events, including cancels, modifications, and executions to specific resting orders. To compute the total posted liquidity at any given price point for a given stock, one must keep track of every order, cancel, modification, and execution during the course of the trading day.

In contrast, the level-book method prints a message for every event that impacts the order book at a given price point for each stock, but does not print distinct order messages with their own order ids. The total posted liquidity at any given price point for a given stock is readily ascertained from the most recent level-book message for that price point.

Most exchanges currently use the more granular order-based method for their direct feeds, including NYSE Arca, BATS, Chicago (CHX), Direct Edge, Nasdaq, Nasdaq BX, Nasdaq PSX and National. NYSE and NYSE MKT (Amex) use the level-book method.

Impact on Some Market Activity Measures

In Data Highlight 2013-01, Trade to Order Volume Ratios, we stated that the “order cancellation data series is a simple measure of the number of displayed orders canceled per the number executed, and is mathematically related to the inverse of the trade-to-order volume ratio.” Metrics for both of these data series can be plotted for each exchange using the Data Visualization tool.

Some market participants have observed via the data visualization tool (as well as the downloadable individual time series files) that the cancel-to-trade ratio for NYSE and AMEX computes to a higher level than for most other exchanges, and similarly the trade-to-order volume ratio computes to a lower level than for most other exchanges. Given that the NYSE and AMEX both use the level-book method to report market activity on their direct feeds, we have explored the extent to which this might impact the computation, or interpretation, of these two metrics.

We begin by noting that the trade-to-order volume ratio is based on counting the total number of shares traded on an exchange as a fraction of the total number of shares posted on that exchange during continuous market hours. This computation is therefore not dependent on how many individual messages are used to convey such information, nor whether a single trade for 200 shares is reported as one trade for 200 shares or two trades for 100 shares each. Observed values for these ratios should not be influenced by the method an exchange uses (order-based or level-book) to report its activity.

However, this is not necessarily the case for the cancel-to-trade ratio metric. Consider the appearance of the order book after three orders are added to a new price level: one buy order for 100 shares at $10.00, one buy order for 300 shares at $10.00 and one buy order for 100 shares at $10.00. For feeds using the order-based method, each of these orders will be individually reported as 100, 300, and then 100 shares. For feeds using the level-book method, there will be three separate update messages showing a total of 100, 400, and then 500 shares bid at $10.00. If these three orders are then sequentially canceled, an order-based feed will print three cancel messages, one for each original order with a matching order id. Similarly, a level-based feed will print three messages, but in the form of updates showing 400, 100, and then 0 shares available at $10.00. In either format, there are a total of three messages printed as a result of the cancels.

But suppose that instead of the orders being canceled, they are executed as a result of an incoming market order for 500 shares. Direct feeds using the order-based mechanism will report three distinct trades, of 100, 300, and 100 shares each, with three unique order ids tied to the original resting orders. But the level-book feed will report only one trade for the total 500 shares. This example demonstrates how the same 500-share market order yields a different trade count depending on whether the direct feed uses the order-based or level-book approach. As such, the cancel-to-trade ratio computed for the level-book feeds can differ due to any marketable order that interacts with multiple resting orders at the same price point, and are therefore reported as a single trade message.

Because of the differences in these reporting methods, it may be inappropriate to directly compare or aggregate the cancel-to-trade ratio metrics derived from level-book feeds versus order-based feeds. Since most exchanges currently utilize the order-based method, to avoid mixing data derived from different reporting methods, we will temporarily exclude NYSE and Amex data in computations of the aggregate cancel-to-trade ratio statistic. We have also updated prior computations of this metric to correct for this exclusion.

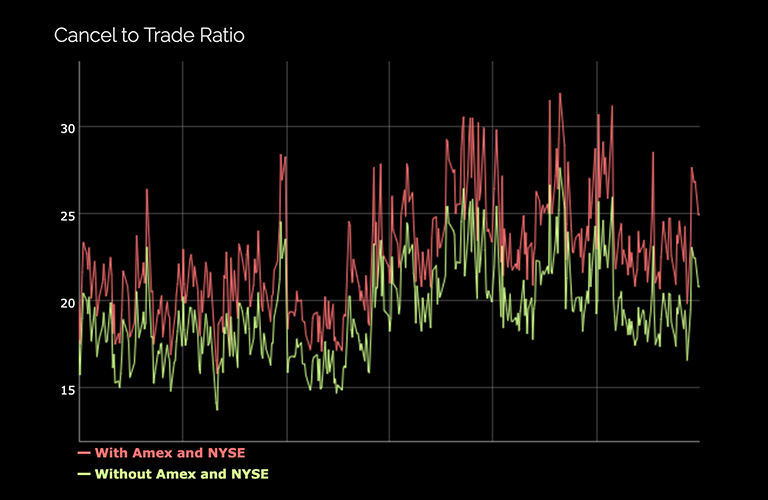

The chart below shows the impact of removing Amex and NYSE message counts from the aggregate cancel-to-trade measure.

Print or Download

Order Book Reporting Methods and Their Impact on Some Market Activity Measures (PDF, 146 KB)

Data Downloads

Visit the Market Activity Data Downloads page

Methodology

Learn how the SEC constructs odd lot rates and other metrics.

Launch the Data Visualization Tool

The cancel-to-trade ratio with NYSE and Amex excluded is slightly lower than the ratio computed with these two level-book exchanges included. The average difference in the cancel-to-trade ratio for the 18 months ending December 2013 is 3.2 (22.6 with Amex and NYSE versus 19.4 without).

We further note that the nature of level book reporting also affects computation of the odd lot rate and odd lot volume metrics. Though executions resulting from incoming, executable, odd lot orders are reported similarly by the two reporting mechanisms, executions against odd lot resting orders could result in different reported trade sizes. In Data Highlight 2014-01, Odd Lot Rates in a Post-Transparency World, we explain how round-lot marketable orders may result in the reporting of odd-lot trade executions if the marketable order interacts with any residual odd-lot resting orders (i.e. round-lot resting orders that were only partially executed due to a prior odd-lot marketable order). However, this effect is more pronounced for trades reported according to the order-based method than the level-book method, because (as described above), the level-book method will report a single message that aggregates execution at the same price level.

These differences may have implications for researchers undertaking trade-size studies (including odd-lot studies) based on data from the CTS and UTDF Consolidates Tapes. A single marketable order that is executed at a single price point against multiple resting orders will be reported to the tape by NYSE and Amex as a single execution. In general, this same combination of orders will be reported to the tape by all other exchanges using the order-based method as a series of smaller executions (one per resting order) that sum to size of the original marketable order. For example, if we remove NYSE and Amex trade executions from our aggregate calculation of odd lot rates and volume over the 18 month period ending in December 2013, the average rate increases 0.52 percentage points (from 19.99% with NYSE and Amex included to 20.51% with NYSE and Amex excluded), and the average odd lot volume increases 0.35 percentage points (from 4.99% with NYSE and Amex included to 5.34% with NYSE and Amex excluded). Though we have not separately computed metrics related to overall average trade sizes, these too would presumably be affected by the different reporting methods.

Important Changes to some Market Activity Data Metrics

Due to the differences regarding the data reported using the level-book method compared to the order-based method, and to avoid potential misinterpretations due to comparing such data across these mechanisms, the following metrics for NYSE and Amex will be temporarily removed from the website chart utility: Cancel-to-Trade Ratio, Odd Lot Ratio and Odd Lot Volume. Furthermore, the aggregate charts, including the decile charts, for these three metrics will temporarily exclude the contributions from NYSE and Amex; the Quarterly User Files will also not include NYSE and Amex for these three measures.[1]

However, the Monthly User Files will continue to carry the inputs to these metrics on a ticker-exchange basis (as they have in the past), including the NYSE and Amex. The level-book reporting mechanism has no impact on exchange-traded product metrics (since exchange-traded products are not traded on NYSE) and also do not impact the Trade-Order Volume metric for corporate stocks. These measures remain unchanged in the historic charts and are available in the User Files.

There are no changes to any of the metrics associated with the speed of order and trade executions, nor any of the histograms summarizing these distributions. Due to the lack of unique order-ids, data from exchanges using the level-book method to report were never included in such calculations.

[1] Staff will be reviewing the extent to which additional analyses of level-book book data could be undertaken that better facilitates aggregating the various metrics produced from such data with metrics derived from order-based data.

This analysis was prepared by the Staff of the U.S. Securities and Exchange Commission. The Commission has expressed no view regarding such analysis or any statement contained therein.

Last Reviewed or Updated: Aug. 13, 2025