Statement on Reducing Investor Protections around Private Markets

Thank you to the terrific Staff in our Division of Corporation Finance, including especially Director Bill Hinman, for their hard work in advance of today’s open meeting. This team has certainly earned the time off I hope you’ll take over the coming holiday season.[1]

Today’s release proposes significant changes to rules governing investing in our private markets. The release is right to say that it has been decades since we have updated these rules, so they’re ripe for review. But what we need is careful, data-driven analysis of how to best balance the risks investors face in these markets with the potential rewards of participation. Instead, the release repeats by rote the intuition that exposing investors to these markets comes without corresponding costs.[2] Because there is no free lunch in financial markets, and pretending otherwise puts ordinary investors at risk, I respectfully dissent.

* * * *

The release does not take seriously the investor protection concerns present in private markets. When voting to support our concept release in this area last year, I urged colleagues to carefully study the risk of fraud in exempt offerings.[3] Instead, the release before us today includes virtually no analysis of the costs of expanding eligibility to participate in exempt offerings. This kind of one-sided assessment of difficult choices serves no one—especially not investors.

Consider, for example, the proposal’s suggestion that investors who use advisors to participate in private-market transactions need less protection than others.[4] The intuition behind this suggestion is that investors can efficiently identify and avoid brokers in this area who fail to protect them from fraud. But that is an empirical assertion that should be tested rather than assumed away. Because the release includes no real analysis of these questions, my Office dug into the data ourselves.

Combining the public data on the Commission’s website on private securities issuances with information on complaints against brokers, we examined how investors can be harmed in these markets.[5] The results offer two striking facts that should give those concerned about investor protection real pause about any suggestion that advisors will protect ordinary families from fraud in our private markets.

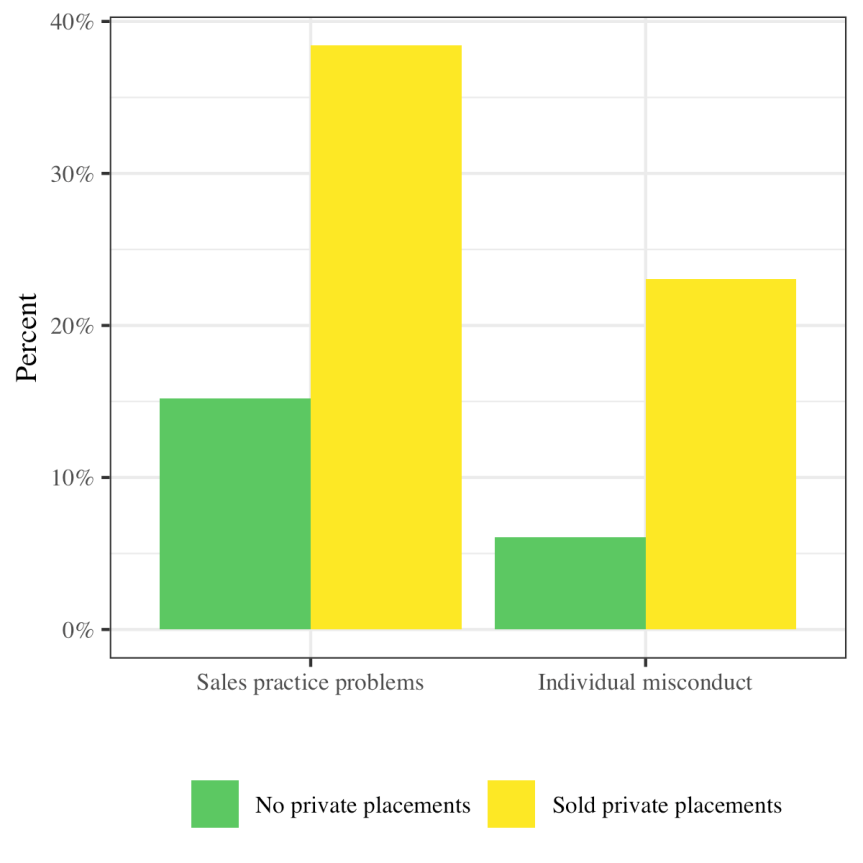

First, brokers who put investors in private securities are unusually likely to be the subject of both customer complaints related to sales practices and regulatory inquiries about misconduct.[6] Contrary to the release’s intuition that brokers will protect ordinary families investing in private markets, the evidence shows that those families will be dealing with the brokers most likely to have wronged clients in the past:

Figure 1. Potential for Investor Harm with Brokers Engaging in Private Placements.

That fact highlights the importance of our second finding: consistent with recent research in this area, we find that past investor harm facilitated by brokers in our private markets is highly predictive of investor harm in the future.[7] That means that even supposedly sophisticated investors under our current standards have difficulty avoiding high-risk brokers in the private-placement market.[8] And if investors are already struggling to sort good brokers from bad in these markets, it’s far from clear why we should expose even more investors to those risks.

The evidence makes clear that the Commission must do more to protect investors in private markets than hope that brokers will do it for us. And it shows that we have a great deal more work to do if we hope to make the hard choices reflected in today’s release on the basis of actual evidence rather than guesswork about market efficiency.

* * * *

But I’m an optimist. Perhaps the most important thing about today’s proposal is that it’s just that: a proposal. I hope that the evidence my Office has provided offers a starting point for detailed study of these matters. And I urge investors of all types to come forward to help the Commission engage with actual evidence about balancing the benefits of today’s proposed changes with their very real costs for ordinary American investors.

[1] I doubt that anyone—inside or outside the Commission—is in the market for advice as to how to spend the coming weeks before the New Year. I would point out, however, that in just three days a great American film franchise will launch its next chapter. Star Wars Episode IX: The Rise of Skywalker (2019) (Abrams, J.J., dir.). Many contested questions of law and life can be resolved by reference to these films. See, e.g., Star Wars Episode V: The Empire Strikes Back (1980) (Lucas, G., dir.) (remarks of Yoda) (“Try not! Do or do not; there is no try.”); Star Wars Episode VIII: The Last Jedi (2017) (Johnson, R., dir.) (remarks of Yoda) (“[W]e are what they grow beyond. That is the true burden of all masters.”). The rest can resolved by listening to The Beatles.

[2] See, e.g., Sec. & Exch. Comm’n, Proposed Rule: Amending the “Accredited Investor” Definition, Rel. Nos. 33-10734; 34-87784 (Dec. 18, 2019), at 80 [Proposing Release] (noting that “certain geographic areas of the United States, such as the Midwest and South regions, have a lower cost of living, and therefore investors in those regions are already less likely to qualify as accredited investors under the current financial thresholds,” and that an “increase in the financial thresholds would exacerbate this current disparity,” without pointing out that investors in those regions would also avoid the costs of fraud associated with private markets”); id. at 41 (same: asserting that employees of certain funds “may be excluded from participating” in private offerings, without noting the corresponding fact that the employee would therefore avoid the costs of fraud associated with access to those funds); id. at 80 (claiming that “a sharp decrease in the accredited-investor pool may result in a higher cost of capital for companies,” without noting that we are in the midst of the frothiest private capital markets in generations).

[3] See Mark Schoeff Jr., SEC Commissioner Jackson Seeks Data on Potential Harm of Easing Rules for Private Placements, InvestmentNews (July 1, 2019) (“The questions in this release involve a fundamental trade-off: the costs families suffer when investors are victims of fraud versus the benefits of broader access to capital. Strikingly, the release says that the commission lacks data to measure fraud in this space. . . . Without that evidence, it’s hard to see how the commission can strike the basic balance any rules in this area would require.”).

[4] See Proposing Release, supra note 2, at 82-83 (inviting comment on whether an investor “that is advised by a registered investment adviser or broker-dealer [should] be considered an accredited investor”).

[5] We collected data on private placements from the Commission’s Form D data page, see Sec. & Exch. Comm’n, Form D Data Sets (Sept. 2009-2019) (providing structured data from Notices of Exempt Offerings of Securities filed with the Commission), and merged those data with information on broker conduct, which FINRA makes available through its BrokerCheck web portal. Following Hammad Qureshi & Jonathan S. Sokobin, Do Investors Have Valuable Information About Brokers? FINRA Office of the Chief Economist Working Paper (2015), we proxy for investor harm using customer complaints because we do not have data on individual investor harm. Specifically, we narrow our focus to customer complaints related to private placements and direct investments. Customer complaints are not, of course, a perfect proxy for investor harm. But we consider such complaints to reflect a lower bound on investor harm, because meritless complaints will serve as noise in our statistical models, whereas we have no way to detect or address under-reporting.

[6] We collected information on individual and firm misconduct as well as firm-level data on complaints—for example, past complaints related to private placements, total firm complaints and firm sales practice complaints. We define serious complaints as those related to misrepresentations, suitability failures, misappropriation of customer funds, unauthorized trading, excessive trading, excessive fees, and theft.

[7] Our analysis was inspired both by recent academic work in this area, see, e.g., Stephen G. Dimmock & William C. Gerken, Predicting Fraud by Investment Managers, 105 J. Fin. Econ. 153 (2012); Mark Egan, Gregor Matvos & Amit Seru, The Market for Financial Adviser Misconduct, 127 J. Pol. Econ. (2019), as well as recent public reporting on the subject, Jean Eaglesham & Coulter Jones, Firms with Troubled Brokers are Often Behind Sales of Private Stakes, Wall St. J. (2018).

[8] Contemporaneously with the issuance of this statement, my Office has publicly posted a Data Appendix describing this analysis in detail—and, as always, we welcome comments on these important issues. See Office of Commissioner Robert J. Jackson, Jr., Online Appendix to Commissioner Jackson Statement on Accredited Investor (Dec. 16, 2019), 10 & tbl. 2 (documenting, in specification (3) of panel (a), the positive and statistically significant correlation between previous complaints related to private placements and the probability of future complaints).

Last Reviewed or Updated: Dec. 18, 2019