Financial Reporting Manual

TOPIC 2 - Other Financial Statements Required

This topic identifies circumstances in which financial statements of entities other than the registrant (or predecessor(s) of the registrant) are required to be included in filings. The guidance applicable to financial statements of the registrant (in Topic 1) applies also to financial statements of the other entities, unless specified otherwise in this topic.

NOTE to TOPIC 2

The staff may, where consistent with the protection of investors, permit the omission of one or more of the financial statements required by Regulation S-X or the filing in substitution therefor of appropriate statements of comparable character under Rule 3-13 of Regulation S-X. See “Communications with the Division of Corporation Finance’s Office of Chief Accountant” section for additional information about requesting relief. In addition, the staff may require other financial statements as necessary for a fair presentation of the financial condition of any entity whose financial statements are either required or otherwise necessary for the protection of investors. [S-X 3‑13 and S-X 8-01, Note 5] (Last updated 7/1/2019)

2000BUSINESSES ACQUIRED OR TO BE ACQUIRED (Excluding Target Companies in Form S-4) [S-X 3-05, S-X 8-04]

(Last updated: 9/30/2008)

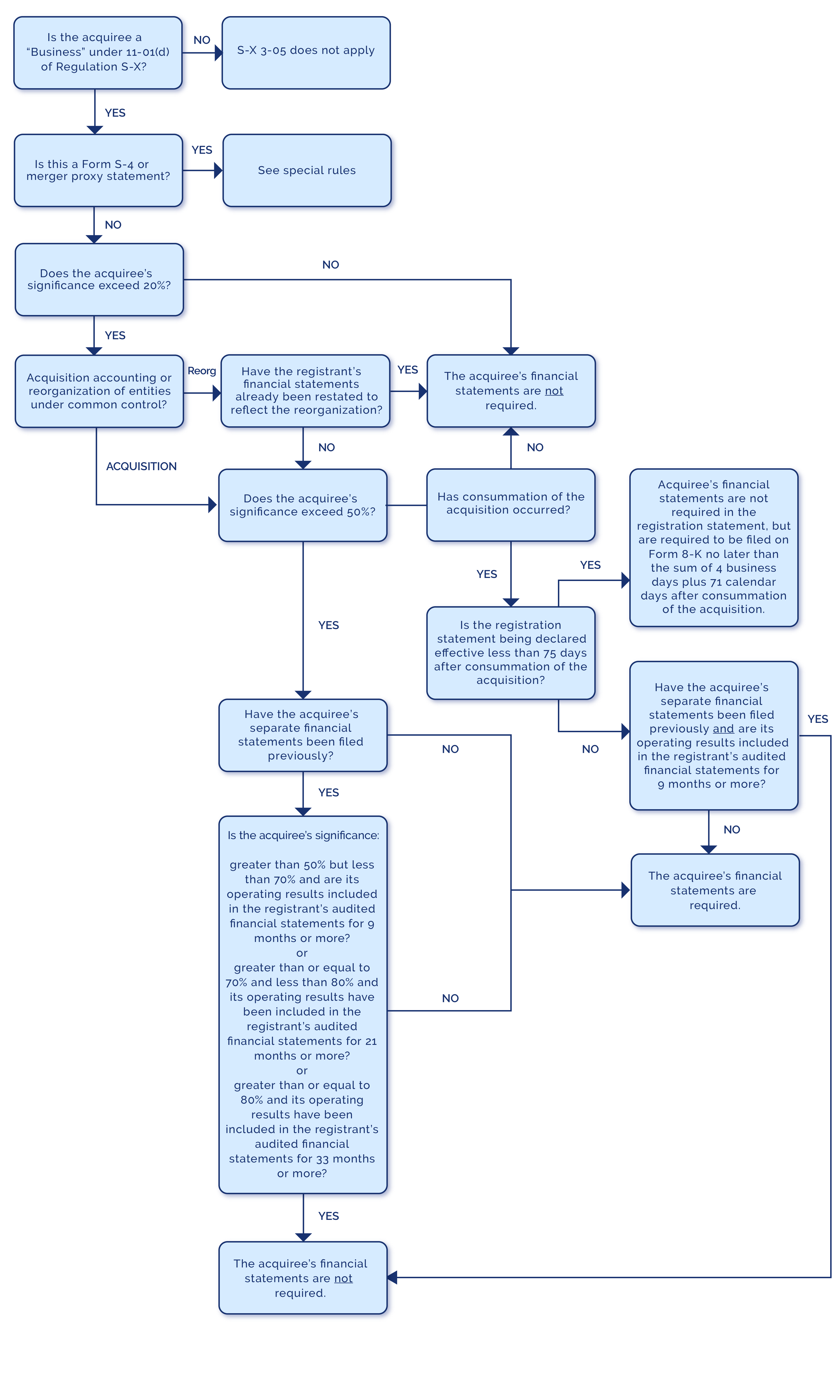

Overview - In general, S-X 3-05 and S-X 8-04 require the filing of separate pre-acquisition historical financial statements when the acquisition of a significant business has occurred or is probable. A flowchart to assist you is located at Section 2060.

| Section | Description |

|---|---|

| 2005 | Definitions and Requirements |

| 2010 | Determination of a Business |

| 2015 | Measuring Significance - Basics |

| 2020 | Implementation Points - Amounts Used to Measure Significance |

| 2025 | Implementation Points - Financial Statements Used to Measure Significance |

| 2030 | Financial Statement Periods Required Under S-X 3-05 and S-X 8-04 |

| 2035 | Individually Insignificant Acquirees |

| 2040 | When To Present Financial Statements |

| 2045 | Age of Financial Statements - Basics |

| 2050 | Age of Financial Statements - Interaction of S-X 3-05(b)(4) and Form 8-K |

| 2055 | Foreign Business, Hostile Tender Offers, Troubled Financial Institutions |

| 2060 | Flowchart Overview of S-X 3-05 |

| 2065 | Acquisitions of Selected Parts of an Entity |

| 2070 | SAB 80: Application of S-X 3-05 in Initial Registration Statements |

2005Definitions and Requirements

2005.1Financial statements of the acquired business are generally the same as those as if the acquired company were a registrant as described in Topic 1, except that the number of years of audited financial statements is determined by the level of significance (Section 2030 below). Refer to Sections 2045 and 2050 regarding age of financial statements.

Exceptions: An acquired business that is a nonpublic entity, as that term is defined in GAAP, need not include disclosures if specifically excluded from the scope of the FASB standard. Examples include:

- Segment information under ASC 280 [ASC 280-10-15-3],

- Certain disclosures about employers' pensions and other postretirement benefits [ASC 715-20-50-5]

- Earnings per share under ASC 260 [ASC 260-10-05-1]

2005.2Supplemental schedules (S-X Article 12) are not required to be filed.

2005.3"Acquisition" and Equity Method Investee - Acquisition includes acquisition of an interest in a business that is accounted for under the equity method. Refer to Section 2010 regarding definition of a "business".

2005.4"Probable" - Assessment of "probability" requires consideration of all available facts. Acquisition is probable where registrant's financial statements alone would not provide adequate financial information to make an investment decision. [FRC 506.02(c)(ii)]

2005.5Acquiree of an Acquiree or Investee of an Acquiree - The requirements of S-X 3-05 and S-X 8-04 apply to acquisitions made by the registrant or its predecessor(s). Those rules call for financial statements of the acquiree and its predecessor(s), if applicable. Financial statements of recently acquired businesses of the acquiree or equity method investees of the acquiree need not be filed unless their omission would render the acquiree's financial statements misleading or substantially incomplete. (Last updated: 3/31/2010)

2005.6Acquisition of a "Predecessor" - S-X 3-05 and S-X 8-04 do not apply to the acquisition of a business that is a predecessor of the registrant, as defined in Regulation C, Rule 405. Instead, look to S-X 3-01/3-02 or S-X 8-02/8-03 to determine the financial statement requirements for an acquired business that is a predecessor of the registrant.

2005.7"Shell Company" is both Legal and Accounting Acquirer - If a shell company, other than a "Business Combination Related Shell Company" (both as defined in Exchange Act Rule 12b-2 and Regulation C, Rule 405), acquires an operating entity in a transaction in which the shell company is both the legal and accounting acquirer, the acquired entity will be a predecessor of the shell company and therefore S-X 3-05 and S-X 8-04 do not apply. If a shell company acquires an operating entity in a transaction accounted for as the acquisition of the shell company by the operating entity (i.e., shell company is the legal acquirer, but the accounting acquiree) the transaction is a reverse recapitalization of the operating entity and therefore S-X 3-05 and S-X 8-04 do not apply. See Topic 12 for further discussion of the reporting requirements for reverse recapitalizations.

2005.8Acquisition or Disposition by a Consolidated Variable Interest Entity - An acquisition or disposition by a variable interest entity that is consolidated in the registrant's financial statements pursuant to ASC 810 is subject to the Form 8-K and S-X reporting requirements even if the consolidated variable interest entity does not meet the S-X 1-02(n) definition of "majority-owned subsidiary."

(Last updated: 6/30/2011)

NOTE to SECTION 2005.8

Item 2.01 of Form 8-K refers to acquisitions or dispositions by "the registrant or any of its majority-owned subsidiaries." Because this reference preceded the variable interest entity consolidation model, the staff believes the intent of this reference is to require reporting of significant acquisitions and dispositions made by the registrant or its consolidated subsidiaries, regardless of whether the consolidated subsidiaries are voting interest entities or variable interest entities. (Last updated: 6/30/2011)

2010Determination of a Business [S-X 11-01(d)]

2010.1Reporting versus Accounting - The determination of what constitutes a business for reporting purposes (e.g., S-X 3-05 and Item 2.01 of Form 8-K) is made by reference to the definition of a "business" in S-X 11-01(d). The determination of what constitutes a business for accounting purposes (e.g., whether acquired net assets constitute a business for purposes of determining whether a business combination as defined in ASC-MG and ASC 805 has occurred) is made by reference to ASC-MG and ASC 805. It is possible for the determination to be different under the two requirements.

(Last updated: 12/31/2011)

2010.2A separate entity, subsidiary, division or possibly a separate product line - A "business" for purposes of S-X 3-05 is identified by evaluating whether there is sufficient continuity of operations so that disclosure of prior financial information is material to an understanding of future operations. There is a presumption in S-X 11-01(d) that a separate entity, subsidiary, or division is a business. A lesser component, such as a product line, also may be considered a business. In evaluating whether a lesser component is a business, S-X 11-01(d) requires registrants to consider the following:

- Will the nature of the revenue producing activity generally remain the same?

- Will the facilities, employee base, distribution system, sales force, customer base, operating rights, production techniques, or trade names remain after the acquisition?

NOTE to SECTION 2010.2

The staff's analysis of whether an acquisition constitutes the acquisition of a business, rather than of assets, focuses primarily on whether the nature of the revenue producing activity previously associated with the acquired assets will remain generally the same after the acquisition. New carrying values of assets, or changes in financing, management, operating procedures, or other aspects of the business are not unusual following a business acquisition. Such changes typically do not eliminate the relevance of historical financial statements. Registrants that have succeeded to a revenue producing activity by merger or acquisition, with at least one of the other factors listed above remaining after the acquisition, are encouraged to obtain concurrence from the staff in advance of a filing if they intend to omit financial statements related to the assets and activity. Registrants may direct requests related to appropriate financial statements of an acquired entity or group of assets to CF-OCA.

2010.3An investment accounted for under the equity method - The staff considers the acquisition of an investment accounted for under the equity method to be a business for reporting purposes.

2010.4A working interest in an oil and gas property - The staff considers the acquisition of a working interest in an oil and gas property to be a business for reporting purposes. Refer to Section 2065.11 "Unique Considerations for Acquisitions of Oil and Gas Properties – General." (Last updated: 10/20/2014)

2010.5Bank branch acquisitions - The assumption of customer deposits at bank branches may constitute the acquisition of a business if historical revenue producing activity is reasonably traceable to the management or customer and deposit base of the acquired branches, and that activity will remain generally the same following the acquisition.

2010.6Insurance policy acquisitions - Acquisitions of blocks of insurance policies by an insurance company or the assumption of policy liabilities in reinsurance transactions may also be deemed the acquisition of a business because the right to receive future premiums generally indicates continuity of historical revenues. The degree of continuity between historical investment income streams and the assets acquired to fund the acquired policy liabilities should also be considered.

2015Measuring Significance – Basics [S-X 3-05(b)(2)]

NOTE to SECTION 2015

Registrants may request CF-OCA interpretation in unusual situations or relief where strict application of the rules and guidelines results in a requirement that is unreasonable under the circumstances.

2015.1Registrants must measure the significance of an acquired business under S-X 3-05 and S-X 8-04 using three tests, the:

- Asset test,

- Investment test, and

- Income test.

These tests are described in further detail below.

NOTE to SECTION 2015.1

In certain circumstances, registrants preparing an initial registration statement may consider applying SAB 80 instead of S-X 3-05 or S-X 8-04. See further discussion at Section 2070, "SAB 80: Application of S-X 3-05 in Initial Registration Statements (SAB Topic 1J)."

2015.2Financial Statements Used to Measure Significance - Generally, compare the most recent pre-acquisition annual financial statements of the acquired business to the registrant's pre-acquisition consolidated financial statements as of the end of the most recently completed audited fiscal year required to be filed with the SEC. Financial statements of both the acquired business and the registrant used to measure significance must be prepared in accordance with the comprehensive basis of accounting described in Section 2015.3, "Comprehensive Basis of Accounting Used to Measure Significance."

If a change in the reporting entity or a reorganization will occur at or after effectiveness of an initial registration statement but no later than closing of the IPO, the staff will consider requests for relief to use the combined financial statement amounts as the denominator for purposes of significance calculations in determining other financial statement requirements for the filing (e.g., S-X 3-05 and 3-09). (Last updated: 3/31/2010)

2015.3Comprehensive Basis of Accounting Used to Measure Significance - A registrant that files its financial statements in accordance with or is required to provide reconciliation to U.S. GAAP should determine significance using amounts for both the acquired business and the registrant determined in accordance with U.S. GAAP; that is, both the numerator and denominator of the significance test would be determined in accordance with U.S. GAAP. A foreign private issuer that files its financial statements in accordance with IFRS as issued by the IASB should determine significance using amounts for both the acquired business and the registrant determined in accordance with IFRS as issued by the IASB; that is both the numerator and denominator of the significance test would be determined in accordance with IFRS as issued by the IASB. To illustrate these requirements, if a registrant that files its financial statements in accordance with U.S. GAAP acquires, both legally and for accounting purposes, a foreign private issuer or a foreign business that files its financial statements in accordance with IFRS as issued by the IASB, significance (both the numerator and denominator) must be determined in accordance with U.S. GAAP. This is true even though the acquired business did not reconcile its financial statements to U.S. GAAP.

2015.4Asset Test - Compare registrant's share of acquired business's total assets to the registrant's consolidated total assets. Ordinary receivables and other working capital amounts not acquired should nevertheless be included as part of the assets of the acquired enterprise in tests of significance relative to the registrant's assets because that working capital is expected to be required and funded after the acquisition.

2015.5Investment Test - Acquisition Accounting under ASC 805 and IFRS 3 as issued by the IASB - Compare the total GAAP purchase price of the acquired business, as adjusted below, to the registrant's consolidated total assets.

GAAP purchase price in this context means the "consideration transferred", as that term is used in the applicable accounting standard. It includes the acquisition-date fair value of all contingent consideration and excludes acquisition-related costs.

The adjustment - For purposes of the "investment" test, "consideration transferred" should be adjusted to exclude carrying value of assets transferred by the acquirer to the acquired business that will remain with the combined entity after the business combination.

NOTE to SECTION 2015.5

The numerator of the investment test for the purchase of an equity method investment should include transaction costs, consistent with the accounting under ASC 323-10. The numerator should also include contingent consideration (on a gross basis) if the likelihood of payment is more than remote. (Last updated: 3/31/2010)

2015.6[Reserved]

(Last updated: 10/30/2020)

2015.7Investment Test - Reorganization of Entities Under Common Control - Compare the net book value of the acquired business to the registrant's consolidated assets and compare the number of shares exchanged to registrant's outstanding shares at the date the combination is initiated.

2015.8Income Test - Compare registrant's equity in the acquired business's income from continuing operations before taxes to that of the registrant.

There are three computational notes to the income test included at S-X 1-02(w). The second computational note indicates that if the registrant's income for the most recent fiscal year is 10% or more lower than the average of the registrant's income for the last five fiscal years, then the average income of the registrant should be used for this computation. This computational note also applies if the registrant reported a loss, rather than income. If the registrant reported a loss, the registrant should compare the absolute value of its reported loss to its average income for the last five fiscal years to determine if the registrant is required to use average income. In computing the registrant's average income for the last five fiscal years, loss years should be assigned a value of zero in computing the numerator for this average, but the denominator should be "5". Also, the acquiree's income may not be averaged. (Last updated: 12/31/2010)

2015.9Significance – Absolute Values - In the case of a single acquisition, if either the registrant or the acquired business reported a pretax loss and the other entity reported pretax income, use the absolute values.

2015.10Significance – Denominator - The acquired business is not considered part of the registrant's denominator in determining significance for purposes of S-X 3-05 [S-X 1-02(w)]

2015.11Significance – Intercompany Transactions- When measuring significance for all three S-X 1-02(w) tests, intercompany transactions between the registrant and acquiree should be eliminated in the same way that would occur if the acquiree were consolidated. See by analogy S-X 1-02(w)(2).

(Last updated: 9/30/2009)

2015.12Significance – "Related Businesses" - Acquisitions of "related businesses" must be treated as a single business acquisition. Businesses are related under S-X 3-05 if:

- they are under common control or management, or

- their acquisitions are dependent on each other or a single common event or condition.

2015.13Significance – Rounding - Do not round the results of the significance tests.

2020Implementation Points – Amounts used to Measure Significance [S-X 1-02(w)]

2020.1Significance Implementation – No Alternative Tests of Significance

The staff generally will not accept alternative significance tests. The tests should be performed based on the requirements of S-X 3-05, 3-09, and 4-08(g), as applicable. If after performing the required significance tests a registrant believes that the tests specify periods beyond those reasonably necessary to inform investors, the registrant may make a written request to CF-OCA to waive one or more years of financial statements. Such requests should set forth the relevant factors considered by the registrant. In making this request, registrants should consider all facts and circumstances that provide an indication of the relative size of the acquired business. (Last updated: 7/1/2019)

2020.2Significance Implementation - Business Combinations - Measurement Period Adjustments under ASC 805 and IFRS 3

In some circumstances, ASC 805 and IFRS 3 require retrospective adjustment of provisional amounts recognized at the acquisition date and the recognition of additional assets or liabilities that were not recognized at the acquisition date. The pre-acquisition financial statements for the most recently completed fiscal year used to measure significance should include measurement period adjustments for acquisitions completed within the most recently completed fiscal year when new information obtained about facts and circumstances that existed at the acquisition date for those acquisitions is known: (A) prior to effectiveness of an IPO for a new registrant or (B) on or before the date the initial Item 2.01 Form 8-K reporting the acquisition must be filed for an existing registrant. (Last updated: 9/30/2009)

2020.3Significance Implementation - Business Combination Achieved in Stages or Step Acquisition of a Rule 11-01(d) Business – General

If a registrant increases its investment in a business relative to the prior year, base the tests of significance on the increase in the registrant's proportionate interest in assets and net income during the year, rather than the cumulative interest to date. However, step acquisitions which are part of a single plan to be completed within a twelve month period should be aggregated.

NOTE to SECTION 2020.3

The guidance to base significance on the increase in the registrant's proportionate interest applies even if the registrant must discontinue applying the cost method and start applying the equity method as a result of the increase in investment.

2020.4Significance Implementation - Business Combination Achieved in Stages (a.k.a. Step Acquisition) – Remeasurement

Under ASC 805 and IFRS 3 as issued by the IASB, the acquirer's previously held equity interest in the acquiree is remeasured at its acquisition-date fair value with any resulting gain or loss recognized in earnings. The remeasurement of the previously held equity interest is not included in the asset or the investment test and the resulting gain or loss from remeasurement would be excluded from the income test as it is not included in the registrant's most recently completed fiscal year.

2020.5Significance Implementation - Acquiring an Additional Interest in a Consolidated Entity

(Last updated: 9/30/2011)

When a registrant increases its investment in a company that is already reflected as a consolidated subsidiary in the audited financial statements of the registrant for a complete fiscal year, financial statements of the acquired investment are ordinarily not required. However, pro forma information may be required.

The staff’s view that financial statements are ordinarily not required is premised on S-X 3-05(b)(4)(iii) which states that separate financial statements of the acquired business need not be presented once the operating results of the acquired business have been reflected in the audited consolidated financial statements of the registrant for a complete fiscal year unless such financial statements have not been previously filed or unless the acquired business is of major significance. Illustrative, but not all-inclusive, examples of when historical financial statements of an acquired business may be required in a step acquisition include:

- acquired business financial statements have not been previously filed for the entire period for which historical financial statements of the acquired entity would be required under S-X 3-05;

- acquired business is of major significance; or

- S-X 3-05 does not apply; such as a proxy statement or Form S-4 requirement to present the target’s financial statements for the same periods that would be required in an annual report sent to security holders, if an annual report was required.

Also, note that while S-X 11-01(c) states that pro forma effects of a business combination need not be presented if the acquired business’ financial statements are not presented, we believe such pro forma financial statements are required pursuant to S-X 11-01(a)(8) when pro forma financial information giving effect to the step acquisition would be material to investors.

2020.6Significance Implementation - Public Offering Proceeds

Registrant's assets may not be increased for purposes of the significance tests by including the pro forma effect of public offering proceeds received after the balance sheet date.

2020.7Significance Implementation - Statements of Revenues and Direct Expenses

A registrant that has received an accommodation from CF-OCA to present a statement of revenue and direct expenses for the acquired business in lieu of full financial statements (See Section 2065) should not adjust the registrant’s pretax income (i.e., the denominator in the income test) to exclude corporate overhead even though the target’s pretax revenues less direct expenses (i.e., the numerator) excludes indirect expenses. If after performing the required significance tests using the target’s pretax revenues less direct expenses and the registrant’s pretax income, a registrant believes that the tests specify periods beyond those reasonably necessary to inform investors, the registrant may make a written request to CF-OCA to waive one or more years of financial statements.

2020.8Significance Implementation - Related Businesses – General

(Last updated: 9/30/2012)

S-X 3-05 requires that related businesses be treated as a single business when measuring significance. Further guidance on this requirement is included below. If S-X 3-05 significance is met, separate financial statements of each of the related businesses are required, except that financial statements of the related businesses that are under common control or management may be, but are not required to be, presented on a combined basis for any annual or interim periods specified in S-X 3-05 for which the businesses are under common control or management. If the registrant believes that application of the significance tests results in a requirement to present financial statements of one or more related businesses that are not reasonably necessary to inform investors, the registrant may make a request to CF-OCA for relief.

NOTES:

- If related businesses have different fiscal year ends, a registrant should not conform the fiscal year-ends of the related businesses for purposes of the significance tests.

- The reference to “periods specified in S-X 3-05” is meant to clarify that in order to present financial statements of related businesses on a combined basis for an annual or interim period specified in S-X 3-05, the related businesses must be under common control or management for the entirety of that annual or interim period.

- S-X 3-05(a)(3) states in part “Acquisitions of a group of related businesses that are probable or that have occurred subsequent to the latest fiscal year-end for which audited financial statements of the registrant have been filed shall be treated under this section [emphasis added] as if they are a single business combination.” The staff interprets this requirement to mean that S-X 1-02(w) Computational Note 3, which indicates that entities reporting losses should not be aggregated with entities reporting income, does not apply to the calculation of significance for related businesses. (Last updated: 9/30/2012

2020.9Significance Implementation - Related Businesses - Asset and Investment Tests

(Last updated: 9/30/2012)

Both the asset test and the investment test should be performed for each related business using the guidance provided in Section 2015. If either the sum of each related business’s asset test significance or the sum of each related business’s investment test significance exceeds the S-X 3-05 significance levels (see Section 2030), separate financial statements should be provided for the periods required by S-X 3-05 for each related business, except that financial statements for the related businesses that are under common control or management may be, but are not required to be, presented on a combined basis for any annual or interim periods specified in S-X 3-05 for which the businesses are under common control or management. See the Notes at Section 2020.8 for further guidance.

2020.10Significance Implementation - Related Businesses – Income Test

(Last updated: 9/30/2012)

S-X 3-05 indicates that related businesses should be treated as if they are a single business combination. Therefore, calculate the income test significance using the combined income or loss from continuing operations before income taxes of all of the related businesses. The combined income or loss should be used to measure income test significance irrespective of whether any of the related businesses are under common control or management. If the income test significance exceeds the S-X 3-05 significance levels (see Section 2030), separate financial statements should be provided for the periods required by S-X 3-05 for each related business, except that financial statements of the related businesses that are under common control or management may be, but are not required to be, presented on a combined basis for any annual or interim periods specified in S-X 3-05 for which the businesses are under common control or management. See the Notes at Section 2020.8 for further guidance.

2025Implementation Points – Financial Statements Used to Measure Significance [S-X 1-02(w)]

2025.1Significance Implementation - Discontinued Operations and Changes in Accounting Principle

Subsequent to filing its Form 10-K, a registrant may be required to include (or incorporate by reference) into a registration statement its audited annual financial statements giving retrospective effect to a discontinued operation or a change in accounting principle that was appropriately not reflected in the audited financial statements for the most recently completed fiscal year included in its Form 10-K. See Topic 13 for a discussion of this requirement. In these circumstances, we have interpreted the guidance in S-X 3-05 to require registrants to perform significance tests based on the registrant’s financial statements that reflect retrospective application for the most recently completed fiscal year for:

- Individual businesses acquired after the date the retrospectively adjusted financial statements are filed;

- Probable acquisitions; and

- Aggregate impact of all individually insignificant businesses that have occurred since the end of the most recently completed fiscal year.

NOTES to SECTION 2025.1

- Solely for purposes of assessing significance of individual acquisitions completed on or before the date the retrospectively adjusted financial statements are filed (and not, for example, for purposes of assessing the aggregate impact of all individually insignificant businesses that have occurred since the end of the most recently completed fiscal year), significance may be measured based on either (A) the registrant’s audited financial statements for its most recently completed fiscal year that were filed prior to the retrospectively adjusted financial statements giving effect to the discontinued operation or (B) the registrant’s filed financial statements for the most recently completed fiscal year that reflect retrospective application of the discontinued operation. A registrant must consistently use the financial statements it chooses (i.e., either (A) or (B) above) to measure significance of all individual acquisitions completed on or before the date the retrospectively adjusted financial statements are filed. (Last updated: 3/31/2009)

- The staff’s rationale for the position above follows. A registrant must report on Form 8-K an acquisition of a significant individual business. For purposes of measuring significance under S-X 3-05 and S-X 8-04, the staff links the acquisition date for a significant individual business to the date retrospectively adjusted financial statements are filed in order to ensure that an appropriate conclusion that an acquired business was not significant for purposes of Form 8-K will not be changed by a subsequent discontinued operation. Such a link is not necessary for either a probable acquisition or an acquisition of an individually insignificant business because the registrant has no Item 2.01 Form 8-K reporting obligation for these events.

2025.2Significance Implementation - Form 10-K Filed Subsequent to Acquisition

(Last updated: 3/31/2009)

Generally, a registrant measures significance using its pre-acquisition consolidated financial statements as of the end of the most recently completed audited fiscal year required to be filed with the SEC. If the acquisition is made after the registrant’s most recent fiscal year end and the registrant files its Form 10-K for the most recent fiscal year before the date financial statements of the acquired business would be required to be filed under Item 9.01 of Form 8-K, the registrant may evaluate significance using the registrant’s financial statements for most recent fiscal year reported in its Form 10-K. Alternatively, the registrant may choose to evaluate significance using the registrant’s financial statements for the most recently completed audited fiscal year required to be on file with the SEC as of the consummation date.

2025.3Significance Implementation - Pro Forma Financial Statements (S-X Article 11) Used to Measure Significance

If the acquisition is made after reporting a previous significant acquisition or disposition on Form 8-K or non-IPO registration statement that includes all information required by Form 8-K, the registrant may evaluate significance using registrant’s pro forma financial information rather than historical pre-acquisition financial statements. For purposes of evaluating significance in this situation:

- Income Test - Compare income from continuing operations before income taxes for the acquired entity's latest fiscal year to the pro forma statement of comprehensive income for the latest audited annual period provided in the Form 8-K or registration statement.

- Investment and Asset Tests - Compare the registrant's investment in the acquired entity and the assets of the acquired entity for the latest fiscal year to the pro forma balance sheet comprising the latest audited balance sheet of the registrant. That pro forma balance sheet may or may not have been included in the Form 8-K or registration statement, depending on when the Form 8-K or registration statement was filed.

For example: If a calendar year-end registrant filed a registration statement containing a pro forma balance sheet as of June 30, 2007 giving effect to an acquisition consummated on September 14, 2007 and then made an acquisition on November 30, 2007, the asset and investment test would be based on a pro forma balance sheet as of December 31, 2006 (the last audited balance sheet on file with the SEC).

NOTES to SECTION 2025.3

- If the registrant chooses to evaluate significance of an acquisition or disposition using the registrant’s pro forma financial information, the staff would expect the registrant to consistently apply that methodology for evaluating significance to all subsequent acquisitions or dispositions for the remainder of the fiscal year.

- If the registrant chooses to compute significance using pro forma information, it must do so for all three significance tests.

- The acquired entity’s total assets and income from continuing operations before income taxes should NOT be adjusted for purchase accounting. That is, use the acquired entity’s historical amounts and the registrant’s pro forma amounts.

- The registrant’s pro forma amounts should only include those pro forma adjustments directly attributable to the transaction (e.g., purchase price allocation, depreciation, and amortization) in the pro forma statement of comprehensive income and balance sheet.

- Use the registrant’s pro forma annual balance sheet to determine significance even if that pro forma annual balance sheet is not presented or required to be presented in the Form 8-K.

- The registrant’s pro forma amounts should not give effect to either probable or insignificant acquisitions. S-X 3-05(b)(3) only permits measuring significance using the registrant’s pro forma amounts for (a) completed acquisitions that are (b) significant and (c) for which historical financial statements have been filed on Form 8-K.

2025.4Significance Implementation - Exchange Transaction (Acquisition and Disposition)

If the transaction is an exchange transaction in which the registrant and another party each contribute businesses to a joint venture (or the “Newco”) in exchange for an equity interest in the Newco measure the significance of the disposition (registrant’s contributed business) and the acquisition (other party’s contributed business) separately to determine whether pro forma information about the disposition and receipt of an equity investment is required, and whether audited financial statements of the business contributed by the other party are required.

Significance of the acquisition should be based on the acquired percentage of the other party’s business compared to the registrant’s historical financial statements (without adjustment for the related disposition of the business contributed by the registrant to the joint venture). Whether or not the transaction is accounted for at fair value, the investment test should be based on the fair value of the consideration given up or the consideration received, whichever is more reliably determinable.

If reporting of both the disposition and the acquisition are required by Form 8-K, a registrant may be unable to present a pro forma statement of comprehensive income depicting the joint venture formation because financial statements of the business contributed by the other party are not available. Those financial statements and related pro forma financial statements need not be filed until 71 calendar days after the date that the initial report reporting the transactions on Form 8-K must be filed (that is, the sum of 4 business days after the transaction is consummated plus 71 calendar days). Pro forma financial statements depicting a significant disposition are ordinarily required to be filed within 4 business days of the disposition. In these circumstances, the initial Form 8-K reporting the transaction should include a narrative description of the effects of the disposition, quantified to the extent practicable, and complete pro forma information depicting the effects of the exchange of interests should be filed at the time that the audited financial statements of the acquired business are filed.

2025.5Significance Implementation - In Existence for Less Than One Year

If the registrant and/or the acquiree has been in existence for less than one year, do not annualize the historical statement of comprehensive income; measure significance using the audited historical statement of comprehensive income that complies with the age of financial statement requirements (see Section 2045 for the acquiree and Section 1200 for the registrant), regardless of the number of months it includes. If the registrant or the acquiree has been in existence for more than one year, measure significance using income for full 12 months; do not adjust the audited statement of comprehensive income to equal the same number of months as acquiree or registrant that has been in existence for less than one year.

NOTE to SECTION 2025.5

Registrants may request a waiver from CF-OCA if they believe S-X 3-05 produces anomalous results.

2025.6Significance Implementation - Change in Fiscal Year

(Last updated: 3/31/2009)

If a registrant or acquiree has changed its fiscal year and the transition period (See definition at Section 1360.1) is less than 9 months, measure significance using either (A) the most recently completed audited fiscal year prior to the change or (B) audited financial statements for the 12 months ending on the last day of the transition period. If both the registrant and the acquiree have changed their fiscal years, registrants should measure significance using a consistent approach [either (A) or (B)] for both the registrant and the acquiree [not (A) for one and (B) for the other]. If the transition period is greater than 9 months, use the audited financial statements for that period.

2025.7Significance Implementation - Acquisition after a Reverse Acquisition

If an acquisition is made after a transaction accounted for as a reverse acquisition of the registrant but before the registrant’s audited financial statements for the fiscal year in which the reverse acquisition occurred are filed and the audited financial statements for the accounting acquirer have been filed with the SEC then measure significance against the accounting acquirer’s financial statements.

2025.8Significance Implementation - Acquisition after a Reverse Recapitalization

If an acquisition occurs after a reverse recapitalization of the legal target (see Topic 12) but before the registrant’s audited financial statements for the fiscal year in which the reverse recapitalization occurred are filed and the audited financial statements for the legal target have been filed with the SEC then measure significance against the legal target’s financial statements.

2025.9Significance Implementation - Acquisition after Shell Company Acquires Predecessor

If an acquisition is made subsequent to the acquisition by a shell company, as defined in Exchange Act Rule 12b-2, of an entity deemed the registrant’s predecessor (but not accounted for as a reverse acquisition or reverse recapitalization), then measure significance against the historical financial statements of the registrant.

2025.10Significance Implementation - Registrant is a Successor to a Predecessor Company

In certain cases, a registrant that is a successor to a predecessor company may not have a full year of statement of comprehensive income information available to use as the denominator in the calculation of the income test. In these cases, the significant subsidiary income test should be calculated using only the results of operations of the successor company in the denominator.

If the results are anomalous, CF-OCA will consider a request by the registrant to perform the significance test using pro forma amounts determined in accordance with S-X Article 11 as if the predecessor had been acquired at the beginning of the fiscal year being measured. The staff generally believes that combining the historical results of the successor and predecessor without S-X Article 11 pro forma adjustments is not an appropriate surrogate for the significance test. (Last updated: 3/31/2010)

2025.11Significance Implementation - Acquisition of a Business that is a Successor to a Predecessor Company

For the acquisition of a business that is the successor to a predecessor company (not the registrant), or when an acquiree’s historical financial statements include predecessor and successor periods, the measurement of significance under the income test will depend on the particular facts and circumstances.

If audited successor financial statements of the acquiree include twelve months of successor results, the income test should be applied in the normal fashion.

If audited successor financial statements of the acquiree include less than twelve months of successor results, it will generally be necessary to use pro forma amounts of the successor for the year determined in accordance with S-X Article 11. The objective of this process is to determine a surrogate for the annual historical statement of comprehensive income of the acquired business. Thus, the pro forma amounts would be determined using the basis of the acquired successor business – not the registrant’s subsequent new basis. The staff generally believes that combining the historical results of the successor and predecessor without S-X Article 11 pro forma adjustments is not an appropriate surrogate for the significance test. The convention of “9 months equals 12 months” in S-X 3-06 is not applicable in this situation. In these situations, CF-OCA should be consulted prior to filing.

If the most recent audited financial statements of the acquiree include only predecessor results, use the historical predecessor period statement of comprehensive income information as the numerator for calculating the income test. Pro forma information should not be used. (Last updated: 3/31/2010)

2025.12Significance Implementation - SAB 97 “Put-Together” Transactions

In transactions in which more than two entities combine concurrent with an IPO, measure significance against the accounting acquirer (regardless of whether or not the accounting acquirer is a Newco). All of the acquired businesses are considered related under S-X 3-05(a)(3) and S-X 8-04(a)(2) and therefore must be grouped and assessed for significance against the accounting acquirer as a single acquisition. See Section 2015.12. Because related businesses must be treated as a single business acquisition under S-X 3-05 and S-X 8-04, SAB 80 may not be applied to SAB 97 “put together” transactions. Upon written request, the staff will consider whether relief from the literal application of S-X 3-05 is appropriate.

2025.13Significance Implementation - Tests of significance after a SAB 97 “put-together” IPO

If a new acquisition takes place after an IPO but before the filing of the registrant’s first Form 10-K, measure significance against the audited financial statements of the accounting acquirer for the most recent fiscal year that was included in the IPO registration statement. If a new acquisition takes place after the filing of the registrant’s first Form 10-K, measure significance against the audited financial statements of the registrant for the most recent fiscal year in the Form 10-K. In some cases, such as when the IPO occurs close to the registrant’s year end, the registrant’s financial statements presented in Form 10-K may only include operations for a very short period of time. Upon written request, and depending on the proximity of the SAB 97 transaction to the balance sheet date, the staff will consider whether relief from the literal application of S-X 3-05 is appropriate.

2030Financial Statement Periods Required Under S-X 3-05 and S-X 8-04

2030.1See the table below for general requirements. Below the table are exceptions to the general requirements relating to: (Last updated: 7/1/2019)

- Omitting Acquiree Balance Sheet

- Form 10 and Smaller Reporting Company Registrant

- Initial Public Offerings – Using Pre-Acquisition and Post-Acquisition Audited Results

| If the Greatest of the Three Calculations Described in Section 2015 | S-X 3-05 | S-X 8-04 |

|---|---|---|

| Does not exceed 20% | No financial statements required. | No financial statements required. |

| Exceeds 20% but not 40% | Financial statements for the most recent fiscal year (audited) and the latest required interim period (unaudited) that precedes the acquisition (See FRM 2045), and the corresponding interim period of the preceding year (unaudited). | Financial statements for the most recent fiscal year (audited) and the latest required interim period (unaudited) that precedes the acquisition (See FRM 2045), and the corresponding interim period of the preceding year (unaudited). |

| Exceeds 40% but not 50% | Financial statements for the two most recent fiscal years (audited) and the latest required interim period (unaudited) that precedes the acquisition (See FRM 2045), and the corresponding interim period of the preceding year (unaudited). | Financial statements for the two most recent fiscal years (audited) and the latest required interim period (unaudited) that precedes the acquisition (See FRM 2045), and the corresponding interim period of the preceding year (unaudited). |

| Exceeds 50% | Financial statements for full three years (audited) and the latest required interim period (unaudited) that precedes the acquisition (See FRM 2045), and the corresponding interim period of the preceding year (unaudited). Exception: Financial statements for the earliest of the three fiscal years may be omitted if net revenues of the acquired business in its most recent fiscal year are less than $100 million. See also exception for EGCs in Section 10220.5. (Last updated: 10/30/2020) |

Financial statements for the two most recent fiscal years (audited) and the latest required interim period (unaudited) that precedes the acquisition (See FRM 2045), and the corresponding interim period of the preceding year (unaudited). |

2030.2Omitting Acquiree Balance Sheet - Balance sheet of the acquired company is not required when the audited annual balance sheet of registrant is as of a date after consummation of the acquisition.

2030.3[Reserved] (Last updated: 7/1/2019)

2030.4Initial Registration Statements – Using Pre-Acquisition and Post-Acquisition Audited Results - Registrants filing initial registration statements may apply the period of time in which the operations of an acquired business are included in the audited statement of comprehensive income of the acquirer to reduce the number of periods for which pre-acquisition statements of comprehensive income are required. However, registrants applying such an approach can have no gap between the audited pre-acquisition and audited post-acquisition periods. For example, if an acquisition is consummated on April 15, 2007 and the acquiree’s highest level of significance was 45%, S-X 3-05 would require the acquiree’s audited annual financial statements to be filed for the two years ended December 31, 2006 (assuming both registrant and acquiree have calendar year-ends). In lieu of financial statements for those periods, the staff will accept audited financial statements of the acquiree for the year ended December 31, 2006 and the period from January 1, 2007 through April 14, 2007 provided that audited financial statements of the registrant for the year ended December 31, 2007 have been filed.

2030.5Financial Statements in a Registration Statement of a Non-reporting Business Acquired, or to be Acquired, when One of the Combining Entities Meets the Smaller Reporting Company Criteria and the Other Does Not -

If the registrant/acquirer is subject to S-X 3-05, the non-reporting business’ financial statements must comply with S-X reporting requirements applicable to entities that are not smaller reporting companies. If the registrant/acquirer is subject to S-X Rule 8-04, the non-reporting business’ financial statements may comply with scaled reporting requirements for a smaller reporting company. These are the same requirements for filing financial statements of an acquired non-reporting business in a Form 8-K (see Section 2200.2), except for reverse acquisitions. There are different requirements for filing financial statements of a non-reporting target in an S-4 registration statement (see Section 2200.2). (Last updated: 12/31/2011)

2035Individually Insignificant Acquirees

2035.1Applicability - The requirement under S-X 3-05 to file financial statements of individually insignificant businesses under certain circumstances is applicable only to registration statements and proxies. Form 8-K does not require audited financial statements of insignificant acquirees unless they are "related businesses" and significant on a combined basis. See Section 2015.12, “Significance – Related Businesses”.

2035.2Definition - The reference in S-X 3-05 to individually insignificant acquisitions includes:

- any consummated acquisitions whose significance does not exceed 20% that were consummated after the balance sheet date of the most recent annual audited financial statements included in the registration or proxy statement through the effective date of the registration statement or the date the proxy statement is mailed;

- any probable acquisitions whose significance does not exceed 50%; and

- any consummated acquisitions whose significance exceeds 20%, but does not exceed 50%, for which financial statements are not yet required because of the 75-day rule in S-X 3-05(b)(4). (Last updated: 10/20/2014)

NOTE TO SECTION 2035.2

Why does the staff require the inclusion of significant acquired businesses for which financial statements are not yet required because of the 75-day rule [S-X 3-05(b)(4)] in the test of the aggregate significance of individually insignificant acquired businesses consummated since the most recent audited balance sheet date? [S-X 3-05(b)(2)]

In 1996, S-X 3-05 was amended to permit the exclusion of historical financial statements for certain significant acquisitions which did not exceed 50% significance [S-X 3-05(b)(4)(i)]. However, S-X 3-05(b)(4) was not intended to circumvent the requirement in S-X 3-05(b)(2) to consider the aggregate significance of all acquired businesses which were not yet filed. Therefore, even though a literal read of S-X 3-05(b)(4) might suggest that registrants may omit financial statements of significant businesses for which financial statements are not yet required because of the 75-day rule, the staff believes it is necessary to include those significant businesses in the analysis of the aggregate significance of individually insignificant acquisitions under S-X 3-05(b)(2). To do otherwise could lead to the presentation of financial statements for less than a mathematical majority of businesses acquired since the most recent audited balance sheet that have an aggregate significance in excess of 50%.

2035.3Financial Statements Required – Mathematical Majority - If the aggregate of either the asset, investment or income significance test of all insignificant acquisitions (i.e., (A), (B) and (C) above) exceeds 50%, provide financial statements for the mathematical majority (combined if appropriate) for the most recent fiscal year and the latest interim period preceding the acquisition. For purposes of determining the mathematical majority, audited financial statements should be provided for those probable and acquired entities that constitute more than 50% of the aggregate asset, income, or investment test determined to be the most significant. Consider the following example.

Example:

Example Facts: A registrant with a calendar year end files a registration statement which is effective October 2, 2008. The following individually insignificant business acquisitions, for which no audited financial statements were filed on Form 8-K, and significant businesses for which financial statements are not yet required because of the 75-day rule in S-X 3-05(b)(4) have occurred since the registrant’s audited financial statements were filed in its 2007 Form 10-K:

| Date Acquired | Investment Test % | Asset Test % | Income Test % | |

|---|---|---|---|---|

| Business A | 1/21/2008 | 10 | 19 | 8 |

| Business B | 2/24/2008 | 10 | 7 | 6 |

| Business C | 4/11/2008 | 11 | 6 | 5 |

| Business D | 7/7/2008 | 13 | 11 | 5 |

| Business E | 8/18/2008 | 17 | 10 | 21 |

| Probable F | N/A | 9 | 6 | 4 |

| Aggregate | 70 | 58 | 49 |

Example Analysis: Since the investment test yields the greatest significance on an aggregate basis (70%), financial statements of the businesses adding up to in excess of 35% under the investment test column must be provided. In this case, financial statements for any combination of three businesses that includes Business E or any combination of four businesses would meet the requirement. No combination of three that excludes Business E would meet the requirement. Financial statements of Business E are not yet required to be filed because of S-X 3-05(b)(4); therefore in this fact pattern, it is possible to use a combination of more than three businesses that excludes Business E even though Business E is significant under the income test. As shown in the example above, even though the registrant is not required to file a Form 8-K with audited financial statements of Business E until 11/3/2008, those financial statements may need to be included in the registration statement.

2035.4Significance – Financial Statements Used to Measure Significance

The aggregate significance of the individually insignificant acquisitions described in Section 2035.3 should be measured for each acquisition using the financial statements described in Section 2015.2 at the registration statement effective date. Measuring significance using the financial statements described in Section 2015.2 at the registration statement effective date may require the use of either financial statements for a more recent fiscal year than the annual financial statements used to measure significance at the acquisition date, or financial statements for the same fiscal year that have been retrospectively adjusted after the acquisition date for a change in accounting principle or a discontinued operation (see Section 2025.1). Therefore, the significance of an individually insignificant acquisition measured using the annual financial statements described in Section 2015.2 at the registration statement effective date may differ from the significance of that individually insignificant acquisition measured using the annual financial statements described in Section 2015.2 at the acquisition date. (Last updated: 3/31/2010)

NOTE TO SECTION 2035.4

An appropriate conclusion that an acquisition was not individually significant at the acquisition date is not changed by the measurement of the aggregate significance of individually insignificant acquisitions. For example, measuring the aggregate significance of individually insignificant acquisitions using the financial statements described in Section 2015.2 at the registration statement effective date may cause an acquisition that was appropriately determined to be individually insignificant at the acquisition date to have significance in excess of 20%. This calculated significance is used only to determine the aggregate significance of the individually insignificant acquisitions in accordance with the guidance in Section 2035.3; it does not change the conclusion of individual insignificance appropriately determined at the acquisition date. (Last updated: 3/31/2010)

2035.5Significance – Income Test – Entities with Pre-Tax Loss versus Entities with Pre-Tax Income - For purposes of the income test, S-X 1-02(w) Computational Note 3 indicates that entities reporting losses should not be aggregated with entities reporting income. Therefore, significance must be determined separately for both the group of individually insignificant acquisitions with income and the group of individually insignificant acquisitions with losses. The absolute values of the results of operations of the two groups should not be aggregated for purposes of determining significance. If the income test significance of either the group of individually insignificant acquisitions with income or the group of individually insignificant acquisitions with losses is higher than the significance computed under either the investment or asset tests in S-X 1-02(w), the absolute values of the income test significance of the two groups would be aggregated for purposes of selecting the mathematical majority.

For example: Assume registrant has $100 of income from continuing operations before income taxes for the year ended December 31, 2007. Registrant made the following acquisitions in 2008 and files a registration statement in December 2008.

| Date Acquired | Income (Loss) | Significance | Aggregate Acquirees with Income | Aggregate Acquirees with Loss | |

|---|---|---|---|---|---|

| Business A | 1/18/2008 | $(8) | 8% | 8% | |

| Business B | 2/4/2008 | 9 | 9% | 9% | |

| Business C | 3/17/2008 | (13) | 13% | 13% | |

| Business D | 6/13/2008 | 16 | 16% | 16% | |

| Business E | 7/3/2008 | (11) | 11% | 11% | |

| Business F | 8/4/2008 | 10 | 10% | 10% | |

| Probable G | N/A | 18 | 18% | 18% | |

| Aggregate | 21 | 21% | 53% | 32% |

Because some individually insignificant acquirees have income and some have losses, significance must be determined separately for both the group of individually insignificant acquisitions with income and the group of individually insignificant acquisitions with losses. Aggregate significance for purposes of S-X 3-05 is 85% (i.e., the sum of the absolute values of 53% and (32%)). Financial statements of a mathematical majority of all individually insignificant acquisitions, regardless of whether they had income or loss, must be filed. In this example, in order to compute the mathematical majority, the aggregate significance determined on an absolute value basis of the individually insignificant acquisitions filed must be at least 42.6% (i.e.50.1% of the 85% aggregate significance). For example, filing separate financial statements for Business C, Business D and Probable G would satisfy this requirement.

2035.6Significance – Using Pro Forma Financial Statements - S-X 3-05 permits a registrant to evaluate significance of acquirees using the pro forma financial information filed on Form 8-K in connection with a previous significant acquisition. However, a registrant may not circumvent the requirement to file audited data of a majority of individually insignificant acquirees by filing a Form 8-K containing financial statements of one or more insignificant acquirees and testing significance of the remaining unaudited acquirees, against either the historical or resulting pro forma financial statements. If a registrant has filed a Form 8-K for a previous significant acquisition, the 50% aggregation test may be applied against the pro forma financial statements included in that Form 8-K.

For example: A registrant files a registration statement on July 14, 2008 that includes audited financial statements for the year ended December 31, 2007 and interim period statements for the three months ended March 31, 2008. The registrant had total assets of $1,000 at December 31, 2007 and reported income from continuing operations before taxes of $100 for the year then ended. The registrant had, or expects to have, the following acquisitions since December 31, 2007

| See computational note below | Date Acquired | Investment $ |

Investment % |

Assets $ |

Assets % |

Income $ |

Income % |

Highest Significance |

|---|---|---|---|---|---|---|---|---|

| Significant acquisitions: | ||||||||

| Business A* | 4/7/2008 | 210 | 21 | 100 | 10 | 30 | 30 | 30% |

| Insignificant acquisitions: | ||||||||

| Business B | 2/4/2008 | 40 | 3 | 20 | 2 | 9 | 7 | N/A |

| Business C | 3/17/2008 | 60 | 5 | 40 | 3 | 13 | 10 | N/A |

| Business D | 6/13/2008 | 160 | 13 | 80 | 7 | 15 | 12 | N/A |

| Business E | 7/3/2008 | 50 | 4 | 20 | 2 | 11 | 9 | N/A |

| Probable F | N/A | 205 | 17 | 100 | 8 | 18 | 14 | N/A |

| Aggregate | 515 | 42 | 260 | 22 | 66 | 52 | 52% |

* Computational note: In this example, audited financial statements and pro forma financial information were filed on Form 8-K for Target A on 6/16/2008. Significance percentages in chart above are based on registrant’s election to measure significance using pro forma financial information giving effect to the acquisition of Business A. For purposes of this example, assume the pro forma financial information as of and for the year ended December 31, 2007 reflects purchase accounting as follows:

| Assets | Income | |

|---|---|---|

| Registrant historical | $1000 | $100 |

| Adjustments | 210 | 25 |

| Pro forma | $1210 | $125 |

In this example, the income test yields the highest aggregate significance test (52%). The registration statement must include financial statements for acquired businesses that total to more than 26% (50% * 52%) to meet the S-X 3-05 requirement. Had the aggregate significance under each test been less than 50% using pro forma information, no financial statements for any of the individual entities would be required in the registration statement.

2040When to Present Financial Statements

2040.1Financial statements of acquired businesses are required as follows:

| Form | Financial Statement Requirements |

|---|---|

| Registration Statements and Proxies |

|

| Form 8-K |

NOTE: While an Item 2.01 Form 8-K is not required for business acquisitions at or below 20% significance, registrants may elect to report business acquisitions at or below 20% significance pursuant to Item 8.01 of Form 8-K even if financial information is not provided. |

2040.2“Major Significance” and Previously Filed Acquiree Financial Statements Generally, previously filed financial statements of an acquired business need not be presented once the acquired operations are included in at least nine months of post-acquisition audited results unless the acquisition is of major significance [S-X 3-05(b)(4)(iii)]. Although the acquisition may be of major significance at lower thresholds due to factors specific to the registrant, the staff presumes that the acquisition is of such major significance that investors need previously filed financial statements of the acquired company in a registration or proxy statement if:

- the acquired business is included in audited results of the registrant for less than 21 months and its significance was equal to or greater than 70% and less than 80%; or

- the acquired business is included in audited results of the registrant for less than 33 months and was significant at the 80% or greater level.

If the acquired business is of major significance, the financial statements of the acquired business should continue to be presented in a registration or proxy statement for the number of periods prior to the acquisition such that the combination of pre- and post-acquisition periods presented cover the equivalent number of periods specified in S-X 3-02. [S-X 3-05(b)(4)(iii)]. The requirement to present the equivalent number of periods specified in S-X 3-02 does not mean that the audited periods presented must be continuous. Also, registrants should include the complete financial statements of the acquired business notwithstanding the reference to the statement of comprehensive income in the example provided in S-X 3-05(b)(4)(iii); however the balance sheets of the acquired business may be excluded by the registrant if the audited balance sheet of the registrant is as of a date after consummation of the acquisition.

2045Age of Financial Statements - Basics

2045.1This section covers three broad components:

- 1933 Act registration statements,

- Proxy statements, and

- Form 8-K.

See Section 2050 for a discussion of “Age of Financial Statements - Interaction of S-X 3-05(b)(4) and Instruction to Item 9.01 of Form 8-K”

2045.21933 Act Registration Statement - Age of Financial Statements – General

(Last updated: 6/30/2009)

The registrant should comply with age-of-financial-statement rules with respect to itself and all completed and probable acquirees at the effective date. Any updated financial statements required to be included or incorporated by reference as appropriate in the registration statement but which were not required to be filed previously in a specific Exchange Act report may be filed under cover of Form 8-K pursuant to Item 8.01.

For example: A registrant files a Form 8-K on August 6 (i.e., the 4th business day subsequent to consummation) reporting the acquisition of a business on July 31 that is not an accelerated filer or a large accelerated filer. That Form 8-K included unaudited financial statements for the 3 months ended March 31. If a registration statement is filed after August 12, the financial statements of the acquired entity must be updated through June 30 so that the acquired entity's financial statements meet the age of financial statement requirements of Regulation S-X. If the acquisition was consummated on or prior to June 30, updated financial statements would not be required.

2045.31933 Act Registration Statement - Age of Financial Statements - Delayed and Continuous Offerings

(Last updated: 3/31/2009)

After effectiveness, a domestic registrant has no specific obligation to update the prospectus except as stipulated by 1933 Act Section 10(a)(3) and S-K 512(a) with respect to any fundamental change. If an acquisition would be significant under S-X 3-05, management should consider whether the probability of consummation of the transaction would represent a fundamental change. It is the responsibility of management to determine what constitutes a fundamental change. The registrant should also consider whether individually insignificant acquisitions occurring subsequent to effectiveness, when combined with individually insignificant acquisitions that occurred after the most recent audited balance sheet in the registration statement but prior to effectiveness, may be of such significance in the aggregate that an amendment is necessary. Notwithstanding the guidance in Section 2045.3, offerings pursuant to effective registration statements cannot proceed if the significance of an acquisition exceeds 50% and financial statements have not been filed. See Section 2050.3.

2045.41933 Act Registration Statement - Age of Financial Statements - Well-Known Seasoned Issuers

“Well-known seasoned issuer” is defined in Regulation C, Rule 405. Automatic shelf registration statements and post-effective amendments of well-known seasoned issuers become effective immediately upon filing [Regulation C, Rule 462(e) and (f)]. Immediate effectiveness does not exempt a well-known seasoned issuer from the requirement to comply with the age of financial statement requirements with respect to itself and all completed and probable acquirees at the time of effectiveness. Consider the following examples.

Example 1: Consummated Acquisition in Excess of 50% Significant; Probable Acquisition in Excess of 50% Significant; or Aggregate of Individually Insignificant Acquisitions since the End of Registrant’s Most Recently Completed Fiscal Year is in Excess of 50% Significant

Financial statements of the acquired or to be acquired businesses for the periods specified by S-X 3-05 must be included or incorporated in the automatic shelf registration statement prior to filing the automatic shelf registration statement or post-effective amendment, even if such financial statements are not yet required to be filed on Form 8-K.

Example 2: Consummated or Probable Acquisition in Excess of 20% But Not in Excess of 50%

Financial statements of an acquired or to be acquired business that is significant in excess of 20% but not in excess of 50% need not be filed prior to the effective date (i.e., the filing date) of an automatic shelf registration statement or post-effective amendment filed by a well-known seasoned issuer if the effective date occurs during the 4 business days plus 71 calendar day period subsequent to consummation.

2045.51933 Act Registration Statement - Age of ANNUAL Financial Statements -

| Acquiree’s Filing Status | Effective date of Registration Statement | Acquiree Financial Statements |

|---|---|---|

| NOT an Accelerated Filer, and NOT a Large Accelerated Filer | Registrant’s filing is effective after 45 days but not more than 89 days after the acquiree’s fiscal year end | Updating requirement dependent on the registrant’s (not the acquiree’s) eligibility for relief under S-X 3-01(c). After a reverse acquisition accounted for as a business combination, consider the accounting acquirer's ability to meet the requirements of S-X 3-01(c) in determining the need to update. |

| Filing is effective after 89th day after acquiree’s fiscal year end | Acquiree’s most recent fiscal year must be audited | |

| Accelerated Filer | Registrant’s filing is effective after 45 days but not more than 74 days after the acquiree’s fiscal year end | Updating requirement dependent on the registrant’s (not the acquiree’s) eligibility for relief under S-X 3-01(c). After a reverse acquisition accounted for as a business combination, consider the accounting acquirer's ability to meet the requirements of S-X 3-01(c) in determining the need to update. |

| Filing is effective after 74th day after acquiree’s fiscal year end | Acquiree’s most recent fiscal year must be audited | |

| Large Accelerated Filer | Registrant’s filing is effective after 45 days but not more than 59 days after the acquiree’s fiscal year end | Updating requirement dependent on the registrant’s (not the acquiree’s) eligibility for relief under S-X 3-01(c). After a reverse acquisition accounted for as a business combination, consider the accounting acquirer's ability to meet the requirements of S-X 3-01(c) in determining the need to update. |

| Filing is effective after 59th day after acquiree’s fiscal year end | Acquiree’s most recent fiscal year must be audited |

NOTE TO SECTION 2045.5

For purposes of evaluating the financial statement updating requirements relating to a significant acquired or probable-to-be-acquired business, the reference in S-X 3-01(c)(2) to the registrant’s (or in a reverse acquisition, the accounting acquirer’s) “most recent fiscal year for which audited financial statements are not yet available” should be replaced with “the most recently completed fiscal year prior to the acquisition date” irrespective of whether or not those financial statements are available. (Last updated: 3/31/2010)

2045.61933 Act Registration Statement Age of Financial Statements- Requirement to File Acquiree’s ANNUAL Financial Statements that are More Recent than Registrant’s Financial Statements - In limited circumstances involving a registrant that would be required to update after the 45th day, applying this rule results in a requirement to file audited financial statements of the acquiree as of a date more recent than is required for the registrant. If the registrant believes providing updated audited financial statements would impose an unreasonable burden under the circumstances, the registrant may request CF-OCA to consider granting relief if the acquiree's financial statements are updated on an unaudited basis through either the registrant's latest balance sheet date or the acquiree's year-end. Requests for relief should be made in writing prior to filing.

For example: A registrant with a December 31, 2007 year end is required under S-X 3-01(c) to update its audited financial statements after February 14, 2008 in a registration statement. The registrant is acquiring a business with a November 30, 2007 year end. The acquired business is neither an accelerated filer nor a large accelerated filer. If the registration statement is effective February 1, 2008, the registration statement would require audited financial statements of the registrant for the year ended December 31, 2006 and unaudited financial statements for the nine months ended September 30, 2007. Unless relief is obtained, the target’s audited financial statements would be required for the year ended November 30, 2007 since February 1 is beyond 45 days after target’s year end and the registrant is not eligible for relief under S-X 3-01(c).

2045.71933 Act Registration Statement - Age of INTERIM Financial Statements - For interim period financial statements in a 1933 Act registration statement, age requirements are the same as if the acquiree were the registrant (see Section 1200), however the requirement to audit interim period information depends on whether the acquired business is a predecessor and, if not a predecessor, whether the registrant applied S-X 3-05 or SAB 80, which is discussed at Section 2070.

2045.81933 Act Registration Statement Age of INTERIM Financial Statements - Predecessor – If the acquired business is a “predecessor” of the registrant (See Section 1170), and the acquisition date is on or before the registrant’s most recent audited balance sheet required to be included in the registration statement, then interim financial statements of the predecessor should be presented and audited through the date of acquisition. If the acquired business is a “predecessor” of the registrant and the acquisition date is after the registrant’s most recent audited balance sheet required to be included in the registration statement, then interim financial statements of the predecessor should be presented for the same periods as if the predecessor were the registrant and may be unaudited. In this circumstance, the predecessor period between registrant’s latest balance sheet and acquisition date would need to be audited in registrant’s next Form 10-K.

2045.91933 Act Registration Statement Age of INTERIM Financial Statements –S-X 3-05 Acquiree– If significance is measured using S-X 3-05, interim financial statements of an acquired business need not be audited. Age requirements are the same as if the acquiree were the registrant. See Section 1200. Consequently, financial statements of an acquired business need not be updated if the omitted period is less than a complete quarter. However, disclosure of significant events occurring during the omitted interim period may be necessary.

For example: If an acquisition subject to S-X 3-05 or S-X 8-04 (i.e., not a predecessor) was consummated on September 29, the staff generally would not require that the financial statements of the acquired entity be updated past June 30. However, disclosure of significant events occurring during the omitted interim period may be necessary.

2045.101933 Act Registration Statement Age of INTERIM Financial Statements –S-X 3-05 Acquiree and Updating Form 8-K - In some cases, the financial statements provided in Form 8-K may need to be updated in a registration statement to comply with the 135-day rule (for an acquired business that is neither an accelerated filer nor a large accelerated filer) or the 130 day rule (for an acquired business that is either an accelerated filer or a large accelerated filer). See Section 1200.

For example: A registrant files a Form 8-K reporting an acquisition of a business that is neither an accelerated filer nor a large accelerated filer which occurred on July 10. The registrant and the acquiree have calendar fiscal year ends. The Form 8-K includes the acquiree’s interim financial statements as of March 31. The staff is likely to not accelerate the effective date of a registration statement filed in December of the same year unless the acquiree’s financial statements are updated through at least June 30.

2045.111933 Act Registration Statement Age of INTERIM Financial Statements - SAB 80 Acquiree- If significance is measured using SAB 80, see Section 2070, “SAB 80: Application of S-X 3-05 in Initial Registration Statements,” and the discussion in Section 2070.9, “Interim Financial Statements.”

2045.12Proxy Statements - Age of Financial Statements - For purposes of proxy statements, the staff interprets the updating requirements in the same manner as under the 1933 Act.

2045.13Form 8-K Age of Financial Statements - General. The staff believes that the age of financial statements in a Form 8-K should be determined by reference to the filing date of the Form 8-K initially reporting consummation of the acquisition. If no filing is made timely (on or prior to the 4th business day following the acquisition date), the age of financial statements required to be filed should be determined by reference to the 4th business day after the consummation of the acquisition. See Section 2045.17 for an exception to this position.

2045.14Form 8-K - Age of ANNUAL Financial Statements