Statement on Proposals Relating to Regulation Best Interest, Form CRS, Restrictions on the Use of Certain Names or Titles, and Commission Interpretation Regarding the Standard of Conduct for Investment Advisers

I would like to join Chairman Clayton in thanking the staff for their extremely hard work on these proposals. This truly was a Herculean task done in a very short period of time.

Over two hundred years ago, before any organized stock exchanges, twenty-four brokers came together under the leafy branches of a Buttonwood tree on Wall Street and established a new standard of conduct for stock trading. That agreement, known as the Buttonwood Agreement, was a mere two sentences long.[1] Those two sentences plainly set out the rules for stock trading and moderated the amount of commissions that could be charged to investors. The importance of those sentences cannot be overstated. That standard of conduct gave investors confidence, and brought stock trading out of the streets and coffeehouses and into stock exchanges, benefiting the entire American economy.

Today, we consider a package of proposals over 1,000 pages long, with more than 1,800 footnotes. Like the Buttonwood Agreement, this package also purports to establish a standard of conduct. Specifically, it purports to reform the way financial professionals interact with their retail clients, and to introduce new rules for financial professionals when they give advice. However, despite the hype, today’s proposals fail to provide comprehensive reform or adequately enhance existing rules. In fact, one might say, the Emperor has no clothes.[2]

For at least the last decade, investors have been asking for some type of fiduciary duty standard for broker-dealers who are giving advice.[3] Unfortunately, the proposals before the Commission today squander the opportunity to act in the best interest of investors. Instead, the proposals essentially maintain the status quo.

Regulation Best Interest

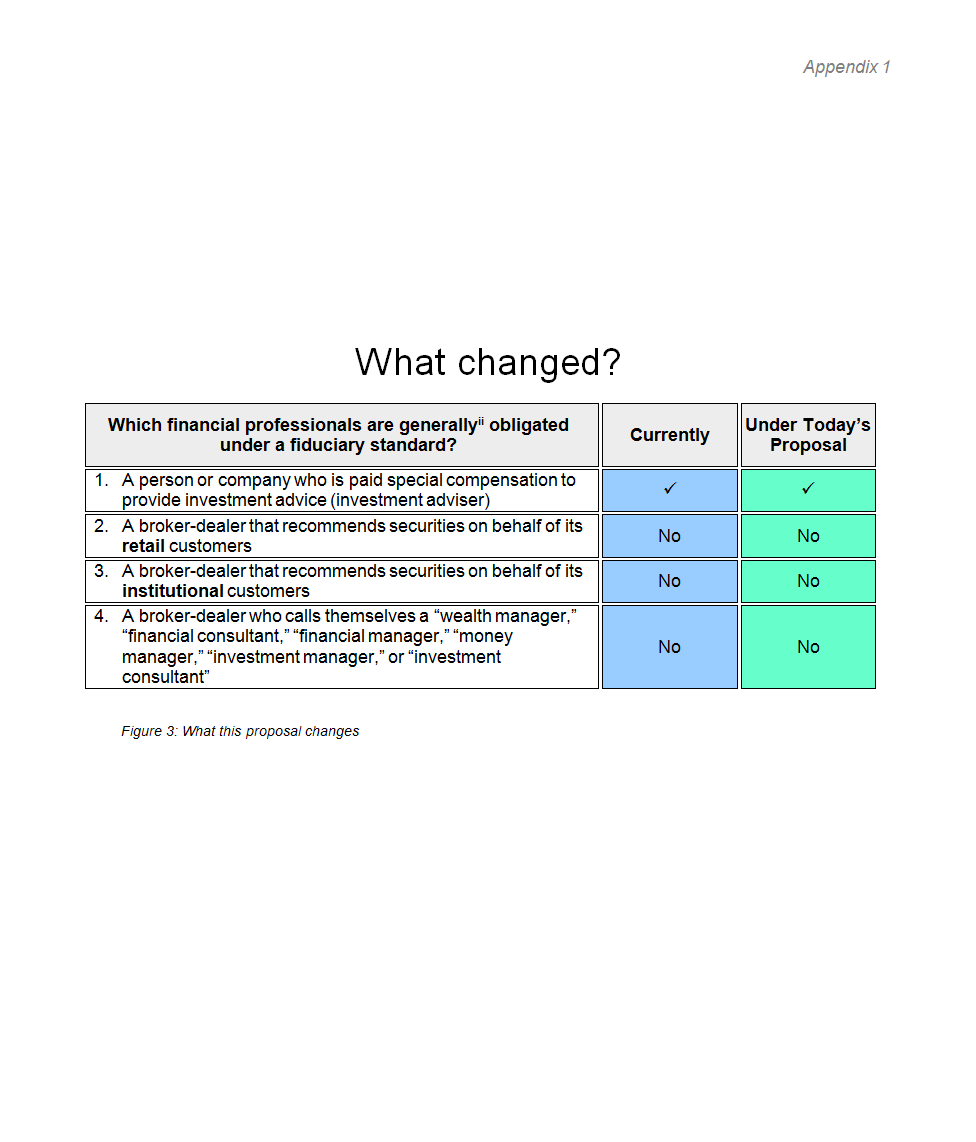

Let’s turn to the first of the proposed rules before us today—Regulation Best Interest. The Commission is engaging in this rulemaking because there is widespread concern that the current regulatory system for financial professionals does not adequately protect investors. Listening week after week to the Commission’s enforcement staff as they discuss their investigations into fraud, deceit, and misconduct involving financial professionals, it is clear to me that existing broker-dealer standards are not sufficient. The benchmark against which we should measure the efficacy of today’s proposed regulation is whether it will prevent this type of harm. Or, at a minimum, whether the proposal will make it easier for investors themselves—or the government—to help get their money back. I fear that this proposal may fall short of accomplishing either. Instead, it merely reaffirms that broker-dealers have to meet their suitability obligations,[4] requires some policies and procedures, and mandates a few disclosures. I said “reaffirms” because most of this is already required by FINRA or the federal securities laws.[5] With so much we could do to protect retail investors, it’s hard to fathom why we are being asked to vote on this particular proposal today.

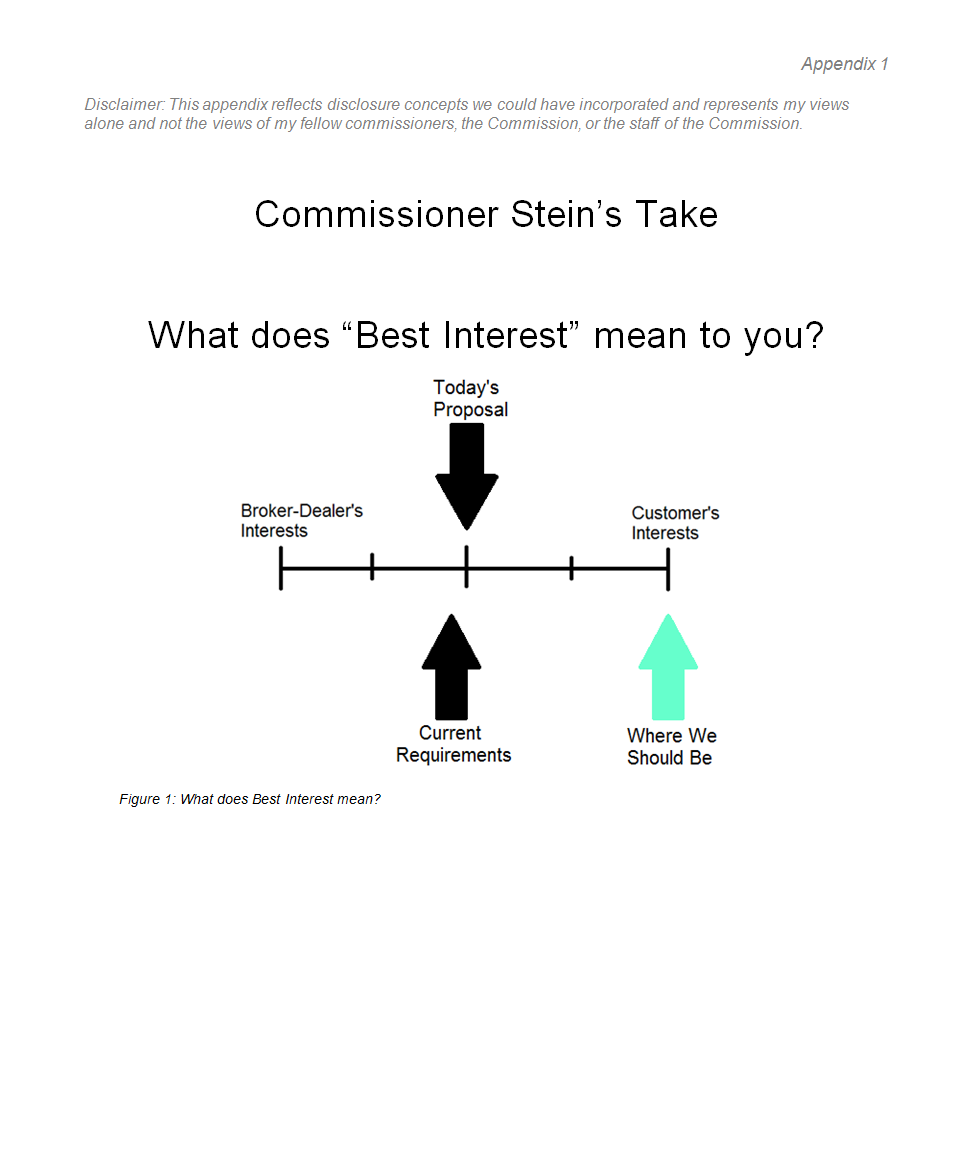

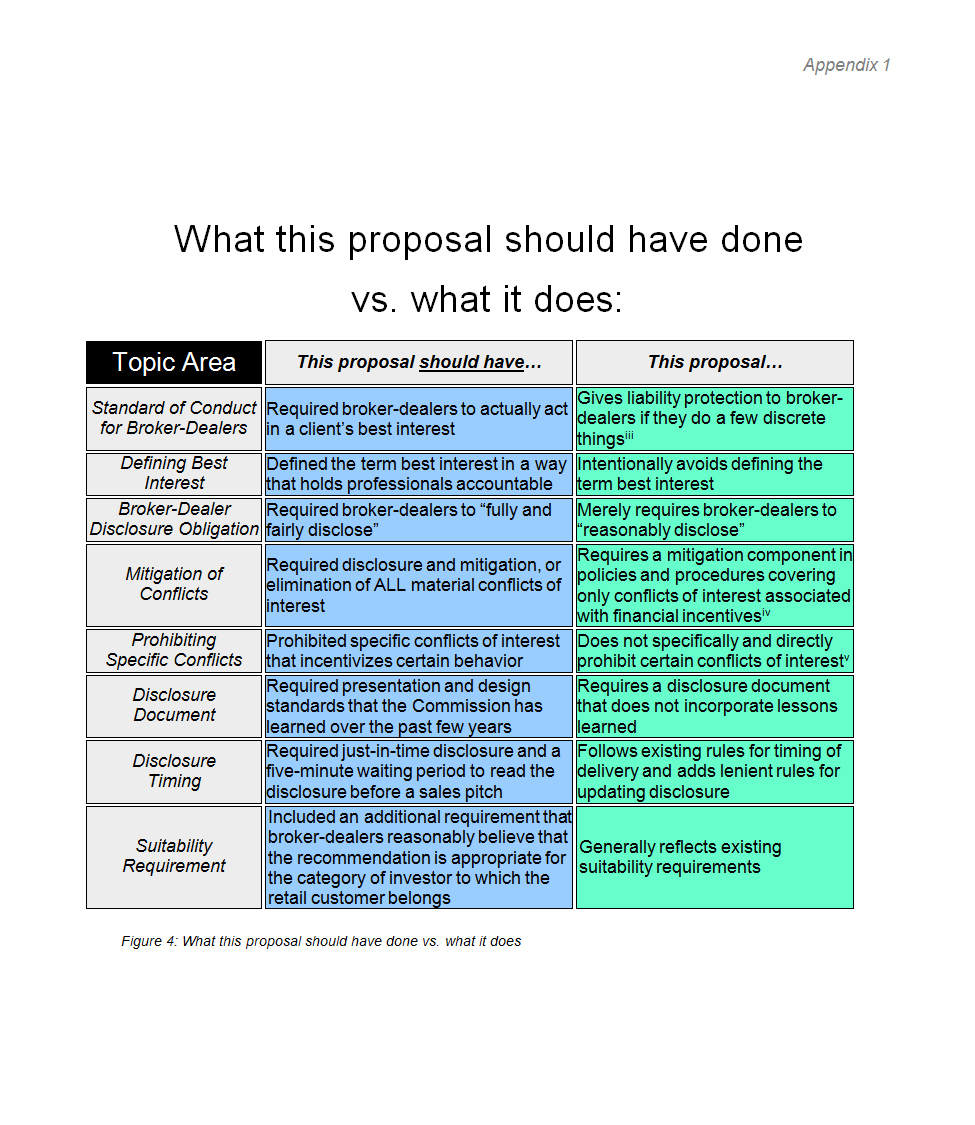

So what does the proposed rule do? Let’s start with its name—Regulation Best Interest. This name implies that when broker-dealers give advice they will be required to put their customers’ interests ahead of their own. Unfortunately, this is not the case under today’s proposal.[6] Despite repeated requests to define what best interest means in the rule text, it was decided that there was no need to define it.[7]

Instead, this proposal allows a broker-dealer to meet its “best interest” obligation by doing three things: providing some “reasonable” disclosure about its relationship with the customer, fulfilling what are essentially the existing standards for broker-dealer conduct (i.e., suitability),[8] and having reasonably designed policies and procedures to eliminate, or mitigate and disclose the broker-dealer’s competing interests. By doing these three things, the proposed regulation protects the broker-dealer from liability or penalty, or what lawyers call a “safe harbor.” It protects the broker-dealer, not the customer.

To state it differently, does this proposal require financial professionals to put their customers’ interests first, and fully and fairly disclose any conflicting interests? No. Does this proposal require all financial professionals who make investment recommendations related to retail customers to do so as fiduciaries? No. Does this proposal require financial professionals to provide retail customers with the best available options? No.

Could we have proposed a best interest standard? Yes, we could have proposed such a standard.[9] Unfortunately, today we are not. We also could have made the provisions in the proposed safe harbor serve as a floor, instead of a ceiling. Instead, the proposal merely requires broker-dealers to meet certain minimal obligations in order to get the protections of the safe harbor and thus be in compliance with their “best interest standard.”[10]

In addition, as I mentioned previously, because there is no definition of the best interest standard in the proposal, the name of the rule, in and of itself, is confusing. Calling the proposal Regulation Best Interest could cause retail investors to reasonably believe that broker-dealers are required to act in their clients’ best interests. Perhaps it would be more accurate to call this proposal “Regulation Status Quo.” Calling it Regulation Best Interest is not just confusing, it is in effect a form of mislabeling, which may be misleading and which could have deleterious consequences.[11] Indeed, one of the recommendations we are considering today is a proposal to restrict the use of the terms “advisor” and “adviser” by a broker-dealer unless it is also registered as an investment adviser. We should be logically consistent ourselves.

So what else could we have done? Well, we could have required broker-dealers to actually eliminate or mitigate conflicts of interest, instead of requiring broker-dealers to have reasonably designed policies and procedures. We could have required broker-dealers to provide “full and fair” disclosure, instead of just “reasonable” disclosure. Moreover, we could have made a few small tweaks to the current suitability standard, so that relief could be obtained for all investors when broker-dealer misconduct is widespread.[12] In sum, we could have expected more from financial professionals who provide retail investors with investment advice. If they are going to give advice in the first place, broker-dealers should truly act in the best interest of their customers given the impact this advice can have on retail investors’ financial well-being.[13]

Furthermore, I am concerned that this rule will not only confuse retail investors, but also broker-dealers. In particular, the lack of a definition of best interest, the use of similar terms to mean different things,[14] the use of different terms to mean the same things,[15] and the possibility that the SEC and FINRA interpret the same language in their suitability standards differently.[16] All of these concerns would make it difficult for the industry to discern a clear compliance path. Any resulting confusion may well result in higher compliance costs for broker-dealers, which will likely be passed onto the investor. What’s more, the lack of a clear standard is not likely to give investors more confidence in the broker-dealer business model.

I still have many questions regarding proposed Regulation Best Interest. Indeed, I invite the public to weigh in on the many questions, which will be contained in an appendix to this statement posted online.

Relationship Summary

The remainder of today’s package, while in some respects less concerning than proposed Regulation Best Interest, nonetheless stops short of proposing meaningful change.[17] The second component of today’s package concerns how investment professionals should communicate with their clients. Throughout its history, the Commission has placed reliance on full and fair disclosure as a component of its investor protection mandate. When it’s done well, fair and objective disclosure is fundamental to sound decision-making. Relevant and reliable information allows the public to make informed decisions about what to purchase—whether it’s a type of car, a type of milk, a type of stock, or in the case at hand, the type of financial professional to hire. Simply put, good disclosure empowers a person to decide for him or herself the appropriate course of action. However, disclosure must have the appropriate form and content. And it must be presented at the appropriate time for it to be meaningful and effective. Today’s proposal is disappointing in this regard.

Today’s proposal is intended to help cure investor confusion. More specifically, it is designed to help retail investors understand the difference between hiring an investment adviser versus hiring a broker-dealer. To this end, the proposal would require an investment adviser or a broker-dealer to provide a brief relationship summary to retail investors to inform them about the relationships and services it offers. The summary would also describe the standard of conduct under which the adviser or broker-dealer operates, its fees, specified conflicts of interest, and whether it has reportable legal or disciplinary events.[18] To be sure, these are areas where disclosure might help cure investor confusion. The question I have, though, is whether we are proposing disclosure that is both too generic and too legalistic such that retail investors won’t bother to read it. We are all too familiar with the stilted boiler-plate jargon that riddles today’s corporate disclosure documents. And we, at the Commission, understand far more about what makes disclosure effective than is evident in today’s proposed rules. Take the following passage from the mock relationship summary:

We must act in your best interest and not place our interests ahead of yours when we recommend an investment or an investment strategy involving securities. When we provide any service to you, we must treat you fairly and comply with a number of specific obligations. Unless we agree otherwise, we are not required to monitor your portfolio or investments on an ongoing basis.[19]

These three sentences are intended to describe a broker-dealer’s obligation to its retail clients. But what I am asking is whether this passage would be effective in curing retail investor confusion regarding the obligation it is describing. As an initial matter, the disclosure is confusing. What does best interest mean? We may never know because Regulation Best Interest, as I described earlier, does not define what best interest means.[20] Furthermore, would this disclosure stand up to the test of a high-pressure sales situation, where the investment professional uses every tactic in the book to entice the investor to sign on the dotted line? If, as commenters have suggested in the Commission’s Study on Investment Advisers and Broker-Dealers, “retail investors…find the standards of care confusing…,”[21] a simplified recitation of a broker-dealer’s obligation goes only part of the way.

We should be proposing disclosure that goes a step further. The disclosure should provide a retail investor with a meaningful understanding of the application of the obligations to the investor. In other words: What does best interest mean to me, in my particular situation? Or, with respect to fees, how much would I pay per year for an advisory account? How much for a typical brokerage account? What would my return be without netting fees? What would make those fees less or more? Without these types of disclosures, we will likely run the risk that a retail investor simply glances at these words and shoves them in the back of the file cabinet, or worse, the recycling bin, along with the rest of the boilerplate disclosure he or she receives.

In fact, today’s proposal in some ways recognizes the inadequacy of the proposed disclosure. At the end—not the beginning—of the relationship summary is a list of “Key Questions to Ask.”[22] The release states that these questions are “intend[ed] to encourage retail investors to have conversations with their financial professionals about how the firm’s services, fees, conflicts and disciplinary events affect them.”[23]

Let’s think about this for a moment. We are asking a retail investor to flip through four pages of boilerplate text, read through a series of questions, and then take the initiative to engage in a conversation with his or her financial professional about matters with which he or she may not be familiar. Why are we, in effect, placing the onus on a retail investor to cure his or her own confusion? Shouldn’t we be helping financial professionals develop disclosure that would help cure such confusion? What’s more, the efficacy of this approach is wholly dictated by the veracity of the financial professional’s oral responses. And when you combine this with the proposal’s delivery and extremely generous updating requirements,[24] I wonder if what is being proposed will actually spawn more confusion. I fear that this proposed disclosure will not only fail to add incremental value, but may also draw attention away from specific, decision-useful information.

Perhaps we could expect retail investors to flip through and take seriously four pages of boilerplate language if its presentation was visually dynamic and engaging. But, here too, the proposal falls short. And we, at the Commission, don’t have any excuse, to boot. We have learned over the years—most recently at the October 2017 Investor Advisory Committee meeting[25] and the March 2017 POSITIER Evidence Summit[26]— that using certain visual, design-oriented techniques could get more investors to pay attention to the “fine print.”[27] Some examples include:

- providing disclosure in the form of tables, bullet point lists, check lists, and other formats that provide greater structure and comprehensibility;

- using more white space, avoiding the temptation to overcrowd the communication;

- color-coding information to illustrate parts of the disclosure more effectively; or

- illustrating the disclosure content with visuals like icons, charts, pictograms, and other media that take it out of abstract text and ground it through imagery.[28]

What does today’s proposal do on this front? It states that “firms would be permitted to use charts, graphs, tables, and other graphics or text features to explain the information, so long as the information is responsive to[,] and meets the requirements in[,] the Instructions (including the space limitations).”[29] Not especially encouraging in its use of new techniques.

I recognize that we and our staff at the Commission are not necessarily graphic artists, but we would be foolish not to at least try and capitalize on what we’ve learned from those who are. We could propose that the relationship summary explicitly require these elements and request comment on specific forms that may work. In fact, I invite the public to review an example—which will be posted in another appendix to this statement online—of some forms of presentation today’s proposal could have utilized. I also recognize that there may be cost or administrative challenges for firms to provide more personalized disclosure. But, again, this is a proposal. If we are trying in earnest to help retail investors understand what they are getting into, we should at the very least try to sufficiently advance the ball.

Restrictions on the Use of Certain Names or Titles

The third element of today’s package is a proposal to restrict a broker-dealer from using the words “adviser” or “advisor” in its name or title when communicating with a retail investor, unless the broker-dealer is a registered investment adviser. This proposal, like the relationship summary, moves in the right direction. But more can, and should be done. After all, restricting the use of only two words presents an obvious “whack-a-mole” problem.

It seems to me that a broader, more principles-based approach would prove far more effective. For example, we could preclude a broker-dealer from “holding itself out” as an investment adviser to the extent it is not an investment adviser or acting in an advisory capacity. Perhaps this could take the form contained in the money market funds rule?[30] Or it could be premised on the antifraud concept of a materially misleading statement? I welcome comment on what might be the most effective approach to achieve this end, taking into account the Commission’s authority and any other legal concerns. In particular, I hope that the public provides strong empirical data that quantifies the harm to investors, individually and in the aggregate, that would occur if the Commission does not adopt a “holding out” approach.[31]

Proposed Commission Interpretation on Investment Adviser’s Fiduciary Duty

The final component of today’s package is a proposed Commission interpretation of the fiduciary duty owed by an investment adviser.[32] Importantly, the proposed interpretation is limited to certain aspects of an adviser’s fiduciary duty under section 206 of the Advisers Act.[33] And, even then, it is not intended to be an exhaustive resource.[34] I understand that an adviser’s fiduciary obligations are seen by some as ambiguous. I think clarification of the law is always a good thing. I am just a little confused as to why the Commission might be in the best position to issue interpretive guidance on an area that is heavily informed by decades of common law. I am also worried that, by limiting the interpretation to those duties under section 206, we may be, indirectly, suggesting a narrowing of an adviser’s broader fiduciary duties.

Conclusion

Unfortunately, the problem we are attempting to address is an insidious one. We must remember that today’s proposals will have real effects on real people.[35] After all, most investors will not realize that they should have been earning a higher return or haven’t been presented with the best investment options.[36] Our decision regarding the standard to which a financial professional must be held may affect someone’s ability to buy a new home, send a child to college, or retire. The impact of the proposed rules is especially important in today’s era, with most employers no longer providing pension plans.[37] This makes it all the more important that we give retail investors a fighting chance. Their future depends upon us getting this right. When the question is whether to defer to financial professionals’ historical practices that have caused known harm, or to give investors better disclosure and better advice, we should err on the side of the retail investor. It is the financial professionals who have the information and the ability to fix the problem—not their customers. Thus, when there is a question of where the burden of uncertainty should rest—it should rest with the more informed party—the financial professional. Unfortunately, today’s package of proposals in many ways continues to place the burden on the retail investor. What’s more, I believe the proposals, in their recommended forms, would make it difficult for the Commission to adopt materially improved rules going forward. As a result, I find myself unable to support today’s package of proposals.

Commissioner Stein’s Requests for Comment

General

- Should the Commission’s proposal require financial professionals to provide their retail customers with unconflicted investment advice?

- Should the Commission’s proposal require all financial professionals to put the interests of retail customers first, before their own interests? Why or why not?

- Should the Commission’s proposal allow different standards for different groups that give investment advice to retail investors? For example, should the Commission require investment advisers to be impartial and disinterested on an ongoing basis, but subject other investment intermediaries (such as broker-dealers) to episodic standard of conduct? Why or why not?

“Best Interest”

- Should the Commission’s proposal define what “best interest” means? Should the Commission adopt the following definition:

“To act in the best interest” means when a broker, dealer, or natural person who is an associated person of a broker or dealer, makes a recommendation, the recommendation reflects the care, skill, prudence, and diligence that a prudent person acting in a like capacity and familiar with such matters would use taking into consideration all of the facts and circumstances, including the investment profile of the Retail Customer to whom the recommendation is made?

If the Commission does not define “best interest,” will broker-dealers and their customers understand their obligation?

- How does a broker-dealer’s obligations to retail customers change under the Commission’s proposal? The current suitability standard requires broker-dealers to give recommendations that are in the best interest of their clients. How is the proposal different than the current standard?

- What is the difference between the following three standards of conduct that would be applicable to broker-dealers:

- Proposed Regulation “Best Interest” for retail customers;

- FINRA’s suitability standards for other non-institutional customers; and

- FINRA’s institutional suitability obligations for institutional customers?

- Should dually registered advisers (broker-dealers and investment advisers) be required to tell their retail customers, in writing, when they switch between roles? For example, should retail customers be told when a registered financial adviser with a fiduciary duty switches to a financial advisor with no fiduciary duty (e.g., proposed Regulation Best Interest)? Should retail customers receive notice of the implications of this change?

- Should broker-dealers who agree to monitor their clients’ accounts be subject to the proposed best interest standard? Or should they be required to register as investment advisers or held to a fiduciary standard?

- Should broker-dealers who have discretionary authority over their customers’ accounts be required to register as investment advisers or held to a fiduciary standard?

- Should the Commission’s proposed best interest standard apply only to “securities transactions” or to “transactions involving securities”?

Material Conflicts

- Should the Commission’s proposal require broker-dealers to eliminate or mitigate and disclose all material conflicts of interest? Why or why not?

- The Commission’s proposal does not prohibit any material conflicts. Should the Commission’s proposal prohibit certain material conflicts of interest? Why or why not?

- Should individual broker-dealers, as well as broker-dealer entities, be required to mitigate and disclose their conflicts of interest?

- How is the proposed requirement for a broker-dealer to “reasonably disclose” material facts related to the scope and term of the relationship different from existing obligations under the federal securities laws, state law, and self-regulatory organization rules? Should we require broker-dealers—who possess greater information than their retail customers—to fully and fairly disclose the scope and terms of the relationship?

- Should the “reasonableness” of a recommendation depend only upon the suite of products offered by the broker-dealer? For example, should a broker-dealer consider other products in the marketplace, such as those that are offered by other firms?

Public Interest and Investor Protection

- Should the Commission promulgate this rule under the anti-fraud provisions of the Exchange Act?

- Is this rule, given the safe harbor it contains, enforceable by the Commission? What proof would be necessary to bring an action? How does the safe harbor relate to the intended purpose of the rule, to ensure that broker-dealers make recommendations that are in their customers’ best interest? Would there be unintended consequences?

- How would the proposal advance the Commission’s ability to obtain recompense for all the victims of widespread breaches of the suitability requirement? Would the Commission need to prove the unsuitability of the recommendation for each, of possibly thousands, of harmed customers? For instance, should the Commission have required broker-dealers to reasonably believe that the recommendation is appropriate for the category of investor to which the retail customer belongs?

- Should the proposed “best interest” standard be confined to the safe harbor contained in the rule, or should it be a larger, more encompassing obligation?

- Should a broker-dealer’s obligation be limited to the moment in time in which the recommendation is made? Are there circumstances in which that recommendation should be updated if it has not yet been acted on?

[1] “We the Subscribers, Brokers for the Purchase and Sale of Public Stock, do hereby solemnly promise and pledge ourselves to each other, that we will not buy or sell from this day for any person whatsoever, any kind of Public Stock, at a less rate than one quarter per cent Commission on the Specie value and that we will give a preference to each other in our Negotiations.” Buttonwood Agreement, available at http://www.sechistorical.org/collection/papers/1790/1792_0517_NYSEButtonwood.pdf.

[2] Hans Christian Andersen, “The Emperor’s New Clothes.”

[3] “Nearly all U.S. investors support the fiduciary standard for investment professionals providing advice….[T]he person providing the advice should put your interests ahead of theirs and should have to tell you upfront about any fees or commissions they earn and any conflicts of interest that potentially could influence that advice.” Info Group|ORC, U.S. Investors & The Fiduciary Standard: A National Opinion Survey at 4 (Sept. 15, 2010), available at https://www.cfp.net/docs/public-policy/us_investors_opinion_survey_2010-09-16.pdf?sfvrsn=2.

“More than nine out of ten (93 percent) Americans said it is important that all financial advisors be legally required to put their clients’ best interests first when providing retirement investment advice”, Financial Engines, In Whose Best Interest? What Americans know and what they want when it comes to retirement investment advice at 1 (Mar. 2016), available at https://financialengines.com/docs/financial-engines-best-interest-report-040416.pdf.

“An overwhelming majority of retirement account holders ages 25+…believe it is important for financial advisors to give financial advice in a client’s best interest.” S. Kathi Brown, Attitudes Toward The Importance of Unbiased Financial Advice, AARP Research (May 2016), available at https://www.aarp.org/research/topics/economics/info-2016/attitudes-toward-unbiased-financial-advice.html (including findings from a national survey of adults ages 25 and older conducted in 2016).

[4] See, e.g., Proposing Release, Regulation Best Interest (“Proposing Release”) at Section I. n.6. (“FINRA and a number of cases have interpreted FINRA’s suitability rule as requiring a broker-dealer to make recommendations that are ‘consistent with his customers’ best interests’ or are not ‘clearly contrary to the best interest of the customer….’”) (internal citations omitted); Proposing Release, at Section I. n.7 (“As discussed herein, some of the enhancements that Regulation Best Interest would make to existing suitability obligations under the federal securities laws, such as the collection of information requirement related to a customer’s investment profile, the inability to disclose away a broker-dealer’s suitability obligation, and a requirement to make recommendations that are ‘consistent with his customers’ best interests,’ reflect obligations that already exist under the FINRA suitability rule or have been articulated in related FINRA interpretations and case law. Unless otherwise indicated, our discussion of how Regulation Best Interest compares with existing suitability obligations focuses on what is currently required under the Exchange Act.”) (internal cross-references omitted) (emphasis added).

[5] I note that there are three arguable improvements in the proposed rule and the guidance in the release text. First, the definition of churning has been expanded. See Proposing Release, at Section II.D.2.c. And second, the rule requires policies and procedures reasonably designed to mitigate certain material conflicts of interest arising from financial incentives associated with recommendations. See Proposing Release, at Section II.D.3. Finally, there may be some benefit to consolidating certain provisions that apply to broker-dealers under one federal regime. However, I do not believe that these modest improvements overcome the harm caused by the confusion over what “best interest” means.

See Proposing Release, at Section I.A. (“As noted, broker-dealers are subject to comprehensive regulation under the Exchange Act and SRO rules, and a number of obligations attach when a broker-dealer makes a recommendation to a customer. Under the federal securities laws and SRO rules, broker-dealers have a duty of fair dealing, which, among other things, requires broker-dealers to make only suitable recommendations to customers and to receive only fair and reasonable compensation. Broker-dealers are also subject to general and specific requirements aimed at addressing certain conflicts of interest, including requirements to eliminate, mitigate, or disclose certain conflicts of interest.”); Section I.A. nn.9-14; Section II.D n. 175 (“Exchange Act Rule 10b-10, which generally requires a broker-dealer effecting customer transactions in securities (other than U.S. savings bonds or municipal securities) to provide written notification to the customer, at or before completion of the transaction, disclosing information specific to the transaction, including whether the broker-dealer is acting as agent or principal and its compensation, as well as any third-party remuneration it has received or will receive. 17 CFR 240.10b-10. See also Exchange Act Rules 15c1-5 and 15c1-6, which require a broker-dealer to disclose in writing to the customer if it has any control, affiliation, or interest in a security it is offering or the issuer of such security. 17 CFR 240.15c1-5 and 15c1-6. There are also specific, additional obligations that apply, for example, to recommendations by research analysts in research reports and to public appearances under Regulation Analyst Certification (AC). See, e.g., 17 CFR 242.500 et seq. Finally, SRO rules apply to specific situations, such as FINRA Rule 2124 [Net Transactions with Customers]; FINRA Rule 2262 [Disclosure of Control Relationship with Issuer], and FINRA Rule 2269 [Disclosure of Participation or Interest in Primary or Secondary Distribution].”); Section II.D. n.176 (noting that “[b]roker-dealers are liable under the antifraud provisions for failure to disclose material information to their customers when they have a duty to make such disclosure”; that “a broker-dealer’s duty to disclose material information under the antifraud provisions is broader when the broker-dealer is making a recommendation to its customer”; and that “broker-dealers generally are liable under the antifraud provisions if they do not give ‘honest and complete information’ or disclose any material adverse facts or material conflicts of interest, including any economic self-interest.”) (internal citations omitted); Section II.D.1.c. n.207 (“For example, the Commission has indicated that failureto disclose the nature and extent ofa conflict of interest may violate Securities Act Section 17(a)(2).”); Section II.D.1.c. n.208 (noting that brokers must give “honest and complete information when recommending a purchase or sale”); Section II.D.2.b. n.239 (noting that, “a broker’s recommendation must be suitable for the client in light of the client’s investment objectives”, that brokers must only make recommendation for which they have “reasonable grounds to believe me[e]t the customers’ expressed needs and objectives.”).

[6] Proposing Release, at Section II.A. (“In other words, the broker-dealer’s financial interest can and will inevitably exist, but these interests cannot be the predominant motivating factor behind the recommendation.”) (emphasis added); Proposing Release, at Section II.B. (“We believe that a broker-dealer would violate proposed Regulation Best Interest’s Care Obligation and Conflict of Interest Obligations, if any recommendation was predominantly motivated by the broker-dealer’s self-interest (e.g., self-enrichment, self-dealing, or self-promotion) . . . .””) (emphasis added).

[7] Proposing Release, at Section II.B. (“We are not proposing to define ‘best interest’ at this time.”).

[8] To make matters worse, we are allowing the reasonableness of their recommendations to be judged only by the products that they themselves offer, not by what they could have reasonably offered. There is no obligation to present the best available options. Proposing Release, at Section II.B. (“broker-dealers generally should consider reasonably available alternatives offered by the broker-dealer as part of having a reasonable basis for making the recommendation”).

[9] See Section 913(g) of the Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. 111-203 (2010), available at https://www.gpo.gov/fdsys/pkg/PLAW-111publ203/pdf/PLAW-111publ203.pdf (“The Commission may promulgate rules to provide that the standard of conduct for all brokers, dealers, and investment advisers, when providing personalized investment advice about securities to retail customers (and such other customers as the Commission may by rule provide), shall be to act in the best interest of the customer without regard to the financial or other interest of the broker, dealer, or investment adviser providing the advice.”).

For instance, we could have defined “to act in the best interest” to mean that when a broker, dealer, or natural person who is an associated person of a broker or dealer, makes a recommendation, the recommendation reflects the care, skill, prudence, and diligence that a prudent person acting in a like capacity and familiar with such matters would use taking into consideration all of the facts and circumstances, including the investment profile of the retail customer to whom the recommendation is made.

[10] Proposing Release, at Section VIII. § 240.15l-1(a)(2) (noting that “[t]he best interest obligation in paragraph (a)(1) shall be satisfied if” the broker-dealer provides reasonable disclosures about the scope and terms of the relationship, fulfills the suitability standard, and has policies and procedures regarding conflicts of interest) (emphasis added).

[11] In other contexts, there are rules prohibiting deceptive or misleading names. For example, Section 35(d) of the Investment Company Act of 1940 (“Investment Company Act”) makes it “unlawful for any registered investment company to adopt as a part of the name or title of such company . . . any . . . words that the Commission finds are materially deceptive or misleading. . . .” In this context, mutual funds cannot include a type of investment or industry in the fund name without “adopt[ing] a policy to invest, under normal circumstances, at least 80% of the value of its Assets in the particular type of investments, or in investments in the particular industry or industries, suggested by the Fund's name.” See rule 35d-1 under the Investment Company Act [17 C.F.R. § 270.35d-1].

[12] For example, we could have required broker-dealers to reasonably believe that their recommendation are not only suitable for “some customer,” but for the category of customer to which the retail customer belongs.

[13] For instance, the Commission has explained the impact of fees on investment portfolios: “fees may seem small, but over time they can have a major impact on your investment portfolio. . . . In 20 years, 1.00% annual fees reduce [a $100,000] portfolio . . . by $30,000 compared to a portfolio with a 0.25% annual fee.” SEC, Updated Investor Bulleting: How Fees and Expenses Affect Your Investment Portfolio, September 8, 2016, available at https://www.investor.gov/additional-resources/news-alerts/alerts-bulletins/updated-investor-bulletin-how-fees-expenses-affect.

[14] Proposing Release, at Section II.C.4. (“The proposed definition of ‘retail customer’ also differs from the definition of ‘retail investor’ proposed in the Relationship Summary Proposal. . . .”).

[15] Proposing Release, at Section II.A. (“We request comment below, however, on whether our proposed rule should instead incorporate the ‘without regard to’ language set forth in Section 913 and the 913 Study recommendation, which we believe would also generally correspond to the DOL’s language in the BIC Exemption, but interpret that phrase in the same manner as the ‘without placing the financial or other interest . . . ahead of the interest of the retail customer’ approach set forth above.”) (quoting the rule text in Regulation Best Interest in the second instance).

[16] Proposing Release, at Section I.B. n.89 (“Generally, when a requirement of proposed Regulation Best Interest is based on a similar SRO standard, we would expect – at least as an initial matter – to take into account the SRO’s interpretation and enforcement of its standard when we interpret and enforce our rule. At the same time, we would not be bound by an SRO’s interpretation and enforcement of an SRO rule, and our policy objectives and judgments may diverge from those of a particular SRO. Accordingly, we would also expect to take into account such differences in interpreting and enforcing our rules.”).

[17] Today’s proposals have been presented as a package of interrelated rules and form changes. For this reason, while there will be distinct votes on each recommendation, I view today’s proposals as they have been presented—as a singular package of proposals.

[18] See Proposing Release, Form CRS Relationship Summary; Amendments to Form ADV; Required Disclosures in Retail Communications and Restrictions on the use of Certain Names or Titles (“CRS Proposing Release”), at Section II.

[19] See Proposed Broker-Dealer Mock Relationship Summary. See also Proposed Form ADV, Part 3: Instructions to Form CRS (“Proposed CRS Instructions”), Item 3.B.

[20] See supra note 7 and accompanying text.

[21] Staff of the U.S. Securities and Exchange Commission, Study on Investment Advisers and Broker-Dealers as Required by Section 913 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Jan. 2011) (“913 Study”), available at www.sec.gov/news/studies/2011/913studyfinal.pdf, at v.

[22] See Proposed CRS Instructions, Item 8.

[23] CRS Proposing Release, at Section II.B.8. (emphasis added).

[24] See CRS Proposing Release, at Sections II.C.2. and II.C.3. The proposal would require a firm to update its relationship summary within 30 days whenever the relationship summary becomes materially inaccurate. It is not clear to me why we would propose to allow financial professionals 30 days to update generic disclosure.

[25] See Discussion Regarding Electronic Delivery of Information to Retail Investors Investor as Owner Subcommittee, SEC Investor Advisory Committee (Oct. 2017), available at https://www.sec.gov/spotlight/investor-advisory-committee-2012/iac101217-agenda.htm.

[26] See Press Release, SEC’s Office of the Investor Advocate to Hold Evidence Summit, Launch Investor Research Initiative (Mar. 2, 2017), available at https://www.sec.gov/news/pressrelease/2017-59.html.

[27] In this proposal, the Commission fails to consider its own guidance to “assure[] the orderly and clear presentation of complex information so that investors have the best possible chance of understanding it.” See A Plain English Handbook: How to Create Clear SEC Disclosure Documents, Office of Investor Education and Assistance, U.S. Securities and Exchange Commission, at 5 (Aug. 1998), available at https://www.sec.gov/pdf/handbook.pdf.

[28] See, e.g., Margaret Hagen, Designing 21st-Centurey Disclosures for Financial Decision Making, Stanford Law School and Policy Lab (2016), available at https://law.stanford.edu/wp-content/uploads/2016/10/Hagan-Designing-21st-Century-Disclsoures-for-Wise-Financial-Decision-Making-FINAL-2016.pdf.

[29] CRS Proposing Release, at Section II.A (emphasis added).

[30] See rule 2a-7 under the Investment Company Act [17 C.F.R. § 270.2a-7].

[31] This analysis should assume and incorporate the changes being proposed pursuant to Regulation Best Interest, in Form CRS, and the labeling restrictions currently in the proposal.

[32] The related release also requests comment on licensing and continuing education requirements for personnel of SEC-registered investment advisers; delivery of account statements to clients with investment advisory accounts; and financial responsibility requirements for SEC-registered investment advisers, including fidelity bonds. See Proposing Release, Proposed Commission Interpretation Regarding Standard of Conduct for Investment Advisers; Request for Comment on Enhancing Investment Adviser Regulation (“Fiduciary Proposing Release”), at Section IV.

[33] See Fiduciary Proposing Release, at Section I. See also Section 206 under the Investment Advisers Act of 1940 [15 U.S.C. § 80b-6].

[34] See Fiduciary Proposing Release, at Section I, n.7.

[35] Letter from Consumer Federation of America to Jay Clayton (Sep. 14, 2017), pp. 29-31, available at https://www.sec.gov/comments/ia-bd-conduct-standards/cll4-2447346-161075.pdf; Bob Veres, The Awful Consequences of Non-Fiduciary Advice, INSIDE INFORMATION, available at http://www.bobveres.com/uncategorized/the-awful-consequences-of-non-fiduciary-advice-2/.

[36] The White House Council of Economic Advisers estimated that “conflicted advice leads to lower investment returns. . . . [and] . . . . large and economically meaningful costs for Americans’ retirement savings” with estimates of the total annual cost associated with retirement savings exceeding $17 billion. The Effects of Conflicted Investment Advice on Retirement Savings, February 2015, available at https://obamawhitehouse.archives.gov/sites/default/files/docs/cea_coi_report_final.pdf. Others have estimated the harm from conflicted investment advice to be $20 to $40 billion per year (Consumer Federation of America 2017 letter, available at https://www.sec.gov/comments/ia-bd-conduct-standards/cll4-2447346-161075.pdf), and $21 billion per year (Letter from Marnie C. Lambert, President, Public Investors Arbitration Bar Association (Aug. 11, 2017), available at https://www.sec.gov/comments/ia-bd-conduct-standards/cll4-2215713-160615.pdf).

[37] “Many individuals report that they have no retirement savings, and—among those who are saving—a number of respondents indicate that they lack confidence in their ability to manage their retirement investments.” Federal Reserve System Board of Governors, Report on the Economic Well-Being of U.S. Households in 2015 (May 2016), available at https://www.federalreserve.gov/2015-report-economic-well-being-us-households-201605.pdf.

Last Reviewed or Updated: May 2, 2024