SEC Proposes to Improve the Retail Investor Experience through Modernized Fund Shareholder Reports and Disclosures

Washington D.C., Aug. 5, 2020 —

The Securities and Exchange Commission today proposed comprehensive modifications to the mutual fund and exchange-traded fund disclosure framework to better serve the needs of retail investors. The proposed disclosure framework would feature concise and visually engaging shareholder reports that would highlight information that is particularly important for retail investors to assess and monitor their fund investments. The proposal is a central component of the Commission’s investor experience initiative and responds to comments the Commission received in response to a 2018 request for comment on retail investors’ experience with fund disclosure.

“The Commission is committed to improving the Main Street investor experience and modernizing information content and delivery,” said SEC Chairman Jay Clayton. “By encouraging fund disclosures that use modern communication techniques to emphasize clearly and concisely the information investors find most useful, today’s proposal should facilitate better-informed decision making.”

The proposal would:

- require streamlined reports to shareholders that would include, among other things, fund expenses, performance, illustrations of holdings, and material fund changes;

- significantly revise the content of these items to better align disclosures with developments in the markets and investor expectations;

- encourage funds to use graphic or text features—such as tables, bullet lists, and question-and-answer formats—to promote effective communication; and

- promote a layered and comprehensive disclosure framework by continuing to make available online certain information that is currently required in shareholder reports but may be less relevant to retail shareholders generally.

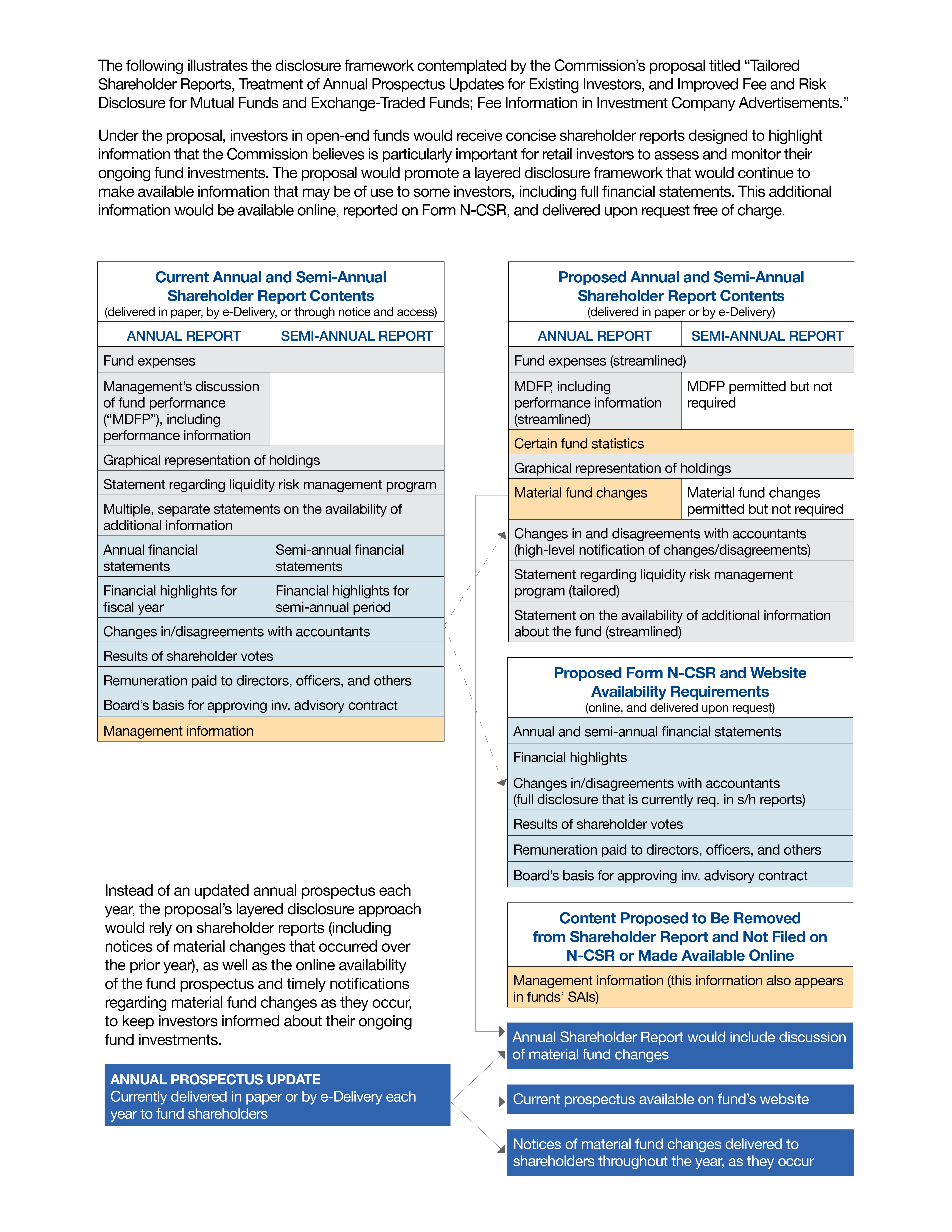

The proposed framework would provide an alternative approach to keeping investors informed about their ongoing fund investments. Instead of receiving both prospectus updates and shareholder reports, which today can be lengthy and complex, existing investors would receive the streamlined shareholder report. This would provide investors with timely and concise information to effectively assess and monitor their fund investments. Information currently required in shareholder reports that is not included in the streamlined shareholder report would be available online, delivered free of charge upon request, and filed on a semi-annual basis with the Commission.

In addition, the proposal would amend prospectus disclosure requirements to provide greater clarity and more consistent information regarding fees, expenses, and principal risks. To improve fee- and expense-related information more broadly, the proposal would also amend investment company advertising rules to promote more transparent and balanced statements about investment costs. The proposed advertising rule amendments would affect all registered investment companies and business development companies.

The proposal will be published on SEC.gov and in the Federal Register. The public comment period will begin following publication on SEC.gov and remain open for 60 days after publication in the Federal Register.

***

FACT SHEET

Tailored Shareholder Reports, Treatment of Annual Prospectus Updates for Existing Investors, and Improved Fee and Risk Disclosure for Mutual Funds and Exchange-Traded Funds; Fee Information in Investment Company Advertisements

August 5, 2020

Action

The Commission is proposing modifications to the disclosure framework for mutual funds and exchange-traded funds (“ETFs”) registered on Form N-1A (“open-end funds”) that would highlight key information for investors. The Commission is also proposing amendments to the advertising rules for registered investment companies and business development companies.

Highlights

Shareholder Reports Tailored to the Needs of Retail Shareholders

Based on feedback from investors and the Commission’s experience with fund disclosure, the proposed amendments affecting open-end funds’ shareholder reports are designed to highlight information that is particularly important for retail shareholders to assess and monitor their fund investments. This information would include, among other things, fund expenses, performance, illustrations of holdings, and material fund changes. The proposal would encourage open-end funds to use graphic or text features—such as tables, bullet lists, and question-and-answer formats—to promote effective communication. It would also provide flexibility for open-end funds to make electronic versions of their shareholder reports more user-friendly and interactive.

Availability of Additional Information on Form N-CSR and Online

Certain information currently included in an open-end fund’s annual and semi-annual reports may be less relevant to retail shareholders, and of more interest to financial professionals and those investors who desire more in-depth information. Under the proposal, this information would be available online, delivered free of charge upon request, and filed on a semi-annual basis with the Commission on Form N-CSR. This information would include, for example, the schedule of investments and other financial statement elements.

Tailoring Required Disclosures to Needs of New and Ongoing Fund Investors

Currently, open-end fund shareholders generally receive an updated annual prospectus each year. Proposed new rule 498B would provide an alternative approach to keep investors informed about their fund investment and any fund updates that occur year over year. Under this proposed rule, new investors would receive a fund prospectus in connection with their initial investment in an open-end fund, as they currently do, but funds would not deliver annual prospectus updates to shareholders thereafter. Instead, under the proposed layered disclosure framework, funds would keep shareholders informed through the shareholder report (including a summary in the annual report of material changes over the prior year), as well as timely notifications of material fund changes as they occur. Current versions of the fund’s prospectus would remain available online and would be delivered upon request in paper or electronically, consistent with the shareholder’s delivery preference.

Amendments to Scope of Rule 30e-3 to Exclude Open-End Funds

Under the existing framework, beginning as early as January 1, 2021, funds may begin relying on rule 30e-3. This rule generally permits funds to satisfy shareholder report transmission requirements by making these reports and other materials available online and providing a notice of the reports’ online availability, instead of directly providing the reports to shareholders. Investors who prefer to receive the full reports in paper may—at any time—choose that option free of charge.

Taking into account feedback from investors in response to the 2018 request for comment, and as part of the Commission’s continuing efforts to search for better ways of providing investors with disclosure they need, the proposal would amend the scope of rule 30e-3 to exclude open-end funds. The proposal would not affect the availability of rule 30e-3 for other registered management companies (such as registered closed-end funds) or registered unit investment trusts.

This amendment would help ensure that all open-end fund shareholders would experience the anticipated benefits of the proposal’s modified disclosure framework, which contemplates direct transmission of concise shareholder reports that serve as the central source of fund disclosure for existing shareholders. The proposed framework is designed to provide a more effective means for investors to access and use fund information, while continuing to recognize investor delivery preferences and reducing expenses associated with printing and mailing.

Improvements to Prospectus Disclosure of Fund Fees and Risks

The proposal would amend open-end fund prospectus disclosure to help investors more readily understand fund fees and risks, which investors have identified as two areas that are critically important in assessing a prospective fund investment, and yet often can be complex and confusing.

Using layered disclosure principles, the proposal would tailor disclosures of these topics to different types of investors’ informational needs. The proposal would, in part, (1) replace the existing fee table in the summary section of the statutory prospectus with a simplified fee summary, (2) move the existing fee table to the statutory prospectus, for use by investors seeking additional details about fund fees, and (3) replace certain terms in the current fee table with terms that may be clearer to investors.

The amendments also would refine current requirements for funds to disclose the “acquired fund fees and expenses” associated with investments in other funds. Specifically, the proposal would permit open-end funds that make limited investments in other funds to disclose the fees and expenses associated with those investments (“acquired fund fees and expenses”) in a footnote to the fee table and fee summary, rather than as a fee table line item.

The proposal would improve open-end fund prospectus risk disclosure by making it clearer and more specifically tailored to a fund. The proposal would, in part, (1) promote the disclosure of a fund’s principal risks, rather than additional, often overwhelming, disclosures about non-principal risks, and (2) tailor principal risk disclosure by specifying how principal risks can be assessed.

Fee and Expense Information in Investment Company Advertisements

The proposal would require that presentations of investment company fees and expenses in advertisements and sales literature are consistent with relevant prospectus fee table presentations and are reasonably current. The proposed amendments also address representations of fund fees and expenses that could be materially misleading. These amendments would affect all registered investment company and business development company advertisements.

What’s Next?

The proposal will be published on SEC.gov and in the Federal Register. The public comment period will begin following publication on SEC.gov and remain open for 60 days after publication in the Federal Register.

The Commission also approved for use two short-form feedback fliers to gather information from investors and funds, respectively. These feedback fliers are particularly directed at retail investors and smaller funds and are designed to help them provide feedback on the proposal. However, the Commission welcomes feedback from all interested commenters.

###

Last Reviewed or Updated: Oct. 4, 2023