UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended June 30, 2020

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE EXCHANGE ACT OF 1934 | |

For the transition period from ____________________ to _____________________

Commission file number 001-33365

____________________________________________________________________________________________

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

(Address of principal executive offices) | (Zip Code) | ||||

(610 ) 989‑0340

____________________________________________________________________________________________

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol | Name Of Each Exchange On Which Registered |

None | None | None |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

Large accelerated filer | ☐ | ☑ | |

Non-accelerated filer (Do not check if a smaller reporting company) | ☐ | Smaller reporting company | |

Emerging growth company | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant computed by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter, December 31, 2019, was $392,704,066 .

As of August 31, 2020, there were 65,226,175 outstanding shares of Common Stock, no par value.

USA TECHNOLOGIES, INC.

TABLE OF CONTENTS

PAGE | |||

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Form 10‑K contains certain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding, among other things, the anticipated financial and operating results of the Company. For this purpose, forward-looking statements are any statements contained herein that are not statements of historical fact and include, but are not limited to, those preceded by or that include the words, “estimate,” “could,” “should,” “would,” “likely,” “may,” “will,” “plan,” “intend,” “believes,” “expects,” “anticipates,” “projected,” or similar expressions. Those statements are subject to known and unknown risks, uncertainties and other factors that could cause the actual results to differ materially from those contemplated by the statements. The forward-looking information is based on various factors and was derived using numerous assumptions. Important factors that could cause the Company’s actual results to differ materially from those projected, include, for example:

• | general economic, market or business conditions unrelated to our operating performance, including the impact of the coronavirus disease 2019 (COVID-19) pandemic on the Company's operations, financial condition, and the demand for the Company’s products and services; |

• | failure to comply with the financial covenants of our credit agreement with JPMorgan Chase Bank, N.A. entered into on August 14, 2020; |

• | the ability of the Company to raise funds in the future through sales of securities or debt financing in order to sustain its operations in the normal course of business or if an unexpected or unusual event would occur; |

• | the ability of the Company to compete with its competitors to obtain market share; |

• | whether the Company’s current or future customers purchase, lease, rent or utilize ePort devices or our other products in the future at levels currently anticipated by our Company; |

• | whether the Company’s customers continue to utilize the Company’s transaction processing and related services, as our customer agreements are generally cancelable by the customer on thirty to sixty days’ notice; |

• | the ability of the Company to satisfy its trade obligations included in accounts payable and accrued expenses; |

• | the ability of the Company to sell to third party lenders all or a portion of our finance receivables, or to do so in a timely manner; |

• | the ability of a sufficient number of our customers to utilize third party financing companies under our QuickStart program in order to improve our net cash used by operating activities; |

• | the incurrence by us of any unanticipated or unusual non-operating expenses which would require us to divert our cash resources from achieving our business plan; |

• | the ability of the Company to predict or estimate its future quarterly or annual revenue and expenses given the developing and unpredictable market for its products; |

• | the ability of the Company to retain key customers from whom a significant portion of its revenue are derived; |

• | the ability of a key customer to reduce or delay purchasing products from the Company; |

• | the ability of the Company to obtain widespread commercial acceptance of its products and service offerings such as ePort QuickConnect, mobile payment and loyalty programs; |

• | whether any patents issued to the Company will provide the Company with any competitive advantages or adequate protection for its products, or would be challenged, invalidated or circumvented by others; |

• | the ability of the Company to operate without infringing the intellectual property rights of others; |

• | the ability of our products and services to avoid unauthorized hacking or credit card fraud; |

• | whether we are able to fully remediate our material weaknesses in our internal controls over financial reporting as of June 30, 2021 or continue to experience material weaknesses in our internal controls over financial reporting in the future, and are not able to accurately or timely report our financial condition or results of operations; |

• | whether our suppliers would increase their prices, reduce their output or change their terms of sale; |

• | whether the listing application for the Company’s securities which has been filed by the Company with The Nasdaq Stock Market LLC (“Nasdaq”) will be granted in a timely manner; and |

• | the risks associated with the currently pending litigation or possible regulatory action arising from the internal investigation conducted by the Audit Committee in fiscal year 2019 and its findings (the “2019 Investigation”), from the failure to timely file our periodic reports with the Securities and Exchange Commission, from the restatement of the affected |

3

financial statements, from allegations related to the registration statement for the follow-on public offering, or from potential litigation or other claims arising from the shareholder demands for derivative action.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. Actual results or business conditions may differ materially from those projected or suggested in forward-looking statements as a result of various factors including, but not limited to, those described above and in Part I, Item 1A, “Risk Factors” of this Form 10‑K. We cannot assure you that we have identified all the factors that create uncertainties. Moreover, new risks emerge from time to time and it is not possible for our management to predict all risks, nor can we assess the impact of all risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ from those contained in any forward-looking statements. Readers should not place undue reliance on forward-looking statements.

Any forward-looking statement made by us in this Form 10‑K speaks only as of the date of this Form 10‑K. Unless required by law, we undertake no obligation to publicly revise any forward-looking statement to reflect circumstances or events after the date of this Form 10‑K or to reflect the occurrence of unanticipated events.

4

USA TECHNOLOGIES, INC.

PART I

Item 1. Business.

OVERVIEW

USA Technologies, Inc. (the “Company”, “We”, “USAT”, or “Our”) was incorporated in the Commonwealth of Pennsylvania in January 1992. We are a provider of technology-enabled integrated solutions that facilitate electronic payments primarily within the unattended point of sale (“POS”) market. We are a leading provider in the small ticket beverage and food vending industry in the United States and are expanding our solutions and services in other unattended and self-service market segments, such as amusement, commercial laundry, air/vac, car wash, kiosk and others. Our systems allow distributed assets to accept cashless payments such as through the use of credit cards, debit cards, and mobile payments and support end-to-end logistics with cloud-based software services for advanced analytics, dynamic operational scheduling, automated pre-kitting, proactive malfunction management, responsive merchandising, inventory management, warehouse purchasing and accounting management.

We derive the majority of our revenues from license and transaction fees resulting from transactions on, as well as services provided by, our ePort Connect™ and Seed™ software services. These services include cashless payment, loyalty programs, inventory management, route logistics optimization, warehouse and accounting management, and responsive merchandising. Devices operating on the company’s platform and using our services include those resulting from the sale or lease of our POS electronic payment devices, telemetry devices or certified payment software or the servicing of similar third-party installed POS terminals or telemetry devices. The majority of ePort Connect customers pay a monthly fee plus a blended transaction rate on the transaction dollar volume processed by the Company. Transactions on the ePort Connect service, therefore, are the most significant driver of the Company’s revenues, particularly revenues from software license and transaction fees.

During the fiscal year ended June 30, 2020, the Company processed approximately 881.1 million cashless transactions totaling approximately $1.7 billion in transaction dollars, representing a 4.0% increase in transaction volume and a 5.0% increase in dollars processed from the 847.2 million cashless transactions totaling approximately $1.6 billion during the fiscal year ended June 30, 2019.

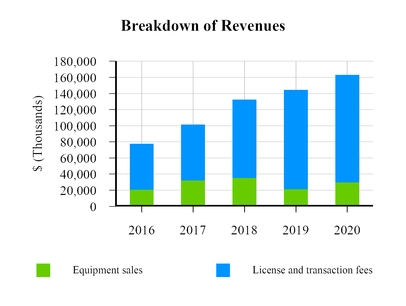

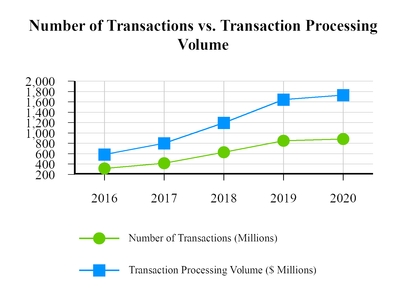

5

The above charts show the increases over the last five fiscal years in the number of transactions, revenues and the dollar value of transactions handled by us. The vertical bars depict total revenues, segmented by license and transaction and Seed services fees and equipment revenues. The bottom chart depicts the number of transactions on our ePort Connect and Seed services and the dollar value of transactions handled by the Company, as of the end of each of the last five fiscal years. Since 2016, the number of transactions processed annually increased by 31.1%, 51.2%, 35.1%, and 4.0% year-over-year for fiscal years 2017, 2018, 2019, and 2020, respectively. Over the same period, revenues have increased 30.8%, 30.6%, 9.0%, and 12.9%, with a 5-year compound annual growth rate of 16.0%. Our 2020 results were impacted by COVID-19 as discussed later in this section.

Our cashless solutions and services have been designed to simplify the transition to cashless payments for traditionally cash-only based businesses. As such, they are turn-key and include our comprehensive ePort Connect service and POS electronic payment devices or certified payment software, which are able to process traditional magnetic stripe credit and debit cards, contactless credit and debit cards and mobile payments. Standard services through ePort Connect are maintained on our proprietary operating systems and include merchant account setup on behalf of the customer, automatic processing and settlement, sales reporting and 24x7 customer support. Other value-added services that customers can choose from include cashless deployment planning, cashless performance review, loyalty products and services, and vending management solutions. Our solutions also provide flexibility to execute a variety of payment applications on a single system, transaction security, connectivity options, compliance with certification standards, and centralized, accurate, real-time sales and inventory data to manage distributed assets (wireless telemetry and Internet of Things (“IoT”)). Our Seed services complement our cashless services and provide customers with advanced

6

operational analytics, dynamic route scheduling, automated pre-kitting, proactive equipment malfunction management, responsive merchandising, inventory management, warehouse purchasing, and accounting management.

Our customers range from global food service organizations to small businesses that operate primarily in the self-serve, small ticket retail markets including beverage and food vending, amusement and arcade machines, smartphones via our ePort Online solution, commercial laundry, and various other self-serve kiosk applications as well as equipment developers or manufacturers who incorporate our ePort Connect service into their product offerings.

We believe that we have a history of being a market leader in cashless payments and software-based back office services for the unattended market with a recognized brand name, a value-added proposition for our customers and a reputation of innovation in our products and services. We believe that these attributes position us to capitalize on industry trends.

COVID-19

A novel strain of coronavirus (“COVID-19”) was first identified in China in December 2019 and subsequently declared a global pandemic in March 2020 by the World Health Organization. COVID-19 containment measures began in parts of the United States in March 2020 resulting in forced closure of non-essential businesses and social distancing protocols. COVID-19 has impacted our business, significantly reducing foot traffic to distributed assets containing our electronic payment solutions and reducing discretionary spending by consumers. The Company did not observe meaningful reductions in processing volume until mid-March, when average daily processing volume decreased approximately 40%. By mid-April, processing volumes began to recover and have shown a steady improvement by approximately 30% over the mid-March levels. At this time, we have observed geographic disparities in containment measures and are unable to reasonably estimate the length of time that these measures will be in effect in the United States. Furthermore, even after containment measures are lifted there can be no assurance as to the time required to regain operations and sales at levels prior to the pandemic.

In response to the outbreak and business disruption, first and foremost, we have prioritized the health and safety of our employees by implementing work-from-home measures while continuing to serve our customers. Additionally, we have created an internal task force to lead measures to protect the business in light of the volatility and uncertainty caused by the COVID-19 pandemic, including ensuring the safety of our employees and our community by implementing work from home policies, conserving liquidity, evaluating cost saving actions, partnering with customers to position USAT for renewed growth post crisis, and pausing on international expansion. The liquidity conservation and cost savings initiatives include but are not limited to: a 20% salary reduction for the senior leadership team until December 2020; deferral of all cash-based director fees until calendar year 2021; a temporary furlough of about 10% of our employee base; negotiations with and concessions from vendors in regard to cost reductions and/or payment deferrals; an increased collection effort to reduce outstanding accounts receivables; and various supply chain/inventory improvements. Our supply chain network has not been significantly disrupted and we are continuously monitoring it for the impact of COVID-19.

We have agreed to concessions on price and/or payment terms with certain customers who have been negatively impacted by COVID-19 and may negotiate additional concessions on price and/or payment terms. These concessions did not have a material impact on our financial results as of and for the year ended June 30, 2020.

We continue to monitor the rapidly evolving situation and guidance from federal, state and local public health authorities. As such, given the dynamic nature of this situation, the Company cannot reasonably estimate the impacts of COVID-19 on our financial condition, results of operations or cash flows in the future. However, based on current trends and if the pandemic is not substantially contained in the near future, COVID-19 may have a material adverse impact on our revenue growth as well as our overall profitability in fiscal year 2021, and may lead to higher sales-related, inventory-related, and operating reserves. Further, a sustained downturn may also result in a decrease in the fair value of our goodwill or other intangible assets, causing them to exceed their carrying value. This may require us to recognize an impairment to those assets.

Definition of a connection

Management believes that connections provide insight into trends and relationships about the Company’s strategy of driving growth. The Company counts a telemeter and/or cashless payment device (for example, an ePort cashless payment device or Seed telemeter) as a connection upon shipment of an activated device to a customer under contract, at which time the device is capable of transmitting cashless payment and other data to USALive, the Company’s online reporting platform, or utilizing the Seed management services.

The Company counts a self-service retail location that does not utilize our telemeter and/or cashless payment device as a connection upon (i) receipt of notice from a customer under contract of a location that has been enabled with our API software, and (ii) our

7

subsequent activation of the location on our platform which enables the location to utilize our payment transaction and logistics management services.

A connection to our device does not necessarily mean that our telemeter or cashless payment device has already been installed by the customer at a location, or has begun accepting and transmitting payment transactions, or has actually begun utilizing management services, or that the Company has begun receiving monthly service fees in connection with the device. Likewise, a non-device connection does not necessarily mean that the location has begun transmitting payment transactions, or has actually begun utilizing the management services, or that the Company has begun receiving monthly service fees. Rather, at the time of shipment of the device or the activation of the non-device location on our platform, the customer becomes obligated to pay the one-time activation fee (if applicable), and is obligated to pay monthly service fees and lease payments (if applicable) in accordance with the terms of the customer’s contract with the Company.

A self-service retail location that utilizes an ePort cashless payment device as well as Seed management services constitutes only one connection.

Our customer contracts provide that the customer may deactivate a device or a non-device location, as the case may be, from our platform by prior notice to us (generally thirty to sixty days). We will no longer count an existing connection as a connection following the receipt of instructions from the customer to deactivate the device or non-device location, as the case may be, upon the expiration of the applicable notice period, provided that the notice is in accordance with the terms of the customer contract. A previously installed telemeter or cashless payment system that is no longer being utilized by our customer is considered and reported as an existing connection unless and until the customer provides the appropriate notice under the contract and the applicable notice period has expired.

THE INDUSTRY

We operate primarily in the small ticket electronic payments and vending management industry and, more specifically, the broad unattended POS market. We provide our customers the ability to accept cashless payment “on the go” through mobile-based payment services. Our solutions and services facilitate electronic payments in industries that used to rely on cash transactions, allowing our customers to simplify inventory, warehouse, logistics, and accounting management. We believe the following industry trends are driving growth in demand for electronic payment systems and advanced logistics management in general and more specifically within the markets we serve:

• | Shift toward digital payments accelerating as consumers move to adopt contactless payments; |

• | Increase in consumer demand for non-traditional items in unattended retail; |

• | Improving POS and mobile payment technology; and |

• | Increasing demand for business efficiency through modern, cloud-based logistics and inventory management systems. |

Shift Toward Digital Payments Accelerating as Consumers Move to Adopt Contactless Payments.

There is an ongoing behavioral shift away from using paper-based methods of payment, including cash and checks, towards that of electronic-based (digital) methods of payment. COVID-19 is accelerating the move to a cashless-preferred economy. In a recent study analyzing 120,000 cashless terminals from January to July 2020, USAT found that cashless payments were accelerating at a rapid pace, with contactless payments driving much of that growth. In January 2020, 53.1% of total sales were made with cashless payments, and by July, 61.7% of total sales were made with cashless payments - with contactless payments growing 51% as a percentage of total cashless payments. In the seven months during this study, USAT has seen contactless payments grow eight times as fast as non-contactless payments, showing that contactless payments are giving consumers a safe, secure and easy way to buy goods and services.

Increase in Consumer Demand for Non-Traditional Items in Unattended Retail.

As Millennials and the first members of Generation Z take a greater share of the workforce and influence in retail, a study released in February 2020 by PYMNTS and USA Technologies found that these younger generations are bringing greater opportunities for retailers to sell non-traditional, higher ticket items such as consumer electronics through unattended channels. According to the Future of Unattended Retail Study, which queried more than 2,300 people across the United States, 35% of Millennials and 29% of Generation Z would be willing to spend more if non-traditional products were offered.

8

Increase in Merchant/Operator Demand for Electronic Payments.

We believe that, increasingly, merchants and operators of unattended payment locations (e.g., vending machines, laundry, tabletop games, etc.) are utilizing electronic payment alternatives, with an emphasis on contactless transactions due to COVID-19 impacts on how consumers pay, as a means to improve business results. In addition, electronic payment systems can provide merchants and operators real-time sales and inventory data utilized for back-office reporting and forecasting, like the Company’s Seed solutions and services, helping them to manage their business more efficiently.

Increase in Demand for Integrated Payment Solutions.

As unattended retailers look to diversify their business and offer more than one business line, an integrated solution becomes critical to operating with full visibility, control and manageable growth across their POS network. According to the 2018 Industry Census conducted by the National Automatic Merchandising Association (NAMA), 62% of owners of unattended retail businesses, were “blended,” offering more than one business line.

We believe that merchants have come to value payment solutions that are integrated or bundled with other solutions and software. As described earlier under Overview, our Seed services provide an end-to-end enterprise solution to our customers. We also view our integrated solutions as a significant advantage over the competition.

Increase in Demand for Networked Assets.

IoT technology includes capturing value from wireless modules and electronic devices to improve business productivity and customer service. In addition, networked assets can provide valuable information regarding consumers’ purchasing patterns and payment preferences, allowing operators to more effectively tailor their offerings to consumers. Our services connect offline machines and devices and bring intelligence and operating efficiencies to the device and operator through our value-added services.

COVID-19’s Impact to Creating More Contactless Experiences in Unattended Retail.

COVID-19 has created increased awareness to consumers around contactless payments to provide easy, safe and secure ways of transacting in both retail and unattended retail. According to a Mastercard consumer study conducted in April 2020, 79% of respondents worldwide say they are now using contactless payments. Mastercard also reported that worldwide, contactless transactions grew twice as fast as non-contactless transactions in the grocery and drug store categories between February and March 2020. Along with the rise of digital payments, we believe that while COVID-19 presents challenges for many industries, it is creating opportunities in unattended retail. With many hospital cafeterias closed and human contact fraught due to the COVID-19 pandemic, healthy vending machine companies are stepping in to fill the void, reported Eater.com. Vending machines are also becoming a destination to provide personal protective equipment products directly to consumers; airports are quickly adopting machines to provide consumers easy and safe access to masks, gloves, hand sanitizer, wipes, etc. We believe that POS terminals that are enabled to accept contactless and mobile payments stand to benefit from these evolving trends in mobile payment. Mobile payments include digital wallet applications, including Apple Pay, Google Pay, Samsung Pay, and others, which are popular alternatives to the traditional credit or debit card, providing alternate security protocols and a safe way for consumers to pay.

OUR TECHNOLOGY-BASED SOLUTION

Our solutions are designed to be turn-key and include the ePort Connect service, which is a cashless payment gateway, the Seed services, which provide customers with remote inventory management, logistics, warehouse and accounting management, and product merchandising solutions. Our POS electronic payment devices contain certified payment software which is able to process traditional magnetic stripe as well as contactless credit and debit cards and NFC-equipped mobile devices to enable mobile payments. We believe that our ability to bundle our products and services, as well as the ability to tailor and customize them to individual customer needs, makes it easy and efficient for our customers to adopt and deploy our technology, and results in a leading service in the small-ticket, unattended retail market today.

The Product. The Company offers customers several different ways to connect and manage their distributed assets. These range from our QuickConnect™ Web service and our Seed Cloud platform, more fully described below under the section “OUR PRODUCTS,” and encrypted magnetic stripe card readers to our ePort® hardware that can be attached to the door of a stand-alone terminal.

The Platform. Our ePort Connect service platform is designed to transmit from our customers’ terminals payment information for processing and sales and diagnostic data for storage and reporting to our customers through USA Live and/or Seed Cloud, along with third-party software solutions. Also, the platform, through server-based software applications, provides remote management

9

information, and enables control of the networked device’s functionality. Through our platform we have the ability to upload software and update devices remotely enabling us to manage the devices easily and efficiently (e.g., change protocol functionality, provide software upgrades, and change terminal display messages).

The Connectivity Mediums. The client devices (described below) are interconnected for the transfer of our customers’ data through our ePort Connect platform that provides wireless-based connectivity. Increased wireless connectivity options, coverage and reliability have allowed us to service a greater number of geographically dispersed customer locations. Additionally, we make it easy for our customers to deploy wireless solutions by acting as a single point of contact. We have contracted with Verizon Wireless and AT&T Mobility in order to supply our customers with wireless network coverage.

Data Security. We are listed on the Visa Global Registry of Service Providers, meaning that we have provided Visa with a Report on Compliance (RoC) issued by a qualified security assessor validating our compliance with the Payment Card Industry Data Security Standard (PCI DSS). Our entry on this registry is required to be renewed annually, and our next renewal date is December 31, 2020.

OUR SERVICES

For the fiscal year ended June 30, 2020, license and transaction fees generated by our ePort Connect and Seed services represented 82% of the Company’s revenues, compared to 85% of the Company’s revenues for the fiscal year ended June 30, 2019. Our ePort Connect solution provides customers with all of the following services, under one cohesive service umbrella:

• | Diverse POS options. We offer our customers the ability to connect to a variety of cashless acceptance devices or software. |

• | Card Processing Services. Through our existing relationships with card processors and card associations, we provide merchant account and terminal ID set up, pre-negotiated discounted fees on small ticket purchases, and direct electronic funds transfers to our customers’ bank accounts for all settled card transactions as well as ensure compliance with processing protocols. |

• | Customer/Consumer Services. We support our installed base by providing help desk support, repairs, and replacement services. All inbound consumer billing inquiries are handled through a 24‑hour help desk, thereby reducing our customers’ exposure to consumer billing inquiries and potential chargebacks. Maintenance updates and enhancements to software, settings, and features from our platform are sent over-the-air to our ePort card readers, allowing us to provide remote maintenance services. |

• | Online Sales Reporting. Via the USALive and Seed Cloud online reporting system, we provide customers with a host of sales and operational data, including information regarding their credit and cash transactions, user configuration, reporting by machine and region, by date range and transaction type, data reports for operations and finance, graphical reporting of sales, and condition monitoring for equipment service, as well as activation of new devices and redeployments. |

• | Seed Vending Management. The Seed vending management software provides cloud and mobile solutions for advanced operational analytics, dynamic route scheduling, automated pre-kitting, proactive equipment malfunction management, responsive merchandising, inventory management, warehouse purchasing, and accounting management for any unattended retail points of service, including vending machines, micromarkets, and office coffee services. |

• | Other Services. USAT offers services to support our customers that fully leverages the Company’s industry expertise and access to data. These services include our loyalty program, two-tier pricing and special promotions. In addition, planning, project management, deployment, installation support, Seed implementation, marketing and performance evaluation, as well as wireless account activations, distributions, and relationships with wireless providers. |

In connection with ePort Connect services, we enter into a Services Agreement with our customers which provides for processing and licensing of the solution. Under its terms, we act as a provider of cashless financial services for the customer’s distributed assets, and collect certain of our fees from settled funds, including activation fees, monthly service fees, and transaction processing fees.

In connection with providing Seed vending management solutions, we enter into Subscription Agreements with our customers. Pursuant to the Subscription Agreement and the related Master Service Agreement, the customer typically agrees to a term of five years. For some of these customers we serve as the merchant of record and collect our fees from settled funds.

10

OUR PRODUCTS

ePort is the Company’s integrated payment device, which is currently deployed in self-service, unattended market applications such as vending, amusement and arcade. Our ePort product facilitates cashless payments by capturing payment information and transmitting it to our platform for authorization with the payment system (e.g., credit card processors). Additional capabilities of our ePort consist of control/access management by authorized users, collection of audit information (e.g., date and time of sale and sales amount), diagnostic information of the host equipment, and transmission of this data back to our platform for web-based reporting, or to a compatible remote management system. Our ePort products are available in several distinctive modular hardware configurations, and as hardware, software-as-a-service, offering our customers flexibility to install a POS solution that best fits their needs and consumer demands. We offer hardware lease and rental options through our JumpStart and QuickStart programs.

• | ePort G‑9 is a two-piece design for traditional magnetic stripe credit/debit cards and contactless cards with features that support enhanced acceptance options, consumer engagement offerings and advanced diagnostics. This device is also used to support Canada’s unattended retail market with its functionality to accept Interac Flash (tap). |

• | ePort G10-S is a 4G LTE cashless payment device that enables faster processing and enhanced functionality for payment and consumer engagement applications. It supports functionality that requires higher speeds and large data loads, operates on the AT&T and Verizon networks, and has built-in NFC support for mobile payments, traditional credit and debit cards, in addition to EMV-contactless options. |

• | Seed Telemeter is a legacy telemetry device enabling operators to manage machine data across their network to realize the benefit of the Seed Cloud. |

• | ePort Interactive is a 4G LTE cloud-based interactive media and content delivery management system, enabling delivery of nutritional information, remote refunds, loyalty programs, and multimedia-marketing. |

We offer integrated software solutions that leverage payment devices in the field, ePort or third-party, to connect into our platform of advanced data management, analytics, route scheduling, as well as other offerings identified below:

• | QuickConnect is a web service that allows a client application to securely interface with the Company’s ePort Connect service. |

• | ePortConnect is a cashless payments gateway that connects devices through network solutions, to USAT’s back-end platform for processing payments, transferring data into cloud-based management software, inclusive of Seed Cloud and USALive, along with enabling third-party integrations. |

• | USALive is a software-as-a-service, that provides an intuitive portal for ePort cashless device customers. Providing them an easy-to-use interface for tracking cashless and cash sales, machine and device level health, along with sales reporting for management of devices. |

• | Seed Cloud is an enterprise-grade vending management solution which provides cloud and mobile solutions for advanced operational analytics, dynamic route scheduling, automated pre-kitting, proactive equipment malfunction management, responsive merchandising, inventory management, warehouse purchasing, and accounting management that is layered on, and takes advantage of, the data provided by both Seed and ePort devices. |

Another form of our ePort technology is ePort Online, which enables customers to use USALive to securely process cards typically held on file for the purpose of online billing and recurring charges. ePort Online helps USAT’s customers reduce paper invoicing and collections.

SPECIFIC MARKETS WE SERVE

Our current customers are primarily in the self-serve, small ticket retail markets in North America, including beverage and food vending and kiosk, commercial laundry, car wash, tolls, amusement and gaming, air and vacuum services, and office coffee. We estimate that there are approximately 16 million to 18 million potential connections in this self-serve, small ticket retail market in North America. The 1,320,000 connections to our service as of June 30, 2020 constitute 7% of these potential connections, compared to 1,169,000 connections to our service as of June 30, 2019, which constituted 6% of these potential connections. While these industry sectors represent only a small fraction of our total market potential, as described below, these are the areas where we have gained the most traction to date. In addition to being our current primary markets, we believe these sectors serve as a proof-of-concept for other unattended POS industry applications.

11

Vending. According to the 2018 Census of the Convenience Services Industry conducted by Technomic for NAMA, the convenience services industry, which consists of vending machines, micro markets, office coffee service (OCS) and pantry services, is estimated to represent a total annual revenue of $26 billion, a 4% increase since 2016. The Census found that while the vending segment of the convenience services industry continued to contract (-3% since 2016), micro markets, OCS and pantry service segments have more than made up for the shortfall. According to the Census, micro markets continued their rapid expansion, with revenues growing 99% over the previous two years, while OCS grew at 7%. The Company believes these machines represent a significant market opportunity for electronic payment conversion when compared to the Company’s existing ePort Connect service base and the overall low rate of industry adoption to date. For example, in another study conducted by Automatic Merchandiser (2019 State of the Industry Report) that included a representative 2.1 million machines, cashless adoption was estimated at 59% in 2018. Connected vending machines using telemeters to collect data are now used by 41% of respondents, which is an increase from the last two years, reported Automatic Merchandiser - showing opportunity to remove manual processes with technology solutions. With the continued shift to electronic payments and the advancement in mobile and POS technology, we believe that the traditional beverage and food vending industry will continue to look to cashless payments and telemetry systems to improve their business results.

Kiosk. The kiosk industry posted its third consecutive year of double-digit growth in 2019, according to the 2020 Kiosk Market Census Report which is published annually. Kiosk sales jumped 17.9% in 2019, closely aligning to the growth rates discussed in the previous two years of the report and showing continuous adoption of self-service technology by consumers. Interactive kiosk sales - excluding automated teller, refreshment and amusement vending machines - totaled an estimated $11.9 billion in 2019. We believe that kiosks are becoming increasingly popular as credit, debit or contactless payment options enable kiosks to sell an increased variety of items. In addition, the study points to rising mobile commerce and improved IoT technology as driving growth in self-service markets, similar to the factors discussed in the previous two years of the report. As merchants continue to seek new ways to reach their customers through kiosk applications, we believe the need for a reliable cashless payment provider experienced with machine integration, PCI compliance and cashless payment services designed specifically for the unattended market will be of increasing value in this market. Our existing kiosk customers integrate with our cashless payment services via our QuickConnect Web service using one of our encrypted readers or ePort POS technologies.

Laundry. Our primary opportunities in laundry consist of the coin-operated commercial laundry and multi-housing laundry markets. According to the Coin Laundry Association, the U.S. commercial laundry industry is comprised of about 29,500 coin laundries in the U.S., with an estimated gross annual revenue of nearly $5 billion.

Amusement and Entertainment. Our current customers and primary opportunities in the amusement and entertainment markets are typically classified as “street/route business,” which are standalone businesses that are open to the general public and that offer card/coin-operated games such as claw machines, amusement park machines (i.e. body dryers), bowling alleys and bar entertainment (i.e. digital music machines, dart machines, etc.). According to the 2019 IBISWorld Industry Report on Arcade, Food & Entertainment Complexes in the U.S., this industry represents $2.5 billion, including $1.2 billion from card/coin-operated games, with approximately 6,900 businesses within this segment of the amusement and entertainment market. Our existing customers in the amusement and entertainment markets leverage our ePort Connect Platform to enable cashless acceptance, remote machine monitoring, and pulse capability for cashless devices. ePort Connect’s pulse capability enables coin/token based unattended retail environments to accept cashless by using pulse voltages to imitate coin and bill payments, and trigger machines to play.

OUR COMPETITIVE STRENGTHS

We believe that we benefit in the marketplace, and with our existing customers, from a number of advantages gained through our over twenty-five years in the industry. They include:

1. | One-Stop Shop, End-to-End Solution. We believe that our ability to offer our customers one point of contact through a bundled cashless payment and software solution makes it easy and efficient for our customers to adopt and deploy our comprehensive platform and results in a service that is unmatched in the small ticket, self-service retail market today. To our knowledge, other cashless payment and vending management solutions available in the market today require the operator to set up their own accounts for cashless processing (i.e., act as the merchant of record) and manage multiple service providers (i.e., hardware terminal manufacturer, wireless network provider, and/or credit card processor). We interface directly with our card processor and wireless service provider, and, with our hardware solutions, are able to offer a bundled and integrated solution to our customers for whom we serve as the merchant of record. |

2. | Trusted Brand Name. We believe that the ePort has a strong national reputation for quality, reliability, and innovation. Similarly, we believe that the Seed Cloud platform has a strong reputation for providing innovative software solutions that solve every day customer challenges. We believe that card associations, payment processors, and merchants/operators trust our system solutions and services to handle financial transactions in a secure operating environment, along with providing them accurate |

12

data to manage their business efficiently through our software application. Our trusted brand name is exemplified by our high level of customer retention and a number of multi-year agreements with customers for use of our ePort Connect service. We have agreements with partners like First Data, Visa, MasterCard, Chase Paymentech and Verizon Wireless that allow us to provide these solutions to our customers.

3. | Market Leadership. We believe we have one of the largest installed bases of unattended POS electronic payment systems in the unattended small ticket retail market for food and beverage in the United States and we are continuing to expand to other adjacent markets such as laundry, amusement, gaming, and kiosks. Our installed base supports our sales and marketing initiatives by enhancing our ability to establish or expand our market position. In addition, this data, in combination with our industry experts and analysis, enables us to offer Premium Services to our customers to help them deploy and better leverage our technology in their locations. We believe our installed base also provides multiple opportunities for referrals for new business, either from the merchant or operator of the deployed asset, through one of our several strategic partnerships, or as equipment upgrade and upsell opportunities for new technologies that will occur as part of upcoming industry-wide wireless network upgrades. |

4. | Attractive Value Proposition for Our Customers. We believe that our solutions provide our customers an attractive value proposition. Our solutions and services make possible increased purchases by consumers who in the past were limited to the physical cash on hand while making a purchase at an unattended terminal, thereby increasing the universe of potential customers and the size and value of the purchases of those customers. In addition, we offer value-added offerings and services such as Two-Tier Pricing, which allows the operator to charge different amounts for the same product depending upon whether the consumer chooses to pay by cash or credit/debit. Consumer engagement services further extend the potential for customers to build new revenue opportunities, customer loyalty and brand distinction. One of such services is provided through the ePort interactive platform, our cloud-based interactive media and content delivery management system, which enables delivery of nutritional information, remote refunds, loyalty programs, and multimedia-marketing campaigns for the unattended and self-serve retail markets. Lastly, with our Seed Cloud, we provide the ability for customers to pursue additional opportunities to reduce costs and improve operating efficiencies with tools such as advanced operational analytics, dynamic route scheduling, automated pre-kitting, proactive equipment malfunction management, responsive merchandising, inventory management, warehouse purchasing, and accounting management on a modern, cloud-based SaaS offering. |

5. | Increasing Scale and Market Footprint. The continued growth in connections to the Company’s ePort Connect and Seed services provides us brand credibility, improved revenue, and the footprint to market and distribute our products and services more effectively and in more markets than most of our competitors. |

6. | Customer-Focused Research and Development. Our research and development initiatives focus primarily on adding features and functionality to our electronic payment solutions and logistics management platform based on customer input and emerging market trends. As of June 30, 2020, we have 72 patents (US and International) in force, and 4 United States and 6 international patent applications pending. We have generated considerable intellectual property and know-how associated with creating a seamless, end-to-end experience for our customers. |

OUR GROWTH OPPORTUNITY

Our primary objective is to continue to enhance our position as a leading provider of technology that enables electronic payment transactions, advanced logistics management, and value-added services primarily at small-ticket, self-service retail locations such as vending, kiosks, commercial laundry, and other similar markets. We plan to execute our growth strategy organically and through strategic acquisitions. Key elements of our strategy are to:

Leverage Existing Customers/Partners. We have a solid base of key customers across multiple markets, particularly in vending, that have currently deployed our solutions and services to a portion of their deployed base. Approximately 80% of our new connections during the fiscal year ended June 30, 2020 and approximately 86% of our new connections during the fiscal year ended June 30, 2019 were from existing customers. We estimate that our current customers represent approximately 3.3 million potential connections. Based on the 1.3 million connections we service as of June 30, 2020, there remain approximately 2.0 million potential connections from our current customers that could be connected to our service. As a result, they are a key component of our plan to drive future sales. We have worked to build these relationships, drive future deployments, and develop customized network interfaces. Our customers have seen the benefits of our products and services first-hand and we believe they currently represent the largest opportunity to scale recurring revenue and connections to our service.

Expand Distribution and Sales Reach. We are intently focused on driving profitable growth through efficient sales channels. Our sales resources and new distribution relationships have led to increased penetration in markets such as amusement and arcade, and commercial laundry.

13

Further Penetrate Attractive Adjacent Markets. We plan to continue to introduce our turn-key solutions and services to various adjacent markets such as the broad-based kiosk market and other similar markets by leveraging our expertise in cashless payment integration combined with the capacity and uniqueness of our ePort Connect solution.

Capitalize on Opportunities in International Markets. We are currently focused on the U.S. and Canadian markets for our ePort devices and related ePort Connect service but may seek to establish a presence in electronic payment markets outside of the U.S. and Canada. In order to do so, however, we would have to invest in additional sales and marketing and research and development resources targeted towards these regions, and the Company's current focus remains on the U.S. and Canadian markets for the near-term due to resource constraints. At this time, the Company believes the most efficient route to these markets will be achieved by working closely with its global partners to leverage their expertise and experience in navigating those markets.

Capitalize on the emerging contactless, NFC, and growing mobile payments trends. With approximately 93% of our cashless connected base enabled to accept NFC payments (including mobile wallets), the Company believes that continued increases in consumer preferences towards contactless payments, including mobile wallets like Apple Pay and Samsung Pay, represent a significant opportunity for the Company to further drive adoption. Additionally, as of June 30, 2020, the Company has approximately 260 thousand EMV enabled devices and continues to see accelerated adoption. As the variety of payment methods expands and consumer behaviors evolve, the ability to make credit and debit card payments at unattended terminals is highly in demand among consumers, with 70% of U.S., U.K. and Australian respondents in the 2018 TNS Unattended Terminals Survey saying they would prefer unattended vending machines and kiosks to accept both card and cash payments. This same survey found that 57% of adults between the ages of 18 and 34 were willing to make a payment at an unattended terminal with a digital wallet such as Apple Pay, Samsung Pay or Google Pay. Further, 33% of the U.S. respondents said they would be willing to make a payment at an unattended kiosk or vending machine using a wearable device, such as a bracelet, fitness tracker, keyring, etc. As consumers continue to adopt these new methods of cashless payments, it is our belief that adoption will continue to accelerate at a rapid pace and result in more rapid adoption of cashless solutions like the Company’s ePort in the markets that we serve.

Continuous Innovation. We are continuously enhancing our solutions and services in order to satisfy our customers and the end-consumers relying on our products at the POS locations. We are making investments in new products and services, and continously partnering with other players within the ecosystem to drive additional value of combined service offerings to our customers and opportunities. Our product innovation team is always working to enhance our operational and payments platform to drive easier integration and customer implementation as well as establish compatibility with other electronic payment solution providers’ technologies. We believe our continued innovation will lead to further adoption of USAT’s solutions and services in the unattended POS payments market.

Comprehensive Service and Support. In addition to its industry-leading ePort cashless payments system, the Company seeks to provide its customers with a comprehensive, value-added ePort Connect service that is designed to encourage optimal return on investment through business planning and performance optimization; business metrics through the Company’s KnowledgeBase of data; a loyalty and rewards program for consumer engagement; marketing strategy and executional support; sales data and machine alerts; DEX data transmission; and the ability to extend cashless payments capabilities and the full suite of services across multiple aspects of an operator’s business including micro-markets contract food industry, online payments and mobile payments.

Leverage Intellectual Property. Through June 30, 2020, we have 72 U.S. and foreign patents in force that contain various claims, including claims relating to payment processing, networking and energy management devices. In addition, we own numerous trademarks, copyrights, and trade secrets. We will continue to explore ways to leverage this intellectual property in order to add value for our customers, attain an increased share of the market, and generate licensing revenues.

SALES AND MARKETING

The Company’s sales strategy includes both direct sales and channel development, depending on the particular dynamics of each of our markets. Our marketing strategy is diversified and includes demand generation strategies such as paid advertising, search engine optimization, content curation, direct mail, and digital automation; product and partner strategies such as commercialization of new products to market, payment and integration partner webinars, podcasts, joint-studies, and digital advertising; along with marketing events and communications that include media relations, conferences (both virtual and in-person), social media, and client referrals. As of June 30, 2020, the Company was marketing and selling its products primarily through its full and part-time sales and marketing staff consisting of 31 people.

Direct Sales

Our direct sales efforts are currently primarily focused on the convenience services industry in the United States, inclusive of beverage and food vending, although we continue to further develop our presence in other market segments.

14

Indirect Sales/ Distribution

As part of our strategy to expand our sales reach while optimizing resources, we have agreements with select resellers in the car wash, amusement and arcade, and vending markets. We also have a distribution and white label program with the Wittern Group (“Wittern”), a manufacturer of vending machines, pursuant to which Wittern embeds our Seed cashless hardware, called GreenLite, into its vending machines and sells Seed services to its customers. We have also entered into agreements with resellers and distributors in connection with our energy management products.

Marketing

Our marketing strategy includes advertising and outreach initiatives designed to build brand awareness, position USAT as thought leaders within unattended retail, make clear USAT’s competitive strengths, and prove the value of our services to our opportunity markets-both for existing and prospective customers. Activities include creating company and product presence on the web including www.usatech.com and www.energymisers.com, digital advertising, SEO (Search Engine Optimization), and social media; the use of direct mail and email campaigns; educational and instructional online training sessions; content curation through blogs, whitepapers, guides, podcasts, and joint industry studies; advertising in vertically-oriented trade publications; participating in industry tradeshows and events; and working closely with customers and key strategic partners on co-marketing opportunities and new, innovative solutions that drive customer and consumer adoption of our services.

IMPORTANT RELATIONSHIPS

Verizon Wireless

In April 2011, we signed an agreement with Verizon for access to their digital wireless wide area network for the transport of data, including credit card transactions and inventory management data. The initial term of the agreement was three years, which was extended until April 2016. Since the end of the term, the agreement automatically renewed and will continue to automatically renew for successive one month periods unless terminated by either party upon thirty days’ notice.

On September 21, 2011, the Company and Verizon entered into a Joint Marketing Addendum (the “Verizon Agreement”) which amended the agreement described above. Pursuant to the Verizon Agreement, the Company and Verizon would work together to help identify business opportunities for the Company’s products and services. Verizon may introduce the Company to existing or potential Verizon customers that Verizon believes are potential purchasers of the Company’s products or services and may attend sales calls with the Company made to these customers. The Company and Verizon would collaborate on marketing and communications materials that would be used by each of them to educate and inform customers regarding their joint marketing work. Verizon has the right to list the Company’s products and services in its Data Solutions Guide for use by its sales and marketing employees and in its external website. The Verizon Marketing Agreement is terminable by either party upon 45 days’ notice.

VISA

As of July 1, 2017, we entered into a three-year agreement with Visa U.S.A. Inc. (“Visa”), pursuant to which Visa has agreed to continue to make available to the Company certain promotional interchange reimbursement fees for small ticket debit and credit card transactions in the unattended beverage and food vending merchant category code, as well as for small ticket regulated debit card transactions in the other unattended vending and/or retail merchant category codes covered by the agreement. As previously reported, following implementation of the Durbin Amendment, Visa had significantly increased its interchange fees for small ticket regulated debit card transactions effective October 1, 2011. The promotional interchange reimbursement fees provided by the aforementioned agreement will continue until September 30, 2020. The Company is having discussions with Visa on a new agreement.

MasterCard

On January 12, 2015, we entered into a three-year MasterCard Acceptance Agreement (“MasterCard Agreement”) with MasterCard International Incorporated ("MasterCard"), pursuant to which MasterCard has agreed to make available to us reduced interchange rates for small ticket debit card transactions in certain merchant category codes. As previously reported, MasterCard had significantly increased its interchange rates for small ticket regulated debit card transactions effective October 1, 2011, and as a result, the Company ceased accepting MasterCard debit card products in mid-November 2011. Pursuant to the MasterCard Agreement, however, the Company is currently accepting MasterCard debit card products for small ticket debit card transactions in the unattended beverage and food vending merchant category code. The Company and MasterCard entered into a first amendment on April 27, 2015, pursuant to which the conditions under, or the transactions to, which the MasterCard custom pricing would be available, was amended. The reduced interchange rates became effective on April 20, 2015. Pursuant to an amendment effective

15

July 17, 2018, the agreement was extended until March 1, 2019, and will automatically renew for successive one-year terms thereafter, unless either party provides 60 days’ advance notice of non-renewal.

Chase Paymentech

We entered into a five-year Third Party Payment Processor Agreement, dated April 24, 2015 with Paymentech, LLC, through its member, JPMorgan Chase Bank, N.A. (“Chase Paymentech”), pursuant to which Chase Paymentech will act as the provider of credit and debit card transaction processing services (including authorization, conveyance and settlement of transactions) to the Company, which acts as the merchant of record. The Agreement provides that Chase Paymentech will act as the exclusive provider of transaction processing services to the Company for at least 250 million transactions per year. The Agreement provides that Chase Paymentech may modify the pricing for its services upon 30‑days’ notice, and in connection with certain such increases, the Company has the right to terminate the Agreement upon 120‑days’ notice. Following the expiry of the initial term of the Agreement on April 24, 2020, the Agreement will automatically renew for successive one-year terms unless either party provides 30 days’ advance notice of non-renewal.

First Data

In March 2020, we signed an agreement with First Data Merchant Services LLC (“First Data”), and Wells Fargo Bank, N.A., where First Data became the Company’s primary provider of credit and debit card transaction processing services (including data capture, authorization, or settlement of transactions) for payment transactions submitted from locations in the United States, and First Data will replace Chase Paymentech as the primary provider of credit and debit card transaction processing services to the Company. Following an initial six month implementation period beginning in March 2020, the agreement will continue for a five year period and automatically renews for consecutive one-year periods thereafter unless the agreement is terminated by First Data or the Company upon at least 90-days’ notice prior to the end of the initial five year period or at any time during a one-year renewal term. The Company will pay to First Data the fees and charges set forth in the agreement, including acquiring fees charged by First Data and fees imposed on the payment transactions by the payment organizations and networks and other third parties. The agreement provides that First Data will provide certain incentive or other payments or credits to the Company during the term of the agreement.

Compass/Foodbuy

On June 30, 2009, we entered into a Master Purchase Agreement (“MPA”) with Foodbuy, LLC (“Foodbuy”), the procurement company for Compass Group USA, Inc. (“Compass”) and other customers. The MPA provides, among other things that, USAT shall be a preferred supplier and provider to Foodbuy and its customers, including Compass, of USAT’s products and services. The MPA automatically renews for successive one-year periods unless terminated by either party upon sixty days’ notice prior to the end of any such one-year renewal period. In addition, on July 1, 2009, USAT and Compass, in conjunction with the MPA described above, also entered into a three-year ePort Connect Services Agreement pursuant to which USAT will provide Compass with all card processing, data, network, communications and financial services, and DEX telemetry data services required in connection with all Compass vending machines utilizing ePorts. The agreement automatically renews for successive one-year periods unless terminated by either party upon sixty days’ notice prior to the end of any such one-year renewal period. During the fiscal years ended June 30, 2020 and June 30, 2019, Compass represented approximately 16% and 17% of our total revenues, respectively. Our Seed Pro software is utilized by vending machines operated by Compass for dynamic scheduling, pre-kitting, asset health management, and merchandising to Compass’s customers nationwide.

Global Payments

For many of our customers who receive Seed vending management solutions and Seed cashless services from us, the credit and debit card transaction processing services are provided by Global Payments, Inc. We entered into a three-year agreement with Global Payments on April 6, 2018, pursuant to which Global Payments acts as the provider of credit and debit card transaction processing services (including authorization and conveyance) for transactions on points of sale owned or operated by our customers. Our agreement with Global Payments automatically renews for successive one-year periods unless either party provides 60 days’ notice of non-renewal to the other party.

AT&T

In August 2017, we signed an agreement with AT&T for access to their LTE machine to machine wireless wide area network for the transport of data, including credit card transactions and inventory management data. The initial term of the agreement is five years. The agreement will automatically renew for successive one year periods unless terminated by either party upon thirty days’ notice.

16

MANUFACTURING

The Company utilizes independent third-party companies for the manufacturing of its products. Our internal manufacturing process mainly consists of quality assurance of materials and testing of finished goods received from our contract manufacturers. We have not entered into a long-term contract with our contract manufacturers, nor have we agreed to commit to purchase certain quantities of materials or finished goods from our manufacturers beyond those submitted under routine purchase orders, typically covering short-term forecasts.

COMPETITION

Our competitors are increasingly and actively marketing products and services that compete with our products and services in the vending industry, including manufacturers who may include in their new vending machines their own (or another third party’s) cashless payment systems and services. In addition to these competitors, there are also numerous credit card processors that offer card processing services to traditional retail establishments that could decide to offer similar services to the industries that we serve.

In the cashless laundry market, our joint solution with Setomatic Systems competes with hardware manufacturers, who provide joint solutions to their customers in partnership with payment processors, and with at least one competitor who provides an integrated hardware and payment processing solution.

TRADEMARKS, PROPRIETARY INFORMATION, AND PATENTS

The Company owns US federal registrations for the following trademarks and service marks: Because Machines Can't Cry For Help®, Blue Light Sequence®, Business Express®, Buzzbox®, Cantaloupe circle logo (design only), Cantaloupe Systems®, Cantaloupe Systems & design (Cantaloupe circle logo), Compuvend®, CM2iQ®, Creating Value Through Innovation®, EnergyMiser®, ePort®, ePort Connect®, ePort Edge®, ePort GO®, ePort Mobile®, eSuds®, Intelligent Vending®, SnackMiser®, Openvdi®, Routemaster®, Seed®, Seed & design, Seed Office®, SeedCashless & design, TransAct®, USA Technologies® USALive®, VendingMiser®, VendPro®, PC EXPRESS®, VENDSCREEN®, VM2iQ®, and Warehouse Master®.

Much of the technology developed or to be developed by the Company is subject to trade secret protection. To reduce the risk of loss of trade secret protection through disclosure, the Company has entered into confidentiality agreements with its key employees. There can be no assurance that the Company will be successful in maintaining such trade secret protection, that they will be recognized as trade secrets by a court of law, or that others will not capitalize on certain aspects of the Company’s technology.

From the incorporation of our Company in 1992, through June 30, 2020, 130 patents have been granted to the Company or its subsidiaries, including 95 United States patents and 35 foreign patents, and 4 United States and 6 international patent applications are pending. Of the 130 patents, 72 are still in force at June 30, 2020. Our patents expire between 2020 and 2038.

EMPLOYEES

As of June 30, 2020, the Company had 141 full-time employees and 6 part-time employees.

AVAILABLE INFORMATION

The public may read and copy any materials the Company files with the Securities and Exchange Commission (“SEC”), including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements for our annual stockholder meetings, and amendments to those reports, at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site that contains reports, proxy and other information regarding issuers that file electronically. Such information can be accessed through the internet at www.sec.gov. These reports are also available free of charge on our website, www.usatech.com, as soon as reasonably practical after we electronically file the material with, or furnish it to, the SEC.

17

Item 1A. Risk Factors.

Risks Relating to Our Business

We have a history of losses since inception and if we continue to incur losses, the price of our shares can be expected to fall.

We experienced losses from inception through June 30, 2012, and from fiscal year 2015 through fiscal year 2020. For fiscal years 2020, 2019, and 2018, we incurred a net loss of $40.6 million, $29.9 million, and $11.3 million, respectively. In light of our recent history of losses as well as the length of our history of losses, profitability in the foreseeable future is not assured. Until the Company’s products and services can generate sufficient annual revenues, the Company will be required to use its cash and cash equivalents on hand and may raise capital to meet its cash flow requirements including the issuance of common stock or debt financing. Additionally, if we continue to incur losses in the future, the price of our common stock can be expected to fall.

We may require additional financing or find it necessary to raise capital to sustain our operations and without it we may not be able to achieve our business plan.

At June 30, 2020, we had a net working capital surplus of $5.0 million and cash and cash equivalents of $31.7 million. We had net cash (used in) provided by operating activities of $(14.1) million, $(28.2) million, and $12.4 million for fiscal years ended 2020, 2019, and 2018, respectively. Unless we maintain or grow our current level of operations, we may need additional funds to continue these operations. We may also need additional capital to respond to unusual or unanticipated non-operational events. Such non-operational events include but are not limited to shareholder class action lawsuits, government inquiries or enforcement actions that could potentially arise from the circumstances that gave rise to our restatements, extended filing delays in filing our periodic reports and the impact of COVID-19 on our business. Should the financing that we require to sustain our working capital needs be unavailable or prohibitively expensive when we require it, the consequences could have a material adverse effect on our business, operating results, financial condition and prospects.

Failure to comply with any of the financial covenants under the Company’s credit agreement could result in an event of default which may accelerate our outstanding indebtedness or other obligations and have a material adverse impact on our business, liquidity position and financial position.

On August 14, 2020, the Company entered into a credit agreement with JPMorgan Chase Bank, N.A. (the “2021 JPMorgan Credit Agreement”) for a $5 million secured revolving credit facility and a $15 million secured term facility, which includes an uncommitted expansion feature that allows the Company to increase the total revolving commitments and/or add new tranches of term loans in an aggregate amount not to exceed $5 million. The obligations under the 2021 JPMorgan Credit Agreement are secured by first priority security interest in substantially all of the Company's assets. The 2021 JPMorgan Credit Agreement contains financial covenants requiring the Company (i) to maintain an adjusted quick ratio of not less than 2.00 to 1.00, not less than 2.50 to 1.00 beginning October 1, 2020, not less than 2.75 to 1.00 beginning January 1, 2021 and 3.00 to 1.00 beginning April 1, 2021 and (ii) to maintain, as of the end of each of its fiscal quarters commencing with the fiscal quarter ended December 31, 2021, a total leverage ratio of not greater than 3.00 to 1.00.

Failure to comply with the foregoing financial covenants, if not cured or waived, will result in an event of default that could trigger acceleration of our indebtedness, which would require us to repay all amounts owed under the 2021 JPMorgan Credit Agreement and could have a material adverse impact on our business, liquidity position and financial position.

We cannot be certain that our future operating results will be sufficient to ensure compliance with the financial covenants in our 2021 JPMorgan Credit Agreement or to remedy any defaults. In addition, in the event of any event of default and related acceleration, we may not have or be able to obtain sufficient funds to make the accelerated payments required under the 2021 JPMorgan Credit Agreement.

The loss of one or more of our key customers could significantly reduce our revenues, results of operations, and net income.

We have derived, and believe we may continue to derive, a significant portion of our revenues from one large customer or a limited number of large customers. Customer concentrations for the years ended June 30, 2020, 2019 and 2018 were as follows:

For the year ended June 30, | |||||||||

Single customer | 2020 | 2019 | 2018 | ||||||

Total revenue | 16 | % | 17 | % | 16 | % | |||

18

The loss of such customers could materially adversely affect our revenues. Additionally, a major customer in one year may not purchase any of our products or services in another year, which may negatively affect our financial performance. We have offered, and may in the future offer, discounts to our large customers to incentivize them to continue to utilize our products and services. If we are required to sell products to any of our large customers at reduced prices or unfavorable terms, our results of operations and revenue could be materially adversely affected. Further, there is no assurance that our customers will continue to utilize our transaction processing and related services as our customer agreements are generally cancelable by the customer on thirty to sixty days’ notice.

We depend on our key personnel and, if they leave us, or if we are unable to attract highly skilled personnel, our business could be adversely affected.

We are dependent on key management personnel, including the Chief Executive Officer, Sean Feeney, and the rest of the executive leadership team and several functional areas within the Company. The loss of services from these officers and employees could dramatically affect our business prospects. Our executive officers and certain of our officers and employees are particularly valuable to us because:

• | they have specialized knowledge about our company and operations; |

• | they have specialized skills that are important to our operations; or |

• | they would be particularly difficult to replace. |

We have entered into an employment agreement with Mr. Feeney, which contains customary restrictive covenants, including perpetual confidentiality, non-disparagement, and intellectual property covenants, as well as a non-compete, non-solicit of customers and suppliers, and non-solicit of employees (including a no-hire) that each apply during employment and for two years following any termination.