srcl-ex991_6.htm

EXHIBIT 99.1

FOR FURTHER INFORMATION CONTACT:

Investor Relations 847-607-2012

Stericycle, Inc. Reports Results for the Fourth Quarter and Full-Year Ended 2017

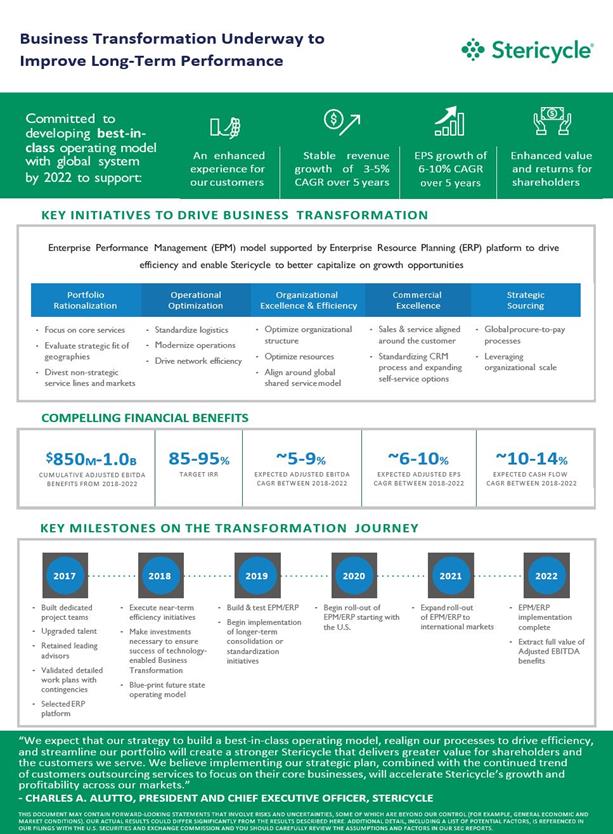

Provides Update on Comprehensive Business Transformation to Build Best-in-Class Operating Model

Program Expected to Drive Operational Efficiencies and Improve Long-Term Financial Performance, with $850 Million to $1 Billion in Cumulative Adjusted EBITDA* Benefits over 2018-2022

LAKE FOREST, Ill., Feb. 21, 2018 - Stericycle, Inc. (Nasdaq: SRCL) today reported results for the fourth quarter and the full-year ended December 31, 2017. The Company also provided additional details on its Business Transformation, which is expected to deliver $850 million to $1 billion of cumulative Adjusted EBITDA* benefits over the next five years.

“Stericycle has evolved significantly over the past 28 years, and today we are executing a company-wide, comprehensive strategy to position Stericycle for continued success well into the future,” said Charles A. Alutto, President and Chief Executive Officer. “Our strategy focuses on building a best-in-class enterprise performance management (“EPM”) operating model and includes streamlining our portfolio, realigning our processes and organizational structure to drive efficiency, and implementing an enterprise resource planning (“ERP”) system. We believe that the implementation of our strategic plan, combined with the continued trend of customers outsourcing services to focus on their core businesses, will accelerate Stericycle’s growth and profitability across our markets and deliver greater value to our shareholders.”

BUSINESS TRANSFORMATION AND PILLARS OF SUCCESS

Stericycle today provided additional details regarding its Business Transformation, which the Company began executing during the fourth quarter of 2017, to improve long-term operational and financial performance. As part of the Business Transformation, Stericycle plans to build a best-in-class EPM operating model to enable the Company to operate more efficiently, provide an enhanced experience to customers, better capitalize on future growth opportunities, and establish greater controls and oversight to drive more consistent results. Additionally, a key component of the Business Transformation is the implementation of an ERP system, which will leverage standard

1

processes throughout the organization to accelerate decision making, expedite acquisition integration, remediate compliance and control issues, and enable real-time analytics. For further information, see the accompanying Transformation Overview at http://investors.stericycle.com.

Key initiatives of the Business Transformation include:

|

|

• |

Portfolio Rationalization: Executing on a comprehensive review of the Company’s global service lines to identify and pursue the divestiture of non-strategic assets. |

|

|

• |

Operational Optimization: Standardizing route planning logistics, modernizing field operations, and driving network efficiency across facilities. |

|

|

• |

Organizational Excellence and Efficiency: Redesigning the Company’s organizational structure to optimize resources and align around a global shared business services model. |

|

|

• |

Commercial Excellence: Aligning our sales and service organizations around the customer, standardizing our customer relationship management processes, and expanding customer self-service options. |

|

|

• |

Strategic Sourcing: Reducing spend through global procure-to-pay processes and leveraging organizational scale. |

Transformation initiatives, inclusive of the implementation of best-in-class systems, are expected to deliver Adjusted EBITDA between 2018 and 2022 at a compound annual growth rate of 5% to 9%* and an Adjusted EPS compound annual growth rate of 6% to 10%*. Over this same period, the Company projects that it will generate a substantial amount of free cash flow, equivalent to a compound annual growth rate of 10% to 14%*. Stericycle expects to record approximately $275 to $300 million in adjusting items and capital expenditures associated with the Business Transformation over five years, with those investments delivering an anticipated internal rate of return greater than 85%.

2

FOURTH-QUARTER HIGHLIGHTS COMPARED TO PRIOR YEAR:

|

|

• |

Revenues of $887.8 million, a decrease of 2.1% |

|

|

• |

Gross profit of $344.0 million a decrease of 6.2%, and Adjusted gross profit of $345.1 million, a decrease of 7.5% |

|

|

• |

Earnings per share (“EPS”) of $0.97, due primarily to the favorable impact of $1.52 from U.S. tax reform, offset by a $0.79 non-cash goodwill impairment charge in Latin America and $0.20 of Business Transformation related expenses. Adjusted earnings per share (“Adjusted EPS”) of $1.00, inclusive of non-cash fixed asset depreciation and write-off charges, partially offset by international tax benefits |

|

|

• |

Began executing on comprehensive Business Transformation to align Stericycle with future growth opportunities, drive operational efficiencies and improve long-term financial performance |

FOURTH-QUARTER RESULTS

“During the fourth quarter, we continued to experience high growth from secure information destruction and the expansion of additional services within the hospital market, offset by an anticipated challenging comparison in Communication and Related Services due to a record recall event during the fourth quarter of 2016,” said Charles A. Alutto, President and Chief Executive Officer. “We began execution of our Business Transformation with the reorganization of our global workforce and are now focused on implementing additional measures to drive efficiencies. By standardizing our global processes and consolidating our disparate business systems, we will better position the company for long-term growth and improved financial performance.”

Revenues for the quarter ended December 31, 2017 were $887.8 million, a decrease of 2.1% from $906.4 million in the fourth quarter of last year. Acquisitions contributed $6.8 million to revenues. Divestitures reduced revenues by $10.2 million. On a constant currency basis, revenues decreased 3.0% compared to the fourth quarter of last year. Organic revenues decreased 2.6%, or decreased 2.4% when adjusted for Manufacturing and Industrial Services. Organic revenues were down as a result of a record recall event in our Communication and Related Service business in the fourth quarter of 2016. See Tables 1-A and 1-C.

Gross profit was $344.0 million, a decrease of 6.2% from $366.7 million in the fourth quarter of last year. Adjusted gross profit was $345.1 million, a decrease of 7.5% from $373.2 million in the fourth quarter of last year. Gross profit and Adjusted gross profit as a percentage of revenues were 38.7% and 38.9%, respectively, compared to 40.5% and 41.2%, respectively, in the fourth quarter of last year. See Unaudited Condensed Consolidated Statements of Income and Table 2-A.

3

EPS increased to $0.97 from $0.15 in the fourth quarter of last year, due primarily to the favorable impact of $1.52 from U.S. tax reform, offset by a $0.79 non-cash goodwill impairment charge in Latin America and $0.20 of Business Transformation related expenses. Adjusted EPS was $1.00 for the current quarter and the same quarter last year. The current quarter is inclusive of $0.14 of non-cash fixed asset depreciation and write-off charges. See Unaudited Condensed Consolidated Statements of Income and Table 2-A.

Cash flow from operations for the quarter was $116.6 million, down 18.5% from $143.0 million in the same period last year. For the quarter, the Company primarily allocated cash as follows: $8.8 million in dividends to its preferred shareholders; $3.4 million for preferred share repurchases; $26.3 million reduction in net debt; $28.7 million for acquisitions; and $51.3 million for capital expenditures, inclusive of $10.9 million for Business Transformation.

FULL-YEAR HIGHLIGHTS COMPARED TO PRIOR YEAR

|

|

• |

Revenues of $3.58 billion, an increase of 0.5% |

|

|

• |

Gross profit of $1.46 billion, a decrease of 1.6% and Adjusted gross profit of $1.46 billion, a decrease of 2.2% |

|

|

• |

EPS of $0.27, a decrease of 87.0%, due primarily to the impact of the previously announced small quantity customer class action settlement (the “Settlement”) and certain non-recurring litigation matters of $2.38, a $0.79 non-cash goodwill impairment charge in Latin America, and $0.23 of Business Transformation related expenses, partially offset by favorable impact of $1.52 from U.S. tax reform. Adjusted EPS of $4.34, a decrease of 4.2% |

FULL-YEAR RESULTS

Revenues for the full-year 2017 were $3.58 billion, an increase of 0.5% from $3.56 billion last year. Acquisitions contributed $32.2 million to revenues. Divestitures reduced revenues by $21.6 million. On a constant currency basis, revenues increased 0.8% compared to last year. Organic revenues grew 0.6%, or 1.4% when adjusted for Manufacturing and Industrial Services. See Tables 1B-1C.

Gross profit was $1.46 billion, a decrease of 1.6% from $1.49 billion last year. Adjusted gross profit was $1.46 billion, a decrease of 2.2% from $1.50 billion last year. Gross profit and Adjusted gross profit as a percentage of revenues were 40.8% and 40.9%, respectively, compared to 41.7% and 42.0%, respectively, last year. See Unaudited Condensed Consolidated Statements of Income and Table 2-B.

4

EPS decreased 87.0% to $0.27 from $2.08 last year, due primarily to the impact of the previously announced Settlement and certain non-recurring litigation matters of $2.38, a $0.79 non-cash goodwill impairment charge in Latin America, and $0.23 of Business Transformation related expenses, partially offset by favorable impact of $1.52 from U.S. tax reform. Adjusted EPS decreased 4.2% to $4.34 from $4.53 last year. See Unaudited Condensed Consolidated Statements of Income and Table 2-B.

Cash flow from operations for the year ended 2017 was $508.6 million, down 9.3% from $560.8 million last year. For the year, the Company primarily allocated cash as follows: $36.3 million in dividends to its preferred shareholders; $34.2 million for preferred share repurchases; a $256.3 million reduction in net debt; $52.5 million for acquisitions; and $143.0 million for capital expenditures.

“Our Business Transformation is expected to deliver significant financial benefits to Stericycle shareholders, including $850 million to $1 billion cumulative Adjusted EBITDA* benefit and Adjusted EBITDA* margin improvement at a compound annual growth rate of 5% to 9% between 2018 and 2022,” said Daniel V. Ginnetti, Executive Vice President and Chief Financial Officer. “We have made significant progress repaying our outstanding debt and continue to execute a disciplined capital deployment plan. In all, we believe the incremental benefits of the Business Transformation combined with our strong cash flow generation will provide the Company with numerous levers for additional value creation.”

U.S. CORPORATE TAX REFORM COMMENTARY

With the newly approved U.S. Tax Cuts and Jobs Act of 2017, the Company recorded a provisional amount of $129.8 million as an income tax benefit in the fourth quarter of 2017. This provisional amount is based on a benefit of $167.7 million for the expected reversal of certain deferred tax assets and liabilities in accordance with the corporate tax rate decrease from 35% to 21%, less a one-time transition tax of $24.3 million on remitted foreign earnings and profits and $13.6 million of expected foreign withholding taxes.

“The benefit of recently-enacted U.S. tax reform legislation will provide additional cash flow that we intend to utilize in support of our capital allocation priorities,” said Ginnetti.

* The Company is unable to forecast the comparable long-range U.S. GAAP financial measures without unreasonable effort due to the uncertainty and related unpredictability of non-recurring adjusted items exclusive of the Business Transformation investments referenced above.

5

FINANCIAL OUTLOOK

Stericycle today provided financial guidance for the full-year 2018, as summarized in the following table.

|

(In millions, except per share data) |

|

|

Revenues |

$3,480 - $3,630 |

|

|

Regulated Waste and Compliance Services |

$1,920 - $1,970 |

|

|

Secure Information Destruction Services |

$870 - $910 |

|

|

Communication and Related Services |

$355 - $385 |

|

|

Manufacturing and Industrial Services |

$335 - $365 |

|

|

|

|

|

|

|

Income from Operations |

$365 - $370 |

|

|

Adjusted EBITDA (a) |

$760 - $810 |

|

|

Interest Expense |

$95 - $100 |

|

|

Tax Rate |

26.0% - 26.5% |

|

|

Depreciation |

$130 - $140 |

|

|

Intangible Amortization |

$120 - $130 |

|

|

Diluted Earnings Per Share |

$2.09 - $2.21 |

|

|

Adjusted Diluted Earnings Per Share |

$4.45 - $4.85 |

|

|

Shares Outstanding |

|

90.5 |

|

|

|

|

|

|

|

Net Cash from Operating Activities |

$510 - $560 |

|

|

Capital Expenditures |

$160 - $180 |

|

|

Free Cash Flow |

$330 - $400 |

|

(a) Adjusted Earnings Before Interest, Tax, Depreciation and Amortization (Adjusted EBITDA) is Income from operations excluding specified items, inclusive of Depreciation and Intangible Amortization.

The Company’s guidance does not include amounts related to future acquisitions, divestitures or non-recurring litigation matters as the Company is not able to forecast these items without unreasonable effort. In addition, the Company’s guidance is based on currently known items and certain core business assumptions, including $0.17 from preferred share repurchases and using foreign exchange rates as of the end of December 2017. See Table 4.

CONFERENCE CALL INFORMATION

Conference call to be held February 21, 2018, 4:00 p.m. Central time – Dial 866-516-6872 at least 5 minutes before start time. Presentation materials will be posted 30 minutes prior to the conference call at http://investors.stericycle.com. If you are unable to participate on the call, a replay will be available for 30 days by dialing 855-859-2056 or 404-537-3406, access code 9994249. To hear a live simulcast of the call or access the audio archive, visit the investor relations page on http://investors.stericycle.com.

SAFE HARBOR STATEMENT

This document may contain forward-looking statements that involve risks and uncertainties, some of which are beyond our control (for example, general economic and market conditions). Our actual results could differ significantly from the results described here. Factors that could cause such differences include changes in governmental regulation of the collection, transportation, treatment and disposal of regulated waste or the proper handling and protection of personal and confidential information, the level of government enforcement of regulations governing regulated waste collection and treatment or the proper handling and protection of personal and confidential information, decreases in the volume of regulated wastes or personal and confidential information we

6

collect from customers, our ability to execute on our Business Transformation initiatives and achieve the anticipated benefits and cost savings, our obligations to service our substantial indebtedness and comply with the covenants and restrictions contained in our private placement notes and our credit agreement, political, economic, inflationary, currency and other risks related to our foreign operations, the outcome of pending or future litigation including litigation with respect to the U.S. Foreign Corrupt Practices Act, changing market conditions in the healthcare industry, competition and demand for services in the regulated waste and secure information destruction industries, our failure to maintain an effective system of internal control over financial reporting, disruptions in or attacks on our information technology systems, changes in the demand and price for recycled paper, charges related to our portfolio optimization strategy or the failure of our portfolio optimization strategy to achieve the desired results, as well as other factors described in our filings with the U.S. Securities and Exchange Commission, including our most recently filed Annual Report on Form 10-K and subsequent Forms 10-Q. As a result, past financial performance should not be considered a reliable indicator of future performance, and investors should not use historical trends to anticipate future results or trends. To the extent permitted under applicable law, we make no commitment to disclose any subsequent revisions to forward-looking statements.

7

|

STERICYCLE, INC. |

|

|

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF INCOME |

|

|

(In millions, except per share data) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three Months Ended December 31, |

|

|

Years Ended December 31, |

|

|

|

2017 |

|

|

2016 |

|

% Change |

|

|

2017 |

|

|

2016 |

|

% Change |

|

|

Revenues |

$ |

887.8 |

|

|

$ |

906.4 |

|

|

(2.1 |

%) |

|

$ |

3,580.7 |

|

|

$ |

3,562.3 |

|

|

0.5 |

% |

|

Cost of revenues |

|

543.8 |

|

|

|

539.7 |

|

|

0.8 |

% |

|

|

2,118.2 |

|

|

|

2,075.4 |

|

|

2.1 |

% |

|

Gross profit |

|

344.0 |

|

|

|

366.7 |

|

|

(6.2 |

%) |

|

|

1,462.5 |

|

|

|

1,486.9 |

|

|

(1.6 |

%) |

|

Selling, general and administrative expenses |

|

367.4 |

|

|

|

298.0 |

|

|

23.3 |

% |

|

|

1,470.1 |

|

|

|

1,053.1 |

|

|

39.6 |

% |

|

(Loss) income from operations |

|

(23.4 |

) |

|

|

68.7 |

|

|

(134.1 |

%) |

|

|

(7.6 |

) |

|

|

433.8 |

|

|

(101.8 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense, net |

|

(22.2 |

) |

|

|

(24.7 |

) |

|

(10.1 |

%) |

|

|

(93.7 |

) |

|

|

(97.8 |

) |

|

(4.2 |

%) |

|

Other expense, net |

|

(1.1 |

) |

|

|

(7.5 |

) |

|

(85.3 |

%) |

|

|

(6.6 |

) |

|

|

(7.9 |

) |

|

(16.5 |

%) |

|

(Loss) income before income taxes |

|

(46.7 |

) |

|

|

36.5 |

|

|

(227.9 |

%) |

|

|

(107.9 |

) |

|

|

328.1 |

|

|

(132.9 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income tax (benefit) expense |

|

(136.3 |

) |

|

|

17.6 |

|

nm |

|

|

|

(150.9 |

) |

|

|

120.2 |

|

|

(225.5 |

%) |

|

Net income |

|

89.6 |

|

|

|

18.9 |

|

|

374.1 |

% |

|

|

43.0 |

|

|

|

207.9 |

|

|

(79.3 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income attributable to noncontrolling interests |

|

0.4 |

|

|

|

0.2 |

|

|

100.0 |

% |

|

|

0.6 |

|

|

|

1.6 |

|

|

(62.5 |

%) |

|

Net income attributable to Stericycle, Inc. |

|

89.2 |

|

|

|

18.7 |

|

|

377.0 |

% |

|

|

42.4 |

|

|

|

206.3 |

|

|

(79.4 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mandatory convertible preferred stock dividend |

|

8.8 |

|

|

|

9.6 |

|

|

(8.3 |

%) |

|

|

36.3 |

|

|

|

39.4 |

|

|

(7.9 |

%) |

|

Gain on repurchase of preferred stock |

|

(2.9 |

) |

|

|

(3.6 |

) |

|

(19.4 |

%) |

|

|

(17.3 |

) |

|

|

(11.3 |

) |

|

53.1 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income attributable to common shareholders |

$ |

83.3 |

|

|

$ |

12.7 |

|

nm |

|

|

$ |

23.4 |

|

|

$ |

178.2 |

|

|

(86.9 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per common share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

$ |

0.98 |

|

|

$ |

0.15 |

|

nm |

|

|

$ |

0.27 |

|

|

$ |

2.10 |

|

|

(87.1 |

%) |

|

Diluted |

$ |

0.97 |

|

|

$ |

0.15 |

|

nm |

|

|

$ |

0.27 |

|

|

$ |

2.08 |

|

|

(87.0 |

%) |

|

Weighted average common shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

85.4 |

|

|

|

85.1 |

|

|

|

|

|

|

85.3 |

|

|

|

84.9 |

|

|

|

|

|

Diluted |

|

85.6 |

|

|

|

85.4 |

|

|

|

|

|

|

85.6 |

|

|

|

85.6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statistics (as a % of Revenues) - U.S. GAAP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross profit |

|

38.7 |

% |

|

|

40.5 |

% |

|

|

|

|

|

40.8 |

% |

|

|

41.7 |

% |

|

|

|

|

Selling, general and administrative expenses |

|

41.4 |

% |

|

|

32.9 |

% |

|

|

|

|

|

41.1 |

% |

|

|

29.6 |

% |

|

|

|

|

(Loss) income from operations |

|

-2.6 |

% |

|

|

7.6 |

% |

|

|

|

|

|

-0.2 |

% |

|

|

12.2 |

% |

|

|

|

|

EBITDA (1) |

|

5.5 |

% |

|

|

13.8 |

% |

|

|

|

|

|

6.8 |

% |

|

|

19.3 |

% |

|

|

|

|

Effective tax rate |

|

-291.9 |

% |

|

|

48.2 |

% |

|

|

|

|

|

-139.9 |

% |

|

|

36.6 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statistics (as a % of Revenues) - Adjusted (2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted gross profit |

|

38.9 |

% |

|

|

41.2 |

% |

|

|

|

|

|

40.9 |

% |

|

|

42.0 |

% |

|

|

|

|

Adjusted selling, general and administrative expenses |

|

21.8 |

% |

|

|

23.1 |

% |

|

|

|

|

|

21.9 |

% |

|

|

21.6 |

% |

|

|

|

|

Adjusted EBITA |

|

17.1 |

% |

|

|

18.0 |

% |

|

|

|

|

|

19.0 |

% |

|

|

20.4 |

% |

|

|

|

|

Adjusted EBITDA |

|

21.8 |

% |

|

|

21.2 |

% |

|

|

|

|

|

22.7 |

% |

|

|

23.9 |

% |

|

|

|

|

Effective tax rate |

|

26.6 |

% |

|

|

29.7 |

% |

|

|

|

|

|

32.7 |

% |

|

|

33.5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted gross profit (3) |

$ |

345.1 |

|

|

$ |

373.2 |

|

|

(7.5 |

%) |

|

$ |

1,463.6 |

|

|

$ |

1,495.9 |

|

|

(2.2 |

%) |

|

Adjusted EBITA (4) |

$ |

151.5 |

|

|

$ |

163.5 |

|

|

(7.3 |

%) |

|

$ |

680.9 |

|

|

$ |

727.6 |

|

|

(6.4 |

%) |

|

Adjusted EBITDA (5) |

$ |

193.9 |

|

|

$ |

192.6 |

|

|

0.7 |

% |

|

$ |

812.0 |

|

|

$ |

850.8 |

|

|

(4.6 |

%) |

|

Adjusted net Income attributable to common shareholders |

$ |

90.9 |

|

|

$ |

90.7 |

|

|

0.2 |

% |

|

$ |

393.4 |

|

|

$ |

412.7 |

|

|

(4.7 |

%) |

|

Adjusted Diluted Earnings Per Share |

$ |

1.00 |

|

|

$ |

1.00 |

|

|

– |

|

|

$ |

4.34 |

|

|

$ |

4.53 |

|

|

(4.2 |

%) |

|

Diluted shares outstanding, under if-converted method |

|

90.6 |

|

|

|

90.8 |

|

|

(0.2 |

%) |

|

|

90.7 |

|

|

|

91.1 |

|

|

(0.5 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation |

$ |

42.4 |

|

|

$ |

29.1 |

|

|

45.7 |

% |

|

$ |

131.1 |

|

|

$ |

123.2 |

|

|

6.4 |

% |

|

Intangible amortization |

$ |

29.9 |

|

|

$ |

27.0 |

|

|

10.7 |

% |

|

$ |

118.4 |

|

|

$ |

129.3 |

|

|

(8.4 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

nm - Percentage change is not meaningful.

|

|

(1) (Loss) income from operations excluding Depreciation and Intangible Amortization is referred to as Earnings Before Interest, Tax and Depreciation and Amortization (EBITDA).

(2) Adjusted financial measures are Non-GAAP measures and exclude specific items as described and reconciled to comparable U.S. GAAP financial measures in the Reconciliation of U.S. GAAP to Non-GAAP Financial Measures contained in this Press Release.

(3) Adjusted gross profit excluding specified items, as indicated in the previous footnote.

(4) Adjusted Earnings Before Interest, Tax and Amortization (Adjusted EBITA) is Income from operations excluding specified items, inclusive of Intangible Amortization.

(5) Adjusted Earnings Before Interest, Tax, Depreciation and Amortization (Adjusted EBITDA) is Income from operations excluding specified items, inclusive of Depreciation and Intangible Amortization.

8

|

STERICYCLE, INC. |

|

|

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS |

|

|

(In millions) |

|

|

|

|

|

|

|

|

|

|

|

|

December 31, |

|

|

|

2017 |

|

|

2016 |

|

|

ASSETS |

|

|

|

|

|

|

|

|

Current Assets: |

|

|

|

|

|

|

|

|

Cash and cash equivalents |

$ |

42.2 |

|

|

$ |

44.2 |

|

|

Accounts receivable, net |

|

624.1 |

|

|

|

634.9 |

|

|

Prepaid expenses |

|

80.0 |

|

|

|

46.2 |

|

|

Other current assets |

|

46.3 |

|

|

|

39.2 |

|

|

Assets held for sale |

|

20.8 |

|

|

|

9.1 |

|

|

Total Current Assets |

|

813.4 |

|

|

|

773.6 |

|

|

Property, plant and equipment, net |

|

741.0 |

|

|

|

723.9 |

|

|

Goodwill |

|

3,604.0 |

|

|

|

3,591.0 |

|

|

Intangible assets, net |

|

1,791.5 |

|

|

|

1,862.0 |

|

|

Other assets |

|

38.4 |

|

|

|

29.6 |

|

|

Total Assets |

$ |

6,988.3 |

|

|

$ |

6,980.1 |

|

|

|

|

|

|

|

|

|

|

|

LIABILITIES AND SHAREHOLDERS' EQUITY |

|

|

|

|

|

|

|

|

Current Liabilities: |

|

|

|

|

|

|

|

|

Current portion of long-term debt |

$ |

119.5 |

|

|

$ |

72.8 |

|

|

Bank overdrafts |

|

7.0 |

|

|

|

4.4 |

|

|

Accounts payable |

|

195.2 |

|

|

|

172.3 |

|

|

Accrued liabilities |

|

588.1 |

|

|

|

228.5 |

|

|

Deferred revenues |

|

17.9 |

|

|

|

17.9 |

|

|

Other current liabilities |

|

36.6 |

|

|

|

44.1 |

|

|

Liabilities held for sale |

|

5.1 |

|

|

|

2.9 |

|

|

Total Current Liabilities |

|

969.4 |

|

|

|

542.9 |

|

|

|

|

|

|

|

|

|

|

|

Long-term debt, net |

|

2,615.3 |

|

|

|

2,877.3 |

|

|

Deferred income taxes |

|

371.1 |

|

|

|

645.4 |

|

|

Long-term tax payable |

|

55.8 |

|

|

|

34.2 |

|

|

Other liabilities |

|

68.1 |

|

|

|

63.9 |

|

|

Total Liabilities |

|

4,079.7 |

|

|

|

4,163.7 |

|

|

|

|

|

|

|

|

|

|

|

Commitments and contingencies |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equity: |

|

|

|

|

|

|

|

|

Preferred stock |

|

- |

|

|

|

- |

|

|

Common stock |

|

0.9 |

|

|

|

0.8 |

|

|

Additional paid-in capital |

|

1,153.2 |

|

|

|

1,166.5 |

|

|

Retained earnings |

|

2,029.5 |

|

|

|

2,006.1 |

|

|

Accumulated other comprehensive loss |

|

(287.0 |

) |

|

|

(367.6 |

) |

|

Total Shareholders' Equity |

|

2,896.6 |

|

|

|

2,805.8 |

|

|

Noncontrolling interests |

|

12.0 |

|

|

|

10.6 |

|

|

Total Equity |

|

2,908.6 |

|

|

|

2,816.4 |

|

|

Total Liabilities and Equity |

$ |

6,988.3 |

|

|

$ |

6,980.1 |

|

9

|

STERICYCLE, INC. |

|

|

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS |

|

|

(In millions) |

|

|

|

|

|

|

|

|

|

|

|

Years Ended December 31, |

|

|

|

2017 |

|

2016 |

|

|

OPERATING ACTIVITIES: |

|

|

|

|

|

|

|

Net Income |

$ |

43.0 |

|

$ |

207.9 |

|

|

Adjustments to reconcile net income to net cash provided by operating activities: |

|

|

|

|

|

|

|

Depreciation |

|

131.1 |

|

|

123.2 |

|

|

Intangible amortization |

|

118.4 |

|

|

129.3 |

|

|

Stock-based compensation expense |

|

21.3 |

|

|

20.5 |

|

|

Deferred income taxes |

|

(290.2 |

) |

|

7.1 |

|

|

Asset impairment charges and loss (gain) on disposal of assets held for sale |

|

112.2 |

|

|

28.5 |

|

|

Other, net |

|

(6.7 |

) |

|

1.0 |

|

|

Changes in operating assets and liabilities, net of effect of acquisitions and divestitures: |

|

|

|

|

|

|

|

Accounts receivable |

|

17.1 |

|

|

(43.1 |

) |

|

Prepaid expenses |

|

(33.9 |

) |

|

(1.2 |

) |

|

Accounts payable |

|

22.9 |

|

|

5.2 |

|

|

Accrued liabilities |

|

363.0 |

|

|

28.5 |

|

|

Other assets and liabilities |

|

10.4 |

|

|

53.9 |

|

|

Net cash provided by operating activities |

|

508.6 |

|

|

560.8 |

|

|

|

|

|

|

|

|

|

|

INVESTING ACTIVITIES: |

|

|

|

|

|

|

|

Capital expenditures |

|

(143.0 |

) |

|

(136.2 |

) |

|

Payments for acquisitions, net of cash acquired |

|

(52.5 |

) |

|

(63.9 |

) |

|

Proceeds from divestitures of businesses and sale of other assets |

|

2.5 |

|

|

2.1 |

|

|

Other, net |

|

- |

|

|

2.4 |

|

|

Net cash used in investing activities |

|

(193.0 |

) |

|

(195.6 |

) |

|

|

|

|

|

|

|

|

|

FINANCING ACTIVITIES: |

|

|

|

|

|

|

|

Repayments of long-term debt and other obligations |

|

(62.1 |

) |

|

(89.2 |

) |

|

Repayments of foreign bank debt, net |

|

(18.6 |

) |

|

(7.9 |

) |

|

Repayments of term loan, net |

|

(50.0 |

) |

|

(250.0 |

) |

|

Repayment of private placement of long-term note |

|

(175.0 |

) |

|

- |

|

|

Proceeds from senior credit facility, net |

|

49.4 |

|

|

71.6 |

|

|

Proceeds from (repayment of) bank overdrafts, net |

|

2.4 |

|

|

(13.6 |

) |

|

Payments of capital lease obligations |

|

(3.6 |

) |

|

(5.3 |

) |

|

Payments of deferred financing costs |

|

(2.7 |

) |

|

(0.6 |

) |

|

Proceeds from issuance (repurchase of) common stock, net |

|

10.2 |

|

|

(3.3 |

) |

|

Payments for repurchase of mandatory convertible preferred stock |

|

(34.2 |

) |

|

(30.9 |

) |

|

Dividends paid on mandatory convertible preferred stock |

|

(36.3 |

) |

|

(39.4 |

) |

|

Payments to noncontrolling interests |

|

(0.7 |

) |

|

(8.2 |

) |

|

Net cash used in financing activities |

|

(321.2 |

) |

|

(376.8 |

) |

|

|

|

|

|

|

|

|

|

Effect of exchange rate changes on cash and cash equivalents |

|

3.6 |

|

|

0.2 |

|

|

Net change in cash and cash equivalents |

|

(2.0 |

) |

|

(11.4 |

) |

|

Cash and cash equivalents at beginning of year |

|

44.2 |

|

|

55.6 |

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents at end of year |

$ |

42.2 |

|

$ |

44.2 |

|

|

|

|

|

|

|

|

|

|

SUPPLEMENTAL CASH FLOW INFORMATION: |

|

|

|

|

|

|

|

Net issuances of obligations for acquisitions |

$ |

16.5 |

|

$ |

44.2 |

|

|

Accrued capital expenditures |

$ |

5.0 |

|

$ |

6.2 |

|

|

Interest paid during the year |

$ |

85.8 |

|

$ |

88.8 |

|

|

Income taxes paid during the year, net of refunds |

$ |

128.9 |

|

$ |

111.5 |

|

10

RECONCILIATION OF U.S. GAAP TO NON-GAAP FINANCIAL MEASURES (UNAUDITED)

Table 1 – A: RECONCILIATION OF REVENUES TO ADJUSTED REVENUES –

THREE MONTHS ENDED DECEMBER 31, 2017

|

|

|

Three Months Ended December 31, |

|

|

|

|

In millions |

|

|

Percentage Change (%) |

|

|

|

|

2017 |

|

|

|

|

2016 |

|

|

Change |

|

|

Organic |

|

Acquisitions, Net of Divestitures |

|

Foreign Exchange |

|

Change |

|

|

Revenues by Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Regulated Waste and Compliance Services |

|

$ |

497.7 |

|

|

|

|

$ |

512.8 |

|

|

$ |

(15.1 |

) |

|

|

(2.3 |

%) |

|

(1.6 |

%) |

|

0.9 |

% |

|

(2.9 |

%) |

|

Secure Information Destruction Services |

|

|

202.2 |

|

|

|

|

|

185.2 |

|

|

|

17.0 |

|

|

|

5.5 |

% |

|

2.3 |

% |

|

1.4 |

% |

|

9.2 |

% |

|

Communication and Related Services |

|

|

97.2 |

|

|

|

|

|

112.4 |

|

|

|

(15.2 |

) |

|

|

(15.4 |

%) |

|

1.1 |

% |

|

0.7 |

% |

|

(13.5 |

%) |

|

Manufacturing and Industrial Services |

|

|

90.7 |

|

|

|

|

|

96.0 |

|

|

|

(5.3 |

) |

|

|

(4.7 |

%) |

|

(0.8 |

%) |

|

(0.0 |

%) |

|

(5.5 |

%) |

|

Total Revenues |

|

|

887.8 |

|

|

|

|

|

906.4 |

|

|

|

(18.6 |

) |

|

|

(2.6 |

%) |

|

(0.4 |

%) |

|

0.9 |

% |

|

(2.1 |

%) |

|

Less: Manufacturing and Industrial Services |

|

|

(90.7 |

) |

|

|

|

|

(96.0 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Revenues, as Adjusted |

|

$ |

797.1 |

|

|

|

|

$ |

810.4 |

|

|

$ |

(13.3 |

) |

|

|

(2.4 |

%) |

|

(0.3 |

%) |

|

1.0 |

% |

|

(1.6 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenues by Geography |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Domestic and Canada |

|

$ |

716.4 |

|

|

|

|

$ |

725.3 |

|

|

$ |

(8.9 |

) |

|

|

(2.2 |

%) |

|

0.7 |

% |

|

0.3 |

% |

|

(1.2 |

%) |

|

International |

|

|

171.4 |

|

|

|

|

|

181.1 |

|

|

|

(9.7 |

) |

|

|

(4.2 |

%) |

|

(4.8 |

%) |

|

3.6 |

% |

|

(5.4 |

%) |

|

Total Revenues |

|

$ |

887.8 |

|

|

|

|

$ |

906.4 |

|

|

$ |

(18.6 |

) |

|

|

(2.6 |

%) |

|

(0.4 |

%) |

|

0.9 |

% |

|

(2.1 |

%) |

Table 1 – B: RECONCILIATION OF REVENUES TO ADJUSTED REVENUES –

YEAR ENDED DECEMBER 31, 2017

|

|

|

Year Ended December 31, |

|

|

|

|

In millions |

|

|

Percentage Change (%) |

|

|

|

|

2017 |

|

|

|

|

2016 |

|

|

Change |

|

|

Organic |

|

Acquisitions, Net of Divestitures |

|

Foreign Exchange |

|

Change |

|

|

Revenues by Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Regulated Waste and Compliance Services |

|

$ |

2,023.6 |

|

|

|

|

$ |

2,063.0 |

|

|

$ |

(39.4 |

) |

|

|

(1.0 |

%) |

|

(0.6 |

%) |

|

(0.3 |

%) |

|

(1.9 |

%) |

|

Secure Information Destruction Services |

|

|

823.4 |

|

|

|

|

|

747.5 |

|

|

|

75.9 |

|

|

|

7.4 |

% |

|

2.9 |

% |

|

(0.2 |

%) |

|

10.2 |

% |

|

Communication and Related Services |

|

|

382.6 |

|

|

|

|

|

370.4 |

|

|

|

12.2 |

|

|

|

2.2 |

% |

|

1.3 |

% |

|

(0.2 |

%) |

|

3.3 |

% |

|

Manufacturing and Industrial Services |

|

|

351.1 |

|

|

|

|

|

381.4 |

|

|

|

(30.3 |

) |

|

|

(6.1 |

%) |

|

(0.8 |

%) |

|

(1.0 |

%) |

|

(7.9 |

%) |

|

Total Revenues |

|

|

3,580.7 |

|

|

|

|

|

3,562.3 |

|

|

|

18.4 |

|

|

|

0.6 |

% |

|

0.3 |

% |

|

(0.3 |

%) |

|

0.5 |

% |

|

Less: Manufacturing and Industrial Services |

|

|

(351.1 |

) |

|

|

|

|

(381.4 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Revenues, as Adjusted |

|

$ |

3,229.6 |

|

|

|

|

$ |

3,180.9 |

|

|

$ |

48.7 |

|

|

|

1.4 |

% |

|

0.4 |

% |

|

(0.3 |

%) |

|

1.5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenues by Geography |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Domestic and Canada |

|

$ |

2,873.1 |

|

|

|

|

$ |

2,810.6 |

|

|

$ |

62.5 |

|

|

|

1.2 |

% |

|

0.9 |

% |

|

0.1 |

% |

|

2.2 |

% |

|

International |

|

|

707.6 |

|

|

|

|

|

751.7 |

|

|

|

(44.1 |

) |

|

|

(1.8 |

%) |

|

(2.0 |

%) |

|

(2.1 |

%) |

|

(5.9 |

%) |

|

Total Revenues |

|

$ |

3,580.7 |

|

|

|

|

$ |

3,562.3 |

|

|

$ |

18.4 |

|

|

|

0.6 |

% |

|

0.3 |

% |

|

(0.3 |

%) |

|

0.5 |

% |

Table 1 – C: DISAGGREGATED REVENUES CHANGE

|

(In millions) |

|

|

|

Three Months Ended December 31, 2017 |

|

|

Year Ended

December 31, 2017 |

|

|

Organic |

$ |

(23.6 |

) |

|

$ |

20.1 |

|

|

Acquisitions |

|

6.8 |

|

|

|

32.2 |

|

|

Divestitures |

|

(10.2 |

) |

|

|

(21.6 |

) |

|

Foreign exchange |

|

8.4 |

|

|

|

(12.3 |

) |

|

Total Change |

$ |

(18.6 |

) |

|

$ |

18.4 |

|

11

Table 2 – A: THREE MONTHS ENDED DECEMBER 31, 2017 AND 2016

|

(In millions, except per share data) |

|

|

|

Three Months Ended December 31, 2017 |

|

|

|

Gross Profit |

|

|

Selling, General and Administrative Expenses |

|

|

(Loss) Income from Operations (b) |

|

|

Net Income Attributable to Common Shareholders (c) |

|

|

Diluted Earnings Per Share |

|

|

U.S. GAAP Financial Measures |

$ |

344.0 |

|

|

$ |

367.4 |

|

|

$ |

(23.4 |

) |

|

$ |

83.3 |

|

|

$ |

0.97 |

|

|

Adjustments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Transformation (1) |

|

0.7 |

|

|

|

(26.4 |

) |

|

|

27.1 |

|

|

|

17.4 |

|

|

|

0.20 |

|

|

Intangible Amortization (2) |

|

- |

|

|

|

(29.9 |

) |

|

|

29.9 |

|

|

|

19.6 |

|

|

|

0.23 |

|

|

Acquisition and Integration (3) |

|

- |

|

|

|

(7.2 |

) |

|

|

7.2 |

|

|

|

3.9 |

|

|

|

0.05 |

|

|

Operational Optimization (4) |

|

0.4 |

|

|

|

(18.3 |

) |

|

|

18.7 |

|

|

|

12.2 |

|

|

|

0.14 |

|

|

Divestitures (5) |

|

- |

|

|

|

3.2 |

|

|

|

(3.2 |

) |

|

|

(3.1 |

) |

|

|

(0.04 |

) |

|

Litigation, Settlements and Regulatory Compliance (6) |

|

- |

|

|

|

(22.7 |

) |

|

|

22.7 |

|

|

|

6.8 |

|

|

|

0.08 |

|

|

Capital Allocation (7) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

8.8 |

|

|

|

0.05 |

|

|

Impairment (8) |

|

- |

|

|

|

(65.0 |

) |

|

|

65.0 |

|

|

|

67.2 |

|

|

|

0.79 |

|

|

Other (9) |

|

- |

|

|

|

(7.5 |

) |

|

|

7.5 |

|

|

|

4.6 |

|

|

|

0.05 |

|

|

U.S. Tax Reform (10) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

(129.8 |

) |

|

|

(1.52 |

) |

|

Adjusted Financial Measures (a) |

$ |

345.1 |

|

|

$ |

193.6 |

|

|

$ |

151.5 |

|

|

$ |

90.9 |

|

|

$ |

1.00 |

|

|

(In millions, except per share data) |

|

|

|

Three Months Ended December 31, 2016 |

|

|

|

Gross Profit |

|

|

Selling, General and Administrative Expenses |

|

|

Income from Operations (b) |

|

|

Net Income Attributable to Common Shareholders (c) |

|

|

Diluted Earnings Per Share |

|

|

U.S. GAAP Financial Measures |

$ |

366.7 |

|

|

$ |

298.0 |

|

|

$ |

68.7 |

|

|

$ |

12.7 |

|

|

$ |

0.15 |

|

|

Adjustments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Transformation (1) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

Intangible Amortization (2) |

|

- |

|

|

|

(27.0 |

) |

|

|

27.0 |

|

|

|

17.3 |

|

|

|

0.20 |

|

|

Acquisition and Integration (3) |

|

- |

|

|

|

(14.9 |

) |

|

|

14.9 |

|

|

|

15.5 |

|

|

|

0.19 |

|

|

Operational Optimization (4) |

|

6.5 |

|

|

|

(7.3 |

) |

|

|

13.8 |

|

|

|

2.9 |

|

|

|

0.03 |

|

|

Divestitures (5) |

|

- |

|

|

|

(27.1 |

) |

|

|

27.1 |

|

|

|

23.1 |

|

|

|

0.27 |

|

|

Litigation, Settlements and Regulatory Compliance (6) |

|

- |

|

|

|

(1.8 |

) |

|

|

1.8 |

|

|

|

1.1 |

|

|

|

0.01 |

|

|

Capital Allocation (7) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

9.6 |

|

|

|

0.05 |

|

|

Impairment (8) |

|

- |

|

|

|

(1.4 |

) |

|

|

1.4 |

|

|

|

1.4 |

|

|

|

0.02 |

|

|

Other (9) |

|

- |

|

|

|

(8.8 |

) |

|

|

8.8 |

|

|

|

7.1 |

|

|

|

0.08 |

|

|

U.S. Tax Reform (10) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

Adjusted Financial Measures (a) |

$ |

373.2 |

|

|

$ |

209.7 |

|

|

$ |

163.5 |

|

|

$ |

90.7 |

|

|

$ |

1.00 |

|

U.S. GAAP results for the three months ended December 31, 2017 and 2016 include:

(1) Business Transformation

2017: Cost of revenues (“COR”) includes $0.7 million for employee termination. Selling, general and administrative expenses (“SG&A”) include $12.1 million of consulting and professional services, $10.8 million for employee termination, $2.4 million non-cash impairment of long-lived assets, and $1.1 million of other related expenses.

2016: No Business Transformation initiatives.

(2) Intangible Amortization

2017 and 2016: SG&A includes $29.9 million and $27.0 million, respectively, of intangible amortization expense from acquisitions.

(3) Acquisition and Integration

2017: SG&A includes $4.5 million acquisition expenses, $4.0 million integration expenses, and a $1.3 million favorable change in fair value of contingent consideration. During the fourth quarter of 2017, we made 6 acquisitions.

2016: SG&A includes $1.8 million acquisition expenses and $13.1 million integration expenses. During the fourth quarter of 2016, we made 9 acquisitions.

(4) Operational Optimization

2017: COR includes $0.4 million of charges related to facility rationalization in the U.K. SG&A includes $8.8 million of charges related to facility rationalization in Japan, primarily non-cash impairment charges for long-lived assets and operating permits; $6.9 million of charges, primarily in the U.S., to improve operational efficiency; $1.9 million in non-cash impairment charges in the U.S. and Brazil; and $0.7 million related to contract exit charges in the U.K.

12

2016: COR includes $6.5 million of charges to exit certain of our patient transport services contracts in the U.K. SG&A includes $7.3 million primarily for consulting and professional services to reduce operational redundancies in the U.S.

(5) Divestitures

2017: SG&A includes a $3.0 million gain on the sale of assets held for sale in South Africa, and a $0.2 million change in fair value of assets held for sale in the U.K.

2016: SG&A includes a $25.5 million charge on certain of our U.K. operations that were classified as assets held for sale, primarily non-cash impairment charges for customer relationships, operating permits, goodwill and long-lived assets, and a $1.6 million loss from sale of certain assets in the U.K.

(6) Litigation, Settlements, and Regulatory Compliance

2017 and 2016: SG&A includes $22.7 million and $1.8 million, respectively, in regulatory compliance, consulting and professional services, primarily related to certain non-recurring litigation matters.

(7) Capital Allocation

2017 and 2016 includes dividends on our Series A mandatory convertible preferred stock of $8.8 million and $9.6 million, respectively.

For the purpose of calculating the ultimate EPS impact of our mandatory convertible preferred stock, we show the impact by excluding the mandatory convertible preferred stock dividend and using the “if-converted” method of share dilution. This provides insight to how our diluted share count will be affected after these preferred shares are converted to common shares.

The impact of excluding the preferred stock dividend from Adjusted Diluted EPS is $0.10 and $0.11 for the fourth quarter 2017 and 2016, respectively. The increase in diluted shares outstanding under the “if-converted” method is 5.0 million and 5.4 million for the fourth quarter 2017 and 2016, respectively.

The impact of all adjusted items under the “if-converted” method to our Adjusted Diluted EPS has a dilutive effect of $0.05 and $0.06 for the fourth quarter 2017 and 2016, respectively.

(8) Impairment

2017: SG&A includes a $65.0 million non-cash goodwill impairment charge in Latin America.

2016: SG&A includes a $1.4 million non-cash operating permit impairment charge in Japan.

(9) Other

2017: SG&A includes $7.5 million of consulting and professional services related to the implementation of the new revenue recognition and lease accounting standards as well as internal control remediation activities.

2016: SG&A includes $8.8 million of consulting and professional services related to internal control remediation activities and implementation of the new revenue recognition standard. Other expense, net includes a $2.5 million non-cash impairment charge.

(10) U.S. Tax Reform

2017 includes tax benefit of $129.8 million from the provisional recording of the impact of U.S. tax reform.

(a) The Non-GAAP financial measures contained in this press release are reconciled to the most comparable measures calculated in accordance with U.S. GAAP in the schedules attached to this release. Management believes the Non-GAAP financial measures represent the amounts directly related to the ongoing operations of the business and uses these measures in evaluating performance. All Non-GAAP financial measures are intended to supplement the applicable U.S. GAAP measures and should not be considered in isolation from, or a replacement for, financial measures prepared in accordance with U.S. GAAP and may not be comparable to, or calculated in the same manner as Non-GAAP financial measures published by other companies.

(b) Adjusted Earnings Before Interest, Tax and Amortization (Adjusted EBITA) is Income from operations excluding specified items, inclusive of Intangible Amortization.

(c) Under the Net Income Attributable to Common Shareholder column, adjustments are shown net of tax in aggregate of $46.5 million and $28.9 million for the three months ended December 31, 2017 and 2016, respectively, based on applying either the statutory tax rate for the jurisdictions in which the adjustment occurred or, by adjusting the tax effect to consider the impact of applying an annual effective tax rate on an interim basis.

13

Table 2 – B: YEARS ENDED DECEMBER 31, 2017 AND 2016

|

(In millions, except per share data) |

|

|

|

Year Ended December 31, 2017 |

|

|

|

Gross Profit |

|

|

Selling, General and Administrative Expenses |

|

|

Income from Operations (b) |

|

|

Net Income Attributable to Common Shareholders (c) |

|

|

Diluted Earnings Per Share |

|

|

U.S. GAAP Financial Measures |

$ |

1,462.5 |

|

|

$ |

1,470.1 |

|

|

$ |

(7.6 |

) |

|

$ |

23.4 |

|

|

$ |

0.27 |

|

|

Adjustments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Transformation (1) |

|

0.7 |

|

|

|

(30.6 |

) |

|

|

31.3 |

|

|

|

20.0 |

|

|

|

0.23 |

|

|

Intangible Amortization (2) |

|

- |

|

|

|

(118.4 |

) |

|

|

118.4 |

|

|

|

77.4 |

|

|

|

0.90 |

|

|

Acquisition and Integration (3) |

|

- |

|

|

|

(40.7 |

) |

|

|

40.7 |

|

|

|

26.2 |

|

|

|

0.31 |

|

|

Operational Optimization (4) |

|

0.4 |

|

|

|

(70.7 |

) |

|

|

71.1 |

|

|

|

46.8 |

|

|

|

0.55 |

|

|

Divestitures (5) |

|

- |

|

|

|

(9.5 |

) |

|

|

9.5 |

|

|

|

7.1 |

|

|

|

0.08 |

|

|

Litigation, Settlements and Regulatory Compliance (6) |

|

- |

|

|

|

(327.7 |

) |

|

|

327.7 |

|

|

|

203.5 |

|

|

|

2.38 |

|

|

Capital Allocation (7) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

36.3 |

|

|

|

0.17 |

|

|

Impairment (8) |

|

- |

|

|

|

(65.0 |

) |

|

|

65.0 |

|

|

|

67.2 |

|

|

|

0.79 |

|

|

Other (9) |

|

- |

|

|

|

(24.8 |

) |

|

|

24.8 |

|

|

|

15.3 |

|

|

|

0.18 |

|

|

U.S. Tax Reform (10) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

(129.8 |

) |

|

|

(1.52 |

) |

|

Adjusted Financial Measures (a) |

$ |

1,463.6 |

|

|

$ |

782.7 |

|

|

$ |

680.9 |

|

|

$ |

393.4 |

|

|

$ |

4.34 |

|

|

(In millions, except per share data) |

|

|

|

Year Ended December 31, 2016 |

|

|

|

Gross Profit |

|

|

Selling, General and Administrative Expenses |

|

|

Income from Operations (b) |

|

|

Net Income Attributable to Common Shareholders (c) |

|

|

Diluted Earnings Per Share |

|

|

U.S. GAAP Financial Measures |

$ |

1,486.9 |

|

|

$ |

1,053.1 |

|

|

$ |

433.8 |

|

|

$ |

178.2 |

|

|

$ |

2.08 |

|

|

Adjustments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Transformation (1) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

Intangible Amortization (2) |

|

- |

|

|

|

(129.3 |

) |

|

|

129.3 |

|

|

|

83.5 |

|

|

|

0.98 |

|

|

Acquisition and Integration (3) |

|

|

|

|

|

(60.9 |

) |

|

|

60.9 |

|

|

|

38.1 |

|

|

|

0.44 |

|

|

Operational Optimization (4) |

|

9.0 |

|

|

|

(50.1 |

) |

|

|

59.1 |

|

|

|

40.4 |

|

|

|

0.47 |

|

|

Divestitures (5) |

|

- |

|

|

|

(27.1 |

) |

|

|

27.1 |

|

|

|

23.2 |

|

|

|

0.27 |

|

|

Litigation, Settlements and Regulatory Compliance (6) |

|

- |

|

|

|

(7.2 |

) |

|

|

7.2 |

|

|

|

4.4 |

|

|

|

0.05 |

|

|

Capital Allocation (7) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

39.4 |

|

|

|

0.17 |

|

|

Impairment (8) |

|

- |

|

|

|

(1.4 |

) |

|

|

1.4 |

|

|

|

1.4 |

|

|

|

0.02 |

|

|

Other (9) |

|

- |

|

|

|

(8.8 |

) |

|

|

8.8 |

|

|

|

4.1 |

|

|

|

0.05 |

|

|

U.S. Tax Reform (10) |

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

Adjusted Financial Measures (a) |

$ |

1,495.9 |

|

|

$ |

768.3 |

|

|

$ |

727.6 |

|

|

$ |

412.7 |

|

|

$ |

4.53 |

|

U.S. GAAP results for the years ended December 31, 2017 and 2016 include:

(1) Business Transformation

2017: COR includes $0.7 million for employee termination. SG&A includes $16.4 million of consulting and professional services, $10.8 million for employee termination, $2.4 million non-cash impairment of long-lived assets, and $1.0 million of other related expenses.

2016: No Business Transformation initiatives.

(2) Intangible Amortization

2017 and 2016: SG&A includes $118.4 million and $129.3 million, respectively, of intangible amortization expense from acquisitions.

(3) Acquisition and Integration

2017: SG&A includes $10.6 million acquisition expenses, $30.5 million integration expenses, and a $0.4 million favorable change in fair value of contingent consideration. During 2017, we made 30 acquisitions.

2016: SG&A includes $9.6 million acquisition expenses, $53.3 million integration expenses, primarily related to the fourth quarter 2015 Shred-it acquisition, and a $2.0 million favorable change in fair value of contingent consideration. During 2016, we made 31 acquisitions.

(4) Operational Optimization

2017: COR includes $0.4 million of charges related to facility rationalization in the U.K. SG&A includes $41.6 million in the U.S. ($8.9 million non-cash impairment charges related to operating permits and rationalization of tradenames, $1.6 million employee termination, $9.2 million consulting and professional services to reduce operational redundancies, and $21.9 million to improve operational efficiency; $15.7 million operational optimization costs in Latin America ($3.2 million employee termination, $8.3 million non-cash impairment charges for long-lived assets, operating permits and

14

customer relationships, and $4.2 million other rationalization and environmental costs); $8.8 million of charges related to facility rationalization in Japan, primarily non-cash impairment charges for long-lived assets and operating permits; and $4.6 million of contract exit charges in the U.K.

2016: COR includes $9.0 million of charges to exit certain of our patient transport services contracts in the U.K. SG&A includes $17.5 million of charges to exit certain of our patient transport services contracts and plant conversion expense in the U.K. and $32.6 million operational optimization costs ($4.5 million employee termination, $12.0 million consulting and professional services, and $16.1 million to improve operational efficiency).

(5) Divestitures

2017: SG&A includes $5.9 million of non-cash asset impairment charges related to changes in the fair value of disposal groups held for sale in the U.K., and a $6.6 million loss from sale of certain assets and liabilities in the U.K., partially offset by a $3.0 million gain on the sale of assets held for sale in South Africa.

2016: SG&A includes a $25.5 million charge on certain of our U.K. operations that were classified as assets held for sale, primarily non-cash impairment charges for customer relationships, operating permits, goodwill and long-lived assets, and a $1.6 million loss from the sale of certain assets in the U.K.

(6) Litigation, Settlements, and Regulatory Compliance

2017: SG&A includes $295.0 million for the small quantity customer class action settlement and $32.7 million in regulatory compliance, consulting and professional services, primarily related to certain non-recurring litigation matters.

2016: SG&A includes $7.2 million in regulatory compliance, consulting and professional services, primarily related to certain non-recurring litigation matters.

(7) Capital Allocation

2017 and 2016 includes dividends on our Series A mandatory convertible preferred stock of $36.3 million and $39.4 million, respectively.

For the purpose of calculating the ultimate EPS impact of our mandatory convertible preferred stock, we show the impact by excluding the mandatory convertible preferred stock dividend and using the “if-converted” method of share dilution. This provides insight to how our diluted share count will be affected after these preferred shares are converted to common shares.

The impact of excluding the preferred stock dividend from Adjusted Diluted EPS is $0.42 and $0.46 for the year ended 2017 and 2016, respectively.

The increase in diluted shares outstanding under the “if-converted” method is 5.1 million and 5.5 million for the year ended 2017 and 2016, respectively.

The impact of all adjusted items under the “if-converted” method to our Adjusted Diluted EPS has a dilutive effect of $0.25 and $0.29 for the year ended 2017 and 2016, respectively.

(8) Impairment

2017: SG&A includes a $65.0 million non-cash goodwill impairment charge in Latin America.

2016: SG&A includes a $1.4 million non-cash operating permit impairment charge in Japan.

(9) Other

2017: SG&A includes $24.8 million of consulting and professional services related to the implementation of the new revenue recognition and lease accounting standards as well as internal control remediation activities.

2016: SG&A includes $8.8 million of consulting and professional services related to internal control remediation activities and implementation of the new revenue recognition standard. Other expense, net includes a $2.5 million non-cash impairment charge, offset by a $3.1 million gain from an insurance settlement.

(10) U.S. Tax Reform

2017 includes tax benefit of $129.8 million from the provisional recording of the impact of U.S. tax reform.

(a) The Non-GAAP financial measures contained in this press release are reconciled to the most comparable measures calculated in accordance with U.S. GAAP in the schedules attached to this release. Management believes the Non-GAAP financial measures represent the amounts directly related to the ongoing operations of the business and uses these measures in evaluating performance. All Non-GAAP financial measures are intended to supplement the applicable U.S. GAAP measures and should not be considered in isolation from, or a replacement for, financial measures prepared in accordance with U.S. GAAP and may not be comparable to, or calculated in the same manner as Non-GAAP financial measures published by other companies.