FORM

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

For the fiscal year ended

OR

For the transition period from _________ to __________.

Commission file number

(Exact name of registrant as specified in its charter) |

| ||

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

| ||

(Address of principal executive offices) |

| (Zip Code) |

Registrant's telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol |

| Name of each exchange on which registered |

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an “emerging growth company”. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

|

| Emerging Growth Company |

If an emerging growth company, indicate by checkmark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act): Yes

The aggregate market value of the voting stock held by non-affiliates of the Registrant, based upon the closing sale price of the registrant’s common stock on March 31, 2022, as quoted on the NYSE American, was $

As of December 14, 2022, the Registrant had

Documents Incorporated by Reference: None

FORWARD-LOOKING STATEMENTS

This report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. You can generally identify these forward-looking statements by forward-looking words such as “anticipates,” “believes,” “expects,” “intends,” “future,” “could,” “estimates,” “plans,” “would,” “should,” “potential,” “continues” and similar words or expressions (as well as other words or expressions referencing future events, conditions or circumstances). These forward-looking statements involve risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements, including, but not limited to:

| · | the progress and timing of, and the amount of expenses associated with, our research, development and commercialization activities for our product candidates, including Multikine; |

| · | our expectations regarding the timing, costs and outcome of any pending or future litigation matters, lawsuits or arbitration proceeding; |

| · | the success of our clinical studies for our product candidates; |

| · | our ability to obtain U.S. and foreign regulatory approval for our product candidates and the ability of our product candidates to meet existing or future regulatory standards; |

| · | our expectations regarding federal, state and foreign regulatory requirements; |

| · | the therapeutic benefits and effectiveness of our product candidates; |

| · | the safety profile and related adverse events of our product candidates; |

| · | our ability to manufacture sufficient amounts of Multikine or our other product candidates for use in our clinical studies or, if approved, for commercialization activities following such regulatory approvals; |

| · | our plans with respect to collaborations and licenses related to the development, manufacture or sale of our product candidates; |

| · | business disruption and related risks resulting from the recent pandemic of the novel coronavirus 2019 (COVID-19); |

| · | our expectations as to future financial performance, expense levels and liquidity sources; |

| · | our ability to compete with other companies that are or may be developing or selling products that are competitive with our product candidates; |

| · | anticipated trends and challenges in our potential markets; |

| · | our ability to attract, retain and motivate key personnel; |

| · | our ability to continue as a going concern; and |

| · | our liquidity. |

All forward-looking statements are expressly qualified in their entirety by this cautionary statement. The forward-looking statements contained in this report speak only as of their respective dates. Except to the extent required by applicable laws and regulations, we undertake no obligation to update these forward-looking statements to reflect new information, events or circumstances or to reflect the occurrence of unanticipated events. In light of these risks and uncertainties, the forward-looking events and circumstances described in this report may not occur and actual results could differ materially from those anticipated or implied in such forward-looking statements. Accordingly, you are cautioned not to place undue reliance on these forward-looking statements.

| 2 |

PART I

ITEM 1. BUSINESS

CEL-SCI Corporation (CEL-SCI) is a clinical-stage biotechnology company focused on finding the best way to activate the immune system to fight cancer and infectious diseases. Its lead investigational therapy Multikine® (Leukocyte Interleukin, Injection) completed a pivotal Phase 3 clinical trial for patients who are newly diagnosed with locally advanced (stage III and IV) primary (not yet treated) squamous cell carcinoma of the head and neck (SCCHN). Multikine has received Orphan Drug Status from the U.S. Food and Drug Administration(FDA) for this indication. The study is believed to be the biggest Phase 3 head and neck cancer study ever with 928 patients and lasted almost 10 years. This trial was under the management of two clinical research organizations(CROs): ICON plc.(ICON) and Ergomed Clinical Research Limited (Ergomed).

On June 28, 2021, the Company announced top line results from its pivotal Phase 3 study for Multikine. The Phase 3 results showed a long-term 5-year overall survival (OS) benefit in the treatment arm that received Multikine treatment followed by surgery and radiation (the lower risk to recurrence treatment arm). This survival benefit was robust and durable and added no toxicity to the overall treatment, something not commonly seen with cancer drugs. In fact, the survival benefit increased over time and at 5-years the overall survival benefit reached an absolute 14.1% advantage for the Multikine treated arm over control (n=380, total study patients treated with surgery plus radiation), control arm 48.6%, Multikine arm 62.7% survival.

The study used the standard of care treatment for advanced primary head and neck cancer patients as a comparison. The patients received surgery followed by either radiation or chemoradiation (chemotherapy and radiation at the same time), as determined by the physician. This means that there were 2 treatment arms, 1) surgery plus radiation or 2) surgery plus chemoradiation. The arm that received Multikine treatment followed by surgery and radiation showed great survival benefit, but when chemotherapy was added in the second treatment arm, the immunological effect of Multikine was negated. Therefore, when the two treatment arms were combined the study did not achieve its primary endpoint of a 10% improvement in overall survival.

However, the analysis of the separate treatment arms was prespecified in the protocol and carried out prior to the Company becoming unblinded. The OS benefit of 14.1% at 5 years for this treatment arm exceeded the 10% OS benefit set out for the study population as a whole. The OS results for this treatment arm are significant (two-sided p=0.0236, HR=0.68) and the effect is robust, durable and increasing over time. In addition, the study had a significant number of patients who had partial and even complete tumor responses following the 3-week treatment with Multikine. Most of those were among the patients who did not receive chemotherapy. It was also discovered that patients who have tumor burden reductions (early tumor responders) have significantly improved survival. The results from the Phase 3 cancer study proved that Multikine met all of the protocol required benefits stated in the study protocol in patients in the treatment arm receiving surgery and radiation as their standard therapies. The Company will be filing for and seeking FDA approval for the use of Multikine in the treatment of advanced primary head and neck cancer in this patient population of about 210,000 patients annually worldwide.

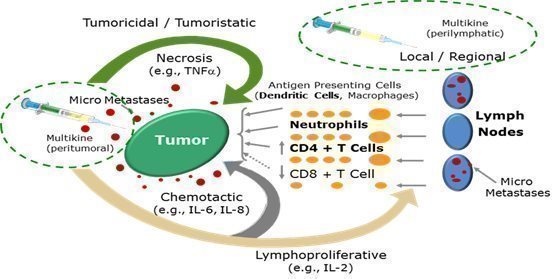

CEL-SCI’s investigational immunotherapy Multikine is being used in a different way than cancer immunotherapy is usually used. It is given before any other therapy has been administered because that is when the immune system is thought to be strongest (as a neoadjuvant). It is also administered locally around the tumors and near the draining lymph node. In the Phase 3 clinical trial, Multikine was given locally for three weeks, five days per week as a first line treatment before surgery, radiation or radiochemotherapy. The goal is to help the intact immune system “see” the cancer and kill the micro metastases that usually cause recurrence of the cancer. In short, CEL-SCI believes that local administration and administration of Multikine before weakening of the immune system by surgery and radiation will result in improved outcomes and better overall survival rates for patients suffering from head and neck cancer.

CEL-SCI is also investigating a peptide-based immunotherapy (CEL-4000) as a vaccine for rheumatoid arthritis using its LEAPS technology platform.

CEL-SCI was formed as a Colorado corporation in 1983. CEL-SCI’s principal office is located at 8229 Boone Boulevard, Suite 802, Vienna, VA 22182. CEL-SCI’s telephone number is 703-506-9460 and its website is www.cel-sci.com. CEL-SCI does not incorporate the information on its website into this report, and you should not consider it part of this report.

CEL-SCI makes its electronic filings with the Securities and Exchange Commission (SEC), including its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports. These filings are available on its website free of charge as soon as practicable after they are filed or furnished to the SEC.

| 3 |

CEL-SCI’S PRODUCTS

CEL-SCI is a clinical-stage biotechnology company dedicated to research and development directed at improving the treatment of cancer and other diseases by using the immune system, the body’s natural defense system. CEL-SCI is currently focused on the development of the following product candidates and technologies:

| 1) | Multikine, an investigational immunotherapy under development for the potential treatment of certain head and neck cancers; |

|

|

|

| 2) | L.E.A.P.S. (Ligand Epitope Antigen Presentation System) technology, or LEAPS, with a product candidate CEL-4000, under development for the potential treatment of rheumatoid arthritis. |

None of CEL-SCI’s product candidates have been approved for sale, barter or exchange by the FDA or any other regulatory agency for any use to treat disease in humans nor has the safety or efficacy of these products been established for any use. There can be no assurance that obtaining marketing approval from the FDA in the United States and by comparable agencies in most foreign countries will be granted.

MULTIKINE

CEL-SCI’s lead investigational therapy, Multikine, is currently being developed as a potential therapeutic agent directed at using the immune system to produce an anti-tumor immune response. Data from Phase 1 and Phase 2 clinical trials suggest that Multikine may help the immune system “see” the tumor and then attack it, enabling the body’s own anti-tumor immune response to fight the tumor. Multikine is the trademark that CEL-SCI has registered for this investigational therapy, and this proprietary name is subject to review by the FDA, in connection with CEL-SCI’s future anticipated regulatory submission for approval in the United States. Multikine has not been licensed or approved for sale, barter or exchange by the FDA or any other regulatory agency, such as the European Medicine Agency(EMA), and neither its safety nor its efficacy been established.

Multikine is an immunotherapy product candidate comprised of a patented defined mixture of 14 human natural cytokines. If commercial approval is obtained, CEL-SCI intends to manufacture Multikine in a proprietary manner in CEL-SCI’s manufacturing facility near Baltimore, Maryland, USA. CEL-SCI spent over 10 years and more than $100 million developing and validating the manufacturing process for Multikine. The pro-inflammatory cytokine mixture includes interleukins, interferons, chemokines and colony-stimulating factors, which contain elements of the body’s natural mix of defenses against cancer.

Multikine is designed to be used in a different way than cancer immunotherapy is generally being used. Generally, cancer immunotherapy is given to patients who have already failed other treatments such as surgery, radiation and/or chemotherapy and most of the time it is administered systemically. Multikine on the other hand is administered locally to treat tumors and their microenvironment before any other therapy has been administered because it is believed that this is the time when the immune system would be strongest and most amenable to activation against the tumor. For example, in the Phase 3 clinical trial, Multikine was injected locally around the tumor and near the adjacent draining lymph nodes for three weeks, five days a week as a first treatment before surgery, radiation and/or chemotherapy. The goal is to help the intact immune system recognize and kill the tumor micro metastases that usually cause recurrence of the cancer. In short, CEL-SCI believes that the local administration of Multikine before weakening of the immune system by surgery, chemotherapy and radiation will result in better anti-tumor response than if Multikine were administered after surgery and radiation. In clinical studies of Multikine, administration of the investigational therapy to head and neck cancer patients has demonstrated the potential for lesser or no appreciable toxicity.

| 4 |

Source: Adapted from Timar et al., Journal of Clinical Oncology 23(15) May 20, 2005

The first indication CEL-SCI is pursuing for its investigational drug product candidate Multikine is an indication for the neoadjuvant therapy in patients with squamous cell carcinoma of the head and neck, or SCCHN (hereafter also referred to as advanced primary head and neck cancer).

On May 27, 2022, CEL-SCI announced the American Society of Clinical Oncology (ASCO) published two abstracts related to its pivotal Phase 3 Multikine head and neck cancer clinical trial. The poster was presented by CEL-SCI’s Chief Scientific Officer, Eyal Talor, Ph.D. at the 2022 ASCO Annual Meeting on June 6, 2022 in Chicago, Illinois. The abstract titles and corresponding links are as follows:

| · | “Leukocyte interleukin injection (LI) immunotherapy extends overall survival (OS) in treatment-naive low-risk (LR) locally advanced primary squamous cell carcinoma of the head and neck: The IT-MATTERS study.” |

| o | Link to abstract: https://meetings.asco.org/abstracts-presentations/207201 |

| o | Link to poster: https://cel-sci.com/wp-content/uploads/2022/06/CEL-SCI-ASCO-2022-Poster-6032-June-6-Head-and-Neck-Cancer-1.pdf |

| · | “Novel algorithm for assigning risk/disease-directed treatment (DDT) choice in locally advanced primary squamous cell carcinoma of the head and neck (SCCHN): Using pretreatment data only.” |

| o | Link to abstract: https://meetings.asco.org/abstracts-presentations/207202/ |

At ASCO 2022, CEL-SCI presented data that showed the following:

| · | 14.1% absolute advantage in overall survival (OS) at 5-years in the lower-risk-for-recurrence treatment arm (62.7% vs 48.6%) of patients with previously untreated locally advanced primary squamous cell carcinoma of the head and neck (Multikine+CIZ) versus the standard of care (SOC) control patients. Patients in the “lower-risk-for-recurrence” treatment arm are those with no adverse features discovered during surgery and who are therefore supposed to receive radiotherapy only after surgery. However, “lower-risk” does not mean low risk, as this treatment arm without CEL-SCI’s investigational Multikine still saw less than 50% survival 5-years post standard of care treatment alone (control group). |

|

|

|

| · | Nearly 4-year increase in median survival in this treatment arm (101.7 months for Multikine+CIZ versus 55.2 months for the SOC alone). |

| 5 |

| · | Objective response before surgery (partial and complete tumor responses): |

| o | In 8.5% (45/529) of Multikine-treated patients in the intent-to-treat (ITT) population (n=923) versus zero in the SOC alone (control). |

| o | In 16.0% (34/212) of Multikine-treated patients in this treatment arm (n=380) versus zero in the SOC alone (control). |

| · | Complete tumor response before surgery in five of the early responders, all five of which were in the Multikine+CIZ treatment arm. |

| · | Objective responses before surgery were prognostic for improved survival and significant for reduced death rate: |

| o | In the overall ITT population, 22.2% death rate (n=45) among objective responders before surgery versus 54.1% death rate for the Multikine non-responders (n=484). |

| o | In the Proposed Indication, 17.6% death rate (n=34) among objective responders before surgery versus 42.7% death rate for the Multikine non-responders (n=178). |

| · | Histopathological analysis confirmed the effect of Multikine, as 61 markers, ratios, and combinations showed a statistically significant effect (two-sided p<0.05) favoring the Multikine+CIZ treatment arm versus the SOC alone (control) for OS, Progression Free Survival (PFS), and Locoregional Control (LRC) outcomes. |

| · | Additional (confirmatory) progression-free survival (PFS) benefit in the Proposed Indication was observed for Multikine+CIZ versus the SOC alone. |

| · | Pre-specified analysis of the Proposed Indication was noted and discussed in the original study protocol and pre-specified in the statistical analysis plan. The Proposed Indication comprised about 40% of all study participants. |

| · | The overall incidence of adverse events and serious adverse events in the Multikine arms was not substantially different versus the SOC alone. |

CEL-SCI also presented a selection process (algorithm) that allows physicians to select before surgery those patients who are intended to receive only radiotherapy after surgery.

On September 12, 2022, CEL-SCI announced two poster presentations were delivered at the European Society for Medical Oncology (EMSO) annual Congress. Data presented were from CEL-SCI’s pivotal Phase 3 study and summarized below:

Poster Presentation: Early response to Neoadjuvant Leukocyte Interleukin Injection (LI) immunotherapy extends overall survival (OS) in locally advanced primary squamous cell carcinoma (SCC) of the head & neck (HN): the IT-MATTERS Study

| · | Early tumor response (early response) to neoadjuvant Multikine-Treatment is noted before surgery (occurring at median 5 weeks post-randomization) adding credibility to the isolated impact of early treatment |

| · | Early response provides a positive signal to both patients and care providers (early in the treatment course) |

| · | Early response was noted only in the Multikine* (Leukocyte Interleukin Injection) treatment groups and not in the control group |

| · | Early response occurs in both the Lower Risk and Higher Risk groups for recurrence (Risk as defined per NCCN Guidelines) |

| · | Early response is prognostic and predictive for overall survival in: |

| · | The overall population; and |

| · | The Lower Risk population |

| · | Benefit was also seen in Multikine-treated Lower Risk non-responders |

| · | Link to poster: https://cel-sci.com/wp-content/uploads/2022/09/CEL-SCI-ESMO-690P-Early-Responders-Poster-FINAL.pdf |

| · | Link to video presentation: https://youtu.be/zMoFtweVGzs |

| 6 |

Poster Presentation: Histopathology (HP) biomarkers confirm Leukocyte Interleukin Injection (LI) treatment (Tx) outcome in naïve locally advanced primary head & neck squamous cell carcinoma (SCCHN) the IT-MATTERS Study

| · | Pre-defined markers, ratios, and combinations derived from Multikine treated tumor samples at surgery contribute to Multikine efficacy for all three efficacy endpoints (OS), progression free survival (PFS), and local regional control (LRC) |

| · | Broad representation of markers, ratios, and combinations overall and for Lower Risk (LR) for the OS, PFS, LRC efficacy study endpoints |

| · | There were 61 (21.9%) favorable overall and 54 (19.4%) favorable Lower Risk treatment group outcomes (much beyond 2.5% chance) and only a total of five instances (1.9%) [all High Risk] having unfavorable treatment group outcome (within the realm of chance) |

| · | These biomarkers were prognostic for superior efficacy of the post-surgery adjuvant radiotherapy as compared to adjuvant chemoradiotherapy |

| · | The results support the Lower Risk treatment advantage (0.68 HR, Wald p<0.05) significantly favoring Multikine+CIZ+ SOC vs SOC alone |

| · | Link to poster: https://cel-sci.com/wp-content/uploads/2022/09/CEL-SCI-ESMO-128P-HP-Poster-FINAL.pdf |

The study used the standard of care treatment for advanced primary head and neck cancer patients as a comparison. The patients received surgery followed by either radiation or chemoradiation (chemotherapy and radiation at the same time), as determined by the physician based on pathology from surgery. This means that there were 2 distinctly different treatment arms, 1) surgery plus radiation or 2) surgery plus chemoradiation. The arm that received Multikine treatment followed by surgery and radiation showed great survival benefit, but when chemotherapy was added in the second treatment arm, the immunological effect of Multikine was negated. Therefore, when the two treatment arms were combined the study did not achieve its primary endpoint of a 10% improvement in overall survival.

However, the analysis of the separate treatment arms was prespecified in the protocol and carried out prior to the Company becoming unblinded. The OS benefit of 14.1% at 5 years for this treatment arm exceeded the 10% OS benefit set out for the study population as a whole. The OS results for this treatment arm are significant (two-sided p=0.0236, HR=0.68) and the effect is robust, durable and increasing over time. The results from the Phase 3 cancer study proved that Multikine met all of the protocol required benefits stated in the study protocol in patients in the treatment arm receiving surgery and radiation as their standard therapies.

CEL-SCI also presented data at the ESMO cancer meeting in September 2022. Particularly important is the early tumor response (ER) seen as a direct result of the 3-week Multikine treatment. LR means lower risk for recurrence which is scheduled to be treated with surgery and radiotherapy, HR means higher risk for recurrence which is scheduled to be treated with surgery followed by radiotherapy and concurrent chemotherapy. MK means Multikine. OS means Overall Survival.

There were 45 objective Early Tumor Responses (5 complete and 40 partial responders) and 462 deaths (50.1%); the 5 complete responders [CRs] were all confirmed by pathology. ERs were only observed in the two Multikine-treated groups (8.5% combined MK; 16% LR combined MK vs 3.7% HR MK; 15.2% LR MK+CIZ+SOC). ERs were more commonly seen in the LR group (16.0%) vs the HR group (3.7%). No responders were seen in the SOC patients. In the MK-treated groups, death rates fell significantly for ERs vs non-responders (54.1% vs 22.2% combined MK; 42.5% vs 17.6% LR combined MK groups; 40.7% vs 12.5% LR (MK+CIZ+SOC); the corresponding hazard ratios (HZR) were 0.301 (Wald p<0.0001) overall, 0.348 (p=0.0067) for LR MK, and 0.246 (p=0.01) for LR MK=CIZ=SO in support of ER being supportive.

| 7 |

Assuming no OS prolongation for the remaining 84.8%, this equates to a 46.5% OS gain corresponding to the observed 0.68 HZR (1/1.465) for the ITT Lower Risk LI (MK)+CIZ+SOC group; this was consistent with the observed 46.5-month median OS advantage for LR LI+CIZ+SOC (101.7 months) vs LR SOC (55.2 months). ER was also predictive; among the 45 responders; there were only 10 deaths (22.2%) in contrast to 452 (51.5%) for the overall ITT population. Thus, ER was predictive from both a modeling and outcome perspective. The conclusions were as follows: Objective ER was only observed for the MK treatments. Multiple ERs were observed across LR (n=34), HR (n=10), and UC (n=1). ER from MK treatment is not only prognostic but also predicts a most favorable OS outcome.

Since CEL-SCI launched its Phase 3 clinical trial for Multikine, CEL-SCI has incurred expenses of approximately $64.1 million as of September 30, 2022 on direct costs for the Phase 3 clinical trial. CEL-SCI estimates it will incur additional expenses of approximately $0.6 million for the remainder of the Phase 3 clinical trial and the filing of the clinical study report to the FDA. It should be noted that this estimate is based only on the information currently available from the CROs responsible for managing the Phase 3 clinical trial and does not include other related costs, e.g., preparations for the potential commercial manufacture of the drug.

Ultimately, the decision as to whether CEL-SCI’s drug product candidate is safe and effective can only be made by the FDA and/or by other regulatory authorities based upon an assessment of all of the data from an entire drug development program submitted as part of an application for marketing approval. As detailed in the Risk Factors section of this report, the current Phase 3 clinical study for CEL-SCI’s investigational drug may or may not be able to be used as the pivotal study supporting a marketing application in the United States, and, if not, at least one entirely new Phase 3 pivotal study would need to be conducted to support a marketing application in the United States. However, CEL-SCI does not believe that this would be ethical or supported by the survival data for this unmet medical need.

Development Agreements for Multikine

In August 2008, CEL-SCI signed an agreement with Teva Pharmaceutical Industries Ltd., or Teva, that gives Teva the exclusive right and license to market, distribute and sell Multikine, if approved, in Israel and Turkey for treatment of head and neck cancer. The agreement terminates on a country-by-country basis 10 years after the product launch in each country or upon a material breach or upon bankruptcy of either party. The agreement will automatically extend for additional two-year terms unless either party gives notice of its intent not to extend the agreement. If CEL-SCI develops Multikine for other oncology indications and Teva indicates a desire to participate, the parties have agreed to negotiate in good faith with respect to Teva’s participation and contribution in future clinical trials.

Teva has agreed to use all reasonable efforts to obtain regulatory approval to market and sell Multikine in its territory at its own cost and expense. Pursuant to the agreement, it is CEL-SCI’s responsibility to supply Multikine and Teva’s responsibility to sell Multikine, if approved by regulatory authorities in the relevant countries. Net sales will be divided 50/50 between the two parties. Teva also initially agreed to fund certain activities relating to the conduct of a clinical trial in Israel as part of the global Phase 3 trial for Multikine. In January 2012, pursuant to an assignment and assumption agreement between CEL-SCI, Teva and GCP Clinical Studies Ltd., or GCP, Teva transferred all of its rights and obligations concerning the Phase 3 trial in Israel to GCP.

In July 2011, Serbia and Croatia were added to Teva’s territory, pursuant to a joinder agreement between CEL-SCI and PLIVA Hrvatska d.o.o., or PLIVA, an affiliate of Teva’s, subject to similar terms as described above.

| 8 |

In consideration for the rights granted by CEL-SCI to PLIVA under the joinder agreement, CEL-SCI will be paid by PLIVA (in U.S. dollars):

| · | $100,000 upon EMA grant of Marketing Authorization for Multikine; |

|

|

|

| · | $50,000 upon Croatia’s grant of reimbursement status for Multikine in Croatia; and |

|

|

|

| · | $50,000 upon Serbia’s grant of reimbursement status for Multikine in Serbia. |

In November 2000, CEL-SCI signed an agreement with Orient Europharma Co., Ltd., or Orient Europharma, of Taiwan, which was amended in October 2008 and again in June 2010. Pursuant to this agreement, as amended, Orient Europharma has the exclusive marketing and distribution rights to Multikine, if approved by regulatory authorities, for head and neck cancer, naso-pharyngeal cancer and potentially cervical cancer indications in Taiwan, Singapore, Malaysia, Hong Kong, the Philippines, South Korea, Australia and New Zealand. CEL-SCI has granted Orient Europharma the first right of negotiation with respect to Thailand and China.

The agreement requires Orient Europharma to fund 10% of the cost of the clinical trials needed to obtain marketing approvals in these countries for head and neck cancer, naso-pharyngeal cancer and potentially cervical cancer.

If Multikine is approved for sale, Orient Europharma will purchase Multikine from CEL-SCI for 35% of the gross selling price in each country.Orient Europharma is obligated to use the same diligent efforts to develop, register, market, sell and distribute Multikine in its territory as with its own products or other licensed products.

The agreement will terminate on a country-by-country basis 15 years after the product approval for Multikine in each country, at which point the agreement will be automatically extended for successive two year periods, unless either party gives notice of its intent not to extend the agreement. The agreement may also be terminated upon the bankruptcy of either party or material misrepresentations that are not cured within 60 days. If the agreement ends before the 15-year term through no fault of either party, CEL-SCI will reimburse Orient Europharma for a prorated part of Orient Europhorma’s costs towards the clinical trials of Multikine. If Orient Europharma fails to make certain minimum purchases of Multikine during the term of the agreement, Orient Europhorma’s rights to the territory will become non-exclusive.

CEL-SCI has a licensing agreement with Byron Biopharma LLC (Byron) under which CEL-SCI granted Byron an exclusive license to market and distribute Multikine in the Republic of South Africa, if approved. This license will terminate 20 years after marketing approval in South Africa or after the bankruptcy or uncured material breach by either party. After the 20-year period has expired, the agreement will be automatically extended for successive two-year periods, unless either party gives notice of its intent not to extend the agreement.

Pursuant to the agreement, Byron will be responsible for registering Multikine in South Africa. If Multikine is approved for sale in South Africa, CEL-SCI will be responsible for manufacturing the product, while Byron will be responsible for sales in South Africa. Sales revenues will be divided equally between CEL-SCI and Byron.

LEAPS

CEL-SCI’s patented T-cell Modulation Process, referred to as LEAPS (Ligand Epitope Antigen Presentation System), uses “heteroconjugates” to direct the body to choose a specific immune response. LEAPS is designed to stimulate the human immune system to more effectively fight bacterial, viral and parasitic infections as well as autoimmune conditions, allergies, transplantation rejection and cancer, when it cannot do so on its own. LEAPS combines T-cell binding ligands with small, disease associated, peptide antigens and may provide a new method to treat and prevent certain diseases.

The ability to generate a specific immune response is important because many diseases are often not combated effectively due to the body’s selection of the “inappropriate” immune response. The capability to specifically reprogram an immune response may offer a more effective approach than existing vaccines and drugs in attacking an underlying disease.

| 9 |

LEAPS Candidates: CEL-2000, CEL-4000 and DerG-PG275(Cit)

On September 19, 2017, CEL-SCI announced that it had been awarded a Phase 2 Small Business Innovation Research (SBIR) grant in the amount of $1.5 million from the National Institute of Arthritis and Musculoskeletal and Skin Diseases(NIAMS), which is part of the U.S. National Institutes of Health (NIH). This grant provided funding to allow CEL-SCI to advance its first LEAPS product candidate, CEL-4000, towards an Investigational New Drug (IND) application for a Phase 1 safety study, by funding IND enabling studies and additional mechanism of action studies, among other preclinical development activities. Work on CEL-4000 was conducted at CEL-SCI’s research laboratory and Rush University Medical Center in Chicago, Illinois in the laboratories of Tibor Glant, MD, Ph.D., Jorge O. Galante Professor of Orthopedic Surgery and Katalin Mikecz, MD, Ph.D. Professor of Orthopedic Surgery & Biochemistry. The SBIR grant was awarded based on published data described below by Dr. Glant's team in collaboration with CEL-SCI showing that the administration of a proprietary peptide using CEL-SCI's LEAPS technology prevented the development, and lessened the severity, including inflammation, of experimental proteoglycan induced arthritis (PGIA or GIA) when it was administered after the disease was induced in animals. This grant has been fully expended.

In May 2019, CEL-SCI announced that a newly discovered LEAPS conjugate acts alone and can complement CEL-4000 therapeutically when administered in combination to an animal model of Rheumatoid Arthritis (RA). This new LEAPS conjugate appears to act on T cell pathways by a new mechanism that is different from the pathways used by the CEL-4000 vaccine. The data was presented at the American Association of Immunologists 103rd Annual Meeting (Immunology 2019) by Daniel Zimmerman, Ph.D., CEL-SCI’s Senior Vice President of Research, Cellular Immunology. The work was performed in conjunction with researchers at Rush University Medical Center, Chicago, Illinois and was funded by the SBIR Phase 2 Grant.

In July 2019, one of CEL-SCI’s collaborators from Rush, Dr. Adrienn Markovics, presented new LEAPS data at i-Chem2019, International Conference on Immunity and Immunochemistry. Data presented was for a new second RA conjugate discovered which acts alone and can complement the existing CEL-4000 RA vaccine in an animal model of RA. The combination of the two RA conjugates provided not only broader epitope coverage, but also a greater therapeutic effect than either conjugate alone. The LEAPS work was performed in conjunction with researchers at CEL-SCI on CEL-4000 and a newly discovered LEAPS conjugate, DerG-PG275Cit. Both conjugates were evaluated alone and in combination in the model of proteoglycan (PG) induced arthritis (PGIA) called recombinant PG G1 domain-induced arthritis (GIA), an autoimmune mouse model of RA.

In February 2017 and November 2016, CEL-SCI announced preclinical data that demonstrate its investigational new drug candidate CEL-4000 has the potential to treat rheumatoid arthritis. This study was supported in part by the SBIR Phase I Grant and was conducted in collaboration with Drs. Katalin Mikecz and Tibor Glant, and their research team at Rush University Medical Center in Chicago, IL. This work was published in an article entitled “An epitope-specific DerG-PG70 LEAPS vaccine modulates T cell responses and suppresses arthritis progression in two related murine models of rheumatoid arthritis” and can be found online at https://www.ncbi.nlm.nih.gov/pmc/articles/PMC5568759/.

Prior to the SBIR Phase 2 grant in 2014, CEL-SCI was awarded a Phase 1 SBIR grant in the amount of $225,000 from NIAMS. This grant funded the development of CEL-SCI’s LEAPS technology as a potential treatment for rheumatoid arthritis, an autoimmune disease of the joints. The work was conducted at Rush University Medical Center in Chicago, Illinois in the laboratories of Tibor Glant, MD, Ph.D., Katalin Mikecz, MD, Ph.D., and Allison Finnegan, Ph.D. Professor of Medicine.

| 10 |

With the support of these SBIR grants, CEL-SCI is developing several new drug candidates, CEL-2000 and CEL-4000, as potential rheumatoid arthritis therapeutic treatments. The data from animal studies using the CEL-2000 treatment suggests that it could be used against rheumatoid arthritis with fewer administrations than those required by other anti-rheumatoid arthritis treatments currently on the market for arthritic conditions associated with the Th17 signature cytokine TNF-a. The preclinical data indicates these peptides could be used against rheumatoid arthritis where a Th1 signature cytokine (IFN-γ) is dominant. CEL-2000 and CEL-4000 each have the potential to become a personalized, disease-specific therapy that acts at an earlier step in the disease process than current therapies, and which may be useful in patients not responding to existing rheumatoid arthritis therapies. CEL-SCI believes this represents a large unmet medical need in the rheumatoid arthritis market.

In March 2015, CEL-SCI and its collaborators published a review article on vaccine therapies for rheumatoid arthritis based in part on work supported by the SBIR Phase 1 grant. The article is entitled “Rheumatoid arthritis vaccine therapies: perspectives and lessons from therapeutic Ligand Epitope Antigen Presentation System vaccines for models of rheumatoid arthritis” and was published in Expert Review of Vaccines 1 - 18 and can be found online at http://www.ncbi.nlm.nih.gov/pubmed/25787143.

Accordingly, even though the various LEAPS candidates have not yet been given to humans, they have been tested in vitro with human cells. They have induced similar cytokine responses that were seen in these animal models, which may indicate that the LEAPS technology might translate to humans. The LEAPS candidates have demonstrated protection against lethal herpes simplex virus (HSV1) and H1N1 influenza infection as a prophylactic or therapeutic agent in animals. They have also shown some level of activity in animals in two autoimmune conditions, curtailing and sometimes preventing disease progression in arthritis and myocarditis animal models.

None of the LEAPS investigational products have been approved for sale, barter or exchange by the FDA or any other regulatory agency for any use to treat disease in animals or humans. The safety or efficacy of these products has not been established for any use. Lastly, no definitive conclusions can be drawn from the early-phase, preclinical-trials data involving these investigational products. Before obtaining marketing approval from the FDA in the United States, and by comparable agencies in most foreign countries, these product candidates must undergo rigorous preclinical and clinical testing which is costly and time consuming and subject to unanticipated delays. There can be no assurance that these approvals will be granted.

INTELLECTUAL PROPERTY

Patents and other proprietary rights are essential to CEL-SCI’s business. CEL-SCI files patent applications to protect its technologies, inventions and improvements that CEL-SCI considers important to the development of its business. CEL-SCI’S intellectual property portfolio covers its proprietary technologies, including Multikine and LEAPS, by multiple issued patents and pending patent applications in the United States and in key foreign markets.

Multikine is protected by a U.S. patent, which is a composition-of-matter patent issued in May 2005 that, in its current format, expires in 2023. Additional composition-of-matter patents for Multikine have been issued in Germany (issued in June 2011 and currently set to expire in 2025), China (issued in May 2011 and currently set to expire in 2024), Japan (issued in November 2012 and currently set to expire in 2025), and three in Europe (issued in September 2015, May 2016 and October 2017, currently set to expire in 2025 and 2026). The most recent patent issued in October 2017, patent # EP 1 879 618 B1, titled “A Method for Modulating HLA Class II Tumor Cell Surface Expression With A Cytokine Mixture,” addresses Multikine’s mechanism of action to make tumors more visible to the immune system. This new patent is important because, along with the other Multikine issued patents, it addresses how Multikine enables the immune system to recognize and attack the tumor. One way tumor cells evade the immune system is by expressing human leukocyte antigens (HLA) on the tumor cell surface, thus appearing as ‘self’ to the immune cells and therefore the tumor cells are not attacked. It is important to note that the tumors of the Multikine-treated best responders in CEL-SCI’s prior Phase 2 studies had no HLA Class II expressed on the cell surface following Multikine treatment as compared to controls. This points to Multikine’s ability to modulate HLA expression on the tumor cell surface, thereby allowing the immune system to recognize and attack the tumor.

| 11 |

In addition to the patents that offer certain protections for Multikine, the method of manufacture for Multikine, a complex biological product, is held by CEL-SCI as a trade secret. CEL-SCI considers this to be its best protection from competitors.

LEAPS is protected by patents in the United States issued between January 2019 and June 2021. The LEAPS patents, which expire between 2027 and 2032, include overlapping claims, with composition of both matter (new chemical entity), process and methods-of-use, to maximize and extend the coverage in their current format. One issued U.S. application is a joint application with Northeast Ohio Medical University (“Neoucom”) and CEL-SCI will share the ability to use the patent, unless CEL-SCI licenses the rights to the patent from Neoucom. In October 2017 and October 2020, patents were issued in Europe for LEAPS, which expire in 2029 and 2034, respectively.

CEL-SCI has five patent applications pending in the United States for LEAPS, which, if issued, would extend protection through 2040, subject to any potential patent term extensions.

As of December 27, 2022, there were no contested proceedings and/or third-party claims with respect to CEL-SCI’s patents or patent applications.

MANUFACTURING FACILITY

Before starting the Phase 3 clinical trial, for reasons related to regulatory considerations, CEL-SCI built a dedicated manufacturing facility to produce its investigational biological product candidate Multikine. This facility produced multiple clinical lots for the Phase 3 clinical trial and has also passed quality systems review by a European Union Qualified Person on several occasions. CEL-SCI expanded the manufacturing facility so CEL-SCI will be able to meet the expected demand for Multikine, if FDA approval is granted. This expansion was completed at the end of 2021, allowing CEL-SCI employees to return to work inside the manufacturing facility. The facility is currently undergoing validation.

CEL-SCI’s lease on the manufacturing facility expires on October 31, 2028. At that time CEL-SCI can either purchase the facility or extend its lease. See Item 2 of this report for more information concerning the terms of this lease.

GOVERNMENT REGULATION

The FDA and other regulatory authorities at federal, state and local levels and in foreign countries extensively regulate, among other things, the research, development, testing, manufacture, quality control, import, export, safety, effectiveness, labeling, packaging, storage, distribution, record keeping, approval, advertising, promotion, marketing and post-approval monitoring and reporting of biologics such as those CEL-SCI is developing. CEL-SCI, along with third party contractors, will be required to navigate the various preclinical, clinical and commercial approval requirements of the governing regulatory agencies of the countries in which it wishes to conduct studies or seek approval or licensure of its product candidates. The process of obtaining regulatory approvals and the subsequent compliance with appropriate federal, state, local, and foreign statutes and regulations requires the expenditure of substantial time and financial resources.

| 12 |

U.S. Food and Drug Administration Regulation of Biological Products

In the United States, the FDA regulates biological products under the Federal Food, Drug, and Cosmetic Act, or FDCA, and the Public Health Service Act, or PHSA, and their implementing regulations. The process required by the FDA before biological product candidates may be marketed in the United States generally involves the following:

| · | completion of preclinical laboratory tests and animal studies performed in accordance with the FDA’s Good Laboratory Practice (GLP) regulations; |

|

|

|

| · | submission to the FDA of an investigational new drug application, or IND, which must become effective before clinical trials may begin and must be updated annually; |

|

|

|

| · | approval by an independent Institutional Review Board, or IRB, or ethics committee at each clinical site before the trial is initiated; |

|

|

|

| · | performance of adequate and well-controlled human clinical trials in compliance with Good Clinical Practice (GCP) regulations to establish the safety, purity and potency of the proposed biologic product candidate for its intended purpose; |

|

|

|

| · | preparation of and submission to the FDA of a Biologics License Application (BLA) after completion of clinical trials; |

|

|

|

| · | satisfactory completion of an FDA Advisory Committee review, if applicable; |

|

|

|

| · | a determination by the FDA within 60 days of its receipt of a BLA to file the application for review; |

|

|

|

| · | satisfactory completion of an FDA pre-approval inspection of the manufacturing facility or facilities at which the proposed product is produced to assess compliance with current Good Manufacturing Practice (cGMP) requirements and to assure that the facilities, methods and controls are adequate to preserve the biological product’s continued safety, purity and potency, and of selected clinical investigations to assess compliance with GCPs; and |

|

|

|

| · | FDA review and approval of the BLA to permit commercial marketing of the product for particular indications for use in the United States. |

Prior to commencing the first clinical trial with a product candidate in the U.S., CEL-SCI must submit an IND to the FDA. An IND is a request for authorization from the FDA to administer an investigational product to humans. The central focus of an IND submission is on the general investigational plan and the protocol(s) for human studies. The IND also includes results of animal and in vitro studies assessing the toxicology, pharmacokinetics, pharmacology, and pharmacodynamic characteristics of the product; chemistry, manufacturing, and controls information; and any available human data or literature to support the use of the investigational product. An IND must become effective before human clinical trials may begin. The IND automatically becomes effective 30 days after receipt by the FDA, unless the FDA, within the 30-day time period, raises safety concerns or questions about the proposed clinical trial. In such a case, the IND may be placed on clinical hold and the IND sponsor and the FDA must resolve any outstanding concerns or questions before the clinical trial can begin. Submission of an IND therefore may or may not result in FDA authorization to commence a clinical trial.

| 13 |

Clinical trials involve the administration of the investigational product to human subjects under the supervision of qualified investigators in accordance with GCPs, which include the requirement that all research subjects provide their informed consent for their participation in any clinical study. Clinical trials are conducted under protocols detailing, among other things, the objectives of the study, the parameters to be used in monitoring safety and the effectiveness criteria to be evaluated. A separate submission to the existing IND must be made for each successive clinical trial conducted during product development and for any subsequent protocol amendments. Furthermore, an independent IRB for each site proposing to conduct the clinical trial must review and approve the plan for any clinical trial and its informed consent form before the clinical trial commences at that site, and must monitor the study until completed. Regulatory authorities, the IRB or the sponsor may suspend a clinical trial at any time on various grounds, including a finding that the subjects are being exposed to an unacceptable health risk. Some studies also include oversight by an independent group of qualified experts organized by the clinical study sponsor, known as a data safety monitoring board (DSMB) or independent data monitoring committee (IDMC), which provides recommendations for whether or not a study should move forward at designated check points based on access to certain data from the study and may suggest halting the clinical trial if it determines that there is an unacceptable safety risk for subjects or other grounds, such as no demonstration of efficacy. There are also requirements governing the reporting of ongoing clinical studies and clinical study results to public registries.

For purposes of approval of a Biologics License Application, or BLA, human clinical trials are typically conducted in three or four sequential phases that may overlap.

● Phase 1 — The investigational product is initially introduced into healthy human subjects or patients with the target disease or condition. These studies are designed to test the safety, dosage tolerance, absorption, metabolism and distribution of the investigational product in humans and the side effects associated with increasing doses.

● Phase 2 — The investigational product is administered to a limited patient population with a specified disease or condition to evaluate the preliminary efficacy, optimal dosages and dosing schedule and to identify possible adverse side effects and safety risks. Multiple Phase 2 clinical trials may be conducted to obtain information prior to beginning larger and more expensive Phase 3 clinical trials.

● Phase 3 — The investigational product is administered to an expanded patient population to further evaluate dosage, to provide statistically significant evidence of clinical efficacy and to further test for safety, generally at multiple geographically dispersed clinical trial sites. These clinical trials are intended to establish the overall risk/benefit ratio of the investigational product and to provide an adequate basis for product approval.

● Phase 4 — In some cases, the FDA may require, or companies may voluntarily pursue, additional clinical trials after a product is approved to gain more information about the product. The FDA may also make these so-called Phase 4 or post-marketing studies a condition to approval of the BLA.

Phase 1, Phase 2 and Phase 3 testing may not be completed successfully within a specified period, if at all, and there can be no assurance that the data collected will support FDA approval or licensure of the product. Concurrent with clinical trials, companies may complete additional animal studies and develop additional information about the biological characteristics of the product candidate, and must finalize a process for manufacturing the product in commercial quantities in accordance with cGMP requirements. The manufacturing process must be capable of consistently producing quality batches of the product candidate and, among other things, must develop methods for testing the identity, strength, quality and purity of the final product. Additionally, appropriate packaging must be selected and tested and stability studies must be conducted to demonstrate that the product candidate does not undergo unacceptable deterioration over its shelf life.

| 14 |

BLA Submission and Review by the FDA

Assuming successful completion of all required testing in accordance with all applicable regulatory requirements, the results of product development, nonclinical studies and clinical trials are submitted to the FDA as part of a BLA requesting approval to market the product for one or more indications. The BLA must include all relevant data available from pertinent preclinical and clinical studies, including negative or ambiguous results as well as positive findings, together with detailed information relating to the product’s chemistry, manufacturing, controls, and proposed labeling, among other things. Data can come from company-sponsored clinical studies intended to test the safety and effectiveness of a use of the product, or from a number of alternative sources, including studies initiated by investigators.

In most cases, the submission of a BLA is subject to a substantial application user fee. Under the goals and policies agreed to by the FDA under the Prescription Drug User Fee Act, or PDUFA, for original BLAs, the FDA’s goal is to review the BLA within ten months after it accepts the application for filing, or, if the product relates to an unmet medical need in a serious or life-threatening indication and has received a priority review designation, six months after the FDA accepts the application for filing.

After filing the marketing application, the FDA reviews a BLA to determine, among other things, whether a product is safe, pure and potent and the facility in which it is manufactured, processed, packed, or held meets standards designed to assure the product’s continued safety, purity and potency. Before approving a BLA, the FDA will typically inspect the facility or facilities where the product is manufactured. The FDA will not approve a biological product for marketing unless it determines that the manufacturing processes and facilities are in compliance with cGMP requirements and adequate to assure consistent production of the product within required specifications. Additionally, before approving a BLA, the FDA will typically inspect one or more clinical sites to assure compliance with GCPs. If the FDA determines that the data provided in the application, or the manufacturing process or manufacturing facilities for the product are not acceptable, it will outline the deficiencies in the submission and often will request additional testing or information. Notwithstanding the submission of any requested additional information, the FDA ultimately may decide that the application does not satisfy the regulatory criteria for approval. The FDA also may refer applications for novel biologic candidates which present difficult questions of safety or efficacy to an advisory committee, typically a panel that includes clinicians and other experts, for review, evaluation and a recommendation as to whether the application should be approved and under what conditions, if any. The FDA is not bound by recommendations of an advisory committee, but it considers such recommendations when making decisions on approval.

After the FDA evaluates a BLA and conducts inspections of manufacturing facilities where the biological product and/or its drug substance will be produced, the FDA may issue an approval letter or a Complete Response Letter. An approval letter authorizes commercial marketing of the product with specific prescribing information for specific indications. A Complete Response Letter indicates that the review cycle of the application is complete but the application is not ready for approval. A Complete Response Letter may request additional information or clarification, including new clinical studies. The FDA may delay or refuse approval of a BLA if applicable regulatory criteria are not satisfied, require additional testing or information and/or require post-marketing testing and surveillance to monitor safety or efficacy of a product. If a Complete Response Letter is issued, the applicant may either resubmit the BLA, addressing all of the deficiencies identified in the letter, or withdraw the application. Even if such data and information are submitted, the FDA may decide that the re-submitted BLA does not satisfy the criteria for approval.

| 15 |

If a product receives regulatory approval, such approval is limited to the conditions of use (e.g., patient population, indication) described in the application. Further, depending on the specific risk(s) to be addressed, the FDA may require that contraindications, warnings or precautions be included in the product labeling, require that post-approval trials, including Phase 4 clinical trials, be conducted to further assess a product’s safety after approval, require testing and surveillance programs to monitor the product after commercialization, or impose other conditions, including distribution and use restrictions or other risk management mechanisms under a Risk Evaluation and Mitigation Strategy, or REMS, plan if it determines that a REMS is necessary to ensure that the benefits of the product outweigh its risks and to assure the safe use of the biological product, which can materially affect the potential market and profitability of the product. The REMS plan could include medication guides, physician communication plans, or elements to assure safe use, such as restricted distribution methods, patient registries and other risk minimization tools. The FDA also may condition approval on, among other things, changes to proposed labeling or the development of adequate controls and specifications. Once approved, the FDA may withdraw the product approval if compliance with pre- and post-marketing regulatory standards is not maintained or if problems occur after the product reaches the marketplace. The FDA may prevent or limit further marketing of a product based on the results of post-marketing trials or surveillance programs. After approval, some types of changes to the approved product, such as adding new indications, manufacturing changes and additional labeling claims, are subject to further testing requirements and FDA review and approval.

Expedited Review and Approval

A sponsor may seek approval of its product candidate under programs designed to accelerate the FDA’s review and approval of new drugs and biological products that meet certain criteria. Specifically, new drugs and biological products are eligible for fast track designation if they are intended to treat a serious or life-threatening condition and demonstrate the potential to address unmet medical needs for the condition. For a fast track product, the FDA may consider sections of the BLA for review on a rolling basis before the complete application is submitted if relevant criteria are met. A fast track designated product candidate may also qualify for priority review.

Under the accelerated approval program, the FDA may approve a BLA on the basis of either a surrogate endpoint that is reasonably likely to predict a clinical benefit, or on a clinical endpoint that can be measured earlier than irreversible morbidity or mortality, that is reasonably likely to predict an effect on irreversible morbidity or mortality or other clinical benefit, taking into account the severity, rarity, or prevalence of the condition and the availability or lack of alternative treatments. Post-marketing studies or completion of ongoing studies after marketing approval are generally required to verify the biologic’s clinical benefit in relationship to the surrogate endpoint or ultimate outcome in relationship to the clinical benefit. In addition, the Food and Drug Administration Safety and Innovation Act, or FDASIA, which was enacted and signed into law in 2012, established the new Breakthrough Therapy designation. A sponsor may seek FDA designation of its product candidate as a breakthrough therapy if the product candidate is intended, alone or in combination with one or more other drugs or biologics, to treat a serious or life-threatening disease or condition and preliminary clinical evidence indicates that the therapy may demonstrate substantial improvement over existing therapies on one or more clinically significant endpoints, such as substantial treatment effects observed early in clinical development. Sponsors may request the FDA to designate a breakthrough therapy at the time of or any time after the submission of an IND, but ideally before an end-of-phase 2 meeting with the FDA. If the FDA designates a breakthrough therapy, it may take actions appropriate to expedite the development and review of the application, which may include holding meetings with the sponsor and the review team throughout the development of the therapy; providing timely advice to, and interactive communication with, the sponsor regarding the development of the drug to ensure that the development program to gather the nonclinical and clinical data necessary for approval is as efficient as practicable; involving senior managers and experienced review staff, as appropriate, in a collaborative, cross-disciplinary review; assigning a cross-disciplinary project lead for the FDA review team to facilitate an efficient review of the development program and to serve as a scientific liaison between the review team and the sponsor; and considering alternative clinical trial designs when scientifically appropriate, which may result in smaller trials or more efficient trials that require less time to complete and may minimize the number of patients exposed to a potentially less efficacious treatment.

Fast Track designation, priority review and breakthrough therapy designation do not change the standards for approval but may expedite the development or approval process.

| 16 |

Post-Approval Requirements

All therapeutic products manufactured or distributed pursuant to FDA approval or licensure are subject to pervasive and continuing regulation by the FDA, including, among other things, requirements relating to record-keeping, reporting of adverse experiences, periodic reporting, product sampling and distribution, and advertising and promotion of the product. After approval, most changes to the approved product, such as adding new indications or other labeling claims, are subject to prior FDA review and approval. There also are continuing, annual user fee requirements under the PDUFA for any marketed products and the establishments at which such products are manufactured, as well as new application fees for supplemental applications containing clinical data. Biologic manufacturers and their subcontractors are required to register their establishments with the FDA and certain state agencies, and are subject to periodic unannounced inspections by the FDA and certain state agencies for compliance with cGMP requirements, which impose significant procedural and documentation requirements. Changes to the manufacturing process are strictly regulated and, depending on the significance of the change, may require prior FDA approval before being implemented. FDA regulations also require investigation and correction of any deviations from cGMP and impose reporting requirements on manufacturers. Accordingly, manufacturers must continue to expend time, money and effort in the area of production and quality control to maintain compliance with cGMP and other aspects of regulatory compliance. CEL-SCI cannot be certain that it, or CEL-SCI’s present or future suppliers, will be able to comply with the cGMP regulations and other FDA regulatory requirements. If CEL-SCI is not able to comply with these requirements, the FDA may, among other things, take enforcement action or seek sanctions against use, impose restrictions on a product or its manufacturer, require CEL-SCI to recall a product from distribution, or withdraw approval of the BLA.

The FDA may withdraw approval if compliance with regulatory requirements and standards is not maintained or if problems occur after the product reaches the market. Later discovery of previously unknown problems with a product, including adverse events of unanticipated severity or frequency, or with manufacturing processes, or failure to comply with regulatory requirements, may result in revisions to the approved labeling to add new safety information; imposition of post-market studies or clinical studies to assess new safety risks; or imposition of distribution restrictions or other restrictions under a REMS program. Other potential consequences include, among other things:

| · | restrictions on the marketing or manufacturing of the product, complete withdrawal of the product from the market or product recalls; |

|

|

|

| · | fines, warning letters or holds on post-approval clinical studies; |

|

|

|

| · | refusal of the FDA to approve pending applications or supplements to approved applications, or suspension or revocation of product license approvals; |

|

|

|

| · | product seizure or detention, or refusal to permit the import or export of products; |

|

|

|

| · | injunctions or the imposition of civil or criminal penalties; and |

|

|

|

| · | consent decrees, corporate integrity agreements, debarment, or exclusion from federal healthcare programs; or mandated modification of promotional materials and labeling and the issuance of corrective information. |

| 17 |

The FDA closely regulates the marketing, labeling, advertising and promotion of drugs and biologics. A company can make only those claims relating to safety and efficacy, purity and potency that are approved by the FDA and in accordance with the provisions of the approved label. The FDA and other agencies actively enforce the laws and regulations prohibiting the promotion of unapproved, or “off-label,” uses. Failure to comply with these requirements can result in, among other things, adverse publicity, warning letters, corrective advertising and potential civil and criminal penalties. Physicians may prescribe legally available products for uses that are not described in the product’s labeling and that differ from those tested and approved by the FDA. Such off-label uses are common across medical specialties. Physicians may believe that such off-label uses are the best treatment for many patients in varied circumstances. The FDA does not regulate the behavior of physicians in their choice of treatments. The FDA does, however, restrict manufacturer’s communications on the subject of off-label use of their products.

Orphan Drug Designation

Under the Orphan Drug Act, the FDA may grant orphan drug designation to drugs or biologics intended to treat a rare disease or condition that affects fewer than 200,000 individuals in the United States, or if it affects more than 200,000 individuals in the United States and there is no reasonable expectation that the cost of developing and making the drug for this type of disease or condition will be recovered from sales in the United States.

In the United States, orphan drug designation entitles a party to financial incentives such as opportunities for grant funding towards clinical trial costs, tax advantages and user-fee waivers. In addition, if a product receives the first FDA approval for the indication for which it has orphan designation, the product is entitled to orphan drug exclusivity, which means the FDA may not approve any other application to market a drug for the same indication for a period of 7 years, except in limited circumstances, such as a showing of clinical superiority over the product with orphan exclusivity. Orphan drug exclusivity also could block the approval of one of CEL-SCI’s products for seven years if a competitor obtains approval of a product before CEL-SCI does, as defined by the FDA, for the same indication CEL-SCI is seeking, or if CEL-SCI’s product candidate is determined to be contained within the scope of the competitor’s product for the same indication or disease. If one of CEL-SCI’s products designated as an orphan drug receives marketing approval for an indication broader than that which is designated, it may not be entitled to orphan drug exclusivity. Orphan drug status in the European Union has similar, but not identical, requirements and benefits.

Orphan drug designation must be requested before submitting a BLA to the FDA for review and approval. After the FDA grants orphan drug designation, the identity of the therapeutic agent and its potential orphan use are disclosed publicly by the FDA. Orphan drug designation does not convey any advantage in, or shorten the duration of, the regulatory review and approval process.

Multikine has received Orphan Drug Status from the FDA.

Other U.S. Health Care Laws

CEL-SCI’s sales, promotion, medical education and other activities following product approval will be subject to regulation by numerous regulatory and law enforcement authorities in the United States in addition to the FDA, including potentially the Federal Trade Commission, the Department of Justice, the Centers for Medicare and Medicaid Services, other divisions of the Department of Health and Human Services and state and local governments. CEL-SCI’s promotional and scientific/educational programs must comply with the anti-kickback provisions of the Social Security Act, the Foreign Corrupt Practices Act, the False Claims Act, the Physician Payments Sunshine Act, the Veterans Health Care Act and similar state laws.

| 18 |

Depending on the circumstances, failure to meet these applicable regulatory requirements can result in criminal prosecution, fines or other penalties, exclusion from government health care programs, injunctions, recall or seizure of products, total or partial suspension of production, denial or withdrawal of pre-marketing product approvals, private “qui tam” actions brought by individual whistleblowers under the False Claims Act in the name of the government or refusal to allow CEL-SCI to enter into supply contracts, including government contracts.

Coverage, Pricing and Reimbursement in the U.S.

Sales of pharmaceutical products depend significantly on the availability of third-party coverage and reimbursement. Third-party payors include government health administrative authorities, managed care providers, private health insurers and other organizations. These third-party payors are increasingly challenging the price and examining the cost-effectiveness of medical products and services. In addition, significant uncertainty exists as to the reimbursement status of newly approved healthcare products and new drug classes, including biological products such as CEL-SCI’s product candidates. CEL-SCI may need to conduct expensive clinical studies to demonstrate the comparative cost-effectiveness of its products. The product candidates that CEL-SCI develops may not be considered cost-effective. It is time consuming and expensive for CEL-SCI to seek reimbursement from third- party payors. Reimbursement may not be available or sufficient to allow CEL-SCI to sell its products on a competitive and profitable basis.

The United States and some foreign jurisdictions are considering or have enacted a number of legislative and regulatory proposals to change the healthcare system in ways that could affect CEL-SCI’s ability to sell its products profitably. Among policy makers and payors in the United States and elsewhere, there is significant interest in promoting changes in healthcare systems with the stated goals of containing healthcare costs, improving quality and/or expanding access. In the United States, the pharmaceutical industry has been a particular focus of these efforts and has been significantly affected by major legislative initiatives.

Foreign Regulation

In addition to regulations in the United States, CEL-SCI will be subject to a variety of foreign regulations governing clinical trials and commercial sales and distribution of its products to the extent CEL-SCI chooses to develop or sell any products outside of the United States. The approval process varies from country to country and the time may be longer or shorter than that required to obtain FDA approval. The requirements governing the conduct of clinical trials, product licensing, pricing and reimbursement vary greatly from country to country.

ITEM 1B. RISK FACTORS

The risks described below could adversely affect the price of CEL-SCI’s common stock.

Risk Factor Summary

CEL-SCI has incurred significant losses since its inception and anticipates that it will continue to incur significant losses for the foreseeable future and may never achieve or maintain profitability.

CEL-SCI will require substantial additional capital to remain in operation. A failure to obtain this necessary capital when needed could force CEL-SCI to delay, limit, reduce or terminate the product candidates’ development or commercialization efforts.

The costs of the product candidates’ development and clinical trials are difficult to estimate and will be very high for many years, preventing CEL-SCI from making a profit for the foreseeable future, if ever.

| 19 |

CEL-SCI has not established a definite plan for the marketing of Multikine, if approved.

CEL-SCI depends heavily on the success of Multikine, for which top line Phase 3 data has been announced, while its other candidates are still in preclinical phases. CEL-SCI’s product candidates must undergo rigorous preclinical and clinical testing and regulatory approvals, which could be costly and time-consuming and subject CEL-SCI to unanticipated delays or prevent CEL-SCI from marketing any products. If CEL-SCI is unable to advance its product candidates in clinical development, obtain regulatory approval and ultimately commercialize its product candidates, or experiences significant delays in doing so, CEL-SCI’s business will be materially harmed.

Even if CEL-SCI obtains regulatory approval for its investigational products, CEL-SCI will be subject to stringent, ongoing government regulation.

CEL-SCI’s product candidates may cause undesirable side effects or have other properties that could delay or prevent their regulatory approval, limit the commercial utility of an approved prescribing label, or result in significant negative consequences following marketing approval, if any.

Biologics carry unique risks and uncertainties, which could have a negative impact on future results of CEL-SCI’s operations.

The current and future relationships with healthcare professionals, principal investigators, consultants, potential customers and third-party payors in the United States and elsewhere may be subject, directly or indirectly, to applicable healthcare laws and regulations.

CEL-SCI’s commercial success depends, in part, upon attaining significant market acceptance of its product candidates, if approved, among physicians, patients, healthcare payors and major operators of cancer clinics.

CEL-SCI’s patents might not protect its technology from competitors, in which case CEL-SCI may not have any advantage over competitors in selling any products that CEL-SCI may develop.

Much of CEL-SCI’s intellectual property is protected as trade secrets or confidential know-how, not by patents.

You may experience future dilution as a result of future equity offerings or other equity issuances by CEL-SCI.

The price of CEL-SCI’s common stock has been volatile and is likely to continue to be volatile, which could result in substantial losses for CEL-SCI’s shareholders.

CEL-SCI faces business disruption and related risks resulting from the recent pandemic of COVID-19 which could have a material adverse effect on CEL-SCI's business plan.

| 20 |

Risks Related to CEL-SCI

CEL-SCI faces business disruption and related risks resulting from the recent pandemic of COVID-19 which could have a material adverse effect on our business plan.