UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2021

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from______ to______

Commission File Number: 333-254800

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

__________________________

(Address of principal executive offices)

(646 ) 661-7600

(Registrant’s telephone number, including area code)

None

(Former name, former address and former fiscal year, if changed since last report)

__________________________

Securities registered pursuant to Section 12(b) of the Act: None

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||||||||

| ☒ | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Aggregate market value of the registrant’s common stock held by non-affiliates of the registrant, based upon the closing price of a share of the registrant’s Class A common stock on June 30, 2021 as reported on the Canadian Stock Exchange on that date: $1,431,234,747

As of March 7, 2022, there were 173,302,518 shares of the registrant’s Class A common stock, par value $0.001, and 65,000 shares of the registrant’s Class B common stock, par value $0.001, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

ASCEND WELLNESS HOLDINGS, INC

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K for Ascend Wellness Holdings, Inc. and its subsidiaries (collectively referred to as “AWH,” “Ascend,” “we,” “us,” “our,” or the “Company”) contains both historical and forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. We make forward-looking statements related to future expectations, estimates, and projections that are uncertain and often contain words such as, but not limited to, “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “intend,” “likely,” “may,” “outlook,” “plan,” “predict,” “should,” “target,” or other similar words or phrases. These statements are not guarantees of future performance and are subject to known and unknown risks, uncertainties, and assumptions that are difficult to predict. Factors that might cause such differences include, but are not limited to, those discussed in Part I of this Form 10-K under Item 1A., “Risk Factors,” and we urge readers to consider these risks and uncertainties in evaluating our forward-looking statements. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated, or intended. The forward-looking statements contained herein are based on certain key expectations and assumptions, including, but not limited to, with respect to expectations and assumptions concerning receipt and/or maintenance of required licenses and success of our operations, are based on estimates prepared by us using data from publicly available governmental sources as well as from industry analysis, and on assumptions based on data and knowledge of this industry that we believe to be reasonable. We caution readers not to place undue reliance upon any such forward-looking statements, which speak only as of the date made. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events, or otherwise, except as required by law.

1

PART I

ITEM 1. BUSINESS

Background

Ascend Wellness Holdings, Inc. (“AWH,” “Ascend,” “we,” “us,” “our,” or the “Company”) is a vertically integrated multi-state cannabis operator focused on operating in adult-use or near-term adult-use states in primarily limited license markets. Ascend’s core business is the cultivation, manufacturing and distribution of cannabis consumer packaged goods, which are sold through company-owned retail stores and to third-party licensed retail cannabis stores. The Company is a reporting issuer in the United States. The Company’s shares of Class A common stock are listed in Canada on the Canadian Securities Exchange (“CSE”) under the symbol “AAWH.U.” and in the United States on the OTCQX Best Market (the “OTCQX”) under the symbol “AAWH.” Ascend is an emerging growth company under federal securities laws and as such Ascend is able to elect to follow scaled disclosure requirements for this filing.

The Company was founded in 2018 with initial operations in Illinois and has since expanded its operational footprint, primarily through acquisitions, and now has operations or financial interests in five U.S. geographic markets: Illinois, Massachusetts, Michigan, New Jersey, and Ohio. As of December 31, 2021, Ascend has 20 open dispensaries, 18 of which are in states which have passed legislation permitting recreational cannabis. Ascend also operates cultivation facilities in five states with 176,000 square feet of canopy. The Company has a pipeline with fully-financed expansion plans to achieve 24 open dispensaries and 255,000 square feet of canopy generating 127,500 pounds of cannabis annually post build-out, which it hopes to complete by the end of 2022.

Ascend believes in bettering lives through cannabis. The mission is to improve the lives of its employees, patients, customers and the communities they serve through the use of the cannabis plant. As of March 1, 2022, AWH employed approximately 1,500 people across the cultivation, processing, retail, and corporate functions.

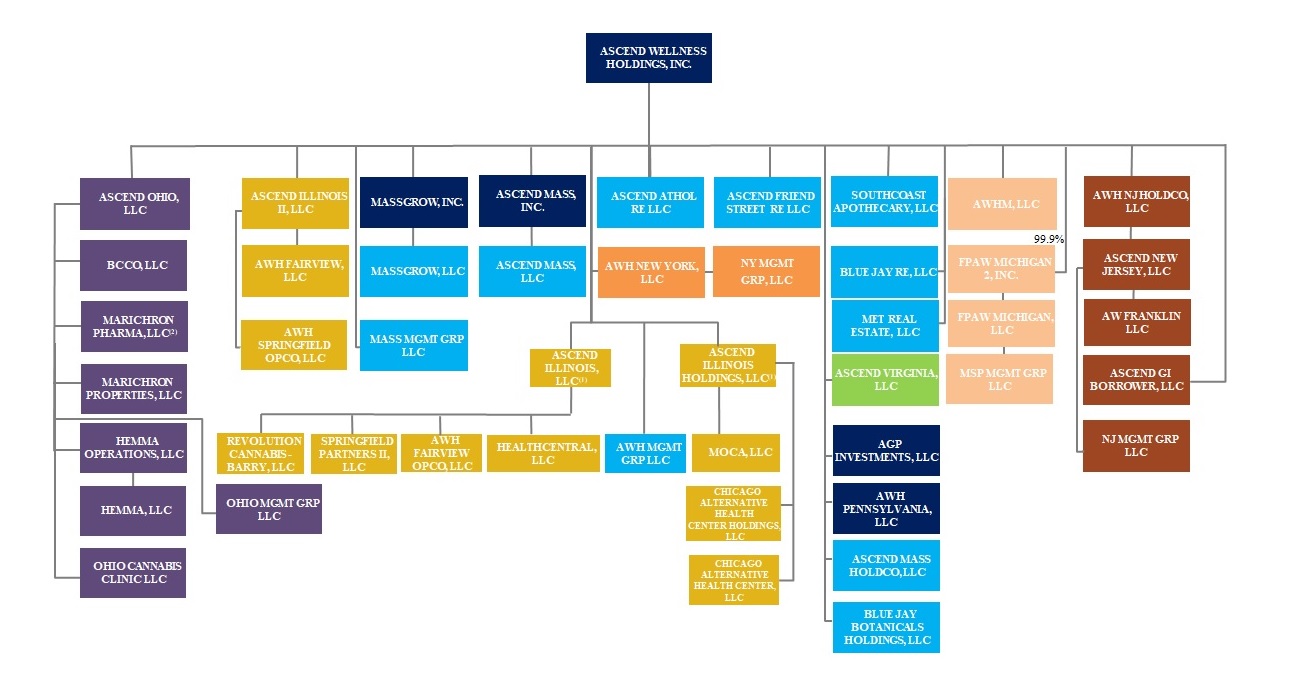

The following organizational chart describes our current organizational structure. See Exhibit 21.1 to this filing for a list of AWH’s subsidiaries. All lines represent 100% ownership of outstanding securities of the applicable subsidiary unless otherwise noted. In part, the complexity of the organization structure is due to state licensing requirements that mandate that the Company maintain the corporate identity of the operating license holders.

2

__________________

(1)In process of transfer to AWH. The Illinois Department of Financial and Professional Regulation is currently reviewing the transfer application.

(2)We have entered into an agreement to acquire Marichron Pharma, LLC, but cannot submit a transfer request until Marichron Pharma, LLC receives a certificate of operation.

Legend for state of incorporation:

AWH’s registered office is located at 1209 Orange Street, Wilmington, DE 19801. The Company’s headquarters are located at 1411 Broadway, 16th Floor, New York, NY 10018.

History of the Company

Founding and Incorporation

The Company was originally formed on May 15, 2018 as Ascend Group Partners, LLC, and changed its name to “Ascend Wellness Holdings, LLC” on September 10, 2018. On April 22, 2021, Ascend Wellness Holdings, LLC converted into a Delaware corporation and changed its name to “Ascend Wellness Holdings, Inc.” and effected a 2-for-1 reverse stock split, which is retrospectively presented for all periods in this filing and referred to as the “Conversion.” As a result of the Conversion, the members of Ascend Wellness Holdings, LLC became holders of shares of stock of Ascend Wellness Holdings, Inc.

Following the Conversion, the Company has authorized 750,000,000 shares of Class A common stock with a par value of $0.001 per share, 100,000 shares of Class B common stock with a par value of $0.001 per share, and 10,000,000 shares of preferred stock with a par value of $0.001 per share. The rights of the holders of Class A common stock and Class B common stock are identical, except for voting and conversion rights. Each share of Class A common stock is entitled to one vote per share. Each share of Class B common stock is entitled to 1,000 votes per share and is convertible at any time into one share of Class A common stock at the option of the holder.

Initial Public Offering

On May 4, 2021, the Company completed an Initial Public Offering (“IPO”) of its Class A common stock, in which it issued and sold 10.0 million shares of Class A common stock at a price of $8.00 per share. On May 7, 2021, the underwriters exercised their over-allotment option in full and we issued and sold an additional 1.5 million shares of Class A common stock. AWH received total net proceeds of approximately $86.1 million after deducting underwriting discounts and commissions and certain other direct offering expenses paid by the Company. In connection with the IPO, the historical common units, Series Seed Preferred Units, Series Seed+ Preferred Units, and Real Estate Preferred Units then-outstanding automatically converted into a total of 113.3 million shares of Class A common stock and 65 thousand historical common units were allocated as shares of Class B common stock. Additionally, 3.4 million shares of Class A common stock were issued for a beneficial conversion feature associated with the conversion of certain historical preferred units and the Company’s convertible notes, plus accrued interest, converted into 37.4 million shares of Class A common stock. The Company’s shares of Class A common stock are listed on the CSE under the ticker symbol “AAWH.U” and are quoted on the OTCQX Best Market under the symbol “AAWH.”

3

Outstanding Securities

As of December 31, 2021, the Company had approximately 181.0 million fully diluted shares outstanding, including approximately 171.5 million shares of Class A common stock, approximately 0.1 million shares of Class B common stock, approximately 8.0 million total unvested restricted stock awards and restricted stock units, and approximately 1.4 million warrants outstanding, which are in the money and calculated using the treasury stock method based on the closing stock price of the shares of Class A common stock on the CSE on December 31, 2021 of $6.61 per share.

Financing History

Historically, Ascend has used private financing as a source of liquidity for its short-term working capital needs and general corporate purposes. During the first quarter of 2021, Ascend raised $49.5 million through the issuance of convertible notes to further finance its expanded operations and acquisitions. Subsequent to the IPO, the Company entered into a new credit facility in August 2021, which provides for a $210.0 million term loan that bears interest at a rate of 9.5% per annum, due quarterly. Proceeds from the term loan were used, in part, to prepay approximately $75.6 million of existing debt and the remainder will be used to finance future growth initiatives and acquisitions.

To date, the Company has funded many of its expansion projects via sale leaseback transactions. The significant sale leaseback financings are further described below:

•In August 2018, AWH acquired the real property where its Athol, Massachusetts cultivation facility is located. In April 2020, AWH executed a sale leaseback agreement with Innovative Industrial Properties, Inc. (“IIP”) with a sale price of $26.8 million and a tenant improvement allowance (“TIA”) of $22.2 million to fund the expansion of the cultivation facility.

•In December 2018, AWH acquired the real property where its Barry, Illinois cultivation facility is located and simultaneously executed a sale leaseback agreement with IIP with a sale price of $19.0 million and an in initial TIA of $6.0 million. The TIA has subsequently increased to $52.0 million as we have expanded the cultivation facility, including the addition of a greenhouse.

•In June 2019, AWH acquired the real property where its Lansing, Michigan cultivation facility is located. In July 2019, AWH executed a sale leaseback agreement with IIP with a sale price of $4.8 million and a TIA of $15.0 million to fund the expansion of the facility.

•In January 2022, AWH acquired the real property where the Franklin, New Jersey cultivation facility is located. In February 2022, AWH executed a sale leaseback agreement with IIP with a sale price of $35.4 million and a TIA of $4.6 million to fund the expansion of the facility.

4

Acquisitions

The Company has grown rapidly by strategically acquiring licenses and operations. Ascend’s core acquisition philosophy has been to acquire assets in: marquee locations, limited-license states, and recreational or near-recreational markets. Growth via acquisition has allowed Ascend to strategically select and to operate primarily in highly competitive market dynamics. The Company’s key transactions are detailed in the table below.

| Seller | Assets | Locations | Date | Additional Information | ||||||||||||||||||||||

| Revolution Cannabis-Barry, LLC | Cultivation | -Barry, IL | December 2018 | This was the Company’s first operational cultivation facility. The Company has since expanded the site by adding a greenhouse, lab, and kitchen. | ||||||||||||||||||||||

| HealthCentral, LLC | 2 Dispensaries | -Springfield, IL -Collinsville, IL | January 2019 | These locations were initially medical dispensaries and have since become two of Ascend’s highest performing recreational stores, following the legalization of adult-use in January 2019. | ||||||||||||||||||||||

| MOCA, LLC | 2 Dispensaries | -Chicago, IL (Logan Square and River North) | Signed in August 2020 and close in December 2020 | This acquisition was the Company’s first entry into the Chicago market and was included in our consolidated results as a Variable Interest Entity (“VIE”) from August 2020 through closing in December 2020. | ||||||||||||||||||||||

| Southcoast Apothecary, LLC | 1 Dispensary | -New Bedford, MA | Initial transaction closed in February 2020 and property purchase closed in August 2020 | The New Bedford location is our first expansion into Southern Massachusetts and the recreational dispensary is expected to open in the first half of 2022. | ||||||||||||||||||||||

| Greenleaf Compassion Center LLC | 3 Dispensaries and 1 Cultivation | Medical dispensaries located in: -Montclair, NJ -Rochelle Park, NJ -Fort Lee, NJ Cultivation located in: -Franklin, NJ | September 2020 | At the time of closing only the Montclair location was operational. We subsequently opened the Rochelle Park dispensary in May 2021 and expect to open the Fort Lee dispensary in 2022. Currently, both open dispensaries have been serving medical patients. The state has passed legislation to legalize sale of adult-use cannabis and is implementing the program. | ||||||||||||||||||||||

| Chicago Alternative Health Center, LLC and Chicago Alternative Health Center Holdings, LLC | 2 Dispensaries | -Chicago, IL (Chicago Ridge and Archer) | Signed in December 2020 and closed in January 2022 | Collectively referred to as “Midway,” at the time of signing, the Archer location was operational and the Ascend by Midway - Chicago Ridge location opened in April 2021. Midway has been included in our consolidated results as a VIE since the initial signing in December 2020. | ||||||||||||||||||||||

5

| FPAW Michigan 2, Inc. | 6 Dispensaries | -3 dispensaries in the Grand Rapids, MI area -1 dispensary in the Ann Arbor, MI area -1 dispensary in Battle Creek, MI -1 dispensary in the Detroit, MI area | December 2020 | FPAW Michigan 2, Inc. (“FPAW”) was owned by one of the founders of AWH, who assigned 99.9% of its membership interest to AWH in December 2020 and was consolidated as a VIE prior to that date. Two dispensaries in the Grand Rapids, MI area opened in September 2020 and March 2021, and a third is expected in late 2022 or early 2023. The Battle Creek and Detroit area dispensaries each opened in June 2020 and the Ann Arbor dispensary opened in August 2020. AWH continues to consider further development of a second Ann Arbor location, as well as a location in East Lansing. | ||||||||||||||||||||||

| Hemma, LLC | 1 Cultivation | -Monroe, OH | May 2021 | AWH’s first cultivation site in Ohio with expansion potential. | ||||||||||||||||||||||

| BCCO, LLC | 1 Dispensary | -Carroll, OH | October 2021 | Medical dispensary located in the greater Columbus area. | ||||||||||||||||||||||

| Ohio Cannabis Clinic, LLC | 1 Dispensary | -Coshocton, OH | December 2021 | Medical dispensary located in the greater Columbus area. | ||||||||||||||||||||||

Description of the Business

Overview of the Company

Ascend is a vertically integrated multi-state cannabis operator focused on adult-use or near-term adult-use cannabis states in limited license markets. The core business is the cultivation, manufacturing, and distribution of cannabis consumer packaged goods, which Ascend sells through company-owned retail stores and to third-party licensed retail cannabis stores. Ascend believes in bettering lives through cannabis. The mission is to improve the lives of its employees, patients, customers and the communities we serve through the use of the cannabis plant.

The consumer products portfolio is generated primarily from plant material that the Company grows and processes. As of December 31, 2021, AWH produces consumer-packaged goods in five manufacturing facilities with 176,000 square feet of cumulative canopy and total capacity of 88,000 pounds annually. Ascend is currently undergoing expansions to 255,000 square feet of cumulative canopy, which it hopes to complete by the end of 2022. As of December 31, 2021, the product portfolio consists of 224 SKUs, across a range of cannabis product categories, including flower, pre-rolls, concentrates, vapes, edibles and other cannabis-related products. All of the expansion plans are subject to capital allocation decisions, the evolving regulatory environment and the COVID-19 pandemic. See “Forward-Looking Statements.”

Product Offering

Ascend produces and distributes cannabis products for its wholesale partners and AWH owned retail stores. Ascend’s goal is to provide wholesale partners and retail customers with consistent access to quality cannabis products while maintaining a variety of form-factors and SKUs. Ascend currently produces its full product set with multiple form factors in Illinois where it has a lab and kitchen. Ascend is in the process of building labs and kitchens at many of its other cultivation facilities so it can produce other form factors such as edibles, in addition to flower and pre-rolls, in all of the states in which it operates. Ascend’s in-house brands offer a variety of options to satisfy every potential customer’s budget and preference. Ascend’s approach to branding is to have brands that fit the “good”, “better”, and “best” consumer categories. The in-house brands include: SimplyHerb, Ozone, and Ozone Reserve. SimplyHerb is the “good” brand and the most price accessible product with SKUs targeted for the price conscious, value-driven buyer. SimplyHerb is currently produced in Illinois, Massachusetts, and Michigan. Ozone is the “better” brand aimed at providing quality products to the seasoned connoisseur as well as the canna-curious. Ozone Reserve is the “best” offering with premier products including exotic flower, refined concentrates, purified oils, as well as resins and distillates. Ozone and Ozone Reserve are currently produced and sold in Illinois,

6

Massachusetts, Michigan, New Jersey, and Ohio. Ozone products have been well received in the market. Ozone has been cited as having the second highest sales of any branded product in Illinois for 2021.

In addition to producing its own brands, AWH also partners with multiple premiere brands for which it cultivates and sells products targeted to different demographics. Among our partners are Lowell Farms, Flower by Edie Parker, and 1906. This model allows AWH to target customer demographics that complement its base-markets and leverage brand recognition of our partners, while crafting and selling their tried-and-true products. For example:

•Lowell Smokes, by Lowell Farms, allows AWH to leverage the Lowell Farms brand amongst the male demographic seeking premium pre-rolls.

•Edie Parker, is a Women-led fashion and lifestyle company that launched a cannabis brand, “Flower by Edie Parker.” The Flower by Edie Parker line provides AWH with a product aimed to attract the female consumer.

•1906, is a brand targeted to consumers looking for premier edible experiences. 1906 gives AWH the ability to provide a competitive edible offering.

The Company is pursuing a longer term goal to have 50% of sales derived from the wholesale business and 50% of sales derived from the retail business, with 50% of products sold in Ascend retail dispensaries being in-house or partner branded products. With this strategy, AWH expects to benefit from vertical margins, while maintaining an offering with options and variety for its retail consumers. No customer represented more than 10% of the Company’s net revenue during 2021, 2020, or 2019.

Strategy

AWH is committed to running the business aligned with its core strategic principles. These include a focus on:

•Achieving vertical integration and scale in limited-license markets. The Company is committed to being vertically integrated in every state in which it operates. This entails controlling the entire supply chain from seed to sale. AWH is currently vertically integrated in all five states of operation. Four of the five markets in which AWH operates, are in states that pose restrictions limiting the number of licenses allowable, creating a more competitive dynamic. AWH is committed to being a top player in each of the states in which it operates. AWH does not intend to expanded to new states without obtaining a large presence and proposes to expand to a new state if it has plans to expand operations to meet the states maximum allowable number of dispensaries and cultivation footprint.

•Key flagship locations. AWH is dedicated to securing retail sites in key flagship locations. AWH believes that location is critical when it comes to the success and long-term sustainability of a dispensary. By situating the stores in marquee locations, AWH believes the barriers to entry for competition are higher. Some of AWH’s flagship locations include: 1) Ascend Collinsville, which is strategically located in the retail corridor near St. Louis, 2) Ascend Boston, which is located in downtown Boston between TD Garden and Faneuil Hall, and 3) Ascend Rochelle Park, which is located on Route 17 just a mile from the Garden State Plaza in highly trafficked northern New Jersey.

•Disciplined capital allocation and execution of mergers and acquisitions. AWH has a disciplined capital allocation strategy. The Company only deploys capital in markets and on projects which it believes will be accretive to its shareholders. To date, the bulk of the Company’s expansion has been through acquisition. The Company views M&A as the fastest path to growth given the barriers to entry and the regulatory environment in the cannabis industry. Largely due to early license awards, there are a number of independent and single-state operators in the markets in which we operate today. These assets represent attractive acquisition opportunities, as the Company can leverage its local permitting expertise and operational and financial resources to optimize the performance of these assets. Most of the Company’s acquisitions have been negotiated and priced prior to the respective state’s passing of recreational legislation. Many of the assets AWH has acquired have historically underperformed under their previous

7

ownership and AWH has been able to improve the financial performance of acquired assets by implementing its standard operating procedures and technology, thereby allowing for AWH to make acquisitions that create significant value for shareholders.

The Company has been successful in opening facilities and dispensaries and expects continued growth to be driven by opening new operational facilities and dispensaries under our current licenses, expansion of our current facilities, and increased consumer demand.

General Development of the Business

As of December 31, 2021, AWH has direct or indirect operations or financial interests in five U.S. geographic markets: Illinois, Massachusetts, Michigan, New Jersey, and Ohio. AWH has expanded its operational footprint primarily through several acquisitions as identified above. See acquisition history in “History of the Company.”

In addition to the acquisitions the Company has made, AWH has benefited from several cultivation expansion opportunities. The material cultivation expansion projects that have been completed or are underway are detailed below:

•Illinois. In 2019, AWH added a lab and kitchen and scaled the Illinois Cultivation it had acquired through the original acquisition of Revolution Cannabis-Barry LLC in 2018. In 2020, AWH commenced a large construction project to add a 125,000 square foot greenhouse with 58,000 square feet of canopy to its Barry, IL cultivation center. Prior to expansion, the facility had 55,000 square feet of indoor canopy and a lab and kitchen. The greenhouse was largely completed in December 2021 and the Company planted the first 3,600 plants in the greenhouse the first week of 2022. Now, AWH has scaled Illinois cultivation operations to 113,000 total square feet of canopy.

•Massachusetts. The Company acquired real property of its Athol cultivation site in 2018. In 2019, the Company began Phase 1 of its cultivation build in Athol, MA and commenced cultivation activities in 2020. By Q2 2021, the Company had completed 17,000 square feet of canopy at the site, concluding Phase 1. The Company recently added an incremental 37,000 square feet of canopy and is in the process of adding a lab and kitchen.

•New Jersey. In early 2021, AWH commenced Phase 1 of expansion of the Franklin, NJ cultivation center it had acquired through Greenleaf Compassion Center, LLC. By Q3 2021 the Company had 16,000 square feet of canopy online. The Company plans to add an additional 26,000 square feet of canopy and a lab and kitchen to the current site by the end of 2022. In November 2021, AWH acquired the land adjacent to the Franklin, New Jersey cultivation site. Between the two sites, the Company plans to add an incremental 108,000 square feet of canopy by the end of 2023, for a total of 150,000 square feet.

•Michigan. In 2021, AWH phased in 28,000 feet of canopy at the Lansing, MI location. The Company plans to add a lab to the facility in 2022 so it can expand the offering in the state by producing additional form factors such as edibles.

Operations Summary

AWH’s core business is the cultivation, manufacturing, and distribution of cannabis consumer packaged goods, which are sold through company-owned retail stores and to third-party licensed retail cannabis stores. The Company is committed to being vertically integrated in every state in which it operates, which entails controlling the entire supply chain from seed to sale. AWH has been successful in opening facilities and dispensaries, and expects the majority of future growth to be driven by opening new operational facilities and dispensaries under current licenses, expansion of current facilities and increased consumer demand.

8

Cultivation

AWH’s cultivation practices have been engineered for scalability and repeatability as the Company expands into additional states. AWH aims to continuously refine cultivation operations to rapidly scale output without sacrificing quality and consistency. Future expansion is planned to provide the infrastructure to diversify the seed supply and further mechanize and automate harvest operations. AWH believes it will be able to continue to rapidly scale cultivation by: (i) commencing operations at additional cultivation sites; (ii) expanding canopy at existing cultivation sites; and (iii) increasing yields by dialing in genetics and environmental conditions and increasing the number of harvests. AWH is focused on driving biomass cost per gram lower with the goal of creating a competitive advantage in the limited license states in which the Company operates. AWH has used strain rationalization, improved cultivation practices, and investments in technology to drive higher yields per square foot than the industry average.

Manufacturing

AWH’s manufacturing operations are centered around the quality of products and the efficiency of production. AWH strives to produce high quality, consistent products across its manufacturing facilities, and has implemented strict brand and quality assurance standards and standard operating procedures in an effort to ensure consistent product and consumer experience across all operating markets. AWH is focused on scaling capacity, improving yields, and increasing efficiency. AWH is standardizing and increasing capacity in hydrocarbon and ethanol extraction wherever possible with the goal of maximizing product quality and throughput and improve crude yields and are making investments in manufacturing and extraction technology, including high speed flower packaging, cartridge filling and automated pre-rolling as drivers of labor efficiency.

Wholesale distribution

During the fourth quarter of 2021, approximately 33% of AWH sales were generated by sales of Ascend products to third-party retailers. AWH aims to grow the wholesale business to half of the total business by: 1) increasing wholesale market share and expanding penetration within wholesale distribution, 2) selling higher volumes of product to wholesale customers, and 3) expanding the category set to higher value products sold to wholesale customers. As of December 31, 2021, AWH sold products to 99% of the dispensaries in Illinois, but the Company has room to significantly increase market penetration across its other states. AWH has internal sales managers dedicated to these penetration efforts.

AWH is also acutely focused on category management and expansion. AWH’s development efforts are focused on pre-rolls, vapes, edibles, and other ready-to-use product forms that it expects to outperform whole flower over time. The Company is also concentrating on expanding the vape offering, including live products and ratio products that represent fast growing segments of the vape category, and expanding the pre-roll offering. The Company expects the pre-roll category to grow significantly as the preferred way to consume flower for many customers. In 2021, AWH launched a pre-roll partnership with Lowell Smokes and in 2022, the Company plans to launch multiple additional pre-roll SKUs in smaller sizes, innovative multi-pack options, and premium infused pre-rolls. AWH is also expanding the edibles manufacturing capabilities to provide micro-dose product forms along with additional forms desired by the market. Strategic partnerships are a key part of diversifying and expanding the Company’s offering.

9

Retail

AWH operates both licensed retail adult-use and medicinal cannabis dispensaries. The Ascend retail brand aims to elevate the cannabis shopping experience by combining consistent and convenient customer service with high-quality products and exclusive brand partnerships. AWH believes the retail operating principles described below differentiate the Company from its competitors.

•Location. All of the Company’s dispensaries are located in key retail locations. AWH believes location is a huge barrier to entry for defending its competitive positioning overtime. Each of the Company’s dispensaries are located within a turn off of a major highway or in a highly trafficked downtown.

•Vision. Ascend believes in using the power of the cannabis plant to help people better their lives. As a company, AWH has a strong commitment to the success of the brand and maintaining this vision.

•People and Culture. AWH aims to hire store managers with prior experience in cannabis and has an acute focus on talent development for the rest of the store employees. The Company has an extensive onboarding and training program focused not only on brand and product knowledge, but also on creating a great customer experience. AWH employees are motivated by daily sales goals set at the stores. AWH reaches these goals by ensuring it has the right product and the right talent in place to deliver a best-in-class customer experience. Stores measure week over week sales growth, peak days for volume, transactions, gross margin and other key performance metrics.

•High Volume Focus. AWH is focused on driving high transaction volume in its retail stores. The Company improves traffic with increased number of point of sales systems, optimized store layouts, and enhanced menu management.

•Omni-channel experiences. As customer shopping preferences continue to evolve and customers increasingly shop across multiple channels, AWH strives to create a best-in-class, omni-channel customer experience. These experiences have been especially critical to operations during the COVID-19 pandemic. Omnichannel experiences include:

◦Reserve-Online-Pickup-in-Store. This allows customers to purchase merchandise through letsascend.com and pick-up the merchandise in-store, which often drives incremental in-store sales. Over 90% of customers in Collinsville utilize the Reserve-Online-Pickup-in-Store option.

◦Delivery. In Q4 2021, AWH launched pilot delivery programs in Newton, Massachusetts, and throughout Michigan, allowing AWH to bring customers the products they enjoy straight to the comfort of their homes.

◦Curbside Pickup. This offering allows customers to have their orders brought directly to their vehicles.

◦Online Consultations and Real-time Chat. This allows customers to interact with associates, ask questions and build their basket ahead of their in-store visit, driving associate productivity and incremental sales.

Strategic Sourcing

Ascend continues to focus on supply chain optimization and strategic sourcing as the Company scales, allowing our growing base to provide leverage across the organization. This includes a focus on supplier rationalization, so that best-in-class supply partners are providing full end-to-end service across the enterprise. Building a common base of operating procedures, packaging and supply components, and supply partners across the organization is critical to this strategic direction.

10

Environmental, Social, and Governance

Environmental, Social, and Governance (“ESG”) initiatives are at the core of AWH’s guiding principles. AWH is committed to creating an inclusive, sustainable company that provides best-in-class governance. Below are a few of the key ESG initiatives at Ascend.

•Social Justice. While AWH understands and appreciates how fortunate the Company is to be in a position to help build and guide the future of modern cannabis, AWH is also acutely aware of the lives that have been destroyed, especially in minority communities, through decades of unjust laws and inequitable enforcement. AWH has been a long standing partner with the Last Prisoner Project (LPP) to support their effort to push to get non-violent offenders released from prison. In 2021, AWH on-boarded a Vice President of Social Justice who is leading the charge for AWH’s internal social justice initiatives. Under this leadership, AWH has contributed funds to the Continuing Legal Education (CLE) institute which seeks to educate attorneys interested in learning the ins and outs of the expungement process. AWH will continue to look for other opportunities to collaborate with nonprofits and legal organizations to sponsor and coordinate expungement clinics. In January 2022, AWH launched a nonprofit foundation incubating and supporting individuals who qualify as social equity applicants.

•Diversity and Inclusion. People are the Company’s greatest asset. The team is comprised of a consortium of skilled and passionate professionals and partners from a diverse range of fields. AWH believes in building a diverse team, creating a space where ALL feel welcome and have the opportunity to grow while contributing to the success of AWH. AWH recently launched three Employee Resource Groups (ERGs) for the LGBTQ+, Black, and Female communities within AWH. These are voluntary, employee-led groups that foster a diverse, inclusive workplace aligned with organizational mission, values, goals, business practices, and objectives.

•Environmental. AWH recently commenced the process to gather baseline energy and water usage metrics. In January 2022, AWH began planting in its first greenhouse at our Barry, Illinois cultivation location. Greenhouses consume less energy than indoor grows because they subsidize their energy needs with the sun. Quality is still maintained as conditions are maintained with HVAC systems and supplemental light is available. AWH will continue to explore other operational solutions to lower its environmental impact.

•Governance. Best-in-class governance and disclosure are important to AWH. The Company has a majority independent board, provides GAAP financials, and publishes its key governance policies, as well as provides access to its whistleblower hotline on its investor website. The Company monitors disclosures relative to its peers to help maintain best-in-class practices.

Human Capital

As of December 31, 2021, we had approximately 1,500 employees, approximately 89% of whom were in field operations and approximately 11% of whom were in corporate administrative and management. We offer our employees opportunities to grow and develop their careers and provide them with a wide array of company paid benefits and compensation packages which we believe are competitive relative to our peers in the industry. As of December 31, 2021, 26% of leadership positions were held by ethnic minorities and 37% of leadership positions were held by females. AWH will continue to work towards achieving a more equitable balance of genders and ethnicities across the company and in leadership.

Employee safety and health in the workplace is one of our core values. The COVID-19 pandemic has underscored the importance of keeping our employees safe and healthy. In response to the pandemic, we have taken actions aligned with the World Health Organization and the Centers for Disease Control and Prevention to protect our workforce so they can more safely and effectively perform their work.

The Company’s number and levels of employees are continually aligned with the pace and growth of our business and management believes it has sufficient human capital to operate the business successfully.

11

Operations by State

The following is an overview of our cultivation and dispensary assets by state that are currently operational, as well as our expected asset base once fully built out.

Cultivation assets:

Across its cultivation assets, as of December 31, 2021 AWH had 176,000 square feet of total canopy, which is defined as the square footage of flower, vegetation, and propagation tables. AWH anticipates expanding to 255,000 square feet of total canopy by the end of 2022. The Company estimates each square foot of total canopy has the power to generate approximately half a pound of cannabis per year. All of the Company’s cultivation and planned cultivation facilities are indoor, with the exception of the 55,000 square foot greenhouse in Illinois. The Company believes that indoor grow facilities allow for fine-tuned controls which help enable AWH to grow high-quality cannabis. All of the cultivation projects underway are expansion projects to existing cultivation facilities. The Company deems these as lower risk than green fielding at new sites that are not yet permitted for cultivation operations. The new cultivation plans are flexible and will ultimately depend on market conditions, local licensing, construction, and other regulatory permissions. All of our expansion plans are subject to capital allocation decisions, the evolving regulatory environment and the COVID-19 pandemic. See “Forward-Looking Statements.”

| State | Square Feet of Canopy as of December 31, 2021 | Square Feet Planned by Year End 2022(1) | Additional Comments | |||||||||||||||||

| Illinois | 113,000 | 113,000 | Located in Barry, Illinois, the cultivation facility also has ethane and butane-based extraction equipment and kitchen. The Company is awaiting state approval to plant in the new greenhouse. | |||||||||||||||||

| Michigan | 28,000 | 28,000 | Located in Lansing, Michigan, the cultivation facility has 28,000 square feet of canopy. The Company is adding a kitchen in 2022. | |||||||||||||||||

| Massachusetts | 17,000 | 54,000 | Located in Athol, Massachusetts, the cultivation facility is undergoing phase 2 expansion which it plans to complete in 2022. The Company is also adding an ethane and butane-based extraction equipment and kitchen. | |||||||||||||||||

| New Jersey | 16,000 | 42,000 | Located in Franklin, New Jersey, the cultivation facility is undergoing phase 2 expansion which will add 26,000 square feet of canopy and a lab and kitchen. The Company plans to complete phase 2 in 2022. AWH also purchased the land adjacent to the facility in Q4 2021 and plans to add an incremental 100,000 square feet of canopy to the site in 2023. | |||||||||||||||||

| Ohio | 2,000 | 18,000 | Located in Monroe, OH the facility currently has 2,000 square feet of canopy. The Company plans to add 35,000 square feet of quad stacked canopy. The Company has a pending acquisition of a processing facility located near the cultivation facility. | |||||||||||||||||

(1) See “Forward-Looking Statements.”

Dispensary assets:

As of December 31, 2021, AWH had 20 open and operating retail locations. By the end of 2022, AWH anticipates expanding to 24 open and operating dispensaries. The new store opening plans are also flexible and will ultimately depend on market conditions, local licensing, construction, and other regulatory permissions. All of the dispensary plans are subject to capital allocation decisions, the evolving regulatory environment and the COVID-19 pandemic. See “ Forward-Looking Statements.”

12

| State | Open Dispensaries as of December 31, 2021 | Owned Dispensaries and Licenses as of December 31, 2021 | Comments | |||||||||||||||||

| Illinois | 8 | 8 | 4 dispensaries in the Chicago area; 2 in Southern IL bordering Missouri; 2 near Springfield, IL. The state caps recreational dispensary licenses at 10 stores per owner. | |||||||||||||||||

| Massachusetts | 2 | 3 | 1 dispensary in downtown Boston; 1 in Newton; 1 license and building under construction in New Bedford. The state caps recreational dispensary licenses at 3 stores per owner. | |||||||||||||||||

| New Jersey | 2 | 3 | 1 dispensary in Rochelle Park; 1 in Montclair; 1 license and building under construction in Fort Lee. The state caps recreational dispensary licenses at 3 stores per owner. | |||||||||||||||||

| Michigan | 6 | 8 | 6 dispensaries throughout the state; 1 license and building under construction in Grand Rapids and 1 license and building under construction in East Lansing | |||||||||||||||||

| Ohio | 2 | 2 | 2 dispensaries in the greater Columbus area. The state caps dispensary licenses at 5 stores per owner. | |||||||||||||||||

Licenses

The following chart summarizes the U.S. states in which we operate or have an investment as of December 31, 2021, along with the nature of the operations, whether such activities carried on are direct, indirect or ancillary in nature, the number of dispensary, cultivation and other licenses held by each entity, and whether such entity has any operation, cultivation, or processing facilities.

| State | Entity | Adult-Use/Medical | Direct/Indirect/ Ancillary | Dispensary Licenses | Cultivation/ Processing/ Distribution Licenses | Operational Dispensaries | Operational Cultivation/ Processing Facilities | |||||||||||||||||||||||||||||||||||||

| Illinois | HealthCentral LLC | AU, M | Direct | 4 | — | 4 | — | |||||||||||||||||||||||||||||||||||||

| Illinois | Revolution Cannabis-Barry LLC | AU, M | Direct | — | 2 | — | 1(4) | |||||||||||||||||||||||||||||||||||||

| Illinois | MOCA LLC | AU, M | Direct | 2 | — | 2 | — | |||||||||||||||||||||||||||||||||||||

| Illinois | Chicago Alternative Health Center, LLC | AU, M | Direct | 2 | — | 2 | — | |||||||||||||||||||||||||||||||||||||

| Mass. | MassGrow LLC | AU | Direct | — | 2(1) | — | 1 | |||||||||||||||||||||||||||||||||||||

| Mass. | Ascend Mass LLC | AU | Direct | 3 | — | 2 | — | |||||||||||||||||||||||||||||||||||||

New Jersey | Ascend New Jersey LLC(2) | M | Direct | 3 | 1 | 2 | 1 | |||||||||||||||||||||||||||||||||||||

| New York | MedMen NY, Inc.(3) | M | Ancillary | 4 | 1 | 4 | 1 | |||||||||||||||||||||||||||||||||||||

| Michigan | FPAW Michigan LLC | AU, M | Direct | 6 | 1 | 6 | 1 | |||||||||||||||||||||||||||||||||||||

| Ohio | BCCO, LLC | M | Direct | 1 | — | 1 | — | |||||||||||||||||||||||||||||||||||||

| Ohio | Ohio Cannabis Clinic, LLC | M | Direct | 1 | — | 1 | — | |||||||||||||||||||||||||||||||||||||

| Ohio | Hemma, LLC | M | Direct | — | 1 | — | 1 | |||||||||||||||||||||||||||||||||||||

Ohio | Marichron Pharma, LLC(3) | M | Ancillary | — | 1 | — | — | |||||||||||||||||||||||||||||||||||||

Total | 26 | 9 | 24 | 6 | ||||||||||||||||||||||||||||||||||||||||

(1)Provisionally licensed for processing.

(2)An ATC permit enables the holder to pursue two additional satellite dispensary locations.

13

(3)On February 25, 2021, the Company entered into a definitive investment agreement (the “Investment Agreement”) with subsidiaries of MedMen Enterprises, Inc. (“MedMen”) to acquire MedMen NY, Inc., a licensed registered organization in New York. In December 2021, the Company contends the parties received approval to close the transactions. On January 2, 2022, MedMen purported to terminate the Investment Agreement. The Company has brought suit against MedMen requesting specific performance of MedMen’s obligations under the Investment Agreement and other relief as the Commercial Division of the Supreme Court of New York may determine as appropriate. Refer to “Item 7., Management’s Discussion and Analysis of Financial Condition and Results of Operations–Legal Matters–MedMen NY Litigation,” for additional information related to this matter.

(4)Cultivation and processing operations are co-located at our Barry, IL facility.

Competitive Conditions

Competition

The Company primarily competes with:

•Multi-State Operators (“MSOs”). AWH competes with MSOs from a retail and wholesale perspective, including Trulieve Cannabis Corp., Cresco Labs Inc., Green Thumb Industries Inc., Curaleaf Holdings Inc., TerrAscend Corp., Columbia Care Inc,, and Ayr Wellness Inc, among others. The specific competitors vary for each state of AWH’s operations. For example, Cresco is AWH’s primary wholesale competitor in Illinois, but not as big of a wholesale competitor in New Jersey.

•Single State Operators (“SSOs”). AWH competes with many single state operators across its portfolio.

•Consumer Packaged Goods Companies (“CPG Companies”). Although not a competitive threat today, AWH anticipates CPG Companies gaining a larger presence in the industry if and when cannabis is rendered federally legal.

•Pharmaceutical Companies. Although not a competitive threat today, AWH anticipates pharmaceutical companies gaining a larger presence in the industry if and when cannabis is rendered federally legal.

The Company believes it is well-poised in its competitive positioning due to the competitive advantages highlighted below:

•Scale and vertical integration. The Company’s scale helps it compete, particularly, against the SSOs who may not be able to obtain the same operating synergies that AWH can. AWH is vertically integrated in each of its states of operation and only operates in states where it can have where it believes it can be a top 5 player one day.

•Access to capital. The Company’s access to capital helps it compete, particularly, against the SSOs who may not have the resources that AWH does. AWH management has also been able to leverage its extensive capital markets knowledge, securing $210.0 million in senior debt with an interest rate of 9.5% per annum, which at the time of the deal was an industry leading cost of capital.

•States of operation. With the exception of Michigan, all of AWH’s states of operation are limited license.

•Management. AWH has a diverse management team with experience spanning capital markets, cannabis industry, regulatory, and operations. The management team has proven it can lead, by becoming a top 3 operator in the state of Illinois.

•Location and second mover advantage. While many competitors who were early entrants to the space were pushed into industrial parks or off the beaten path, AWH locations can often be found on the corner of Main & Main, surrounded by other top tier businesses such as Trader Joe’s & Starbucks. This is because AWH entered the business slightly later than some of its peers. In doing so, the Company strategically acquired locations, rather than pursuing a lottery strategy to obtain licenses. AWH was able to use its ‘second-mover advantage’ to secure highly desirable retail locations, many of which it considers to be flagship stores.

14

•Differentiated portfolio of brands. AWH provides a robust offering and a wide range of branded products spanning every price point with products targeted to every demographic.

Overview of Government Regulation

On February 8, 2018, the Canadian Securities Administrators revised their previously released Staff Notice 51-532 – Issuers with U.S. Marijuana-Related Activities (“Staff Notice 51-532”), which provides specific disclosure expectations for issuers that currently have, or are in the process of developing, cannabis related activities in the United States as permitted within a particular State’s regulatory framework. In accordance with the Staff Notice 51-532, below is a discussion of the federal and state-level U.S. regulatory regimes in those jurisdictions where we are currently directly involved, through our subsidiaries, in the cannabis industry. Our subsidiaries and licensed operators with which we have contractual relationships are directly engaged in the manufacture, possession, sale, or distribution of cannabis in the adult-use and/or medical cannabis marketplace in the states of Illinois, Massachusetts, Michigan, New Jersey, and Ohio. In accordance with Staff Notice 51-532, we evaluate, monitor, and reassess this disclosure, and any related risks, on an ongoing basis and the same will be supplemented and amended to investors in public filings, including in the event of government policy changes or the introduction of new or amended guidance, laws, or regulations regarding cannabis regulation. We intend to promptly remedy any material known occurrences of non-compliance with applicable state and local cannabis rules and regulations, and intend to publicly disclose any material non-compliance, citations, or notices of violation which may have an impact on our licenses, business activities, or operations.

The U.S. federal government regulates drugs through the Controlled Substances Act (21 U.S.C. § 811) (the “CSA”), which places controlled substances, including cannabis, in a schedule. Cannabis is classified as a Schedule I controlled substance. The CSA explicitly prohibits the manufacturing, distribution, selling and possession of cannabis and cannabis-derived products as a consequence of its Schedule I classification. Classification of substances under the CSA is determined jointly by the United States Drug Enforcement Administration (the “DEA”) and the FDA. The United States Department of Justice (the “DOJ”) defines Schedule I drugs and substances as drugs with no currently accepted medical use, a high potential for abuse, and a lack of accepted safety for use under medical supervision. However, the FDA has approved Epidiolex, which contains a purified form of cannabidiol (“CBD”), a non-psychoactive cannabinoid in the cannabis plant, for the treatment of seizures associated with two epilepsy conditions. The FDA has not approved cannabis or cannabis compounds as a safe and effective drug for any other condition. Moreover, under the 2018 Farm Bill or Agriculture Improvement Act of 2018, CBD remains a Schedule I controlled substance under the CSA, with a narrow exception for CBD derived from hemp with a tetrahydrocannabinol, which is commonly referred to as tetrahydrocannabinol (“THC”), concentration of less than 0.3%.

Unlike in Canada, where federal legislation uniformly governs the cultivation, distribution, sale, and possession of medical and adult-use cannabis under the Cannabis Act, S.C. 2018, c. 16, and the Cannabis for Medical Purposes Regulations, cannabis is largely regulated at the state level in the United States. To date, there are 37 states, plus the District of Columbia (and the territories of Guam, Puerto Rico, the U.S. Virgin Islands and the Northern Mariana Islands), that have laws and/or regulations that recognize, in one form or another, legitimate medical uses for cannabis and consumer use of cannabis in connection with medical treatment. In addition, the Northern Mariana Islands, Guam, the District of Columbia, and 18 states, including Alaska, Arizona, California, Colorado, Connecticut, Illinois, Maine, Massachusetts, Michigan, Montana, Nevada, New Jersey, New Mexico, New York, Oregon, Vermont, Virginia, and Washington have legalized cannabis for adult-use. Eleven states have also enacted low-THC/high-CBD only laws for medical cannabis patients.

State laws that permit and regulate the production, distribution and use of cannabis for adult-use or medical purposes are in direct conflict with the CSA, which makes cannabis use, distribution and possession federally illegal. Although certain states and territories of the U.S. authorize medical or adult-use cannabis production and distribution by licensed or registered entities, under U.S. federal law, the possession, cultivation, and transfer of cannabis and any related drug paraphernalia is illegal and any such acts are criminal acts under any and all circumstances under the CSA. The Supremacy Clause of the United States Constitution establishes that the United States Constitution and federal laws made pursuant to it are paramount and in case of conflict between federal and state law, the federal law shall apply. Although the Company’s activities are compliant with applicable United States

15

state and local law, strict compliance with state and local laws with respect to cannabis may neither absolve the Company of liability under United States federal law, nor may it provide a defense to any federal proceeding which may be brought against the Company.

The Obama administration attempted to address the inconsistent treatment of cannabis under state and federal law in the Cole Memorandum which outlined certain priorities for the DOJ relating to the prosecution of cannabis offenses. The Cole Memorandum acknowledged that, notwithstanding the designation of cannabis as a Schedule I controlled substance at the federal level, several states had enacted laws authorizing the use of cannabis for medical or adult-use purposes. The Cole Memorandum noted that jurisdictions that have enacted laws legalizing cannabis in some form have also implemented strong and effective regulatory and enforcement systems to control the cultivation, processing, distribution, sale and possession of cannabis. As such, conduct in compliance with those laws and regulations is less likely to implicate the Cole Memorandum’s enforcement priorities. The DOJ did not provide (and has not provided since) specific guidelines for what regulatory and enforcement systems would be deemed sufficient under the Cole Memorandum. In light of limited investigative and prosecutorial resources, the Cole Memorandum concluded that the DOJ should be focused on addressing only the most significant threats related to cannabis, such as distribution of cannabis from states where cannabis is legal to those where cannabis is illegal, the diversion of cannabis revenues to illicit drug cartels and sales of cannabis to minors.

On January 4, 2018, former U.S. Attorney General Jeff Sessions issued the Sessions Memorandum, which rescinded the Cole Memorandum effective upon its issuance. The Sessions Memorandum stated, in part, that current law reflects “Congress’ determination that cannabis is a dangerous drug and cannabis activity is a serious crime,” and Mr. Sessions directed all U.S. Attorneys to enforce the laws enacted by Congress by following well-established principles when pursuing prosecutions related to cannabis activities. We are not aware of any prosecutions of investment companies doing routine business with licensed cannabis related businesses in light of the new DOJ position. However, there can be no assurance that the federal government will not enforce federal laws relating to cannabis in the future. As a result of the Sessions Memorandum, federal prosecutors are now free to utilize their prosecutorial discretion to decide whether to prosecute cannabis activities, despite the existence of state-level laws that may be inconsistent with federal prohibitions. No direction was given to federal prosecutors in the Sessions Memorandum as to the priority they should ascribe to such cannabis activities, and thus it is uncertain how active U.S. federal prosecutors will be in relation to such activities.

The former Attorneys General who succeeded former Attorney General Sessions following his resignation did not provide a clear policy directive for the United States as it pertains to state-legal cannabis related activities. President Joseph R. Biden was sworn in as the 46th United States President on January 20, 2021. President Biden nominated Merrick Garland to serve as Attorney General in his administration. It is not yet known whether the Department of Justice under President Biden and Attorney General Garland, confirmed on March 10, 2021, will re-adopt the Cole Memorandum or announce a substantive cannabis enforcement policy. At Mr. Garland’s confirmation hearing, he stated, “It does not seem to me a useful use of limited resources that we have, to be pursuing prosecutions in states that have legalized and that are regulating the use of marijuana, either medically or otherwise.” He has not, however, reissued the Cole Memorandum or otherwise provided guidance. If the Department of Justice policy under Attorney General Garland were to aggressively pursue financiers or owners of cannabis-related businesses, and United States Attorneys followed such Department of Justice policies through pursuing prosecutions, then the Company could face (i) seizure of its cash and other assets used to support or derived from its cannabis operations, (ii) the arrest of its employees, directors, officers, managers and investors, and charges of ancillary criminal violations of the Controlled Substances Act for aiding and abetting and conspiring to violate the Controlled Substances Act by virtue of providing financial support to cannabis companies that service or provide goods to state-licensed or permitted cultivators, processors, distributors, and/or retailers of cannabis, and/or (iii) the barring of its employees, directors, officers, managers and investors who are not United States citizens from entry into the United States for life. Unless and until the United States Congress amends the Controlled Substances Act with respect to cannabis (and as to the timing or scope of any such potential amendments there can be no assurance), there is a risk that federal authorities may enforce current U.S. federal law criminalizing cannabis.

16

While federal prosecutors appear to continue to use the Cole Memorandum’s priorities as an enforcement guide, the prosecutorial effects resulting from the rescission of the Cole Memorandum and the implementation of the Sessions Memorandum remain uncertain. The sheer size of the cannabis industry, in addition to participation by state and local governments and investors, suggests that a large-scale federal enforcement operation may create unwanted political backlash for the DOJ. It is also possible that the revocation of the Cole Memorandum could motivate Congress to reconcile federal and state laws. While Congress is considering and has considered legislation that may address these issues, there can be no assurance that such legislation passes. Regardless, at this time, cannabis remains a Schedule I controlled substance at the federal level. The U.S. federal government has always reserved the right to enforce federal law in regard to the sale and disbursement of medical or adult-use cannabis, even if state law authorizes such sale and disbursement. It is unclear whether the risk of enforcement has been altered.

Additionally, under United States federal law, it may potentially be a violation of federal money laundering statutes for financial institutions to take any proceeds from the sale of cannabis or any other Schedule I controlled substance. Canadian banks are likewise hesitant to deal with cannabis companies, due to the uncertain legal and regulatory framework of the industry. Banks and other financial institutions, particularly those that are federally chartered in the United States, could be prosecuted and possibly convicted of money laundering for providing services to cannabis businesses. While Congress is considering legislation that may address these issues, there can be no assurance of the content of any proposed legislation or that such legislation is ever passed.

Despite these laws, the U.S. Department of the Treasury’s United States Financial Crimes Enforcement Network (“FinCEN”) issued a memorandum (the “FinCEN Memorandum”) outlining the pathways for financial institutions to bank state-sanctioned cannabis businesses in compliance with federal enforcement priorities. The FinCEN Memorandum echoed the enforcement priorities of the Cole Memorandum and states that in some circumstances, it is permissible for banks to provide services to cannabis-related businesses without risking prosecution for violation of federal money laundering laws. Under these guidelines, financial institutions must submit a Suspicious Activity Report (“SAR”) in connection with all cannabis-related banking activities by any client of such financial institution, in accordance with federal money laundering laws. These cannabis-related SARs are divided into three categories - cannabis limited, cannabis priority, and cannabis terminated - based on the financial institution’s belief that the business in question follows state law, is operating outside of compliance with state law, or where the banking relationship has been terminated, respectively. On the same day that the FinCEN Memorandum was published, the DOJ issued a memorandum (the “2014 Cole Memorandum”) directing prosecutors to apply the enforcement priorities of the Cole Memorandum in determining whether to charge individuals or institutions with crimes related to financial transactions involving the proceeds of cannabis-related conduct. The 2014 Cole Memorandum has been rescinded as of January 4, 2018, along with the Cole Memorandum, removing guidance that enforcement of applicable financial crimes against state-compliant actors was not a DOJ priority.

However, former Attorney General Sessions’ revocation of the Cole Memorandum and the 2014 Cole Memorandum has not affected the status of the FinCEN Memorandum, nor has the Department of the Treasury given any indication that it intends to rescind the FinCEN Memorandum itself. Though it was originally intended for the 2014 Cole Memorandum and the FinCEN Memorandum to work in tandem, the FinCEN Memorandum is a standalone document which explicitly lists the eight enforcement priorities originally cited in the Cole Memorandum. As such, the FinCEN Memorandum remains intact, indicating that the Department of the Treasury and FinCEN intend to continue abiding by its guidance. However, in the United States, it is difficult for cannabis-based businesses to open and maintain a bank account with any bank or other financial institution.

One legislative safeguard for the medical cannabis industry, appended to the federal budget bill, remains in place following the rescission of the Cole Memorandum. For fiscal years 2015, 2016, 2017, 2018, 2019, 2020, and 2021, Congress has included a rider to the Consolidated Appropriations Acts (currently referred to as the “Rohrabacher/Blumenauer Amendment”) to prevent the federal government from using congressionally appropriated funds to enforce federal cannabis laws against regulated medical cannabis actors operating in compliance with state and local law. The Rohrabacher/Blumenauer Amendment was included in the Consolidated Appropriations Act, 2021 signed into legislation by President Trump in December 2020 that remained in effect until September 30, 2021. On September 30, 2021 and December 3, 2021, President Biden signed short-term continuing resolutions to extend current appropriations, most recently through February 18, 2022. On February 8, 2022, the

17

House passed a third continuing resolution to extend current appropriations through March 11, 2022, but the Senate has not yet acted on the measure. There is no guarantee that the Rohrabacher/Blumenauer Amendment will be included in the omnibus appropriations package or a continuing budget resolution once the current Consolidated Appropriations Act, 2021 expires.

Despite the rescission of the Cole Memorandum, the DOJ appears to continue to adhere to the enforcement priorities set forth in the Cole Memorandum. The Cole Memorandum and the Rohrabacher/Blumenauer Amendment gave licensed cannabis operators (particularly medical cannabis operators) and investors in states with legal regimes greater certainty regarding the DOJ’s enforcement priorities and the risk of operating cannabis businesses. While the Sessions Memorandum has introduced some uncertainty regarding federal enforcement, the cannabis industry continues to experience growth in legal medical and adult-use markets across the United States. Accordingly, as an industry best practice, we continue to employ the following policies to ensure compliance with the guidance provided by the Cole Memorandum:

•ensure that its operations are compliant with all licensing requirements as established by the applicable state, county, municipality, town, township, borough, and other political/administrative divisions;

•ensure that its cannabis related activities adhere to the scope of the licensing obtained (for example: in the states where cannabis is permitted only for adult-use, the products are only sold to individuals who meet the requisite age requirements);

•implement policies and procedures to ensure that cannabis products are not distributed to minors;

•implement policies and procedures in place to ensure that funds are not distributed to criminal enterprises, gangs or cartels;

•implement an inventory tracking system and necessary procedures to ensure that such compliance system is effective in tracking inventory and preventing diversion of cannabis or cannabis products into those states where cannabis is not permitted by state law, or cross any state lines in general;

•ensure that its state-authorized cannabis business activity is not used as a cover or pretense for trafficking of other illegal drugs, and is not engaged in any other illegal activity, or any activities that are contrary to any applicable anti-money laundering statutes; and

•ensure that its products comply with applicable regulations and contain necessary disclaimers about the contents of the products to prevent adverse public health consequences from cannabis use and prevent impaired driving.

On June 7, 2018, the Strengthening the Tenth Amendment Through Entrusting States Act (the “STATES Act”) was introduced in the Senate by Republican Senator Cory Gardner of Colorado and Democratic Senator Elizabeth Warren of Massachusetts. A companion bill was introduced in the House by Democratic representative Jared Polis of Colorado. The bill provides in relevant part that the provisions of the CSA, as applied to cannabis, “shall not apply to any person acting in compliance with state law relating to the manufacture, production, possession, distribution, dispensation, administration, or delivery of marijuana.” Even though cannabis will remain within Schedule I of the CSA under the STATES Act, the bill makes the CSA unenforceable to the extent it conflicts with state law. In essence, the bill extends the limitations afforded by the protection within the federal budget-which prevents the DOJ and the DEA from using funds to enforce federal law against state-legal medical cannabis commercial activity-to both medical and adult-use cannabis activity in all states where it has been legalized. The STATES Act was reintroduced on April 4, 2019 in both the House and the Senate. Since the STATES Act is currently draft legislation, there is no guarantee that the STATES Act will become law in its current form.

18

On December 4, 2020, the House of Representatives passed the Marijuana Opportunity Reinvestment and Expungement Act of 2019 (the “MORE Act”). The MORE Act would provide for the removal of cannabis from the list of controlled substances in the CSA and other federal legislation. It would end the applicability of Section 280E to cannabis businesses but would impose a 5% federal excise tax. The MORE Act was not passed by the Senate prior to the end of the 116th Congress, but an updated version was subsequently reintroduced in the House of Representatives on May 28, 2021. On September 30, 2021, the House Judiciary Committee voted to advance the MORE Act once again in a first step towards passage in the full Hose. Before it could become law, the MORE Act would need to be passed by the House of Representatives and Senate and then signed into law by the president. There is no guarantee the MORE Act will become law in its current form.

H.R. 1595, the SAFE Banking Act of 2019, which would expand financial services in the United States to cannabis-related legitimate businesses and service providers, was introduced in the House of Representatives on March 7, 2019 with bipartisan support. On April 11, 2019, S. 1200, the Senate version of the SAFE Banking Act, was filed. This bill also has bipartisan support and more than a fifth of the total Senate, 27 members, co-sponsored it. On September 25, 2019, H.R. 1595 passed in the House of Representatives by a vote of 321 to 103, but it stalled in the Senate. The SAFE Banking Act passed the House again on May 15, 2020, when it was included in the COVID-19 stimulus bill, the Health and Economic Recovery Omnibus Emergency Solutions Act. However, that measure also stalled in the Senate. The SAFE Banking Act passed the House again on April 19, 2021 as H.R. 1996, by a vote of 321 – 101. On September 23, 2021, the House approved the National Defense Authorization Act (“NDAA”) that contained the provisions of the SAFE Banking Act. The SAFE Banking Act was subsequently removed from the NDAA by the House-Senate conference committee on December 7, 2021, and was not included in the final version of the NDAA. On February 4, 2022, the House approved The America COMPETES Act of 2022, which includes the provisions of the Safe Banking Act. The America COMPETES Act now advances to the Senate for consideration. There is no guarantee the SAFE Banking Act will become law in its current form, if at all.

Compliance with Applicable State Laws in the United States

We are in compliance with applicable cannabis licensing requirements and the regulatory framework enacted by each state in which we currently operate. We have in place a detailed compliance program and an internal legal and compliance department, and we are building out our operational compliance team across all states in which we operate. Our compliance department is overseen by our chief compliance officer and further consists of compliance professionals who oversee and ensure compliance in each of our jurisdictions and facilities. We also have external state and local regulatory/compliance counsel engaged in every jurisdiction in which we operate.

We provide training for all employees, using various methods on the following topics relevant to job tasks: compliance with state laws and rules; patient education materials; education materials for recreational customers; security in our facilities and establishments; handwashing and sanitation practices; packaging procedures; state mandated tracking software; establishment specific tracking; track and trace; inventory and POS software; audit procedures; epidemic responses; emergency situation response; dispensing procedures; patient/client check-in procedure; employee education and consultation materials; packaging and labeling requirements; cannabis waste and destruction; active shooter response; robbery response; fire response; bomb-threat response; sexual harassment; drug free workplace; internet and phone usage; discrimination harassment; workplace violence; hygiene and clothing requirements; hand washing; medical emergency response; biocontamination response; gas leak response; visitor access; discounts for special groups; customer loyalty programs; client intake; storage and recall of products; the science of cannabis; speaking with physicians; edibles education; reconciling transactions; inventory control; receiving inventory; shipping inventory; corrective and preventive action plans; filing corrective and preventive action reports; pesticides; wastewater; irrigation systems; fertilizer; beneficial organisms; climate control; transplanting; inventory tagging; pruning; defoliation; drying, trimming and curing; storage of products; maintaining confidentiality; cash handling; and preventing diversion of products.

We emphasize security and inventory control to ensure strict monitoring of cannabis and inventory, from delivery by a licensed distributor to sale or disposal. Only authorized, properly trained employees are allowed to access our computerized inventory control system.

19

We monitor all compliance notifications from the regulators and inspectors in each market and timely resolve any issues identified. We keep records of all compliance notifications received from the state regulators or inspectors, as well as how and when an issue was resolved. Moreover, we monitor news sources for information regarding developments at the state and federal level relating to the regulation and criminalization of cannabis.

Further, we have created comprehensive standard operating procedures that include detailed descriptions and instructions for receiving shipments of inventory, inventory tracking, recordkeeping and record retention practices related to inventory. We also have comprehensive standard operating procedures in place for performing inventory reconciliation, and ensuring the accuracy of inventory tracking and recordkeeping. We maintain accurate records of our inventory at all licensed facilities. Adherence to our standard operating procedures is mandatory and ensures that our operations are compliant with the rules set forth by the applicable state and local laws, regulations, ordinances, licenses and other requirements. We ensure adherence to standard operating procedures by regularly conducting internal inspections and ensures that any issues identified are resolved quickly and thoroughly.

We maintain strict compliance guidelines with respect to online reservations of products. No purchase and sale transactions may be completed online. A patient, patient’s primary caregiver or customer may reserve products online, but the patient or customer must be physically present at one of our dispensaries to complete the transaction. This requirement allows our dispensary staff to ensure that our standard operating procedures (including its compliance programs) are applied to all patients, patient’s primary caregivers and customers in connection with the purchase and sale of products.