Table of Contents

As filed with the Securities and Exchange Commission on November 15, 2018

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-10

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

| HYDRO ONE HOLDINGS LIMITED |

HYDRO ONE LIMITED |

(Exact name of each Co-Registrant as specified in its charter)

| Ontario, Canada | Ontario, Canada | |

| (Province or Other Jurisdiction of Incorporation or Organization) | ||

| 4911 | 4911 | |

| (Primary Standard Industrial Classification Code Number (if applicable)) | ||

| Not Applicable | Not Applicable | |

| (I.R.S. Employer Identification Number (if applicable)) | ||

483 Bay Street

South Tower, 8th Floor

Toronto Ontario M5G 2P5

Canada

(416) 345-5000

(Address and telephone number of Co-Registrants’ principal executive offices)

C T Corporation System

111 Eighth Avenue

New York, New York 10011

(212) 894-8700

(Name, address (including zip code) and telephone number (including area code) of agent for service in the United States)

Copies to:

| James Scarlett Chief Legal Officer 483 Bay Street, South Tower, 8th Floor Toronto Ontario M5G 2P5 Canada (416) 345-5000 |

Rob Lando Osler, Hoskin & Harcourt LLP 620 Eighth Avenue, 36th Floor New York, New York 10018 (212) 867-5800 |

Approximate date of commencement of proposed sale of the securities to the public:

From time to time after the effective date of this Registration Statement

Province of Ontario, Canada

(Principal jurisdiction regulating this offering (if applicable))

It is proposed that this filing shall become effective (check appropriate box):

| A.☐ | Upon filing with the Commission pursuant to Rule 467(a) (if in connection with an offering being made contemporaneously in the United States and Canada) | |||

| B.☒ | At some future date (check the appropriate box below): | |||

| 1.☐ |

pursuant to Rule 467(b) on at (designate a time not sooner than 7 calendar days after filing). | |||

| 2.☐ |

pursuant to Rule 467(b) on at (designate a time 7 calendar days or sooner after filing) because the securities regulatory authority in the review jurisdiction has issued a receipt or notification of clearance on . | |||

| 3.☐ |

pursuant to Rule 467(b) as soon as practicable after notification of the Commission by the Co-Registrants or the Canadian securities regulatory authority of the review jurisdiction that a receipt or notification of clearance has been issued with respect hereto. | |||

| 4.☒ |

after the filing of the next amendment to this form (if preliminary material is being filed). | |||

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to the home jurisdiction’s shelf short form prospectus offering procedures, check the following box. ☒

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of each class of securities to be registered |

Amount to be registered |

Proposed maximum offering price per share (1) |

Proposed maximum aggregate offering price (1) |

Amount of registration fee (2) | ||||

| Debt Securities of Hydro One Holdings Limited |

US$3,000,000,000 | 100% | US$3,000,000,000 | US$0 | ||||

| Guarantee of Hydro One Limited of Hydro One Holdings Limited Debt Securities |

(3) | (3) | (3) | None | ||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated solely for purposes of calculating the registration fee pursuant to Rule 457(o) of the U.S. Securities Act of 1933, as amended (the “Securities Act”). |

| (2) | The registrant previously paid a registration fee of US$373,500 in connection with its registration of US$3,000,000,000 in maximum aggregate offering price of debt securities on its registration statement on Form F-10 (File No. 333-225519) initially filed with the Securities and Exchange Commission on June 8, 2018 (the “Prior Registration Statement”). The Prior Registration Statement has since been withdrawn and no securities were offered, sold or issued thereunder prior to such withdrawal. Pursuant to Rule 457(p) under the Securities Act, the registrant is offsetting US$363,600 of the previous registration fee of US$373,500 paid under the Prior Registration Statement against the total registration fee of US$363,600 due herewith. As a result, no registration fee is payable in connection with this registration statement. |

| (3) | No separate consideration will be received for the guarantee of Hydro One Limited of the debt securities of Hydro One Holdings Limited, and so, pursuant to Rule 457(n) under the Securities Act, no separate fee is payable with respect to the guarantee. |

The Co-Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registration Statement shall become effective as provided in Rule 467 under the Securities Act or on such date as the U.S. Securities and Exchange Commission, acting pursuant to Section 8(a) of the Securities Act, may determine.

Table of Contents

A copy of this preliminary short form base shelf prospectus has been filed with the securities regulatory authority in the Province of Ontario, but has not yet become final for the purpose of the sale of securities. Information contained in this preliminary short form base shelf prospectus may not be complete and may have to be amended. The securities may not be sold until a receipt for the short form base shelf prospectus is obtained from the securities regulatory authority.

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise.

This short form prospectus has been filed under legislation in the Province of Ontario that permits certain information about these securities to be determined after this prospectus has become final and that permits the omission from this prospectus of that information. The legislation requires the delivery to purchasers of a prospectus supplement containing the omitted information within a specified period of time after agreeing to purchase any of these securities.

Information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the United States Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This short form prospectus shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of these securities in any state in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state.

This short form prospectus constitutes a public offering of these securities only in those jurisdictions where they may be lawfully offered for sale and therein only by persons permitted to sell such securities.

Information has been incorporated by reference in this short form prospectus from documents filed with the securities regulatory authority in the Province of Ontario. Copies of the documents incorporated herein by reference may be obtained on request without charge from the Corporate Secretary of Hydro One Limited at 483 Bay Street, South Tower, 8th Floor, Toronto, Ontario M5G 2P5, (416) 345-6313 and are also available electronically at www.sedar.com.

PRELIMINARY SHORT FORM BASE SHELF PROSPECTUS

| New Issue | November 15, 2018 |

HYDRO ONE HOLDINGS LIMITED

U.S.$3,000,000,000

Debt Securities

Fully and Unconditionally Guaranteed by

HYDRO ONE LIMITED

Hydro One Holdings Limited (“HOHL” or the “Issuer”), an indirect wholly-owned subsidiary of Hydro One Limited, may from time to time issue, offer and sell debentures, notes or other evidence of indebtedness of any kind, nature or description (collectively, “Debt Securities”) under this short form base shelf prospectus (the “Prospectus”). The Debt Securities will be fully and unconditionally guaranteed as to payment of principal, premium (if any), interest and certain other amounts by Hydro One Limited. The Debt Securities offered hereby may be offered or sold separately or together, in separate series, in amounts, at prices and on terms to be determined based on market conditions at the time of sale and set forth in one or more prospectus supplements to the Prospectus (each, a “Prospectus Supplement” and together, the “Prospectus Supplements”).

Table of Contents

The aggregate initial offering price of Debt Securities (or the United States dollar equivalent thereof if the Debt Securities are denominated in any other currency or currency unit) that may be sold pursuant to this Prospectus during the 25-month period that this Prospectus, including any amendments hereto, remains effective is limited to U.S.$3,000,000,000.

All information permitted under applicable laws to be omitted from this Prospectus will be contained in one or more Prospectus Supplements that will be delivered to purchasers together with this Prospectus. Each Prospectus Supplement will be incorporated by reference into this Prospectus for the purposes of securities legislation as of the date of such Prospectus Supplement and only for the purposes of the distribution of the Debt Securities to which such Prospectus Supplement pertains.

Unless otherwise specified in the applicable Prospectus Supplement, Debt Securities will not be listed on any securities exchange. There is currently no market through which the Debt Securities may be sold, and purchasers may not be able to resell such Debt Securities purchased under this Prospectus and any applicable Prospectus Supplement. This may affect the pricing of such Debt Securities in the secondary market, the transparency and availability of trading prices, the liquidity of the Debt Securities and the extent of issuer regulation. See “Risk Factors” and “Underwriting”.

The Debt Securities offered hereby have not been qualified for sale under the securities laws of any province or territory of Canada (other than the Province of Ontario) and, unless otherwise provided in the Prospectus Supplement relating to a particular issue of Debt Securities, will not be offered or sold, directly or indirectly, in Canada or to any resident of Canada.

Unless otherwise indicated in the Prospectus Supplement relating to an offering of Debt Securities, the particular offering of Debt Securities will be subject to approval of certain legal matters on behalf of the Issuer and Hydro One Limited by Osler, Hoskin & Harcourt LLP.

Investing in the Debt Securities involves significant risks. Prospective investors should carefully read and consider the risk factors described or referenced under the heading “Cautionary Note Regarding Forward-Looking Information” and “Risk Factors” in this Prospectus, contained in any of the documents incorporated by reference herein, and in any applicable Prospectus Supplement, before purchasing Debt Securities.

HOHL and Hydro One Limited are permitted, under the multi-jurisdictional disclosure system adopted by the United States (“U.S.”), to prepare this Prospectus in accordance with Canadian disclosure requirements. Prospective investors should be aware that such requirements are different from those of the U.S.

Unless otherwise stated therein, all financial statements incorporated by reference in this Prospectus have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”).

Prospective investors should be aware that the acquisition of the Debt Securities described herein may have tax consequences both in Canada and the U.S. This Prospectus does not, and any applicable Prospectus Supplement may not fully, describe these tax consequences. Prospective investors should read the tax discussion in any applicable Prospectus Supplement, but note that such discussion may be only a general summary that does not cover all tax matters that may be of importance to a prospective investor. Each prospective investor is urged to consult its own tax advisors about the tax consequences relating to the purchase, ownership and disposition of the Debt Securities in light of the investor’s own circumstances.

A purchaser’s ability to enforce civil liabilities under U.S. federal securities laws may be affected adversely by the fact that both the Issuer and Hydro One Limited are organized under the laws of the Province of Ontario, substantially all of the officers and directors of the Issuer and Hydro One Limited and some of the experts named in this Prospectus are non-U.S. residents, and a substantial portion of the assets of the Issuer and Hydro One Limited and the assets of such experts named in this Prospectus are located outside of the U.S.

Purchasers are advised that it may not be possible for investors to enforce judgments obtained in Canada against any person or company that is incorporated, continued or otherwise organized under the laws of a foreign jurisdiction or resides outside Canada, even if the party has appointed an agent for service of process. See “Consent to Jurisdiction and Service”.

The Debt Securities have not been approved or disapproved by the U.S. Securities and Exchange Commission (the “SEC”) or any state securities commission, nor has the SEC or any state securities commission passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

Table of Contents

The specific terms of the Debt Securities will be set forth in an accompanying Prospectus Supplement and may include the designation of the particular series, the aggregate principal amount of Debt Securities being offered, any limit on the aggregate principal amount of the Debt Securities of any series being offered, the issue and delivery date, the maturity date, the offering price, the interest rate or method of determining the interest rate, the interest payment date(s), any redemption provisions, any repayment provisions and any other material terms and conditions of the Debt Securities.

The Issuer reserves the right to include in a Prospectus Supplement specific variable terms pertaining to the Debt Securities that are not within the descriptions set forth in this Prospectus.

No underwriter, dealer or agent has been involved in the preparation of this Prospectus or has performed any review of the contents of this Prospectus.

This Prospectus constitutes a public offering of Debt Securities in only those jurisdictions where they may be lawfully offered for sale and therein only by persons permitted to sell the Debt Securities. The Issuer may offer and sell the Debt Securities to, or through, underwriters or dealers purchasing as principals and may also sell the Debt Securities to one or more purchasers directly or through agents. See “Underwriting”.

A Prospectus Supplement relating to a particular offering of Debt Securities will identify each underwriter, dealer or agent, as the case may be, engaged by the Issuer in connection with the offering and sale of the Debt Securities, and will set forth the terms of the offering of the Debt Securities, including the public offering price of such Debt Securities (or the manner of determination thereof if offered on a non-fixed price basis), the method of distribution of such Debt Securities, including, to the extent applicable, the proceeds to, and the portion of expenses borne by, the Issuer from such sale, any underwriting fees, discounts or commissions and any discounts or concessions allowed, re-allowed or paid by any underwriter to other dealers and other material terms of the plan of distribution. If offered on a non-fixed price basis, Debt Securities may be offered at market prices prevailing at the time of sale, at prices related to such prevailing market prices or at prices to be negotiated with purchasers at the time of sale, which prices may vary between purchasers and during the period of distribution. If Debt Securities are offered on a non-fixed price basis, the underwriters’, dealers’ or agents’ compensation, as applicable, will be increased or decreased by the amount by which the aggregate price paid for Debt Securities by the purchasers exceeds or is less than the gross proceeds paid by the underwriters, dealers or agents to the Issuer. See “Underwriting”.

In connection with any offering of Debt Securities (unless otherwise specified in a Prospectus Supplement), the underwriters, dealers or agents may over-allot or effect transactions which stabilize, maintain or otherwise affect the market price of the Debt Securities offered at levels other than those which might otherwise prevail on the open market. These transactions may be commenced, interrupted or discontinued at any time. See “Underwriting”.

The head and registered office of each of the Issuer and Hydro One Limited is located at 483 Bay Street, South Tower, 8th Floor, Toronto, Ontario, M5G 2P5.

Table of Contents

| 1 | ||||

| 2 | ||||

| 2 | ||||

| 3 | ||||

| 3 | ||||

| 6 | ||||

| 6 | ||||

| 7 | ||||

| 7 | ||||

| 8 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| 23 | ||||

| 24 | ||||

| 24 | ||||

| 25 | ||||

| 25 | ||||

| 26 | ||||

| 26 | ||||

| TRANSFER AGENT, REGISTRAR, PAYING AGENT AND INDENTURE TRUSTEE |

26 |

Table of Contents

In this Prospectus and in any Prospectus Supplement, unless otherwise noted or the context otherwise requires, references to “Hydro One” or the “Company” refer to Hydro One Limited and its subsidiaries taken together as a whole. References to “Hydro One Inc.” refer only to Hydro One Inc., references to “Hydro One Limited” refer only to Hydro One Limited and references to “HOHL” or the “Issuer” refer only to Hydro One Holdings Limited.

All references in this Prospectus to “dollars” and “$” are to Canadian dollars, unless otherwise expressly stated. Unless otherwise expressly stated therein, the financial information of Hydro One Limited contained in the documents incorporated by reference herein are presented in Canadian dollars. Hydro One Limited prepares and presents its financial statements in accordance with U.S. GAAP. Unless otherwise indicated, all financial information included and incorporated by reference in this Prospectus or included in any Prospectus Supplement is prepared in accordance with U.S. GAAP.

This Prospectus provides a general description of Debt Securities that the Issuer may offer. Each time the Issuer sells Debt Securities under this Prospectus, the Issuer will provide you with a Prospectus Supplement that will contain specific information about the terms of that offering. The Prospectus Supplement may also add, update or change information contained in this Prospectus. Before investing in any Debt Securities, a prospective investor should read both this Prospectus and any applicable Prospectus Supplement, together with the additional information described below and in the applicable Prospectus Supplement under “Documents Incorporated by Reference”.

This Prospectus includes or the documents incorporated by reference herein include a summary of certain material agreements of Hydro One Limited. The summary descriptions are not complete and are qualified by reference to the terms of the material agreements, which have been filed with the Canadian securities regulatory authorities and are available on SEDAR under Hydro One Limited’s profile at www.sedar.com. Investors are encouraged to read the full text of such material agreements.

Each of the Issuer and Hydro One Limited is responsible for the information contained in or incorporated by reference in this Prospectus or any applicable Prospectus Supplement. Neither the Issuer nor Hydro One Limited has authorized anyone to provide you with different or additional information. Investors should only rely on the information contained in this Prospectus or any Prospectus Supplement and in the documents incorporated by reference herein and therein and investors are not entitled to rely on parts of such information to the exclusion of others. The Issuer is not making an offer of Debt Securities in any jurisdiction where the offer is not permitted by law. You should not assume that the information contained in or incorporated by reference in this Prospectus or any applicable Prospectus Supplement is accurate as of any date other than the date of the applicable document.

- 1 -

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

This Prospectus, including the documents incorporated by reference herein, contains “forward-looking information” within the meaning of applicable Canadian securities laws and the United States Private Securities Litigation Reform Act of 1995 that is based on current expectations, estimates, forecasts and projections about Hydro One’s business and the industry in which Hydro One operates and includes beliefs and assumptions made by management. Such information includes, but is not limited to: statements about the Company’s business and statements concerning the content of future Prospectus Supplements. Additional forward-looking information is identified in the various documents incorporated by reference in this Prospectus, including in the section entitled “Forward-Looking Information” in Hydro One Limited’s most recent annual information form and the section entitled “Forward-Looking Statements and Information” in Hydro One Limited’s most recent annual management’s discussion and analysis of financial results. Words such as “aim”, “could”, “would”, “expect”, “anticipate”, “intend”, “attempt”, “may”, “plan”, “will”, “believe”, “seek”, “estimate”, “goal”, “target” and variations of such words and similar expression are intended to identify such forward-looking information. The forward-looking information contained or incorporated by reference in this Prospectus are not guarantees of future performance and involve assumptions and risks and uncertainties that are difficult to predict. In particular, this forward-looking information is based on a variety of factors and assumptions including, but not limited to: no unforeseen changes in the legislative and operating framework for Ontario’s electricity market; favourable decisions from the Ontario Energy Board and other regulatory bodies concerning outstanding and future rate and other applications; no unexpected delays in obtaining required approvals; no unforeseen changes in rate orders or rate setting methodologies for the Company’s distribution and transmission businesses; no unfavourable changes in environmental regulation; continued use of U.S. GAAP; a stable regulatory environment; no significant changes to the Company’s current credit ratings; and no significant event occurring outside the ordinary course of business. These assumptions are based on information currently available to the Company including information obtained from third-party sources. Actual results may differ materially from those predicted by such forward-looking information. While the Company does not know what impact any of these differences may have, the Company’s business, results of operations, financial condition and credit stability may be materially adversely affected if any such differences occur. Factors that could cause actual results or outcomes to differ materially from the results expressed or implied by forward-looking information are discussed in more detail under “Risk Factors” in this Prospectus or in any Prospectus Supplement and in the various documents incorporated by reference in this Prospectus, including in the sections entitled “Forward-Looking Information” and “Risk Factors” in Hydro One Limited’s most recent annual information form, the sections entitled “Risk Management and Risk Factors” and “Forward-Looking Statements and Information” in Hydro One Limited’s most recent annual management’s discussion and analysis of financial results and the section entitled “Forward-Looking Statements and Information” in Hydro One Limited’s most recent interim management’s discussion and analysis of financial results. You should carefully consider these and other factors and not place undue reliance on forward-looking information.

Neither the Issuer nor Hydro One Limited undertakes or assumes any obligation to update or revise any forward-looking information for any reason, except as required by applicable securities laws.

WHERE TO FIND ADDITIONAL INFORMATION

The Issuer and Hydro One Limited have filed with the SEC, under the United States Securities Act of 1933, as amended, a registration statement on Form F-10 relating to the Debt Securities qualified by this Prospectus (the “Registration Statement”). This Prospectus, which constitutes a part of the Registration Statement, does not contain all of the information contained in the Registration Statement, certain items of which are contained in the exhibits to the Registration Statement as permitted by the rules and regulations of the SEC. For further information with respect to Hydro One and the Debt Securities offered pursuant to this Prospectus and any Prospectus Supplement, reference is made to the Registration Statement and to the exhibits filed therewith. Statements included or incorporated by reference in this Prospectus about the contents of certain documents are not necessarily complete, and in each instance, reference is made to the copy of the document filed as an exhibit to the Registration Statement. Each such statement is qualified in its entirety by such reference.

- 2 -

Table of Contents

Under the multi-jurisdictional disclosure system adopted by the U.S., documents and other information that Hydro One Limited files with the SEC may be prepared in accordance with the disclosure requirements of Canada, which are different from those of the U.S. You may read and download any public document that Hydro One Limited has filed with the Ontario Securities Commission on SEDAR at www.sedar.com.

DOCUMENTS FILED AS PART OF THE REGISTRATION STATEMENT

The following documents have been filed with the SEC as part of the Registration Statement: (i) the documents referred to under the heading “Documents Incorporated by Reference”; (ii) the consent of KPMG LLP; (iii) the consent of Deloitte & Touche LLP; (iv) the consent of Osler, Hoskin & Harcourt LLP; (v) the powers of attorney from the directors and officers of each of the Issuer and Hydro One Limited; (vi) the Indenture dated as of June 8, 2018 (the “Indenture”) between HOHL, as issuer, Hydro One Limited, as guarantor, Computershare Trust Company, N.A., as U.S. trustee (the “U.S. Trustee”), and Computershare Trust Company of Canada, as Canadian co-trustee (the “Canadian Co-Trustee”, and together with the U.S. Trustee, the “Trustees”); and (vii) the Statement of Eligibility on Form T-1 under the United States Trust Indenture Act of 1939 of Computershare Trust Company, N.A.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents, filed by Hydro One Limited with the Ontario Securities Commission, are specifically incorporated by reference into, and form an integral part of, this Prospectus:

| (a) | the annual information form of Hydro One Limited dated March 29, 2018 for the year ended December 31, 2017; |

| (b) | the comparative audited consolidated financial statements of Hydro One Limited as at and for the years ended December 31, 2017 and December 31, 2016, together with the notes thereto and the independent auditors’ reports thereon (the “2017 Annual Financial Statements”); |

| (c) | management’s discussion and analysis in respect of the 2017 Annual Financial Statements; |

| (d) | the unaudited condensed interim consolidated financial statements of Hydro One Limited as at September 30, 2018 and for the three and nine month periods ended September 30, 2018 and 2017, together with the notes thereto (the “Interim Financial Statements”); |

| (e) | management’s discussion and analysis in respect of the Interim Financial Statements; |

| (f) | the management information circular of Hydro One Limited dated March 19, 2018 prepared in connection with the annual meeting of shareholders of Hydro One Limited held on May 15, 2018; |

| (g) | the unaudited pro forma condensed consolidated financial statements of Hydro One Limited dated November 15, 2018 that give effect to the proposed acquisition of Avista Corporation and which include the pro forma consolidated balance sheet of Hydro One Limited as at September 30, 2018, the consolidated pro forma statement of operations of Hydro One Limited for the nine months ended September 30, 2018 and the consolidated pro forma statement of operations of Hydro One Limited for the year ended December 31, 2017, and as filed on SEDAR by Hydro One Limited on November 15, 2018; |

| (h) | the material change report of Hydro One Limited dated July 11, 2018 in respect of an agreement with the Province of Ontario for the orderly replacement of the board of directors of Hydro One Limited and Hydro One Inc. and the retirement of Hydro One Limited’s Chief Executive Officer; |

| (i) | the material change report of Hydro One Limited dated August 14, 2018 announcing the new board of directors of Hydro One Limited; |

| (j) | the following sections of the annual report on Form 10-K of Avista Corporation for the fiscal year ended December 31, 2017 as filed by Avista Corporation with the SEC, and as filed on SEDAR by Hydro One Limited on June 8, 2018: |

| (i) | the sections entitled “Acronyms and Terms” and “Forward-Looking Statements”; |

| (ii) | Item 1. Business; |

| (iii) | Item 1A. Risk Factors; |

| (iv) | Item 2. Properties; |

| (v) | Item 3. Legal Proceedings; |

- 3 -

Table of Contents

| (vi) | Item 6. Selected Financial Data; |

| (vii) | Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations; |

| (viii) | Item 7A. Quantitative and Qualitative Disclosures About Market Risk; and |

| (ix) | Item 8. Financial Statements and Supplementary Data; and |

| (k) | the following sections of the quarterly report on Form 10-Q of Avista Corporation for the quarterly period ended September 30, 2018 as filed by Avista Corporation with the SEC, and filed on SEDAR by Hydro One Limited on November 15, 2018: |

| (i) | the sections entitled “Acronyms and Terms” and “Forward-Looking Statements”; |

| (ii) | Part I – Item 1. Condensed Consolidated Financial Statements, other than the Report of Independent Registered Public Accounting Firm; |

| (iii) | Part I – Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations; |

| (iv) | Part I – Item 3. Quantitative and Qualitative Disclosures About Market Risk; |

| (v) | Part I – Item 4. Controls and Procedures; |

| (vi) | Part II – Item 1. Legal Proceedings; |

| (vii) | Part II – Item 1A. Risk Factors; and |

| (viii) | Part II – Item 2. Unregistered Sales of Equity Securities and Use of Proceeds – Dividend Restrictions. |

Any document of the type referred to above, any annual information form, annual or quarterly financial statements, annual or quarterly management’s discussion and analysis, annual or interim consolidating summary financial information of Hydro One Limited, the Issuer and any subsidiaries of Hydro One Limited other than the Issuer on a combined basis with consolidating adjustments and total consolidated amounts (“Summary Financial Information”), management information circular, material change report (excluding confidential material change reports), business acquisition report or other disclosure document required to be incorporated by reference into a prospectus filed under National Instrument 44-101 – Short Form Prospectus Distributions filed by Hydro One Limited or the Issuer with the Ontario Securities Commission after the date of this Prospectus and prior to 25 months from the date hereof shall be deemed to be incorporated by reference into this Prospectus. To the extent that any document or information incorporated by reference in this Prospectus is included in a report that is filed with or furnished to the SEC, such document or information shall be deemed to be incorporated by reference as an exhibit to the Registration Statement.

Upon a new annual information form and the related annual audited consolidated financial statements and accompanying management’s discussion and analysis being filed by Hydro One Limited with and, where required, accepted by, the Ontario Securities Commission during the term of this Prospectus, the previous annual information form, the previous annual audited consolidated financial statements and accompanying management’s discussion and analysis and all interim financial statements and accompanying management’s discussion and analysis, all material change reports filed by Hydro One Limited prior to the commencement of the then current fiscal year and any business acquisition report for acquisitions completed since the beginning of the financial year in respect of which Hydro One Limited’s new annual information form is filed (unless such report is incorporated by reference into the new annual information form filed or less than nine months of the acquired business’ or related businesses’ operations are incorporated into Hydro One Limited’s most recent audited annual financial statements), shall be deemed no longer to be incorporated into this Prospectus for purposes of future offers and sales of Debt Securities hereunder. Upon an interim financial statement and accompanying management’s discussion and analysis being filed by Hydro One Limited with and, where required, accepted by, the Ontario Securities Commission during the currency of this Prospectus, all interim financial statements and accompanying management’s discussion and analysis filed prior to the new interim financial statements shall be deemed no longer to be incorporated into this Prospectus for purposes of future offers and sales of Debt Securities hereunder. Upon a new management information circular relating to an annual meeting of shareholders of Hydro One Limited being filed by Hydro One Limited with and, where required, accepted by, the Ontario Securities Commission during the term of this Prospectus, the management information circular for the preceding annual meeting of shareholders of Hydro One Limited shall be deemed no longer to be incorporated by reference into this Prospectus for purposes of future offers and sales of Debt Securities hereunder.

- 4 -

Table of Contents

Upon new unaudited pro forma financial statements of Hydro One Limited that give effect to the proposed acquisition of Avista Corporation being filed by Hydro One Limited with and, where required, accepted by, the Ontario Securities Commission during the term of this Prospectus, the previous unaudited pro forma financial statements of Hydro One Limited that give effect to the proposed acquisition of Avista Corporation shall be deemed no longer to be incorporated by reference in this Prospectus for purpose of future offers and sales of Debt Securities hereunder. Upon a new Form 10-K of Avista Corporation being filed by Hydro One Limited with and, where required, accepted by, the Ontario Securities Commission during the term of this Prospectus, the previous Form 10-K of Avista Corporation and all previous Form 10-Q’s of Avista Corporation shall be deemed no longer to be incorporated by reference in this Prospectus for purpose of future offers and sales of Debt Securities hereunder. Upon a business acquisition report in respect of the completion of the acquisition of Avista Corporation by Hydro One Limited being filed by Hydro One Limited with and, where required, accepted by, the Ontario Securities Commission during the term of this Prospectus, or upon the announcement by Hydro One Limited that the acquisition of Avista Corporation is not being completed, the previous unaudited pro forma financial statements of Hydro One Limited that give effect to the proposed acquisition of Avista Corporation, the previous Form 10-K of Avista Corporation and all previous Form 10-Q’s of Avista Corporation shall be deemed no longer to be incorporated by reference in this Prospectus for purpose of future offers and sales of Debt Securities hereunder.

Upon new annual Summary Financial Information being filed by the Issuer with and, where required, accepted by, the Ontario Securities Commission during the term of this Prospectus, the previous annual Summary Financial Information and all interim Summary Financial Information included in the Prospectus or filed prior to the commencement of the then current fiscal year shall be deemed no longer to be included or incorporated by reference into this Prospectus for purposes of future offers and sales of Debt Securities hereunder. Upon new interim Summary Financial Information being filed by the Issuer with and, where required, accepted by, the Ontario Securities Commission during the term of this Prospectus, the previous interim Summary Financial Information included in the Prospectus or filed by the Issuer prior to the new interim Summary Financial Information being filed shall be deemed no longer to be included or incorporated by reference into this Prospectus for purposes of future offers and sales of Debt Securities hereunder.

Certain marketing materials (as that term is defined in applicable securities legislation in Canada) may be provided to Canadian investors in connection with a distribution of Debt Securities under this Prospectus and any applicable Prospectus Supplement. Any “template version” of any such “marketing materials” (as those terms are defined in National Instrument 41-101 – General Prospectus Requirements) pertaining to a distribution of Debt Securities, and filed by Hydro One Limited or the Issuer after the date of the applicable Prospectus Supplement for the offering and before termination of the distribution of such Debt Securities, will be deemed to be incorporated by reference in such Prospectus Supplement for the purposes of the distribution of Debt Securities to which the Prospectus Supplement pertains.

A Prospectus Supplement containing the specific terms of any offering of Debt Securities will be delivered to purchasers of such Debt Securities together with this Prospectus and will be deemed to be incorporated by reference in this Prospectus as of the date of the Prospectus Supplement solely for the purposes of the offering of Debt Securities thereunder.

- 5 -

Table of Contents

Any statement contained in a document incorporated or deemed to be incorporated by reference herein shall be deemed to be modified or superseded, for the purposes of this Prospectus, to the extent that a statement contained herein, or in any other subsequently filed document that also is, or is deemed to be, incorporated by reference herein, modifies or supersedes that statement. The modifying or superseding statement need not state that it has modified or superseded a prior statement or include any other information set forth in the document that it modifies or supersedes. The making of a modifying or superseding statement shall not be deemed an admission for any purposes that the modified or superseded statement, when made, constituted a misrepresentation, an untrue statement of a material fact or an omission to state a material fact that was required to be stated or that was necessary to make a statement not misleading in light of the circumstances in which it was made. Any statement so modified or superseded shall not constitute a part of this Prospectus, except as so modified or superseded.

Copies of the documents incorporated by reference herein may be obtained on request without charge from the Corporate Secretary of Hydro One Limited at 483 Bay Street, South Tower, 8th Floor, Toronto, Ontario, M5G 2P5, telephone (416) 345-6313, and are also available electronically at www.sedar.com.

In this Prospectus, unless otherwise specified or the context otherwise requires, all dollar amounts are expressed in Canadian dollars. References to “dollars” or “$” are to lawful currency of Canada. References to “U.S. dollars” or “U.S.$” are to lawful currency of the United States of America.

The following table sets forth: (i) for the years ended December 31, 2016 and December 31, 2015, the average noon exchange rate and the high, low and period end noon exchange rates of one U.S. dollar in exchange for Canadian dollars as reported by the Bank of Canada; and (ii) for the year ended December 31, 2017 and for the nine months ended September 30, 2018 and September 30, 2017, the daily average exchange rate and the high, low and period end daily average exchange rates of one U.S. dollar in exchange for Canadian dollars as reported by the Bank of Canada.

| Year ended December 31, |

Nine months ended September 30, |

|||||||||||||||||||

| 2017 | 2016 | 2015 | 2018 | 2017 | ||||||||||||||||

| High |

1.3743 | 1.4589 | 1.3990 | 1.3310 | 1.3743 | |||||||||||||||

| Low |

1.2128 | 1.2544 | 1.1728 | 1.2288 | 1.2128 | |||||||||||||||

| Average |

1.2986 | 1.3248 | 1.2787 | 1.2876 | 1.3074 | |||||||||||||||

| Period End |

1.2545 | 1.3427 | 1.3840 | 1.2945 | 1.2480 | |||||||||||||||

As of November 14, 2018, the daily average exchange rate as reported by the Bank of Canada was U.S.$1.00 = $1.3235.

HOHL was incorporated on August 25, 2017 under the Business Corporations Act (Ontario) and is an indirect, wholly-owned subsidiary of Hydro One Limited. HOHL has no significant assets or liabilities, no subsidiaries (other than certain wholly-owned subsidiaries incorporated to facilitate the acquisition of Avista Corporation) and no ongoing business operations of its own, other than certain foreign exchange derivative contracts associated with funding the acquisition of Avista Corporation. HOHL is intended to be used to facilitate the funding transactions necessary to fund a portion of the purchase price for the indirect acquisition by Hydro One Limited of Avista Corporation (the “Merger”). See “Use of Proceeds”.

- 6 -

Table of Contents

Hydro One Limited was incorporated on August 31, 2015 under the Business Corporations Act (Ontario). On October 31, 2015, Hydro One Limited acquired all of the issued and outstanding shares of Hydro One Inc. from the Province of Ontario (the “Province”) in exchange for the issuance of Common Shares and Series 1 preferred shares to the Province.

Hydro One is the largest electricity transmission and distribution company in Ontario. Through its wholly-owned subsidiary, Hydro One Inc., Hydro One owns and operates substantially all of Ontario’s electricity transmission network and is the largest electricity distributor in Ontario by number of customers. Hydro One owns and operates approximately 30,000 circuit kilometres of high-voltage transmission lines and approximately 123,000 circuit kilometres of primary low-voltage distribution lines.

Hydro One has three business segments: (i) transmission; (ii) distribution; and (iii) other business.

Hydro One’s transmission business consists of owning, operating and maintaining its transmission system, which accounts for approximately 98% of Ontario’s transmission capacity based on revenue approved by the Ontario Energy Board. This includes Hydro One’s approximately 66% interest in B2M Limited Partnership, a limited partnership between Hydro One and the Saugeen Ojibway Nation in respect of the Bruce-to-Milton transmission line. Hydro One’s transmission business is a rate-regulated business that earns revenues mainly from charging transmission rates that must be approved by the Ontario Energy Board. Hydro One’s transmission business accounted for approximately 53% of the Company’s total assets as at December 31, 2017, and approximately 51% of its total revenues, net of purchased power, in 2017. All of Hydro One’s transmission business is carried out by its wholly-owned subsidiary Hydro One Inc., through its wholly-owned subsidiary Hydro One Networks Inc. and through other wholly-owned subsidiaries of Hydro One Inc. that own and control Hydro One Sault Ste. Marie LP, as well as the portion of Hydro One’s transmission business held through B2M Limited Partnership, which Hydro One controls.

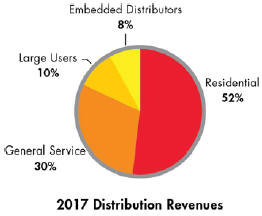

Hydro One’s distribution business consists of owning, operating and maintaining its distribution system, which Hydro One, through Hydro One Inc., owns primarily through its wholly-owned subsidiary, Hydro One Networks Inc., the largest local distribution company in Ontario. Hydro One’s distribution system is also the largest in Ontario, and principally serves rural communities. Hydro One’s distribution business is a rate-regulated business that earns revenues mainly by charging distribution rates that must be approved by the Ontario Energy Board. Hydro One’s distribution business accounted for approximately 36% of its total assets as at December 31, 2017 and approximately 48% of its total revenues, net of purchased power, in 2017.

Hydro One’s other business segment consists principally of Hydro One’s telecommunications business, as well as certain corporate activities. The telecommunications business provides telecommunications support for Hydro One’s transmission and distribution businesses. The telecommunications business also offers communications and information technology solutions to organizations with broadband network requirements. Hydro One’s other business segment is not rate regulated. The other business segment, which in addition to the telecommunications business also includes a deferred tax asset, accounted for approximately 11% of Hydro One’s total assets as at December 31, 2017 and approximately 1% of Hydro One’s total revenues, net of purchased power, in 2017.

The address of the head and registered office of Hydro One is 483 Bay Street, South Tower, 8th Floor, Toronto, Ontario, M5G 2P5.

- 7 -

Table of Contents

Prospective investors in a particular offering of Debt Securities should carefully consider the risks presented in this Prospectus, as well as the information and risk factors contained in the Prospectus Supplement relating to that offering and any and all other information incorporated by reference in this Prospectus. Discussions of certain risks affecting Hydro One are generally provided and described in documents filed by Hydro One Limited with the Ontario Securities Commission from time to time and which are incorporated by reference into this Prospectus, including Hydro One Limited’s annual information form and annual and interim management’s discussion and analysis. In particular, see the sections entitled “Forward-Looking Information” and “Risk Factors” in Hydro One Limited’s most recent annual information form, the sections entitled “Risk Management and Risk Factors” and “Forward-Looking Statements and Information” in Hydro One Limited’s most recent annual management’s discussion and analysis of financial results and the section entitled “Forward-Looking Statements and Information” in Hydro One Limited’s most recent interim management’s discussion and analysis of financial results. If any event arising from these or any other risks occurs, Hydro One’s business, prospects, financial condition, results of operations or cash flows could be materially adversely affected.

In addition, the following additional risk factors will be relevant to prospective investors of Debt Securities.

Reliance on Hydro One Limited as guarantor of the Debt Securities

The Issuer is not expected to have any assets, property or operations other than any Debt Securities it issues, loans it obtains from other third party lenders, loans or other investments it obtains from its affiliates, any associated hedging arrangements and any investments it makes with any such proceeds obtained from these activities. Therefore, the holders of Debt Securities are relying principally on the full and unconditional guarantee of the Debt Securities provided by Hydro One Limited and the financial position and creditworthiness of Hydro One Limited in respect of the payment of the amounts owing under and in respect of the Debt Securities. The financial position and creditworthiness of Hydro One Limited is subject to the risk factors incorporated by reference in this Prospectus.

The Debt Securities will be effectively subordinated to the debt and other liabilities of the Issuer’s and Hydro One Limited’s subsidiaries

Neither the Issuer’s nor Hydro One Limited’s subsidiaries (other than the Issuer) will guarantee or otherwise be responsible for the payment of principal, premium, Additional Amounts (as defined below) or interest required to be made by the Issuer or Hydro One Limited on the Debt Securities. Accordingly, the Debt Securities will be effectively subordinated to all existing and future liabilities of the Issuer’s and Hydro One Limited’s subsidiaries (other than the Issuer). In the event of an insolvency, bankruptcy, liquidation, reorganization or similar proceeding in respect of any of the Issuer’s or Hydro One Limited’s subsidiaries, holders of Debt Securities will have no right to proceed against the assets of such subsidiaries. Creditors of such subsidiaries would generally be entitled to payment in full from such assets before any assets are made available for distribution to the Issuer or Hydro One Limited, as applicable, to pay its debts and other obligations.

The Indenture does not limit the amount of debt that the Issuer, Hydro One Limited or any of their subsidiaries may incur or restrict their ability to engage in other transactions that may adversely affect holders of the Debt Securities

The Indenture does not limit the amount of debt that the Issuer or Hydro One Limited may incur. In addition, the Indenture does not contain any financial covenants or other provisions that would afford the holders of Debt Securities any substantial protection if the Issuer or Hydro One Limited participates in a highly leveraged transaction. In addition, the Indenture does not limit the ability of the Issuer or Hydro One Limited to pay dividends, make distributions, repurchase outstanding shares or mortgage, pledge, encumber or charge any of their assets to secure any indebtedness or other financing. As a result of the foregoing, when evaluating the terms of the Debt Securities, a prospective investor should be aware that the terms of the Indenture and the Debt Securities do not restrict the ability of the Issuer or Hydro One Limited to engage in, or otherwise be a party to, various corporate transactions that could have an adverse impact on a purchaser’s investment in the Debt Securities.

- 8 -

Table of Contents

The Debt Securities are not secured by any assets of the Issuer or Hydro One Limited and any secured creditors will have a prior claim on the assets of the Issuer or Hydro One Limited, as applicable

The Debt Securities are not secured by any assets of the Issuer or Hydro One Limited. If either the Issuer or Hydro One Limited incurs any secured debt, its assets would be subject to prior claims of its secured creditors. In such circumstances, it is possible that there would be insufficient assets remaining from which claims of the holders of any Debt Securities could be satisfied.

The Issuer and Hydro One Limited may be unable to generate the cash flow to service their debt obligations

There is no guarantee that the Issuer and/or Hydro One Limited will generate sufficient cash flow to enable them to service their indebtedness, including the Debt Securities. The ability of the Issuer and Hydro One Limited to pay their expenses and satisfy their debt obligations will depend on their future performance, which will be affected by general economic, financial, competitive, legislative, regulatory and other factors outside their control. Both the Issuer and Hydro One Limited are holding companies and therefore depend on dividends and other distributions from their subsidiaries. As a result, distributions or advances from those subsidiaries are the principal source of funds necessary to meet the debt service obligations of the Issuer and Hydro One Limited. The Issuer and Hydro One Limited believe that cash flow from operations and available cash will be adequate for the foreseeable future. However, if the Issuer and/or Hydro One Limited are unable to generate sufficient cash flow to service their debt, the Issuer and/or Hydro One Limited, as applicable, may be required to sell assets, reduce capital expenditures, refinance all or a portion of any outstanding debt, including the Debt Securities, or obtain additional financing. There is no guarantee that the Issuer and/or Hydro One Limited will be able to refinance their debt, sell assets or incur additional indebtedness on terms acceptable to them, or at all.

In addition, in connection with its proposed acquisition of Avista Corporation, Hydro One Limited has agreed to make certain commitments in proceedings before various state utility commissions in the United States. The commitments, if adopted, will have the effect of isolating the assets of Avista Corporation and its subsidiaries from creditors of Hydro One Limited and its other subsidiaries (including the Issuer) and protecting the financial integrity of Avista Corporation. Among other things, the commitments: require Avista Corporation to satisfy certain metrics relating to earnings, maintain a minimum percentage of common equity in its capital structure and maintain certain credit ratings, in each case as a condition to the payment of dividends; impose restrictions on intercompany loans; impose restrictions on the pledge of Avista’s utility assets; and impose requirements regarding the independence of the board and management of Avista Corporation. Such commitments may limit the ability of Hydro One Limited and its subsidiaries to obtain funds from Avista Corporation. This may limit the ability of Hydro One Limited and the Issuer to meet their payment obligations on the Debt Securities, which would have an adverse effect on the holders of the Debt Securities.

Changes in credit ratings may adversely affect the value of the Debt Securities

In connection with any offering of Debt Securities, the Issuer expects to receive a credit rating for the Debt Securities being offered from one or more credit rating agencies. Such ratings are limited in scope and may not address all material risks related to the structure of, market for, or other factors related to the value of, the Debt Securities, but rather reflect only the view of each rating agency at the time the rating is issued. There can be no assurance that the credit ratings assigned to the Debt Securities of any series will remain in effect for any given period of time or that such ratings will not be lowered, suspended or withdrawn entirely by one or more of the rating agencies if, in such rating agency’s judgment, circumstances so warrant.

In addition, credit rating agencies evaluate the industry in which Hydro One operates as a whole and may change their credit rating for Hydro One Limited or the Issuer based on their overall view of such industry. Actual or anticipated changes or downgrades in Hydro One Limited’s or the Issuer’s credit ratings, including any announcement that Hydro One Limited’s or the Issuer’s ratings are under further review for a downgrade, could affect the market value of the Debt Securities and increase corporate borrowing costs for the Issuer.

- 9 -

Table of Contents

The rights of holders of Debt Securities may change

Holders of Debt Securities will be bound by the terms and conditions of the Indenture. The terms and conditions of the Indenture may, however, be amended in certain circumstances, including with the approval of a majority of holders of outstanding Debt Securities of any series being affected.

No existing trading market

The Debt Securities will constitute a new issue of securities for which there is no existing trading market. The Issuer does not intend to list the Debt Securities on any securities exchange or any automated quotation system. Accordingly, there can be no assurance that a trading market for the Debt Securities will ever develop or will be maintained. If a trading market does not develop or is not maintained, it may be difficult or impossible to resell the Debt Securities. Further, there can be no assurance as to the liquidity of any market that may develop for the Debt Securities, the ability of any purchaser to sell the Debt Securities or the price at which a purchaser will be able to sell the Debt Securities. Further, trading prices of the Debt Securities will depend on many factors, including prevailing interest rates, financial condition and results of operations of Hydro One Limited, the then-current credit ratings assigned to the Debt Securities and the markets for similar securities.

Prevailing yields on similar securities

The prevailing yield on debt securities with comparable maturities will affect the market value of the Debt Securities. Assuming all other factors remain unchanged, the market value of the Debt Securities will decline as prevailing yields for similar securities rise and will increase as prevailing yields for similar securities decline. Fluctuations in prevailing yields may also impact borrowing costs of the Issuer which may adversely affect its creditworthiness. It is impossible to predict whether prevailing rates will rise or fall.

Risk of optional redemption

The Issuer may elect to redeem the Debt Securities prior to their maturity (to the extent the terms of the Debt Securities provide for optional redemption prior to maturity), in whole or in part, at any time or from time to time, especially when prevailing interest rates are lower than the rate borne by the Debt Securities. If prevailing interest rates are lower than the interest rate borne by the Debt Securities at the time of redemption, a purchaser may not be able to reinvest the redemption proceeds in a comparable security at an effective interest rate that is at least equal to the interest rate on the Debt Securities being redeemed. See “Description of Debt Securities – Optional Redemption”.

Potential difficulties in enforcing civil liabilities outside Canada

Each of the Issuer and Hydro One Limited is incorporated under the laws of Ontario, Canada and substantially all of the Issuer’s and Hydro One Limited’s assets are currently located in Canada. Substantially all of the directors and officers of each of the Issuer and Hydro One Limited, and some of the experts named in the Prospectus, are non-U.S. residents, and a substantial portion of the assets of each of the Issuer, Hydro One Limited and such experts named in the Prospectus are located outside of the U.S. Each of the Issuer and Hydro One Limited agree, in accordance with the terms of the Indenture, to accept service of process in any suit, action or proceeding with respect to the Indenture or any Debt Securities brought in any federal or state court located in New York City by an agent designated for such purpose, and to submit to the jurisdiction of such courts in connection with such suits, actions or proceedings. Nevertheless, it may be difficult for holders of Debt Securities to effect service of process within the U.S. upon directors, officers and experts who are not residents of the U.S. or to realize in Canada upon judgments of courts of the U.S. predicated upon civil liability under U.S. federal or state securities laws or other laws of the U.S.

- 10 -

Table of Contents

Canadian bankruptcy and insolvency laws may impair the Trustees’ ability to enforce remedies under the Indenture or the Debt Securities

The right of the Trustees to enforce remedies under the Indenture and the Debt Securities could be delayed by the provisions of applicable Canadian federal bankruptcy, insolvency and other restructuring legislation if the benefit of such legislation is sought with respect to the Issuer and/or Hydro One Limited. Canadian federal bankruptcy, insolvency and other restructuring legislation (including certain provisions of corporate statutes) contain provisions enabling an obligor to prepare and file a restructuring proposal for consideration by all or some of its creditors, to be voted on by the various classes of creditors affected thereby. A restructuring proposal may have the effect of compromising the obligations under the outstanding Debt Securities. A restructuring proposal, if accepted by the requisite majorities of each affected class of creditors, and if approved by the relevant Canadian court, would be binding on all creditors within each affected class of securities, including those creditors that did not vote to accept the proposal. Moreover, such legislation, in certain circumstances, permits the insolvent debtor to retain possession and administration of its property, subject to court oversight, even though it may be in default under the applicable debt instrument, during the period that the stay against proceedings remains in place. Canadian federal bankruptcy, insolvency and other restructuring legislation also contemplate the granting of super priority security interests or charges on the assets of the debtor company to secure the repayment of any amounts to be borrowed to facilitate the insolvency proceeding, any amounts owing for the fees and costs of professionals involved in the insolvency proceeding, obligations of directors of the company with respect to their statutory liabilities and sometimes other amounts.

The powers of the court under the Bankruptcy and Insolvency Act (Canada), and particularly under the Companies Creditors Arrangement Act (Canada), have been interpreted and exercised broadly so as to protect a restructuring entity from actions taken by creditors and other parties. Accordingly, neither the Issuer nor Hydro One Limited can predict whether payments under the outstanding Debt Securities would be made during any proceedings in bankruptcy, insolvency or other restructuring, whether or when the Trustees could exercise their rights under the Indenture or whether and to what extent holders of the Debt Securities would be compensated for any compromise of obligations or any delays in payment, if any, of principal, premium, Additional Amounts (as defined below) or interest.

There have been no material changes in Hydro One Limited’s share and loan capital, on a consolidated basis, since the date of the Interim Financial Statements, other than as noted below.

Since September 30, 2018, Hydro One Inc. has repaid $750,000,000 of its maturing long-term debt under its medium term notes program and has issued approximately $720,000,000 and repaid approximately $265,000,000 in commercial paper.

The net proceeds of any offering of Debt Securities will be used for the purposes set forth in the applicable Prospectus Supplement, including financing, directly or indirectly, or refinancing previously incurred indebtedness incurred to pay the purchase price payable for the Merger pursuant to the terms of the Agreement and Plan of Merger dated as of July 19, 2017 among Hydro One Limited, Olympus Holding Corp., Olympus Corp. (an indirect wholly-owned subsidiary of the Issuer) and Avista Corporation.

- 11 -

Table of Contents

The cash purchase price of the Merger and the Merger-related costs are expected to be financed at the closing of the Merger with a combination of some or all of the following sources: (i) net proceeds of the first instalment from the sale in August 2017 of $1.54 billion aggregate principal amount of 4.00% convertible unsecured subordinated debentures of Hydro One Limited represented by instalment receipts; (ii) net proceeds of any offering of Debt Securities pursuant to a Prospectus Supplement; (iii) amounts drawn under the existing $250 million operating credit facility of Hydro One Limited; (iv) amounts drawn under a non-revolving equity bridge loan agreement entered into between 2587264 Ontario Inc., a wholly owned subsidiary of Hydro One Limited, and a financial institution in an aggregate principal amount of $1 billion; (v) amounts drawn under a non-revolving debt bridge credit agreement entered into between the Issuer, Hydro One Limited, as guarantor, and certain financial institutions in an aggregate principal amount of US$2.6 billion; (vi) net proceeds of any offering of securities pursuant to a prospectus supplement to Hydro One Limited’s short form base shelf prospectus dated June 18, 2018; and (vii) existing cash on hand and other sources available to Hydro One.

Earnings coverage ratios will be provided as required in the applicable Prospectus Supplement with respect to any offering and sale of Debt Securities pursuant to this Prospectus.

- 12 -

Table of Contents

The Debt Securities offered hereby may be sold by the Issuer: (i) to, or through, underwriters, dealers or agents purchasing as principal or acting as agent; (ii) directly to one or more purchasers; or (iii) through a combination of any of these methods of sale. The Debt Securities may be sold at fixed prices or non-fixed prices, such as prices determined by reference to the prevailing price of the Debt Securities in a specified market, at market prices prevailing at the time of sale or at prices to be negotiated with purchasers, which prices may vary as between purchasers and during the period of distribution of the Debt Securities.

A Prospectus Supplement relating to a particular offering of Debt Securities will identify each underwriter, dealer or agent, as the case may be, engaged by the Issuer in connection with the offering and sale of the Debt Securities, and will set forth the terms of the offering of the Debt Securities, including the public offering price of such Debt Securities (or the manner of determination thereof if offered on a non-fixed price basis), the method of distribution of such Debt Securities, including, to the extent applicable, the proceeds to, and the portion of expenses borne by, the Issuer from such sale, any underwriting fees, discounts or commissions and any discounts or concessions allowed, re-allowed or paid by any underwriter to other dealers and other material terms of the plan of distribution. Only underwriters, dealers or agents so named in the applicable Prospectus Supplement are deemed to be underwriters, dealers or agents, as the case may be, in connection with the Debt Securities offered thereby. Unless otherwise indicated in a Prospectus Supplement, any agent is acting on a best efforts basis for the period of its appointment.

The Debt Securities may be sold, from time to time in one or more transactions at a fixed price or prices which may be changed or at market prices prevailing at the time of sale, at prices related to such prevailing market prices or at negotiated prices. The prices at which the Debt Securities may be offered may vary between purchasers and during the period of distribution. If, in connection with the offering of Debt Securities at a fixed price or prices, the underwriters have made a bona fide effort to sell all of the Debt Securities at the initial offering price fixed in the applicable Prospectus Supplement, the public offering price may be decreased and thereafter further changed, from time to time, to an amount not greater than the initial public offering price fixed in such Prospectus Supplement, in which case the compensation realized by the underwriters will be decreased by the amount that the aggregate price paid by purchasers for the Debt Securities is less than the gross proceeds paid by the underwriters to the Issuer.

If underwriters or dealers purchase Debt Securities as principal, the Debt Securities will be acquired by the underwriters or dealers for their own account and may be resold from time to time in one or more transactions, including negotiated transactions, at a fixed public offering price or at varying prices determined at the time of sale. The obligations of the underwriters or dealers to purchase such Debt Securities will be subject to certain conditions precedent, and the underwriters or dealers will be obligated to purchase all of the Debt Securities offered pursuant to any Prospectus Supplement if any of such Debt Securities are purchased. Any public offering price and any discounts or concessions allowed, re-allowed or paid to dealers may be changed from time to time.

Underwriters, dealers and agents who participate in the distribution of the Debt Securities may be entitled under agreements which may be entered into with the Issuer and Hydro One Limited to indemnification by the Issuer and Hydro One Limited against certain liabilities, including liabilities under securities legislation, or to contribution with respect to payments which such underwriters, dealers or agents may be required to make in respect thereof. Those underwriters, dealers and agents may be customers of, engage in transactions with, or perform services for, Hydro One in the ordinary course of business.

The Debt Securities offered hereby have not been qualified for sale under the securities laws of any province or territory of Canada (other than the Province of Ontario) and, unless otherwise provided in the Prospectus Supplement relating to a particular issue of Debt Securities, will not be offered or sold, directly or indirectly, in Canada or to any resident of Canada.

- 13 -

Table of Contents

Each issue by the Issuer of Debt Securities will be a new issue of securities with no established trading market. Unless otherwise specified in a Prospectus Supplement relating to an offering of Debt Securities, such Debt Securities will not be listed on any securities or stock exchange. Any underwriters, dealers or agents to or through whom such Debt Securities are sold may make a market in such Debt Securities, but they will not be obligated to do so and may discontinue any market making at any time without notice. No assurance can be given that a trading market in any such Debt Securities will develop or as to the liquidity of any trading market for such Debt Securities.

Unless otherwise specified in a Prospectus Supplement relating to an offering of Debt Securities, in connection with any offering of Debt Securities, the underwriters, dealers or agents may over-allot or effect transactions which stabilize, maintain or otherwise affect the market price of the Debt Securities offered at levels other than those which might otherwise prevail on the open market. These transactions may be commenced, interrupted or discontinued at any time.

DESCRIPTION OF DEBT SECURITIES

The following description sets forth certain general terms and provisions of the Debt Securities. The particular terms and provisions of Debt Securities offered pursuant to any Prospectus Supplement, and the extent to which the general terms and provisions described below may apply to them, will be described in the Prospectus Supplement filed in respect of such Debt Securities. No convertible, exchangeable or exercisable securities will be offered pursuant to this Prospectus or any Prospectus Supplement.

The Issuer will deliver an undertaking to the Ontario Securities Commission whereby it will undertake to file the periodic and timely disclosure of Hydro One Limited, as guarantor of the Debt Securities, similar to the disclosure required under Item 12.1 of Form 44-101F1 – Short Form Prospectus for so long as the Debt Securities being distributed under the applicable Prospectus Supplement are issued and outstanding. For so long as the applicable requirements of Item 13.4 of National Instrument 51-102 – Continuous Disclosure Obligations (“NI 51-102”) are satisfied, the Issuer intends to comply with its filing obligations set out in the undertaking by filing the notice permitted to be filed under Item 13.4(2)(d)(ii)(A) of NI 51-102 indicating that it is relying on the continuous disclosure documents filed by Hydro One Limited and that such documents can be found for viewing in electronic format at www.sedar.com under the company profile for Hydro One Limited.

Unless otherwise specified in a Prospectus Supplement, the Debt Securities will be issued under the Indenture, as the same may be amended, restated, supplemented or replaced from time to time. A copy of the Indenture has been filed with the SEC as an exhibit to the Registration Statement of which this Prospectus is a part. The Indenture is also available on SEDAR under Hydro One Limited’s profile at www.sedar.com.

The following description of the material terms and provisions of the Debt Securities and the Indenture is only a summary and is qualified in its entirety by reference to the provisions of the Indenture.

Terms of the Debt Securities

The Debt Securities may be issued in one or more separate series and each such series will rank pari passu with each other series without discrimination, preference or priority, regardless of the actual date of issue, and with all other unsecured and unsubordinated indebtedness of the Issuer or Hydro One Limited, as guarantor. The Prospectus Supplement for a particular series of Debt Securities will disclose the specific terms of such Debt Securities for such series. Those terms may include some or all of the following:

| • | the title of such series; |

| • | any limit on the aggregate principal amount of the Debt Securities of such series; |

- 14 -

Table of Contents

| • | the person to whom any interest shall be payable if other than the person in whose name the Debt Securities of such series are registered on the regular record date for such interest payment; |

| • | the date or dates on which principal is payable or the method for determining such date or dates, and any right to change the date on which principal is payable; |

| • | the interest rate or rates, if any, or the method for determining the interest rate or rates; |

| • | the date or dates from which interest will accrue, or the method for determining such date or dates, and the dates on which interest will be payable and the manner of determination of record dates for such payments; |

| • | the right to extend the interest payment periods and, if so, the terms of any such extension; |

| • | the place or places where payments will be made; |

| • | any right of the Issuer to redeem the Debt Securities, and, if so, the terms of such redemption option; |

| • | any obligation to redeem the Debt Securities through a sinking fund or to purchase the Debt Securities through a purchase fund or at the option of the holders of such Debt Securities; |

| • | the denominations in which any Debt Securities will be issued, if other than denominations of U.S.$2,000 and any integral multiple of U.S.$1,000 in excess thereof; |

| • | the identity of each registrar, authenticating agent and/or paying agent if not the U.S. Trustee; |

| • | any index or formula used for determining principal, premium, Additional Amounts (as defined below) or interest; |

| • | the currency or currency units for which the Debt Securities may be purchased and the currency or currency units in which the principal and any premium, Additional Amounts (as defined below) and interest is payable (in each case, if other than U.S. dollars); |

| • | if the principal of, or any premium, Additional Amounts (as defined below) or interest on, any Debt Securities of such series is to be payable, at the election of the Issuer or the holder thereof, in one or more currencies or currency units other than U.S. dollars, the currency or currency units in which the principal of, or any premium, Additional Amounts (as defined below) or interest on, such Debt Securities as to which such election is made shall be payable, the periods within which and the terms and conditions upon which such election is to be made and the amount so payable (or the manner in which such amount shall be determined); |

| • | the portion of the principal payable upon acceleration of maturity, if other than the entire principal; |

| • | the circumstances in which the Issuer and/or Hydro One Limited will be required to pay Additional Amounts (as defined below) in respect of any tax, assessment or government charge in respect of the Debt Securities; |

| • | if the principal payable on the maturity date will not be determinable on one or more dates prior to the maturity date, the amount which will be deemed to be such principal amount or the manner of determining it; |

| • | whether the Debt Securities will be issuable as global securities and, if so, the depositary for such Debt Securities; |

| • | any transfer and exchange provisions of the Debt Securities of such series; |

| • | the events of default with respect to such Debt Securities; |

| • | any addition, modification or deletion in the covenants which apply to such Debt Securities; and |

| • | any other terms and conditions of the Debt Securities which are not inconsistent with applicable trust indenture legislation. |

- 15 -

Table of Contents

Amount Unlimited

The aggregate principal amount of Debt Securities which may be authenticated and delivered under the Indenture is unlimited.

Specified Denominations

Except as otherwise specified in a Prospectus Supplement, the Debt Securities will be issuable in denominations of U.S.$2,000 and any integral multiple of U.S.$1,000 in excess thereof.

Global Securities

The Issuer may issue some or all of the Debt Securities as book-entry securities. The Issuer will register each global security with or on behalf of a securities depositary. Each global security will be deposited with the securities depositary or its nominee or a custodian for the securities depositary.