UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the Fiscal Year Ended | |

OR | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the Transition Period from to

Commission File Number:

(Exact Name of Registrant as Specified in Its Charter)

(State or Other Jurisdiction of | (I.R.S. Employer |

Incorporation or Organization) | Identification No.) |

(Address of Principal Executive Offices) | (Zip Code) |

(

(Registrant’s Telephone Number, Including Area Code)

Title of Each Class |

| Trading Symbol |

| Name of Each Exchange on Which Registered |

ICAN |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ☐ | Accelerated Filer ☐ | Smaller reporting company | Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

As at May 31, 2023, the aggregate market value of the registrant’s Common Shares held by non-affiliates was approximately $

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant's definitive proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than March 29, 2024, in connection with the registrant’s 2023 annual meeting of shareholders, are incorporated herein by reference into Part III of this Annual Report on Form 10-K.

TRILOGY METALS INC.

TABLE OF CONTENTS

2

Unless the context otherwise requires, the words “we,” “us,” “our,” the “Company” and “Trilogy” refer to Trilogy Metals Inc., formerly NovaCopper Inc. (“Trilogy” or “Trilogy Metals”), a British Columbia corporation, either alone or together with its subsidiaries as the context requires, as of November 30, 2023.

CURRENCY

All dollar amounts are in United States currency unless otherwise stated. References to C$ or CDN$ refer to Canadian currency, and $ or US$ to United States currency.

FORWARD-LOOKING STATEMENTS

The information discussed in this Annual Report on Form 10-K includes “forward-looking information” and “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), and applicable Canadian securities laws. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, operating costs, cash flow estimates, production estimates and similar statements relating to the economic viability of a project, timelines, strategic plans, statements relating anticipated activity with respect to the Ambler Mining District Industrial Access Project (“Ambler Access Project” or “AAP”), the Company’s plans and expectations relating to the Upper Kobuk Mineral Projects (as defined herein), completion of transactions, market prices for precious and base metals, the results of the NI 43-101 Arctic Report and S-K 1300 Arctic Report (as defined herein), the timing of the final SEIS (as defined herein) and a Record of Decision, or other statements that are not statements of fact. These statements relate to analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management.

Statements concerning mineral resource estimates may also be deemed to constitute “forward-looking statements” to the extent that they involve estimates of the mineralization that will be encountered if the property is developed. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, identified by words or phrases such as “expects”, “is expected”, “anticipates”, “believes”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”, “potential”, “possible” or variations thereof or stating that certain actions, events, conditions or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements. Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to differ from those reflected in the forward-looking statements, including, without limitation:

| ● | risks related to inability to define proven and probable reserves; |

| ● | risks related to our ability to finance the development of our mineral properties through external financing, strategic alliances, the sale of property interests or otherwise; |

| ● | uncertainty as to whether there will ever be production at the Company’s mineral exploration and development properties; |

| ● | risks related to our ability to commence production and generate material revenues or obtain adequate financing for our planned exploration and development activities; |

| ● | risks related to lack of infrastructure including but not limited to the risk whether or not the Ambler Access Project will receive the requisite permits and, if it does, whether the Alaska Industrial Development and Export Authority (“AIDEA”) will build the AAP; |

| ● | risks related to inclement weather which may delay or hinder exploration activities at our mineral properties; |

3

| ● | risks related to our dependence on a third party for the development of our projects; |

| ● | none of the Company’s mineral properties are in production or are under development; |

| ● | commodity price fluctuations; |

| ● | uncertainty related to title to our mineral properties; |

| ● | our history of losses and expectation of future losses; |

| ● | risks related to increases in demand for equipment, skilled labor and services needed for exploration and development of mineral properties and related cost increases; |

| ● | uncertainties relating to the assumptions underlying our resource estimates, such as metal pricing, metallurgy, mineability, marketability and operating and capital costs; |

| ● | uncertainty related to inferred, indicated and measured mineral resources; |

| ● | mining and development risks, including risks related to infrastructure, accidents, equipment breakdowns, labor disputes or other unanticipated difficulties with or interruptions in development, construction or production; |

| ● | uncertainty related to successfully acquiring commercially mineable mineral rights; |

| ● | risks and uncertainties relating to the interpretation of drill results, the geology, grade and continuity of our mineral deposits; |

| ● | risks related to governmental regulation and permits, including environmental regulation, including the risk that more stringent requirements or standards may be adopted or applied due to circumstances unrelated to the Company and outside of our control; |

| ● | the risk that permits and governmental approvals necessary to develop and operate mines at our mineral properties will not be available on a timely basis or at all; |

| ● | risks related to the need for reclamation activities on our properties and uncertainty of cost estimates related thereto; |

| ● | risks related to the acquisition and integration of operations or projects; |

| ● | risks related to industry competition in the acquisition of exploration properties and the recruitment and retention of qualified personnel; |

| ● | our need to attract and retain qualified management and technical personnel; |

| ● | risks related to conflicts of interests of some of our directors and officers; |

| ● | risks related to potential future litigation; |

| ● | risks related to market events and general economic conditions; |

| ● | risks related to future sales or issuances of equity securities decreasing the value of existing Trilogy common shares (“Common Shares”), diluting voting power and reducing future earnings per share; |

| ● | risks related to the voting power of our major shareholders and the impact that a sale by such shareholders may have on our share price; |

4

| ● | uncertainty as to the volatility in the price of the Company’s Common Shares; |

| ● | the Company’s expectation of not paying cash dividends; |

| ● | adverse federal income tax consequences for U.S. shareholders should the Company be a passive foreign investment company; |

| ● | risks related to global climate change; |

| ● | risks related to adverse publicity from non-governmental organizations; |

| ● | uncertainty as to our ability to maintain the adequacy of internal control over financial reporting as per the requirements of Section 404 of the Sarbanes-Oxley Act (“SOX”); |

| ● | increased regulatory compliance costs, associated with rules and regulations promulgated by the United States Securities and Exchange Commission (“SEC”), Canadian Securities Administrators, the NYSE American, the Toronto Stock Exchange (“TSX”), and the Financial Accounting Standards Boards, and more specifically, our efforts to comply with the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”); and |

| ● | risks related to the future effects of the COVID-19 pandemic. |

This list is not exhaustive of the factors that may affect any of our forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and our actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to in this report under the heading “Risk Factors” and elsewhere.

Our forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made. In connection with the forward-looking statements contained herein, we have made certain assumptions about our business, including about:

| ● | our ability to achieve production at our Arctic and Bornite Projects (as defined herein); |

| ● | the accuracy of our mineral resource estimates; |

| ● | the results, costs and timing of future exploration drilling and engineering; |

| ● | timing and receipt of approvals, consents and permits under applicable legislation; |

| ● | the adequacy of our financial resources; |

| ● | the receipt of third party contractual, regulatory and governmental approvals for the exploration, development, construction and production of our properties; |

| ● | our expected ability to develop adequate infrastructure and that the cost of doing so will be reasonable; |

| ● | continued good relationships with South32 (as defined below), local communities and other stakeholders; |

| ● | there being no significant disruptions affecting operations, whether relating to labor, supply, power, damage to equipment or other matters; |

| ● | expected trends and specific assumptions regarding metal prices and currency exchange rates; and |

5

| ● | prices for and availability of fuel, electricity, parts and equipment and other key supplies remaining consistent with current levels. |

We have also assumed that no significant events will occur outside of our normal course of business. Although we have attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. We believe that the assumptions inherent in the forward-looking statements are reasonable as of the date hereof. However, forward-looking statements are not guarantees of future performance and, accordingly, undue reliance should not be put on such statements due to the inherent uncertainty therein. We do not assume any obligation to update forward-looking statements if circumstances or management’s beliefs, expectations or opinions should change, except as required by law. For the reasons set forth above, investors should not place undue reliance on forward-looking statements. All forward-looking statements contained herein are qualified by these cautionary statements.

TECHNICAL INFORMATION

Richard Gosse, a Qualified Person under NI 43-101 and S-K 1300 (as defined herein) and an employee and Vice President Exploration of the Company has reviewed and approved the scientific and technical information contained in this Annual Report on Form 10-K.

PART I

Item 1. BUSINESS

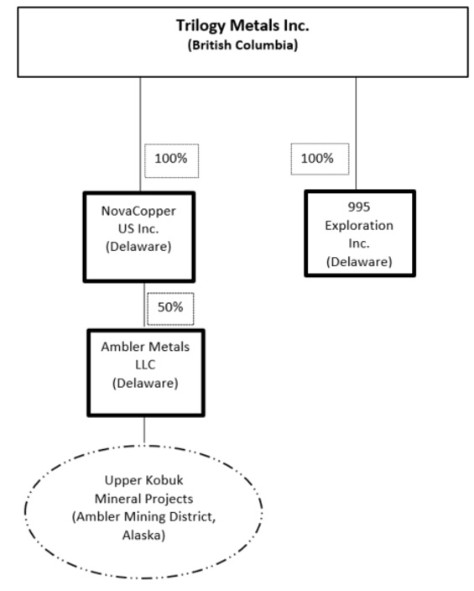

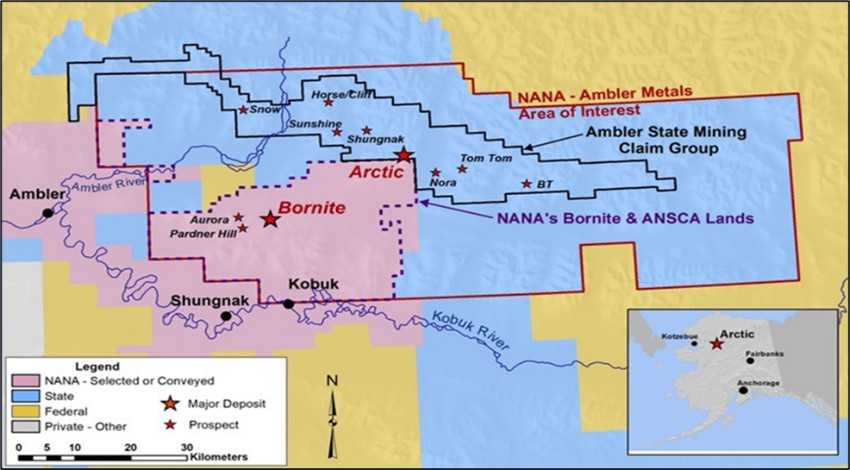

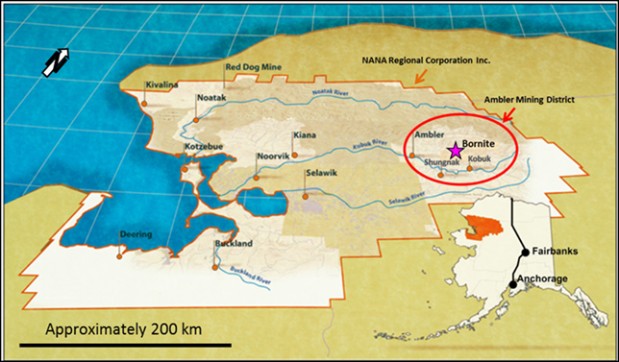

Our principal business is the exploration and development of the Upper Kobuk Mineral Projects (“Upper Kobuk Mineral Projects” or “UKMP” or “UKMP Projects”) located in the Ambler Mining District in Northwest Alaska, United States. The Upper Kobuk Mineral Projects are held by Ambler Metals LLC (“Ambler Metals”), a limited liability company owned equally by Trilogy and South32 Limited (“South32”), and is comprised of the (i) Arctic Project, which contains a high-grade polymetallic volcanogenic massive sulfide (“VMS”) deposit (“Arctic Project”); and (ii) Bornite Project, which contains a carbonate-hosted copper - cobalt deposit (“Bornite Project”). Our goals include expanding mineral resources and advancing the UKMP Projects through technical, engineering and feasibility studies so that production decisions can be made on those projects. Our interest in Ambler Metals is held by a wholly-owned subsidiary, NovaCopper US Inc. (dba Trilogy Metals US) (“Trilogy Metals US”), registered to do business in the State of Alaska. We also conduct early-stage exploration through a wholly owned subsidiary, 995 Exploration Inc.

Name, Address and Incorporation

Trilogy Metals Inc. was incorporated on April 27, 2011 under the name NovaCopper Inc. pursuant to the terms of the Business Corporations Act (British Columbia). NovaCopper Inc. changed its name to Trilogy Metals Inc. on September 1, 2016 to better reflect its diversified metals resource base. Our registered office is located at Suite 2600, Three Bentall Centre, 595 Burrard Street, Vancouver, British Columbia, Canada, and our executive office is located at Suite 1150, 609 Granville Street, Vancouver, British Columbia, Canada.

6

Corporate Organization Chart

The following chart depicts our corporate structure together with the jurisdiction of incorporation of our subsidiaries at November 30, 2023. All ownership is 100% unless otherwise stated.

On February 11, 2020, the Company’s Upper Kobuk Mineral Projects were transferred to Ambler Metals, a newly incorporated limited liability company incorporated under the laws of Delaware. Each of Trilogy and South32 hold a 50% interest in Ambler Metals. All mineral resources and mineral reserve estimates with respect to the Arctic Project and Bornite Project that are disclosed in this Annual Report on Form 10-K are reported on a 100% basis unless otherwise noted.

Business Cycle

Our business, at its current exploration phase, is cyclical. Exploration activities are conducted primarily during snow-free months in Alaska. The optimum field season at the Upper Kobuk Mineral Projects is from late May to late September. The length of the snow-free season at the Upper Kobuk Mineral Projects varies from about May through November at lower elevations and from July through September at higher elevations.

Trilogy’s Strategy

Our business strategy is focused on creating value for stakeholders through our ownership and advancement of the Arctic Project and exploration and advancement of the Bornite Project with our joint venture partner, South32, and through the pursuit of similarly attractive mining projects. We plan to:

| ● | advance the Arctic Project towards development with key activities including increased definition of the NI 43-101 and S-K 1300 mineral resources and reserves contained in the Arctic FS, additional metallurgical and geotechnical studies and the advancement of baseline environmental studies; |

7

| ● | advance exploration in the Ambler Mining District and, in particular, at the Bornite Project, pursuant to the NANA Agreement (as more particularly described under “History of Trilogy – Agreement with NANA Regional Corporation”) through resource development and initial technical studies; and |

| ● | pursue project level or corporate transactions that are value accretive. |

Significant Developments in 2023

| ● | On January 25, 2023, the Company announced the second set of drilling results from the 2022 field season at the Upper Kobuk Mineral Projects and on February 27, 2023, the Company announced the third set of drilling results from the 2022 field season at the UKMP. |

| ● | On February 14, 2023, the Company announced an updated feasibility study technical report for the Arctic Project and an updated resource for the Bornite Project, and filed NI 43-101 technical reports for both projects with the Canadian securities regulators. In addition, the Company announced technical report summaries for both projects prepared in accordance with S-K 1300 and which were filed as exhibits with the annual report on Form 10-K. |

| ● | On April 25, 2023, the Company completed non-brokered private placement of 5,854,545 Common Shares at a price of $0.55 per Common Share for gross proceeds of $3.2 million. After legal and stock exchange fees, the Company received net proceeds of $3.1 million. |

| ● | On September 11, 2023 the Company provided an update on the activities at the UKMP with the Bornite camp opening. |

| ● | On October 19, 2023, the Company announced that the United States Bureau of Land Management’s (“BLM”) had filed the draft Supplemental Environmental Impact Statement (“SEIS”) on its website https://eplanning.blm.gov/eplanning-ui/project/57323/570 and anticipated being in the federal register on October 20, 2023. The draft SEIS was open for a 60-day public comment period, until December 19, 2023. The BLM reconfirmed they anticipate a final SEIS is expected in the first quarter of 2024, and a Record of Decision within the second quarter of 2024. |

Significant Developments in 2022

| ● | On January 11, 2022, the Company announced the 2022 program and budget of approximately $28.5 million for the advancement of the UKMP located in Northwestern Alaska. The budget was 100% funded by Ambler Metals. |

| ● | On January 20, 2022, the Company announced an updated mineral resource for the Bornite Project. |

| ● | On February 7, 2022, the Company announced that the AIDEA had formally approved the proposed plan and budget for the 2022 summer field season activities and services of up to $30.8 million for the Ambler Access Project. The cost was shared 50/50 by AIDEA and Ambler Metals. |

| ● | On February 23, 2022, the Company announced that the United States Department of the Interior (“DOI”) filed a motion to remand the Final Environmental Impact Statement (“FEIS”) and suspend the right-of-way permits issued to AIDEA for the Ambler Access Project. The DOI has stated that the suspension of the road permits will allow it to carry out additional supplemental work on the FEIS. The motion also indicated that the DOI has requested that the lawsuits filed against the DOI by a coalition of national and Alaska environmental non-government organizations be suspended. The lawsuits had been filed in response to the BLM issuance of the Joint Record of Decision (“JROD”), that authorized a right-of-way across federally managed lands for AIDEA and the AAP. |

8

| ● | On June 8, 2022, the Company announced that Ambler Metals had commenced mobilization for the upcoming exploration field program at the UKMP. |

| ● | On September 21, 2022, the Company announced that the BLM had published in the Federal Register a Notice of Intent (“NOI”) that it will prepare the SEIS for the proposed Ambler Mining District Industrial Access Road. The NOI indicates that: |

| ● | The BLM will accept comments related to the SEIS for 45 days so that the BLM can determine which, if any, additional impacts and resources related to identified deficiencies should be more thoroughly assessed to facilitate integrating the BLM’s National Environmental Policy Act (“NEPA”) analysis with its ongoing Alaska National Interest Lands Conservation Act Section 810 and National Historic Preservation Act Section 106 processes; |

| ● | Input by Alaska Native Tribes and Corporations will continue to be of critical importance and that BLM will continue to consult with these entities under applicable guidance; and |

| ● | Preparation of the SEIS in compliance with NEPA will additionally help the BLM to fulfill its obligations under applicable law. |

| ● | On November 23, 2022, the Company announced that the BLM submitted a status report in accordance with the Voluntary Remand dated May 17, 2022 stating that the comment period ended on November 4, 2022 for the scoping process of the SEIS and that the BLM currently anticipates publishing a draft SEIS during the second quarter of calendar year 2023, which will be open for public comment upon publication. The BLM also anticipates publishing a final SEIS, conducting final pre-decision consultation with Alaska Native Tribes and Corporations, and issuing a Record of Decision, all within the fourth quarter of calendar year 2023. |

Significant Developments in 2021

| ● | On January 6, 2021, the BLM, the National Park Service and the AIDEA signed Right-of-Way agreements giving AIDEA the ability to cross federally owned and managed lands along the route for the Ambler Road Project approved in the Joint Record of Decision. The agreements grant a 50-year right-of-way on federally owned and managed land by the federal agencies for the future development of the Ambler Mining District Industrial Access Road. The authorizing documents with the two agencies are the final federal permits required for the Ambler Road Project. |

| ● | In a press release dated February 11, 2021, the Company announced its approval for Ambler Metals to enter into an Ambler Access Development Agreement (the “Development Agreement”) with AIDEA. The Development Agreement defines how AIDEA and Ambler Metals will work cooperatively together on the pre-development work for the Ambler Access Project to address funding and oversight of the project’s feasibility and permitting activities until the parties reach a decision on the construction of the project. The cost of the pre-development work and activities will be paid 50% by AIDEA and 50% by Ambler Metals based on an annually agreed program and budget. Under the Development Agreement, Ambler Metals and AIDEA agree to contribute up to $35 million each for pre-development costs of the Ambler Access Project through December 31, 2024. |

| ● | In a press release dated April 19, 2021, the Company announced that the AIDEA had formally approved the proposed plan and budget for the 2021 summer field season activities and services of up to $13 million for the Ambler Access Project. The cost was to be shared 50/50 by AIDEA and Ambler Metals. The Board of AIDEA authorized up to $6.5 million for field season activities. These funds were to be matched by up to another $6.5 million from Ambler Metals under the terms of the Ambler Access Development Agreement that was approved by the AIDEA Board on February 10, 2021 and subsequently executed by both parties, resulting in a total budget for 2021 of up to $13 million. The AAP is a proposed 211-mile, east-west running controlled industrial access road that would provide industrial access to the Ambler Mining District in northwestern Alaska. |

9

| ● | In a press release dated May 17, 2021, the Company announced that Ambler Metals had finalized the details of the 2021 exploration field program at the UKMP for the previously approved $27 million exploration budget. The exploration program was aligned with a strategy developed by the Company and South32 which prioritizes the exploration budget within the UKMP. The strategy defines a program that advances the highest priority projects and exploration targets, both VMS and Carbonate-Hosted Copper (“CHC”), ranging from early-stage geophysical anomalies that were identified during the 2019 airborne Versatile Time Domain Electromagnetic (“VTEM”) survey to advanced VMS and CHC prospects with historical resources. The site camp opened on June 1, 2021. |

History of Trilogy

Spin-Out

We were formerly a wholly-owned subsidiary of NovaGold Resources Inc. (“NovaGold”). In April 2012, Trilogy Common Shares were distributed to NovaGold shareholders pursuant to a Plan of Arrangement under the Companies Act (Nova Scotia) and were listed and posted for trading on the TSX and on the NYSE American.

Name Change

We changed our corporate name to Trilogy Metals Inc. from NovaCopper Inc. in 2016 to better reflect the diversity of minerals at our UKMP Projects. On September 8, 2016, upon the opening of the markets our shares began trading on the TSX and the NYSE American under the symbol “TMQ”.

Agreement with NANA Regional Corporation

On October 19, 2011, NANA Regional Corporation, Inc. (“NANA”), an Alaska Native Corporation headquartered in Kotzebue, Alaska, and Trilogy Metals US entered an Exploration Agreement and Option Agreement (as amended, the “NANA Agreement”) for the cooperative development of NANA’s respective resource interests in the Ambler Mining District of Northwest Alaska. Upon the formation of Ambler Metals, the Company assigned its rights and obligations under the NANA Agreement to Ambler Metals. The NANA Agreement consolidates Ambler Metals’ and NANA’s land holdings into an approximately 142,831-hectare land package and provides a framework for the exploration and any future development of this high-grade and prospective poly-metallic belt.

The NANA Agreement grants Ambler Metals the nonexclusive right to enter on, and the exclusive right to explore, the Bornite lands and the Alaska Native Claims Settlement Act (“ANCSA”) lands (each as defined in the NANA Agreement) and in connection therewith, to construct and utilize temporary access roads, camps, airstrips and other incidental works. In consideration for this right, Trilogy Metals US previously paid to NANA $4 million in cash. Ambler Metals is also required to make payments to NANA for scholarship purposes in accordance with the terms of the NANA Agreement. Ambler Metals has further agreed to use reasonable commercial efforts to train and employ NANA shareholders to perform work for Ambler Metals in connection with its operations on the Bornite lands, ANCSA lands and Ambler lands (as defined in the NANA Agreement) (collectively, the “Lands”). The NANA Agreement has a term of 20 years, with an option in favour of Ambler Metals to extend the term for an additional 10 years. The NANA Agreement may be terminated by mutual agreement of the parties or by NANA if Ambler Metals does not meet certain expenditure requirements on the Bornite lands and ANCSA lands.

If, following receipt of a feasibility study and the release for public comment of a related draft environmental impact statement, Ambler Metals decides to proceed with construction of a mine on the Lands, Ambler Metals will notify NANA in writing and NANA will have 120 days to elect to either (a) exercise a non-transferrable back-in-right to acquire an undivided ownership interest between 16% and 25% (as specified by NANA) of that specific project; or (b) not exercise its back-in-right, and instead receive a net proceeds royalty equal to 15% of the net proceeds realized by Ambler Metals from such project (following the recoupment by Ambler Metals of all costs incurred, including operating, capital and carrying costs). The cost to exercise such back-in-right is equal to the percentage interest in the project multiplied by the difference between (i) all costs incurred by Ambler Metals or its affiliates on the project, including historical costs

10

incurred prior to the date of the NANA Agreement together with interest on the costs; and (ii) $40 million (subject to exceptions). This amount will be payable by NANA to Ambler Metals in cash at the time the parties enter into a joint venture agreement and in no event will the amount be less than zero.

In the event that NANA elects to exercise its back-in-right, the parties will as soon as reasonably practicable form a joint venture, with NANA’s interest being between 16% to 25% and Ambler Metals owning the balance of the interest in the joint venture. Upon formation of the joint venture, the joint venture will assume all of the obligations of Ambler Metals and be entitled to all the benefits of Ambler Metals under the NANA Agreement in connection with the mine to be developed and the related Lands. A party’s failure to pay its proportionate share of costs in connection with the joint venture will result in dilution of its interest. Each party will have a right of first refusal over any proposed transfer of the other party’s interest in the joint venture other than to an affiliate or for the purposes of granting security. A transfer by either party of any net proceeds royalty interest in a project other than for financing purposes will also be subject to a first right of refusal. A transfer of NANA’s net smelter return on the Lands is subject to a first right of refusal by Ambler Metals.

In connection with possible development of a mine on the Bornite lands or ANCSA lands, Ambler Metals and NANA will execute a mining lease to allow Ambler Metals or the joint venture to construct and operate a mine on the Bornite lands or ANCSA lands. These leases will provide NANA a 2% net smelter royalty as to production from the Bornite lands and a 2.5% net smelter royalty as to production from the ANCSA lands. If Ambler Metals decides to proceed with construction of a mine on the Ambler lands, NANA will enter into a surface use agreement with Ambler Metals which will afford Ambler Metals access to the Ambler lands along routes approved by NANA on the Bornite lands or ANCSA lands. In consideration for the grant of such surface use rights, Ambler Metals will grant NANA a 1% net smelter royalty on production and an annual payment of $755 per acre as adjusted for inflation each year beginning with the second anniversary of the effective date of the NANA Agreement and for each of the first 400 acres (and $100 for each additional acre) of the lands owned by NANA and used for access which are disturbed and not reclaimed.

Ambler Metals has formed an oversight committee with NANA, which consists of four representatives from each of Ambler Metals and NANA (the “Oversight Committee”). The Oversight Committee is responsible for certain planning and oversight matters carried out by us under the NANA Agreement. The planning and oversight matters that are the subject of the NANA Agreement will be determined by majority vote. The representatives of each of Ambler Metals and NANA attending a meeting will have one vote in the aggregate and in the event of a tie, the Ambler Metals representatives jointly shall have a deciding vote on all matters other than Subsistence Matters, as that term is defined in the NANA Agreement. There shall be no deciding vote on Subsistence Matters and Ambler Metals may not proceed with such matters unless approved by majority vote of the Oversight Committee or with the consent of NANA, such consent not to be unreasonably withheld or delayed.

Principal Markets

We do not currently have a principal market. Our principal objective is to become a producer of copper.

Specialized Skill and Knowledge

All aspects of our business require specialized skills and knowledge. Such skills and knowledge include the areas of geology, mining and accounting. See “Executive Officers of Trilogy” for details as to the specific skills and knowledge of our directors and management.

Environmental Protection

Mining is an extractive industry that impacts the environment. Along with our joint venture partner, South32, our goal is to evaluate ways to minimize that impact and to develop safe, responsible and profitable operations by developing natural resources for the benefit of our employees, shareholders and communities and maintain high standards for environmental performance at the UKMP Projects. We strive to meet or exceed environmental standards at the UKMP Projects. One way Ambler Metals does this is through collaborations with local communities in Alaska, including Native

11

Alaskan groups. Ambler Metals’ environmental performance will be overseen at the Ambler-board and Trilogy-board level and environmental performance is the responsibility of the project manager. All new activities and operations will be managed for compliance with applicable laws and regulations. In the absence of regulation, best management practices will be applied to manage environmental risk. Furthermore, we will strive to limit releases to the air, land or water and appropriately treat and dispose of waste.

For a more detailed discussion of the various government laws and regulations applicable to our operations and potential negative effects of these laws and regulations, see Item 1A. Risk Factors, and Item 2 Properties, Environmental, Permitting, Social and Closure Considerations below.

Employees

As of November 30, 2023, we had 5 full-time employees, all except our CEO, were employed at our executive office in Vancouver, BC. We have entered into executive employment agreements with the CEO and CFO (each as defined herein).

Information About Our Executive Officers

As of November 30, 2023, we had two executive officers, namely Tony Giardini and Elaine Sanders. The following information is presented as of November 30, 2023.

Name and Residence |

| Age |

| Held Office Since |

| Business Experience During Past Five Years | ||

Tony Giardini | 64 | June 1, 2020(1) | Chief Executive Officer of Trilogy (2020 – present); President of Ivanhoe Mines Ltd. (May 2019 – March 2020); Chief Financial Officer of Kinross Gold Corporation (December 2012 - April 2019) | |||||

Elaine Sanders | 54 | January 30, 2012(2) | Vice President and Chief Financial Officer of Trilogy (2012 – present); Corporate Secretary of Trilogy (2011 – present) |

| (1) | Mr. Giardini was appointed President and Chief Executive Officer on June 1, 2020. |

| (2) | Ms. Sanders was appointed Chief Financial Officer on January 30, 2012. She became a full-time employee of the Company on November 13, 2012. |

Competitive Conditions

The mineral exploration and development industry is competitive in all phases of exploration, development and production. There is a high degree of competition faced by us in Alaska and elsewhere for skilled management employees, suitable contractors for drilling operations, technical and engineering resources, and necessary exploration and mining equipment, and many of these competitor companies have greater financial resources, operational expertise, and/or more advanced properties than us. Additionally, our operations are in a remote location where skilled resources and support services are limited. We have in place experienced management personnel and continue to evaluate the required expertise and skills to carry out our operations. As a result of this competition, we may be unable to achieve our exploration and development in the future on terms we consider acceptable or at all. See “Item 1A. Risk Factors.”

Available Information

We make available, free of charge, on or through our website, at www.trilogymetals.com our Annual Report on Form 10-K, which includes our audited financial statements, our Quarterly Reports on Form 10-Q, and our Current Reports on

12

Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. The SEC maintains a website that contains reports, proxy and information statements, and other information at www.sec.gov. Our website and the information contained therein or connected thereto are not intended to be, and are not incorporated into this Annual Report on Form 10-K.

Item 1A. RISK FACTORS

Investing in our securities is speculative and involves a high degree of risk due to the nature of our business and the present stage of exploration of our mineral properties. The following risk factors, as well as risks currently unknown to us, could materially adversely affect our future business, operations and financial condition and could cause them to differ materially from the estimates described in forward-looking information relating to Trilogy, or our business, property or financial results, each of which could cause purchasers of securities to lose all or part of their investments.

Risks Related to the future of the COVID Pandemic

The outbreak of the coronavirus (COVID-19) may affect our operations.

The Company faces risks related to health epidemics and other outbreaks of communicable diseases, which could significantly disrupt its operations and may materially and adversely affect its business and financial conditions.

The Company’s business could be adversely impacted by the effects of the coronavirus or other epidemics. In December 2019, a novel strain of the coronavirus (“COVID-19”) emerged in China and the virus has now spread around the world, including Canada and the U.S. The extent to which COVID-19 impacts the Company’s business, including exploration and development activities at Ambler Metals and the market for its securities, will depend on future developments, which are uncertain and cannot be predicted at this time, and include the duration, severity and scope of the outbreak and the actions taken to contain or treat the coronavirus outbreak. In particular, the continued spread of the coronavirus and travel and other restrictions established to curb the spread of the COVID-19, has and could continue to materially and adversely impact the Company’s business including without limitation, the planned exploration programs at Ambler Metals, employee health, workforce productivity, increased insurance premiums, limitations on travel, the availability of industry experts and personnel, the timing to process drill and other metallurgical testing, interruption of supplies from third parties upon which the Company relies and other factors that will depend on future developments beyond the Company’s control, which may have a material and adverse effect on the its business, financial condition and results of operations.

There can be no assurance that the Company's personnel will not be impacted by these pandemic diseases and ultimately see its workforce productivity reduced or incur increased medical costs or insurance premiums as a result of these health risks.

Risks Related to the Company’s Mineral Properties

We may not have sufficient funds to develop our mineral projects or to complete further exploration programs.

We have limited financial resources. We currently generate no mining operating revenue and must primarily finance exploration activity and the development of mineral projects by other means. Although South32 funded Ambler Metals in the amount of US$145 million upon formation of the joint venture in 2020, in the future, once our share of such amount has been expended or we wish to acquire any other properties outside of Ambler Metals, our ability to continue exploration, development and production activities, if any, will depend on our ability to obtain additional external financing. Any unexpected costs, problems or delays could severely impact our ability to continue exploration and development activities. The failure to meet ongoing obligations on a timely basis could result in a loss or a substantial dilution of our interests in projects.

The sources of external financing that we may use for these purposes include project or bank financing or public or private offerings of equity and debt. In addition, we may enter into one or more strategic alliances or joint ventures, in

13

addition to our joint venture with South32, sell marketable securities held by the Company, decide to sell certain property interests, or utilize one or a combination of all of these alternatives. The financing alternative we choose may not be available on acceptable terms, or at all. If additional financing is not available, we may have to postpone further exploration or development of, or sell our interest in, one or more of our principal properties.

Even if one of our mineral projects is determined to be economically viable to develop into a mine, such development may not be successful.

If the development of one of our projects is found to be economically feasible and approved by our board of directors (the “Board”) and in the case of the UKMP Projects, by our joint venture partner, South32, such development will require obtaining permits and financing, the construction and operation of mines, processing plants and related infrastructure, including road access. As a result, we are and will continue to be subject to all of the risks associated with establishing new mining operations, including:

| ● | the timing and cost, which can be considerable, of the construction of mining and processing facilities and related infrastructure; |

| ● | the availability and cost of skilled labor and mining equipment; |

| ● | the availability and cost of appropriate smelting and refining arrangements; |

| ● | the need to obtain necessary environmental and other governmental approvals and permits and the timing of the receipt of those approvals and permits; |

| ● | the availability of funds to finance construction and development activities; |

| ● | potential opposition from non-governmental organizations, environmental groups or local groups which may delay or prevent development activities; and |

| ● | potential increases in construction and operating costs due to changes in the cost of fuel, power, materials and supplies. |

The costs, timing and complexities of developing our projects may be greater than anticipated because our property interests are not located in developed areas, and, as a result, our property interests are not currently served by appropriate road access, water and power supply and other support infrastructure. Cost estimates may increase significantly as more detailed engineering work is completed on a project. It is common in new mining operations to experience unexpected costs, problems and delays during construction, development and mine start-up. In addition, delays in the early stages of mineral production often occur. Accordingly, we cannot provide assurance that we will ever achieve, or that our activities will result in, profitable mining operations at the UKMP Projects or any other property that we may acquire.

In addition, there can be no assurance that our mineral exploration activities will result in any discoveries of new mineralization. If further mineralization is discovered there is also no assurance that the mineralization would be economical for commercial production. Discovery of mineral deposits is dependent upon a number of factors and significantly influenced by the technical skill of the exploration personnel involved. The commercial viability of a mineral deposit is also dependent upon a number of factors which are beyond our control, including the attributes of the deposit, commodity prices, government policies and regulation and environmental protection.

14

The Upper Kobuk Mineral Projects are located in a remote area of Alaska, and access to them is limited. Exploration and any future development or production activities may be limited and delayed by infrastructure challenges, inclement weather and a shortened exploration season.

We cannot provide assurances that the proposed AAP that would provide access to the Ambler Mining District will be built, that it will be built in a timely manner, that the cost of accessing the proposed road will be reasonable, that it will be built in the manner contemplated, or that it will sufficiently satisfy the requirements of the Upper Kobuk Mineral Projects. The proposed AAP requires significant permitting and approvals, and the JROD issued in 2020 is currently subject to lawsuits which could delay or prevent the project. Further, changes in the U.S. federal administration may result in changes in interpretations or priorities which may further delay or prevent the proposed AAP.

In addition, successful development of the Upper Kobuk Mineral Projects will require the development of the necessary infrastructure. If adequate infrastructure is not available in a timely manner, there can be no assurance that:

| ● | the development of the Upper Kobuk Mineral Projects will be commenced or completed on a timely basis, if at all; |

| ● | the resulting operations will achieve the anticipated production volume; or |

| ● | the construction costs and operating costs associated with the development of the Upper Kobuk Mineral Projects will not be higher than anticipated. |

As the Upper Kobuk Mineral Projects are located in a remote area, exploration, development and production activities may be limited and delayed by inclement weather and a shortened exploration season. The exploration of the UKMP Projects has also been impacted by COVID-19. See “Risks Related to the future of COVID-19” above.

We are dependent on a third party that participates in exploration and development of our Upper Kobuk Mineral Projects.

In December 2019, South32 exercised its option to acquire a 50% interest in Ambler Metals. The formation of Ambler Metals was completed in February 2020 and Ambler Metals now owns the Upper Kobuk Mineral Projects. Our success with respect to the Upper Kobuk Mineral Projects depends on the efforts and expertise of South32 with whom we have contracted; we hold a 50% interest and the remaining 50% interest is held by South32, who is not under our control or direction. We are dependent on them for the progress and development of the Upper Kobuk Mineral Projects. South32 may also have different priorities which could impact the timing and cost of development of the Upper Kobuk Mineral Projects. The third party may also be in default of its agreement with us, without our knowledge, which may put the mineral property and related assets at risk. The existence or occurrence of one or more of the following circumstances and events could have a material adverse impact on our ability to achieve our business plan, profitability, or the viability of our interests held with the third party, which could have a material adverse impact on our business, future cash flows, earnings, results of operations and financial condition: (i) disagreement with our business partner on how to develop and operate the Upper Kobuk Mineral Projects efficiently; (ii) inability to exert influence over certain strategic decisions made in respect of the jointly-held Upper Kobuk Mineral Projects; (iii) inability of our business partner to meet its obligations to the joint business or third parties; and (iv) litigation with our business partner regarding joint business matters.

We have no history of production and no revenue from mining operations.

We have a very limited history of operations and to date have generated no revenue from mining operations. As such, we are subject to many risks common to such enterprises, including under-capitalization, cash shortages, limitations with respect to personnel, financial and other resources and lack of significant revenues. There is no assurance that the Upper Kobuk Mineral Projects, or any other future projects will be commercially mineable, and we may never generate revenues from our mining operations.

15

Changes in the market price of copper, zinc and other metals, which in the past have fluctuated widely, will affect our ability to finance continued exploration and development of our projects and affect our operations and financial condition.

Our long-term viability will depend, in large part, on the market price of copper, zinc and other metals. The market prices for these metals are volatile and are affected by numerous factors beyond our control, including:

| ● | global or regional consumption patterns; |

| ● | the supply of, and demand for, these metals; |

| ● | speculative activities; |

| ● | the availability and costs of metal substitutes; |

| ● | expectations for inflation; and |

| ● | political and economic conditions, including interest rates and currency values. |

We cannot predict the effect of these factors on metal prices. A decrease in the market price of copper, zinc and other metals could affect our ability to raise funds to finance the exploration and development of any of our mineral projects, which would have a material adverse effect on our financial condition and results of operations. The market price of copper, zinc and other metals may not remain at current levels. In particular, an increase in worldwide supply, and consequent downward pressure on prices, may result over the longer term from increased copper production from mines developed or expanded as a result of current metal price levels. There is no assurance that a profitable market may exist or continue to exist.

Title and other rights to our properties may be subject to challenge.

We cannot provide assurance that title to our properties will not be challenged. We (through our interest in Ambler Metals) indirectly own mineral claims which constitute our property holdings. We may not have, or may not be able to obtain, all necessary surface rights to develop a property. Title insurance is generally not available for mineral properties and our ability to ensure that we have obtained a secure claim to individual mining properties may be severely constrained. Our mineral properties may be subject to prior unregistered agreements, transfers or claims, and title may be affected by, among other things, undetected defects. We have not conducted surveys of all of the claims in which we hold direct or indirect interests. A successful claim contesting our title to a property will cause us to lose our rights to explore and, if warranted, develop that property or undertake or continue production thereon. This could result in our not being compensated for our prior expenditures relating to the property. In addition, our ability to continue to explore and develop the property may be subject to agreements with other third parties including agreements with native corporations and first nations groups, for instance, the lands at the Upper Kobuk Mineral Projects are subject to the NANA Agreement (as more particularly described under "History of Trilogy - Agreement with NANA Regional Corporation").

We will incur losses for the foreseeable future.

We expect to incur losses unless and until such time as our mineral projects generate sufficient revenues to fund continuing operations. The exploration and development of our mineral properties will require the commitment of substantial financial resources that may not be available.

The amount and timing of expenditures will depend on a number of factors, including the progress of ongoing exploration and development, the results of consultants’ analyses and recommendations, the rate at which operating losses are incurred, the execution of any joint venture agreements with strategic partners and the acquisition of additional property interests, some of which are beyond our control. We cannot provide assurance that we will ever achieve profitability.

16

High metal prices in past years have encouraged increased mining exploration, development and construction activity, which has increased demand for, and cost of, exploration, development and construction services and equipment.

The relative strength of metal prices in past years has encouraged increases in mining exploration, development and construction activities around the world, which has resulted in increased demand for, and cost of, exploration, development and construction services and equipment. Increased demand for and cost of services and equipment could result in delays if services or equipment cannot be obtained in a timely manner due to inadequate availability and may cause scheduling difficulties due to the need to coordinate the availability of services or equipment, any of which could materially increase project exploration, development and/or construction costs.

Risks Relating to the Mining Industry and Mineral Reserves

Mineral resource and reserve calculations are only estimates.

Any figures presented for mineral resources or reserves in this Form 10-K and in our other filings with securities regulatory authorities and those which may be presented in the future are and will only be estimates. There is a degree of uncertainty attributable to the calculation of mineral reserves and mineral resources. Until mineral reserves or mineral resources are actually mined and processed, the quantity of metal and grades must be considered as estimates only and no assurances can be given that the indicated levels of metals will be produced. In making determinations about whether to advance any of our projects to development, we must rely upon estimated calculations as to the mineral resources or reserves and grades of mineralization on our properties.

The estimating of mineral reserves and mineral resources is a subjective process that relies on the judgment of the persons preparing the estimates. The process relies on the quantity and quality of available data and is based on knowledge, mining experience, analysis of drilling results and industry practices. Valid estimates made at a given time may significantly change when new information becomes available. While we believe that the mineral resource estimates included in this Form 10-K for the Upper Kobuk Mineral Projects are well-established and reflect management’s best estimates, by their nature mineral resource estimates are imprecise and depend, to a certain extent, upon analysis of drilling results and statistical inferences that may ultimately prove to be inaccurate. There can be no assurances that actual results will meet the estimates contained in feasibility studies or pre-feasibility studies. As well, further studies are required.

Estimated mineral reserves or mineral resources may have to be recalculated based on changes in metal prices, further exploration or development activity or actual production experience. This could materially and adversely affect estimates of the volume or grade of mineralization, estimated recovery rates or other important factors that influence mineral reserve or mineral resource estimates. The extent to which mineral resources may ultimately be reclassified as mineral reserves is dependent upon the demonstration of their profitable recovery. Any material changes in mineral resource estimates and grades of mineralization will affect the economic viability of placing a property into production and a property’s return on capital. We cannot provide assurance that mineralization can be mined or processed profitably.

Our mineral resource estimates have been determined and valued based on assumed future metal prices, cut-off grades and operating costs that may prove to be inaccurate. Extended declines in market prices for copper, zinc, lead, gold and silver may render portions of our mineralization uneconomic and result in reduced reported mineral resources, which in turn could have a material adverse effect on our results of operations or financial condition. We cannot provide assurance that mineral recovery rates achieved in small scale tests will be duplicated in large scale tests under on-site conditions or in production scale.

A reduction in any mineral reserves that may be estimated by us could have an adverse impact on our future cash flows, earnings, results of operations and financial condition. No assurances can be given that any mineral resource estimates for the Upper Kobuk Mineral Projects will ultimately be reclassified as mineral reserves. See “Cautionary Note to United States Investors.”

17

Significant uncertainty exists related to inferred mineral resources.

There is a risk that inferred mineral resources referred to in this Form 10-K cannot be converted into measured or indicated mineral resources as there may be limited ability to assess geological continuity. It is reasonably expected that the majority of inferred mineral resources could be upgraded to indicated mineral resources with continued exploration. See “Cautionary Note to United States Investors.”

Mining is inherently risky and subject to conditions or events beyond our control.

The development and operation of a mine is inherently dangerous and involves many risks that even a combination of experience, knowledge and careful evaluation may not be able to overcome, including:

| ● | unusual or unexpected geological formations; |

| ● | metallurgical and other processing problems; |

| ● | metal losses; |

| ● | environmental hazards; |

| ● | power outages; |

| ● | labor disruptions; |

| ● | industrial accidents; |

| ● | periodic interruptions due to inclement or hazardous weather conditions; |

| ● | flooding, explosions, fire, rockbursts, cave-ins and landslides; |

| ● | mechanical equipment and facility performance problems; and |

| ● | the availability of materials and equipment. |

These risks could result in damage to, or destruction of, mineral properties, production facilities or other properties, personal injury or death, including to our employees, environmental damage, delays in mining, increased production costs, asset write downs, monetary losses and possible legal liability. We may not be able to obtain insurance to cover these risks at economically feasible premiums, or at all. The Company's insurance premiums have increased in recent years and in other circumstances the scope of insurance coverage has been reduced. The Company also expects insurance premiums to increase due to the impacts of COVID-19. Insurance against certain environmental risks, including potential liability for pollution and other hazards associated with mineral exploration and production, is not generally available to companies within the mining industry. We may suffer a material adverse effect on our business if we incur losses related to any significant events that are not covered by our insurance policies.

We cannot provide assurance that we will successfully acquire commercially mineable mineral rights.

Exploration for and development of copper properties involves significant financial risks which even a combination of careful evaluation, experience and knowledge may not eliminate. While the discovery of an ore body may result in substantial rewards, few properties which are explored are ultimately developed into producing mines. Major expenses may be required to establish reserves by drilling, constructing mining and processing facilities at a site, developing metallurgical processes and extracting metals from ore. We cannot ensure that our current exploration and development programs will result in profitable commercial mining operations.

18

The economic feasibility of development projects is based upon many factors, including the accuracy of mineral resource estimates; metallurgical recoveries; capital and operating costs; government regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting and environmental protection; and metal prices, which are highly volatile. Development projects are also subject to the successful completion of feasibility studies, issuance of necessary governmental permits and availability of adequate financing.

Most exploration projects do not result in the discovery of commercially mineable ore deposits, and no assurance can be given that any anticipated level of recovery of ore reserves, if any, will be realized or that any identified mineral deposit will ever qualify as a commercially mineable (or viable) ore body which can be legally and economically exploited. Estimates of mineral reserves, mineral resources, mineral deposits and production costs can also be affected by such factors as environmental permitting regulations and requirements, weather, environmental factors, unforeseen technical difficulties, the metallurgy of the mineralization forming the mineral deposit, unusual or unexpected geological formations and work interruptions. If current exploration programs do not result in the discovery of commercial ore, we may need to write-off part or all of our investment in our existing exploration stage properties and may need to acquire additional properties.

Material changes in mineral reserves, if any, grades, stripping ratios or recovery rates may affect the economic viability of any project. Our future growth and productivity will depend, in part, on our ability to develop commercially mineable mineral rights at our existing properties or identify and acquire other commercially mineable mineral rights, and on the costs and results of continued exploration and potential development programs. Mineral exploration is highly speculative in nature and is frequently non-productive. Substantial expenditures are required to:

| ● | establish mineral resources and reserves through drilling and metallurgical and other testing techniques; |

| ● | determine metal content and metallurgical recovery processes to extract metal from the ore; and |

| ● | construct, renovate or expand mining and processing facilities. |

In addition, if we discover ore, it would take several years from the initial phases of exploration until production is possible. During this time, the economic feasibility of production may change. As a result of these uncertainties, there can be no assurance that we will successfully acquire commercially mineable (or viable) mineral rights.

Risks Relating to Government Regulation

We are subject to significant governmental regulations.

Our exploration activities are subject to extensive federal, state, provincial and local laws and regulations governing various matters, including:

| ● | environmental protection; |

| ● | the management and use of toxic substances and explosives; |

| ● | the management of natural resources; |

| ● | the exploration and development of mineral properties, including reclamation; |

| ● | exports; |

| ● | price controls; |

| ● | taxation and mining royalties; |

| ● | management of tailing and other waste generated by operations; |

19

| ● | labor standards and occupational health and safety, including mine safety; |

| ● | historic and cultural preservation; and |

| ● | transportation. |

Failure to comply with applicable laws and regulations may result in civil or criminal fines or penalties or enforcement actions, including orders issued by regulatory or judicial authorities enjoining, curtailing or closing operations or requiring corrective measures, installation of additional equipment or remedial actions, any of which could result in significant expenditures. We may also be required to compensate private parties suffering loss or damage by reason of a breach of such laws, regulations or permitting requirements. It is also possible that future laws and regulations, or more stringent enforcement of current laws and regulations by governmental authorities, could cause us to incur additional expense or capital expenditure restrictions, suspensions or closing of our activities and delays in the exploration and development of our properties.

We require further permits in order to conduct current and anticipated future operations, and delays in obtaining or failure to obtain such permits, or a failure to comply with the terms of any such permits that we have obtained, would adversely affect our business.

Our current and anticipated future operations, including further exploration, development and commencement of production on our mineral properties, require permits from various governmental authorities. Obtaining or renewing governmental permits is a complex and time-consuming process. The duration and success of efforts to obtain and renew permits are contingent upon many variables not within our control. Due to the preliminary stages of the Upper Kobuk Mineral Projects, it is difficult to assess what specific permitting requirements will ultimately apply.

Shortage of qualified and experienced personnel in the U.S. federal and Alaskan State agencies to coordinate a federally led joint environmental impact statement process could result in delays or inefficiencies. Backlog within the permitting agencies could affect the permitting timeline or potential of the Upper Kobuk Mineral Projects, as may negative public perception of mining projects in general due to circumstances unrelated to the Company and outside of its control. Other factors that could affect the permitting timeline include (i) the number of other large-scale projects currently in a more advanced stage of development which could slow down the review process for the Upper Kobuk Mineral Projects and (ii) significant public response regarding the Upper Kobuk Mineral Projects.

We cannot provide assurance that all permits that we require for our operations, including any for construction of mining facilities or conduct of mining, will be obtainable or renewable on reasonable terms, or at all. Delays or a failure to obtain such required permits, or the expiry, revocation or failure to comply with the terms of any such permits that we have obtained, would adversely affect our business.

Our activities are subject to environmental laws and regulations that may increase our costs and restrict our operations.

All of our exploration, potential development and production activities are subject to regulation by governmental agencies under various environmental laws. These laws address emissions into the air, discharges into water, management of waste, management of hazardous substances, protection of natural resources, antiquities and endangered species and reclamation of lands disturbed by mining operations. Environmental legislation is evolving, and the general trend has been towards stricter standards and enforcement, increased fines and penalties for noncompliance, more stringent environmental assessments of proposed projects and increasing responsibility for companies and their officers, directors and employees. Compliance with environmental laws and regulations may require significant capital outlays on our behalf and may cause material changes or delays in our intended activities.

Several regulatory initiatives are currently ongoing within the State of Alaska that have the potential to influence the permitting process for the Upper Kobuk Mineral Projects. These include revisions to Alaska's Water Quality Standards regarding mixing zones regulations, which are currently under Environmental Protection Agency review, and which revisions may be required in order to authorize a mixing zone for discharge in Subarctic Creek. Future changes in these

20

laws or regulations could have a significant adverse impact on some portion of our business, requiring us to re-evaluate those activities at that time.

Environmental hazards may exist on our properties that are unknown to us at the present time and that have been caused by previous owners or operators or that may have occurred naturally. We may be liable for remediating such damage.

Failure to comply with applicable environmental laws, regulations and permitting requirements may result in enforcement actions thereunder, including orders issued by regulatory or judicial authorities, causing operations to cease or to be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment or remedial actions.

Land reclamation requirements for our exploration properties may be burdensome.

Land reclamation requirements are generally imposed on mineral exploration companies (as well as companies with mining operations) in order to minimize long term effects of land disturbance. Reclamation may include requirements to:

| ● | treat ground and surface water to applicable water quality standards; |

| ● | control dispersion of potentially deleterious effluents; and |

| ● | reasonably re-establish pre-disturbance landforms and vegetation. |

In order to carry out reclamation obligations imposed on us in connection with exploration, potential development and production activities, we must allocate financial resources that might otherwise be spent on further exploration and development programs. In addition, regulatory changes could increase our obligations to perform reclamation and mine closing activities. If we are required to carry out unanticipated reclamation work, our financial position could be adversely affected.

Risks Related to the Acquisition of New Projects

Risks inherent in acquisitions of new properties.

We may actively pursue the acquisition of exploration, development and production assets consistent with our acquisition and growth strategy. From time to time, we may also acquire securities of or other interests in companies with respect to which we may enter into acquisitions or other transactions. Acquisition transactions involve inherent risks, including but not limited to:

| ● | accurately assessing the value, strengths, weaknesses, contingent and other liabilities and potential profitability of acquisition candidates; |

| ● | ability to achieve identified and anticipated operating and financial synergies; |

| ● | unanticipated costs; |

| ● | diversion of management attention from existing business; |

| ● | potential loss of our key employees or key employees of any business acquired; |

| ● | unanticipated changes in business, industry or general economic conditions that affect the assumptions underlying the acquisition; |

| ● | decline in the value of acquired properties, companies or securities; |

21

| ● | assimilating the operations of an acquired business or property in a timely and efficient manner; |

| ● | maintaining our financial and strategic focus while integrating the acquired business or property; |

| ● | implementing uniform standards, controls, procedures and policies at the acquired business, as appropriate; and |

| ● | to the extent that we make an acquisition outside of markets in which it has previously operated, conducting and managing operations in a new operating environment. |

Acquiring additional businesses or properties could place increased pressure on our cash flow if such acquisitions involve a cash consideration. The integration of our existing operations with any acquired business will require significant expenditures of time, attention and funds. Achievement of the benefits expected from consolidation would require us to incur significant costs in connection with, among other things, implementing financial and planning systems. We may not be able to integrate the operations of a recently acquired business or restructure our previously existing business operations without encountering difficulties and delays. In addition, this integration may require significant attention from our management team, which may detract attention from our day-to-day operations. Over the short-term, difficulties associated with integration could have a material adverse effect on our business, operating results, financial condition and the price of our Common Shares. In addition, the acquisition of mineral properties may subject us to unforeseen liabilities, including environmental liabilities, which could have a material adverse effect on us. There can be no assurance that any future acquisitions will be successfully integrated into our existing operations.

Any one or more of these factors or other risks could cause us not to realize the anticipated benefits of an acquisition of properties or companies and could have a material adverse effect on our financial condition.

We face industry competition in the acquisition of exploration properties and the recruitment and retention of qualified personnel.

We compete with other exploration and producing companies, many of which are better capitalized, have greater financial resources, operational experience and technical capabilities or are further advanced in their development or are significantly larger and have access to greater mineral reserves, for the acquisition of mineral claims, leases and other mineral interests as well as for the recruitment and retention of qualified employees and other personnel. If we require and are unsuccessful in acquiring additional mineral properties or in recruiting and retaining qualified personnel, we will not be able to grow at the rate we desire, or at all.

Risks Related to the Company’s Executive Officers and Board of Directors

We may experience difficulty attracting and retaining qualified management and technical personnel to grow our business.

We are dependent on the services of key executives and other highly skilled and experienced personnel to advance our corporate objectives as well as the identification of new opportunities for growth and funding. Mr. Giardini and Ms. Sanders are currently our only executive officers. It will be necessary for us to recruit additional skilled and experienced executives. Our inability to do so, or the loss of any of these persons or our inability to attract and retain suitable replacements for them, or additional highly skilled employees required for our activities, would have a material adverse effect on our business and financial condition.

Some of our directors and officers have conflicts of interest as a result of their involvement with other natural resource companies.

Certain of our directors and officers also serve as directors or officers, in other companies involved in natural resource exploration and development or mining-related activities, including, in particular, NovaGold. To the extent that such other companies may participate in ventures in which we may participate in, or in ventures which we may seek to

22

participate in, our directors and officers may have a conflict of interest in negotiating and concluding terms respecting the extent of such participation. In all cases where our directors and officers have an interest in other companies, such other companies may also compete with us for the acquisition of mineral property investments. Any decision made by any of these directors and officers involving Trilogy will be made in accordance with their duties and obligations to deal fairly and in good faith with a view to the best interests of Trilogy and its shareholders. In addition, each of the directors is required to declare and refrain from voting on any matter in which these directors may have a conflict of interest in accordance with the procedures set forth in the Business Corporations Act (British Columbia) and other applicable laws. In appropriate cases, the Company will establish a special committee of independent directors to review a matter in which several directors, or management, may have a conflict. Nonetheless, as a result of these conflicts of interest, the Company may not have an opportunity to participate in certain transactions, which may have a material adverse effect on the Company’s business, financial condition, results of operation and prospects.

General Risk Factors

General economic conditions may adversely affect our growth, future profitability and ability to finance.