UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2021

Commission file number 1-14287

| (State of incorporation) | (IRS Employer Identification No.) | ||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐. No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐. No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| ☒ | Emerging growth company | |||||||||||||

| Non-accelerated filer | ☐ | |||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of Common Stock held by non-affiliates computed by reference to the price at which the Common Stock was last sold as reported on the New York Stock Exchange as of June 30, 2021, was $257.9 million. As of March 1, 2022, there were 13,673,933 shares of the registrant’s Class A Common Stock, par value $0.10 per share, and 719,200 shares of the registrant’s Class B Common Stock, par value $0.10 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the 2022 annual meeting of shareholders to be filed with the Securities and Exchange commission within 120 days after the end of fiscal year 2021 are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

| Page | ||||||||

| PART I | ||||||||

Items 1. | Business | |||||||

Item 1A. | Risk Factors | |||||||

Item 1B. | Unresolved Staff Comments | |||||||

Item 2. | Properties | |||||||

Item 3. | Legal Proceedings | |||||||

Item 4. | Mine Safety Disclosures | |||||||

| PART II | ||||||||

Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |||||||

Item 6. | ||||||||

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||||||

Item 8. | Financial Statements and Supplementary Data | |||||||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |||||||

Item 9A. | Controls and Procedures | |||||||

Item 9B. | Other Information | |||||||

| PART III | ||||||||

Item 10. | Directors, Executive Officers and Corporate Governance | |||||||

Item 11. | Executive Compensation | |||||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |||||||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | |||||||

Item 14. | Principal Accounting Fees and Services | |||||||

| PART IV | ||||||||

Item 15. | Exhibits and Financial Statement Schedules | |||||||

Item 16. | Form 10-K Summary | |||||||

Exhibit Index | ||||||||

Signatures | ||||||||

Consolidated Financial Statements | ||||||||

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, including Management’s Discussion and Analysis of Financial Condition and Results of Operations in Part II, Item 7, contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934. In this context, forward-looking statements mean statements related to future events, may address our expected future business and financial performance, and often contain words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “will”, “should”, “could”, “would” or “may” and other words of similar meaning. Forward-looking statements by their nature address matters that are, to different degrees, uncertain.

For Centrus Energy Corp., particular risks and uncertainties that could cause our actual future results to differ materially from those expressed in our forward-looking statements include but are not limited to the following which are, and will be, exacerbated by the novel coronavirus (“COVID-19”) pandemic and any worsening of the global business and economic environment as a result; risks related to the war in Ukraine and geopolitical conflicts and the imposition of sanctions or other measures that could impact our ability to obtain or sell low enriched uranium (LEU) under our existing supply contract with the Russian government-owned entity TENEX, Joint-Stock Company (“TENEX”); risks related to natural and other disasters, including the continued impact of the March 2011 earthquake and tsunami in Japan on the nuclear industry and on our business, results of operations and prospects; risks related to financial difficulties experienced by customers or suppliers, including possible bankruptcies, insolvencies or any other inability to pay for our products or services or delays in making timely payment; risks related to pandemics and other health crises, such as the global COVID-19 pandemic and subsequent variants; the impact and potential extended duration of the current supply/demand imbalance in the market for low-enriched uranium (“LEU”); risks related to our ability to sell the LEU we procure pursuant to our purchase obligations under our supply agreements including those imposed under the 1992 Russian Suspension Agreement as amended (“RSA”), international trade legislation and other international trade restrictions; risks related to existing or new trade barriers and contract terms that limit our ability to procure LEU for, or deliver LEU to customers; pricing trends and demand in the uranium and enrichment markets and their impact on our profitability; risks related to the movement and timing of customer orders; risks related to our dependence on others for deliveries of LEU including deliveries from TENEX, under a commercial supply agreement with TENEX and deliveries under a long-term commercial supply agreement with Orano Cycle (“Orano”); risks associated with our reliance on third-party suppliers to provide essential products and services to us; risks related to the fact that we face significant competition from major producers who may be less cost sensitive or are wholly or partially government owned; risks that our ability to compete in foreign markets may be limited for various reasons; risks related to the fact that our revenue is largely dependent on our largest customers; risks related to our sales order book, including uncertainty concerning customer actions under current contracts and in future contracting due to market conditions and our lack of current production capability; risks related to whether or when government funding or demand for high-assay low-enriched uranium (“HALEU”) for government or commercial uses will materialize; risks and uncertainties regarding funding for continuation and deployment of the American Centrifuge technology; risks related to our ability to perform and absorb costs under our agreement with the U.S. Department of Energy (“DOE”) to deploy a cascade of centrifuges to demonstrate production of HALEU for advanced reactors (the “HALEU Contract”) or to obtain contracts and funding to be able to continue operations and our ability to obtain and/or perform under other agreements; risks that we may not obtain the full benefit of the HALEU Contract and may not be able to operate the HALEU enrichment facility to produce HALEU after the completion of the existing HALEU Contract or that the HALEU enrichment facility may not be available to us as a future source of supply; risks related to uncertainty regarding our ability to commercially deploy competitive enrichment technology; risks related to the potential for further demobilization or termination of our American Centrifuge work; risks that we will not be able to timely complete the work that we are obligated to perform; risks related to our ability to perform fixed-price and cost-share contracts such as the HALEU Contract, including the risk that costs could be higher than expected; risks related to our significant long-term liabilities, including material unfunded defined benefit pension plan obligations and postretirement health and life benefit obligations; risks relating to our 8.25% notes (the “8.25% Notes”) maturing in February 2027; the risks of revenue and operating results fluctuating significantly from quarter to quarter, and in some cases, year to year; risks related to the impact of financial market conditions on our business, liquidity, prospects, pension assets and insurance facilities; risks related to the Company’s capital concentration; risks related to the value of our intangible assets related to the sales order book and customer relationships; risks related to the limited trading markets in our securities; risks related to decisions made by our Class B stockholders regarding their investment in the Company based upon factors that are unrelated to the Company’s performance; risks that a small number of holders of our Class A Common Stock, par value $0.10 per share (“Class A Common Stock”), (whose interests may not be aligned with other holders of our Class A Common Stock), may exert significant influence over the direction of the Company; risks related to the use of our net operating losses (“NOLs”) carryforwards and net unrealized built-in losses (“NUBILs”) to offset future taxable income and the use of the Rights Agreement (as defined herein) to prevent an “ownership change” as defined in Section 382 of the Internal Revenue Code of 1986, as amended (the “Code”) and our ability to generate taxable income to utilize all or a portion of the NOLs and NUBILs prior to the expiration thereof; failures or security breaches of our information technology systems; risks related to our ability to attract and retain key personnel; risks related to the potential for DOE to seek to terminate or exercise its

3

remedies under its agreements with the Company; risks related to actions, including government reviews, that may be taken by the United States government, the Russian government or other governments that could affect our ability to perform under our contract obligations or the ability of our sources of supply to perform under their contract obligations to us; risks related to our ability to perform and receive timely payment under agreements with DOE or other government agencies, including risks and uncertainties related to the ongoing funding by the government and potential audits; risks related to changes or termination of agreements with the U.S. government or other counterparties; risks related to the competitive environment for our products and services; risks related to changes in the nuclear energy industry; risks related to the competitive bidding process associated with obtaining contracts, including government contracts; risks that we will be unable to obtain new business opportunities or achieve market acceptance of our products and services or that products or services provided by others will render our products or services obsolete or noncompetitive; risks related to potential strategic transactions that could be difficult to implement, disrupt our business or change our business profile significantly; risks related to the outcome of legal proceedings and other contingencies (including lawsuits and government investigations or audits); risks related to the impact of government regulation and policies including by the DOE and the U.S. Nuclear Regulatory Commission; risks of accidents during the transportation, handling or processing of hazardous or radioactive material that may pose a health risk to humans or animals, cause property or environmental damage, or result in precautionary evacuations; risks associated with claims and litigation arising from past activities at sites we currently operate or past activities at sites that we no longer operate, including the Paducah, Kentucky, and Portsmouth, Ohio, gaseous diffusion plants; and other risks and uncertainties discussed in this and our other filings with the Securities and Exchange Commission (“SEC”).

For a discussion of these risks and uncertainties and other factors that may affect our future results, please see Part I, Item 1A, Risk Factors, the other sections of this Annual Report on Form 10-K and our subsequently filed documents. These factors may not constitute all factors that could cause actual results to differ from those discussed in any forward-looking statement. Accordingly, forward-looking statements should not be relied upon as a predictor of actual results. Readers are urged to carefully review and consider the various disclosures made in this report and in our other filings with the SEC that attempt to advise interested parties of the risks and factors that may affect our business. We do not undertake to update our forward-looking statements to reflect events or circumstances that may arise after the date of this Annual Report on Form 10-K, except as required by law.

4

PART I

Item 1. Business

Overview

Centrus Energy Corp., a Delaware corporation, is a trusted supplier of enriched uranium for nuclear fuel and services for the nuclear power industry, which provides a reliable source of carbon-free energy. References to “Centrus”, the “Company”, “our”, or “we” include Centrus Energy Corp. and its wholly-owned subsidiaries as well as the predecessor to Centrus, unless the context otherwise indicates. We were incorporated in 1998 as part of the privatization of the United States Enrichment Corporation.

Centrus operates two business segments: (a) low-enriched uranium (“LEU”), which supplies various components of nuclear fuel to commercial customers from our global network of suppliers, and (b) technical solutions, which provides advanced engineering, design, and manufacturing services to government and private sector customers and is deploying uranium enrichment and other capabilities necessary for production of advanced nuclear fuel to power existing and next-generation reactors around the world.

Our LEU segment provides most of the Company’s revenue and involves the sale of enriched uranium for nuclear fuel to customers that are primarily utilities which operate commercial nuclear power plants. The majority of these sales are for the enrichment component of LEU, which is measured in separative work units (“SWU”). Centrus also sells natural uranium (the raw material needed to produce LEU) and occasionally sells LEU with the natural uranium, uranium conversion, and SWU components combined into one sale.

LEU is a critical component in the production of nuclear fuel for reactors that produce electricity. We supply LEU and its components to both domestic and international utilities for use in nuclear reactors worldwide. We provide LEU from multiple sources, including our inventory, medium and long-term supply contracts, and spot purchases. As a long-term supplier of LEU to our customers, our objective is to provide value through the reliability and diversity of our supply sources.

Our global order book includes long-term sales contracts with major utilities to 2029. We have secured cost-competitive supplies of SWU under long-term contracts through the end of this decade to allow us to fill our existing customer orders and make new sales. A market-related price reset provision in our largest supply contract took effect at the beginning of 2019 – when market prices for SWU were near historic lows – which has significantly lowered our cost of sales and contributed to improved margins.

In October 2020, the U.S. Department of Commerce (“DOC”) reached agreement with the Russian Federation on an extension of the 1992 Russian Suspension Agreement, a trade agreement which allows for Russian-origin nuclear fuel to be exported to the United States in limited quantities, with an import quantity in each year. The two parties agreed to extend the agreement through 2040 and to set aside a significant portion of the quota for Centrus’ shipments to the United States through 2028 to execute our long-term supply (purchase) agreement (the “TENEX Supply Contract”) with the Russian government entity, TENEX, Joint-Stock Company (“TENEX”). This outcome also allows sufficient quota for Centrus to continue serving its utility customers. Refer to Item 1A Risk Factors - Operational Risks for further discussion.

Under a contract with the U.S. Department of Energy (“DOE”), our technical solutions segment is deploying uranium enrichment and other capabilities necessary for production of advanced nuclear fuel to meet the evolving needs of the global nuclear industry and the U.S. government. We also are leveraging our unique technical expertise, operational experience, and specialized facilities to expand and diversify our business beyond uranium enrichment, offering new services to existing and new customers in complementary markets.

5

Our technical solutions segment is working to restore America’s domestic uranium enrichment capability, to play a critical role in meeting U.S. national security and energy security requirements, in advancing America’s nonproliferation objectives and in delivering the next-generation nuclear fuels that will power the future of nuclear energy as it provides reliable carbon-free power around the world.

The United States has not had domestic uranium enrichment capability suitable to meet U.S. national security requirements since the Paducah Gaseous Diffusion Plant (“Paducah GDP”) shut down in 2013. Longstanding U.S. policy and binding nonproliferation agreements prohibit the use of foreign-origin enrichment technology for U.S. national security missions. Our AC100M centrifuge currently is the only deployment-ready U.S. uranium enrichment technology that can meet these national security requirements, albeit requiring one minor change in sourcing of materials.

Centrus is working to pioneer U.S. production of High-Assay, Low-Enriched Uranium (“HALEU”), enabling the deployment of a new generation of HALEU-fueled reactors to meet the world’s growing need for carbon-free power. HALEU is a high-performance nuclear fuel component which is expected to be required by a number of advanced reactor and fuel designs that are now under development for commercial and government uses. While existing reactors typically operate on LEU with the uranium-235 isotope concentration below 5%, HALEU is further enriched so that the uranium-235 concentration is between 5% and 20%. The higher U-235 concentration offers a number of potential advantages, which may include better fuel utilization, improved performance, fewer refueling outages, simpler reactor designs, reduced waste volumes, and greater nonproliferation resistance.

The lack of a domestic HALEU supply is widely viewed as a major obstacle to the successful commercialization of these new reactors. As the only company with a license from the Nuclear Regulatory Commission (“NRC”) to enrich up to 20% uranium-235 assay HALEU, Centrus is uniquely positioned to fill a critical gap in the supply chain and facilitate the deployment of these promising next-generation reactors.

The DOE has experienced a COVID-19 related supply chain delay in obtaining the HALEU storage cylinders. Since it is not possible to begin HALEU production without the storage cylinders, it would not be possible to complete the operational portion of the demonstration before the June 1, 2022 expiration date of the existing contract. As a result, the DOE elected to change the scope of the existing contract and move the operational portion of the demonstration to a new, competitively-awarded, contract that would provide for operations beyond the term of the existing contract. On February 7, 2022, the DOE issued a pre-solicitation notice for a request for proposal to complete the HALEU demonstration facility and to produce HALEU, noting that the “the Administration supports longer-term demonstration of production capability.” The pre-solicitation notice outlines a two-phase approach. Phase 1 consists of completing installation of the centrifuges – which DOE expects will take up to one year from contract signing – followed by one full year of cascade operations. Phase 2 consists of three optional, 3-year extensions to produce HALEU, so that the prospective contract could help support a total of one to ten years of cascade operations in addition to completing construction and centrifuge installation.

Centrus believes it is well-positioned to compete for a follow-on contract to operate the machines in our facility near Piketon but there is no assurance that DOE will award such a contract to the Company. Congress has not yet adopted a Fiscal Year 2022 appropriations bill for the DOE, and there is no assurance that the proposed program will be approved and funded.

The U.S. government has been operating under a series of continuing resolutions in Fiscal Year 2022. The DOE continues to support the HALEU program during the continuing resolution period, and has incrementally increased the government’s cost share ceiling as funds have become available.

Additional COVID-19-related impacts, delays in DOE furnishing equipment, or changes to the existing scope of the HALEU Contract could result in further material increases to our estimate of the costs required to complete the existing HALEU Contract, and delay completion of the contract. The Company currently does not have a contractual obligation to perform work in excess of the funding provided by DOE and, therefore, no additional costs

6

have been accrued as of December 31, 2021. If DOE does not commit to fully fund the additional costs, and the Company nevertheless commits to a plan to complete the remaining activities of the HALEU Contract, we may incur material additional costs or losses in future periods that could have an adverse impact on our financial condition and liquidity.

We believe our investment in HALEU technology will position the Company to meet the needs of government and commercial customers in the future as they deploy advanced reactors and next generation fuels. At present, there are a number of advanced reactors under development. For example, nine of the ten advanced reactor designs selected by the DOE for its Advanced Reactor Demonstration Program will require HALEU. In addition, the first non-light water reactor to begin active NRC-license review requires HALEU. The U.S. Department of Defense also plans to construct a prototype HALEU-fueled mobile microreactor in the next three to four years as part of a program called “Project Pele.” The U.S. Air Force also announced plans to deploy a microreactor at Eielson Air Force Base in Alaska. While the use of HALEU is not an express requirement of the Air Force program, the vast majority of microreactor designs are expected to need HALEU. On December 14, 2021, DOE issued a request for information related to a potential program to fund the availability of HALEU.

Advanced nuclear reactors promise to provide an important source of reliable carbon-free power. While there is no commercial market for HALEU today, we believe that by investing in HALEU technology now, and as the only American-based company currently pursuing HALEU enrichment capability and possessing an NRC license for such production, the Company could be positioned to capitalize on a potential new market as the demand for HALEU-based fuels increases in the mid to late-2020s with the development of advanced reactors. However, there are no guarantees about whether or when government or commercial demand for HALEU will materialize, and there are a number of technical, regulatory, and economic hurdles that must be overcome for these fuels and reactors to come to the market. Also, foreign government-owned and operated competitors could seek to enter the market and offer HALEU at more competitive prices. There is one known foreign government-owned entity which currently has the capability to produce HALEU, although this entity is currently subject to trade restrictions that limit the amount of material from this source which may be imported into the United States. Other foreign government owned entities which are not currently subject to U.S. trade restrictions, however, may enter the market. One such foreign government owned entity has expressed an interest in and potential capability for HALEU production but has not committed publicly to enter the market to enrich above 10% uranium-235 enrichment assays. This entity has indicated publicly that it would take six to seven years to be able to produce HALEU.

For further details, refer to Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations - Market Conditions and Outlook. For a discussion of the potential risks and uncertainties facing our business, see Part I, Item 1A, Risk Factors.

Low Enriched Uranium

LEU consists of two components: separative work units (“SWU”) and natural uranium. Revenue from our LEU segment is derived primarily from:

•sales of the SWU component of LEU,

•sales of both the SWU and natural uranium components of LEU, and

•sales of natural uranium.

Our LEU segment accounted for approximately 62% of our total revenue in 2021. Our customers are primarily domestic and international utilities that operate nuclear power plants. Our agreements with electric utilities are primarily medium and long-term, fixed-commitment contracts under which our customers are obligated to purchase a specified quantity of the SWU component of LEU from us. Our agreements for natural uranium and enriched uranium product sales, where we sell both the SWU and uranium component of LEU, are generally shorter-term, fixed-commitment contracts.

7

Uranium and Enrichment

Uranium is a naturally occurring element and is mined from deposits located in Kazakhstan, Canada, Australia, and several other countries, including the United States. According to the World Nuclear Association (“WNA”), there are adequate measured resources of natural uranium to fuel nuclear power at current usage rates for about 90 years. In its natural state, uranium is principally comprised of two isotopes: uranium-235 (“U235”) and uranium-238 (“U238”). The concentration of U235 in natural uranium is only 0.711% by weight. Uranium enrichment is the process by which the concentration of U235 is increased. Most commercial nuclear power reactors require LEU fuel with a U235 concentration greater than natural uranium of up to 5% by weight. Future reactor designs currently under development will likely require higher U235 concentration levels of up to 20%.

SWU is a standard unit of measurement that represents the effort required to sort natural uranium between enriched uranium having a higher percentage of U235 and depleted uranium having a lower percentage of U235. The SWU contained in LEU is calculated using an industry standard formula based on the physics of enrichment. The amount of enrichment deemed to be contained in LEU under this formula is commonly referred to as its SWU component and the quantity of natural uranium deemed to be contained in LEU under this formula is referred to as its uranium or “feed” component.

While in some cases customers purchase both the SWU and uranium components of LEU from us, utility customers typically provide the natural uranium to us as part of their enrichment contracts and in exchange we deliver LEU to these customers and charge for the SWU component. Title to natural uranium provided by customers generally remains with the customer until Centrus delivers the LEU, at which time title to LEU is transferred to the customer, and Centrus takes title to the natural uranium.

The following outlines the steps for converting natural uranium into LEU fuel, commonly known as the nuclear fuel cycle:

Mining and Milling. Natural, or unenriched, uranium is removed from the earth in the form of ore and then crushed and concentrated.

Conversion. Uranium concentrates (“U3O8”) are combined with fluorine gas to produce uranium hexafluoride (“UF6”), a solid at room temperature and a gas when heated. UF6 is shipped to an enrichment plant.

Enrichment. UF6 is enriched in a process that increases the concentration of the U235 isotope in the UF6 from its natural state of 0.711% up to 5%, or LEU, which is usable as a fuel for current light water commercial nuclear power reactors. Future commercial reactor designs may use uranium enriched up to 20% U235, or HALEU.

Fuel Fabrication. LEU is then converted to uranium oxide and formed into small ceramic pellets by fabricators. The pellets are loaded into metal tubes that form fuel assemblies, which are shipped to nuclear power plants. As the advanced reactor market develops, HALEU may be converted to uranium oxide, metal, chloride or fluoride salts, or other forms and loaded into a variety of fuel assembly types optimized for the specific reactor design.

Nuclear Power Plant. The fuel assemblies are loaded into nuclear reactors to create energy from a controlled chain reaction. Nuclear power plants generate approximately 20% of U.S. electricity and 10% of the world’s electricity.

Used Fuel Storage. After the nuclear fuel has been in a reactor for several years its efficiency is reduced and the assembly is removed from the reactor’s core. The used fuel is warm and radioactive and is kept in a deep pool of water for several years. Many utilities have elected to then move the used fuel into steel or concrete and steel casks for interim storage.

8

LEU Segment Order Book

Our order book of sales under contract in the LEU segment (“order book”) extends to 2029. For the years ended December 31, 2021 and 2020, our order book was approximately $986 million and $960 million, respectively. The order book is the estimated aggregate dollar amount of revenue for future SWU and uranium deliveries, and includes approximately $348.2 million of deferred revenue and advances from customers as of December 31, 2021, whereby customers have made advance payments to be applied against future deliveries. We estimate that approximately 3% of our order book is at risk related to customer operations.

Most of our customer contracts provide for fixed purchases of SWU during a given year. Our order book estimate is based partially on customers’ estimates of the timing and size of their fuel requirements and other assumptions that are subject to change. For example, depending on the terms of specific contracts, the customer may be able to increase or decrease the quantity delivered within an agreed range. Our order book estimate is also based on our estimates of selling prices, which may be subject to change. For example, depending on the terms of specific contracts, prices may be adjusted based on escalation using a general inflation index, published SWU price indicators prevailing at the time of delivery, and other factors, all of which are variable. We use external composite forecasts of future market prices and inflation rates in our pricing estimates. Refer to Part I, Item 1A, Risk Factors, for a discussion of risks related to our order book.

Suppliers

We have a diverse base of supply that includes:

•existing inventory of LEU (refer to Note 4, Inventories),

•mid-term and long-term contracts with enrichment producers,

•purchases and loans from secondary sources including fabricators and utility operators of nuclear power plants that have excess inventory, and

•spot purchases of SWU, uranium and LEU.

We aim to continue to further diversify this base of supply and take advantage of opportunities to obtain additional short and long-term supplies of LEU. Currently, our largest suppliers of SWU are TENEX and the French government owned company Orano Cycle (“Orano”).

Under the TENEX Supply Contract, we purchase SWU contained in LEU, and we deliver natural uranium to TENEX for the LEU’s uranium component. The TENEX Supply Contract extends through 2028. We typically pay for the SWU contained in the LEU, and supply natural uranium to TENEX for the natural uranium component. SWU pricing is determined by a formula that uses a combination of market-related price points and other factors. The LEU that we obtain from TENEX under the TENEX Supply Contract currently is subject to quotas and other restrictions under an agreement between the United States and the Russian Federation governing exports of Russian uranium products to the United States (the “RSA”). This agreement extends through 2040 under an amendment signed in October 2020 by the DOC and the Russian State Atomic Energy Corporation (“ROSATOM”). The October 2020 amendment provides quotas for shipments of Russian uranium products to the United States after 2020, and allocates a substantial portion of the quotas through 2028 to Centrus for use under the TENEX Supply Contract to supply LEU for use in U.S. reactors. These quotas will allow us to continue to supply Russian LEU to our U.S. customers through 2028. The terms of the RSA, as extended, were also adopted into law by the U.S. Congress in the Consolidated Appropriations Act, 2021. Refer to Item 1A Risk Factors - Operational Risks for further discussion.

9

The amount of SWU we must purchase from TENEX under the TENEX Supply Contract exceeds our current sales order book and, therefore, we will need to make new sales to place all the Russian LEU we must order to meet our SWU purchase obligations to TENEX. Although the quotas cover most of the LEU that we must order to fulfill our purchase obligations under the TENEX Supply Contract, we expect that a small portion of the Russian LEU that we order during the term of the TENEX Supply Contract will need to be delivered to customers who will use it in non-U.S. reactors.

We also have an agreement with Orano (the “Orano Supply Agreement”) for the long-term supply of SWU contained in LEU, commencing in 2023. Under the Orano Supply Agreement, we will purchase SWU contained in LEU received from Orano, and then deliver natural uranium to Orano for the natural uranium feed material component of LEU. We had the option to extend the six-year purchase period for an additional two years and have recently elected to take the additional supply in 2029. The Orano Supply Agreement provides flexibility to adjust purchase volumes, subject to annual minimums and maximums, in fixed amounts that vary year by year. The pricing for the purchased SWU is determined by a formula that uses a combination of market-related price points and other factors, and is subject to certain floors and ceilings. Prices are payable in a combination of U.S. dollars and euros.

We procure LEU from other sources under short-term and long-term contracts and have inventories available that diversify our supply portfolio and provide flexibility to help us meet the needs of our customers. We also have agreements to borrow SWU which we can use to optimize our purchases and deliveries over time.

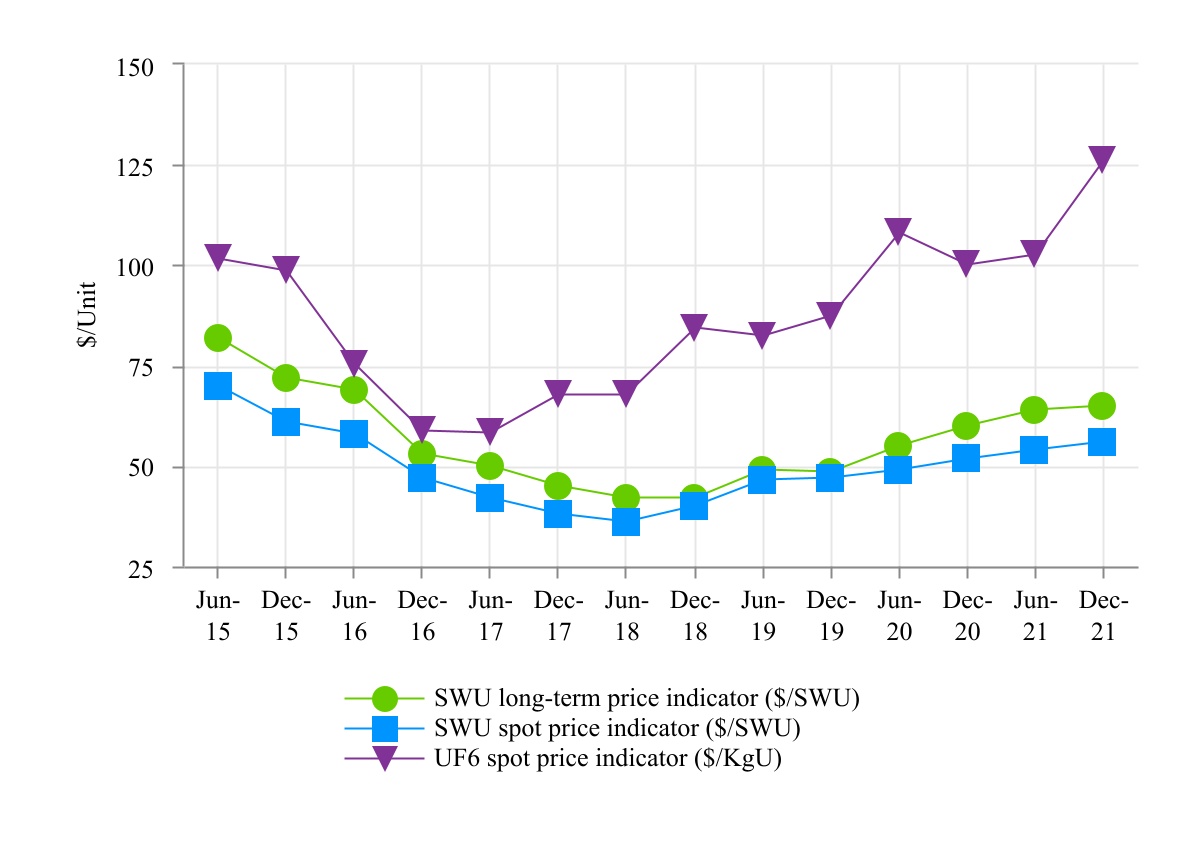

Market prices for SWU fell substantially in the aftermath of the nuclear incident at Fukushima, Japan in 2011, bottoming out in August of 2018. While prices have been rising, they are still lower than market prices prior to Fukushima. Recent purchases of SWU and our long-term contract with Orano reflect these lower market prices. Additionally, prices under the TENEX Supply Contract have been adjusted to reflect lower market prices based on a one-time market related price reset that was agreed to when we signed the contract in 2011. The reset occurred in 2018, reducing the unit cost per SWU for our purchases from 2019 through 2028.

Technical Solutions

Our technical solutions segment reflects our technical, manufacturing, engineering, and operations services offered to public and private sector customers, including the American Centrifuge engineering, procurement, construction, manufacturing and operations services being performed under the HALEU Contract. With our private sector customers, we seek to leverage our domestic enrichment experience, engineering know-how and precision manufacturing facility to assist customers with a range of engineering, design and advanced manufacturing projects, including the production of fuel for next-generation nuclear reactors and the development of related facilities. Refer to Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations - COVID-19 Update.

10

Government Contracting

On October 31, 2019, we signed the cost-share HALEU Contract with DOE to deploy a cascade of centrifuges to demonstrate production of HALEU for advanced reactors. The three-year program has been under way since May 31, 2019, when the Company and DOE signed an interim HALEU letter agreement that allowed work to begin while the full contract was being finalized. We have significantly invested in advanced technology because of the potential for future growth into new areas of business for the Company, while also preserving our unique workforce at our Technology and Manufacturing Center in Oak Ridge, Tennessee, and our production facility near Piketon, Ohio. The Company entered into this cost-share contract with DOE as a critical first step on the road back to the commercial production of enriched uranium, which the Company had terminated in 2013 with the closure of the Paducah GDP. The HALEU Contract, if fully implemented, is expected to result in the Company having readied the 16-machine cascade to enrich uranium to the 20% concentration in the uranium-235 isotope that is required by many of the advanced reactor concepts now under development. Centrus is currently the only company with an NRC license to enrich uranium up to the 20% concentration that is contained in HALEU.

In 2019, under the HALEU Contract, DOE agreed to reimburse the Company for 80% of its costs incurred in performing the contract, up to a maximum of $115 million (which was recently increased to $126.7 million, as noted below). The Company’s cost share is the corresponding 20% and any costs the Company elects to incur above these amounts. Costs under the HALEU Contract include program costs, including internal labor, third-party services and materials, and associated indirect costs that are classified as Cost of Sales, and an allocation of corporate costs supporting the program that are classified as Selling, General and Administrative Expenses. Services to be provided over the three-year contract include constructing and assembling centrifuge machines and related infrastructure, and training and qualifying the workforce for operation of the facility. When estimates of total costs for such an integrated, construction-type contract exceed estimates of total revenue to be earned, a provision for the remaining loss on the contract is recorded to Cost of Sales in the period the loss is determined. Our corporate costs supporting the program are recognized as expense, as incurred over the duration of the contract term. The accrued loss on the contract is being adjusted over the remaining contract term based on actual results, remaining program cost projections, and the Company’s anticipated cost-share.

Further, while we still anticipate completing construction of the cascade in 2022, due to a COVID-19 related supply chain delay in the DOE-supplied HALEU storage cylinders, production will commence under another contract that the DOE plans to compete later this year. The U.S. government has been operating under a series of continuing resolutions in Fiscal Year 2022. The DOE continues to support the HALEU program during the continuing resolution period, and has incrementally increased the government’s cost share ceiling as funds have become available. Currently, DOE has provided incremental funding, and increased the government’s cost share ceiling to $126.7 million. For further discussion, refer to Item 7, Management Discussion and Analysis, of this 10-K report.

Our HALEU Contract expires June 1, 2022, and although we believe demand for HALEU will emerge over the next several years, there are no guarantees about whether or when government or commercial demand for HALEU will materialize, and there are a number of technical, regulatory and economic hurdles that must be overcome for these fuels and reactors to come to the market.

Commercial Contracting

In 2018, we entered into two services agreements with X-energy to provide technical and resource support for the conceptual and preliminary design of its Tri-Structural Isotropic (“TRISO”) fuel manufacturing process. Both of these contracts have been completed. In August 2021, we entered into a new services agreement with X-energy to provide design services for detailed design of the TRISO fuel manufacturing facility and various support services for establishing their TRISO Research and Development Center. The task orders under the new agreement may include in-kind contributions that we are not currently, but may provide, at our discretion.

11

Competition and Foreign Trade

It is estimated that the enrichment industry market for commercial nuclear reactors powered by low enriched uranium (“LEU”) is currently about 57.5 million SWU per year. Our global market share of enrichment for the LEU market is less than 5%. Global LEU suppliers in our highly competitive industry compete on the basis of price and reliability of supply. The four largest LEU suppliers comprise over 95% of market share combined:

•ROSATOM, a Russian government entity, which sells LEU through its wholly-owned subsidiary TENEX;

•Urenco, a consortium of companies owned or controlled by the British and Dutch governments and two German utilities;

•Orano, a company largely owned by the French government that was formerly part of the French government; and

•China Nuclear Energy Industry Corporation (“CNEIC”), a company owned by the Chinese government.

The production capacity for ROSATOM/TENEX is estimated by the World Nuclear Association to be approximately 28.7 million SWU per year. Imports of LEU and other uranium products produced in the Russian Federation are subject to restrictions as described below under — Russian Suspension Agreement.

Urenco reported installed capacity at its European and U.S. enrichment facilities of 19.6 million SWU per year at the end of 2020.

Orano’s gas centrifuge enrichment plant in France began commercial operations in 2011 and the plant’s nominal capacity of 7.5 million SWU was reportedly in service at the end of 2016. Orano has reported that it has suspended planned capacity expansions beyond 7.5 million SWU.

CNEIC has emerged as a significant producer primarily focused on supplying domestic requirements in China. CNEIC’s commercial SWU production capacity is estimated to be approximately 10.7 million SWU per year in 2020.

All of our current competitors are owned or controlled, in whole or in part, by foreign governments, and operate enrichment technologies developed with the financial support of foreign governments. These competitors may make business decisions in both domestic and international markets that are influenced by political or economic policy considerations rather than exclusively by commercial considerations.

LEU also may be produced by down-blending government stockpiles of highly-enriched uranium. Governments control the timing and availability of highly-enriched uranium released for this purpose, and the release of this material to the market could impact market conditions. Given the current oversupplied nuclear fuel market, any additional LEU from down-blended highly-enriched uranium released into the market would have a negative effect on prices for LEU.

Our LEU supply to foreign customers is exported under the terms of international agreements governing nuclear cooperation between the United States and the government of the country of destination or other entities, such as the European Union or the International Atomic Energy Agency. The LEU supplied to us is subject to the terms of cooperation agreements between the country in which the material is produced and the country of destination or other entities.

12

Russian Suspension Agreement

Imports into the United States of LEU and other uranium products produced in the Russian Federation, including LEU imported by Centrus under the TENEX Supply Contract, are subject, through December 31, 2040, to quotas imposed under U.S. legislation enacted into law in September 2008 and December 2020, and under the RSA, as amended in 2008 and 2020. These quotas limit the amount of Russian LEU that can be imported into the United States for U.S. consumption1.

The RSA is a trade agreement between the DOC and the Russian State Atomic Energy Corporation (“ROSATOM”) originally signed in 1992 suspended an anti-dumping duty investigation of Russian uranium, and imposed quantitative limits on exports of Russian uranium products, including LEU, to the United States. Under an amendment signed on October 5, 2020, the RSA’s limits on shipments of Russian uranium product to the United States were extended through at least 2040. Additionally, under legislation passed by the U.S. Congress shortly after the amendment was signed, the material terms of the extended RSA were enacted into law.

Under this law and the RSA, imports of Russian uranium products will peak in 2023 at 24% of the forecasted U.S. demand for enrichment and then begin to decline, reaching 15% by 2028. Despite the fact that overall limits will ramp down, the RSA extension agreement explicitly sets aside sufficient quota in 2021-2028 for Centrus. The RSA and the legislation provide for a revision of the quotas in 2023, 2029, and 2035 to take account of SWU demand forecasts that will be published by the WNA in the future. Any quota adjustment or other change to the RSA could affect our ability to implement the TENEX Supply Contract through sales to customers who take delivery in the United States, which is our most significant market.

The actual size of the annual quotas allocated to Centrus for the TENEX Supply Contract are confidential, but a public version of the quotas shows that they represent a significant portion of the total quotas provided under the RSA in 2021-2028. The quotas provided for the TENEX Supply Contract are expected to be adequate to support the Company’s long-term strategic goals and to permit enriched uranium procured from TENEX during the remaining term of the TENEX Supply Contract to be imported to supply U.S. utilities, thereby securing a key part of the Company’s supply base for the benefit of its customers and providing the revenues needed by the Company to support its work on HALEU and other advanced technology projects in the United States.

For further details, refer to Part I, Item 1A, Risk Factors - Our future prospects are tied directly to the nuclear energy industry worldwide, and the financial difficulties experienced by, and operating conditions of, our customers and suppliers could adversely affect our results of operations and financial condition.

Other Actions Adversely Affecting International Trade

In 2018, in connection with the withdrawal by the United States from a 2015 multilateral agreement known as the Joint Comprehensive Plan of Action (“JCPOA”) the U.S. government re-imposed sanctions on Iran’s Atomic Energy Organization of Iran (“AEOI”) and a number of its subsidiaries. Waivers were granted to allow non-Iranian entities to continue to work on certain programs that, among other things, allowed affiliates of ROSATOM to continue work on nuclear projects in Iran. These waivers have expired or been terminated and as a result, the U.S. government could decide to impose sanctions on Russian entities that may be involved in nuclear work in Iran, including ROSATOM or its subsidiaries. These sanctions could affect companies owned by ROSATOM, including TENEX, even if they are not doing work in Iran. To date, no sanctions have been imposed or announced on TENEX or any other ROSATOM subsidiary involved in the TENEX Supply Contract, in respect to the work of ROSATOM or its subsidiaries in Iran.

1 The term “quota” is used herein for simplicity. The amounts of Russian uranium products that can be shipped to the United States are referred to as export limits in the RSA and import limits in the legislation, but from a practical perspective have identical effect.

13

DOE Facilities

We produced LEU through 2001 at the former Portsmouth Gaseous Diffusion Plant (“Portsmouth GDP”) in Piketon, Ohio and through 2013 at the former Paducah GDP in Paducah, Kentucky, which we had leased from DOE. We currently store our existing inventory at third-party offsite licensed locations under agreements with the operators of those facilities. The Portsmouth GDP and Paducah GDP were operated by agencies of the U.S. government for more than 40 years prior to the creation of the Company through privatization of the Government enterprise in 1998. As a result of such operation, there are contamination and other potential environmental liabilities associated with the Government’s prior operation of the plants. The USEC Privatization Act and our former leases for the plants provide that DOE remains responsible for the decontamination and decommissioning (“D&D”) of the gaseous diffusion plants. Further, DOE continued operations as well as cleanup activities, both during and subsequent, to our operations at the facilities.

We lease facilities and related personal property near Piketon, Ohio from DOE. In connection with a letter agreement that preceded the HALEU Contract, DOE and Centrus amended the lease agreement, which was scheduled to expire by its terms on June 30, 2019. The lease was extended until May 31, 2022. In September 2021, the Company and the DOE renewed and extended the lease until December 31, 2025. Any facilities or equipment constructed or installed under the HALEU Contract, or other contract with DOE will be owned by DOE and may be returned to DOE in an “as is” condition at the end of the lease term. DOE will be responsible for the D&D of any returned facilities or equipment. If we determine the equipment and facilities may benefit Centrus after completion of the HALEU program, we can extend the facility lease and ownership of the equipment will be transferred to us, subject to mutual agreement regarding D&D and other issues, including those impacted by DOE’s recent decision to competitively award a separate contract for operations of the HALEU cascade following the expiration of our HALEU Contract, which may be awarded to a third party.

14

Human Capital Management

Our employees in Maryland, Ohio, and Tennessee are dedicated to our corporate philosophy based in honesty, trust, and with the highest levels of integrity, safety and security. Every day these values drive how we operate our business; govern how we interact with each other and our customers, partners, and suppliers; guide the way that we treat our workforce; and determine how we connect with our communities. Our commitment to ethical business practices is outlined in our Code of Business Conduct. Each employee is required to acknowledge receipt, understanding of, and compliance with our standards.

Due to the highly specialized nature of our business we need to hire and train skilled and qualified personnel to design, build, and operate our state of the art equipment, and to perform a broad range of services to support our country and our customers. Our work requires that we attract people who are dedicated to consistently performing quality work and, for many of our positions, are able to obtain a security clearance. We recognize that our success as a company depends on our ability to attract, develop, and retain such a workforce. We are dedicated to promoting the health, welfare and safety of our employees. Part of our responsibility includes treating all employees with dignity and respect and providing them with fair, market-based, competitive, and equitable compensation. We recognize and reward the performance of our employees in line with our pay-for-performance philosophy and provide a comprehensive suite of benefit options that enables our employees and their dependents to live healthy and productive lives.

Safety in our workplaces is paramount. We take measures to prevent workplace hazards, encourage safe behaviors and enforce a culture of continuous improvement to ensure our processes help eliminate incidents and injuries and comply with governing health and safety laws.

We are committed to promoting diversity of thought, experience, perspectives, backgrounds, and capabilities to drive innovation and to strengthen the solutions we deliver to our customers because we believe this diversity leads to better outcomes. We proudly support a culture of inclusion and encourage a work environment that respects diverse opinions, values individual skills, and celebrates the unique experiences our employees possess. To ensure a diverse group of candidates is considered for each opening we enlist the services of a Human Resource Consulting firm that provides services and products related to Affirmative Action Programs (“AAPs”) and equal employment opportunity as required by the U.S. Department of Labor's Office of Federal Contract Compliance Programs (“OFCCP”).

Our values motivate us to promote strong workplace practices with opportunities for development and training. Our training and development efforts focus on ensuring that the workforce is appropriately trained on critical job skills as well as leadership attributes that are consistent with our philosophy. During the COVID-19 pandemic, we transitioned our headquarters staff to work from home. We have endeavored to maintain the highest levels of safety for our operations staff, who are in open offices, with enforcement of social distancing, face masks, and also 100% daily temperature screening. All non-bargaining unit employees of the Company, including those working from home, are either fully vaccinated (95%) against the COVID-19 virus or working with accommodations (5%).

A summary of our employees by location is as follows:

| No. of Employees at December 31, | ||||||||||||||

| Location | 2021 | 2020 | ||||||||||||

| Piketon, OH | 115 | 107 | ||||||||||||

| Oak Ridge, TN | 101 | 105 | ||||||||||||

| Bethesda, MD | 50 | 53 | ||||||||||||

| Other | — | 2 | ||||||||||||

| Total Employees | 266 | 267 | ||||||||||||

15

On January 16, 2020, members of the United Steelworkers (“USW”) Local 689-5 ratified a new collective bargaining agreement for the employees represented by the USW at the advanced technology facility near Piketon, Ohio. The contract term is through October 1, 2022.

16

Executive Officers

Executive officers are elected by and serve at the discretion of the Board of Directors. The Executive officers as of December 31, 2021, are as follows:

| Name | Age | Position | ||||||

| Daniel B. Poneman | 65 | President and Chief Executive Officer | ||||||

| Larry B. Cutlip | 62 | Senior Vice President, Field Operations | ||||||

| Dennis J. Scott | 62 | Senior Vice President, General Counsel, Chief Compliance Officer and Corporate Secretary | ||||||

| Philip O. Strawbridge | 67 | Senior Vice President, Chief Financial Officer, Chief Administrative Officer and Treasurer | ||||||

| John M.A. Donelson | 57 | Senior Vice President and Chief Marketing Officer | ||||||

Daniel B. Poneman has been President and Chief Executive Officer since April 2015 and was Chief Strategic Officer in March 2015. Prior to joining the Company, Mr. Poneman was Deputy Secretary of Energy from May 2009 to October 2014, in which capacity he also served as Chief Operating Officer of DOE.

Larry B. Cutlip has been Senior Vice President, Field Operations since January 2018, was Vice President, Field Operations from May 2016 through December 2017, was Deputy Director of the American Centrifuge Project from January 2015 to May 2016, was Director, Centrifuge Manufacturing from April 2008 to December 2014, was Director, Program Management and Strategic Planning from December 2005 to April 2008, was Manager, Engineering from May 1999 to December 2005, and held positions in operations management and engineering at the Company and its predecessors since 1981.

Dennis J. Scott has been Senior Vice President, General Counsel, Chief Compliance Officer and Corporate Secretary since January 2018 and was Vice President, General Counsel, Chief Compliance Officer and Corporate Secretary from May 2016 through December 2017. Mr. Scott was Deputy General Counsel and Director, Corporate Compliance from April 2011 to May 2016, Acting Deputy General Counsel from August 2010 to April 2011, Assistant General Counsel and Director, Corporate Compliance from April 2005 to August 2010 and Assistant General Counsel from January 1994 to April 2005.

Philip O. Strawbridge has been Senior Vice President, Chief Financial Officer, Chief Administrative Officer and Treasurer since September 2019. Prior to joining the Company, Mr. Strawbridge served as an executive adviser at Court Square Capital from 2010 to 2013. Mr. Strawbridge served in various executive positions including Chief Financial Officer at EnergySolutions, a nuclear services and technology company, from 2006 to 2010. He was Chief Executive Officer and Chief Operating Officer of BNG America, which provided nuclear waste management services and technology to U.S. Government and commercial clients, from 1999 until BNG America was acquired by EnergySolutions in early 2006.

John M.A. Donelson has been Senior Vice President and Chief Marketing Officer since October 2019 and was Vice President, Sales and Chief Marketing Officer from January 2018 through October 2019. Mr. Donelson was Vice President, Marketing, Sales and Power from April 2011 through December 2017, Vice President, Marketing and Sales from December 2005 to April 2011, Director, North American and European Sales from June 2004 to December 2005, Director, North American Sales from August 2000 to June 2004 and Senior Sales Executive from July 1999 to August 2000.

17

Available Information

Our website is www.centrusenergy.com. We make available on our website, or upon request, without charge, access to our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed with, or furnished to, the Securities and Exchange Commission, pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as soon as reasonably practicable after such reports are electronically filed with, or furnished to, the Securities and Exchange Commission.

Our code of business conduct (the “Code of Business Conduct”) provides a brief summary of the standards of conduct that are at the foundation of our business operations. The Code of Business Conduct states that we conduct our business in strict compliance with all applicable laws. Each employee must read the Code of Business Conduct and sign a form stating that he or she has read, understands and agrees to comply with the Code of Business Conduct. A copy of the Code of Business Conduct is available on our website or upon request without charge. We will disclose on the website any amendments to, or waivers from, the code of business conduct that are required to be publicly disclosed.

We also make available on our website or upon request, free of charge, our Code of Business Conduct, Board of Directors Governance Guidelines, and our Board committee charters.

18

Item 1A. Risk Factors

The following discussion sets forth the material risk factors that could affect our financial condition and operations. Readers should not consider any descriptions to be a complete set of all potential risks that could affect us.

War in Ukraine

The current war in Ukraine has led to the U.S., Russia and other countries imposing sanctions and other measures that restrict international trade. The situation is rapidly changing, and it is not possible to predict future actions that could be taken. The Company has multiple sources of supply; however, the supply contract with Tenex remains our largest source. At present, sanctions have not impacted the ability of the Company or TENEX to perform under the TENEX supply contract. Recently sanctions have been imposed by the U.S. on exports of fossil fuels. Russia has imposed sanctions on the export of commodities but does not include the export of LEU. Additional sanctions or other measures by the U.S. or foreign governments (including the Russian government) could be imposed. Any sanctions or measures directed at trade in LEU from Russia or the parties involved in such trade or otherwise could interfere with, or prevent, implementation of the TENEX Supply Contract. While the initial sanctions announced do not affect the ability of the Company or TENEX to implement the TENEX Supply Contract, the situation at this time is unpredictable and therefore there is no assurance that future developments would not have a material adverse effect on the Company’s procurement, payment, delivery or sale of LEU under the TENEX Supply Contract.

If measures were taken to limit the supply of Russian LEU or to prohibit or limit dealings with Russian entities, including, but not limited to, TENEX or ROSATOM, the Company would seek a license, waiver or other approval from the government imposing such measures to ensure that the Company could continue to fulfill its purchase and sales obligations. There is no assurance that such a license, waiver, or approval would be granted. If a license, waiver or approval were not granted, the Company would need to look to alternative sources of LEU to replace the LEU that it could not procure from TENEX. The Company has contracts for alternative sources that could be used to mitigate a portion of the near term impacts. However, to the extent these sources were insufficient or more expensive or additional supply cannot be obtained, it could have a material adverse impact on our business, results of operations, and competitive position.

Economic and Industry Risks

Our future prospects are tied directly to the nuclear energy industry worldwide, and the financial difficulties experienced by, and operating conditions of, our customers and suppliers could adversely affect our results of operations and financial condition.

Potential events that could affect either our customers or suppliers under current or future contracts with us or the nuclear industry as a whole, include:

•pandemics, armed conflicts (including the war in Ukraine), government actions and other events that disrupt supply chains, production, transportation, payments and importation of nuclear materials or other critical supplies or services;

•natural or other disasters (such as the 2011 Fukushima disaster) impacting nuclear facilities or involving shipments of nuclear materials;

•changes in U.S. or foreign government policies and priorities;

•regulatory actions or changes in regulations by nuclear regulatory bodies applicable to us, our suppliers or our customers;

•decisions by agencies, courts or other bodies under applicable trade and other laws applicable to us, our suppliers or our customers;

•disruptions in other areas of the nuclear fuel cycle, such as uranium supplies or conversion;

•civic opposition to, or changes in government policies regarding, nuclear operations;

•business decisions concerning reactors or reactor operations;

19

•the financial condition of reactor owners and operations;

•the need for generating capacity; or

•consolidation within the electric power industry.

These events could adversely affect us to the extent they result in a reduction or elimination of customers’ contractual requirements to purchase from us; the suspension or reduction of nuclear reactor operations; the reduction or blocking of supplies of raw materials, natural or enriched uranium or separative work units (SWU), lower demand, burdensome regulation, disruptions of shipments, production importation or payment (including the blocking or restriction of transportation services or hardware); increased competition from third parties; and increased costs or difficulties or increased liability for actual or threatened property damage or personal injury. Additionally, customers may face financial difficulties, including from factors unrelated to the nuclear industry, that could affect their willingness or ability to make purchases. We cannot provide any assurance that events will not preclude us from making deliveries to our customers, increase our costs or that our customers, suppliers, or contractors will not default on their obligations to us or file for bankruptcy protection. If a customer files for bankruptcy protection, for example, we likely would be unable to collect all, or even a significant portion, of amounts that are owed to us. A default and bankruptcy filing by one or more customers or suppliers, or events (such as government actions) which prevent or limit our ability to obtain or sell material or services, could have a material adverse effect on our business, financial position, results of operations, or cash flows.

Our business, financial and operating performance could be adversely affected by epidemics and other health related issues including but not limited to the coronavirus disease 2019 (“COVID-19”) pandemic.

The global outbreak of COVID-19 was declared a pandemic by the World Health Organization and a national emergency by the U.S. Government and has negatively affected the U.S. and global economies, disrupted supply chains, and has resulted in significant travel, transport, and other restrictions. The COVID-19 outbreak has disrupted the supply chains and day-to-day operations of the Company, our suppliers, our contractors, and our customers, which could materially adversely affect our operations. In this regard, global supply chains and the timely availability of products or product components sourced domestically or imported from other nations, including SWU contained in LEU we purchase, could be materially disrupted by quarantines, slowdowns or shutdowns, border closings, and travel restrictions resulting from the global COVID-19 pandemic or other global pandemic or health crises. Further, impacts of COVID-19 infections and other COVID-19 pandemic related impacts on our management and workforce, or our suppliers, contractors, or customers, could adversely impact our business. While we have taken steps to protect our workforce and carry on operations, we may not be able to mitigate all of the potential impacts. We anticipate increased costs related to, or resulting from, the COVID-19 pandemic, due to, among other things, delays in supplier deliveries, impacts of travel restrictions, site access and quarantine requirements, and the impacts of remote work and adjusted work schedules.

The impacts of the COVID-19 pandemic have been primarily affecting our technical solutions segment since much of the work required under the HALEU Contract must be performed on the Company’s sites and on our suppliers’ sites. As a result, our costs under the HALEU Contract have been impacted. Further, as a result of the U.S. Department of Energy (“DOE”) not supplying us cylinders as required under the HALEU Contract, operation of the cascade has been deferred and will be performed under a subsequent competitively bid contract that may or may not be awarded to us.

In the event that the COVID-19 pandemic prevents our employees or our contractors from working in-person at our site or, our suppliers are unable to provide goods and services on the schedule we anticipated, the impacts on our schedule and costs could be material. Again, while we have worked to mitigate the impact, we are experiencing increased costs as the result of the impact of the pandemic on their operations.

We continue to work with our customers, employees, contractors, suppliers and communities to address the impacts of the COVID-19 pandemic and to take actions in an effort to mitigate adverse consequences. However, the ultimate impact of the COVID-19 pandemic on our operations and financial performance in future periods,

20

including our ability to execute our strategic plan and programs in the expected timeframe, remains uncertain and will depend on future pandemic related developments, including the duration of the pandemic and any potential subsequent variants of COVID-19 and related government actions to prevent and manage disease spread, all of which are uncertain and cannot be predicted. The long-term impacts of the COVID-19 pandemic on us or on government budgets, our customers, contractors and suppliers that could impact our business are also difficult to predict but could adversely affect our business, results of operations, and prospects.

The continued excess supply of LEU in the market could adversely affect market prices and our business results.

Events related to the March 2011 earthquake and tsunami that caused irreparable damage to four reactors in Fukushima, Japan created an over-supply of nuclear fuel that continues to heavily influence market prices. In addition, reactor operators facing aggressive price competition from natural gas and subsidized renewable generation like wind and solar, have closed or are planning to close reactors, further reducing demand for our product and services. Despite the decrease in demand, some of our competitors supported by foreign governments continued to expand their capacity. Market uncertainty, and reduced demand, coupled with excess capacity and supply has adversely affected our ability to sell LEU and SWU and could adversely affect our business, results of operations, and prospects.

Our business is exposed to price volatility associated the procurement of SWU and uranium.

The Company is exposed to commodity price risk for purchases of SWU and uranium. Our earnings and cash flows are therefore exposed to variability of spot and forward market prices in the markets in which it operates. The supply markets for SWU and uranium are subject to price fluctuations and availability restrictions.

Operational Risks

Restrictions on imports or sales of SWU or uranium that we buy from our Russian supplier and our other sources of supply could adversely affect profitability and the viability of our business.

The majority of the SWU and LEU that we use to fill existing contracts with customers is sourced from outside the United States, including from Russia under the TENEX Supply Agreement, and we expect the arrangement to continue into the future. Our ability to place this SWU and LEU into existing and future contracts with customers is subject to trade restrictions, sanctions, and other limitations imposed by the United States and other governments and our customers. For example, our imports from Russia are subject to U.S. quotas. Given the quotas, restrictions, and customer limitations that limit our ability to sell SWU and LEU purchased under the TENEX Supply Agreement both in the United States and globally, there is no guarantee that we can make sufficient sales to meet our minimum purchase obligation under the TENEX Supply Agreement. (For further information refer to Part I, Item 1, Competition and Foreign Trade).

Further, currently evolving international events, including the war in Ukraine could result in new or additional sanctions or other U.S. or foreign government actions that could directly or indirectly limit or prevent our purchase, importation, or ability to sell material under our TENEX Supply Agreement. Even absent such restrictions, some of our U.S. and foreign customers are unable or unwilling to accept Russian SWU and uranium.

Geopolitical events, including domestic or international reactions or responses to such events, as well as concerns about national security or other issues, also could lead to U.S. or foreign government or international actions that could disrupt our ability to purchase, sell, or make deliveries of LEU, SWU, or other uranium products, or even to continue to do business with one or more of our suppliers or their affiliates. Our inability to meet our purchase or sales obligations, or to earn revenues from U.S. and international sales, would adversely affect our financial condition, results of operations, cash flows, and the viability of our business. All of these outcomes, individually and collectively, could cause us to incur significant financial losses, in addition to impeding or preventing us from fulfilling our existing contracts, or winning new contracts, and could adversely affect our profitability and the viability of our business.

21

We may be unable to sell all of the LEU we are required to purchase under supply agreements for prices that cover our costs, which could adversely affect profitability and the viability of our business.

We may not achieve the anticipated benefits from supply agreements we enter into. The prices we are charged under some supply agreements are determined by formulas that may not be aligned with the prevailing market prices at the time we enter into contracts with customers. As a result, the sales prices in our contracts may not cover our purchase costs, or those purchase costs may limit our ability to secure profitable sales.

We are dependent on purchases from our suppliers and other sources to meet our obligations to customers and rely on third parties to provide essential services.

We are currently dependent on purchases from suppliers to meet our obligations to customers, including purchases from the Russian government entity, TENEX. A significant delay in, or stoppage or termination of, deliveries of material to us under our supply agreements, could adversely affect our ability to make deliveries to customers. The recent action of Russian military forces in Ukraine has escalated tensions between Russia and the U.S. The U.S. has imposed, and is likely to impose additional, financial and economic sanctions and export controls against certain Russian organizations and/or individuals. Sanctions and export controls, as well as any actions by Russia, could adversely affect our supply and our ability to meet our obligations to customers.

We also rely on third parties to provide essential services to the Company, such as the storage and management of inventory, transportation, and radiation protection. Those service providers may not perform on time, with the desired quality, or at all for a variety of reasons, many of which are outside our control. An interruption of deliveries from our suppliers or the provision of essential services by third parties, could adversely impact our business, results of operations, and prospects.

We face significant competition from major producers who may be less cost sensitive or may be favored due to support from foreign governments.

We compete with major producers of LEU, all of which are wholly or substantially owned by governments: Orano (France), Rosatom/TENEX (Russia), Urenco (the Netherlands, the United Kingdom and two German utilities), and CNEIC (China). Our competitors have greater financial resources than we do. Foreign competitors enjoy financial and other support from their government owners, which may enable them to be less cost or profit-sensitive than we are. In addition, decisions by foreign competitors may be influenced by political and economic policy considerations rather than commercial considerations. For example, foreign competitors may elect to increase their production or exports of LEU, SWU, or other uranium products, including HALEU, even when not justified by market conditions, thereby depressing prices and reducing demand for our LEU, SWU, and other uranium products. This could adversely affect our business, results of operations, and prospects. Moreover, our competitors may be better positioned to take advantage of improved market conditions and increase capacity to meet any future market expansion.

The ability to compete in certain foreign markets may be limited for legal, political, economic or other reasons.