UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2021

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _______to_______

Commission File Number 001-03492

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

(281 ) 871-2699

(Registrant's telephone number, including area code)

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

| Securities registered pursuant to Section 12(g) of the Act: None | ||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated Filer | ☐ | ||||||||||||

| Non-accelerated Filer | ☐ | Smaller Reporting Company | ||||||||||||

| Emerging Growth Company | ||||||||||||||

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

The aggregate market value of Halliburton Company Common Stock held by non-affiliates on June 30, 2021, determined using the per share closing price on the New York Stock Exchange Composite tape of $23.12 on that date, was approximately $18.2 billion.

As of January 28, 2022, there were 898,571,517 shares of Halliburton Company Common Stock, $2.50 par value per share, outstanding.

Portions of the Halliburton Company Proxy Statement for our 2022 Annual Meeting of Shareholders (File No. 001-03492) are incorporated by reference into Part III of this report.

HALLIBURTON COMPANY

Index to Form 10-K

For the Year Ended December 31, 2021

| PART I | PAGE | |||||||

| PART II | ||||||||

| PART III | ||||||||

| PART IV | ||||||||

i

| Item 1 | Business | ||||||||

PART I

Item 1. Business.

Description of business and strategy

Halliburton Company is one of the world's largest providers of products and services to the energy industry. Its predecessor was established in 1919 and incorporated under the laws of the State of Delaware in 1924. Inspired by the past and leading into the future, what started with a single product from a single location is now a global enterprise. Our value proposition is to collaborate and engineer solutions to maximize asset value for our customers. We strive to achieve strong cash flows and returns for our shareholders by delivering technology and services that improve efficiency, increase recovery, and maximize production for our customers. We are proud of our over 100 years of operation, innovation, collaboration, and execution. Halliburton has fostered a culture of unparalleled service to the world's major, national, and independent oil and gas producers. With over 40,000 employees, representing 130 nationalities in more than 70 countries, we help our customers maximize asset value throughout the lifecycle of the reservoir - from locating hydrocarbons and managing geological data, to drilling and formation evaluation, well construction and completion, and optimizing production throughout the life of the asset.

2021 Highlights

- Financial: Internationally we delivered profitable growth with revenue and operating income increasing every quarter in 2021. In North America, strong operating leverage allowed us to maximize the value of our business as U.S. land activity rebounded. Overall, our Completion and Production and Drilling and Evaluation operating segments finished the year with 15% and 12% operating margins, respectively, and generated strong cash flows from operations.

- Digital: Our accelerated deployment and integration of digitally enabled technologies created technical differentiation in the market and contributed to our higher margins.

- Capital efficiency: We advanced technologies and made strategic choices that kept our capital expenditures to 5.2% of revenue, which is in the range of our 5-6% of revenue target.

- Sustainable energy: We announced our science-based emission reduction targets, added eleven new participating companies to Halliburton Labs, our clean energy accelerator, and were named to the Dow Jones Sustainability Index North America for Energy Equipment and Services, which highlights the top 10% most sustainable North America companies in identified industries as determined by S&P Global through their Corporate Sustainability Assessment.

2022 Focus

- International: Allocate our capital to the highest return opportunities, continue investing in digital technologies that maximize our asset value to drive profitable growth, and increase our international growth in our specialty chemicals and artificial lift businesses.

- North America: Continue to build on the operating leverage we have created, maximize cash flow by utilizing our premium low-emissions equipment, and continue developing differentiated technologies focused around the wellbore.

- Digital: Continue to accelerate the deployment and integration of digitalization and automation technologies that create differentiation, both internally and for our customers.

- Capital efficiency: Maintain our capital expenditures in the range of 5-6% of revenue while focusing on technological advancements and process changes that reduce our manufacturing and maintenance costs and improve how we move equipment and respond to market opportunities.

- Sustainable energy: Leverage the increasing number of participants in and scope of Halliburton Labs to gain insight into developing value chains in the clean energy space and continue to develop and deploy low-carbon solutions to help oil and gas operators lower their current emissions profiles while also using our existing technologies in renewable energy applications.

For further discussion on our business strategies, see "Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Business Environment and Results of Operations-Business Outlook."

Operating segments

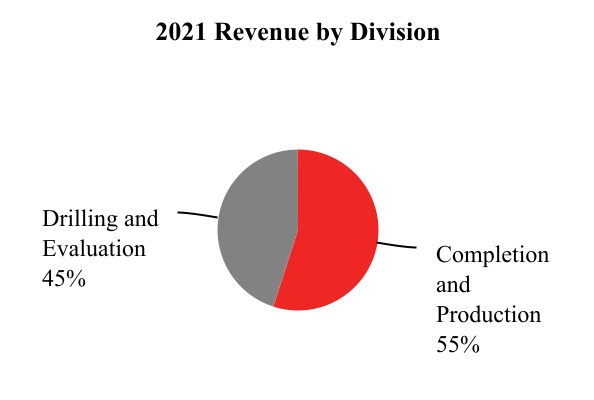

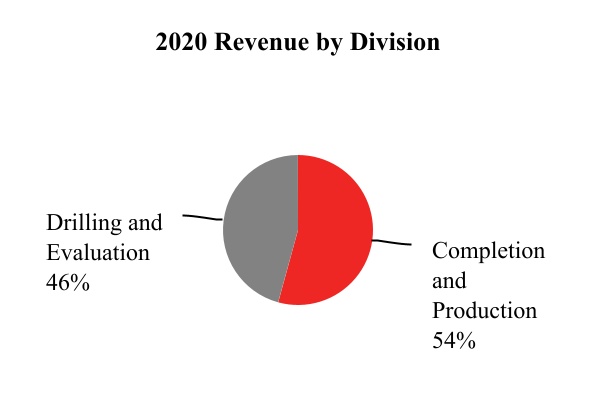

We operate under two divisions, which form the basis for the two operating segments we report, the Completion and Production segment and the Drilling and Evaluation segment.

Completion and Production delivers cementing, stimulation, intervention, pressure control, artificial lift, and completion products and services. The segment consists of the following product service lines:

HAL 2021 FORM 10-K | 1

| Item 1 | Business | ||||||||

- Production Enhancement: includes stimulation services and sand control services. Stimulation services optimize oil and natural gas reservoir production through a variety of pressure pumping services, and chemical processes, commonly known as hydraulic fracturing and acidizing. Sand control services include fluid and chemical systems for the prevention of formation sand production.

- Cementing: involves bonding the well and well casing while isolating fluid zones and maximizing wellbore stability. Our cementing product service line also provides casing equipment.

- Completion Tools: provides downhole solutions and services to our customers to complete their wells, including well completion products and services, intelligent well completions, liner hanger systems, sand control systems, multilateral systems, and service tools.

- Production Solutions: provides customized well intervention solutions to increase well performance, which includes coiled tubing, hydraulic workover units, downhole tools, pumping services, and nitrogen services.

- Artificial Lift: provides services to maximize reservoir and wellbore recovery by applying lifting technology, intelligent field management solutions, and related services throughout the life of the well, including electrical submersible pumps.

- Pipeline & Process Services: provides a complete range of pre-commissioning, commissioning, maintenance, and decommissioning services to the onshore and offshore pipeline and process plant construction commissioning and maintenance industries.

Drilling and Evaluation provides field and reservoir modeling, drilling, fluids and specialty chemicals, evaluation and precise wellbore placement solutions that enable customers to model, measure, drill, and optimize their well construction activities. The segment consists of the following product service lines:

- Baroid: provides drilling fluid systems, performance additives, completion fluids, solids control, specialized testing equipment, and waste management services for oil and natural gas drilling, completion, and workover operations. It also provides customized specialty oilfield completion, production, and downstream water and process treatment chemicals and services.

- Sperry Drilling: provides drilling systems and services that offer directional control for precise wellbore placement while providing important measurements about the characteristics of the drill string and geological formations while drilling wells. These services include directional and horizontal drilling, measurement-while-drilling, logging-while-drilling, surface data logging, and rig site information systems.

- Wireline and Perforating: provides open-hole logging services that supply information on formation evaluation and reservoir fluid analysis, including formation lithology, rock properties, and reservoir fluid properties. Also offered are cased-hole and slickline services, including perforating, pipe recovery services, through-casing formation evaluation and reservoir monitoring, casing and cement integrity measurements, and well intervention services.

- Drill Bits and Services: provides roller cone rock bits, fixed cutter bits, hole enlargement and related downhole tools and services used in drilling oil and natural gas wells. In addition, coring equipment and services are provided to acquire cores of the formation drilled for evaluation.

- Landmark Software and Services: provides cloud based digital services and artificial intelligence solutions on an open architecture for subsurface insights, integrated well construction, and reservoir and production management for the upstream oil and natural gas industry.

- Testing and Subsea: provides acquisition and analysis of dynamic reservoir information and reservoir optimization solutions to the oil and natural gas industry through a broad portfolio of test tools, data acquisition services, fluid sampling, surface well testing, subsea safety systems, and underbalanced applications.

- Halliburton Project Management: provides integrated solutions to our customers by leveraging the full line of our oilfield services, products, and technologies to solve customer challenges throughout the oilfield lifecycle, including project management and integrated asset management.

HAL 2021 FORM 10-K | 2

| Item 1 | Business | ||||||||

The following charts depict our revenue split between our two operating segments for the years ended December 31, 2021 and 2020.

See Note 3 to the consolidated financial statements for further financial information related to each of our business segments.

Markets and competition

We are one of the world’s largest diversified energy services companies. Our services and products are sold in highly competitive markets throughout the world. Competitive factors impacting sales of our services and products include: price; service delivery; health, safety, and environmental standards and practices; service quality; global talent retention; understanding the geological characteristics of the hydrocarbon reservoir; product quality; warranty; and technical proficiency.

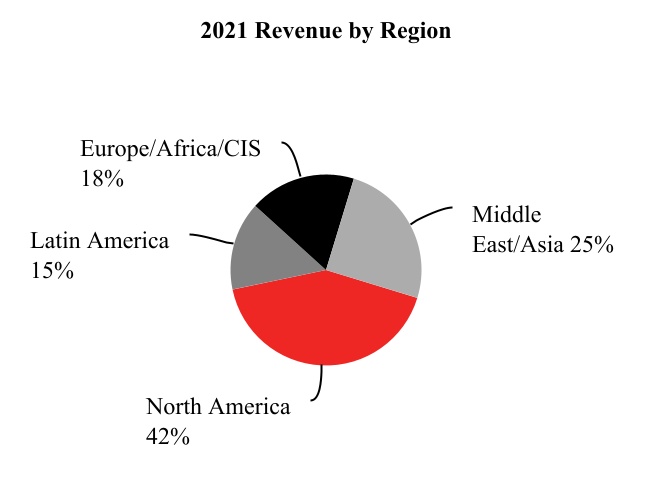

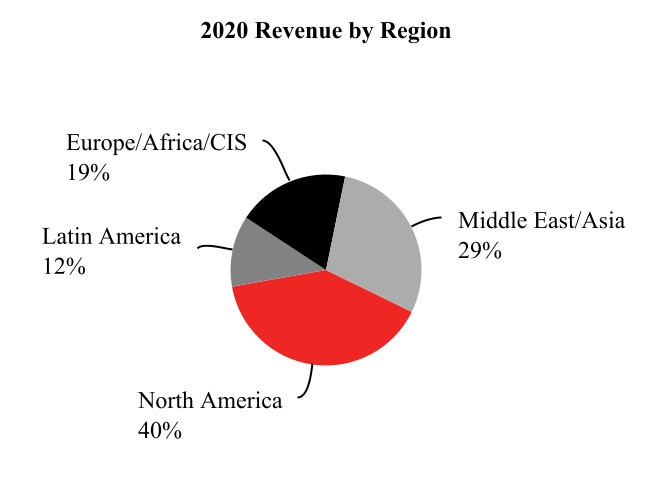

We conduct business worldwide in more than 70 countries. The business operations of our divisions are organized around four primary geographic regions: North America, Latin America, Europe/Africa/CIS, and Middle East/Asia. In 2021, 2020, and 2019, based on the location of services provided and products sold, 40%, 38%, and 51%, respectively, of our consolidated revenue was from the United States. No other country accounted for more than 10% of our consolidated revenue during these periods. See "Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” for additional information about our geographic operations. Because the markets for our services and products are vast and cross numerous geographic lines, it is not practicable to provide a meaningful estimate of the total number of our competitors. The industries we serve are highly competitive, and we have many substantial competitors. Most of our services and products are marketed through our service and sales organizations.

The following charts depict our revenue split between our four primary geographic regions for the years ended December 31, 2021 and 2020.

HAL 2021 FORM 10-K | 3

| Item 1 | Business | ||||||||

Our operations in some countries may be adversely affected by unsettled political conditions, acts of terrorism, civil unrest, force majeure, war or other armed conflict, health or similar issues, sanctions, expropriation or other governmental actions, inflation, changes in foreign currency exchange rates, foreign currency exchange restrictions and highly inflationary currencies, as well as other geopolitical factors. We believe the geographic diversification of our business activities reduces the risk that an interruption of operations in any one country, other than the United States, would be materially adverse to our business, consolidated results of operations, or consolidated financial condition.

Information regarding our exposure to foreign currency fluctuations, risk concentration, and financial instruments used to minimize risk is included in "Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Financial Instrument Market Risk” and in Note 15 to the consolidated financial statements.

Customers

Our revenue during the past three years was derived from the sale of services and products to the energy industry. No single customer represented more than 10% of our consolidated revenue in any period presented.

Raw materials

Raw materials essential to our business are normally readily available. Market conditions can trigger constraints in the supply of certain raw materials, such as proppants (primarily sand), hydrochloric acid, and gels. We are always striving to ensure the availability of resources and manage raw material costs. Our procurement department uses our relationships and buying power to enhance our access to key materials at competitive prices.

Patents

We own a large number of patents and have pending a substantial number of patent applications covering various products and processes. We are also licensed to utilize technology covered by patents owned by others, and we license others to utilize technology covered by our patents. We do not consider any particular patent to be material to our business operations.

Seasonality

Weather and natural phenomena can temporarily affect the performance of our services, but the widespread geographical locations of our operations mitigate those effects. Examples of how weather can impact our business include:

- the severity and duration of the winter in North America can have a significant impact on drilling activity and on natural gas storage levels;

- the timing and duration of the spring thaw in Canada directly affects activity levels due to road restrictions;

- typhoons and hurricanes can disrupt coastal and offshore operations; and

- severe weather during the winter normally results in reduced activity levels in the North Sea and Russia.

Additionally, customer spending patterns for completion tools typically result in higher activity in the fourth quarter of the year. We recognize revenue on customer software contract sales predominantly in the first and fourth quarters of the year.

Our workforce

Our workforce is our top asset in enabling us to accomplish innovative, high-quality work for our customers and to address the world’s energy challenges. To attract and retain talent, we strive to provide a safe and inclusive working environment along with competitive benefits. As of December 31, 2021, we employed over 40,000 people worldwide representing 130 nationalities, operated in more than 70 countries, and approximately 18% of our employees were subject to collective bargaining agreements. Based upon the geographic diversification of our employees, we do not believe any risk of loss from employee strikes or other collective actions are material to the conduct of our operations taken as a whole.

Recruiting and Turnover

Given the size and geographic scope of our workforce, we have a robust world-wide recruiting apparatus, which includes personnel devoted to recruiting and retention, online job postings, and recruiting programs we have established at academic institutions for internships and entry-level roles. In order to increase the number of diverse employees, we have developed relationships with diversity-focused student organizations, provide professional development sessions to students, engage our Employee Resource Groups (ERGs) to participate in select university events, and participate in outreach efforts through programs supported by our Educational Advisory Board.

Our attrition in 2021 was down significantly compared to 2020 and we were able to rehire more than 2,800 former employees in 2021, despite a tight labor market. We have found that hiring former employees allows us to add needed personnel who are able to apply their experience and contribute quickly.

HAL 2021 FORM 10-K | 4

| Item 1 | Business | ||||||||

Diversity, equity, and inclusion

With our large employee base and global breadth, we are one of the world’s most diverse companies. Our Code of Business Conduct describes our commitment to diversity, equity, and inclusion, which is supported by our recruitment and employment practices. It is a priority to continue to increase the diversity of our workforce, both in general and in leadership positions. Furthermore, we strive to increase the percentage of local nationals that we employ in each region of operations to better communicate with local customers and other contractors, share knowledge of the culture and values of the local population, improve local economies, and make our workforce more representative of the populations where we provide our services. In 2021, 92% of our workforce and 86% of management was localized. In 2021, 13% of our workforce and 13% of our managers were female.

Leadership

We have more than 8,000 employees in management roles. The ongoing identification and development of leadership talent ensures business continuity and strengthens our competitive advantage, both of which are critical for our short and long-term success. In 2021, we identified approximately 18,000 potential successors for our managers during succession management planning. One of our most significant investments in the development of our future leaders is our executive education programs. In 2021, approximately 25% of the participants in these programs were female and 40 different nationalities were represented, despite travel restrictions impacting many countries.

As part of our commitment to employee engagement, we solicit feedback from employees on their workplace challenges, and empower them to share their perspectives and ideas to improve the overall employee experience, including performance, development, and work-life balance. Notably, according to a survey we conducted in 2021, 87% of our employees felt that Halliburton and their colleagues value their unique traits and ways of working.

Benefits and well-being

We provide our employees around the world with benefits that address the needs of our workforce and their families. We evaluate our benefits package to identify opportunities for improvement and to remain competitive. In 2021, we enhanced healthcare benefits for United States employees to help them better plan for medical expenditures and to obtain additional support in getting second medical opinions and navigating health plans. In response to ongoing mental health concerns related to the COVID-19 pandemic, we expanded our Employee Assistance Program (EAP) from six countries to 43 countries worldwide. By the end of 2021, more than 32,000 employees had access to the EAP compared to approximately 14,500 in 2020.

Safety

Safety in the workplace is one of our highest priorities. We have many safety programs in place, including our Journey to ZERO initiative, to maintain our strong performance and improve proactive identification and management of safety risks. In 2021, we enhanced risk management processes, incident investigations, and training, including options for virtual training when feasible. As a result of our focus on safety, for the years ended December 31, 2021 and December 31, 2020, our recordable incident rates were 0.25% and 0.20%, non-productive times were 0.30% and 0.30%, lost-time incident rates were 0.09% and 0.06%, preventable recordable vehicle incident rates were 0.16% and 0.06%, respectively, and there were no job related fatalities in either year.

Government regulation

We are subject to numerous environmental, legal, and regulatory requirements related to our operations worldwide. For further information related to environmental matters and regulation, see Note 10 to the consolidated financial statements and "Item 1(a). Risk Factors.”

Hydraulic fracturing

Hydraulic fracturing is a process that creates fractures extending from the well bore into the rock formation to enable natural gas or oil to move more easily from the rock pores to a production conduit. A significant portion of our Completion and Production segment provides hydraulic fracturing services to customers developing shale natural gas and shale oil. From time to time, questions arise about the scope of our operations in the shale natural gas and shale oil sectors, and the extent to which these operations may affect human health and the environment.

HAL 2021 FORM 10-K | 5

| Item 1 | Business | ||||||||

At the direction of our customer, we design and generally implement a hydraulic fracturing operation to stimulate the well's production, once the well has been drilled, cased, and cemented. Our customer is generally responsible for providing the base fluid (usually water) used in the hydraulic fracturing of a well. We frequently supply the proppant (primarily sand) and at least a portion of the additives used in the overall fracturing fluid mixture. In addition, we mix the additives and proppant with the base fluid and pump the mixture down the wellbore to create the desired fractures in the target formation. The customer is responsible for disposing and/or recycling for further use any materials that are subsequently produced or pumped out of the well, including flowback fluids and produced water.

As part of the process of constructing the well, the customer will take a number of steps designed to protect drinking water resources. In particular, the casing and cementing of the well are designed to provide 'zonal isolation' so that the fluids pumped down the wellbore and the oil and natural gas and other materials that are subsequently pumped out of the well will not come into contact with shallow aquifers or other shallow formations through which those materials could potentially migrate to freshwater aquifers or the surface.

The potential environmental impacts of hydraulic fracturing have been studied by numerous government entities and others. In 2004, the United States Environmental Protection Agency (EPA) conducted an extensive study of hydraulic fracturing practices, focusing on coalbed methane wells, and their potential effect on underground sources of drinking water. The EPA’s study concluded that hydraulic fracturing of coalbed methane wells poses little or no threat to underground sources of drinking water. In December 2016, the EPA released a final report, “Hydraulic Fracturing for Oil and Gas: Impacts from the Hydraulic Fracturing Water Cycle on Drinking Water Resources in the United States” representing the culmination of a six-year study requested by Congress. While the EPA report noted a potential for some impact to drinking water sources caused by hydraulic fracturing, the agency confirmed the overall incidence of impacts is low. Moreover, a number of the areas of potential impact identified in the report involve activities for which we are not generally responsible, such as potential impacts associated with withdrawals of surface water for use as a base fluid and management of wastewater.

We have proactively developed processes to provide our customers with the chemical constituents of our hydraulic fracturing fluids to enable our customers to comply with state laws as well as voluntary standards established by the Chemical Disclosure Registry, www.fracfocus.org. We have invested considerable resources in developing hydraulic fracturing technologies, in both the equipment and chemistry portions of our business, which offer our customers a variety of environment-friendly options related to the use of hydraulic fracturing fluid additives and other aspects of our hydraulic fracturing operations. We created a hydraulic fracturing fluid system comprised of materials sourced entirely from the food industry. In addition, we have engineered a process that uses ultraviolet light to control the growth of bacteria in hydraulic fracturing fluids, allowing customers to minimize the use of chemical biocides. We are committed to the continued development of innovative chemical and mechanical technologies that allow for more economical and environment-friendly development of the world’s oil and natural gas reserves, and that reduce noise while complying with Tier 4 lower emission legislation.

In evaluating any environmental risks that may be associated with our hydraulic fracturing services, it is helpful to understand the role that we play in the development of shale natural gas and shale oil. Our principal task generally is to manage the process of injecting fracturing fluids into the borehole to stimulate the well. Thus, based on the provisions in our contracts and applicable law, the primary environmental risks we face are potential pre-injection spills or releases of stored fracturing fluids and potential spills or releases of fuel or other fluids associated with pumps, blenders, conveyors, or other above-ground equipment used in the hydraulic fracturing process.

Although possible concerns have been raised about hydraulic fracturing, the circumstances described above have helped to mitigate those concerns. To date, we have not been obligated to compensate any indemnified party for any environmental liability arising directly from hydraulic fracturing, although there can be no assurance that such obligations or liabilities will not arise in the future. For further information on risks related to hydraulic fracturing, see "Item 1(a). Risk Factors.”

Working capital

We fund our business operations through a combination of available cash and equivalents, short-term investments, and cash flow generated from operations. In addition, our revolving credit facility is available for additional working capital needs.

HAL 2021 FORM 10-K | 6

| Item 1 | Business | ||||||||

Web site access - www.halliburton.com

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished to the Securities and Exchange Commission (SEC) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available at www.halliburton.com soon thereafter. The SEC website www.sec.gov contains our reports, proxy and information statements and our other SEC filings. Our Code of Business Conduct, which applies to all our employees and Directors and serves as a code of ethics for our principal executive officer, principal financial officer, principal accounting officer, and other persons performing similar functions, can be found at www.halliburton.com. Any amendments to our Code of Business Conduct or any waivers from provisions of our Code of Business Conduct granted to the specified officers above are also disclosed on our web site within four business days after the date of any amendment or waiver pertaining to these officers. There have been no waivers from provisions of our Code of Business Conduct for the years 2021, 2020, or 2019. Except to the extent expressly stated otherwise, information contained on or accessible from our web site or any other web site is not incorporated by reference into this annual report on Form 10-K and should not be considered part of this report.

HAL 2021 FORM 10-K | 7

| Item 1 | Business | ||||||||

Executive Officers of the Registrant

The following table indicates the names and ages of the executive officers of Halliburton Company as of February 4, 2022, including all offices and positions held by each in the past five years:

| Name and Age | Offices Held and Term of Office | |||||||

| Van H. Beckwith (Age 56) | Executive Vice President, Secretary and Chief Legal Officer of Halliburton Company, since December 2020 | |||||||

| Senior Vice President and General Counsel, January 2020 to December 2020 | ||||||||

| Partner, Baker Botts L.L.P., January 1999 to December 2019 | ||||||||

| Eric J. Carre (Age 55) | Executive Vice President, Global Business Lines of Halliburton Company, since May 2016 | |||||||

| Charles E. Geer, Jr. (Age 51) | Senior Vice President and Chief Accounting Officer of Halliburton Company, since December 2019 | |||||||

Vice President and Corporate Controller of Halliburton Company, January 2015 to December 2019 | ||||||||

| Myrtle L. Jones (Age 62) | Senior Vice President, Tax of Halliburton Company, since March 2013 | |||||||

| Lance Loeffler (Age 44) | Executive Vice President and Chief Financial Officer of Halliburton Company, since November 2018 | |||||||

Vice President of Investor Relations of Halliburton Company, April 2016 to November 2018 | ||||||||

| Timothy M. McKeon (Age 49) | Senior Vice President and Treasurer of Halliburton Company, since January 2022 | |||||||

| Vice President and Treasurer of Halliburton Company, January 2014 to December 2021 | ||||||||

| Jeffrey A. Miller (Age 58) | Chairman of the Board, President and Chief Executive Officer of Halliburton Company, since January 2019 | |||||||

Member of the Board of Directors, President and Chief Executive Officer of Halliburton Company, June 2017 to December 2018 | ||||||||

Member of the Board of Directors and President of Halliburton Company, August 2014 to May 2017 | ||||||||

| Lawrence J. Pope (Age 53) | Executive Vice President of Administration and Chief Human Resources Officer of Halliburton Company, since January 2008 | |||||||

| Joe D. Rainey (Age 65) | President, Eastern Hemisphere of Halliburton Company, since January 2011 | |||||||

| Mark J. Richard (Age 60) | President, Western Hemisphere of Halliburton Company, since February 2019 | |||||||

Senior Vice President, Northern U.S. Region of Halliburton Company, August 2018 to January 2019 | ||||||||

Senior Vice President, Business Development and Marketing of Halliburton Company, November 2015 to July 2018 | ||||||||

| Jill D. Sharp (Age 51) | Senior Vice President, Internal Assurance Services of Halliburton Company, since January 2022 | |||||||

| Vice President, Internal Assurance Services of Halliburton Company, September 2021 to December 2021 | ||||||||

| Vice President, Finance - Western Hemisphere of Halliburton Company, October 2016 to August 2021 | ||||||||

There are no family relationships between the executive officers of the registrant or between any director and any executive officer of the registrant.

HAL 2021 FORM 10-K | 8

| Item 1(a) | Risk Factors | ||||||||

Item 1(a). Risk Factors.

When considering an investment in Halliburton Company, all of the risk factors described below and other information included and incorporated by reference in this annual report should be carefully considered. Any of these risk factors could have a significant or material adverse effect on our business, results of operations, financial condition, or cash flows. Additional risks and uncertainties not currently known to us or that we currently deem immaterial may also adversely affect our business, financial condition, results of operations, or cash flows.

Industry Environment Related

Trends in oil and natural gas prices affect the level of exploration, development, and production activity of our customers and the demand for our services and products, which could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Demand for our services and products is particularly sensitive to the level of exploration, development, and production activity of, and the corresponding capital spending by, oil and natural gas companies. The level of exploration, development, and production activity is directly affected by trends in oil and natural gas prices, which historically have been volatile and are likely to continue to be volatile. Prices for oil and natural gas are subject to large fluctuations in response to relatively minor changes in the supply of and demand for oil and natural gas, market uncertainty, and a variety of other economic factors that are beyond our control. Given the long-term nature of many large-scale development projects, even the perception of longer-term lower oil and natural gas prices by oil and natural gas companies can cause them to reduce or defer major expenditures. Any prolonged reductions of commodity prices or expectations of such reductions could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition, and could result in asset impairments and severance costs.

Factors affecting the prices of oil and natural gas include:

- the level of supply and demand for oil and natural gas;

- the ability or willingness of the Organization of Petroleum Exporting Countries and the expanded alliance collectively known as OPEC+ to set and maintain oil production levels;

- the level of oil production in the U.S. and by other non-OPEC+ countries;

- oil refining capacity and shifts in end-customer preferences toward fuel efficiency and the use of natural gas;

- the cost of, and constraints associated with, producing and delivering oil and natural gas;

- governmental regulations, including the policies of governments regarding the exploration for and production and development of their oil and natural gas reserves;

- weather conditions, natural disasters, and health or similar issues, such as pandemics or epidemics;

- worldwide political, military, and economic conditions; and

- increased demand for alternative energy and electric vehicles and increased emphasis on decarbonization, including government initiatives to promote the use of renewable energy sources and public sentiment around alternatives to oil and gas.

Our business is dependent on capital spending by our customers, and reductions in capital spending could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Our business is directly affected by changes in capital expenditures by our customers, and reductions in their capital spending could reduce demand for our services and products and have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition. Some of the items that may impact our customer's capital spending include:

- oil and natural gas prices, including volatility of oil and natural gas prices and expectations regarding future prices;

- the inability of our customers to access capital on economically advantageous terms, which may be impacted by, among other things, a decrease of investors' interest in hydrocarbon producers because of environmental and sustainability initiatives;

- changes in customers' capital allocation, including an increased allocation to the production of renewable energy, leading to less focus on oil and natural gas production growth;

- restrictions on our customers' ability to get their produced oil and natural gas to market due to infrastructure limitations;

- the consolidation of our customers;

- customer personnel changes; and

- adverse developments in the business or operations of our customers, including write-downs of oil and natural gas reserves and borrowing base reductions under customers' credit facilities.

HAL 2021 FORM 10-K | 9

| Item 1(a) | Risk Factors | ||||||||

Liabilities arising out of our products and services could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Events can occur at sites where our products and equipment are produced or installed, or where we conduct our operations or provide our services, or at chemical blending or manufacturing facilities, including well blowouts and equipment or materials failures, which could result in explosions, fires, personal injuries, property damage (including surface and subsurface damage), pollution, and potential legal responsibility. Generally, we rely on liability insurance coverage and on contractual indemnities, releases, and limitations of liability with our customers to protect us from potential liability related to such occurrences. However, we do not have these contractual provisions in all contracts, and even where we do, it is possible that the respective customer or insurer could seek to avoid or be financially unable to meet its obligations, or a court may decline to enforce such provisions. Damages that are not indemnified or released could greatly exceed available insurance coverage and could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Our business could be materially and adversely affected by severe or unseasonable weather where we have operations.

Our business could be materially and adversely affected by severe weather, particularly in Canada, the Gulf of Mexico, Russia, and the North Sea. Many experts believe global climate change could increase the frequency and severity of extreme weather conditions. Repercussions of severe or unseasonable weather conditions may include:

- evacuation of personnel and curtailment of services;

- weather-related damage to offshore drilling rigs resulting in suspension of operations;

- weather-related damage to our facilities and project work sites;

- inability to deliver materials to jobsites in accordance with contract schedules;

- decreases in demand for oil and natural gas during unseasonably warm winters; and

- loss of productivity.

Our failure to protect our proprietary information and any successful intellectual property challenges or infringement proceedings against us could materially and adversely affect our competitive position.

We rely on a variety of intellectual property rights that we use in our services and products. We may not be able to successfully preserve these intellectual property rights in the future, and these rights could be invalidated, circumvented, or challenged. In addition, the laws of some foreign countries in which our services and products may be sold do not protect intellectual property rights to the same extent as the laws of the United States. Courts could find that others infringe our patent rights or that our products and services may infringe the intellectual property rights of others. Our failure to protect our proprietary information and any successful intellectual property challenges or infringement proceedings against us could materially and adversely affect our competitive position.

If we are not able to design, develop and produce commercially competitive products and to implement commercially competitive services in a timely manner in response to changes in the market, customer requirements, competitive pressures, and technology trends, our business and consolidated results of operations could be materially and adversely affected, and the value of our intellectual property may be reduced.

The market for our services and products is characterized by continual technological developments to provide better and more reliable performance and services. If we are not able to design, develop, and produce commercially competitive products and to implement commercially competitive services in a timely manner in response to changes in the market, customer requirements, competitive pressures, and technology trends, our business and consolidated results of operations could be materially and adversely affected, and the value of our intellectual property may be reduced. Likewise, if our proprietary technologies, equipment, facilities, or work processes become obsolete, we may no longer be competitive, and our business and consolidated results of operations could be materially and adversely affected.

We sometimes provide integrated project management services in the form of long-term, fixed price contracts that may require us to assume additional risks associated with cost over-runs, operating cost inflation, labor availability and productivity, supplier and contractor pricing and performance, and potential claims for liquidated damages.

We sometimes provide integrated project management services outside our normal discrete business in the form of long-term, fixed price contracts. Some of these contracts are required by our customers, primarily national oil companies (NOCs). These services include acting as project managers as well as service providers and may require us to assume additional risks associated with cost over-runs. These customers may provide us with inaccurate information in relation to their reserves, which is a subjective process that involves location and volume estimation, that may result in cost over-runs, delays, and project losses. In addition, NOCs often operate in countries with unsettled political conditions, war, civil unrest, or other types of community issues. These issues may also result in cost over-runs, delays, and project losses.

HAL 2021 FORM 10-K | 10

| Item 1(a) | Risk Factors | ||||||||

Providing services on an integrated basis may also require us to assume additional risks associated with operating cost inflation, labor availability and productivity, supplier pricing and performance, and potential claims for liquidated damages. We rely on third-party subcontractors and equipment providers to assist us with the completion of these types of contracts. To the extent that we cannot engage subcontractors or acquire equipment or materials in a timely manner and on reasonable terms, our ability to complete a project in accordance with stated deadlines or at a profit may be impaired. If the amount we are required to pay for these goods and services exceeds the amount we have estimated in bidding for fixed-price work, we could experience losses in the performance of these contracts. These delays and additional costs may be substantial, and we may be required to compensate our customers for these delays. This may reduce the profit to be realized or result in a loss on a project.

Constraints in the supply of, prices for and availability of transportation of raw materials can have a material adverse effect on our business and consolidated results of operations.

Raw materials essential to our business, such as proppants (primarily sand), hydrochloric acid, and gels, including guar gum, are normally readily available. Shortage of raw materials as a result of high levels of demand or loss of suppliers during market challenges can trigger constraints in the supply chain of those raw materials, particularly where we have a relationship with a single supplier for a particular resource. Many of the raw materials essential to our business require the use of rail, storage, and trucking services to transport the materials to our jobsites. These services, particularly during times of high demand, may cause delays in the arrival of or otherwise constrain our supply of raw materials. These constraints could have a material adverse effect on our business and consolidated results of operations. In addition, price increases imposed by our vendors for raw materials and transportation providers used in our business, and the inability to pass these increases through to our customers could have a material adverse effect on our business and consolidated results of operations.

Our ability to operate and our growth potential could be materially and adversely affected if we cannot attract, employ, and retain technical personnel at a competitive cost.

Many of the services that we provide and the products that we sell are complex and highly engineered and often must perform or be performed in harsh conditions. We believe that our success depends upon our ability to attract, employ, and retain technical personnel with the ability to design, utilize, and enhance these services and products. A significant increase in the wages paid by competing employers could result in a reduction of our skilled labor force, increases in the wage rates that we must pay, or both. If either of these events were to occur, our cost structure could increase, our margins could decrease, and any growth potential could be impaired.

Laws and Regulations Related

Our operations outside the United States require us to comply with a number of United States and international regulations, violations of which could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Our operations outside the United States require us to comply with a number of United States and international regulations. For example, our operations in countries outside the United States are subject to the United States Foreign Corrupt Practices Act (FCPA), which prohibits United States companies and their agents and employees from providing anything of value to a foreign official for the purposes of influencing any act or decision of these individuals in their official capacity to help obtain or retain business, direct business to any person or corporate entity, or obtain any unfair advantage. Our activities create the risk of unauthorized payments or offers of payments by our employees, agents, or joint venture partners that could be in violation of anti-corruption laws, even though some of these parties are not subject to our control. We have internal control policies and procedures and have implemented training and compliance programs for our employees and agents with respect to the FCPA. However, we cannot assure that our policies, procedures, and programs will always protect us from reckless or criminal acts committed by our employees or agents. We are also subject to the risks that our employees, joint venture partners and agents outside of the United States may fail to comply with other applicable laws. Allegations of violations of applicable anti-corruption laws have resulted and may in the future result in internal, independent, or government investigations. Violations of anti-corruption laws may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could have a material adverse effect on our business, consolidated results of operations and consolidated financial condition.

HAL 2021 FORM 10-K | 11

| Item 1(a) | Risk Factors | ||||||||

In addition, the shipment of goods, services, and technology across international borders subjects us to extensive trade laws and regulations. Our import activities are governed by the unique customs laws and regulations in each of the countries where we operate. Moreover, many countries, including the United States, control the export, re-export, and in-country transfer of certain goods, services, and technology and impose related export recordkeeping and reporting obligations. Governments may also impose economic sanctions against certain countries, persons, and entities that may restrict or prohibit transactions involving such countries, persons, and entities, which may limit or prevent our conduct of business in certain jurisdictions. During 2014, the United States and European Union imposed sectoral sanctions directed at Russia’s oil and gas industry. Among other things, these sanctions restrict the provision of U.S. and EU goods, services, and technology in support of exploration or production for deep water, Arctic offshore, or shale projects that have the potential to produce oil in Russia. These sanctions resulted in our winding down and ending work on two projects in Russia in 2014 and have prevented us from pursuing certain other projects in Russia. In 2017 and 2018, the U.S. Government imposed additional sanctions against Russia, Russia’s oil and gas industry, and certain Russian companies. In connection with increasing tensions between Russia and the United States regarding Russia’s intentions with respect to Ukraine, the United States has threatened to impose aggressive additional sanctions against Russia if Russia invades Ukraine. Our ability to engage in certain future projects in Russia or involving certain Russian customers is dependent upon whether or not our involvement in such projects is restricted under U.S. or EU sanctions laws and the extent to which any of our current or prospective operations in Russia or with certain Russian customers may be subject to those laws. Those laws may change from time to time, and any expansion of sanctions against Russia’s oil and gas industry could further hinder our ability to do business in Russia or with certain Russian customers, which could have a material adverse effect on our consolidated results of operations.

The U.S. Government imposed sanctions against Venezuela that have effectively required us to discontinue our operations there. Consequently, in connection with us winding down our operations in Venezuela, we wrote down all of our remaining investment in Venezuela in 2020. As of December 29, 2020, we no longer had any employees in Venezuela, although we continue to maintain our local entity, facilities, and equipment in-country, as permitted under applicable law. We are not currently conducting any other operational activities in Venezuela.

The laws and regulations concerning import activity, export recordkeeping and reporting, export control and economic sanctions are complex and constantly changing. These laws and regulations can cause delays in shipments and unscheduled operational downtime. Moreover, any failure to comply with applicable legal and regulatory trading obligations could result in criminal and civil penalties and sanctions, such as fines, imprisonment, debarment from governmental contracts, seizure of shipments, and loss of import and export privileges. In addition, investigations by governmental authorities and legal, social, economic, and political issues in these countries could have a material adverse effect on our business, consolidated results of operations and consolidated financial condition.

Changes in, compliance with, or our failure to comply with laws in the countries in which we conduct business may negatively impact our ability to provide services in, make sales of equipment to, and transfer personnel or equipment among some of those countries and could have a material adverse effect on our business and consolidated results of operations.

In the countries in which we conduct business, we are subject to multiple and, at times, inconsistent regulatory regimes, including those that govern our use of radioactive materials, explosives, and chemicals in the course of our operations. Various national and international regulatory regimes govern the shipment of these items. Many countries, but not all, impose special controls upon the export and import of radioactive materials, explosives, and chemicals. Our ability to do business is subject to maintaining required licenses and complying with these multiple regulatory requirements applicable to these special products. In addition, the various laws governing import and export of both products and technology apply to a wide range of services and products we offer. In turn, this can affect our employment practices of hiring people of different nationalities because these laws may prohibit or limit access to some products or technology by employees of various nationalities. Changes in, compliance with, or our failure to comply with these laws may negatively impact our ability to provide services in, make sales of equipment to, and transfer personnel or equipment among some of the countries in which we operate and could have a material adverse effect on our business and consolidated results of operations.

HAL 2021 FORM 10-K | 12

| Item 1(a) | Risk Factors | ||||||||

The adoption of any future federal, state, or local laws or implementing regulations imposing reporting obligations on, or limiting or banning, the hydraulic fracturing process could make it more difficult to complete natural gas and oil wells and could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Various federal and state legislative and regulatory initiatives, as well as actions in other countries, have been or could be undertaken that could result in additional requirements or restrictions being imposed on hydraulic fracturing operations. For example, the United States may seek to adopt federal regulations or enact federal laws that would impose additional regulatory requirements on or even prohibit hydraulic fracturing in some areas. Legislation and/or regulations have been adopted in many U.S. states that require additional disclosure regarding chemicals used in the hydraulic fracturing process but that generally include protections for proprietary information. Legislation, regulations, and/or policies have also been adopted at the state level that impose other types of requirements on hydraulic fracturing operations (such as limits on operations in the event of certain levels of seismic activity). Additional legislation and/or regulations have been adopted or are being considered at the state and local level that could impose further chemical disclosure or other regulatory requirements (such as prohibitions on hydraulic fracturing operations in certain areas) that could affect our operations. Four states (New York, Maryland, Vermont, and Washington) have banned the use of high volume hydraulic fracturing, Oregon has adopted a five-year moratorium, and Colorado has enacted legislation providing local governments with regulatory authority over hydraulic fracturing operations. Local jurisdictions in some states have adopted ordinances that restrict or in certain cases prohibit the use of hydraulic fracturing, although many of these ordinances have been challenged and some have been overturned. In addition, governmental authorities in various foreign countries where we have provided or may provide hydraulic fracturing services have imposed or are considering imposing various restrictions or conditions that may affect hydraulic fracturing operations. The adoption of any future federal, state, local, or foreign laws or regulations imposing reporting obligations on, or limiting or banning, the hydraulic fracturing process could make it more difficult to complete natural gas and oil wells and could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Liability for cleanup costs, natural resource damages and other damages arising as a result of environmental laws and regulations could be substantial and could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

We are subject to numerous environmental laws and regulations in the United States and the other countries where we do business. We evaluate and address the environmental impact of our operations by assessing and remediating contaminated properties to avoid future liabilities and comply with legal and regulatory requirements. From time to time, claims have been made against us under environmental laws and regulations. In the United States, environmental laws and regulations typically impose strict liability. Strict liability means that in some situations we could be exposed to liability for cleanup costs, natural resource damages, and other damages as a result of our conduct that was lawful at the time it occurred or the conduct of prior operators or other third parties. We are periodically notified of potential liabilities at federal and state superfund sites. These potential liabilities may arise from both historical Halliburton operations and the historical operations of companies that we have acquired. Our exposure at these sites may be materially impacted by unforeseen adverse developments both in the final remediation costs and with respect to the final allocation among the various parties involved at the sites. The relevant regulatory agency may bring suit against us for amounts in excess of what we have accrued and what we believe is our proportionate share of remediation costs at any superfund site. We also could be subject to third-party claims, including punitive damages, with respect to environmental matters for which we have been named as a potentially responsible party. Liability for damages arising as a result of environmental laws or related third-party claims could be substantial and could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Failure on our part to comply with, and the costs of compliance with, applicable health, safety, and environmental requirements could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

In addition to the numerous environmental laws and regulations that apply to our operations, we are subject to a variety of laws and regulations in the United States and other countries relating to health and safety. Among those laws and regulations are those covering hazardous materials and requiring emission performance standards for facilities. For example, our well service operations routinely involve the handling of significant amounts of waste materials, some of which are classified as hazardous substances. We also store, transport, and use radioactive and explosive materials in certain of our operations. Applicable regulatory requirements include those concerning:

- the containment and disposal of hazardous substances, oilfield waste, and other waste materials;

- the production, storage, transportation and use of explosive materials;

- the importation and use of radioactive materials;

- the use of underground storage tanks;

- the use of underground injection wells; and

- the protection of worker safety both onshore and offshore.

HAL 2021 FORM 10-K | 13

| Item 1(a) | Risk Factors | ||||||||

These and other requirements generally are becoming increasingly strict. The failure to comply with the requirements, many of which may be applied retroactively, may result in:

- administrative, civil, and criminal penalties;

- revocation of permits to conduct business; and

- corrective action orders, including orders to investigate and/or clean up contamination.

Failure on our part to comply with applicable health, safety, and environmental laws and regulations or costs arising from regulatory compliance, including compliance with changes in or expansion of applicable regulatory requirements, could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Existing or future laws, regulations, treaties, or international agreements related to greenhouse gases, climate change, and alternative energy sources could have a negative impact on our business and may result in additional compliance obligations that could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Changes in or the adoption or enactment of laws, regulations, treaties or international agreements related to greenhouse gases, climate change, and alternative energy sources, including changes that may make it more expensive to explore for and produce oil and natural gas, may negatively impact demand for our services and products. For example, oil and natural gas exploration and production may decline as a result of environmental requirements, including land use policies responsive to environmental concerns. State, national, and international governments and agencies in areas in which we conduct business continue to evaluate, and in some instances adopt, climate-related legislation and other regulatory initiatives that would restrict emissions of greenhouse gases. The President of the United States has issued Executive Orders seeking to adopt new regulations and policies to address climate change and to suspend, revise, or rescind prior agency actions that the administration identified as conflicting with its climate policies. These include Executive Orders requiring a review of current U.S. federal lands leasing and permitting practices, as well as a temporary halt of new leasing of U.S. federal lands and offshore waters available for oil and gas exploration. The Executive Orders halting the leasing of U.S. federal lands were challenged in court and remain subject to litigation. As a result of the review of leasing and permitting practices, the U.S. Department of the Interior has recommended increasing the royalty rate payable to the U.S. government by operators, as well as bonding requirements and emissions requirements for operators. Some form of these recommendations may become applicable to operations on U.S. federal leases, which could have a negative effect on exploration and production of oil and natural gas given the increased costs associated with any such changes. In February 2021, the United States formally re-joined the Paris Agreement. The Paris Agreement requires countries to review and “represent a progression” in their intended nationally determined contributions, which set greenhouse gases emission reduction goals, every five years. Though we are closely following developments in this area and changes in the regulatory landscape in the United States, we cannot predict how or when those challenges may ultimately impact our business. Because our business depends on the level of activity in the oil and natural gas industry, existing or future laws, regulations, treaties, or international agreements related to greenhouse gases and climate change, including incentives to conserve energy or use alternative energy sources, may reduce demand for oil and natural gas and could have a negative impact on our business. Likewise, such restrictions may result in additional compliance obligations with respect to the release, capture, sequestration, and use of carbon dioxide. The efforts we have taken, and may undertake in the future, to respond to these evolving or new regulations and to environmental initiatives of customers, investors, and others may increase our costs. These and other environmental requirements could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

The Company could be subject to changes in its tax rates, the adoption of new tax legislation, tax audits, or exposure to additional tax liabilities that could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

We are subject to taxes in the U.S. and numerous jurisdictions where we operate and our subsidiaries are organized. Due to economic and political conditions, tax rates in the U.S. and other jurisdictions may be subject to significant change. In addition, our tax returns are subject to examination by the U.S. and other tax authorities and governmental bodies. We regularly assess the likelihood of an adverse outcome resulting from these examinations to determine the adequacy of our provision for taxes. There can be no assurance as to the outcome of the examinations. An increase in tax rates, particularly in the U.S., changes in our ability to realize our deferred tax assets, or adverse outcomes resulting from examinations of our tax returns could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

HAL 2021 FORM 10-K | 14

| Item 1(a) | Risk Factors | ||||||||

Our operations are subject to political and economic instability and risk of government actions that could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

We are exposed to risks inherent in doing business in each of the countries in which we operate. Our operations are subject to various risks unique to each country that could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition. With respect to any particular country, these risks may include:

- political and economic instability, including:

•civil unrest, acts of terrorism, war, and other armed conflict;

•inflation; and

•currency fluctuations, devaluations, and conversion restrictions; and

- governmental actions that may:

•result in expropriation and nationalization of our assets in that country;

•result in confiscatory taxation or other adverse tax policies;

•limit or disrupt markets or our customers and our operations, restrict payments, or limit the movement of funds;

•impose sanctions on our ability to conduct business with certain customers or persons;

•result in the deprivation of contract rights; and

•result in the inability to obtain or retain licenses required for operation.

For example, due to the unsettled political conditions in many oil-producing countries, our operations, revenue, and profits are subject to the adverse consequences of war, terrorism, civil unrest, strikes, currency controls, and governmental actions. These, and other risks described above, could result in the loss of our personnel or assets, cause us to evacuate our personnel from certain countries, cause us to increase spending on security worldwide, cause us to cease operating in certain countries, disrupt financial and commercial markets, including the supply of and pricing for oil and natural gas, and generate greater political and economic instability in some of the geographic areas in which we operate. Areas where we operate that have significant risk include, but are not limited to: the Middle East, North Africa, Angola, Argentina, Azerbaijan, Brazil, Indonesia, Kazakhstan, Mexico, Mozambique, Nigeria, Papa New Guinea, Russia, and Ukraine. In addition, any possible reprisals as a consequence of military or other action, such as acts of terrorism in the United States or elsewhere, could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

General Risk Factors

The COVID-19 pandemic and related economic repercussions could have a material adverse effect on our business, liquidity, consolidated results of operations, and consolidated financial condition.

The COVID-19 pandemic and related economic repercussions created significant volatility, uncertainty, and turmoil in the oil and gas industry during the last two years. Since the onset of the pandemic in early 2020, these events directly affected our business and exacerbated the negative impact from many of the risks our business is subject to, including those relating to the worldwide demand for oil and natural gas, our customers' capital spending and the impact on oil and natural gas prices. In addition, the pandemic and efforts to mitigate its spread have resulted in logistical challenges to our operations, including travel restrictions that prevent our personnel from commuting to certain facilities and job sites. These logistical challenges could increase if the pandemic worsens or persists.

Oil demand during 2020 and 2021 was substantially less than demand in 2019 as a result of the virus and corresponding measures taken around the world to mitigate its spread. Though demand began to increase during the latter part of 2021, a worsening of the virus could result in an increase in mitigation efforts and a reduction in demand for oil and gas and our services and products.

Given the nature and significance of the events described above, we are not able to enumerate all related potential risks to our business; however, we believe that in addition to the impacts described above, other current and potential impacts of these recent events include, but are not limited to:

•disruption to our supply chain for raw materials essential to our business, including restrictions on importing and exporting products and inflationary pressures;

•notices from customers, suppliers, and other third parties arguing that their non-performance under our contracts with them is permitted as a result of force majeure or other reasons;

•liquidity challenges, including impacts related to delayed customer payments and payment defaults associated with customer liquidity issues and bankruptcies;

•a credit rating downgrade of our corporate debt and potentially higher borrowing costs in the future;

•cybersecurity issues, as digital technologies may become more vulnerable and experience a higher rate of cyberattacks in the current environment of remote connectivity;

HAL 2021 FORM 10-K | 15

| Item 1(a) | Risk Factors | ||||||||

•litigation risk and possible loss contingencies related to COVID-19 and its impact, including with respect to commercial contracts, employee matters, and insurance arrangements;

•additional costs associated with rationalization of our portfolio of real estate facilities, including possible exit of leases and facility closures to align with expected activity and workforce capacity;

•additional asset impairments, including an impairment of the carrying value of our goodwill, along with other accounting charges;

•infections and quarantining of our employees and the personnel of our customers, suppliers, and other third parties in areas in which we operate;

•actions undertaken by national, regional, and local governments and health officials to contain COVID-19 or treat its effects; and

•a structural shift in the global economy and its demand for oil and natural gas as a result of changes in the way people work, travel, and interact, or in connection with a global recession or depression.

Given the dynamic nature of these events, we cannot reasonably estimate the period of time that the COVID-19 pandemic and related market conditions will persist or any changes in their severity, the full extent of the impact they will have on our business, financial condition, results of operations or cash flows or the pace or extent of any recovery. For more information, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Executive Overview.”

Our operations are subject to cyberattacks that could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

We are increasingly dependent on digital technologies and services to conduct our business. We use these technologies for internal purposes, including data storage, processing, and transmissions, as well as in our interactions with our business associates, such as customers and suppliers. Examples of these digital technologies include analytics, automation, and cloud services. Our digital technologies and services, and those of our business associates, are subject to the risk of cyberattacks and, given the nature of such attacks, some incidents can remain undetected for a period of time despite efforts to detect and respond to them in a timely manner. We routinely monitor our systems for cyber threats and have processes in place to detect and remediate vulnerabilities. Nevertheless, we have experienced occasional cyberattacks and attempted breaches over the past year, including attacks resulting from phishing emails and malware infections. We detected and remediated all of these incidents. Even if we successfully defend our own digital technologies and services, we also rely on our business associates, with whom we may share data and services, to defend their digital technologies and services against attack. No known leakage of material financial, technical or customer data occurred as a result of cyberattacks against us and none of the incidents mentioned above had a material adverse effect on our business, operations, reputation, or consolidated results of operations or consolidated financial condition.

If our systems, or our business associates' systems, for protecting against cybersecurity risks prove not to be sufficient, we could be adversely affected by, among other things: loss of or damage to intellectual property, proprietary, or confidential information, or customer, supplier, or employee data; interruption of our business operations; and increased costs required to prevent, respond to, or mitigate cybersecurity attacks. These risks could harm our reputation and our relationships with our business associates, employees, and other third parties, and may result in claims against us. These risks could have a material adverse effect on our business, consolidated results of operations and consolidated financial condition.

We are subject to foreign currency exchange risks and limitations on our ability to reinvest earnings from operations in one country to fund the capital needs of our operations in other countries or to repatriate assets from some countries.

A sizable portion of our consolidated revenue and consolidated operating expenses is in foreign currencies. As a result, we are subject to significant risks, including:

- foreign currency exchange risks resulting from changes in foreign currency exchange rates and the implementation of exchange controls; and

- limitations on our ability to reinvest earnings from operations in one country to fund the capital needs of our operations in other countries.

As an example, we conduct business in countries that have restricted or limited trading markets for their local currencies and restrict or limit cash repatriation. We may accumulate cash in those geographies, but we may be limited in our ability to convert our profits into United States dollars or to repatriate the profits from those countries.

HAL 2021 FORM 10-K | 16

| Item 1(a) | Risk Factors | ||||||||

If we lose one or more of our significant customers or if our customers delay paying or fail to pay a significant amount of our outstanding receivables, it could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

We depend on a limited number of significant customers. While no single customer represented more than 10% of consolidated revenue in any period presented, the loss of one or more significant customers could have a material adverse effect on our business and our consolidated results of operations.

In most cases, we bill our customers for our services in arrears and are, therefore, subject to our customers delaying or failing to pay our invoices. We may experience increased delays and failures due to, among other reasons, a reduction in our customers’ cash flow from operations and their access to the credit markets, particularly in weak economic or commodity price environments. If our customers delay paying or fail to pay us a significant amount of our outstanding receivables, it could have a material adverse effect on our business, consolidated results of operations and consolidated financial condition.

Our acquisitions, dispositions and investments may not result in anticipated benefits and may present risks not originally contemplated, which may have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.