Remarks at the ICI Global Asset Management Asia Forum

Good afternoon. It is a pleasure to join you in Singapore. The capital markets between the United States and Asia share significant interlinks. Today, I will present some perspectives on matters affecting the Asia-Pacific (APAC) region, reflecting my individual views as a Commissioner at the U.S. Securities and Exchange Commission.[1] I also will provide an overview of certain regulatory developments in the United States.

The Importance of Robust Capital Markets

In 1980, the famed economist Milton Friedman was invited here to deliver the Inaugural Singapore Lecture organized by the Institute of Southeast Asian Studies.[2] At the time, Singapore had been an independent republic for only 15 years. Dr. Friedman, in his remarks titled The Invisible Hand in Economics and Politics, observed that Singapore had “promoted a free market” and that “[t]hat free market has enabled Singapore to thrive.”[3]

Forty years later, the prominence of Singapore in the global capital markets reflects the importance of its market-based approach to economic development. Like the United States, the success of Singapore’s economy can be tied in part to entrepreneurial spirit. From the hawker stands to the largest corporations, a sense of economic opportunity drives so many to pursue their dreams and passions. That is why start-up financing, capital formation, and risk are fundamental to a thriving economy. Capital markets “help people with ideas become entrepreneurs and help small businesses grow into big companies.”[4]

Capital markets also provide individuals and institutions with opportunities to invest. While investments do not guarantee financial gain – and are always accompanied by the risk of loss – investments can produce greater returns than bank savings over the long run. In the United States, the securities laws are designed to require public companies to disclose and report relevant financial information necessary to make an informed investment decision. Rather than eliminating risk, these requirements empower investors to make their own determinations on risk tolerance in pursuit of potential financial return. Additionally, the U.S. securities laws regulate asset managers and pooled investment vehicles in a manner designed to mitigate potential conflicts of interest while permitting investors to choose a risk-return profile from a wide variety of investment strategies.

When individuals and institutions seek to limit risk, they often turn to banking products, such as savings accounts and certificates of deposits. As a tradeoff for this safety, these products offer returns far lower than what a successful investment might offer. Accordingly, instead of the disclosure regime set forth in the securities laws, banking organizations and their products are subject to prudential regulation, which primarily aims to ensure safety and soundness.

A healthy economy provides opportunities from both a vibrant capital market and a robust banking sector. Regulators should avoid directing the manner in which market participants allocate their capital among these options. Importantly, regulators should recognize that risk is an inherent – and necessary – component of properly functioning capital markets. The application of prudential-like regulations to the capital markets not only hurts businesses and investors, but leads to diminished economic growth, jobs creation, and innovation.

The Importance of the Asset Management Industry to Capital Markets

The role of the asset management industry in the capital markets has continued to increase over the years. According to one report, global assets under management (AUM) reached $126 trillion in 2022, which represents 28% of global financial assets.[5] This percentage is an increase from 23% a decade ago.[6] In the United States alone, nearly 15,000 SEC-registered investment advisers provided asset management services to more than 64 million clients in 2021.[7] Asset managers serve a broad range of clients, including individuals, pooled investment vehicles, and institutions.

The asset management industry enables clients to have diversified portfolios at a relatively low cost. Asset managers also offer expertise that enables clients to allocate capital in a sophisticated manner. For example, while the average retail investor may not be in a position to review and analyze the lengthy financial disclosures and other information regarding the universe of potential investments, asset managers can do that. This asset allocation function is crucial to the proper functioning of the capital markets. Further, the ability to hire asset managers that specialize in specific sectors allows investors to fine tune portfolio risk-return exposures.

The Growth of the APAC Market

Over the past couple of decades, APAC economies have experienced tremendous growth. From 2000 to 2021, total gross domestic product (GDP) in the APAC region increased from $9 trillion to $35 trillion.[8] The total GDP of the APAC region now accounts for roughly 37% of world GDP.[9] In tandem with this growth, the average annual amount of equity capital raised by Asian companies through initial public offerings (IPOs) increased from $46 billion during the period 2000 - 2008 to $67 billion during the period 2009 - 2018.[10] This contrasts with a decrease in the amount of equity capital raised by U.S. and European companies through IPOs during comparable periods.[11] Through the third quarter of 2022, Singapore, Japan, Hong Kong and China collectively account for over 20% of global equity market capitalization.[12]

The future outlook for the APAC region remains largely optimistic. One recent survey of capital markets participants in selected APAC markets reveals that a majority intend to continue to expand their business presence in the region.[13] However, despite their plans for future growth in the APAC region, certain survey respondents cited some headwinds – including the regulatory environment – as emerging challenges over the next three years.[14]

The Importance of Effective Regulation

The development and implementation of effective regulations can provide the APAC region with further opportunities for growth. On the one hand, there is the U.S. model, which has proven to be historically successful in regulating the capital markets. In the United States, a disclosure-based regulatory regime allows investors to reach their own decisions on how to allocate capital. To the extent that investors hire asset managers to make investment decisions on their behalf, federal statutes address the potential conflicts that those arrangements might create.[15] Importantly, the U.S. securities laws are not designed to limit the freedom of investment decision or opportunities for risk-taking in pursuit of potential returns.

On the other hand, some policymakers advocate for subjecting the capital markets to more prudential regulation. In April 2009, the G-20 established the Financial Stability Board (FSB) with a mandate to “[promote] international financial stability.”[16] Empowered by this broad mandate, the FSB has issued policy recommendations to ensure that “the structure of asset managers and their funds…does not contribute to undue risk in the global financial system.”[17] These recommendations address supposed vulnerabilities, such as: (1) the liquidity mismatch between portfolio holdings and redemption terms and conditions for open-ended funds, (2) leverage within investment funds, (3) operational risk and challenges at asset managers in stressed conditions, and (4) securities lending activities of asset managers and funds.[18]

The FSB consists mostly of banking regulators and finance ministry officials.[19] Its policy posture can reflect the viewpoints of prudential regulators who often do not appreciate how asset management differs from banking. To the FSB, any market-based financial activity outside of the banking system is a form of “shadow banking” that potentially poses systemic risks justifying the imposition of bank-like regulations on non-bank entities.[20] As one witness testified during a U.S. Senate hearing on the role of the FSB, “it is a good thing to have capital markets as well as banks. It is a good thing to have lively risk taking as well as lending.”[21] Unlike banks, the ability of U.S. mutual funds and ETFs to use leverage is limited by statute, and asset managers who manage those funds act as agents rather than principals. The result is that investment risk is spread among the millions of individuals that comprise the investing public. One industry group remarked that “the systemic risk concerns specific to the asset management industry are misplaced and may reflect a lack of understanding regarding the ways that this industry differs from other financial services industries, such as the banking industry.”[22]

Perhaps the FSB’s misplaced recommendations about capital markets can be attributed to the fact that the FSB is disproportionately influenced by European prudential regulators. Not only are European members represented at the national level, but also through European supranational entities, such as the European Central Bank and the European Commission.[23] On the FSB’s steering committee, 20 individuals are from Europe as compared to eight from Asia and seven from North America.[24] The outsized influence of Europe stands in stark contrast to the relative size of the European Union’s (EU) economy and capital markets. In fact, as of 2021, the GDP of the EU was just over $17 trillion, which is less than half the GDP of the APAC region.[25]

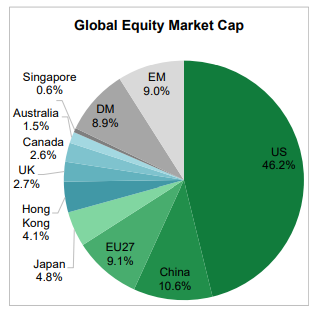

Additionally, with a market representing only 9.1% of the global equity market capitalization, the EU’s equity markets are less than half the size of the combined equity markets of China, Japan, Hong Kong, and Singapore.[26] Of the 2,700 global IPOs in 2021, less than 12% were in the EU, while more than 60% were in the U.S. and Asia.[27]

As of the Third Quarter of 2022, Source: SIFMA[28]

The limitations on risk-taking within the EU are embedded in regulations, as EU investment firms are subject to prudential rules that “aim to ensure that [they] have sufficient resources to cover potential losses from their activities.”[29] According to the EU, this “reduces the risk of the failure of those firms and hence the risk of undue economic harm to their customers or disruption in markets they operate in.”[30] But limitations on risk also mean limiting the potential to participate in the upside.

The FSB has committed to working jointly with the International Organization of Securities Commissions (IOSCO) in forming recommendations affecting the capital markets. IOSCO is comprised of securities regulators around the world. IOSCO’s expertise in securities regulation is an important and necessary counterpoint to the FSB perspective. On November 10, 2022, the FSB released a report that describes progress over the past year and planned work by the FSB to enhance the resilience of non-bank financial intermediation.[31] The report notes that the FSB, in consultation with IOSCO, plans to revise certain policy recommendations regarding asset managers and investment funds due to “new insights into liquidity management challenges” that have come to light.[32] Given the track record of the FSB favoring a prudential regulatory regime – even after consulting with IOSCO – I would encourage serious consideration of the report’s disclaimer that the FSB’s “activities, including any decisions reached in their context, shall not be binding or give rise to any legal rights or obligations.”[33]

Current U.S. Regulatory Matters

Perhaps the strongest evidence that prudential regulation of asset managers is unnecessary is the effectiveness of the regulatory framework developed in the United States. Two federal statutes – the Investment Advisers Act of 1940 (Advisers Act) and the Investment Company Act of 1940 (Investment Company Act) – have contributed to the growth of a thriving independent asset management industry. These statutes regulate the investment advisers that manage other people’s money and the pooled investment vehicles that they operate. This regulatory framework strikes a balance between investor protection and the freedom to take on risk.

The Advisers Act largely relies on a disclosure framework to ensure that clients of investment advisers are empowered to make informed decisions. However, recognizing the unique conflicts of interest that an investment adviser might face when managing a pooled investment vehicle, the Investment Company Act goes beyond a disclosure framework by imposing certain substantive requirements on the operation of investment companies. These requirements govern areas such as the valuation of fund assets,[34] advisory contract approvals,[35] and transactions with affiliates.[36] The Investment Company Act also limits a fund’s ability to use leverage[37] or invest in illiquid assets.[38] Taken together, these protections address the risks that the FSB cites when it calls for prudential regulation of the asset management space.

Whether the Commission might deviate from its historic – and successful – approach is a concern. The Commission currently is in the midst of an ambitious rulemaking agenda. Many of the recently-proposed rules are geared toward the asset management industry. One proposed rule would seek to enhance how funds manage their liquidity risks.[39] The rule would introduce entirely new requirements to the operation of mutual funds, including the use of swing pricing and the institution of a hard close for purchases and redemptions of fund shares at 4:00 pm Eastern time. While I support the notion that funds should have sufficient liquidity and must be resilient at all times, particularly during market stress, I have strong reservations whether the proposed requirements, which appear very prescriptive and costly, would effectively address such concerns. Nonetheless, I did appreciate the alternatives to the proposed requirements that were discussed, including redemption fees, dual pricing, and alternatives to a hard 4:00 pm close.

Another proposal would impose disclosure requirements on investment advisers and investment companies that market themselves on environmental, social, and governance (ESG) factors.[40] Among other things, the rule would require specific disclosure requirements regarding ESG strategies. Certain environmentally focused funds would be required to disclose the greenhouse gas emissions associated with their portfolio holdings. A separate proposal would bring the term “ESG” under the purview of Rule 35d-1 under the Investment Company Act, which is known as the “names rule.”[41] Under the names rule, a fund must invest at least 80% of its assets in the investment focus suggested by the fund’s name.[42]

The federal securities laws already require investment advisers to disclose accurate information about how they invest client assets. I question the need to adopt unique, highly-prescriptive disclosure requirements specifically targeted at ESG investment strategies. The current rules appear to provide the Commission with sufficient authority to bring enforcement actions against investment advisers that engage in “greenwashing” by marketing products as ESG-focused without incorporating ESG into their investment strategies.

For example, this past May, the Commission brought an enforcement action against an investment adviser for misstatements and omissions about ESG considerations in making investment decisions for certain mutual funds that it managed.[43] Any adviser that materially misstates its investment strategies already violates the law, and the Commission has the authority and resources to address that misconduct. Given that, the overlay of specific ESG disclosure requirements appears to solve for a problem that is already sufficiently addressed by the Advisers Act and the Investment Company Act.

Nevertheless, I appreciate the discussions that have been prompted by these proposals. However, it is important that the United States maintains a gold-standard regulatory framework that both fosters capital formation and protects investors.

Conclusion

It has been a pleasure to speak to you today in Singapore, a country that exemplifies the potential that is unleashed with the proper combination of free markets, international trade, and the rule of law. Due to these factors, Singapore is well-positioned to contribute significantly to the growth of the capital markets in the APAC region.

Many exciting developments are already underway. For example, I note that the Singapore Exchange recently joined Euroclear Bank’s exchange-traded fund ecosystem. This partnership resulted in a significant milestone: the first cross-listing of a UCITS international exchange-traded fund on both the Hong Kong and Singapore exchanges.[44] Singapore can unleash even further potential in the years and decades to come.

Thank you.

[1] As a reminder, my remarks today reflect solely my individual views as a Commissioner and do not necessarily reflect the views of the full Commission or my fellow Commissioners.

[2] See, The Invisible Hand in Economics and Politics, Milton Friedman (Oct. 14, 1980), available at https://miltonfriedman.hoover.org/internal/media/dispatcher/271090/full

[3] Id. at 4.

[4] See Understanding Capital Markets, Federal Reserve Bank of St. Louis, available at https://www.stlouisfed.org/education/tools-for-enhancing-the-stock-market-game-invest-it-forward/episode-1-understanding-capital-markets.

[5] See The Great Reset: North American asset management in 2022, McKinsey & Company (Oct. 2022), available at https://www.mckinsey.com/~/media/mckinsey/industries/financial%20services/our%20insights/the%20great%20reset%20north%20american%20asset%20management%20in%202022/the-great-reset-north-american-asset-management-in-2022.pdf.

[6] Id.

[7] See Investment Adviser Association Industry Snapshot 2022: Evolution Revolution Reimagined, 2nd Edition, available at https://investmentadviser.org/wp-content/uploads/2022/06/Snapshot2022.pdf.

[8] See The ascent of APAC in the global economy, S&P Global Market Intelligence (Aug. 16, 2022), available at https://www.spglobal.com/marketintelligence/en/mi/research-analysis/ascent-of-apac-in-the-global-economy.html.

[9] Id.

[10] See OECD Equity Market Review of Asia 2019, OECD Capital Market Series, available at https://www.oecd.org/corporate/ca/OECD-Equity-Market-Review-Asia-2019.pdf.

[11] Id.

[12] See Research Quarterly: Equities, Securities Industry and Financial Markets Association (“SIFMA”) (Oct. 19, 2022), available at https://www.sifma.org/wp-content/uploads/2022/10/US-Research-Quarterly-Equity-2022-10-19-SIFMA.pdf.

[13] See ASIFMA 2022: Asia-Pacific Capital Markets Survey, Asia Securities Industry and Financial Markets Association, available at https://www.asifma.org/wp-content/uploads/2021/12/asifma-2022-apac-capital-markets-survey.pdf.

[14] Id.

[15] For example, an investment adviser is prohibited from entering into transactions with its clients on a principal basis unless it can satisfy certain conditions that are designed to protect the client. See Section 206(3) of the Investment Advisers Act of 1940.

[16] See About the FSB, available at https://www.fsb.org/about/.

[17] See Policy Recommendations to Address Structural Vulnerabilities from Asset Management Activities, Financial Stability Board (Jan. 12, 2017), available at https://www.fsb.org/wp-content/uploads/FSB-Policy-Recommendations-on-Asset-Management-Structural-Vulnerabilities.pdf.

[18] Id.

[19] See Members of the FSB, available at https://www.fsb.org/about/organisation-and-governance/members-of-the-financial-stability-board/.

[20] See, e.g., Assessment of shadow banking activities, risks and the adequacy of post-crisis policy tools to address financial stability concerns, Financial Stability Board (Jul. 3, 2017), available at https://www.fsb.org/wp-content/uploads/P300617-1.pdf. (“[A] rise in assets held in certain investment funds has increased the risks from liquidity transformation, underscoring the importance of effective operationalisation and implementation of policies agreed to address this, in particular those to address structural vulnerabilities in asset management activities.”)

[21] See Statement of Adam S. Posen, President, Peterson Institute for International Economics, The Role of the Financial Stability Board in the U.S. Regulatory Framework, Hearing Before the Committee on Banking, Housing, and Urban Affairs, United States Congress (Jul. 8, 2015), available at https://www.govinfo.gov/content/pkg/CHRG-114shrg97398/html/CHRG-114shrg97398.htm.

[22] See Regulation of the Asset Management/Advisory Industry, CFA Institute, available at https://www.cfainstitute.org/en/advocacy/issues/regulation-of-asset-management-advisory-industry#sort=%40pubbrowsedate%20descending.

[23] See Members of the FSB, supra note 19.

[24] Id.

[25] See GDP (current US$) – European Union, The World Bank, available at https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=EU.

[26] See SIFMA, supra note 12.

[27] See Capital markets union is key to a sovereign EU, Theodor Weimer, Financial Times (Feb. 25, 2022), available at https://www.ft.com/content/6b5008f0-d101-4ed5-9270-bae5c32d7389.

[28] See SIFMA, supra note 12.

[29] See Prudential rules for investment firms, European Commission, available at https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/financial-markets/prudential-rules-investment-firms_en.

[30] Id.

[31] See Enhancing the Resilience of Non-Bank Financial Intermediation: Progress Report, FSB (Nov. 10, 2022), available at https://www.fsb.org/wp-content/uploads/P101122.pdf.

[32] Id.

[33] Id.

[34] See Section 2(a)(41) of the Investment Company Act.

[35] See Section 15 of the Investment Company Act.

[36] See Section 17 of the Investment Company Act.

[37] See Section 18 of the Investment Company Act.

[38] See Section 22(e) of the Investment Company Act and Rule 22e-4 under the Investment Company Act.

[39] See Open-End Fund Liquidity Programs and Swing Pricing; Form N-PORT Reporting, Release No. IC-34746 (Nov. 2, 2022), available at https://www.sec.gov/rules/proposed/2022/33-11130.pdf.

[40] See Enhanced Disclosures by Certain Investment Advisers and Investment Companies About Environmental, Social, and Governance Investment Practices, Release No. IC-34594 (May 25, 2022) [87 FR 36654 (Jun. 17, 2022)], available at https://www.sec.gov/rules/proposed/2022/ia-6034.pdf.

[41] See Investment Company Names, Release No. IC-34593 (May 25, 2022) [87 FR 36594 (Jun. 17, 2022)], available at https://www.sec.gov/rules/proposed/2022/ic-34593.pdf.

[42] See Rule 35d-1 under the Investment Company Act.

[43] See BNY Mellon Investment Adviser, Inc., Release No. IC-34591 (May 23, 2022), available at https://www.sec.gov/litigation/admin/2022/ia-6032.pdf.

[44] See The first cross-listing of iETFs in Asia Pacific, Euroclear (Oct. 20, 2022), available at https://www.euroclear.com/newsandinsights/en/press/2022/2022-mr-16-eb-support-cross-listing-of-ietfs-in-asia.html.

Last Reviewed or Updated: Nov. 30, 2022