UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

FORM 10-K

| (Mark one) | ||

| [✓] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

For the fiscal year ended: March 28, 2020 | ||

|

or | ||

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission File Number: 000-03905

TRANSCAT, INC.

(Exact name of registrant as specified in its charter)

| Ohio | 16-0874418 | ||

| (State or other jurisdiction of | (I.R.S. Employer | ||

| incorporation or organization) | Identification No.) |

35 Vantage Point Drive, Rochester, New York 14624

(Address of principal executive offices) (Zip Code)

(585) 352-7777

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common Stock, $0.50 par value | TRNS | Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [✓]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [✓]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [✓] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [✓] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [✓] |

| Non-accelerated filer [ ] | Smaller reporting company [✓] |

| Emerging growth company [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. [✓]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes [ ] No [✓]

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant on September 27, 2019 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $170.3 million. The market value calculation was determined using the closing sale price of the registrant’s common stock on September 27, 2019, as reported on the Nasdaq Global Market.

The number of shares of common stock of the registrant outstanding as of June 3, 2020 was 7,388,881.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement relating to the Annual Meeting of Shareholders to be held on September 9, 2020 have been incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this report.

FORWARD-LOOKING STATEMENTS

This report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements relate to expectations, estimates, beliefs, assumptions and predictions of future events and are identified by words such as “anticipates,” “believes,” “estimates,” “expects,” “projects,” “intends,” “could,” “may,” and other similar words. Forward-looking statements are not statements of historical fact and thus are subject to risks, uncertainties and other factors that could cause actual results to differ materially from historical results or those expressed in such forward-looking statements. You should evaluate forward-looking statements in light of important risk factors and uncertainties that may affect our operating and financial results and our ability to achieve our financial objectives. These factors include, but are not limited to, the Company’s response to the coronavirus (“COVID-19”) pandemic, the highly competitive nature of the industries in which we compete and in the nature of our two business segments, cybersecurity risks, the risk of significant disruptions in our information technology systems, our inability to recruit, train and retain quality employees, skilled technicians and senior management, fluctuations in our operating results, competition in the rental market, the volatility of our stock price, our ability to adapt our technology, reliance on our enterprise resource planning system, technology updates, risks related to our acquisition strategy and the integration of the businesses we acquire, volatility in our customers’ industries, changes in vendor rebate programs, our vendors abilities to provide desired inventory, the risks related to current and future indebtedness, the relatively low trading volume of our common stock, foreign currency rate fluctuations and the impact of general economic conditions on our business. These risk factors and uncertainties are more fully described by us under the heading “Risk Factors” in Item IA. of Part I of this report. You should not place undue reliance on our forward-looking statements. Except as required by law, we undertake no obligation to update, correct or publicly announce any revisions to any of the forward-looking statements contained in this report, whether as a result of new information, future events or otherwise.

BUSINESS OVERVIEW

Transcat, Inc. (“Transcat”, the “Company,” “we” or “us”) is a leading provider of accredited calibration and laboratory instrument services and a value-added distributor of professional grade test, measurement and control instrumentation. We are focused on providing services and products to highly regulated industries, particularly the life science industry, which includes pharmaceutical, biotechnology, medical device and other FDA-regulated businesses. Additional industries served include FAA-regulated businesses, including aerospace and defense industrial manufacturing; energy and utilities, including oil and gas and alternative energy; and other industries that require accuracy in their processes, confirmation of the capabilities of their equipment, and for which the risk of failure is very costly.

We conduct our business through two operating segments: service (“Service”) and distribution (“Distribution”). See Note 7 to our Consolidated Financial Statements in this report for financial information for these segments. We concentrate on attracting new customers in each segment, retaining existing customers and cross-selling to customers to increase our total revenue. We serve approximately 25,000 customers through our Service and Distribution segments, with approximately 25% to 30% of those customers transacting with us through both of our business segments.

Through our Service segment, we offer calibration, repair, inspection, analytical qualifications, preventative maintenance, consulting and other related services, a majority of which are processed through our proprietary asset management system, CalTrak® (“CalTrak®”) and our online customer portal, C3®. Our Service model is flexible, and we cater to our customers’ needs by offering a variety of services and solutions including permanent and periodic on-site services, mobile calibration services, pickup and delivery and in-house services. As of the end of our fiscal year ended March 28, 2020 (“fiscal year 2020”), we operated twenty-two calibration service centers (“Calibration Service Centers”) strategically located across the United States, Puerto Rico, and Canada. We also serve our customers on-site at their facilities for daily, weekly or longer-term periods. In addition, we have several imbedded customer-site locations that we refer to as “client-based labs,” where we provide calibration services, and in some cases other related services, exclusively for the customer and where we reside and work every day. We also have a fleet of mobile calibration laboratories that can provide service at customer sites which may not have the space or utility capabilities we require to service their equipment.

1

All of our Calibration Service Centers have obtained ISO/IEC 17025:2017 scopes of accreditation. Our accreditations are the cornerstone of our quality program, which we believe is among the best in the industry. Our dedication to quality is highly valued by businesses that operate in the industries we serve, particularly those in life science and other regulated industries, and our accreditations provide our customers with confidence that they will receive a consistent and uniform service, regardless of which of our service centers completes the service.

Through our Distribution segment, we sell and rent national and proprietary brand instruments to customers globally. Through our website, in-house sales team and printed and digital marketing materials, we offer access to more than 150,000 test, measurement and control instruments, including products from approximately 500 leading brands. Most instruments we sell and rent require calibration service to ensure that they maintain the most precise measurements. By having the capability to calibrate these instruments at the time of sale and at regular post-sale intervals, we can give customers a value-added service that most of our competitors are unable to provide. Calibrating before shipping means the customer can place their instruments into service immediately upon receipt, reducing downtime. Other value-added options we offer through our Distribution segment include equipment kitting (which is especially valued in the power generation sector), equipment rentals and used equipment sales.

Our commitment to quality goes beyond the services and products we deliver. Our sales, customer service and support teams provide expert advice, application assistance and technical support to our customers. Since calibration is an intangible service, our customers rely on us to uphold high standards and provide integrity in our people and processes.

Our customers include leading manufacturers in the life science/pharmaceutical, energy, defense, aerospace and industrial process control sectors. We believe our customers do business with us because of our integrity and commitment to quality service, our broad range of product and service offerings, our proprietary asset management system, CalTrak®, and our online customer portal, C3®. In our fiscal year ended March 30, 2019 (“fiscal year 2019”) through fiscal year 2020, no customer or controlled group of customers accounted for 5% or more of our total revenue. The loss of any single customer would not have a material adverse effect on our business, cash flows, balance sheet, or results of operations.

Transcat was incorporated in Ohio in 1964. We are headquartered in Rochester, New York and employ 772 people, including approximately 165 in our corporate headquarters. Our executive offices are located at 35 Vantage Point Drive, Rochester, New York 14624. Our telephone number is 585-352-7777. Our website is www.transcat.com. We trade on the Nasdaq Global Market under the ticker symbol “TRNS”.

OUR STRATEGY

Our two operating segments are highly complementary in that their offerings are of value to customers within the same industries. Our strategy is to leverage the complementary nature of our operating segments in ways that add value for all customers who select Transcat as their source for test and measurement equipment and/or calibration and laboratory instrument services. We strive to differentiate ourselves within the markets we serve and build barriers to competitive entry by offering a broad range of products and services and by integrating our product and service offerings in a value-added manner to benefit our customers’ operations.

During fiscal year 2020, we continued to commit capital, people and leadership investments to advance our “Operational Excellence” initiative. These initiatives are resulting in increased productivity and operational efficiency and further differentiation from our competitors as we leverage technology and process improvements to improve our effectiveness and our customers’ experiences. Our Operational Excellence is a multi-year, ever-evolving program that we believe will deliver certain short-term benefits but is focused on the use of technology and process improvements to create an infrastructure to support our strategic goals over a longer timeframe.

Within the Service segment, our strategy is to drive double-digit revenue growth through both organic expansion and acquisitions. We expect to achieve mid-to-high single digit organic revenue growth in this segment. We have adopted an integrated sales model to drive sales and capitalize on the cross-selling opportunities between our two segments, especially leveraging our Distribution relationships to develop new Service relationships. We leverage these relationships with our unique value proposition which resonates strongly with customers who rely on accredited calibration services and/or laboratory instrument services to maintain the integrity of their processes and/or meet the demands of regulated business environments. Our customer base values our superior quality programs and requires precise measurement capability in their processes to minimize risk, waste and defects. We execute this strategy by leveraging our quality programs, metrology expertise, multiple locations, qualified technicians, breadth of capabilities, and on-site and depot service options. Together, this allows us to meet the most rigorous quality demands of our most highly regulated customers while simultaneously being nimble enough to meet their business needs.

2

We expect to continue to grow our Service business organically by taking market share from other third-party providers and original equipment manufacturers (“OEMs”), as well as by targeting the outsourcing of in-house calibration labs as multi-year client-based lab contracts. We believe an important element in taking market share is our ability to expand into new technical capabilities that are in demand by our current and target customer base.

The other component to our Service growth strategy is acquisitions. There are three drivers of our acquisition strategy: geographic expansion, increased capabilities and infrastructure leverage. The majority of our acquisition opportunities have been in the $500 thousand to $10 million annual revenue range, and we are disciplined in our approach to selecting target companies. One focus of our Operational Excellence initiative is to strengthen our acquisition integration process, allowing us to capitalize on acquired sales and cost synergies at a faster pace.

Our Distribution segment strategy is to be the premier distributor and rental source of leading test and measurement equipment while also providing cross-selling opportunities for our Service segment. Through our vendor relationships we have access to more than 150,000 products, which we market to our existing and prospective customers both with and without value-added service options that are unique to Transcat. In addition to offering pre-shipment value-added services, we offer our customers the options of renting selected test and measurement equipment or buying used equipment, furthering our ability to answer all of our customers’ test and measurement equipment needs. We continuously evaluate our offerings and add new in-demand vendors and products. In recent years we have expanded the number of SKUs that we stock and the number of SKUs that are sold with pre-shipment calibrations and have increased our focus on digital marketing to capitalize on the ever-growing B2B ecommerce trend. Our equipment rental business continues to grow, and with it used equipment sales. Having new, used and rental equipment further differentiates us from our Service segment competitors.

We see these various methods of meeting our Distribution customers’ needs as a way to differentiate ourselves and to diversify this segment’s customer base from its historically niche market. This differentiation and diversification strategy has been deliberately instituted in recent years as a means to mitigate the effect of price-driven competition and to lessen the impact that any particular industry or market will have on the overall performance of this segment.

As part of our growth strategy, we completed three business acquisitions during our fiscal year 2020 and two acquisitions during our fiscal year 2019:

| ● | Effective February 21, 2020, we acquired substantially all of the assets of TTE Laboratories, Inc. (“TTE"), a Boston, MA-based provider of pipette equipment and services. |

| ● | Effective July 19, 2019, we acquired Infinite Integral Solutions Inc. (“IIS”). IIS, a Mississauga, Ontario, Canada company, the owner and developer of the CalTree™ suite of software solutions for the automation of calibration procedures and datasheet generation. |

| ● | Effective April 1, 2019, we acquired substantially all of the assets of Gauge Repair Service (“GRS”), a Los Angeles, California-based provider of calibration services. |

| ● | Effective August 31, 2018, we acquired substantially all of the assets of Angel’s Instrumentation, Inc. (“Angel’s”), a Virginia-based provider of calibration services. |

| ● | Effective June 12, 2018, we acquired substantially all of the assets of NBS Calibration, Inc. (“NBS”), an Arizona-based provider of calibration services. |

Our acquisition strategy primarily targets service businesses that expand our geographic reach, increase the depth and/or breadth of our service capabilities and expertise and leverage our infrastructure. The table below illustrates the strategical drivers for the acquisitions described above:

| Geographic | Increased | Leveraged | |

| Expansion | Capabilities | Infrastructure | |

| TTE | ✓ | ✓ | |

| IIS | ✓ | ✓ | |

| GRS | ✓ | ✓ | |

| Angel’s | ✓ | ✓ | |

| NBS | ✓ | ✓ |

3

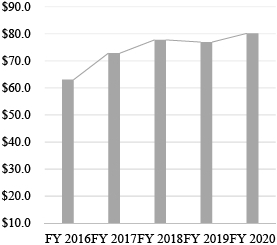

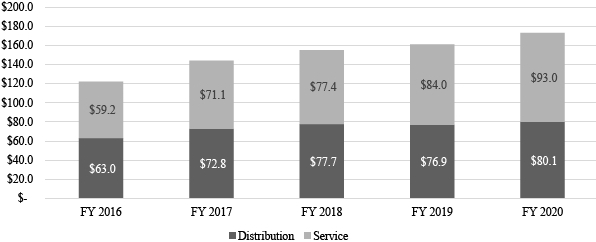

We believe our combined Service and Distribution segment offerings, experience, technical expertise and integrity create a unique and compelling value proposition for our customers, and we intend to continue to grow our business through organic revenue growth and business acquisitions. We consider the attributes of our Service segment which include higher gross margins and recurring revenue streams from customers in regulated industries to be more compelling and scalable than our legacy Distribution segment. For this reason, we expect our Service segment to be the primary source of revenue and earnings growth in future fiscal years. The charts below illustrate Service, Distribution and consolidated revenue over the past five years:

| Service Revenue Trend (in millions) |

Distribution Sales Trend (in millions) | |

|

|

|

|

Consolidated Revenue (in millions) |

|

4

SEGMENTS

Service Segment

Calibration. Calibration is the act of comparing a unit or instrument of unknown value to a standard of known value and reporting the result in some specifically defined form. After the calibration has been completed, a decision is made, based on rigorously defined parameters, regarding what, if anything, should be done to the unit to conform to the required standards or specifications. The decision may be to adjust, optimize or repair a unit; limit the use, range or rating of a unit; scrap the unit; or leave the unit as is. The purpose of calibration is to significantly reduce the risk of product or process failures caused by inaccurate measurements. In addition to its being an element of quality control and risk management, calibration improves an operation’s productivity and efficiency to optimal levels by assuring accurate, reliable instruments and processes.

The need for calibration is often driven by regulation, which identifies a requirement for quality calibration and laboratory instrument services as a critical component of a company’s business operation. We specifically target industries and companies that are regulated by the FDA, FAA or other regulatory bodies. As a result of the various levels of regulation within our target industries, our customers’ calibration and laboratory instrument service sourcing decisions are generally made based on the provider’s quality systems, accreditation, reliability, trust, customer service and documentation of services. To maintain our competitive position in this segment, we maintain internationally recognized third-party accredited quality systems, further detailed in the section entitled “Service Quality” below, and provide our customers with access to proprietary asset management software solutions, which offer tools to manage their internal calibration programs and provide them with visibility to their service records.

Through our Service segment, we perform recurring periodic calibrations (typically ranging from three-month to twenty-four month intervals) on new and customer-owned instruments. We perform approximately 500,000 calibrations annually and can address a significant majority of the items requested to be calibrated with our in-house capabilities. For customers’ calibration needs in less common and highly specialized disciplines, we subcontract some calibrations to third-party vendors that have unique or proprietary capabilities. While typically representing approximately 13% to 15% of our Service segment revenue, we believe the management of these items is highly valued by our customers and providing this service has enabled us to continue our pursuit of having the broadest calibration offerings in these targeted markets.

Compliance Services. Our compliance services include analytical qualification, validation, remediation and preventative maintenance services. Our analytical qualification and validation services provide a comprehensive and highly specialized service offering focused on life science-related industries. Analytical qualifications and validation services include validations to specifically documented protocols that are commonly used in highly-regulated life science industries including installation qualification (“IQ”), operational qualification (“OQ”), and performance qualification (“PQ”). Most of the demand for our qualification, validation and preventative maintenance services comes from companies and institutions engaged in pharmaceutical manufacturing and research and development.

Our goal is to deliver specialized technical services with a quality assurance approach, which maximizes document accuracy and on-time job delivery. These industries demand knowledgeable contract services, and Transcat meets these demands with current good manufacturing practice (“cGMP”) and good laboratory practice (“GLP”) compliant services. Companies within these innovative and cutting-edge life science industries need a reliable alternative to the OEMs and the “generalist” service providers who cannot meet their industry-specific needs. We believe our value proposition to the life science industries is unique as a result of offering a comprehensive suite of both traditional calibration and laboratory instrument and other analytical services.

Analytical qualifications and preventative maintenance services are typically based on service agreements for periodic service and tend to generate recurring revenue. Some validation services are based on certain customer processes. While some validation services may not be repeated, we generally develop relationships with these customers that lead to demand for additional unique validation services. Remediation services are based on specific regulatory actions and are generally project-based and required by a customer for a finite period of time. Remediation revenue is not recurring by its nature.

Other Services. We provide other services to our customers such as inspection, repair and consulting services, which appeal to customers across all sectors in our customer base. These are generally value-added services and allow us to provide “one-stop shopping” for our customers.

5

Service Value Proposition. Our calibration services strategy encompasses multiple ways to manage a customer’s calibration and laboratory instrument service needs:

| 1) | We offer an “Integrated Calibration Service Solution” that provides a complete wrap-around service, which can be delivered in the following ways: |

| ● | in-house services: services are performed at one of our twenty-two Calibration Service Centers (often accompanied by pick-up and delivery services); |

| ● | periodic on-site services: Transcat technicians travel to a customer’s location, including aboard vessels docked at shipyards, and provide bench-top or in-line calibration or laboratory services on predetermined service cycles; |

| ● | client-based-laboratory services: Transcat establishes and manages a calibration service program within a customer’s facility; and |

| ● | mobile calibration services: services are completed on a customer’s property within one of our mobile calibration units. |

| 2) | For companies that maintain an internal calibration operation, we can provide: |

| ● | calibration of their primary calibration assets, also called “standards”; and |

| ● | overflow capability, either on-site or at one of our Calibration Service Centers, during periods of high demand. |

Inclusive with all the above services, we provide total program management including logistics, remediation and consultation services when needed.

We strive to provide the broadest accredited calibration offering to our targeted markets, which includes certification of our technicians pursuant to the American Society for Quality standards, complete calibration management encompassing the entire metrology function, and access to our complementary service and product offerings. We believe our calibration services are of the highest technical and quality levels, with broad ranges of accreditation.

Our Compliance Services strategy is to identify and establish long-term relationships with life science research and development and manufacturing customers who require analytical qualifications, validation, remediation and/or preventative maintenance services. In most cases, these customers are life science companies, including pharmaceutical and biotechnology companies engaged in research and development and manufacturing, which are subject to extensive government regulation. The services we provide to these regulated customers are typically a critical component of the customer’s overall compliance program. Because many laboratory instrument service customers operate in regulated industries, these same customers typically also require accredited calibration services. This requirement allows a natural synergy between our laboratory instrument and calibration services. Our strategy includes cross-selling our services within our customer accounts to maximize our revenue opportunities with each customer.

Proprietary Asset Management Software. CalTrak® is our proprietary documentation and asset management software which is used to integrate and manage both the workflow of our Calibration Service Centers and our customers’ assets. With CalTrak®, we are able to provide our customers with timely and consistent calibration service while optimizing our own efficiencies. CalTrak® has been validated to U.S. federal regulations 21 CFR Part 820.75 and 21 CFR Part 11, as applicable. This validation is important to pharmaceutical and other FDA-regulated industries where federal regulations can be particularly stringent.

Additionally, C3® provides our customers with web-based asset management capability and a safe and secure off-site archive of calibration and other service records that can be accessed 24 hours a day through our secure password-protected website. C3® stands for Compliance, Control and Cost, and we see these as the major areas of focus for our clients within the regulatory environment as it relates to instrument calibration. We specifically designed C3® to assist our customers in increasing efficiency, driving compliance to quality system and enhancing control of instrumentation, all while bringing their overall metrology costs down. Understanding the regulated environments that our clients operate within, we customized the platform to allow for single system of record utilization via capabilities that allow clients to track and manage instruments maintained internally in addition to instruments supported by Transcat. C3® is validated to 21 CFR Part 820.75 and 21 CFR Part 11 to meet stringent FDA requirements.

Through CalTrak® and C3®, each customer calibration is tracked and automatically cross-referenced to the assets used to perform the calibration, providing traceability.

6

Service Marketing and Sales. Under our integrated sales model, we have both inside and outside sales teams that seek to acquire new customers in our targeted markets by leveraging our unique value proposition, including our broad geographic footprint and comprehensive suite of services. We target regulated, enterprise customers with multiple manufacturing operations throughout North America. We leverage our ability to manage the complete life cycle of instrumentation from purchase of calibrated equipment to long-term service and maintenance requirements. Connecting all the dots by using new and used product sales, rentals, and repair and calibration services is the goal of our marketing and sales initiatives. We also have a team of customer success managers focused on delivering ever-increasing value for our existing customers. We utilize print media, trade shows and web-based initiatives to market our services to customers and prospective customers with a strategic focus in the highly regulated industries including life science and other FDA-regulated industries, aerospace and defense, energy and utilities, and chemical manufacturing. We also target industrial manufacturing and other industries that appreciate the value of quality calibrations.

Service Competition. The calibration services industry is highly fragmented and is composed of companies ranging from internationally recognized and accredited OEM’s, to non-accredited sole proprietors as well as companies that perform their own calibrations in-house, resulting in a tremendous range of service levels and capabilities. A large percentage of calibration companies are small businesses that generally do not have a range of capabilities as broad as ours. There are also several companies with whom we compete that have national or regional operations.

We differentiate ourselves from our competitors by demonstrating our commitment to quality, having a wide range of capabilities that are tailored to the markets we serve, having a geographical footprint that spans North America and providing a comprehensive suite of services that spans many manufacturers and is not limited to certain product lines or brands. Our unique ability to bundle our products with our compliance and calibration services also provides a high level of differentiation from our competitors. As one of the only North American compliance and calibration service providers who also distributes product, our customers can seamlessly replace instruments that cannot be calibrated or are otherwise deemed to be at end of life. Our close knowledge of the products we distribute also allows our service staff to consult and advise customers on what products are best suited for their in-house calibration needs. We also believe that our proprietary software is a key differentiator from our competitors. CalTrak® and C3® are utilized by our customers in an integrated manner, providing a competitive barrier as customers realize synergies and efficiencies as a result of this integration.

In fiscal year 2020, we invested in a software solution for the automation of calibration procedures and datasheet generation. We are in the early testing phases with the rollout for the first limited set of calibration disciplines. In fiscal year 2019, we expanded our range of capabilities by making significant capital and staffing investments in reference-level radio frequency/microwave calibration capabilities. This allowed us to increase business with our prestigious clients in the enterprise computer manufacturing and aerospace defense sectors. In addition, we grew our mobile calibration laboratory fleet and added the ability to carry inventory and sell products while onsite. This was done to strategically target onsite calibration and instrument sales to the wind energy sector. We believe this mobile approach combined with our high-quality significantly improves our differentiation in this space.

Competition for laboratory instrument services is composed of both small local and regional service providers and large multi-national OEMs. We believe we are generally financially stronger, service a larger customer base and are typically able to offer a larger suite of services than many of the small local and regional competitors. The large OEMs may offer specialized services and brand-specific expertise which we do not offer, but they are generally focused on providing specialized services only for their proprietary brands and product lines, rather than servicing an array of brands and product lines as we do. We believe our competitive advantages in the laboratory instrument services market are our financial and technical resources, turnaround time, and flexibility to react quickly to customers’ needs. The breadth of our suite of laboratory instrument service, combined with our calibration service offerings, also differentiates us from our competitors by allowing us to be our customers’ one-source accredited services provider for their entire calibration and compliance programs.

Service Quality. The accreditation process is the only system currently in existence that validates measurement competence. To ensure that the quality and consistency of our calibrations are consistent with the global metrology network, designed to standardize measurements worldwide, we have sought and achieved international levels of quality and accreditation to provide uniformity across all locations with advanced levels of training for our technical staff. Our Calibration Service Centers are accredited to ISO/IEC 17025:2017 by ANSI-ASQ National Accreditation Board (“ANAB”) and other accrediting bodies. These accrediting bodies are International Laboratory Accreditation Cooperation Mutual Recognition Arrangement (“ILAC MRA”) signatories, are proficient in the technical aspects of the chemistry and physics that underlie metrology, and provide an objective, third-party, internationally accepted evaluation of the quality, consistency, and competency of our calibration processes. Accreditation also requires that all measurement standards used for accredited measurements have a fully documented path, known as Metrological Traceability, through the National Institute of Standards and Technology or the National Research Council (the National Measurement Institutes for the United States and Canada, respectively), or to other national or international standards bodies, or to measurable conditions created in our Calibration Service Centers, or accepted fundamental and/or natural physical constants, ratio type of calibration, or by comparison to consensus standards, all inclusive of measurement uncertainties.

7

The importance of this international oversight to our customers is the assurance that our service documentation will be accepted worldwide, removing one of the barriers to trade that they may experience if using a calibration laboratory provider whose accrediting body is not an ILAC MRA signatory. To provide the widest range of services to our customers in our target markets, our ISO/IEC 17025:2017 accreditations extend across many technical disciplines, including working-level and reference-level capabilities. We believe our scope of accreditation to ISO/IEC 17025:2017 to be the broadest for the industries we serve.

To reinforce our belief in the importance of calibration quality, we are leveraging a branding campaign for our Service segment that is centered around three simple words – “Calibrated by Transcat®”. We believe we have established a strong, differentiated brand that has a deep and meaningful association with quality, compliance and control. We want the phrase “Calibrated by Transcat®” to be synonymous with risk reduction and quality compliance.

Acquired calibration labs might use other quality registration systems. We continually evaluate when to integrate acquired quality systems with the focus on minimizing business disruptions and disruptions to our customers while maintaining our commitment to quality.

Our scopes of accreditation can be found at http://www.transcat.com/calibration-services/accreditation/calibration-lab-certificates.

Distribution Segment

Distribution Summary. We distribute professional grade test, measurement and control instrumentation throughout North America and internationally. Our customers use test and measurement instruments to ensure that their processes, and ultimately their end products, are within specification. Utilization of such diagnostic instrumentation also allows for continuous improvement processes to be in place, increasing the accuracies of their measurements. The industrial test and measurement instrumentation market, in those geographic areas where we predominately operate, has historically been serviced by broad-based national equipment distributors and niche or specialty-focused organizations such as Transcat. We offer value-added services such as calibration/certification of equipment purchases, equipment rentals, used equipment for sale, and equipment kitting. In recent years, online-based distributors have become more prevalent. To more effectively compete with these online-based distributors, we have continued to make improvements to our digital platform, including enhanced e-commerce capabilities.

We believe that a customer chooses a distributor based on a number of different criteria, including product availability, price, ease of doing business, timely delivery and accuracy of orders, consistent product quality, technical competence of the representative serving them and availability of value-added services. The decision to buy is generally made by plant engineers, quality managers, or their purchasing personnel, and products are typically obtained from one or more distributors as replacements, upgrades, or for expansion of manufacturing and research and development facilities. As a result, sales to Distribution customers are somewhat unpredictable and potentially non-recurring. Our online presence, including our website and e-newsletters; Master Catalog; supplemental mailings and other sales and marketing activities are designed to create interest and maintain a constant presence in front of our customers to ensure we receive the order when they are ready to purchase.

We provide our customers with value-added services, including technical support, to ensure our customers receive the right product for their application, and more comprehensive instrument suitability studies to customers in regulated industries who are concerned about the technical uncertainties that their testing or in-process instruments may bring to a process. We consider our biggest value-added service for our Distribution customers is the option to have calibration service performed on their new product purchases prior to shipment, allowing them to place newly acquired equipment directly into service upon receipt, saving downtime. We also offer online procurement, credit card payment options, same day shipment of in-stock items, kitted products, the option to rent, training programs and a variety of custom product offerings. Items are regularly added to and deleted from our product offerings on the basis of customer demand, recommendations of suppliers, sales volumes and other factors. Because of the breadth of our product and service offerings, we are often a “one-stop shop” for our customers who gain operational efficiency by dealing with just one distributor for most or all of their test and measurement instrumentation needs.

8

In fiscal year 2020, our Distribution segment performed well against our corporate strategy. We grew our core set of customers while focusing on strategic pricing initiatives that drove incremental gross profit. Our focus on higher margin channels such as used equipment and rentals will be a continual focus to bolster profitability in the Distribution segment. This effort is intended to offset competitive pressures in our legacy distribution business.

Distribution Marketing and Sales. We market, create demand and sell to our customers through multiple direct sales channels including our website, digital and print advertising, proactive outbound sales and an inbound call center. Our outbound and inbound sales teams are staffed with technically trained personnel who are available to help guide product selection. Our website serves as a sales channel for our products and services, and provides search capability, detailed product information, in-stock availability, selection guides, demo videos and downloadable product specification sheets. We have made investments in our website to implement the latest marketing technologies which allow us to provide an intuitive customer experience, with simple product comparison and quoting, ease at checkout and automated post-order follow-up. We also operate and maintain several industry-specific service websites, obtained through recent acquisitions. For example, the URL www.pipettes.com was obtained in connection with the acquisition of TTE. TTE focuses on selling pipettes, pipette supplies and related services to its customers. We believe with our digital marketing experience we can expand the web traffic and sales through www.pipettes.com.

We use a multichannel approach to reach our customers and prospective customers including our Master Catalog, periodic supplemental catalogs, website, e-newsletters, and other direct sales and marketing programs. Our digital marketing strategy includes ongoing investment in search engine optimization, application-specific digital content, pay-per-click search engine advertising, and product listings on online marketplaces such as Amazon and Google Shopping. We continue to invest in back-end technologies designed to provide a seamless customer experience across all our marketing channels. During fiscal year 2020, we proactively communicated with our customers and prospective customers through direct mail catalogs, email newsletters, vertical email drip campaigns, retargeting ads, educational webinars, and outbound sales calls. Some of the key factors that determine the marketing materials a customer may receive include relevancy of new product introductions, current promotions, purchase history, the customer’s market segment, and the contact’s job function.

As a result of strong relationships with our product vendors and our historical marketing program results, we have the opportunity to carry out co-branded marketing initiatives, aimed at our existing customers and our prospective customer base, for which we receive cooperative advertising support. These co-branded marketing initiatives typically feature specific vendors, new products or targeted product categories and take the form of direct mailers, web-based initiatives or outbound sales efforts.

Distribution Competition. The distribution market for industrial test and measurement instrumentation is fragmented and highly competitive. Our competitors range from large national distributors and manufacturers that sell directly to customers to small local distributors and online distributors. Key competitive factors typically include customer service and support, quality, lead time, inventory availability, brand recognition and price. To address our customers’ needs for technical support and product application assistance, we employ a staff of highly trained technical sales specialists. In order to maintain this competitive advantage, technical training is an integral part of developing our sales staff. To differentiate ourselves from competitors, we offer pre-shipment calibration or performance data reports which allow customers to receive our products and immediately place them into service, saving them downtime and money.

Online distributors, including Amazon which sells lower price-point products, have become prominent competitors for sales of handheld test and measurement equipment, competing primarily on price. While online competitors lack the value-added services we offer in our Distribution segment, they have been successful in capturing some market share in the worldwide market for test and measurement instruments. To stay ahead of growing competition from these online distributors and in keeping with the general trend of increased use of e-commerce, we continue to invest in our digital platform including a well-indexed website with improved design and functionality. In addition, we have diversified our offerings by expanding the brands and product lines that we offer and adding higher gross margin equipment rentals and used equipment sales, which we believe makes Transcat unique among our competitors.

9

Distribution Suppliers and Purchasing. We believe that effective purchasing is a key element to maintaining and enhancing our position as a provider of high-quality test and measurement instruments. We frequently evaluate our purchase requirements and suppliers’ offerings to obtain products at the best possible cost. We obtain our products from approximately 500 suppliers of brand name and private-labeled equipment. In fiscal year 2020, our top 10 vendors accounted for approximately 73% of our aggregate Distribution business.

We plan our product mix and inventory stock to best serve the anticipated needs of our customers, whose individual purchases vary in size. We can usually ship our top selling products to our customers the same day they are ordered.

Distribution Vendor Rebates. We have agreements with certain product vendors that provide for rebates based on meeting a specified cumulative level of purchases and/or incremental distribution sales. These rebates are recorded as a reduction of cost of distribution sales. Purchase rebates are calculated and recorded quarterly based upon our volume of purchases with specific vendors during the quarter. Point of sale rebate programs that are based on year-over-year sales performance on a calendar year basis are recorded as earned, on a quarterly basis, based upon the estimated level of annual achievement. Point of sale rebate programs that are based on year-over-year sales performance on a quarterly basis are recorded as earned in the respective quarter.

Distribution Operations. Our Distribution operations primarily take place at our 48,500 square-foot facility in Rochester, New York which includes 17,000 square feet of warehouse space. The Rochester location also serves as our corporate headquarters, houses our customer service, sales and administrative functions, and is a Calibration Service Center. We also have two smaller warehouse facilities. Our Wisconsin warehouse fulfills orders for certain large industrial scales and our Fullerton, California warehouse fulfills orders for used equipment and rental equipment. In fiscal year 2020, we shipped approximately 31,000 product orders.

Distribution Backlog. Distribution orders include orders for instruments that we routinely stock in our inventory, customized products, and other products ordered less frequently, which we do not stock. Pending product shipments are primarily backorders, but also include products that are requested to be calibrated in one of our Calibration Service Centers prior to shipment, orders required by the customer to be shipped complete or at a future date, and other orders awaiting final credit or management review prior to shipment. Our total backlog was $4.3 million and $3.9 million as of March 28, 2020 and March 30, 2019, respectively.

CUSTOMER SERVICE AND SUPPORT

Key elements of our customer service approach are our business development sales team, outbound sales team, account management team, inbound sales and customer service organization. To ensure the quality of service provided, we monitor our customer service through customer surveys, call monitoring and daily statistical reports.

| ● | Mail to Transcat, Inc., 35 Vantage Point Drive, Rochester, NY 14624; |

| ● | Telephone at 1-800-828-1470; |

| ● | Email at sales@transcat.com; |

| ● | Online at www.transcat.com; or |

| ● | Fax at 1-800-395-0543 |

INFORMATION REGARDING EXPORT SALES

In fiscal years 2020 and 2019, approximately 10% of our total revenue resulted from sales to customers outside the United States. Of those export sales in fiscal year 2020, approximately 12% were denominated in U.S. dollars and the remaining 88% were in Canadian dollars. Our revenue is subject to the customary risks of operating in an international environment, including the potential imposition of trade or foreign exchange restrictions, tariff and other tax increases, fluctuations in exchange rates and unstable political situations, any one or more of which could have a material adverse effect on our business, cash flows, balance sheet or results of operations. See “Foreign Currency” in Item 7A. of Part II and Note 7 to our Consolidated Financial Statements in this report for further details.

INFORMATION SYSTEMS

We utilize a turnkey enterprise software solution from Infor, Inc. (“Infor”) called Application Plus to manage our business and operations segments. This software includes a suite of fully integrated modules to manage our business functions, including customer service, warehouse management, inventory management, financial management, customer relations management and business intelligence. This solution is a fully mature business package and has been subject to more than 20 years of refinement. We utilize customer relationship management (“CRM”) software offered by SalesForce.com, Inc., which is strategically partnered with Infor, allowing us to fully integrate the CRM software with our Infor enterprise software.

10

We also utilize CalTrak®, our proprietary document and asset management system, to manage documentation, workflow and customers’ assets within and amongst most of our Calibration Service Centers. In addition to functioning as an internal documentation, workflow, and asset management system, CalTrak®, through C3®, provides customers with web-based calibration cycle management service and access to documentation relating to services completed by Transcat. Certain recent acquisitions utilize either third-party or their own proprietary calibration management systems. We continually evaluate when to integrate these acquired systems with a focus on obtaining operational synergies while imposing minimal disruption to customers.

INTELLECTUAL PROPERTY

We have federally registered trademarks for Transcat®, CalTrak®, C3® and Procision™, which we consider to be of material importance to our business. The registrations for these trademarks are in good standing with the U.S. Patent & Trademark Office. Our CalTrak® trademark is also registered in Canada for one class with the Canada Intellectual Property Office. Our trademark registrations must be renewed at various times, and we intend to renew our trademarks, as necessary, for the foreseeable future.

In addition, we own www.transcat.com and www.transcat.ca among other Internet domain names. As with phone numbers, we do not have, and cannot acquire any property rights to an Internet address. The regulation of domain names in the United States and in other countries is also subject to change. Regulatory bodies could establish additional top-level domains, appoint additional domain name registrars or modify the requirements for holding domain names. As a result, we might not be able to maintain our domain names or obtain comparable domain names, which could harm our business.

SEASONALITY

Our business has certain historical seasonal factors. Historically, our fiscal third and fourth quarters have been stronger than our fiscal first and second quarters due to the operating cycles of our industrial sector customers. Our Distribution segment has historically been strongest in our third fiscal quarter while Service has historically been strongest in our fourth fiscal quarter.

FISCAL YEAR

We operate on a 52/53 week fiscal year, ending the last Saturday in March. In a 52-week fiscal year, each of the four quarters is a 13-week period. In a 53-week fiscal year, the last quarter is a 14-week period. Fiscal year 2020 and 2019 both consisted of 52 weeks. Fiscal year 2021 which ends on March 27, 2021 (“fiscal year 2021”) will also have 52 weeks.

ENVIRONMENTAL MATTERS

We believe that we are in compliance with federal, state, and local provisions relating to the protection of the environment, and that continued compliance will not have any material effect on our capital expenditures, earnings, or competitive position.

EMPLOYEES

At the end of fiscal year 2020, we had 772 employees, including 50 part-time employees, compared with 685 employees, including 28 part-time employees, at the end of fiscal year 2019.

AVAILABLE INFORMATION

We file Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements and other information with the Securities and Exchange Commission (“SEC”). Our filings with the SEC are available on the SEC’s website at www.sec.gov. We also maintain a website at www.transcat.com. We make available, free of charge, in the Investor Relations section of our website, documents we file with or furnish to the SEC, including our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports. We make this information available as soon as reasonably practicable after we electronically file such materials with, or furnish such information to, the SEC. The other information found on our website is not part of this or any other report we file with, or furnish to, the SEC. Copies of such documents are available in print at no charge to any shareholder who makes a request. Such requests should be made to our corporate secretary at our corporate headquarters, 35 Vantage Point Drive, Rochester, New York 14624.

11

You should consider carefully the following risks and all other information included in this report. The risks and uncertainties described below and elsewhere in this report are not the only ones facing our business. If any of the following risks were to actually occur, our business, financial condition or results of operations would likely suffer. In that case, the trading price of our common stock could fall and you could lose all or part of your investment.

Our business, results of operations and financial condition may be adversely impacted by the COVID-19 pandemic. The COVID-19 pandemic has negatively affected the U.S. and global economies, disrupted global supply chains, resulted in significant travel and transport restrictions, including mandated closures and orders to “shelter-in-place,” and created significant disruption of the financial markets. We are closely monitoring the impact of the COVID-19 pandemic on all aspects of our business, including how it will impact our customers, employees and supply chain. Given the critical nature of the services and products that we provide, our calibration labs, distribution centers and support offices have remained open during the pandemic. While the COVID-19 pandemic did not have a material adverse effect on our reported results for the fourth quarter of fiscal year 2020, we are unable to predict the ultimate impact that it may have on our business, future results of operations, financial position or cash flows. The extent to which our operations may be impacted by the COVID-19 pandemic will depend largely on future developments, which are highly uncertain and cannot be accurately predicted. We may experience additional operating costs due to increased challenges with our workforce (including as a result of illness, absenteeism or government orders), access to supplies, capital, and fundamental support services (such as shipping and transportation). Even after the COVID-19 pandemic has subsided, we may experience materially adverse impacts to our business due to any resulting economic recession or depression. Furthermore, the impacts of a potential worsening of global economic conditions and the continued disruptions to and volatility in the financial markets remain unknown.

The impact of the COVID-19 pandemic may also exacerbate other risks discussed in this section, any of which could have a material adverse effect on us. This situation is changing rapidly and additional impacts may arise that we are not aware of currently.

The COVID-19 pandemic may significantly disrupt our workforce and internal operations. The COVID-19 pandemic may significantly disrupt our workforce if a significant percentage of our employees are unable to work due to illness, quarantines, government actions, facility closures in response to the pandemic, fear of acquiring COVID-19 while performing essential business functions, or as a result of recent changes to unemployment insurance where unemployed workers can receive, in the short-term, benefits in excess of what would be offered for working for us. As part of our response to the pandemic, we instituted hazard pay for certain employees that perform essential work at customer sites. While we remain fully operational as an essential business, we cannot guarantee that we will be able to adequately staff our operations when needed, particularly as the COVID-19 pandemic progresses, which may strain our existing personnel, increase costs, and negatively impact our operations. As a result, our internal operations may experience disruptions. The pandemic may create additional challenges in attracting and retaining quality employees in the future. In addition, COVID-19 related-illness could impact members of our board of directors resulting in absenteeism from meetings of the directors or committees of directors, making it more difficult to convene the quorums of the full board of directors or its committees needed to conduct meetings for the management of our affairs. We cannot predict the extent to which the COVID-19 pandemic may disrupt our workforce and internal operations.

We have taken certain precautions due to the COVID-19 pandemic that could negatively impact our business. In response to the COVID-19 pandemic, we have taken measures intended to protect the health and well-being of our employees, customers, and communities, which could negatively impact our business. These measures include temporarily requiring all non-essential employees (personnel whose roles allow) to work remotely, restricting work-related travel except for direct onsite service to our customers, restricting non-essential visitors from entering our sites, increasing the frequency and extent of cleaning and disinfecting facilities, workstations, and equipment, developing social distancing plans, and instituting specialized training to ensure the safe handling of our customers’ critical equipment. The health of our workforce, customers and communities is of primary concern and we may take further actions as may be required by government authorities or as we determine are in the best interests of our employees, customers and others. In addition, our management team has, and will likely continue to, spend significant time, attention and resources monitoring the COVID-19 pandemic and seeking to manage its effects on our business and workforce. The extent to which the pandemic and our precautionary measures may impact our business will depend on future developments, which are highly uncertain and cannot be predicted at this time.

The industries in which we compete are highly competitive, and we may not be able to compete successfully. Within our Service segment, we provide calibration services and compete in an industry that is highly fragmented and is composed of companies ranging from internationally recognized and accredited corporations to non-accredited sole proprietors, resulting in a tremendous range of service levels and capabilities. Also, within our Service segment, we provide compliance services and compete in an industry that is composed of both small local and regional service providers and large multi-national companies who are also OEMs. Within our Service segment, some of our larger competitors may have broader service capabilities and may have greater name recognition than us. Some manufacturers of the products we sell may also offer calibration and compliance services for their products.

12

Within our Distribution segment, we compete with numerous companies, including several major manufacturers and distributors. Most of our products are available from several sources and our customers tend to have relationships with several distributors. Competitors in the product distribution industry could also obtain exclusive rights to market particular products, which we would then be unable to market. Manufacturers could also increase their efforts to sell directly to end-users and bypass distributors like us. Industry consolidation among distributors, the unavailability of products, whether due to our inability to gain access to products or interruptions in supply from manufacturers, including as a result of the COVID-19 pandemic, or the emergence of new competitors could also increase competition and adversely affect our business or results of operations.

In each of the industries in which we compete, some of our competitors have greater financial and other resources than we do, which could allow them to compete more successfully. In the future, we may be unable to compete successfully and competitive pressures may reduce our sales.

Competition in our Distribution segment is changing with an increase in web-based distributors. We may not be able to compete successfully. We face substantial and increased competition throughout the world, especially in our Distribution segment. The competition is changing, with web-based distributors becoming more prevalent and increasing their market share. Some of our competitors are much larger than us. Changes in the competitive landscape pose new challenges that could adversely affect our ability to compete. Entry or expansion of other vendors into this market may establish competitors that have larger customer bases and substantially greater financial and other resources with which to pursue marketing and distribution of products. Their current customer base and relationships, as well as their relationships and ability to negotiate with manufacturers, may also provide them with a competitive advantage. If we are unable to effectively compete with our current and future competitors, our ability to sell products could be harmed and could result in a negative impact on our Distribution segment. Any erosion of our competitive position could have a material adverse effect on our business, results of operations, and financial condition.

Cybersecurity incidents could adversely affect our business by causing a disruption to our operations, a compromise or corruption of our confidential information and/or damage to our business relationships, all of which could negatively impact our business, results of operations or financial condition. We rely extensively on information technology (“IT”) systems, some of which are provided by third parties, to support our business activities, including for orders and the storage, processing and transmission of our electronic, business-related, information assets used in or necessary to conduct business. The data we store and process may include customer payment information, personal information concerning our employees, confidential financial information and other types of sensitive business-related information. Numerous and evolving cybersecurity threats pose potential risks to the security of our IT systems, networks and services, as well as the confidentiality, availability and integrity of our data. To mitigate the spread of COVID-19, some of our office personnel transitioned to remote work environments which may exacerbate various cybersecurity risks to our business, including an increased risk of phishing and other social engineering attacks, and an increased risk of unauthorized dissemination of sensitive personal, proprietary or other confidential information. Global cybersecurity threats can range from uncoordinated individual attempts to gain unauthorized access to our IT systems to sophisticated and targeted measures known as advanced persistent threats. The techniques used in these attacks change frequently and may be difficult to detect for periods of time and we may face difficulties in anticipating and implementing adequate preventative measures. While we employ comprehensive measures to prevent, detect, address and mitigate these threats (including access controls, data encryption, vulnerability assessments, management training, continuous monitoring of our IT networks and systems and maintenance of backup and protective systems), cybersecurity incidents, depending on their nature and scope, could potentially result in the misappropriation, destruction, corruption or unavailability of critical data or proprietary information and the disruption of business operations. The potential consequences of a material cybersecurity incident include reputational damage, compromised employee, customer, or third-party information, litigation with third parties, regulatory actions, and increased cybersecurity protection and remediation costs, which in turn could adversely affect our business and results of operations. In addition, the laws and regulations governing security of data on IT systems and otherwise held by companies is evolving and adding layers of complexity in the form of new requirements and increasing costs of attempting to protect IT systems and data and complying with new cybersecurity regulations.

13

If we experience a significant disruption in, or breach in security of, our IT systems, or if we fail to implement new systems and software successfully, our business could be adversely affected. Our IT systems may be susceptible to damage, disruptions or shutdowns due to power outages, hardware failures, telecommunication failures, user errors, catastrophes or other unforeseen events. Our IT systems also may experience interruptions, delays or cessations of service or produce errors in connection with system integration, software upgrades or system migration work that takes place from time to time. In addition, technology resources may be strained due to the increase in the number of remote users in response to the COVID-19 pandemic. If we were to experience a prolonged system disruption in the IT systems that involve our interactions with customers or suppliers, it could result in the loss of sales and customers and significant incremental costs, which could adversely affect our business.

Our revenue and ability to achieve our stated corporate objectives depends on our senior management and our ability to retain recruit, train and retain quality employees. Our success is dependent on our senior management and our ability to attract, retain and motivate qualified personnel, especially skilled service technicians. Competition for senior management is intense, and we may not be successful in attracting and retaining key personnel. Qualified skilled service technicians are in high demand and are subject to competing offers. The ability to meet our labor needs while controlling costs associated with hiring and training new employees is subject to external factors such as unemployment levels and prevailing wage rates. The loss of services of any member of our senior management team or key employees, and the inability to attract and retain other qualified personnel, especially skilled service technicians, could affect our ability to achieve our stated corporate objectives and could adversely impact our business and results of operations.

We expect that our quarterly results of operations will fluctuate. Such fluctuations could cause our stock price to decline. A large portion of our expenses for our Service segment, including expenses for facilities, equipment and personnel are relatively fixed. Accordingly, if revenues decline or do not grow as we anticipate, we may not be able to correspondingly reduce our expenses in any particular quarter. Our quarterly revenues and operating results have fluctuated in the past and are likely to do so in the future. Historically, our fiscal third and fourth quarters have been stronger than our fiscal first and second quarters due to industrial operating cycles. Fluctuations in industrial demand for products we sell and services we provide, including as a result of the COVID-19 pandemic, could cause our revenues and operating results to fluctuate. If our operating results in some quarters fail to meet the expectations of stock market analysts and investors, our stock price may decline.

If we do not effectively compete in the rental test and measurement equipment market, our operating results may be adversely affected. We compete in the rental market on the basis of a number of factors, including equipment availability, price, service and reliability. Some of our competitors may offer similar equipment for rent at lower prices and may offer more extensive servicing, or financing options. In addition, if the supply of rental equipment available on the market significantly increases, demand for and pricing of our rental products could be adversely impacted lowering our gross margins on rentals. Further, customers’ confronting competing budget priorities and more limited resources as a result of the COVID-19 pandemic could lead to less demand for rental equipment and increased pressure on pricing. Failure to adequately forecast the adoption of and demand for equipment may cause us not to meet our customers’ rental equipment requirements and may adversely affect our operating results.

Our stock price may be volatile. The stock market, from time to time, has experienced significant price and volume fluctuations that are both related and unrelated to the operating performance of companies. Our stock may be affected by market volatility and by our own performance. The following factors, among others, may have a significant effect on the market price of our common stock:

| ● | The impact of the COVID-19 pandemic on the capital markets; |

| ● | Developments in our relationships with current or future manufacturers of products we distribute; |

| ● | Announcements by us or our competitors of significant acquisitions, strategic partnerships, joint ventures or capital commitments; |

| ● | Litigation or governmental proceedings or announcements involving us or our industry; |

| ● | Economic and other external factors, such as disasters or other crises; |

| ● | Sales of our common stock or other securities in the open market; |

| ● | Repurchases of our common stock on the open market or in privately-negotiated transactions; |

| ● | Period-to-period fluctuations in our operating results; and |

| ● | Our ability to satisfy our debt obligations. |

14

If we fail to adapt our technology to meet customer needs and preferences, the demand for our products and services may diminish. Our future success will depend on our ability to develop services and solutions that keep pace with technological change, evolving industry standards and changing customer preferences in the markets we serve. We cannot be sure that we will be successful in adapting existing or developing new technology or services in a timely or cost-effective manner or that the solutions we do develop will be successful in the marketplace. Our failure to keep pace with changes in technology, industry standards and customer preferences in the markets we serve could diminish our ability to retain and attract customers and retain our competitive position, which could adversely impact our business and results of operations.

We rely on our CalTrak®, Application Plus (our enterprise resource planning system) and other management information systems for inventory management, distribution, workflow, accounting and other functions. If our CalTrak®, Application Plus or other management information systems fail to adequately perform these functions, experience an interruption in their operation or a security breach, our business and results of operations could be adversely affected. The efficient operation of our business depends on our management information systems. We rely on our CalTrak®, Application Plus and other management information systems to effectively manage accounting and financial functions, customer service, warehouse management, order entry, order fulfillment, inventory replenishment, documentation, asset management, and workflow. Our management information systems are vulnerable to damage or interruption from computer viruses or hackers, natural or man-made disasters, vandalism, terrorist attacks, power loss, or other computer systems, internet, telecommunications or data network failures. Any such interruptions to our management information systems could disrupt our business and could result in decreased revenues, increased overhead costs, excess inventory and product shortages, causing our business and results of operations to suffer. In addition, our management information systems are vulnerable to security breaches. Our security measures or those of our third-party service providers may fail to detect or prevent such security breaches. Security breaches could result in the unauthorized publication of our confidential business or proprietary information, the unauthorized release of customer, vendor, or employee data and payment information, the violation of privacy or other laws, and the exposure to litigation, any of which could harm our business and results of operations.

Our enterprise resource planning system is aging, and we may experience issues from any implementation of a new enterprise resource planning system. We have an enterprise resource planning system (“ERP”) to assist with the collection, storage, management and interpretation of data from our business activities to support future growth and to integrate significant processes. Although we use current versions of software and have support agreements in place, due to the age of our ERP, we anticipate that a new ERP will be required to be implemented sometime in the future. ERP implementations are complex and time-consuming and involve substantial expenditures on system software and implementation activities, as well as changes in business processes. Our ERP system is critical to our ability to accurately maintain books and records, record transactions, provide important information to our management and prepare our consolidated financial statements. ERP implementations also require the transformation of business and financial processes in order to reap the benefits of the ERP system; any such transformation involves risks inherent in the conversion to a new computer system, including loss of information and potential disruption to our normal operations. Any disruptions, delays or deficiencies in the design and implementation of a new ERP system could adversely affect our ability to process orders, provide services and customer support, send invoices and track payments, fulfill contractual obligations or otherwise operate our business. Additionally, if the ERP system does not operate as intended, the effectiveness of our internal control over financial reporting could be adversely affected or our ability to assess it adequately could be delayed.

We may not successfully integrate business acquisitions. We completed three acquisitions during fiscal year 2020 and two acquisitions during fiscal year 2019. If we fail to accurately assess and successfully integrate any recent or future business acquisitions, we may not achieve the anticipated benefits, which could result in lower revenues, unanticipated operating expenses, reduced profitability and dilution of our book value per share. Successful integration involves many challenges, including:

| ● |

The difficulty of integrating acquired operations and personnel with our existing operations, which could be exacerbated by the impact of the COVID-19 pandemic; |

| ● |

The difficulty of developing and marketing new products and services; |

| ● |

The diversion of our management’s attention as a result of evaluating, negotiating and integrating acquisitions; |

| ● |

Our exposure to unforeseen liabilities of acquired companies; and |

| ● |

The loss of key employees of an acquired operation. |

In addition, an acquisition could adversely impact cash flows and/or operating results, and dilute shareholder interests, for many reasons, including:

| ● |

Charges to our income to reflect the impairment of acquired intangible assets, including goodwill; |

| ● |

Interest costs and debt service requirements for any debt incurred in connection with an acquisition or new business venture; and |

| ● |