UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from __________ to __________.

Commission File Number 001-16191

(Exact name of registrant as specified in its charter)

| State or other jurisdiction of | (I.R.S. Employer | |||||||

| incorporation or organization | Identification No.) | |||||||

(Address of principal executive offices)

(Zip Code)

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None | ||||||||||||||

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. | þ | No | ||||||||||||

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | Yes | þ | ||||||||||||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | þ | No | ||||||||||||

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | þ | No | ||||||||||||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See definitions of “large accelerated filer,” "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act. | ||||||||||||||

| þ | Accelerated filer | o | ||||||||||||

| Non-accelerated filer | o | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | o | |||||||||||||

| Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act by the registered public accounting firm that prepared or issued its audit report. | ||||||||||||||

| If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. | ||||||||||||||

| Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). | o | |||||||||||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | Yes | þ | No | |||||||||||

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2023, was $1,486,501,585 .

As of January 31, 2024, there were 18,620,098 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2023 annual meeting of shareholders (the “2023 Proxy Statement”) are incorporated by reference in Part III.

1

Tennant Company

Form 10–K

Table of Contents

| Page | |||||||||||||||||

2

TENNANT COMPANY

2023

ANNUAL REPORT

Form 10–K

PART I

ITEM 1 – Business

General Development of Business

Founded in 1870 by George H. Tennant, Tennant Company ("the Company, we, us, or our"), headquartered in Eden Prairie, Minnesota, is a world leader in designing, manufacturing and marketing of solutions that help create a cleaner, safer and healthier world. Tennant was incorporated as a Minnesota corporation in 1909 and began as a one-man woodworking business, eventually evolving into a successful wood flooring and wood products company, and finally into a manufacturer of floor cleaning equipment. Throughout its history, the Company has remained focused on advancing our industry by aggressively pursuing new technologies and creating a culture that celebrates innovation.

Today, the Company has 11 global manufacturing locations and operates in three geographic areas including the Americas, Europe, Middle East and Africa (EMEA) and Asia Pacific (APAC). We aggregate our operating segments into one reportable segment that consists of the design, manufacture, sale and servicing of products used primarily in the maintenance of nonresidential surfaces. The Company is committed to developing innovative and sustainable solutions that help our customers clean spaces more effectively with high-performance solutions that minimize waste, reduce costs, improve safety and further sustainability goals.

Principal Products, Markets and Distribution

The Company offers products and solutions consisting of manual and mechanized cleaning equipment for both industrial and commercial use, detergent-free and other sustainable cleaning technologies, aftermarket parts and consumables, equipment maintenance and repair services, and business solutions such as financing, rental and leasing programs, and machine-to-machine asset management solutions. The Company is committed to developing cleaning technologies, including autonomous solutions, which increase cleaning productivity. We have strong brand presence in the global markets we serve, offering both premium and mid-tier products for each region to meet customer needs.

The Company's products are used in many types of environments including: factories and warehouses, distribution centers, office buildings, public venues such as arenas and stadiums, office buildings, schools and universities, hospitals and clinics, and more. The Company markets its offerings under the following brands: Tennant®, Nobles®, Alfa Uma Empresa Tennant™, IPC, Gaomei and Rongen brands as well as private-label brands. The Company has a portfolio of differentiated technology solutions that includes IRIS® as an asset management solution, ec-H2O NanoClean® as a detergent-free cleaning solution, and ReadySource® as a rapid-drying carpet cleaning technology. The Company's more than 40,000 customers include contract cleaners to whom organizations outsource facilities maintenance, as well as businesses that perform facilities maintenance themselves. The Company reaches these customers through the industry's largest direct sales and service organization and through a strong and well-supported network of authorized distributors worldwide.

The Company has an extensive global field service network. We sell products directly in 15 countries and through distributors in more than 100 countries.

3

Raw Materials and Component Parts

Steel, metal alloys and resin are the primary raw materials used to manufacture our mechanized cleaning equipment. We purchase various component parts, electronics and services used in production, logistics and product development processes from third parties. The Company has experienced cost inflation and constrained supply of certain raw materials and component parts. The Company continues work to minimize the impact of cost inflation and market supply challenges by employing local-for-local and region-for-region manufacturing and sourcing to allow us to manufacture our products closer to our customers. At the same time, our engineering teams are evaluating platform design to allow for available parts and to increase our sourcing flexibility.

Intellectual Property

The Company owns a broad range of intellectual property rights in both the United States and a number of foreign countries. Our patents, proprietary technologies and trade secrets, customer relationships, licenses, trademarks, trade names and brand names in the aggregate constitute a valuable asset, but we do not regard our business as being materially dependent upon any single item or category of intellectual property. We take appropriate measures to protect our intellectual property to the extent such intellectual property can be protected.

Research and Development

Research and development expenses include scientific research costs such as salaries, prototypes, shop supplies, testing, technical information technology and administrative expenditures as well as an allocation of corporate costs. We conduct research and development activities to develop new products and to enhance the functionality, effectiveness, ease of use and reliability of our existing products. We believe that our research and development efforts have been, and continue to be, key drivers of our success in the marketplace.

Seasonality

Although the Company’s business is not seasonal in the traditional sense, the percentage of revenues in each quarter typically ranges from 22% to 28% of the total year. The first quarter tends to be at the low end of the range reflecting customers’ initial slow ramp up of capital purchases and the Company’s efforts to close out orders at the end of each year. The second and fourth quarters tend to be toward the high end of the range and the third quarter is typically in the middle of the range.

Major Customers

The Company sells a wide range of products to a diversified base of customers around the world and has no material concentration of credit risk or significant payment terms extended to customers.

Competition

Public industry data concerning global market share is limited; however, through an assessment of validated third-party sources and sponsored third-party market studies, the Company is confident in its position as a world-leading manufacturer of floor maintenance and cleaning equipment. Several global competitors compete with the Company in virtually every geography of the world. Additionally, small regional competitors are also significant competitors who vary by country, vertical market, product category or channel. The Company competes primarily on the basis of offering a broad line of high-quality, innovative products supported by an extensive sales and service network in major markets.

Human Capital

As of December 31, 2023, we employed approximately 4,457 employees who are guided by our vision to design, manufacture and market sustainable solutions that help create a cleaner, safer and healthier world.

Ethics and Employee Safety

4

Tennant Company has a commitment to our employees to foster and uphold a culture of integrity and stewardship. We ensure that our employees are not only aware of ethical standards, but actively contribute to maintaining them. As part of this commitment, Tennant conducts annual Code of Conduct training that empowers our staff with the knowledge and tools to make ethical decisions in their roles. We understand the importance of fostering an environment where concerns can be raised without fear of reprisal. To facilitate this, we offer various avenues for reporting concerns, including a dedicated ethics hotline accessible both via phone and online.

We prioritize the health and safety of all employees. We operate under our established safety programs and employ an experienced team of health and safety specialists to provide support to employees globally. All locations work diligently to meet and/or exceed regulatory standards applicable to each site. Tennant employees are empowered to stop work anytime there is a potential hazard identified. Each site maintains public and confidential ways for employees to report safety concerns to ensure employees feel free to report their concerns.

Talent

We believe attraction, development, engagement, and retention of a diverse group of employees is key to achieving our organizational objectives. We focus on creating a high-performance culture, which includes our annual performance management process for all employees which aligns with our employee and leadership competency frameworks.

To support employee development, we have deployed a number of resources including our philosophy and development tools for all employees via our intranet. We also provide leaders access to on-demand eLearnings and targeted live training sessions. In addition, we engage in annual talent conversations to help identify, develop, and deploy talent to achieve our objectives and address talent risks.

We believe talent feedback is key to engagement and survey our employees regularly. Also, we provide other feedback and engagement avenues such as all employee quarterly town halls and leadership meetings. We take action to drive improvement in our ability to engage and retain talent.

Diversity, Equity, and Inclusion (DE&I)

Tennant Company believes that an inclusive and diverse workforce contributes to our business success. The inclusion of diverse perspectives enables innovation and our ability to serve customers. We continue our DE&I focus through strategies which engage and educate our employees, promote inclusion, and drive effective governance.

Tennant Company proudly continues our commitment to be an equal opportunity employer. We make employment decisions based on the basis of individual skill, ability, reliability, productivity, and other factors important to performance.

Women represent 50% of our executive management team and 33% of our Board of Directors as of December 31, 2023.

Gender Equitable Pay

Tennant Company annually performs a gender wage gap for its United States employees that controls for title, grade and work location, which are legitimate and non-discretionary reasons for pay differences. The most recent assessment found that the median total income for females was 99.6% of the median total income for males, suggesting there is no evidence of a gender pay gap in the United States at Tennant Company.

Employee Gender Statistics

5

The following table represents employees by region and gender as of December 31, 2023:

| Female | Male | Total | |||||||||

| Americas | 439 | 1,910 | 2,349 | ||||||||

| Europe, Middle East, Africa | 446 | 1,195 | 1,641 | ||||||||

| Asia Pacific | 140 | 327 | 467 | ||||||||

| Total | 1,025 | 3,432 | 4,457 | ||||||||

Total Rewards

Tennant Company’s philosophy is to reward employees competitively for the work they perform consistent with position, skill level, experience, knowledge and geographic location. Each year, we evaluate the competitiveness of our pay levels against relevant labor markets and adjust our programs as appropriate. We offer a comprehensive total rewards package to our employees that includes pay, benefits, recognition, and well-being programs which are tailored by geographic location, statutory requirements, and competitive practice.

Available Information

The Company's internet address is www.tennantco.com. The Company makes available free of charge, through the Investor Relations website at investors.tennantco.com, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable when such material is filed electronically with, or furnished to, the Securities and Exchange Commission (“SEC”). The SEC also maintains an internet site that contains reports, proxy and information statements, and other information, which can be accessed at sec.gov.

Information About Our Executive Officers

The list below identifies those persons designated as executive officers of the Company, including their age, positions held with the Company and their business experience during the past five or more years.

Barb Balinski, Senior Vice President, Innovation and Technology

Barb Balinski (60) joined the Company in 2018 as Vice President of Engineering and in March 2021, she was named Senior Vice President, Innovation and Technology, leading Research & Development (R&D), Marketing, and Information Technology (IT) functions for Tennant Company. Prior to joining Tennant, Ms. Balinski held leadership positions of increasing responsibility with the engineering team for the Integrated Business Units at Whirlpool Corporation, a multinational manufacturer of home appliances, from 2005 to 2017, most recently as Director, Product Development, from 2013 to 2017. Prior to Whirlpool Corporation, she spent eleven years with Saturn Corporation, a subsidiary of General Motors.

David W. Huml, President and Chief Executive Officer

David W. Huml (55) has served as the Company's President and Chief Executive Officer since March 2021, after serving as Chief Operating Officer from March 2020 to March 2021. Mr. Huml joined the Company in November 2014 as Senior Vice President, Global Marketing and was named President and Chief Executive Officer March 1, 2021. In January 2016, he also assumed oversight for the Company's APAC business unit, and in January 2017, he assumed oversight for the Company's EMEA business. From 2006 to October 2014, he held various positions with Pentair plc, a global manufacturer of water and fluid solutions, valves and controls, equipment protection and thermal management products, most recently as Vice President, Applied Water Platform. From 1992 to 2006, he held various positions with Graco Inc., a designer, manufacturer and marketer of systems and equipment to move, measure, control, dispense and spray fluid and coating materials, including Worldwide Director of Marketing, Contractor Equipment Division.

6

Kristin A. Erickson, Senior Vice President, General Counsel and Corporate Secretary

Kristin A. Erickson (51) has served as the Company's Senior Vice President, General Counsel and Corporate Secretary since December 2020. Ms. Erickson joined the Company's legal department in April 2008, serving in roles of increasing responsibility, including as Vice President, Deputy General Counsel and Chief Compliance Officer from 2019 to 2020, and as Interim General Counsel and Corporate Secretary in 2020. Prior to joining Tennant in 2008, she served as Senior Counsel and Assistant Secretary for MoneyGram International, Inc., from 2004 to 2008. She started her career as a corporate attorney for Lindquist & Vennum, PLLP (n/k/a Ballard Spahr LLP).

Fay West, Senior Vice President, Chief Financial Officer

Fay West (54) joined the Company in April 2021 as Senior Vice President and Chief Financial Officer. Prior to joining Tennant, she was Senior Vice President and Chief Financial Officer of SunCoke Energy, Inc., a raw material processing and handling company, from 2014 to 2021. Before joining SunCoke Energy, Inc., in 2011, as Vice President and Controller, she was Assistant Controller at United Continental Holdings, Inc. Prior to that role, she served in several leadership roles at PepsiAmericas, Inc., including Vice President of Accounting and Financial Reporting, and Director of Financial Reporting. Prior to joining PepsiAmericas, Inc., she was Vice President and Controller of GATX Rail Company.

Richard H. Zay, Senior Vice President, Chief Commercial Officer

Richard H. Zay (53) has served as the Company's Senior Vice President, Chief Commercial Officer since March 2021. Mr. Zay joined the Company in June 2010 as Vice President, Global Marketing and was named Senior Vice President, Global Marketing in October 2013 and Senior Vice President of the Americas business unit for the Company in 2014. In 2018, he assumed responsibility for Tennant Research and Development as well. From 2006 to June 2010, he held various positions with Whirlpool Corporation, most recently as General Manager, KitchenAid Brand. From 1993 to 2006, he held various positions with Maytag Corporation, including Vice President, Jenn-Air Brand, Director of Marketing, Maytag Brand, and Director of Cooking Category Management.

Brock R. Christianson, Senior Vice President, Chief Human Resources Officer

Brock R. Christianson (54) joined the Company in November 2023 as Senior Vice President, Chief Human Resources Officer. From 2017 to October 2023, Mr. Christianson served in various Human Resources Vice President roles at Thrivent, a Fortune 500 financial services company. He held senior positions at Honeywell International from 2011 to 2017, including global Vice President of HR for the Environmental, Combustion, and Controls business unit. From 1998 to 2011, he worked at Medtronic, a global healthcare technology leader, where he held HR leadership roles in corporate, business units, and EMEA. Prior to Medtronic, he held HR and consulting roles with Emerson Electric and Ernst & Young.

ITEM 1A – Risk Factors

The following are risk factors known to us that could materially adversely affect our business, financial condition or operating results.

Macroeconomic Risks

We may encounter financial difficulties if the United States or other global economies experience an additional or continued long-term economic downturn, decreasing the demand for our products and negatively affecting our sales growth.

Our product sales are sensitive to declines in capital spending by our customers. Decreased demand for our products could result in decreased revenues, profitability and cash flows and may impair our ability to maintain our operations and fund our obligations to others. In the event of a continued long-term economic downturn in the U.S. or other global economies, our revenues could decline to the point that we may have to take cost-saving measures, such as restructuring actions. In addition, other fixed costs would have to be reduced to a level that is in line with a lower level of sales. A long-term economic downturn that puts downward pressure on sales could also negatively affect investor perception relative to our publicly stated profit targets.

7

Our operations could be adversely affected by geopolitical tensions or health epidemics.

We may be adversely impacted by factors outside of our control, including geopolitical tensions or public health epidemics. Geopolitical tensions, acts of violence or war, or other international conflicts may also adversely impact our operations. Public health epidemics, such as the COVID-19 pandemic, have impacted economic markets, manufacturing operations, supply chains, employment and consumer behavior in nearly every geographic region and industry across the world, and we have been, and may in the future be, adversely affected as a result.

Our global operations are subject to laws and regulations that impose significant compliance costs and create reputational and legal risk.

Due to the international scope of our operations, we are subject to a complex system of commercial, tax, compliance and trade regulations around the world. Recent years have seen an increase in the development and enforcement of laws regarding trade, tax compliance, data-privacy, sustainability, labor and safety and anti-corruption, including the U.S. Foreign Corrupt Practices Act, and similar laws from other countries. Our numerous foreign subsidiaries and affiliates are governed by laws, rules and business practices that differ from those of the U.S., but because we are a U.S.-based company, oftentimes they are also subject to U.S. laws which can create a conflict. Despite our due diligence, there is a risk that we do not have adequate resources or comprehensive processes to stay current on changes in laws or regulations applicable to us worldwide and maintain compliance with those changes. Increased compliance requirements may lead to increased costs and erosion of desired profit margin. As a result, it is possible that the activities of these entities may not comply with U.S. laws or business practices or our Code of Conduct. Violations of the U.S. or local laws may result in severe criminal or civil sanctions, could disrupt our business, and result in an adverse effect on our reputation, business and results of operations or financial condition. We cannot predict the nature, scope or effect of future regulatory requirements to which our operations might be subject or the manner in which existing laws might be administered or interpreted.

Industry Risks

We may be unable to take advantage of product pricing due to the competitive marketplace and increased price sensitivity.

Simplification of our customer product pricing is a key initiative to reduce the complexity in which we operate. The current competitive landscape, coupled with macroeconomic factors such as inflation, could impact our ability to achieve our pricing targets and influence demand. These pressures, along with internal constraints, may limit our ability to sell our products at our expected prices and may result in a change to the mix of product offerings that affect gross margin rates. Increasing our prices in this competitive market, where customers are very price sensitive, could have an adverse effect on our financial condition or operating results.

We are subject to competitive risks associated with developing innovative products and technologies, including, but not limited to, our inability to expand as rapidly or aggressively in the global market as our competitors, our customers ceasing to pay for innovation and competitive challenges to our products, technology and the underlying intellectual property.

Our products are sold in competitive markets throughout the world. Competition is based on product features and design, brand recognition, reliability, durability, technology, breadth of product offerings, price, customer relationships and after-sale service. Although we believe that the performance and price of our products will produce competitive solutions for our customers’ needs, certain products are priced higher than our competitors’ products. This is due to our dedication to innovation and continued investments in research and development. We believe that customers will pay for the innovations and quality in our products. However, it may be difficult for us to compete with lower priced products offered by our competitors and there can be no assurance that our customers will continue to choose our products over products offered by our competitors. If our products, markets and services are not competitive, we may experience a decline in sales volume, an increase in price discounting and a loss of market share, which would adversely impact our revenues, margin and the success of our operations.

Third parties may also initiate litigation to challenge the validity of our patents or claims, allege that we infringe upon their patents, violate our patents or they may use their resources to design comparable products that avoid infringing our patents. Regardless of whether such litigation is successful, such litigation could

8

significantly increase our costs and divert management’s attention from the operation of our business, which could adversely affect our results of operations and financial condition.

Disruption in the availability of, quality, or increases in the cost of, raw materials and components that we purchase or labor required to manufacture our products could negatively impact our operating results or financial condition.

Our sales growth and expanding geographical footprint, coupled with suppliers’ potential credit issues, could lead to an increased risk of a breakdown in our supply chain. Our use of sole-source vendors for certain parts creates a concentration risk. There is an increased risk of defects due to the highly configured nature of our purchased component parts that could result in quality issues, returns or production slowdowns. In addition, modularization may lead to more sole-sourced products, and as we seek to outsource the design of certain key components, we risk loss of proprietary control and becoming more reliant on a sole source. There is also a risk that the vendors we choose to supply our parts and equipment fail to comply with our quality expectations, thus damaging our reputation for quality and negatively impacting sales.

Global supplier production for various component parts is limited. We may experience disruption of the supply of key component parts. Cost inflation and market supply challenges may negatively impact our financial results.

We have and may continue to experience higher than normal wage inflation due to skilled labor shortages. The labor shortages have unfavorably impacted our gross profit margins and could continue to do so if actions we are taking are not effective at offsetting these rising costs. Changes and uncertainties related to government fiscal and tax policies, including increased duties, tariffs, or other restrictions, could adversely affect demand for our products, the cost of the products we manufacture or our ability to cost-effectively source raw materials, all of which could have a negative impact on our financial results.

Increasing cost pressures could negatively impact our ability to achieve our strategic objectives and affect our financial results.

We are dependent on key suppliers to make certain materials available at a contracted price. Labor, overhead, and material costs have increased and we may not be able to offset these increased manufacturing costs with a higher finished product price. We also may not be able to push those direct cost increases onto our customers in a timely manner given the competitive environment. A decline in demand for our products may have a direct impact on our ability to achieve better pricing through volume discounts.

We are subject to product liability claims and product quality issues that could adversely affect our operating results or financial condition.

Our business exposes us to potential product liability risks that are inherent in the design, manufacturing and distribution of our products. If products are used incorrectly by our customers, injury may result leading to product liability claims against us. Some of our products or product improvements may have defects or risks that we have not yet identified that may give rise to product quality issues, liability and warranty claims. Quality issues may also arise due to changes in parts or specifications with suppliers and/or changes in suppliers. If product liability claims are brought against us for damages that are in excess of our insurance coverage or for uninsured liabilities and it is determined we are liable, our business could be adversely impacted. Any losses we suffer from any liability claims, and the effect that any product liability litigation may have upon the reputation and marketability of our products, may have a negative impact on our business and operating results. We could experience a material design or manufacturing failure in our products, a quality system failure, other safety issues, or heightened regulatory scrutiny that could warrant a recall of some of our products. Any unforeseen product quality problems could result in loss of market share, reduced sales and higher warranty expense.

9

Operational Risks

Our ability to effectively operate our Company could be adversely affected if we are unable to attract and retain key personnel and other highly skilled employees, provide employee development opportunities and create effective succession planning strategies.

Our growth strategy, expanding global footprint, changing workforce demographics and increased improvements in technology and business processes designed to enhance the customer experience are putting increased pressure on human capital strategies designed to attract, retain and develop top talent.

Our continued success will depend on, among other things, the skills and services of our executive officers and other key personnel. Our ability to attract and retain highly qualified managerial, technical, manufacturing, research, sales and marketing personnel also impacts our ability to effectively operate our business. As companies grow and increase their hiring activities, there is an inherent risk of increased employee turnover and the loss of valuable employees in key positions, especially in emerging markets. We believe the increased loss of key personnel within a concentrated region could adversely affect our sales performance.

We may not be able to develop or manage strategic planning and growth processes or the related operational plans to deliver on our strategies and establish a broad organization alignment, thereby impairing our ability to achieve future performance expectations.

We are continuing to refine our global company strategy to guide our next phase of performance as our structure has become more complex. We continue to consolidate and reallocate resources as part of our ongoing efforts to optimize our cost structure and to drive synergies. Our operating results may be negatively impacted if we are unable to implement new processes and manage organizational changes, which include changes to our go-to-market strategy, systems and processes; simultaneous focus on expense control and growth; and introduction of alternative cleaning methods. In addition, if we do not effectively realize and sustain the benefits that these transformations are designed to produce, we may not fully realize the anticipated savings of these actions or they may negatively impact our ability to serve our customers or meet our strategic objectives.

We may not be able to upgrade and evolve our information technology systems as quickly as we wish and we may encounter difficulties as we upgrade and evolve these systems to support our growth strategy and business operations, which could adversely impact our abilities to accomplish anticipated future cost savings and better serve our customers.

We have many information technology systems that are important to the operation of our business and are in need of upgrading in order to effectively implement our enterprise strategy. Given our greater emphasis on customer-facing technologies, we may not have adequate resources to upgrade our systems at the pace which the current business environment demands. Additionally, significantly upgrading and evolving the capabilities of our existing systems, including ERP modernization, could lead to inefficient or ineffective use of our technology due to lack of training or expertise in these evolving technology systems. These factors, among other things, could lead to significant expenses, adversely impacting our results of operations and hindering our ability to offer better technology solutions to our customers.

We may encounter risks to our IT infrastructure, such as access and security, that may not be adequately designed to protect critical data and systems from theft, corruption, unauthorized usage, viruses, sabotage or unintentional misuse.

Global cybersecurity threats and incidents can range from uncoordinated individual attempts to gain unauthorized access to IT systems to sophisticated and targeted measures known as advanced persistent threats, directed at the Company, its products and its customers. We experience cybersecurity threats and incidents from time to time; however, to date, none have been material. We seek to deploy comprehensive measures to deter, prevent, detect, react to and mitigate these threats, including identity and access controls, data protection, vulnerability assessments, continuous monitoring of our IT networks and systems and maintenance of backup and protective systems.

10

Despite these efforts, cybersecurity incidents, depending on their nature and scope, could potentially result in the misappropriation, destruction, corruption or unavailability of critical data and confidential or proprietary information (our own or that of third parties) and the disruption of business operations. The potential consequences of a material cybersecurity incident include financial loss, reputational damage, litigation with third parties, theft of intellectual property, diminution in the value of our investment in research, development and engineering, and increased cybersecurity protection and remediation costs due to the increasing sophistication and proliferation of threats, which in turn could adversely affect our competitiveness and results of operations.

We may be unable to conduct business if we experience a significant business interruption in our computer systems, manufacturing plants or distribution facilities for a significant period of time.

We rely on our computer systems, manufacturing plants and distribution facilities to efficiently operate our business. If we experience an interruption in the functionality in any of these items for a significant period of time for any reason, we may not have adequate business continuity planning contingencies in place to allow us to continue our normal business operations on a long-term basis. In addition, the increase in customer-facing technology raises the risk of a lapse in business operations. Therefore, significant long-term interruption in our business could cause a decline in sales, an increase in expenses and could adversely impact our financial results.

Our ability to manage the health and safety of our global workforce may lead to increased business disruption and financial penalties.

We remain focused on the health and safety measures that impact our business from a manufacturing perspective. Our manufacturing teams monitor the effectiveness of our wellness and safety programs. The Company may be required to make enhancements and incur costs related to any new health guidelines and protocols to adapt to new health crises, which may adversely affect our business, financial conditions, or operating results.

We may consider acquisitions of suitable candidates to accomplish our growth objectives. We may not be able to successfully integrate the businesses we acquire to achieve operational efficiencies, including synergistic and other benefits of acquisition.

We may consider, as part of our growth strategy, supplementing our organic growth through acquisitions of complementary businesses or products. We have engaged in acquisitions in the past and we may determine that future acquisitions may provide meaningful opportunities to grow our business and improve profitability. Acquisitions allow us to enhance the breadth of our product offerings and expand the market and geographic participation of our products and services.

However, our success in growing by acquisition is dependent upon identifying businesses to acquire, integrating the newly acquired businesses with our existing businesses and complying with the terms of our credit facilities. We may incur difficulties in the realignment and integration of business activities when assimilating the operations and products of an acquired business or in realizing projected efficiencies, cost savings, revenue synergies and profit margins. Acquired businesses may not achieve the levels of revenue, profit, productivity or otherwise perform as expected. We are also subject to incurring unanticipated liabilities and contingencies associated with an acquired entity that are not identified or fully understood in the due diligence process. Current or future acquisitions may not be successful or accretive to earnings if the acquired businesses do not achieve expected financial results.

In addition, we may record significant goodwill or other intangible assets in connection with an acquisition. We are required to perform impairment tests at least annually and whenever events indicate that the carrying value may not be recoverable from future cash flows. If we determine that any intangible asset values need to be written down to their fair values, this could result in a charge that may be material to our operating results and financial condition.

Inadequate funding or insufficient innovation of new technologies may result in an inability to develop and commercialize new innovative products and services.

We strive to develop new and innovative products and services to differentiate ourselves in the marketplace. New product development relies heavily on our financial and resource investments in both the

11

short-term and long-term. If we fail to adequately fund product development projects or fund a project which ultimately does not gain the market acceptance we anticipated, we risk not meeting our customers' expectations, which could result in decreased revenues, declines in margin and loss of market share.

ITEM 1B – Unresolved Staff Comments

None.

ITEM 1C – Cybersecurity

Risk Management and Strategy

We recognize the critical importance of developing, implementing, and maintaining robust cybersecurity processes to safeguard our information systems and protect the confidentiality, integrity, and availability of our data. Our approach to assessing, prioritizing, and effecting cybersecurity processes and projects is based on standards from the National Institute of Standards and Technology (NIST).

We have established an enterprise risk management (ERM) program that considers our enterprise strategy, information from internal stakeholders, and information from external sources (e.g., emerging risks and trends, evaluations by third parties, and best practices) to identify, assess, categorize, and monitor risks including cybersecurity risks. The ERM program develops enterprise risk profiles to address individual risk drivers, develop action plans, and monitor against key risk indicators. At least annually, the ERM program is presented to our Board, Audit Committee, and members of management.

We have strategically integrated cybersecurity risk management into our broader ERM program to promote a company-wide culture of cybersecurity risk management. This integration ensures that cybersecurity considerations are an integral part of our decision-making processes. Our strategy includes regular employee training and awareness on cybersecurity risks and related best practices, required password complexity, the use of multi-factor authentication, information security protocols, anti-virus and anti-ransomware software, a patch management program, the execution of table top exercises on a periodic basis, established policies and protocols for cyber incident response planning and reporting, and ongoing internal cybersecurity testing. Our risk management team works closely with our IT department to continuously evaluate and address cybersecurity risks in alignment with our business objectives and operational needs.

We test our ability to respond to cybersecurity incidents on a recurring basis. Additionally, we engage third-party service providers to assist with the ongoing monitoring for cybersecurity events and incidents, as well as to complete risk quantification analysis and perform penetration and vulnerability testing. If any gaps are identified, the third-party service providers also assist with incident assessment and response. We conduct thorough up-front security assessments of all third-party providers before engagement, led by our Vice President, Chief Information Office (CIO) and our cybersecurity team, and we maintain ongoing monitoring to ensure compliance with our cybersecurity standards. This approach is designed to mitigate risks related to security incidents originating from third-parties.

We have not encountered cybersecurity incidents or identified risks from cybersecurity threats that have materially impaired our operations or financial standing.

Governance

Within our organization, we have a management team responsible for assessing and managing cybersecurity risks. The team is led by our CIO and consists of the Cyber Security Incident Response Team (CSIRT) and internal audit personnel. The CSIRT is comprised of IT management and experienced cybersecurity personnel. The role of the CSIRT is to promptly handle an incident so that containment, investigation, and recovery can occur quickly. Where third-party services are leveraged, they ensure they are engaged as necessary. The CSIRT Leader oversees and prioritizes actions during an incident's detection, analysis, and containment. They are also responsible for conveying the special requirements of high severity incidents to the rest of the organization as well as communicating potential impacts to the CIO. Additionally, they are responsible for understanding the SLAs in place with third parties, and the role third parties may play in specific response scenarios. Our CIO has more than 30 years of experience in IT, enterprise security, and cyber risk management and has previously held global IT infrastructure and business solutions roles, including nearly 20 years in such positions in the manufacturing industry. In addition, our CSIRT Leader has 30 years of

12

technology and cybersecurity experience and has previously held data security and global IT infrastructure positions at risk management and asset protection services companies. Effective February 2, 2024, our CIO has retired from employment and continues to serve as our CIO as a contractor through April 2024. During this time, he will continue his existing duties including oversight and management of cybersecurity risks. An active search is underway for a new CIO.

The CIO and CSIRT, in combination with the Senior Vice President, Technology and Innovation and CEO, play a pivotal role in informing the Audit Committee of the Board of Directors on cybersecurity risks. The Audit Committee is central to the Board's oversight of cybersecurity risks and bears the primary responsibility for this domain. The Audit Committee is composed of board members with diverse expertise including risk management, technology, and finance, equipping them to oversee cybersecurity risks effectively.

The Vice President, CIO provides comprehensive quarterly briefings to the Audit Committee. These briefings encompass a broad range of topics, including:

•Current cybersecurity landscape and emerging threats;

•Status of ongoing cybersecurity initiatives and strategies;

•Incident reports and learnings from any cybersecurity events; and

•Compliance with regulatory requirements and industry standards.

In addition to our quarterly meetings, the Audit Committee, CIO and CEO maintain an ongoing dialogue regarding emerging or potential cybersecurity risks. The CIO and CEO provide updates on any significant developments in the cybersecurity domain, ensuring the Board's oversight is proactive and responsive. The Audit Committee actively participates in strategic decisions related to cybersecurity, as well as tabletop exercises for tactical response readiness. This involvement ensures that cybersecurity considerations are integrated into the broader strategic objectives of Tennant Company. The Audit Committee conducts an annual review of the Company's cybersecurity posture and the effectiveness of its risk management strategies. This review helps in identifying areas for improvement and ensuring the alignment of cybersecurity efforts with the overall risk management framework.

ITEM 2 – Properties

The Company’s corporate offices are owned by the Company and are located in the Minneapolis, Minnesota metropolitan area. Manufacturing facilities located in Golden Valley, Minnesota; Holland, Michigan; Uden, The Netherlands; and the Italian cities of Venice, Cremona and Reggio Emilia and in the Province of Padua are owned by the Company. Manufacturing facilities located in Louisville, Kentucky; São Paulo, Brazil; Hefei, China; and another facility in the Province of Padua are leased to the Company. In addition, we use a dedicated, third-party plant in Germany that specially manufactures heavy–duty stainless steel scrubbers and sweepers to IPC designs. IPC also owns a minor tools and supplies assembly operation in China to service local customers. The facilities are in good operating condition, suitable for their respective uses and adequate for current needs.

Sales offices, warehouse and storage facilities are leased in various locations in the United States, Canada, Mexico, Brazil, Portugal, Spain, Italy, Germany, France, The Netherlands, Belgium, Norway, the United Kingdom, Japan, China, India, Australia, and New Zealand. The Company’s facilities are in good operating condition, suitable for their respective uses and adequate for current needs.

Further information regarding the Company’s property and lease commitments is included in Note 15 to the consolidated financial statements.

ITEM 3 – Legal Proceedings

There are no material pending legal proceedings other than ordinary litigation incidental to the Company’s business.

13

ITEM 4 – Mine Safety Disclosures

Not applicable.

14

PART II

ITEM 5 – Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

MARKET INFORMATION – Tennant's common stock is traded on the New York Stock Exchange, under the ticker symbol TNC. As of February 10, 2024, there were 254 shareholders of record.

DIVIDEND INFORMATION – Cash dividends on Tennant’s common stock have been paid for 79 consecutive years. Tennant’s annual cash dividend payout increased for the 52nd consecutive year to $1.075 per share in 2023, an increase of $0.06 per share over 2022. Dividends are generally declared each quarter. On February 13, 2024, the Company announced a quarterly cash dividend of $0.28 per share payable March 15, 2024, to shareholders of record on February 29, 2024.

DIVIDEND REINVESTMENT OR DIRECT DEPOSIT OPTIONS – Shareholders have the option of reinvesting quarterly dividends in additional shares of Company stock or having dividends deposited directly to a bank account. The Transfer Agent should be contacted for additional information.

TRANSFER AGENT AND REGISTRAR – Shareholders with a change of address or questions about their account may contact:

Equiniti Trust Company

Shareowner Services

P.O. Box 64874

St. Paul, MN 55164-0854

(800) 468-9716

SHARE REPURCHASES – Share repurchases are made from time to time in the open market or through privately negotiated transactions. During the twelve months ended December 31, 2023, the Company paid $21.7 million to repurchase 290,920 shares of its common stock. The most recent share repurchase program approved by the Board of Directors on October 31, 2016 authorized the repurchase of 1,000,000 shares of our common stock.

| For the Quarter Ended December 31, 2023 | Total Number of Shares Purchased(a) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | |||||||||||||||||||

| October 1–31, 2023 | 69,447 | $ | 75.19 | 69,447 | 877,788 | ||||||||||||||||||

| November 1–30, 2023 | 53,979 | $ | 84.66 | 53,332 | 824,456 | ||||||||||||||||||

| December 1–31, 2023 | 3,043 | $ | 86.06 | 3,043 | 821,413 | ||||||||||||||||||

| Total | 126,469 | $ | 79.50 | 125,822 | 821,413 | ||||||||||||||||||

(a)Includes 647 shares delivered or attested to in satisfaction of the exercise price and/or tax withholding obligations by employees who exercised stock options or restricted stock under employee share-based compensation plans.

15

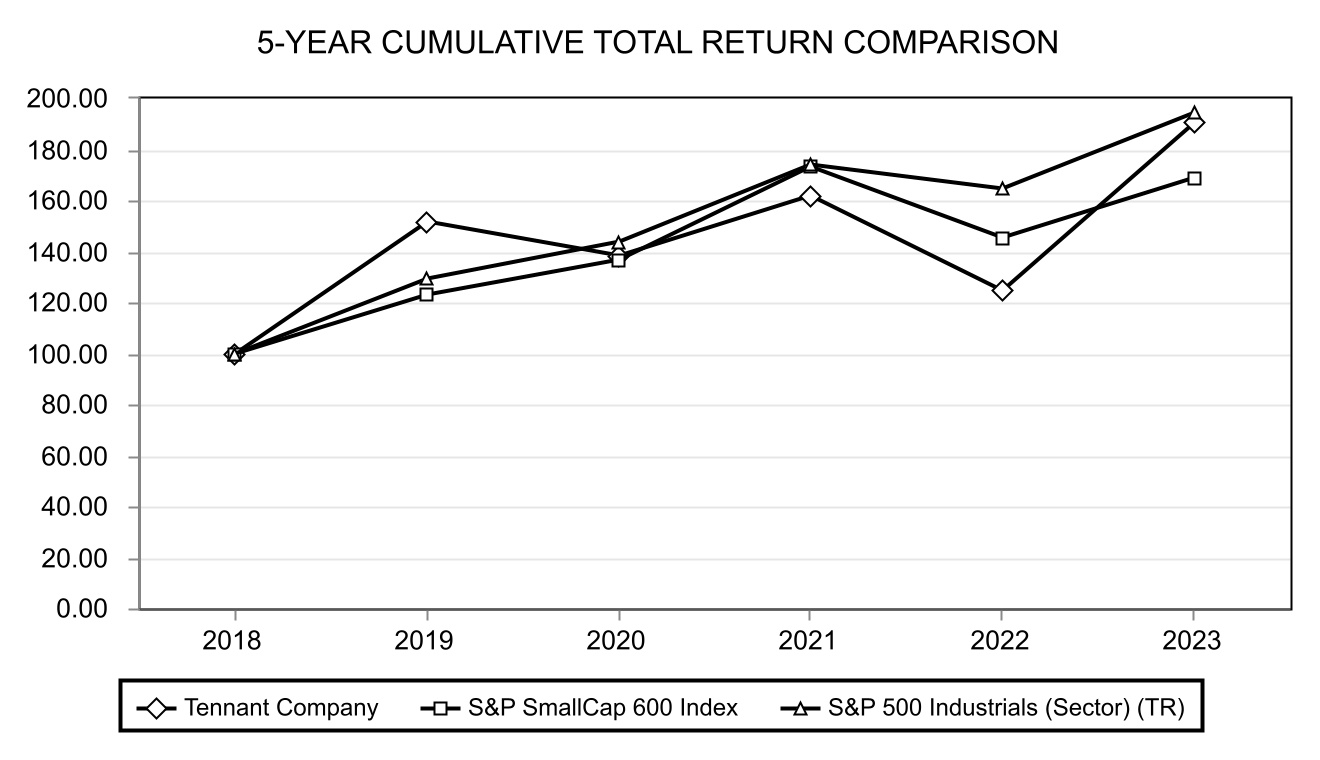

STOCK PERFORMANCE GRAPH – The following graph compares the cumulative total shareholder return on Tennant’s common stock to two indices: S&P SmallCap 600 and S&P 500 Industrials (Sector). The graph below compares the performance for the last five fiscal years, assuming an investment of $100 on December 31, 2018, including the reinvestment of all dividends.

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | ||||||||||||||||||||||||||||||

| Tennant Company | $ | 100 | $ | 152 | $ | 138 | $ | 162 | $ | 125 | $ | 190 | |||||||||||||||||||||||

| S&P SmallCap 600 | $ | 100 | $ | 123 | $ | 137 | $ | 173 | $ | 145 | $ | 169 | |||||||||||||||||||||||

| S&P 500 Industrials (Sector) (TR) | $ | 100 | $ | 129 | $ | 144 | $ | 174 | $ | 164 | $ | 194 | |||||||||||||||||||||||

Source: Zacks Investment Research, Inc.

ITEM 6 – [Reserved]

16

ITEM 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following Management's Discussion and Analysis of Financial Condition and Results of Operations (MD&A) provides a comparison of the Company's results of operations, as well as liquidity and capital resources for the years ended December 31, 2023 and 2022. The MD&A should be read in conjunction with the Company's consolidated financial statements and notes included in Item 8 of this Annual Report. Throughout this MD&A, the Company refers to measures used by management to evaluate performance, including financial measures that are not defined under generally accepted accounting principles (GAAP) in the U.S. Net sales excluding foreign currency translation (i.e., organic sales) is not a measure of financial performance under GAAP; however, the Company believes it is useful in understanding its financial results and provides comparable measures for understanding the operating results of the Company between different periods.

The year-over-year comparisons in this MD&A are as of and for the years ended December 31, 2023 and December 31, 2022, unless stated otherwise. The discussion of 2021 results and related year-over-year comparisons as of and for the years ended December 31, 2022 and December 31, 2021 are found in Part II, Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations," of our Form 10-K for the year ended December 31, 2022.

Overview

Tennant Company is a world leader in designing, manufacturing and marketing solutions that help create a cleaner, safer, healthier world. The Company is committed to creating and commercializing breakthrough, sustainable cleaning innovations to enhance its broad suite of products, including floor maintenance and cleaning equipment, detergent-free and other sustainable cleaning technologies, aftermarket parts and consumables, equipment maintenance and repair service, and asset management solutions. Our products are used in many types of environments, including factories and warehouses, distribution centers, office buildings, public venues such as arenas and stadiums, schools and universities, hospitals and clinics, and more. Customers include contract cleaners to whom organizations outsource facilities maintenance as well as businesses that perform facilities maintenance themselves. The Company reaches these customers through the industry's largest direct sales and service organization and through a strong and well-supported network of authorized distributors worldwide.

Macroeconomic Events

Supply chain challenges continue to impact the global economy. Our operating performance throughout 2023 has benefited from fewer supply chain disruptions enabling us to obtain key component parts, increase production and reduce backlog. We continue to address and adapt to these temporary supply chain disruptions by employing local-for-local and region-for-region manufacturing and sourcing strategies, which allows us to contain costs and manufacture our products closer to our customers. At the same time, our engineering teams are evaluating our platform design to increase our sourcing flexibility.

We are impacted by customer spend and global demand for our products. We have been able to successfully manage volatility in demand through our broad and expanding product offerings.

The global nature of our operations subjects us to exposures resulting from both foreign currency exchange fluctuations in the normal course of business and geopolitical risks stemming from global conflicts. While we do not have any direct operations or employees in areas experiencing conflict, our operating results have been and may continue to be negatively impacted by supply chain constraints and inflationary pressures stemming from these conflicts.

As described in Part I, Item 1A - Risk Factors, we may encounter financial difficulties if the United States or other global economies experience an additional or continued long-term economic downturn as our product sales are sensitive to declines in capital spending by our customers. Any sustained adverse impacts to our business, the industries in which we operate, market demand for our products, and/or certain suppliers or customers may also affect our future results of operations, financial position, or cash flows. We are actively monitoring the macroeconomic environment, especially the potential impact of global supply chain constraints on cost inflation, and the potential decreased demand for our products.

17

Outlook

While global economic conditions continue to be uncertain, including the ability to attract and retain skilled labor, lingering and targeted supply chain disruptions, and evolving compliance regulations, we remain agile as we continue to manage evolving conditions. We are confident in the long-term growth trends for all our products and services in the markets we serve.

Historical Results

The following table compares the historical results of operations for the years ended December 31, 2023, and 2022 in dollars and as a percentage of net sales (in millions, except per share amounts and percentages):

| 2023 | % | 2022 | % | ||||||||||||||||||||

| Net sales | $ | 1,243.6 | 100.0 | $ | 1,092.2 | 100.0 | |||||||||||||||||

| Cost of sales | 715.8 | 57.6 | 671.3 | 61.5 | |||||||||||||||||||

| Gross profit | 527.8 | 42.4 | 420.9 | 38.5 | |||||||||||||||||||

| Selling and administrative expense | 352.6 | 28.4 | 306.3 | 28.0 | |||||||||||||||||||

| Research and development expense | 36.6 | 2.9 | 31.1 | 2.8 | |||||||||||||||||||

| Gain on sale of assets | — | — | (3.7) | (0.3) | |||||||||||||||||||

| Operating income | 138.6 | 11.1 | 87.2 | 8.0 | |||||||||||||||||||

| Interest expense, net | (13.5) | (1.1) | (7.1) | (0.7) | |||||||||||||||||||

| Net foreign currency transaction gain (loss) | 0.3 | — | (1.2) | (0.1) | |||||||||||||||||||

| Other (expense) income, net | (1.6) | (0.1) | 0.6 | 0.1 | |||||||||||||||||||

| Income before income taxes | 123.8 | 10.0 | 79.5 | 7.3 | |||||||||||||||||||

| Income tax expense | 14.3 | 1.1 | 13.2 | 1.2 | |||||||||||||||||||

| Net income | 109.5 | 8.8 | 66.3 | 6.1 | |||||||||||||||||||

| Net income per share - diluted | $ | 5.83 | $ | 3.55 | |||||||||||||||||||

Net Sales

Consolidated net sales in 2023 totaled $1,243.6 million, a 13.9% increase as compared to consolidated net sales of $1,092.2 million in 2022.

The 13.9% increase in consolidated net sales was driven by:

•Organic sales increase of approximately 13.6% primarily due to the impact of higher selling prices across all regions and volume increases; and

•A net favorable impact from foreign currency exchange across all business units of approximately 0.3%.

Our strong organic sales increase was mainly supported by our ability to reduce backlog through the procurement of key component parts to facilitate increased production output.

The following table sets forth annual net sales by geographic area and the related percentage change from the prior year (in millions, except percentages):

| 2023 | % | 2022 | % | ||||||||||||||||||||

| Americas | $ | 840.3 | 19.0 | $ | 705.9 | 7.2 | |||||||||||||||||

| Europe, Middle East and Africa (EMEA) | 314.4 | 4.2 | 301.6 | (9.1) | |||||||||||||||||||

| Asia Pacific (APAC) | 88.9 | 5.0 | 84.7 | (15.8) | |||||||||||||||||||

| Total | $ | 1,243.6 | 13.9 | $ | 1,092.2 | 0.1 | |||||||||||||||||

18

Americas

Net sales in the Americas were $840.3 million in 2023, an increase of 19.0% from 2022. Organic sales grew 18.9%, driven equally by price realization and increased volume across all geographies. Foreign currency exchange within the Americas favorably impacted net sales by approximately 0.1%.

Europe, Middle East and Africa ("EMEA")

EMEA net sales were $314.4 million in 2023, an increase of 4.2% from 2022. Organic sales grew 2.6% in EMEA, driven by price realization in all product categories, partially offset by lower EMEA volumes that were impacted by weaker-than-expected market conditions. Foreign currency exchange within EMEA favorably impacted net sales by approximately 1.6%.

Asia Pacific ("APAC")

APAC net sales were $88.9 million in 2023, an increase of 5.0% from 2022. Organic sales grew 8.6% in APAC, driven by price realization in Australia and volume increases in Australia and China. Foreign currency exchange within APAC unfavorably impacted net sales by approximately 3.6% in 2023.

Backlog

Backlog is one of the many indicators of business conditions in the Company's markets. Our order backlog was approximately $186.2 million at December 31, 2023 compared to $326.4 million at December 31, 2022. The decrease in our order backlog is the result of the Company's ability to obtain key component parts and increase production levels. Backlog includes orders that can be cancelled or postponed at the option of the customer at any time without penalty.

Gross Profit

Gross profit margin of 42.4% was 390 basis points higher in 2023 compared to 2022. The margin rate increase was the result of price realization and cost saving initiatives, which more than offset the multi-year impact of inflation.

Operating Expenses

Selling and Administrative Expense

Selling and Administrative expense ("S&A expense") was $352.6 million in 2023, an increase of $46.3 million compared to 2022. As a percentage of net sales, S&A expense in 2023 increased 40 basis points to 28.4% from 28.0% in 2022. The S&A expense increase was driven by higher variable costs linked to improved operating performance as well as strategic investments aimed at fostering future growth.

Research and Development Expense

Research and Development ("R&D") expense was $36.6 million, or 2.9% of net sales, in 2023, nearly flat as a percentage of net sales compared to 2022.

We conduct research and development activities to develop new products and to enhance the functionality, effectiveness, ease of use and reliability of our existing products. We believe that our research and development efforts have been, and continue to be, key drivers of our success in the marketplace.

Total Other Expense, Net

Interest Expense, Net

Interest expense, net was $13.5 million in 2023, an increase of $6.4 million compared to 2022. The increase was the result of rising interest rates on our variable interest rate debt, partially offset by lower debt levels.

Our debt portfolio as of December 31, 2023 was comprised of debt predominately in U.S. dollars. The Company manages its floating rate debt exposure using fixed rate interest rate swaps to reduce the Company's risk of the possibility of increased interest costs.

19

Foreign Currency Transaction Gain/Loss

Net foreign currency transaction gain was $0.3 million in 2023, compared to a $1.2 million loss in 2022. The favorable impact was primarily due to weakening of the Chinese Renminbi relative to the U.S. dollar on foreign U.S. dollar denominated receivables during 2023, compared to strengthening of the U.S. dollar relative to the Brazilian real on foreign denominated liabilities in 2022.

Income Taxes

The effective tax rate for 2023 was 11.6% compared to 16.6% in 2022. The decrease in the effective tax rate was primarily driven by certain nonrecurring tax items. Both the 2023 and 2022 tax rates include benefits related to a reduction to a deferred tax liability on undistributed foreign earnings as those cumulative earnings were reduced by current year statutory book losses. These nonrecurring events had one-time impacts of (12.0%) in 2023 and (7.2%) in 2022.

In December 2021, the Organization for Economic Cooperation and Development (OECD), which is an international public policy setting organization comprised of member countries including the U.S., published a proposal for the establishment of a global minimum tax rate of 15% (the "Pillar Two rule"). The OECD has recommended that the Pillar Two rule become effective for fiscal years beginning on or after January 1, 2024. To date, member states are in various stages of implementing the rules through local legislation, and the OECD continues to refine the technical guidance. We are closely monitoring developments of the Pillar Two rule and are currently evaluating the potential effect in each of the countries we operate in.

In general, it is our practice and intention to permanently reinvest the earnings of our foreign subsidiaries and repatriate earnings only when the tax impact is zero or immaterial. No deferred taxes have been provided for withholding taxes or other taxes that would result in repatriation of our foreign investments to the U.S.

Liquidity and Capital Resources

Liquidity

Our primary liquidity needs are to fund working capital, fund investments, service our debt, maintain cash reserves and invest in capital expenditures. Our sources of liquidity include cash generated from operations, borrowings under our revolving credit facility and from time to time, debt and equity offerings. We believe our current resources are sufficient to meet our working capital requirements for our current business for at least the next 12 months and thereafter for the foreseeable future.

Cash, cash equivalents and restricted cash totaled $117.1 million at December 31, 2023, as compared to $77.4 million as of December 31, 2022. Wherever possible, cash management is centralized and intercompany financing is used to provide working capital to subsidiaries as needed. Our current ratio was 2.1 as of December 31, 2023 and 2.2 as of December 31, 2022. Our primary working capital, which is comprised of accounts receivable, inventories and accounts payable was $312.1 million as of December 31, 2023 and $332.0 million as of December 31, 2022. Our debt-to-capital ratio was 25.8% as of December 31, 2023, compared to 40.9% as of December 31, 2022.

On February 13, 2024, the Company's Board of Directors authorized a quarterly cash dividend of $0.28 per share payable on March 15, 2024, to shareholders of record at the close of business on February 29, 2024.

Cash Flow from Operating Activities

Net cash provided by operating activities in 2023 was $188.4 million compared to net cash provided by operating activities of $25.1 million in 2022. The increase in cash provided was the result of strong operating performance and managed reductions in working capital investments.

Cash Flow from Investing Activities

Net cash used in investing activities in 2023 was $23.2 million compared to net cash used in investing activities of $24.5 million in 2022. The decrease in cash outflows was primarily driven by reduced property, plant and equipment investments as the Company continues to deploy cash flow toward operational capital needs.

20

Cash Flow from Financing Activities

Net cash used in financing activities in 2023 was $122.6 million compared to net cash provided by financing activities of $8.1 million in 2022. The increase in cash used was primarily driven by repayments of borrowings and share repurchases.

Cash Requirements

The Company believes the liquidity available from the combination of expected cash generated by operating activities, existing cash and available credit under existing credit facilities will be sufficient to meet its short-term and long-term cash requirements. Significant contractual obligations include principal and interest payments on long-term debt (Note 9) and operating lease commitments (Note 15). We also have contractual purchase obligations of approximately $76 million for 2024.

Newly Issued Accounting Guidance

See Note 2 to the consolidated financial statements for information on new accounting pronouncements.

In October 2023, the FASB issued ASU 2023-06 Disclosure Improvements: Codification Amendments in Response to the SEC's Disclosure Update and Simplification Initiative, which aims to clarify or improve disclosure and presentation requirements on a variety of topics and align the requirements in the FASB accounting standard with the Securities and Exchange Commission regulations. This guidance is effective for the Company no later than June 30, 2027. We do not expect the amendments in this update to have a material impact on our consolidated financial statements.

In November 2023, the FASB issued ASU 2023-07 Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures, which requires an entity to disclose significant segment expenses impacting profit and loss that are regularly provided to the chief operating decision maker. The amendments in this ASU are required to be adopted for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted. We are currently evaluating the impact of adoption on our financial disclosures.

In December 2023, the FASB issued ASU 2023-09 Income Taxes (Topic 740): Improvements to Income Tax Disclosures, which is intended to enhance the transparency and decision usefulness of income tax disclosures. The amendments in ASU 2023-09 address investor requests for enhanced income tax information primarily through changes to the rate reconciliation and income taxes paid information. The amendments in this ASU are required to be adopted for fiscal years beginning after December 15, 2024. Early adoption is permitted for annual financial statements that have not yet been issued. The amendments should be applied on a prospective basis although retrospective application is permitted. We are currently evaluating the impact of adoption on our financial disclosures.

No other new accounting pronouncements issued but not yet effective have had, or are expected to have, a material impact on our results of operations or financial position.

Critical Accounting Policies and Estimates

Our consolidated financial statements are based on the selection and application of accounting principles generally accepted in the United States of America, which require us to make estimates and assumptions about future events that affect the amounts reported in our consolidated financial statements and the accompanying notes. Our significant accounting policies are described in Note 1 to the consolidated financial statements. Future events and their effects cannot be determined with absolute certainty. Therefore, the determination of estimates requires the exercise of judgment. Actual results could differ from those estimates, and any such differences may be material to the consolidated financial statements. We believe that the following policies may involve a higher degree of judgment and complexity in their application and represent the critical accounting policies used in the preparation of our consolidated financial statements. If different assumptions or conditions were to prevail, the results could be materially different from our reported results.

Goodwill – Goodwill represents the excess of cost over the fair value of net assets of businesses acquired and is allocated to our reporting units at the time of the acquisition. We analyze goodwill on an annual basis and when an event occurs or circumstances change that may reduce the fair value of a reporting unit below its

21

carrying amount. We have the option of first analyzing qualitative factors to determine whether it is more likely than not that the fair value of any reporting unit is less than its carrying amount. However, we may elect to perform a quantitative goodwill impairment test in lieu of the qualitative test. An entity must recognize an impairment charge for the amount by which the carrying amount exceeds the reporting unit’s fair value. Subsequent reversal of goodwill impairment charges is not permitted.

When we perform a qualitative goodwill test, we analyze qualitative factors to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount as a basis for determining whether it is necessary to perform the quantitative goodwill impairment test. If the qualitative test indicates there may be an impairment, we perform the quantitative test, which measures the amount of the goodwill impairment, if any. To perform the quantitative test, we calculate the fair value of each reporting unit, primarily utilizing the income approach. The income approach is based on discounted cash flow models that use reporting unit estimates for forecasted future financial performance, including revenues, margins, operating expenses, capital expenditures, depreciation, amortization, tax and discount rates. These estimates are developed as part of our planning process based on assumed growth rates, along with historical data and various internal estimates. Projected future cash flows are then discounted to a present value employing a discount rate that properly accounts for the estimated risk-adjusted weighted-average cost of capital relevant to each reporting unit.

We perform our annual goodwill impairment analysis as of October 1 and when an event occurs or circumstances change that may reduce the fair value of a reporting unit below its carrying amount.

In 2023, we elected to perform the qualitative test on all reporting units. Our test indicated that there is no goodwill impairment in any of our reporting units as of our annual assessment date.

We had goodwill of $187.4 million and $182.0 million at December 31, 2023 and 2022, respectively.

Income Taxes – We are required to estimate our income taxes in each of the jurisdictions in which we operate. This process involves estimating our actual current tax obligations based on expected income, statutory tax rates and tax planning opportunities in the various jurisdictions. We also establish reserves for uncertain tax matters that are complex in nature and uncertain as to the ultimate outcome. Although we believe that our tax return positions are fully supportable, we consider our ability to ultimately prevail in defending these matters when establishing these reserves. We adjust our reserves in light of changing facts and circumstances, such as the closing of a tax audit. We believe that our current reserves are adequate. However, the ultimate outcome may differ from our estimates and assumptions and could impact the income tax expense reflected in our consolidated statements of income.

Tax law requires certain items to be included in our tax return at different times than the items are reflected in our results of operations. Some of these differences are permanent, such as expenses that are not deductible in our tax returns, and some differences will reverse over time, such as depreciation expense on property, plant and equipment. These temporary differences result in deferred tax assets and liabilities, which are included within our consolidated balance sheets. Deferred tax assets generally represent items that can be used as a tax deduction or credit in our tax returns in future years but have already been recorded as an expense in our consolidated statements of income. We assess the likelihood that our deferred tax assets will be recovered from future taxable income, and, based on management’s judgment, to the extent we believe that recovery is not more likely than not, we establish a valuation allowance against those deferred tax assets. The deferred tax asset valuation allowance could be materially different from actual results because of changes in the mix of future taxable income, the relationship between book and taxable income and our tax planning strategies. As of December 31, 2023, a valuation allowance of $3.2 million was recorded against foreign and state tax credit carryforwards.

22

Cautionary Factors Relevant to Forward-Looking Information

This Annual Report on Form 10-K, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7, contains certain statements that are considered “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “project,” or “continue” or similar words or the negative thereof. These statements do not relate to strictly historical or current facts and provide current expectations of forecasts of future events. Any such expectations or forecasts of future events are subject to a variety of factors. Particular risks and uncertainties presently facing us include:

•Geopolitical and economic uncertainty throughout the world.

•Ability to comply with global laws and regulations.

•Ability to adapt to price sensitivity.

•Competition in our business.

•Fluctuations in the cost, quality or availability of raw materials and purchased components.

•Ability to adjust pricing to respond to cost pressures.

•Unforeseen product liability claims or product quality issues.

•Ability to attract, retain and develop key personnel and create effective succession planning strategies.

•Ability to effectively manage strategic plan or growth processes.

•Ability to successfully upgrade and evolve our information technology systems.

•Ability to successfully protect our information technology systems from cybersecurity risks.

•Occurrence of a significant business interruption.

•Ability to maintain the health and safety of our workforce.