,

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

Commission file number:

(Exact Name of Registrant as Specified in Its Charter)

|

||

(State or Other Jurisdiction of Incorporation or Organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

||

(Address of Principal Executive Offices) |

|

(Zip Code) |

Registrant’s Telephone Number, Including Area Code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class |

|

Trading Symbol(s) |

Name of Each Exchange on Which Registered |

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

☐ |

|

☒ |

|

Non-accelerated filer |

☐ |

|

Smaller reporting company |

|

|

|

|

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the registrant’s $0.01 par value common equity held by non-affiliates as of the last business day of the registrant’s most recently completed second quarter was $

DOCUMENTS INCORPORATED BY REFERENCE

Auditor Firm Id: |

Auditor Name: |

Auditor Location: |

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

PAGE |

|

PART I |

|

|

Item 1. |

1 |

|

Item 1A. |

3 |

|

Item 1B. |

16 |

|

Item 1C. |

16 |

|

Item 2. |

17 |

|

Item 3. |

17 |

|

Item 4. |

17 |

|

Item 4A. |

18 |

|

|

|

|

PART II |

|

|

Item 5. |

20 |

|

Item 6. |

20 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

21 |

Item 7A. |

30 |

|

Item 8. |

31 |

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. |

62 |

Item 9A. |

62 |

|

Item 9B. |

62 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions That Prevent Inspections |

62 |

|

|

|

PART III |

|

|

Item 10. |

63 |

|

Item 11. |

63 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. |

63 |

Item 13. |

Certain Relationships and Related Transactions, and Director Independence. |

63 |

Item 14. |

63 |

|

|

|

|

PART IV |

|

|

Item 15. |

64 |

|

Schedule II |

68 |

|

Item 16. |

69 |

|

|

|

|

|

70 |

|

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements made by us or on our behalf. We have included or incorporated by reference in this Annual Report on Form 10-K (including in the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (“MD&A”)) and from time to time our management may make statements that may constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based upon management’s current expectations, estimates, assumptions and beliefs concerning future events and conditions and may discuss, among other things, the impact of COVID-19, supply chain disruptions, increased energy costs and semiconductor chip shortages, rising interest rates, the Russian military invasion of Ukraine (the “Ukraine Conflict” ) and the United Auto Workers (“UAW”) strike, on our future growth and earnings. Any statement that is not historical in nature is a forward-looking statement and may be identified using words and phrases such as “expects,” “anticipates,” “believes,” “will,” “will likely result,” “will continue,” “plans to,” “could,” “continue,” “estimates” and similar expressions. These statements include our belief regarding general automotive industry and market conditions and growth rates, as well as general domestic and international economic conditions.

Readers are cautioned not to place undue reliance on forward-looking statements. Forward-looking statements are necessarily subject to risks, uncertainties and other factors, many of which are outside the control of the Company, which could cause actual results to differ materially from such statements and from the Company’s historical results and experience. These risks, uncertainties and other factors include, but are not limited to, those described in Part I, Item 1A, “Risk Factors” and Part II - Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report on Form 10-K and elsewhere in this Annual Report and those described from time to time in our other reports filed with the Securities and Exchange Commission.

Readers are cautioned that it is not possible to predict or identify all of the risks, uncertainties and other factors that may affect future results and that the risks described herein should not be considered to be a complete list. Any forward-looking statement speaks only as of the date on which such statement is made, and the Company undertakes no obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

ITEM 1 - BUSINESS

Description of Business and Industry

The principal business of Superior Industries International, Inc. (referred to herein as the “Company,” “Superior,” or “we” and “our”) is the design and manufacture of aluminum wheels for sale to original equipment manufacturers (“OEMs”) in North America and Europe and to the aftermarket in Europe. We employ approximately 6,600 full-time employees, operating in seven manufacturing facilities in North America and Europe. We are one of the largest aluminum wheel suppliers to global OEMs and one of the leading European aluminum wheel aftermarket manufacturers and suppliers. Our OEM aluminum wheels accounted for approximately 94 percent of our sales in 2023 and were primarily sold for factory installation on vehicle models manufactured by BMW (including Mini), Ford, GM, Honda, Jaguar-Land Rover, Lucid Motors, Mazda, Mercedes-Benz Group, Mitsubishi, Nissan, Peugeot, Renault, Stellantis, Subaru, Suzuki, Toyota, VW Group (Volkswagen, Audi, Skoda, Porsche) and Volvo. We sell aluminum wheels to the European aftermarket under the brands ATS, RIAL, ALUTEC and ANZIO. North America and Europe represent the principal markets for our products, but we have a diversified global customer base consisting of North American, European and Asian OEMs.

Demand for our products is mainly driven by light-vehicle production levels in North America and Europe and customer take rates on specific vehicle platforms that we serve and wheel SKUs that we produce. North American light-vehicle production in 2023 was 15.7 million vehicles, as compared to 14.3 million and 13.0 million vehicles in 2022 and 2021, respectively. In Western and Central Europe, light-vehicle production in 2023 was 15.3 million vehicles, as compared to 13.5 million and 12.8 million vehicles in 2022 and 2021, respectively. While industry production volumes in 2020 were adversely impacted by the COVID-19 pandemic, 2021 and 2022 volumes were constrained by the semiconductor chip and other supply chain shortages which started in the first two quarters of 2021, worsened in the last half of the year and continued throughout 2022, and, with respect to 2022, the Ukraine Conflict. Production volumes increased in 2023 due to easing of the semiconductor chip shortage despite the decline in the fourth quarter resulting from the UAW strike.

The majority of our customers’ wheel programs are awarded two to four years before actual production is scheduled to begin. Our purchase orders with OEMs are typically specific to a particular vehicle model. Each year, the automotive manufacturers introduce new models, update existing models and discontinue certain models. In this process, we may be selected as the supplier on a new model, we may continue as the supplier on an updated model or we may lose the supply contract for a new or updated model to a competitor.

Customer Dependence

We have proven our ability to be a consistent producer of high-quality aluminum wheels with the capability to meet our customers’ requirements regarding delivery, overall customer service, price, quality, and technology. We continually strive to enhance our relationships with our customers through continuous improvement programs, not only through our manufacturing operations but in the engineering, design, development and quality areas as well.

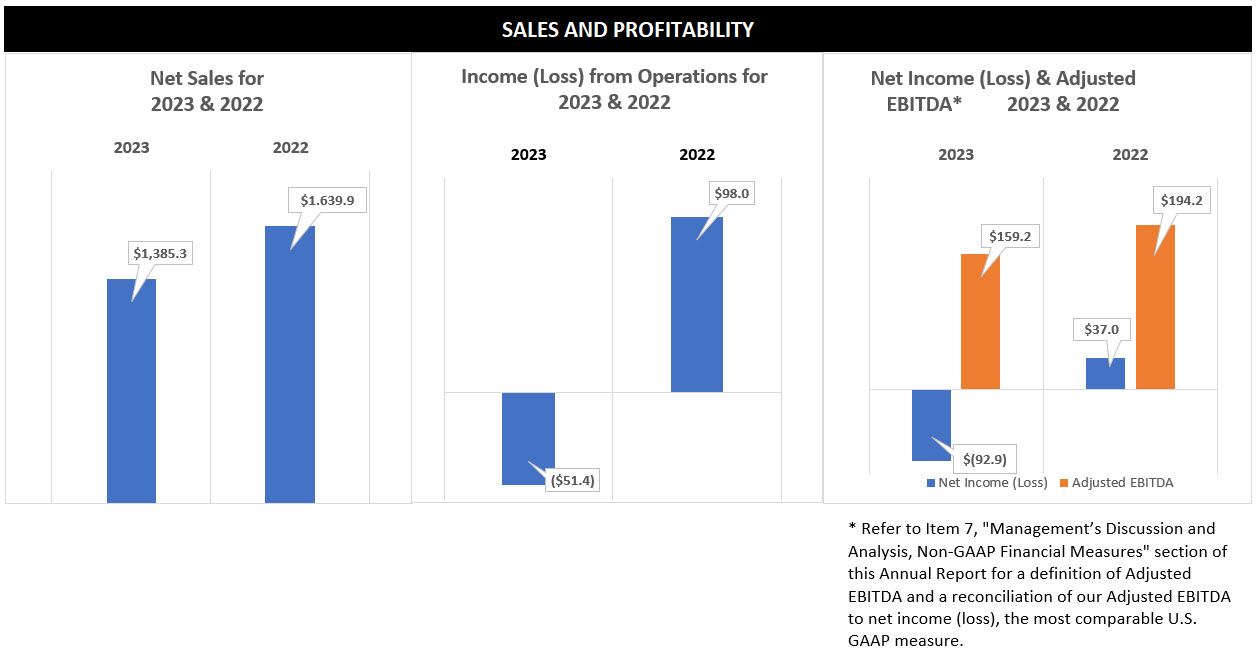

GM, Ford, VW Group and Toyota were our only customers individually accounting for 10 percent or more of our consolidated sales in 2023. In 2022 GM, Ford and VW Group each individually accounted for 10 percent or more of our consolidated sales and Toyota accounted for 9 percent of our consolidated sales. Our sales to these customers in 2023 and 2022 were as follows:

|

|

2023 |

|

|

2022 |

|

||||||

(Dollars in millions) |

|

Percent of |

|

Dollars |

|

|

Percent of |

|

Dollars |

|

||

GM |

|

21% |

|

$ |

288.6 |

|

|

26% |

|

$ |

431.3 |

|

Ford |

|

15% |

|

$ |

207.2 |

|

|

16% |

|

$ |

253.9 |

|

VW Group |

|

15% |

|

$ |

203.0 |

|

|

14% |

|

$ |

223.4 |

|

Toyota |

|

11% |

|

$ |

151.1 |

|

|

9% |

|

$ |

156.2 |

|

The loss of all or a substantial portion of our sales to these customers would have a significant adverse effect on our financial results. Refer to Item 1A, “Risk Factors,” of this Annual Report.

Raw Materials

Aluminum accounted for the vast majority of our total raw material requirements during 2023. Our aluminum requirements are met through purchase orders with major global producers. During 2023, we successfully secured aluminum commitments from our primary suppliers sufficient to meet our production requirements, and we anticipate being able to source aluminum requirements to meet our expected level of production in 2024.

1

We have contractual price adjustment clauses with our OEM customers to minimize the aluminum price risk, as well as the price risk associated with silicon and alloy premium. In the aftermarket business, we use derivatives to hedge price variability on our aluminum purchases.

When market conditions warrant, we may also enter into purchase commitments to secure the supply of certain other commodities used in the manufacture of our products, such as natural gas, electricity and other raw materials.

Foreign Operations

We manufacture all of our North American products in Mexico for sale in the United States, Canada and Mexico. The overall cost for us to manufacture wheels in Mexico is currently lower than in the United States, due to lower labor costs as a result of lower prevailing wage rates. In the past, we manufactured our products for the European market in Poland and Germany. Effective with the insolvency filing and deconsolidation of our operations in Germany on August 31, 2023, we now manufacture all of our products for Europe in Poland. Similar to our Mexican operations, the overall cost to manufacture wheels in Poland is lower than in both the United States and Germany at the present time due principally to lower labor costs.

We may enter into forward contracts, option contracts, swaps, collars or other derivative instruments to hedge the effect of foreign currency fluctuations on expected future cash flows and on certain existing assets and liabilities. In such cases, subsidiaries, whose functional currency is the U.S. dollar or the Euro, may hedge a portion of their forecasted foreign currency costs denominated in the Mexican Peso and Polish Zloty, respectively, in order to reduce the effect of fluctuating foreign currency exchange rates on our margins and cash flows.

Competition

Competition in the market for aluminum wheels is based primarily on delivery, overall customer service, price, quality and technology. Competition is global in nature with a significant volume of exports from Asia into North America and, to a lesser extent, Europe. Some of the key competitors in North America include Central Motor Wheel of America, CITIC Dicastal Co., Ltd., Prime Wheel Corporation, Enkei, Hands Corporation, and Ronal. Key European competitors include Ronal, Borbet, Maxion and CMS. We believe we are one of the leading manufacturers of alloy wheels in the European aftermarket, where the competition is highly fragmented. Key aftermarket competitors include Alcar, Brock, Borbet, ATU and Mak.

Research and Development

Our policy is to continuously review, improve and develop our engineering capabilities to satisfy our customer requirements in the most efficient and cost-effective manner available. We strive to achieve this objective by attracting and retaining top engineering talent and by maintaining the latest state-of-the-art computer technology to support engineering development. Our engineering centers located in Fayetteville, Arkansas and Lüdensheid, Germany, support our research and development in North America and Europe for our global OEM customers. Research and development of our European aftermarket wheels is performed in Bad Dürkheim, Germany.

Government Regulation

Safety standards in the manufacture of vehicles and automotive equipment have been established under the National Traffic and Motor Vehicle Safety Act of 1966, as amended. We believe that we are in compliance with all federal standards currently applicable to OEM suppliers and to automotive manufacturers.

Environmental Compliance

Our manufacturing facilities, like most other manufacturing companies, are subject to solid waste, water and air pollution control standards mandated by federal, state and local laws. Violators of these laws are subject to fines and, in extreme cases, plant closure. We believe our facilities are in material compliance with all presently applicable standards. The cost of environmental compliance was approximately $3.0 million in 2023 and $2.9 million in 2022. We expect that future environmental compliance expenditures will approximate these levels and will not have a material effect on our consolidated financial position or results of operations. However, climate change legislation or regulations restricting emission of “greenhouse gases” could result in increased operating costs and reduced demand for the vehicles that use our products. Refer to Item 1A, “Risk Factors—We are subject to various environmental laws” of this Annual Report.

Sustainability

We published our 2023 Sustainability Report in December 2023. That report reflected the results of the materiality assessment we conducted in 2021 to identify the sustainability interests of our stakeholders and develop our sustainability strategy. Based on that input, we remain committed to reducing natural gas, electricity and water consumption and solid waste and air emissions at our facilities. All Superior manufacturing facilities have implemented Environmental Management Systems that are ISO14001 certified and are subject to annual audits by an independent third party.

2

The 2023 Sustainability Report confirmed our goal to be carbon neutral by 2039 and reported the carbon footprint of our global operations. We reduced our carbon footprint by approximately 12% and our emissions per pound of aluminum shipped by 21% versus 2020 levels. We continue to explore opportunities to:

Furthermore, our research and development team continues to develop light weighting solutions, such as our patented Alulite™ technology, and aerodynamic solutions that will assist in reducing our customers’ carbon footprint. We also collaborate with our customers and suppliers regarding sustainability practices throughout their supply chains.

Employees

As of December 31, 2023, we employed approximately 6,600 full-time employees, with 4,000 employees in North America and 2,600 employees in Europe.

Segment Information

We have aligned our executive management structure, organization and operations to focus on our performance in our North American and European regions. Financial information about our reporting segments is contained in Note 5, “Business Segments” in the Notes to Consolidated Financial Statements in Item 8, “Financial Statements and Supplementary Data” of this Annual Report.

History

We were initially incorporated in Delaware in 1969. Our entry into the OEM aluminum wheel business in 1973 resulted from our successful development of manufacturing technology, quality control and quality assurance techniques that enabled us to satisfy the quality and volume requirements of the OEM market for aluminum wheels. The first aluminum wheel for a domestic OEM customer was a Mustang wheel for Ford. On May 30, 2017, we acquired a majority interest in UNIWHEELS AG, which was a European supplier of OEM and aftermarket aluminum wheels. UNIWHEELS AG was renamed in 2018 to Superior Industries Europe AG. Our stock is traded on the New York Stock Exchange (“NYSE”) under the symbol “SUP.”

Available Information

Our Annual Report on Form 10-K, quarterly reports on Form 10-Q and any amendments thereto are available, without charge, on or through our website, www.supind.com, under “Investor Relations,” as soon as reasonably practicable after they are filed electronically with the Securities and Exchange Commission (the “SEC”). Also included on our website, www.supind.com, under “Investor Relations,” is our Code of Conduct, which, among others, applies to our Chief Executive Officer, Chief Financial Officer and Principal Accounting Officer. Copies of all SEC filings and our Code of Conduct are also available, without charge, upon request from Superior Industries International, Inc., Investor Relations, 26600 Telegraph Road, Suite 400, Southfield, Michigan 48033.

The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements and other information related to issuers that file electronically with the SEC. The content on any website referred to in this Annual Report on Form 10-K is not incorporated by reference in this Annual Report on Form 10-K.

ITEM 1A. Risk Factors

The following discussion of risk factors contains “forward-looking” statements, which may be important to understanding any statement in this Annual Report or elsewhere. The following information should be read in conjunction with Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (the “MD&A”) and Item 8, “Financial Statements and Supplementary Data” of this Annual Report.

Our business routinely encounters and addresses risks and uncertainties. Our business, results of operations, financial condition and cash flows could be materially adversely affected by the factors described below. Discussion about the important risks that our business encounters can also be found in the MD&A and in the business description in Item 1, “Business” of this Annual Report. Below, we have described our present view of the most significant risks and uncertainties we face. Additional risks and uncertainties not presently known to us, or that we currently do not consider significant, could also potentially impair our business, results of operations, financial condition and cash flows. Our reactions to these risks and uncertainties as well as our competitors’ and customers’ reactions will affect our future operating results.

3

Industry and Economic Risks

The automotive industry is cyclical and volatility in the automotive industry could adversely affect our financial performance.

Predominantly, our sales are made to the European and U.S. automotive markets. Therefore, our financial performance depends largely on conditions in the European and U.S. automotive industry, which in turn can be affected significantly by broad economic and financial market conditions. Consumer demand for automobiles is subject to considerable volatility as a result of consumer confidence in general economic conditions, levels of employment, prevailing wages, general levels of inflation, fuel prices and the availability and cost of consumer credit, as well as changing consumer preferences. Demand for aluminum wheels can be further affected by other factors, including pricing and performance comparisons to competitive products. Finally, the demand for our products is influenced by shifts of market share between vehicle manufacturers and the market penetration of the specific vehicle models being sold by our customers. Decreases in demand for automobiles in Europe and the United States could adversely affect the valuation of our productive assets, results of operations, financial condition and cash flows.

We operate in a highly competitive industry and efforts by our competitors to gain market share could adversely affect our financial performance.

The global automotive component supply industry is highly competitive. Competition is based on a number of factors, including delivery, overall customer service, price, quality, technology and available capacity to meet customer demands. Some of our competitors are companies, or divisions or subsidiaries of companies, which are larger and have greater financial and other resources than we do. We cannot ensure that our products will be able to compete successfully with the products of these competitors. In particular, our ability to maintain or increase manufacturing capacity typically requires significant investments in facilities, equipment and personnel. Additionally, as a result of evolving customer requirements, we may incur labor costs at premium rates, experience increased maintenance expenses or have to replace our machinery and equipment on an accelerated basis. Furthermore, the markets in which we compete have attracted new entrants, particularly from low-cost countries. As a result, our sales levels and margins continue to be adversely affected by pricing pressures reflective of significant competition from producers located in low-cost foreign markets, such as China and Morocco. Such competition with lower cost structures poses a significant threat to our ability to compete globally. These factors have led to our customers awarding business to foreign competitors in the past, and they may continue to do so in the future. In addition, any of our competitors may foresee the course of market developments more accurately, develop products that are superior to our products, have the ability to produce similar products at a lower cost or adapt more quickly to new technologies or evolving customer requirements. Consequently, our products may not be able to compete successfully with competitors’ products.

The COVID-19 pandemic, resulting economic downturn, consequent decline in automotive industry production volumes and attendant supply chain shortages have disrupted, and may continue to disrupt our business, which may have a material adverse impact on our business, results of operations, financial condition and cash flows.

The COVID-19 pandemic arose in early 2020 causing a widespread health crisis that resulted in a global economic downturn and significant reduction in automotive industry production volumes due to government mandated closure of production facilities, as well as significant volatility in the financial markets. In 2021 and 2022, automotive industry production volumes increased but remained lower than 2019 pre-pandemic production levels primarily due to supply chain disruptions, including semiconductor chip and other shortages, which arose in the first two quarters of 2021, worsened in the last half of the year and continued throughout 2022. In 2023, semiconductor chip shortages have eased and production volumes have further recovered. However, any resurgence of the pandemic, economic decline and volatility, market volatility or attendant supply chain disruptions could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Specific risks to our Company include the following:

To the extent these risks adversely affect our operations and global economic conditions more generally, it may also have the effect of heightening many of the other risks described herein.

4

Risks Relating to Our Business, Strategy and Operations

A limited number of customers represent a large percentage of our sales. The loss of a significant customer or decrease in demand could adversely affect our operating results.

GM, Ford, VW Group, Toyota, Volvo and BMW, together, represented 76 percent and 77 percent of our sales in 2023 and 2022, respectively. Global procurement practices, including demand for price reductions may make it more difficult for us to maintain long-term supply arrangements with our customers, and there are no guarantees that we will be able to negotiate supply arrangements with our customers on terms acceptable to us in the future. The contracts we have entered into with most of our customers provide that we will manufacture wheels for a particular vehicle model, rather than manufacture a specific quantity of products. Such contracts range from one year to the life of the model (usually three to five years), typically are nonexclusive and do not require the purchase by the customer of any minimum number of wheels from us. Therefore, a significant decrease in consumer demand for certain key models or group of related models sold by any of our major customers, or a decision by a manufacturer not to purchase from us, or to discontinue purchasing from us, for a particular model or group of models, could adversely affect our results of operations, financial condition and cash flows.

We may be unable to successfully launch new products and/or achieve technological advances which could adversely affect our ability to compete resulting in an adverse impact on our financial condition, operating results and cash flows.

In order to compete effectively in the global automotive component supply industry, we must be able to launch new products and adopt technologies to meet our customers’ demands in a timely manner. However, we cannot ensure that we will be able to install and certify the equipment needed for new product programs in time for the start of production, or that the transitioning of our manufacturing facilities and resources under new product programs will not impact production rates or other operational efficiency measures at our facilities. In addition, we cannot ensure that our customers will execute the launch of their new product programs on schedule. We are also subject to the risks generally associated with new product introductions and applications, including lack of market acceptance, delays in product development and failure of products to operate properly. The global automotive industry is experiencing a period of significant technological change. As a result, the success of our business requires us to develop and/or incorporate leading technologies. Such technologies may be subject to rapid obsolescence. Our inability to maintain access to these technologies (either through development or licensing) may adversely affect our ability to compete. If we are unable to differentiate our products, maintain a low-cost footprint or compete effectively with technology-focused new market entrants, we may lose market share or be forced to reduce prices, thereby lowering our margins. Any such occurrences could adversely affect our financial condition, operating results and cash flows.

Increases in the costs and restrictions on availability of raw materials could adversely affect our operating margins and cash flow.

Generally, we obtain our raw materials, supplies and energy requirements from various sources. Although we currently maintain alternative sources, our business is subject to the risk of price increases and periodic delays in delivery. Fluctuations in the prices of raw materials may be driven by the supply and demand for that commodity or governmental regulation, including trade laws and tariffs. If any of our suppliers seek bankruptcy relief or otherwise cannot continue their business as anticipated, the availability or price of raw materials could be adversely affected. Both domestic and international markets in which we operate experienced significant inflationary pressures in fiscal year 2022, which continued in 2023. In addition, the Federal Reserve in the United States and other central banks in various countries have raised, and may again raise, interest rates in response to concerns about inflation, which, coupled with reduced government spending and volatility in financial markets, may have the effect of further increasing economic uncertainty and heightening these risks. Interest rate increases or other government actions taken to reduce inflation could also result in recessionary pressures in many parts of the world. While there was some improvement in the latter part of 2022 and 2023, we expect inflationary pressure to continue to impact our raw material and other costs in 2024.

Although our OEM contracts provide for the pass through of fluctuating aluminum and certain other raw material costs, we may not be able to do so in the future. Moreover, we establish our aftermarket selling prices six months in advance of the spring and winter sales periods. The aluminum we use to manufacture wheels contains alloying materials. The cost of alloying materials is therefore a component of the overall cost of a wheel. The price of the alloys we purchase is based on certain published market indices; however, certain of our OEM customer agreements do not provide price adjustments for changes in market prices of alloying materials. Increases or decreases in the market prices of alloying materials could have an adverse effect on our operating margins and cash flows. Furthermore, certain of our customers are not obligated to accept energy or other supply cost increases that we may attempt to pass along to them. The inability to pass such cost increases on to our customers could adversely affect our operating margins and cash flows.

In 2021, aluminum prices increased by approximately 45 percent and, while we were able to protect the margins of our OEM business by passing these costs on to our customers, rising aluminum prices increased our investment in working capital and therefore reduced our operating cash flow. In addition, since we are not able to pass aluminum price increases on to our aftermarket customers, the margins of our aftermarket business were adversely affected in 2021 and 2022. While aluminum prices began to decline in the latter part of 2022 and 2023, they remained somewhat elevated in relation to historical levels during 2023. In addition, rising silicon, natural gas and electricity costs increased significantly beginning in 2021 and remained somewhat elevated in 2022 and 2023. If unabated, they could continue to adversely affect our margins in 2024.

5

Aluminum and alloy pricing, and the timing of our receipt of payment from customers for aluminum and certain other raw material price fluctuations, may have a material effect on our operating margins and cash flows.

The cost of aluminum is a significant component in the overall cost of our wheels and in our selling prices to customers. Our OEM customer prices are adjusted for fluctuations in aluminum based on changes in certain published market indices, but the timing of price adjustments is based on specific customer agreements and can vary from monthly to quarterly. As a result, the timing of aluminum and certain other raw material price adjustments with customers in sales rarely will match the timing of such changes in cost of sales and can result in fluctuations in our gross profit. This is especially true during periods of frequent and dramatic increases or decreases in the market price of aluminum.

Any protracted labor disruption, such as a strike by unionized employees of our customers, may have a material adverse effect on our business, results of operations, cash flows and financial condition.

A significant portion of our revenues are attributable to customers with unionized work forces. Any protracted labor disruption at those customers due to strikes would have a material adverse impact on the Company’s business, results of operations, cash flows and financial condition.

We experience continual pressure from our customers to reduce costs and, if we are unable to generate sufficient cost reductions, our revenues, operating margins and cash flows could be adversely affected.

The global vehicle market is highly competitive, resulting in continual cost-cutting initiatives by our customers. Customer concentration, supplier fragmentation and product commoditization have translated into continual pressure from OEMs to reduce the price of our products. It is possible that pricing pressures beyond our expectations could intensify as OEMs pursue restructuring or other cost-cutting initiatives. If we are unable to generate sufficient production cost savings in the future to offset such price reductions, our operating margins and cash flows could be adversely affected. In addition, changes in OEMs’ purchasing policies or payment practices could have an adverse effect on our business. Our OEM customers typically attempt to qualify more than one supplier for the vehicle programs we participate on and for programs we may bid on in the future. Accordingly, our OEM customers may be able to negotiate favorable pricing or may decrease wheel orders from us. Such actions may result in decreased sales volumes and unit price reductions for the Company, resulting in lower revenues, operating margins and cash flows.

We may be unable to successfully implement cost-saving measures or achieve expected benefits under our plans to improve operations which could negatively impact our financial position, results of operations and cash flow.

As part of our ongoing focus to provide high quality products at reasonable prices, we continually analyze our business to further improve our operations and identify cost-cutting measures. We may be unable to successfully identify or implement plans targeting these initiatives or fail to realize the benefits of the plans we have already implemented, as a result of operational difficulties, a weakening of the economy or other factors. Cost reductions may not fully offset decreases in the prices of our products due to the time required to develop and implement cost reduction initiatives. Additional factors such as inconsistent customer ordering patterns, increasing product complexity and heightened quality standards may increase our costs and may make it more difficult to reduce our costs. It is possible that the costs we incur to implement improvement strategies may negatively impact our financial position, results of operations and cash flow.

We may be unable to attract and retain key personnel, including our senior management team, which may adversely affect our ability to conduct our business.

Our success depends, in part, on our ability to attract, hire, train and retain qualified managerial, operational, engineering, sales and marketing personnel. We face significant competition for these types of employees in our industry. We may be unsuccessful in attracting and retaining the personnel we require to conduct our operations successfully. In addition, key personnel may leave us and compete against us. Our success also depends, to a significant extent, on the continued service of our senior management team. During the last several years we have experienced significant turnover in our senior management members, additional losses of members of our senior management team or other experienced senior employees could impair our ability to execute our business plans and strategic initiatives, cause us to lose customers and experience lower revenues, or lead to employee morale problems and/or the loss of other key employees.

Purchase of additional shares of Superior Industries Europe AG (formerly UNIWHEELS AG) may require a higher purchase price.

Superior executed a Domination and Profit Loss Transfer Agreement (the “DPLTA”) which became effective in January 2018. According to the terms of the DPLTA, we offered to purchase any outstanding shares of UNIWHEELS AG for cash consideration of €62.18 per share. The cash consideration paid to shareholders for shares tendered under the DPTLA may be subject to change based on appraisal proceedings that the minority shareholders of UNIWHEELS AG have initiated.

6

Legal, Compliance and Regulatory Risks

We are from time to time subject to litigation, which could adversely affect our results of operations, financial condition or cash flows.

The nature of our business exposes us to litigation in the ordinary course of our business. We are exposed to potential product liability and warranty risks that are inherent in the design, manufacture and sale of automotive products, the failure of which could result in property damage, personal injury or death. Accordingly, individual or class action suits alleging product liability or warranty claims could result. Although we currently maintain what we believe to be suitable and adequate product liability insurance in excess of our self-insured amounts, we cannot guarantee that we will be able to maintain such insurance on acceptable terms or that such insurance will provide adequate protection against future liabilities. In addition, if any of our products prove to be defective, we may be required to participate in a recall. A successful claim brought against us or a requirement to participate in any product recall, could have a material adverse effect on our results of operations, financial condition or cash flows.

Our business requires extensive product development activities to launch new products. Accordingly, there is a risk that wheels under development may not be ready by the start of production or may fail to meet the customer’s specifications. In any such case, warranty or compensation claims might be raised, or litigation might be commenced, against the Company.

Moreover, there are risks related to civil liability under our customer supply contracts (civil liability clauses in contracts with customers, contractual risks related to civil liability for causing delay in production launch, etc.). If we fail to ensure production launch as and when required by the customer, thus jeopardizing production processes at the customer’s facilities, this could lead to increased costs, giving rise to recourse claims against, or causing loss of orders by, the Company. This could also have an adverse effect on our results of operations, financial condition or cash flows.

Furthermore, sales of products to our OEM customers are subject to contracts that involve numerous terms and conditions and incorporate extensive documentation developed throughout the sales and contracting process, including quotes and product specifications. These terms and conditions can be complex and may be subject to differing interpretations, which could result in contractual disputes. Contractual disputes may be costly, time-consuming, may result in contract or relationship terminations, and could harm our reputation as well as also have an adverse effect on our results of operations, financial condition or cash flows.

International trade agreements and our international operations make us vulnerable to risks associated with doing business in foreign countries that can affect our business, financial condition, results of operations and cash flows.

We manufacture our products in Mexico and Poland and we sell our products internationally. Accordingly, unfavorable changes in foreign cost structures, trade protection laws, tariffs on aluminum or wheels, regulations and policies affecting trade and investments and social, political, labor or economic conditions in a specific country or region, among other factors, could have a negative effect on our business and results of operations. Legal and regulatory requirements differ among jurisdictions worldwide. Violations of these laws and regulations could result in fines, criminal sanctions, prohibitions on the conduct of our business and damage to our reputation. Although we have policies, controls and procedures designed to ensure compliance with these laws, our employees, contractors, or agents may violate our policies.

It remains unclear what the U.S. administration or foreign governments, including China, will or will not do with respect to tariffs or other international trade agreements and policies. In 2018, 25% tariffs (the “301 tariffs”) were imposed by the United States Trade Representative (the “USTR”) on various products imported from China, including aluminum wheels, based on Section 301 of the Trade Act of 1974. While the 301 tariffs are currently still in effect, there is a risk they could be removed or not extended. For example, on October 17, 2022, the USTR initiated the second phase of its four-year review of the 301 tariffs, which focuses on the merits of maintaining the tariffs versus taking alternative actions. Removal of these tariffs may increase competitive pressure from Chinese producers who have cost advantages. This may have an adverse effect on our business, financial condition, results of operations and cash flows.

Mexico has passed new labor laws that are intended to make it easier for Mexican workers to unionize and that enhance certain benefits. Our cost of manufacturing in Mexico increased $2.0 million in 2023 as a result of enhanced vacation benefits. Our cost of manufacturing in Mexico could be subject to further increases in the event of unionization or as a result of further legislation, which could have an adverse effect on our business, financial condition, results of operations and cash flows.

A trade war, other governmental action related to tariffs or international trade agreements, changes in United States social, political, regulatory and economic conditions or in laws and policies governing foreign trade, manufacturing, development and investment in the territories and countries where we currently manufacture and sell products, and any resulting negative sentiments towards the United States, these territories and countries as a result of such changes, likely would have an adverse effect on our business, financial condition, results of operations and cash flows.

The cost of manufacturing our products in Mexico and Poland may be affected by tariffs imposed by any of these countries or the United States, trade protection laws, policies and other regulations affecting trade and investments, social, political, labor, or general economic conditions. Other factors that can affect the business and financial results of our Mexican and Polish operations include, but are not limited to, changes in cost structures, currency effects of the Mexican Peso, Euro and Polish Zloty, availability and competency of personnel and developments in tax regulations.

7

We are subject to various environmental laws.

We incur costs to comply with applicable environmental, health and safety laws and regulations in the ordinary course of our business. We cannot ensure that we have been or will be at all times in complete compliance with such laws and regulations. Failure to comply with such laws and regulations could result in material fines or sanctions. Additionally, changes to such laws or regulations may have a significant impact on our cash flows, financial condition and results of operations.

We are subject to various foreign, federal, state and local environmental laws, ordinances and regulations, including those governing discharges into the air and water, the storage, handling and disposal of solid and hazardous wastes, the remediation of soil and groundwater contaminated by hazardous substances or wastes and the health and safety of our employees. The nature of our current and former operations and the history of industrial uses at some of our facilities expose us to the risk of liabilities or claims with respect to environmental and worker health and safety matters which could have a material adverse effect on our financial condition.

Further, changes in legislation or regulation imposing reporting obligations on, or limiting emissions of greenhouse gases from, or otherwise impacting or limiting our equipment, operations, or the vehicles that use our products could adversely affect demand for those vehicles or require us to incur costs to become compliant with such regulations.

Capital Structure Risks

We do not expect to generate sufficient cash to repay all of our indebtedness (including the Term Loan Facility and Notes) by their respective maturity dates and we may be forced to take other actions to satisfy these obligations, which may not be successful. In addition, we may be unable to repay the redeemable preferred stock upon redemption by the holder.

The Company’s capital structure is heavily leveraged as a result of debt incurred in connection with the 2017 acquisition of our European business, part of which was refinanced on December 15, 2022. At December 31, 2023, our capital structure consisted of:

The Company also has available unused commitments under its revolving credit facility (the “Revolving Credit Facility”) of $55.1 million at December 31, 2023. In the event unrestricted cash and cash equivalents fall below $37.5 million at any quarter end (or up to $50.0 million following any increases in the commitment under the Revolving Credit Facility), the available commitment under the Revolving Credit Facility would be reduced by the amount of any shortfall. At December 31, 2023, unrestricted cash and cash equivalents substantially exceeded the requirement.

The Revolving Credit Facility and the Term Loan Facility are scheduled to mature on December 15, 2027 and December 15, 2028, respectively. However, in the event the Company has not repaid, refinanced or otherwise extended the Notes beyond the maturity date of the Term Loan Facility by the date 91 days prior to June 15, 2025 or has not redeemed, refinanced or otherwise extended the unconditional redemption date of the redeemable preferred stock beyond the maturity date of the Term Loan Facility by the date 91 days prior to September 14, 2025, the Term Loan Facility and Revolving Credit Facility would mature 91 days prior to June 15, 2025 or September 14, 2025, respectively. In this event, we would be required to pay all amounts outstanding under the SSCF sooner than they otherwise would be due and we may not be able to raise sufficient funds to pay such amounts on a timely basis, on terms we find acceptable, or at all.

Our ability to make scheduled payments or to refinance our debt obligations depends on our financial and operating performance, which is subject to prevailing economic, industry and competitive conditions and to certain other factors beyond our control. At the present time, we do not expect to generate sufficient cash to repay all principal due under our indebtedness, in full by the respective maturity dates, which will likely require us to refinance a portion or all of our outstanding debt. Our ability to restructure or refinance our debt will depend on the condition of the capital and credit markets and our financial condition at such time. We might not be able to refinance the debt on satisfactory terms. Any refinancing of our debt could be at higher interest rates and associated transactions costs and may require us to comply with more onerous covenants, which could further restrict our business operations and limit our financial flexibility. In addition, any failure to make payments of interest and principal on our outstanding indebtedness on a timely basis would likely result in a reduction of our credit ratings, which could harm our ability to incur additional indebtedness or issue equity, or to refinance all or portions of these obligations.

8

In the absence of sufficient cash flows, refinancing or adequate funds available under credit facilities, we could face substantial liquidity constraints and might be required to reduce or delay capital expenditures, seek additional capital, sell material assets or operations to attempt to meet our debt service and other obligations. The credit agreements governing the SSCF and the indenture governing the Notes (the “Indenture”) restrict our ability to conduct asset sales and/or use the proceeds from asset sales. We may not be able to consummate these asset sales to raise capital or sell assets at prices and on terms that we believe are fair, and any proceeds that we do receive may not be adequate to meet any debt service obligations then due. If we cannot meet our debt service obligations, the holders of our debt may accelerate our debt and, to the extent such debt is secured, foreclose on our assets. In such an event, we may not have sufficient assets to repay all of our debt.

Under the Certificate of Designations for our redeemable preferred stock, the holders may redeem the preferred stock either as a result of the occurrence of an early redemption event (a change in control, recapitalization, merger, sale of substantially all of the Company’s assets, liquidation or delisting of the Company’s common stock from the NYSE) or on or after September 14, 2025. The redemption obligation of our redeemable preferred stock consists of a redemption price equal to the greater of two times the then-current Stated Value (defined in the Certificate of Designations as $150.0 million, plus any accrued and unpaid dividends or dividends paid-in-kind), currently $300.0 million, or the product of the number of common shares into which the redeemable preferred stock could be converted (5.3 million shares currently) and the then-current market price of our common stock. Any redemption payment would be limited to cash legally available to pay such redemption. The shares of preferred stock that have not been redeemed would continue to receive a dividend of 9 percent per annum on the then-current Stated Value, as defined in the Certificate of Designations, until such shares of preferred stock are redeemed. The Board would have to evaluate periodically the ability of the Company to make any remaining payments until the full redemption amount has been paid. A redemption payment, if required, for some or all of our outstanding shares of preferred stock would negatively impact our liquidity and could adversely affect our business, results of operations and financial condition.

Our substantial indebtedness and the corresponding interest expense could adversely affect our financial condition

We have a significant amount of indebtedness. As of December 31, 2023, our total debt was $637.5 million ($616.0 million net of unamortized debt discount and issuance costs of $21.5 million). Additionally, we had availability of $55.1 million under the Revolving Credit Facility at December 31, 2023. In the event unrestricted cash and cash equivalents fall below $37.5 million at any quarter end (or up to $50.0 million following any increases in the commitment under the Revolving Credit Facility), the available commitment under the Revolving Credit Facility would be reduced by the amount of any shortfall. At December 31, 2023, unrestricted cash and cash equivalents exceeded the liquidity requirement and, accordingly, the full commitment was available, less outstanding letters of credit.

A significant portion of our cash flow from operations will be used to pay our interest expense and will not be available for other business purposes. We cannot be certain that our business will generate sufficient cash flow or that we will be able to enter into future financings that will provide sufficient proceeds to meet or pay the interest on our debt.

Subject to the limits contained in the credit agreements governing the SSCF and the Indenture and our other debt instruments, we may be able to incur substantial additional debt from time to time to finance working capital, capital expenditures, investments or acquisitions, or for other purposes. If we do so, the risks related to our high level of debt could intensify.

In addition, the Indenture and the credit agreements governing the SSCF and our other debt instruments contain restrictive covenants that among other things, could limit our ability to incur liens, engage in mergers and acquisitions, sell, transfer or otherwise dispose of assets, make investments or acquisitions, redeem our capital stock or pay dividends. In addition, the SSCF requires us to maintain appropriate insurance coverages, including insurance with respect to assets which secure the underlying debt obligations. Our failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of the maturity of all of our debt.

A downgrade of our credit rating or a decrease of the prices of the Company’s common stock or the Notes could adversely impact our financial performance.

The Company, its SSCF, and the Notes, are rated by Standard and Poor’s and Moody’s. These ratings are widely followed by investors, customers, and suppliers, and a downgrade by one or both of these rating agencies might cause: suppliers to cancel our contracts, demand price increases, or decrease payment terms; customers to reduce their business activities with us; or investors to reconsider investments in financial instruments issued by Superior, all of which might cause a decrease of the price of our common stock or our Notes.

9

A decrease in our common stock or Notes prices, in turn, might accelerate such negative trends. A reduction in the price of the Notes implies an increase of the yield debt investors demand to provide us with financing, which, in turn, would make it more difficult for us to refinance our existing debt, redeemable preferred stock obligations and/or future debt.

The terms of the credit agreements governing the SSCF, the Indenture, and other debt instruments, as well as the documents governing other debt that we may incur in the future, may restrict our current and future operations, particularly our ability to respond to changes or to take certain actions.

The Indenture, the credit agreements governing the SSCF and our other debt instruments, and the documents governing other debt that we may incur in the future, may contain a number of covenants that impose significant operating and financial restrictions on us and may limit our ability to engage in acts that may be in our long-term best interests, including restrictions on our ability to:

In addition, the restrictive covenants in the credit agreements governing the SSCF and other debt instruments require us to maintain specified financial ratios, including a quarterly secured net leverage ratio and a quarterly total net leverage ratio as well as a minimum liquidity. Our ability to meet those financial ratios and tests can be affected by events beyond our control. We may not meet those ratios and tests.

A breach of the covenants or restrictions under the Indenture, under the credit agreements governing the SSCF, or under other debt instruments could result in an event of default under the applicable indebtedness. Such a default may allow the creditors under such facility to accelerate the maturity of the related debt, which may result in the acceleration of the maturity date of any other debt to which a cross-acceleration or cross-default provision applies. In addition, an event of default under the credit agreements governing our SSCF would permit the lenders under our revolving credit facilities to terminate all commitments to extend further credit under these facilities. Furthermore, if we were unable to repay the amounts due and payable under the SSCF or under other secured debt instruments, those lenders could proceed against the collateral granted to them to secure that indebtedness. We have pledged substantially all of our assets as collateral under the SSCF. In the event our lenders or holders of the Notes accelerate the repayment of our borrowings, we may not have sufficient assets to repay that indebtedness or be able to borrow sufficient funds to refinance it. Even if we are able to obtain new financing, it may not be on commercially reasonable terms or on terms acceptable to us. As a result of these restrictions, we may be:

These restrictions, along with restrictions that may be contained in agreements evidencing or governing other future indebtedness, may affect our ability to grow or pursue other important initiatives in accordance with our growth strategy.

10

Our variable rate indebtedness subjects us to interest rate risk, which could cause our debt service obligations to increase significantly.

Borrowings under our SSCF are at variable rates of interest and expose us to interest rate risk. If interest rates increase, our debt service obligations on the variable rate indebtedness will increase even though the amount borrowed remains the same, and our net income and cash flows, including cash available for servicing our indebtedness, would correspondingly decrease. As of December 31, 2023, $396.0 million of our debt was variable rate debt. Our anticipated annual interest expense on $396.0 million of variable rate debt at the current rate of 13.4 percent would be $53.1 million. We have entered into interest rate swaps exchanging floating for fixed rate interest payments in order to reduce interest rate volatility. As of December 31, 2023, we had outstanding interest rate swaps with an aggregate notional amount of $200.0 million, with $50.0 million maturing December 31, 2024 and $150.0 million maturing December 31, 2025. In the future, we may again enter into interest rate swaps to reduce interest rate volatility. However, we may not maintain interest rate swaps with respect to all of our variable rate indebtedness, and any swaps we enter into may not fully mitigate our interest rate risk.

We may be adversely affected by changes in the secured overnight financing rate (“SOFR”) or Euro Interbank Offered Rate (“EURIBOR”) reporting practices, the method in which SOFR or EURIBOR is determined or the use of alternative reference rates.

The interest rates under our SSCF are calculated using SOFR (or, in certain cases, EURIBOR), or alternate base rates. The Federal Reserve Bank of New York (the “FRBNY”) began to publish SOFR in April 2018. SOFR was developed for use in certain U.S. dollar derivatives and other financial contracts as an alternative to the U.S. dollar London interbank offered rate (“U.S. dollar LIBOR”). Although the FRBNY has also begun publishing historical indicative SOFR going back to 2014, such historical indicative data inherently involves assumptions, estimates and approximations. Therefore, SOFR has limited performance history and no actual investment based on the performance of SOFR was possible before April 2018. The level of SOFR in future periods may bear little or no relation to the historical level of SOFR. In addition, the differences between SOFR and U.S. dollar LIBOR may mean that market participants would not consider SOFR a suitable substitute or successor for all of the purposes for which U.S. dollar LIBOR historically has been used (including, without limitation, as a representation of the unsecured short-term funding costs of banks), which may, in turn, lessen market acceptance of SOFR or lead to changes to the method in which SOFR is determined.

On September 21, 2017, the European Central Bank announced that it would be part of a new working group tasked with the identification and adoption of a “risk free overnight rate” to serve as a basis for an alternative to benchmarks used in a variety of financial instruments and contracts used in the euro area. On September 13, 2018, the working group on euro risk-free rates recommended the new euro short-term rate (“€STR”) as the new risk free rate for the euro area. €STR was published for the first time on October 2, 2019. In addition, in response to regulatory scrutiny and applicable legal requirements, the European Money Markets Institute (the “EMMI”), as administrator of EURIBOR, conducted a series of consultations on a proposed reformed hybrid methodology for EURIBOR. In July 2019, EMMI published its EURIBOR Benchmark Statement setting forth its reformed hybrid methodology and received regulatory authorization for the continued administration of EURIBOR.

In the future, SOFR and EURIBOR could be subject to further regulatory scrutiny, reform efforts and/or other actions. It is not possible to predict the effect of these changes, other reforms or the establishment of alternative reference rates in the United Kingdom, the United States or elsewhere. To the extent these interest rates increase, our interest expense will increase, which could adversely affect our financial condition, operating results and cash flows.

A delisting of our common stock from the NYSE could reduce the liquidity and market price of our common stock; reduce the number of investors and analysts that cover our common stock; limit our ability to issue additional shares and damage our reputation which could have a material adverse impact on our business, results of operations and financial condition. In addition, a delisting of our common stock from the NYSE could cause a redemption of some or all of our outstanding redeemable preferred stock which would negatively impact our liquidity.

We are required under the NYSE continued listing standards to maintain a market capitalization of at least $50 million, over a consecutive 30 trading-day period, or maintain stockholders’ equity of at least $50 million. If our market capitalization were to fall below $50 million over a consecutive 30-day trading period, we would be noncompliant with NYSE continued listing standards which could result in delisting. As of December 31, 2023, our market capitalization was $89.9 million.

A delisting of our common stock could have a material adverse impact on our business, results of operations and financial condition by, among other things: reducing the liquidity and market price of our common stock; reducing the number of investors, including institutional investors, willing to hold or acquire our common stock, which could negatively impact our ability to raise equity; decreasing the amount of news and analyst coverage relating to us; limiting our ability to issue additional securities, obtain additional financing or pursue strategic restructuring, refinancing or other transactions; and impacting our reputation and, as a consequence, our ability to attract new business.

11

In addition, the holder of our redeemable preferred stock has the right to redeem all of the outstanding shares of redeemable preferred stock if our common stock is delisted from the NYSE. If this were to occur, we would be required to: (1) increase the then carrying value of the redeemable preferred stock to the $300 million redemption value through a corresponding charge (decrease) to our retained earnings, and (2) make a redemption payment in any amount up to $300 million if our Board determined there was cash legally available to fund a full or partial redemption. A redemption payment, if required, for some or all of our outstanding shares of preferred stock would negatively impact our liquidity and could adversely affect our business, results of operations and financial condition.

Taxation Risks

We are subject to taxation related risks in multiple jurisdictions.

We are a U.S.-based multinational company subject to tax in multiple U.S. and foreign tax jurisdictions. Significant judgment is required in determining our global provision for income taxes, deferred tax assets or liabilities and in evaluating our tax positions on a worldwide basis. While we believe our tax positions are consistent with the tax laws in the jurisdictions in which we conduct our business, it is possible that these positions may be overturned by jurisdictional tax authorities, which may have a significant impact on our global provision for income taxes. Tax laws are dynamic and subject to change; new laws are passed and new interpretations of the law are issued or applied. Changes in tax laws or interpretations of tax laws may result in higher taxes, including making it more costly to move funds amongst different tax jurisdictions. We are subject to ongoing tax audits and may be subject to tax litigation. Audits and litigation can involve complex issues, which may require an extended period of time to resolve and can be highly subjective.

In addition, governmental tax authorities are increasingly scrutinizing the tax positions of companies. Many countries in the European Union, as well as a number of other countries and organizations such as the Organization for Economic Co-operation and Development, are actively changing existing tax laws, including a global minimum tax, that, if enacted, could increase our tax obligations in countries where we do business. The impact of tax law changes and tax law interpretation could adversely affect our results of operations, financial condition, cash flows and liquidity.

We may fail to comply with conditions of the state tax incentive programs in Poland.

The Company carries out its business activity in Poland in the area of Tarnobrzeg Special Economic Zone “Euro-Park Wislosan,” sub-zone of Stalowa Wola, Poland which provides various state income tax incentives under certain conditions. The Company conducts its business activity pursuant to permits that stipulate production, trade, and service activities relating to products and services manufactured/provided in the zone. These activities include processing of metals and applying coating on metals, tools, other finished metal products, machines for metallurgy, other parts and accessories for motor vehicles, excluding motorcycles, as well as services relating to recovery of segregated materials and recycled materials. The permits required that certain conditions be met, which include increasing the number of employees, keeping the number of employees at such level and incurring certain levels of capital expenditures. In addition, particular permits indicate deadlines for completion of respective stages of investments.

As of December 31, 2023, the Company has five permits that are effective until 2026. As of December 31, 2023, the Company utilized Polish Zloty 310.3 million of the zone-related credit and has fully utilized all credits available under the permits. The Company believes that we have satisfied all conditions required under the permits, however, if the Polish authorities determined that these conditions were not fully satisfied, the Company would have to repay tax incentives received together with interest which could have a material negative impact on our assets, financial condition, results of operations and cash flows.

Tax regulations in Poland are dynamic and subject to varying interpretations, both inside state authorities and between state authorities and enterprises, which can result in a lack of clarity and consistent application. As a result, tax risks in Poland are higher than in countries with a more developed tax system. Tax settlements and other areas of activity subject to specific regulations (e.g., customs or foreign exchange matters) may be inspected by administrative bodies which are entitled to impose penalties and sanctions. Tax settlements may be subject to inspections for five years from the end of the year in which the tax has been paid. Consequently, the Company may be subject to additional material tax liabilities, based on the result of these tax audits.

We are currently unable to fully deduct interest charges on German and U.S. indebtedness.

The interest deduction barriers under German tax law (Zinsschranke) and U.S. tax law limit the tax deductibility of interest expenses. If no exception to these limits applies, the annual net interest expense (interest expense less interest income) is deductible up to 30 percent of the EBITDA taxable in Germany and up to 30 percent of the EBIT taxable in the United States. Nondeductible interest expenses can be carried forward. Interest carry-forwards are subject to the same tax cancellation rules as tax loss carry-forwards. Whenever interest expenses are not deductible or if an interest carry-forward is lost, the tax burden in future assessment periods could rise, which might have alone, or in combination, a material adverse effect on our assets, financial condition, results of operation or cash flows.

12

We may be exposed to risks related to existing and future profit and loss transfer agreements executed with German subsidiaries of our European operations.

Profit and loss transfer agreements are one of the prerequisites of the taxation of Superior and its German subsidiaries as a German tax group. For tax purposes, a profit and loss transfer agreement must have a contract term for a minimum of five years. In addition, such agreement must be fully executed. If a profit and loss transfer agreement or its actual execution does not meet the prerequisites for taxation as a German tax group, Superior Industries International Germany GmbH (“SII Germany”), formerly known as Superior Industries International AG, and each subsidiary are taxed on their own income (and under certain circumstances even with retrospective effect). Additionally, 5 percent of dividends from a subsidiary to SII Germany, or other Superior European controlling entities within the European Union would be regarded as nondeductible expenses at the SII Germany level, or level of other Superior European controlling entities. Furthermore, the compensation of a loss of a subsidiary would be regarded as a contribution by SII Germany into the subsidiary and thus, would not directly reduce SII Germany’s profits. As a consequence, if the profit and loss transfer agreements do not meet the prerequisites of a German tax group, this could have a future material adverse effect on our assets, financial condition, results of operations or cash flows.

General Risk Factors

The Ukraine Conflict may have a material adverse effect on our business, financial condition, results of operations and cash flows.

On February 24, 2022, Russia launched a military invasion of Ukraine (the “Ukraine Conflict”). In response to the Russian invasion, various countries have developed comprehensive and coordinated sanctions and export restrictions on Russia, as well as on certain Russian products and certain Russian individuals. These countries and others could impose wider sanctions and take other actions in the future. In addition, the retaliatory measures that have been taken, and could be taken in the future, by NATO, the United States and other countries, have created global security concerns that could result in broader European military and political conflicts and otherwise have a substantial impact on regional and global economies, any or all of which could adversely affect our business, particularly our European operations.

The Ukraine Conflict has also given rise to macroeconomic risks which led, and may continue to lead, to significant declines in global and regional economic growth, particularly in Europe. These risks may not only reduce global demand and automotive production volumes but also have caused, and may continue to cause, further supply chain disruption and drive higher energy and commodity prices, including increases in aluminum, and silicon, as well as inflation and higher interest rates. Energy prices in Europe, particularly in Poland, increased significantly during 2022, partly due to the impact of the Ukraine Conflict and related sanctions and retaliatory measures, but have subsequently declined somewhat in 2023. Our OEM customers have, at times, temporarily shut down or lowered production as a result of the related supply disruption.

The impact of the Ukraine Conflict, including economic sanctions and export controls such as restrictions on energy exports, or additional military conflict, as well as potential responses to such actions by Russia, is currently unknown. It has led and may continue to lead to further increases of our costs, affect our supply chain and customers, and reduce our sales, earnings and cash flows. In addition, the continuation of the Ukraine Conflict could lead to other disruptions, instability and volatility in global markets that could adversely impact our operations. To the extent the Ukraine Conflict adversely affects our operations and global economic conditions more generally, it may also have the effect of heightening many of the other risks described herein.

We may not be able to renew our various insurance policies or renew them on terms and conditions acceptable to us.

We carry a variety of property, liability, and other insurance policies. These insurance policies might not cover all possible future risks we are exposed to, or we might not be able to successfully enforce an insurance claim. Additionally, although we carry insurance, coverage is limited to losses in excess of any applicable deductible. Coverage under such insurance is also limited to losses up to but not in excess of any applicable coverage limit. Furthermore, we may not be able to renew our various insurance policies or may have to renew them at terms and conditions adverse or unacceptable to us.

Fluctuations in foreign currencies and commodity and energy prices may adversely impact our financial results.

Due to our operations outside of the United States, we experience exposure to foreign currency gains and losses in the ordinary course of our business. We settle transactions between currencies (i.e., U.S. dollar to Mexican Peso, Euro to U.S. dollar, U.S. dollar to Euro and Euro to Polish Zloty). To the extent possible, we attempt to match the timing and magnitude of transaction settlements between currencies to create a “natural hedge.” Based on our current business model and levels of production and sales activity, the net imbalance between currencies depends on specific circumstances. While changes in the terms of the contracts with our customers will create an imbalance between currencies that we hedge with foreign currency forward or option contracts, there can be no assurances that our hedging program will effectively offset the impact of the imbalance between currencies or that the net transaction balance will not change significantly in the future.

13