SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS

PURSUANT TO SECTION 13 OR 15(d) THE SECURITIES EXCHANGE ACT OF 1934

(Mark One)

Ö ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ___________

Commission File Number 0-4776

STURM, RUGER & COMPANY, INC.

(Exact Name of Registrant as Specified in Its Charter)

|

Delaware (State or Other Jurisdiction of Incorporation or Organization) |

06-0633559 (I.R.S. Employer Identification No.) |

|

1 Lacey Place, Southport, Connecticut (Address of Principal Executive Offices) |

06890 (Zip Code) |

(203) 259-7843

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class Common Stock, $1 par value |

Name of Each Exchange on Which Registered New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES Ö NO

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES NO Ö

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES Ö NO

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K [ ].

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. Large accelerated filer [ Ö ] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [ ].

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).YES NO Ö

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

YES Ö NO

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of June 30, 2017:

Common Stock, $1 par value - $1,076,065,000

The number of shares outstanding of the registrant's common stock as of February 23, 2018:

Common Stock, $1 par value –17,427,090 shares

DOCUMENTS INCORPORATED BY REFERENCE.

Portions of the registrant’s Proxy Statement relating to the 2018 Annual Meeting of Stockholders to be held May 9, 2018 are incorporated by reference into Part III (Items 10 through 14) of this Report.

1

2

| PART IV | ||

| Item 15. | Exhibits and Financial Statement Schedule | 76 |

| Signatures | 79 | |

| Exhibit Index | 79 | |

| Financial Statement Schedule | 82 | |

| Exhibits | 83 | |

EXPLANATORY NOTE:

In this Annual Report on Form 10-K, Sturm, Ruger & Company, Inc. and Subsidiary (the “Company”) makes forward-looking statements and projections concerning future expectations. Such statements are based on current expectations and are subject to certain qualifying risks and uncertainties, such as market demand, sales levels of firearms, anticipated castings sales and earnings, the need for external financing for operations or capital expenditures, the results of pending litigation against the Company, the impact of future firearms control and environmental legislation, and accounting estimates, any one or more of which could cause actual results to differ materially from those projected. Words such as “expect,” “believe,” “anticipate,” “intend,” “estimate,” “will,” “should,” “could” and other words and terms of similar meaning, typically identify such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date made. The Company undertakes no obligation to publish revised forward-looking statements to reflect events or circumstances after the date such forward-looking statements are made or to reflect the occurrence of subsequent unanticipated events.

3

PART I

Company Overview

Sturm, Ruger & Company, Inc. and Subsidiary (the “Company”) is principally engaged in the design, manufacture, and sale of firearms to domestic customers. Virtually all of the Company’s sales for the year ended December 31, 2017 were from the firearms segment, with approximately 1% from the castings segment. Export sales represent approximately 4% of firearms sales. The Company’s design and manufacturing operations are located in the United States and almost all product content is domestic.

The Company has been in business since 1949 and was incorporated in its present form under the laws of Delaware in 1969. The Company primarily offers products in three industry product categories – rifles, pistols, and revolvers. The Company’s firearms are sold through independent wholesale distributors, principally to the commercial sporting market.

The Company manufactures and sells investment castings made from steel alloys and metal injection molding (“MIM”) parts for internal use in the firearms segment and has minimal sales to outside customers. The castings and MIM parts sold to outside customers, either directly or through manufacturers’ representatives, represented approximately 1% of the Company’s total sales for the year ended December 31, 2017.

For the years ended December 31, 2017, 2016, and 2015, net sales attributable to the Company's firearms operations were $517.7 million, $658.4 million and $544.9 million. The balance of the Company's net sales for the aforementioned periods was attributable to its castings operations.

Firearms Products

The Company presently manufactures firearm products, under the “Ruger” name and trademark, in the following industry categories:

| Rifles | Revolvers | ||||

| · | Single-shot | · | Single-action | ||

| · | Autoloading | · | Double-action | ||

| · | Bolt-action | ||||

| · | Modern sporting | ||||

| Pistols | |||||

| · | Rimfire autoloading | ||||

| · | Centerfire autoloading | ||||

Most firearms are available in several models based upon caliber, finish, barrel length, and other features.

4

Rifles

A rifle is a long gun with spiral grooves cut into the interior of the barrel to give the bullet a stabilizing spin after it leaves the barrel. Net sales of rifles by the Company accounted for $243.0 million, $264.9 million, and $208.5 million of total net sales for the years 2017, 2016, and 2015, respectively.

Pistols

A pistol is a handgun in which the ammunition chamber is an integral part of the barrel and which typically is fed ammunition from a magazine contained in the grip. Net sales of pistols by the Company accounted for $176.2 million, $250.0 million, and $192.2 million of revenues for the years 2017, 2016, and 2015, respectively.

Revolvers

A revolver is a handgun that has a cylinder that holds the ammunition in a series of chambers which are successively aligned with the barrel of the gun during each firing cycle. There are two general types of revolvers, single-action and double-action. To fire a single-action revolver, the hammer is pulled back to cock the gun and align the cylinder before the trigger is pulled. To fire a double-action revolver, a single trigger pull advances the cylinder and cocks and releases the hammer. Net sales of revolvers by the Company accounted for $74.6 million, $104.9 million, and $113.3 million of revenues for the years 2017, 2016, and 2015, respectively.

Accessories

The Company also manufactures and sells accessories and replacement parts for its firearms. These sales accounted for $23.9 million, $38.6 million, and $30.3 million of total net sales for the years 2017, 2016, and 2015, respectively.

Castings Products

Net sales attributable to the Company’s casting operations (excluding intercompany transactions) accounted for $4.6 million, $5.9 million, and $6.2 million, for 2017, 2016, and 2015, respectively. These sales represented approximately 1% of total net sales in each of these years.

Manufacturing

Firearms

The Company produces one model of pistol, all of its revolvers and most of its rifles at the Newport, New Hampshire facility. Most of the Company’s pistols are produced at the Prescott, Arizona facility. Some rifle models and two pistol models are produced at the Mayodan, North Carolina facility.

Many of the basic metal component parts of the firearms manufactured by the Company are produced by the Company's castings segment through processes known as precision investment casting. The Company also uses many MIM parts in its firearms. See "Manufacturing- Investment Castings and Metal Injected Moldings" below for a description of these processes. The Company believes that investment castings and MIM parts provide greater design flexibility and result in component parts which are generally close to their ultimate shape and, therefore, require less machining than processes requiring machining a solid billet of metal to obtain a part.

5

Through the use of investment castings and MIM parts, the Company endeavors to produce durable and less costly component parts for its firearms.

All assembly, inspection, and testing of firearms manufactured by the Company are performed at the Company's manufacturing facilities. Every firearm, including every chamber of every revolver manufactured by the Company, is test-fired prior to shipment.

Investment Castings and Metal Injection Moldings

To produce a product by the investment casting method, a wax model of the part is created and coated (“invested”) with several layers of ceramic material. The shell is then heated to melt the interior wax, which is poured off, leaving a hollow mold. To cast the desired part, molten metal is poured into the mold and allowed to cool and solidify. The mold is then broken off to reveal a near net shape cast metal part.

Metal injection molding is a three part powder metallurgy process by which a feedstock consisting of finely powdered metal and binders is processed through injection molding, debinding, and sintering equipment to produce steel, stainless steel, and alloy parts of complex shape and geometry. This process allows for high volume production while eliminating many of the wastes of traditional metal working methods, yielding net shape and near net shape parts.

Marketing and Distribution

Firearms

The Company's firearms are primarily marketed through a network of federally licensed, independent wholesale distributors who purchase the products directly from the Company. They resell to federally licensed, independent retail firearms dealers who in turn resell to legally authorized end users. All retail purchasers are subject to a point-of-sale background check by law enforcement. These end users include sportsmen, hunters, people interested in self-defense, law enforcement and other governmental organizations, and gun collectors. Each distributor carries the entire line of firearms manufactured by the Company for the commercial market. Currently, 19 distributors service the domestic commercial market, with an additional 23 distributors servicing the domestic law enforcement market and 41 distributors servicing the export market.

In 2017, the Company’s largest customers and the percent of total sales they represented were as follows: Davidson’s-21%; Lipsey’s-18%; Sports South-13%; and Jerry’s/Ellett Brothers-12%.

In 2016, the Company’s largest customers and the percent of total sales they represented were as follows: Davidson’s-19%; Lipsey’s-17%; Jerry’s/Ellett Brothers-15%; and Sports South-14%.

In 2015, the Company’s largest customers and the percent of total sales they represented were as follows: Davidson’s-18%; Lipsey’s-17%; Sports South-13%, and Jerry’s/Ellett Brothers-11%.

The Company employs 14 employees who service these distributors and call on retailers and law enforcement agencies. Because the ultimate demand for the Company's firearms comes from end users rather than from the independent wholesale distributors, the Company believes that the

6

loss of any distributor would not have a material, long-term adverse effect on the Company, but may have a material adverse effect on the Company’s financial results for a particular period. The Company considers its relationships with its distributors to be satisfactory.

The Company also exports its firearms through a network of selected commercial distributors and directly to certain foreign customers, consisting primarily of law enforcement agencies and foreign governments. Foreign sales were less than 5% of the Company's consolidated net sales for each of the past three fiscal years.

The Company does not consider its overall firearms business to be predictably seasonal; however, orders of many models of firearms from the distributors tend to be stronger in the first quarter of the year and weaker in the third quarter of the year. This is due in part to the timing of the distributor show season, which occurs during the first quarter.

Investment Castings and Metal Injection Moldings

The castings segment provides castings and MIM parts for the Company’s firearms segment. In addition, the castings segment produces some products for a number of customers in a variety of industries.

Competition

Firearms

Competition in the firearms industry is intense and comes from both foreign and domestic manufacturers. While some of these competitors concentrate on a single industry product category such as rifles or pistols, several competitors manufacture products in all four industry categories (rifles, shotguns, pistols, and revolvers). The principal methods of competition in the industry are product innovation, quality, availability, brand, and price. The Company believes that it can compete effectively with all of its present competitors.

Investment Castings and Metal Injection Moldings

There are a large number of investment castings and MIM manufacturers, both domestic and foreign, with which the Company competes. Competition varies based on the type of investment castings products and the end use of the product. Companies offering alternative methods of manufacturing such as wire electric discharge machining (EDM) and advancements in computer numeric controlled (CNC) machining also compete with the Company’s castings segment. Many of these competitors are larger corporations than the Company with substantially greater financial resources than the Company, which could affect the Company’s ability to compete with these competitors. The principal methods of competition in the industry are quality, price, and production lead time.

Employees

As of February 1, 2018, the Company employed approximately 1,750 full-time employees, approximately 27% of whom had at least ten years of service with the Company. From time to time, the Company uses temporary employees to supplement its workforce. As of February 1, 2018, the Company had no temporary employees.

7

None of the Company's employees are subject to a collective bargaining agreement.

Research and Development

In 2017, 2016, and 2015, the Company spent approximately $9.8 million, $8.7 million, and $8.5 million, respectively, on research and development activities relating to new products and the improvement of existing products. As of February 1, 2018, the Company had approximately 70 employees whose primary responsibilities were research and development activities.

Patents and Trademarks

The Company owns various United States and foreign patents and trademarks which have been secured over a period of years and which expire at various times. It is the policy of the Company to apply for patents and trademarks whenever new products or processes deemed commercially valuable are developed or marketed by the Company. However, none of these patents and trademarks are considered to be fundamental to any important product or manufacturing process of the Company and, although the Company deems its patents and trademarks to be of value, it does not consider its business materially dependent on patent or trademark protection.

Environmental Matters

The Company is committed to achieving high standards of environmental quality and product safety, and strives to provide a safe and healthy workplace for its employees and others in the communities in which it operates. The Company has programs in place that monitor compliance with various environmental regulations. However, in the normal course of its manufacturing operations the Company is subject to governmental proceedings and orders pertaining to waste disposal, air emissions, and water discharges into the environment. These regulations are integrated into the Company’s manufacturing, assembly, and testing processes. The Company believes that it is generally in compliance with applicable environmental regulations and that the outcome of any environmental proceedings and orders will not have a material adverse effect on the financial position of the Company, but could have a material adverse effect on the financial results for a particular period.

8

Executive Officers of the Company

Set forth below are the names, ages, and positions of the executive officers of the Company. Officers serve at the discretion of the Board of Directors of the Company.

| Name | Age | Position With Company |

| Christopher J. Killoy | 59 | President and Chief Executive Officer |

| Thomas A. Dineen | 49 | Senior Vice President, Treasurer and Chief Financial Officer |

| Thomas P. Sullivan | 57 | Senior Vice President of Operations |

| Kevin B. Reid, Sr. | 57 | Vice President, General Counsel and Corporate Secretary |

| Shawn C. Leska | 46 | Vice President, Sales |

Christopher J. Killoy became President & Chief Executive Officer on May 9, 2017. Previously he served as President and Chief Operating Officer since January 1, 2014. Prior to that he served as Vice President of Sales and Marketing since November 27, 2006. Mr. Killoy originally joined the Company in 2003 as Executive Director of Sales and Marketing, and subsequently served as Vice President of Sales and Marketing from November 1, 2004 to January 25, 2005.

Thomas A. Dineen became Senior Vice President on July 10, 2017. Previously he served as Vice President since May 24, 2006. Prior to that he served as Treasurer and Chief Financial Officer since May 6, 2003 and had been Assistant Controller since 2001. Mr. Dineen joined the Company as Manager, Corporate Accounting in 1997.

Thomas P. Sullivan became Senior Vice President of Operations on July 1, 2017. Mr. Sullivan joined the Company as Vice President of Newport Operations for the Newport, New Hampshire Firearms and Pine Tree Castings divisions on August 14, 2006.

Kevin B. Reid, Sr. became Vice President and General Counsel on April 23, 2008. Previously he served as the Company’s Director of Marketing from June 4, 2007. Mr. Reid joined the Company in July 2001 as an Assistant General Counsel.

Shawn C. Leska became Vice President, Sales on November 6, 2015. Mr. Leska joined the Company in 1989 and has served in a variety of positions in the sales department. Most recently, Mr. Leska served as Director of Sales since 2011.

Where You Can Find More Information

The Company is subject to the informational requirements of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), and accordingly, files its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Definitive Proxy Statements, Current Reports on Form 8-K,

9

and other information with the Securities and Exchange Commission (the "SEC"). The public may read and copy any materials filed with the SEC at the SEC's Public Reference Room at 100 F Street NE, Washington, DC 20549. Please call the SEC at (800) SEC-0330 for further information on the Public Reference Room. As an electronic filer, the Company's public filings are maintained on the SEC's Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that website is http://www.sec.gov.

The Company makes its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Definitive Proxy Statements, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act accessible free of charge through the Company's Internet site after the Company has electronically filed such material with, or furnished it to, the SEC. The address of that website is http://www.ruger.com. However, such reports may not be accessible through the Company's website as promptly as they are accessible on the SEC’s website.

Additionally, the Company’s corporate governance materials, including its Corporate Governance Guidelines, the charters of the Audit, Compensation, Nominating and Corporate Governance, and Risk Oversight committees, and the Code of Business Conduct and Ethics may also be found under the “Investor Relations” subsection of the “Corporate” section of the Company’s Internet site at http://www.ruger.com/corporate. A copy of the foregoing corporate governance materials is available upon written request to the Corporate Secretary at Sturm, Ruger & Company, Inc., 1 Lacey Place, Southport, Connecticut 06890.

The Company’s operations could be affected by various risks, many of which are beyond its control. Based on current information, the Company believes that the following identifies the most significant risk factors that could adversely affect its business. Past financial performance may not be a reliable indicator of future performance and historical trends should not be used to anticipate results or trends in future periods.

In evaluating the Company’s business, the following risk factors, as well as other information in this report, should be carefully considered.

Changes in government policies and firearms legislation could adversely affect the Company’s financial results.

The sale, purchase, ownership, and use of firearms are subject to thousands of federal, state and local governmental regulations. The basic federal laws are the National Firearms Act, the Federal Firearms Act, and the Gun Control Act of 1968. These laws generally prohibit the private ownership of fully automatic weapons and place certain restrictions on the interstate sale of firearms unless certain licenses are obtained. The Company does not manufacture fully automatic weapons and holds all necessary licenses under these federal laws. Several states currently have laws in effect similar to the aforementioned legislation.

10

In 2005, Congress enacted the Protection of Lawful Commerce in Arms Act (“PLCAA”). The PLCAA was enacted to address abuses by cities and agenda-driven individuals who wrongly sought to make firearms manufacturers liable for legally manufactured and lawfully sold products if those products were later used in criminal acts. The Company believes the PLCAA merely codifies common sense and long standing tort principles. If the PLCAA is repealed or efforts to circumvent it are successful and lawsuits similar to those filed by cities and agenda-driven individuals in the late 1990s and early 2000s are allowed to proceed, it could have a material adverse impact on the Company.

Currently, federal and several states’ legislatures are considering additional legislation relating to the regulation of firearms. These proposed bills are extremely varied, but many seek either to restrict or ban the sale and, in some cases, the ownership of various types of firearms. Other legislation seeks to require new technologies, such as microstamping and so-called “smart gun” technology, that are not proven, reliable or feasible. Such legislation became effective in California in 2013, and has limited our ability to sell certain products in California. If similar legislation is enacted in other states, it could effectively ban or severely limit the sale of affected firearms. There also are legislative proposals to limit magazine capacity.

The Company believes that the lawful private ownership of firearms is guaranteed by the Second Amendment to the United States Constitution and that the widespread private ownership of firearms in the United States will continue. However, there can be no assurance that the regulation of firearms will not become more restrictive in the future and that any such restriction would not have a material adverse effect on the business of the Company.

The Company’s results of operations could be further adversely affected if legislation with diverse requirements is enacted.

With literally thousands of laws being proposed at the federal, state and local levels, if even a small percentage of these laws are enacted and they are incongruent, the Company could find it difficult, expensive or even practically impossible to comply with them, impeding new product development and distribution of existing products.

The Company’s results of operations could be adversely affected by litigation.

The Company faces risks arising from various asserted and unasserted litigation matters. These matters include, but are not limited to, assertions of allegedly defective product design or manufacture, alleged failure to warn, purported class actions against firearms manufacturers, generally seeking relief such as medical expense reimbursement, property damages, and punitive damages arising from accidents involving firearms or the criminal misuse of firearms, and those lawsuits filed on behalf of municipalities alleging harm to the general public. Various factors or developments can lead to changes in current estimates of liabilities such as final adverse judgment, significant settlement or changes in applicable law. A future adverse outcome in any one or more of these matters could have a material adverse effect on the Company’s financial results. See Note 17 to the financial statements which are included in this Annual Report on Form 10-K.

11

Our insurance may be insufficient to protect us from claims or losses.

We maintain insurance coverage with third-party insurers. However, not every risk or liability is or can be protected by insurance, and, for those risks we insure, the limits of coverage we purchase or that are reasonably obtainable in the market may not be sufficient to cover all actual losses or liabilities incurred. Moreover, there is a risk that commercially available liability insurance will not continue to be available to us at a reasonable cost, if at all. If liability claims or losses exceed our current or available insurance coverage, our business and prospects may be harmed.

The Company’s results of operations could be adversely affected by a decrease in demand for Company products.

If demand for the Company’s products decreases significantly, the Company would be unable to efficiently utilize its capacity, and profitability would suffer. Decreased demand could result from a macroeconomic downturn, or could be specific to the firearms industry. If the decrease in demand occurs abruptly, the adverse impact would be even greater.

The financial health of our independent distributors is critical to our success.

Over 90% of our sales are made to 19 federally licensed, independent wholesale distributors. We review our distributors’ financial statements and have credit insurance for many of them. However, our credit evaluations of distributors and credit insurance may not be completely effective, especially if an interest rate increase exacts an additional financial strain.

If one or more independent distributors experience financial distress or liquidity issues, we may not be able to collect our accounts receivable on a timely basis, which would have an adverse impact on our operating results and financial condition.

The Company must comply with various laws and regulations pertaining to workplace safety and environment, environmental matters, and firearms manufacture.

In the normal course of its manufacturing operations, the Company is subject to numerous federal, state and local laws and governmental regulations, and governmental proceedings and orders. These laws and regulations pertain to matters like workplace safety and environment, firearms serial number tracking and control, waste disposal, air emissions and water discharges into the environment. Noncompliance with any one or more of these laws and regulations could have a material adverse impact on the Company.

Misconduct of our employees or contractors could cause us to lose customers and could have a significant adverse impact on our business and reputation.

Misconduct, fraud or other improper activities by our employees or contractors could have a material adverse impact on our business and reputation. Such misconduct could include the failure to comply with federal, state, local or foreign government procurement regulations, regulations regarding the protection of personal information, laws and regulations relating to antitrust and any other applicable laws or regulations.

12

Business disruptions at one of the Company’s manufacturing facilities could adversely affect the Company’s financial results.

The Newport, New Hampshire, Prescott, Arizona and Mayodan, North Carolina facilities are critical to the Company’s success. These facilities house the Company’s principal production, research, development, engineering, design, and shipping operations. Any event that causes a disruption of the operation of any of these facilities for even a relatively short period of time could have a material adverse effect on the Company’s ability to produce and ship products and to provide service to its customers.

We rely on our information and communications systems in our operations. Security breaches and other disruptions could adversely affect our business and results of operations.

Cyber-security threats are significant and evolving and include, among others, malicious software, attempts to gain unauthorized access to data, and other electronic security breaches that could lead to disruptions in mission critical systems, unauthorized release of confidential or otherwise protected information and corruption of data. In addition to security threats, we are also subject to other systems failures, including network, software or hardware failures, whether caused by us, third-party service providers, natural disasters, power shortages, terrorist attacks or other events. The unavailability of our information or communications systems, the failure of these systems to perform as anticipated or any significant breach of data security could cause loss of data, disrupt our operations, lead to financial losses from remedial actions, require significant management attention and resources, and negatively impact our reputation among our customers and the public, which could have a negative impact on our financial condition, results of operations and liquidity.

Price increases for raw materials could adversely affect the Company’s financial results.

Third parties supply the Company with various raw materials for its firearms and castings, such as fabricated steel components, walnut, birch, beech, maple and laminated lumber for rifle stocks, wax, ceramic material, metal alloys, various synthetic products and other component parts. There is a limited supply of these materials in the marketplace at any given time, which can cause the purchase prices to vary based upon numerous market factors. The Company believes that it has adequate quantities of raw materials in inventory or on order to provide ample time to locate and obtain additional items at then-current market cost without interruption of its manufacturing operations. However, if market conditions result in a significant prolonged inflation of certain prices or if adequate quantities of raw materials cannot be obtained, the Company’s manufacturing processes could be interrupted and the Company’s financial condition or results of operations could be materially adversely affected.

Retention of key management is critical to the success of the Company.

We rely on the management and leadership skills of our senior management team. Our senior executives are not bound by employment agreements. The loss of the services of one or more of our senior executives or other key personnel could have a significant adverse impact on our business.

ITEM 1B—UNRESOLVED STAFF COMMENTS

None

13

The Company’s manufacturing operations are carried out at four facilities. The following table sets forth certain information regarding each of these facilities:

|

Approximate Aggregate Square Feet |

Status |

Segment | |

| Newport, New Hampshire | 350,000 | Owned | Firearms/Castings |

| Prescott, Arizona | 230,000 | Leased | Firearms |

| Mayodan, North Carolina | 220,000 | Owned | Firearms |

| Earth City, Missouri | 35,000 | Leased | Castings |

Each firearms facility contains enclosed ranges for testing firearms. The lease of the Prescott facility provides for rental payments which are approximately equivalent to estimated rates for real property taxes.

The Company has other facilities that were not used in its manufacturing operations in 2017:

|

Approximate Aggregate Square Feet |

Status |

Segment | |

| Southport, Connecticut | 25,000 | Owned | Corporate |

|

Newport, New Hampshire (Dorr Woolen Building) |

45,000 |

Owned |

Firearms |

| Enfield, Connecticut | 10,000 | Leased | Firearms |

| Rochester, New Hampshire | 2,000 | Leased | Firearms |

| Fairport, New York | 3,700 | Leased | Corporate |

There are no mortgages or any other major encumbrance on any of the real estate owned by the Company.

The Company’s principal executive offices are located in Southport, Connecticut.

14

The nature of the legal proceedings against the Company is discussed at Note 17 to the financial statements, which are included in this Form 10-K.

The Company has reported all cases instituted against it through September 30, 2017, and the results of those cases, where terminated, to the SEC on its previous Form 10-Q and 10-K reports, to which reference is hereby made.

One lawsuit was formally instituted against the Company during the three months ending December 31, 2017, captioned as David S. Palmer, on behalf of himself and all others similarly situated vs. Sturm, Ruger & Co., and filed in the Circuit Court for the Thirteenth Judicial Circuit in and for Hillsborough County, Florida. The suit alleges breach of warranty and deceptive trade practices related to the sale of 10/22 Target Rifles.

During the three months ending December 31, 2017, the previously reported case of Terry W. Turner v. Sturm, Ruger & Company., Inc. and Winchester Ammunition, Inc. was dismissed, with prejudice.

ITEM 4—MINE SAFETY DISCLOSURES – NOT APPLICABLE

15

PART II

ITEM 5—MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The Company’s common stock is traded on the New York Stock Exchange under the symbol “RGR.” At February 9, 2018, the Company had 1,662 stockholders of record.

The following table sets forth, for the periods indicated, the high and low sales prices for the Company’s common stock as reported on the New York Stock Exchange and dividends paid on the Company’s common stock.

| High | Low | Dividends Per Share | ||||||||||

| 2016: | ||||||||||||

| First Quarter | $ | 78.09 | $ | 49.62 | $ | 0.35 | ||||||

| Second Quarter | 69.73 | 57.25 | 0.48 | |||||||||

| Third Quarter | 70.30 | 54.41 | 0.49 | |||||||||

| Fourth Quarter | 65.95 | 47.15 | 0.41 | |||||||||

| 2017: | ||||||||||||

| First Quarter | $ | 54.45 | $ | 47.75 | $ | 0.44 | ||||||

| Second Quarter | 68.60 | 53.00 | 0.48 | |||||||||

| Third Quarter | 63.90 | 44.80 | 0.23 | |||||||||

| Fourth Quarter | 57.20 | 45.70 | 0.21 | |||||||||

16

Issuer Repurchase of Equity Securities

In 2017, 2016, and 2015 the Company repurchased shares of its common stock. Details of these purchases are as follows:

| Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Program | Maximum Dollar Value of Shares that May Yet Be Purchased Under the Program | ||||||||||||

| First Quarter 2015 | 82,100 | $ | 34.57 | 82,100 | ||||||||||||

| Fourth Quarter 2016 | 283,343 | $ | 49.43 | 283,343 | ||||||||||||

| First Quarter 2017 | ||||||||||||||||

| January 29 to February 25 | 900,997 | $ | 49.70 | 900,997 | ||||||||||||

| February 26 to April 1 | 173,288 | $ | 49.92 | 173,288 | ||||||||||||

| Third Quarter 2017 | ||||||||||||||||

| Jully 30 to August 2 | 4,490 | $ | 47.92 | 4,490 | ||||||||||||

| August 27 to September 30 | 240,933 | $ | 46.30 | 240,933 | ||||||||||||

| Total | 1,685,151 | $ | 48.45 | 1,685,151 | $ | 30,710,000 | ||||||||||

All of these purchases were made with cash held by the Company and no debt was incurred.

At December 31, 2017 approximately $31 million remained authorized for share repurchases.

17

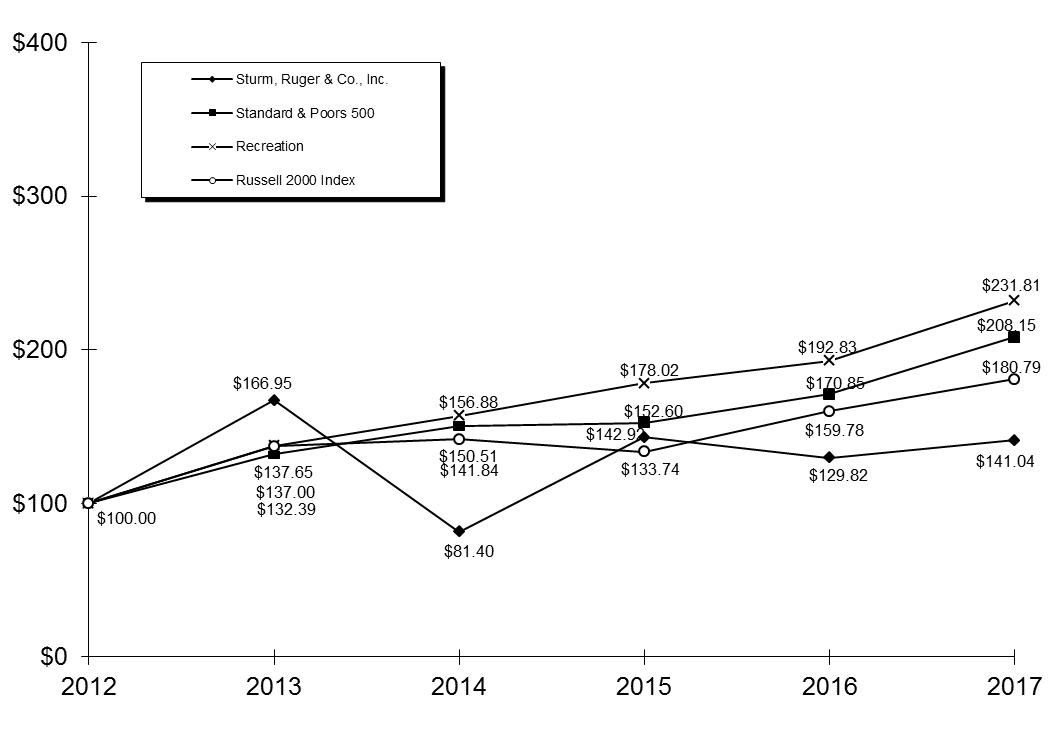

| Comparison of Five-Year Cumulative Total Return* | ||||

| Sturm, Ruger & Co., Inc., Standard & Poor’s 500, Recreation and Russell 2000 Index | ||||

| (Performance Results Through 12/31/17) | ||||

Assumes $100 invested at the close of trading 12/12 in Sturm, Ruger & Co., Inc. common stock, Standard & Poor’s 500, Recreation, and Russell 2000 Index.

* Cumulative total return assumes reinvestment of dividends.

Source: Value Line Publishing LLC

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |

| Sturm, Ruger & Co., Inc. | 100.00 | 166.95 | 81.40 | 142.92 | 129.82 | 141.04 |

| Standard & Poor’s 500 | 100.00 | 132.39 | 150.51 | 152.60 | 170.85 | 208.15 |

| Recreation | 100.00 | 137.65 | 156.88 | 178.02 | 192.83 | 231.81 |

| Russell 2000 Index | 100.00 | 137.00 | 141.84 | 133.74 | 159.78 | 180.79 |

18

Securities Authorized for Issuance Under Equity Compensation Plans

The following table provides information regarding compensation plans under which equity securities of the Company are authorized for issuance as of December 31, 2017:

| Equity Compensation Plan Information | |||

| Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights (a) |

Weighted-average exercise price of outstanding options, warrants and rights (b) * |

Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) (c) |

|

Equity compensation

|

|||

| — | |||

| 2007 Stock Incentive Plan | 228,994 | $8.95 per share | — |

| 2017 Stock Incentive Plan | 22,878 | — | 727,122 |

|

Equity compensation

|

|||

| None. | |||

| Total | 251,872 | $8.95 per share | 727,122 |

| * | Restricted stock units are settled in shares of common stock on a one-for-one basis. Accordingly, such units have been excluded for purposes of computing the weighted-average exercise price. |

19

ITEM 6—SELECTED FINANCIAL DATA

(Dollars in thousands, except per share data)

| December 31, | ||||||||||||||||||||

2017

| 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

| Net firearms sales | $ | 517,701 | $ | 658,433 | $ | 544,850 | $ | 542,267 | $ | 678,552 | ||||||||||

| Net castings sales | 4,555 | 5,895 | 6,244 | 2,207 | 9,724 | |||||||||||||||

| Total net sales | 522,256 | 664,328 | 551,094 | 544,474 | 688,276 | |||||||||||||||

| Cost of products sold | 368,248 | 444,774 | 378,934 | 375,300 | 429,671 | |||||||||||||||

| Gross profit | 154,008 | 219,554 | 172,160 | 169,174 | 258,605 | |||||||||||||||

| Income before income taxes | 77,646 | 135,921 | 96,100 | 57,240 | 175,232 | |||||||||||||||

| Income taxes | 25,504 | 48,449 | 33,974 | 18,612 | 63,960 | |||||||||||||||

| Net income | 52,142 | 87,472 | 62,126 | 38,628 | 111,272 | |||||||||||||||

| Basic earnings per share | 2.94 | 4.62 | 3.32 | 1.99 | 5.76 | |||||||||||||||

| Diluted earnings per share | 2.91 | 4.59 | 3.21 | 1.95 | 5.58 | |||||||||||||||

| Cash dividends per share | $ | 1.36 | $ | 1.73 | $ | 1.10 | $ | 1.62 | $ | 2.12 | ||||||||||

| December 31, | ||||||||||||||||||||

2017

| 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

| Working capital | $ | 114,107 | $ | 133,870 | $ | 107,279 | $ | 57,792 | $ | 69,460 | ||||||||||

| Total assets | 284,318 | 346,879 | 315,883 | 254,382 | 277,118 | |||||||||||||||

| Total stockholders’ equity | 230,149 | 265,900 | 227,738 | 185,462 | 179,086 | |||||||||||||||

| Book value per share | $ | 13.21 | $ | 14.23 | $ | 12.17 | $ | 9.90 | $ | 9.26 | ||||||||||

| Return on stockholders’ equity | 21.0% | 35.4% | 30.1% | 21.2% | 81.2% | |||||||||||||||

| Current ratio | 3.2 to 1 | 2.7 to 1 | 2.3 to 1 | 2.0 to 1 | 1.8 to 1 | |||||||||||||||

| Common shares outstanding | 17,427,100 | 18,688,500 | 18,713,400 | 18,737,000 | 19,348,000 | |||||||||||||||

| Number of stockholders of record | 1,664 | 1,678 | 1,702 | 1,726 | 1,718 | |||||||||||||||

| Number of employees | 1,838 | 2,120 | 1,920 | 1,847 | 1,862 | |||||||||||||||

| Number of temporary employees | 2 | 310 | 205 | 220 | 530 | |||||||||||||||

20

ITEM 7—MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Company Overview

Sturm, Ruger & Company, Inc. (the “Company”) is principally engaged in the design, manufacture, and sale of firearms to domestic customers. Approximately 99% of sales are from firearms. Export sales represent approximately 4% of total sales. The Company’s design and manufacturing operations are located in the United States and almost all product content is domestic. The Company’s firearms are sold through a select number of independent wholesale distributors, principally to the commercial sporting market.

The Company also manufactures investment castings made from steel alloys and metal injection molding (“MIM”) parts for internal use in its firearms and for sale to unaffiliated, third-party customers. Approximately 1% of sales are from the castings segment.

Orders of many models of firearms from the independent distributors tend to be stronger in the first quarter of the year and weaker in the third quarter of the year. This is due in part to the timing of the distributor show season, which occurs during the first quarter.

Results of Operations - 2017

Product Demand

The estimated sell-through of the Company’s products from the independent distributors to retailers decreased 17% in 2017 from 2016. For the same period, the National Instant Criminal Background Check System (“NICS”) background checks (as adjusted by the National Shooting Sports Foundation (“NSSF”)) decreased 11%. The decrease in estimated sell-through of the Company’s products from the independent distributors to retailers is attributable to:

| · | Decreased overall consumer demand in 2017 due to stronger-than-normal demand during most of 2016, likely bolstered by the political campaigns for the November 2016 elections, |

| · | Reduced purchasing by retailers in an effort to reduce their inventories and generate cash, |

| · | Aggressive price discounting and lucrative consumer rebates offered by many of our competitors, and |

| · | Excess industry manufacturing capacity, which exacerbated the above factors. |

New products represented $137.8 million or 27% of firearms sales in 2017, compared to $192.6 million or 29% of firearms sales in 2016. New product sales include only major new products that were introduced in the past two years. In 2017, new products included the Precision Rifle, the Mark IV pistols, the LCP II pistol, and the American pistol. In December 2017, the Company introduced the Pistol Caliber Carbine, the Security 9 pistol, and the EC9s pistol. Due to the timing of these launches, they had only a minimal impact on the 2017 financial results.

21

Estimated sell-through from distributors to retailers and total adjusted NICS background checks:

| 2017 | 2016 | 2015 | ||||||||||

| Estimated Units Sold from Distributors to Retailers (1) | 1,663,100 | 2,007,200 | 1,793,800 | |||||||||

| Total Adjusted NICS Background Checks (2) | 13,967,800 | 15,727,700 | 14,244,200 | |||||||||

| (1) | The estimates for each period were calculated by taking the beginning inventory at the distributors, plus shipments from the Company to distributors during the period, less the ending inventory at distributors. These estimates are only a proxy for actual market demand as they: |

| · | Rely on data provided by independent distributors that are not verified by the Company, |

| · | Do not consider potential timing issues within the distribution channel, including goods-in-transit, and |

| · | Do not consider fluctuations in inventory at retail. |

| (2) | NICS background checks are performed when the ownership of most firearms, either new or used, is transferred by a Federal Firearms Licensee. NICS background checks are also performed for permit applications, permit renewals, and other administrative reasons. |

The adjusted NICS data presented above was derived by the NSSF by subtracting NICS checks that are not directly related to the sale of a firearm, including checks used for concealed carry (“CCW”) permit application checks as well as checks on active CCW permit databases.

Orders Received and Ending Backlog

The Company uses the estimated unit sell-through of our products from the independent distributors to retailers, along with inventory levels at the independent distributors and at the Company, as the key metrics for planning production levels.

Orders Received in 2017 decreased 44% from 2016. Our ending order backlog of 254,900 units at December 31, 2017 decreased 366,500 units from backlog of 621,400 units at December 31, 2016.

22

The units ordered, value of orders received and ending backlog, net of Federal Excise Tax, for the trailing three years are as follows (dollars in millions, except average sales price):

| 2017 | 2016 | 2015 | ||||||||||

| Orders Received | $ | 386.2 | $ | 688.5 | $ | 463.2 | ||||||

| Average Sales Price of Orders Received | $ | 297 | $ | 306 | $ | 303 | ||||||

| Ending Backlog | $ | 75.4 | $ | 195.0 | $ | 137.8 | ||||||

| Average Sales Price of Ending Backlog | $ | 296 | $ | 314 | $ | 320 | ||||||

Production

The Company reviews the estimated sell-through from the independent distributors to retailers, as well as inventory levels at the independent distributors and at the Company, semi-monthly to plan production levels and manage increases in inventory. These reviews resulted in a decrease in total unit production of 24% in 2017 compared to 2016.

Annual Summary Unit Data

Firearms unit data for orders, production, and shipments follows:

| 2017 | 2016 | 2015 | ||||||||||

| Units Ordered | 1,298,800 | 2,246,600 | 1,517,000 | |||||||||

| Units Produced | 1,610,900 | 2,125,500 | 1,721,300 | |||||||||

| Units Shipped | 1,665,300 | 2,055,500 | 1,738,100 | |||||||||

| Average Sales Price | $ | 311 | $ | 320 | $ | 313 | ||||||

| Units – Backlog | 254,900 | 621,400 | 430,300 | |||||||||

Inventories

The Company’s finished goods inventory decreased by 54,500 units during 2017.

Distributor inventories of the Company’s products increased by 2,000 units during 2017 and approximate a reasonable level to support rapid fulfillment of retailer demand.

23

Inventory data follows:

| December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| Units – Company Inventory | 102,900 | 157,400 | 87,400 | |||||||||

| Units – Distributor Inventory (3) | 321,300 | 319,300 | 271,000 | |||||||||

| Total inventory (4) | 424,200 | 476,700 | 358,400 | |||||||||

| (3) | Distributor ending inventory as provided by the independent distributors of the Company’s products. These numbers do not include goods-in-transit inventory that has been shipped from the Company but not yet received by the distributors. |

| (4) | This total does not include inventory at retailers. The Company does not have access to data on retailer inventories. |

Year ended December 31, 2017, as compared to year ended December 31, 2016:

Net Sales

Consolidated net sales were $522.3 million in 2017. This represents a decrease of $142.0 million or 21.4% from 2016 consolidated net sales of $664.3 million.

Firearms segment net sales were $517.7 million in 2017. This represents a decrease of $140.7 million or 21.4% from 2016 firearms net sales of $658.4 million. Firearms unit shipments decreased 19.0% in 2017.

Casting segment net sales were $4.6 million in 2017. This represents a decrease of $1.3 million or 22.7% from 2016 casting sales of $5.9 million.

Cost of Products Sold and Gross Profit

Consolidated cost of products sold was $368.2 million in 2017. This represents a decrease of $76.6 million or 17.2% from 2016 consolidated cost of products sold of $444.8 million.

24

The gross margin was 29.5% in 2017. This represents a decrease from 33.0% in 2016 as illustrated below:

(in thousands)

| Year Ended December 31, | 2017 | 2016 | ||||||||||||||

| Net sales | $ | 522,256 | 100.0% | $ | 664,328 | 100.0% | ||||||||||

| Cost of products sold, before LIFO, overhead and labor rate adjustments to inventory, product liability; and product recall | 367,551 | 70.4% | 441,773 | 66.5% | ||||||||||||

| LIFO expense | 2,639 | 0.5% | 481 | 0.1% | ||||||||||||

| Overhead rate adjustments to inventory | (4,423 | ) | (0.9)% | 482 | 0.1% | |||||||||||

| Labor rate adjustments to inventory | (379 | ) | (0.1)% | (17 | ) | — | ||||||||||

| Product liability | 360 | 0.1% | 2,055 | 0.3% | ||||||||||||

| Product recall | 2,500 | 0.5% | ||||||||||||||

| Total cost of products sold | 368,248 | 70.5% | 444,774 | 67.0% | ||||||||||||

| Gross profit | $ | 154,008 | 29.5% | $ | 219,554 | 33.0% | ||||||||||

Cost of products sold, before LIFO, overhead and labor rate adjustments to inventory, product liability, and product recall- In 2017, cost of products sold, before LIFO, overhead and labor rate adjustments to inventory, product liability increased 3.9% as a percentage of sales compared to 2016. This decreased profitability is attributable to the decrease in sales which resulted in unfavorable de-leveraging of fixed manufacturing costs, including depreciation and indirect labor.

LIFO- Gross inventories decreased by $11.8 million in 2017 and increased $18.1 million in 2016. In 2017 and 2016, the Company recognized LIFO expense of $2.6 million and $0.5 million, respectively, which increased cost of products sold.

Overhead Rate Change- The net impact on inventory in 2017 and 2016 from the change in the overhead rates used to absorb overhead expenses into inventory was an increase of $4.4 million and a decrease of $0.5 million, respectively, reflecting decreased overhead efficiency in 2017 and increased overhead efficiency in 2016. The increase in inventory value in 2017 resulted in a corresponding decrease to cost of products sold and the decrease in inventory value in 2016 resulted in a corresponding increase to cost of products sold.

25

Labor Rate Adjustments- In 2017, the change in inventory value resulting from the change in the labor rates used to absorb labor expenses into inventory was an increase of $0.4 million, reflecting decreased labor efficiency. This increase in inventory value resulted in a corresponding decrease to cost of products sold. In 2016, the change in inventory value resulting from the change in the labor rates used to absorb labor expenses into inventory was de minimis.

Product Liability- This expense includes the cost of outside legal fees, insurance, and other expenses incurred in the management and defense of product liability matters. These costs totaled $0.4 million and $2.1 million in 2017 and 2016, respectively. See Note 17 in the notes to the financial statements “Contingent Liabilities” for further discussion of the Company’s product liability.

Product Recall – In June 2017, the Company discovered that Mark IV pistols manufactured prior to June 1, 2017 had the potential to discharge unintentionally if the safety was not utilized correctly. The Company recalled all Mark IV pistols and recorded a $2.5 million expense in the second quarter, which is the expected total cost of the recall. No such expense was recorded in the prior year.

Gross Profit- Gross profit was $154.0 million or 29.5% of sales in 2017. This is a decrease of $65.6 million from 2016 gross profit of $219.6 million or 33.0% of sales in 2016.

Selling, General and Administrative

Selling, general and administrative expenses were $77.6 million in 2017, a decrease of $7.5 million from $85.1 million in 2016, and an increase from 12.8% of sales in 2016 to 14.9% of sales in 2017. The decrease is primarily attributable to the absence of the “2.5 Million Gun Challenge” and the “Ruger $5 Million Match Challenge”, both of which were in effect in 2016. The decrease was partially offset by increased firearms promotional activities in 2017.

Other Operating Income, net

Other operating income, net was de minimis in 2017 and 2016.

Operating Income

Operating income was $76.3 million or 14.6% of sales in 2017. This is a decrease of $58.1 million from 2016 operating income of $134.4 million or 20.2% of sales.

Royalty Income

Royalty income was $0.5 million in 2017 and $1.1 million in 2016.

Interest Income and Interest Expense

Interest income and interest expense were negligible in 2017 and 2016.

26

Other Income, Net

Other income, net was $0.9 million in 2017, an increase of $0.4 million from income of $0.5 million in 2016.

Income Taxes and Net Income

The effective income tax rate was 32.8% in 2017 and 35.6% in 2016. The decrease in the effective tax rate in 2017 is primarily attributable to:

| · | the inclusion of the tax impact of 2017 equity-based compensation in income taxes, as required by newly issued Accounting Standards Update (ASU) 2016-09, “Improvements to Employee Share Based Payment Accounting”, which reduced the effective tax rate by 0.9%. In the prior year, the tax impact of equity-based compensation was recorded directly into equity, and |

| · | The revaluation of the Company’s net deferred tax liability at December 31, 2017 to reflect the impact of the lower statutory corporate tax rate enacted by the “Tax Cuts and Jobs Act”, which reduced the effective tax rate by 0.7%. |

The effective tax rate is expected to decrease to 24.5% in 2018 principally due to the “2017 Tax Cuts and Jobs Act” which reduces the Federal corporate income tax rate to 21% beginning in 2018.

As a result of the foregoing factors, consolidated net income was $52.1 million in 2017. This represents a decrease of $35.4 million from 2016 consolidated net income of $87.5 million.

Non-GAAP Financial Measure

In an effort to provide investors with additional information regarding its results, the Company refers to various United States generally accepted accounting principles (“GAAP”) financial measures and one non-GAAP financial measure, EBITDA, which management believes provides useful information to investors. This non-GAAP measure may not be comparable to similarly titled measures being disclosed by other companies. In addition, the Company believes that the non-GAAP financial measure should be considered in addition to, and not in lieu of, GAAP financial measures. The Company believes that EBITDA is useful to understanding its operating results and the ongoing performance of its underlying business, as EBITDA provides information on the Company’s ability to meet its capital expenditure and working capital requirements, and is also an indicator of profitability. The Company believes that this reporting provides better transparency and comparability to its operating results. The Company uses both GAAP and non-GAAP financial measures to evaluate the Company’s financial performance.

27

Non-GAAP Reconciliation – EBITDA

EBITDA

(Unaudited, dollars in thousands)

| Year ended December 31, | 2017 | 2016 | ||||||

| Net income | $ | 52,142 | $ | 87,472 | ||||

| Income tax expense | 25,504 | 48,449 | ||||||

| Depreciation and amortization expense | 34,264 | 35,355 | ||||||

| Interest expense | 152 | 186 | ||||||

| Interest income | (27 | ) | (14 | ) | ||||

| EBITDA | $ | 112,035 | $ | 171,448 | ||||

EBITDA is defined as earnings before interest, taxes, and depreciation and amortization. The Company calculates this by adding the amount of interest expense, income tax expense and depreciation and amortization expenses that have been deducted from net income back into net income, and subtracting the amount of interest income that was included in net income from net income to arrive at EBITDA. The Company’s EBITDA calculation also excludes any one-time non-cash, non-operating expense.

28

Quarterly Data

To supplement the summary annual unit data and discussion above, the same data for the last eight quarters follows:

| 2017 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Units Ordered | 467,500 | 221,900 | 214,400 | 395,000 | ||||||||||||

| Units Produced | 320,800 | 327,300 | 432,900 | 529,900 | ||||||||||||

| Units Shipped | 383,200 | 329,100 | 432,000 | 521,000 | ||||||||||||

| Estimated Units Sold from Distributors to Retailers | 425,600 | 341,300 | 362,400 | 533,800 | ||||||||||||

| Total Adjusted NICS Background Checks | 4,210,000 | 2,948,000 | 3,116,000 | 3,694,000 | ||||||||||||

| Average Unit Sales Price | $ | 306 | $ | 315 | $ | 302 | $ | 319 | ||||||||

| Units – Backlog | 254,900 | 170,600 | 277,800 | 495,400 | ||||||||||||

| Units – Company Inventory | 102,900 | 165,400 | 167,200 | 166,200 | ||||||||||||

| Units – Distributor Inventory (5) | 321,300 | 363,800 | 376,000 | 306,400 | ||||||||||||

| 2016 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Units Ordered | 432,100 | 445,700 | 399,400 | 969,400 | ||||||||||||

| Units Produced | 566,200 | 527,600 | 529,600 | 502,100 | ||||||||||||

| Units Shipped | 527,300 | 507,500 | 504,000 | 516,700 | ||||||||||||

| Estimated Units Sold from Distributors to Retailers | 529,100 | 453,400 | 453,700 | 571,000 | ||||||||||||

| Total Adjusted NICS Background Checks | 4,861,000 | 3,519,000 | 3,199,000 | 4,148,000 | ||||||||||||

| Average Unit Sales Price | $ | 304 | $ | 315 | $ | 330 | $ | 332 | ||||||||

| Units – Backlog | 621,400 | 716,600 | 778,400 | 883,000 | ||||||||||||

| Units – Company Inventory | 157,400 | 118,500 | 98,500 | 72,800 | ||||||||||||

| Units – Distributor Inventory (5) | 319,300 | 321,100 | 267,000 | 216,700 | ||||||||||||

| (5) | Distributor ending inventory as provided by the independent distributors of the Company’s products. |

29

(in millions except average sales price, net of Federal Excise Tax)

| 2017 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Orders Received | $ | 129.0 | $ | 62.9 | $ | 62.4 | $ | 131.9 | ||||||||

| Average Sales Price of Orders Received | $ | 276 | $ | 283 | $ | 291 | $ | 334 | ||||||||

| Ending Backlog | $ | 75.4 | $ | 56.6 | $ | 95.0 | $ | 163.8 | ||||||||

| Average Sales Price of Ending Backlog | $ | 296 | $ | 332 | $ | 342 | $ | 331 | ||||||||

| 2016 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Orders Received | $ | 130.2 | $ | 116.5 | $ | 145.7 | $ | 296.1 | ||||||||

| Average Sales Price of Orders Received | $ | 301 | $ | 261 | $ | 365 | $ | 305 | ||||||||

| Ending Backlog | $ | 195.0 | $ | 219.1 | $ | 257.6 | $ | 276.1 | ||||||||

| Average Sales Price of Ending Backlog | $ | 314 | $ | 306 | $ | 331 | $ | 313 | ||||||||

30

Fourth Quarter Gross Profit Analysis

The gross margin for the fourth quarter of 2017 and 2016 was 28.0% and 33.1%, respectively. Details of the gross margin are illustrated below:

(in thousands)

| Three Months Ended December 31, | 2017 | 2016 | ||||||||||||||

| Net sales | $ | 118,230 | 100.0 | % | $ | 161,849 | 100.0 | % | ||||||||

| Cost of products sold, before LIFO, overhead and labor rate adjustments to inventory, and product liability | 85,972 | 72.7 | % | 109,977 | 67.9 | % | ||||||||||

| LIFO (income) expense | 464 | 0.4 | % | (1,295 | ) | (0.8) | % | |||||||||

| Overhead rate adjustments to inventory | (1,132 | ) | (0.9) | % | (756 | ) | (0.5) | % | ||||||||

| Labor rate adjustments to inventory | (71 | ) | (0.1) | % | (133 | ) | (0.1) | % | ||||||||

| Product liability | (97 | ) | (0.1) | % | 560 | 0.4 | % | |||||||||

| Total cost of products sold | 85,136 | 72.0 | % | 108,353 | 66.9 | % | ||||||||||

| Gross profit | $ | 33,094 | 28.0 | % | $ | 53,496 | 33.1 | % | ||||||||

Note: For a discussion of the captions in the above table, please see the “Cost of Products Sold and Gross Profit” discussion above.

31

Results of Operations - 2016

Year ended December 31, 2016, as compared to year ended December 31, 2015:

Annual Summary Unit Data

Firearms unit data for orders, production, shipments and ending inventory, and castings setups (a measure of foundry production) are as follows:

| 2016 | 2015 | 2014 | ||||||||||

| Units Ordered | 2,246,600 | 1,517,000 | 921,900 | |||||||||

| Units Produced | 2,125,500 | 1,721,300 | 1,867,800 | |||||||||

| Units Shipped | 2,055,500 | 1,738,100 | 1,791,300 | |||||||||

| Average Sales Price | $ | 320 | $ | 313 | $ | 303 | ||||||

| Units – Backlog | 621,400 | 430,300 | 651,400 | |||||||||

| Units – Company Inventory | 157,400 | 87,400 | 104,200 | |||||||||

| Units – Distributor Inventory (1) | 319,300 | 271,000 | 326,700 | |||||||||

| Castings Setups | 170,681 | 164,212 | 201,592 | |||||||||

Orders Received and Ending Backlog

(in millions except average sales price, net of Federal Excise Tax):

| 2016 | 2015 | 2014 | ||||||||||

| Orders Received | $ | 688.5 | $ | 463.2 | $ | 286.8 | ||||||

| Average Sales Price of Orders Received (2) | $ | 306 | $ | 303 | $ | 311 | ||||||

| Ending Backlog (2) | $ | 195.0 | $ | 137.8 | $ | 204.2 | ||||||

| Average Sales Price of Ending Backlog (2) | $ | 314 | $ | 320 | $ | 313 | ||||||

| (1) | Distributor ending inventory as provided by the independent distributors of the Company’s products. |

| (2) | Average sales price for orders received and ending backlog is net of Federal Excise Tax of 10% for handguns and 11% for long guns. |

32

Product Demand

The estimated sell-through of the Company’s products from the independent distributors to retailers increased 12% in 2016 from 2015. For the same period, the National Instant Criminal Background Check System (“NICS”) background checks (as adjusted by the National Shooting Sports Foundation (“NSSF”)) increased 10%. The increase in estimated sell-through of the Company’s products from the independent distributors to retailers is attributable to:

| · | stronger-than-normal seasonal industry demand, likely bolstered by the political campaigns for the elections in November, |

| · | strong demand for certain new products, |

| · | increased production of several products in strong demand, and |

| · | greater availability of rimfire ammunition which spurred demand for our 10/22 rifle and other rimfire firearms late in the latter half of the year. |

New products represented $192.6 million or 29% of firearms sales in 2016, compared to $115.4 million or 21% of firearms sales in 2015. New product sales include only major new products that were introduced in the past two years. In 2016, new products included the Precision Rifle, the AR-556 modern sporting rifle, the LC9s pistol, the Mark IV pistols, the LCP II pistol, and the American pistol. The AR-556 and the LC9s pistol will not be considered new products in 2017.

Estimated sell-through from distributors to retailers and total adjusted NICS background checks:

| 2016 | 2015 | 2014 | ||||||||||

| Estimated Units Sold from Distributors to Retailers (1) | 2,007,200 | 1,793,800 | 1,669,700 | |||||||||

| Total Adjusted NICS Background Checks (2) | 15,727,700 | 14,244,200 | 13,090,400 | |||||||||

| (1) | The estimates for each period were calculated by taking the beginning inventory at the distributors, plus shipments from the Company to distributors during the period, less the ending inventory at distributors. These estimates are only a proxy for actual market demand as they: |

| · | Rely on data provided by independent distributors that are not verified by the Company, |

| · | Do not consider potential timing issues within the distribution channel, including goods-in-transit, and |

| · | Do not consider fluctuations in inventory at retail. |

| (2) | NICS background checks are performed when the ownership of most firearms, either new or used, is transferred by a Federal Firearms Licensee. NICS background checks are also performed for permit applications, permit renewals, and other administrative reasons. |

33

The adjusted NICS data presented above was derived by the NSSF by subtracting NICS checks that are not directly related to the sale of a firearm, including checks used for concealed carry (“CCW”) permit application checks as well as checks on active CCW permit databases.

Production

The Company reviews the estimated sell-through from the independent distributors to retailers, as well as inventory levels at the independent distributors and at the Company, semi-monthly to plan production levels and manage increases in inventory. These reviews and increased production capacity of products in strong demand resulted in an increase in total unit production of 23.5% in 2016 compared to 2015.

Inventories

The Company’s finished goods inventory increased by 70,000 units during 2016.

Distributor inventories of the Company’s products increased by 48,300 units during 2016 and approximate a reasonable level to support rapid fulfillment of retailer demand.

Inventory data follows:

| December 31, | ||||||||||||

| 2016 | 2015 | 2014 | ||||||||||

| Units – Company Inventory | 157,400 | 87,400 | 104,200 | |||||||||

| Units – Distributor Inventory (3) | 319,300 | 271,000 | 326,700 | |||||||||

| Total inventory (4) | 476,700 | 358,400 | 430,900 | |||||||||

| (3) | Distributor ending inventory as provided by the independent distributors of the Company’s products. These numbers do not include goods-in-transit inventory that has been shipped from the Company but not yet received by the distributors. |

| (4) | This total does not include inventory at retailers. The Company does not have access to data on retailer inventories. |

34

Quarterly Summary Unit Data

To supplement the summary annual unit data and discussion above, the same data for the last eight quarters follows:

| 2016 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Units Ordered | 432,100 | 445,700 | 399,400 | 969,400 | ||||||||||||

| Units Produced | 566,200 | 527,600 | 529,600 | 502,100 | ||||||||||||

| Units Shipped | 527,300 | 507,500 | 504,000 | 516,700 | ||||||||||||

| Estimated Units Sold from Distributors to Retailers | 529,100 | 453,400 | 453,700 | 571,000 | ||||||||||||

| Total Adjusted NICS Background Checks | 4,861,000 | 3,519,000 | 3,199,000 | 4,148,000 | ||||||||||||

| Average Unit Sales Price | $ | 304 | $ | 315 | $ | 330 | $ | 332 | ||||||||

| Units – Backlog | 621,400 | 716,600 | 778,400 | 883,000 | ||||||||||||

| Units – Company Inventory | 157,400 | 118,500 | 98,500 | 72,800 | ||||||||||||

| Units – Distributor Inventory (5) | 319,300 | 321,100 | 267,000 | 216,700 | ||||||||||||

| 2015 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Units Ordered | 696,400 | 207,500 | 262,400 | 350,700 | ||||||||||||

| Units Produced | 425,400 | 439,900 | 487,000 | 369,000 | ||||||||||||

| Units Shipped | 478,400 | 394,700 | 442,900 | 422,100 | ||||||||||||

| Estimated Units Sold from Distributors to Retailers | 552,700 | 374,900 | 379,400 | 486,800 | ||||||||||||

| Total Adjusted NICS Background Checks | 4,880,000 | 3,050,000 | 2,793,000 | 3,521,000 | ||||||||||||

| Average Unit Sales Price | $ | 315 | $ | 302 | $ | 314 | $ | 321 | ||||||||

| Units – Backlog | 430,300 | 212,300 | 399,500 | 580,000 | ||||||||||||

| Units – Company Inventory | 87,400 | 140,400 | 95,200 | 51,100 | ||||||||||||

| Units – Distributor Inventory (5) | 271,000 | 345,300 | 325,500 | 262,000 | ||||||||||||

35

| (5) | Distributor ending inventory as provided by the independent distributors of the Company’s products. |

(in millions except average sales price, net of Federal Excise Tax)

| 2016 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Orders Received | $ | 130.2 | $ | 116.5 | $ | 145.7 | $ | 296.1 | ||||||||

| Average Sales Price of Orders Received | $ | 301 | $ | 261 | $ | 365 | $ | 305 | ||||||||

| Ending Backlog | $ | 195.0 | $ | 219.1 | $ | 257.6 | $ | 276.1 | ||||||||

| Average Sales Price of Ending Backlog | $ | 314 | $ | 306 | $ | 331 | $ | 313 | ||||||||

| 2015 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Orders Received | $ | 203.4 | $ | 73.1 | $ | 71.9 | $ | 114.8 | ||||||||

| Average Sales Price of Orders Received | $ | 292 | $ | 352 | $ | 274 | $ | 327 | ||||||||

| Ending Backlog | $ | 137.8 | $ | 80.5 | $ | 123.8 | $ | 185.1 | ||||||||

| Average Sales Price of Ending Backlog | $ | 320 | $ | 379 | $ | 310 | $ | 319 | ||||||||

Net Sales

Consolidated net sales were $664.3 million in 2016. This represents an increase of $113.2 million or 20.5% from 2015 consolidated net sales of $551.1 million.

Firearms segment net sales were $658.4 million in 2016. This represents an increase of $113.5 million or 20.8% from 2015 firearms net sales of $544.9 million. Firearms unit shipments increased 18.3% in 2016.

Casting segment net sales were $5.9 million in 2016. This represents a decrease of $0.3 million or 5.6% from 2015 casting sales of $6.2 million.

Cost of Products Sold and Gross Profit

Consolidated cost of products sold was $444.8 million in 2016. This represents an increase of $65.9 million or 17.4% from 2015 consolidated cost of products sold of $378.9 million.

36

The gross margin was 33.0% in 2016. This represents an increase from 31.2% in 2015 as illustrated below:

(in thousands)

| Year Ended December 31, | 2016 | 2015 | ||||||||||||||

| Net sales | $ | 664,328 | 100.0% | $ | 551,094 | 100.0% | ||||||||||

| Cost of products sold, before LIFO, overhead and labor rate adjustments to inventory, and product liability | 441,773 | 66.5% | 375,267 | 68.1% | ||||||||||||

| LIFO expense | 481 | 0.1% | 1,458 | 0.3% | ||||||||||||

| Overhead rate adjustments to inventory | 482 | 0.1% | 1,150 | 0.2% | ||||||||||||

| Labor rate adjustments to inventory | (17 | ) | — | 139 | — | |||||||||||

| Product liability | 2,055 | 0.3% | 920 | 0.2% | ||||||||||||

| Total cost of products sold | 444,774 | 67.0% | 378,934 | 68.8% | ||||||||||||

| Gross profit | $ | 219,554 | 33.0% | $ | 172,160 | 31.2% | ||||||||||

Cost of products sold, before LIFO, overhead and labor rate adjustments to inventory, and product liability- In 2016, cost of products sold, before LIFO, overhead and labor rate adjustments to inventory, and product liability decreased 1.8% as a percentage of sales compared to 2015. This increased profitability is attributable to increased volume and improved productivity.

LIFO- Gross inventories increased by $18.1 million in 2016 and decreased $7.7 million in 2015. In 2016 and 2015, the Company recognized LIFO expense of $0.5 million and $1.5 million, respectively, which increased cost of products sold.

Overhead Rate Change- The net impact on inventory in 2016 and 2015 from the change in the overhead rates used to absorb overhead expenses into inventory was a decrease of $0.5 million and $1.2 million, respectively, reflecting increased overhead efficiency. This decrease in inventory value resulted in a corresponding increase to cost of products sold in 2016 and 2015.

Labor Rate Adjustments- In 2016, the change in inventory value resulting from the change in the labor rates used to absorb labor expenses into inventory was de minimis. In 2015, the change in inventory value resulting from the change in the labor rates used to absorb labor expenses into inventory was a decrease of $0.1 million, reflecting increased labor efficiency. This decrease in inventory value resulted in a corresponding increase to cost of products sold.

37

Product Liability- This expense includes the cost of outside legal fees, insurance, and other expenses incurred in the management and defense of product liability matters. These costs totaled $2.1 million and $0.9 million in 2016 and 2015, respectively. See Note 17 in the notes to the financial statements “Contingent Liabilities” for further discussion of the Company’s product liability.

Gross Profit- Gross profit was $219.6 million or 33.0% of sales in 2016. This is an increase of $47.4 million from 2015 gross profit of $172.2 million or 31.2% of sales in 2015.

Selling, General and Administrative

Selling, general and administrative expenses were $85.1 million in 2016, an increase of $7.4 million from $77.7 million in 2015, and a decrease from 14.1% of sales in 2015 to 12.8% of sales in 2016. The increase in selling, general and administrative expenses is primarily attributable to increased promotional selling expenses, including the “Ruger $5 Million Match Challenge” and the “2.5 Million Gun Challenge” in 2016.

Other Operating Income, net

Other operating income, net consists of the following (in thousands):

| 2016 | 2015 | |||||||

| Gain on sale of operating assets | $ | 5 | $ | 113 | ||||

| Total other operating income, net | $ | 5 | $ | 113 | ||||

Operating Income

Operating income was $134.4 million or 20.2% of sales in 2016. This is an increase of $39.9 million from 2015 operating income of $94.5 million or 17.2% of sales.

Royalty Income

Royalty income was $1.1 million in 2016 and 2015.

Interest Income and Interest Expense

Interest income and interest expense were negligible in 2016 and 2015.

Other Income (Expense), Net

Other income (expense), net was income of $0.5 million in 2016, a decrease of $0.1 million from income of $0.6 million in 2015.

38

Income Taxes and Net Income

The effective income tax rate was 35.6% in 2016 and 35.4% in 2015. The increase in the effective tax rate is primarily attributable to a decrease in the domestic production activities deduction in 2016 compared to 2015.

As a result of the foregoing factors, consolidated net income was $87.5 million in 2016. This represents an increase of $25.4 million from 2015 consolidated net income of $62.1 million.

Non-GAAP Financial Measure

In an effort to provide investors with additional information regarding its results, the Company refers to various United States generally accepted accounting principles (“GAAP”) financial measures and one non-GAAP financial measure, EBITDA, which management believes provides useful information to investors. This non-GAAP measure may not be comparable to similarly titled measures being disclosed by other companies. In addition, the Company believes that the non-GAAP financial measure should be considered in addition to, and not in lieu of, GAAP financial measures. The Company believes that EBITDA is useful to understanding its operating results and the ongoing performance of its underlying business, as EBITDA provides information on the Company’s ability to meet its capital expenditure and working capital requirements, and is also an indicator of profitability. The Company believes that this reporting provides better transparency and comparability to its operating results. The Company uses both GAAP and non-GAAP financial measures to evaluate the Company’s financial performance.

Non-GAAP Reconciliation – EBITDA

EBITDA

(Unaudited, dollars in thousands)

| Year ended December 31, | 2016 | 2015 | ||||||

| Net income | $ | 87,472 | $ | 62,126 | ||||

| Income tax expense | 48,449 | 33,974 | ||||||

| Depreciation and amortization expense | 35,355 | 36,235 | ||||||