UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

Form 10-Q

x Quarterly Report Pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934

For the Period Ended June 30, 2016

or

¨ Transition Report Pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934

For the Transition Period From _____________to _____________

Commission File Number 33-92894

| ALY ENERGY SERVICES, INC. |

| (Exact name of registrant as specified in its charter) |

| Delaware |

| 75-2440201 |

| (State or other jurisdiction of |

| (I.R.S. Employer Identification No.) |

| incorporation or organization) |

|

|

|

|

|

|

| 3 Riverway, Suite 920 |

|

|

| Houston, TX |

| 77056 |

| (Address of Principal Executive Offices) |

| (Zip Code) |

(713)-333-4000

(Registrant’s Telephone Number, including area code.)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Names of Each Exchange on which Registered | |

| Common Stock, $0.001 par value per share | None |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No x

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

| Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

At September 30, 2017, the registrant had 13,818,795 shares of common stock, $0.001 par value, outstanding.

Documents Incorporated by Reference: None

(A Delaware Corporation)

INDEX

|

| Page |

| ||

|

| ||||

|

| 3 |

| ||

| Unaudited Pro Forma Consolidated Balance Sheet as of December 31, 2016 |

| 3 |

| |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| 29 |

| |

|

| 39 |

| ||

|

| 40 | |||

|

| ||||

|

| 42 | |||

|

|

| 43 | ||

| 2 |

PART I – FINANCIAL INFORMATION

|

|

| |||

|

|

|

|

| |

| Index |

| Page |

| |

|

|

|

|

| |

| Unaudited Pro Forma Consolidated Balance Sheet as of December 31, 2016 |

|

| 24 |

|

|

|

|

|

|

|

|

|

| 26 |

| |

| 3 |

| Table of Contents |

| CONDENSED CONSOLIDATED BALANCE SHEETS | ||||||

| (in thousands, except share and per share amounts) |

|

|

| June 30, 2016 |

|

| December 31, 2015 |

| ||

|

|

| (unaudited) |

|

|

|

| ||

| ASSETS |

|

|

|

|

|

| ||

| Current assets |

|

|

|

|

|

| ||

| Cash and cash equivalents |

| $ | 493 |

|

| $ | 514 |

|

| Restricted cash |

|

| 30 |

|

|

| - |

|

| Receivables, net |

|

| 2,118 |

|

|

| 4,409 |

|

| Prepaid expenses and other current assets |

|

| 421 |

|

|

| 957 |

|

| Assets associated with discontinued operations |

|

| 1,632 |

|

|

| 3,428 |

|

| Total current assets |

|

| 4,694 |

|

|

| 9,308 |

|

|

|

|

|

|

|

|

|

|

|

| Property and equipment, net |

|

| 49,216 |

|

|

| 51,789 |

|

| Intangible assets, net |

|

| 6,110 |

|

|

| 7,409 |

|

| Other assets |

|

| 12 |

|

|

| 21 |

|

| Total assets |

| $ | 60,032 |

|

| $ | 68,527 |

|

|

|

|

|

|

|

|

|

|

|

| LIABILITIES AND STOCKHOLDERS' EQUITY |

|

|

|

|

|

|

|

|

| Current liabilities |

|

|

|

|

|

|

|

|

| Accounts payable and accrued expenses |

| $ | 3,065 |

|

| $ | 3,331 |

|

| Current portion of long-term debt |

|

| 22,039 |

|

|

| 20,353 |

|

| Current portion of contingent payment liability |

|

| 976 |

|

|

| 652 |

|

| Liabilities associated with discontinued operations |

|

| 803 |

|

|

| 1,211 |

|

| Total current liabilities |

|

| 26,883 |

|

|

| 25,547 |

|

|

|

|

|

|

|

|

|

|

|

| Long-term debt, net |

|

| 1,365 |

|

|

| 3,185 |

|

| Contingent payment liability, net |

|

| - |

|

|

| 530 |

|

| Deferred tax liabilities |

|

| 5,391 |

|

|

| 7,941 |

|

| Other long-term liabilities |

|

| 31 |

|

|

| 31 |

|

| Total liabilities |

|

| 33,670 |

|

|

| 37,234 |

|

|

|

|

|

|

|

|

|

|

|

| Commitments and contingencies |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Aly Operating redeemable preferred stock |

|

| 4,784 |

|

|

| 4,647 |

|

| Aly Centrifuge redeemable preferred stock |

|

| 9,915 |

|

|

| 9,755 |

|

|

|

|

| 14,699 |

|

|

| 14,402 |

|

| Stockholders' equity |

|

|

|

|

|

|

|

|

| Preferred stock of $0.001 par value |

|

| - |

|

|

| - |

|

| Authorized - 10,000,000, none issued and outstanding as of June 30, 2016 |

|

|

|

|

|

|

|

|

| Authorized - 25,000,000, none issued and outstanding as of December 31, 2015 |

|

|

|

|

|

|

|

|

| Common stock of $0.001 par value |

|

| 7 |

|

|

| 7 |

|

| Authorized - 25,000,000; issued - 6,707,039; outstanding - 6,706,814 as of June 30, 2016 |

|

|

|

|

|

|

|

|

| Authorized - 100,000,000; issued - 6,707,039; outstanding - 6,706,814 as of December 31, 2015 |

|

|

|

|

|

|

|

|

| Additional paid-in-capital |

|

| 28,612 |

|

|

| 28,909 |

|

| Accumulated deficit |

|

| (16,954 | ) |

|

| (12,023 | ) |

| Treasury stock, 225 shares at cost |

|

| (2 | ) |

|

| (2 | ) |

| Total stockholders' equity |

|

| 11,663 |

|

|

| 16,891 |

|

|

|

|

|

|

|

|

|

|

|

| Total liabilities and stockholders' equity |

| $ | 60,032 |

|

| $ | 68,527 |

|

| 4 |

| Table of Contents |

| CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS | |||||||||||

| (in thousands, except share and per share amounts) |

|

|

| For the Three Months Ended June 30, |

|

| For the Six Months Ended June 30, |

| ||||||||||

|

|

| 2016 |

|

| 2015 |

|

| 2016 |

|

| 2015 |

| ||||

|

|

| (unaudited) |

|

| (unaudited) |

| ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

| Revenue |

| $ | 2,669 |

|

| $ | 6,222 |

|

| $ | 6,777 |

|

| $ | 13,284 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operating expenses |

|

| 2,308 |

|

|

| 3,882 |

|

|

| 5,349 |

|

|

| 8,494 |

|

| Depreciation and amortization |

|

| 1,393 |

|

|

| 1,516 |

|

|

| 2,834 |

|

|

| 2,974 |

|

| Selling, general and administrative expenses |

|

| 1,300 |

|

|

| 2,056 |

|

|

| 2,686 |

|

|

| 3,976 |

|

| Reduction in value of assets |

|

| 543 |

|

|

| - |

|

|

| 843 |

|

|

| - |

|

| Total expenses |

|

| 5,544 |

|

|

| 7,454 |

|

|

| 11,712 |

|

|

| 15,444 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loss from continuing operations |

|

| (2,875 | ) |

|

| (1,232 | ) |

|

| (4,935 | ) |

|

| (2,160 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest expense, net |

|

| 560 |

|

|

| 455 |

|

|

| 1,148 |

|

|

| 945 |

|

| Loss from continuing operations before income taxes |

|

| (3,435 | ) |

|

| (1,687 | ) |

|

| (6,083 | ) |

|

| (3,105 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income tax benefit |

|

| (1,636 | ) |

|

| (769 | ) |

|

| (2,534 | ) |

|

| (1,333 | ) |

| Net loss from continuing operations |

|

| (1,799 | ) |

|

| (918 | ) |

|

| (3,549 | ) |

|

| (1,772 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loss from discontinued operations, net of income taxes |

|

| 1,257 |

|

|

| 654 |

|

|

| 1,382 |

|

|

| 1,239 |

|

| Net loss |

|

| (3,056 | ) |

|

| (1,572 | ) |

|

| (4,931 | ) |

|

| (3,011 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Preferred stock dividends |

|

| 181 |

|

|

| 178 |

|

|

| 359 |

|

|

| 353 |

|

| Accretion of preferred stock, net |

|

| (33 | ) |

|

| (32 | ) |

|

| (62 | ) |

|

| (65 | ) |

| Net loss available to common stockholders |

| $ | (3,204 | ) |

| $ | (1,718 | ) |

| $ | (5,228 | ) |

| $ | (3,299 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic and diluted earnings per share information: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net loss from continuing operations available to common stockholders |

| $ | (0.29 | ) |

| $ | (0.18 | ) |

| $ | (0.57 | ) |

| $ | (0.36 | ) |

| Loss from discontinued operations, net of income taxes |

|

| (0.19 | ) |

|

| (0.12 | ) |

|

| (0.21 | ) |

|

| (0.22 | ) |

| Net loss available to common stockholders |

| $ | (0.48 | ) |

| $ | (0.30 | ) |

| $ | (0.78 | ) |

| $ | (0.58 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Weighted-average shares - basic and diluted |

|

| 6,706,814 |

|

|

| 5,654,580 |

|

|

| 6,706,814 |

|

|

| 5,644,678 |

|

| 5 |

| Table of Contents |

| CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS | ||||||||

| (in thousands) |

|

|

| For the Six Months Ended June 30, |

| |||||

|

|

| 2016 |

|

| 2015 |

| ||

|

|

| (unaudited) |

| |||||

|

|

|

|

|

|

|

| ||

| Cash flows from operating activities: |

|

|

|

|

|

| ||

| Net loss |

| $ | (4,931 | ) |

| $ | (3,011 | ) |

| Less: Loss from discontinued operations, net of income taxes |

|

| 1,382 |

|

|

| 1,239 |

|

| Net loss from continuing operations |

|

| (3,549 | ) |

|

| (1,772 | ) |

|

|

|

|

|

|

|

|

|

|

| Adjustments to reconcile net loss to net cash provided by operating activities: |

|

|

|

|

|

|

|

|

| Depreciation and amortization |

|

| 2,834 |

|

|

| 2,974 |

|

| Amortization of deferred loan costs |

|

| 173 |

|

|

| 234 |

|

| Reduction in value of assets |

|

| 843 |

|

|

| - |

|

| Stock-based compensation |

|

| - |

|

|

| 100 |

|

| Bad debt expense |

|

| 34 |

|

|

| 141 |

|

| Fair value adjustments to contingent payment liability |

|

| (206 | ) |

|

| (311 | ) |

| Deferred taxes |

|

| (2,550 | ) |

|

| (1,376 | ) |

| Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

| Receivables |

|

| 2,257 |

|

|

| 4,525 |

|

| Prepaid expenses and other assets |

|

| 545 |

|

|

| 365 |

|

| Accounts payable, accrued expenses and other liabilities |

|

| (266 | ) |

|

| (2,869 | ) |

| Net cash provided by continuing operations |

|

| 115 |

|

|

| 2,011 |

|

| Net cash provided by (used in) discontinued operations |

|

| (18 | ) |

|

| 1,363 |

|

| Net cash provided by operating activities |

|

| 97 |

|

|

| 3,374 |

|

|

|

|

|

|

|

|

|

|

|

| Cash flows from investing activities: |

|

|

|

|

|

|

|

|

| Purchases of property and equipment |

|

| (264 | ) |

|

| (1,149 | ) |

| Proceeds from disposal of property and equipment |

|

| 459 |

|

|

| 30 |

|

| Net cash provided by (used in) continuing operations |

|

| 195 |

|

|

| (1,119 | ) |

| Net cash provided by (used in) discontinued operations |

|

| 39 |

|

|

| (28 | ) |

| Net cash provided by (used in) investing activities |

|

| 234 |

|

|

| (1,147 | ) |

|

|

|

|

|

|

|

|

|

|

| Cash flows from financing activities: |

|

|

|

|

|

|

|

|

| Proceeds from issuance of common stock, net |

|

| - |

|

|

| 550 |

|

| Repayment of long-term debt |

|

| (307 | ) |

|

| (3,553 | ) |

| Payment of contingent payment liability |

|

| - |

|

|

| (862 | ) |

| Payment of deferred loan costs |

|

| - |

|

|

| (32 | ) |

| Net cash used in continuing operations |

|

| (307 | ) |

|

| (3,897 | ) |

| Net cash used in discontinued operations |

|

| (5 | ) |

|

| (4 | ) |

| Net cash used in financing activities |

|

| (312 | ) |

|

| (3,901 | ) |

|

|

|

|

|

|

|

|

|

|

| Net increase (decrease) in cash, cash equivalents, and restricted cash |

|

| 19 |

|

|

| (1,674 | ) |

| Cash, cash equivalents, and restricted cash, beginning of period |

|

| 497 |

|

|

| 2,050 |

|

| Cash, cash equivalents, and restricted cash, end of period |

| $ | 516 |

|

| $ | 376 |

|

| 6 |

| Table of Contents |

NOTE 1 — NATURE OF OPERATIONS AND BASIS OF PRESENTATION

Nature of Operations

Aly Energy Services, Inc., together with its subsidiaries (“Aly Energy” or the “Company”), provides oilfield services, including equipment rental and solids control services to exploration and production companies. The Company operates in select oil and natural gas basins of the contiguous United States. Throughout this report, we refer to Aly Energy and its subsidiaries as “we”, “our” or “us”. References to financial results and operations of the Company in these notes to the condensed consolidated financial statements are limited to continuing operations unless otherwise specified.

On October 26, 2012, we acquired all of the stock of Austin Chalk Petroleum Services Corp. (“Austin Chalk”). Austin Chalk provides surface rental equipment as well as roustabout services which include the rig-up and rig-down of equipment and the hauling of equipment to and from the customer's location.

On April 15, 2014, we acquired the equity interests of United Centrifuge, LLC (“United”) as well as certain assets used in United’s business that were owned by related parties of United (collectively the “United Acquisition”). In connection with the United Acquisition, United merged with and into Aly Centrifuge Inc. (“Aly Centrifuge”), a wholly-owned subsidiary of Aly Energy. United operates within the solids control and fluids management sectors of the oilfield services and rental equipment industry, offering its customers the option of renting centrifuges and auxiliary solids control equipment without personnel or the option of paying for a full-service solids control package which includes operators on-site 24 hours a day.

Discontinued Operations

On July 1, 2014, we acquired all of the issued and outstanding stock of Evolution Guidance Systems Inc. (“Evolution”), an operator of Measurement-While-Drilling (“MWD”) downhole tools. From July 2014 through October 2016, Evolution provided directional drilling and MWD services to a variety of exploration and production companies. On October 26, 2016, we abandoned these operations as a part of a restructuring transaction. The abandonment of these operations meets the criteria established for recognition as discontinued operations under generally accepted accounting principles in the United States of America (“U.S. GAAP”). Therefore, the financial results of our directional drilling and MWD services are presented as discontinued operations in the Company’s condensed consolidated financial statements. Assets and liabilities related to the discontinued operations are included in the line item “Assets associated with discontinued operations” and “Liabilities associated with discontinued operations”, respectively, on the condensed consolidated balance sheets for all periods presented. The results of the discontinued operations are included in the line item “Loss from discontinued operations, net of income taxes” on the condensed consolidated statements of operations for all periods presented. Cash flows from discontinued operations appear in the line items “Net cash provided by (used in) by discontinued operations” on the condensed consolidated statements of cash flows. See “Note 2 – Recent Developments and Subsequent Events” for more information.

Basis of Presentation

Aly Energy has three wholly-owned subsidiaries, Aly Operating Inc. (“Aly Operating”), of which Austin Chalk is a wholly-owned subsidiary, Aly Centrifuge and Evolution. We operate as one business segment which services customers within the United States.

The condensed consolidated financial statements have been prepared in conformity with U.S. GAAP and include the accounts of Aly Energy and each of its subsidiaries in the condensed consolidated balance sheets as of June 30, 2016 and December 31, 2015 and the related condensed consolidated statements of operations and cash flows for each of the periods presented. All significant intercompany transactions and account balances have been eliminated upon consolidation.

Interim Financial Information

The condensed consolidated balance sheet as of December 31, 2015 has been derived from our audited financial statements and the unaudited condensed consolidated financial statements of the Company are prepared in conformity with U.S. GAAP for interim financial reporting. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”). Therefore, these condensed consolidated financial statements should be read along with the annual audited consolidated financial statements and notes thereto included in the Company's Annual Report on Form 10-K for the year ended December 31, 2015. In management’s opinion, all adjustments necessary for a fair statement are reflected in the interim periods presented. Interim results for the three and six months ended June 30, 2016 are not indicative of results that were realized for the full year ending December 31, 2016. For more detail, please see the annual audited consolidated financial statements and notes thereto included in the Company's Annual Report on Form 10-K for the year ended December 31, 2016 filed with the SEC on September 5, 2017.

| 7 |

| Table of Contents |

Use of Estimates

The preparation of condensed consolidated financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions. These estimates and assumptions affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the balance sheet date, and the amounts of revenue and expenses recognized during the reporting period. Areas where critical accounting estimates are made by management include:

|

| · | Allowance for doubtful accounts, |

|

| · | Depreciation and amortization of property and equipment and intangible and other assets, |

|

| · | Impairment of property and equipment, intangible and other assets, and goodwill, |

|

| · | Litigation settlement accrual, |

|

| · | Contingent payment liability, and |

|

| · | Income taxes. |

The Company analyzes its estimates based on historical experience and various other indicative assumptions that it believes to be reasonable under the circumstances. Under different assumptions or conditions, the actual results could differ, possibly materially from those previously estimated. Many of the conditions impacting these assumptions are outside of the Company’s control.

Earnings per Share

Basic earnings per share is computed by dividing income available to common stockholders by the weighted average number of shares of common stock outstanding during the period. Diluted earnings per share is computed in the same manner as basic earnings per share except that the denominator is increased to include the number of additional shares of common stock that could have been outstanding assuming the exercise of outstanding stock options and restricted stock or other convertible instruments, as appropriate.

During the three and six months ended June 30, 2016 and 2015, the Company incurred losses from continuing operations; therefore, the impact of any incremental shares would be anti-dilutive.

Reclassifications

Certain reclassifications have been made to prior period consolidated financial statements to conform to the current period presentations. These reclassifications had no effect on our consolidated financial position, results of operations or cash flows.

Subsequent Events

We conducted our subsequent events review through the date these consolidated financial statements were filed with the SEC. (See “Note 2 – Recent Developments and Subsequent Events” and “Note 5 – Long-term Debt”.)

NOTE 2 — RECENT DEVELOPMENTS AND SUBSEQUENT EVENTS

Operational Restructuring

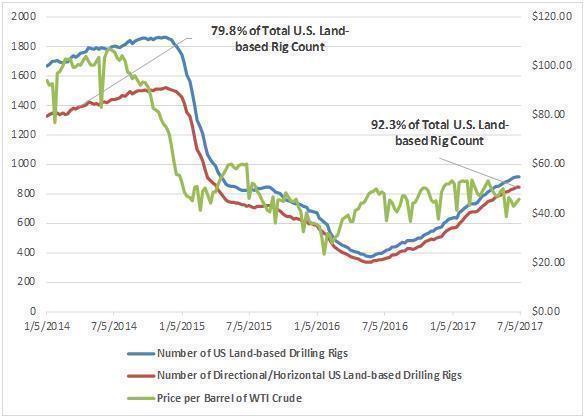

Our activity is tied directly to the rig count and, even though we instituted significant cost cutting measures beginning in 2015, we were unable to cut costs enough to match the decline in our business. As a result, as of December 31, 2015, we were in default of our credit agreement with Wells Fargo Bank, National Association (“Wells Fargo”).

Throughout 2015, in an effort to mitigate the significant declines in pricing and utilization of our equipment, we committed to a reorganization initiative to strengthen our sales and marketing efforts, consolidate support functions, and operate more efficiently. The reorganization effort included, but was not limited to, training our salesforce to enable the cross-selling of our product lines in certain geographical markets, sharing a common support services infrastructure across all reporting units, reducing headcount and wage rates, and rebranding and launching a new web site to increase awareness of our service lines. We recognized some benefit from these measures in late 2015 resulting in increased gross margins and lower selling, general and administrative expenses when compared to the first half of 2015.

| 8 |

| Table of Contents |

During the year ended December 31, 2016, we entered into a series of forbearance agreements with our lender. Under the forbearance agreements, among other provisions, the lenders agreed to forbear from exercising their remedies under the credit agreement. These forbearance agreements permitted us to operate within the parameters of our normal course of business despite the continuing default under the credit agreement. Without these forbearance agreements, our outstanding debt would have been immediately due and payable. Throughout 2016, we remained in default and we did not have sufficient liquidity to repay all of the outstanding debt to the lender at any point during the year ($20.1 million as of December 31, 2015). As such, we may have been forced to file for protection under Chapter 11 of the U.S. Bankruptcy Code.

In early 2016, we were hopeful that a successful operational restructuring would facilitate negotiations to modify the terms of our existing credit facility with Wells Fargo. Our operational restructuring in 2016 consisted of severe cost cuts which were incremental to the year-over-year cost cuts already achieved in 2015 when compared to 2014. In 2016, significant cost savings were primarily generated by:

|

| · | reductions of our employee base, both field employees and sales and administrative employees, to a headcount of approximately 50 as of December 31, 2016 from approximately 125 as of December 31, 2015, |

|

| · | reduction in employer contributions to employee benefits, |

|

| · | closures of certain operating yards and administrative facilities, |

|

| · | strategic decision to cease operations in the northeast which resulted in the reduction of costs related to operating in an incremental market, |

|

| · | modifications to insurance policies, including general liability and workers’ compensation policies, resulting in a $0.5 million or 15.5% reduction in the cost of insurance to $0.6 million for the year ended December 31, 2016 from $1.1 million for the year ended December 31, 2015, |

|

| · | minimization of repair and maintenance activities, resulting in a $0.4 million or 50.0% reduction of repair and maintenance expenses to $0.4 million for the year ended December 31, 2016 from $0.8 million for the year ended December 31, 2015, and |

|

| · | elimination of investments in equipment, unless required to service an existing customer, resulting in a reduction of capital expenditures to $0.4 million for the year ended December 31, 2016 from $2.5 million for the year ended December 31, 2015. |

We also achieved significant cost savings from the decrease in third party costs, such as sub-rental equipment and trucking, and other variable costs which declined with the decrease in activity.

In order to further support our working capital needs, we identified and sold idle and underutilized assets. During 2016, we realized aggregate proceeds from sales of such assets of approximately $0.8 million of which $0.5 million and $0.3 million was used to fund working capital needs and pay down debt, respectively (see “Note 3 – Reduction in Value of Assets and Other Charges”).

Capital Restructuring

Despite our successful operational restructuring efforts, particularly during the first half of 2016, the decline in our activity levels and the declines in customer pricing outpaced the impact of our cost reductions and it became evident that a capital restructuring would also be necessary to continue operations and position our business for an industry turnaround.

In the second quarter of 2016, certain of the Company’s principal stockholders (“Shareholder Group”) began negotiations with Wells Fargo with the objective of consummating a recapitalization transaction (the “Recapitalization”) whereby our obligations under the credit agreement and the outstanding capital leases in favor of Wells Fargo’s equipment finance affiliate and certain other obligations of Aly Energy (collectively the “Aly Senior Obligations”) would be restructured. In August 2016, the Shareholder Group was introduced to a third party, Tiger Finance, LLC (“Tiger”), to provide bridge financing and to extend forbearance until such date as sufficient capital could be raised to complete the Recapitalization.

In September 2016, the Shareholder Group formed Permian Pelican, LLC (“Pelican”) with the objective of raising capital and executing the steps necessary to complete the restructuring, inclusive of successfully effecting the exchange of the Aly Operating redeemable preferred stock, Aly Centrifuge redeemable preferred stock, Aly Centrifuge subordinated debt and liability for a contingent payment into approximately 10% of our common stock on a fully diluted basis.

Effective January 31, 2017, the Recapitalization was completed through the execution and delivery of a Securities Exchange Agreement and a Second Amended and Restated Credit Agreement, and, as a result, the new credit facility, now with Pelican, consisted of a term loan of $5.1 million and a revolving facility of up to $1.0 million as of January 31, 2017. Availability under the revolving credit facility is determined by a borrowing base calculated as 80% of eligible receivables (receivables less than 90 days old).

| 9 |

| Table of Contents |

Subsequent to the Recapitalization, we entered into several further amendments to capitalize on improved market conditions and increased activity in our business:

|

| · | Amendment No. 1, effective March 1, 2017, provided for a delayed draw term loan to be added to the credit facility for the purpose of financing capital expenditures. The agreement permitted us to draw on the delayed draw term loan from time-to-time up until the maturity date of the facility in order to fund up to 80% of the cost of capital expenditures subject to a $0.5 million limit on aggregate borrowings. |

|

| · | Amendment No. 2, effective May 23, 2017, increased the maximum revolving credit amount from $1.0 million to $1.8 million and extended the final maturity date of the facility to December 31, 2019. In consideration of the increase in the revolving credit facility and the extension of the final maturity date, we agreed to issue to Pelican, the lender, as an amendment fee, 1,200 shares of our Series A convertible preferred stock. |

|

| · | Amendment No. 3, effective June 15, 2017, modified maximum potential borrowings under each of the revolving credit facility and the delayed draw term loan without changing the aggregate available borrowings under the credit facility. The amendment reduced the maximum revolving credit amount from $1.8 million to $1.0 million and increased the maximum delayed draw loan borrowings from $0.5 million to $1.3 million and the amendment also increased permitted draws on the delayed draw loan from 80% of the cost of capital expenditures being funded to 90% of the cost of capital expenditures being funded. |

|

|

|

|

To the extent there is free cash flow as defined in the credit agreement, principal payments of 50% of such free cash flow are due annually. The maturity date of all remaining outstanding balances under the credit facility is December 31, 2019.

The obligations under the credit facility are guaranteed by all of our subsidiaries and secured by substantially all of our assets. The credit agreement contains customary events of default and covenants including restrictions on our ability to incur additional indebtedness, pay dividends or make other distributions, grant liens and sell assets. The credit facility does not include any financial covenants. We are in full compliance with the credit facility as of June 30, 2017.

As of June 30, 2017, there were outstanding borrowings of $5.0 million, $0.8 million, and $0.3 million on the term loan, revolving credit facility, and delayed draw term loan, respectively. As of June 30, 2017, we have the availability to borrow an incremental $0.2 million under the revolving credit facility and, if we have capital expenditures which are eligible to be financed, an incremental $1.0 million under the delayed draw term loan to finance 90% of such expenditures.

Recapitalization Summary

The Recapitalization consisted of three restructuring events which took place in the period beginning October 26, 2016 and ending on January 31, 2017. Below is a description of each event:

| The first restructuring event occurred on October 26, 2016 when Tiger acquired the Aly Senior Obligations from Wells Fargo and its equipment affiliate. Simultaneously, Tiger entered into an assignment agreement with Pelican whereby it agreed to sell the Aly Senior Obligations to Pelican on the conditions that (i) Pelican provide $0.5 million of unsecured working capital financing to the Company pending the closing and (ii) the Company transfer to Tiger (in consideration of Tiger’s reduction of the Aly Senior Obligations in the amount of $2.0 million) certain excess equipment and vehicles which the Company was not utilizing and considered unnecessary for its continuing operations.

As a result of the above, we transferred property and equipment with an estimated fair value of $2.6 million, inclusive of $0.4 million of assets associated with discontinued operations, to Tiger and recognized a corresponding reduction in the Aly Senior Obligations of $2.0 million and debt modification fee of $0.6 million. Property and equipment transferred had an aggregate net book value of $18.6 million resulting in an impairment charge of $16.0 million, inclusive of a $0.4 million impairment associated with discontinued operations. As part of this transaction and upon satisfaction of certain conditions, Tiger extended the forbearance period to December 9, 2016.

The second restructuring event occurred on December 12, 2016 when Pelican acquired the Aly Senior Obligations from Tiger. As the new holder of the Aly Senior Obligations, Pelican further extended the forbearance period for the obligations to January 31, 2017, provided the Company was successful in completing the third and final restructuring event on or before such date. |

| 10 |

| Table of Contents |

| Effective January 31, 2017, the final restructuring event occurred and the Recapitalization was completed which resulted in the following: | |

|

|

|

| · | an exchange of certain of the Company’s outstanding obligations (namely, Aly Operating redeemable preferred stock, Aly Centrifuge redeemable preferred stock, Aly Centrifuge subordinated debt and its contingent payment liability) for approximately 10% of our common stock, or 7,111,981 common shares, on a fully diluted basis; |

| · | an exchange of certain amendments to the Aly Senior Obligations (namely, a $16.1 million principal reduction, removal of restrictive covenants and extended maturity of payment obligations) for shares of our Series A convertible preferred stock which represents approximately 80% of our common stock, or 53,628,842 common shares, on a fully diluted basis (liquidation preference of $16.1 million or $1,000 per share); and |

| · | the formation of a new credit agreement with Pelican (consisting of a $5.1 million term loan and $1.0 million revolving credit facility) with an extended maturity date of December 31, 2018. |

The Recapitalization had a significant impact to our capital structure and to our consolidated financial statements and there was a significant dilutive effect to those shareholders who held common stock immediately before the transaction was completed. The Recapitalization has been accounted for in accordance with ASC 470, including (i) the exchange of debt and equity securities accounted for as a troubled debt restructuring and (ii) the issuance of preferred shares in exchange for the extinguishment of debt and other liabilities and for the issuance of a new credit facility.

Troubled Debt Restructuring

Except for the Pelican exchange, each exchange was accounted for as a troubled debt restructuring (“TDR”) since an equity interest in the Company was issued to fully satisfy each debt. A gain on TDR is recognized for the excess of the carrying amount of the debt over the fair value of each equity interest granted. The impact of the Recapitalization includes a “gain on the extinguishment of debt and other liabilities” from the debtors of Aly Centrifuge subordinated debt and the contingent payment liability and a “gain on the extinguishment of redeemable preferred stock” from the holders of Aly Operating redeemable preferred stock and Aly Centrifuge redeemable preferred stock. The share price of common stock as of January 31, 2017 of $0.12 per share was used as the basis of fair value for each equity interested granted.

The impact of the TDR is as follows:

| Extinguishment of Debt and Other Liabilities. The exchange of subordinated debt and contingent payment liability for common stock resulted in a gain of $2.4 million, or $0.36 per share, on the condensed consolidated statement of operations for the three months ended March 31, 2017 and was recorded as an “Issuance of common stock in exchange for the extinguishment of debt and other liabilities” on the condensed consolidated statement of changes in stockholders’ equity (deficit) for the three months ended March 31, 2017. The table below summarizes stock issued and the resulting gain for each extinguishment: |

| ||||||

|

|

| ||||||

| Gain on the Extinguishment of Debt and Other Liabilities | |||||||

|

|

|

|

| ||||

|

|

| Common |

|

| Gain Included in | ||

|

|

| Stock |

|

| Other Expense | ||

| Debt and Other Liabilities Extinguished |

| Issued |

|

| (Income) | ||

|

|

|

|

|

|

|

| |

| Subordinated debt and accrued interest of $1.5 million |

|

|

|

|

| ||

| and $0.3 million, respectively |

|

| 1,200,000 |

|

| $1.6 million | |

|

|

|

|

|

|

|

|

|

| Contingent payment liability of $0.8 million |

|

| 457,494 |

|

| $0.8 million | |

| Extinguishment of Redeemable Preferred Stock. Represents the exchange of Aly Operating redeemable preferred stock and Aly Centrifuge redeemable preferred stock for common stock resulting in a gain of $14.4 million, or $2.14 per share, and recorded as an “Issuance of common stock in exchange for the extinguishment of redeemable preferred stock” on the condensed consolidated statement of changes in stockholders’ equity (deficit) for the three months ended March 31, 2017. The table below summarizes stock issued and the resulting gain for each extinguishment: | |||||||

|

| |||||||

| Gain on the Extinguishment of Redeemable Preferred Stock | |||||||

|

|

|

|

|

|

| ||

|

|

| Common |

|

| Gain Included in |

| |

|

| Stock |

|

| Additional |

| ||

| Redeemable Preferred Stock and Other Obligations |

| Issued |

|

| Paid-in-Capital |

| |

|

|

|

|

|

|

|

| |

| Aly Centifuge preferred and accrued dividends of $8.9 |

|

|

|

|

| ||

| million and $1.2 million, respectively |

|

| 3,039,516 |

|

| $9.8 million | |

|

|

|

|

|

|

|

|

|

| Aly Operating preferred and accrued dividends of $4.0 |

|

|

|

|

|

| |

| million and $0.9 million, respectively |

|

| 2,414,971 |

|

| $4.6 million | |

On January 31, 2017, we issued 7,111,981 shares of our common stock to the former holders of Aly Operating redeemable preferred stock, Aly Centrifuge redeemable preferred stock, Aly Centrifuge subordinated debt, and liability for contingent payment in exchange for the above mentioned extinguishments in connection with our TDR.

Credit Facility Restructuring

Given the nature of the related party relationship between the Company and Pelican, the extinguishment of our Aly Senior Obligations was accounted for as a capital transaction whereby we issued Series A convertible preferred stock in exchange for the extinguishment of our Aly Senior Obligations and the issuance of a new credit facility which resulted in a gain on the extinguishment of debt and other liabilities calculated as the amount above the estimated fair value of the equity interest granted. The share price of common stock as of January 31, 2017 of $0.12 per share was used as the basis of fair value for the equity interested granted.

The impact of the exchange and extinguishment of our Aly Senior Obligations is as follows:

| Old Credit Facility. The partial extinguishment and exchange of our Aly Senior Obligations ($16.1 million principal reduction) for shares of our Series A convertible preferred stock resulted in a gain of $9.7 million which is recorded as an “Issuance of preferred shares in exchange for the extinguishment of debt and other liabilities - Pelican” on the condensed consolidated statement of changes in stockholders’ equity (deficit) for the three months ended March 31, 2017. The components of the Aly Senior Obligations are as follows (in thousands): | ||||

|

| ||||

| Aly Senior Obligations as of January 31, 2017 | ||||

|

|

|

|

| |

| Debt and Other Liabilities Extinguished |

| Amount |

| |

| Credit facility |

| $ | 17,772 |

|

| Accrued fees and interest on credit facility |

|

| 1,414 |

|

| Capital lease obligations |

|

| 1,930 |

|

| Accrued interest on capital lease obligations |

|

| 26 |

|

| Line of credit - Pelican |

|

| 500 |

|

| Total |

| $ | 21,642 |

|

|

|

|

|

|

|

| New Credit Facility. Our new credit agreement with Pelican consists of a $5.1 million term loan and $0.5 million outstanding under a revolving credit facility (which was subsequently amended to $5.0 million and $0.8 million, respectively, as of June 30, 2017 in addition to $0.3 million outstanding under a delayed draw term loan with Pelican) completing the full extinguishment of our old credit facility. | ||||

On January 31, 2017, we issued 16,092 shares of our Series A convertible preferred stock to Pelican in exchange for the above mentioned $16.1 million reduction of the Aly Senior Obligations.

| 12 |

| Table of Contents |

Controlling Shareholder – Pelican

As mentioned above, Pelican purchased our Aly Senior Obligations from Tiger for $5.1 million as a part of the Recapitalization. Effective January 31, 2017, the Recapitalization was completed and resulted in the following:

|

| · | Pelican’s contribution of approximately $16.1 million of the Aly Senior Obligations into shares of Series A convertible preferred stock that represents approximately 80% of our common stock, or 53,628,842 common shares, on a fully diluted basis. The preferred shares carried a liquidation preference of $16.1 million upon issuance. |

|

| · | Amendment of the Company’s credit agreement acquired by Pelican into a new credit agreement (consisting of a $5.1 million term loan and $1.0 million revolving credit arrangement) with an extended maturity date of December 31, 2018. |

On January 31, 2017 upon completion of the Recapitalization, Pelican had the power to vote the substantial majority of the Company’s outstanding common stock. Currently six of our board members and all four of our executive officers hold an ownership interest in Pelican.

On May 23, 2017, in consideration of the increase in the revolving credit facility and the extension of the final maturity date, the Company agreed to issue Pelican an amendment fee of 1,200 shares of our Series A convertible preferred stock.

Other Related Party Transactions

Tim Pirie, who was appointed to our board of directors on March 3, 2015, was one of the sellers of United to us in April 2014. Part of the acquisition price was payable in contingent consideration of which $0.9 million was paid in 2015. Of that amount, approximately $0.1 million was attributable to Mr. Pirie. We did not make any contingent payments during 2016. As of December 31, 2016, we estimated the fair value of future contingent payments to be $0.8 million of which approximately $0.2 million would be attributable to Mr. Pirie. On January 31, 2017, in connection with the Recapitalization, the aggregate contingent payment liability was converted into 457,494 shares of the Company’s common stock of which Mr. Pirie controls all of the voting rights to 326,834 shares.

As part of the acquisition price of United, the sellers also received Aly Centrifuge redeemable preferred stock. On January 31, 2017, the outstanding Aly Centrifuge redeemable preferred stock and accrued PIK dividends were converted into 3,039,517 shares of the Company’s common stock of which Mr. Pirie controls all of the voting rights to 593,815 shares.

Professional Fees - Recapitalization

During 2016, we recorded $0.2 million of expenses for professionals engaged by our former lender, Wells Fargo, whom the Company was required to pay under the terms of our credit facility. On December 12, 2016, these fees were assumed by Pelican and, on January 31, 2017, included within the Aly Senior Obligations refinanced in connection with the Recapitalization.

Discontinued Operations

On October 26, 2016, we abandoned the operations of Evolution, our directional drilling and MWD business, as a part of the Recapitalization. The abandonment of these operations meets the criteria established for recognition as discontinued operations under generally accepted accounting principles in U.S. GAAP.

| 13 |

| Table of Contents |

The following table summarizes the components of loss from discontinued operations, net of income taxes included in the condensed consolidated statements of operations (in thousands):

|

|

| For the Three Months Ended June 30, |

|

| For the Six Months Ended June 30, |

| ||||||||||

|

|

| 2016 |

|

| 2015 |

|

| 2016 |

|

| 2015 |

| ||||

|

|

| (unaudited) |

|

| (unaudited) |

| ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

| Revenue |

| $ | 72 |

|

| $ | 926 |

|

| $ | 252 |

|

| $ | 2,860 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operating expenses |

|

| 26 |

|

|

| 895 |

|

|

| 128 |

|

|

| 2,740 |

|

| Depreciation and amortization |

|

| 172 |

|

|

| 196 |

|

|

| 344 |

|

|

| 391 |

|

| Selling, general and administrative expenses |

|

| 65 |

|

|

| 537 |

|

|

| 159 |

|

|

| 1,049 |

|

| Reduction in value of assets |

|

| 1,255 |

|

|

| - |

|

|

| 1,255 |

|

|

| - |

|

| Total expenses |

|

| 1,518 |

|

|

| 1,628 |

|

|

| 1,886 |

|

|

| 4,180 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loss from discontinued operations |

|

| (1,446 | ) |

|

| (702 | ) |

|

| (1,634 | ) |

|

| (1,320 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest expense, net |

|

| 1 |

|

|

| - |

|

|

| 1 |

|

|

| 1 |

|

| Loss from discontinued operations before income taxes |

|

| (1,447 | ) |

|

| (702 | ) |

|

| (1,635 | ) |

|

| (1,321 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income tax benefit |

|

| (190 | ) |

|

| (48 | ) |

|

| (253 | ) |

|

| (82 | ) |

| Loss from discontinued operations, net of income taxes |

| $ | (1,257 | ) |

| $ | (654 | ) |

| $ | (1,382 | ) |

| $ | (1,239 | ) |

In connection with the Recapitalization and the abandonment of the Evolution assets, we recorded an[AHH2] impairment of property and equipment totaling $1.3 million during the three months ended June 30, 2016 included in the line item “Reduction in value of assets” in the above table. The value remaining for property and equipment, intangibles and goodwill associated with these discontinued operations was reduced to zero on October 26, 2016 upon the execution of the transaction with Tiger.

The following summarizes the assets and liabilities associated with discontinued operations as of June 30, 2016 and December 31, 2015 (in thousands):

|

|

| June 30, 2016 |

|

| December 31, 2015 |

| ||

|

|

| (unaudited) |

|

|

|

| ||

| Current assets |

| $ | 64 |

|

| $ | 222 |

|

| Property and equipment, net |

|

| 508 |

|

|

| 1,933 |

|

| Intangible assets, net |

|

| 793 |

|

|

| 1,004 |

|

| Goodwill |

|

| 264 |

|

|

| 264 |

|

| Other assets |

|

| 3 |

|

|

| 5 |

|

| Total assets |

|

| 1,632 |

|

|

| 3,428 |

|

|

|

|

|

|

|

|

|

|

|

| Current liabilities |

|

| 277 |

|

|

| 436 |

|

| Deferred tax liabilities |

|

| 512 |

|

|

| 754 |

|

| Other liabilities |

|

| 14 |

|

|

| 21 |

|

| Total liabilities |

|

| 803 |

|

|

| 1,211 |

|

|

|

|

|

|

|

|

|

|

|

| Net assets |

| $ | 829 |

|

| $ | 2,217 |

|

By December 31, 2016, the abandonment of these operations and sell-off of the remaining assets was completed with approximately $0.2 million of remaining liabilities assumed by the continuing operations of the Company.

2017 Stock Option Plan

Effective April 4, 2017, the 2017 Stock Option Plan (the “2017 Plan”) was approved by the board of directors. On April 4, we granted approximately 16.9 million common shares under the 2017 Plan which was the maximum amount authorized. The option contract term is 10 years and the exercise price is $0.10. The options vested and became exercisable immediately upon grant. The Company is in the process of determining the value of these options.

NOTE 3 — REDUCTION IN VALUE OF ASSETS AND OTHER CHARGES

During the three months and six months ended June 30, 2016, the Company incurred a reduction in value of assets of $0.5 million and $0.8 million, respectively. The Company did not incur any reduction in value of assets charges during the three and six months ended June 30, 2015.

The components of reduction in value of assets are as follows (in thousands):

|

|

| For the Three Months Ended June 30, |

|

| For the Six Months Ended June 30, |

| ||||||||||

|

|

| 2016 |

|

| 2015 |

|

| 2016 |

|

| 2015 |

| ||||

|

|

| (Unaudited) |

|

| (Unaudited) |

| ||||||||||

| Reduction in value of property and equipment - disposals |

| $ | - |

|

| $ | - |

|

| $ | 300 |

|

| $ | - |

|

| Reduction in value of intangibles |

|

| 543 |

|

|

| - |

|

|

| 543 |

|

|

| - |

|

| Total reduction in value of assets |

| $ | 543 |

|

| $ | - |

|

| $ | 843 |

|

| $ | - |

|

Reduction in Value of Property and Equipment – Disposals

During the six months ended June 30, 2016, the Company recorded a loss on the disposal of property and equipment of $0.3 million when the Company sold idle and underutilized equipment and vehicles with a net book value of $0.8 million for cash proceeds of approximately $0.5 million. Due to the depressed market for oilfield services, these assets were sold for proceeds significantly less than the net book value resulting in higher losses than normal. These assets were sold within the basket of permitted asset sales, as defined in our credit facility, and the Company used the proceeds to fund working capital needs created by the significant deterioration in the industry throughout 2015.

Reduction in Value of Intangibles

During the three months ended June 30, 2016, the Company recorded a $0.5 million reduction in an intangible associated with a non-compete which management determined was non-enforceable. As of June 30, 2016, this intangible was recorded with no value on the condensed consolidated balance sheet. As of December 31, 2015, the non-compete was recorded at $0.7 million on the consolidated balance sheet.

Professional Fees – Recapitalization

During the three and six months ended June 30, 2016, in connection with forbearance agreements and other negotiations with its former lender, Wells Fargo, and in connection with the Recapitalization, the Company recorded an aggregate of approximately $10,000 and $0.1 million in charges, primarily for professional fees, which are included in selling, general and administrative expenses on the condensed consolidated statements of operations.

Severance Expense – Operational Restructuring

During the three months ended June 30, 2016 and 2015, the Company recorded $0.5 million and approximately $95,000 in charges relating to severance due to the significant downturn in the industry. In 2016, we ceased making cash severance payments due to our limited liquidity and we do not know when or if we will be able to satisfy the remaining outstanding severance claims. As such, there was an accrued severance liability balance of $0.5 million as of June 30, 2016 which is included in accounts payable and accrued expenses on the condensed consolidated balance sheet. As of December 31, 2015, an accrued severance liability of $0.1 is included in accrued expenses on the consolidated balance sheet.

| 15 |

| Table of Contents |

NOTE 4 — LONG-LIVED ASSETS

Property and Equipment

Major classifications of property and equipment are as follows (in thousands):

|

|

| June 30, 2016 |

|

| December 31, 2015 |

| ||

|

|

| (unaudited) |

|

|

| |||

|

|

|

|

|

|

|

| ||

| Machinery and equipment |

| $ | 53,798 |

|

| $ | 53,677 |

|

| Vehicles, trucks and trailers |

|

| 4,582 |

|

|

| 5,699 |

|

| Office furniture, fixtures and equipment |

|

| 544 |

|

|

| 544 |

|

| Leasehold improvements |

|

| 213 |

|

|

| 213 |

|

| Buildings |

|

| 212 |

|

|

| 212 |

|

|

|

|

| 59,349 |

|

|

| 60,345 |

|

|

|

|

|

|

|

|

|

|

|

| Less: Accumulated depreciation and amortization |

|

| (10,149 | ) |

|

| (8,758 | ) |

|

|

|

| 49,200 |

|

|

| 51,587 |

|

|

|

|

|

|

|

|

|

|

|

| Assets not yet placed in service |

|

| 16 |

|

|

| 202 |

|

| Property and equipment, net |

| $ | 49,216 |

|

| $ | 51,789 |

|

See “Note 3 – Reduction in Value of Assets and Other Charges” for further discussion on asset disposals during the three and six months ended June 30, 2016 and 2015.

Depreciation and amortization expense related to property and equipment for the three months ended June 30, 2016 and 2015 was $1.0 million and $1.1 million, respectively. Depreciation and amortization expense related to property and equipment for the six months ended June 30, 2016 and 2015 was $2.1 million and $2.2 million, respectively.

Intangible Assets

Intangible assets consist of the following (in thousands):

|

|

| Customer Relationships |

|

| Tradename |

|

| Non-Compete |

|

| Supply Agreements |

|

| Total |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

| As of June 30, 2016 (unaudited): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

| Cost |

| $ | 5,322 |

|

| $ | 2,174 |

|

| $ | 492 |

|

| $ | 1,686 |

|

| $ | 9,674 |

|

| Less: Accumulated amortization |

|

| (1,633 | ) |

|

| (639 | ) |

|

| (361 | ) |

|

| (931 | ) |

|

| (3,564 | ) |

| Net book value |

| $ | 3,689 |

|

| $ | 1,535 |

|

| $ | 131 |

|

| $ | 755 |

|

| $ | 6,110 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| As of December 31, 2015: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cost |

| $ | 5,322 |

|

| $ | 2,174 |

|

| $ | 1,651 |

|

| $ | 1,686 |

|

| $ | 10,833 |

|

| Less: Accumulated amortization |

|

| (1,367 | ) |

|

| (531 | ) |

|

| (806 | ) |

|

| (720 | ) |

|

| (3,424 | ) |

| Net book value |

| $ | 3,955 |

|

| $ | 1,643 |

|

| $ | 845 |

|

| $ | 966 |

|

| $ | 7,409 |

|

Amortization expense in each of the three-month periods ended June 30, 2016 and 2015 was approximately $0.4 million. Amortization expense in each of the six-month periods ended June 30, 2016 and 2015 was approximately $0.8 million.

See further discussion of reduction in value of intangibles during the three and six months ended June 30, 2016 and 2015 in “Note 3 – Reduction in Value of Assets and Other Charges” and “Note 2 –Recent Developments and Subsequent Events” within the Discontinued Operations heading.

| 16 |

| Table of Contents |

NOTE 5 — LONG-TERM DEBT

Credit Facility: Term Loan, Delayed Draw Term Loan, and Revolving Credit Facility

Our primary credit facility with Wells Fargo consisted of a term loan, a delayed draw term loan, and a revolving credit facility (“Credit Facility”, as amended). Obligations under the Credit Facility were as follows:

|

| · | Term loan – In 2014, our original principal balance on the term loan was $25.0 million; this loan required principal payments each quarter of $1.3 million. |

|

| · | Delayed draw term loan – In 2014, our original availability under the delayed draw term loan was $5.0 million; the full availability of the loan was reached in May 2015 and beginning in June 2015 the principal balance of $5.0 million required scheduled principal payments each quarter of $0.3 million. |

|

| · | Revolving credit facility – In 2014, our original availability under the revolving credit facility was $5.0 million; however, after subsequent amendments, our availability was reduced to $1.0 million as of December 31, 2015 and then to zero as of December 31, 2016. There were no outstanding borrowings under the revolving credit facility as of June 30, 2016 and December 31, 2015. |

Borrowings under the Credit Facility were subject to interest at the annual base rate at the greater of:

|

| (i) | the Wells Fargo’s Prime Rate, plus a margin of 1.75%, |

|

| (ii) | the Federal Funds Rate plus 0.5%, plus a margin of 1.75% or |

|

| (iii) | the one-month LIBOR rate on such day plus 1.00%, plus a margin of 1.75%. |

Beginning in July 2016, our rate increased to the default rate of 7.25% in connection with the subsequent amendments and forbearance agreements.

The obligations under the Credit Facility were guaranteed by all of our subsidiaries and secured by substantially all of our assets. The credit agreement contained customary events of default and covenants including restrictions on our ability to incur additional indebtedness, make capital expenditures, pay dividends or make other distributions, grant liens and sell assets.

Effective September 30, 2015, we entered into an amendment to the Credit Facility ("Amendment"). In connection with the execution of the Amendment, we used the proceeds of $3.4 million from a private offering to make the regularly scheduled principal payment of $1.5 million due on September 30, 2015 and to make a prepayment of $1.9 million on the term loan.

The Amendment modified multiple components of the Credit Facility including, but not limited to, the terms listed below. The Amendment:

|

| (i) | waived our covenant default as of June 30, 2015; |

|

| (ii) | deferred all further principal payments on outstanding borrowings under the Credit Facility until March 31, 2017; |

|

| (iii) | revised certain financial covenants to facilitate our compliance with such covenants during the downturn in the oilfield services industry; and, |

|

| (iv) | reduced the size of the revolving credit facility to $1.0 million. |

Due to the significant downturn in the oilfield services industry throughout 2015, as of December 31, 2015, we were not in compliance with certain financial covenants set forth in our Credit Facility due to our poor financial results.

On March 31, 2016, we completed the execution and delivery of a forbearance agreement and amendment to the Credit Facility. Among other provisions, the lenders agreed to forbear from exercising their remedies under the Credit Facility until the earlier of July 10, 2016 or the date on which forbearance was terminated due to specified events, including (i) the occurrence of other defaults under the Credit Facility, (ii) our failure to hire an independent financial advisor prior to April 10, 2016 or (iii) our failure to present a detailed plan for asset sales or equity capital acceptable to the lenders yielding net cash proceeds to us of at least $2.5 million by May 25, 2016. We hired an independent financial advisor and such advisor commenced the engagement prior to the deadline of April 10, 2016. In conjunction with agreeing to forbear from exercising their remedies under the Credit Facility, the lenders reduced the revolving credit portion of the Credit Facility to zero thereby eliminating our ability to borrow additional funds under the Credit Facility.

| 17 |

| Table of Contents |

On May 13, 2016, we further amended the Credit Facility and the forbearance agreement related to such facility to increase our basket of permitted asset sales to $0.6 million in any calendar year provided that any proceeds from permitted asset sales be deposited in a blocked deposit account with Wells Fargo. We also acknowledged that we were unable to comply with certain financial covenants as of March 31, 2016.

On August 5, 2016, we entered into a new agreement with Wells Fargo, the Limited Forbearance Agreement, in which Wells Fargo agreed to forbear from exercising their remedies under the credit agreement until August 31, 2016, conditioned upon the following, among other items: (i) hiring a Chief Restructuring Officer (“CRO”) on terms acceptable to the lender; (ii) having the CRO provide an initial cash forecast budget prior to August 10, 2016 and weekly updates thereafter; (iii) not incurring a variance of more than 10% from the cash flow budgets; and, (iv) paying accrued interest monthly effective July 21, 2016 at the default rate specified in the Credit Facility. As mandated, effective August 5, 2016, our board selected Chris Quinn to serve as CRO of the Company. On October 5, 2016, Wells Fargo extended the forbearance period until October 19, 2016.

On October 26, 2016, in connection with the Recapitalization, the Aly Senior Obligations, which included the Credit Facility and the outstanding equipment financing and capital leases in favor of Wells Fargo and Well Fargo Equipment Finance, respectively, were acquired by Tiger. Simultaneously, we entered into the Third Limited Forbearance Agreement which extended the forbearance period to December 9, 2016 and reduced the Aly Senior Obligations in the amount of $2.0 million, conditioned upon the following, among other items: (i) Tiger entering into an assignment agreement with Pelican; (ii) Pelican providing $500,000 of unsecured working capital financing to the Company pending the closing; and, (iii) the Company transferring to Tiger certain excess equipment and vehicles which the Company was not utilizing and did not consider as necessary for its operations. The Company recorded a debt modification fee of $0.6 million in connection with the execution of the Third Limited Forbearance Agreement.

Effective December 12, 2016, the Aly Senior Obligations were acquired by Pelican. See further discussion in “Note 2 – Recent Developments and Subsequent Events”.

Subordinated Note Payable

On August 15, 2014, we completed a bulk equipment purchase for total consideration of $10.3 million of which $2.0 million was in the form of a subordinated note payable (“Subordinated Note Payable”).

On March 18, 2015, the outstanding Subordinated Note Payable was amended to extend the final maturity date to June 30, 2017 and to increase the interest rate to 10% per annum. Subsequent to an aggregate principal and interest payment of approximately $0.6 million on March 31, 2015, additional payments of interest and principal were not required until June 30, 2017. The Subordinated Note Payable was generally subordinated in right of payment to our indebtedness to its lenders.

In connection with the Recapitalization, the Subordinated Note Payable was converted into 1,200,000 common shares of the Company. This conversion was accounted for as a trouble debt restructuring, see further details in “Note 2 – Recent Developments and Subsequent Events”. As of January 31, 2017, there were no further obligations due under the Subordinated Note Payable.

Equipment Financing and Capital Leases

We finance the purchase of certain vehicles and equipment using long-term equipment loans and using non-cancelable capital leases. Repayment occurs over the term of the loan or lease, typically three to five years, in equal monthly installments which include principal and interest.

Effective June 30, 2016, the Company entered into an amendment for each capital lease outstanding with Wells Fargo Equipment Finance, aggregating $1.9 million, whereby the maturity date was extended by six months and principal payments suspended for a period of six months.

Effective October 26, 2016, our equipment financing and capital leases with Wells Fargo Equipment Finance were included in the Aly Senior Obligations which were acquired by Tiger, then subsequently acquired on December 12, 2016 by Pelican. See further discussion in “Note 2 – Recent Developments and Subsequent Events”.

In January 2017, in order to reduce our debt service obligations, we returned certain underutilized and idle vehicles under capital leases with a net book value of $0.1 million to the lessor in exchange for the release of all outstanding obligations, aggregating to approximately $0.1 million, resulting in a reduction in value of assets of approximately $38,000.

As of January 31, 2017, we had one remaining capital lease with a balance of approximately $9,000 which was assumed by the continuing operations of the Company in connection with our discontinued operations effective December 31, 2016.

| 18 |

| Table of Contents |

Deferred Loan Costs

Costs incurred to obtain financing are capitalized and amortized on a straight-line basis over the term of the loan, which approximates the effective interest method. The amortization of these costs is classified within interest expense on the accompanying condensed consolidated statements of operations and was approximately $0.1 million in each of the three-month periods ended June 30, 2016 and 2015 and approximately $0.2 million in each of the six-month periods ended June 30, 2016 and 2015.

During the fourth quarter of 2016, in connection with various amendments to our credit facility and in connection with the Recapitalization, we incurred an aggregate charge of $0.1 million, classified within interest expense, to write-off all remaining unamortized deferred loan costs. There were no new deferred loan costs recorded in connection with the Recapitalization.

As a result of the adoption of Accounting Standards Update ("ASU") 2015-03, “Simplifying the Presentation of Debt Issuance Costs” on January 1, 2016, the Company reclassified debt issuance costs of $0.2 million and retrospectively reclassified debt issuance costs of $0.4 million as a reduction in the carrying amount of the related Credit Facility as of June 30, 2016 and December 31, 2015, respectively.

Deferred loan costs and accumulated amortization were $1.0 million and $0.8 million, respectively, as of June 30, 2016. Deferred loan costs and accumulated amortization were $1.0 million and $0.6 million, respectively, as of December 31, 2015.

Long-term debt consists of the following (in thousands):

|

|

| June 30, 2016 |

|

| December 31, 2015 |

| ||||||||||

|

|

| Current |

|

| Long-Term |

|

| Current |

|

| Long-Term |

| ||||

|

|

| (Unaudited) |

|

|

|

|

|

|

| |||||||

| Credit facility |

|

|

|

|

|

|

|

|

|

|

|

| ||||

| Term loan |

| $ | 15,573 |

|

| $ | - |

|

| $ | 15,573 |

|

| $ | - |

|

| Delayed draw term loan |

|

| 4,500 |

|

|

| - |

|

|

| 4,500 |

|

|

| - |

|

| Subordinated note payable |

|

| 1,500 |

|

|

| - |

|

|

| - |

|

|

| 1,500 |

|

| Equipment financing and capital leases |

|

| 696 |

|

|

| 1,365 |

|

|

| 683 |

|

|

| 1,685 |

|

|

|

|

| 22,269 |

|

|

| 1,365 |

|

|

| 20,756 |

|

|

| 3,185 |

|

| Less: Deferred loan costs, net |

|

| (230 | ) |

|

| - |

|

|

| (403 | ) |

|

| - |

|

| Total |

| $ | 22,039 |

|

| $ | 1,365 |

|

| $ | 20,353 |

|

| $ | 3,185 |

|

As of June 30, 2016 and December 31, 2015, we had approximately $2.1 million and $2.4 million outstanding under equipment financing and capital leases, respectively. The gross amount of equipment held under capital leases and accumulated amortization of that same equipment was approximately $3.5 million and $1.0 million, respectively, as of December 31, 2015. There were no additions or disposals of equipment held under capital lease during the six months ended June 30, 2015.

NOTE 6 — REDEEMABLE PREFERRED STOCK