Exhibit 13.1

CIVISTA BANCSHARES, INC 2020 Annual report

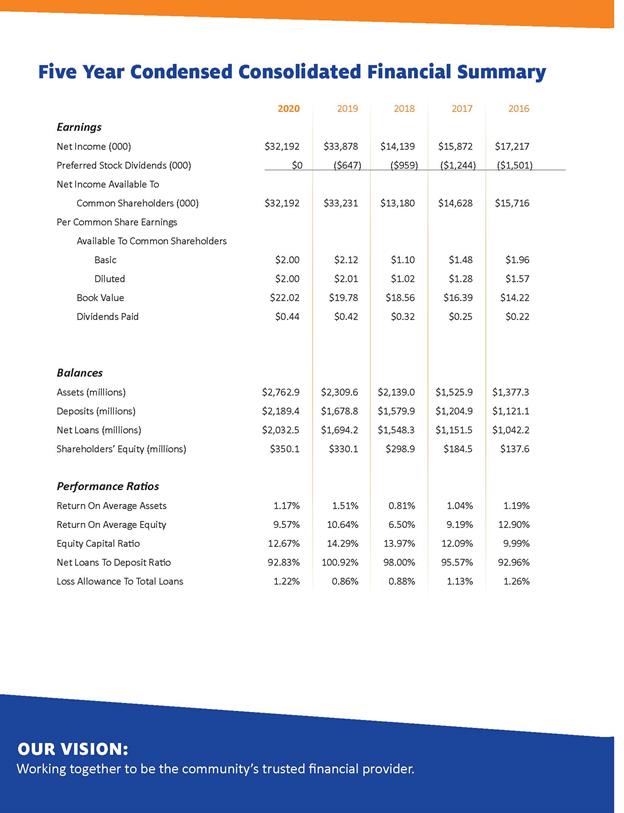

Five Year Condensed Consolidated Financial Summary 2020 2019 2018 2017 2016 $32,192 $33,878 $14,139 $15,872 $17,217 $0 ($647) ($959) ($1,244) ($1,501) $32,192 $33,231 $13,180 $14,628 $15,716 $2.00 $2.00 $22.02 $0.44 Net Income (000) Preferred Stock Dividends (000) Net Income Available To Common Shareholders (000) Per Common Share Earnings Available To Common Shareholders Basic Diluted Book Value Dividends Paid $2,762.9 $2,189.4 $2,032.5 $350.1 1.17% 9.57% 12.67% 92.83% 1.22% $2.12 $2.01 $19.78 $0.42 $2,309.6 $1,678.8 $1,694.2 $330.1 1.51% 10.64% 14.29% 100.92% 0.86% $1.10 $1.02 $18.56 $0.32 Balances Assets (millions) Deposits (millions) Net Loans (millions) Shareholders’ Equity (millions) Performance Ratios Return On Average Assets Return On Average Equity Equity Capital Ratio Net Loans To Deposit Ratio Loss Allowance To Total Loans $2,139.0 $1,579.9 $1,548.3 $298.9 0.81% 6.50% 13.97% 98.00% 0.88% $1.48 $1.28 $16.39 $0.25 $1,525.9 $1,204.9 $1,151.5 $184.5 1.04% 9.19% 12.09% 95.57% 1.13% $1.96 $1.57 $14.22 $0.22 $1,377.3 $1,121.1 $1,042.2 $137.6 1.19% 12.90% 9.99% 92.96% 1.26% OUR VISION: Working together to be the community’s trusted financial provider.

Five Year Condensed Consolidated Financial Summary 2020 2019 2018 2017 2016 $32,192 $33,878 $14,139 $15,872 $17,217 $0 ($647) ($959) ($1,244) ($1,501) $32,192 $33,231 $13,180 $14,628 $15,716 $2.00 $2.00 $22.02 $0.44 Net Income (000) Preferred Stock Dividends (000) Net Income Available To Common Shareholders (000) Per Common Share Earnings Available To Common Shareholders Basic Diluted Book Value Dividends Paid $2,762.9 $2,189.4 $2,032.5 $350.1 1.17% 9.57% 12.67% 92.83% 1.22% $2.12 $2.01 $19.78 $0.42 $2,309.6 $1,678.8 $1,694.2 $330.1 1.51% 10.64% 14.29% 100.92% 0.86% $1.10 $1.02 $18.56 $0.32 Balances Assets (millions) Deposits (millions) Net Loans (millions) Shareholders’ Equity (millions) Performance Ratios Return On Average Assets Return On Average Equity Equity Capital Ratio Net Loans To Deposit Ratio Loss Allowance To Total Loans $2,139.0 $1,579.9 $1,548.3 $298.9 0.81% 6.50% 13.97% 98.00% 0.88% $1.48 $1.28 $16.39 $0.25 $1,525.9 $1,204.9 $1,151.5 $184.5 1.04% 9.19% 12.09% 95.57% 1.13% $1.96 $1.57 $14.22 $0.22 $1,377.3 $1,121.1 $1,042.2 $137.6 1.19% 12.90% 9.99% 92.96% 1.26% OUR VISION: Working together to be the community’s trusted financial provider.

Dear Shareholder, The year 2020 proved to be challenging and unlike any other in our lifetime. COVID-19 created perhaps the greatest health threat ever, costing many lives and infecting millions of people. States issued stay-at-home orders and required some businesses to shut down or operate under restricted hours. Unemployment surged. Yet through it all, Civista employees rose to the challenge, working closely with many of our customers who have been impacted by the COVID-19 pandemic. To help our customers that had been impacted by COVID-19, the bank rolled out a number of financial assistance programs for those facing financial hardship in April 2020. These included consumer, mortgage and commercial loan payment deferral programs and the continued funding of businesses through conventional loans and through the SBA Payroll Protection Program (PPP), a government stimulus program for small businesses. Customer demand for the PPP product, in particular, was high and Civista employees worked countless hours and many long days to open accounts and to provide funding to support community businesses across our footprint. The bank made over 2,300 PPP loans totaling over $259.1 million. Nearly all of these loans were made to small businesses. These businesses employed over 36,000 employees. In addition, our front-line team helped many consumers navigate digital banking services for the first time and answer thousands of stimulus check deposit inquiries. Likewise, our Civista Wealth Management officers helped investors stay their course in what was a turbulent second quarter. Customers and employees also adapted to a new way of doing business. The safety and well-being of our customers and employees was, and is, our top priority. At the onset of the pandemic, to help do our part in slowing the spread of the virus, Civista limited lobby services to ‘by appointment only’ at all of our locations and we restricted employee movement between our offices. In April 2020, we had approximately 70% of our employees working from home and, as of today, we still have over 50% of our employees working remotely. As we shifted our work model, Civista was committed to minimizing service disruptions to our customers. We expanded the hours of our Customer Care Center so that we are now available 24/7, 365 days a year to assist you. We created Civista Curbside Banking, which provides a limited-contact option for customers to conduct select non-cash transactions from the comfort of their vehicles. We invested in video chat and electronic signature technology that allows customers to interact with our bankers from the safety of their homes and offices. And we continue to offer and invest in our digital services such as mobile banking, online banking and digital wallet. These products provide convenient, easy, safe and healthy options for customers to bank with us. As the COVID-19 pandemic persists, we have kept a very close eye on the bank’s capital and liquidity and at this time we believe that we are in a very strong position. We are frequently running stress test scenarios to evaluate capital and liquidity. Those results have been very favorable even in a severe stress test environment. Financially, the bank had one of its most successful years on record. We earned net income of $32.2 million, or $2.00 per diluted share, compared to $33.2 million, or $2.01 per diluted share, in 2019. We also recorded the highest pre-tax, pre-provision net income1 of $47.2 million in our 136-year history. Paycheck protection program Business Helped 2300+ funds secured $259 million employees supported curbside service 1 call 419.625.4123. “202 was a year to discover new potential and find new ways to do things; the ability to think outside the box will serve us better as we move forward. It’s the change in thinking that is the innovative benefit.”-Carl Kessler, information Technology

Dear Shareholder, The year 2020 proved to be challenging and unlike any other in our lifetime. COVID-19 created perhaps the greatest health threat ever, costing many lives and infecting millions of people. States issued stay-at-home orders and required some businesses to shut down or operate under restricted hours. Unemployment surged. Yet through it all, Civista employees rose to the challenge, working closely with many of our customers who have been impacted by the COVID-19 pandemic. To help our customers that had been impacted by COVID-19, the bank rolled out a number of financial assistance programs for those facing financial hardship in April 2020. These included consumer, mortgage and commercial loan payment deferral programs and the continued funding of businesses through conventional loans and through the SBA Payroll Protection Program (PPP), a government stimulus program for small businesses. Customer demand for the PPP product, in particular, was high and Civista employees worked countless hours and many long days to open accounts and to provide funding to support community businesses across our footprint. The bank made over 2,300 PPP loans totaling over $259.1 million. Nearly all of these loans were made to small businesses. These businesses employed over 36,000 employees. In addition, our front-line team helped many consumers navigate digital banking services for the first time and answer thousands of stimulus check deposit inquiries. Likewise, our Civista Wealth Management officers helped investors stay their course in what was a turbulent second quarter. Customers and employees also adapted to a new way of doing business. The safety and well-being of our customers and employees was, and is, our top priority. At the onset of the pandemic, to help do our part in slowing the spread of the virus, Civista limited lobby services to ‘by appointment only’ at all of our locations and we restricted employee movement between our offices. In April 2020, we had approximately 70% of our employees working from home and, as of today, we still have over 50% of our employees working remotely. As we shifted our work model, Civista was committed to minimizing service disruptions to our customers. We expanded the hours of our Customer Care Center so that we are now available 24/7, 365 days a year to assist you. We created Civista Curbside Banking, which provides a limited-contact option for customers to conduct select non-cash transactions from the comfort of their vehicles. We invested in video chat and electronic signature technology that allows customers to interact with our bankers from the safety of their homes and offices. And we continue to offer and invest in our digital services such as mobile banking, online banking and digital wallet. These products provide convenient, easy, safe and healthy options for customers to bank with us. As the COVID-19 pandemic persists, we have kept a very close eye on the bank’s capital and liquidity and at this time we believe that we are in a very strong position. We are frequently running stress test scenarios to evaluate capital and liquidity. Those results have been very favorable even in a severe stress test environment. Financially, the bank had one of its most successful years on record. We earned net income of $32.2 million, or $2.00 per diluted share, compared to $33.2 million, or $2.01 per diluted share, in 2019. We also recorded the highest pre-tax, pre-provision net income1 of $47.2 million in our 136-year history. Paycheck protection program Business Helped 2300+ funds secured $259 million employees supported curbside service 1 call 419.625.4123. “2020 was a year to discover new potential and find new ways to do things; the ability to think outside the box will serve us better as we move forward. It’s the change in thinking that is the innovative benefit.”-Carl Kessler, information Technology

Although we have not experienced any significant losses due to COVID-19 closures, higher unemployment, loan modification deferrals and the loss of income for some of our business clients prompted the bank to provide $10.1 million to our loan loss allowance, which was $9.1 million higher than the previous year. Some of our more significant accomplishments in 2020 included an increase of $348.5 million in our loan portfolio, which included $217.3 million in PPP loans that were still on the books at year end. Removing the effect of the PPP loans, the loan portfolio grew by $131.2 million, or 7.7%, with growth coming across our entire footprint. We had strong growth in commercial real estate and commercial real estate construction loans. Construction activity continues to be vibrant, particularly in the metro markets that we serve. On the consumer side, we experienced record loan production from our residential mortgage team, who generated over $304 million in secondary market loans, which created an additional $5.9 million more income than the previous year. Residential mortgage rates continue to remain at historic low levels making this a great time to purchase or refinance your home. I am so proud of our lending efforts, as it is these dollars that we lend out to customers, who in turn invest back into our communities to make them a stronger and better place to live and work. Our loan portfolio balance was $2.0 billion at the end of the year. Deposit balances grew by $510.6 million, or 30.4%, and our deposit portfolio balance was $2.2 billion at the end of the year. Nearly all of the growth occurred in core deposit accounts with non-interest demand deposits growing $208.3 million. Non-interest income was $28.2 million in 2020, an increase of $5.7 million, or 25.6%. In addition to the previously-mentioned strong residential mortgage production, we had increased earnings in interchange fees, treasury management and wealth management. Other accomplishments in 2020 included the relocation and opening of a new full service branch in Willard, Ohio. The new location is more centrally located in the heart of the community and is much more accessible for our customers. We also launched several financial literacy programs, through our ‘Bank at Work’ program and through our website (www.civista.bank), with the creation of the Civista Learning Vault. The Learning Vault offers quick and easy online learning modules to help customers build their financial knowledge so that they can make more informed financial decisions. We created our first Diversity, Equity and Inclusion Council with members consisting of employees from all departments throughout the bank. The council will help ensure that all voices are heard, valued and embraced. By listening and respecting different perspectives, we will all gain a better understanding of one another and who we are as a company. The bank is committed to providing a welcoming, equitable environment with opportunities for engagement, employment and business relationships regardless of a person’s age, gender, ethnicity, national origin, race, religious beliefs, sexual orientation or military status. The board of directors approved a $13.5 million share repurchase authorization in May 2020. This is an important part of our capital management plan and provides a method to efficiently deploy our capital. Although approved, management temporarily suspended the use of the plan when COVID-19 started in an effort to preserve capital until we had a chance to evaluate what effect the pandemic might have on our balance sheet and particularly our loan portfolio. Once we had a better understanding and comfort level of our capital position and loan portfolio under a severe stress environment, we resumed share repurchases late in the third quarter. We repurchased 154,947 shares for $2 million at a weighted average price of $12.94 per share. Prior to this plan, we repurchased 672,000 shares for $11.4 million at a weighted average price of $16.90 per share. The previous plan expired in early 2020. As we move into 2021, we continue to invest in technology to make the organization more efficient, to make it easier to do business with us, and to enhance the overall customer experience. Several notable projects underway include a digital banking project that is the single largest technology upgrade in the company’s history. This project will enhance and improve most of our digital banking products and services including mobile banking, online banking, bill pay, electronic statement delivery and our treasury management services. We will have the ability to open deposit accounts online and streamline our in-branch new account process. We plan to roll this product out by mid-summer. Also underway is a customer communication project that will improve the format, design and content of customer statements, invoices and notices. We introduced the update of our checking and residential mortgage loan statements in 2020 and work continues on additional commercial and consumer statements and notices. “Team growth...Our team members had to learn new tasks quickly. They did extremely well! They not only learned new tasks, they took ownership!” – Seanna Miller, Customer Care Center 2020

The new statements provide more information and the design and format is easier to read. Civista continues to invest in the communities that we serve. We donate significant dollars to local schools, civic and non- profit organizations throughout our footprint each year. Our employees donate their time serving in leadership roles or as active volunteers at hundreds of organizations where we live and work. In 2020 more than ever, our communities needed support and our employees were there to help. We take great pride in being a community leader and in the commitment that we make to our communities. In closing, I am very pleased with our accomplishments and I am very proud to work with a group of employees who are so committed to each other and to our communities. As I have stated in the past, our goal is to remain an independent community bank and I believe we earn that independence through our actions and results each and every day. I am confident that through our disciplined approach to managing Civista and our long-term focus on driving shareholder value that we will continue to produce positive results. As always, please read your proxy and vote your shares in the company. The annual shareholders meeting is April 20, 2021 at 10 AM. Due to the COVID-19 pandemic, the meeting will be held from our 100 East Water Street, Sandusky, Ohio headquarters. Information including webcast registration instructions and the dial-in number is available at www.CIVB.com. Warmest Regards, Dennis G. Shaffer CEO and President 1 Additional information can be found in the Five-Year Selected Consolidated Financial Data section. Executive Leadership Team Lance A. Morrison, Richard J. Dutton, Paul J. Stark, Donna M. Jaskolski, Dennis G. Shaffer, Charles A. Parcher, John A. Betts, Todd A. Michel Dennis G. Shaffer CEO and President, Civista Bancshares, Inc. and Civista Bank John A. Betts Senior Vice President Richard J. Dutton Senior Vice President Officers Donna M. Waltz-Jaskolski Senior Vice President Todd A. Michel Senior Vice President Lance A. Morrison Senior Vice President, General Counsel and Corporate Secretary Charles A. Parcher Senior Vice President Paul J. Stark Senior Vice President “...Teaching customers who never used our digital services like online or mobile banking gain a little more confidence in how to set up bill pay or make a transfer.” – Gary Weaver, Retail Banking 2020

The new statements provide more information and the design and format is easier to read. Civista continues to invest in the communities that we serve. We donate significant dollars to local schools, civic and non- profit organizations throughout our footprint each year. Our employees donate their time serving in leadership roles or as active volunteers at hundreds of organizations where we live and work. In 2020 more than ever, our communities needed support and our employees were there to help. We take great pride in being a community leader and in the commitment that we make to our communities. In closing, I am very pleased with our accomplishments and I am very proud to work with a group of employees who are so committed to each other and to our communities. As I have stated in the past, our goal is to remain an independent community bank and I believe we earn that independence through our actions and results each and every day. I am confident that through our disciplined approach to managing Civista and our long-term focus on driving shareholder value that we will continue to produce positive results. As always, please read your proxy and vote your shares in the company. The annual shareholders meeting is April 20, 2021 at 10 AM. Due to the COVID-19 pandemic, the meeting will be held from our 100 East Water Street, Sandusky, Ohio headquarters. Information including webcast registration instructions and the dial-in number is available at www.CIVB.com. Warmest Regards, Dennis G. Shaffer CEO and President 1 Additional information can be found in the Five-Year Selected Consolidated Financial Data section. Executive Leadership Team Lance A. Morrison, Richard J. Dutton, Paul J. Stark, Donna M. Jaskolski, Dennis G. Shaffer, Charles A. Parcher, John A. Betts, Todd A. Michel Dennis G. Shaffer CEO and President, Civista Bancshares, Inc. and Civista Bank John A. Betts Senior Vice President Richard J. Dutton Senior Vice President Officers Donna M. Waltz-Jaskolski Senior Vice President Todd A. Michel Senior Vice President Lance A. Morrison Senior Vice President, General Counsel and Corporate Secretary Charles A. Parcher Senior Vice President Paul J. Stark Senior Vice President “...Teaching customers who never used our digital services like online or mobile banking gain a little more confidence in how to set up bill pay or make a transfer.” – Gary Weaver, Retail Banking 2020

Board Of Directors Thomas A. Depler Partner, Poland, Depler & Shepherd Co., LPA Julie A. Mattlin Principal and Owner, DKMG Consulting, LLC James O. Miller Chairman of the Board, Civista Bancshares, Inc. and Civista Bank Dennis E. Murray, Jr. Lead Director Partner, Murray & Murray Co., LPA Allen R. Nickles, CPA, CFE, FCPA, CFF, CICA Of Counsel, Payne, Nickles & Company Civista Bancshares, Inc. M. Patricia Oliver Retired Partner, Tucker Ellis, LLP Founder, The Oliver Consulting Group William F. Ritzmann Former Chairman of the Board, United Community Bancorp and United Community Bank Dennis G. Shaffer CEO and President, Civista Bancshares, Inc. and Civista Bank Harry Singer President and CEO, Sandusco, Inc. and ICM Distributing Company, Inc. Daniel J. White CEO, Norwalk Furniture Corp John O. Bacon President and CEO, The Mack Iron Works Company Barry W. Boerger Self-Employed Grain Farm Operator Thomas A. Depler Partner, Poland, Depler & Shepherd Co., LPA Blythe A. Friedley Owner/President, Friedley & Co. Agency, Inc. Julie A. Mattlin Principal and Owner, DKMG Consulting, LLC Elmer G. McLaughlin Former President and CEO, United Community Bancorp and United Community Bank James O. Miller Chairman of the Board, Civista Bancshares, Inc. and Civista Bank Dennis E. Murray, Jr. Partner, Murray & Murray Co., LPA Allen R. Nickles, CPA, CFE, FCPA, CFF, CICA Of Counsel, Payne, Nickles & Company M. Patricia Oliver Retired Partner, Tucker Ellis, LLP Founder, The Oliver Consulting Group William F. Ritzmann Former Chairman of the Board, United Community Bancorp and United Community Bank Dennis G. Shaffer CEO and President, Civista Bancshares, Inc. and Civista Bank Harry Singer President and CEO, Sandusco, Inc. and ICM Distributing Company, Inc. Daniel J. White CEO, Norwalk Furniture Corp Gerald B. Wurm President, Wurm’s Woodworking Co. and Creative Plastics International Directors Emeritus Civista Bancshares, Inc. and Civista Bank James D. Heckelman Retired, Founder of Dan-Mar Co., Inc. David A. Voight Former Chairman of the Board and Former President and CEO, Civista Bancshares, Inc. and Civista Bank “Many employees faced hardships with no school, daycare, babysitter, etc. I think Civista did a wonderful job to accommodate the employees so we did not have to choose between work and family…. Civista put the safety of our employees and customers first.” – Steffani McVety, Consumer Lending

ANNUAL REPORT

CONTENTS

|

|

1 |

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

6 |

|

|

|

|

|

|

19 |

|

|

|

|

|

|

Financial Statements |

|

|

|

Management’s Report on Internal Control over Financial Reporting |

|

23 |

|

|

24 |

|

|

Report of Independent Registered Public Accounting Firm on Financial Statements |

|

25 |

|

|

28 |

|

|

|

29 |

|

|

|

30 |

|

|

|

31 |

|

|

|

32 |

|

|

|

34 |

This page left blank intentionally.

Five-Year Selected Consolidated Financial Data

(Amounts in thousands, except per share data)

|

|

|

Year ended December 31, |

|

|||||||||||||||||

|

|

|

2020 |

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|

2016 |

|

|||||

|

Statements of income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total interest and dividend income |

|

$ |

99,865 |

|

|

$ |

98,054 |

|

|

$ |

73,677 |

|

|

$ |

58,594 |

|

|

$ |

53,567 |

|

|

Total interest expense |

|

|

10,138 |

|

|

|

12,954 |

|

|

|

7,570 |

|

|

|

4,092 |

|

|

|

3,308 |

|

|

Net interest income |

|

|

89,727 |

|

|

|

85,100 |

|

|

|

66,107 |

|

|

|

54,502 |

|

|

|

50,259 |

|

|

Provision (credit) for loan losses |

|

|

10,112 |

|

|

|

1,035 |

|

|

|

780 |

|

|

|

— |

|

|

|

(1,300 |

) |

|

Net interest income after provision for loan losses |

|

|

79,615 |

|

|

|

84,065 |

|

|

|

65,327 |

|

|

|

54,502 |

|

|

|

51,559 |

|

|

Net gain (loss) on sale of securities |

|

|

94 |

|

|

|

32 |

|

|

|

(413 |

) |

|

|

12 |

|

|

|

19 |

|

|

Other noninterest income |

|

|

28,088 |

|

|

|

22,411 |

|

|

|

18,544 |

|

|

|

16,322 |

|

|

|

16,113 |

|

|

Total noninterest income |

|

|

28,182 |

|

|

|

22,443 |

|

|

|

18,131 |

|

|

|

16,334 |

|

|

|

16,132 |

|

|

Total noninterest expense |

|

|

70,665 |

|

|

|

66,947 |

|

|

|

66,679 |

|

|

|

48,604 |

|

|

|

43,855 |

|

|

Income before federal income taxes |

|

|

37,132 |

|

|

|

39,561 |

|

|

|

16,779 |

|

|

|

22,232 |

|

|

|

23,836 |

|

|

Federal income tax expense |

|

|

4,940 |

|

|

|

5,683 |

|

|

|

2,640 |

|

|

|

6,360 |

|

|

|

6,619 |

|

|

Net income |

|

$ |

32,192 |

|

|

$ |

33,878 |

|

|

$ |

14,139 |

|

|

$ |

15,872 |

|

|

$ |

17,217 |

|

|

Preferred stock dividends and discount accretion |

|

|

— |

|

|

|

647 |

|

|

|

959 |

|

|

|

1,244 |

|

|

|

1,501 |

|

|

Net income available to common shareholders |

|

$ |

32,192 |

|

|

$ |

33,231 |

|

|

$ |

13,180 |

|

|

$ |

14,628 |

|

|

$ |

15,716 |

|

|

Per common share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income available to common shareholders (basic) |

|

|

2.00 |

|

|

|

2.12 |

|

|

|

1.10 |

|

|

|

1.48 |

|

|

|

1.96 |

|

|

Net income available to common shareholders (diluted) |

|

|

2.00 |

|

|

|

2.01 |

|

|

|

1.02 |

|

|

|

1.28 |

|

|

|

1.57 |

|

|

Dividends declared |

|

|

0.44 |

|

|

|

0.42 |

|

|

|

0.32 |

|

|

|

0.25 |

|

|

|

0.22 |

|

|

Book value |

|

|

22.02 |

|

|

|

19.78 |

|

|

|

18.56 |

|

|

|

16.39 |

|

|

|

14.22 |

|

|

Average common shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

16,129,875 |

|

|

|

15,652,881 |

|

|

|

11,971,786 |

|

|

|

9,906,856 |

|

|

|

8,010,399 |

|

|

Diluted |

|

|

16,129,875 |

|

|

|

16,851,740 |

|

|

|

13,855,706 |

|

|

|

12,352,616 |

|

|

|

10,950,961 |

|

|

Year-end balances: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, net |

|

$ |

2,032,474 |

|

|

$ |

1,694,203 |

|

|

$ |

1,548,262 |

|

|

$ |

1,151,527 |

|

|

$ |

1,042,201 |

|

|

Securities |

|

|

384,887 |

|

|

|

379,970 |

|

|

|

368,385 |

|

|

|

245,309 |

|

|

|

209,919 |

|

|

Total assets |

|

|

2,762,918 |

|

|

|

2,309,557 |

|

|

|

2,138,954 |

|

|

|

1,525,857 |

|

|

|

1,377,263 |

|

|

Deposits |

|

|

2,189,398 |

|

|

|

1,678,764 |

|

|

|

1,579,893 |

|

|

|

1,204,923 |

|

|

|

1,121,103 |

|

|

Borrowings |

|

|

183,341 |

|

|

|

274,601 |

|

|

|

245,226 |

|

|

|

123,082 |

|

|

|

106,852 |

|

|

Shareholders’ equity |

|

|

350,108 |

|

|

|

330,126 |

|

|

|

298,898 |

|

|

|

184,461 |

|

|

|

137,616 |

|

|

Average balances: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, net |

|

$ |

1,953,472 |

|

|

$ |

1,598,991 |

|

|

$ |

1,261,568 |

|

|

$ |

1,095,956 |

|

|

$ |

1,011,683 |

|

|

Securities |

|

|

386,703 |

|

|

|

372,886 |

|

|

|

273,998 |

|

|

|

234,249 |

|

|

|

213,496 |

|

|

Total assets |

|

|

2,754,708 |

|

|

|

2,241,111 |

|

|

|

1,742,823 |

|

|

|

1,526,387 |

|

|

|

1,441,717 |

|

|

Deposits |

|

|

2,078,454 |

|

|

|

1,689,801 |

|

|

|

1,341,860 |

|

|

|

1,236,663 |

|

|

|

1,210,283 |

|

|

Borrowings |

|

|

288,551 |

|

|

|

208,932 |

|

|

|

167,752 |

|

|

|

101,880 |

|

|

|

79,391 |

|

|

Shareholders’ equity |

|

|

336,461 |

|

|

|

318,306 |

|

|

|

217,371 |

|

|

|

172,763 |

|

|

|

133,445 |

|

1

Five-Year Selected Ratios

|

|

|

Year ended December 31, |

|

|||||||||||||||||

|

|

|

2020 |

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|

2016 |

|

|||||

|

Net interest margin (1) |

|

|

3.70 |

% |

|

|

4.31 |

% |

|

|

4.21 |

% |

|

|

4.01 |

% |

|

|

3.93 |

% |

|

Return on average total assets |

|

|

1.17 |

|

|

|

1.51 |

|

|

|

0.81 |

|

|

|

1.04 |

|

|

|

1.19 |

|

|

Return on average shareholders’ equity |

|

|

9.57 |

|

|

|

10.64 |

|

|

|

6.50 |

|

|

|

9.19 |

|

|

|

12.90 |

|

|

Dividend payout ratio |

|

|

22.00 |

|

|

|

19.81 |

|

|

|

29.09 |

|

|

|

16.89 |

|

|

|

11.22 |

|

|

Average shareholders’ equity as a percent of average total assets |

|

|

12.21 |

|

|

|

14.20 |

|

|

|

12.47 |

|

|

|

11.32 |

|

|

|

9.26 |

|

|

Net loan charge-offs (recoveries) as a percent of average total loans |

|

|

(0.01 |

) |

|

|

(0.00 |

) |

|

|

0.02 |

|

|

|

0.02 |

|

|

|

(0.02 |

) |

|

Allowance for loan losses as a percent of loans at year-end |

|

|

1.22 |

|

|

|

0.86 |

|

|

|

0.88 |

|

|

|

1.13 |

|

|

|

1.26 |

|

|

Shareholders’ equity as a percent of total year-end assets |

|

|

12.67 |

|

|

|

14.29 |

|

|

|

13.97 |

|

|

|

12.09 |

|

|

|

9.99 |

|

|

|

(1) |

Calculated on a tax-equivalent basis using an effective tax rate of 21% for 2020, 2019 and 2018 and 35% for 2017 and 2016. |

Reconciliation of Non-GAAP Measures

Use of Non-GAAP Measures

To supplement the financial measures prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), we use a non-GAAP financial measure. The reconciliation of this non-GAAP financial measure to the most directly comparable financial measure calculated and presented in accordance with GAAP is shown in the table below. This non-GAAP financial measure should not be considered in isolation from, or as a substitute for or superior to, the financial measure reported in accordance with GAAP. Moreover, this non-GAAP financial measure has limitations in that it does not reflect all the items associated with the operations of the business as determined in accordance with GAAP. Other companies may calculate similarly titled non-GAAP financial measures differently than us, limiting the usefulness of those measures for comparative purposes.

We believe that this non-GAAP financial measure is useful to investors in their assessment of operating performance and the valuation of the Company. Pre-Tax Pre-Provision Net Income (PTPP), is a non-GAAP supplemental measure that is used by management to evaluate and measure the Company’s performance. Management believes that this measure provides users of the Company’s financial information with a more meaningful view of the performance of the Company’s core earnings potential excluding credit related expenses.

|

|

|

Year ended December 31, |

|

|||||||||||||||||

|

(In thousands) |

|

2020 |

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|

2016 |

|

|||||

|

Net income (GAAP) |

|

$ |

32,192 |

|

|

$ |

33,878 |

|

|

$ |

14,139 |

|

|

$ |

15,872 |

|

|

$ |

17,217 |

|

|

Add back: income tax expense |

|

|

4,940 |

|

|

|

5,683 |

|

|

|

2,640 |

|

|

|

6,360 |

|

|

|

6,619 |

|

|

Add back: provision for loan losses |

|

|

10,112 |

|

|

|

1,035 |

|

|

|

780 |

|

|

|

— |

|

|

|

(1,300 |

) |

|

Pre-tax, pre-provision net income |

|

$ |

47,244 |

|

|

$ |

40,596 |

|

|

$ |

17,559 |

|

|

$ |

22,232 |

|

|

$ |

22,536 |

|

2

S hare holder Return Performance

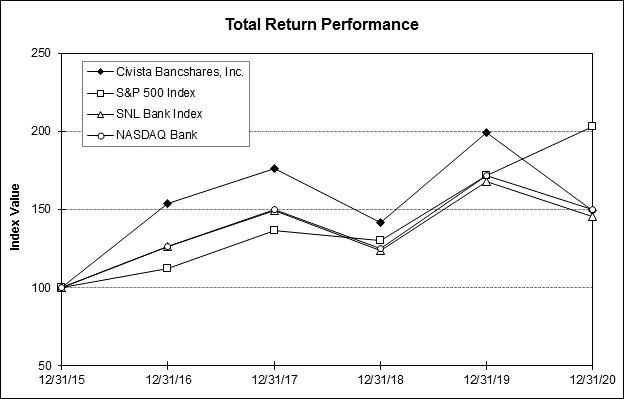

Set forth below is a line graph comparing the five-year cumulative return of the common shares of Civista Bancshares, Inc. (ticker symbol CIVB), based on an initial investment of $100 on December 31, 2015 and assuming reinvestment of dividends, with the cumulative return of the Standard & Poor’s 500 Index, the NASDAQ Bank Index and the SNL Bank Index. The comparative indices were obtained from SNL Securities and NASDAQ.

Annual Report on Form 10-K

A copy of the Company’s Annual Report on Form 10-K, as filed with the Securities and Exchange Commission, will be furnished, free of charge, to shareholders, upon written request to Lance A. Morrison, Secretary of Civista Bancshares, Inc., 100 East Water Street, Sandusky, Ohio 44870.

3

This page left blank intentionally.

4

Common S hares and S hareholder Matters

The common shares of Civista Bancshares, Inc. (“CBI”) trade on The NASDAQ Capital Market under the symbol “CIVB”. As of February 25, 2021, there were 15,847,061 common shares outstanding and held by approximately 1,563 shareholders of record (not including the number of persons or entities holding stock in nominee or street name through various brokerage firms).

The Company paid quarterly dividends on its common shares in the aggregate amounts of $0.44 per share and $0.42 per share in 2020 and 2019, respectively. The Company presently anticipates continuing to pay quarterly dividends in the future at similar levels, subject to compliance with applicable restrictions on the payment of dividends as discussed in the “Liquidity and Capital Resources” section of the Management’s Discussion and Analysis of Financial Condition and Results of Operations and in Note 19 to the Consolidated Financial Statements.

General Development of Business

(Amounts in thousands)

CBI was organized under the laws of the State of Ohio on February 19, 1987 and is a registered financial holding company under the Gramm-Leach-Bliley Financial Modernization Act of 1999, as amended. CBI and its subsidiaries are sometimes referred to together as the “Company”. The Company’s office is located at 100 East Water Street, Sandusky, Ohio. The Company had total consolidated assets of $2,762,918 at December 31, 2020.

CIVISTA BANK (“Civista”), owned by CBI since 1987, opened for business in 1884 as The Citizens National Bank. In 1898, Civista was reorganized under Ohio banking law and was known as The Citizens Bank and Trust Company. In 1908, Civista surrendered its trust charter and began operation as The Citizens Banking Company. The name Civista Bank was introduced during the first quarter of 2015 to solidify our dual Citizens/Champaign brand and distinguish ourselves from the many other banks using the “Citizens” name in our existing and prospective markets. Civista maintains its main office at 100 East Water Street, Sandusky, Ohio and operates branch banking offices in the following Ohio communities: Sandusky (2), Norwalk (2), Berlin Heights, Huron, Port Clinton, Castalia, New Washington, Shelby (2), Willard, Greenwich, Plymouth, Shiloh, Akron, Dublin, Plain City, Russells Point, Urbana (2), West Liberty, Quincy, Dayton(3), Beachwood, and in the following Indiana communities: Lawrenceburg (3), Aurora, West Harrison, Milan, Osgood and Versailles. Civista also operates loan production offices in Westlake, Ohio and Fort Mitchell, Kentucky. Civista accounted for 99.8% of the Company’s consolidated assets at December 31, 2020.

FIRST CITIZENS INSURANCE AGENCY INC. (“FCIA”) was formed to allow the Company to participate in commission revenue generated through its third party insurance agreement. Assets of FCIA were less than one percent of the Company’s consolidated assets as of December 31, 2020.

WATER STREET PROPERTIES, INC. (“WSP”) was formed to hold properties repossessed by CBI subsidiaries. WSP accounted for less than one percent of the Company’s consolidated assets as of December 31, 2020.

FC REFUND SOLUTIONS, INC. (“FCRS”) was formed during 2012 to facilitate payment of individual state and federal income tax refunds. The operations of FCRS were discontinued June 30, 2019 as a result of inactivity. The discontinued operations of FCRS will not affect the Company’s participation in the tax refund processing program.

FIRST CITIZENS INVESTMENTS, INC. (“FCI”) is wholly-owned by Civista and holds and manages its securities portfolio. The operations of FCI are located in Wilmington, Delaware.

FIRST CITIZENS CAPITAL LLC (“FCC”) is wholly-owned by Civista and holds inter-company debt that is eliminated in consolidation. The operations of FCC are located in Wilmington, Delaware.

CIVB RISK MANAGEMENT, INC. (“CRMI”) is a wholly-owned captive insurance company formed in 2017 which insures against certain risks unique to the operations of the Company and its subsidiaries and for which insurance may not be currently available or economically feasible in today's insurance marketplace. Assets of CRMI were less than one percent of the Company’s consolidated assets as of December 31, 2020.

5

Acquisition of United Community Bancorp

On September 14, 2018, CBI completed the acquisition by merger of United Community Bancorp (“UCB”) in a stock and cash transaction for aggregate consideration of approximately $117,344. Immediately following the merger, UCB’s banking subsidiary, United Community Bank, was merged into CBI’s banking subsidiary, Civista Bank. At the time of the merger, UCB had total assets of $537,875, including $298,319 in loans, and $475,944 in deposits. As a result of the merger, we acquired eight offices of UCB in the Indiana communities of Lawrenceburg (3), Aurora, West Harrison, Milan, Osgood and Versailles and a loan production office in Fort Mitchell, Kentucky.

Management’s Discussion and Analysis of Financial Condition and Results of Operations—As of December 31, 2020 and December 31, 2019 and for the Years Ended December 31, 2020, 2019 and 2018

(Amounts in thousands, except per share data)

General

The following paragraphs more fully discuss the significant highlights, changes and trends as they relate to the Company’s financial condition, results of operations, liquidity and capital resources as of December 31, 2020 and 2019, and during the three-year period ended December 31, 2020. This discussion should be read in conjunction with the Consolidated Financial Statements and Notes to the Consolidated Financial Statements, which are included elsewhere in this report.

Forward-Looking Statements

This report may contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), relating to such matters as financial condition, anticipated operating results, cash flows, business line results, credit quality expectations, prospects for new lines of business, economic trends (including interest rates) and similar matters. Forward-looking statements reflect our expectations, estimates or projections concerning future results or events. These statements are generally identified by the use of forward-looking words or phrases such as “believe,” “belief,” “expect,” “anticipate,” “may,” “could,” “intend,” “intent,” “estimate,” “plan,” “foresee,” “likely,” “will,” “should” or other similar words or phrases. Forward-looking statements are not guarantees of performance and are inherently subject to known and unknown risks, uncertainties and assumptions that are difficult to predict and could cause our actual results, performance or achievements to differ materially from those expressed in or implied by the forward-looking statements. Factors that could cause actual results, performance or achievements to differ from those discussed in the forward-looking statements include, but are not limited to, impacts on our business, financial condition and results of operations resulting from the ongoing COVID-19 pandemic, including government regulations and stimulus programs related thereto: changes in financial markets or national or local economic or political conditions; adverse changes in the real estate market; volatility and direction of market interest rates; the transition away from LIBOR as a reference rate for financial contracts; credit risks of lending activities; operational risks; changes in the allowance for loan losses; legislation or regulatory changes or actions; increases in FDIC insurance premiums and assessments; changes in tax laws; accounting changes; inability to raise additional capital if and when needed in the future; unexpected losses of key management; failure, interruption or breach of security of our communications and information systems or those of our third party service providers; unforeseen litigation; increased competition in our market area; failures to manage growth and/or effectively integrate acquisitions; future revenues of our tax refund program; climate change, natural disasters, acts of war or terrorism, and other external events; and other risks identified from time-to-time in the Company’s other public documents on file with the Securities and Exchange Commission.

The forward-looking statements included in this report are only made as of the date of this report, and we disclaim any obligation to publicly update any forward-looking statement to reflect subsequent events or circumstances, except as required by law.

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements, and the purpose of this section is to secure the use of the safe harbor provisions.

6

Financial Condition

At December 31, 2020, the Company’s total assets were $2,762,918, compared to $2,309,557 at December 31, 2019. The increase in assets is primarily the result of increases in cash and due from financial institutions, securities available for sale, loans held for sale, loans and swap assets. Other factors contributing to the change in assets are discussed in the following sections.

Loans held for sale increased $4,716, or 206.4%, from $2,285 at December 31, 2019 to $7,001 at December 31, 2020. The increase is due to an increase in volume due to refinances as rates have declined. At December 31, 2020, 29 loans totaling $7,001 were held for sale as compared to 15 loans totaling $2,285 at December 31, 2019.

At $2,032,474, net loans increased from December 31, 2019 by 20.0%. The increase in net loans was spread across most segments. Commercial & Agriculture loans increased $206,766, Commercial Real Estate – Owner Occupied loans increased $32,807, Commercial Real Estate - Non-Owner Occupied loans increased $112,850, and Real estate construction loans increased $19,784. The increases in the foregoing loan segments were offset by decreases in Residential Real Estate loans of $20,444, Farm Real Estate loans of $1,012 and Consumer and other loans of $2,219. The increase in Commercial & Agriculture loans is the result of our origination of loans under the Paycheck Protection Program (“PPP”) loans totaling $217,295 at December 31, 2020.

Securities available for sale increased by $4,965, or 1.4%, from $358,499 at December 31, 2019 to $363,464 at December 31, 2020. U.S. Treasury securities and obligations of U.S. government agencies increased $2,092 from $19,601 at December 31, 2019 to $21,693 at December 31, 2020. Obligations of states and political subdivisions available for sale increased by $22,978 from 2019 to 2020. Mortgage-backed securities decreased by $20,105 to total $112,759 at December 31, 2020. The Company continues to utilize letters of credit from the Federal Home Loan Bank (FHLB) to replace maturing securities that were pledged for public entities. As of December 31, 2020, the Company was in compliance with all applicable pledging requirements.

Mortgage-backed securities totaled $112,759 at December 31, 2020 and none were considered unusual or “high risk” securities as defined by regulatory authorities. Of this total, $96,872 consisted of pass-through securities issued by the Federal National Mortgage Association (“FNMA”), Federal Home Loan Mortgage Corporation (“FHLMC”), and Government National Mortgage Association (“GNMA”), and $15,887 of these securities were collateralized by mortgage-backed securities issued or guaranteed by FNMA, FHLMC, or GNMA. The average interest rate of the mortgage-backed securities portfolio at December 31, 2020 was 3.1%. The average maturity at December 31, 2020 was approximately 4.7 years.

Securities available for sale had a fair value at December 31, 2020 of $363,464. This fair value includes unrealized gains of approximately $27,183 and unrealized losses of approximately $35. Net unrealized gains totaled $27,148 on December 31, 2020 compared to net unrealized gains of $16,307 on December 31, 2019. The change in unrealized gains is primarily due to changes in market interest rates. Note 3 to the Consolidated Financial Statements provides additional information on unrealized gains and losses.

Premises and equipment, net of accumulated depreciation, decreased $291 from December 31, 2019 to December 31, 2020. The decrease is the result of new purchases of $1,972, offset by disposals of $10 and depreciation of $2,253.

Accrued interest receivable increased $2,328 or 32.8% from December 31, 2019 to December 31, 2020. The increase is the result of loan modifications consisting of the deferral of principal and/or interest payments, which are the result of the COVID-19 pandemic.

Swap assets increased $12,782 from December 31, 2019 to December 31, 2020. The increase is primarily the result of an increase in volume of swap activity related to our Commercial Real Estate loan growth, as well as increases in volume due to the low rate environment.

Bank owned life insurance (BOLI) increased $977 from December 31, 2019 to December 31, 2020. The difference is the result of increases in the cash surrender value of the underlying insurance policies.

7

Year-end deposit balances totaled $ 2 , 189 , 398 in 20 20 compared to $1, 678 , 764 in 201 9 , an increase of $ 510 , 634 , or 30 . 4 %. Overall, the increase in deposits at December 31, 20 20 compared to December 31, 201 9 included increases in noninterest bearing demand deposits of $ 208 , 256 , or 40 . 6 %, interest bearing demand accounts of $ 108 , 465 , or 36 . 0 %, statement and passbook savings accounts of $ 182 , 915 , or 3 1.1 %, certificate of deposit accounts of $ 1 3 , 224 , or 5 . 8 % , offset by a decrease in individual retirement accounts of $ 2 , 226 , or 4 . 6 %. Average deposit balances for 20 20 were $ 2 , 078 , 454 compared to $1, 689 , 801 for 201 9 , an increase of 2 3 . 0 %. Noninterest bearing deposits averaged $ 739 , 648 for 20 20 , compared to $ 550 , 638 for 201 9 , increasing $ 189 , 010 , or 34 . 3 %. Savings, NOW, and MMDA accounts averaged $ 1,050 , 544 for 20 20 compared to $ 869 , 340 for 201 9 . Average certificates of deposit in creased $ 18 , 439 to total an average balance of $ 2 88 , 262 for 20 20 . The increase in year-to-date average balances was impacted by COVID-19 pandemic as the Company’s participation in originating PPP loans resulted in loan proceeds being deposited by borrowers into deposit accounts at Civista and customer deposits of stimulus checks and unemployment benefits also increased average deposit balance s in 2020.

Borrowings from the FHLB of Cincinnati were $125,000 at December 31, 2020 compared to $226,500 at December 31, 2019, a decrease of $101,500. Additional detail regarding these borrowings can be found in Note 10 and Note 11 to the Consolidated Financial Statements. Short-term FHLB advances decreased $101,500 from December 31, 2019 to December 31, 2020. The decrease is due to a decrease in overnight borrowings.

Civista offers repurchase agreements in the form of sweep accounts to commercial checking account customers. These repurchase agreements totaled $28,914 at December 31, 2020 compared to $18,674 at December 31, 2019. U.S. Treasury securities and obligations of U.S. government agencies maintained under Civista’s control are pledged as collateral for the repurchase agreements. Additional detail related to these repurchase agreements can be found in Note 12 to the Consolidated Financial Statements.

Swap liabilities increased $12,846 from December 31, 2019 to December 31, 2020. The increase is primarily the result of an increase in volume of swap activity related to our Commercial Real Estate loan growth, as well as an increase in the fair value resulting from the low interest rate environment.

Total shareholders’ equity increased $19,982, or 6.1%, during 2020 to $350,108. The change in shareholders’ equity resulted from net income of $32,192, a decrease in the Company’s pension liability, net of tax, of $819, an increase in the fair value of securities available for sale, net of tax, of $8,564 and decreases due to the purchase of treasury shares of $13,454 and dividends on common shares of $7,118, respectively. Additionally, $617 was recognized as stock-based compensation in 2020 in connection with the grant of restricted common shares. For further explanation of these items, see Note 1, Note 15 and Note 16 to the Consolidated Financial Statements. The Company paid $0.44 per common share in dividends in 2020 compared to $0.42 per common share in dividends in 2019. Total outstanding common shares at December 31, 2020 were 15,898,032. Total outstanding common shares at December 31, 2019 were 16,687,542. The decrease in common shares outstanding is the result of the repurchase of 830,755 common shares at an average repurchase price of $16.20. The Company repurchased 672,000 common shares pursuant to a stock repurchase program announced on December 17, 2019, 154,947 common shares pursuant to a stock repurchase program announced on May 4, 2020 and 3,808 common shares surrendered to pay taxes upon vesting of restricted shares. The repurchase plan publicly-announced on December 17, 2019 authorized the Company to repurchase up to 672,000 shares of the Company’s common shares until December 17, 2020. The repurchase plan publicly-announced on May 4, 2020 authorized the Company to repurchase a maximum aggregate value of $13,500 of the Company’s common shares until April 20, 2021. The decrease in common shares outstanding was offset by the grant of 26,979 restricted common shares to certain officers under the Company’s 2014 Incentive Plan and the grant of 14,266 common shares to directors of Civista as a retainer for their service. The ratio of total shareholders’ equity to total assets was 12.7% and 14.3%, at December 31, 2020 and 2019, respectively.

8

Results of Operations

The operating results of the Company are affected by general economic conditions, the monetary and fiscal policies of federal agencies and the regulatory policies of agencies that regulate financial institutions. The Company’s cost of funds is influenced by interest rates on competing investments and general market rates of interest. Lending activities are influenced by the demand for real estate loans and other types of loans, which in turn is affected by the interest rates at which such loans are made, general economic conditions and the availability of funds for lending activities.

The Company’s net income primarily depends on its net interest income, which is the difference between the interest income earned on interest-earning assets, such as loans and securities, and interest expense incurred on interest-bearing liabilities, such as deposits and borrowings. The level of net interest income is dependent on the interest rate environment and the volume and composition of interest-earning assets and interest-bearing liabilities. Net income is also affected by provisions for loan losses, service charges, gains on the sale of assets, other non-interest income, noninterest expense and income taxes.

Comparison of Results of Operations for the Years Ended December 31, 2020 and December 31, 2019

Net Income

The Company’s net income for the year ended December 31, 2020 was $32,192, compared to $33,878 for the year ended December 31, 2019. The change in net income was the result of the items discussed in the following sections.

Net Interest Income

Net interest income for 2020 was $89,727, an increase of $4,627, or 5.4%, from 2019. From 2019 to 2020, average earning assets increased 23.3%, interest income increased $1,811, and interest expense on interest-bearing liabilities decreased $2,816. The Company continually examines its rate structure to ensure that its interest rates are competitive and reflective of the current rate environment in which it competes.

Total interest income increased $1,811 to $99,865 for the year ended December 31, 2020, which is attributable to an increase of $2,805 in interest and fees on loans. This change was the result of an increase in the average balance of loans, accompanied by a lower yield on the portfolio. The average balance of loans increased by $340,497 or 21.1% to $1,953,472 for the year ended December 31, 2020, as compared to $1,612,975 for the year ended December 31, 2019. The loan yield decreased to 4.49% for 2020, from 5.27% in 2019.

Interest on taxable securities decreased $1,225 to $5,359 for the year ended December 31, 2020, compared to $6,584 for the same period in 2019. The average balance of taxable securities decreased $16,353 to $183,721 for the year ended December 31, 2020, as compared to $200,074 for the year ended December 31, 2019. The yield on taxable securities decreased 32 basis points to 3.03% for 2020, compared to 3.35% for 2019. Interest on tax-exempt securities increased $476 to $6,123 for the year ended December 31, 2020, compared to $5,647 for the same period in 2019. The average balance of tax-exempt securities increased $30,170 to $202,982 for the year ended December 31, 2020 as compared to $172,812 for the year ended December 31, 2019. The yield on tax-exempt securities decreased 21 basis points to 4.15% for 2020, compared to 4.36% for 2019.

Total interest expense decreased $2,816 or 21.7% to $10,138 for the year ended December 31, 2020, compared with $12,954 for the same period in 2019. The change in interest expense can be attributed to an increase in the average balance of interest-bearing liabilities and a decrease in the average rate paid. For the year ended December 31, 2020, the average balance of interest-bearing liabilities increased $279,262 to $1,627,357, as compared to $1,348,095 for the year ended December 31, 2019. Interest incurred on deposits decreased by $1,176 to $6,881 for the year ended December 31, 2020, compared to $8,057 for the same period in 2019. The change in deposit expense was due to an increase in the average balance of interest-bearing deposits of $199,643 for the year ended December 31, 2020 as compared to the same period in 2019. In addition, the average rate paid on demand and savings accounts decreased from 0.33% in 2019 to 0.17% in 2020 and the average rate paid on time deposits decreased from 1.92% to 1.76% in 2020. Interest expense incurred on FHLB advances and subordinated debentures decreased 41.0% from 2019. The decrease was due to a $27,896 decrease in average balance from 2019 and a decrease in rate from 2019. The average balance of other borrowings increased $101,295 for the period ended December 31, 2020 as compared to the same period in 2019 as a result of the Company’s borrowings under the Paycheck Protection Program Lending Facility (“PPPLF”) to fund PPP loans.

9

Refer to “Distribution of Assets, Liabilities and Shareholders’ Equity; Interest Rates and Interest Differential” and “Changes in Interest Income and Interest Expense Resulting from Changes in Volume and Changes in Rate” on pages 14 through 16 for further analysis of the impact of changes in interest-bearing assets and liabilities on the Company’s net interest income.

Provision and Allowance for Loan Losses

The following table contains information relating to the provision for loan losses, activity in and analysis of the allowance for loan losses as of and for each of the three years in the period ended December 31.

|

|

|

As of and for year ended December 31, |

|

|||||||||

|

|

|

2020 |

|

|

2019 |

|

|

2018 |

|

|||

|

Net loan charge-offs (recoveries) |

|

$ |

(149 |

) |

|

$ |

(53 |

) |

|

$ |

235 |

|

|

Provision (credit) for loan losses charged to expense |

|

|

10,112 |

|

|

|

1,035 |

|

|

|

780 |

|

|

Net loan charge-offs (recoveries) as a percent of average outstanding loans |

|

|

(0.01 |

)% |

|

|

(0.00 |

)% |

|

|

0.02 |

% |

|

Allowance for loan losses |

|

$ |

25,028 |

|

|

$ |

14,767 |

|

|

$ |

13,679 |

|

|

Allowance for loan losses as a percent of year-end outstanding loans |

|

|

1.22 |

% |

|

|

0.86 |

% |

|

|

0.88 |

% |

|

Impaired loans, excluding purchase credit impaired loans (PCI) |

|

$ |

2,666 |

|

|

$ |

3,597 |

|

|

$ |

2,857 |

|

|

Impaired loans as a percent of gross year-end loans (1) |

|

|

0.13 |

% |

|

|

0.21 |

% |

|

|

0.18 |

% |

|

Nonaccrual and 90 days or more past due loans, excluding PCI |

|

$ |

5,125 |

|

|

$ |

5,599 |

|

|

$ |

5,869 |

|

|

Nonaccrual and 90 days or more past due loans, excluding PCI as a percent of gross year-end loans (1) |

|

|

0.25 |

% |

|

|

0.33 |

% |

|

|

0.38 |

% |

|

(1) |

Nonaccrual loans and impaired loans are defined differently. Some loans may be included in both categories, whereas other loans may only be included in one category. A loan is considered nonaccrual if it is maintained on a cash basis because of deterioration in the borrower’s financial condition, where payment in full of principal or interest is not expected and where the principal and interest have been in default for 90 days, unless the asset is both well-secured and in process of collection. A loan is considered impaired when it is probable that all of the interest and principal due will not be collected according to the terms of the original contractual agreement. |

The Company’s policy is to maintain the allowance for loan losses at a level sufficient to provide for probable losses incurred in the current portfolio. Management believes the analysis of the allowance for loan losses supported a reserve of $25,028 at December 31, 2020. The Company provides for loan losses through regular provisions to the allowance for loan losses as necessary. The amount of the provision is affected by loan charge-offs, recoveries and changes in specific and general allocations required for the allowance for loan losses. A number of factors impact the provisions for loan losses, such as the level of higher risk loans in the portfolio, changes in practices related to loans, changes in collateral values and other factors. We continue to actively manage this process and have provided to maintain the reserve at a level that assures adequate coverage ratios.

Provisions for loan losses totaled $10,112, $1,035 and $780 in 2020, 2019 and 2018, respectively. The Company’s provision for loan losses increased $9,077 during 2020. The increase in the provision was due to an increase in the bank’s qualitative factors, primarily changes in international, national, regional and local conditions, related to the economic shutdown driven by COVID-19 and the ongoing payment deferrals on loans modified under the Coronavirus Aid Relief, and Economic Security Act (“CARES Act”). Economic impacts related to the COVID-19 pandemic include the loss of revenue being experience by our business clients, disruption of supply chains, additional employee costs for businesses due to the pandemic, higher unemployment rates throughout our footprint and a large number of customers requesting payment relief. Our Commercial, Commercial Real Estate and Consumer portfolios have been, and are expected to continue to be impacted the most.

Efforts are continually made to analyze each segment of the loan portfolio and quantify risk to assure that reserves are appropriate for each segment and the overall portfolio. Management specifically evaluates loans that are

10

impaired, which includes restructured loans, to estimate potential loss. This analysis includes a review of the loss migration calculation for all loan categories as well as fluctuations and trends in various risk factors that have occurred within the portfolios’ economic life cycle. The analysis also includes assessment of qualitative factors such as credit trends, unemployment trends, vacancy trends and loan growth. The composition and overall level of the loan portfolio and charge-off activity are also factors used to determine the amount of the allowance for loan losses.

Management analyzes each impaired commercial and commercial real estate loan relationship with a balance of $350 or larger, on an individual basis and when it is in nonaccrual status or when an analysis of the borrower’s operating results and financial condition indicates that underlying cash flows are not adequate to meet its debt service requirements. Loans held for sale and leases are excluded from consideration as impaired. Loans are generally moved to nonaccrual status when 90 days or more past due. Impaired loans or portions thereof are charged-off when deemed uncollectible.

Noninterest Income

Noninterest income increased $5,739, or 25.6%, to $28,182 for the year ended December 31, 2020, from $22,443 for the comparable 2019 period. The increase was primarily due to increases in net gain on sale of securities of $62, net gain on sale of loans of $5,856, ATM/Interchange fees of $416 and swap fees of $943, which were partially offset by decreases in service charges of $1,107, net gain (loss) on equity securities of $178 and tax refund processing fees of $375.

Net gain on sale of securities increased due to security sales. Management, from time to time, will reposition the investment portfolio to match liquidity needs of the Company. Net gain on sale of loans increased primarily as a result of an increase in volume of loans sold. During the twelve-months ended December 31, 2020, 1,575 loans were sold, totaling $304,026. During the twelve-months ended December 31, 2019, 709 loans were sold, totaling $125,796. ATM/Interchange fees increased as a result of increased transaction volume. Swap fees increased due to the volume of swaps originated during the twelve-months ended December 31, 2020 as compared to the same period of 2019. Service charges decreased due to Civista waiving $93 of service fees on deposit accounts related to the COVID-19 pandemic. In addition, overdraft fees decreased during 2020. Net gain (loss) on equity securities decreased as a result of market value decreases. Additionally, the Company processes state and federal income tax refund payments for customers of third-party income tax preparation vendors for which we receive a fee for processing the refund payments. These tax refund processing fees decreased as a result of a decrease in the volume of transactions processed during 2020 as compared to 2019.

Noninterest Expense

Noninterest expense increased $3,718, or 5.6%, to $70,665 for the year ended December 31, 2020, from $66,947 for the comparable 2019 period. The increase was primarily due to increases in compensation expense of $3,324, FDIC assessments of $590 and software maintenance expense of $310, which were partially offset by decreases in equipment expense of $240 and marketing expense of $337.

The increase in compensation expense was due to increased payroll, overtime pay, 401k expenses, payroll taxes and commission and incentive based costs, offset by decreases in employee insurance costs and unemployment taxes. The year-to-date average full time equivalent (FTE) employees were 453.4 at December 31, 2020, an increase of 8.6 FTEs over 2019, which increased payroll and payroll related expenses. Payroll and payroll related expenses also increased due to annual pay increases and increases in commission based costs as the result of increased loan activity. The year-over-year increase in FDIC assessments was attributable to small bank assessment credits applied to the 2019 assessment charges. The increase in software maintenance expense is due to a general increase in software maintenance contracts. The decrease in equipment expense is due to lower equipment repair and maintenance cost. The decrease in marketing expense is due to decreases in both advertising and business promotion expenses, primarily related to the COVID-19 pandemic. Event cancellations and postponed outreach efforts contributed to the decrease as our focus was on communicating changes in operations, safety protocols, alternative delivery channels, and economic relief programs with the safety and financial wellness of our employees and customers in mind.

11

Income Tax Expense

Federal income tax expense was $4,940 in 2020 compared to $5,683 in 2019. Federal income tax expense as a percentage of pre-tax income was 13.3% in 2020 compared to 14.4% in 2019. A lower federal effective tax rate than the statutory rate of 21% in 2020 and 2019 is primarily due to tax-exempt interest income from state and municipal investments, municipal loans, income from BOLI and low income housing credits.

Comparison of Results of Operations for the Years Ended December 31, 2019 and December 31, 2018

Net Income

The Company’s net income for the year ended December 31, 2019 was $33,878, compared to $14,139 for the year ended December 31, 2018. The change in net income was the result of the items discussed in the following sections.

Net Interest Income

Net interest income for 2019 was $85,100, an increase of $18,993, or 28.7%, from 2018. From 2018 to 2019, average earning assets increased 26.9%, interest income increased $24,377, and interest expense on interest-bearing liabilities increased $5,384. The Company continually examines its rate structure to ensure that its interest rates are competitive and reflective of the current rate environment in which it competes. The increase in net interest income is largely due to the UCB acquisition.

Total interest income increased $24,377 to $98,054 for the year ended December 31, 2019, which is attributable to an increase of $20,776 in interest and fees on loans. This change was the result of an increase in the average balance of loans, accompanied by a higher yield on the portfolio. The average balance of loans increased by $338,196 or 26.5% to $1,612,975 for the year ended December 31, 2019, as compared to $1,274,779 for the year ended December 31, 2018. The loan yield increased to 5.27% for 2019, from 5.04% in 2018. The increase in average loan balances and interest and fees on loans is largely due to the UCB acquisition.

Interest on taxable securities increased $1,814 to $6,584 for the year ended December 31, 2019, compared to $4,770 for the same period in 2018. The average balance of taxable securities increased $40,623 to $200,074 for the year ended December 31, 2019, as compared to $159,451 for the year ended December 31, 2018. The yield on taxable securities increased 38 basis points to 3.35% for 2019, compared to 2.97% for 2018. Interest on tax-exempt securities increased $1,671 to $5,647 for the year ended December 31, 2019, compared to $3,976 for the same period in 2018. The average balance of tax-exempt securities increased $58,265 to $172,812 for the year ended December 31, 2019 as compared to $114,547 for the year ended December 31, 2018. The yield on tax-exempt securities decreased 7 basis points to 4.36% for 2019, compared to 4.43% for 2018.

Total interest expense increased $5,384 or 71.1% to $12,954 for the year ended December 31, 2019, compared with $7,570 for the same period in 2018. The change in interest expense can be attributed to an increase in the average balance of interest-bearing liabilities and an increase in the average rate paid. For the year ended December 31, 2019, the average balance of interest-bearing liabilities increased $305,246 to $1,348,095, as compared to $1,042,849 for the year ended December 31, 2018. Interest incurred on deposits increased by $4,299 to $8,057 for the year ended December 31, 2019, compared to $3,758 for the same period in 2018, largely due to the UCB acquisition. The change in deposit expense was due to an increase in the average balance of interest-bearing deposits of $264,066 for the year ended December 31, 2019 as compared to the same period in 2018, largely due to the UCB acquisition. In addition, the average rate paid on demand and savings accounts increased from 0.21% in 2018 to 0.33% in 2019 and the average rate paid on time deposits increased from 1.22% to 1.92% in 2019. Interest expense incurred on FHLB advances and subordinated debentures increased 28.6% from 2018. The increase was due to a $41,294 increase in average balance from 2018 and a 2 basis point increase in rate from 2018.

Refer to “Distribution of Assets, Liabilities and Shareholders’ Equity; Interest Rates and Interest Differential” and “Changes in Interest Income and Interest Expense Resulting from Changes in Volume and Changes in Rate” on pages 14 through 16 for further analysis of the impact of changes in interest-bearing assets and liabilities on the Company’s net interest income.

12

Provision and Allowance for Loan Losses

Management believes the analysis of the allowance for loan losses supported a reserve of $14,767 at December 31, 2019.

Provisions (credits) for loan losses totaled $1,035 and, $780 in 2019 and 2018, respectively. The Company’s provision for loan losses increased $255 during 2019 to support loan growth.

Noninterest Income

Noninterest income increased $4,312, or 23.8%, to $22,443 for the year ended December 31, 2019, from $18,131 for the comparable 2018 period. The increase was primarily due to increases in service charges of $1,187, net gain on sale of securities of $445, net gain on equity securities of $95, net gain on sale of loans of $1,086, ATM/Interchange fees of $1,262 and bank owned life insurance of $289.

Service charges, ATM/Interchange fees and bank owned life insurance income increased primarily due to the Company’s acquisition of UCB during the third quarter of 2018. Net gain (loss) on sale of securities increased as a result of management’s decision to reposition the investment portfolio in 2018, which resulted in losses on the sales. Net gain on equity securities increased as a result of market value adjustments. Net gain on sale of loans increased primarily as a result of an increase in the volume of loans sold and the average loan balance of loans sold.

Noninterest Expense

Noninterest expense increased $268, or 0.4%, to $66,947 for the year ended December 31, 2019, from $66,679 for the comparable 2018 period. The increase was primarily due to increases in compensation expense of $1,857, net occupancy expense of $472, equipment expense of $592, state franchise tax of $473, amortization of intangible assets of $579, ATM expense of $818, marketing expense of $229, software maintenance expense of $387 and other operating expense of $2,340, which were partially offset by decreases in contracted data processing expense of $5,308, FDIC assessments of $398 and professional services expense of $1,385.