UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

MARK ONE

[X] Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the Quarterly Period ended March 31, 2021; or

[ ] Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the transition period from ________ to ________

WORLD HEALTH ENERGY HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 000-30256 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

| 1825 NW Corporate Blvd. Suite 110, Boca Raton, FL | 33431 | |

| (Address of principal executive offices) | Zip Code |

(561) 870-0440

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| N/A | N/A | N/A |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] | |

| Non-accelerated filer | [ ] | Smaller reporting company | [X] | |

| Emerging growth company | [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

As of May 11, 2021, 89,789,407,996 shares of the registrant’s common stock, par value $0.0007 per share, were outstanding.

WORLD HEALTH ENERGY HOLDINGS, INC.

Form 10-Q

March 31, 2021

| i |

WORLD HEALTH ENERGY HOLDINGS, INC.

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

AS OF MARCH 31, 2021

WORLD HEALTH ENERGY HOLDINGS, INC .

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

AS OF MARCH 31, 2021

IN U.S. DOLLARS

TABLE OF CONTENTS

| 2 |

WORLD HEALTH ENERGY HOLDINGS, INC .

CONDENSED CONSOLIDATED BALANCE SHEETS

(U.S. dollars except share and per share data)

| March 31, | December 31, | |||||||

| 2021 | 2020 | |||||||

| Assets | (Unaudited) | |||||||

| Current Assets | ||||||||

| Cash and cash equivalents | 141,868 | 359,949 | ||||||

| Accounts receivable, net | 13,360 | 5,086 | ||||||

| Other current assets | 47,205 | 42,178 | ||||||

| Total Current assets | 202,433 | 407,213 | ||||||

| Right Of Use asset arising from operating lease | 230,761 | - | ||||||

| Long term prepaid expenses | 23,995 | 24,883 | ||||||

| Property and Equipment, Net | 26,270 | 26,054 | ||||||

| Total assets | 483,459 | 458,150 | ||||||

| Liabilities and Shareholders’ Deficit | ||||||||

| Current Liabilities | ||||||||

| Accounts payable | 20,860 | 26,284 | ||||||

| Right Of Use liabilities arising from operating lease | 39,610 | - | ||||||

| Other accounts liabilities | 531,580 | 496,874 | ||||||

| Total current liabilities | 592,050 | 523,158 | ||||||

| Liability for employee rights upon retirement | 133,364 | 104,850 | ||||||

| Long term loan from parent company | 1,812,704 | 1,812,704 | ||||||

| Right Of Use liabilities arising from operating lease | 193,994 | |||||||

| Total liabilities | 2,732,112 | 2,440,712 | ||||||

| Stockholders’ Deficit | ||||||||

| Preferred stock, par $0.0007, 10,000,000 shares authorized, 5,000,000 shares issued and outstanding as of March 31, 2021 and December 31, 2020. | 3,500 | 3,500 | ||||||

| Series B Convertible Preferred stock, par $0.0007, 3,870,000 shares authorized, 3,870,000 shares issued and outstanding as of March 31, 2021 and December 31, 2020. | 2,709 | 2,709 | ||||||

| Common stock, par $0.0007, 110,000,000,000 shares authorized, 89,789,407,996 shares issued and outstanding at March 31, 2021 and December 31, 2020. | 62,852,585 | 62,852,585 | ||||||

| Additional paid-in capital | (63,339,224 | ) | (63,339,224 | ) | ||||

| Foreign currency translation adjustments | (5,495 | ) | (5,495 | ) | ||||

| Accumulated deficit | (1,762,728 | ) | (1,496,637 | ) | ||||

| Total stockholders’ deficit | (2,248,653 | ) | (1,982,562 | ) | ||||

| Total liabilities and stockholders’ deficit | 483,459 | 458,150 | ||||||

The accompanying notes are an integral part of the condensed consolidated financial statements.

| 3 |

WORLD HEALTH ENERGY HOLDINGS, INC .

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(U.S. dollars except share and per share data)

| Three months ended | ||||||||

| March 31 | ||||||||

| 2021 | 2020 | |||||||

| (Unaudited) | ||||||||

| Revenues | 32,649 | 3,516 | ||||||

| Research and development expenses | (172,771 | ) | (99,948 | ) | ||||

| General and administrative expenses | (124,485 | ) | (57,406 | ) | ||||

| Operating loss | (264,607 | ) | (153,838 | ) | ||||

| Financing expenses, net | (1,484 | ) | (9,208 | ) | ||||

| Net loss | (266,091 | ) | (163,046 | ) | ||||

| Comprehensive loss | (266,091 | ) | (163,046 | ) | ||||

| Loss per share (basic and diluted) | (0.00 | ) | (0.00 | ) | ||||

The accompanying notes are an integral part of the condensed consolidated financial statements.

| 4 |

WORLD HEALTH ENERGY HOLDINGS, INC .

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ DEFICIT

(U.S. dollars, except share and per share data)

Preferred Stock, $0.0007, Par Value | Preferred Stock B, $0.0007, Par Value | Common Stock, $0.0007, Par Value | Additional | Foreign currency | Total Company’s | |||||||||||||||||||||||||||||||||||

| Number of Shares | Amount | Number of Shares | Amount | Number of Shares | Amount | paid-in capital | translation adjustments | Accumulated deficit | stockholders’ equity | |||||||||||||||||||||||||||||||

| BALANCE AT JANUARY 1, 2020 | - | - | 3,870,000 | 2,709 | - | - | (2,681 | ) | (5,495 | ) | (623,844 | ) | (629,311 | ) | ||||||||||||||||||||||||||

| CHANGES DURING THE PERIOD OF THREE MONTHS ENDED MARCH 31, 2020: | ||||||||||||||||||||||||||||||||||||||||

| Comprehensive loss for three month ended March 31, 2020 | - | - | - | - | - | - | - | - | (163.046 | ) | (163,046 | ) | ||||||||||||||||||||||||||||

| BALANCE AT MARCH 31, 2020 (Unaudited) | - | - | 3,870,000 | 2,709 | - | - | (2,681 | ) | (5,495 | ) | (786,890 | ) | (792,357 | ) | ||||||||||||||||||||||||||

Preferred Stock, $0.0007, Par Value | Preferred Stock B, $0.0007, Par Value | Common Stock, $0.0007, Par Value | Additional | Foreign currency | Total Company’s | |||||||||||||||||||||||||||||||||||

Number of Shares | Amount | Number of Shares | Amount | Number of Shares | Amount | paid-in capital | translation adjustments | Accumulated deficit | stockholders equity | |||||||||||||||||||||||||||||||

| BALANCE AT JANUARY 1, 2021 | 5,000,000 | 3,500 | 3,870,000 | 2,709 | 89,789,407,996 | 62,852,585 | (63,339,224 | ) | (5,495 | ) | (1,496,637 | ) | (1,982,562 | ) | ||||||||||||||||||||||||||

| CHANGES DURING THE PERIOD OF THREE MONTHS ENDED MARCH 31, 2021: | ||||||||||||||||||||||||||||||||||||||||

| Comprehensive loss for three month ended March 31, 2021 | - | - | - | - | - | - | - | - | (266,091 | ) | (266,091 | ) | ||||||||||||||||||||||||||||

| BALANCE AT MARCH 31, 2021 (Unaudited) | 5,000,000 | 3,500 | 3,870,000 | 2,709 | 89,789,407,996 | 62,852,585 | (63,339,224 | ) | (5,495 | ) | (1,762,728 | ) | (2,248,653 | ) | ||||||||||||||||||||||||||

The accompanying notes are an integral part of the condensed consolidated financial statement

| 5 |

WORLD HEALTH ENERGY HOLDINGS, INC .

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(U.S. dollars except)

| Three months ended | ||||||||

| March 31, | ||||||||

| 2021 | 2020 | |||||||

| (Unaudited) | ||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net loss for the period | (266,091 | ) | (163,046 | ) | ||||

| Adjustments required to reconcile net loss for the period to net cash used in operating activities: | ||||||||

| Depreciation and amortization | 13,597 | 10,362 | ||||||

| Increase in liability for employee rights upon retirement | 28,514 | 2,777 | ||||||

| Decrease in accounts receivable | (8,274 | ) | (1,738 | ) | ||||

| Decrease (increase) in other current assets | (4,139 | ) | (12,719 | ) | ||||

| Increase (decrease) in accounts payable | (5,422 | ) | 7,983 | |||||

| Increase in other accounts liabilities | 37,178 | 31,606 | ||||||

| Net cash used in operating activities | (204,637 | ) | (124,775 | ) | ||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Loans granted to related parties | - | (228,898 | ) | |||||

| Proceeds from related parties | 3,521 | - | ||||||

| Purchase of property and equipment | (1,668 | ) | (7,675 | ) | ||||

| Net cash used in investing activities | 1,853 | (236,573 | ) | |||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Payments of lease liability | (15,297 | ) | (6,942 | ) | ||||

| Loan received from parent company | - | 91,785 | ||||||

| Net cash provided by (used in) financing activities | (15,297 | ) | 84,843 | |||||

| INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | (218,081 | ) | (276,505 | ) | ||||

| CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD | 359,949 | 359,461 | ||||||

| CASH AND CASH EQUIVALENTS AT END OF PERIOD | 141,868 | 82,956 | ||||||

| Supplemental disclosure of cash flow information: | ||||||||

| Non cash transactions: | ||||||||

| Initial recognition of operating lease right-of-use assets | 242,906 | - | ||||||

| Initial recognition of operating lease liability | (242,906 | ) | - | |||||

The accompanying notes are an integral part of the condensed consolidated financial statement

| 6 |

WORLD HEALTH ENERGY HOLDINGS, INC .

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

NOTE 1 – GENERAL

| A. | Operations |

World Health Energy Holdings, Inc., (the “Company” or “WHEN”), was formed on May 21, 1986, under the laws of the State of Delaware. The Company has invested in and abandoned a variety of software programs that it strove to commercialize.

UCG, INC. (the “UCG”) was incorporated on September 13, 2017, under the laws of the State of Florida. The Company wholly-owns the issued and outstanding shares of RNA Ltd. (Hereinafter: “RNA”).

RNA is primarily a research and development company that has been performing software design work for UCG in the field of cybersecurity under the terms of development agreement between UCG and RNA. UCG is primarily engaged in the marketing and distribution of cybersecurity related products.

In anticipation of the transaction contemplated under the Merger Agreement, SG 77 Inc. a Delaware Corporation and a wholly-owned subsidiary of UCG (“SG”), was incorporated on April 16, 2020 and all of the cybersecurity rights and interests held by UCG, including the share ownership of RNA, were assigned to SG.

| B. | Merger Transaction |

On April 27, 2020, the Company completed a reverse triangular merger pursuant to the Agreement and Plan of Merger (the “Merger Agreement”) among WHEN, R2GA, Inc., a Delaware corporation and a wholly owned subsidiary of WHEN (“Sub”), UCG, SG, and RNA. Under the terms of the Merger Agreement, R2GA merged with SG, with SG remaining as the surviving corporation and a wholly-owned subsidiary of the WHEN (the “Merger”). The Merger was effective as of April 27, 2020 whereby SG became a direct and wholly owned subsidiary of WHEN and RNA indirect wholly owned subsidiary of the Company. Each of Gaya Rozensweig and George Baumeohl, directors of the Company, are also the sole shareholders and directors of the Company.

As consideration for the Merger, WHEN issued to UCG 3,870,000 Series B Convertible Preferred Stock, par value $0.0007 per share, of WHEN (the “Series B Preferred Shares”). Each share of the Series B Preferred Shares will automatically convert into 100,000 shares of WHEN’s common stock, par value $0.0007 (the “Common Stock”), for an aggregate amount of 387,000,000,000 shares of WHEN’s Common Stock, upon the filing with the Secretary of State of Delaware of an amendment to WHEN’s certificate of incorporation increasing the number of authorized shares of Common Stock that the Company is authorized to issue from time to time.

The Company, collectively with SG, Sub and RNA are hereunder referred to as the “Group”.

The transaction was accounted for as a reverse asset acquisition in accordance with generally accepted accounting principles in the United States of America (“GAAP”). Under this method of accounting, SG was deemed to be the accounting acquirer for financial reporting purposes. This determination was primarily based on the facts that, immediately following the Merger: (i) SG’s stockholders owned a substantial majority of the voting rights in the combined company, (ii) SG designated a majority of the members of the initial board of directors of the combined company, and (iii) SG’s senior management holds all key positions in the senior management of the combined company. As a result of the Recapitalization Transaction, the shareholders of SG received the largest ownership interest in the Company, and SG was determined to be the “accounting acquirer” in the Recapitalization Transaction.

| 7 |

WORLD HEALTH ENERGY HOLDINGS, INC .

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

NOTE 1 – GENERAL (continue)

As a result, the historical financial statements of the Company were replaced with the historical financial statements of SG. The number of shares prior to the reverse capitalization have been retroactively adjusted based on the equivalent number of shares received by the accounting acquirer in the Recapitalization Transaction.

| C. | Going concern uncertainty |

Since inception, the Group has devoted substantially all its efforts to research and development. The Group is still in its development stage and the extent of the Group’s future operating losses and the timing of becoming profitable, if ever, are uncertain. As of March 31, 2021, the Group had $141,868 of cash and cash equivalents, net losses of $266,091, accumulated deficit of $1,762,728, and a negative working capital of $389,617.

The Group will need to secure additional capital in the future in order to meet its anticipated liquidity needs primarily through the sale of additional Common Stock or other equity securities and/or debt financing. Funds from these sources may not be available to the Group on acceptable terms, if at all, and the Group cannot give assurance that it will be successful in securing such additional capital.

These conditions raise substantial doubt about the Company’s ability to continue to operate as a “going concern.” The Company’s ability to continue operating as a going concern is dependent on several factors, among them is the ability to raise sufficient additional funding.

The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

| D. | Risk factors |

The Group face a number of risks, including uncertainties regarding finalization of the development process, demand and market acceptance of the Group’s products, the effects of technological changes, competition and the development of products by competitors. Additionally, other risk factors also exist, such as the ability to manage growth and the effect of planned expansion of operations on the Group’s future results. In addition, the Group expects to continue incurring significant operating costs and losses in connection with the development of its products and increased marketing efforts. As mentioned above, the Group has not yet generated significant revenues from its operations to fund its activities, and therefore the continuance of its activities as a going concern depends on the receipt of additional funding from its current stockholders and investors or from third parties.

| 8 |

WORLD HEALTH ENERGY HOLDINGS, INC .

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND BASIS OF PRESENTATION

Unaudited Interim Financial Statements

The accompanying unaudited condensed consolidated financial statements include the accounts of the Company and its subsidiary, prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) and with the instructions to Form 10-Q. In the opinion of management, the financial statements presented herein have not been audited by an independent registered public accounting firm but include all material adjustments (consisting of normal recurring adjustments) which are, in the opinion of management, necessary for a fair statement of the financial condition, results of operations and cash flows for the three-months ended March 31, 2021. However, these results are not necessarily indicative of results for any other interim period or for the year ended December 31, 2021. The preparation of financial statements in conformity with GAAP requires the Company to make certain estimates and assumptions for the reporting periods covered by the financial statements. These estimates and assumptions affect the reported amounts of assets, liabilities, revenues and expenses. Actual amounts could differ from these estimates.

Certain information and footnote disclosures normally included in financial statements in accordance with generally accepted accounting principles have been omitted pursuant to the rules of the U.S. Securities and Exchange Commission (“SEC”). These financial statements should be read in conjunction with the financial statements and notes thereto contained in the Company’s Annual Report on published on the OTCIQ Alternative Reporting System, for the year ended December 31, 2021.

Principles of Consolidation

The consolidated financial statements are prepared in accordance with US GAAP. The consolidated financial statements of the Company include the Company and its wholly-owned and majority-owned subsidiaries. All inter-company balances and transactions have been eliminated.

Use of Estimates

The preparation of unaudited condensed consolidated financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, certain revenues and expenses, and disclosure of contingent assets and liabilities as of the date of the financial statements. Actual results could differ from those estimates. As applicable to these financial statements, the most significant estimates and assumptions relate to the going concern assumptions.

| 9 |

WORLD HEALTH ENERGY HOLDINGS, INC .

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND BASIS OF PRESENTATION (continue)

Recent Accounting Pronouncements

In August 2020, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (“ASU”) 2020-06, “Debt – Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging – Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity” (“ASU 2020-06”). The guidance in ASU 2020-06 simplifies the accounting for convertible debt and convertible preferred stock by removing the requirements to separately present certain conversion features in equity. In addition, the amendments in the ASU 2020-06 also simplify the guidance in ASC Subtopic 815-40, Derivatives and Hedging: Contracts in Entity’s Own Equity, by removing certain criteria that must be satisfied in order to classify a contract as equity, which is expected to decrease the number of freestanding instruments and embedded derivatives accounted for as assets or liabilities. Finally, the amendments revise the guidance on calculating earnings per share, requiring use of the if-converted method for all convertible instruments and rescinding an entity’s ability to rebut the presumption of share settlement for instruments that may be settled in cash or other assets.

The amendments in ASU 2020-06 are effective for the Company for fiscal years beginning after December 15, 2021. Early adoption is permitted. The guidance must be adopted as of the beginning of the fiscal year of adoption. The Company is currently evaluating the impact of this new guidance, but does not expect it to have a material impact on its financial statements.

NOTE 3 – RELATED PARTIES

| A. | Transactions and balances with related parties |

Three months ended March 31 | ||||||||

| 2021 | 2020 | |||||||

| General and administrative expenses: | ||||||||

| Salaries and fees to officers | 39,413 | 15,107 | ||||||

| Research and development expenses: | ||||||||

| Salaries and fees to officers | 22,653 | 8,536 | ||||||

| 10 |

WORLD HEALTH ENERGY HOLDINGS, INC .

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

NOTE 3 – RELATED PARTIES (continue)

| B. | Balances with related parties and officers: |

| As of March 31, | As of December 31, | |||||||

| 2021 | 2020 | |||||||

| Other accounts liabilities | 183,135 | 191,994 | ||||||

| Long term loan from related party | 1,812,704 | 1,812,704 | ||||||

| Liability for employee rights upon retirement | 102,516 | 95,451 | ||||||

NOTE 4 – COMMITMENTS AND CONTINGENCIES

On October 27, 2020 WHEN filed suit in State Court, Palm Beach County, Florida, against FSC Solutions, Inc. (“FSC”), Eli Gal Levy (“EL”) and Padem Consultants Sprl (collectively, the “Defendants”). The suit relates to the Stock Purchase Agreement entered into by WHEN with FSC and its shareholders, which included EL, pursuant to which WHEN acquired all of the issued and outstanding stock of FSC in exchange for the issuance of 70 billion shares of WHEN unregistered common stock. FSC was the putative owner of a software and trading platform which WHEN intended to use to enter into the on-line trading business. Subsequent to the completion of the acquisition, we determined that FSC did not have control over the trading platform and software we expected to acquire and operate. The Suit sought declaratory judgment to unwind the FSC transaction and cancel the shares of WHEN common stock issued in the FSC transaction that are still outstanding.

A hearing was set for January 6, 2021 whereupon mediation was ordered. The Company has been in discussions with EL to resolve this issue.

| 11 |

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Forward-Looking Statements

The following discussion should be read in conjunction with the financial statements and related notes contained elsewhere in this Quarterly Report on Form 10-Q, as well as our Annual Report on Form 10-K for the fiscal year ended December 31, 2020 as filed with the Securities and Exchange Commission (the “SEC”) on April 15, 2021. Certain statements made in this discussion are “forward-looking statements” within the meaning of the private securities litigation reform act of 1995,. These statements are based upon beliefs of, and information currently available to, the Company’s management as well as estimates and assumptions made by the Company’s management. Readers are cautioned not to place undue reliance on these forward-looking statements, which are only predictions and speak only as of the date hereof. When used herein, the words “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “future,” “intend,” “plan,” “predict,” “project,” “target,” “potential,” “will,” “would,” “could,” “should,” “continue” or the negative of these terms and similar expressions as they relate to the Company or the Company’s management identify forward-looking statements. Such statements reflect the current view of the Company with respect to future events and are subject to risks, uncertainties, assumptions, and other factors, including the risks relating to the Company’s business, industry, and the Company’s operations and results of operations and the effects that the COVID-19 outbreak, or similar pandemics, could have on our business. Should one or more of these risks or uncertainties materialize, or should the underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended, or planned.

The full extent to which the COVID-19 pandemic may directly or indirectly impact our business, results of operations and financial condition will depend on future developments that are uncertain, including as a result of new information that may emerge concerning COVID-19 and the actions taken to contain it or treat COVID-19, as well as the economic impact on local, regional, national and international customers and markets. We have made estimates of the impact of COVID-19 within our financial statements, and although there is currently no major impact, there may be changes to those estimates in future periods. Actual results may differ from these estimates.

Although the Company believes that the expectations reflected in the forward-looking statements are reasonable, the Company cannot guarantee future results, levels of activity, performance, or achievements. Except as required by applicable law, including the securities laws of the United States, the Company does not intend to update any of the forward-looking statements to conform these statements to actual results.

Our financial statements are prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). These accounting principles require us to make certain estimates, judgments and assumptions. We believe that the estimates, judgments and assumptions upon which we rely are reasonable based upon information available to us at the time that these estimates, judgments and assumptions are made. These estimates, judgments and assumptions can affect the reported amounts of assets and liabilities as of the date of the financial statements as well as the reported amounts of revenues and expenses during the periods presented. Our financial statements would be affected to the extent there are material differences between these estimates and actual results. The following discussion should be read in conjunction with our financial statements and notes thereto appearing elsewhere in this report.

Overview

World Health Energy Holdings Inc. (“WHEN”), through its wholly owned subsidiaries SG 77, Inc. (“SG”) and RNA Ltd (“RNA”), is primarily engaged in data security and analytics and provides intelligent security software and services to enterprises and individuals worldwide WHEN leverages artificial intelligence (“AI”) and machine learning to deliver innovative solutions in the areas of cybersecurity, safety focusing on the areas of endpoint security, endpoint management and encryption.

As the digital transformation of enterprises continues to advance, workforces are becoming more dispersed and mobile, and data and applications are increasingly migrating to the cloud. As part of this trend, the number of connected endpoints is growing rapidly, as is their complexity and the volume of data that they process and store. These endpoints, which include smartphones, laptops, desktops, servers, vehicles, industrial equipment and other connected devices in the Internet of Things (“IoT”), are increasingly a target for cyber adversaries. The COVID-19 pandemic has accelerated the decentralization of the workplace prompting many enterprises to shift to substantially remote and mobile work models. At the same time, the threat environment has become increasingly hostile as the number of adversaries grows and the scale and sophistication of their attacks, increasingly focused on the endpoint, continue to develop.

The landscape of increasing vulnerability has created opportunities for secure communications platforms, endpoint cybersecurity and management solutions, analytic tools and related services that help enterprises and individuals to secure their connected endpoints. Our software specializes in data protection, threat detection and response. Our product offerings enable enterprises to protect data stored on premises and in the cloud, confidential data belonging to customers, financial records, strategic and product plans and other intellectual property and, on a parental or guardian level, to monitor minor children’s cyber activities.

We believe that the COVID-19 pandemic, which continues to impact all of society has increased our long-term opportunity to help our customers protect their data and detect threats. Companies around the world now have employees working remotely from potentially vulnerable home networks, accessing critical on-premises data storages and infrastructure through VPNs and sharing information in cloud data stores. We believe this trend is likely to continue in the long-term and that we are striving to capitalize on the opportunity ahead.

| 12 |

Product Offerings & Revenue Model

Our product offerings are comprised of two principal segments, one targeting for commercial enterprises (B2B) and one for the individual users (B2C).

B2B Offerings—The B2B Cybersecurity system software development and implementation program focused on innovative solutions for the constantly evolving cyber challenges of businesses, non-governmental organizations (NGO’s) and governmental entities.

We recently launched OTOGRAPH, our comprehensive cybersecurity and information security system, to enable business enterprises to monitor, analyze and prevent suspicious or harmful behavior on corporate networks and connected devices. The OTOGRAPH is designed to analyze and prevent internal or external abuse or abnormal activity on enterprise devices, such as PCs, mobile phones, servers or any other OS-based IOT device.

The rapid transition to open and cloud-based remote workforce has exposed businesses and organizations across the world to higher risks of cyber-attacks and information security breaches. To enable businesses to better protect their data and workflow, we developed a Business Behavioral Analysis (BBA) system that enables business leaders to track all activity from any given location on a one-stop dashboard. Developed over the past two years, OTOGRAPH provides aggregated data and a wide variety of real-time analytics such as real time monitoring of online behavior, applications and system behavior, data breaches, internal and external connections analytics, productivity analysis and psycholinguistic analysis. Corporations and organizations can then use the dashboard to detect suspicious human or device activities that put their company at risk.

OTOGRAPH was developed based on a state of the art intelligence technology combined with AI technology that processes and analyzes massive amounts of behavioral and communication data and enables organizations to make real time accurate preventive assessments and decisions to protect company assets and ensure operational efficiency. OTOGRAPH deploys a unique Business Behavioral Analysis (BBA) machine learning software. Behavioral digital data is extracted from all endpoint devices that are connected to the company’s network infrastructure – whether physically, wirelessly or remotely. The data is processed and analyzed to learn and to reveal the unique digital behavioral pattern of the organization as a whole and of every endpoint or individual.

OTOGRAPH sets baselines of normal patterns for each, and constantly searches for anomalies – deviations from those expected patterns. The anomalies are detected automatically and instantly, categorized by their type and generate push alerts which are sent to the business leader’s dashboard and enabling him to respond to the threat.

B2C Cybersecurity —The B2C Cybersecurity division targets families concerned with external cyber threats and exposures in addition to monitoring a child’s behavioral patterns that may alert parents to potential tragedies caused by cyber bullying, pedophiles, other predators, and depression.

Our go-to-market strategy focuses principally on generating revenue from software, services and licensing. We intend to sell substantially all of our products and services to distributors and resellers, which will sell to end-user customers, which we refer to in this report as our customers.

Other Corporate Holdings

We currently also have the following subsidiaries.

FSC Solutions, Inc. On June 26, 2015, we entered into a Stock Purchase Agreement (the “Agreement”) with FSC and its shareholders which included Uri Tadelis, our former Chief Executive Officer and Director and our former Directors Chaim J. Lieberman and Gal Levy. The Agreement was effective as of July 1, 2015 which served as the closing date for the acquisition. Pursuant to the terms of the Agreement, we acquired all of the capital stock of FSC in exchange for the issuance of 70 billion shares of our unregistered common stock with the possibility of the issuance of an additional 130 Billion common shares upon FSC meeting certain milestones as outlined in the Agreement. Upon completion of the acquisition of FSC, we intended to employ FSC’s software and trading platform to enter the on-line trading industry. Subsequent to the completion of the acquisition, we determined that FSC did not have control over the trading platform and software we expected to acquire and operate. Please refer to Item 1, Part II, of this report.

World Health Energy, Inc. World Health Energy, Inc. owns an algae-tech business whose primary focus was the production of algae using their proprietary GB3000 growth system. The system quickly and efficiently grows algae for the production of biofuels and food protein. We also sought to produce and market high-quality, low-cost B100 biodiesel. Though, we believe that the Company has been successful in demonstrating the effectiveness of the GB3000 system on a small-scale the Company has not yet been able to raise the necessary capital to implement their technologies on a commercial scale.

| 13 |

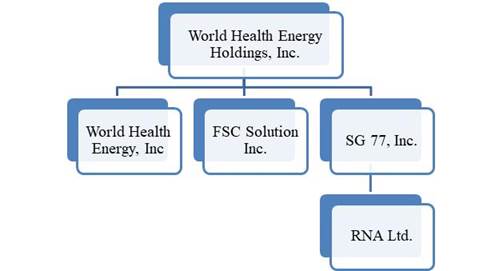

Corporate Structure (Diagram)

The corporate structure of the WHEN Group is reflected below in this diagram

Comparison of the Three Months Ended March 31, 2021 to the Three Months Ended March 31, 2020

The following table presents our results of operations for the three months ended March 31, 2021 and 2020

| Three Months Ended | ||||||||

| March 31 | ||||||||

| 2021 | 2020 | |||||||

| Revenues | 32,649 | 3,516 | ||||||

| Operating Expenses | ||||||||

| Research and development expenses | (172,771 | ) | (99,948 | ) | ||||

| General and administrative expenses | (124,485 | ) | (57,406 | ) | ||||

| Operating loss | (264,607 | ) | (153,838 | ) | ||||

| Financing expenses, net | (1,484 | ) | (9,208 | ) | ||||

| Net loss | (266,091 | ) | (163,046 | ) | ||||

Revenues. Revenues for the three months ended March 31, 2021 and 2020 were $32,649 and $3,516, respectively. Revenues were comprised primarily of software license fees.

Research and Development. Research and development expenses consist of salaries and related expenses, consulting fees, service providers’ costs, related materials and overhead expenses. Research and development expenses increased from $99,948 for the three months ended March 31, 2020 to $172,771 for the three months ended March 31, 2021. The increase resulted primarily from increase in salaries and related expenses associated with our development activities.

General and Administrative Expenses. General and administrative expenses consist primarily of salaries and related expenses and other non-personnel related expenses such as legal expenses. General and administrative expenses increased from $57,406 for the three months ended March 31, 2020 to $124,485 for the three months ended March 31, 2021. The increase is primarily attributable to the increase in salaries and related expenses, professional services other non-personnel related expenses.

Financing Expenses, Net. Financing expenses, net decreased from $9,208 for the three months ended March 31, 2020 to $1,484 for the three months ended March 31, 2020. The decrease is mainly a result of currency exchange differences between the Dollar and the New Israeli Shekel.

Net Loss. Net loss for the March 31, 2021 was $266,091 and is primarily attributable to research and development and general and administrative expenses.

Financial Condition, Liquidity and Capital Resources

Liquidity is the ability of an enterprise to generate adequate amounts of cash to meet its needs for cash requirements. At March 31, 2021, we had current assets of $202,433 compared to total current assets of $407,213 as of December 31, 2020. At March 31, 2021, we had total assets of $483,459 compared to total assets of $458,150 as of December 31, 2020. The increase in total assets is due to a decrease in related parties balance offset by increase in right of use asset arising from operating lease. At March 31, 2021,we had current liabilities of $592,050 as compared to $523,158 as of December 31, 2020. At March 31, 2021, we had total liabilities of $2,732,112 as compared to $2,440,712 as of December 31, 2020. The increase is mainly attributed to the increase in the balance of employees and related institutions, accrued expenses and right of use liabilities arising from operating lease.

At March 31, 2021, we had a cash balance of $141,868 compared to the cash balance of $359,949 as of December 31, 2020. We have no cash equivalents.

| 14 |

At March 31, 2021, we had a working capital deficiency of $389,617 as compared with a working capital deficiency of $115,945 at December 31, 2020.

We expect that our existing cash and cash equivalents as well as expected revenues will enable us to fund our operations and capital expenditure requirements through the fiscal year-end 2021. Our requirements for additional capital during this period will depend on many factors.

We may seek to raise any necessary additional capital through a combination of private or public equity offerings, debt financings, collaborations, strategic alliances, licensing arrangements and other marketing and distribution arrangements. To the extent that we raise additional capital through marketing and distribution arrangements or other collaborations, strategic alliances or licensing arrangements with third parties, we may have to relinquish valuable rights, future revenue streams, or product candidates or to grant licenses on terms that may not be favorable to us. If we raise additional capital through private or public equity offerings, the ownership interest of our existing stockholders will be diluted, and the terms of these securities may include liquidation or other preferences that adversely affect our stockholders’ rights. If we raise additional capital through debt financing, we may be subject to covenants limiting or restricting our ability to take specific actions, such as incurring additional debt, making capital expenditures or declaring dividends.

Going Concern

The accompanying consolidated financial statements have been prepared assuming that we will continue as a going concern. We have a stockholders’ deficit of $2,248,653 and a working capital deficiency of $389,617 at March 31, 2021 as well as negative operating cash flows. These conditions raise substantial doubt about our ability to continue as a going concern. The consolidated financial statements do not include any adjustments that might be necessary if we are unable to continue as a going concern.

Off-Balance Sheet Arrangements We have no off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on the Company’s financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to stockholders.

| ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

Not applicable.

| ITEM 4. | CONTROLS AND PROCEDURES |

Evaluation of Disclosure Controls and Procedures.

We maintain disclosure controls and procedures (as defined in Rule 13a-15(e) under the Exchange Act) that are designed to ensure that information required to be disclosed by us in reports that we file under the Exchange Act is recorded, processed, summarized and reported as specified in the SEC’s rules and forms and that such information required to be disclosed by us in reports that we file under the Exchange Act is accumulated and communicated to our management, including our Interim Chief Executive Officer, to allow timely decisions regarding required disclosure. Management, with the participation of our Interim Chief Executive Officer, performed an evaluation of the effectiveness of our disclosure controls and procedures as of March 31, 2021. Based on that evaluation, our management, including our Interim Chief Executive Officer, concluded that our disclosure controls and procedures were not effective as of March 31, 2021.

Management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving their objectives and management necessarily applies its judgment in evaluating the cost-benefit relationship of possible controls and procedures. As disclosed in Item 9A of our Annual Report on Form 10-K for the year ended December 31, 2020, our management concluded that our internal control over financial reporting was not effective at December 31, 2020. A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the Company’s annual or interim financial statements will not be prevented or detected on a timely basis. The limitation of the Company’s internal control over financial reporting was due to the applied risk-based approach which is indicative of many small companies with limited number of staff in corporate functions. The identified weakness were:

| ● | Material Weakness – We did not maintain effective controls over certain aspects of the financial reporting process because we (i) lacked a sufficient complement of personnel with a level of accounting expertise and an adequate supervisory review structure that is commensurate with our financial reporting requirements and (ii) we lacked controls over the disclosure of our business operations. |

| ● | lack of segregation of duties Significant Deficiencies – Inadequate segregation of duties. |

Our management believes the weaknesses identified above have not had any material effect on our financial results.

We expect to be materially dependent upon third parties to provide us with accounting consulting services for the foreseeable future which we believe will mitigate the impact of the material weaknesses discussed above. Until such time as we have a chief financial officer with the requisite expertise in U.S. GAAP and establish an audit committee and implement internal controls and procedures, there are no assurances that the material weaknesses and significant deficiencies in our disclosure controls and procedures will not result in errors in our financial statements which could lead to a restatement of those financial statements.

Changes in Internal Controls over Financial Reporting.

Except for the material weakness and associated remediation plan, , there have been no changes in our internal control over financial reporting during the fiscal quarter ended March 31, 2021 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

| 15 |

| ITEM 1. | LEGAL PROCEEDINGS |

On October 27, 2020 WHEN filed suit in State Court, Palm Beach County, Florida, against FSC Solutions, Inc. (“FSC”), Eli Gal Levy (“EL”) and Padem Consultants Sprl (collectively, the “Defendants”). The suit relates to the Stock Purchase Agreement entered into by WHEN with FSC and its shareholders, which included EL, pursuant to which WHEN acquired all of the issued and outstanding stock of FSC in exchange for the issuance of 70 billion shares of WHEN unregistered common stock. FSC was the putative owner of a software and trading platform which WHEN intended to use to enter into the on-line trading business. Subsequent to the completion of the acquisition, we determined that FSC did not have control over the trading platform and software we expected to acquire and operate. The Suit sought declaratory judgment to unwind the FSC transaction and cancel the shares of WHEN common stock issued in the FSC transaction that are still outstanding.

A hearing was set for January 6, 2021 whereupon mediation was ordered. The Company has been in discussion with EL to resolve this issue.

From time to time we may become involved in various legal proceedings that arise in the ordinary course of business, including actions related to our intellectual property. Although the outcomes of these legal proceedings cannot be predicted with certainty, we are currently not aware of any such legal proceedings that arise in the ordinary course of business, including actions related to our intellectual property. Although the outcomes of these legal proceedings cannot be predicted with certainty, we are currently not aware of any such legal proceedings or claims that we believe, either individually or in the aggregate, will have a material adverse effect on our business, financial condition, or results of operations.

| ITEM 1A. | RISK FACTORS |

An investment in the Company’s Common Stock involves a number of very significant risks. You should carefully consider the risk factors included in the “Risk Factors” section of our Annual Report on Form 10-K for the year ended December 31, 2020, as filed with the SEC on April 15, 2021, in addition to other information contained in our reports and in this quarterly report in evaluating the Company and its business before purchasing shares of our Common Stock. There have been no material changes to our risk factors contained in our Annual Report on Form 10-K for the year ended December 31, 2020.

| ITEM 2. | UNREGISTERED SALES OF SECURITIES AND USE OF PROCEEDS |

None.

| ITEM 3. | DEFAULTS UPON SENIOR SECURITIES |

None.

| ITEM 4. | MINE SAFETY DISCLOSURES |

None.

| ITEM 5. | OTHER INFORMATION: |

None.

| ITEM 6. | EXHIBITS |

| 31.1* | ||

| 32.1* | ||

| 101.INS | XBRL Instance Document | |

| 101.SCH | XBRL Taxonomy Extension Schema | |

| 101.CAL | XBRL Taxonomy Extension Calculation Linkbase | |

| 101.DEF | XBRL Taxonomy Extension Definition Linkbase | |

| 101.LAB | XBRL Taxonomy Extension Label Linkbase | |

| 101.PRE | XBRL Taxonomy Extension Presentation Linkbase |

* Filed herewith

| 16 |

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| WORLD HEALTH ENERGY HOLDINGS, INC. | ||

| (Registrant) | ||

| By: | /s/ Giora Rozensweig | |

| Giora Rozensweig | ||

| Interim Chief Executive Officer | ||

| (Principal Executive Officer and Principal Financial and Accounting Officer) | ||

| Date: | May 17, 2021 | |

| 17 |