UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR SECTION 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended | |||||

| OR | |||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| For the transition period from _____ to _____ | |||||

Commission file number: 1-13648

_______________________________________________________________________________________________________________

(Exact name of Registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||||||

| (Address of principal executive offices) (Zip Code) | ||||||||

Registrant’s telephone number, including area code: ( | ||||||||

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||

| Title of each class | Trading symbol | Name of each exchange on which registered | ||||||

| Securities registered pursuant to Section 12(g) of the Act: None | ||||||||

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark whether the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☑

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| (Check one): | Accelerated filer ☐ | ||||||||||

Non-accelerated filer ☐ | Smaller reporting company | Emerging growth company | |||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

The aggregate market value of the common stock, par value $.06-2/3 per share (the “Common Stock”), issued and outstanding and held by non-affiliates of the Registrant, based upon the closing price for the Common Stock on the NASDAQ Global Market on June 30, 2021 was approximately $4,224,000,000 . For purposes of this calculation, shares of the Registrant held by directors and officers of the Registrant and under the Registrant’s 401(k)/profit sharing plan have been excluded.

The number of shares outstanding of Common Stock was 32,187,345 as of February 10, 2022.

DOCUMENTS INCORPORATED BY REFERENCE

Cautionary Statement Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are not statements of historical facts, but rather reflect our current expectations or beliefs concerning future events and results. We generally use the words “believes,” “expects,” “intends,” “plans,” “anticipates,” “likely,” “will,” “estimates,” “project” and similar expressions to identify forward-looking statements. Such forward-looking statements, including those concerning our expectations, involve risks, uncertainties and other factors, some of which are beyond our control, which may cause our actual results, performance or achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. The risks, uncertainties and factors that could cause our results to differ materially from our expectations and beliefs include, but are not limited to, those factors set forth in this Annual Report on Form 10-K under “Item 1A. - Risk Factors” below.

We cannot assure you that the expectations or beliefs reflected in these forward-looking statements will prove correct. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You are cautioned not to unduly rely on such forward-looking statements when evaluating the information presented in this Annual Report on Form 10-K and all subsequent written and oral forward-looking statements made by us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained herein.

BALCHEM CORPORATION

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| Page Numbers | ||||||||||||||

PART I

Item 1. Business (All amounts in thousands, except share and per share data)

General:

Balchem Corporation (“Balchem,” the “Company,” “we” or “us”), was incorporated in the State of Maryland in 1967. We develop, manufacture, distribute and market specialty performance ingredients and products for the nutritional, food, pharmaceutical, animal health, medical device sterilization, plant nutrition and industrial markets. Previously, our four reportable segments were: Human Nutrition and Health, Animal Nutrition and Health, Specialty Products, and Industrial Products. However, effective in the first quarter of 2020, in order to align with our strategic focus on health and nutrition, allocation of resources, and evaluation of operating performance, and given the 2019 reduction in portfolio scale of Industrial Products, we have revised our reporting segment structure to three reportable segments: Human Nutrition and Health, Animal Nutrition and Health, and Specialty Products. These reportable segments are strategic businesses that offer products and services to different markets. This realignment has been retrospectively applied. Sales and production of products outside of our reportable segments and other minor business activities are included in "Other and Unallocated" and applied retroactively to 2019. There was no change to the Consolidated Financial Statements as a result of the change to the reportable segments. We expect that the new reportable segment structure will provide investors greater understanding of and alignment with our strategic focus. In order to ensure appropriate transparency and visibility into the financial performance of the Company, sufficient detail will continue to be provided relative to Other and Unallocated, including material contributions from oil and gas and other industrial market activities.

We sell our products through our own sales force, independent distributors and sales agents. Financial information concerning our business, business segments and geographic information appears in Management’s Discussion and Analysis of Financial Condition and Results of Operations under Item 7 below and in the Notes to our Consolidated Financial Statements included under Item 8 below, which information is incorporated herein by reference.

Human Nutrition & Health

The Human Nutrition & Health ("HNH") segment provides human grade choline nutrients and mineral amino acid chelated products through this segment for nutrition and health applications. Choline is recognized to play a key role in the development and structural integrity of brain cell membranes in infants, processing dietary fat, reproductive development and neural functions, such as memory and muscle function. The Company's mineral amino acid chelates, specialized mineral salts, and mineral complexes are used as raw materials for inclusion in premier human nutrition products. Proprietary technology has been combined to create an organic molecule in a form the body can readily assimilate. Sales growth for human nutrition applications is reliant on differentiation from lower-cost competitive products through scientific data, intellectual property and customers' appreciation of brand value. Consequently, the Company makes investments in such activities for long-term value differentiation. This segment also serves the food and beverage industry for beverage, bakery, dairy, confectionary, and savory manufacturers. The Company partners with its customers from ideation through commercialization to bring on-trend beverages, baked goods, confections, dairy and meat products to market. The Company has expertise in trends analysis and product development. When combined with its strong manufacturing capabilities in customized spray dried and emulsified powders, extrusion and agglomeration, blended lipid systems, liquid flavor delivery systems, juice and dairy bases, chocolate systems, as well as ice cream bases and variegates, the Company is a one-stop solutions provider for beverage and dairy product development needs. Additionally, this segment provides microencapsulation solutions to a variety of applications in food, pharmaceutical and nutritional ingredients to enhance performance of nutritional fortification, processing, mixing, and packaging applications and shelf-life. Major product applications are baked goods, refrigerated and frozen dough systems, processed meats, seasoning blends, confections, sports and protein bars, dietary plans, and nutritional supplements. The Company also creates cereal systems for ready-to-eat cereals, grain-based snacks, and cereal based ingredients.

Animal Nutrition & Health

The Company’s Animal Nutrition & Health ("ANH") segment provides nutritional products derived from its microencapsulation and chelation technologies in addition to basic choline chloride. For ruminant animals, the Company’s microencapsulated products boost health and milk production, delivering nutrient supplements that are biologically available, providing required nutritional levels. The Company’s proprietary chelation technology provides enhanced nutrient absorption for various species of production and companion animals and is marketed for use in animal feed throughout the world. ANH also manufactures and supplies choline chloride, an essential nutrient for monogastric animal health, predominantly to the poultry, pet and swine industries. Choline, which is manufactured and sold in both dry and aqueous forms, plays a vital role in the metabolism of fat. In poultry, choline deficiency can result in reduced growth rates and perosis in young birds, while in swine production choline is a necessary and required component of gestating and lactating sow diets for both liver health and prevention of leg deformity.

1

Sales of value-added encapsulated products are highly dependent on overall industry economics as well as the Company's ability to leverage the results of university and field research on the animal health and production benefits of our products. Management believes that success in the commodity-oriented basic choline chloride marketplace is highly dependent on the Company’s ability to maintain its strong reputation for excellent product quality and customer service. The Company continues to drive production efficiencies in order to maintain its competitive-cost position to effectively compete in a competitive global marketplace.

Specialty Products

Ethylene oxide, at the 100% level and blended with carbon dioxide, is sold as a sterilant gas, primarily for use in the health care industry. It is used to sterilize a wide range of medical devices because of its versatility and effectiveness in treating hard or soft surfaces, composites, metals, tubing and different types of plastics without negatively impacting the performance of the device being sterilized. The Company’s 100% ethylene oxide product and blends are distributed worldwide in specially designed, reusable and recyclable drum and cylinder packaging, to assure compliance with safety, quality and environmental standards as outlined by the applicable regulatory agencies in the countries our products are shipped to. The Company’s inventory of these specially built drums and cylinders, along with its five filling facilities, represents a significant capital investment. Contract sterilizers and medical device manufacturers are principal customers for this product. The Company also sells single use canisters with 100% ethylene oxide for use in sterilizing re-usable devices typically processed in autoclave units in hospitals. As a fumigant, ethylene oxide blends are highly effective in killing bacteria, fungi, and insects in spices and other seasoning materials.

The Company also distributes a number of other gases for various uses, most notably propylene oxide and ammonia. Propylene oxide is marketed and sold in the U.S. as a fumigant to aid in the control of insects and microbiological spoilage; and to reduce bacterial and mold contamination in certain shell and processed nut meats, processed spices, cacao beans, cocoa powder, raisins, figs and prunes. The Company distributes its propylene oxide product in the U.S. primarily in recyclable, single-walled, carbon steel cylinders according to standards outlined by the EPA and the DOT. Propylene oxide is also sold worldwide to customers in approved reusable and recyclable drum and cylinder packaging for various chemical synthesis applications, such as increasing paint durability and manufacturing specialty starches and textile coatings. Ammonia is used primarily as a refrigerant, and also for heat treatment of metals and various chemical synthesis applications, and is distributed in reusable and recyclable drum and cylinder drum and cylinder packaging approved for use in the countries these products are shipped to. The Company's inventory of cylinders for these products also represents a significant capital investment.

The Company’s micronutrient agricultural nutrition business sells chelated minerals primarily into high value crops. The Company has a unique and patented two-step approach to solving mineral deficiency in plants to optimize health, yield and shelf-life. First, the Company determines optimal mineral balance for plant health. The Company then has a foliar applied Metalosate® product range, utilizing patented amino acid chelate technology. Its products quickly and efficiently deliver mineral nutrients. As a result, the farmer/grower gets healthier crops that are more resistant to disease and pests, larger yields and healthier food for the consumer with extended shelf life for produce being shipped long distances.

Acquisitions

On December 13, 2019, we completed an acquisition of Zumbro River Brand, Inc. ("Zumbro"), headquartered in Albert Lea, Minnesota. We made payments of $52,403 on the acquisition date, amounting to $47,058 to the former shareholders and $5,345 to Zumbro's lenders to pay Zumbro debt. Considering the cash acquired of $686, net payments made to the former shareholders equaled $46,372. In May 2020, we received an adjustment for working capital acquired of $561. The acquisition was primarily financed through the Company's Credit Agreement (Refer to Note 8, "Revolving Loan"). Zumbro specializes in developing, marketing, and manufacturing agglomerated and extruded products for the food and beverage industry and is a market leader in high protein and specialty extruded snacks, cereals, and crisps, marketed under the brands Z-Crisps®, Whey-Os™, Whey-Vs™, and Z-Texx Complete™. Zumbro is integrated within Balchem's HNH Segment.

On May 27, 2019, we acquired 100 percent of the outstanding common shares of Chemogas Holding NV, a privately held specialty gases company headquartered in Grimbergen, Belgium ("Chemogas"). We made payments of approximately €99,503 (translated to $111,324) on the acquisition date, amounting to approximately €88,579 (translated to $99,102) to the former shareholders and approximately €10,924 (translated to $12,222) to Chemogas' lender to pay off all Chemogas bank debt. Considering the cash acquired of €3,943 (translated to $4,412), net payments made to the former shareholders were €84,636 (translated to $94,690). The acquisition was primarily financed through our Credit Agreement (Refer to Note 8, "Revolving Loan"). Chemogas, through its subsidiary companies, has been a leader in the packaging and distribution of a wide variety of specialty gases, most notably ethylene oxide, primarily in the European and Asian markets, for medical device sterilization. Through its operational and logistical excellence, Chemogas supports its customers' needs across more than 70 countries. With the acquisition, we significantly expand our geographic presence in the packaged ethylene oxide market, enabling us to offer

2

worldwide service and support to its medical device sterilization customers within the Specialty Products segment. The Chemogas sites in Europe and Asia, along with Balchem's sites in the United States form a global network of facilities.

Raw Materials

The raw materials utilized by us in the manufacture of our products are sourced from suppliers both domestically and internationally. Such raw materials include materials derived from petrochemicals, minerals, metals, agricultural commodities and other readily available commodities and are subject to price fluctuations due to market conditions. In 2021, we experienced some difficulties in procuring certain materials due to the challenging macroeconomic environment with global supply chain disruptions because of COVID-19 pandemic. However, we were able to secure most materials from our suppliers and will continue to ensure a sustainable supply chain to support our growing business operations.

Intellectual Property

We currently hold 109 patents in the United States and overseas and use certain trade-names and trademarks. We also use know-how, trade secrets, formulae, and manufacturing techniques that assist in maintaining competitive positions of certain of our products. Formulae and know-how are of particular importance in the manufacture of a number of our proprietary products. We believe that certain of our patents, in the aggregate, are advantageous to our business. However, it is believed that no single patent or related group of patents is currently so material to us that the expiration or termination of any single patent or group of patents would materially affect our business. Our U.S. patents expire between 2022 and 2036. We believe that our sales and competitive position are dependent primarily upon the quality of our products, technical sales efforts and market conditions, rather than on patent protection.

Seasonality

While in general, the businesses of our segments are not seasonal to any material extent, the plant nutrition business within Specialty Products is a seasonal business with the vast majority of sales occurring in the first half of the year, based on the planting season in the northern hemisphere.

Backlog

At December 31, 2021, we had a total backlog of $65,661 (comprised of $45,393 for the HNH segment; $14,483 for the ANH segment; $4,935 for the Specialty Products segment, and $850 for other), as compared to a total backlog of $64,811 at December 31, 2020 (comprised of $52,293 for the HNH segment; $8,620 for the ANH segment; $3,557 for the Specialty Products segment and $341 for other). It has generally been our policy and practice to maintain an inventory of finished products and/or component materials for our segments to enable us to ship products within two months after receipt of a product order. This has been more difficult in 2021 given the macroeconomic and supply chain challenges we have been experiencing, but all orders in the current backlog are expected to be filled in the 2022 fiscal year.

Competition

Our competitors include many large and small companies, some of which have greater financial, research and development, production and other resources than us. Competition in the supplement, food and beverage markets we serve are based primarily on product performance, customer support, quality, service and price. The development of new and improved products is important to our success. This competitive environment requires substantial investments in product and manufacturing process research and development. In addition, the winning and retention of customer acceptance of our food and nutrition products involve substantial expenditures for application testing, either internally or at customer/prospect sites, and sales efforts. Our competition in this market includes a variety of ingredient and nutritional supplement companies many of which are privately-held. Therefore, it is difficult to assess the size of all of our segment competitors or where we rank in comparison to such privately-held competitors.

Competition in the animal feed and industrial markets we serve are based primarily on product performance, customer support, quality, service and price. The markets for our products are subject to competitive risks because these markets are highly price competitive. Our competition in this market includes a variety of animal nutrition and health ingredient companies, along with certain industrial companies, many of which are privately-held. Therefore, we are unable to assess the size of all of our competitors or where we rank in comparison to such privately-held competitors.

In the Specialty Products segment, we face competition from alternative sterilizing technologies and products for our performance gases business. Competition in this marketplace is based primarily on service, reliability, quality, and price. Our competition in this market varies globally, many of which are regional privately-held companies. In our plant nutrition business, competition is

3

based primarily on product performance, customer support, quality, and price. The development of new and improved products is also important to our ability to compete. Our competition in this market is primarily regional privately-held companies.

Research & Development

During the years ended December 31, 2021, 2020 and 2019, we incurred research and development expenses of approximately $13,524, $10,332, and $11,377, respectively, on Company-sponsored research and development for new products, improvements to existing products, and manufacturing processes. We have historically funded our research and development programs with funds available from current operations with the intent of recovering those costs from profits derived from future sales of products resulting from, or enhanced by, the research and development effort.

We prioritize our product development activities in an effort to allocate resources to those product candidates that, we believe, have the greatest commercial potential. Factors we consider in determining the products to pursue include projected markets and needs, status of our proprietary rights, technical feasibility, expected and known product attributes, and estimated costs to bring the product to market.

Capital Projects

We continue to invest in projects across all production facilities and capital expenditures were approximately $36,142, $32,080, and $25,790 for 2021, 2020 and 2019, respectively. In 2021, we invested $20,544 on projects expected to provide favorable returns on investment, including expanded capacity in key product lines in the HNH segment. In addition, we invested $3,138 for environmental, health, safety, and security upgrades to our facilities, $2,330 in automation projects that improved quality and efficiency of our operations, and $2,222 in research and development projects. In 2020, we invested $16,856 on projects expected to provide favorable returns on investment, including expanded capacity in key product lines in the HNH segment. In addition, we invested $3,297 for environmental, health, safety, and security upgrades to our facilities as well as $3,252 in automation projects that improved safety and quality of our operations. In 2019, we invested $6,437 to expand capacity in key product lines in the HNH segment and to invest in several other large projects including a new quality and research and development lab. In addition, we invested $3,739 for environmental, health, safety, and security upgrades to our facilities. Capital expenditures are projected to range from $30,000 to $40,000 for 2022, including our continued efforts to invest in energy and water saving projects, while exploring additional renewable energy opportunities in support of the company's sustainability efforts.

Environmental / Regulatory Matters

The Federal Insecticide, Fungicide and Rodenticide Act (“FIFRA”), a health and safety statute, requires that certain products within our Specialty Products segment must be registered with the EPA because they are considered pesticides. In order to obtain a registration, an applicant typically must demonstrate, through extensive test data, that its product will not cause unreasonable adverse effects on human health or the environment. We hold EPA registrations permitting us to sell ethylene oxide as a medical device sterilant and spice fumigant, and propylene oxide as a fumigant of nuts and spices.

In April 2008, the EPA issued a RED (“Reregistration Eligibility Decision”) for ethylene oxide which permitted the continued use of ethylene oxide “to sterilize medical or laboratory equipment, pharmaceuticals, and aseptic packaging, or to reduce microbial load on musical instruments, cosmetics, whole and ground spices and other seasoning materials and artifacts, archival material or library objects”. In 2013, the EPA has initiated a new registration review of ethylene oxide, in line with and part of the registration review scheduled for a large number of other pesticides. When the Final Work Plan was issued in March 2014, the EPA anticipated that this registration review process would take approximately seven years. In December 2016, the EPA issued its Integrated Risk Information System (“IRIS”) assessment of ethylene oxide (the "IRIS Assessment"), another aspect of EPA’s safety review of ethylene oxide. In November 2020, the EPA issued a Draft Human Health Risk Assessment for Ethylene Oxide (Draft HHRA). In this Draft HHRA, the EPA presented multiple perspectives on risk extrapolation, including the IRIS Assessment. While acknowledging the necessity of maintaining the critical uses of ethylene oxide, based on the range of unit risk provided in this qualitative assessment, the EPA has stated that there should be further mitigation measures implemented which will likely require some label changes. Several mitigation measures are under consideration and the EPA anticipates issuance of a Proposed Interim Decision (PID) in 2022. We believe that EPA intends to reregister ethylene oxide for the uses stated above with the mitigation measures potentially impacting certain users, including Balchem and its customers. The product, when used as a sterilant for certain medical devices, has no known equally effective substitute. In October 2019, the U.S. Food and Drug Administration, in a public statement said, "Although medical devices can be sterilized by several methods, ethylene oxide is the most common method of sterilization of medical devices in the U.S. and is a well-established and scientifically-proven method of preventing harmful microorganisms from reproducing and causing infections." Management believes the lack of availability of this product could not be easily tolerated by various medical device manufacturers or the health care industry due to the resultant infection potential.

4

Similarly, the EPA issued a RED for propylene oxide in August 2006. At that time, the EPA “determined that products containing the active ingredient PPO [propylene oxide] are eligible for reregistration provided that…risk mitigation measures…are adopted.” Our product label was amended as required to reflect these mitigation measures and also to show that propylene oxide has been reclassified as a restricted use pesticide. In 2013, the EPA initiated a new registration review of propylene oxide, in line with and part of the registration review scheduled for a large number of other pesticides. A Final Work Plan was issued in March 2014, and EPA anticipated that this review process would take approximately seven years. In October 2020, the EPA issued both the Proposed Interim Registration Review Decision (PID) and Draft Risk Assessment (DRA) for Propylene Oxide (PPO). In July 2021, the EPA issued the Interim Registration Review Decision. Based on these documents, the use of propylene oxide to treat nuts and spices will continue to be permitted with minimal changes to the current approved level. We expect to submit those changes and the EPA to review and approve them, in the coming months.

Our facility in Verona, Missouri, while held by a prior owner, was designated by the EPA as a Superfund site and placed on the National Priorities List in 1983, because of dioxin contamination on portions of the site. Remediation was conducted by the prior owner under the oversight of the EPA and the Missouri Department of Natural Resources (“MDNR”). While we must maintain the integrity of the capped areas in the remediation areas on the site, the prior owner is responsible for completion of any further Superfund remedy. We are indemnified by the sellers under our May 2001 asset purchase agreement covering our acquisition of the Verona, Missouri facility for potential liabilities associated with the Superfund site and one of the sellers, in turn, has the benefit of certain contractual indemnification by the prior owner that executed the above-described Superfund remedy. In September 2020, BCP Ingredients, Inc. (“BCP”), the Company subsidiary that operates the site received a General Notice Letter from the EPA regarding BCP’s potential liability for contamination at the site and, in February 2022, received a Special Notice Letter from EPA for the performance of a focused remedial investigation/feasibility study at the site with regard to the presence of certain contaminants, including 1,4 dioxane,. We have engaged experts to study site conditions and hydrogeology in connection with preparing our response to the notices.

In connection with normal operations at our plant facilities, we are required to maintain environmental and other permits, including those relating to the ethylene oxide operations.

We believe we are in compliance in all material respects with federal, state, local and international provisions that have been enacted or adopted regulating the discharge of materials into the environment or otherwise relating to the protection of the environment. Such compliance includes the maintenance of required permits under air pollution regulations and compliance with requirements of the Occupational Safety and Health Administration. The cost of such compliance has not had a material effect upon the results of our operations or our financial condition.

We produce products which are required to be manufactured in conformity with current Good Manufacturing Practice (“cGMP”) regulations as interpreted and enforced by the FDA, through third party contract arrangement. Modifications, enhancements or changes in contracted manufacturing facilities or procedures relating to our pharmaceutical products are, in many circumstances, subject to FDA approval, which may be subject to a lengthy application process or which we may be unable to obtain. Any contracted manufacturing facilities that manufacture our pharmaceutical products are periodically subject to inspection by the FDA and other governmental agencies, and operations at these facilities could be interrupted or halted if the results of these inspections are unsatisfactory.

Human Capital

Our employees are our most valued asset and fundamental to our success. As of December 31, 2021, we employed approximately 1,317 full-time employees worldwide, with approximately 17% covered by collective bargaining agreements. Although we are facing challenging labor markets, we believe that we have been successful in attracting skilled and experienced personnel in a competitive environment and that our human capital resources are adequate to perform all business functions. In addition, we continue to enhance technology in order to optimize productivity and performance.

Health and Safety

Protecting the workplace environment and the health and safety of our employees, contractors, visitors, and neighbors is our top priority. Our recordable injury rate, which was defined by recordable injuries per 200,000 hours worked, was 0.99 in 2021. We continually upgrade our facilities to reduce risks and establish procedures with appropriate personnel protection for the safety of our employees. Our safety program is structured around five pillars: process safety, personal safety, industrial hygiene, transportation safety and environmental safety, and focuses on driving higher ownership and engagement from employees and contractors.

In response to the COVID-19 pandemic, we effectively deployed our Crisis Management Plan and activated our Crisis Management Team (CMT), to manage the day-to-day activities and make timely decisions related to the safety of our employees,

5

customers, and the communities in which we operate. We implemented significant changes which comply with government orders and Centers for Disease Control and Prevention (CDC) guidelines. These changes include instituting travel restrictions, a mandatory work from home policy for all of our office employees, and additional safety measures for all of our manufacturing and research and development employees.

Diversity and Inclusion

We recognize that our best performance is achieved when our teams are diverse, and accordingly, diversity and inclusion are important elements of Balchem's Human Resources strategy. We strive to promote inclusion through the implementation of inclusive leadership training across the Company and are committed to increasing representation of minorities throughout the organization. In 2021, our total workforce consisted of 76% male and 24% female among all employees and 50% male and 50% female when excluding supply chain and operations functions. With the support of our Board of Directors, we continue to explore additional diversity and inclusion initiatives.

Training and Well-Being Programs

We strive to develop employee skills and knowledge, which includes training for job-specific technical knowledge, regulatory requirements, and company policies, through our internal learning and development platform. The topics of trainings include the Company's Code of Conduct, anti-harassment and discrimination, foreign corrupt practices, antitrust, cyber security, and various other compliance subjects. Our sponsored employee Continuing Learning program offers a broad base of assistance for employees, including learning and development courses. We also deployed unconscious bias and inclusive leadership training to our management team. Employees have access to healthy lifestyle discounts through our Wellness Center, as well as debt, legal, and financial counseling. Leadership programs, peak performance training and multiple online services and courses enable our employees to choose their own learning paths and work towards achieving their goals for education, finances, and overall well-being.

Performance Review, Compensation and Benefits

Our annual performance review process is an important, objective-based dialogue to foster continuous growth and development by providing an opportunity to establish goals and deliver feedback relative to each employee's performance. Balchem's annual review process is closely aligned with a formal succession planning and talent review process designed to identify and develop the next generation of leaders.

We are dedicated to providing full-time employees with a competitive compensation package that includes medical, dental, vision, and prescription benefits in addition to a 401(k) matching program. Balchem also provides financial support for health and wellness programs such as online financial wellness content, sponsored weight loss programs and subsidized gym memberships. We also provide generous time off and leave benefits, which are important to help ensure employees can enjoy a healthy balance between work and family time.

For the year ended December 31, 2021, our turnover rate was 13% for salaried employees with an average length of service of over 10 years. We are continuing to improve employee retention with effective employment engagement efforts, a productive performance review process, and competitive compensation.

Available Information

Our headquarters is located at 52 Sunrise Park Road, New Hampton, NY 10958. Our telephone number is (845) 326-5600 and our Internet website address is www.balchem.com. We make available through our website, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, and amendments to such reports, as soon as reasonably practicable after they have been electronically filed with the Securities and Exchange Commission (the "SEC"). Such reports are available via a link from the Investor Relations page on our website to a list of our reports on the SEC’s EDGAR website. The address of the SEC's website is www.sec.gov.

Item 1A. Risk Factors

Our business is subject to a high degree of risk and uncertainty, including the following risks and uncertainties, which could adversely affect our business, financial condition, results of operation, cash flows and the trading price of our Common Stock:

Risks related to COVID-19 Pandemic

Our business, results of operations, financial condition, cash flows and stock price can be adversely affected by pandemics, epidemics or other public health emergencies, such as COVID-19.

6

Our business, results of operations, financial condition, cash flows and stock price can be adversely affected by pandemics, epidemics or other public health emergencies, such as COVID-19. The COVID-19 pandemic has resulted in governments around the world implementing certain measures to help control the spread of the virus, including quarantines, "shelter in place" and "stay at home" orders, travel restrictions, business curtailments, school closures, and other measures.

Our businesses have been deemed "essential" under the orders issued by federal, state and local governments. Although we have continued to operate our facilities to date consistent with federal guidelines and state and local orders, COVID-19 or similar viruses and any preventive or protective actions taken by governmental authorities may have a material adverse effect on our operations, supply chain, customers, and transportation networks, including business shutdowns or disruptions. The extent to which viruses such as COVID-19 and their variants may adversely impact our business depends on future developments, which are highly uncertain and unpredictable, depending upon the severity and duration of any virus outbreak and the effectiveness of actions taken globally to contain or mitigate the effects thereof. Any resulting financial impact cannot be estimated reasonably at this time, but may materially adversely affect our business, results of operations, financial condition and cash flows. Additionally, concerns over the economic impact of COVID-19 and its variants have caused extreme volatility in financial and other capital markets which may adversely impact our stock price and may affect our ability to access capital markets. To the extent the COVID-19 pandemic adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described within this report. We have also experienced reductions in the demand for certain of our products due to reductions in elective and non-essential surgical procedures. We implemented mitigation strategies as needed to protect the long-term sustainability of our company and will continue to respond as appropriate.

Business and Financial Risks

Global economic conditions may adversely affect our business, operating results and financial condition.

Unfavorable changes in economic conditions, including inflation, recession, changes in tariffs and trade relations amongst international trading partners, or other changes in economic conditions, may adversely impact the markets in which we operate. These conditions may make it extremely difficult for our customers, our vendors and us to accurately forecast and plan future business activities, and they could cause U.S. and foreign businesses to slow spending on our products which would reduce our revenues and profitability. Furthermore, during challenging economic times our customers may face issues gaining timely access to sufficient credit, which could result in an impairment of their ability to make timely payments to us. If that were to occur, we may be required to increase our allowance for doubtful accounts and cash flow would be negatively impacted. We cannot predict the timing, depth or duration of any economic slowdown or subsequent economic recovery, worldwide, or in the markets in which we operate. Also, at any point in time we have funds in our cash accounts that are with third party financial institutions. These balances in the U.S., Italy, Belgium, Malaysia, Australia, Philippines, and Singapore could exceed the Federal Deposit Insurance Corporation (“FDIC”), Fondo Interbancario di Tutela dei Depositi (“FITD”), Financial Services and Markets Authority ("FSMA"), Perbadanan Insurans Deposit Malaysia ("PIDM"), Australian Prudential Regulation Authority ("APRA"), Philippine Deposit Insurance Corporation ("PDIC"), and Singapore Deposit Insurance Corporation ("SDIC") insurance limits, respectively. While we monitor the cash balances in our accounts, these balances could be impacted if the underlying financial institutions fail or could be subject to other adverse conditions in the financial markets. Additionally, our future results of operations could be adversely affected by changes in the effective tax rate as a result of a change in the mix of earnings in jurisdictions with differing statutory tax rates, changes in tax laws, regulations and judicial rulings or changes in the interpretation thereof.

Raw material shortages or price increases could adversely affect our business and financial results.

The principal raw materials that we use in the manufacture of our products can be subject to price fluctuations due to market conditions and factors beyond our control, including the COVID-19 pandemic and inflationary pressures, both of which have impacted our business over the past two years, accelerated as 2021 progressed and are likely to continue for some time. Such raw materials include materials derived from petrochemicals, minerals, metals, agricultural commodities and other commodities. While the selling prices of our products tend to increase or decrease over time with the cost of raw materials, these changes may not occur simultaneously or to the same degree. At times, including during periods of rapidly increasing raw material prices, we may be unable to pass increases in raw material costs through to our customers due to certain contractual obligations. Such increases in the price of raw materials, if not offset by product price increases, or substitute raw materials, would have an adverse impact on our profitability. We believe we have reliable sources of supply for our raw materials under normal market conditions. We cannot, however, predict the likelihood or impact of any future raw material shortages. Any shortages or unforeseen price increases could have a material adverse impact on our results of operations.

Our international operations subject us to currency translation risk and currency transaction risk which could cause our results to fluctuate from period to period.

7

The financial condition and results of operations of our foreign subsidiaries are reported in Euros, Canadian Dollars, Malaysian Ringgits, Singapore Dollars, Australian Dollars, and Philippine Pesos and then translated into U.S. dollars at the applicable currency exchange rate for inclusion in our consolidated financial statements. Exchange rates between these currencies in recent years have fluctuated and may do so in the future. Furthermore, we incur currency transaction risk whenever we enter into either a purchase or a sales transaction using a currency different than the functional currency. Given the volatility of exchange rates, we may not be able to effectively manage our currency transactions and/or translation risks. Volatility in currency exchange rates could impact our business and financial results.

On May 28, 2019, we entered into a cross-currency swap to manage foreign exchange risk related to our investment in Chemogas. Although we utilize risk management tools, such as derivative instruments, to mitigate market fluctuations in foreign currencies, any changes in strategy in regard to risk management tools can also affect revenue, expenses and results of operations and there can be no assurance that such measures will result in cost savings or that all market fluctuation exposure will be eliminated.

Our debt instruments impose operating and financial restrictions which could have an adverse impact on our business and results of operations.

Our incurrence of indebtedness could have negative consequences to us, including limiting our ability to borrow additional monies for our working capital, capital expenditures, acquisitions, debt service requirements or other general corporate purposes; limiting our flexibility in planning for, or reacting to, changes in our operations, our business or the industries in which we compete; our leverage may place us at a competitive disadvantage by limiting our ability to invest in the business or in further research and development; making us more vulnerable to downturns in our business or the economy; and there would be a material adverse effect on our business and financial condition if we were unable to service our indebtedness or obtain additional financing, as needed.

Our ability to make payments on our indebtedness depends on our ability to generate cash in the future. If we do not generate sufficient cash flow to meet our debt service and working capital requirements, we may need to seek additional financing or sell assets. This may make it more difficult for us to obtain financing on terms that are acceptable to us, or at all. Without any such financing, we could be forced to sell assets to make up for any shortfall in our payment obligations under unfavorable circumstances.

Interest payable in accordance with our five-year senior secured revolving credit agreement (the "Credit Agreement") is based on a fluctuating rate. In light of potential fluctuations, we are exposed to risk resulting from adverse changes in interest rates.

On May 28, 2019, we entered into an interest rate swap to protect us against adverse fluctuations in interest rates by reducing its exposure to variability in cash flows relating to interest payments on a portion of our outstanding debt. We use LIBOR ("the London interbank offered rate") as a reference rate in the derivative agreements. LIBOR is the basic rate of interest used in lending between banks on the London interbank market and is widely used as a reference for setting the interest rate on loans globally. On July 27, 2017, the United Kingdom’s Financial Conduct Authority (FCA), which regulates LIBOR, initially announced that it intends to phase out LIBOR by the end of 2021. FCA recently has formally announced that it has commitments from panel banks to continue to contribute to LIBOR through June 30, 2023 for USD 1-month, 3-month, and 6-month. From July 1, 2023 to June 30, 2033, LIBOR for these instruments will continue publication on a "synthetic" basis with status of "loss of representativeness", i.e. ending their reliance on panel bank submissions and calculated based on a methodology to primarily assist with a very small subset of existing contracts where it is difficult to move to the new reference rate (so called "tough legacy" contract). In preparation for the phase out of LIBOR, we may need to renegotiate our financial obligations and derivative instruments that utilize LIBOR. However, these efforts may not be successful in mitigating the legal and financial risk from changing the reference rate in our legacy agreements. Furthermore, the discontinuation of LIBOR may adversely impact our ability to manage and hedge exposures to fluctuations in interest rates using derivative instruments.

We may not be able to successfully consummate and manage acquisition, joint venture and divestiture activities which could have an impact on our results.

From time to time, we may acquire other businesses, enter into joint ventures and, based on an evaluation of our business portfolio, divest existing businesses. These acquisitions, joint ventures and divestitures may present financial, managerial and operational challenges, including diversion of management attention from existing businesses, difficulty with integrating or separating personnel and financial and other systems, increased expenses, assumption of unknown liabilities and indemnities, and potential disputes with the buyers or sellers. In addition, we may be required to incur asset impairment charges (including charges related to tangible assets, goodwill and other intangible assets) in connection with acquired businesses which may reduce our profitability. If we are unable to consummate such transactions, or successfully integrate and grow acquisitions and achieve contemplated revenue synergies and cost savings, our financial results could be adversely affected. Additionally, joint ventures

8

inherently involve a lesser degree of control over business operations, thereby potentially increasing the financial, legal, operational and/or compliance risks.

Changes in our relationships with our vendors, changes in tax or trade policy, interruptions in our operations or supply chain or increased commodity or supply chain costs could adversely affect our results of operations.

We are dependent on our vendors, including common carriers, to supply merchandise to our distribution centers, stores, and guests. As we continue to add capabilities to quickly move the appropriate amount of inventory at optimal operational costs through our entire supply chain, operating our fulfillment network becomes more complex and challenging. If our fulfillment network does not operate properly, if a vendor fails to deliver on its commitments, or if common carriers have difficulty providing capacity to meet demands for their services like they experienced at times during the last two years, we could experience merchandise out-of-stocks, delivery delays or increased delivery costs, which could lead to lost sales and decreased guest confidence, and adversely affect our results of operations.

A large portion of our merchandise is sourced, directly or indirectly, from outside the U.S. Any major changes in tax or trade policy, such as the imposition of additional tariffs or duties on imported products, between the U.S. and countries from which we source merchandise could require us to take certain actions, including for example raising prices on products we sell and seeking alternative sources of supply from vendors in other countries with whom we have less familiarity, which could adversely affect our reputation, sales, and our results of operations.

Political or financial instability, currency fluctuations, the outbreak of pandemics or other illnesses (such as the COVID-19 pandemic), labor unrest, transport capacity and costs, port security, weather conditions, natural disasters, or other events that could alter or suspend our operations, slow or disrupt port activities, or affect foreign trade are beyond our control and could materially disrupt our supply of merchandise, increase our costs, and/or adversely affect our results of operations. There have been periodic labor disputes impacting the U.S. ports that have caused us to make alternative arrangements to continue the flow of inventory, and if these types of disputes recur, worsen, or occur in other countries through which we source products, it may have a material impact on our costs or inventory supply. Changes in the costs of procuring commodities used in our merchandise or the costs related to our supply chain, could adversely affect our results of operations.

Adverse publicity or consumer concern regarding the safety or quality of food products containing our products, or health concerns, whether with our products, products in the same general class as our products or for food products containing our products, may result in the loss of sales. Also, consumer preferences for products containing our products may change.

We are dependent upon consumers’ perception of the safety, quality and possible dietary benefits of products containing our food ingredient products. As a result, substantial negative publicity concerning our products or other foods and beverages in which our products are used could lead to a loss of consumer confidence in those products, removal of those products from retailers’ shelves and reduced sales and prices of our products. Product quality issues, actual or perceived, or allegations of product contamination, even when false or unfounded, could hurt the image of our products or of brands of products containing our products, and cause consumers to choose other products. Further, any product recall, whether our own or by a third party, whether due to real or unfounded allegations, could impact demand on food products containing our products or even our products. Any of these events could have a material adverse effect on our business, results of operations and financial condition. Consumer preferences, as well as trends, within the food industries change often and our failure to anticipate, identify or react to changes in these preferences and trends could, among other things, lead to reduced demand and price reductions, and could have an adverse effect on our business, results of operations and financial condition. While we continue to diversify our product offerings, developing new products entails risks and we cannot be certain that demand for our products and products containing our products will continue at current levels or increase in the future.

Operational Risks

Our financial success depends in part on the reliability and sufficiency of our manufacturing facilities.

Our revenues depend on the effective operation of our manufacturing, packaging, and processing facilities. The operation of our facilities involves risks, including the breakdown, failure, or substandard performance of equipment, power outages, the improper installation or operation of equipment, explosions, fires, natural disasters, failure to achieve or maintain safety or quality standards, work stoppages, supply or logistical outages, and the need to comply with environmental and other directives of governmental agencies. The occurrence of material operational problems, including, but not limited to, the above events, could adversely affect our profitability during the period of such operational difficulties.

We face risks associated with our sales to customers and manufacturing operations outside the United States.

9

For the year ended December 31, 2021, approximately 27% of our net sales consisted of sales outside the United States. In addition, we conduct a portion of our manufacturing outside the United States. The majority of our foreign sales occur through our foreign subsidiaries and the remainder of our foreign sales result from exports to foreign distributors, resellers and customers. Our foreign sales and operations are subject to a number of risks, including: longer accounts receivable collection periods; the impact of recessions and other economic conditions in economies outside the United States; export duties and quotas; changes in tariffs and trade relations including but not limited to those associated with the North American Free Trade Agreement and the exit of the United Kingdom from the European Union; unexpected changes in regulatory requirements; certification requirements; environmental regulations; reduced protection for intellectual property rights in some countries; potentially adverse tax consequences; political and economic instability; and preference for locally produced products. These factors could have a material adverse impact on our ability to increase or maintain our international sales.

We may, from time to time, experience problems in our labor relations.

In North America, approximately 91 employees, or 8% of our North American workforce, as of December 31, 2021, are represented by a union under a single collective bargaining agreement, which was re-negotiated and is effective as of July 12, 2020. It will expire in 2025. In Europe, approximately 107 employees at our Marano, Ticino, Italy facility are covered by a national collective bargaining agreement, which expires in 2022. Approximately 25 employees at our Bertinoro, Italy facility are also covered by a national collective bargaining agreement, which expired in 2019 and is currently under negotiation. We believe that our present labor relations with all our union employees are satisfactory, however, our failure to renew these agreements on reasonable terms could result in labor disruptions and increased labor costs, which could adversely affect our financial performance. Similarly, if our relations with the union portion of our workforce do not remain positive, such employees could initiate a strike, work stoppage or slowdown in the future. In the event of such an action, we may not be able to adequately meet the needs of our customers using our remaining workforce and our operations and financial condition could be adversely affected. Additionally, other portions of our workforce could become subject to union campaigns.

Technology failures or cyber security breaches could have an adverse effect on the Company’s operations.

We rely on information technology systems to process, transmit, store, and protect electronic information. For example, a significant portion of the communications between our personnel, customers, and suppliers depend on information technology. Our information technology systems may be vulnerable to a variety of interruptions due to events beyond our control including, but not limited to, natural disasters, terrorist attacks, telecommunications failures, computer viruses, hackers, and other security issues. We have technology and information security processes and disaster recovery plans in place to mitigate our risk to these vulnerabilities; however, these measures may not be adequate to ensure that our operations will not be disrupted, should such an event occur. The Company has not experienced any significant information security breaches and as a result, has not incurred any expenses with respect thereto, either with respect to penalties and settlement or otherwise. We have a robust cyber security employee education program and train our employees on email and password security, recognizing phishing and related topics on a regular basis.

Legal Risks

Our business exposes us to potential product liability claims and recalls, which could adversely impact our financial condition and performance.

Our development, manufacture and sales of food ingredient, pharmaceutical and nutritional supplement products involve an inherent risk of exposure to product liability claims, product recalls, product seizures and related adverse publicity. A product liability judgment against us could also result in substantial and unexpected expenditures, affect consumer confidence in our products, and divert management’s attention from other responsibilities. Although we maintain product liability insurance coverage in amounts we believe are customary within the industry, there can be no assurance that this level of coverage is adequate or that we will be able to continue to maintain our existing insurance or obtain comparable insurance at a reasonable cost, if at all. A product recall or a partially or completely uninsured judgment against us could have a material adverse effect on results of operations and financial condition.

Regulatory and Compliance Risks

The loss of governmental permits and approvals would materially harm some of our businesses.

Pursuant to applicable environmental and safety laws and regulations, we are required to obtain and maintain certain governmental permits and approvals, including EPA registrations under FIFRA for two of our products. We maintain EPA FIFRA registrations for ethylene oxide as a medical device sterilant and spice fumigant and for propylene oxide as a fumigant of nuts and spices. The registrations for both products are in the final stages of a FIFRA registration review process begun in 2013. Recent

10

draft documents indicate that the EPA intends to continue the registrations for both ethylene oxide and propylene oxide with certain additional mitigation measures. The EPA may re-examine the registrations in the future in accordance with the provisions of FIFRA. Any future failure of the EPA to allow reregistration of ethylene oxide or propylene oxide would have a material adverse effect on our business and financial results.

Commercial supply of pharmaceutical products that we may develop, subject to cGMP manufacturing regulations, will be performed by third-party cGMP manufacturers. Modifications, enhancements or changes in third-party manufacturing facilities or procedures of our pharmaceutical products are, in many circumstances, subject to FDA approval, which may be subject to a lengthy application process or which we may be unable to obtain. Any third-party cGMP manufacturers that we may use are periodically subject to inspection by the FDA and other governmental agencies, and operations at these facilities could be interrupted or halted if the results of these inspections are unsatisfactory. Failure to comply with the FDA or other governmental regulations can result in fines, unanticipated compliance expenditures, recall or seizure of products, total or partial suspension of production, enforcement actions, injunctions and criminal prosecution, which could have a material adverse effect on our business and financial results.

Permits and approvals may be subject to revocation, modification or denial under certain circumstances. Our operations or activities (including the status of compliance by the prior owner of the Verona, Missouri facility under Superfund remediation) could result in administrative or private actions, revocation of required permits or licenses, or fines, penalties or damages, which could have an adverse effect on us. In addition, we cannot predict the extent to which any legislation or regulation may affect the market for our products or our cost of doing business.

Concerns about ethylene oxide emissions have resulted in certain state actions against certain of our customers that are currently impacting these customers’ ability to use the ethylene oxide process to sterilize medical devices, which may, in turn, affect sales to these customers.

Certain of the Company’s customers who use ethylene oxide in the USA for the sterilization of medical devices have received ongoing state and local scrutiny for environmental concerns at their facilities. This scrutiny is associated with the IRIS Assessment described in the “Environmental / Regulatory Matters” Section above, which deemed exposure to ethylene oxide as unsafe at levels far below those found in the environment. The EPA began using the IRIS Assessment in 2020 to regulate change to existing permissible emissions’ limits at certain non-sterilization ethylene oxide users and producers, and is expected to finalize rules during 2022 that will regulate sterilization users. Additionally, some state and local regulators have drawn their own conclusions from the IRIS Assessment, which has resulted in certain state actions against our customers that are currently impacting, or have impacted at some point, these customers’ ability to use the ethylene oxide process to sterilize medical devices. Because of these actions, one customer facility has been shut down permanently, another was shut down for a period of months and has since restarted, and other customers have taken or are expected to take voluntary downtime to install new abatement equipment. The installation of the new abatement equipment is being done ahead of what is expected to be changes in the EPA regulations. The Company remains confident that the sterilization industry will be able to install abatement equipment to satisfy the new forthcoming EPA requirements. The Company is working with various stakeholders to ensure the EPA considers all available assessments to appropriately quantify ethylene oxide's risks. While the Company believes that EPA will, as it has in the past, ultimately regulate to lower emissions levels based on a combined consideration of the various assessments available and that industry will then adopt practices and procedures to ensure compliance with these new regulations, there is no assurance that this will be the case.

General Risks

Increased competition could hurt our business and financial results.

We face competition in our markets from a number of large and small companies, some of which have greater financial, research and development, production and other resources than we do. Our competitive position is based principally on performance, quality, customer support, service, breadth of product line, manufacturing or packaging technology and the selling prices of our products. Our competitors may improve the design and performance of their products and introduce new products with competitive price and performance characteristics. We expect to do the same to maintain our current competitive position and market share.

Item 1B. Unresolved Staff Comments

None.

11

Item 2. Properties

Our corporate headquarters is located in New Hampton, New York. Our operations are conducted at our owned and leased facilities throughout the U.S. and other foreign countries. These facilities house manufacturing and warehousing operations, as well as administrative offices. We have total 32 locations across the world and some of these locations serve multiple segments.

The following is a summary of our principal properties:

| Segment | Location | Administrative | Manufacturing | Warehousing | ||||||||||||||||||||||

| Corporate | 4 U.S. cities | 4 | - | - | ||||||||||||||||||||||

| HNH | 14 U.S. cities and 3 foreign countries | 2 | 12 | 3 | ||||||||||||||||||||||

| ANH | 5 U.S. cities and 4 foreign countries | 1 | 8 | - | ||||||||||||||||||||||

| Specialty Products | 5 U.S. cities and 7 foreign countries | 2 | 9 | 1 | ||||||||||||||||||||||

| Other | 1 U.S. city and 1 foreign country | - | 2 | - | ||||||||||||||||||||||

We believe that our production facilities and related machinery and equipment are well maintained, suitable for their purpose, and adequate to support our businesses.

Item 3. Legal Proceedings

We are involved in legal proceedings through the normal course of business. Management believes that any unfavorable outcome related to these proceedings will not have a material effect on our financial position, results of operations or liquidity.

Item 4. Mine Safety Disclosures

None.

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

The Common Stock is listed on the Nasdaq Global Market under the symbol “BCPC.”

On February 10, 2022 the closing price for the Common Stock on the Nasdaq Global Market was $138.07.

Record Holders

As of February 10, 2022, the approximate number of holders of record of Common Stock was 64. Such number does not include stockholders who hold their stock in street name.

12

Performance Graph

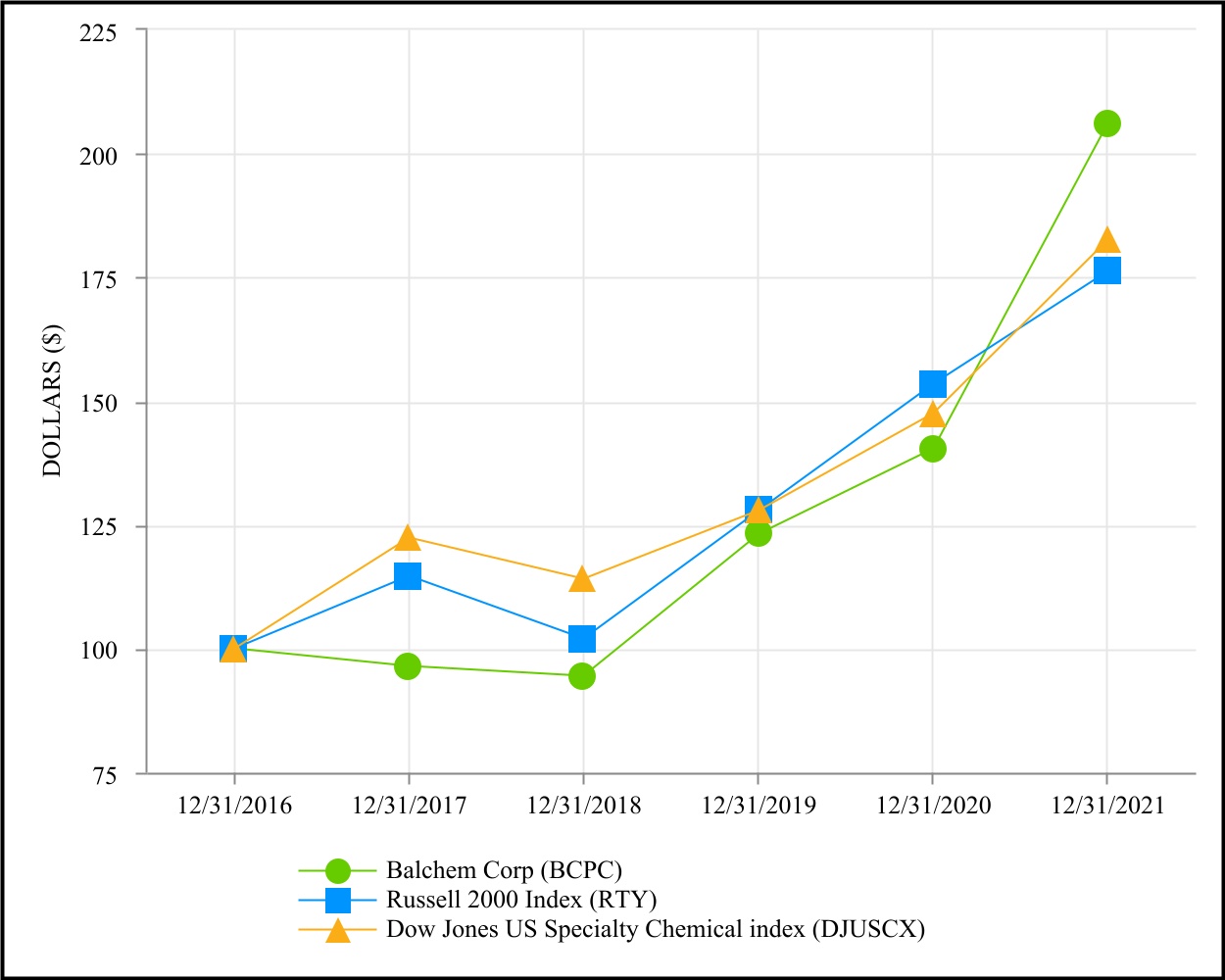

The graph below sets forth the cumulative total stockholder return on the Common Stock (referred to in the table as “BCPC”) for the five years ended December 31, 2021, the overall stock market return during such period for shares comprising the Russell 2000® Index (which we believe includes companies with market capitalization similar to that of us), and the overall stock market return during such period for shares comprising the Dow Jones U.S. Specialty Chemicals Index, in each case assuming a comparable initial investment of $100 on December 31, 2016 and the subsequent reinvestment of dividends. The Russell 2000® Index measures the performance of the shares of the 2000 smallest companies included in the Russell 3000® Index. In light of our industry segments, we do not believe that published industry-specific indices are necessarily representative of stocks comparable to us. Nevertheless, we consider the Dow Jones U.S. Specialty Chemicals Index to be potentially useful as a peer group index with respect to us. The performance of the Common Stock shown on the graph below is historical only and not necessarily indicative of future performance.

13

Issuer Purchase of Equity Securities

The following table summarizes the share repurchase activity for the year ended December 31, 2021:

Total Number of Shares Purchased (1) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Programs(1) | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||||||||||||||||

| January 1-31, 2021 | — | $ | — | — | $ | 123,071,229 | |||||||||||||||||||||||

| February 1-28, 2021 | 13,475 | $ | 118.41 | 13,475 | $ | 139,860,344 | |||||||||||||||||||||||

| March 1-31, 2021 | — | $ | — | — | $ | 139,860,344 | |||||||||||||||||||||||

| First Quarter | 13,475 | 13,475 | |||||||||||||||||||||||||||

| April 1-30, 2021 | 16,838 | $ | 119.89 | 16,838 | $ | 139,592,155 | |||||||||||||||||||||||

| May 1-31, 2021 | 51,623 | $ | 129.34 | 51,623 | $ | 143,914,129 | |||||||||||||||||||||||

| June 1-30, 2021 | 4,188 | $ | 129.99 | 4,188 | $ | 144,099,802 | |||||||||||||||||||||||

| Second Quarter | 72,649 | 72,649 | |||||||||||||||||||||||||||

| July 1-31, 2021 | 45,129 | $ | 129.67 | 45,129 | $ | 137,892,532 | |||||||||||||||||||||||

| August 1-31, 2021 | 15,099 | $ | 129.62 | 15,099 | $ | 135,874,343 | |||||||||||||||||||||||

| September 1-30, 2021 | 847 | $ | 138.98 | 847 | $ | 145,574,840 | |||||||||||||||||||||||

| Third Quarter | 61,075 | 61,075 | |||||||||||||||||||||||||||

| October 1-31, 2021 | 2,926 | $ | 150.28 | 2,926 | $ | 156,973,021 | |||||||||||||||||||||||

| November 1-30, 2021 | 20,147 | $ | 160.29 | 20,147 | $ | 164,200,063 | |||||||||||||||||||||||

| December 1-31, 2021 | 79,576 | $ | 160.95 | 79,576 | $ | 152,061,457 | |||||||||||||||||||||||

| Fourth Quarter | 102,649 | 102,649 | |||||||||||||||||||||||||||

| Total | 249,848 | 249,848 | |||||||||||||||||||||||||||

(1) Our Board of Directors has approved a stock repurchase program. The total authorization under this program is 3,763,038 shares. Since the inception of the program in June 1999, a total of 2,818,244 shares have been purchased. There is no expiration for this program. | |||||||||||||||||||||||||||||

Item 6. [Reserved]

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

(All amounts in thousands, except share and per share data)

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our Consolidated Financial Statements and the related notes included in this report. Refer to Part II, Item 7 in our Annual Report on Form 10-K for the fiscal year ended December 31, 2020 (filed with the SEC on February 19, 2021) for additional discussion of our financial condition and results of operations for the year ended December 31, 2019, as well as our financial condition and results of operations for the year ended December 31, 2020 compared to the year ended December 31, 2019. Those statements in the following discussion that are not historical in nature should be considered to be forward-looking statements that are inherently uncertain. See “Cautionary Statement Regarding Forward-Looking Statements.”

Overview

We develop, manufacture, distribute and market specialty performance ingredients and products for the nutritional, food, pharmaceutical, animal health, medical device sterilization, plant nutrition and industrial markets. Our three reportable segments are strategic businesses that offer products and services to different markets: Human Nutrition & Health, Animal Nutrition &

14

Table of Contents

Health, and Specialty Products, as more fully described in Note 11 of the consolidated financial statements. Sales and production of products outside of our reportable segments and other minor business activities are included in "Other and Unallocated".

Balchem is committed to solving today's challenges to shape a healthier tomorrow by operating responsibly and providing innovative solutions for the health and nutritional needs of the world. Sustainability is at the heart of our company's vision to make the world a healthier place, and we proudly support the Ten Principles of the United Nations Global Compact on human rights, labor, environment and anti-corruption. In January 2022, Balchem was named one of America’s Most Responsible Companies by Newsweek magazine for the second consecutive year. This list, compiled by Newsweek in partnership with Statista Inc., recognizes the most responsible companies in the U.S. across a variety of industries, and is based on publicly available environmental, social and governance (ESG) data. Our Sustainability Framework focuses on the most critical ESG topics relevant to our business and stakeholders. We are very proud of our ESG accomplishments to date and are pleased with the recognition by Newsweek. Balchem will continue to foster these fundamental principles broadly along our entire value chain, develop new ideas and technologies that help us work smarter, and help build a world that is a better place to live.

COVID-19 Response

The COVID-19 response effort has been a primary focus for us since early last year. Our focus has been on employee safety first, keeping our manufacturing sites operational, satisfying customer needs, preserving cash and ensuring strong liquidity, and responding to changes in this dynamic market environment as appropriate.

As a result of our broad based risk mitigation efforts of the direct impacts of the Covid-19 pandemic, our manufacturing sites have been operating at near normal conditions, our research and development teams have continued to innovate in our laboratories, and all of our other employees have been effectively carrying on their responsibilities and functions remotely or in a reduced density hybrid setting.

We are increasingly focused on managing the extraordinary supply chain disruptions that are challenging the markets we operate within that are, at least in part, related to the pandemic and/or the global recovery from the pandemic. We are experiencing severe input cost inflation, raw material shortages, logistics disruptions, and labor availability issues. These indirect pandemic related challenges accelerated as 2021 progressed and are likely to continue for some time.

Segment Results

We sell products for all three segments through our own sales force, independent distributors, and sales agents.

The following tables summarize consolidated net sales by segment and business segment earnings from operations for the three years ended December 31, 2021, 2020 and 2019 (in thousands):

15

Table of Contents

| Business Segment Net Sales | ||||||||||||||||||||

| 2021 | 2020 | 2019 | ||||||||||||||||||

| Human Nutrition & Health | $ | 442,733 | $ | 400,330 | $ | 347,433 | ||||||||||||||

| Animal Nutrition & Health | 226,776 | 192,191 | 177,557 | |||||||||||||||||

| Specialty Products | 117,020 | 103,566 | 92,257 | |||||||||||||||||

Other and Unallocated (1) | 12,494 | 7,557 | 26,458 | |||||||||||||||||

| Total | $ | 799,023 | $ | 703,644 | $ | 643,705 | ||||||||||||||

| Business Segment Earnings From Operations | ||||||||||||||||||||

| 2021 | 2020 | 2019 | ||||||||||||||||||

| Human Nutrition & Health | $ | 76,031 | $ | 61,397 | $ | 48,429 | ||||||||||||||

| Animal Nutrition & Health | 26,179 | 29,979 | 25,868 | |||||||||||||||||

| Specialty Products | 30,020 | 26,801 | 28,513 | |||||||||||||||||

Other and Unallocated (1) | (4,728) | (7,030) | (257) | |||||||||||||||||

| Total | $ | 127,502 | $ | 111,147 | $ | 102,553 | ||||||||||||||

(1) Other and Unallocated consists of a few minor businesses which individually do not meet the quantitative thresholds for separate presentation and corporate expenses that have not been allocated to a segment. Unallocated corporate expenses consist of: (i) Transaction and integration costs, ERP implementation costs, and unallocated legal fees totaling $1,264, $2,410 and $3,436 for years ended December 31, 2021, 2020 and 2019, respectively, and (ii) Unallocated amortization expense of $2,510, $1,606, and $551 for years ended December 31, 2021, 2020, and 2019, respectively, related to an intangible asset in connection with a company-wide ERP system implementation. | ||||||||||||||||||||

Acquisitions