UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 | |||

FORM | |||

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the fiscal year ended | |||

or | |||

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the transition period from to | |||

Commission File Number | |||

FLOTEK INDUSTRIES, INC. |

(Exact name of registrant as specified in its charter) |

(State of other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||

(Address of principal executive offices) | (Zip Code) | |||

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark:

• if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

• if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

• whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

• whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

• whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Act.

Large accelerated filer ☐ Accelerated filer ☒ Non-accelerated filer ☐

Smaller reporting company ☒ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

• whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of voting stock held by non-affiliates of the registrant as of June 28, 2019 (based on the closing market price on the NYSE Composite Tape on June 28, 2019) was approximately $150,815,000 . At March 3, 2020, there were 63,275,372 outstanding shares of the registrant’s common stock, $0.0001 par value.

DOCUMENTS INCORPORATED BY REFERENCE

The information required in Part III of the Annual Report on Form 10-K is incorporated by reference to the registrant’s definitive proxy statement to be filed pursuant to Regulation 14A for the registrant’s 2020 Annual Meeting of Stockholders.

TABLE OF CONTENTS

— | |||

i

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Annual Report”), and in particular, Part II, Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” contains “forward-looking statements” within the meaning of the safe harbor provisions, 15 U.S.C. § 78u-5, of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are not historical facts but instead represent the Company’s current assumptions and beliefs regarding future events, many of which, by their nature, are inherently uncertain and outside the Company’s control. The forward-looking statements contained in this Annual Report are based on information available as of the date of this Annual Report. The forward looking statements relate to future industry trends and economic conditions, forecast performance or results of current and future initiatives and the outcome of contingencies and other uncertainties that may have a significant impact on the Company’s business, future operating results and liquidity. These forward-looking statements generally are identified by words such as “anticipate,” “believe,” “estimate,” “continue,” “intend,”

“expect,” “plan,” “forecast,” “project” and similar expressions, or future-tense or conditional constructions such as “will,” “may,” “should,” “could” and “would,” or the negative thereof or other variations thereon or comparable terminology. The Company cautions that these statements are merely predictions and are not to be considered guarantees of future performance. Forward-looking statements are based upon current expectations and assumptions that are subject to risks and uncertainties that can cause actual results to differ materially from those projected, anticipated or implied. A detailed discussion of potential risks and uncertainties that could cause actual results and events to differ materially from forward-looking statements include, but are not limited to, those discussed in Part I, Item 1A – “Risk Factors” of this Annual Report and periodically in future reports filed with the Securities and Exchange Commission (the “SEC”).

The Company has no obligation to publicly update or revise any forward-looking statements, whether as a result of new information or future events, except as required by law.

ii

PART I

Item 1. Business.

General

Flotek Industries, Inc. (“Flotek” or the “Company”) is a global, technology-driven company that develops and supplies chemistry and services to the oil and gas industries. Flotek also supplied high-value compounds to companies that make food and beverages, cleaning products, cosmetics, and other products that are sold in consumer and industrial markets, which became classified as discontinued operations at December 31, 2018.

The Company was originally incorporated in the Province of British Columbia on May 17, 1985. In October 2001, the Company moved the corporate domicile to Delaware and effected a 120 to 1 reverse stock split by way of a reverse merger with CESI Chemical, Inc. Since then, the Company has grown organically and through a series of acquisitions.

In December 2007, the Company’s common stock began trading on the New York Stock Exchange (“NYSE”) under the stock ticker symbol “FTK.” Annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) are posted to the Company’s website, www.flotekind.com, as soon as practicable subsequent to electronically filing or furnishing to the SEC. Information contained in the Company’s website is not to be considered as part of any regulatory filing. As used herein, “Flotek,” the “Company,” “we,” “our,” and “us” refers to Flotek Industries, Inc. and/or the Company’s wholly owned subsidiaries. The use of these terms is not intended to connote any particular corporate status or relationship.

Recent Developments

During the fourth quarter of 2018, the Company initiated a strategic plan to sell its Consumer and Industrial Chemistry Technologies, (“CICT”) segment, which was completed in the first quarter of 2019. An investment banking advisory services firm was engaged and actively marketed this segment. Effective December 31, 2018, the Company classified the assets, liabilities, and results of operations for this segment as “Discontinued Operations” for all periods presented.

During the fourth quarter of 2016, the Company initiated a strategic restructuring of its business to enable a greater focus on its core businesses in energy chemistry and consumer and industrial chemistry and effective December 31, 2016 classified the Drilling Technologies and Production Technology segments into discontinuing operations. During 2017, the Company completed the sale of substantially all of the assets and transfer of certain specified liabilities and obligations of each of the Drilling Technologies and Production Technologies segments.

Description of Operations and Segments

The Company’s continuing operations have one strategic business segment: Energy Chemistry Technologies (“ECT”). The CICT segment was sold in 2019, and the Drilling Technologies, and Production Technologies segments were sold in 2017 and all three are classified as discontinued operations.

The Company offers competitive products and services derived from technological advances, some of which are patented, and experience in fluid systems applications that are responsive to industry demands in both domestic and international markets. Flotek operates and/or distributes its products in seven domestic and international markets.

Financial information about operating segments and geographic concentration is provided in Note 17 – “Business Segment, Geographic and Major Customer Information” in Part II, Item 8 – “Financial Statements and Supplementary Data” of this Annual Report.

Information about the Company’s operating segment is below.

Energy Chemistry Technologies

The ECT segment designs, develops, manufactures, packages, distributes, delivers, and markets reservoir-centric fluid systems, including specialty and conventional chemistries, for use in oil and gas well drilling, cementing, completion, remediation, and stimulation activities designed to maximize recovery in both new and mature fields. Flotek’s specialty chemistries possess enhanced performance characteristics and are manufactured to perform in a broad range of basins and reservoirs with varying downhole pressures, temperatures and other well-specific conditions customized to customer specifications. This segment has a research and innovation laboratory and technical services laboratories that focus on design improvements, development and viability testing of new chemistry formulations, and continued enhancement of existing products. Flotek’s flagship patented chemistry technologies include Complex nano-Fluid® (“CnF® products”), Pressure reducing Fluids®, and MicroSolv™.

Chemistries branded as Complex nano-Fluid® technologies are patented both domestically and internationally and are performance additives within both oil and natural gas markets. The CnF® product mixtures are stable mixtures of plant derived oils, water, and surface active agents which organize molecules into nano structures. The combined advantage of solvents, surface active agents and water, and the resultant nano structures, improve well treatment results as compared to the independent use of solvents and surface active agents. CnF® products are composed of renewable, plant-derived ingredients and oils that are certified as biodegradable. CnF® chemistries help achieve improved operational and financial

1

results for the Company’s customers in low permeability sand and shale reservoirs.

Chemistries branded as Pressure reducing Fluids® technologies (“PrF® products”) are a patented line of high molecular weight polymers used as friction reducers that reduce turbulence and maximize the use of the polymer at a lower loading rate. The products have proven efficacy in a broad range of water quality, including high brine and high iron environments.

Introduced in April 2018, chemistries branded as MicroSolv™ are a patented line of microemulsion technologies designed to deliver cost-effective performance.

Discontinued Operations

Consumer and Industrial Chemistry Technologies. The CICT segment, reported as discontinued operations, sourced citrus oil domestically and internationally and processed citrus oils. Products produced from processed citrus oil include (1) high value compounds used as additives by companies in the flavors and fragrances markets and (2) environmentally friendly chemistries for use in the oil & gas industry and numerous other industries around the world. The CICT segment designed, developed, and manufactured products that were sold to companies in the flavor and fragrance industries and specialty chemical industry. These technologies were used within food and beverage, fragrance, and household and industrial cleaning products industries.

Drilling Technologies. The Drilling Technologies segment provided downhole drilling tools for use in energy and mining activities. This segment assembled, rented, sold, inspected, and marketed specialized equipment used in energy, mining, and industrial drilling activities. Established tool rental operations were located throughout the United States (the “U.S.”) and in a number of international markets.

Production Technologies. The Production Technologies segment provided pumping system components, electric submersible pumps (“ESPs”), gas separators, production valves, and complementary services. Through the Company’s acquisition of International Artificial Lift, LLC, the Company provided a line of next generation hydraulic pumping units that served to increase and maximize production for oil and natural gas wells.

Seasonality

Overall, operations are not significantly affected by seasonality; however, winter weather conditions can pose delays in clients’ activity levels. Certain working capital components build and recede throughout the year in conjunction with established purchasing and selling cycles that can impact operations and financial position. The performance of certain services within the Company’s remaining ECT segment can be susceptible to both weather and naturally occurring phenomena, including, but not limited to, the following:

• | the severity and duration of winter temperatures in North America, which impacts natural gas storage levels, drilling activity, and commodity prices; |

• | the timing and duration of the Canadian spring thaw and resulting restrictions that impact activity levels; |

• | the timing and impact of hurricanes upon coastal and offshore operations; and |

• | the adverse weather and disease that affect citrus crops in Florida and Brazil which can negatively impact the availability of citrus oils and increase raw material costs for the ECT segment. |

Product Demand and Marketing

Demand for the Company’s energy chemistry products and services is dependent on levels of conventional and non-conventional oil and natural gas well drilling and completion activity, both domestically and internationally. Products in the ECT segment are marketed directly to customers through the Company’s own sales force and through certain contractual agency arrangements. Established customer relationships provide repeat sales opportunities. The Company participates in industry trade shows and publishes technical papers and case studies examining the performance of its chemistries and methodologies for evaluating chemistries more effectively. While the Company’s primary marketing efforts remain focused in North America, a growing amount of resources and effort are focused on emerging international markets, especially in the Middle East and North Africa (“MENA”) and South America. In addition to direct marketing and relationship development, the Company also markets products and services through the use of third party agents primarily in international markets.

Customers

The Company’s customers primarily include major integrated oil and natural gas companies, oilfield service companies, independent oil and natural gas companies, pressure pumping service companies, and national and state-owned oil companies. Within the ECT segment, the Company had two major customers for the year ended December 31, 2019, which accounted for 20% and 10%, respectively, of consolidated revenue, two major customers for the year ended December 31, 2018, which accounted for 12% and 10%, respectively, of consolidated revenue, and one major customer for the year ended December 31, 2017, which accounted for 17% of consolidated revenue. In aggregate, the Company’s largest three customers collectively accounted for 40%, 30%, and 32% of consolidated revenue for the years ended December 31, 2019, 2018, and 2017, respectively.

2

Research and Innovation

The Company is engaged in research and innovation activities focused on the design of reservoir specific, customized chemistries in the ECT segment. In this segment, for the years ended December 31, 2019, 2018, and 2017, the Company incurred $8.9 million, $10.4 million, and $13.1 million, respectively, of research and innovation expense. In 2019, research and innovation expense was approximately 7.4% of consolidated revenue. The Company expects that its 2020 research and innovation investment will continue to remain a significant portion of overall spending to support new product development and customization initiatives for its clients.

Backlog

Due to the nature of the Company’s contractual customer relationships and the way they operate, the Company has historically not had significant backlog order activity.

Intellectual Property

The Company’s policy is to protect its intellectual property, both within and outside of the U.S. The Company considers patent protection for all products and methods deemed to have commercial significance and that may qualify for patent protection. The decision to pursue patent protection is

dependent upon several factors, including whether patent protection can be obtained, cost effectiveness, and alignment with operational and commercial interests. The Company believes its patent and trademark portfolio, combined with confidentiality agreements, trade secrets, proprietary designs, and manufacturing and operational expertise, are necessary and appropriate to protect its intellectual property and ensure continued strategic advantage. Within its continuing operations, the Company has 82 granted patents and approximately 50 pending patent applications filed in the U.S. and abroad, covering various chemical compositions and methods of use. In addition, within its continuing operations, the Company has 60 registered trademarks in the U.S. and abroad, covering a variety of its goods and services.

Competition

The ability to compete in the oilfield services industry is dependent upon the Company’s ability to differentiate its products and services, provide superior quality and service, and maintain a competitive cost structure with sufficient raw material supplies. Activity levels in the oil field goods and services industry are impacted by current and expected oil and natural gas prices, oil and natural gas drilling activity, production levels, and customer drilling and completion designated capital spending. Domestic and international regions in which Flotek operates are highly competitive. The unpredictability of the energy industry and commodity price fluctuations creates both increased risk and opportunity for the products and services of both the Company and its competitors.

Certain oil and natural gas service companies competing with the Company are larger and have access to more resources. Such competitors could be better situated to withstand industry downturns, compete on the basis of price, and acquire and develop new equipment and technologies, all of which could affect the Company’s revenue and profitability. Oil and natural gas service companies also compete for customers and strategic business opportunities. Thus, competition could have a detrimental impact on the Company’s business.

Raw Materials

Materials and components used in the Company’s servicing and manufacturing operations, as well as those purchased for sale, are generally available on the open market from multiple sources. When able, the Company uses multiple suppliers, both domestically and internationally, to purchase raw materials on the open market. The prices paid for raw materials vary based on energy, citrus, and other commodity price fluctuations, tariffs, duties on imported materials, foreign currency exchange rates, business cycle position, and global demand. Higher prices for chemistries, citrus, polymers, and other raw materials could adversely impact future sales and contract fulfillments.

Citrus-based terpene (d-limonene) is an important feedstock for many of the Company’s formulations. In addition, the Company utilizes naturally derived terpenes from other sources and bio-based solvents from other natural sources.

The Company is diligent in its efforts to identify alternate suppliers in its contingency planning for potential supply shortages and in its proactive efforts to reduce costs through competitive bidding practices.

Government Regulations

The Company is subject to federal, state, and local laws and regulations, including laws related to the environment, occupational safety, health, transportation, and trade within the U.S. and other countries in which the Company does business. These laws and regulations strictly govern the manufacture, storage, transportation, sale, use, and disposal of chemistry products. The Company strives to ensure full compliance with all regulatory requirements and is unaware of any material instances of noncompliance.

The Company continually evaluates the environmental impact of its operations and attempts to identify potential liabilities and costs of any environmental remediation, litigation, or associated claims. Several products of the ECT and discontinued CICT segments are considered hazardous materials. In the event of a leak or spill in association with Company operations, the Company could be exposed to risk of material cost, net of insurance proceeds, to remediate any contamination. No environmental claims are currently being litigated, and the Company does not expect that costs related to remediation requirements will have a significant adverse effect on the Company’s consolidated financial position or results of operations.

3

Employees

At December 31, 2019, the Company had 174 employees, exclusive of existing worldwide agency relationships. None of the Company’s employees are covered by a collective bargaining agreement and labor relations are generally positive. Certain international locations have staffing or work arrangements that are contingent upon local work councils or other regulatory approvals.

Available Information and Website

The Company’s website is accessible at www.flotekind.com. Annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are available (see the “Investor Relations” section of the Company’s website), as soon as reasonably practicable, subsequent to electronically filing or otherwise providing reports to the SEC. Corporate governance materials, guidelines, by laws, and code of business conduct and ethics are also available on the website. A copy of corporate governance materials is available upon written request to the Company.

The SEC maintains the www.sec.gov website, which contains reports, proxy and information statements, and other registrant information filed electronically with the SEC.

The Annual Chief Executive Officer Certification required by the NYSE was submitted on June 21, 2019. The certification was not qualified in any respect. Additionally, the Company has filed all principal executive officer and financial officer certifications as required under Sections 302 and 906 of the Sarbanes-Oxley Act of 2002 with this Annual Report. Information with respect to the Company’s executive officers and directors is incorporated herein by reference to information to be included in the proxy statement for the Company’s 2020 Annual Meeting of Stockholders.

The Company has disclosed and will continue to disclose any changes or amendments to the Company’s code of business conduct and ethics as well as waivers to the code of ethics applicable to executive management by posting such changes or waivers on the Company’s website.

Item 1A. Risk Factors.

The Company’s business, financial condition, results of operations, and cash flows are subject to various risks and uncertainties. Readers of this report should not consider any descriptions of these risk factors to be a complete set of all potential risks that could affect Flotek. These factors should be carefully considered together with the other information contained in this Report and the other reports and materials filed by the Company with the SEC. Further, many of these risks are interrelated and, as a result, the occurrence of certain risks could trigger and/or exacerbate other risks. Such a combination could materially increase the severity of the impact of these risks on the Company’s business, results of operations, financial condition, or liquidity.

This Annual Report contains “forward-looking statements,” as defined in the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. Forward-looking statements discuss Company prospects, expected revenue, expenses and profits, strategic and operational initiatives, and other activities. Forward-looking statements also contain suppositions regarding future oil and natural gas industry conditions, both domestically and internationally. The Company’s results could differ materially from those anticipated in the forward-looking statements as a result of a variety of factors, including risks described below and elsewhere. See “Forward-Looking Statements” at the beginning of this Annual Report.

Risks Related to the Company’s Business

The Company’s business is largely dependent upon domestic and international oil and natural gas industry spending.

Spending could be adversely affected by industry conditions or by new or increased governmental regulations, global economic conditions, the availability of credit, and lower oil and natural gas prices. All of these factors are beyond the Company’s control. The resulting reductions in customers’ expenditures could have a significant adverse effect on Company revenue, margins, and overall operating results.

The Company’s ECT segment is dependent upon customers’ willingness to make operating and capital expenditures for exploration, development and production of oil and natural gas in both North American and global markets. Customers’ expectations of a decline in future oil and natural gas market prices could result in curtailed spending, thereby reducing demand for the Company’s products and services. Industry conditions are influenced by numerous factors over which the Company has no control, including the supply of and demand for oil and natural gas, domestic and international economic conditions, political instability in oil and natural gas producing countries and merger and divestiture activity among oil and natural gas producers and service companies.

The price for oil and natural gas is subject to a variety of factors, including, but not limited to:

• | global demand for energy as a result of population growth, economic development, and general economic and business conditions; |

• | the ability of the Organization of Petroleum Exporting Countries (“OPEC”) to set and maintain production levels and the impact of non-OPEC producers on global supply; |

4

• | availability and quantity of natural gas storage; |

• | import and export volumes and pricing of liquefied natural gas; |

• | pipeline capacity to critical markets and out of producing regions; |

• | political and economic uncertainty and socio-political unrest; |

• | cost of exploration, production and transport of oil and natural gas; |

• | technological advances impacting energy production and consumption; and |

• | weather conditions. |

The volatility of oil and natural gas prices and the consequential effect on exploration and production activity could adversely impact the activity levels of the Company’s customers.

Volatile economic conditions could weaken customer exploration and production expenditures, causing reduced demand for the Company’s products and services and a significant adverse effect on the Company’s operating results. It is difficult to predict the pace of industry growth, the direction of oil and natural gas prices, the direction and magnitude of economic activity, and to what extent these conditions could affect the Company. However, reduced cash flow and capital availability could adversely impact the financial condition of the Company’s customers, which could result in customer project modifications, delays or cancellations, general business disruptions, and delay in, or nonpayment of, amounts that are owed to the Company. This could cause a negative impact on the Company’s results of operations and cash flows.

Furthermore, if certain of the Company’s suppliers were to experience significant cash flow constraints or become insolvent as a result of such conditions, a reduction or interruption in supplies or a significant increase in the price of supplies could occur, adversely impacting the Company’s results of operations and cash flows.

The Company’s reliance on unconventional oil production could lessen the positive effects of a general recovery of the oil and gas industry.

The majority of the Company’s current product offerings are used in unconventional oil and gas plays. The Company has little to no exposure to conventional or offshore sectors. In the event that an industry recovery is disproportionately driven by conventional and offshore oil and gas plays, the Company may not have a resulting increase in its operational results.

The Company’s inability to develop and/or introduce new products or differentiate existing products could have an adverse effect on its ability to be responsive to customers’ needs and could result in a loss of customers, as well as adversely affecting the Company’s future success and profitability.

The oil and natural gas industry is characterized by technological advancements that have historically resulted in, and will likely continue to result in, substantial improvements in the scope and quality of oilfield chemistries and their function and performance. Consequently, the Company’s future success is dependent, in part, upon the Company’s continued ability to timely develop innovative products and services. Increasingly sophisticated customer needs and the ability to anticipate and respond to technological and operational advances in the oil and natural gas industry is critical. Proving up new technology requires time and resources, and there is no assurance that the Company will be able to commercialize new technology in a timely manner. If the Company fails to successfully develop and introduce innovative products and services that appeal to customers, or if existing or new market competitors develop superior products and services, the Company’s revenue and profitability could deteriorate.

Increased competition could exert downward pressure on prices charged for the Company’s products and services.

The Company operates in a competitive environment characterized by large and small competitors. Competitors with greater resources and lower cost structures or who are trying to gain market share may be successful in providing competing products and services to the Company’s customers at lower prices than the Company currently charges. Employees of the Company may leave and compete directly with the Company. This may require the Company to lower its prices, resulting in an adverse impact on revenues, margins, and operating results.

If the Company is unable to adequately protect intellectual property rights or is found to infringe upon the intellectual property rights of others, the Company’s business is likely to be adversely affected.

The Company relies on a combination of patents, trademarks, copyrights, trade secrets, non-disclosure agreements, and other security measures to establish and protect the Company’s intellectual property rights. Although the Company believes that existing measures are reasonably adequate to protect intellectual property rights, there is no assurance that the measures taken will prevent misappropriation of proprietary information or dissuade others from independent development of similar products or services. Moreover, there is no assurance that the Company will be able to prevent competitors from copying, reverse engineering, modifying, or otherwise obtaining and/or using the Company’s technology and proprietary rights to create competitive products or services. The Company may not be able to enforce intellectual property rights outside of the U.S. Additionally, the laws of certain countries in which the Company’s products and services are manufactured or marketed may not protect the Company’s proprietary rights to the same extent as do the laws of the U.S. Furthermore, other third parties may infringe, challenge, invalidate, or circumvent the Company’s patents, trademarks, copyrights and trade secrets. In each case, the Company’s ability to compete could be significantly impaired.

5

A portion of the Company’s products and services are without patent protection. The issuance of a patent does not guarantee validity or enforceability. The Company’s patents may not necessarily be valid or enforceable against third parties. The issuance of a patent does not guarantee that the Company has the right to use the patented invention. Third parties may have blocking patents that could be used to prevent the Company from marketing the Company’s own patented products and services and utilizing the Company’s patented technology.

The Company is exposed and, in the future, may be exposed to allegations of patent and other intellectual property infringement from others. The Company may allege infringement of its patents and other intellectual property rights against others. Under either scenario, the Company could become involved in costly litigation or other legal proceedings regarding its patent or other intellectual property rights, from both an enforcement and defensive standpoint. Even if the Company chooses to enforce its patent or other intellectual property rights against a third party, there may be risk that the Company’s patent or other intellectual property rights become invalidated or otherwise unenforceable through legal proceedings. If intellectual property infringement claims are asserted against the Company, the Company could defend itself from such assertions or could seek to obtain a license under the third party’s intellectual property rights in order to mitigate exposure. In the event the Company cannot obtain a license, third parties could file lawsuits or other legal proceedings against the Company, seeking damages (including treble damages) or an injunction against the manufacture, use, sale, offer for sale, or importation of the Company’s products and services. These could result in the Company having to discontinue the use, manufacture, and sale of certain products and services, increase the cost of selling certain products and services, or result in damage to the Company’s reputation. An award of damages, including material royalty payments, or the entry of an injunction order against the use, manufacture, and sale of any of the Company’s products and services found to be infringing, could have an adverse effect on the Company’s results of operations and ability to compete.

The loss of key customers could have an adverse impact on the Company’s results of operations and could result in a decline in the Company’s revenue.

The Company has critical customer relationships which are dependent upon production and development activity related to a handful of customers. In the continuing operations segment reported, revenue derived from the Company’s three largest customers as a percentage of consolidated revenue for the years ended December 31, 2019, 2018, and 2017, totaled 40%, 30%, and 32%, respectively. Customer relationships are historically governed by purchase orders or other short-term contractual obligations as opposed to long-term contracts. The loss of one or more key customers could have an adverse effect on the Company’s results of operations and could result in a decline in the Company’s revenue.

Loss of key suppliers, the inability to secure raw materials on a timely basis, or the Company’s inability to pass commodity price increases on to customers could have an adverse effect on the Company’s ability to service customers’ needs and could result in a loss of customers.

Materials used in servicing and manufacturing operations, as well as those purchased for sale, are generally available on the open market from multiple sources. Acquisition costs and transportation of raw materials to Company facilities have historically been impacted by extreme weather conditions. Certain raw materials used by the ECT segment are available only from limited sources; accordingly, any disruptions to critical suppliers’ operations could adversely impact the Company’s operations. Prices paid for raw materials could be affected by energy products and other commodity prices; weather and disease associated with the Company’s crop dependent raw materials, specifically citrus greening; tariffs and duties on imported materials; foreign currency exchange rates; and phases of the general business cycle and global demand. The ECT segment secures short and long term supply agreements for critical raw materials from both domestic and international vendors.

The prices of key raw materials are subject to market fluctuations, which at times can be significant and unpredictable. Availability of key raw materials weather events, natural disasters and health epidemics in countries from which the Company sources its raw materials may impact prices. The Company may be unable to pass along price increases to its customers, which could result in an adverse impact on margins and operating profits. The Company currently uses purchasing strategies designed, where possible, to align the timing of customer demand with our supply commitments. However, the Company currently does not hedge commodity prices, but may consider such strategies in the future, and there is no guarantee that the Company’s purchasing strategies will prevent cost increases from resulting in adverse impacts on margins and operating profits.

The Company depends on a single-source supplier for citrus terpene, and the loss of this supplier could significantly harm the Company’s business, financial condition, and results of operations.

Citrus-based terpene (d-limonene) is an important feedstock for many of the Company’s formulations. In February 2019, the Company entered into a terpene Supply Agreement (the “Supply Agreement”) with Flotek’s former subsidiary, Florida Chemical Company, LLC (“FCC”), to serve as the Company’s supplier of terpene. The Company depends on FCC to provide it with terpene in a timely manner that meets its quality, quantity, and cost requirements. FCC may encounter problems that preclude it from supplying terpene on the terms set forth in the Supply Agreement, including with respect to pricing and production volumes. In the event that FCC encounters such problems or otherwise breaches the Supply Agreement, the Company’s inability to contract with alternative sources could result in a prolonged interruption in its ability to produce the Company’s formulations. Any such delays or interruptions

6

could ultimately result in a significant increase in the price of the various formulations or a significant reduction in the Company’s margins on these formulations, which could adversely affect the Company’s business, financial condition, and results of operations.

If the Company loses the services of key members of management, the Company may not be able to manage operations and implement growth strategies.

The Company depends on the continued service of the Chief Executive Officer and President, the Chief Financial Officer and other key members of the executive management team, who possess significant expertise and knowledge of the Company’s business and industry. Furthermore, the Chief Executive Officer and President serves as Chairman of the Board of Directors. The Company has entered into employment agreements with certain of these key members; however, at December 31, 2019, the Company only carried key man life insurance for the Chief Executive Officer and President. Any loss or interruption of the services of key members of the Company’s management could significantly reduce the Company’s ability to manage operations effectively and implement strategic business initiatives.

Removal of members of management or directors may be difficult or costly.

The Company’s management, employees and directors may have retention, employment or severance agreements in place. In the event that our employees, management or directors do not have the proper skills for management or operation of the Company, or the Company otherwise wishes to remove them from their position(s), the Company may be required to pay severance or similar payments. Removal of some management and employees by the Company may also be difficult and require negotiations by the Company.

Failure to maintain effective disclosure controls and procedures and internal controls over financial reporting could have an adverse effect on the Company’s operations and the trading price of the Company’s common stock.

Effective internal controls are necessary for the Company to provide reliable financial reports, effectively prevent fraud and operate successfully as a public company. If the Company cannot provide reliable financial reports or effectively prevent fraud, the Company’s reputation and operating results could be harmed. If the Company is unable to maintain effective disclosure controls and procedures and internal controls over financial reporting, the Company may not be able to provide reliable financial reports, which in turn could affect the Company’s operating results or cause the Company to fail to meet its reporting obligations. Ineffective internal controls could also cause investors to lose confidence in reported financial information, which could negatively affect the trading price of the Company’s common stock, limit the ability of the Company to access capital markets in the future, and require additional costs to improve internal control systems and procedures.

Network disruptions, security threats and activity related to global cyber-crime pose risks to the Company’s key operational, reporting and communication systems.

The Company relies on access to information systems for its operations. Failures of, or interference with, access to these systems, such as network communications disruptions, could have an adverse effect on our ability to conduct operations and could directly impact consolidated reporting. Phishing attacks could result in sensitive or confidential information being released by the Company. Security breaches pose a risk to confidential data and intellectual property, which could result in damages to our competitiveness and reputation. The Company’s policies and procedures, system monitoring and data back-up processes may not prevent or mitigate the effects of these potential disruptions or breaches. There can be no assurance that existing or emerging threats will not have an adverse impact on our systems or communications networks.

The Company may pursue strategic acquisitions, joint ventures, and strategic divestitures, which could have an adverse impact on the Company’s business.

The Company’s past and potential future acquisitions, joint ventures, and divestitures involve risks that could adversely affect the Company’s business. Negotiations of potential acquisitions, joint ventures, or other strategic relationships, integration of newly acquired businesses, and/or sales of existing businesses could be time consuming and divert management’s attention from other business concerns. Acquisitions and joint ventures could also expose the Company to unforeseen liabilities or risks associated with new markets or businesses. Unforeseen operational difficulties related to acquisitions and joint ventures could result in diminished financial performance or require a disproportionate amount of the Company’s management’s attention and resources. Additionally, acquisitions could result in the commitment of capital resources without the realization of anticipated returns. Divestitures could result in the loss of future earnings without adequate compensation and the loss of unrealized strategic opportunities.

Failure to manage the Company’s costs during the current period of retraction may have a negative effect on the Company’s ability to reach profitability.

The Company has been in a period of rapid retraction, has sold or discontinued all but one operating segment, and is in the process of adjusting costs and expenses to match its new smaller size. If the Company does not manage its costs and expenses properly, it may not be able to reach profitability.

If the Company does not manage the potential difficulties associated with expansion successfully, the Company’s operating results could be adversely affected.

The Company believes future success will depend, in part, on the Company’s ability to adapt to market opportunities and changes, to successfully integrate the operations of any businesses acquired, expansion of existing product and service

7

lines, and potentially expand into new product and service areas in which the Company may not have prior experience. Factors that could result in strategic business difficulties include, but are not limited to:

• | failure to effectively integrate acquisitions, joint ventures or strategic alliances; |

• | failure to effectively plan for risks associated with expansion into areas in which management lacks prior experience; |

• | lack of experienced management personnel; |

• | increased administrative burdens; |

• | lack of customer retention; |

• | technological obsolescence; and |

• | infrastructure, technological, communication and logistical problems associated with large, expansive operations. |

If the Company fails to manage potential difficulties successfully, the Company’s operating results could be adversely impacted.

The Company’s ability to grow and compete could be adversely affected if adequate capital is not available.

The ability of the Company to grow and be competitive in the market place is dependent on the availability of adequate capital. Access to capital is dependent, in large part, on the Company’s cash flows and the availability of and access to equity and debt financing. The Company cannot guarantee that internally generated cash flows will be sufficient, or that the Company will to be able to obtain equity or debt financing on acceptable terms, or at all. As a result, the Company may not be able to finance strategic growth plans, take advantage of business opportunities, or to respond to competitive pressures. The Company’s existing shelf registration statement expires in September 2020, and there is no guarantee that the Company will file a new shelf registration statement.

Failure to adapt to changing buying habits at the Company’s potential and existing customers could have a negative effect on the Company’s ability to attract and retain business.

The demographics and habits of the purchasing departments of many of the Company’s customers and potential customers is changing. Key decision makers are younger and show different buying habits and approaches. Customers are increasingly using advanced analytics to make purchasing decisions. If the Company does not adapt to these changing purchasing trends, the Company may not be able to attract or retain business.

Failure to collect for goods and services sold to key customers could have an adverse effect on the Company’s financial results, liquidity and cash flows.

The Company performs credit analyses on potential customers; however, credit analysis does not provide full assurance that customers will be willing and/or able to pay for goods and services purchased from the Company.

Furthermore, collectability of international sales can be subject to the laws of foreign countries, which may provide more limited protection to the Company in the event of a dispute over payment. Because sales to domestic and international customers are generally made on an unsecured basis, there can be no assurance of collectability. If one or more major customers are unwilling or unable to pay its debts to the Company, it could have an adverse effect of the Company’s financial results, liquidity and cash flows.

Unforeseen contingencies such as litigation could adversely affect the Company’s financial condition.

The Company is, and from time to time may become, a party to legal proceedings incidental to the Company’s business involving alleged injuries arising from the use of Company products, exposure to hazardous substances, patent infringement, employment matters, commercial disputes, and shareholder lawsuits. The defense of these lawsuits may require significant expenses, divert management’s attention, and may require the Company to pay damages that could adversely affect the Company’s financial condition. In addition, any insurance or indemnification rights that the Company may have may be insufficient or unavailable to protect against potential loss exposures.

The Company’s current insurance policies may not adequately protect the Company’s business from all potential risks.

The Company’s operations are subject to risks inherent in the oil and natural gas industry, such as, but not limited to, accidents, blowouts, explosions, fires, severe weather, oil and chemical spills, and other hazards. These conditions can result in personal injury or loss of life, damage to property, equipment and the environment, as well as suspension of customers’ oil and gas operations. These events could result in damages requiring costly repairs, the interruption of Company business, including the loss of revenue and profits, and/or the Company being named as a defendant in lawsuits asserting large claims. The Company does not have insurance against all foreseeable risks. Consequently, losses and liabilities arising from uninsured or underinsured events could have an adverse effect on the Company’s business, financial condition, and results of operations.

Regulatory pressures, environmental activism, and legislation could result in reduced demand for the Company’s products and services, increase the Company’s costs, and adversely affect the Company’s business, financial condition, and results of operations.

Regulations restricting volatile organic compounds (“VOC”) exist in many states and/or communities which limit demand for certain products. Although citrus oil is considered a VOC, its health, safety, and environmental profile is preferred over other solvents (e.g., BTEX), which is currently creating new market opportunities around the world. Changes in the perception of citrus oils as a preferred VOC, increased consumer activism against hydraulic fracturing or other

8

regulatory or legislative actions by governments could potentially result in materially reduced demand for the Company’s products and services and could adversely affect the Company’s business, financial condition, and results of operations.

The Company is subject to complex foreign, federal, state, and local environmental, health, and safety laws and regulations, which expose the Company to liabilities that could adversely affect the Company’s business, financial condition, and results of operations.

The Company’s operations are subject to foreign, federal, state, and local laws and regulations related to, among other things, the protection of natural resources, injury, health and safety considerations, chemical exposure assessment, waste management, and transportation of waste and other hazardous materials. The Company’s operations expose the Company to risks of environmental liability that could result in fines, penalties, remediation, property damage, and personal injury liability. In order to remain compliant with laws and regulations, the Company maintains permits, authorizations, registrations, and certificates as required from regulatory authorities. Sanctions for noncompliance with such laws and regulations could include assessment of administrative, civil and criminal penalties, revocation of permits, and issuance of corrective action orders.

The Company could incur substantial costs to ensure compliance with existing and future laws and regulations. Laws protecting the environment have generally become more stringent and are expected to continue to evolve and become more complex and restrictive into the future. Failure to comply with applicable laws and regulations could result in material expense associated with future environmental compliance and remediation. The Company’s costs of compliance could also increase if existing laws and regulations are amended or reinterpreted. Such amendments or reinterpretations of existing laws or regulations, or the adoption of new laws or regulations, could curtail exploratory or developmental drilling for, and production of, oil and natural gas which, in turn, could limit demand for the Company’s products and services. Some environmental laws and regulations could also impose joint and strict liability, meaning that the Company could be exposed in certain situations to increased liabilities as a result of the Company’s conduct that was lawful at the time it occurred or conduct of, or conditions caused by, prior operators or other third parties. Remediation expense and other damages arising as a result of such laws and regulations could be substantial and have a material adverse effect on the Company’s financial condition and results of operations.

Changes in law and regulation relating to hydraulic fracturing may have a negative effect on the Company’s operations.

Much of the Company’s revenue is derived from customers engaged in hydraulic fracturing services, a process that creates fractures extending from the well bore through the rock formation to enable natural gas or oil to flow more easily

through the rock pores to a production well. Some states have adopted regulations which require operators to publicly disclose certain non-proprietary information. These regulations could require the reporting and public disclosure of the Company’s proprietary chemistry formulas. In addition, several presidential candidates have proposed additional restrictions on hydraulic fracturing. The adoption of any future federal or state laws or local requirements, or the implementation of regulations imposing reporting obligations on, or otherwise limiting, the hydraulic fracturing process, could increase the difficulty of oil and natural gas well production activity and could have an adverse effect on the Company’s future results of operations.

Regulation of greenhouse gases and/or climate change could have a negative impact on the Company’s business.

Certain scientific studies have suggested that emissions of certain gases, commonly referred to as “greenhouse gases,” which include carbon dioxide, methane, and other volatile organic compounds, may be contributory to the warming effect of the Earth’s atmosphere and other climatic changes. In response to such studies, the issue of climate change and the effect of greenhouse gas emissions, in particular emissions from fossil fuels, is attracting increasing worldwide attention.

Existing or future laws, regulations, treaties, or international agreements related to greenhouse gases, climate change, and indoor air quality, including energy conservation or alternative energy incentives, could have a negative impact on the Company’s operations, if regulations resulted in a reduction in worldwide demand for oil and natural gas. Other results could be increased compliance costs and additional operating restrictions, each of which could have a negative impact on the Company’s operations.

The Company and the Company’s customers are subject to risks associated with doing business outside of the U.S., including political risk, foreign exchange risk, and other uncertainties.

The Company and its customers are subject to risks inherent in doing business outside of the U.S., including, but not limited to:

• | governmental instability; |

• | corruption; |

• | war and other international conflicts; |

• | civil and labor disturbances; |

• | requirements of local ownership; |

• | cartel behavior; |

• | partial or total expropriation or nationalization; |

• | currency devaluation; and |

• | foreign laws and policies, each of which can limit the movement of assets or funds or result in the deprivation of contractual rights or appropriation of property without fair compensation. |

9

Collections from international customers and agents could also prove difficult due to inherent uncertainties in foreign law and judicial procedures. The Company could experience significant difficulty with collections or recovery due to the political or judicial climate in foreign countries where Company operations occur or in which the Company’s products are used.

The Company’s international operations must be compliant with the Foreign Corrupt Practices Act (the “FCPA”) and other applicable U.S. laws. The Company could become liable under these laws for actions taken by employees or agents. Compliance with international laws and regulations could become more complex and expensive thereby creating increased risk as the Company’s international business portfolio grows. Further, the U.S. periodically enacts laws and imposes regulations prohibiting or restricting trade with certain nations. The U.S. government could also change these laws or enact new laws that could restrict or prohibit the Company from doing business in identified foreign countries. The Company conducts, and will continue to conduct, business in currencies other than the U.S. dollar. Historically, the Company has not hedged against foreign currency fluctuations. Accordingly, the Company’s profitability could be affected by fluctuations in foreign exchange rates.

The Company has no control over and can provide no assurances that future laws and regulations will not materially impact the Company’s ability to conduct international business.

The Company’s tax returns are subject to audit by tax authorities. Taxing authorities may make claims for back taxes, interest, and penalties.

The Company is subject to income, property, excise, employment, and other taxes in the U.S. and a variety of other jurisdictions around the world. Tax rules and regulations in the U.S. and around the world are complex and subject to interpretation. From time to time, taxing authorities conduct audits of the Company’s tax filings and may make claims for increased taxes and, in some cases, assess interest and penalties. The assessments for back taxes, interest, and penalties could be significant. If the Company is unsuccessful in contesting these claims, the resulting payments could result in a drain on the Company’s capital resources and liquidity.

Recent U.S. tax legislation, as well as future U.S. tax legislation, may adversely affect our business, results of operations, financial condition and cash flow.

Comprehensive tax reform legislation enacted in December 2017, commonly referred to as the Tax Cuts and Jobs Act (the “2017 Tax Act”), made significant changes to U.S. federal income 2017 tax laws. The 2017 Tax Act, among other things, reduced the corporate income tax rate to 21%, partially limits the deductibility of business interest expense and net operating losses, imposed a one-time tax on unrepatriated earnings from certain foreign subsidiaries, taxes offshore earnings at reduced rates regardless of whether they are repatriated and allows the

immediate deduction of certain new investments instead of deductions for depreciation expense over time. The 2017 Tax Act is complex and far-reaching, and the Company continues to evaluate the actual impact of its enactment on the Company. There may be material adverse effects resulting from the 2017 Tax Act that have not been identified and that could have an adverse effect on the Company’s business, results of operations, financial condition and cash flow.

Risks Related to the Company’s Industry

General economic declines (recessions), limits to credit availability, and industry specific factors could have an adverse effect on energy industry activity resulting in lower demand for the Company’s products and services.

Worldwide economic uncertainty can reduce the availability of liquidity and credit markets to fund the continuation and expansion of industrial business operations worldwide. The shortage of liquidity and credit combined with pressure on worldwide equity markets could continue to impact the worldwide economic climate. Geopolitical unrest around the world may also impact demand for the Company’s products and services both domestically and internationally.

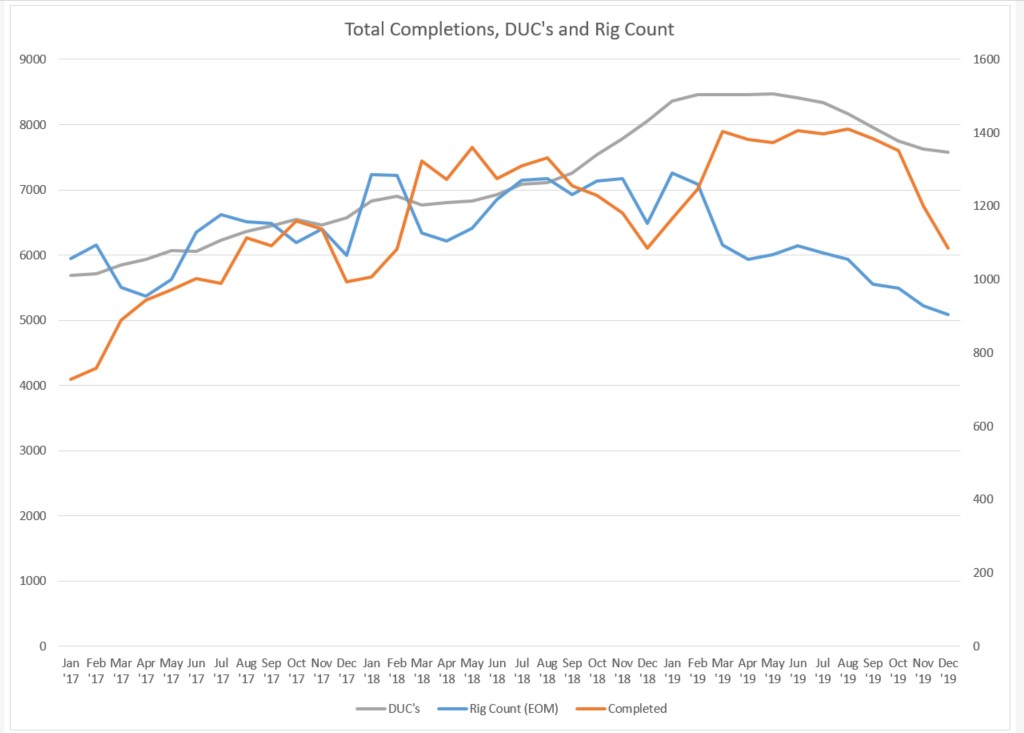

Demand for the Company’s ECT segment’s products and services is dependent on oil and natural gas industry activity and expenditure levels that are directly affected by trends in oil and natural gas prices. Demand for the Company’s products and services is particularly sensitive to levels of exploration, development, and production activity of, and the corresponding capital spending by, oil and natural gas companies, including national oil companies. One indication of drilling and completion activity and spending is rig count, which the Company monitors to gauge market conditions. In addition, the U.S. Energy Information Administration (“EIA”) and other industry data sources report completion activity which is utilized by the Company. Any prolonged reduction in oil and natural gas prices or drop in rig and/or completion count could depress current levels of exploration, development, and production activity. Perceptions of longer-term lower oil and natural gas prices by oil and natural gas companies could similarly reduce or defer major expenditures given the long-term nature of many large-scale development projects. Lower levels of activity could result in a corresponding decline in the demand for the Company’s oil and natural gas well products and services, which could have a material adverse effect on the Company’s revenue and profitability.

Events in global credit markets can significantly impact the availability of credit and associated financing costs for many of the Company’s customers. Many of the Company’s customers finance their drilling and completion programs through third-party lenders or public debt offerings. Lack of available credit or increased costs of borrowing could cause customers to reduce spending on drilling programs, thereby reducing demand and potentially resulting in lower prices for the Company’s products and services. Also, the credit and economic environment could significantly impact the

10

financial condition of some customers over a prolonged period, leading to business disruptions and restricted ability to pay for the Company’s products and services. The Company’s forward-looking statements assume that the Company’s lenders, insurers, and other financial institutions will be able to fulfill their obligations under various credit agreements, insurance policies, and contracts. If any of the Company’s significant lenders, insurers and others are unable to perform under such agreements, and if the Company was unable to find suitable replacements at a reasonable cost, the Company’s results of operations, liquidity, and cash flows could be adversely impacted.

A continuing period of depressed oil and natural gas prices could result in further reductions in demand for the Company’s products and services and adversely affect the Company’s business, financial condition, and results of operations.

The markets for oil and natural gas have historically been volatile. Such volatility in oil and natural gas prices, or the perception by the Company’s customers of unpredictability in oil and natural gas prices, could adversely affect spending levels. The oil and natural gas markets may be volatile in the future. The demand for the Company’s products and services is, in large part, driven by general levels of exploration and production spending and drilling activity by its customers. Future declines in oil or natural gas prices could adversely affect the Company’s business, financial condition, and results of operations.

New and existing competitors within the Company’s industry could have an adverse effect on results of operations.

The oil and natural gas industry is highly competitive. The Company’s principal competitors include numerous small companies capable of competing effectively in the Company’s markets on a local basis, as well as a number of large companies that possess substantially greater financial and other resources than does the Company. Larger competitors may be able to devote greater resources to developing, promoting, and selling products and services. The Company may also face increased competition due to the entry of new competitors including current suppliers that decide to sell their products and services directly to the Company’s customers. As a result of this competition, the Company could experience lower sales or greater operating costs, which could have an adverse effect on the Company’s margins and results of operations.

The Company’s industry has a high rate of employee turnover. Difficulty attracting or retaining personnel or agents could adversely affect the Company’s business.

The Company operates in an industry that has historically been highly competitive in securing qualified personnel with the required technical skills and experience. The Company’s services require skilled personnel able to perform physically demanding work. Due to industry volatility, the demanding nature of the work, and the need for industry specific

knowledge and technical skills, current employees could choose to pursue employment opportunities outside the Company that offer a more desirable work environment and/or higher compensation than is offered by the Company. As a result of these competitive labor conditions, the Company may not be able to find qualified labor, which could limit the Company’s growth. In addition, the cost of attracting and retaining qualified personnel has increased over the past several years due to competitive pressures. In order to attract and retain qualified personnel, the Company may be required to offer increased wages and benefits. If the Company is unable to increase the prices of products and services to compensate for increases in compensation, or is unable to attract and retain qualified personnel, operating results could be adversely affected.

Severe weather could have an adverse impact on the Company’s business.

The Company’s business could be materially and adversely affected by severe weather conditions. Hurricanes, tropical storms, flash floods, blizzards, cold weather, and other severe weather conditions could result in curtailment of services, damage to equipment and facilities, interruption in transportation of products and materials, and loss of productivity. If the Company’s customers are unable to operate or are required to reduce operations due to severe weather conditions, and as a result curtail purchases of the Company’s products and services, the Company’s business could be adversely affected.

A terrorist attack or armed conflict could harm the Company’s business.

Terrorist activities, anti-terrorist efforts, and other armed conflicts involving the U.S. could adversely affect the U.S. and global economies and could prevent the Company from meeting financial and other obligations. The Company could experience loss of business, delays or defaults in payments from payors, or disruptions of fuel supplies and markets if pipelines, production facilities, processing plants, or refineries are direct targets or indirect casualties of an act of terror or war. Such activities could reduce the overall demand for oil and natural gas which, in turn, could also reduce the demand for the Company’s products and services. Terrorist activities and the threat of potential terrorist activities and any resulting economic downturn could adversely affect the Company’s results of operations, impair the ability to raise capital, or otherwise adversely impact the Company’s ability to realize certain business strategies.

The Company may be adversely affected by the recent coronavirus outbreak.

In December 2019, a novel strain of coronavirus was reported to have surfaced in Wuhan, China. While we do not have any operations in China, our operations could be adversely affected to the extent that coronavirus or any other epidemic harms world economy in general and global demand for oil and gas in particular. Our operations may experience

11

disruptions in the event of a global pandemic or restriction on travel that results from a global pandemic, which may materially and adversely affect our business, financial condition and results of operations. The duration of the business disruption and related financial impact cannot be reasonably estimated at this time but may materially affect our ability to operate our business and result in additional costs. The extent to which the coronavirus or other health epidemic may impact our results will depend on future developments, which are highly uncertain and cannot be predicted.

Risks Related to the Company’s Securities

The market price of the Company’s common stock has been and may continue to be volatile.

The market price of the Company’s common stock has historically been subject to significant fluctuations. The following factors, among others, could cause the price of the Company’s common stock to fluctuate due to:

• | variations in the Company’s quarterly results of operations; |

• | changes in market valuations of companies in the Company’s industry; |

• | fluctuations in stock market prices and volume; |

• | fluctuations in oil and natural gas prices; |

• | issuances of common stock or other securities in the future; |

• | additions or departures of key personnel; |

• | announcements by the Company or the Company’s competitors of new business, acquisitions, or joint ventures; and |

• | negative statements made by external parties about the Company’s business in public forums. |

The stock market has experienced significant price and volume fluctuations in recent years that have affected the price of common stock of companies within many industries including the oil and natural gas industry. The price of the Company’s common stock could fluctuate based upon factors that have little to do with the Company’s operational performance, and these fluctuations could materially reduce the Company’s stock price. The Company could be a defendant in a legal case related to a significant loss of value for the shareholders. This could be expensive and divert management’s attention and Company resources, as well as have an adverse effect on the Company’s business, financial condition, and results of operations.

If the Company cannot meet the New York Stock Exchange continued listing requirements, the NYSE may delist the Company’s common stock.

The Company’s common stock is currently listed on the NYSE. In the future, if it is not able to meet the continued listing requirements of the NYSE, which require, among other things, that the average closing price of our common stock be above $1.00 over 30 consecutive trading days, the Company’s

common stock may be delisted. The Company’s closing stock price on March 3, 2020 was $1.47, and on December 31, 2019, closed at $2.00. If the Company is unable to satisfy the NYSE criteria for continued listing, its common stock would be subject to delisting. A delisting of its common stock could negatively impact the Company by, among other things, reducing the liquidity and market price of the its common stock; reducing the number of investors willing to hold or acquire the Company’s common stock, which could negatively impact its ability to raise equity financing; decreasing the amount of news and analyst coverage of the Company; and limiting the Company’s ability to issue additional securities or obtain additional financing in the future. In addition, delisting from the NYSE might negatively impact the Company’s reputation and, as a consequence, its business.

An active market for the Company’s common stock may not continue to exist or may not continue to exist at current trading levels.

Trading volume for the Company’s common stock historically has been very volatile when compared to companies with larger market capitalizations. The Company cannot presume that an active trading market for the Company’s common stock will continue or be sustained. Sales of a significant number of shares of the Company’s common stock in the public market could lower the market price of the Company’s stock.

The Company has no plans to pay dividends on the Company’s common stock, and, therefore, investors will have to look to stock appreciation for return on investments.

The Company does not anticipate paying any cash dividends on the Company’s common stock within the foreseeable future. Any payment of future dividends will be at the discretion of the Company’s board of directors and will depend, among other things, on the Company’s earnings, financial condition, capital requirements, level of indebtedness, statutory and contractual restrictions applying to the payment of dividends, and other considerations deemed relevant by the board of directors. Investors must rely on sales of common stock held after price appreciation, which may never occur, in order to realize a return on their investment. The lack of plans for dividends may make the stock of the Company an unattractive investment for investors who are seeking regular yield.

Certain anti-takeover provisions of the Company’s charter documents and applicable Delaware law could discourage or prevent others from acquiring the Company, which may adversely affect the market price of the Company’s common stock.

The Company’s certificate of incorporation and bylaws contain provisions that:

• | permit the Company to issue, without stockholder approval, up to 100,000 shares of preferred stock, in one or more series and, with respect to each series, to |

12

fix the designation, powers, preferences, and rights of the shares of the series;

• | prohibit stockholders from calling special meetings; |

• | limit the ability of stockholders to act by written consent; |

• | prohibit cumulative voting; and |

• | require advance notice for stockholder proposals and nominations for election to the board of directors to be acted upon at meetings of stockholders. |

In addition, Section 203 of the Delaware General Corporation Law limits business combinations with owners of more than 15% of the Company’s stock without the approval of the board of directors. Aforementioned provisions and other similar provisions make it more difficult for a third party to acquire the Company exclusive of negotiation. The Company’s board of directors could choose not to negotiate with an acquirer deemed not beneficial to or synergistic with the Company’s strategic outlook. If an acquirer were discouraged from offering to acquire the Company or prevented from successfully completing a hostile acquisition by these anti-takeover measures, stockholders could lose the opportunity to sell their shares at a favorable price.

Future issuance of additional shares of common stock could cause dilution of ownership interests and adversely affect the Company’s stock price.

The Company is currently authorized to issue up to 80,000,000 shares of common stock. The Company may, in the future, issue previously authorized and unissued shares of common stock, which would result in the dilution of current stockholders ownership interests. Additional shares are subject to issuance through various equity compensation plans or through the exercise of currently outstanding options. The potential issuance of additional shares of common stock may create downward pressure on the trading price of the Company’s common stock. The Company may also issue additional shares of common stock or other securities that are convertible into or exercisable for common stock in order to raise capital or effectuate other business purposes. Future sales of substantial amounts of common stock, or the perception that sales could occur, could have an adverse effect on the price of the Company’s common stock.

The Company may issue shares of preferred stock or debt securities with greater rights than the Company’s common stock.

Subject to the rules of the NYSE, the Company’s certificate of incorporation authorizes the board of directors to issue one

or more additional series of preferred stock and to set the terms of the issuance without seeking approval from holders of common stock. Currently, there are 100,000 preferred shares authorized, with no shares currently outstanding. Any preferred stock that is issued may rank senior to common stock in terms of dividends, priority and liquidation premiums, and may have greater voting rights than holders of common stock.

The Company’s ability to use net operating loss carryforwards and tax attribute carryforwards to offset future taxable income may be limited.