UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

For the fiscal year ended

OR

For the transition period from ____________ to ____________

Commission file number

(Exact name of registrant as specified in its charter)

| ||

(State or Other Jurisdiction of Incorporation or Organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

|

| |

|

| |

| ||

(Address of Principal Executive Offices) |

| (Zip Code) |

Registrant’s telephone number, including area code ( |

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol(s) |

| Name of each exchange on which registered | |

| The |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act ☐ Yes ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act ☐ Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | ☐ | ☒ | |

|

| ||

Non-accelerated filer | ☐ | Smaller reporting company | |

|

|

| |

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes

The aggregate market value of registrant’s common stock held by non-affiliates at June 30, 2023 was approximately $

As of March 14, 2024, there were

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the Registrant’s Proxy Statement for its Annual Meeting of Stockholders to be held on June 12, 2024, are incorporated by reference in Part III of this Report. Except as expressly incorporated by reference, the Registrant’s Proxy Statement shall not be deemed to be part of this Form 10-K.

Hudson Technologies, Inc.

Index

2

Part I

Item 1. Business

General

Hudson Technologies, Inc. (“Hudson” or the “Company”), incorporated under the laws of New York on January 11, 1991, is a refrigerant services company providing innovative solutions to recurring problems within the refrigeration industry. Hudson has proven, reliable programs that meet customer refrigerant needs by providing environmentally sustainable solutions from initial sale of refrigerant gas through recovery, reclamation and reuse, peak operating performance of equipment through energy efficiency and emergency air conditioning and refrigeration system repair, to final refrigerant disposal and carbon credit trading.

The Company’s operations consist of one reportable segment. The Company’s products and services are primarily used in commercial air conditioning, industrial processing and refrigeration systems, and include refrigerant and industrial gas sales, refrigerant management services consisting primarily of reclamation of refrigerants and RefrigerantSide® Services performed at a customer’s site. RefrigerantSide® Services consists of system decontamination to remove moisture, oils and other contaminants intended to restore systems to designed capacity.As a component of the Company’s products and services, the Company also participates in the generation of carbon offset projects. The Company operates principally through its wholly-owned subsidiary, Hudson Technologies Company. Unless the context requires otherwise, references to the “Company”, “Hudson”, “we”, “us”, “our”, or similar pronouns refer to Hudson Technologies, Inc. and its subsidiaries.

The Company’s executive offices are located at 300 Tice Boulevard, Suite 290, Woodcliff Lake, New Jersey and its telephone number is (845) 735-6000. The Company maintains a website at www.hudsontech.com, the contents of which are not incorporated into this filing.

Industry Background

The Company participates in an industry that is highly regulated, and changes in the regulations affecting our business could affect our operating results. Currently the Company purchases virgin and reclaimable hydrofluoro-olefin (“HFO”) and hydrofluorocarbon (“HFC”) refrigerants and reclaimable, primarily hydrochlorofluorocarbon (“HCFC”) and chlorofluorocarbon (“CFC”) refrigerants from suppliers and its customers. Effective January 1, 1996, the Clean Air Act, as amended (the “Act”) prohibited the production of virgin CFC refrigerants and limited the production of virgin HCFC refrigerants. Effective January 2004, the Act further limited the production of virgin HCFC refrigerants and federal regulations were enacted which established production and consumption allowances for HCFC refrigerants and which imposed limitations on the importation of certain virgin HCFC refrigerants. Under the Act, production of certain virgin HCFC refrigerants was phased out on December 31, 2019 and production of all virgin HCFC refrigerants is scheduled to be phased out by 2030.

The Act, and the federal regulations enacted under authority of the Act, have mandated and/or promoted responsible use practices in the air conditioning and refrigeration industry, which are intended to minimize the release of refrigerants into the atmosphere and encourage the recovery and re-use of refrigerants. The Act prohibits the venting of CFC, HFC and HCFC refrigerants, and prohibits and/or phases down the production of CFC and HCFC refrigerants.

The Act also mandates the recovery of CFC and HCFC refrigerants and promotes and encourages re-use and reclamation of CFC and HCFC refrigerants. Under the Act, owners, operators and companies servicing cooling equipment utilizing CFC and HCFC refrigerants are responsible for the integrity of the systems regardless of the refrigerant being used. In November 2016, the EPA issued a final rule extending these requirements to HFCs and to certain other refrigerants that are approved by the EPA as alternatives for CFC and HCFC refrigerants (the “608 Rule”).

3

HFC refrigerants are used as substitutes for CFC and HCFC refrigerants in certain applications. As a result of the increasing restrictions and limitations on the production and use of CFC and HCFC refrigerants, various sectors of the air conditioning and refrigeration industry have been replacing or modifying equipment that utilize CFC and HCFC refrigerants and have been transitioning to equipment that utilize HFC or HFO refrigerants. Certain HFC refrigerants are highly weighted greenhouse gases that are believed to contribute to global warming and climate change and, as a result, are now subject to various state regulations relating to the sale, use and emissions of HFC refrigerants, as well as federal restrictions on the production and consumption of HFCs under the AIM Act (as set forth below). The Company expects that HFC refrigerants eventually will be replaced by HFOs or other types of products with lower global warming potentials.

In October 2016, more than 200 countries, including the United States, agreed to amend the Montreal Protocol to phase down production of HFCs by 85% by 2047. The amendment establishes timetables for all developed and developing countries to freeze and then reduce production and use of HFCs, with the first reductions by developed countries in 2019. The amendment became effective January 1, 2019 as more than 197 countries have ratified the amendment.

AIM Act

The United States Environmental Protection Agency (“EPA”) issued several final rules establishing the framework to allocate allowances for virgin production and consumption of hydrofluorocarbon refrigerants (“HFCs”) that currently provide allowances through 2028. The EPA is responsible for the administration of the HFC phase down enacted by Congress under the AIM Act.

The AIM Act directs the EPA to address the reduction in virgin HFCs and provides authority to do so in three respects:

| 1) | phase down the production and consumption of listed HFCs, |

| 2) | manage these HFCs and their substitutes including reclamation of refrigerants, and |

| 3) | facilitate the transition to next-generation technologies. |

Congress required that the EPA consider ways to promote reclamation in all phases of its implementation of the AIM Act. The AIM Act introduced a stepdown of 10% from baseline levels in 2022 and 2023, and establishes a cumulative 40% reduction in the baseline for 2024. Hudson received allocation allowances for calendar years 2022, 2023 and 2024 equal to approximately 3 million, 3 million and 1.9 million Metric Tons Exchange Value Equivalents, respectively, per year, or approximately 1% of the total HFC consumption. Reclamation will be critical to maintaining necessary HFC supply levels to ensure an orderly phasedown. Reclamation is not subject to the allowance system or restricted from use.

On October 6, 2023, the EPA announced the latest actions to phase down HFCs under the AIM Act:

1) | Finalization of the Technology Transition Rule- The first new action is a final rule to accelerate the ongoing transition to more efficient and climate-safe technologies in new refrigeration, heating and cooling systems and other products by restricting the use of HFCs where alternatives are already available. The rule, which applies to both imported and domestically manufactured products, bans HFCs in certain equipment and sets a limit on the global warming potentials (GWPs) of the HFCs that can be used in each subsector, with compliance dates ranging from 2025 to 2028. |

In December 2023, the EPA announced an interim final rule on this matter, which provides an additional year, until January 1, 2026, for the installation of new residential and light commercial A/C and heat pump systems that use components manufactured or imported prior to January 1, 2025. Importantly, to qualify for the extended compliance deadline, all components of a system using the higher GWP HFC must be manufactured or imported prior to January 1, 2025.

2) | Proposed Refrigerant Management Rule- The second action is a proposed rule to better manage and reuse existing HFCs, including by reducing wasteful leaks from equipment and supporting HFC recycling and reclamation. The proposed rule, which is expected to be finalized during the third quarter of 2024, includes requirements for repairing leaky equipment, use of automatic leak detection systems on large refrigeration systems, use of reclaimed HFCs for certain applications, recovery of HFCs from cylinders before their disposal, and a container tracking system. |

4

Products and Services

Sustainability

From its inception, the Company has sold refrigerants, and has provided refrigerant reclamation and refrigerant management services that are designed to recover and reuse refrigerants, thereby protecting the environment from release of refrigerants to the atmosphere and the corresponding ozone depletion and global warming impact and supporting the circular economy. The reclamation process allows the refrigerant to be re-used thereby eliminating the need to destroy or manufacture additional refrigerant and eliminating the corresponding impact to the environment associated with the destruction and manufacturing. The Company believes it is the largest refrigerant reclaimer in the United States. In addition, the Company participates in the creation and monetization of verified emission reductions utilizing third party protocols.

The Company provides a complete offering of refrigerant management services, which primarily include reclamation of refrigerants, laboratory testing through the Company’s laboratory, which has been certified by the Air Conditioning, Heating and Refrigeration Institute (“AHRI”), and banking (storage) services tailored to individual customer requirements. The Company also separates “crossed” (i.e. commingled) refrigerants and provides re-usable cylinder refurbishment and hydrostatic testing services.

The Company has also created alternative solutions to reactive and preventative maintenance procedures that are performed on commercial and industrial refrigeration systems. These services, known as RefrigerantSide® Services, reduce the system’s energy consumption and improve the system’s operating performance, and complement the Company’s refrigerant sales and refrigerant reclamation and management services. These services also preserve system refrigerant charges, reducing the need for manufacture of additional refrigerant.

Refrigerant and Industrial Gas Sales

The Company sells reclaimed and virgin (new) refrigerants to a variety of customers in the air conditioning and refrigeration industry. The Company continues to sell reclaimed CFC and certain HCFC based refrigerants, which are no longer manufactured, and HFC’s, which are being phased down as discussed above. The Company purchases virgin refrigerants, such as HFC’s and HFO’s, from several suppliers and resold by the Company. Additionally, the Company regularly purchases used or contaminated refrigerants, from many different sources, which refrigerants are then reclaimed using the Company’s high speed proprietary reclamation equipment, its proprietary Zugibeast® system, and then are resold by the Company.

The Company also sells industrial gases to a variety of industry customers, predominantly to users in or involved with the US Military. In July 2016 the Company was awarded, as prime contractor, a five-year contract, together with a five-year renewal option which was exercised in July 2021, by the United States Defense Logistics Agency (“DLA”) for the management, supply, and sale of refrigerants, compressed gases, cylinders and related services.

RefrigerantSide® Services

The Company provides decontamination and recovery services that are performed at a customer’s site through the use of portable, high volume, high-speed proprietary equipment, including the proprietary Zugibeast® system. Certain of these RefrigerantSide® Services, which encompass system decontamination, and refrigerant recovery and reclamation, are also proprietary and are covered by process patents.

In addition to the decontamination and recovery services previously described, the Company also provides predictive and diagnostic services for its customers. The Company offers diagnostic services that are intended to predict potential problems in air conditioning, process cooling and refrigeration systems before they occur. The Company’s Chiller Chemistry® offering integrates several fluid tests of an operating system and the corresponding laboratory results into an engineering report providing its customers with an understanding of the current condition of the fluids, the cause for any abnormal findings and the potential consequences if the abnormal findings are not remediated. Fluid Chemistry®, an abbreviated version of the Company’s Chiller Chemistry® offering, is designed to quickly identify systems that require further examination.

5

The Company has also been awarded several US patents for its SmartEnergy OPS®, which is a system for measuring, modifying and improving the efficiency of energy systems, including air conditioning and refrigeration systems, in industrial and commercial applications. This service is a web-based real time continuous monitoring service applicable to a facility’s chiller plant systems. The SmartEnergy OPS® offering enables customers to monitor and improve their chiller plant performance and proactively identify and correct system inefficiencies. SmartEnergy OPS® is able to identify specific inefficiencies in the operation of chiller plant systems and, when used with Hudson’s RefrigerantSide ® Services, can increase the efficiency of the operating systems thereby reducing energy usage and costs. Improving the system efficiency reduces power consumption thereby directly reducing CO 2 emissions at the power plants or onsite. Lastly, the Company’s ChillSmart® offering, which combines the system optimization with the Company’s Chiller Chemistry ® offering, provides a snapshot of a packaged chiller’s operating efficiency and health. ChillSmart® provides a very effective predictive maintenance tool and helps our customers to identify the operating chillers that cause higher operating costs.

The Company’s engineers who developed and support SmartEnergy OPS® are recognized as Energy Experts and Qualified Best Practices Specialists by the United States Department of Energy (“DOE”) in the areas of Steam and Process Heating under the DOE “Best Practices” program, and are the Lead International Energy Experts for steam, chillers and refrigeration systems for the United Nations Industrial Development Organization (“UNIDO”). The Company’s staff have trained more than 4,000 industrial plant personnel in the US and internationally and have developed, and are currently delivering, training curriculums in 12 different countries. The Company’s staff have completed more than 200 industrial ESAs in the US and internationally.

Carbon Offset Projects

CFC refrigerants are ozone depleting substances and are also highly weighted greenhouse gases that contribute to global warming and climate change. The destruction of CFC refrigerants may be eligible for verified emission reductions that can be converted and monetized into carbon offset credits, which then can be traded in the emerging carbon offset markets. The Company is pursuing opportunities to acquire CFC refrigerants and is developing relationships within the emerging environmental markets in order to implement opportunities for the creation and monetization of verified emission reductions from the destruction of CFC refrigerants.

In October 2015, the American Carbon Registry (“ACR”) established a methodology to provide, among other things, a quantification framework for the creation of carbon offset credits for the use of certified reclaimed HFC refrigerants. The Company is pursuing opportunities to acquire HFC refrigerants and is developing relationships within the emerging environmental markets in order to implement opportunities for the creation and monetization of verified emission reductions from the reclamation of HFC refrigerants.

Suppliers

The Company purchases refrigerants from a variety of manufacturers, wholesalers, distributors, bulk gas brokers and from other sources within the air conditioning, refrigeration and automotive aftermarket industries.

Customers

The Company provides its products and services to commercial, industrial and governmental customers, as well as to refrigerant wholesalers, distributors, contractors and to refrigeration equipment manufacturers. Agreements with larger customers generally provide for standardized pricing for specified services. The Company generates sales by customer purchase order on a real-time basis and therefore does not carry a backlog of sales.

For the year ended December 31, 2023, there was one customer accounting for greater than 10% of the Company’s revenues and one customer accounted for over 10% of the outstanding accounts receivable at December 31, 2023. For the year ended December 31, 2022, there was no customer that accounted for 10% of the Company’s revenues, but one customer accounted for over 10% of the outstanding accounts receivable at December 31, 2022. For the year ended December 31, 2021, one customer accounted for 10% of the Company’s revenues and one customer accounted for over 10% of the outstanding accounts receivable at December 31, 2021.

6

Strategic Relationships

Hudson announced the following strategic relationships:

| - | In, January 2022, Hudson entered into an agreement with AprilAire, the leading provider of professional grade healthy air solutions for homes, to meet the requirements of the recently finalized California Air Resources Board (CARB) Regulation Order for Reclaimed Refrigerant Use for Manufacturers of AC Equipment. Hudson will supply reclaimed refrigerant to AprilAire for use in its range of healthy indoor air quality solutions. |

| - | In, August 2022, Hudson entered into an agreement with Lennox International Inc., a global leader in energy-efficient climate-control solutions, to align their efforts to meet the CARB Regulation Order for Certified Reclaimed Refrigerant Use Requirements for Manufacturers of AC Equipment. Under the agreement, Hudson will be the exclusive supplier of certified reclaimed refrigerants to Lennox for the aftermarket support of their residential HVAC systems. |

Marketing

Marketing programs are conducted through the efforts of the Company’s executive officers, marketing personnel and Company sales personnel. Hudson employs various marketing methods, including digital marketing, segment targeted outreach, social media, trade and industry events, webinars, in-person solicitation, print advertising, response to quotation requests and the internet through the Company’s website (www.hudsontech.com). Information on the Company’s website is not part of this report.

The Company’s sales personnel are compensated on a combination of a base salary and commission. The Company’s executive officers devote significant time and effort to customer relationships.

Competition

The Company competes primarily on the basis of the performance of its proprietary high volume, high-speed equipment used in its operations, the breadth of services offered by the Company, including proprietary RefrigerantSide® Services and other on-site services, and price, particularly with respect to refrigerant sales.

The Company competes with numerous regional and national companies that market reclaimed and virgin refrigerants and provide refrigerant reclamation services. Certain of these competitors may possess greater financial, marketing, distribution and other resources for the sale and distribution of refrigerants than the Company.

Hudson’s RefrigerantSide® Services provide solutions to certain problems within the refrigeration industry and, as such, the demand and market acceptance for these services are subject to uncertainty. Competition for these services primarily consists of traditional periodic maintenance and repair methods of solving the industry’s problems. The Company’s marketing strategy is to educate the marketplace that its alternative solutions are available and that RefrigerantSide® Services are superior to traditional methods.

Risk Management

The Company carries insurance coverage that it considers sufficient to protect the Company’s assets and operations. The Company attempts to operate in a professional and prudent manner and to reduce potential liability risks through specific risk management efforts, including ongoing employee training.

The refrigerant industry involves potentially significant risks of statutory and common law liability for environmental damage and personal injury. The Company, and in certain instances, its officers, directors and employees, may be subject to claims arising from the Company’s on-site or off-site services, including the improper release, spillage, misuse or mishandling of refrigerants classified as hazardous or non-hazardous substances or materials. The Company may be held strictly liable for damages, which could be substantial, regardless of whether it exercised due care and complied with all relevant laws and regulations.

Hudson maintains environmental impairment insurance of $10,000,000 per occurrence, and $10,000,000 annual in the aggregate.

7

Government Regulation

The business of refrigerant and industrial gas sales, reclamation and management is subject to extensive, stringent and frequently changing federal, state and local laws and substantial regulation under these laws by governmental agencies, including the EPA, the United States Occupational Safety and Health Administration (“OSHA”) and the United States Department of Transportation (“DOT”).

Among other things, these regulatory authorities impose requirements which regulate the handling, packaging, labeling, transportation and disposal of hazardous and non-hazardous materials and the health and safety of workers, and require the Company and, in certain instances, its employees, to obtain and maintain licenses in connection with its operations. This extensive regulatory framework imposes significant compliance burdens and risks on the Company.

Hudson and its customers are subject to the requirements of the Clean Air Act and the AIM Act, and the regulations promulgated thereunder by the EPA, which make it unlawful for any person in the course of maintaining, servicing, repairing, and disposing of air conditioning or refrigeration equipment, to knowingly vent or otherwise release or dispose of ozone depleting substances, and non-ozone depleting substitutes, used as refrigerants.

Pursuant to the Act, reclaimed refrigerant must satisfy the same purity standards as newly manufactured, virgin refrigerants in accordance with standards established by AHRI prior to resale to a person other than the owner of the equipment from which it was recovered. The EPA administers a certification program pursuant to which applicants certify to reclaim refrigerants in compliance with AHRI standards. The Company has two of only four certified refrigerant testing laboratories in the United States under AHRI’s laboratory certification program, which is a voluntary program that certifies the ability of a laboratory to test refrigerant in accordance with the AHRI 700 standard. In addition, the EPA has established a mandatory certification program for air conditioning and refrigeration technicians. Hudson’s technicians have applied for or obtained such certification.

The Company may also be subject to regulations adopted by the EPA which impose reporting requirements arising out of the importation, purchase, production, use and/or emissions of certain greenhouse gases, including HFCs.

The Company is also subject to regulations adopted by the DOT which classify most refrigerants and industrial gases handled by the Company as hazardous materials or substances and imposes requirements for handling, packaging, labeling and transporting refrigerants and which regulate the use and operation of the Company’s commercial motor vehicles used in the Company’s business.

The Resource Conservation and Recovery Act of 1976, as amended (“RCRA”), requires facilities that treat, store or dispose of hazardous wastes to comply with certain operating standards. Before transportation and disposal of hazardous wastes off-site, generators of such waste must package and label their shipments consistent with detailed regulations and prepare a manifest identifying the material and stating its destination. The transporter must deliver the hazardous waste in accordance with the manifest to a facility with an appropriate RCRA permit. Under RCRA, impurities removed from refrigerants consisting of oils mixed with water and other contaminants are not presumed to be hazardous waste.

The Emergency Planning and Community Right-to-Know Act of 1986, as amended, requires the annual reporting by the Company of Emergency and Hazardous Chemical Inventories (Tier II reports) to the various states in which the Company operates and requires the Company to file annual Toxic Chemical Release Inventory Forms with the EPA.

The Comprehensive Environmental Response, Compensation and Liability Act of 1980 (“CERCLA”), establishes liability for clean-up costs and environmental damages to current and former facility owners and operators, as well as persons who transport or arrange for transportation of hazardous substances. Almost all states have similar statutes regulating the handling and storage of hazardous substances, hazardous wastes and non-hazardous wastes. Many such statutes impose requirements that are more stringent than their federal counterparts. The Company could be subject to substantial liability under these statutes to private parties and government entities, in some instances without any fault, for fines, remediation costs and environmental damage, as a result of the mishandling, release, or existence of any hazardous substances at any of its facilities.

The Occupational Safety and Health Act of 1970, as amended, mandates requirements for a safe work place for employees and special procedures and measures for the handling of certain hazardous and toxic substances. State laws, in certain circumstances, mandate additional measures for facilities handling specified materials. The Company is also subject to regulations adopted by the California Air Resources Board which impose certain reporting requirements arising out of the reclamation and sale of refrigerants that takes place within the State of California.

8

The Company believes that it is in material compliance with all applicable regulations that are material to its business operations.

Quality Assurance & Environmental Compliance

The Company utilizes in-house quality and regulatory compliance control procedures. Hudson maintains its own analytical testing laboratories, which are AHRI certified, to assure that reclaimed refrigerants comply with AHRI purity standards and employs portable testing equipment when performing on-site services to verify certain quality specifications. The Company employs twelve persons engaged full-time in quality control and to monitor the Company’s operations for regulatory compliance.

Human Capital Resources

On February 1, 2024, the Company had 237 full time employees including air conditioning and refrigeration technicians, chemists, engineers, sales and administrative personnel. None of the Company’s employees are represented by a union. The Company believes it has good relations with its employees.

Patents and Proprietary Information

The Company holds several U.S. and foreign patents, as well as pending patent applications, related to certain RefrigerantSide® Services and supporting systems developed by the Company for systems and processes for measuring and improving the efficiency of refrigeration systems, and for certain refrigerant recycling and reclamation technologies. These patents will expire between December 2024 and December 2036.

There can be no assurance as to the breadth or degree of protection that patents may afford the Company, that any patent applications will result in issued patents or that patents will not be circumvented or invalidated. Technological development in the refrigerant industry may result in extensive patent filings and a rapid rate of issuance of new patents. Although the Company believes that its existing patents and the Company’s equipment do not and will not infringe upon existing patents or violate proprietary rights of others, it is possible that the Company’s existing patent rights may not be valid or that infringement of existing or future patents or violations of proprietary rights of others may occur. In the event the Company’s equipment or processes infringe, or are alleged to infringe, patents or other proprietary rights of others, the Company may be required to modify the design of its equipment or processes, obtain a license or defend a possible patent infringement action. There can be no assurance that the Company will have the financial or other resources necessary to enforce or defend a patent infringement or proprietary rights violation action or that the Company will not become liable for damages.

The Company also relies on trade secrets and proprietary know-how, and employs various methods to protect its technology. However, such methods may not afford complete protection and there can be no assurance that others will not independently develop such know-how or obtain access to the Company’s know-how, concepts, ideas and documentation. Failure to protect its trade secrets could have a material adverse effect on the Company.

SEC Filings

The Company makes available on its internet website copies of its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments thereto, as soon as reasonably practicable after they are filed with the Securities and Exchange Commission.

Item 1A. Risk Factors

There are many important factors, including those discussed below (and above as described under “Business-Patents and Proprietary Information”), that have affected, and in the future could affect Hudson’s business including, but not limited to, the factors discussed below, which should be reviewed carefully together with the other information contained in this report. Some of the factors are beyond Hudson’s control and future trends are difficult to predict.

9

Risks Related to Business Strategy and Operations

Our existing and future debt obligations could impair our liquidity and financial condition.

Our existing credit facility, consisting of an asset-based lending facility of up to $75 million from Wells Fargo Bank, National Association (“Wells Fargo Bank”) and other lenders, is secured by substantially all of our assets and contains formulas that limit the amount of our future borrowings under that facility. Moreover, the terms of our credit facility also includes financial and negative covenants that, among other things, may limit our ability to incur additional indebtedness. If we violate any loan covenants and do not obtain a waiver from our lenders, our indebtedness under the credit facilities would become immediately due and payable, and the lenders could foreclose on their security, which could materially adversely affect our business and future financial condition and could require us to curtail or otherwise cease our existing operations.

Our revenues, results of operations and cash flows could be materially and adversely affected by changes in commodity prices.

Our revenues, results of operations and cash flows are affected by market prices for refrigerant gases. Commodity prices generally are affected by a wide range of factors beyond our control, including weather, seasonality, the availability and adequacy of supply, government regulation and policies and general political and economic conditions. We are exposed to fluctuating commodity prices as the result of our inventory of various refrigerant gases. At any time, our inventory levels may be substantial. We have processes in place to monitor exposures to these risks and engage in strategies to manage these risks. If these controls and strategies are not successful in mitigating our exposure to these fluctuations, we could be materially and adversely affected.

We may need additional financing to satisfy our future capital requirements, which may not be readily available to us.

Our capital requirements may be significant in the future. We may incur additional expenses in the development and implementation of our operations. Due to fluctuations in the price, demand and availability of new refrigerants, our existing credit facility led by Wells Fargo Bank that expires in March 2027 may not in the future be sufficient to provide all of the capital that we need to acquire and manage our inventories of new refrigerant. As a result, we may be required to seek additional equity or debt financing in order to develop our RefrigerantSide® Services business, our refrigerant sales business and our other businesses. We have no current arrangements with respect to, or sources of, additional financing other than our existing credit facility. There can be no assurance that we will be able to obtain any additional financing on terms acceptable to us or at all. Our inability to obtain financing, if and when needed, could materially adversely affect our business and future financial condition and could require us to curtail or otherwise cease our existing operations.

Adverse weather or economic downturn could adversely impact our financial results.

Our business could be negatively impacted by adverse weather or economic downturns. Weather is a significant factor in determining market demand for the refrigerants sold by us, and to a lesser extent, our RefrigerantSide® Services. Unusually cool temperatures in the spring and summer tend to depress demand for, and price of, refrigerants we sell. Protracted periods of cooler than normal spring and summer weather could result in a substantial reduction in our sales which could adversely affect our financial position as well as our results of operations. An economic downturn could cause customers to postpone or cancel purchases of the Company’s products or services. Either or both of these conditions could have severe negative implications to our business that may exacerbate many of the risk factors we identified in this report but not limited, to the following:

Liquidity

These conditions could reduce our liquidity, which could have a negative impact on our financial condition and results of operations.

Demand

These conditions could lower the demand and/or price for our product and services, which would have a negative impact on our results of operations.

Financial Covenants

These conditions could impact our ability to meet our loan covenants which, if we are unable to obtain a waiver from our lenders, could materially adversely affect our business and future financial condition and could require us to curtail or otherwise cease our existing operations.

10

Our business is impacted by customer concentration.

In July 2016, we were awarded, as prime contractor, a five-year contract, including a five-year renewal option (which has been exercised), by the United States Defense Logistics Agency (“DLA”) for the management and supply of refrigerants, compressed gases, cylinders and related items to US Military commands and installations, Federal civilian agencies and foreign militaries. Our contract with DLA expires in July 2026. For the years ended December 31, 2023, 2022 and 2021, the DLA accounted for 18%, 8% and 10% of our revenues. The loss of DLA as a customer could have a material adverse effect on our financial position and results of operations.

Our information technology systems, processes, and sites may suffer interruptions, failures, or attacks which could affect our ability to conduct business.

Our information technology systems provide critical data connectivity, information and services for internal and external users. These include, among other things, processing transactions, summarizing and reporting results of operations, complying with regulatory, legal or tax requirements, storing project information and other processes necessary to manage the business. Our systems and technologies, or those of third parties on which we rely, could fail or become unreliable due to equipment failures, software viruses, cyber threats, terrorist acts, natural disasters, power failures or other causes. Cybersecurity threats are evolving and include, but are not limited to, malicious software, cyber espionage, attempts to gain unauthorized access to our sensitive information, including that of our customers, suppliers, and subcontractors, and other electronic security breaches that could lead to disruptions in mission critical systems, unauthorized release of confidential or otherwise protected information, and corruption of data. Although we utilize various procedures and controls to monitor and mitigate these threats, there can be no assurance that these procedures and controls will be sufficient to prevent security threats from materializing. If any of these events were to materialize, the costs related to cyber or other security threats or disruptions may not be fully insured or indemnified and could have a material adverse effect on our reputation, operating results, and financial condition.

Risks Related to Regulatory and Environmental Matters

The nature of our business exposes us to potential liability.

The refrigerant recovery and reclamation industry involves potentially significant risks of statutory and common law liability for environmental damage and personal injury. We, and in certain instances, our officers, directors and employees, may be subject to claims arising from our on-site or off-site services, including the improper release, spillage, misuse or mishandling of refrigerants classified as hazardous or non-hazardous substances or materials. We may be strictly liable for damages, which could be substantial, regardless of whether we exercised due care and complied with all relevant laws and regulations. Our current insurance coverage may not be sufficient to cover potential claims, and adequate levels of insurance coverage may not be available in the future at a reasonable cost. A partially or completely uninsured claim against us, if successful and of sufficient magnitude would have a material adverse effect on our business and financial condition.

Our business and financial condition is substantially dependent on the sale and continued environmental regulation of refrigerants.

Our business and prospects are largely dependent upon continued regulation of the use and disposition of refrigerants. Changes in government regulations relating to the emission of refrigerants into the atmosphere could have a material adverse effect on us. Failure by government authorities to otherwise continue to enforce existing regulations or significant relaxation of regulatory requirements could also adversely affect demand for our services and products.

Our business is subject to significant regulatory compliance burdens.

The refrigerant reclamation and management business is subject to extensive, stringent and frequently changing federal, state and local laws and substantial regulation under these laws by governmental agencies, including the EPA, the OSHA and DOT. Although we believe that we are in material compliance with all applicable regulations material to our business operations, amendments to existing statutes and regulations or adoption of new statutes and regulations that affect the marketing and sale of refrigerant could require us to continually alter our methods of operation and/or discontinue the sale of certain of our products resulting in costs to us that could be substantial. We may not be able, for financial or other reasons, to comply with applicable laws, regulations and permit requirements, particularly as we seek to enter into new geographic markets. Our failure to comply with applicable laws, rules or regulations or permit requirements could subject us to civil remedies, including substantial fines, penalties and injunctions, as well as possible criminal sanctions, which would, if of significant magnitude, materially adversely impact our operations and future financial condition.

11

A number of factors could negatively impact the price and/or availability of refrigerants, which would, in turn, adversely affect our business and financial condition.

Refrigerant sales continue to represent a significant majority of our revenues. Therefore, our business is substantially dependent on the availability of both new and used refrigerants in large quantities, which may be affected by several factors including, without limitation: (i) commercial production and consumption limitations imposed by the Act and legislative limitations and ban on HCFC refrigerants; (ii) the amendment to the Montreal Protocol, the AIM Act, and any legislation and regulation enacted to implement the amendment, imposes limitations on production and consumption of HFC refrigerants; (iii) introduction of new refrigerants and air conditioning and refrigeration equipment; (iv) price competition resulting from additional market entrants; (v) changes in government regulation on the use and production of refrigerants; and (vi) reduction in price and/or demand for refrigerants. Sufficient amounts of new and/or used refrigerants may not be available to us in the future, particularly as a result of the further phase down of HFC production, or may not be available on commercially reasonable terms. Additionally, we may be subject to price fluctuations, periodic delays or shortages of new and/or used refrigerants. Our failure to obtain and resell sufficient quantities of virgin refrigerants on commercially reasonable terms, or at all, or to obtain, reclaim and resell sufficient quantities of used refrigerants would have a material adverse effect on our operating margins and results of operations.

Issues relating to potential global warming and climate change could have an impact on our business.

Refrigerants are considered to be strong greenhouse gases that are believed to contribute to global warming and climate change and are now subject to various state and federal regulations relating to the sale, use and emissions of refrigerants. Current and future global warming and climate change or related legislation and/or regulations may impose additional compliance burdens on us and on our customers and suppliers which could potentially result in increased administrative costs, decreased demand in the marketplace for our products, and/or increased costs for our supplies and products. In addition, an amendment to the Montreal Protocol has established timetables for all developed and developing countries to freeze and then reduce production and use of HFCs by 85% by 2047, with the first reductions by developed countries in 2019. The amendment became effective January 1, 2019. In December 2020, AIM Act legislation was enacted in the United States that requires the phasedown of virgin production of HFCs.

Risks Related to Our Common Stock and Other General Risks

As a result of competition, and the strength of some of our competitors in the market, we may not be able to compete effectively.

The markets for our services and products are highly competitive. We compete with numerous regional and national companies which provide refrigerant recovery and reclamation services, as well as companies which market and deal in new and reclaimed alternative refrigerants, including certain of our suppliers, some of which possess greater financial, marketing, distribution and other resources than us. We also compete with numerous manufacturers of refrigerant recovery and reclamation equipment. Certain of these competitors have established reputations for success in the service of air conditioning and refrigeration systems. We may not be able to compete successfully, particularly as we seek to enter into new markets.

We have the ability to designate and issue preferred stock, which may have rights, preferences and privileges greater than Hudson’s common stock and which could impede a subsequent change in control of us.

Our Certificate of Incorporation authorizes our Board of Directors to issue up to 5,000,000 shares of “blank check” preferred stock and to fix the rights, preferences, privileges and restrictions, including voting rights, of these shares, without further shareholder approval. The rights of the holders of our common stock will be subject to, and may be adversely affected by, the rights of holders of any additional preferred stock that may be issued by us in the future. Our ability to issue preferred stock without shareholder approval could have the effect of making it more difficult for a third party to acquire a majority of our voting stock, thereby delaying, deferring or preventing a change in control of us.

If our common stock were delisted from NASDAQ it could be subject to “penny stock” rules which would negatively impact its liquidity and our shareholders’ ability to sell their shares.

Our common stock is currently listed on the NASDAQ Capital Market. We must comply with numerous NASDAQ Marketplace rules in order to continue the listing of our common stock on NASDAQ. There can be no assurance that we can continue to meet the rules required to maintain the NASDAQ listing of our common stock. If we are unable to maintain our listing on NASDAQ, the market liquidity of our common stock may be severely limited.

12

Our management has significant control over our affairs.

Currently, our officers and directors collectively beneficially own approximately 7.8% of our outstanding common stock. Accordingly, our officers and directors are in a position to significantly affect major corporate transactions and the election of our directors. There is no provision for cumulative voting for our directors.

We may fail to successfully integrate any additional acquisitions made by us into our operations.

As part of our business strategy, we may look for opportunities to grow by acquiring other product lines, technologies or facilities that complement or expand our existing business. We may be unable to identify additional suitable acquisition candidates or negotiate acceptable terms. In addition, we may not be able to successfully integrate any assets, liabilities, customers, systems or management personnel we may acquire into our operations and we may not be able to realize related revenue synergies and cost savings within expected time frames. There can be no assurance that we will be able to successfully integrate any prior or future acquisition.

Item 1B. Unresolved Staff Comments

None.

Item 1C. Cybersecurity

Risk Management and Strategy

Our corporate information technology, communication networks, enterprise applications, accounting and financial reporting platforms, and related systems, and those that we offer to our customers are necessary for the operation of our business. We use these systems, among others, to manage our customer and vendor relationships, for internal communications, for accounting to operate record-keeping functions, and for many other key aspects of our business. Our business operations rely on the secure collection, storage, transmission, and other processing of proprietary, confidential, and sensitive data.

We have implemented and maintain various information security processes designed to identify, assess and manage material risks from cybersecurity threats to our critical computer networks, third-party hosted services, communications systems, hardware and software, and our critical data, including intellectual property, confidential information that is proprietary, strategic or competitive in nature, and tenant data (“Information Systems and Data”).

We rely on a multidisciplinary team, including our information security function, legal department, management, and third-party service providers, as described further below, to identify, assess, and manage cybersecurity threats and risks. We identify and assess risks from cybersecurity threats by monitoring and evaluating our threat environment and our risk profile using various methods including, for example, using manual and automated tools, subscribing to reports and services that identify cybersecurity threats, analyzing reports of threats and threat actors, conducting scans of the threat environment, evaluating our industry’s risk profile, utilizing internal and external audits, and conducting threat and vulnerability assessments.

Depending on the environment, we implement and maintain various technical, physical, and organizational measures, processes, standards, and/or policies designed to manage and mitigate material risks from cybersecurity threats to our Information Systems and Data, including risk assessments, incident detection and response, vulnerability management, disaster recovery and business continuity plans, internal controls within our accounting and financial reporting functions, encryption of data, network security controls, access controls, physical security, asset management, systems monitoring, vendor risk management program, employee training, and penetration testing.

We work with third parties from time to time that assist us to identify, assess, and manage cybersecurity risks, including professional services firms, consulting firms, threat intelligence service providers, and penetration testing firms.

To operate our business, we utilize certain third-party service providers to perform a variety of functions. We seek to engage reliable, reputable service providers that maintain cybersecurity programs. Depending on the nature of the services provided, the sensitivity and quantity of information processed, and the identity of the service provider, our vendor management process may include reviewing the cybersecurity practices of such provider, contractually imposing obligations on the provider, conducting security assessments, and conducting periodic reassessments during their engagement.

13

We are not aware of any risks from cybersecurity threats, including as a result of any cybersecurity incidents, which have materially affected or are reasonably likely to materially affect our Company, including our business strategy, results of operations, or financial condition.

Governance

Our full Board oversees the Company’s enterprise risk management process, including the management of risks arising from cybersecurity threats. The Board receives regular presentations and reports from management who are responsible for managing and assessing cybersecurity risks, which address a wide range of topics including recent developments, evolving standards, vulnerability assessments, third-party and independent reviews, the threat environment, technological trends and information security considerations. The Board also receives prompt and timely information regarding any cybersecurity incident that meets established reporting thresholds, as well as ongoing updates regarding any such incident until it has been addressed.

Management plays a crucial role in assessing and managing material risks from cybersecurity threats. At the management level, the Company’s cybersecurity risk management and strategy is led by its Director of IT, who reports to the CFO. The qualifications of the Director of IT include over 25 years of IT management, cybersecurity, and information governance experience. The Director of IT is regularly informed about the latest developments in cybersecurity, including emerging threats and technologies to adapt security measures accordingly. This ongoing knowledge acquisition is crucial for the effective prevention, detection, mitigation, and remediation of cybersecurity incidents. Management’s role includes:

| ● | Risk Assessment: Management conducts annual cybersecurity risk assessments to identify and evaluate potential threats and vulnerabilities. Management considers the likelihood and potential impact of various cybersecurity risks, considering the Company’s assets, systems, and operations, to prioritize mitigation efforts. |

| ● | Cybersecurity Policies and Procedures: Management reviews and approves the Company’s cybersecurity policies and procedures and communicates these policies and procedures to all employees to ensure adherence to established security protocols. |

| ● | Compliance with Regulations: Management implements and maintains compliance with relevant cybersecurity regulations and standards applicable to the Company. |

| ● | Budgeting and Resource Allocation: Management reviews budgets for cybersecurity initiatives and ensures that adequate resources are allocated to address cybersecurity risks and that investments in cybersecurity align with the Company’s risk tolerance and strategic objectives. |

The Director of IT is promptly informed of potential cybersecurity risks, threats, and vulnerabilities by the Company’s IT Helpdesk. Once an incident has been identified, the Director of IT and the IT network security team assess the criticality and impact of the incident on the Company’s business operations. The Director of IT then formulates and oversees a response to contain, eradicate and resolve incidents in accordance with the Company’s incident response plan. Management is responsible for reporting incidents to the appropriate authorities as necessary and engaging the senior leadership on all material incidents.

Item 2. Properties

The Company’s headquarters are located in a multi-tenant building in Woodcliff Lake, New Jersey, which houses the Company’s executive officers, its accounting and administrative staff, and its information technology staff and equipment. The Company’s key reclamation, processing and cylinder refurbishment facilities are located in Champaign, Illinois, Smyrna, Georgia and Ontario, California. The Company also sells industrial gases out of facilities located in Escondido, California and in Champaign, Illinois. The Company maintains smaller reclamation and cylinder refurbishing facilities in Ontario, California. The Company also maintains four smaller service depots for the performance of its RefrigerantSide® Services and maintains three sales and telemarketing offices.

14

Hudson’s key operational facilities are as follows:

Location |

| Owned or Leased |

| Description |

Woodcliff Lake, New Jersey | Leased | Company headquarters and administrative offices | ||

Champaign, Illinois | Owned | Reclamation and separation of refrigerants and cylinder refurbishment | ||

Champaign, Illinois | Leased | Refrigerant packaging, cylinder refurbishment, RefrigerantSide® Service depot, refrigerant and industrial gases storage | ||

Smyrna, Georgia | Leased | Reclamation and separation of refrigerants and cylinder refurbishment center | ||

Smyrna, Georgia | Owned | Refrigerant storage | ||

Escondido, California | Leased | Refrigerant and Industrial gas storage and cylinder refurbishment center | ||

Ontario, California | Leased | Refrigerant reclamation and cylinder refurbishment center |

Item 3. Legal Proceedings

None.

Item 4. Mine Safety Disclosures

Not Applicable.

Part II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company’s common stock trades on the NASDAQ Capital Market under the symbol “HDSN”.

The number of record holders of the Company’s common stock was approximately 87 as of March 8, 2024. The Company believes that there are approximately 4,000 beneficial owners of its common stock.

To date, the Company has not declared or paid any cash dividends on its common stock. The payment of dividends, if any, in the future is within the discretion of the Board of Directors and will depend upon the Company’s earnings, its capital requirements and financial condition, borrowing covenants, and other relevant factors. The Company presently intends to retain all earnings, if any, to finance the Company’s operations and development of its business and does not expect to declare or pay any cash dividends on its common stock in the foreseeable future. In addition, the Company has a credit facility with Wells Fargo Bank, National Association among other things, restricts the Company’s ability to declare or pay any cash dividends on its capital stock.

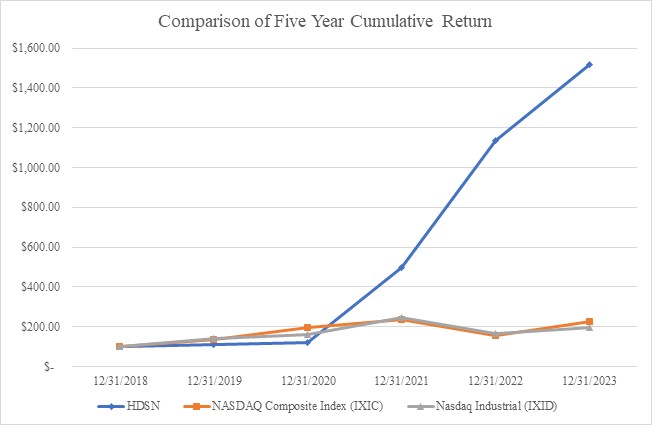

Stock Price Performance Graph

The following graph illustrates a comparison of the total cumulative five-year stockholder return of a $100 investment in our common stock on December 31, 2018, to two indices: the NASDAQ Composite Index and the Nasdaq Industrial Index. The stockholder return shown in the graph below is not necessarily indicative of future performance, and we do not make or endorse any predictions as to future stockholder returns.

15

The above Stock Price Performance Graph and related information shall not be deemed “soliciting material” or to be “filed” with the Securities and Exchange Commission, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or Securities Exchange Act of 1934, each as amended, except to the extent that we specifically incorporate it by reference into such filing.

Item 6. [Reserved]

Not applicable.

16

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Certain statements, contained in this section and elsewhere in this Form 10-K, constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve a number of known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, but are not limited to, changes in the laws and regulations affecting the industry, changes in the demand and price for refrigerants (including unfavorable market conditions adversely affecting the demand for, and the price of refrigerants), the Company’s ability to source refrigerants, regulatory and economic factors, seasonality, competition, litigation, the nature of supplier or customer arrangements that become available to the Company in the future, adverse weather conditions, possible technological obsolescence of existing products and services, possible reduction in the carrying value of long-lived assets, estimates of the useful life of its assets, potential environmental liability, customer concentration, the ability to obtain financing, the ability to meet financial covenants under our financing facility, any delays or interruptions in bringing products and services to market, the timely availability of any requisite permits and authorizations from governmental entities and third parties as well as factors relating to doing business outside the United States, including changes in the laws, regulations, policies, and political, financial and economic conditions, including inflation, interest and currency exchange rates, of countries in which the Company may seek to conduct business, the Company’s ability to successfully integrate any assets it acquires from third parties into its operations, and other risks detailed in this report, and in the Company’s other subsequent filings with the Securities and Exchange Commission (“SEC”). The words “believe”, “expect”, “anticipate”, “may”, “plan”, “should” and similar expressions identify forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date the statement was made.

Critical Accounting Estimates

The Company’s discussion and analysis of its financial condition and results of operations are based upon its consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of these consolidated financial statements requires the Company to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses and related disclosure of contingent assets and liabilities. Several of the Company’s accounting policies involve significant judgments, uncertainties and estimates. The Company bases its estimates on historical experience and on various other assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities. Actual results may differ from these estimates under different assumptions or conditions. To the extent that actual results differ from management’s judgments and estimates, there could be a material adverse effect on the Company. On a continuous basis, the Company evaluates its estimates, including, but not limited to, those estimates related to its inventory reserves, goodwill and intangible assets.

Inventory

For inventory, the Company evaluates both current and anticipated sales prices of its products to determine if a write down of inventory to net realizable value is necessary. Net realizable value represents the estimated selling price in the ordinary course of business, less reasonably predictable costs of completion and disposal. The determination if a write-down to net realizable value is necessary is primarily affected by the market prices for the refrigerant gases we sell. Commodity prices generally are affected by a wide range of factors beyond our control, including weather, seasonality, the availability and adequacy of supply, government regulation and policies and general political and economic conditions. At any time, our inventory levels may be substantial and fluctuate, which will materially impact our estimates of net realizable value.

Goodwill

The Company has made acquisitions that included a significant amount of goodwill and other intangible assets. The Company applies the purchase method of accounting for acquisitions, which among other things, requires the recognition of goodwill (which represents the excess of the purchase price of the acquisition over the fair value of the net assets acquired and identified intangible assets). We test our goodwill for impairment on an annual basis (the first day of the fourth quarter) and between annual tests if an event occurs or circumstances change that would more likely than not reduce the fair value of an asset below its carrying value. Other intangible assets that meet certain criteria are amortized over their estimated useful lives.

17

An impairment charge is recorded based on the excess of a reporting unit’s carrying amount over its fair value. An impairment charge would be recognized when the carrying amount exceeds the estimated fair value of a reporting unit. These impairment evaluations use many assumptions and estimates in determining an impairment loss, including certain assumptions and estimates related to future earnings. If the Company does not achieve its earnings objectives, the assumptions and estimates underlying these impairment evaluations could be adversely affected, which could result in an asset impairment charge that would negatively impact operating results.

There were no goodwill impairment losses recognized in any of the three years ended December 31, 2023, 2022 and 2021.

Overview

The Company is a leading provider of sustainable refrigerant products and services to the Heating Ventilation Air Conditioning and Refrigeration (“HVACR”) industry. For nearly three decades, we have demonstrated our commitment to our customers and the environment by becoming one of the United States’ largest refrigerant reclaimers through multimillion dollar investments in the plants and advanced separation technology required to recover a wide variety of refrigerants and restoring them to Air-Conditioning, Heating, and Refrigeration Institute (“AHRI”) standard for reuse as certified EMERALD Refrigerants™.

The Company’s products and services are primarily used in commercial air conditioning, industrial processing and refrigeration systems, and include refrigerant and industrial gas sales, refrigerant management services consisting primarily of reclamation of refrigerants and RefrigerantSide® Services performed at a customer’s site, consisting of system decontamination to remove moisture, oils and other contaminants.

Sales of refrigerants continue to represent a significant majority of the Company’s revenues.

The Company also sells industrial gases to a variety of industry customers, predominantly to users in, or involved with, the US Military. In July 2016, the Company was awarded, as prime contractor, a five-year fixed price contract, including a five-year renewal option which has been exercised, awarded to it by the United States Defense Logistics Agency (“DLA”) for the management and supply of refrigerants, compressed gases, cylinders and related items to US Military commands and installations, Federal civilian agencies and foreign militaries. Primary users include the US Army, Navy, Air Force, Marine Corps and Coast Guard. Our contract with DLA expires in July 2026.

Results of Operations

Year ended December 31, 2023 as compared to the year ended December 31, 2022

Revenues for the year ended December 31, 2023 were $289.0 million, a decrease of $36.2 million or 11% from the $325.2 million reported during the comparable 2022 period. The decrease was mainly attributable to lower selling prices of certain refrigerants sold, partially offset by increase in revenues from our DLA and carbon credit programs.

Cost of sales for the year ended December 31, 2023 was $177.5 million or 61% of sales. Cost of sales for the year ended December 31, 2022 was $162.3 million or 50% of sales. The increase in the cost of sales percentage from 61% to 50% is primarily due to the lower selling prices of certain refrigerants sold, as described above.

Selling, general and administrative (“SG&A”) expenses for the year ended December 31, 2023 were $30.5 million, an increase of $1.9 million from the $28.6 million reported during the comparable 2022 period. The increase in SG&A was primarily due to an increased number of employees and stock compensation.

Amortization expense was $2.8 million during 2023 and 2022, respectively.

Other expense for 2023 was $8.4 million, compared to the $14.3 million of other expense reported during the comparable 2022 period. During the third quarter of 2023, the Company repaid in full the remaining $32.5 million principal balance outstanding under its Term Loan Facility. In conjunction with this payoff, the Company recorded a non-cash write off of $3.4 million of deferred financing costs. Similarly, during the first quarter of 2022, the Company recorded a non-cash write off of $4.7 million of deferred financing cost. Excluding these write offs, total interest expense for the year 2023 decreased by $4.7 million from the comparable 2022 period.

18

Income tax expense for 2023 was $17.6 million compared to income tax expense of $13.4 million for 2022. The key drivers of increased income tax expense are the reversal of valuation allowance during 2022 for federal NOLs that were fully utilized and can no longer reduce taxable income. Income tax expense for federal and state income tax purposes was determined by applying statutory income tax rates to pre-tax income after adjusting for certain items.

The net income for the year ended December 31, 2023 was $52.2 million, a decrease of $51.6 million from the $103.8 million of net income reported during the comparable 2022 period, primarily due to lower revenues, higher cost of sales and a higher tax rate, as described above.

Year ended December 31, 2022 as compared to the year ended December 31, 2021

Management’s discussion and analysis of the year ended December 31, 2022 as compared to the year ended December 31, 2021 is contained in the Company’s Annual Report on Form 10-K filed with the Securities and Exchange Commission on March 14, 2023.

Liquidity and Capital Resources

At December 31, 2023, the Company had working capital, which represents current assets less current liabilities, of $146.4 million, an increase of $22.2 million from the working capital of $124.2 million at December 31, 2022. The increase in working capital is primarily attributable to continued profitability and the timing of borrowings, accounts receivable and inventory.

Inventory and trade receivables are principal components of current assets. At December 31, 2023, the Company had inventory of $154.5 million, an increase of $9.1 million from $145.4 million at December 31, 2022. The Company’s ability to sell and replace its inventory on a timely basis and the prices at which it can be sold are subject, among other things, to current market conditions and the nature of supplier or customer arrangements and the Company’s ability to source CFC and HCFC based refrigerants (which are no longer being produced) and HFC refrigerants (virgin production currently in the process of being phased down) and HFO refrigerants.

At December 31, 2023, the Company had trade receivables, net of credit losses, of $25.2 million, an increase of $4.3 million from $20.9 million at December 31, 2022, mainly due to timing. The Company typically generates its most significant revenue during the second and third quarters of any given year. The Company’s trade receivables are concentrated with various wholesalers, brokers, contractors and end-users within the refrigeration industry that are primarily located in the continental United States. The Company has historically financed its working capital requirements through cash flows from operations, debt, and the issuance of equity securities.

Net cash provided by operating activities for the year ended December 31, 2023 was $58.5 million, when compared to the net cash provided by operating activities of $62.8 million for the comparable 2022 period. As discussed above, selling prices of certain refrigerants declined in 2023. Another contributory factor was the timing of accounts receivable and inventory balances.

Net cash used in investing activities for 2023 was $3.6 million when compared to the net cash used in investing activities of $3.7 million for the comparable 2022 period.

Net cash used in financing activities for 2023 was $47.8 million, compared with net cash used in financing activities of $57.4 million for 2022. The Company refinanced its term loan debt during the first quarter of 2022, as described below, and paid off its remaining $32.5 million term loan debt during the third quarter of 2023.

At December 31, 2023, cash and cash equivalents were $12.4 million, or approximately $7.1 million higher than the $5.3 million of cash and cash equivalents at December 31, 2022.

Revolving Credit Facility

On March 2, 2022, Hudson Technologies Company (“HTC”) and Hudson Holdings, Inc. (“Holdings”), as borrowers (collectively, the “Borrowers”), and Hudson Technologies, Inc. (the “Company”) as a guarantor, entered into an Amended and Restated Credit Agreement (the “Amended Wells Fargo Facility”) with Wells Fargo Bank, National Association, as administrative agent and lender (“Agent” or “Wells Fargo”) and such other lenders as have or may thereafter become a party to the Amended Wells Fargo Facility. The Amended Wells Fargo facility amended and restated the prior Wells Fargo Facility entered into on December 19, 2019.

19

Under the terms of the Amended Wells Fargo Facility, the Borrowers: (i) immediately borrowed $15 million in the form of a “first in last out” term loan (the “FILO Tranche”) and (ii) may borrow from time to time, up to $75 million at any time consisting of revolving loans (the “Revolving Loans”) in a maximum amount up to the lesser of $75 million and a borrowing base that is calculated based on the outstanding amount of the Borrowers’ eligible receivables and eligible inventory, as described in the Amended Wells Fargo Facility. The Amended Wells Fargo Facility also contains a sublimit of $9 million for swing line loans and $2 million for letters of credit. The Company currently has a $0.9 million letter of credit outstanding. The FILO Tranche was repaid in full in July 2023 and may not be reborrowed.

Amounts borrowed under the Amended Wells Fargo Facility may be used for working capital needs, certain permitted acquisitions, and to reimburse drawings under letters of credit.

Interest under the Amended Wells Fargo Facility is payable in arrears on the first day of each month. Interest charges with respect to Revolving Loans are computed on the actual principal amount of Revolving Loans outstanding at a rate per annum equal to (A) with respect to Base Rate loans, the sum of (i) a rate per annum equal to the higher of (1) 1.0%, (2) the federal funds rate plus 0.5%, (3) one month term SOFR plus 1.0%, and (4) the prime commercial lending rate of Wells Fargo, plus (ii) between 1.25% and 1.75% depending on average monthly undrawn availability and (B) with respect to SOFR loans, the sum of the applicable SOFR rate plus between 2.36% and 2.86% depending on average quarterly undrawn availability. Interest charges with respect to the FILO Tranche were computed on the actual principal amount of FILO Tranche loans outstanding at a rate per annum equal to (A) with respect to Base Rate FILO Tranche loans, the sum of (i) a rate per annum equal to the higher of (1) 1.0%, (2) the federal funds rate plus 0.5%, (3) one month term SOFR plus 1.0%, and (4) the prime commercial lending rate of Wells Fargo, plus (ii) 6.5% and (B) with respect to SOFR FILO Tranche loans, the sum of the applicable SOFR rate plus 7.50%. The Amended Wells Fargo Facility also includes a monthly unused line fee ranging from 0.35% to 0.75% per annum determined based upon the level of average Revolving Loans outstanding during the immediately preceding month measured against the total Revolving Loans that may be borrowed under the Amended Wells Fargo Facility.