UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2020

OR

Commission File Number 0-24000

| (Exact name of registrant as specified in its charter) | ||||||||

| (State or other jurisdiction of | (IRS Employer | |||||||||||||

| incorporation or organization) | Identification No.) | |||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

| (Registrant’s telephone number, including area code) | |||||||||||

Securities registered pursuant to Section 12(b) of the Act:

| stated value $0.0292 per share | |||||||||||||||||

| (Title of each class) | (Trading Symbol) | (Name of each exchange on which registered) | |||||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

| ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | ||||||||||||||||||||||

| Smaller reporting company | Emerging growth company | |||||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Aggregate market value of voting and non-voting common stock held by non-affiliates as of the last business day of the registrant's most recently completed second fiscal quarter: $4.8 billion of Class A non-voting common stock as of June 30, 2020. There is no active market for the Class B voting common stock. The Class B common stock is closely held by few shareholders.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date:

DOCUMENTS INCORPORATED BY REFERENCE

INDEX

| PART | ITEM NUMBER AND CAPTION | PAGE | |||||||||

2

PART I

ITEM 1. BUSINESS

General

Erie Indemnity Company ("Indemnity", "we", "us", "our") is a publicly held Pennsylvania business corporation that has since its incorporation in 1925 served as the attorney-in-fact for the subscribers (policyholders) at the Erie Insurance Exchange ("Exchange"). The Exchange, which also commenced business in 1925, is a Pennsylvania-domiciled reciprocal insurer that writes property and casualty insurance. The Exchange has wholly owned property and casualty subsidiaries including: Erie Insurance Company, Erie Insurance Company of New York, Erie Insurance Property & Casualty Company and Flagship City Insurance Company, and a wholly owned life insurance company, Erie Family Life Insurance Company ("EFL").

Our primary function as attorney-in-fact is to perform policy issuance and renewal services on behalf of the subscribers at the Exchange. We also act as attorney-in-fact on behalf of the Exchange with respect to all claims handling and investment management services, as well as the service provider for all claims handling, life insurance, and investment management services for its insurance subsidiaries, collectively referred to as "administrative services". Acting as attorney-in-fact in these two capacities is done in accordance with a subscriber's agreement (a limited power of attorney) executed individually by each subscriber (policyholder), which appoints us as their common attorney-in-fact to transact certain business on their behalf. Pursuant to the subscriber’s agreement for acting as attorney-in-fact in these two capacities, we earn a management fee calculated as a percentage, not to exceed 25%, of the direct and affiliated assumed premiums written by the Exchange. The management fee rate is set at least annually by our Board of Directors. The process of setting the management fee rate includes the evaluation of current year operating results compared to both prior year and industry estimated results for both Indemnity and the Exchange, and consideration of several factors for both entities including: their relative financial strength and capital position; projected revenue, expense and earnings for the subsequent year; future capital needs; as well as competitive position.

Services

The policy issuance and renewal services we provide to the Exchange are related to the sales, underwriting and issuance of policies. The sales related services we provide include agent compensation and certain sales and advertising support services. Agent compensation includes scheduled commissions to agents based upon premiums written as well as additional commissions and bonuses to agents, which are earned by achieving targeted measures. Agent compensation comprised approximately 66% of our 2020 policy issuance and renewal expenses. The underwriting services we provide include underwriting and policy processing and comprised approximately 10% of our 2020 policy issuance and renewal expenses. The remaining services we provide include customer service and administrative support. We also provide information technology services that support all the functions listed above that comprised approximately 11% of our 2020 policy issuance and renewal expenses. Included in these expenses are allocations of costs for departments that support these policy issuance and renewal functions.

By virtue of its legal structure as a reciprocal insurer, the Exchange does not have any employees or officers. Therefore, it enters into contractual relationships by and through an attorney-in-fact. Indemnity serves as the attorney-in-fact on behalf of the Exchange with respect to its administrative services. The Exchange's insurance subsidiaries also utilize Indemnity for these services in accordance with the service agreements between each of the subsidiaries and Indemnity. Claims handling services include costs incurred in the claims process, including the adjustment, investigation, defense, recording and payment functions. Life insurance management services include costs incurred in the management and processing of life insurance business. Investment management services are related to investment trading activity, accounting and all other functions attributable to the investment of funds. Included in these expenses are allocations of costs for departments that support these administrative functions. The amounts incurred for these services are reimbursed to Indemnity at cost in accordance with the subscriber's agreement and the service agreements. State insurance regulations require that intercompany service agreements and any material amendments be approved in advance by the state insurance department.

Erie Insurance Exchange

As our primary purpose is to manage the affairs at the Exchange for the benefit of the subscribers (policyholders) through the policy issuance and renewal services and administrative services, the Exchange is our sole customer. Our earnings are largely generated from management fees based on the direct and affiliated assumed premiums written by the Exchange. We have no direct competition in providing these services to the Exchange.

The Exchange generates revenue by insuring preferred and standard risks, with personal lines comprising 71% of the 2020 direct and affiliated assumed written premiums and commercial lines comprising the remaining 29%. The principal personal lines products are private passenger automobile and homeowners. The principal commercial lines products are commercial multi-peril, commercial automobile and workers compensation. Historically, due to policy renewal and sales patterns, the

3

Exchange's direct and affiliated assumed written premiums are greater in the second and third quarters than in the first and fourth quarters of the calendar year.

The Exchange is represented by independent agencies that serve as its sole distribution channel. In addition to their principal role as salespersons, the independent agents play a significant role as underwriting and service providers and are an integral part of the Exchange's success.

Our results of operations are tied to the growth and financial condition of the Exchange. If any events occurred that impaired the Exchange's ability to grow or sustain its financial condition, including but not limited to reduced financial strength ratings, disruption in the independent agency relationships, significant catastrophe losses, or products not meeting customer demands, the Exchange could find it more difficult to retain its existing business and attract new business. A decline in the business of the Exchange almost certainly would have as a consequence a decline in the total premiums paid and a correspondingly adverse effect on the amount of the management fees we receive. We also have an exposure to a concentration of credit risk related to the unsecured receivables due from the Exchange for its management fee and cost reimbursements. See Part II, Item 8. "Financial Statements and Supplementary Data - Note 16, Concentrations of Credit Risk, of Notes to Financial Statements" contained within this report. See the risk factors related to our dependency on the growth and financial condition of the Exchange in Item 1A. "Risk Factors" contained within this report.

Competition

Our primary function as attorney-in-fact is to perform policy issuance and renewal services on behalf of the subscribers at the Exchange. We also act as attorney-in-fact on behalf of the Exchange, as well as the service provider for its insurance subsidiaries, with respect to all administrative services. There are a limited number of companies that provide services under a reciprocal insurance exchange structure. We do not directly compete against other such companies, given we are appointed by the subscribers at the Exchange to provide these services.

The direct and affiliated assumed premiums written by the Exchange drive our management fee which is our primary source of revenue. The property and casualty insurance industry is highly competitive. Property and casualty insurers generally compete on the basis of customer service, price, consumer recognition, coverages offered, claims handling, financial stability and geographic coverage. Vigorous competition, particularly in the personal lines automobile and homeowners lines of business, is provided by large, well-capitalized national companies, some of which have broad distribution networks of employed or captive agents, by smaller regional insurers, and by large companies who market and sell personal lines products directly to consumers. Innovations by competitors or other market participants may also increase the level of competition in the industry. In addition, because the insurance products of the Exchange are marketed exclusively through independent insurance agents, the Exchange faces competition within its appointed agencies based upon ease of doing business, product, price, and service

relationships.

Market competition bears directly on the price charged for insurance products and services subject to regulatory limitations. Industry capital levels can also significantly affect prices charged for coverage. Growth is driven by a company's ability to provide insurance services and competitive prices while maintaining target profit margins. Growth is a product of a company's ability to retain existing customers and to attract new customers, as well as movement in the average premium per policy.

The Exchange's business model is designed to provide the advantages of localized marketing and claims servicing with the economies of scale and low cost of operations from centralized support services. The Exchange also carefully selects the independent agencies that represent it and seeks to be the lead insurer with its agents in order to enhance the agency relationship and the likelihood of receiving the most desirable underwriting opportunities from its agents.

The Exchange’s strategic focus as a reciprocal insurer is to employ a disciplined underwriting philosophy and to leverage its strong surplus position to generate higher risk adjusted investment returns. The goal is to produce acceptable returns, on a long-term basis, through careful risk selection, rational pricing and superior investment returns. This focus allows the Exchange to accomplish its mission of providing as near perfect protection, as near perfect service as is humanly possible at the lowest possible costs.

See the risk factors related to our dependency on the growth and financial condition of the Exchange in Item 1A. "Risk Factors" contained within this report for further discussion on competition in the insurance industry.

4

Human Capital Management

Our success is largely dependent upon our ability to attract, retain, and develop diverse talent while maintaining our service-based culture. We strive to create a value proposition for our employees through trust and collaboration while providing competitive compensation, benefits, and other reward programs. Our low turnover and high tenure are reflective of our culture and the mutual commitment that exists between employees and the company.

Our human capital management strategy, including initiatives to shape our workforce and workplace, is designed to ensure we are well positioned for the future. Areas of focus include talent acquisition, performance management, succession planning, learning and development, and diversity and inclusion. Our investments in human capital include programs aimed at preparing our employees for internal advancement. We hold a shared responsibility view of retirement planning whereby the company provides tools and resources that employees are expected to use to achieve their retirement goals. We set ourselves apart by offering both a 401(k) plan and a noncontributory defined benefit pension plan.

We use the following human capital metrics as part of managing our business:

| Years ended December 31, | ||||||||||||||||||||

| 2020 | 2019 | 2018 | ||||||||||||||||||

| Workforce size | ||||||||||||||||||||

Full-time (1) | 5,849 | 5,772 | 5,544 | |||||||||||||||||

| Part-time | 31 | 41 | 54 | |||||||||||||||||

Temporary (2) | 34 | 32 | 41 | |||||||||||||||||

Turnover (3) | 5.3 | % | 5.6 | % | 6.0 | % | ||||||||||||||

Average tenure (4) | 12.5 | 12.3 | 12.5 | |||||||||||||||||

(1) Includes 50% of employees who provide claims and life insurance management services exclusively for the Exchange and its subsidiaries. The Exchange and its subsidiaries reimburse us monthly for the cost of these services.

(2) Temporary employees are hired for short-term work and paid directly by us.

(3) The percentage of employees who left voluntarily or involuntarily, including retirements. Calculated using the number of employees who exited, divided by the average headcount of the period.

(4) The average number of years employees have been employed with the organization. Total number of years divided by average headcount of full-time and part-time employees for the period.

As we recognize the importance of employee engagement on the outcomes we achieve as an organization, we also work with independent external partners to administer confidential surveys to collect feedback on the employee experience. We have partnered with the Great Place to Work® ("GPTW") Institute since 2012 but did not apply for Top 100 Companies ranking until 2020 (outcome yet unknown). Eighty-seven percent of employees participated in the 2020 survey, which is a strong indicator of engagement. We received the highest possible honors outside of ranking for our prior three surveys: Great Place to Work-Certified™ in 2020 and 2017, and Great-rated in 2014. Our overall GPTW score has trended upwards over the last three surveys and is favorable compared to the benchmark of the companies ranked on the Great Place to Work® Top 100 Companies List.

5

Government Regulation

Most states have enacted legislation that regulates insurance holding company systems, defined as two or more affiliated persons, one or more of which is an insurer. Indemnity and the Exchange, and its wholly owned subsidiaries, meet the definition of an insurance holding company system.

Each insurance company in the holding company system is required to register with the insurance supervisory authority of its state of domicile and furnish information regarding the operations of companies within the holding company system that may materially affect the operations, management, or financial condition of the insurers within the system. Pursuant to these laws, the respective insurance departments may examine us and the Exchange and its wholly owned subsidiaries at any time, and may require disclosure and/or prior approval of certain transactions with the insurers and us, as an insurance holding company.

All transactions within a holding company system affecting the member insurers of the holding company system must be fair and reasonable and any charges or fees for services performed must be reasonable. Approval by the applicable insurance commissioner is required prior to the consummation of transactions affecting the members within a holding company system.

Website Access

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports are available free of charge on our website at www.erieinsurance.com as soon as reasonably practicable after such material is filed electronically with the Securities and Exchange Commission. Additionally, copies of our annual report on Form 10-K are available free of charge, upon written request, by contacting Investor Relations, Erie Indemnity Company, 100 Erie Insurance Place, Erie, PA 16530, or calling (800) 458-0811.

ITEM 1A. RISK FACTORS

Our business involves various risks and uncertainties, including, but not limited to those discussed in this section. The risks and uncertainties described in the risk factors below, or any additional risk outside of those discussed below, could have a material adverse effect on our business, financial condition, operating results, cash flows, or liquidity if they were to develop into actual events. This information should be considered carefully together with the other information contained in this report and in other reports and materials we file periodically with the Securities and Exchange Commission.

Our risks have been divided into the following categories:

Risks related to Erie Insurance Exchange – risks related to our dependence on our relationship with the Exchange associated with management fees, premium growth, and financial condition, as the Exchange is our sole customer and principal source of revenue

Operating risks – risks stemming from events or circumstances that directly or indirectly affect our operations, including our operations as attorney-in-fact for the Exchange

Market, Capital, and Liquidity risks – risks that may impact the values or results or our investment portfolio, ability to meet financial obligations or covenants, or obtain capital as necessary

Although we have organized risks generally according to these categories in the discussion below, risks may have impacts in more than one category and are included where the impact is most significant.

Risks related to Erie Insurance Exchange

If the management fee rate paid by the Exchange is reduced or if there is a significant decrease in the amount of direct and affiliated assumed premiums written by the Exchange, revenues and profitability could be materially adversely affected.

We are dependent upon management fees paid by the Exchange, which represent our principal source of revenue. Pursuant to the subscriber's agreement with the subscribers at the Exchange, we may retain up to 25% of all direct and affiliated assumed premiums written by the Exchange. Therefore, management fee revenue from the Exchange is calculated by multiplying the management fee rate by the direct and affiliated assumed premiums written by the Exchange. Accordingly, any reduction in direct and affiliated assumed premiums written by the Exchange and/or the management fee rate would have a negative effect on our revenues and net income.

6

The management fee rate is determined by our Board of Directors and may not exceed 25% of the direct and affiliated assumed premiums written by the Exchange. The Board of Directors sets the management fee rate each December for the following year. At their discretion, the rate can be changed at any time. The process of setting the management fee rate includes the evaluation of current year operating results compared to both prior year and industry estimated results for both Indemnity and the Exchange, and consideration of several factors for both entities including: their relative financial strength and capital position; projected revenue, expense and earnings for the subsequent year; future capital needs; as well as competitive position. The evaluation of these factors could result in a reduction to the management fee rate and our revenues and profitability could be materially adversely affected.

Serving as the attorney-in-fact in the reciprocal insurance exchange structure results in the Exchange being our sole customer. We have an interest in the growth of the Exchange as our earnings are largely generated from management fees based on the direct and affiliated assumed premiums written by the Exchange. If the Exchange's ability to grow or renew policies were adversely impacted, the premium revenue of the Exchange would be adversely affected which would reduce our management fee revenue. The circumstances or events that might impair the Exchange's ability to grow include, but are not limited to, the items discussed below.

Unfavorable changes in macroeconomic conditions, including declining consumer confidence, inflation, high unemployment, and the threat of recession, among others, may lead the Exchange's customers to modify coverage, not renew policies, or even cancel policies, which could adversely affect the premium revenue of the Exchange, and consequently our management fee.

The Exchange faces significant competition from other regional and national insurance companies. The property and casualty insurance industry is highly competitive on the basis of product, price and service. If the Exchange's competitors offer property and casualty products with more coverage or offer lower rates, and the Exchange is unable to implement product improvements quickly enough to keep pace, its ability to grow and renew its business may be adversely impacted. In addition, due to the Exchange's premium concentration in the automobile and homeowners insurance markets, it may be more sensitive to trends that could affect auto and home insurance coverages and rates over time, for example changing vehicle usage, usage-based methods of determining premiums, ownership and driving patterns such as ride sharing, advancements in vehicle or home technology or safety features such as accident and loss prevention technologies, the development of autonomous vehicles, or residential occupancy patterns, among other factors. Innovations by competitors or other market participants may increase the level of competition in the industry. If we fail to respond to those innovations on a timely basis, our competitive position and results may be materially adversely affected.

The Exchange markets and sells its insurance products through independent, non-exclusive insurance agencies. These agencies are not obligated to sell only the Exchange's insurance products, and generally also sell products of the Exchange's competitors. If agencies do not maintain their current levels of marketing efforts, bind the Exchange to unacceptable risks, place business with competing insurers, or the Exchange is unsuccessful in attracting or retaining agencies in its distribution system as well as maintaining its relationships with those agencies, the Exchange's ability to grow and renew its business may be adversely impacted. Additionally, consumer preferences may cause the insurance industry as a whole to migrate to a delivery system other than independent agencies.

The Exchange maintains a brand recognized for customer service. The perceived performance, actions, conduct and behaviors of employees, independent insurance agency representatives, and third-party service partners may result in reputational harm to the Exchange's brand. Specific incidents which may cause harm include but are not limited to disputes, long customer wait times, errors in processing a claim, failure to protect sensitive customer data, and negative or inaccurate social media or traditional media communications. Likewise, an inability to match or exceed the service provided by competitors, which is increasingly relying on digital delivery and enhanced distribution technology, may impede the Exchange's ability to maintain and/or grow its customer base. If third-party service providers fail to perform as anticipated, the Exchange may experience operational difficulties, increased costs and reputational damage. If an extreme catastrophic event were to occur in a heavily concentrated geographic area of subscribers/policyholders, an extraordinarily high number of claims could have the potential to strain claims processing and affect the Exchange's ability to satisfy its customers. Any reputational harm to the Exchange could have the potential to impair its ability to grow and renew its business.

We have an interest in the financial condition of the Exchange based on serving as the attorney-in-fact in the reciprocal insurance exchange structure and the Exchange being our sole customer. If the Exchange were to fail to maintain acceptable financial strength ratings, its competitive position in the insurance industry would be adversely affected. If a rating downgrade led to customers not renewing or canceling policies, or impacted the Exchange's ability to attract new customers, the premium revenue of the Exchange would be adversely affected which would reduce our management fee revenue. The circumstances or events that might impair the Exchange's financial condition include, but are not limited to, the items discussed below.

7

Financial strength ratings are an important factor in establishing the competitive position of insurance companies such as the Exchange. Higher ratings generally indicate greater financial stability and a stronger ability to meet ongoing obligations to policyholders. The Exchange's A.M. Best rating is currently A+ ("Superior"). Rating agencies periodically review insurers' ratings and change their rating criteria; therefore, the Exchange's current rating may not be maintained in the future. A significant downgrade in this or other ratings could reduce the competitive position of the Exchange, making it more difficult to attract profitable business in the highly competitive property and casualty insurance market and potentially result in reduced sales of its products and lower premium revenue.

The performance of the Exchange's investment portfolio is subject to a variety of investment risks. The Exchange's investment portfolio is comprised principally of fixed income securities, equity securities and limited partnerships. The fixed income portfolio is subject to a number of risks including, but not limited to, interest rate risk, investment credit risk, sector/concentration risk and liquidity risk. The Exchange's common stock and preferred equity securities have exposure to price risk, the risk of potential loss in estimated fair value resulting from an adverse change in prices. Limited partnerships are significantly less liquid and generally involve higher degrees of price risk than publicly traded securities. Limited partnerships, like publicly traded securities, have exposure to market volatility; but unlike fixed income securities, cash flows and return expectations are less predictable. If any investments in the Exchange's investment portfolio were to suffer a substantial decrease in value, the Exchange's financial position could be materially adversely affected through increased unrealized losses or impairments. A significant decrease in the Exchange's portfolio could also put it, or its subsidiaries, at risk of failing to satisfy regulatory or rating agency minimum capital requirements.

Property and casualty insurers are subject to extensive regulatory supervision in the states in which they do business. This regulatory oversight includes, by way of example, matters relating to licensing, examination, rate setting, market conduct, policy forms, limitations on the nature and amount of certain investments, claims practices, mandated participation in involuntary markets and guaranty funds, reserve adequacy, insurer solvency, restrictions on underwriting standards, accounting standards, and transactions between affiliates. Such regulation and supervision are primarily for the benefit and protection of policyholders. Changes in applicable insurance laws, tax statutes, regulations, or changes in the way regulators administer those laws, tax statutes, or regulations could adversely impact the Exchange's business, cash flows, results of operations, financial condition, or operating environment and increase its exposure to loss or put it at a competitive disadvantage, which could result in reduced sales of its products and lower premium revenue.

Property and casualty insurers face a significant risk of litigation and regulatory investigations and actions in the ordinary course of operating their businesses including the risk of class action lawsuits and claims regarding the infringement of the intellectual property of others. Plaintiffs in class action and other lawsuits against the Exchange may seek large or indeterminate amounts of damages, including punitive and treble damages, which may remain unknown for substantial periods of time. The Exchange is also subject to various regulatory inquiries, such as information requests, subpoenas, and books and record examinations from state and federal regulators and authorities.

As insurance industry practices and legal, judicial, social and other environmental conditions change, unexpected and unintended issues related to claims and coverage may emerge. In some instances, these emerging issues may not become apparent for some time after the Exchange has issued the affected insurance policies. As a result, the full extent of liability under the Exchange's insurance policies may not be known for many years after the policies are issued. These issues may adversely affect the Exchange's business by either extending coverage beyond its underwriting intent or by increasing the number or size of claims.

The Exchange's insurance operations are exposed to claims arising out of catastrophes. Common natural catastrophic events include hurricanes, earthquakes, tornadoes, hail storms, and severe winter weather. The frequency and severity of these catastrophes is inherently unpredictable. Changing climate conditions have added to the unpredictability, frequency and severity of natural disasters and have created additional uncertainty as to future trends and exposures. A single catastrophic occurrence or aggregation of multiple smaller occurrences within its geographical region of the Exchange or its assumed property reinsurance portfolio could adversely affect the financial condition of the Exchange. Man-made disasters such as terrorist attacks and riots could also cause losses from insurance claims related to the property and casualty insurance operations, which could adversely affect its financial condition.

If the impacts of the COVID-19 pandemic impair the Exchange’s ability to grow or its financial condition, it could have a material adverse effect on our business, financial condition, results of operations, or cash flows.

On March 11, 2020, the World Health Organization declared the outbreak of COVID-19 a global pandemic. The significant economic disruption and uncertainty resulting from the COVID-19 pandemic that began in 2020 continues to evolve and the pandemic’s ultimate impact and duration remain highly uncertain at this time. If future waves of the virus occur or effective

8

medical treatments are not administered, future restrictions, including business closures and stay at home orders, and a prolonged recession remain a possibility. The resulting effects, including a decline in consumer activity, lower demand for certain services, high unemployment, payroll declines, and reduced personal income may cause customers to modify coverages, not renew or cancel policies, which may have a negative impact on the Exchange’s written premiums, and therefore our management fees. Accordingly, the extent and duration of the effects on future customer demand and buying practices remains uncertain. A specific action taken by the Exchange both in response to changes in exposure as less driving occurs and to provide financial relief to the policyholders has resulted in a certain reduction to the Exchange’s written premiums. In 2020, the Exchange and its subsidiaries announced an estimated $200 million in personal and commercial auto rate reductions effective beginning July 1, 2020 at the time of new policy issuance or policy renewal. Estimated remaining rate reductions related to this event of $110 million in premiums and a corresponding decrease of $28 million in management fee revenue will impact both the Exchanges’ written premium and our management fee revenue in 2021. Longer term, there could be sustained changes in driving patterns if working remotely becomes more common and accepted, potentially having a negative impact on premium revenues. Further declines in economic conditions, potential regulatory actions, or competitive pressure could also impact the Exchange’s rates and written premium, and therefore our management fees.

The Exchange is represented by independent agencies that serve as its sole distribution channel. The economic impact of the pandemic on independent agents’ business operations or systems capabilities could make it difficult for independent agents to write new business and retain existing business and/or constrain the ability to recruit new agents, thereby impeding premium growth. While independent agents have been able to work remotely or safely in their offices, future waves of the virus could adversely impact their operations and their ability to write new business and provide service to existing policyholders. More broadly, independent agents may face challenges sustaining their own business operations and financial conditions that could result in the sale or closure of their businesses, thereby reducing the agency force of the Exchange. Further, the COVID-19 pandemic could be an accelerant to shifting consumer behaviors toward increased digital interactions.

The unknown risks related to the COVID-19 pandemic may cause additional uncertainty in the process of estimating loss and loss adjustment expense reserves. For example, the behavior of claimants and policyholders may change in unexpected ways, the disruption to the court system may impact the timing and amounts of claims settlements, and the actions taken by governmental bodies, both legislative and regulatory, in reaction to COVID-19 and their related impacts are hard to predict. As a result, the Exchange's estimated level of loss and loss adjustment expense reserves may change.

The Exchange’s financial condition could be impacted by defaults or delays in collecting premiums from customers due to economic hardships. Regulatory actions including temporary suspension of policy cancellations for the nonpayment of premiums and relaxing due dates for premium payments could also have a negative impact to the Exchange. If there were legislative action to retroactively mandate coverage irrespective of terms, exclusions or other conditions included in business interruption policies that would otherwise preclude coverage, this could have a material impact on the financial condition, results of operations and cash flows of the Exchange.

The Exchange and its subsidiaries have been named as defendants in a number of pandemic-related lawsuits and, therefore, are subject to the risks and uncertainties of such litigation. There is also a risk that the Exchange could suffer reputational harm if any actions taken are not viewed as sufficient responses to the pandemic by customers or consumer organizations.

While the Exchange’s investment portfolio was negatively impacted by the significant disruption to financial markets in the first quarter of 2020 as a result of the COVID-19 pandemic, market conditions substantially recovered through the remainder of the year. The value of the Exchange’s invested assets could be adversely impacted and there is potential for further impairments on its investment portfolio as long as market conditions remain volatile in response to the developments of this pandemic and the related economic impacts.

The duration and extent of the impact on the Exchange’s business, strategy, financial condition, results of operations and cash flows cannot be estimated with a high degree of certainty at this time given the ongoing developments of this pandemic and the related impacts on the economy and financial markets.

Operating risks

If the costs of providing services to the Exchange are not controlled, our profitability could be materially adversely affected.

Pursuant to the subscriber's agreement, we perform policy issuance and renewal services for the subscribers at the Exchange and we serve as the attorney-in-fact on behalf of the Exchange with respect to its administrative services. The most significant costs we incur in providing policy issuance and renewal services are commissions, employee costs, and technology costs.

9

Commissions to independent agents are our largest expense. Commissions include scheduled commissions to agents based upon premiums written as well as additional commissions and bonuses to agents, which are earned by achieving certain targeted measures. Changes to commission rates or bonus programs may result in increased future costs and lower profitability. Our second largest expense is employee costs, including salaries, healthcare, pension, and other benefit costs. Regulatory developments, provider relationships, and demographic and economic factors that are beyond our control indicate that employee healthcare costs could continue to increase which could reduce our profitability. The defined benefit pension plan we offer to our employees is affected by variable factors such as the interest rate used to discount pension liabilities, asset performance and changes in retirement patterns, which are beyond our control and any related future costs increases would reduce our profitability.

Technological development is necessary to facilitate ease of doing business for employees, agents and customers. Insurance company technological developments are focused on simplifying and improving the customer experience, increasing efficiencies, redesigning products and addressing other potentially disruptive changes in the insurance industry. As we continue to develop technology initiatives in order to remain competitive, our profitability could be negatively impacted as we invest in system development.

If we are unable to attract, develop, and retain talented executives, key managers, and employees our financial conditions and results of operations could be adversely affected.

Our success is largely dependent upon our ability to attract and retain talented executives and other key management. Talent is defined as people with the right skills, knowledge, abilities, character, and motivation. The loss of the services and leadership of certain key officers and the failure to attract and develop talented new executives and managers could prevent us from successfully communicating, implementing, and executing business strategies.

Our success also depends on our ability to attract, develop, and retain a talented employee base. The inability to staff all functions of our business with employees possessing the appropriate talent, failure to recognize and respond to changing trends and other circumstances that affect our employees, or failure to instill appropriate cultural expectations and behavioral norms within our employees could have an adverse effect on our business performance. Staffing appropriately talented employees for the handling of claims and servicing of customers, rendering of disciplined underwriting, and effective sales and marketing are critical to the core functions of our business. In addition, talented employees in the actuarial, finance, human resources, law, and information technology areas are also essential to support our core functions.

If we are unable to ensure system availability or effectively manage technology initiatives, we may experience adverse financial consequences and/or may be unable to compete effectively.

Our business is highly dependent upon the effectiveness of our technology and information systems which support key functions of our core business operations including processing applications and premium payments, providing customer support, performing actuarial and financial analysis, and maintaining key data. Additionally, the Exchange relies heavily on technology systems for processing claims. In order to support our business processes and strategic initiatives in a cost and resource efficient manner, we must maintain the effectiveness of existing technology systems and continue to both develop new, and enhance existing, technology systems. As we invest in the development of our systems, costs and completion times could exceed original estimates, and/or the project may not deliver the anticipated benefit or perform as expected. If we do not effectively and efficiently manage and upgrade our technology systems, our ability to serve our customers and implement our strategic initiatives could be adversely impacted.

Additionally, we depend on a large amount of data to price policies appropriately, track exposures, perform financial analysis, report to regulatory bodies, and ultimately make business decisions. Should this data be inaccurate or insufficient, risk exposure may be underestimated and/or poor business decisions may be made. This may in turn lead to adverse operational or financial performance and adverse customer or investor confidence.

If we experience difficulties with technology, data and network security, including as a result of cyber attacks, third-party relationships or cloud-based relationships, our ability to conduct our business could be adversely impacted.

In the normal course of business, we collect, use, store and where appropriate, disclose data concerning individuals and businesses. We also conduct business using third-party vendors who may provide software, data storage, cloud-based computing and other technology services. We have on occasion experienced, and will continue to experience, cyber threats to our data and systems. Cyber threats can create significant risks such as destruction of systems or data, denial or interruption of service, disruption of transaction execution, loss or exposure of customer data, theft or exposure of our intellectual property,

10

theft of funds or disruption of other important business functions. The business we conduct with our third-party vendors may expose us to increased risk related to data security, service disruptions or effectiveness of our control system.

In addition, we are subject to numerous federal and state data privacy laws relating to the privacy of the nonpublic personal information of our customers, employees and others. The improper access, disclosure, or misuse or mishandling of information sent to or received from a customer, employee or third party could result in legal liability, regulatory action and reputational damage. Third parties on whom we rely for certain business processing functions are also subject to these risks, and their failure to adhere to these laws and regulations could negatively impact us.

We employ a company-wide cybersecurity program of technical, administrative, physical and disclosure controls intended to reduce the risk of cyber threats and protect our information, as well as to communicate potential material threats and incidents. Our cybersecurity philosophy and approach align to the National Institute of Standards and Technology Cybersecurity Framework and its core elements to identify, protect, detect, respond and recover from the various forms of cyber threats. Our practices include, but are not limited to, cybersecurity protocols and controls, system monitoring and detection, communication of incidents to appropriate management, vendor risk management, and ongoing privacy and cybersecurity training for employees and contractors concerning cyber risk. We periodically assess the effectiveness of our cybersecurity efforts including independent validation and verification and security assessments conducted by independent third parties. The number, complexity and sophistication of cyber threats continue to increase over time. The controls we have implemented, and continue to develop, may not be sufficient to prevent events like unauthorized physical or electronic access, denial of service, cyber attacks, or other security breaches to our computer systems or those of third parties with whom we do business. In some cases, such events may not be immediately detected and/or the impact of such events immediately determined.

Our Board of Directors oversees our activities with respect to managing cyber risk through its Risk Committee. Management periodically reports on our cybersecurity risk management program including our risk evaluation and the results of independent third-party security assessments, and our efforts to mitigate cyber related risks.

To date, we are not aware of any material cybersecurity breach with respect to our systems or data. Any cyber incident or other security breach could cause disruption in our business operations and may result in other negative consequences including significant remediation costs, loss of revenue, additional regulatory scrutiny, fines, litigation, monetary damages and reputational harm. While we maintain cyber liability insurance to mitigate the financial risk around cyber incidents, such insurance may not cover all costs associated with the consequences of information or systems being compromised. As a result, in the event of a material cybersecurity breach, our business, cash flows, financial condition or results of operations could be materially, adversely affected.

If events occurred causing interruption of our operations, facilities, systems or business functions, it could have a material adverse effect on our operations and financial results.

We have an established business continuity plan to ensure the continuation of core business operations in the event that normal business operations could not be performed due to a catastrophic or other event. While we continue to test and assess our business continuity plan to validate it meets the needs of our core business operations and addresses multiple business interruption events, there is no assurance that core business operations could be performed upon the occurrence of such an event. Employee absence, physical premises damage, systems failures or outages could compromise our ability to perform our business functions in a timely manner, which could harm our ability to conduct business and hurt our relationships with our business partners and customers. Our business continuity is also dependent on third-party personnel, infrastructure and systems on which we rely. Our operations and those of our third-party vendors may become vulnerable to damage or disruption due to circumstances beyond our or their control, such as from catastrophic events, power anomalies or outages, natural disasters, network failures, and cyber attacks. Disruption of our operations for any reason could result in a material adverse effect on our business, cash flows, financial condition, or results of operations.

We are subject to applicable insurance laws, tax statutes, and regulations, as well as claims and legal proceedings, which, if determined unfavorably, could have a material adverse effect on our business, results of operations, or financial condition.

We face a significant risk of litigation and regulatory investigations and actions in the ordinary course of operating our businesses including the risk of class action lawsuits. We are, have been, or may become subject to class actions and individual suits alleging breach of fiduciary or other duties, including our obligations to indemnify directors and officers in connection with certain legal matters. We are also subject to litigation arising out of our general business activities such as contractual and employment relationships and claims regarding the infringement of the intellectual property of others. Plaintiffs in class action and other lawsuits against us may seek large or indeterminate amounts of damages, including punitive and treble damages, which may remain unknown for substantial periods of time. We are also subject to various regulatory inquiries, such as

11

information requests, subpoenas, and books and record examinations from state and federal regulators and authorities. In addition, changes in the way regulators administer applicable laws, tax statutes, or regulations could adversely impact our business, cash flows, results of operations, or financial condition.

The effect of the COVID-19 pandemic on our operations, the business operations of our customers and/or independent agents, or our third-party vendor operations, could have a material adverse effect on our business, financial condition, results of operations, or cash flows.

If the COVID-19 pandemic results in conditions that constrain the Exchange’s ability to grow its written premiums, our management fee revenue could be negatively impacted. Certain expenses within our cost of operations could increase as a result of the pandemic, including but not limited to agent compensation, technology costs, and potentially healthcare costs, among others. Our agent incentive bonuses include a profitability component. If claims frequency and loss expenses continue to decline, the profitability component of our agent incentive bonuses will continue to improve, increasing our agent compensation costs. Technology costs may continue to increase as a result of supporting remote work capabilities for our employees. If a significant number of our employees and/or their dependents were to become infected, there is a potential for increased healthcare costs for treatments on COVID-19 as well as the potential for increased use of third-party services to maintain service. Also, future pension costs could increase as a result of a lower discount rate or investment returns related to the adverse market conditions caused by the COVID-19 pandemic.

Our business continuity plans were implemented upon the outbreak of this pandemic, including transitioning the vast majority of our employees and third-party contractors to remote work capabilities. We have had no significant interruption to our core business processes or systems to date. We have processes in place with our critical third-party vendors to understand impacts on their business and their business continuity plans. We have had no significant interruption to any third-party vendor relationships, business processes or systems to date. No significant challenges have been identified in our, or our third-party vendor’s ongoing business continuity plans, however if future challenges were to arise, this could result in an adverse effect on our business, financial condition, results of operations or cash flows. Also, while we have not experienced any delays in internal initiatives to date, future challenges could arise that impact the timing and execution of certain initiatives. Having shifted to remote working arrangements, we also face a heightened risk of cybersecurity attacks or data security incidents. While cyber threats have remained at a constant level, new cybersecurity tactics, techniques, and practices continue to evolve. Additionally, we are more dependent on internet and telecommunications access and capabilities. If we experience difficulties with technology, data and network security, telecommunications access, outsourcing relationships or cloud-based technology, our ability to conduct our business could be negatively impacted.

Indemnity’s workforce is largely concentrated in Erie, Pennsylvania. If a significant outbreak affects the labor force in this area, or if a significant operating function had a high level of infections at one time, it could impact the policy acquisition, underwriting, claims and/or support services provided to the policyholders of the Exchange and/or our independent agents.

With the increasing number of COVID-19 related disputes, there is a risk that Indemnity could become subject to pandemic related litigation. It is also possible that changes in economic conditions and steps taken by federal, state and local governments in response to COVID-19 could require an increase in taxes at the federal, state and local levels, which would adversely impact our results of operations.

While Indemnity’s investment portfolio was negatively impacted by the significant disruption to financial markets in the first quarter of 2020 as a result of the COVID-19 pandemic, market conditions substantially recovered through the remainder of the year. The value of our invested assets could be adversely impacted and there is potential for further impairments in our investment portfolio as long as market conditions remain volatile in response to the developments of this pandemic and the related economic impacts.

The duration and extent of the impact on our business, strategy, financial condition, results of operations and cash flows cannot be estimated with a high degree of certainty at this time given the ongoing developments of this pandemic and the related impacts on the economy and financial markets.

Market, Capital, and Liquidity risks

The performance of our investment portfolio is subject to a variety of investment risks, which may in turn have a material adverse effect on our results of operations or financial condition.

At December 31, 2020, our investment portfolio consisted of approximately 84% fixed maturity securities, with the remaining 16% invested in equity securities and other investments.

12

General economic conditions and other factors beyond our control can adversely affect the value of our investments and the realization of net investment income, or result in realized investment losses. In addition, downward economic trends also may have an adverse effect on our investment results by negatively impacting the business conditions and impairing credit for the issuers of securities held in our respective investment portfolios. This could reduce fair values of investments and generate significant unrealized losses or impairment charges which may adversely affect our financial results.

The performance of the fixed income portfolio is subject to a number of risks including, but not limited to:

•Interest rate risk - the risk of adverse changes in the value of fixed income securities as a result of increases in market interest rates.

•Investment credit risk - the risk that the value of certain investments may decrease due to the deterioration in financial condition of, or the liquidity available to, one or more issuers of those securities or, in the case of structured securities, due to the deterioration of the loans or other assets that underlie the securities, which, in each case, also includes the risk of permanent loss.

•Sector/Concentration risk - the risk that the portfolio may be too heavily concentrated in the securities of one or more issuers, sectors, or industries. Events or developments that have a negative impact on any particular industry, group of related industries, or geographic region may have a greater adverse effect on our investment portfolio to the extent that the portfolio is concentrated within those issuers, sectors, or industries.

•Liquidity risk - the risk that we will not be able to convert investment securities into cash on favorable terms and on a timely basis, or that we will not be able to sell them at all, when desired. Disruptions in the financial markets or a lack of buyers for the specific securities that we are trying to sell, could prevent us from liquidating securities or cause a reduction in prices to levels that are not acceptable to us.

•Reinvestment risk - the possibility that the cash flows produced by an investment will have to be reinvested at a reduced rate of return. Approximately 38% of our fixed maturity portfolio is expected to mature over the next three years.

Our equity securities have exposure to price risk. Equity markets, sectors, industries, and individual securities may also be subject to some of the same risks that affect our fixed income portfolio, as discussed above.

All of our fixed income and equity securities are subject to market volatility. To the extent that future market volatility negatively impacts our investments, our financial condition will be negatively impacted. We review the fixed income portfolio on a continuous basis to evaluate positions that are in an unrealized loss position to determine whether impairments are a result of credit loss or other factors. Inherent in management's evaluation of a security are assumptions and estimates about the operations of the issuer and its future earnings potential. The primary factors considered in our review of investment valuation include the extent to which fair value is less than cost, historical operating performance and financial condition of the issuer, short- and long-term prospects of the issuer and its industry, specific events that occurred affecting the issuer, including rating downgrades, and, depending on the type of security, our intent to sell or our ability and intent to retain the investment for a period of time sufficient to allow for a recovery in value. As the process for determining impairments is highly subjective, changes in our assessments may have a material effect on our operating results and financial condition. See also Part II, Item 7A. "Quantitative and Qualitative Disclosures about Market Risk".

In July 2017, the United Kingdom’s Financial Conduct Authority ("FCA"), which regulates the London Interbank Offered Rate (“LIBOR”), announced that it intends to phase out LIBOR by the end of 2021. After this date, the FCA will no longer require banks to make LIBOR submissions. Following discussions with the FCA and other official sector bodies, the Intercontinental Exchange Benchmark Administration announced in November 2020 that it is considering the publication of certain USD LIBOR settings through June 30, 2023. Approximately 23% of our investment portfolio includes securities with LIBOR exposure where the stated final maturity date extends beyond June 30, 2023. For securities without adequate fallback provisions already in place, there are ongoing efforts to establish an alternative reference rate. The transition of our investments to an alternative reference rate may result in adverse changes to the value and return on those investments. Due to uncertainty surrounding alternative rates, we are unable to predict the overall impact of this change at this time.

Deteriorating capital and credit market conditions or a failure to accurately estimate capital needs may significantly affect our ability to meet liquidity needs and access capital.

13

Sufficient liquidity and capital levels are required to pay operating expenses, income taxes, and to provide the necessary resources to fund future growth opportunities, satisfy certain financial covenants, pay dividends on common stock, and repurchase common stock. Management estimates the appropriate level of capital necessary based upon current and projected results, which includes evaluating potential risks. Failure to accurately estimate our capital needs may have a material adverse effect on our financial condition until additional sources of capital can be obtained. Further, a deteriorating financial condition may create a negative perception of us by third parties, including investors, and financial institutions, which could impact our ability to access additional capital in the debt or equity markets.

Our primary sources of liquidity are management fee revenue and cash flows generated from our investment portfolio. In the event our current sources do not satisfy our liquidity needs, we have the ability to access our $100 million bank revolving line of credit, from which there were no borrowings as of December 31, 2020, or liquidate assets in our investment portfolio. Volatility in the financial markets could limit our ability to sell certain of our fixed income securities or cause such investments to sell at deep discounts.

In the event these traditional sources of liquidity are not available, we may have to seek additional financing. Our access to funds will depend upon a number of factors including current market conditions, the availability of credit, market liquidity, and the timing of obtaining credit ratings. In deteriorating market conditions, there can be no assurance that we will obtain additional financing, or, if available, that the cost of financing will not substantially increase and affect our overall profitability.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

14

ITEM 2. PROPERTIES

Indemnity and the Exchange share a corporate home office complex in Erie, Pennsylvania, which comprises approximately 996,000 square feet. Our square footage increased as the construction of the new office building was completed in the fourth quarter of 2020. Additionally, we lease two office buildings and one warehouse facility from third parties. We are charged rent for the related square footage we occupy.

Indemnity and the Exchange also operate 25 field offices in 12 states to perform primarily claims-related activities. The Exchange owns seven field offices, Indemnity owns property, a portion of which houses one field office, and leases the remaining field offices from third parties. Commitments for properties leased from other parties expire periodically through 2027. We expect that most leases will be renewed or replaced upon expiration. Rental costs of shared facilities are allocated based upon usage or square footage occupied.

Due to the uncertainty of the COVID-19 pandemic, approximately 90% of our workforce has been working remote since March 2020. We expect to return to our offices when conditions are feasible and safe.

15

ITEM 3. LEGAL PROCEEDINGS

State Court Lawsuit Against Erie Indemnity Company

Erie Indemnity Company ("Indemnity") was named as a defendant in a complaint filed on August 1, 2012 by alleged subscribers of the Erie Insurance Exchange (the "Exchange") in the Court of Common Pleas Civil Division of Fayette County, Pennsylvania captioned Erie Insurance Exchange, an unincorporated association, by Joseph S. Sullivan and Anita Sullivan, Patricia R. Beltz, and Jenna L. DeBord, trustees ad litem v. Erie Indemnity Co. (the "Sullivan" lawsuit).

As subsequently amended, the complaint alleges that, beginning on September 1, 1997, Indemnity retained "Service Charges" (installment fees) and "Added Service Charges" (late fees and policy reinstatement charges) on policies written by Exchange and its insurance subsidiaries, which allegedly should have been paid to Exchange, in the amount of approximately $308 million. In addition to their claim for monetary relief on behalf of Exchange, Plaintiffs seek an accounting of all so-called intercompany transactions between Indemnity and Exchange from 1996 to date. Plaintiffs allege that Indemnity breached its contractual, fiduciary, and equitable duties by retaining Service Charges and Added Service Charges that should have been retained by Exchange. Plaintiffs bring these same claims under three separate derivative-type theories. First, Plaintiffs purport to bring suit as members of Exchange on behalf of Exchange. Second, Plaintiffs purport to bring suit as trustees ad litem on behalf of Exchange. Third, Plaintiffs purport to bring suit on behalf of Exchange pursuant to Rule 1506 of the Pennsylvania Rules of Civil Procedure, which allows shareholders to bring suit derivatively on behalf of a corporation or similar entity.

Indemnity filed a motion in the state court in November 2012 seeking dismissal of the lawsuit. On December 19, 2013, the court granted Indemnity’s motion in part, holding that the Pennsylvania Insurance Holding Company Act "provides the [Pennsylvania Insurance] Department with special competence to address the subject matter of plaintiff’s claims" and referring "all issues" in the Sullivan lawsuit to the Pennsylvania Insurance Department (the "Department") for "its views and any determination." The court stayed all further proceedings and reserved decision on all other grounds for dismissal raised by Indemnity. Plaintiffs sought reconsideration of the court’s order, and on January 13, 2014, the court entered a revised order affirming its prior order and clarifying that the Department "shall decide any and all issues within its jurisdiction." On January 30, 2014, Plaintiffs asked the court to certify its order to permit an immediate appeal to the Superior Court of Pennsylvania and to stay any proceedings in the Department pending completion of any appeal. On February 18, 2014, the court issued an order denying Plaintiffs’ motion. On March 20, 2014, Plaintiffs filed a petition for review with the Superior Court, which was denied by the Superior Court on May 5, 2014.

The Sullivan matter was assigned to an Administrative Judge within the Department for determination. The parties agreed that an evidentiary hearing was not required, entered into a stipulated record, and submitted briefing to the Department. Oral argument was held before the Administrative Judge on January 6, 2015. On April 29, 2015, the Department issued a declaratory opinion and order: (1) finding that the transactions between Exchange and Indemnity in which Indemnity retained or received revenue from installment and other service charges from Exchange subscribers complied with applicable insurance laws and regulations and that Indemnity properly retained charges paid by Exchange policyholders for certain installment premium payment plans, dishonored payments, policy cancellations, and policy reinstatements; and (2) returning jurisdiction over the matter to the Fayette County Court of Common Pleas.

On May 26, 2015, Plaintiffs appealed the Department’s decision to the Pennsylvania Commonwealth Court. Oral argument was held before the Commonwealth Court en banc on December 9, 2015. On January 27, 2016, the Commonwealth Court issued an opinion vacating the Department’s ruling and directing the Department to return the case to the Court of Common Pleas, essentially holding that the primary jurisdiction referral of the trial court was improper at this time because the allegations of the complaint do not implicate the special competency of the Department.

On February 26, 2016, Indemnity filed a petition for allowance of appeal to the Pennsylvania Supreme Court seeking further review of the Commonwealth Court opinion. On March 14, 2016, Plaintiffs filed an answer opposing Indemnity’s petition for allowance of appeal; and, on March 28, 2016, Indemnity sought permission to file a reply brief in further support of its petition for allowance of appeal. On August 10, 2016, the Pennsylvania Supreme Court denied Indemnity’s petition for allowance of appeal; and the Sullivan lawsuit returned to the Court of Common Pleas of Fayette County.

On September 12, 2016, Plaintiffs filed a motion to stay the Sullivan lawsuit pending the outcome of the Federal Court Lawsuit they filed against Indemnity and former and current Directors of Indemnity on July 8, 2016. (See below.) Indemnity filed an opposition to Plaintiff’s motion to stay on September 19, 2016; and filed amended preliminary objections seeking dismissal of the Sullivan lawsuit on September 20, 2016. The motion to stay and the amended preliminary objections remain pending. On June 27, 2018, Plaintiffs filed a motion for a status conference in the Sullivan lawsuit.

16

On July 30, 2018, the Court held a status conference and thereafter lifted the stay of proceedings. On September 28, 2018, Indemnity filed a Motion to Enforce the Federal Judgment in the Beltz II lawsuit, seeking dismissal of the Sullivan lawsuit with prejudice. On October 26, 2018, Plaintiffs filed an opposition to that Motion; and Indemnity filed a reply in further support on November 5, 2018. Oral argument was held on Indemnity’s Motion on November 20, 2018 and on July 30, 2019.

On December 2, 2020, the Court entered an order in the Sullivan lawsuit granting Indemnity’s request for relief and dismissing Plaintiff’s Second Amended Complaint with prejudice.

Federal Court Lawsuit Against Erie Indemnity Company and Directors

On February 6, 2013, a lawsuit was filed in the United States District Court for the Western District of Pennsylvania, captioned Erie Insurance Exchange, an unincorporated association, by members Patricia R. Beltz, Joseph S. Sullivan and Anita Sullivan, and Patricia R. Beltz, on behalf of herself and others similarly situate v. Richard L. Stover; J. Ralph Borneman, Jr.; Terrence W. Cavanaugh; Jonathan Hirt Hagen; Susan Hirt Hagen; Thomas B. Hagen; C. Scott Hartz; Claude C. Lilly, III; Lucian L. Morrison; Thomas W. Palmer; Martin P. Sheffield; Elizabeth H. Vorsheck; and Robert C. Wilburn (the "Beltz" lawsuit), by alleged policyholders of Exchange who are also the plaintiffs in the Sullivan lawsuit. The individuals named as defendants in the Beltz lawsuit were the then-current Directors of Indemnity.

As subsequently amended, the Beltz lawsuit asserts many of the same allegations and claims for monetary relief as in the Sullivan lawsuit. Plaintiffs purport to sue on behalf of all policyholders of Exchange, or, alternatively, on behalf of Exchange itself. Indemnity filed a motion to intervene as a Party Defendant in the Beltz lawsuit in July 2013, and the Directors filed a motion to dismiss the lawsuit in August 2013. On February 10, 2014, the court entered an order granting Indemnity’s motion to intervene and permitting Indemnity to join the Directors’ motion to dismiss; granting in part the Directors’ motion to dismiss; referring the matter to the Department to decide any and all issues within its jurisdiction; denying all other relief sought in the Directors’ motion as moot; and dismissing the case without prejudice. To avoid duplicative proceedings and expedite the Department’s review, the Parties stipulated that only the Sullivan action would proceed before the Department and any final and non-appealable determinations made by the Department in the Sullivan action will be applied to the Beltz action.

On March 7, 2014, Plaintiffs filed a notice of appeal to the United States Court of Appeals for the Third Circuit. Indemnity filed a motion to dismiss the appeal on March 26, 2014. On November 17, 2014, the Third Circuit deferred ruling on Indemnity’s motion to dismiss the appeal and instructed the parties to address that motion, as well as the merits of Plaintiffs’ appeal, in the parties’ briefing. Briefing was completed on April 2, 2015. In light of the Department’s April 29, 2015 decision in Sullivan, the Parties then jointly requested that the Beltz appeal be voluntarily dismissed as moot on June 5, 2015. The Third Circuit did not rule on the Parties’ request for dismissal and instead held oral argument as scheduled on June 8, 2015. On July 16, 2015, the Third Circuit issued an opinion and judgment dismissing the appeal. The Third Circuit found that it lacked appellate jurisdiction over the appeal, because the District Court’s February 10, 2014 order referring the matter to the Department was not a final, appealable order.

On July 8, 2016, the Beltz plaintiffs filed a new action labeled as a "Verified Derivative And Class Action Complaint" in the United States District Court for the Western District of Pennsylvania. The action is captioned Patricia R. Beltz, Joseph S. Sullivan, and Anita Sullivan, individually and on behalf of all others similarly situated, and derivatively on behalf of Nominal Defendant Erie Insurance Exchange v. Erie Indemnity Company; Kaj Ahlmann; John T. Baily; Samuel P. Black, III; J. Ralph Borneman, Jr.; Terrence W. Cavanaugh; Wilson C. Cooney; LuAnn Datesh; Patricia A. Goldman; Jonathan Hirt Hagen; Thomas B. Hagen; C. Scott Hartz; Samuel P. Katz; Gwendolyn King; Claude C. Lilly, III; Martin J. Lippert; George R. Lucore; Jeffrey A. Ludrof; Edmund J. Mehl; Henry N. Nassau; Thomas W. Palmer; Martin P. Sheffield; Seth E. Schofield; Richard L. Stover; Jan R. Van Gorder; Elizabeth A. Hirt Vorsheck; Harry H. Weil; and Robert C. Wilburn (the "Beltz II" lawsuit). The individual defendants are all present or former Directors of Indemnity (the "Directors").

The allegations of the Beltz II lawsuit arise from the same fundamental, underlying claims as the Sullivan and prior Beltz litigation, i.e., that Indemnity improperly retained Service Charges and Added Service Charges. The Beltz II lawsuit alleges that the retention of the Service Charges and Added Service Charges was improper because, for among other reasons, that retention constituted a breach of the Subscriber’s Agreement and an Implied Covenant of Good Faith and Fair Dealing by Indemnity, breaches of fiduciary duty by Indemnity and the other defendants, conversion by Indemnity, and unjust enrichment by defendants Jonathan Hirt Hagen, Thomas B. Hagen, and Elizabeth A. Hirt Vorsheck, at the expense of Exchange. The Beltz II lawsuit requests, among other things, that a judgment be entered against the Defendants certifying the action as a class action pursuant to Rule 23 of the Federal Rules of Civil Procedure; declaring Plaintiffs as representatives of the Class and Plaintiffs’ counsel as counsel for the Class; declaring the conduct alleged as unlawful, including, but not limited to, Defendants’ retention of the Service Charges and Added Service Charges; enjoining Defendants from continuing to retain the Service Charges and Added Service Charges; and awarding compensatory and punitive damages and interest.

17

On September 23, 2016, Indemnity filed a motion to dismiss the Beltz II lawsuit. On September 30, 2016, the Directors filed their own motions to dismiss the Beltz II lawsuit. On July 17, 2017, the Court granted Indemnity’s and the Directors’ motions to dismiss the Beltz II lawsuit, dismissing the case in its entirety. The Court ruled that "the Subscriber’s Agreement does not govern the separate and additional charges at issue in the Complaint" and, therefore, dismissed the breach of contract claim against Indemnity for failure to state a claim. The Court also ruled that the remaining claims, including the claims for breach of fiduciary duty against Indemnity and the Directors, are barred by the applicable statutes of limitation or fail to state legally cognizable claims. On August 14, 2017, Plaintiffs filed a notice of appeal to the United States Court of Appeals for the Third Circuit.

On May 10, 2018, the United States Court of Appeals for the Third Circuit affirmed the District Court’s dismissal of the Beltz II lawsuit. On May 24, 2018, Plaintiffs filed a petition seeking rehearing of their appeal before the Third Circuit. The Third Circuit denied that petition on June 14, 2018.

For additional information on contingencies, see Part II, Item 8. "Financial Statements and Supplementary Data - Note 17, Commitment and Contingencies, of Notes to Financial Statements".

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

18

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Common Stock Market Prices and Dividends

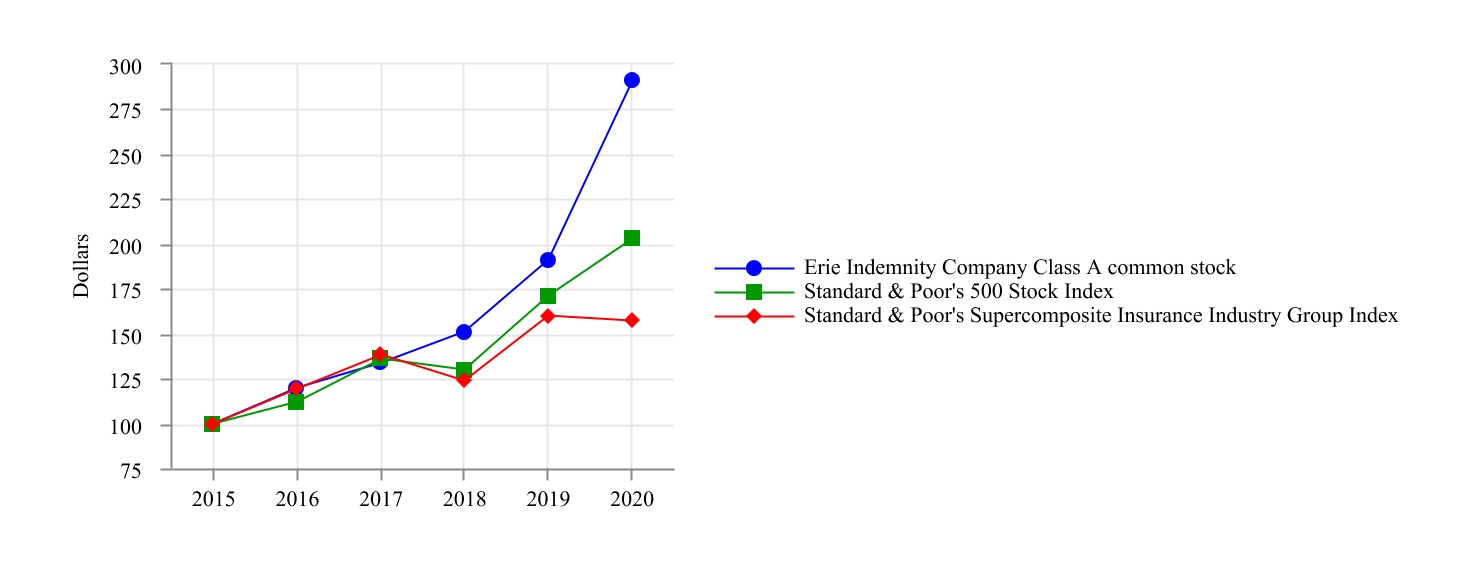

Our Class A, non-voting common stock trades on The NASDAQ Stock MarketSM LLC under the symbol "ERIE". No established trading market exists for the Class B voting common stock. Broadridge Corporate Issuer Solutions, Inc. serves as our transfer agent and registrar. As of February 19, 2021, there were approximately 561 shareholders of record for the Class A non-voting common stock and 9 shareholders of record for the Class B voting common stock.