Exhibit 99.2 Strategically Positioning Truist Insurance Holdings for Long-Term Success Bill Rogers – Chairman & CEO Mike Maguire – CFO John Howard – Chief Insurance Officer Truist Financial Corporation February 16, 2023 1

Forward-looking statements This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, regarding the financial condition, results of operations, business plans and the future performance of Truist. Words such as “anticipates,” “believes,” “estimates,” “expects,” “forecasts,” “intends,” “plans,” “projects,” “may,” “will,” “should,” “would,” “could” and other similar expressions are intended to identify these forward-looking statements. Forward-looking statements are not based on historical facts but instead represent management’s expectations and assumptions reg arding Truist’s business, the economy and other future conditions. Such statements involve inherent uncertainties, risks and changes in circumstances that are difficult to predict. As such, Truist’s actual results may differ materially from those contemplated by forward-looking statements. While there can be no assurance that any list of risks and uncertainties or risk factors is complete, important factors that could cause actual results to differ materially from those contemplated by forward-looking statements include the following, without limitation, as well as the risks and uncertainties more fully discussed under Part I, Item 1A -Risk Factors in our Annual Report on Form 10-K for the year ended December 31, 2021 and in Truist’s subsequent filings with the Securities and Exchange Commission: – changes in the interest rate environment, including the replacement of LIBOR as an interest rate benchmark, could adversely affect Truist’s revenue and expenses, the value of assets and obligations, and the availability and cost of capital, cash flows, and liquidity; – Truist is subject to credit risk by lending or committing to lend money, may have more credit risk and higher credit losses to the extent that loans are concentrated by loan type, industry segment, borrower type or location of the borrower or collateral, and may suffer losses if the value of collateral declines in stressed market conditions; – inability to access short-term funding or liquidity, loss of client deposits or changes in Truist’s credit ratings could increase the cost of funding or limit access to capital markets; – general economic or business conditions, either globally, nationally or regionally, may be less favorable than expected, including as a result of supply chain disruptions, inflationary pressures and labor shortages, and instability in global geopolitica l matters, including due to an outbreak or escalation of hostilities, or volatility in financial markets could result in, among other things, slower deposit or asset growth, a deterioration in credit quality, or a reduced demand for credit, insurance, or other services; – the monetary and fiscal policies of the federal government and its agencies, including in response to rising inflation, could have a material adverse effect on the economy and Truist’s profitability; – the effects of COVID-19 have adversely impacted the Company’s operations and financial performance and could have similar adverse impacts in future periods; – risk management oversight functions may not identify or address risks adequately, and management may not be able to effective ly manage credit risk; – there are risks resulting from the extensive use of models in Truist’s business, which may impact decisions made by management and regulators; – deposit attrition, client loss or revenue loss following completed mergers or acquisitions may be greater than anticipated; – Truist could fail to execute on strategic or operational plans, including the ability to successfully complete or integrate mergers and acquisitions; – increased competition, including from (i) new or existing competitors that could have greater financial resources or be subject to different regulatory standards or compliance costs, and (ii) products and services offered by non-bank financial technology companies, may reduce Truist’s client base, cause Truist to lower prices for its products and services in order to maintain market share or otherwise adversely impact Truist’s businesses or results of operations; – failure to maintain or enhance Truist’s competitive position with respect to new products, services, and technology, whether it fails to anticipate client expectatio ns or because its technological developments fail to perform as desired or do not achieve market acceptance or regulatory approval or for other reasons, may cause Truist to lose market share or incur additional expense; – negative public opinion could damage Truist’s reputation and adversely impact business and revenues; – regulatory matters, litigation or other legal actions may result in, among other things, costs, fines, penalties, restriction s on Truist’s business activities, reputational harm, negative publicity, or other adverse consequences; – Truist faces substantial legal and operational risks in safeguarding personal information; – evolving legislative, accounting and regulatory standards, including with respect to climate, capital, and liquidity requirem ents, and results of regulatory examinations may adversely affect Truist’s financial condition and results of operations; – increased scrutiny regarding Truist’s consumer sales practices, training practices, incentive compensation design, and governance could damage its reputation and a dversely impact business and revenues; – accounting policies and processes require management to make estimates about matters that are uncertain, including the potential write down to goodwill if there is an elongated period of decline in market value for Truist’s stock and adverse economic conditions are sustained over a period of time; – Truist faces risks related to originating and selling mortgages, including repurchase and indemnity demands from purchasers related to representations and warranties on loans sold, which could result in an increase in the amount of losses for loan repurchases; – there are risks relating to Truist’s role as a loan servicer, including an increase in the scope or costs of the services Truist is required to perform without any corresponding increase in servicing fees or a breach of Truist’s obligations as servicer; – Truist’s success depends on hiring and retaining key teammates, and if these individuals leave or change roles without effective replacements, Truist’s operations could be adversely impacted, which could be exacerbated in the increased work -from-home environment as job markets may be less constrained by physical geography; – Truist’s operations rely on its ability, and the ability of key external parties, to maintain appropriate -staffed workforces, and on the competence, trustworthiness, health and safety of teammates; – Truist faces the risk of fraud or misconduct by internal or external parties, which Truist may not be able to prevent, detect, or mitigate; – security risks, including denial of service attacks, hacking, social engineering attacks targeting Truist’s teammates and clients, malware intrusion, data corruption attempts, system breaches, cyber-attacks, which have increased in frequency with current geopolitical tensions, identity theft, ransomware attacks, and physical security risks, such as natural disasters, environmental conditions, and intent ional acts of destruction, could result in the disclosure of confidential information, adversely affect Truist’s business or reputation or create significant legal or financial exposure; and – widespread outages of operational, communication, or other systems, whether internal or provided by third parties, natural or other disasters (including acts of terrorism and pandemics), and the effects of climate change, including physical risks, such as more frequent and intense weather events, and risks related to the transition to a lower carbon economy, such as regulatory or technological changes or shifts in market dynamics or consumer preferences, could have an adverse effect on Truist’s financial condition and results of operations, lead to material disruption of Truist’s operations or the ability or willingness of clients to access Truist’s products and services. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date they are made. Except to the extent required by applicable law or regulation, Truist undertakes no obligation to revise or update any forward-looking statements. 2 2

Non-GAAP information This presentation contains financial information and performance measures determined by methods other than in accordance with accounting principles generally accepted in the United States of America ( GAAP ). Truist’s management uses these “non-GAAP” measures in their analysis of the Corporation's performance and the efficiency of its operations. Management believes these non-GAAP measures provide a greater understanding of ongoing operations, enhance comparability of results with prior periods and demonstrate the ef fects of significant items in the current period. The Company believes a meaningful analysis of its financial performance requires an understanding of the factors underlying that performance. Truist’s management believes investors may find these non-GAAP financial measures useful. These disclosures should not be viewed as a substitute for financial measures determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. Below is a listing of the types of non-GAAP measures used in this presentation: Adjusted Performance Measures - The adjusted performance measures, including adjusted net income available to common shareholders and adjusted diluted EPS ar e non-GAAP in that they exclude merger-related and restructuring charges, other selected items, and amortization of intangible assets, as applicable to tangible measures. Truist’s management uses these measures in their analysis of the Corporation’s performance. Truist’s management believes these measures provide a greater understanding of ongoing operations and enhance comparability of results with prior periods, as well as demonstrate the effects of significant gains and charges. Insurance Holdings Adjusted EBITDA - EBITDA is a non-GAAP measurement of operating profitability that is calculated by adding back interest, taxes, depreciation, an d amortization to net income. Truist’s management also adds back merger-related and restructuring charges, incremental operating expenses related to the merger, and other selected items. Truist’s management uses this measure in its analysis of the Corporation’s Insurance Holdings segment. Truist’s management believes this measure provides a greater understanding of ongoing operations and enhances comparability of results with prior periods and insurance brokerage peers, as well as demonstrates th e effects of significant gains and charges. 3 3

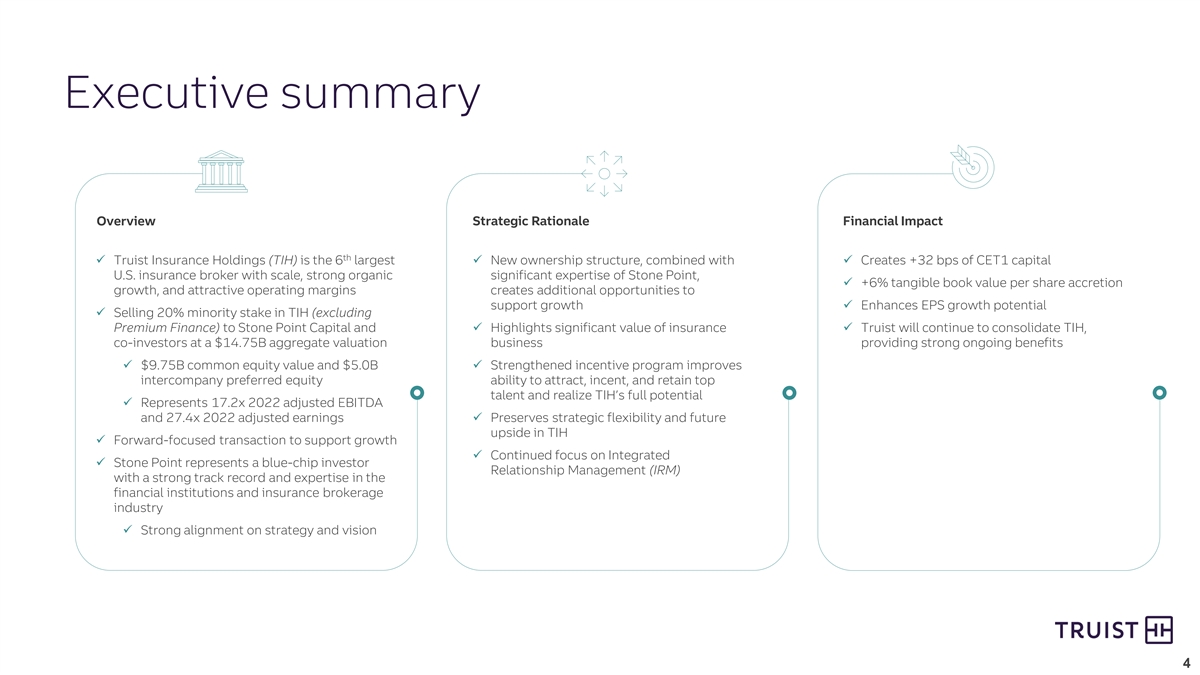

Executive summary Overview Strategic Rationale Financial Impact th ü Truist Insurance Holdings (TIH) is the 6 largest ü New ownership structure, combined with ü Creates +32 bps of CET1 capital U.S. insurance broker with scale, strong organic significant expertise of Stone Point, ü +6% tangible book value per share accretion growth, and attractive operating margins creates additional opportunities to support growth ü Enhances EPS growth potential ü Selling 20% minority stake in TIH (excluding Premium Finance) to Stone Point Capital and ü Highlights significant value of insurance ü Truist will continue to consolidate TIH, co-investors at a $14.75B aggregate valuation business providing strong ongoing benefits ü $9.75B common equity value and $5.0B ü Strengthened incentive program improves intercompany preferred equity ability to attract, incent, and retain top talent and realize TIH’s full potential ü Represents 17.2x 2022 adjusted EBITDA and 27.4x 2022 adjusted earningsü Preserves strategic flexibility and future upside in TIH ü Forward-focused transaction to support growth ü Continued focus on Integrated ü Stone Point represents a blue-chip investor Relationship Management (IRM) with a strong track record and expertise in the financial institutions and insurance brokerage industry ü Strong alignment on strategy and vision 4 4

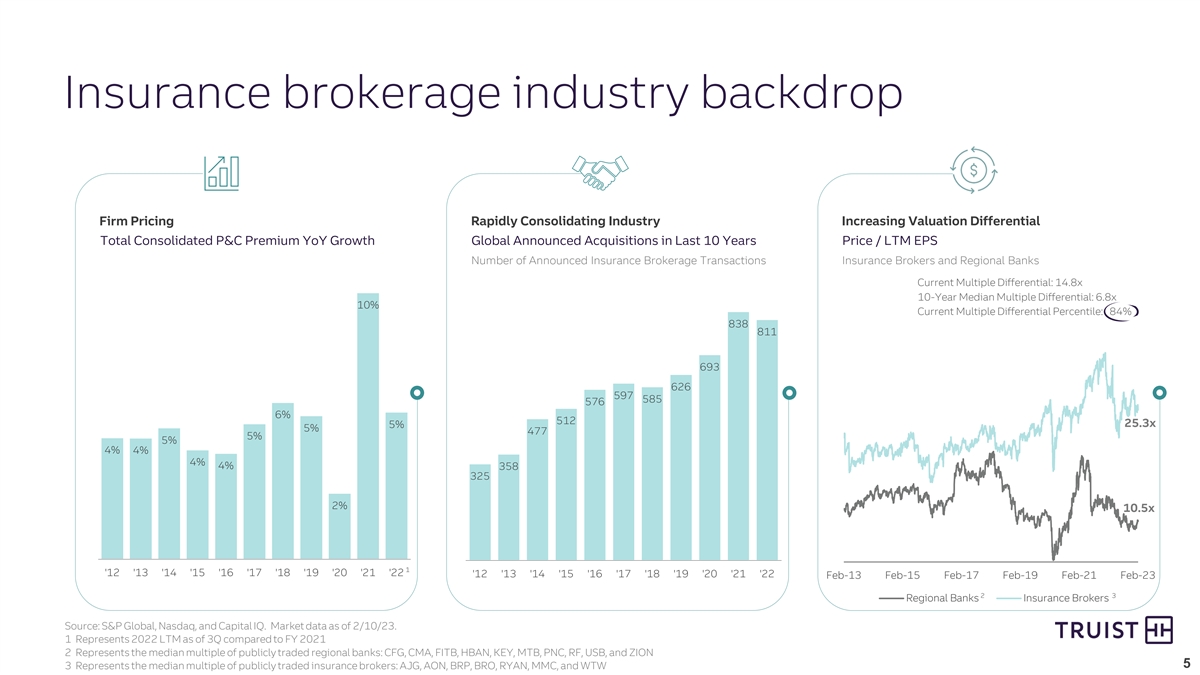

Insurance brokerage industry backdrop Firm Pricing Rapidly Consolidating Industry Increasing Valuation Differential Total Consolidated P&C Premium YoY Growth Global Announced Acquisitions in Last 10 Years Price / LTM EPS Number of Announced Insurance Brokerage Transactions Insurance Brokers and Regional Banks Current Multiple Differential: 14.8x 10-Year Median Multiple Differential: 6.8x 10% Current Multiple Differential Percentile: 84% 838 811 693 626 597 585 576 6% 512 5% 25.3x 5% 477 5% 5% 4% 4% 4% 4% 358 325 2% 10.5x 1 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 Feb-13 Feb-15 Feb-17 Feb-19 Feb-21 Feb-23 2 3 Regional Banks Insurance Brokers Source: S&P Global, Nasdaq, and Capital IQ. Market data as of 2/10/23. 1 Represents 2022 LTM as of 3Q compared to FY 2021 2 Represents the median multiple of publicly traded regional banks: CFG, CMA, FITB, HBAN, KEY, MTB, PNC, RF, USB, and ZION 5 5 3 Represents the median multiple of publicly traded insurance brokers: AJG, AON, BRP, BRO, RYAN, MMC, and WTW

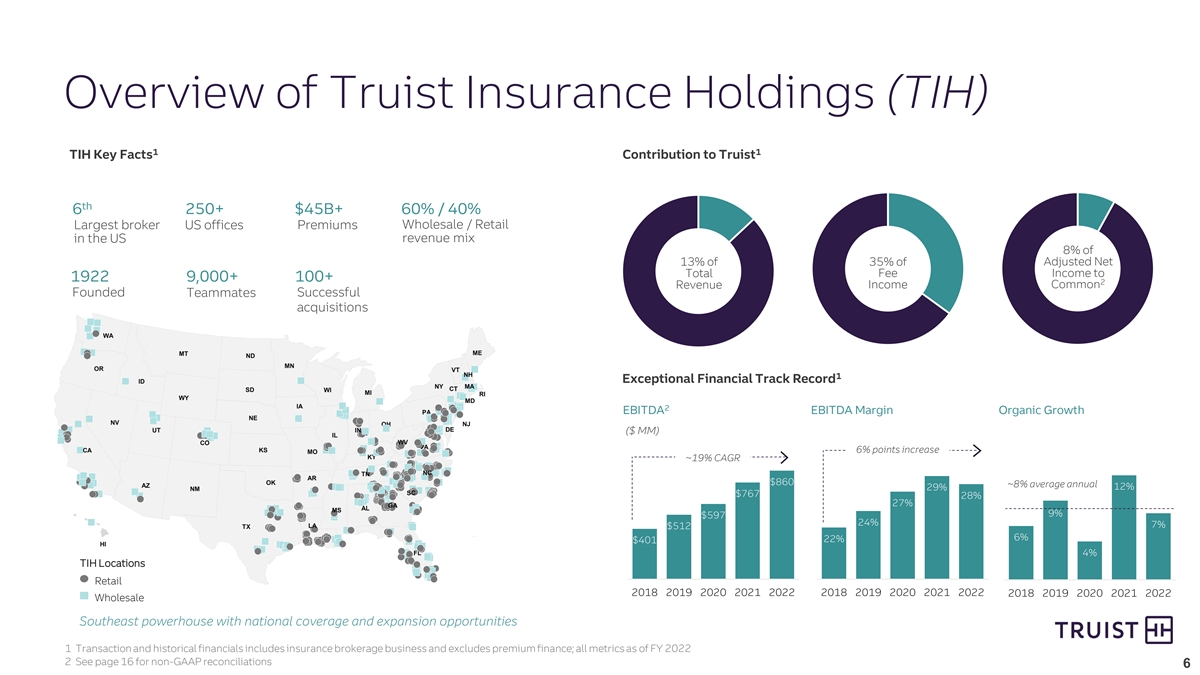

Overview of Truist Insurance Holdings (TIH) 1 1 TIH Key Facts Contribution to Truist th 6 250+ $45B+ 60% / 40% Largest broker Premiums Wholesale / Retail US offices in the US revenue mix 8% of Adjusted Net 13% of 35% of Total Fee Income to 1922 9,000+ 100+ 2 Revenue Income Common Founded Successful Teammates acquisitions WA ME MT ND MN OR VT NH 1 Exceptional Financial Track Record ID NY MA CT SD WI MI RI WY MD IA 2 EBITDA EBITDA Margin Organic Growth PA NE NV OH NJ UT IN DE ($ MM) IL CO WV VA CA KS 6% points increase MO KY ~19% CAGR NC TN AR OK $860 AZ ~8% average annual 12% NM 29% SC $767 28% 27% GA AL MS 9% $597 24% 7% TX LA $512 6% 22% $401 HI FL 4% TIH Locations Retail 2018 2019 2020 2021 2022 2018 2019 2020 2021 2022 2018 2019 2020 2021 2022 Wholesale Southeast powerhouse with national coverage and expansion opportunities 1 Transaction and historical financials includes insurance brokerage business and excludes premium finance; all metrics as of FY 2022 2 See page 16 for non-GAAP reconciliations 6

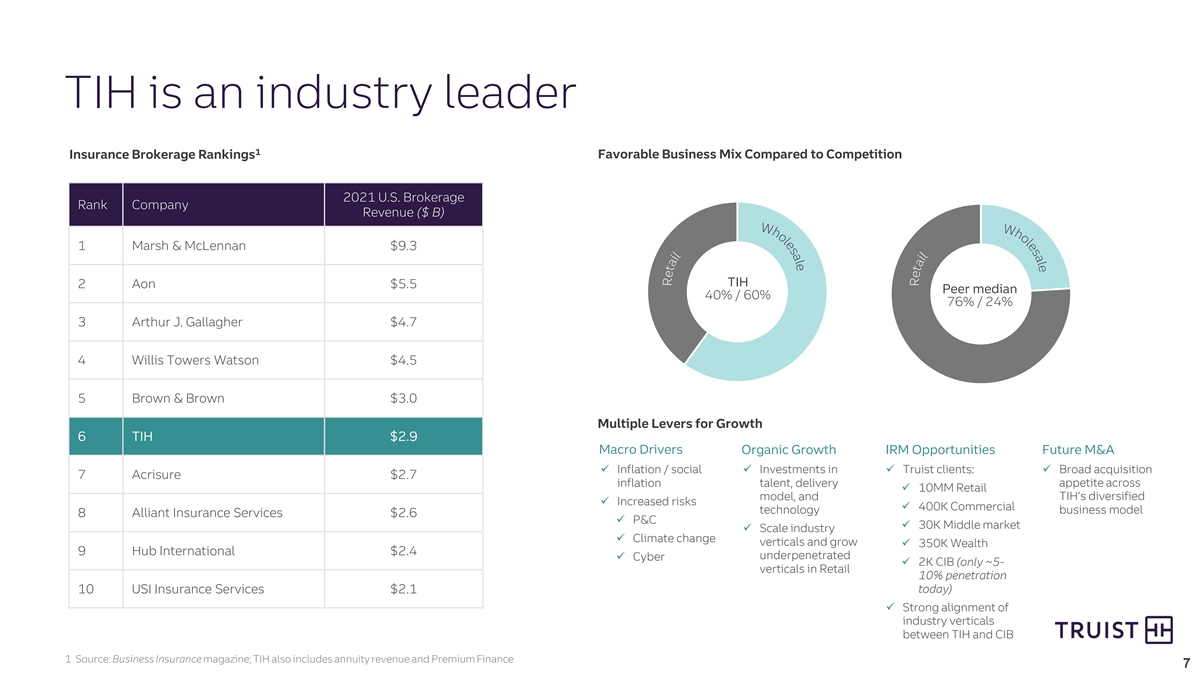

TIH is an industry leader 1 Insurance Brokerage Rankings Favorable Business Mix Compared to Competition 2021 U.S. Brokerage Rank Company Revenue ($ B) 1 Marsh & McLennan $9.3 TIH 2 Aon $5.5 Peer median 40% / 60% 76% / 24% 3 Arthur J. Gallagher $4.7 4 Willis Towers Watson $4.5 5 Brown & Brown $3.0 Multiple Levers for Growth 6 TIH $2.9 Macro Drivers Organic Growth IRM Opportunities Future M&A ü Inflation / social ü Investments in ü Truist clients:ü Broad acquisition 7 Acrisure $2.7 appetite across inflation talent, delivery ü 10MM Retail model, and TIH’s diversified ü Increased risks ü 400K Commercial technology business model 8 Alliant Insurance Services $2.6 ü P&C ü 30K Middle market ü Scale industry ü Climate change verticals and grow ü 350K Wealth 9 Hub International $2.4 underpenetrated ü Cyber ü 2K CIB (only ~5- verticals in Retail 10% penetration today) 10 USI Insurance Services $2.1 ü Strong alignment of industry verticals between TIH and CIB 1 Source: Business Insurance magazine; TIH also includes annuity revenue and Premium Finance 7

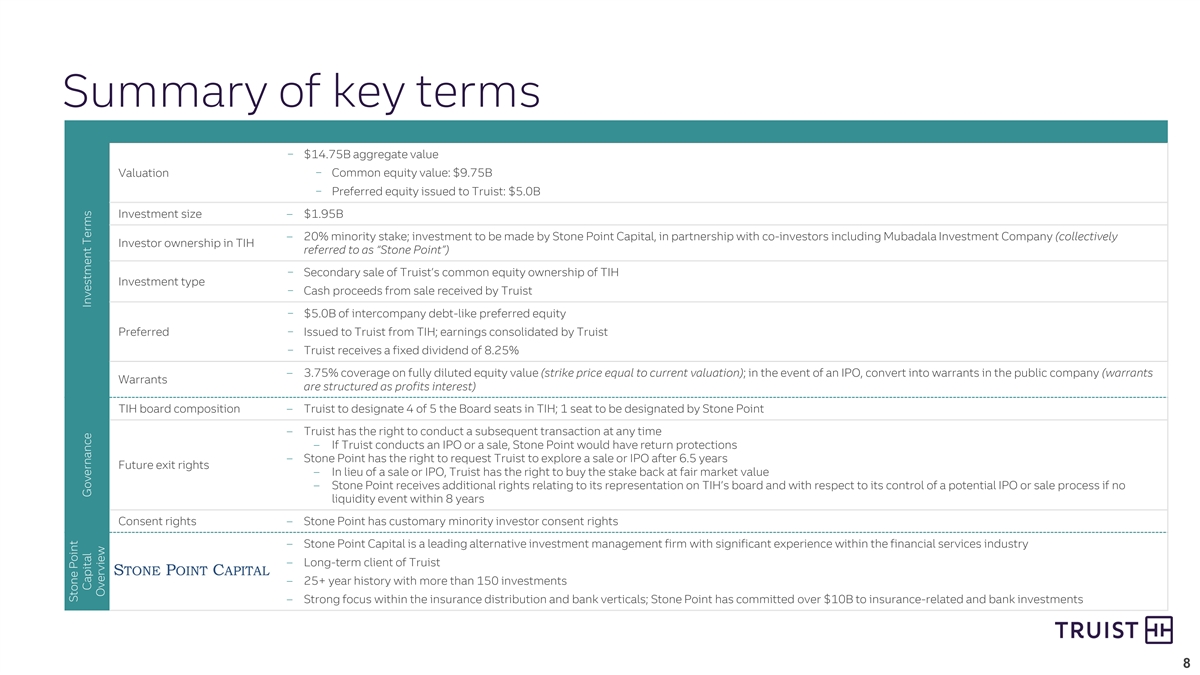

Summary of key terms − $14.75B aggregate value Valuation − Common equity value: $9.75B − Preferred equity issued to Truist: $5.0B Investment size – $1.95B – 20% minority stake; investment to be made by Stone Point Capital, in partnership with co-investors including Mubadala Investment Company (collectively Investor ownership in TIH referred to as “Stone Point”) − Secondary sale of Truist’s common equity ownership of TIH Investment type − Cash proceeds from sale received by Truist − $5.0B of intercompany debt-like preferred equity Preferred − Issued to Truist from TIH; earnings consolidated by Truist − Truist receives a fixed dividend of 8.25% – 3.75% coverage on fully diluted equity value (strike price equal to current valuation); in the event of an IPO, convert into warrants in the public company (warrants Warrants are structured as profits interest) TIH board composition – Truist to designate 4 of 5 the Board seats in TIH; 1 seat to be designated by Stone Point – Truist has the right to conduct a subsequent transaction at any time – If Truist conducts an IPO or a sale, Stone Point would have return protections – Stone Point has the right to request Truist to explore a sale or IPO after 6.5 years Future exit rights – In lieu of a sale or IPO, Truist has the right to buy the stake back at fair market value – Stone Point receives additional rights relating to its representation on TIH’s board and with respect to its control of a potential IPO or sale process if no liquidity event within 8 years Consent rights – Stone Point has customary minority investor consent rights – Stone Point Capital is a leading alternative investment management firm with significant experience within the financial services industry – Long-term client of Truist – 25+ year history with more than 150 investments – Strong focus within the insurance distribution and bank verticals; Stone Point has committed over $10B to insurance-related and bank investments 8 Stone Point Capital Governance Investment Terms Overview

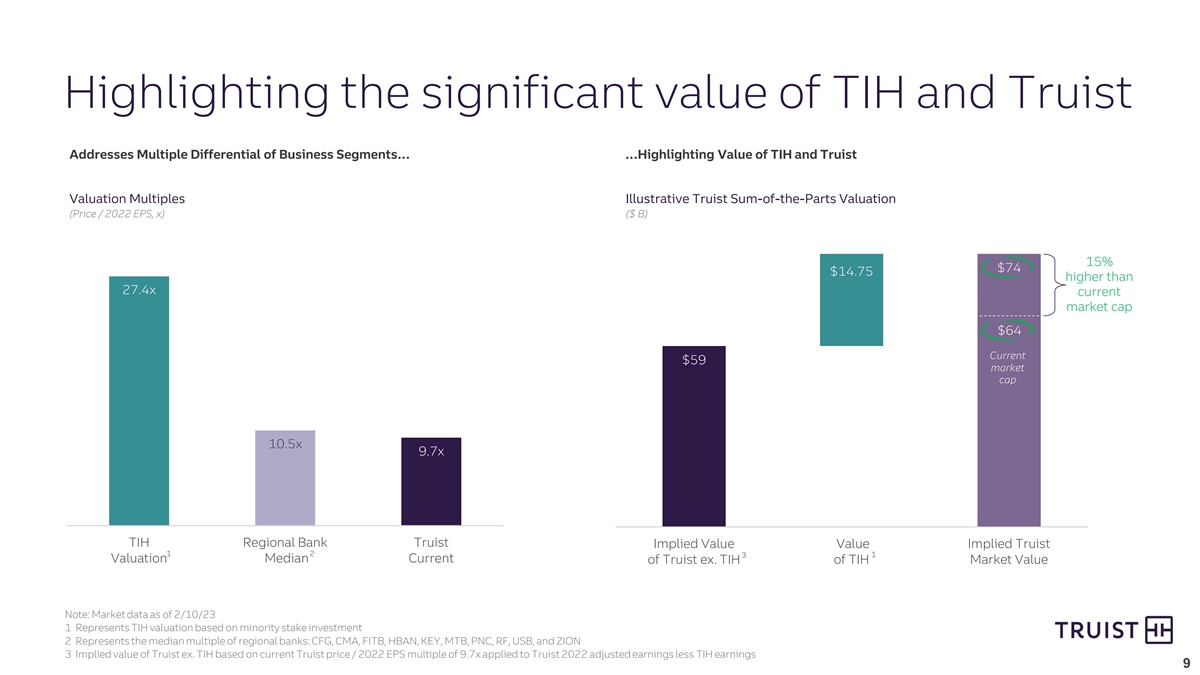

Highlighting the significant value of TIH and Truist Addresses Multiple Differential of Business Segments… …Highlighting Value of TIH and Truist Valuation Multiples Illustrative Truist Sum-of-the-Parts Valuation (Price / 2022 EPS, x) ($ B) 15% $74 $14.75 higher than 27.4x current market cap $64 Current $59 market cap 10.5x 9.7x TIH Regional Bank Truist Implied Value Value Implied Truist 1 2 3 1 Valuation Median Current of Truist ex. TIH of TIH Market Value Note: Market data as of 2/10/23 1 Represents TIH valuation based on minority stake investment 2 Represents the median multiple of regional banks: CFG, CMA, FITB, HBAN, KEY, MTB, PNC, RF, USB, and ZION 3 Implied value of Truist ex. TIH based on current Truist price / 2022 EPS multiple of 9.7x applied to Truist 2022 adjusted earnings less TIH earnings 9

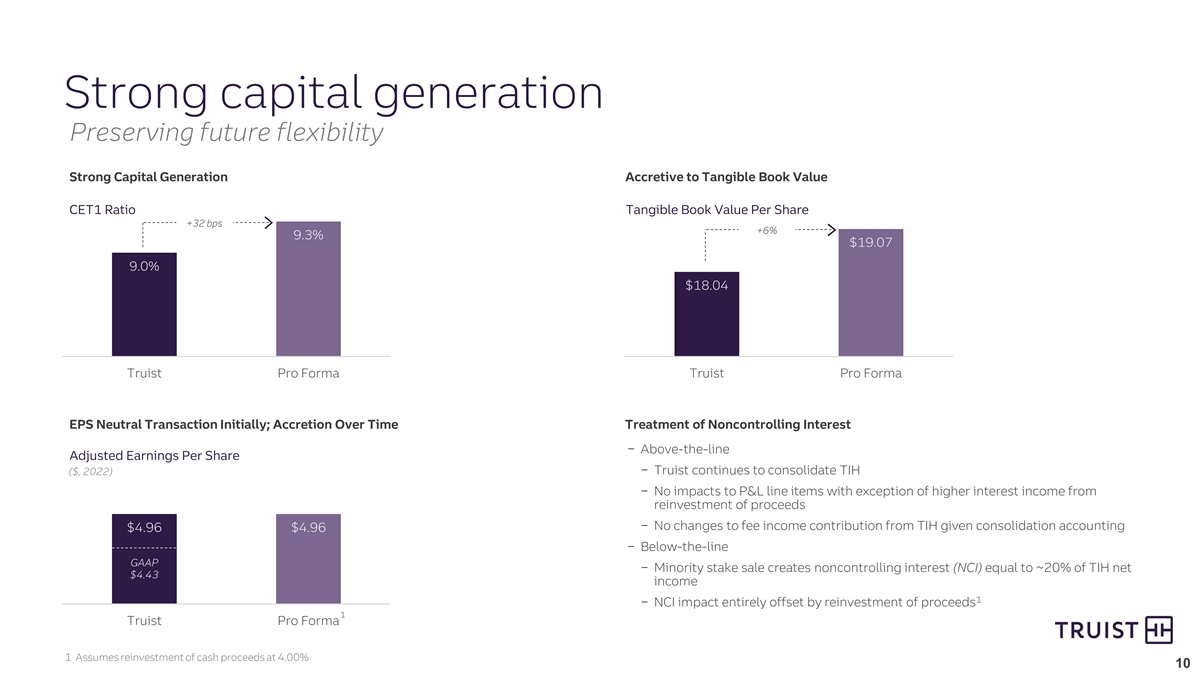

Strong capital generation Preserving future flexibility Strong Capital Generation Accretive to Tangible Book Value CET1 Ratio Tangible Book Value Per Share +32 bps +6% 9.3% $19.07 9.0% $18.04 Truist Pro Forma Truist Pro Forma EPS Neutral Transaction Initially; Accretion Over Time Treatment of Noncontrolling Interest − Above-the-line Adjusted Earnings Per Share ($, 2022) − Truist continues to consolidate TIH − No impacts to P&L line items with exception of higher interest income from reinvestment of proceeds − No changes to fee income contribution from TIH given consolidation accounting $4.96 $4.96 − Below-the-line GAAP − Minority stake sale creates noncontrolling interest (NCI) equal to ~20% of TIH net $4.43 income 1 − NCI impact entirely offset by reinvestment of proceeds 1 Truist Pro Forma 1 Assumes reinvestment of cash proceeds at 4.00% 10

Conclusion Compelling Strategic Rationale Attractive Financial Impacts ü New ownership structure, combined with ü Creates +32 bps of CET1 capital significant expertise of Stone Point, creates additional opportunities to support growth ü +6% tangible book value per share accretion ü Enhances EPS growth potential ü Highlights significant value of insurance business Transaction ü Truist will continue to consolidate TIH, providing Terms ü Strengthened incentive program improves strong ongoing benefits ability to attract, incent, and retain top talent and realize TIH’s full potential ü Preserves strategic flexibility and future upside in TIH ü Continued focus on Integrated Relationship Management (IRM) 11 11

Appendix Appendix

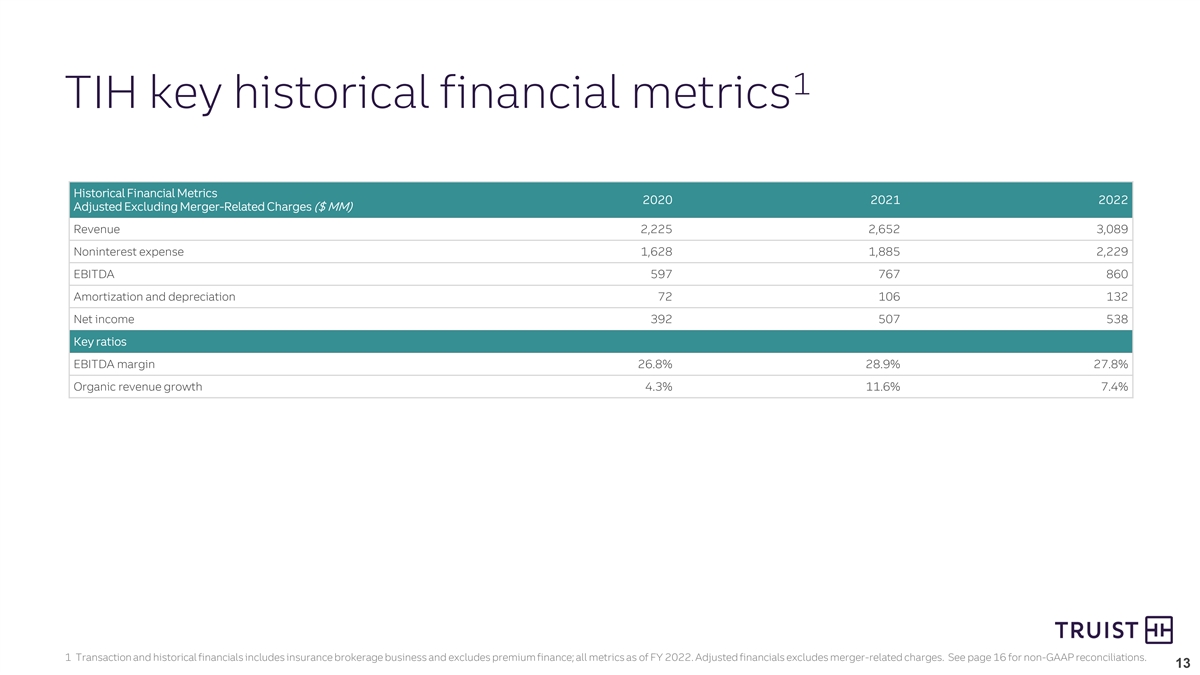

1 TIH key historical financial metrics Historical Financial Metrics 2020 2021 2022 Adjusted Excluding Merger-Related Charges ($ MM) Revenue 2,225 2,652 3,089 Noninterest expense 1,628 1,885 2,229 EBITDA 597 767 860 Amortization and depreciation 72 106 132 Net income 392 507 538 Key ratios EBITDA margin 26.8% 28.9% 27.8% Organic revenue growth 4.3% 11.6% 7.4% 1 Transaction and historical financials includes insurance brokerage business and excludes premium finance; all metrics as of FY 2022. Adjusted financials excludes merger-related charges. See page 16 for non-GAAP reconciliations. 13 13

Illustrative pro forma financial impacts Illustrative Financial Statement Impact Illustrative Net Transaction Capital & Cash Truist ($ MM) 1 ($ MM) Minority Stake Sale Reinvestment of Proceeds Pro Forma Current Stake sale proceeds 1,950 Balance Sheet Taxes due (387) Cash and securities 150,935 1,538 - 152,473 DTL created (143) Common equity 53,841 1,340 - 55,181 Noncontrolling interest created (54) Noncontrolling interest 23 54 - 77 Estimated transaction expenses (25) Net common equity created 1,340 Capital CET1 ratio (%) 9.0 - - 9.3 Net cash proceeds (after-tax) 1,538 TBV per share ($) 18.04 - - 19.07 2 Adjusted Earnings Impact – 2022 Pre-tax pre-provision revenue 10,107 - 62 10,169 Pre-tax income 8,747 - 62 8,809 Tax expense 1,764 (24) 15 1,755 Net income 6,983 24 47 7,054 Noncontrolling interest 7 70 - 77 attribution Preferred dividends 333 - - 333 3 Net income to common 6,643 (46) 47 6,644 Earnings per share ($) 4.96 4.96 1 Assumes reinvestment of cash proceeds at 4.00% 2 Pro forma financial impacts for earnings items shown relative to 2022 adjusted financials for illustrative purposes and 12/31/2022 for balance sheet. Transaction includes insurance brokerage business and excludes premium finance; all metrics as of FY 2022. Represents adjusted financials excluding merger-related and restructuring charges and other selected items. Adjusted metrics are non-GAAP measures. Truist’s management believes these measures provide a greater understanding of ongoing operations and enhances comparability of results with prior periods. Reconciliations to GAAP can be found in appendix of this presentation or the 4Q22 earnings presentation. 3 Represents impact of ~20% of TIH partnership net income (net of preferred dividend payment to Truist) 14 14

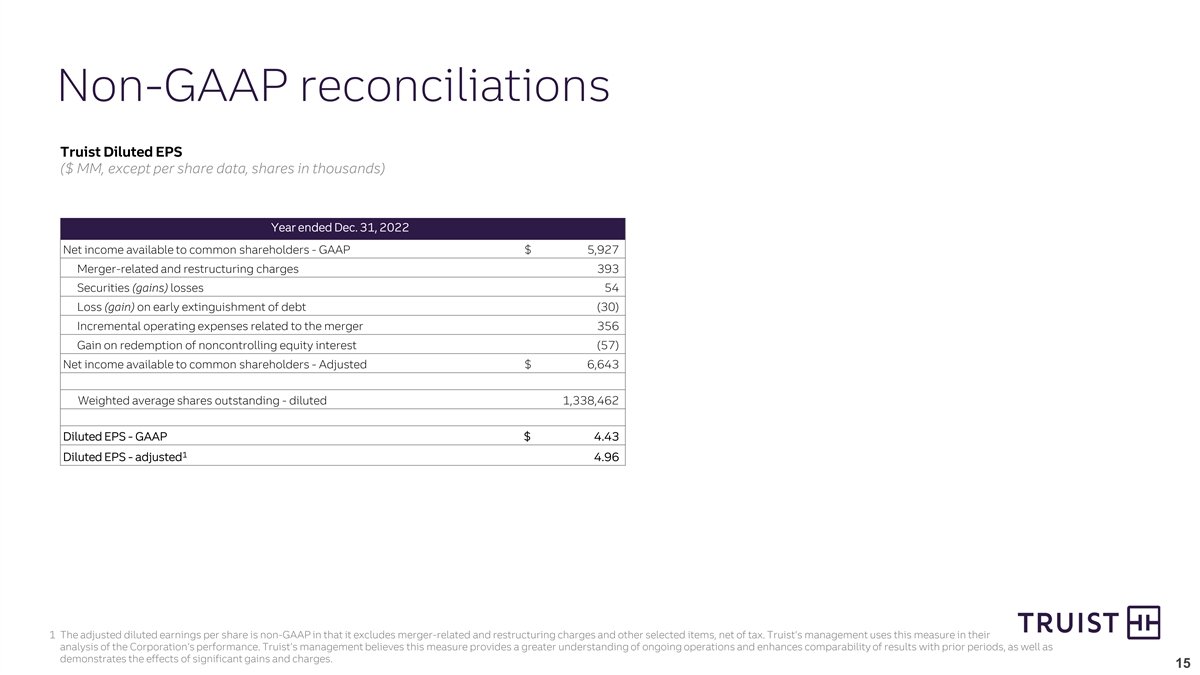

Non-GAAP reconciliations Truist Diluted EPS ($ MM, except per share data, shares in thousands) Year ended Dec. 31, 2022 Net income available to common shareholders - GAAP $ 5,927 Merger-related and restructuring charges 393 Securities (gains) losses 54 Loss (gain) on early extinguishment of debt (30) Incremental operating expenses related to the merger 356 Gain on redemption of noncontrolling equity interest (57) Net income available to common shareholders - Adjusted $ 6,643 Weighted average shares outstanding - diluted 1,338,462 Diluted EPS - GAAP $ 4.43 1 Diluted EPS - adjusted 4.96 1 The adjusted diluted earnings per share is non-GAAP in that it excludes merger-related and restructuring charges and other selected items, net of tax. Truist’s management uses this measure in their analysis of the Corporation’s performance. Truist’s management believes this measure provides a greater understanding of ongoing operations and enhances comparability of results with prior periods, as well as demonstrates the effects of significant gains and charges. A-15 15

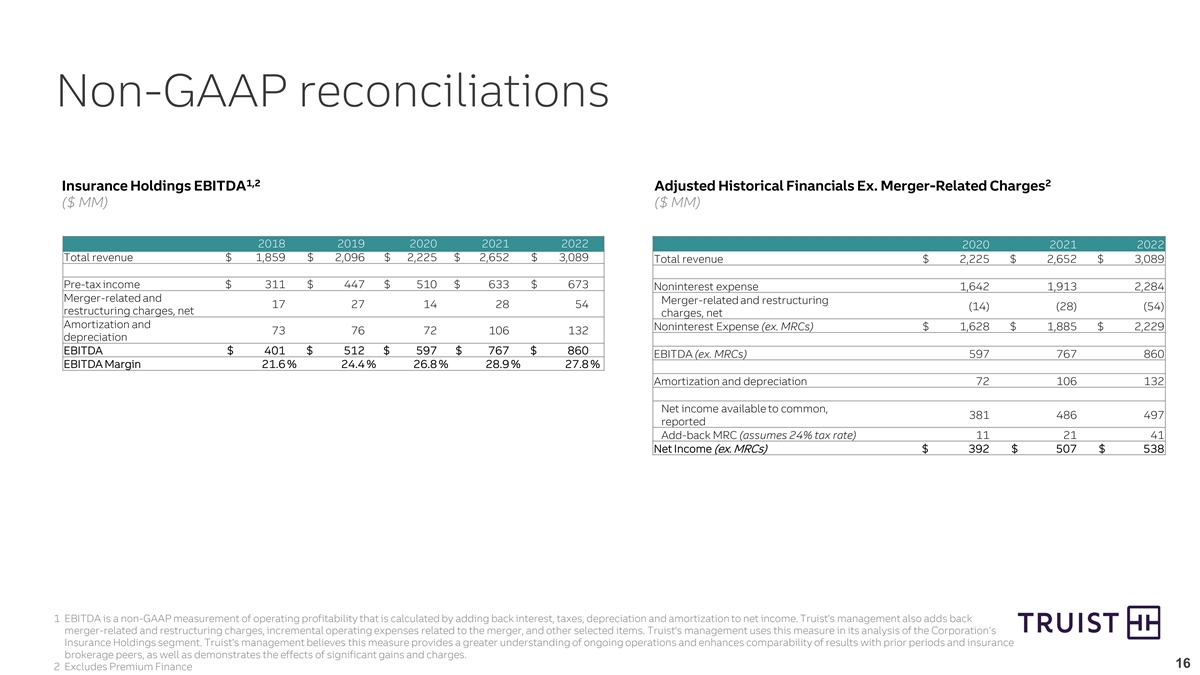

Non-GAAP reconciliations 1,2 2 Insurance Holdings EBITDA Adjusted Historical Financials Ex. Merger-Related Charges ($ MM) ($ MM) 2018 2019 2020 2021 2022 2020 2021 2022 Total revenue $ 1,859 $ 2,096 $ 2,225 $ 2,652 $ 3,089 Total revenue $ 2,225 $ 2,652 $ 3,089 Pre-tax income $ 311 $ 447 $ 510 $ 633 $ 673 Noninterest expense 1,642 1,913 2,284 Merger-related and Merger-related and restructuring 17 27 14 28 54 (14) (28) (54) restructuring charges, net charges, net Amortization and Noninterest Expense (ex. MRCs) $ 1,628 $ 1,885 $ 2,229 73 76 72 106 132 depreciation EBITDA $ 401 $ 512 $ 597 $ 767 $ 860 EBITDA (ex. MRCs) 597 767 860 EBITDA Margin 21.6 % 24.4 % 26.8 % 28.9 % 27.8 % Amortization and depreciation 72 106 132 Net income available to common, 381 486 497 reported Add-back MRC (assumes 24% tax rate) 11 21 41 Net Income (ex. MRCs) $ 392 $ 507 $ 538 1 EBITDA is a non-GAAP measurement of operating profitability that is calculated by adding back interest, taxes, depreciation and amortization to net income. Truist's management also adds back merger-related and restructuring charges, incremental operating expenses related to the merger, and other selected items. Truist's management uses this measure in its analysis of the Corporation’s Insurance Holdings segment. Truist's management believes this measure provides a greater understanding of ongoing operations and enhances comparability of results with prior periods and insurance brokerage peers, as well as demonstrates the effects of significant gains and charges. A-16 16 2 Excludes Premium Finance