UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended | |

or | |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | |

Commission File Number

(Exact name of registrant as specified in its charter)

| ||

(State or other jurisdiction of | (I.R.S. Employer Identification No.) | |

incorporation and organization) |

(Address of principal executive offices, including zip code) | ( (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ |

Smaller reporting company | |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

As of June 30, 2023, the aggregate market value of voting stock held by non-affiliates of the Registrant, based on the closing price of the Common Stock on June 30, 2023 (the last business day of the Registrant’s most recently completed second quarter) as quoted on the NYSE American, was approximately $

As of March 15, 2024,

Document Incorporated by Reference

Portions of the registrant’s Definitive Proxy Statement relating to the 2024 Annual Meeting of Stockholders, which will be filed with the Securities and Exchange Commission within 120 days after the end of the registrant’s fiscal year ended December 31, 2023, are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

ARMATA PHARMACEUTICALS, INC.

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Annual Report”) and certain information incorporated herein by reference contain forward-looking statements, which are provided under the “safe harbor” protection of the Private Securities Litigation Reform Act of 1995. These statements relate to future events, results or to our future financial performance and involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or events to be materially different from any future results, performance or events expressed or implied by the forward-looking statements. Forward-looking statements in this Annual Report include, but are not limited to, statements regarding:

| ● | our estimates regarding anticipated operating losses, capital requirements and needs for additional funds; |

| ● | our ability to raise additional capital when needed and to continue as a going concern; |

| ● | our ability to manufacture, or otherwise secure the manufacture of, sufficient amounts of our product candidates for our preclinical studies and clinical trials; |

| ● | our clinical development plans, including planned clinical trials; |

| ● | our research and development plans, including our clinical development plans; |

| ● | our ability to select combinations of phages to formulate our product candidates; |

| ● | our development of bacteriophage-based therapies; |

| ● | the potential use of bacteriophages to treat bacterial infections; |

| ● | the potential future of antibiotic resistance; |

| ● | our ability for bacteriophage therapies to disrupt and destroy biofilms and restore sensitivity to antibiotics; |

| ● | our planned development strategy, presenting data to regulatory agencies and defining planned clinical studies; |

| ● | the expected timing of additional clinical trials, including Phase 1b/Phase 2 or registrational clinical trials; |

| ● | our ability to manufacture and secure sufficient quantities of our product candidates for clinical trials; |

| ● | the drug product candidates to be supplied by us for clinical trials; |

| ● | the potential for bacteriophage technology being uniquely positioned to address the global threat of antibiotic resistance; |

| ● | the safety and efficacy of our product candidates; |

| ● | our anticipated regulatory pathways for our product candidates; |

| ● | the activities to be performed by specific parties in connection with clinical trials; |

| ● | our ability to successfully complete preclinical and clinical development of, and obtain regulatory approval of our product candidates and commercialize any approved products on our expected timeframes or at all; |

| ● | our pursuit of additional indications; |

3

| ● | the content and timing of submissions to and decisions made by the U.S. Food and Drug Administration (the “FDA”) and other regulatory agencies; |

| ● | our ability to leverage the experience of our management team and to attract and retain management and other key personnel; |

| ● | the capacities and performance of our suppliers, manufacturers, contract research organizations (“CROs”) and other third parties over whom we have limited control; |

| ● | our ability to staff and maintain our Marina del Rey production facility under fully compliant current Good Manufacturing Practices (“cGMP”); |

| ● | the actions of our competitors and success of competing drugs or other therapies that are or may become available; |

| ● | our expectations with respect to future growth and investments in our infrastructure, and our ability to effectively manage any such growth; |

| ● | the size and potential growth of the markets for any of our product candidates, and our ability to capture share in or impact the size of those markets; |

| ● | the benefits of our product candidates; |

| ● | potential market growth and market and industry trends; |

| ● | maintaining collaborations with third parties including our partnerships with the Cystic Fibrosis Foundation (“CFF”), and the U.S. Department of Defense (the “DoD”); |

| ● | potential future collaborations with third parties and the potential markets and market opportunities for product candidates; |

| ● | our ability to achieve our vision, including improvements through engineering and success of clinical trials; |

| ● | our ability to meet anticipated milestones in the development and testing of the relevant product; |

| ● | our ability to be a leader in the development of phage-based therapeutics; |

| ● | the expected use of proceeds from the $16.3 million DoD grant; |

| ● | the effects of government regulation and regulatory developments, and our ability and the ability of the third parties with whom we engage to comply with applicable regulatory requirements; |

| ● | the accuracy of our estimates regarding future expenses, revenues, capital requirements and need for additional financing; |

| ● | our expectations regarding future planned expenditures; |

| ● | our ability to achieve and maintain effective internal control over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act; |

| ● | our ability to obtain, maintain and successfully enforce adequate patent and other intellectual property protection of any of our products and product candidates; |

4

| ● | our ability to protect our intellectual property, including pending and issued patents; |

| ● | our ability to operate our business without infringing the intellectual property rights of others; |

| ● | our ability to advance our clinical development programs; |

| ● | the effects of the ongoing conflict between the Ukraine and Russia and the recent and potential future bank failures or other geopolitical events; and |

| ● | statements of belief and any statement of assumptions underlying any of the foregoing. |

In some cases, you can identify these statements by terms such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “will,” “would” or the negative of those terms, and similar expressions. These forward-looking statements reflect our management’s beliefs and views with respect to future events and are based on estimates and assumptions as of the date of this Annual Report and are subject to risks and uncertainties. We discuss many of these risks in greater detail in the section entitled “Risk Factors.” Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Annual Report, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain. Given these uncertainties, you should not place undue reliance on any of the forward-looking statements included in this Annual Report. In addition, this Annual Report also contains estimates, projections and other information concerning our industry, our business, and the markets for our product candidates, as well as data regarding market research, estimates and forecasts prepared by our management. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. These statements are based upon information available to us as of the date of this Annual Report, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information.

Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, whether as a result of new information, future events, or otherwise.

This Annual Report includes trademarks and registered trademarks of Armata Pharmaceuticals, Inc. Products or service names of other companies mentioned in this Annual Report may be trademarks or registered trademarks of their respective owners.

As used in this Annual Report, unless the context requires otherwise, the “Company,” “we,” “us” and “our” refer to Armata Pharmaceuticals, Inc. and its wholly owned subsidiaries.

5

PART I

Item 1. BUSINESS

Overview

We are a clinical-stage biotechnology company focused on the development of pathogen-specific bacteriophage therapeutics for the treatment of antibiotic-resistant and difficult-to-treat bacterial infections using our proprietary bacteriophage-based technology. We see bacteriophages as an alternative to antibiotics and an essential response to growing bacterial resistance to current classes of antibiotics. Bacteriophages or “phages” have a powerful and highly differentiated mechanism of action that enables binding to and killing of targeted bacteria while preserving the human microbiome. This is in direct contrast to traditional broad-spectrum antibiotics which can alter the human microbiome increasing susceptibility to opportunistic pathogens, such as C. difficile. We believe that phages represent a promising means to effectively treat bacterial infections as an alternative to broad-spectrum antibiotics, especially for patients with bacterial infections resistant to current standard of care therapies, including the multidrug-resistant or “superbug” strains of bacteria. We are a leading developer of phage therapeutics and are uniquely positioned to address the growing worldwide threat of antibiotic-resistant bacterial infections. We are completing two critical Phase 2 trials to ensure a pathway towards pivotal Phase 3 trials.

We are combining our proprietary approach and expertise in identifying, characterizing and developing both naturally-occurring and engineered (synthetic) bacteriophages with our proprietary phage-specific host-engineered current good manufacturing practice (“cGMP”) manufacturing capabilities to advance a target pipeline of high-quality bacteriophage product candidates for advanced development. We are advancing two lead candidates to address both chronic and acute bacterial infections.

Our first lead candidate focused primarily on chronic bacterial infections is the clinical phage candidate for Pseudomonas aeruginosa (“P. aeruginosa”). On October 14, 2020, we received the approval to proceed from the U.S. Food and Drug Administration (the “FDA”) for our Investigational New Drug (“IND”) application for AP-PA02. In the first quarter of 2023, Armata announced positive topline results from the completed “SWARM-P.a.” study – a Phase 1b/2a, multicenter, double-blind, randomized, placebo-controlled, single ascending dose (“SAD”) and multiple ascending dose (“MAD”) clinical trial to evaluate the safety and tolerability of inhaled AP-PA02 in subjects with cystic fibrosis (“CF”) and chronic pulmonary P. aeruginosa infection. Data indicated that AP-PA02 was well-tolerated with a treatment emergent adverse event profile similar to placebo. Pharmacokinetcs (PK) findings confirm AP-PA02 can be effectively delivered to the lungs through nebulization with minimal systemic exposure, with single ascending doses and multiple ascending doses resulting in a proportional increase in exposure as measured in induced sputum and exposure achievement relatively consistent across patient subjects. Additionally, bacterial levels of P. aeruginosa in the sputum measured at several timepoints suggest improvement in bacterial load reduction for subjects treated with AP-PA02 at the end of treatment as compared to placebo after ten days of dosing. In addition, a correlation was seen between increasing phage dose and reduction in the bacterial load supporting the biologic plausibility of a bacterial specific mechanism of action and creating the opportunity for phage as a therapeutic alternative to inhaled antibiotics. This study was supported by the Cystic Fibrosis Foundation (“CFF”), which granted Armata a Therapeutics Development Award of $5.0 million. Following these promising Phase 1b/2a results of favorable safety and tolerability profile and plausible mechanism of action, an additional confirmatory Phase 2 trial was initiated in patients with similar chronic pulmonary infections due to Pseudomonas aeruginosa.

On February 22, 2022, Armata announced that it had received from the FDA the approval to proceed for our IND application for AP-PA02, in a second indication, non-cystic fibrosis bronchiectasis (“NCFB”). We initiated a Phase 2 trial (“Tailwind”) in NCFB in 2022 and reported first patient dosing in the first quarter of 2023. The “Tailwind” study is a Phase 2, multicenter, double-blind, randomized, placebo-controlled study to evaluate the safety, phage kinetics, and efficacy of inhaled AP-PA02 phage therapeutic in subjects with NCFB and chronic pulmonary Pseudomonas aeruginosa infection. We are actively accelerating enrollment and increasing phage dosing with the goal of defining a safe and promising biologic correlation for a Phase 3 definitive trial in 2025 which will evaluate phage as an alternative to antibiotics in chronic pulmonary infections.

6

In parallel, we have an acute bacterial infection clinical development plan focused on Staphylococcus aureus bacteremia, a difficult-to-treat and often life-threatening infection that can result in high morbidity and mortality and for which bacterial resistance to antibiotics is growing.

We are advancing a phage product candidate for Staphylococcus aureus (“S. aureus”) for the treatment of complicated S. aureus bacteremia, AP-SA02. On June 15, 2020, we entered into an agreement (the “MTEC Agreement”) with the Medical Technology Enterprise Consortium (“MTEC”), pursuant to which we expect to receive a $15.0 million grant and entered into a three-year program administered by the U.S Department of Defense (the “DoD”) through MTEC with funding from the Defense Health Agency and Joint Warfighter Medical Research Program. On September 29, 2022, the MTEC Agreement was modified to increase the total award by $1.3 million to $16.3 million and extend the term into the second half of 2024. The grant is being used to partially fund a Phase 1/2, multi-center, randomized, double-blind, placebo-controlled dose escalation study that will assess the safety, tolerability, and efficacy of our phage-based candidate, AP-SA02, for the treatment of adults with S. aureus bacteremia. On November 17, 2021, Armata announced that it had received from the FDA the approval to proceed for our IND application for AP-SA02. We are focused on accelerating enrollment of the Phase 2a segment of the “diSArm” study, evaluating safety with higher intravenous doses, which is possible due to the high purity of Armata’s phage product candidates. We are committed to developing a definitive efficacy trial in 2025 focused on phage as an alternative to broad-spectrum antibiotics and/or antibiotic sparing to decrease the utilize of broad-spectrum antibiotics and their detrimental impact on the normal human microbiome.

On August 1, 2022, Armata announced that it had received from the FDA the approval to proceed for our IND application for AP-SA02, in a second indication, prosthetic joint infections (“PJI”). We had planned to initiate a Phase 1b/2a trial in 2023, however in light of the growing concerns of both PJI and wound infections, we are revising the protocol to include both indications. Driven by data from the bacteremia study, and with sufficient funding, we may in the future initiate a Phase 1b/2a trial to assess the safety and tolerability of intravenous and intra-articular AP-SA02 as an adjunct to standard of care antibiotics in adults undergoing treatment of periprosthetic joint infections and/or wound infections caused by S. aureus.

We remain committed to conducting randomized controlled clinical trials required for FDA approval in order to move toward the commercialization of its phage products as alternatives to traditional antibiotics, providing a potential method of treating patients suffering from drug-resistant and difficult-to-treat bacterial infections.

Recent Financing

2024 Credit Agreement

On March 4, 2024, we entered into a credit and security agreement (the “2024 Credit Agreement”) for a loan in an aggregate amount of $35.0 million with Innoviva Strategic Opportunities LLC (“Innoviva SO”), a wholly owned subsidiary of Innoviva, Inc. (NASDAQ: INVA) (collectively, “Innoviva”), our principal stockholder and a related party. The 2024 loan bears interest at an annual rate of 14% and matures on June 4, 2025. Principal and accrued interest are payable at maturity. Repayment of the Loan is guaranteed by our domestic subsidiaries, and the loan is secured by substantially all of our assets. Concurrently with the execution of the 2024 loan, we amended certain provisions of the Convertible Loan and Credit Agreement to, among other things, conform certain terms relating to permitted indebtedness and permitted liens.

2023 Credit Agreement

On July 10, 2023, we entered into a credit and security agreement (the “2023 Credit Agreement”) for a loan in an aggregate amount of $25.0 million with Innoviva. This loan bears interest at an annual rate of 14% and matures on January 10, 2025. Principal and accrued interest are payable at maturity. Repayment of the loan is guaranteed by our domestic subsidiaries, and the loan is secured by substantially all of our assets.

2023 Convertible Credit Agreement

7

On January 10, 2023, we entered into a secured convertible credit and security agreement (the “Convertible Credit Agreement”) with Innoviva, which was amended in July 2023. The Convertible Credit Agreement provides for a secured term loan facility in an aggregate amount of $30.0 million, which bears interest at a rate of 8.0% per annum, and matures on January 10, 2025. Repayment of this loan is guaranteed by our domestic subsidiaries and foreign material subsidiaries, and the convertible loan is secured by substantially all of our assets and the subsidiary guarantors. The Convertible Credit Agreement provides for various conversion and repayment options, including the conversion of principal and accrued interest into the shares of common stock upon a Qualified Financing (as defined below) and we have an option to repay the loan prior to maturity.

The Convertible Credit Agreement provides that if there is a financing from new investors of at least $30.0 million (a “Qualified Financing”), the outstanding principal amount of and all accrued and unpaid interest on the Convertible Loan shall be converted into shares of common stock, at a price per share equal to a 15.0% discount to the lowest price per share for common stock paid by investors in such Qualified Financing. The Convertible Credit Agreement also required us to file a registration statement for the resale of all securities issued to the lender in connection with any conversion under the Convertible Credit Agreement, which we originally filed on February 13, 2023 and which was declared effective by the Securities and Exchange Commission (the “SEC”) on April 6, 2023. The Convertible Credit Agreement also confers upon the lender the option to convert any outstanding Convertible Loan amount, including all accrued and unpaid interest thereon, at the lender’s option, into shares of common stock at a price per share equal to the greater of book value or market value per share of common stock on the date immediately preceding the effective date of the Convertible Credit Agreement, which was $1.52 (as may be appropriately adjusted for any stock split, combination or similar act).

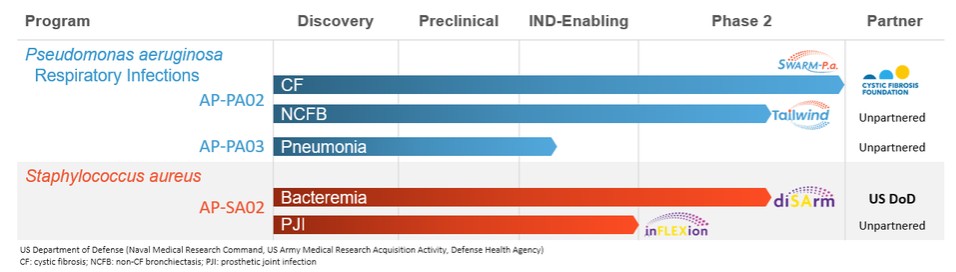

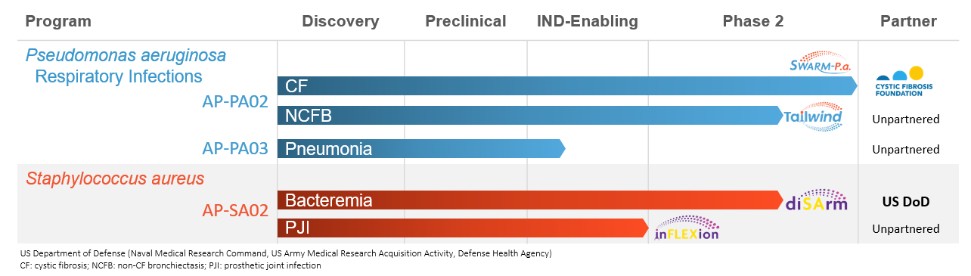

Pipeline

The following chart summarizes the status of our phage product candidate development programs and partners.

Strategy

Our strategy is to demonstrate the safety, tolerability and definitive efficacy of multiple phage products in randomized controlled clinical trials required for FDA approval and to support commercialization in both acute and chronic indications of high unmet medical need, including bacterial infections caused by multidrug-resistant and difficult-to-treat pathogens. Our fully integrated product development capabilities from bench to clinic enable the discovery of optimal phage product candidates, and include the effective adaptation of phages to uniquely engineered host cells, essential for efficient process development and resulting in improved purity, stability, and manufacturability, to power rigorous clinical trials. Our microbiological surveillance and synthetic biology capabilities drive long-term product life cycle management. We intend to:

| ● | Advance clinical trials of AP-PA02 in patients with CF and NCFB, both chronic pulmonary P. aeruginosa infections, as an alternative to inhaled antibiotics. |

8

| ● | Develop bacteriophage therapeutics, including AP-PA03, for the treatment of other antibiotic-resistant and difficult-to-treat P. aeruginosa infections such as acute bacterial pneumonia. |

| ● | Advance clinical trials of AP-SA02 in patients with bacteremia due to acute infection with S. aureus, including MRSA, as an alternative to antibiotics or to significantly limit duration of antibiotic use. |

| ● | Develop AP-SA02 for the treatment of other antibiotic-resistant and difficult-to-treat S. aureus infections such as PJI and wound infections. |

The Need for New Anti-Infective Therapies

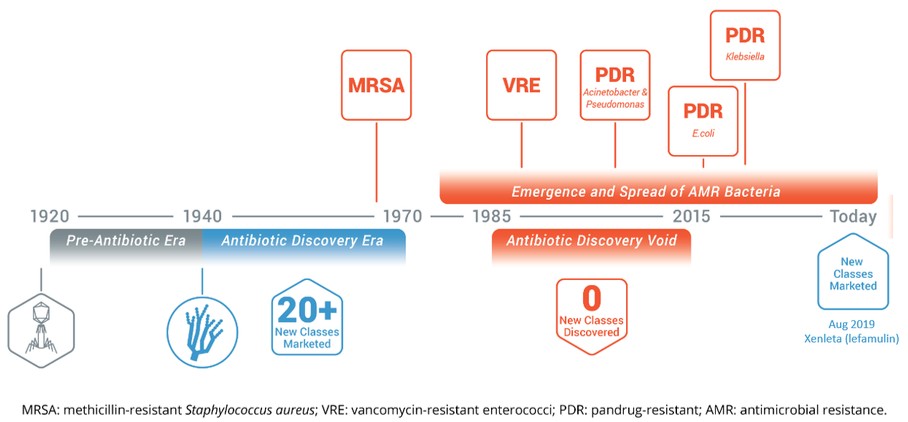

The introduction of penicillin in the early 1940s marked the start of the antibiotic discovery era, during which more than 20 new classes of antibiotic were marketed over a period of three decades. The first case of the “superbug”, Methicillin-resistant S. aureus (“MRSA”), in the United States occurred in 1968. A void in the discovery of new classes of antibiotics lasting approximately 30 years drove the emergence and spread of antibiotic-resistant bacteria, including vancomycin-resistant enterococci (“VRE”), and pandrug-resistant strains of Acinetobacter baumannii, P. aeruginosa, Escherichia coli and Klebsiella pneumoniae.

The dramatic and continuous emergence of antibiotic-resistant bacteria, and the lack of novel next generation antibiotics in the pipeline, has prompted calls to action from many of the world’s major health bodies such as the U.S. Centers for Disease Control and Prevention (the “CDC”), and the World Health Organization (the “WHO”), who warn of an “antibiotic cliff” and a “post-antibiotic era.” A growing list of infections – such as pneumonia, tuberculosis, bacteremia/septicemia, gonorrhea, and foodborne diseases – are becoming harder, and sometimes impossible, to treat as antibiotics become less effective. In 2009, the European Antimicrobial Resistance Surveillance System concluded that “the loss of effective antimicrobial therapy increasingly threatens the delivery of crucial health services in hospitals and in the community.” This conclusion was reinforced by The Antimicrobial Availability Task Force of the Infectious Diseases Society of America (the “IDSA”), and the European Centre for Disease Prevention and Control in conjunction with the European Medicines Agency (the “EMA”).

The IDSA and the WHO regard antimicrobial resistance as one of the greatest threats to human health worldwide. The Review on Antimicrobial Resistance, a global project commissioned by the British government and the Wellcome Trust, reports that at least 700,000 people die each year of drug resistance in illnesses that include bacterial infections. The report predicts that, by 2050, 10 million lives a year worldwide (more people than currently die from cancer) and a cumulative $100 trillion of economic output are at risk due to the rise of drug-resistant infections. The CDC estimates

9

that at least 2 million people in the United States develop infections due to resistant bacteria resulting in more than 23,000 deaths each year. A 2018 study from the Washington University School of Medicine indicated that the number of deaths would be between 153,113 and 162,044, which suggests that the CDC estimates may be dramatic underestimations. It is estimated that 50% of hospital-acquired infections are resistant to first-line anti-infective therapies. The cumulative annual healthcare costs for treating drug-resistant bacterial infections in the United States alone is calculated at $21 billion to $34 billion, with over 8 million additional hospital days. It is for these reasons that we believe there is a critical and pressing need to develop new and novel antibacterial therapies to combat the rise in antibiotic-resistance bacteria.

Increased public funding as well as foundation funding will be essential to bring new approaches forward through full cycle development. Definitive clinical trials to test promising novel therapeutics as alternatives to classic antibiotics must be funded in order to combat the growing issue of drug-resistant bacterial infections across the globe.

Anti-Infective Therapeutics Market

The market opportunity for antibiotics is large, with the market estimated to exceed $58 billion in annual sales globally by 2027. Almost one in every five deaths worldwide occurs as a result of infection and, according to the WHO, many bacterial infections will become difficult or impossible to cure as the efficacy of current standard-of-care antibiotics wanes. Despite the advances in antimicrobial and vaccine development, infectious diseases still remain the third-leading cause of death in the United States and the second-leading cause of death worldwide.

The number of new antibiotics approved by the FDA and other global regulatory authorities has declined consistently over the last two decades. A recent review from WHO on the number of new antibiotics currently in the pipeline shows that just 12 new antibiotics have entered the market in the five years from 2017-21, and there are fewer than 30 under development in clinical trials against pathogens considered critical by WHO such as Pseudomonas aeruginosa This is compared with more than 2,000 new product candidates in the drug pipeline for cancer. Historically, the success rate from Phase 1 to marketing approval is only one in five for infectious disease products. We, therefore, believe there is a need for new approaches to treat serious and life-threatening bacterial infections.

Hospital-acquired (nosocomial) infections are a major healthcare problem throughout the world, affecting developed countries as well as resource-poor countries. The WHO reports that hospital-acquired infections are among the major causes of death and increased morbidity among hospitalized patients. In the US alone, the CDC estimates that hospital-acquired infections account for ~1.7 million infections and 99,000 associated deaths each year.

Compounding the above situations is the alarming and continuing rise in the prevalence of multidrug-resistant bacterial infections. This, coupled with the lack of new antibiotics in current discovery and development pipelines, has generated a significant clinical management problem worldwide, leading to increases in morbidity and mortality due to these antibiotic-resistant bacteria as well as increases in healthcare costs.

Bacteriophage therapy has the potential to be an alternative to antibiotics in treating bacterial infections.

Bacteriophage Therapy

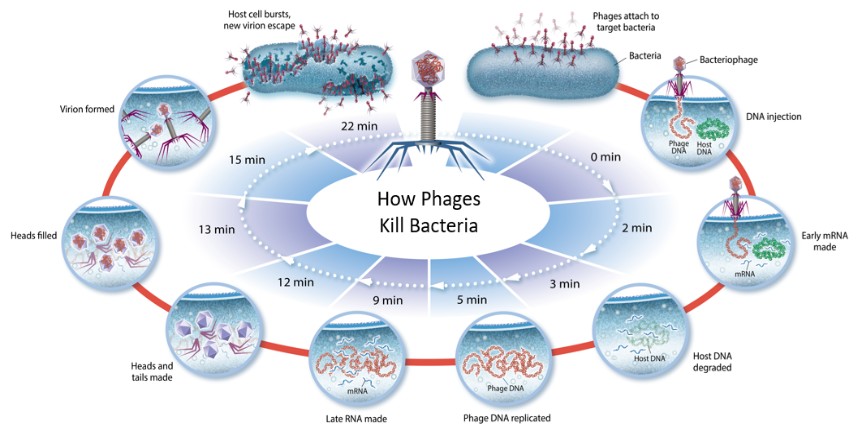

Bacteriophages, also known as phages, are ubiquitous viruses, found wherever bacteria exist. It is estimated there are more bacteriophages than every other organism on Earth combined. Phages are natural predators of bacteria, and the name “bacteriophage” translates as “eaters of bacteria”. Phages infect and rapidly kill the bacterial host by multiplying inside and then bursting through the cell membrane in order to release the next generation of phages into the surrounding environment, ready to infect and kill additional nearby target bacterial cells until the bacteria have been eliminated. When there are no target bacteria left for the phages to infect, the phages are removed through the body’s natural clearance processes. In contrast to broad-spectrum antibiotics, phages are highly targeted to specific bacteria, and do not attack the normal human microbiome on the skin, the gut or other areas critical to maintaining our defenses against more opportunistic infections like C. difficile.

10

Phages have the potential to provide both an alternative to, and/or a synergistic approach with, antibiotic therapy. Phages offer several differentiating attributes compared to classic antibiotics:

| ● | Highly specific/selective bactericidal agents, sparing the microbiome. Since each strain of phage specifically binds and kills only a particular bacterial host, phages may be a precision tool to reduce or eliminate specific strains of harmful bacteria without exposing patients to risks of eliminating the beneficial bacteria of our microbiomes through the use of current standard of care antibiotics. Such risks could include serious opportunistic infections such as Clostridium difficile infection and VRE infection. |

| ● | No known toxicities associated with chemical structures. Antibiotic use is often associated with toxicities (e.g. kidneys, bone marrow, hearing). Phages are highly unlikely to carry structural features or be metabolized by the body to produce structural elements that confer chemical toxicities associated with small molecules. |

| ● | Distinct mechanism of bactericidal action. Since phages use different mechanisms of action, their activity is independent of antibiotic resistance and as such could provide much needed therapy for multi-drug resistant infections. |

| ● | Replication competent. It is possible that phage replication at the site of infection facilitates effective dosing. |

| ● | High potential for added functionality through genetic engineering. Phage genomes can be modified to confer benefits that address limitations, if any, that are observed during clinical development. Traits such as host range, burst size and biofilm disruption can be improved. These potential improvements help to assure phage therapeutics efficacy in difficult settings and over time as new isolates emerge. |

Phages were discovered in 1915 at the Pasteur Institute and were shown to kill bacteria taken from patients suffering from dysentery. Furthermore, it was noted that phage numbers rose as patients recovered from infection, suggesting a direct association. Throughout the pre-antibiotic era, phages were widely used as an effective therapeutic agent to combat a variety of bacterial infections. However, phage use was displaced by the common use of broad-spectrum antibiotics in the early 1940s, with antibiotics being seen for many years as the superior treatment to combat bacterial disease, particularly in Western medicine. This attitude persisted until the development of the wide-ranging, and in some cases total, resistance to antibiotics seen within the last 10 years. We believe that the continuing emergence of antibiotic-resistant bacteria provides the opportunity to revitalize phage use.

11

There are hundreds of cases published in the scientific and medical literature describing the use of phage therapy in human medicine over more than 90 years, mostly in the former Soviet Union and Eastern Europe. Phage therapy is still commonly used today in Russia, Poland and Georgia, with numerous reports of success in treating serious infectious diseases caused by many pathogenic bacterial species. However, the safety and effectiveness of these therapies have not been conclusively established due to the lack of randomized controlled clinical studies.

Recently, Western medicine has seen a rise in the clinical evaluation of phages. In the United Kingdom, two early-stage clinical trials of P. aeruginosa phage cocktails showed no adverse effects in patients. One study (Phase 1/2a) demonstrated efficacy in a small trial of 12 patients with chronic multidrug-resistant P. aeruginosa otitis treated with a cocktail of six natural phages. Since 2016, there have been a number of “compassionate use” cases in which patients suffering from various serious or life-threatening infections have been treated with phage therapy under physician-sponsored Emergency Investigational New Drug Applications with high rates of success and no adverse effects attributable to the therapy. Most notable was the well-documented case in 2016 of Tom Patterson, whose disseminated multidrug-resistant Acinetobacter baumannii infection was successfully treated with phage-based therapeutic cocktails administered intravenously and intraperitoneally. An 82-year-old male with an aortic graft (heart implant) infected with pandrug-resistant P. aeruginosa was successfully treated with a single application of phage, marking Yale University’s first case using phage therapy under Emergency IND. By early 2019, Yale University had treated more than half-a-dozen compassionate use cases, the majority individuals with CF with antibiotic-resistant lung infection. In 2018, a 15-year-old CF patient with a disseminated Mycobacterium abscessus lung infection was treated intravenously with a three-phage cocktail following lung transplantation. That patient’s case represents another milestone for phage therapy – the first person to be treated with genetically modified phages.

A consistent takeaway from these early phage therapy uses, and from the more recent clinical trials and compassionate use cases, is that phage therapy is generally well tolerated, with generally no reports of serious adverse events when administered by inhalation. Intravenous use of phage has been more limited due to bacterial cell wall and other contaminants in the final phage product. Phages have previously received approvals for use in cleaning food facilities and as a food additive for human consumption by the FDA and the EMA, and as agricultural bacterial pest treatments by the United States Department of Agriculture. Phages have met the criteria to be considered as “generally recognized as safe”, or “GRAS”, in the food and food contact surface categories.

With the growing problem of antimicrobial resistance, we believe it is essential that phage safety and efficacy be demonstrated by conducting rigorous well-powered clinical trials required for FDA approval, in order to move toward commercialization of phage therapy as an alternative to traditional antibiotics and to bring a potential solution to all patients suffering from drug-resistant bacterial infections. Armata has been focused on enhancing the overall quality of its manufactured phages through engineering and adaptation to maximize production titers while ensuring high level of purity.

Target Markets and Medical Need

Pulmonary Bacterial Infections

P. aeruginosa is consistently recognized by the CDC, and other public health agencies, as among the most dangerous and difficult-to-treat pathogens associated with significant impacts on health, quality of life, and economic burden. Regular standard-of-care antibiotics treatments often fail to completely eradicate the pathogen, and the problem is further complicated by rising rates of antibiotic resistance due to a growing number of multidrug-resistant isolates emerging, particularly with long term use. P. aeruginosa is particularly problematic for CF patients given that their already compromised immune system leads to chronic infections. In addition to CF lung infections, P. aeruginosa is responsible for other respiratory infections with high unmet medical need, including NCFB and hospitalized pneumonia.

P. aeruginosa Infection is a Major Cause of Morbidity and Mortality in Cystic Fibrosis

CF is a genetic disease caused by mutations in the CF transmembrane conductance regulator (“CFTR”) gene. CF affects over 40,000 people in the United States (105,000 people worldwide) with approximately 1,000 new diagnoses per year. Dysfunction of the CFTR gene leads to dysfunction in multiple organs, but particularly the lungs, where a

12

failure of hydration of airway secretions results in thick mucus, chronic inflammation, airway remodeling, and recurrent infections. Lung function continues to decline over time, punctuated by pulmonary exacerbations with increased cough, shortness of breath, and infections that result in rapid declines in lung function. For these reasons, CF remains the most common fatal hereditary lung disease.

Outcomes for people with CF have improved significantly in recent years through early screening, the development and use of CFTR modulators, and other therapies. However, people with CF still suffer significant morbidity and mortality due to pulmonary infection with P. aeruginosa. Chronic P. aeruginosa infections occur in 45% of CF patients by age 40, and are strongly associated with worsening lung function, frequent pulmonary exacerbations, and increased mortality. In 2022, the median predicted survival age was 68 years. Although many patients with chronic P. aeruginosa benefit from routine suppressive inhaled antibiotic therapy, large numbers of CF patients still experience clinical deterioration despite these treatments, hence the need for more effective therapies, ideally with a different mechanism of action compared to traditional antibiotics, for the treatment of chronic P. aeruginosa infection. GlobalData projects that total antibiotic sales in the CF market will exceed $900 million in the United States in 2030.

Non-Cystic Fibrosis Bronchiectasis

NCFB is a chronic respiratory disease affecting more than 100,000 people in the United States and 200,000 people in Europe, characterized by recurrent respiratory infections that lead to a vicious cycle of impaired mucociliary clearance, chronic infection, bronchial inflammation, and progressive lung function loss. P. aeruginosa is the most prevalent pathogen responsible for these recurrent infections. It is found in approximately 30% of cases and is associated with enhanced disease progression, including poorer lung function and lower quality of life, more frequent exacerbations, 7-fold increase in hospitalizations, and 3-fold increase in death. NCFB patients frequently become chronically colonized with multidrug-resistant strains of P. aeruginosa because of the need for repeated courses of antibiotic treatment. There are currently no approved inhaled antibiotics for the treatment of NCFB patients with chronic P. aeruginosa respiratory infections.

Hospitalized Pneumonia

Hospital-acquired pneumonia and ventilated-associated pneumonia is one of the most common causes of death among all hospital‐acquired infections, with approximately 300,000 hospitalizations each year in the United States due to Pseudomonas. Infection with Pseudomonas results in mortality rates ranging as high as 35‐50%, drives considerable healthcare costs (in excess of $40,000 per patient), and accounts for around 50% of all intensive care unit antibiotics.

Staphylococcus aureus Infections

Bacteremia

Bacteremia is a bacterial infection of the bloodstream. A common diagnosis, the CDC estimates that up to 1.7 million people in the U.S. develop bacteremia each year. S. aureus is the most commonly identified pathogen in both hospital- and community-acquired bloodstream infections. Annually in the U.S. there are approximately 200,000 hospitalizations for S. aureus bacteremia (“SAB”). Despite conventional antibiotics, mortality in SAB results in the death of up to 40% of all cases and 57% of patients over the age of 85. Patients with comorbidities such as alcoholism, malignancy, diabetes, end-stage renal disease requiring hemodialysis, and immunosuppression are at even higher risk for death when SAB develops. Age-adjusted mortality assessments show that SAB mortality is higher than that of AIDS, tuberculosis, or viral hepatitis, and comparable to mortality rates for breast or prostate cancer. Outcomes are even poorer for SAB due to methicillin-resistant S. aureus (“MRSA”), classified as a serious threat to global health by the CDC and a high priority threat by the WHO, with higher rates of complications and increased mortality as compared to methicillin-susceptible S. aureus (“MSSA”). Average hospital costs to patients with nosocomial SAB ranges between $40,000 (MSSA) and $114,000 (MRSA). Treatment failures are common in SAB, with highest rates due to MRSA. These failures can be attributed in part to poor penetration of some tissues by antibiotics, slow onset of bactericidal effects, emerging resistance patterns, and biofilm formation. While biofilms can render traditional antibiotics ineffective, phages may have the ability to penetrate the biofilm allowing rapid and efficient infection of the host and amplification at the site of infection. Daptomycin (approved in 2005; based on clinical cure rates of less than 50%) and vancomycin are the

13

only two antibiotics with label indications in the U.S. for the treatment of SAB, and the emergence of drug-resistant S. aureus isolates, including to these two standard of care drugs, represents a major threat in terms of increasing morbidity, mortality and health care utilization.

Prosthetic Joint Infection and Wound Infection

The total number of prosthetic joint infection (“PJI”)-related revision surgeries is expected to more than double from 70,000 in 2020 to 144,000 in 2040 in the United States and European Union Five (France, Germany, Italy, Spain, and the United Kingdom), at an annual growth rate of 5.6% due to a growing elderly population. The United States is the largest market for PJI, accounting for 61% of PJI-related revision surgery in 2020 (estimated to be 71% by 2040), each estimated to cost $150,000. S. aureus PJI infections are among the most commonly observed, accounting for up to 47% of all infections. PJI caused by biofilm-forming bacteria, such as S. aureus, is challenging to treat and requires both surgery and long-term antibiotic use. Lack of efficacy against biofilms is a common cause of re-infection or treatment failure in PJI. Moreover, growing antibiotic resistance complicates treatment strategies and antibiotic choice for the treatment of PJI. Phage therapy has been successful in patients who have failed conventional antibiotic treatment, including two 2020 case studies in which phages were administered by intravenous or intraarticular routes and shown to be generally well tolerated. Similarly, secondary and tertiary wound infections due to S. aureus are a growing issue worldwide.

Platform Technologies

Synthetic Phage Platform

Phages, natural predators of bacteria, have been in an uninterrupted battle for millions of years – evolving to kill or evade. These powerful natural well-adapted phages can be purposely engineered to be more efficient killers. The use of synthetic biology tools enables us to precisely engineer natural phages in ways that further improve their pharmacological properties and antimicrobial activity. Attributes of engineered phages can include expanded host range, improved potency which is a fundamental drug property that can translate into improved clinical efficacy, and importantly, biofilm disruption, which is a critical aspect of serious infections that needs to be addressed.

| Phage Discovery and Phenotyping: Development of synthetic phage products that target a specific pathogen begins with the isolation of powerful natural phages from environmental and clinical samples. Our large library of multidrug-resistant pathogens and microbiome targets aids in the identification of the optimal phage candidates for downstream engineering. | ||

| Bioinformatics Powers Engineering: We employ next-generation sequencing, proprietary sequencing databases and software, bioinformatics, and comparative genomics, for the analyses of our phages. | ||

| Engineering Host and Phage to Confer Desirable Properties: Depending on the target pathogen, identified natural phages are engineered to enable desirable phenotypes such as wide host range, payload expression, biofilm degradation, resistance prevention, and bioactive peptide display. Engineered phages are evaluated both in vitro and in vivo to determine pharmacological and toxicological parameters to confirm their potential in the clinic. | ||

| Formulation Development and Chemistry, Manufacturing, and Controls: We have developed and acquired highly skilled process development and phage manufacturing expertise to manage our proprietary platforms with proven capabilities from the bench to clinic. Our research and development facilities are equipped with cGMP compliant manufacturing suites enabling the production, | ||

14

purification, testing and release of reproducible batches of phage clinical trial material exhibiting high purity and high titer designed to be tolerated for both intravenous and inhaled administration. | |||

Preclinical and Clinical Development Programs

Overview

We are committed to developing novel phage therapies, with drug development expertise and product development capabilities that span bench to clinic, including in-house phage-specific cGMP manufacturing. Our phage discovery platform in which we screen panels of clinically-relevant isolates against our extensive phage library utilizing proprietary methods that identify phage combinations with superior attributes, together with our phage-specific cGMP compliant manufacturing facilities, uniquely enables us to efficiently identify optimal product candidates. Our microbiological surveillance and synthetic biology capabilities drive long-term product life cycle management.

Our therapeutic phage candidates aim to address areas of significant unmet medical need, by targeting key drug-resistant bacteria, including those on the WHO’s global priority pathogens list, and the priority pathogens list issued by the CDC. The long-term potential for phage therapy is broad reaching, including potential use as front-line therapy. However, first indications will be as adjunct therapy in indications with high unmet need, which demands careful patient population selection to assure that a treatment effect with the phage cocktail can be observed over and above the efficacy of standard-of-care antibiotics.

We are developing and advancing a broad pipeline of natural and synthetic phage candidates, including clinical candidates for P. aeruginosa and S. aureus, two bacterial pathogens known to have significant morbidity and mortality despite standard-of-care antibiotic usage. P. aeruginosa and S. aureus are causative agents for difficult-to-treat infections: P. aeruginosa, with its mucoid and multidrug-resistant strains, is a dominant culprit in chronic respiratory infections in CF and NCFB patients as well as acute pneumonia in hospitalized patients; S. aureus, with its heteroresistant and MRSA strains, has been implicated in systemic (e.g., bacteremia) as well as prosthetic-related and wound infections. By advancing randomized controlled clinical trials using P. aeruginosa and S. aureus natural phage cocktails, Armata will gain experience treating site-specific as well as systemic infections.

Pseudomonas aeruginosa Phage Product Candidate, AP-PA02

Historical Background

AP-PA02 was developed as a next-generation replacement for AP-PA01 (previously known as AB-PA01). A total of 10 patients with serious or life-threatening P. aeruginosa infections not responding to antibiotic therapy were treated with AP-PA01, along with antibiotics, under single-patient expanded access programs in the United States (authorized under Emergency INDs by the FDA) and in Australia (authorized under the Special Access Scheme by the Australian Therapeutic Goods Administration). The treated patients’ infections included bacteremia, native and prosthetic valve endocarditis, recurrent pneumonia (CF, post-transplant), ventilated-associated pneumonia, prosthetic joint infection, ventricular assist device infection, and septicemia due to burns. Investigators concluded that intravenous and nebulized administration of AP-PA01 was well-tolerated with no treatment-related serious adverse events. One of these cases was published in August 2019, in the peer-reviewed journal Infection, after AP-PA01 was used to successfully treat a CF patient who had developed a multidrug-resistant P. aeruginosa infection. Another success with AP-PA01, used to treat a 77-year-old with ventilated-associated pneumonia and empyema, was published in November 2019, in the American Journal of Respiratory and Critical Care Medicine. We no longer offer AP-PA01 through any expanded access program.

In August 2018, we held a Type B pre-IND meeting with the U.S. FDA regarding a proposed Phase 1/2 clinical study of AP-PA01 for the treatment of P. aeruginosa respiratory infections (ventilated-associated pneumonia). Feedback from the FDA in September 2018 included: agreement on product specifications, manufacturing and analytical plan, and a stability program. Furthermore, the FDA noted that preclinical toxicology studies are not required for AP-PA01 to enter clinical development.

15

Human exposure through treatment of single patients with AP-PA01 under the expanded access program has been helpful in demonstrating the promise and safety of phage therapy. Feedback from the pre-IND meeting has been insightful for the regulatory path required for phage therapeutics in general, and specifically for a phage product candidate intended for respiratory infection. We, therefore, have leveraged our experiences with AP-PA01 to derive a development plan for the next-generation product candidate, AP-PA02.

Preclinical Development of AP-PA02

AP-PA02 is one example of the novel candidates to emerge from our robust research and development capabilities, and significantly improves upon our original P. aeruginosa phage product candidate, AP-PA01. The phages that comprise AP-PA02 were selected with desired attributes for a product candidate targeting P. aeruginosa lung infections. Different methods were deployed, including microbiological, bioinformatics and comparative genomics, in order to identify optimal attributes for the product candidate. Susceptibility, killing kinetics, and biofilm eradication, was assessed using P. aeruginosa isolates from CF patients to determine antimicrobial activity and potency of AP-PA02. Viability in relevant biological fluids, and compatibility with current standard of care therapies for CF patients, was verified to confirm suitability of AP-PA02 for clinical use in this patient population. Immune stimulation was assessed to assure the lack of inflammatory impact by AP-PA02. Animal studies were conducted to provide insight into safe and efficacious dose levels that would support the expectation of pharmacological activity (i.e., antimicrobial potential of phage) in the lung compartment following an inhaled route of administration. In parallel, we initiated manufacturing feasibility and process optimization efforts with the goal of achieving high-quality phage product free of endotoxin and host cell proteins whilst maintaining adequate phage titers.

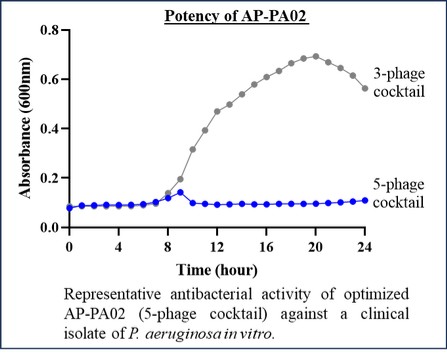

AP-PA02 is comprised of a cocktail of adapted natural P. aeruginosa phages originating from distinct families and subfamilies, targeting multiple receptor classes, functioning with compatibility (i.e., the phages don’t interfere with one another) and cooperativity (i.e., the phages work together for a better outcome), and further characterized by being highly potent and having a broad host range and overlap. Prior to initiating the SWARM-P.a. trial (described below), our clinical isolate screening and phage collections yielded a three-phage AP-PA02 cocktail with compelling host-range coverage. We subsequently modified AP-PA02 to include additional phage genera that increase potency and broaden coverage of strains of P. aeruginosa found in CF patients. The optimized five-phage AP-PA02 cocktail provided coverage against at least 90% of tested CF clinical isolates and has shown superior in vitro potency as well as improved efficacy in an animal model of infection. The improvements in AP-PA02 reflect our core strategy of utilizing clinical isolate surveillance data to drive enhancement of product composition.

Preclinical highlights of AP-PA02 include:

| ● | Significantly reduced P. aeruginosa biofilm mass in vitro; |

16

| ● | Persistence of active phage particles in the lung; |

| ● | Limited systemic and off-target organ distribution; |

| ● | Significantly decreased mortality in a murine model of acute P. aeruginosa lung infection; |

| ● | Components are stable in blood and sputum; |

| ● | Not antagonistic with tobramycin nor aztreonam; and |

| ● | Components maintain activity in the presence of other CF therapies. |

We developed AP-PA02 as a sterile liquid formulation, suitable for delivery by inhalation. Clinical trial material of AP-PA02 is currently manufactured under cGMP at our production facility in Marina del Rey, California.

Clinical Development of AP-PA02 in Cystic Fibrosis: Completed Phase 1b/2a Study

On October 14, 2020, Armata received approval for the study to proceed from the FDA for its IND to initiate the “SWARM-P.a.” study – a Phase 1b/2a, multicenter, double-blind, randomized, placebo-controlled, single ascending dose (“SAD”) and multiple ascending dose (“MAD”) clinical trial to evaluate the safety, tolerability and phage recovery profile of AP-PA02 administered by inhalation in subjects with cystic fibrosis and chronic pulmonary Pseudomonas aeruginosa infection. Primary Endpoints (SAD and MAD) included incidence and severity of treatment-emergent, adverse events. Secondary Endpoints (MAD) included changes in P. aeruginosa colony-forming units. We looked at clinical parameters as a part of exploratory endpoints for the SAD and MAD cohorts. The SWARM-P.a. study was supported by a $5 million Therapeutics Development Award from the CFF.

In the first quarter of 2023, Armata announced positive topline results from the completed “SWARM-P.a.” study. Data indicate that AP-PA02 was well-tolerated with a treatment emergent adverse event profile similar to placebo. Pharmacokinetcs (PK) findings confirm that AP-PA02 can be effectively delivered to the lungs through nebulization with minimal systemic exposure, with single ascending doses and multiple ascending doses resulting in a proportional increase in exposure as measured in induced sputum and exposure achievement relatively consistent across patient subjects. Additionally, bacterial levels of P. aeruginosa in the sputum measured at several timepoints suggest improvement in bacterial load reduction for subjects treated with AP-PA02 at the end of treatment as compared to placebo after ten days of dosing.

Additive Clinical Indication for Our AP-PA02 P. aeruginosa Phage Product Candidate: Ensuring Patient Population for Definitive Phase 3 Trial

With positive outcomes from the first clinical study, SWARM-P.a., we initiated a follow-on Phase 2 study investigating the efficacy of AP-PA02 in NCFB patients chronically infected with P. aeruginosa. Screening P. aeruginosa isolates from people diagnosed with NCFB revealed that the five-phage AP-PA02 cocktail offers broad coverage and robust potency in this indication as well. On February 22, 2022, Armata announced that it had received from the FDA the approval to proceed for our IND application for AP-PA02, in a second indication, NCFB. The Company initiated a Phase 2 trial (“Tailwind”) in NCFB in late 2022 and reported first patient dosing in the first quarter of 2023. The “Tailwind” study is a Phase 2, multicenter, double-blind, randomized, placebo-controlled study to evaluate the safety, phage kinetics, and efficacy of inhaled AP-PA02 phage therapeutic in subjects with NCFB and chronic pulmonary Pseudomonas aeruginosa infection. Throughout 2023, the Company worked closely with clinical sites to rapidly expand enrollment to position the Phase 2 trial for completion in 2024 and have data available to support a pivotal trial in 2025. Enrollment of the Phase 2 trial is ongoing, with AP-PA02 continuing to demonstrate a favorable safety and tolerability profile, and insights from blinded data of the relationship between phage dose and microbiological impact on P. aeruginosa confirms the findings in the cystic fibrosis SWARM-P.a. Phase 2a trial. We are carefully evaluating the impact of AP-PA02 on P. aeruginosa in patients not taking antibiotics in order to confirm the independent impact of phage treatment.

17

AP-PA03 for Antibiotic-Resistant and Difficult-to-Treat Acute Bacterial Pneumonia

Conversely and representing the different physiology of acute pneumonia lung infections as compared to chronic CF and NCFB respiratory infections, a novel cocktail is in development for the clinical indication of acute hospitalized pneumonia. We have deployed our extensive P. aeruginosa clinical isolate collection and phage library to identify a candidate phage cocktail, AP-PA03.

Staphylococcus aureus Phage Product Candidate, AP-SA02

Historical Background

AP-SA02 was developed as a more advanced version of AP-SA01 (previously known as AB-SA01).

The therapeutic potential of AP-SA01 has been demonstrated through:

| ● | Efficacy in murine methicillin-resistant and methicillin-susceptible S. aureus pneumonia models, and sheep sinus biofilm model. |

| ● | Demonstration of safety and tolerability in two completed investigator-initiated Phase 1 studies (topical administration: intact skin of healthy adults; intrasinal administration: patients suffering from S. aureus-derived chronic rhinosinusitis). |

| ● | AP-SA01 was provided for use under single-patient expanded access programs in the United States (Emergency INDs, per the Food and Drug Administration) or Australia (Special Access Scheme, per the Australian Therapeutic Goods Administration). A total of 18 patients with serious or life-threatening S. aureus infections (including bacteremia, endocarditis, ventricular-assist device infection, prosthetic joint infection) not responding to standard-of-care antibiotic therapy were treated with AP-SA01. AP-SA01 was administered intravenously, with most patients treated for 14 days, every 12 hours as an adjunct to antibiotic therapy. Investigators concluded that intravenous administration of AP-SA01 was well-tolerated with no treatment-related serious adverse events. We no longer offer AP-SA01 through any expanded access program. |

Human exposure through treatment of single patients with AP-SA01 under the expanded access program has been helpful in demonstrating the promise of phage therapy and warrants further study to support safety and efficacy through randomized controlled trials required to support registration. Feedback from a Type B pre-IND meeting with the FDA in August 2018 has been insightful for the regulatory path required for phage therapeutics in general, and specifically for a phage product candidate intended for systemic delivery. We therefore have leveraged our experiences with AP-SA01 to derive a development plan for AP-SA02.

Product Optimization: Development of AP-SA02

AP-SA02 is a novel biologic product candidate comprised of a cocktail of adapted natural lytic phages that target the problematic pathogen, S. aureus.

Preclinical highlights of AP-SA02 include:

| ● | Potent antimicrobial activity against approximately 95% of S. aureus clinical isolates tested, including drug-resistant isolates (MRSA: methicillin-resistant S. aureus and VRSA: vancomycin-resistant S. aureus); |

| ● | Unique mechanism of action offers independent or synergistic benefit with standard of care antibiotics; |

| ● | Component phages are stable and retain infectivity after exposure to relevant biological fluids; and |

18

| ● | Penetrates pre-existing S. aureus biofilms. |

We have developed AP-SA02 as a sterile solution, suitable for delivery by intravenous administration. Clinical trial material of AP-SA02 is currently manufactured under cGMP at our production facility in Marina del Rey, California to support the required regulatory filing(s) for clinical entry in the United States and ex-U.S.

Clinical Development of AP-SA02 in Bacteremia

On November 17, 2021, Armata received approval for the study to proceed from the FDA for its IND to initiate the “diSArm” study – a Phase 1b/2a, randomized, double‐blind, placebo‐controlled, multiple ascending dose escalation study of the safety, tolerability, and efficacy of intravenous AP‐SA02 as an adjunct to best available antibiotic therapy compared to best available antibiotic therapy alone for the treatment of adults with bacteremia due to Staphylococcus aureus. The objectives of this study are to: (i) demonstrate safety and tolerability of multiple different dose levels of AP-SA02; (ii) evaluate optimal dosing through safety, pharmacokinetics and microbial efficacy; and (iii) explore efficacy through evaluation of key meaningful endpoints. The study is being conducted at sites in the United States and also at sites abroad in Australia.

The Phase 1b/2a study is partially funded by a $15.0 million award from the DoD through MTEC with funding from the Defense Health Agency and Joint Warfighter Medical Research Program. On September 29, 2022, the MTEC Agreement was modified to increase the total award by $1.3 million to $16.3 million and extend the term into the second half of 2024.

Data from this Phase 1b/2a study will be invaluable for a follow-on trial that is being designed to demonstrate efficacy of AP-SA02 in treating S. aureus bacteremia. We anticipate findings from the Phase 1b/2a study will provide the basis for constructing a robust trial strategy for registration which can be the basis for an End-of-Phase-2 meeting with the FDA that enables us to obtain agreement on a path to approval in late 2024, early 2025.

Additional Clinical Indications for AP-SA02

Improved patient outcomes are needed for other Staphylococcal infections, in settings such as PJI and wound infections, for which antimicrobial resistance is a growing concern. We believe AP-SA02 could also have a meaningful impact in these indications, particularly infections caused by methicillin-resistant S. aureus (“MRSA”). On August 1, 2022, we announced that we had received from the FDA the approval to proceed for our IND application for AP-SA02, in a second indication, PJI. We had planned to initiate a Phase 1b/2a trial in 2023; however, in light of the growing concerns of both PJI and wound infection, we are revising the protocol to include both indications, which will assess the safety and tolerability of intravenous and intra-articular AP-SA02 as an adjunct to standard of care antibiotics in adults undergoing debridement, antibiotics, and implant retention for the treatment of periprosthetic joint infections and/or wound infections caused by S. aureus.

Discovery Research

In addition to developing our more advanced pipeline programs described above, we continue phage discovery efforts by screening other interesting bacterial targets against our phage library in order to further expand our pipeline. Klebsiella pneumoniae phage, for example, is a potentially important addition to treatment options for serious lung infections.

Furthermore, our team of microbiologists and synthetic biologists hunt for natural phages and evaluate the suitability of these natural phages for engineering and adaptation using our synthetic phage platform. These powerful natural well-adapted phages can be purposely engineered to be more efficient killers. The use of synthetic biology tools enables us to precisely engineer natural phages in ways that further improve their pharmacological properties and antimicrobial activity. Attributes of engineered phages can include expanded host range, improved potency which is a

19

fundamental drug property that can translate into improved clinical efficacy, and importantly, biofilm disruption, which is a critical aspect of serious infections that needs to be addressed.

Manufacturing

We currently produce clinical quantities of each of our bacteriophage product candidates at our cGMP-compliant manufacturing facility in Marina del Rey, California. This facility has approximately 35,500 square feet of laboratory and office space, including 3,000 square feet of cGMP laboratory space, designed to produce clinical quantities of each of our product candidates and to perform in-house Quality Control (“QC”) testing. We operate in-house process development activities through to the production, purification, formulation, and release of our therapeutic phage cocktails for use in human clinical trials. Our facility is licensed by the California Department of Public Health for drug manufacturing and is subject to periodic, unannounced inspections for compliance with cGMP and other state and federal laws and regulations. The facility is subject to periodic inspections by the City of Los Angeles and Los Angeles County for fire hazard and waste management and is in compliance with all applicable regulations. Our facility is staffed with an independent Quality Unit and Manufacturing and Facilities personnel trained under cGMPs.

Our current formulations for our P. aeruginosa and S. aureus phage product candidates are intended for inhaled and intravenous delivery, both requiring our drug products to be sterile. Our Marina del Rey facility is capable of manufacturing sterile drug products, utilizing ISO-certified cleanrooms and ISO 5-certified biological safety cabinets. The facility also houses an ISO 5-certified closed system isolator. We may further optimize future formulations of our product candidates which may or may not require assurance of sterility.

For our manufacturing facility we have been able to access and hire highly skilled process development and phage manufacturing expertise and believe that we have control of our proprietary platform from phage identification through final product fill and finish and release. Manufacturing campaigns are managed by a specialist team of our internal staff, which is designed to promote compliance with the technical aspects and regulatory requirements of the manufacturing process. We have developed a cGMP-compliant manufacturing process that utilizes both industry standard and proprietary methods for the manufacture of our product candidates. Our process is designed to be scalable to meet our clinical study needs, and to fulfill the requirements of regulators for human studies.

Although our facility is capable of manufacturing our phage product candidates, we rely on, and may continue to rely on, third-party contract manufacturers for the manufacture of certain raw materials, components, or packaging of the product candidates that may be developed for clinical testing, as well as for commercialization. We are constructing the new manufacturing facility in Los Angeles, California and plan to move manufacturing processes to this new facility in the second half of 2024.

Intellectual Property

General

Our goal is to protect the proprietary technology that we believe is important to our business, including to obtain, maintain and enforce patent protection for our product candidates, formulations, processes, methods and any other proprietary technologies, preserve our trade secrets and operate without infringing on the proprietary rights of other parties, both in the United States and in other countries. Our policy is to actively seek to obtain, where appropriate, the broadest intellectual property protection possible for our current product candidates and any future product candidates, proprietary information and proprietary technology through a combination of contractual arrangements and patents, both in the United States and abroad. However, patent protection may not afford us with complete protection against competitors who seek to circumvent our patents.

We also rely on trademarks, trade secrets, know-how, continuing technological innovation and in-licensing opportunities to develop and maintain our proprietary position. We also depend upon the skills, knowledge, experience and know-how of our management and research and development personnel, as well as that of our advisors, consultants and other contractors. To help protect our proprietary processes and know-how, which is not patentable, and for inventions for which patents may be difficult to enforce, we currently and will in the future rely on trade secret

20

protection and contractual obligations with third parties to protect our interests and to develop and maintain our competitive position. To this end, we require all of our employees, consultants, advisors and other contractors to enter into agreements with contractual obligations that prohibit the disclosure of confidential information and, where applicable, require disclosure and assignment to us of the ideas, developments, discoveries and inventions important to our business.

Our success in preserving market exclusivity for our product candidates relies on patent protection, including extensions to this where appropriate, and on data exclusivity relating to an approved biologic. This may be extended by orphan drug and/or pediatric use protection where appropriate. Once any regulatory period of data exclusivity expires, depending on the status of our patent coverage, we may not be able to prevent others from marketing and selling biosimilar versions of our product candidates. We are also dependent upon the diligence of our appointed agents in national jurisdictions, acting for and on our behalf, which manage the prosecution of pending domestic and foreign patent applications and maintain granted domestic and foreign patents.

Because patent applications in the United States and certain other jurisdictions are maintained in secrecy for 18 months or potentially even longer, and because publication of discoveries in the scientific or patent literature often lags behind actual discoveries and patent application filings, we cannot be certain of the priority of inventions covered by pending patent applications. Accordingly, we may not have been the first to invent the subject matter disclosed in some of our patent applications or the first to file patent applications covering such subject matter, and we may have to participate in interference proceedings or derivation proceedings declared by the United States Patent and Trademark Office (the “USPTO”) to determine priority of invention.

Bacteriophage Patent Portfolio

As of December 31, 2023, we owned or had exclusive license rights to a total of 151 patents and applications: 13 U.S. patents, 10 U.S. patent applications, 73 foreign patents, and 55 foreign patent applications, with nominal expiration on various dates between 2024 and 2044. Patent term adjustments or patent term extensions could result in later expiration dates. We believe these patents and applications cover our lead phage therapeutic programs and use thereof, synthetic phage and methods of manufacture thereof, beneficial effects of bacteriophage treatment - including treatment and prevention of bacteria-associated cancers, bacteriophage combinations, the sequential use of bacteriophages in combination with conventional antibiotics, genetic sequence variations, methods to reduce antibiotic resistance, methods to treat bacterial biofilms, methods to design therapeutic combination panels of bacteriophage, disinfection methods using bacteriophages, and bacteriophage mutants having increased bacterial host spectra.

Competition

The development and commercialization of new drugs is highly competitive. We face competition from many different sources, including commercial pharmaceutical and biotechnology enterprises, academic institutions, government agencies and private and public research institutions all seeking to develop novel treatment modalities for bacterial infections. Many of our competitors have significantly greater financial, product development, manufacturing and marketing resources than us. Large pharmaceutical companies have extensive experience in clinical development and obtaining regulatory approval for drug products. In addition, many universities and private and public research institutes are active in antibacterial research, some in direct competition with us. We also may compete with these organizations to recruit scientists and clinical development personnel.

Our ability to compete successfully will depend largely on our ability to leverage our collective experience in drug discovery, development and commercialization to:

| ● | discover and develop medicines that are differentiated from other products in the market; |

| ● | obtain patent and/or proprietary protection for our products and technologies; |

| ● | obtain required regulatory approvals; |

21

| ● | obtain a commercial partner; |

| ● | commercialize our drugs, if approved; and |

| ● | attract and retain high-quality research, development and commercial personnel. |

Key factors affecting the success of any approved product include its efficacy, safety profile, drug interactions, method of administration, pricing, reimbursement and level of promotional activity relative to those of competing drugs.