Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2016

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 0-23486

NN, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 62-1096725 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

207 Mockingbird Lane

Johnson City, Tennessee 37604

(Address of principal executive offices, including zip code)

(423) 434-8300

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☒ | |||

| Non-accelerated filer |

☐ (Do not check if a smaller reporting company) |

Smaller reporting company |

☐ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of November 1, 2016, there were 27,239,637 shares of the registrant’s common stock, par value $0.01 per share, outstanding.

Table of Contents

NN, Inc.

| Page No. | ||||||

| Item 1. | Financial Statements | 3 | ||||

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 17 | ||||

| Item 3. | Quantitative and Qualitative Disclosures about Market Risk | 25 | ||||

| Item 4. | Controls and Procedures | 25 | ||||

| Item 1. | Legal Proceedings | 25 | ||||

| Item 1A. | Risk Factors | 26 | ||||

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 26 | ||||

| Item 3. | Defaults Upon Senior Securities | 26 | ||||

| Item 4. | Mine Safety Disclosures | 26 | ||||

| Item 5. | Other Information | 26 | ||||

| Item 6. | Exhibits | 26 | ||||

| 27 | ||||||

2

Table of Contents

| Item 1. | Financial Statements |

NN, Inc.

Condensed Consolidated Statements of Net Income and Comprehensive Income (Loss)

(Unaudited)

| Three Months ended September 30, |

Nine Months ended September 30, |

|||||||||||||||

| (in thousands, except per share data) |

2016 | 2015 | 2016 | 2015 | ||||||||||||

| Net sales |

$ | 204,961 | $ | 154,824 | $ | 631,459 | $ | 483,425 | ||||||||

| Cost of products sold (exclusive of depreciation and amortization shown separately below) |

152,538 | 120,195 | 469,086 | 378,220 | ||||||||||||

| Selling, general and administrative |

18,347 | 11,949 | 60,651 | 37,910 | ||||||||||||

| Acquisition related costs excluded from selling, general and administrative |

— | 3,948 | — | 3,948 | ||||||||||||

| Depreciation and amortization |

14,693 | 8,610 | 47,177 | 25,702 | ||||||||||||

| Restructuring and impairment charges |

656 | — | 7,241 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income from operations |

18,727 | 10,122 | 47,304 | 37,645 | ||||||||||||

| Interest expense |

16,337 | 4,584 | 48,924 | 16,543 | ||||||||||||

| Write-off of unamortized debt issuance costs |

2,589 | — | 2,589 | — | ||||||||||||

| Derivative payments on interest rate swap |

609 | — | 609 | — | ||||||||||||

| Derivative losses on change in interest rate swap fair value |

3,130 | — | 3,130 | — | ||||||||||||

| Other (income) expense, net |

(235 | ) | 593 | (2,188 | ) | 2,012 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) before provision (benefit) for income taxes and share of net income from joint venture |

(3,703 | ) | 4,945 | (5,760 | ) | 19,090 | ||||||||||

| Provision (benefit) expense for income taxes |

(6,423 | ) | 936 | (6,469 | ) | 4,009 | ||||||||||

| Share of net income from joint venture |

1,427 | 621 | 4,170 | 2,503 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

$ | 4,147 | $ | 4,630 | $ | 4,879 | $ | 17,584 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other comprehensive income (loss): |

||||||||||||||||

| Change in fair value of interest rate swap |

4,211 | (1,419 | ) | 3,130 | (3,044 | ) | ||||||||||

| Foreign currency translation gain (loss) |

382 | (5,332 | ) | 4,176 | (17,562 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other comprehensive income (loss) |

4,593 | (6,751 | ) | 7,306 | (20,606 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income (loss) |

$ | 8,740 | $ | (2,121 | ) | $ | 12,185 | $ | (3,022 | ) | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic net income per share: |

||||||||||||||||

| Net income |

$ | 0.15 | $ | 0.17 | $ | 0.18 | $ | 0.87 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average shares outstanding |

27,159 | 26,839 | 26,973 | 20,122 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted net income per share: |

||||||||||||||||

| Net income |

$ | 0.15 | $ | 0.17 | $ | 0.18 | $ | 0.86 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average shares outstanding |

27,322 | 27,167 | 27,103 | 20,467 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cash dividends per common share |

$ | 0.07 | $ | 0.07 | $ | 0.21 | $ | 0.21 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The accompanying notes are an integral part of the Condensed Consolidated Financial Statements.

3

Table of Contents

NN, Inc.

Condensed Consolidated Balance Sheets

(Unaudited)

| September 30, | December 31, | |||||||

| (in thousands, except per share data) |

2016 | 2015 | ||||||

| Assets |

||||||||

| Current assets: |

||||||||

| Cash |

$ | 14,788 | $ | 15,087 | ||||

| Accounts receivable, net |

147,427 | 123,005 | ||||||

| Inventories |

118,834 | 119,836 | ||||||

| Income tax receivable |

682 | 3,989 | ||||||

| Current deferred tax assets |

— | 6,696 | ||||||

| Other current assets |

13,758 | 11,568 | ||||||

|

|

|

|

|

|||||

| Total current assets |

295,489 | 280,181 | ||||||

| Property, plant and equipment, net |

325,969 | 318,968 | ||||||

| Goodwill, net |

448,254 | 449,898 | ||||||

| Intangible assets, net |

261,953 | 282,169 | ||||||

| Non-current deferred tax assets |

— | 742 | ||||||

| Investment in joint venture |

38,925 | 38,462 | ||||||

| Other non-current assets |

11,058 | 10,147 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 1,381,648 | $ | 1,380,567 | ||||

|

|

|

|

|

|||||

| Liabilities and Stockholders’ Equity |

||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 69,730 | $ | 69,101 | ||||

| Accrued salaries, wages and benefits |

26,181 | 21,125 | ||||||

| Income taxes payable |

— | 5,350 | ||||||

| Current maturities of long-term debt |

8,621 | 11,714 | ||||||

| Current portion of obligation under capital lease |

3,933 | 4,786 | ||||||

| Other current liabilities |

27,910 | 21,275 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

136,375 | 133,351 | ||||||

| Non-current deferred tax liabilities |

105,132 | 117,459 | ||||||

| Long-term debt, net of current portion |

795,692 | 795,400 | ||||||

| Accrued post-employment benefits |

6,091 | 6,157 | ||||||

| Obligation under capital lease, net of current portion |

6,792 | 9,573 | ||||||

| Other |

5,223 | 4,746 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

1,055,305 | 1,066,686 | ||||||

| Total stockholders’ equity |

326,343 | 313,881 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 1,381,648 | $ | 1,380,567 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of the Condensed Consolidated Financial Statements.

4

Table of Contents

NN, Inc.

Condensed Consolidated Statement of Changes in Stockholders’ Equity

(Unaudited)

| Common Stock | Accumulated | |||||||||||||||||||||||||||

| Number | Additional | other | Non- | |||||||||||||||||||||||||

| of | Par | paid in | Retained | comprehensive | controlling | |||||||||||||||||||||||

| (in thousands of dollars and shares) | shares | value | capital | earnings | income (loss) | interest | Total | |||||||||||||||||||||

| Balance, December 31, 2015 |

26,849 | $ | 269 | $ | 277,582 | $ | 55,151 | $ | (19,153 | ) | $ | 32 | $ | 313,881 | ||||||||||||||

| Net income |

— | — | — | 4,879 | — | — | 4,879 | |||||||||||||||||||||

| Dividends paid |

— | — | — | (5,677 | ) | — | — | (5,677 | ) | |||||||||||||||||||

| Stock option expense |

— | — | 679 | — | — | — | 679 | |||||||||||||||||||||

| Shares issued for option exercises |

242 | 2 | 2,551 | — | — | — | 2,553 | |||||||||||||||||||||

| Restricted and performance based stock compensation expense |

152 | 1 | 2,880 | — | — | — | 2,881 | |||||||||||||||||||||

| Restricted shares forgiven for taxes and forfeited |

(21 | ) | — | (159 | ) | — | — | — | (159 | ) | ||||||||||||||||||

| Foreign currency translation gain |

— | — | — | — | 4,176 | — | 4,176 | |||||||||||||||||||||

| Change in fair value of interest rate swap |

— | — | — | — | 3,130 | — | 3,130 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Balance, September 30, 2016 |

27,222 | $ | 272 | $ | 283,533 | $ | 54,353 | $ | (11,847 | ) | $ | 32 | $ | 326,343 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

The accompanying notes are an integral part of the Condensed Consolidated Financial Statements.

5

Table of Contents

NN, Inc.

Condensed Consolidated Statements of Cash Flows

(Unaudited)

| Nine Months ended | ||||||||

| September 30, | ||||||||

| (in thousands of dollars) |

2016 | 2015 | ||||||

| Cash flows from operating activities: |

||||||||

| Net income |

$ | 4,879 | $ | 17,584 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: |

||||||||

| Depreciation and amortization |

47,177 | 25,702 | ||||||

| Amortization of debt issuance costs |

3,048 | 1,827 | ||||||

| Interest rate swap: |

||||||||

| Total derivative losses (gains), net |

3,130 | — | ||||||

| Write-off of unamortized debt issuance costs |

2,589 | — | ||||||

| Joint venture net income in excess of cash received |

(463 | ) | (2,503 | ) | ||||

| Compensation expense from issuance of restricted stock and incentive stock options |

3,560 | 2,919 | ||||||

| Non-cash restructuring and impairment charges |

1,891 | — | ||||||

| Changes in operating assets and liabilities: |

||||||||

| Accounts receivable |

(24,422 | ) | (11,361 | ) | ||||

| Inventories |

1,663 | (3,940 | ) | |||||

| Accounts payable |

629 | (8,380 | ) | |||||

| Other assets and liabilities |

2,451 | (8,593 | ) | |||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

46,132 | 13,255 | ||||||

|

|

|

|

|

|||||

| Cash flows from investing activities: |

||||||||

| Acquisition of property, plant and equipment |

(32,166 | ) | (26,318 | ) | ||||

| Proceeds from measurement period adjustments to previous acquisition |

1,635 | — | ||||||

| Proceeds from disposals of property, plant and equipment |

366 | 441 | ||||||

| Cash paid to acquire businesses, net of cash received |

— | (9,017 | ) | |||||

| Capital contributions to joint venture |

— | 869 | ||||||

|

|

|

|

|

|||||

| Net cash used by investing activities |

(30,165 | ) | (34,025 | ) | ||||

|

|

|

|

|

|||||

| Cash flows from financing activities: |

||||||||

| Debt issue costs paid |

(3,692 | ) | (136 | ) | ||||

| Dividends Paid |

(5,677 | ) | (4,554 | ) | ||||

| Proceeds from long-term debt |

39,000 | 8,517 | ||||||

| Repayment of long-term debt |

(39,562 | ) | (149,530 | ) | ||||

| Repayments of short-term debt, net |

(4,101 | ) | (1,458 | ) | ||||

| Proceeds from shares issued |

— | 173,052 | ||||||

| Proceeds from issuance of stock and exercise of stock options |

2,553 | 1,831 | ||||||

| Principal payments on capital lease |

(3,465 | ) | (3,990 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by (used in) financing activities |

(14,944 | ) | 23,732 | |||||

|

|

|

|

|

|||||

| Effect of exchange rate changes on cash flows |

(1,322 | ) | (177 | ) | ||||

| Net change in cash and cash equivalents |

(299 | ) | 2,785 | |||||

| Cash and cash equivalents at beginning of year |

15,087 | 37,317 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of year |

$ | 14,788 | $ | 40,102 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of the Condensed Consolidated Financial Statements.

6

Table of Contents

NN, Inc.

Notes to Condensed Consolidated Financial Statements

September 30, 2016 and 2015

(Unaudited)

(In thousands, except per share data)

Note 1. Interim Financial Statements

We are a diversified industrial company and a leading global manufacturer of high precision bearing components, industrial plastic products and precision metal components to a variety of markets on a global basis. We have 41 manufacturing plants in North America, Western Europe, Eastern Europe, South America and China. Our business is aggregated into three reportable segments, the Precision Bearing Components Group (formerly known as our Metal Bearing Components Group), the Precision Engineered Products Group (formerly known as our Plastics and Rubber Components Group) and the Autocam Precision Components Group. As used in this Quarterly Report on Form 10-Q, the terms “NN”, “the Company”, “we”, “our”, or “us” mean NN, Inc. and its subsidiaries.

The accompanying Condensed Consolidated Financial Statements of NN, Inc. have not been audited, except that the Condensed Consolidated Balance Sheet at December 31, 2015 was derived from our audited consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2015 (the “2015 Annual Report”), which was filed with the U.S. Securities and Exchange Commission, or the SEC, on March 15, 2016. In our opinion, these Condensed Consolidated Financial Statements reflect all adjustments necessary to fairly state the results of operations for the three and nine month periods ended September 30, 2016 and 2015, our financial position at September 30, 2016 and December 31, 2015, and the cash flows for the nine month periods ended September 30, 2016 and 2015 on a basis consistent with our audited consolidated financial statements. These adjustments are of a normal recurring nature and are, in the opinion of management, necessary to present fairly our financial position and operating results for the interim periods.

Included in the Selling, general and administrative expense line item in the Condensed Consolidated Statement of Net Income during the nine months ended September 30, 2016 is an out of period adjustment in the amount of $0.4 million, to correct compensation expense recorded with respect to share-based awards previously granted to executives who, either at the time of such grant or during the applicable vesting period, were eligible to retire from the Company, upon which the vesting of all or a portion of these awards would be accelerated.

Included in the Derivative losses on change in interest rate swap fair value line item in the Condensed Consolidated Statement of Net Income during the three months ended September 30, 2016 is an out of period adjustment in the amount of $0.5 million, related to the second quarter of 2016. The adjustment was recorded to correct other comprehensive income that should have been recorded to earnings in second quarter because the third quarter forecasted hedged transaction was no longer probable of occurring.

Certain information and footnote disclosures normally included in the consolidated financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted from the interim financial statements presented in this Quarterly Report on Form 10-Q. These unaudited, Condensed Consolidated Financial Statements should be read in conjunction with our audited consolidated financial statements and the notes thereto included in our 2015 Annual Report. The results for the nine months ended September 30, 2016 are not necessarily indicative of results for the year ending December 31, 2016 or any other future periods.

Newly Adopted Accounting Standards

During the first quarter of 2016, we adopted the following Accounting Standard Updates (“ASU”), and as necessary, certain reclassifications have been made to conform to the current year presentation:

We adopted ASU No. 2015-03, Interest - Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs (“ASU 2015-03”), which provides guidance on simplifying the presentation of debt issuance costs on the balance sheet. To simplify presentation of debt issuance costs, the amendments in ASU 2015-03 require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The recognition and measurement guidance for debt issuance costs are not affected by the amendments in this update. In accordance with ASU 2015-03, we are applying the new guidance on a retrospective basis, wherein the balance sheet of each individual period presented was adjusted to reflect the period-specific effects of applying the new guidance.

We adopted ASU No. 2015-11, Inventory (Topic 330) - Simplifying the Measurement of Inventory (“ASU 2015-11”), which simplifies the subsequent measurement of inventories by replacing the lower of cost or market test with a lower of cost and net realizable value test. The subsequent measurement of inventory test, historically three measurements under lower of cost or market, is replaced by lower of cost and net realizable value test. Thus, we will compare the cost of inventory to only one measure, its net realizable value. When evidence exists that the net realizable value of inventory is less than its cost (due to damage, physical deterioration, obsolescence, changes in price levels or other causes), we will recognize the difference as a loss in earnings in the period in which it occurs. In accordance with ASU 2015-11, we are applying the new guidance on a prospective basis.

7

Table of Contents

We adopted ASU No. 2015-16, Business Combinations (Topic 805) - Simplifying the Accounting for Measurement-Period Adjustments (“ASU 2015-16”), which eliminates the requirement that an acquirer in a business combination account for measurement-period adjustments retrospectively. Instead, we will recognize a measurement-period adjustment during the period in which we determine the amount of the adjustment, including the effect on earnings of any amounts we would have recorded in previous periods if the accounting had been completed at the acquisition date. In accordance with ASU 2015-16, we are applying the new guidance on a prospective basis to adjustments to provisional amounts that occur after December 31, 2015. That is, ASU 2015-16 applies to open measurement periods, regardless of the acquisition date.

We adopted ASU No. 2015-17, Income Taxes (Topic 740), Balance Sheet Classification of Deferred Taxes (“ASU 2015-17”). We will classify all deferred tax assets and liabilities as noncurrent on the balance sheet instead of separating deferred taxes into current and noncurrent amounts. In addition, we will no longer allocate valuation allowances between current and noncurrent deferred tax assets because those allowances also will be classified as noncurrent. We have elected to apply ASU 2015-17 on a prospective basis. Therefore, the prior periods were not retroactively adjusted.

Issuance of New Accounting Standards

In 2014, the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) issued the joint revenue recognition standard. Since its release, there have been multiple proposed and finalized amendments made to the revenue recognition standard. The revenue recognition standard is effective for public companies beginning January 1, 2018 with full retrospective or modified retrospective adoption permitted. This standard will change current revenue practices, processes, systems, controls, and disclosures and take time and resources to adopt. Factors that will affect pre and post-implementation include, but are not limited to, identifying all the contracts that exist and whether incidental obligations or marketing incentives included in those contracts are performance obligations. The revenue recognition standard will impact the timing of when revenue received under these performance obligations is recognized.

On February 25, 2016, the FASB issued ASU 2016-02, Leases (“ASU 2016-02”). ASU 2016-02 creates Topic 842, Leases, in the FASB Accounting Standards Codification (“FASB ASC”) and supersedes FASB ASC 840, Leases. Entities that hold numerous equipment and real estate leases, in particular those with numerous operating leases, will be most affected by the new guidance. The leasing accounting standard is effective for public companies beginning January 1, 2019 with modified retrospective adoption required and early adoption permitted. The amendments in ASU 2016-02 are expected to impact balance sheets at many companies by adding lease-related assets and liabilities. This may affect compliance with contractual agreements and loan covenants. We are currently evaluating the impacts of the lease accounting standards on our financial position or results of operations and related disclosures.

On August 27, 2014, the FASB issued ASU 2014-15, Presentation of Financial Statements – Going Concern, (“ASU 2014-15”) which provides guidance on determining when and how to disclose going-concern uncertainties in the financial statements. The new standard requires management to perform interim and annual assessments of an entity’s ability to continue as a going concern within one year of the date the financial statements are issued. An entity must provide certain disclosures if “conditions or events raise substantial doubt about the entity’s ability to continue as a going concern.” ASU 2014-15 applies to all entities and is effective for annual periods ending after December 15, 2016, and interim periods thereafter, with early adoption permitted. We will be adopting ASU 2014-15 beginning December 31, 2016, which will involve adding policies and procedures around our assessments to continue as a going concern.

The FASB issued ASU 2016-15, Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments (“ASU 2016-15”). ASU 2016-15 provides clarification on how certain cash receipts and cash payments are presented and classified on the statement of cash flows. ASU 2016-15 is effective for annual and interim periods beginning in 2018 and is required to be adopted using a retrospective approach if practicable, with early adoption permitted. The Company does not expect the adoption of ASU 2016-15 to have a material impact on its Consolidated Statement of Cash Flows.

Except for per share data or as otherwise indicated, all dollar amounts presented in the tables in these Notes to the Condensed Consolidated Financial Statements are in thousands.

8

Table of Contents

Note 2. Acquisitions

PEP

As reported in our 2015 Annual Report, we completed the acquisition of Precision Engineered Products Holdings, Inc. (“PEP”) on October 19, 2015. During the nine months ended September 30, 2016, we finalized all issues related to customary working capital adjustments, fixed assets and income taxes. The changes primarily arose from differences noted during acquisition integration and finalizing return to provision adjustments. As a result, we adjusted the preliminary allocation of the purchase price initially recorded at the PEP acquisition date to reflect these measurement period adjustments.

The following table summarizes the final purchase price allocation for the PEP acquisition:

| As Reported on December 31, 2015 |

Subsequent Adjustments to fair value |

Restated as of September 30, 2016 |

||||||||||

| Consideration: |

||||||||||||

| Cash paid |

$ | 621,196 | $ | — | $ | 621,196 | ||||||

| Cash adjustment |

— | (1,635 | ) | (1,635 | ) | |||||||

|

|

|

|

|

|

|

|||||||

| Total consideration |

$ | 621,196 | $ | (1,635 | ) | $ | 619,561 | |||||

|

|

|

|

|

|

|

|||||||

| Fair value of assets acquired and liabilities assumed on October 19, 2015: |

||||||||||||

| Current assets |

$ | 69,331 | $ | 452 | $ | 69,783 | ||||||

| Property, plant and equipment |

56,163 | (962 | ) | 55,201 | ||||||||

| Intangible assets subject to amortization |

240,490 | — | 240,490 | |||||||||

| Other non-current assets |

1,500 | — | 1,500 | |||||||||

| Goodwill |

364,450 | (1,805 | ) | 362,645 | ||||||||

|

|

|

|

|

|

|

|||||||

| Total assets acquired |

731,934 | (2,315 | ) | 729,619 | ||||||||

|

|

|

|

|

|

|

|||||||

| Current liabilities |

21,131 | — | 21,131 | |||||||||

| Non-current deferred tax liabilities |

87,578 | (680 | ) | 86,898 | ||||||||

| Other non-current liabilities |

2,029 | — | 2,029 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total liabilities assumed |

110,738 | (680 | ) | 110,058 | ||||||||

|

|

|

|

|

|

|

|||||||

| Net assets acquired |

$ | 621,196 | $ | (1,635 | ) | $ | 619,561 | |||||

|

|

|

|

|

|

|

|||||||

In accordance with ASU 2015-16 as noted above in Note 1, we have recognized measurement-period adjustments during the period in which we determine the amount of the adjustment, including the effect on earnings of any amounts we would have recorded in previous periods if the accounting had been completed at the acquisition date.

Note 3. Inventories

Inventories are comprised of the following:

| September 30, 2016 |

December 31, 2015 |

|||||||

| Raw materials |

$ | 50,862 | $ | 50,204 | ||||

| Work in process |

33,857 | 30,604 | ||||||

| Finished goods |

34,115 | 39,028 | ||||||

|

|

|

|

|

|||||

| Inventories |

$ | 118,834 | $ | 119,836 | ||||

|

|

|

|

|

|||||

Inventories on consignment at customer locations as of September 30, 2016 and December 31, 2015 totaled $4.8 million and $5.1 million, respectively, for both dates.

Inventories are stated at the lower of cost or net realizable value. Cost is determined using the average cost method. The inventory valuations above were developed using normalized production capacities for each of our manufacturing locations. Any costs from abnormal excess capacity or under-utilization of fixed production overheads are expensed in the period incurred and are not included as a component of inventory valuation.

9

Table of Contents

Note 4. Net Income Per Share

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Net income |

$ | 4,147 | $ | 4,630 | $ | 4,879 | $ | 17,584 | ||||||||

| Weighted average shares outstanding |

27,159 | 26,839 | 26,973 | 20,122 | ||||||||||||

| Effect of dilutive stock options |

163 | 328 | 130 | 345 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted shares outstanding |

27,322 | 27,167 | 27,103 | 20,467 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic net income per share |

$ | 0.15 | $ | 0.17 | $ | 0.18 | $ | 0.87 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted net income per share |

$ | 0.15 | $ | 0.17 | $ | 0.18 | $ | 0.86 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

For both the three and nine month periods ended September 30, 2016, approximately 0.6 million and 0.7 million potentially dilutive stock options, respectively, had the effect of being anti-dilutive and were excluded from the calculation of diluted earnings per share. For both the three and nine month periods ended September 30, 2015, approximately 0.7 million potentially dilutive stock options had the effect of being anti-dilutive and were excluded from the calculation of diluted earnings per share.

Note 5. Segment Information

The segment information and the accounting policies of each segment are the same as those described in the notes to the consolidated financial statements entitled “Segment Information” and “Summary of Significant Accounting Policies and Practices,” respectively, included in our 2015 Annual Report. Our business is aggregated into three reportable segments, the Precision Bearing Components Group (formerly known as our Metal Bearing Components Group), the Precision Engineered Products Group (formerly known as our Plastics and Rubber Components Group) and the Autocam Precision Components Group. We account for inter-segment sales and transfers at current market prices. We did not have any significant inter-segment transactions during the three and nine month periods ended September 30, 2016 and 2015.

| Precision Bearing Components Group |

Autocam Precision Components Group |

Precision Engineered Components Group |

Corporate and Consolidations |

Total | ||||||||||||||||

| Three Months ended September 30, 2016 |

||||||||||||||||||||

| Revenues from external customers |

$ | 58,247 | $ | 80,492 | $ | 66,222 | $ | — | $ | 204,961 | ||||||||||

| Income (loss) from operations |

$ | 5,840 | $ | 8,464 | $ | 9,913 | $ | (5,490 | ) | $ | 18,727 | |||||||||

| Nine Months ended September 30, 2016 |

||||||||||||||||||||

| Revenues from external customers |

$ | 188,149 | $ | 247,473 | $ | 195,837 | $ | — | $ | 631,459 | ||||||||||

| Income (loss) from operations |

$ | 18,639 | $ | 22,761 | $ | 26,116 | $ | (20,212 | ) | $ | 47,304 | |||||||||

| Total assets |

$ | 224,531 | $ | 421,946 | $ | 727,656 | $ | 7,515 | $ | 1,381,648 | ||||||||||

| Three Months ended September 30, 2015 |

||||||||||||||||||||

| Revenues from external customers |

$ | 60,545 | $ | 83,243 | $ | 11,036 | $ | — | $ | 154,824 | ||||||||||

| Income (loss) from operations |

$ | 6,633 | $ | 10,894 | $ | 595 | $ | (8,000 | ) | $ | 10,122 | |||||||||

| Nine Months ended September 30, 2015 |

||||||||||||||||||||

| Revenues from external customers |

$ | 203,041 | $ | 252,336 | $ | 28,048 | $ | — | $ | 483,425 | ||||||||||

| Income (loss) from operations |

$ | 25,125 | $ | 27,707 | $ | 1,309 | $ | (16,496 | ) | $ | 37,645 | |||||||||

| Total assets |

$ | 209,120 | $ | 431,478 | $ | 28,808 | $ | 50,070 | $ | 719,476 | ||||||||||

10

Table of Contents

Note 6. Long-Term Debt

Long-term debt at September 30, 2016 and December 31, 2015 consisted of the following:

| September 30, | Restated December 31, |

|||||||

| 2016 | 2015 | |||||||

| Borrowings under our $545.0 million Senior Secured Term Loan B bearing interest at the greater of 0.75% or 1 month LIBOR (0.53% at September 30, 2016) plus an applicable margin of 4.25% at September 30, 2016, expiring October 19, 2022, net of debt issuance costs of $21.1 million at September 30, 2016 and $20.6 million at December 31, 2015. |

$ | 525,203 | $ | 552,957 | ||||

| Borrowings under our $133.0 million Senior Secured Revolver bearing interest at LIBOR (0.53% at September 30, 2016) plus an applicable margin of 3.50% at September 30, 2016, expiring October 19, 2020, net of debt issuance costs of $2.6 million at September 30, 2016 and $2.9 million at December 31, 2015. |

30,405 | 3,547 | ||||||

| Borrowings under our $250.0 million Senior Notes bearing interest at 10.25%, maturing on November 1, 2020, net of debt issuance costs of $5.2 million at September 30, 2016 and $5.9 million at December 31, 2015. |

244,822 | 244,088 | ||||||

| French Safeguard Obligations (Autocam) |

496 | 2,000 | ||||||

| Brazilian lines of credit and equipment notes (Autocam) |

681 | 826 | ||||||

| Chinese line of credit (Autocam) |

2,706 | 3,696 | ||||||

|

|

|

|

|

|||||

| Total debt |

804,313 | 807,114 | ||||||

| Less current maturities of long-term debt |

8,621 | 11,714 | ||||||

|

|

|

|

|

|||||

| Long-term debt, excluding current maturities of long-term debt |

$ | 795,692 | $ | 795,400 | ||||

|

|

|

|

|

|||||

On September 30, 2016, we amended and restated our credit facility, which lowered the interest rate and rate floor on the Company’s Senior Secured Term Loan B (the “Term Loan B”). The new applicable rate for the Term Loan B is London Inter Bank Offering Rate (“LIBOR”), subject to a 0.75% rate floor, plus 4.25%, which in combination is 75 basis points lower (or 0.75%) than the previous rate. There were no changes to the maturities or covenants under the Term Loan B. Concurrent with the amended and restated Term Loan B, the Senior Secured Revolving Credit Facility (the “Senior Secured Revolver”) was upsized from $100 million to $133 million. Proceeds were drawn under the Senior Secured Revolver to pay down debt under the Term Loan B, reducing the debt under the Term Loan B to $545 million. There were no changes to the Senior Secured Revolver maturities, and the covenant threshold was increased from $30 million to $39.9 million (30% drawn threshold). The refinancing and debt transactions resulted in lower principal amounts outstanding on the Term Loan B, increased borrowings under the Senior Secured Revolver and a lower effective interest rate for the overall debt holdings.

In conjunction with the amended and restated credit facility, we incurred $3.7 million in debt issuance costs. We wrote off a total of $2.6 million in debt issuance costs related to the modification and extinguishment of debt.

As part of the merger with Autocam Corporation (“Autocam”) in 2014, we assumed certain foreign credit facilities. These facilities relate to local borrowings in France, Brazil and China. These facilities are with financial institutions in the countries in which foreign plants operate and are used to fund working capital and equipment purchases in those countries. The following paragraphs describe these foreign credit facilities.

Our French operation (acquired with Autocam) has liabilities with certain creditors subject to Safeguard protection. The liabilities are being paid annually over a 10-year period until 2019 and carry a zero percent interest rate. Amounts due as of September 30, 2016 to those creditors opting to be paid over a 10-year period totaled $0.5 million, of which $0.1 million is included in current maturities of long-term debt and $0.4 million is included in long-term debt, net of current portion, on the Condensed Consolidated Balance Sheet.

The Brazilian equipment notes represent borrowings from certain Brazilian banks to fund equipment purchases for Autocam’s Brazilian plants. These credit facilities have annual interest rates ranging from 2.5% to 9.1%.

The Chinese line of credit is a working capital line of credit with a Chinese bank bearing an annual interest rate ranging from 1.35% to 4.88%.

11

Table of Contents

As discussed in Note 1, we have adopted ASU 2015-03, which provides guidance on simplifying the presentation of debt issuance costs on the balance sheet. To simplify presentation of debt issuance costs, the amendments in ASU 2015-03 require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The following table displays the debt amounts reported as of December 31, 2015, restated for the adoption of ASU 2015-03. The debt issuance costs were reclassified from other non-current assets and directly applied to the associated liability.

| Reported December 31, 2015 |

ASU 2015-13 Reclass |

Restated December 31, 2015 |

||||||||||

| Borrowings under our $575.0* million Senior Secured Term Loan B |

$ | 562,580 | $ | (9,623 | ) | $ | 552,957 | |||||

| Borrowings under our $100.0** million Senior Secured Revolver |

6,462 | (2,915 | ) | 3,547 | ||||||||

| Borrowings under our $250.0 million Senior Notes |

244,509 | (421 | ) | 244,088 | ||||||||

| French Safeguard Obligations (Autocam) |

2,000 | 2,000 | ||||||||||

| Brazilian lines of credit and equipment notes (Autocam) |

826 | 826 | ||||||||||

| Chinese line of credit (Autocam) |

3,696 | 3,696 | ||||||||||

|

|

|

|

|

|||||||||

| Total debt |

820,073 | 807,114 | ||||||||||

| Less current maturities of long-term debt |

11,714 | 11,714 | ||||||||||

|

|

|

|

|

|||||||||

| Long-term debt, excluding current maturities of long-term debt |

$ | 808,359 | $ | 795,400 | ||||||||

|

|

|

|

|

|||||||||

| * | Amended from $575 million down to $545 million on September 30, 2016. |

| ** | Amended from $100 million up to $133 million on September 30, 2016. |

Note 7. Goodwill, Net

The changes in the carrying amount of goodwill, net, for the nine months ended September 30, 2016 are as follows:

| Precision Bearing Components Group |

Autocam Precision Components Group |

Precision Engineered Products Group |

Total | |||||||||||||

| Balance as of December 31, 2015 |

$ | 9,111 | $ | 73,992 | $ | 366,795 | $ | 449,898 | ||||||||

| Currency impacts |

161 | — | — | 161 | ||||||||||||

| Goodwill changes from measurement period |

— | — | (1,805 | ) | (1,805 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance as of September 30, 2016 |

$ | 9,272 | $ | 73,992 | $ | 364,990 | $ | 448,254 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The goodwill balances are tested for impairment on an annual basis during the fourth quarter and more often if a triggering event occurs. As noted in Note 2. Acquisitions, some measurement period adjustments to goodwill were made for the PEP acquisition. As of September 30, 2016, there were no indications of impairment at the reporting units with goodwill balances.

Note 8. Intangible Assets, Net

The changes in the carrying amount of intangible assets, net, for the nine months ended September 30, 2016 are as follows:

| Precision | Autocam | Precision | ||||||||||||||

| Bearing | Precision | Engineered | ||||||||||||||

| Components | Components | Products | ||||||||||||||

| Group | Group | Group | Total | |||||||||||||

| Balance as of December 31, 2015 |

$ | 1,952 | $ | 46,417 | $ | 233,800 | $ | 282,169 | ||||||||

| Amortization |

(156 | ) | (2,721 | ) | (17,488 | ) | (20,365 | ) | ||||||||

| Currency impacts |

24 | 125 | — | 149 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance as of September 30, 2016 |

$ | 1,820 | $ | 43,821 | $ | 216,312 | $ | 261,953 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Note 9. Shared-Based Compensation

During the three and nine months ended September 30, 2016 and 2015, approximately $0.9 million and $3.6 million in 2016 and $1.1 million and $2.9 million in 2015, respectively, of compensation expense was recognized in selling, general and administrative expense for all share-based awards. During the nine months ended September 30, 2016, we granted 152,510 restricted stock awards, 167,000 option awards, and 202,330 performance based awards to non-executive directors, officers and certain other key employees. During the nine months ended September 30, 2015, we granted 114,475 restricted stock awards, 54,600 option awards and 71,550 performance based awards to non-executive directors, officers and certain other key employees.

12

Table of Contents

The shares of restricted stock granted during the nine months ended September 30, 2016, vest pro-rata over three years for officers and certain other key employees and over one year for non-executive directors. During the three and nine months ended September 30, 2016 and 2015, we incurred $0.4 million and $2.0 million in 2016 and $0.6 million and $1.7 million in 2015, respectively, in expense related to restricted stock. The fair value of the shares issued was determined by using the grant date closing price of our common stock.

The performance share units granted during the nine months ended September 30, 2016 will be satisfied in the form of shares of common stock during 2019 if certain performance and/or market conditions are met. We are recognizing the compensation expense over the three-year period in which the performance and market conditions are measured. During the three and nine months ended September 30, 2016 and 2015, we incurred $0.3 million and $0.9 million in 2016, and $0.3 million and $0.5 million in 2015, respectively, in expense related to performance share units. The fair value of the performance share units issued was determined by using the grant date closing price of our common stock for the units with a performance condition and a Monte Carlo valuation model for the units that have a market condition.

We incurred $0.2 million and $0.7 million in 2016 and $0.2 million and $0.7 million in 2015 of stock option expense in the three and nine months ended September 30, 2016 and 2015, respectively. The weighted average grant date fair value of options granted during the nine months ended September 30, 2016, was $5.02. The fair value of our options cannot be determined by market value, because our options are not traded in an open market. Accordingly, we utilized the Black Scholes financial pricing model to estimate the fair value. The weighted average assumptions relevant to determining the fair value of the 2016 stock option grants are below:

| 2016 Stock Option Awards |

||||

| Term |

6 years | |||

| Risk free interest rate |

1.43 | % | ||

| Dividend yield |

2.48 | % | ||

| Expected volatility |

59.23 | % | ||

| Expected forfeiture rate |

3.00 | % | ||

The following table provides a reconciliation of option activity for the nine months ended September 30, 2016:

| Weighted- | ||||||||||||||||

| Weighted- | Average | |||||||||||||||

| Average | Remaining | |||||||||||||||

| Exercise | Contractual | Aggregate | ||||||||||||||

| Options |

Shares (000) | Price | Term (years) | Intrinsic Value | ||||||||||||

| Outstanding at January 1, 2016 |

1,034 | $ | 12.09 | |||||||||||||

| Granted |

167 | $ | 11.31 | |||||||||||||

| Exercised |

(242 | ) | $ | 10.54 | ||||||||||||

| Forfeited or expired |

(33 | ) | $ | 17.38 | ||||||||||||

|

|

|

|

|

|||||||||||||

| Outstanding at September 30, 2016 |

926 | $ | 12.16 | 6.1 | $ | 6,092 | (1) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Exercisable at September 30, 2016 |

714 | $ | 11.54 | 5.2 | $ | 1,086 | (1) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | The intrinsic value is the amount by which the market price of our stock was greater than the exercise price of any individual option grant at September 30, 2016. |

Note 10. Provision for Income Taxes

The Company’s effective income tax rate for the three months ended September 30, 2016 and 2015, was 173% and 19%, respectively. The Company’s effective income tax rate for the nine months ended September 30, 2016 and 2015, was 112% and 21%, respectively. The higher effective income tax rate for the three months and nine months ended September 30, 2016 was driven by an increase in the full year effective income tax rate. The increase in full year effective income tax rate was primarily due to a mix of higher U.S. losses with lower earnings attributed to foreign subsidiaries. The full year effective income tax rate applied to our consolidated year-to-date loss increased from 10% to 112%, resulting in a $6 million decrease in income tax expense in the third quarter. Excluding this increase, the tax rate for the third quarter would have been 15% (versus 173%).

13

Table of Contents

Note 11. Commitments and Contingencies

Brazil ICMS Tax Matter

Prior to our acquisition of Autocam, Autocam’s Brazilian subsidiary received notification from the Brazilian tax authorities regarding ICMS (state value added tax or VAT) tax credits claimed on intermediary materials (tooling and perishable items) used in the manufacturing process. The Brazilian tax authority notification disallowed state ICMS credits claimed on intermediary materials based on the argument that these items are not intrinsically related to the manufacturing process. Autocam Brazil filed an administrative defense with the Brazilian tax authority arguing, among other matters, that it should qualify for an ICMS tax credit, contending that the intermediary materials are directly related to the manufacturing process.

We believe that we have substantial legal and factual defenses, and we plan to defend our interests in this matter vigorously. While we believe a loss is not probable, we estimate the range of possible losses related to this assessment is from $0 to $6.0 million. No amount was accrued at September 30, 2016 for this matter. There was no material change in the status of this matter from December 31, 2015 to September 30, 2016.

We are entitled to indemnification from the former shareholders of Autocam, subject to the limitations and procedures set forth in the agreement and plan of merger relating to our acquisition of Autocam. Management believes the indemnification would include amounts owed for the tax, interest and penalties related to this matter.

All Other Legal Matters

All other legal proceedings are of an ordinary and routine nature and are incidental to our operations. Management believes that such proceedings should not, individually or in the aggregate, have a material adverse effect on our business, financial condition, results of operations or cash flows. In making that determination, we analyze the facts and circumstances of each case at least quarterly in consultation with our attorneys and determine a range of reasonably possible outcomes.

Note 12. Investment in Non-Consolidated Joint Venture

As part of the Autocam Precision Components Group, we own a 49% investment in a joint venture with an unrelated entity called Wuxi Weifu Autocam Precision Machinery Company, Ltd. (the “JV”), a Chinese company located in Wuxi, China.

Below are the components of our JV investment balance at September 30, 2016:

| Balance as of December 31, 2015 |

$ | 38,462 | ||

| Our share of cumulative earnings |

4,545 | |||

| Dividends declared and paid by joint venture |

(3,707 | ) | ||

| Accretion of basis difference from purchase accounting |

(375 | ) | ||

|

|

|

|||

| Balance as of September 30, 2016 |

$ | 38,925 | ||

|

|

|

The following table summarizes balance sheet information for the JV:

| September 30, 2016 |

December 31, 2015 |

|||||||

| Current assets |

$ | 32,425 | $ | 24,663 | ||||

| Non-current assets |

22,875 | 22,847 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 55,300 | $ | 47,510 | ||||

|

|

|

|

|

|||||

| Current liabilities |

$ | 16,540 | $ | 11,171 | ||||

|

|

|

|

|

|||||

| Total liabilities |

$ | 16,540 | $ | 11,171 | ||||

|

|

|

|

|

|||||

Dividends of $3.7 million were declared and paid by the JV during the three months ended September 30, 2016. We had sales to the JV of approximately $0.1 million during the three and nine months ended September 30, 2016. Amounts due to us from the JV were $0.2 million as of September 30, 2016.

Note 13. Fair Value Measurements

We present fair value measurements and disclosures applicable to both our financial and nonfinancial assets and liabilities that are measured and reported on a fair value basis. Fair value is an exit price representing the expected amount we would receive to sell an asset or pay to transfer a liability in an orderly transaction with market participants at the measurement date. We have followed consistent methods and assumptions to estimate the fair values as more fully described in our 2015 Annual Report.

14

Table of Contents

Our financial instruments that are subject to fair value disclosure consist of cash and cash equivalents, accounts receivable, accounts payable, derivatives and long-term debt. At September 30, 2016, the carrying values of all of these financial instruments, except the long-term debt with fixed interest rates, approximated fair value. The fair value of floating-rate debt approximates the carrying amount because the interest rates paid are based on short-term maturities. The fair value of our fixed-rate long-term debt is estimated based on the Bloomberg algorithm, which takes into account similar sized and industry debt (a Level 2 category fair value measurement). As of September 30, 2016, the fair value of our fixed-rate debt was $263.8 million, and $258.6 net of debt issuance costs.

Fair value principles prioritize valuation inputs across three broad levels. Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities. Level 2 inputs are quoted prices for similar assets and liabilities in active markets or inputs that are observable for the asset or liability, either directly or indirectly through market corroboration, for substantially the full term of the financial instrument. Level 3 inputs are unobservable inputs based on the assumptions used to measure assets and liabilities at fair value. An asset or liability’s classification within the various levels is determined based on the lowest level input that is significant to the fair value measurement.

Recurring Fair Value Measurements

The following table summarizes the assets and liabilities measured at fair value on a recurring basis for our interest rate swap derivative financial instrument:

| Fair Value Measurements at September 30, 2016 | ||||||||||||||||

| Quoted Prices in | ||||||||||||||||

| Active Markets | Significant Other | Significant | ||||||||||||||

| September 30, | for Identical | Observable Inputs | Unobservable | |||||||||||||

| Description |

2016 | Assets (Level 1) | (Level 2) | Inputs (Level 3) | ||||||||||||

| Derivative asset - current |

$ | 22 | $ | — | $ | 22 | $ | — | ||||||||

| Derivative asset - noncurrent |

198 | — | 198 | — | ||||||||||||

| Derivative liability - current |

(1,956 | ) | — | (1,956 | ) | — | ||||||||||

| Derivative liability - noncurrent |

(2,164 | ) | — | (2,164 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | (3,900 | ) | $ | — | $ | (3,900 | ) | $ | — | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Fair Value Measurements at December 31, 2015 | ||||||||||||||||

| Quoted Prices in | ||||||||||||||||

| Active Markets | Significant Other | Significant | ||||||||||||||

| December 31, | for Identical | Observable Inputs | Unobservable | |||||||||||||

| Description |

2015 | Assets (Level 1) | (Level 2) | Inputs (Level 3) | ||||||||||||

| Derivative asset - current |

$ | 388 | $ | — | $ | 388 | $ | — | ||||||||

| Derivative asset - noncurrent |

368 | — | 368 | — | ||||||||||||

| Derivative liability - current |

(2,098 | ) | — | (2,098 | ) | — | ||||||||||

| Derivative liability - noncurrent |

(1,673 | ) | — | (1,673 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | (3,015 | ) | $ | — | $ | (3,015 | ) | $ | — | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

Our policy is to manage interest expense using a mix of fixed and variable rate debt. To manage this mix effectively, we may enter into interest rate swaps in which we agree to exchange the difference between fixed and variable interest amounts calculated by reference to an agreed upon notional principal amount.

Our $150 million interest rate swap went into effect on December 29, 2015, at which time our interest rate was effectively 6.966%. The objective of the hedge was to eliminate the variability of cash flows in interest payments on the first $150 million of variable interest rate debt (the Term Loan B). The variable rate benchmark was the three month LIBOR rate for both the Term Loan B and the interest rate swap. The changes in cash flows of the interest rate swap were expected to exactly offset the changes in cash flows of the Term Loan B. The hedged risk was the interest rate risk exposure to changes in the interest payments, attributable to changes in the benchmark three-month LIBOR interest rates (subject to a 1.0% LIBOR index floor) from December 29, 2015 through December 31, 2018. As disclosed in Note 6. Long-Term Debt, the LIBOR floor index was lowered to 0.75% on September 30, 2016, and our intent regarding future interest rate resets changed. Three-month LIBOR was above the floor, and it was more economical to use one-month LIBOR. Based upon these facts we chose to discontinue Hodge Accounting. Therefore, we assessed the amounts deferred in accumulated other comprehensive income (“AOCI”) as the forecasted transactions would not be probable that the company would use the three-month LIBOR through the remainder of the derivative duration. As a result, all amounts of AOCI were reclassified to earnings. Prospectively, we will account for the interest rate swap on a mark-to-market basis. The change in reporting will have no impact on our reported cash flows, although future results of operations on a GAAP basis will be affected by the potential volatility of mark-to-market gains and losses which fluctuate with changes in interest rates.

15

Table of Contents

The inputs for determining fair value of the interest rate swap are classified as Level 2 inputs. Level 2 fair value is based on estimates using standard pricing models. These standard pricing models use inputs which are derived from or corroborated by observable market data such as interest rate yield curves, index forward curves, discount curves, and volatility surfaces. Counterparties to these derivative contracts are highly rated financial institutions which we believe carry only a minimal risk of nonperformance.

We have elected to present the derivative contracts on a gross basis in the Condensed Consolidated Balance Sheet included within other current assets and other non-current assets and other current liabilities and other non-current liabilities. Had we chosen to present the derivative contract on a net basis, we would have a derivative in a net liability position of $3.9 million as of September 30, 2016. We do not have any cash collateral due under such agreements.

As of September 30, 2016, we reported no gains or losses in AOCI related to the interest rate swaps. In connection with lowering the LIBOR index floor from 1.0% to 0.75% within the $150 million interest rate swap, we received a $0.3 million payment that increased the net liability position on the $150 million interest rate swap. The payment was reported as a reduction to derivative asset (other current assets) on the Condensed Consolidated Balance Sheets. Additionally, during the nine months ended September 30, 2016 when the interest rate swap was accounted for in accordance with hedge accounting, the periodic settlements and related reclassification of other comprehensive income was $1.4 million of net hedging losses on the interest rate swap in the interest expense line on the Condensed Consolidated Statements of Net Income. We recognized $0.6 million of interest rate swap settlements for the third quarter of 2016 in the Derivative payments on interest rate swap line on the Condensed Consolidated Statements of Net Income. If there are no changes in the interest rates for the next twelve months, we expect to make $1.9 million in cash payments related to the interest rates swap. See the following “Derivatives’ Hedging Relationships” section of this Note 13 for more information regarding the impact of the interest rate swaps on our Condensed Consolidated Financial Statements.

Derivatives’ Hedging Relationships

| Amount | Pre-tax amount of gain/(loss) | |||||||||||||||||||

| recognized in Other | Location of gain/(loss) | reclassified from | ||||||||||||||||||

| Comprehensive Income | reclassified from | AOCI into Net Income | ||||||||||||||||||

| (effective portion) | AOCI into | (effective portion) | ||||||||||||||||||

| September 30, | December 31, | Net Income (effective | September 30, | December 31, | ||||||||||||||||

| Derivatives’ Cash Flow Hedging Relationships |

2016 | 2015 | portion) | 2016 | 2015 | |||||||||||||||

| Forward starting interest rate swap contract |

$ | — | $ | (3,015 | ) | Interest Expense | $ | 1,393 | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

| $ | — | $ | (3,015 | ) | $ | 1,393 | $ | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

As of September 30, 2016, we did not own derivative instruments that were classified as fair value hedges or trading securities. In addition, as of September 30, 2016, we did not own derivative instruments containing credit risk contingencies.

Note 14. Restructuring and Impairment Charges

Severance and restructuring costs totaling $0.7 million and $7.2 million were recognized in the three and nine months ended September 30, 2016, comprised of initiatives impacting each of our segments. Of the amounts presented as restructuring costs for Precision Engineered Products, $0.9 million, relate primarily to integration costs.

Within the Precision Bearing Components Group, restructuring initiatives to optimize operations in the U.S., Italy, the Netherlands, Mexico and at segment headquarters resulted in a charge of $2.4 million, which consisted of severance costs relating to headcount reductions.

Within the Autocam Precision Components Group, certain restructuring programs, including the closure of one facility, the Wheeling Plant, resulted in a charge of $3.9 million.

The following table summarizes severance and restructuring activity related to actions incurred for the three and nine months ended September 30, 2016:

| Three Months Ended | Nine Months Ended | |||||||

| September 30, | September 30, | |||||||

| 2016 | 2016 | |||||||

| Severance and other employee costs |

$ | 497 | $ | 4,315 | ||||

| Site closure and other associated cost |

159 | 2,926 | ||||||

|

|

|

|

|

|||||

| Restructuring and impairment charges |

$ | 656 | $ | 7,241 | ||||

|

|

|

|

|

|||||

| Reserve | Reserve | |||||||||||||||

| Balance at | Paid in | Balance at | ||||||||||||||

| December 31, 2015 | Charges | 2016 | September 30 2016 | |||||||||||||

| Severance and other employee costs |

$ | 2,464 | $ | 4,315 | $ | (4,145 | ) | $ | 2,634 | |||||||

| Site closure and other associated cost |

1,845 | 2,926 | (3,519 | ) | 1,252 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 4,309 | $ | 7,241 | $ | (7,664 | ) | $ | 3,886 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

16

Table of Contents

Note 15. Subsequent Event

Subsequent to September 30, 2016, an additional bank was added to our Senior Secured Revolver, increasing our borrowing capacity from $133 million to $143 million, which also increased our covenant threshold to $42.9 million (30% drawn threshold). Additional debt issuance costs of approximately $0.3 million were incurred related to debt issuance costs.

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Forward-Looking Statements

This Quarterly Report on Form 10-Q contains forward-looking statements that are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These statements may discuss goals, intentions and expectations as to future trends, plans, events, results of operations or financial condition, or state other information relating to us, based on current beliefs of management as well as assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “may,” “possible,” “potential,” “predict,” “project” or other similar words, phrases or expressions. Forward-looking statements involve a number of risks and uncertainties that are outside of our control and that may cause actual results to be materially different from such forward-looking statements. Such factors include, among others, general economic conditions and economic conditions in the industrial sector, competitive influences, risks that current customers will commence or increase captive production, risks of capacity underutilization, quality issues, availability of raw materials, currency and other risks associated with international trade, our dependence on certain major customers, the impact of acquisitions and divestitures, unanticipated difficulties integrating acquisitions, new laws and governmental regulations, and other risk factors and cautionary statements listed from time-to-time in our periodic reports filed with the Securities and Exchange Commission. We disclaim any obligation to update any such factors or to publicly announce the result of any revisions to any of the forward-looking statements included herein or therein to reflect future events or developments.

For additional information concerning such risk factors and cautionary statements, please see the section titled “Item 1A. Risk Factors” in our 2015 Annual Report on Form 10-K for the fiscal year ended December 31, 2015, which we filed with the SEC on March 15, 2016 (the “2015 Annual Report”).

Results of Operations

Factors That May Influence Results of Operations

The following is a description of factors that have influenced our nine months ended September 30, 2016 results of operations that we believe are important to provide an understanding of our business and results of operations.

2015 Acquisitions

During the year ended December 31, 2015, we completed the acquisition of Caprock Manufacturing, Inc. and Caprock Enclosures, LLC (collectively, “Caprock”) and Precision Engineered Products Holdings, Inc. (“PEP”). We acquired Caprock on May 29, 2015 and PEP on October 19, 2015. Because these acquisitions occurred during various times in 2015, our results of operations for the three and nine months ended September 30, 2015 do not include all, if any, of the operations of both acquisitions.

In an effort to enhance the comparability of the current and prior year periods, we have aggregated into “acquisitions” within each financial line item comparison for the three and nine months ended September 30, 2016, the impacts of the acquisitions completed in 2015 that were not included in the comparative prior year period. The remaining changes relate to the legacy NN businesses. For more information about the 2015 acquisitions including background on the acquired companies, the purchase price allocations and pro forma information, as required, please refer to Note 2 of the Notes to Consolidated Financial Statements included in our 2015 Annual Report and Note 2 of the Notes to Condensed Consolidated Financial Statements included in this Quarterly Report on Form 10-Q.

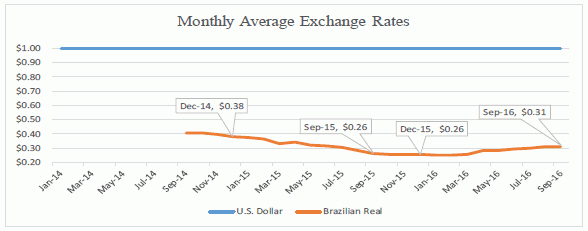

Devaluation of the Euro and Brazilian Real against the U.S. Dollar

The euro devalued against the U.S. dollar beginning in the latter part of the third quarter of 2014 and accelerated during the fourth quarter of 2014 and into the first quarter of 2015. During the nine months ended September 30, 2016, the exchange rate from euro to U.S. dollar slightly increased by 3%, compared to a 9% decline in value for the same period in 2015.

17

Table of Contents

Additionally, the devaluation of the Brazilian real had an impact in comparing Autocam’s sales. During the nine months ended September 30, 2016, the exchange rate from the Brazilian real to the U.S. dollar increased by 19%, compared to a 32% decline in value for the same period in 2015.

The euro and real translation impact, and the translation impact of other currencies, is highlighted below as “foreign exchange effects.”

18

Table of Contents

OVERALL RESULTS

Three Months Ended September 30, 2016 Compared to the Three Months Ended September 30, 2015

| Consolidated NN, Inc. | ||||||||||||||||

| Three Months ended September 30, | ||||||||||||||||

| 2016 | 2015 | Change | ||||||||||||||

| Net sales |

$ | 204,961 | $ | 154,824 | $ | 50,137 | ||||||||||

| Acquisitions |

57,919 | |||||||||||||||

| Foreign exchange effects |

(298 | ) | ||||||||||||||

| Sale of a plant |

(2,298 | ) | ||||||||||||||

| Volume |

(3,082 | ) | ||||||||||||||

| Price/material infation pass-through/mix |

(2,104 | ) | ||||||||||||||

| Cost of products sold (exclusive of depreciation and amortization shown separately below) |

152,538 | 120,195 | 32,343 | |||||||||||||

| Acquisitions |

37,222 | |||||||||||||||

| Foreign exchange effects |

(192 | ) | ||||||||||||||

| Sale of a plant |

(1,731 | ) | ||||||||||||||

| Volume |

(2,026 | ) | ||||||||||||||

| Cost reduction projects and other cost changes |

(930 | ) | ||||||||||||||

| Selling, general and administrative |

18,347 | 11,949 | 6,398 | |||||||||||||

| Acquisitions |

4,619 | |||||||||||||||

| Foreign exchange effects |

(3 | ) | ||||||||||||||

| Infrastructure and staffing costs |

1,782 | |||||||||||||||

| Acquisition related costs excluded from selling, general and administrative |

— | 3,948 | (3,948 | ) | ||||||||||||

| Depreciation and amortization |

14,693 | 8,610 | 6,083 | |||||||||||||

| Acquisitions |

5,990 | |||||||||||||||

| Foreign exchange effects |

(19 | ) | ||||||||||||||

| Increase in expense |

112 | |||||||||||||||

| Restructuring and impairment charges |

656 | — | 656 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Income from operations |

18,727 | 10,122 | 8,605 | |||||||||||||

| Interest expense |

16,337 | 4,584 | 11,753 | |||||||||||||

| Write-off of unamortized debt issuance cost |

2,589 | — | 2,589 | |||||||||||||

| Derivative payments on interest rate swap |

609 | — | 609 | |||||||||||||

| Derivative losses on change in interest rate swap fair value |

3,130 | — | 3,130 | |||||||||||||

| Other (income) expense, net |

(235 | ) | 593 | (828 | ) | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before provision (benefit) for income taxes and share of net income from joint venture |

(3,703 | ) | 4,945 | (8,648 | ) | |||||||||||

| Provision (benefit) expense for income taxes |

(6,423 | ) | 936 | (7,359 | ) | |||||||||||

| Share of net income from joint venture |

1,427 | 621 | 806 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 4,147 | $ | 4,630 | $ | (483 | ) | |||||||||

|

|

|

|

|

|

|

|||||||||||

Net Sales. Net sales increased during the third quarter of 2016 from the third quarter of 2015 due to sales from PEP business that was acquired in the fourth quarter of 2015. The third quarter of 2016 included the net sales of the PEP acquisition, whereas net sales for the third quarter of 2015 did not included net sales of PEP. Partially offsetting these increases were both the sale of the Delta Rubber plant in November 2015 and the impact of devaluation of the euro and other currency denominated sales, as discussed above. Additionally, we had lower sales prices, changes in product mix, and volumes. These decreases in volume relate to global industrial weakness.

Cost of Products Sold (exclusive of depreciation and amortization shown separately below). The increase in cost of products sold was primarily due to the addition of production costs from the acquired PEP business, as discussed above. Partially offsetting these increases was the impact of the devaluation of the euro and other currency denominated costs, as discussed above. Additionally, increases were partially offset by volume and cost savings from production process improvement projects.

Selling, General and Administrative. The majority of the increase during 2016 was due to the selling, general and administrative costs from the acquired PEP business. Additionally, administrative costs were incurred for infrastructure and staffing costs related to our strategic initiatives.

Depreciation and Amortization. The increase in 2016 was due to depreciation and amortization from the acquired PEP business. This additional depreciation and amortization includes the related step-ups of certain property, plant and equipment to fair value and the addition of intangible assets principally for customer relationships and trade names related to the purchase price allocation of the new acquisitions.

19

Table of Contents

Interest expense. Interest expense increased $11.8 million due to higher overall debt levels in the third quarter of 2016 and related amortization of debt issuance costs, primarily related to acquisitions.

| Three Months ended September 30, | ||||||||

| Source |

2016 | 2015 | ||||||

| Interest on debt |

$ | 14,943 | $ | 3,836 | ||||

| Interest rate swaps settlements |

466 | — | ||||||

| Amortization of debt issuance costs |

1,062 | 628 | ||||||

| Capital lease interest |

283 | 453 | ||||||

| Capitalized interest (1) |

(417 | ) | (333 | ) | ||||

|

|

|

|

|

|||||

| Total interest expense |

$ | 16,337 | $ | 4,584 | ||||

|

|

|

|

|

|||||

| Debt issuance costs write-off |

$ | 2,589 | $ | — | ||||

|

|

|

|

|

|||||

| (1) | Capitalized interest primarily relates to the equipment construction efforts at the various plants. |

RESULTS BY SEGMENT

PRECISION BEARING COMPONENTS GROUP

| Three Months ended September 30, | ||||||||||||||||

| 2016 | 2015 | Change | ||||||||||||||

| Net sales |

$ | 58,247 | $ | 60,545 | $ | (2,298 | ) | |||||||||

| Foreign exchange effects |

(256 | ) | ||||||||||||||

| Volume |

(1,879 | ) | ||||||||||||||

| Price/material infation pass-through/mix |

(163 | ) | ||||||||||||||

| Income from operations |

$ | 5,840 | $ | 6,633 | $ | (793 | ) | |||||||||

|

|

|

|

|

|

|

|||||||||||

Net sales decreased during the third quarter of 2016 from the third quarter of 2015 principally due to lower volumes and changes to product mix. The lower volumes were primarily due to global industrial market weakness and declines in heavy truck demand.

The decrease in income from operations was consistent with the decrease in net sales.

AUTOCAM PRECISION COMPONENTS GROUP

| Three Months ended September 30, | ||||||||||||||||

| 2016 | 2015 | Change | ||||||||||||||

| Net sales |

$ | 80,492 | $ | 83,243 | $ | (2,751 | ) | |||||||||

| Foreign exchange effects |

(42 | ) | ||||||||||||||

| Volume |

(1,203 | ) | ||||||||||||||

| Price/material infation pass-through/mix |

(1,506 | ) | ||||||||||||||

| Income from operations |

$ | 8,464 | $ | 10,894 | $ | (2,430 | ) | |||||||||

|

|

|

|

|

|

|

|||||||||||

The decrease in net sales in the third quarter of 2016 were due to industrial market weakness and lower demand with those customers.

The decrease in income from operations was consistent with the decrease in net sales, and due to restructuring charges in 2016 related to our Wheeling plant closure.

20

Table of Contents

PRECISION ENGINEERED PRODUCTS GROUP

| Three Months ended September 30, | ||||||||||||||||

| 2016 | 2015 | Change | ||||||||||||||

| Net sales |

$ | 66,222 | $ | 11,036 | $ | 55,186 | ||||||||||

| Acquisitions |

57,919 | |||||||||||||||

| Sale of a plant |

(2,298 | ) | ||||||||||||||

| Volume |

(435 | ) | ||||||||||||||

| Income from operations |

$ | 9,913 | $ | 595 | $ | 9,318 | ||||||||||

|

|

|