Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2016

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 000-23486

NN, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 62-1096725 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

207 Mockingbird Lane

Johnson City, Tennessee 37604

(Address of principal executive offices, including zip code)

(423) 434-8310

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of April 26, 2016, there were 26,984,822 shares of the registrant’s common stock, par value $0.01 per share, outstanding.

Table of Contents

NN, Inc.

| Page No. | ||||||

| Item 1. |

Financial Statements | |||||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 16 | ||||

| Item 3. |

Quantitative and Qualitative Disclosures about Market Risk | 21 | ||||

| Item 4. |

Controls and Procedures | 22 | ||||

| Item 1. |

Legal Proceedings | 22 | ||||

| Item 1A. |

Risk Factors | 22 | ||||

| Item 2. |

Unregistered Sales of Equity Securities and Use of Proceeds | 23 | ||||

| Item 3. |

Defaults Upon Senior Securities | 23 | ||||

| Item 4. |

Mine Safety Disclosures | 23 | ||||

| Item 5. |

Other Information | 23 | ||||

| Item 6. |

Exhibits | 23 | ||||

| 24 | ||||||

2

Table of Contents

| Item 1. | Financial Statements |

NN, Inc.

Condensed Consolidated Statements of Operations and Comprehensive Income (Loss)

(Unaudited)

| Three Months ended March 31, |

||||||||

| (in thousands, except per share data) |

2016 | 2015 | ||||||

| Net sales |

$ | 212,226 | $ | 163,746 | ||||

| Cost of products sold (exclusive of depreciation and amortization shown separately below) |

159,754 | 129,317 | ||||||

| Selling, general and administrative |

20,712 | 12,001 | ||||||

| Depreciation and amortization |

17,348 | 8,494 | ||||||

| Restructuring and impairment charges |

2,538 | — | ||||||

|

|

|

|

|

|||||

| Income from operations |

11,874 | 13,934 | ||||||

| Interest expense |

16,422 | 5,938 | ||||||

| Other (income) expense, net |

(1,129 | ) | 1,400 | |||||

|

|

|

|

|

|||||

| Income (loss) before provision (benefit) for income taxes and share of net income from joint venture |

(3,419 | ) | 6,596 | |||||

| Provision (benefit) expense for income taxes |

(720 | ) | 1,456 | |||||

| Share of net income from joint venture |

1,400 | 861 | ||||||

|

|

|

|

|

|||||

| Net (loss) income |

$ | (1,299 | ) | $ | 6,001 | |||

|

|

|

|

|

|||||

| Other comprehensive income (loss): |

||||||||

| Change in fair value of interest rate hedge |

(1,002 | ) | (1,564 | ) | ||||

| Foreign currency translation gain (loss) |

6,719 | (16,293 | ) | |||||

|

|

|

|

|

|||||

| Comprehensive income (loss) |

$ | 4,418 | $ | (11,856 | ) | |||

|

|

|

|

|

|||||

| Basic income (loss) per share: |

||||||||

| Net income (loss) |

$ | (0.05 | ) | $ | 0.32 | |||

|

|

|

|

|

|||||

| Weighted average shares outstanding |

26,869 | 18,996 | ||||||

|

|

|

|

|

|||||

| Diluted income (loss) per share: |

||||||||

| Net income (loss) |

$ | (0.05 | ) | $ | 0.31 | |||

|

|

|

|

|

|||||

| Weighted average shares outstanding |

26,869 | 19,380 | ||||||

|

|

|

|

|

|||||

| Cash dividends per common share |

$ | 0.07 | $ | 0.07 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of the Condensed Consolidated Financial Statements.

3

Table of Contents

NN, Inc.

Condensed Consolidated Balance Sheets

(Unaudited)

| March 31, | December 31, | |||||||

| (in thousands, except per share data) |

2016 | 2015 | ||||||

| Assets |

||||||||

| Current assets: |

||||||||

| Cash |

$ | 15,079 | $ | 15,087 | ||||

| Accounts receivable, net |

143,323 | 123,005 | ||||||

| Inventories |

120,119 | 119,836 | ||||||

| Income tax receivable |

3,989 | 3,989 | ||||||

| Current deferred tax assets |

— | 6,696 | ||||||

| Other current assets |

13,125 | 11,568 | ||||||

|

|

|

|

|

|||||

| Total current assets |

295,635 | 280,181 | ||||||

| Property, plant and equipment, net |

325,222 | 318,968 | ||||||

| Goodwill, net |

450,190 | 449,898 | ||||||

| Intangible assets, net |

273,807 | 282,169 | ||||||

| Non-current deferred tax assets |

— | 742 | ||||||

| Investment in joint venture |

39,862 | 38,462 | ||||||

| Other non-current assets |

10,901 | 10,147 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 1,395,617 | $ | 1,380,567 | ||||

|

|

|

|

|

|||||

| Liabilities and Stockholders’ Equity |

||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 70,292 | $ | 69,101 | ||||

| Accrued salaries, wages and benefits |

24,341 | 21,125 | ||||||

| Income taxes payable |

3,525 | 5,350 | ||||||

| Current maturities of long-term debt |

11,947 | 11,714 | ||||||

| Current portion of obligation under capital lease |

4,440 | 4,786 | ||||||

| Other current liabilities |

26,938 | 21,275 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

141,483 | 133,351 | ||||||

| Non-current deferred tax liabilities |

111,050 | 117,459 | ||||||

| Long-term debt, net of current portion |

804,672 | 795,400 | ||||||

| Accrued post-employment benefits |

6,177 | 6,157 | ||||||

| Obligation under capital lease, net of current portion |

8,646 | 9,573 | ||||||

| Other |

6,257 | 4,746 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

1,078,285 | 1,066,686 | ||||||

| Total stockholders’ equity |

317,332 | 313,881 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 1,395,617 | $ | 1,380,567 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of the Condensed Consolidated Financial Statements.

4

Table of Contents

NN, Inc.

Condensed Consolidated Statements of Changes in Stockholders’ Equity

(Unaudited)

| Common Stock | Accumulated | |||||||||||||||||||||||||||

| Number | Additional | other | Non- | |||||||||||||||||||||||||

| of | Par | paid in | Retained | comprehensive | controlling | |||||||||||||||||||||||

| (in thousands of dollars and shares) | shares | value | capital | earnings | income | interest | Total | |||||||||||||||||||||

| Balance, December 31, 2015 |

26,849 | $ | 269 | $ | 277,582 | $ | 55,151 | $ | (19,153 | ) | $ | 32 | $ | 313,881 | ||||||||||||||

| Net income (loss) |

— | — | — | (1,299 | ) | — | — | (1,299 | ) | |||||||||||||||||||

| Dividends paid |

— | — | — | (1,879 | ) | — | — | (1,879 | ) | |||||||||||||||||||

| Stock option expense |

— | — | 202 | — | — | — | 202 | |||||||||||||||||||||

| Restricted and performance based stock compensation expense |

143 | — | 799 | — | — | — | 799 | |||||||||||||||||||||

| Restricted shares forgiven for taxes |

(7 | ) | — | (89 | ) | — | — | — | (89 | ) | ||||||||||||||||||

| Foreign currency translation gain |

— | — | — | — | 6,719 | — | 6,719 | |||||||||||||||||||||

| Change in fair value of interest rate hedge |

— | — | — | — | (1,002 | ) | — | (1,002 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Balance, March 31, 2016 |

26,985 | $ | 269 | $ | 278,494 | $ | 51,973 | $ | (13,436 | ) | $ | 32 | $ | 317,332 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

The accompanying notes are an integral part of the Condensed Consolidated Financial Statements.

5

Table of Contents

NN, Inc.

Condensed Consolidated Statements of Cash Flows

(Unaudited)

| Three Months Ended | ||||||||

| March 31, | ||||||||

| (in thousands of dollars) |

2016 | 2015 | ||||||

| Cash flows from operating activities: |

||||||||

| Net income (loss) |

$ | (1,299 | ) | $ | 6,001 | |||

| Adjustments to reconcile net income (loss) to net cash provided by (used by) operating activities: |

||||||||

| Depreciation and amortization |

17,348 | 8,494 | ||||||

| Amortization of debt issuance costs |

911 | 554 | ||||||

| Joint venture net income in excess of cash received |

(1,400 | ) | (861 | ) | ||||

| Compensation expense from issuance of restricted stock and incentive stock options |

1,001 | 783 | ||||||

| Non-cash restructuring and impairment charges |

1,505 | — | ||||||

| Changes in operating assets and liabilities: |

||||||||

| Accounts receivable |

(20,318 | ) | (24,006 | ) | ||||

| Inventories |

(283 | ) | 2,386 | |||||

| Accounts payable |

1,191 | (7,696 | ) | |||||

| Other assets and liabilities |

4,776 | (3,073 | ) | |||||

|

|

|

|

|

|||||

| Net cash provided by (used by) operating activities |

3,432 | (17,418 | ) | |||||

|

|

|

|

|

|||||

| Cash flows from investing activities: |

||||||||

| Acquisition of property, plant and equipment |

(8,008 | ) | (8,318 | ) | ||||

| Proceeds from disposals of property, plant and equipment |

17 | 246 | ||||||

| Capital contributions to joint venture |

— | (1,372 | ) | |||||

|

|

|

|

|

|||||

| Net cash used by investing activities |

(7,991 | ) | (9,444 | ) | ||||

|

|

|

|

|

|||||

| Cash flows from financing activities: |

||||||||

| Debt issue costs paid |

— | (132 | ) | |||||

| Dividends Paid |

(1,879 | ) | (1,328 | ) | ||||

| Proceeds from long-term debt |

11,000 | 9,109 | ||||||

| Repayment of long-term debt |

(1,437 | ) | — | |||||

| Proceeds (repayment) of short-term debt, net |

(969 | ) | — | |||||

| Proceeds from issuance of stock and exercise of stock options |

— | 157 | ||||||

| Principal payments on capital lease |

(1,342 | ) | (1,325 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by financing activities |

5,373 | 6,481 | ||||||

|

|

|

|

|

|||||

| Effect of exchange rate changes on cash flows |

(822 | ) | (176 | ) | ||||

| Net change in cash and cash equivalents |

(8 | ) | (20,557 | ) | ||||

| Cash and cash equivalents at beginning of year |

15,087 | 37,317 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of year |

$ | 15,079 | $ | 16,760 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of the Condensed Consolidated Financial Statements.

6

Table of Contents

NN, Inc.

Notes to Condensed Consolidated Financial Statements - unaudited

March 31, 2016

Note 1. Interim Financial Statements

We are a diversified industrial company and a leading global manufacturer of high precision bearing components, industrial plastic products and precision metal components to a variety of markets on a global basis. We have 42 manufacturing plants in North America, Western Europe, Eastern Europe, South America and China. Our business is aggregated into three reportable segments, the Precision Bearing Components Group (formerly known as our Metal Bearing Components Group), the Precision Engineered Products Group (formerly known as our Plastics and Rubber Components Group) and the Autocam Precision Components Group. As used in this Quarterly Report on Form 10-Q, the terms “NN”, “the Company”, “we”, “our”, or “us” mean NN, Inc. and its subsidiaries.

The accompanying Condensed Consolidated Financial Statements of NN, Inc. have not been audited, except that the Condensed Consolidated Balance Sheet at December 31, 2015 was derived from our audited consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2015, which was filed with the U.S. Securities and Exchange Commission, or SEC, on March 15, 2016. In our opinion, these financial statements reflect all adjustments necessary to fairly state the results of operations for the three month periods ended March 31, 2016 and 2015, our financial position at March 31, 2016 and December 31, 2015, and the cash flows for the three month periods ended March 31, 2016 and 2015 on a basis consistent with our audited financial statements. These adjustments are of a normal recurring nature and are, in the opinion of management, necessary to present fairly our financial position and operating results for the interim periods.

Certain information and footnote disclosures normally included in the consolidated financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted from the interim financial statements presented in this Quarterly Report on Form 10-Q. These unaudited, Condensed Consolidated Financial Statements should be read in conjunction with our audited consolidated financial statements and the notes thereto included in our most recent Annual Report on Form 10-K for the year ended December 31, 2015, which we filed with the SEC on March 15, 2016. The results for the three month periods ended March 31, 2016 are not necessarily indicative of results for the year ending December 31, 2016 or any other future periods.

During the first quarter of 2016, we adopted the following Accounting Standard Updates (“ASU”), and as necessary, certain reclassifications have been made to conform to the current year presentation:

We adopted ASU No. 2015-03, Interest - Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs (“ASU 2015-03”), which provides guidance on simplifying the presentation of debt issuance costs on the balance sheet. To simplify presentation of debt issuance costs, the amendments in ASU 2015-03 require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The recognition and measurement guidance for debt issuance costs are not affected by the amendments in this update. In accordance with ASU 2015-03, we are applying the new guidance on a retrospective basis, wherein the balance sheet of each individual period presented was adjusted to reflect the period-specific effects of applying the new guidance.

We adopted ASU No. 2015-11, Inventory (Topic 330) - Simplifying the Measurement of Inventory (“ASU 2015-11”), which simplifies the subsequent measurement of inventories by replacing the lower of cost or market test with a lower of cost and net realizable value test. The subsequent measurement of inventory test, historically three measurements under lower of cost or market, is replaced by lower of cost and net realizable value test. Thus, we will compare the cost of inventory to only one measure, its net realizable value. When evidence exists that the net realizable value of inventory is less than its cost (due to damage, physical deterioration, obsolescence, changes in price levels or other causes), we will recognize the difference as a loss in earning in the period in which it occurs. In accordance with ASU 2015-11, we are applying the new guidance on a prospective basis.

We adopted ASU No. 2015-16, Business Combinations (Topic 805) - Simplifying the Accounting for Measurement-Period Adjustments (“ASU 2015-16), which eliminates the requirement that an acquirer in a business combination account for measurement-period adjustments retrospectively. Instead, we will recognize a measurement-period adjustment during the period in which we determine the amount of the adjustment, including the effect on earnings of any amounts it would have recorded in previous periods if the accounting had been completed at the acquisition date. In accordance with ASU 2015-16, we are applying the new guidance on a prospective basis to adjustments to provisional amounts that occur after December 31, 2015. That is, the ASU applies to open measurement periods, regardless of the acquisition date.

7

Table of Contents

We adopted ASU No. 2015-17, Income Taxes (Topic 740), Balance Sheet Classification of Deferred Taxes (“ASU 2015-17”). We will classify all deferred tax assets and liabilities as noncurrent on the balance sheet instead of separating deferred taxes into current and noncurrent amounts. In addition, we will no longer allocate valuation allowances between current and noncurrent deferred tax assets because those allowances also will be classified as noncurrent. We have chosen to apply ASU 2015-17 on a prospective basis. Therefore, the prior periods were not retroactively adjusted.

Except for per share data or as otherwise indicated, all dollar amounts presented in the tables are in thousands.

Note 2. Acquisitions

The 2015 acquisition of Precision Engineered Products Holdings, Inc. (“PEP Acquisition”), which was completed on October 19, 2015, continues to be reviewed regarding the finalization of fair market valuation relating to customary working capital adjustments and income taxes. Any changes in the preliminary purchase price allocation will be subject to the newly adopted ASU 2015-16 as noted above in Note 1.

Note 3. Inventories

Inventories are comprised of the following:

| March 31, 2016 |

December 31, 2015 |

|||||||

| Raw materials |

$ | 39,766 | $ | 50,204 | ||||

| Work in process |

33,807 | 30,604 | ||||||

| Finished goods |

46,546 | 39,028 | ||||||

|

|

|

|

|

|||||

| Inventories |

$ | 120,119 | $ | 119,836 | ||||

|

|

|

|

|

|||||

Inventories on consignment at customer locations as of March 31, 2016 and December 31, 2015 totaled $3.9 million and $5.1 million, respectively.

As noted in Note 1 above, we have adopted ASU 2015-11. Therefore, inventories are stated at the lower of cost or net realizable value. Cost is determined using the average cost method. The inventory valuations above were developed using normalized production capacities for each of our manufacturing locations. Any costs from abnormal excess capacity or under-utilization of fixed production overheads are expensed in the period incurred and are not included as a component of inventory valuation.

Note 4. Net (Loss) Income Per Share

| Three Months Ended | ||||||||

| March 31, | ||||||||

| 2016 | 2015 | |||||||

| Net income (loss) |

$ | (1,299 | ) | $ | 6,001 | |||

| Weighted average shares outstanding |

26,869 | 18,996 | ||||||

| Effect of dilutive stock options |

— | 384 | ||||||

|

|

|

|

|

|||||

| Diluted shares outstanding |

26,869 | 19,380 | ||||||

|

|

|

|

|

|||||

| Basic net income (loss) per share |

$ | (0.05 | ) | $ | 0.32 | |||

|

|

|

|

|

|||||

| Diluted net income (loss) per share |

$ | (0.05 | ) | $ | 0.31 | |||

|

|

|

|

|

|||||

Given the net loss for the three months ended March 31, 2016, all options are considered anti-dilutive. There were no anti-dilutive options excluded from the dilutive shares outstanding for the three month periods ended March 31, 2015.

8

Table of Contents

Note 5. Segment Information

The segment information and the accounting policies of each segment are the same as those described in the notes to the consolidated financial statements entitled “Segment Information” and “Summary of Significant Accounting Policies and Practices,” respectively, included in our Annual Report on Form 10-K for the fiscal year ended December 31, 2015, which we filed with the SEC on March 15, 2016. Our business is aggregated into three reportable segments, the Precision Bearing Components Group (formerly known as our Metal Bearing Components Group), the Precision Engineered Products Group (formerly known as our Plastics and Rubber Components Group) and the Autocam Precision Components Group. We account for inter-segment sales and transfers at current market prices. We did not have any significant inter-segment transactions during the three months ended March 31, 2016 and 2015.

| Precision | Autocam | Precision | ||||||||||||||||||

| Bearing | Precision | Engineered | Corporate | |||||||||||||||||

| Components | Components | Components | and | |||||||||||||||||

| Group | Group | Group | Consolidations | Total | ||||||||||||||||

| Three Months ended March 31, 2016 |

||||||||||||||||||||

| Revenues from external customers |

$ | 64,745 | $ | 83,990 | $ | 63,491 | $ | — | $ | 212,226 | ||||||||||

| Income (loss) from operations |

$ | 6,326 | $ | 6,527 | $ | 5,421 | $ | (6,400 | ) | $ | 11,874 | |||||||||

| Total assets |

$ | 227,852 | $ | 426,741 | $ | 737,956 | $ | 3,068 | $ | 1,395,617 | ||||||||||

| Three Months ended March 31, 2015 |

||||||||||||||||||||

| Revenues from external customers |

$ | 73,236 | $ | 82,622 | $ | 7,888 | $ | — | $ | 163,746 | ||||||||||

| Income (loss) from operations |

$ | 9,089 | $ | 7,718 | $ | 213 | $ | (3,086 | ) | $ | 13,934 | |||||||||

| Total assets |

$ | 204,032 | $ | 439,542 | $ | 18,023 | $ | 32,789 | $ | 694,386 | ||||||||||

Note 6. Long-Term Debt and Short-Term Debt

Long-term debt and short-term debt at March 31, 2016 and December 31, 2015 consisted of the following:

| Restated | ||||||||

| March 31, | December 31, | |||||||

| 2016 | 2015 | |||||||

| Borrowings under our $575.0 million Senior Secured Term Loan B bearing interest the greater of 1% or 3 month LIBOR (0.63% at March 31, 2016, 0.61% at December 31, 2015) plus an applicable margin of 4.75% at March 31, 2016, expiring October 19, 2022, net of debt issuance costs of $20.1 million at March 31, 2016 and $20.6 million at December 31, 2015. |

552,038 | 552,957 | ||||||

| Borrowings under our $100.0 million Senior Secured Revolver bearing interest at LIBOR (0.43% at March 31, 2016, 0.42% at December 31, 2015) plus an applicable margin of 3.50% at March 31, 2016, expiring October 19, 2020, net of debt issuance costs of $2.8 million at March 31, 2016 and $2.9 million at December 31, 2015. |

15,211 | 3,547 | ||||||

| Borrowings under our $250.0 million Senior Notes bearing interest at 10.25%, maturing on November 1, 2020, net of debt issuance costs of $5.7 million at March 31, 2016 and $5.9 million at December 31, 2015. |

244,330 | 244,088 | ||||||

| French Safeguard Obligations (Autocam) |

507 | 2,000 | ||||||

| Brazilian lines of credit and equipment notes (Autocam) |

812 | 826 | ||||||

| Chinese line of credit (Autocam) |

3,721 | 3,696 | ||||||

|

|

|

|

|

|||||

| Total debt |

816,619 | 807,114 | ||||||

| Less current maturities of long-term debt |

11,947 | 11,714 | ||||||

|

|

|

|

|

|||||

| Long-term debt, excluding current maturities of long-term debt |

$ | 804,672 | $ | 795,400 | ||||

|

|

|

|

|

|||||

9

Table of Contents

On October 19, 2015, concurrent with the PEP Acquisition, we: (i) entered into a new senior secured term loan facility in the amount of up to $525 million with a seven year maturity (the “New Term Loan Credit Facility”); (ii) entered into a new senior secured revolving credit facility in the amount of up to $100 million with a five year maturity (together with the New Term Loan Credit Facility, the “New Senior Credit Facilities”); and (iii) issued of $300 million of 10.25% senior notes due 2020 (the “Senior Notes”). The New Senior Credit Facilities replaced our existing credit facilities. On November 9, 2015, an incremental term loan of $50 million was drawn on the New Term Loan Credit Facility and the proceeds were used to repurchase approximately $50 million of the Senior Notes.

The interest applicable to borrowings under the New Senior Credit Facilities are based upon a fluctuating rate of interest measured by reference to either, at our option, (i) a base rate, plus an applicable margin, or (ii) the greater of the London Interbank Offered Rate (“LIBOR”) or 1.0%, plus an applicable margin. The initial applicable margin for all borrowings under the New Term Loan Credit Facility is 3.75% per annum with respect to base rate borrowings and 4.75% per annum with respect to LIBOR borrowings. The initial applicable margin for New Senior Secured Revolving Credit Facility borrowings is 2.5% per annum with respect to base rate borrowings and 3.5% per annum with respect to LIBOR borrowings, which shall be in effect until we provide a compliance certificate, as required by the credit agreement. Thereafter, the applicable margin shall be determined by reference to a ratio of our consolidated leverage ratio. Our obligations under the New Senior Credit Facilities are guaranteed by certain of our direct and indirect, existing and future domestic subsidiaries, subject to customary exceptions and limitations. The New Senior Credit Facilities are secured by a first priority lien over substantially all of NN’s and each guarantor’s assets, subject to certain customary exceptions. The New Senior Credit Facilities are subject to negative covenants that, among other things subject to certain exceptions, limit our ability and the ability of its restricted subsidiaries to: (i) incur liens; (ii) incur indebtedness; (iii) make investments and acquisitions, (iv) merge, liquidate or dissolve, (v) sell assets, including capital stock of subsidiaries; (vi) pay dividends on capital stock or redeem, repurchase or retire capital stock; (viii) alter our business; (viii) engage in transactions with our affiliates; and (ix) enter into agreements limiting subsidiary dividends and distributions. In the event borrowings under the New Senior Secured Revolving Credit Facility exceed 30.0% of the aggregate commitments under the revolver, we will become subject to a financial covenant that requires us to maintain a specified consolidated net leverage ratio. The credit agreement provides that we have the right to request one or more increases in the revolving loan commitments or term loan commitment up to $100.0 million in the aggregate. In total, we have paid debt issuance costs of $21.1 million related to the New Term Loan Credit Facility and $2.3 million related to the New Senior Secured Revolving Credit Facility, which are being amortized into interest expense over the life of the New Senior Credit Facilities.

The Senior Notes will mature on November 1, 2020. Interest will be payable semi-annually in arrears on May 1 and November 1 of each year, commencing May 2016. Under the Senior Notes, we received proceeds of $293.3 million net of a discount of $6.8 million, which is being amortized into interest expense over the life of the Senior Notes. We have paid a total of $7.3 million in debt issuance costs, which includes the $6.8 million of debt discount, all of which is being amortized into interest expense over the life of the Senior Notes. The Senior Notes will be guaranteed by each existing direct and indirect domestic restricted subsidiaries (excluding immaterial subsidiaries). The Senior Notes and guarantees will be senior unsecured obligations of the issuer and the guarantors, respectively, and will rank pari passu in right of payments with all existing and future senior debt and senior to all existing and future subordinated debt of the issuer and guarantors. The Senior Notes and guarantees will be effectively subordinated to all existing and future secured debt of the issuer and guarantors to the extent of the assets securing such debt. In addition, the Senior Notes and the guarantees will be structurally subordinated to all indebtedness and other liabilities and preferred stock of our subsidiaries that do not guarantee the Senior Notes. The Senior Notes have not been registered under the Securities Act of 1933, as amended, or any state securities law and may not be offered or sold within the United States or to, or for the benefit of, a U.S. person (as defined by Regulation S under the Securities Act) except in transactions exempt from, or not subject to, the registration requirements of the Securities Act. The Senior Notes were offered and sold only to persons reasonably believed to be “qualified institutional buyers” (as defined in Rule 144A under the Securities Act) and to persons outside the United States under Regulations S. We will use our commercially reasonable efforts to register notes having substantially identical terms (other than restrictions on transfer and additional interest) as the Senior Notes with the SEC as part of an offer to exchange registered exchange notes for the Senior Notes. We will use our commercially reasonable effort to file a registration statement for the exchange notes with the SEC and cause that registration statement to be declared effective 300 days of the issue date of the Senior Notes. If we fail to register the Senior Notes, than annual interest rate on the Senior Notes will increase by 0.25%. The annual interest rate on the Senior Notes will increase by an additional 0.25% for each subsequent 90-day period during which a registration default continues, up to a maximum additional interest rate of 1.0% per year.

As part of the merger with Autocam, we assumed certain foreign credit facilities. These facilities relate to local borrowings in France, Brazil and China. These facilities are with financial institutions in the countries in which foreign plants operate and are meant to fund working capital and equipment purchases in those countries. Below is a description of the credit facilities.

Our French operation (acquired with Autocam) has liabilities with certain creditors subject to Safeguard protection. The liabilities are being paid annually over a 10-year period until 2019 and carry a zero percent interest rate. Amounts due as of March 31, 2016, to those creditors opting to be paid over a 10-year period totaled $0.5 million and are included in current maturities of long-term debt of $0.4 million and long-term debt, net of current portion of $0.1 million.

10

Table of Contents

The Brazilian equipment notes represent borrowings from certain Brazilian banks to fund equipment purchases for Autocam’s Brazilian plants. These credit facilities have annual interest rates ranging from 2.5% to 9.1%.

The Chinese line of credit is a working capital line of credit with a Chinese bank bearing an annual interest rate of 4.95%.

As discussed in Note 1, we have adopted ASU 2015-03, which provides guidance on simplifying the presentation of debt issuance costs on the balance sheet. To simplify presentation of debt issuance costs, the amendments in ASU No. 2015-03 require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The table below displays the audited debt footnote amounts for the year ended December 31, 2015 restated for the adoption of ASU 2015-03. The debt issuance costs were reclassified from other non-current assets and directly applied to the associated liability.

| Audited December 31, 2015 |

ASU 2015-13 Reclass |

Restated December 31, 2015 |

||||||||||

| Borrowings under our $575.0 million Senior Secured Term Loan B |

$ | 562,580 | $ | (9,623 | ) | $ | 552,957 | |||||

| Borrowings under our $100.0 million Senior Secured Revolver |

6,462 | (2,915 | ) | 3,547 | ||||||||

| Borrowings under our $250.0 million Senior Notes |

244,509 | (421 | ) | 244,088 | ||||||||

| French Safeguard Obligations (Autocam) |

2,000 | 2,000 | ||||||||||

| Brazilian lines of credit and equipment notes (Autocam) |

826 | 826 | ||||||||||

| Chinese line of credit (Autocam) |

3,696 | 3,696 | ||||||||||

|

|

|

|

|

|||||||||

| Total debt |

820,073 | 807,114 | ||||||||||

| Less current maturities of long-term debt |

11,714 | 11,714 | ||||||||||

|

|

|

|

|

|||||||||

| Long-term debt, excluding current maturities of long-term debt |

808,359 | 795,400 | ||||||||||

|

|

|

|

|

|||||||||

Note 7. Goodwill, net

The changes in the carrying amount of goodwill, net for the three month period ended March 31, 2016 are as follows:

| Precision Bearing Components Group |

Autocam Precision Components Group |

Precision Engineered Products Group |

Total | |||||||||||||

| Balance as of December 31, 2015 |

$ | 9,111 | $ | 73,992 | $ | 366,795 | $ | 449,898 | ||||||||

| Currency impacts |

292 | — | — | 292 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance as of March 31, 2016 |

$ | 9,403 | $ | 73,992 | $ | 366,795 | $ | 450,190 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The goodwill balances are tested for impairment on an annual basis during the fourth quarter and between annual tests if a triggering event occurs. As of March 31, 2016, there were no indications of impairment at the reporting units with goodwill balances.

Note 8. Intangible Assets, Net

The changes in the carrying amount of intangible assets, net for the three month period ended March 31, 2016 are as follows:

| Precision Bearing Components Group |

Autocam Precision Components Group |

Precision Engineered Products Group |

Total | |||||||||||||

| Balance as of December 31, 2015 |

$ | 1,952 | $ | 46,417 | $ | 233,800 | $ | 282,169 | ||||||||

| Amortization |

(53 | ) | (940 | ) | (7,471 | ) | (8,464 | ) | ||||||||

| Currency impacts |

46 | 56 | — | 102 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance as of March 31, 2016 |

$ | 1,945 | $ | 45,533 | $ | 226,329 | $ | 273,807 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

11

Table of Contents

Note 9. Stock-Based Compensation

During the three months ended March 31, 2016 and 2015, approximately $1.0 million and $0.7 million, respectively, of compensation expense was recognized in selling, general and administrative expense for all share-based awards. During the three months ended March 31, 2016, there were 149,665 restricted stock awards and 167,000 option awards to non-executive directors, officers and certain other key employees. Additionally, during the three months ended March 31, 2016, there were 202,330 performance stock units issued to officers and certain key employees. During the three months ended March 31, 2015, there were 67,200 shares of restricted stock granted to non-executive directors, officers and certain other key employees.

The shares of restricted stock granted during the three months ended March 31, 2016, vest pro-rata over three years for officers and certain other key employees and over one year for non-executive directors. During the three months ended March 31, 2016 and 2015, we incurred $0.6 million and $0.5 million, respectively, in expense related to restricted stock. The fair value of the shares issued was determined by using the grant date closing price of our common stock.

The performance stock units granted during the three month period ended March 31, 2016 will be satisfied in the form of shares of common stock during 2019 depending on meeting certain performance and/or market conditions. We are recognizing the compensation expense over the three year period in which the performance and market conditions are measured. During the three months ended March 31, 2016 and 2015, we incurred $0.2 million and $0, respectively, in expense related to performance stock units. The fair value of the performance share units issued was determined by using the grant date closing price of our common stock for the units with a performance condition and a Monte Carlo valuation model for the units that have a market condition.

We incurred $0.2 million and $0.3 million of stock option expense in the three months ended March 31, 2016 and 2015, respectively. The fair value of our options cannot be determined by market value, because our options are not traded in an open market. Accordingly, we utilized the Black Scholes financial pricing model to estimate the fair value.

The following table provides a reconciliation of option activity for the three months ended March 31, 2016:

| Options |

Shares (000) | Weighted- Average Exercise Price |

Weighted- Average Remaining Contractual Term |

Aggregate Intrinsic Value |

||||||||||||

| Outstanding at January 1, 2016 |

1,034 | $ | 12.09 | |||||||||||||

| Granted |

167 | $ | 11.31 | |||||||||||||

| Exercised |

— | $ | — | |||||||||||||

| Forfeited or expired |

(10 | ) | $ | 17.98 | ||||||||||||

|

|

|

|

|

|||||||||||||

| Outstanding at March 31, 2016 |

1,191 | $ | 11.93 | 6.2 | $ | 3,312 | (1) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Exercisable at March 31, 2016 |

963 | $ | 11.35 | 5.3 | $ | 2,916 | (1) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | The intrinsic value is the amount by which the market price of our stock was greater than the exercise price of any individual option grant at March 31, 2016. |

Note 10. Provision for Income Taxes

For the three months ended March 31, 2016 and 2015, our effective tax rates were 21% and 22%, respectively. The difference between the U.S. federal statutory tax rate of 34% and our effective tax rates was primarily due to non-U.S. based earnings being taxed at lower rates reducing the effective rates for the three months ended March 31, 2016. The difference between the U.S. federal statutory tax rate of 34% and our effective tax rate in the three months ended March 31, 2015 of 22% was due to non-U.S. based earnings being taxed at lower rates reducing the effective rates for the three months ended March 31, 2015 by 10%. As of March 31, 2016, we do not foresee any significant changes to our unrecognized tax benefits within the next twelve months.

In accordance with ASU 2015-17, we have classified all deferred tax assets and liabilities as noncurrent on the balance sheet instead of separating deferred taxes into current and noncurrent amounts. In addition, we will no longer allocate valuation allowances between current and noncurrent deferred tax assets because those allowances also will be classified as noncurrent.

12

Table of Contents

Note 11. Commitments and Contingencies

Brazil ICMS Tax Matter

Prior to our acquisition of Autocam, Autocam’s Brazilian subsidiary received notification from the Brazilian tax authorities regarding ICMS (state value added tax or VAT) tax credits claimed on intermediary materials (tooling and perishable items) used in the manufacturing process. The Brazilian tax authority notification disallowed state ICMS credits claimed on intermediary materials based on the argument that these items are not intrinsically related to the manufacturing process. Autocam Brazil filed an administrative defense with the Brazilian tax authority arguing, among other matters, that it should qualify for an ICMS tax credit, contending that the intermediary materials are directly related to the manufacturing process.

We believe that we have substantial legal and factual defenses, and plan to defend our interests in this matter vigorously. While we believe a loss is not probable, we estimate the range of possible losses related to this assessment is from $0 to $6.0 million. No amount was accrued at March 31, 2016 for this matter. There was no material change in the status of this matter from December 31, 2015 to March 31, 2016.

We are entitled to indemnification from the former shareholders of Autocam, subject to the limitations and procedures set forth in the agreement and plan of merger relating to our acquisition of Autocam. Management believes the indemnification would include amounts owed for the tax, interest and penalties related to this matter.

All other legal proceedings are of an ordinary and routine nature and are incidental to our operations. Management believes that such proceedings should not, individually or in the aggregate, have a material adverse effect on our business, financial condition, results of operations or cash flows. In making that determination, we analyze the facts and circumstances of each case at least quarterly in consultation with our attorneys and determine a range of reasonably possible outcomes.

Note 12. Investment in Non-Consolidated Joint Venture

As part of the Autocam Precision Components Group, we own a 49% investment in a joint venture with an unrelated entity called Wuxi Weifu Autocam Precision Machinery Company, Ltd., a Chinese company located in Wuxi, China (the “JV”).

Below are the components of our JV investment balance at March 31, 2016:

| Balance as of December 31, 2015 |

$ | 38,462 | ||

| Our share of cumulative earnings |

1,547 | |||

| Accretion of basis difference from purchase accounting |

(147 | ) | ||

|

|

|

|||

| Balance as of March 31, 2016 |

$ | 39,862 | ||

|

|

|

Set forth below is summarized balance sheet information for the JV:

| March 31, 2016 |

December 31, 2015 |

|||||||

| Current assets |

$ | 29,263 | $ | 24,663 | ||||

| Non-current assets |

23,646 | 22,847 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 52,909 | $ | 47,510 | ||||

|

|

|

|

|

|||||

| Current liabilities |

$ | 11,233 | $ | 11,171 | ||||

|

|

|

|

|

|||||

| Total liabilities |

$ | 11,233 | $ | 11,171 | ||||

|

|

|

|

|

|||||

No dividends were declared and paid by the JV during the three months ended March 31, 2016. We had sales to the JV of less than $0.1 million during the three months ended March 31, 2016. Amounts due to us from the JV were $0.1 million as of March 31, 2016.

Note 13. Fair Value Measurements

We present fair value measurements and disclosures applicable to both our financial and nonfinancial assets and liabilities that are measured and reported on a fair value basis. Fair value is an exit price representing the expected amount we would receive to sell an asset or pay to transfer a liability in an orderly transaction with market participants at the measurement date. We have followed consistent methods and assumptions to estimate the fair values as more fully described in our Annual Report on Form 10-K for the year ended December 31, 2015, which we filed with the SEC on March 15, 2016.

13

Table of Contents

Our financial instruments that are subject to fair value disclosure consist of cash and cash equivalents, accounts receivable, accounts payable, derivatives and long-term debt. At March 31, 2016, the carrying values of all of these financial instruments, except the long-term debt with fixed interest rates, approximated fair value. The fair value of floating-rate debt approximates the carrying amount because the interest rates paid are based on short-term maturities. The fair value of our fixed-rate long-term debt is estimated based on the Bloomberg algorithm taking into to account similar sized and industry debt (a Level 2 category fair value measurement). As of March 31, 2016, the fair value of our fixed-rate debt was $222.7 million.

Recurring Fair Value Measurements

The following table summarizes the assets and liabilities measured at fair value on a recurring basis for our interest rate swap derivative financial instrument:

| Fair Value Measurements at March 31, 2016 | ||||||||||||||||

| Description |

March 31, 2016 |

Quoted Prices in Active Markets for Identical Assets (Level 1) |

Significant Other Observable Inputs (Level 2) |

Significant Unobservable Inputs (Level 3) |

||||||||||||

| Derivative Asset—current |

$ | 463 | $ | — | $ | 463 | $ | — | ||||||||

| Derivative Asset—noncurrent |

950 | — | 950 | — | ||||||||||||

| Derivative Liability—current |

(2,258 | ) | — | (2,258 | ) | — | ||||||||||

| Derivative Liability—noncurrent |

(3,172 | ) | — | (3,172 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | (4,017 | ) | $ | — | $ | (4,017 | ) | $ | — | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Fair Value Measurements at December 31, 2015 |

||||||||||||||||

| Description |

December 31, 2015 |

Quoted Prices in Active Markets for Identical Assets (Level 1) |

Significant Other Observable Inputs (Level 2) |

Significant Unobservable Inputs (Level 3) |

||||||||||||

| Derivative Asset—current |

$ | 388 | $ | — | $ | 388 | $ | — | ||||||||

| Derivative Asset—noncurrent |

368 | — | 368 | — | ||||||||||||

| Derivative Liability—current |

(2,098 | ) | — | (2,098 | ) | — | ||||||||||

| Derivative Liability—noncurrent |

(1,673 | ) | — | (1,673 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | (3,015 | ) | $ | — | $ | (3,015 | ) | $ | — | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

Our policy is to manage interest expense using a mix of fixed and variable rate debt. To manage this mix effectively, we may enter into interest rate swaps in which we agree to exchange the difference between fixed and variable interest amounts calculated by reference to an agreed upon notional principal amount.

Our $150.0 million interest rate swap went into effect on December 29, 2015, at which time our interest rate was effectively 6.966% until December 31, 2018. The hedge instrument will be 100% effective and as such the mark to market gains or losses on this hedge will be included in accumulated other comprehensive income (loss) to the extent effective, and reclassified into interest expense over the term of the related debt instruments.

The interest rate swap derivative is classified as Level 2. Level 2 fair value is based on estimates using standard pricing models. These standard pricing models use inputs which are derived from or corroborated by observable market data such as interest rate yield curves, index forward curves, discount curves, and volatility surfaces. Counterparties to these derivative contracts are highly rated financial institutions which we believe carry only a minimal risk of nonperformance.

We have elected to present the derivative contracts on a gross basis in the Condensed Consolidated Balance Sheet included within other current and non-current assets and other current and non-current liabilities. Had we chosen to present the derivative contract on a net basis, we would have a derivative in a net liability position of $4.0 million as of March 31, 2016. We do not have any cash collateral due under such agreements.

As of March 31, 2016, we reported a loss in accumulated other comprehensive income (“AOCI”) of $4.0 million related to the interest rate swaps. In connection with periodic settlements and related reclassification of other comprehensive income, we recognized $0.5 million of net hedging losses on the interest rate swaps in the interest expense line on the Condensed Consolidated Statements of Operations during the three months ended March 31, 2016. If there are no changes in the interest rates for the next twelve months, we expect $1.8 million to be reclassified out of AOCI to interest expense. See the following “Derivatives’ Hedging Relationships” section for the impact of the interest rate swaps on our Condensed Consolidated Financial Statements.

14

Table of Contents

Derivatives’ Hedging Relationships

| Amount of after tax of gain/ (loss) recognized in Other Comprehensive Income on Derivatives (effective portion) |

Location of gain/(loss) reclassified from Accumulated Other Comprehensive Income into Income (effective portion) |

Pre-tax amount of gain/(loss) reclassified from Accumulated Other Comprehensive Income into Income (effective portion) |

||||||||||||||||

| Derivatives’ Cash Flow Hedging Relationships |

March 31, 2016 |

December 31, 2015 |

March 31, 2016 |

December 31, 2015 |

||||||||||||||

| Forward starting interest rate swap contract |

$ | (4,017 | ) | $ | (3,015 | ) | Interest Expense | $ | (461 | ) | $ | — | ||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | (4,017 | ) | $ | (3,015 | ) | $ | (461 | ) | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

As of March 31, 2016, we did not own derivative instruments that were classified as fair value hedges or trading securities. In addition, as of March 31, 2016, we did not own derivative instruments containing credit risk contingencies.

Note 14. Restructuring and Impairment Charges

Below is a summary of all the impairment and restructuring charges in the Condensed Consolidated Statement of Operations and Comprehensive Income (Loss) for the three months ended March 31, 2016 and 2015 and Condensed Consolidated Balance Sheet as of March 31, 2016 and December 31, 2015:

| March 31, 2016 |

March 31, 2015 |

|||||||

| Impairment of tangible assets |

$ | 33 | $ | — | ||||

| Restructuring charges |

1,526 | — | ||||||

|

|

|

|

|

|||||

| Restructuring and impairment charges |

$ | 1,559 | $ | — | ||||

|

|

|

|

|

|||||

| Reserve Balance at December 31, 2015 |

Charges | Paid in 2016 |

Reserve Balance at March 31, 2016 |

|||||||||||||

| Severance and other employee costs |

$ | 445 | $ | 815 | $ | (399 | ) | $ | 861 | |||||||

| Site closure and other associated cost |

1,845 | 744 | (553 | ) | 2,036 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 2,290 | $ | 1,559 | $ | (952 | ) | $ | 2,897 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

Impairments of Tangible Assets and Restructuring Activity

On November 5, 2015, we announced the closure of our Wheeling plant, which is included in the Autocam Precision Components Group. A portion of the sales and productive assets will be relocated to existing plants within the Autocam Precision Components Group. During the first quarter of 2016, we accrued a restructuring charge of approximately $0.8 million related to severance and employees, and $0.7 million in impairments related to assets and inventory at the Wheeling Plant. The closure is expected to be finalized during the first half of 2016.

15

Table of Contents

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Forward-Looking Statements

This Quarterly Report on Form 10-Q contains forward-looking statements that are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These statements may discuss goals, intentions and expectations as to future trends, plans, events, results of operations or financial condition, or state other information relating to us, based on current beliefs of management as well as assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “may,” “possible,” “potential,” “predict,” “project” or other similar words, phrases or expressions. Forward-looking statements involve a number of risks and uncertainties that are outside of our control and that may cause actual results to be materially different from such forward-looking statements. Such factors include, among others, general economic conditions and economic conditions in the industrial sector, competitive influences, risks that current customers will commence or increase captive production, risks of capacity underutilization, quality issues, availability of raw materials, currency and other risks associated with international trade, our dependence on certain major customers, the impact of acquisitions and divestitures, unanticipated difficulties integrating acquisitions, new laws and governmental regulations, and other risk factors and cautionary statements listed from time-to-time in our periodic reports filed with the Securities and Exchange Commission. We disclaim any obligation to update any such factors or to publicly announce the result of any revisions to any of the forward-looking statements included herein or therein to reflect future events or developments.

For additional information concerning such risk factors and cautionary statements, please see the section titled “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended December 31, 2015, which we filed with the SEC on March 15, 2016.

Results of Operations

Factors That May Influence Results of Operations

The following is a description of factors that have influenced our three months ended March 31, 2016 results of operations that we believe are important to provide an understanding of our business and results of operations.

2015 Acquisitions

During the year ended December 31, 2015, we completed the acquisition of two companies: Caprock and PEP. We acquired Caprock on May 29, 2015 and PEP on October 19, 2015. Because these acquisitions occurred after March 31, 2015, our results of operations for the three months ended March 31, 2015 do not include any of the operations of either acquisition.

In an effort to enhance the comparability of the current and prior year periods, we have aggregated into “acquisitions” within each financial line item comparison below for the three months ended March 31, 2016, the impacts of the acquisitions completed in 2015 that were not included in the comparative prior year period. The remaining changes relate to the legacy NN businesses. For more information about the 2015 acquisitions including background on the acquired companies, the purchase price allocations and pro forma information, as required, please refer to Note 2 of the Notes to Consolidated Financial Statements included in our Annual Report on Form 10-K for the year ended December 31, 2015 which we filed with the SEC on March 15, 2016 and Note 2 of the Notes to Condensed Consolidated Financial Statements included in this Quarterly Report on Form 10-Q.

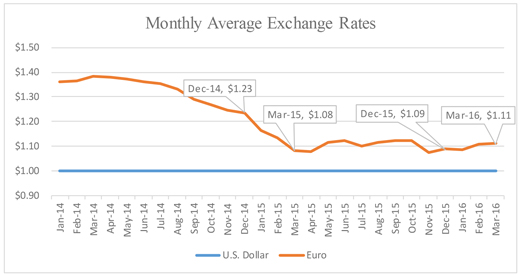

Devaluation of the Euro and Brazilian Real against the U.S. Dollar

The euro devalued against the U.S. dollar beginning in the latter part of the third quarter of 2014 and accelerated during the fourth quarter of 2014 and into the first quarter of 2015. During the three months ended March 31, 2016, the exchange rate from euro to U.S. dollar slightly increased 2%, compared to a 12% decline in value for the same period in 2015.

16

Table of Contents

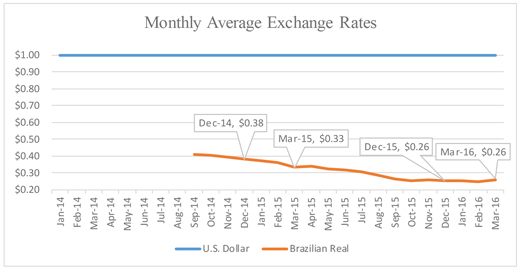

Additionally, the devaluation of the Brazilian real had an impact in comparing Autocam’s sales. During the three months ended March 31, 2016, the exchange rate from the Brazilian real to U.S. dollar remained relatively flat, compared to a 13% decline in value for the same period in 2015.

The euro and real translation impact, and the translation impact of other currencies, is highlighted below as “foreign exchange effects”.

17

Table of Contents

OVERALL RESULTS

Three Months Ended March 31, 2016 Compared to the Three Months Ended March 31, 2015

| Consolidated NN, Inc. Three Months ended March 31, |

||||||||||||||||

| 2016 | 2015 | Change | ||||||||||||||

| Net sales |

$ | 212,226 | $ | 163,746 | $ | 48,480 | ||||||||||

| Acquisitions |

57,825 | |||||||||||||||

| Foreign exchange effects |

(3,727 | ) | ||||||||||||||

| Sale of a plant |

(2,263 | ) | ||||||||||||||

| Volume |

797 | |||||||||||||||

| Price/material inflation pass - through/mix |

(4,152 | ) | ||||||||||||||

| Cost of products sold (exclusive of depreciation and amortization shown separately below) |

159,754 | 129,317 | 30,437 | |||||||||||||

| Acquisitions |

37,935 | |||||||||||||||

| Foreign exchange effects |

(3,047 | ) | ||||||||||||||

| Cost reduction projects and other cost changes |

(5,486 | ) | ||||||||||||||

| Volume |

517 | |||||||||||||||

| Mix/other |

518 | |||||||||||||||

| Selling, general and administrative |

20,712 | 12,001 | 8,711 | |||||||||||||

| Acquisitions |

5,519 | |||||||||||||||

| Foreign exchange effects |

(325 | ) | ||||||||||||||

| Infrastructure and staffing costs |

3,517 | |||||||||||||||

| Depreciation and amortization |

17,348 | 8,494 | 8,854 | |||||||||||||

| Acquisitions |

8,698 | |||||||||||||||

| Foreign exchange effects |

(324 | ) | ||||||||||||||

| Increase in expense |

480 | |||||||||||||||

| Restructuring and impairment charges |

2,538 | — | 2,538 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Income from operations |

11,874 | 13,934 | (2,060 | ) | ||||||||||||

| Interest expense |

16,422 | 5,938 | 10,484 | |||||||||||||

| Other expense, net |

(1,129 | ) | 1,400 | (2,529 | ) | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before provision (benefit) for income taxes and share of net income from joint venture |

(3,419 | ) | 6,596 | (10,015 | ) | |||||||||||

| Provision (benefit) for income taxes |

(720 | ) | 1,456 | (2,176 | ) | |||||||||||

| Share of net income from joint venture |

1,400 | 861 | 539 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Net (loss) income |

$ | (1,299 | ) | $ | 6,001 | $ | (7,300 | ) | ||||||||

|

|

|

|

|

|

|

|||||||||||

Net Sales. Net sales increased during the first quarter of 2016 from the first quarter of 2015 due to sales from the acquired companies. The first quarter of 2016 included the net sales of the PEP and Caprock acquisitions, each of which closed after the first quarter of 2015. Partially offsetting these increases was the impact of devaluation of the euro and other currency denominated sales, as discussed above. Additionally, we had lower sales prices and changes in product mix, offset by an increase in volumes.

Cost of Products Sold (exclusive of depreciation and amortization shown separately below). Cost of products sold was primarily impacted by the addition of production costs from the companies acquired 2015, as discussed above. Partially offsetting these increases was the impact of the devaluation of the euro and other currency denominated costs, as discussed above. Additionally, we incurred incremental integration and process enhancement costs.

Selling, General and Administrative. The majority of the increase during 2016 was due to the selling, general and administrative costs carried over from the companies acquired in 2015. Additional administrative costs were incurred related to our infrastructure, including staffing and related costs.

Depreciation and amortization. The increase in 2016 was due to depreciation and amortization from the acquisitions in 2015. This additional depreciation and amortization includes the related step-ups of certain property, plant and equipment to fair value and the addition of intangible assets principally for customer relationships and trade names related to the purchase price allocation of the new acquisitions.

Interest expense. Interest expense increased $10.5 million due to higher overall debts level in the first quarter of 2016 and related amortization of debt issuance costs.

18

Table of Contents

| Three Months Ended March 31, | ||||||||

| Source |

2016 | 2015 | ||||||

| Interest on debt |

$ | 15,106 | $ | 5,178 | ||||

| Interest rate swaps settlements |

461 | — | ||||||

| Amortization of debt issuance costs |

939 | 580 | ||||||

| Capital lease interest |

283 | 516 | ||||||

| Capitalized interest (1) |

(367 | ) | (336 | ) | ||||

|

|

|

|

|

|||||

| Total interest expense |

$ | 16,422 | $ | 5,938 | ||||

|

|

|

|

|

|||||

| (1) | Capitalized interest primarily relates to the construction efforts on the various plants. |

RESULTS BY SEGMENT

PRECISION BEARING COMPONENTS GROUP

| Three Months ended March 31, | ||||||||||||||||

| 2016 | 2015 | Change | ||||||||||||||

| Net sales |

$ | 64,745 | $ | 73,236 | $ | (8,491 | ) | |||||||||

| Foreign exchange effects |

(1,357 | ) | ||||||||||||||

| Product mix |

(1,170 | ) | ||||||||||||||

| Volume |

(4,447 | ) | ||||||||||||||

| Other |

(1,517 | ) | ||||||||||||||

| Income from operations |

$ | 6,326 | $ | 9,089 | $ | (2,763 | ) | |||||||||

|

|

|

|

|

|

|

|||||||||||

Net sales decreased during the first quarter of 2016 from the first quarter of 2015 principally due to lower volumes and changes to product mix. Additionally, the devaluation of the euro on euro denominated sales, as discussed above, contributed to the lower net sales. The lower volumes were primarily due to European industrial market weakness and declines in heavy truck demand. Additionally, the business was impacted by customers delaying start-ups of certain new sales programs.

The gross profit percentages remained relatively consistent for both periods and the decrease in income from operations was consistent with the decrease in net sales, except for additional restructuring charges related to personnel.

AUTOCAM PRECISION COMPONENTS GROUP

| Three Months ended March 31, | ||||||||||||||||

| 2016 | 2015 | Change | ||||||||||||||

| Net sales |

$ | 83,990 | $ | 82,622 | $ | 1,368 | ||||||||||

| Foreign exchange effects |

(2,369 | ) | ||||||||||||||

| Price |

(1,506 | ) | ||||||||||||||

| Volume |

5,244 | |||||||||||||||

| Other |

(1 | ) | ||||||||||||||

| Income from operations |

$ | 6,527 | $ | 7,718 | $ | (1,191 | ) | |||||||||

|

|

|

|

|

|

|

|||||||||||

The increased net sales in the first quarter of 2016 were due to increased volumes related to the demand for CAFÉ products, specifically GDI, and strong HVAC sales. The volume increase was offset by foreign exchange effects and product pricing.

Income from operations decreased primarily due to restructuring charges of $1.6 million related to our Wheeling plant closure. This decrease was partially offset by the increased net sales and consistent gross profit percentages.

19

Table of Contents

PRECISION ENGINEERED PRODUCTS GROUP

| Three Months ended March 31, | ||||||||||||||||

| 2016 | 2015 | Change | ||||||||||||||

| Net sales |

$ | 63,491 | $ | 7,888 | $ | 55,603 | ||||||||||

| Acquisitions |

57,825 | |||||||||||||||

| Sale of a plant |

(2,263 | ) | ||||||||||||||

| Other |

41 | |||||||||||||||

| Income from operations |

$ | 5,421 | $ | 213 | $ | 5,208 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

The increase in net sales and income from operations during the third quarter of 2015 was due primarily to the PEP Acquisition, offset by the sale of Delta Rubber in the fourth quarter of 2015.

Changes in Financial Condition from December 31, 2015 to March 31, 2016.

From December 31, 2015 to March 13, 2016, our total assets increased $15.1 million and our current assets increased $15.5 million. The asset balance during the first quarter of 2016 was driven by a seasonal increase in accounts receivable. Despite the increase in net sales, we held inventory levels flat with days inventory outstanding decreasing 8 days.

From December 31, 2015 to March 31, 2016, our total liabilities increased $11.6 million. The majority of the increase was due to the $9.5 million increase in short and long-term debt.

Working capital, which consists principally of accounts receivable and inventories offset by accounts payable and current maturities of long-term debt, was $154.2 million at March 31, 2016, compared to $146.8 million at December 31, 2015. The increase in working capital was due primarily to the increase in accounts receivable, as discussed above.

Cash provided by operations was $3.4 million in the first quarter of 2016 compared with cash used by operations of $17.4 million in the first quarter of 2015. The difference was due to increased earnings, net of noncash activity, and a smaller increase in working capital during the first quarter of 2016.

Cash used by investing activities was $8.0 million in the first quarter of 2016 compared with cash used by investing activities of $9.4 million in the first quarter of 2015. The primary difference was a capital contribution of $1.4 million to the China JV in the same period last year.

Cash provided by financing activities was $5.4 million in the first quarter of 2016 compared with cash provided by financing activities of $6.5 million in the first quarter of 2015. The difference was primarily related to using debt to fund working capital.

Liquidity and Capital Resources

Amounts outstanding under our Senior Secured Term Loan B facility, Senior Notes, and our Senior Secured Revolver facility as of March 31, 2016, were $840.1 million. As of March 31, 2016, we could borrow up to $79.4 million under our Senior Secured Revolver facility subject to certain limitations. The $79.4 million of availability is net of $2.7 million of outstanding letters of credit at March 31, 2016, which are considered as usage of the Senior Secured Revolver facility.

Our Senior Secured Term Loan B facility requires us to pay quarterly 0.25% (or $1.4 million) of the initial principal amount over the next seven years with the remaining principal amount due on the maturity date. Additionally, as long as LIBOR stays below 1.00%, we will be paying 5.75% per annum in interest. If the LIBOR exceeds 1.00%, then the rate will be the variable LIBOR rate plus an applicable margin of 4.75%. Based on the outstanding balance at March 31, 2016, the annual interest payments would have been $32.9 million.

Our Senior Notes require us to pay annual interest of 10.25% payable semi-annually in arrears on May 1 and November 1 of each year. Based on the outstanding balance at March 31, 2016, the annual interest payments would have been $25.6 million.

Our Senior Secured Revolver facility requires us to pay interest rate of LIBOR plus an applicable margin of 3.50%. Based on the outstanding balance at March 31, 2016, the annual interest payments would have been $0.6 million.

We believe that funds generated from our consolidated operations will provide sufficient cash flow to service these required debt and interest payments under these facilities.

20

Table of Contents

Our arrangements with our domestic customers typically provide that payments are due within 30 to 60 days following the date of our shipment of goods, while arrangements with foreign customers of our domestic business (other than foreign customers that have entered into an inventory management program with us) generally provide that payments are due within 60 to 120 days following the date of shipment to allow for additional transit time and customs clearance. Under the Precision Bearing Components Group’s inventory management program with certain customers, payments typically are due within 30 days after the customer uses the product. Our arrangements with European customers regarding due dates vary from 30 to 90 days following date of sale for European based customers and 60 to 120 days from customers outside of Europe to allow for additional transit time and customs clearance.

Our sales and receivables can be influenced by seasonality due to our relative percentage of European business coupled with many foreign customers slowing production during the month of August.

We invoice and receive payment from many of our customers in euros as well as other currencies. Additionally, we are party to various third party and intercompany loans, payables and receivables denominated in currencies other than the U.S. dollar. As a result of these sales, loans, payables and receivables, our foreign exchange transaction and translation risk has increased. Various strategies to manage this risk are available to management including producing and selling in local currencies and hedging programs. As of March 31, 2016, no currency hedges were in place. In addition, a strengthening of the U.S. dollar and/or euro against foreign currencies could impair our ability to compete with international competitors for foreign as well as domestic sales.

For the next twelve months, we expect to spend approximately $40 to $50 million on capital expenditures, the majority of which relate to new or expanded business. We believe that funds generated from operations and borrowings from the credit facilities will be sufficient to finance our capital expenditures and working capital needs through this period. We base this assertion on our current availability for borrowing of up to $79.4 million and our forecasted positive cash flow from operations for the next twelve months.

Seasonality and Fluctuation in Quarterly Results

Historically, our net sales in the Precision Bearing Components Group have been of a seasonal nature as a substantial portion of our sales are to European customers who have significantly slower production during the month of August.

Off-Balance Sheet Arrangements

We are not a party to any off-balance sheet arrangements that have, or are reasonably likely to have, a material current or future effect on our financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources.

Critical Accounting Policies

Our critical accounting policies, including the assumptions and judgments underlying them, are disclosed in our Annual Report on Form 10-K for the year ended December 31, 2015, which was filed with the SEC on March 15, 2016, including those policies as discussed in Note 1 to the Notes to Consolidated Financial Statements included in our Annual Report on Form 10-K for the year ended December 31, 2015, which we filed with the SEC on March 15, 2016. There have been no changes to these policies during the three month period ended March 31, 2016, except as discussed in Note 1 to the Notes to Condensed Consolidated Financial Statements.

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk |

We are exposed to changes in financial market conditions in the normal course of our business due to use of certain financial instruments as well as transacting business in various foreign currencies. To mitigate the exposure to these market risks, we have established policies, procedures and internal processes governing our management of financial market risks. We are exposed to changes in interest rates primarily as a result of our borrowing activities. At March 31, 2016, we had $18.0 million outstanding under our variable rate revolving credit facilities. See Note 6 of the Notes to Condensed Consolidated Financial Statements in this Quarterly Report on Form 10-Q. At March 31, 2016, a one-percent increase in the interest rate charged on our outstanding variable rate borrowings would result in interest expense increasing annually by approximately $0.2 million.

Our policy is to manage interest expense using a mix of fixed and variable rate debt. As such, we entered into a $150.0 million interest rate swap that went into effect on December 29, 2015 and fixed our interest rate at 6.966% for a portion of our Senior Secured Term Loan B. The nature and amount of our borrowings may vary as a result of future business requirements, market conditions and other factors.

Translation of our operating cash flows denominated in foreign currencies is impacted by changes in foreign exchange rates. Our Precision Bearing Components Group invoices and receives payment in currencies other than the U.S. dollar including the euro. Additionally, we participate in various third party and intercompany loans, payables and receivables denominated in currencies other than the U.S. dollar. To help reduce exposure to foreign currency fluctuation, we have incurred debt in euros in the past and have, from time to time, used foreign currency hedges to hedge currency exposures when these exposures meet certain discretionary levels. We did not hold a position in any foreign currency hedging instruments as of March 31, 2016.

21

Table of Contents

| Item 4. | Controls and Procedures |