00009142082020FYFALSEus-gaap:AccountingStandardsUpdate201601MemberP3YP5YP2Yus-gaap:AccountsPayableAndAccruedLiabilitiesCurrentAndNoncurrentus-gaap:AccountsPayableAndAccruedLiabilitiesCurrentAndNoncurrentus-gaap:OtherAssetsP7Y00009142082020-01-012020-12-31iso4217:USD00009142082020-06-30xbrli:shares00009142082021-01-3100009142082020-12-3100009142082019-12-31iso4217:USDxbrli:shares0000914208us-gaap:InvestmentAdviceMember2020-01-012020-12-310000914208us-gaap:InvestmentAdviceMember2019-01-012019-12-310000914208us-gaap:InvestmentAdviceMember2018-01-012018-12-310000914208us-gaap:DistributionAndShareholderServiceMember2020-01-012020-12-310000914208us-gaap:DistributionAndShareholderServiceMember2019-01-012019-12-310000914208us-gaap:DistributionAndShareholderServiceMember2018-01-012018-12-310000914208us-gaap:InvestmentPerformanceMember2020-01-012020-12-310000914208us-gaap:InvestmentPerformanceMember2019-01-012019-12-310000914208us-gaap:InvestmentPerformanceMember2018-01-012018-12-310000914208us-gaap:FinancialServiceOtherMember2020-01-012020-12-310000914208us-gaap:FinancialServiceOtherMember2019-01-012019-12-310000914208us-gaap:FinancialServiceOtherMember2018-01-012018-12-3100009142082019-01-012019-12-3100009142082018-01-012018-12-3100009142082018-12-3100009142082017-12-310000914208us-gaap:PreferredStockMember2019-12-310000914208us-gaap:CommonStockMember2019-12-310000914208us-gaap:AdditionalPaidInCapitalMember2019-12-310000914208us-gaap:TreasuryStockMember2019-12-310000914208us-gaap:RetainedEarningsMember2019-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310000914208us-gaap:ParentMember2019-12-310000914208us-gaap:NoncontrollingInterestMember2019-12-310000914208us-gaap:RetainedEarningsMember2020-01-012020-12-310000914208us-gaap:ParentMember2020-01-012020-12-310000914208us-gaap:NoncontrollingInterestMember2020-01-012020-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310000914208us-gaap:PreferredStockMember2020-01-012020-12-310000914208us-gaap:CommonStockMember2020-01-012020-12-310000914208us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310000914208us-gaap:TreasuryStockMember2020-01-012020-12-310000914208us-gaap:PreferredStockMember2020-12-310000914208us-gaap:CommonStockMember2020-12-310000914208us-gaap:AdditionalPaidInCapitalMember2020-12-310000914208us-gaap:TreasuryStockMember2020-12-310000914208us-gaap:RetainedEarningsMember2020-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310000914208us-gaap:ParentMember2020-12-310000914208us-gaap:NoncontrollingInterestMember2020-12-310000914208us-gaap:PreferredStockMember2018-12-310000914208us-gaap:CommonStockMember2018-12-310000914208us-gaap:AdditionalPaidInCapitalMember2018-12-310000914208us-gaap:TreasuryStockMember2018-12-310000914208us-gaap:RetainedEarningsMember2018-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-310000914208us-gaap:ParentMember2018-12-310000914208us-gaap:NoncontrollingInterestMember2018-12-310000914208us-gaap:RetainedEarningsMember2019-01-012019-12-310000914208us-gaap:ParentMember2019-01-012019-12-310000914208us-gaap:NoncontrollingInterestMember2019-01-012019-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310000914208us-gaap:PreferredStockMember2019-01-012019-12-310000914208us-gaap:CommonStockMember2019-01-012019-12-310000914208us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310000914208us-gaap:TreasuryStockMember2019-01-012019-12-310000914208us-gaap:CommonStockMember2017-12-310000914208us-gaap:AdditionalPaidInCapitalMember2017-12-310000914208us-gaap:TreasuryStockMember2017-12-310000914208us-gaap:RetainedEarningsMember2017-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMember2017-12-310000914208us-gaap:ParentMember2017-12-310000914208us-gaap:NoncontrollingInterestMember2017-12-3100009142082017-01-012017-12-310000914208us-gaap:RetainedEarningsMembersrt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2017-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMembersrt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2017-12-310000914208srt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2017-12-310000914208us-gaap:CommonStockMembersrt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMember2017-12-310000914208srt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMemberus-gaap:AdditionalPaidInCapitalMember2017-12-310000914208us-gaap:TreasuryStockMembersrt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMember2017-12-310000914208srt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMemberus-gaap:RetainedEarningsMember2017-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMembersrt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMember2017-12-310000914208srt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMemberus-gaap:ParentMember2017-12-310000914208us-gaap:NoncontrollingInterestMembersrt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMember2017-12-310000914208srt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMember2017-12-310000914208us-gaap:RetainedEarningsMember2018-01-012018-12-310000914208us-gaap:ParentMember2018-01-012018-12-310000914208us-gaap:NoncontrollingInterestMember2018-01-012018-12-310000914208us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-01-012018-12-310000914208us-gaap:AdditionalPaidInCapitalMember2018-01-012018-12-310000914208us-gaap:TreasuryStockMember2018-01-012018-12-310000914208srt:MinimumMember2020-01-012020-12-310000914208srt:MaximumMember2020-01-012020-12-31xbrli:pure0000914208us-gaap:BuildingMember2020-01-012020-12-310000914208us-gaap:SoftwareDevelopmentMembersrt:MinimumMember2020-01-012020-12-310000914208us-gaap:SoftwareDevelopmentMembersrt:MaximumMember2020-01-012020-12-31ivz:reporting_unit0000914208ivz:OppenheimerFundsMember2020-12-310000914208ivz:OppenheimerFundsMember2019-05-242020-12-310000914208us-gaap:CommonStockMemberivz:OppenheimerFundsMember2019-05-242020-12-310000914208us-gaap:PreferredStockMemberivz:OppenheimerFundsMember2019-05-242020-12-310000914208ivz:EmployeeSharebasedAwardsMemberivz:OppenheimerFundsMember2019-05-242020-12-310000914208ivz:ManagementContractsMemberivz:OppenheimerFundsMember2019-01-012019-12-310000914208ivz:ManagementContractsMemberivz:OppenheimerFundsMember2019-05-242020-12-310000914208us-gaap:TradeNamesMemberivz:OppenheimerFundsMember2019-05-242020-12-310000914208us-gaap:TradeNamesMemberivz:OppenheimerFundsMember2019-01-012019-12-310000914208ivz:OppenheimerFundsMemberus-gaap:TradeNamesMember2019-05-242020-12-310000914208ivz:OppenheimerFundsMember2020-03-310000914208ivz:OppenheimerFundsMember2020-01-012020-03-310000914208us-gaap:CommonStockMemberivz:OppenheimerFundsMemberivz:MassMutualMember2019-05-242019-05-240000914208us-gaap:CommonStockMemberivz:OppenheimerFundsMemberivz:MassMutualMember2019-05-240000914208ivz:OthersMemberus-gaap:CommonStockMemberivz:OppenheimerFundsMember2019-05-242019-05-240000914208ivz:OthersMemberus-gaap:CommonStockMemberivz:OppenheimerFundsMember2019-05-240000914208us-gaap:PreferredStockMemberivz:OppenheimerFundsMember2019-05-240000914208ivz:OppenheimerFundsMember2020-01-012020-12-310000914208ivz:OppenheimerFundsMember2019-01-012019-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310000914208us-gaap:MoneyMarketFundsMember2020-12-310000914208us-gaap:FairValueInputsLevel1Memberus-gaap:MoneyMarketFundsMember2020-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:MoneyMarketFundsMember2020-12-310000914208us-gaap:MoneyMarketFundsMemberus-gaap:FairValueInputsLevel3Member2020-12-310000914208ivz:SeedMoneyMember2020-12-310000914208ivz:SeedMoneyMemberus-gaap:FairValueInputsLevel1Member2020-12-310000914208us-gaap:FairValueInputsLevel2Memberivz:SeedMoneyMember2020-12-310000914208ivz:SeedMoneyMemberus-gaap:FairValueInputsLevel3Member2020-12-310000914208ivz:DeferredCompensationArrangementsMember2020-12-310000914208us-gaap:FairValueInputsLevel1Memberivz:DeferredCompensationArrangementsMember2020-12-310000914208us-gaap:FairValueInputsLevel2Memberivz:DeferredCompensationArrangementsMember2020-12-310000914208us-gaap:FairValueInputsLevel3Memberivz:DeferredCompensationArrangementsMember2020-12-310000914208us-gaap:EquitySecuritiesMember2020-12-310000914208us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel1Member2020-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:EquitySecuritiesMember2020-12-310000914208us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Member2020-12-310000914208us-gaap:FairValueInputsLevel1Member2020-12-310000914208us-gaap:FairValueInputsLevel2Member2020-12-310000914208us-gaap:FairValueInputsLevel3Member2020-12-310000914208us-gaap:LiabilityMember2020-12-310000914208us-gaap:LiabilityMemberus-gaap:FairValueInputsLevel1Member2020-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:LiabilityMember2020-12-310000914208us-gaap:LiabilityMemberus-gaap:FairValueInputsLevel3Member2020-12-310000914208us-gaap:MoneyMarketFundsMember2019-12-310000914208us-gaap:FairValueInputsLevel1Memberus-gaap:MoneyMarketFundsMember2019-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:MoneyMarketFundsMember2019-12-310000914208us-gaap:MoneyMarketFundsMemberus-gaap:FairValueInputsLevel3Member2019-12-310000914208ivz:SeedMoneyMember2019-12-310000914208ivz:SeedMoneyMemberus-gaap:FairValueInputsLevel1Member2019-12-310000914208us-gaap:FairValueInputsLevel2Memberivz:SeedMoneyMember2019-12-310000914208ivz:SeedMoneyMemberus-gaap:FairValueInputsLevel3Member2019-12-310000914208ivz:DeferredCompensationArrangementsMember2019-12-310000914208us-gaap:FairValueInputsLevel1Memberivz:DeferredCompensationArrangementsMember2019-12-310000914208us-gaap:FairValueInputsLevel2Memberivz:DeferredCompensationArrangementsMember2019-12-310000914208us-gaap:FairValueInputsLevel3Memberivz:DeferredCompensationArrangementsMember2019-12-310000914208us-gaap:EquitySecuritiesMember2019-12-310000914208us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel1Member2019-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:EquitySecuritiesMember2019-12-310000914208us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Member2019-12-310000914208us-gaap:FairValueInputsLevel1Member2019-12-310000914208us-gaap:FairValueInputsLevel2Member2019-12-310000914208us-gaap:FairValueInputsLevel3Member2019-12-310000914208us-gaap:LiabilityMember2019-12-310000914208us-gaap:LiabilityMemberus-gaap:FairValueInputsLevel1Member2019-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:LiabilityMember2019-12-310000914208us-gaap:LiabilityMemberus-gaap:FairValueInputsLevel3Member2019-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMember2020-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMember2019-12-310000914208us-gaap:ForeignExchangeOptionMemberus-gaap:DesignatedAsHedgingInstrumentMember2020-01-012020-12-310000914208us-gaap:ForeignExchangeOptionMemberus-gaap:DesignatedAsHedgingInstrumentMember2019-01-012019-12-310000914208us-gaap:TotalReturnSwapMemberus-gaap:DesignatedAsHedgingInstrumentMember2020-12-310000914208us-gaap:TotalReturnSwapMemberus-gaap:DesignatedAsHedgingInstrumentMember2020-01-012020-12-310000914208us-gaap:TotalReturnSwapMemberus-gaap:DesignatedAsHedgingInstrumentMember2019-01-012019-12-310000914208us-gaap:TotalReturnSwapMemberus-gaap:NondesignatedMember2019-12-310000914208us-gaap:TotalReturnSwapMemberus-gaap:NondesignatedMember2020-01-012020-12-310000914208us-gaap:TotalReturnSwapMemberus-gaap:NondesignatedMember2019-01-012019-12-310000914208ivz:DeutscheBankAcquisitionMember2020-12-310000914208us-gaap:MeasurementInputLongTermRevenueGrowthRateMemberivz:OppenheimerFundsMember2020-12-310000914208us-gaap:MeasurementInputDiscountRateMemberivz:OppenheimerFundsMember2020-12-310000914208us-gaap:LiabilityMemberus-gaap:FairValueInputsLevel3Member2018-12-310000914208us-gaap:LiabilityMemberus-gaap:FairValueInputsLevel3Member2020-01-012020-12-310000914208us-gaap:LiabilityMemberus-gaap:FairValueInputsLevel3Member2019-01-012019-12-310000914208ivz:SeedMoneyMember2020-12-310000914208ivz:SeedMoneyMember2019-12-310000914208ivz:DeferredCompensationArrangementsMember2020-12-310000914208ivz:DeferredCompensationArrangementsMember2019-12-310000914208us-gaap:ShortTermInvestmentsMember2020-01-012020-12-310000914208us-gaap:ShortTermInvestmentsMember2019-01-012019-12-310000914208ivz:HuanengInvescoWLRInvestmentConsultingCompanyLimitedMembercountry:CN2020-12-310000914208ivz:InvescoGreatWalLfundManagementCompanyLimitedMembercountry:CN2020-12-310000914208country:PLivz:PocztylionArkaMember2020-12-310000914208country:DEivz:VvImmobilienVerwaltungsUndBeteiligungsGmbhMember2020-12-310000914208country:DEivz:HvhImmobilienUndBeteiligungsGmbhMember2020-12-310000914208us-gaap:TechnologyEquipmentMember2020-12-310000914208us-gaap:TechnologyEquipmentMember2019-12-310000914208us-gaap:ComputerSoftwareIntangibleAssetMember2020-12-310000914208us-gaap:ComputerSoftwareIntangibleAssetMember2019-12-310000914208us-gaap:LandAndBuildingMember2020-12-310000914208us-gaap:LandAndBuildingMember2019-12-310000914208us-gaap:LeaseholdImprovementsMember2020-12-310000914208us-gaap:LeaseholdImprovementsMember2019-12-310000914208us-gaap:ConstructionInProgressMember2020-12-310000914208us-gaap:ConstructionInProgressMember2019-12-310000914208us-gaap:CustomerContractsMember2020-12-310000914208us-gaap:CustomerContractsMember2020-12-310000914208us-gaap:DevelopedTechnologyRightsMember2020-12-310000914208us-gaap:OtherIntangibleAssetsMember2020-12-310000914208us-gaap:CustomerContractsMember2019-12-310000914208us-gaap:CustomerContractsMember2019-12-310000914208us-gaap:DevelopedTechnologyRightsMember2019-12-310000914208us-gaap:OtherIntangibleAssetsMember2019-12-310000914208ivz:OppenheimerFundsAcquisitionMember2020-01-012020-12-310000914208ivz:OppenheimerFundsAcquisitionMember2019-01-012019-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:LineOfCreditMember2020-12-310000914208us-gaap:LineOfCreditMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:LineOfCreditMember2019-12-310000914208us-gaap:LineOfCreditMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:DueNovember302022Memberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMemberivz:DueNovember302022Memberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:DueNovember302022Memberus-gaap:UnsecuredDebtMember2019-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMemberivz:DueNovember302022Memberus-gaap:UnsecuredDebtMember2019-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:SeniorNotesDueJanuary302024Memberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMemberivz:SeniorNotesDueJanuary302024Memberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:SeniorNotesDueJanuary302024Memberus-gaap:UnsecuredDebtMember2019-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMemberivz:SeniorNotesDueJanuary302024Memberus-gaap:UnsecuredDebtMember2019-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:SeniorNotesDueJanuary152026MemberMemberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMemberivz:SeniorNotesDueJanuary152026MemberMemberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:SeniorNotesDueJanuary152026MemberMemberus-gaap:UnsecuredDebtMember2019-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMemberivz:SeniorNotesDueJanuary152026MemberMemberus-gaap:UnsecuredDebtMember2019-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:SeniorNotesDueNovember302043Memberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMemberivz:SeniorNotesDueNovember302043Memberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:SeniorNotesDueNovember302043Memberus-gaap:UnsecuredDebtMember2019-12-310000914208us-gaap:EstimateOfFairValueFairValueDisclosureMemberivz:SeniorNotesDueNovember302043Memberus-gaap:UnsecuredDebtMember2019-12-310000914208us-gaap:CarryingReportedAmountFairValueDisclosureMemberivz:CreditFacilityandUnsecuredSeniorNotesDueAugustandNovember2022Memberus-gaap:UnsecuredDebtMember2020-12-310000914208us-gaap:LineOfCreditMemberus-gaap:PrimeRateMember2020-01-012020-12-310000914208us-gaap:LineOfCreditMemberus-gaap:LondonInterbankOfferedRateLIBORMember2020-01-012020-12-310000914208us-gaap:LineOfCreditMemberus-gaap:BaseRateMember2020-01-012020-12-310000914208us-gaap:LineOfCreditMember2020-01-012020-12-310000914208us-gaap:LetterOfCreditMember2020-12-310000914208us-gaap:LetterOfCreditMember2020-01-012020-12-3100009142082019-05-242019-05-240000914208us-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnMay13th2019Member2020-12-310000914208us-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnMay13th2019Member2019-12-310000914208us-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnMay13th2019Member2020-01-012020-12-310000914208us-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnMay13th2019Member2019-01-012019-12-310000914208us-gaap:SubsequentEventMemberus-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnMay13th2019Member2021-01-042021-01-040000914208us-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnJuly2nd2019Member2019-12-310000914208us-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnJuly2nd2019Member2020-12-310000914208us-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnJuly2nd2019Member2020-01-012020-12-310000914208us-gaap:ForwardContractsMemberivz:ForwardContract200MillionEnteredOnJuly2nd2019Member2019-01-012019-12-310000914208ivz:ForwardContract100MillionEnteredOnAugust27th2019Memberus-gaap:ForwardContractsMember2019-12-310000914208ivz:ForwardContract100MillionEnteredOnAugust27th2019Memberus-gaap:ForwardContractsMember2020-12-310000914208ivz:ForwardContract100MillionEnteredOnAugust27th2019Memberus-gaap:ForwardContractsMember2020-01-012020-12-310000914208ivz:ForwardContract100MillionEnteredOnAugust27th2019Memberus-gaap:ForwardContractsMember2019-01-012019-12-310000914208us-gaap:ForwardContractsMember2020-01-012020-12-310000914208us-gaap:ForwardContractsMember2020-12-310000914208us-gaap:ForwardContractsMember2019-01-012019-12-310000914208us-gaap:ForwardContractsMember2019-12-310000914208us-gaap:ForwardContractsMember2020-01-012020-03-310000914208us-gaap:ForwardContractsMember2020-03-310000914208us-gaap:AccumulatedTranslationAdjustmentMember2020-01-012020-12-310000914208us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-01-012020-12-310000914208ivz:EquityMethodInvestmentAdjustmentMember2020-01-012020-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2020-01-012020-12-310000914208us-gaap:AccumulatedTranslationAdjustmentMember2019-12-310000914208us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-12-310000914208ivz:EquityMethodInvestmentAdjustmentMember2019-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2019-12-310000914208us-gaap:AccumulatedTranslationAdjustmentMember2020-12-310000914208us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-12-310000914208ivz:EquityMethodInvestmentAdjustmentMember2020-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2020-12-310000914208us-gaap:AccumulatedTranslationAdjustmentMember2019-01-012019-12-310000914208us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-01-012019-12-310000914208ivz:EquityMethodInvestmentAdjustmentMember2019-01-012019-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2019-01-012019-12-310000914208us-gaap:AccumulatedTranslationAdjustmentMember2018-12-310000914208us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2018-12-310000914208ivz:EquityMethodInvestmentAdjustmentMember2018-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2018-12-310000914208us-gaap:AccumulatedTranslationAdjustmentMember2018-01-012018-12-310000914208us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2018-01-012018-12-310000914208ivz:EquityMethodInvestmentAdjustmentMember2018-01-012018-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2018-01-012018-12-310000914208us-gaap:AccumulatedTranslationAdjustmentMember2017-12-310000914208us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2017-12-310000914208ivz:EquityMethodInvestmentAdjustmentMember2017-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2017-12-310000914208us-gaap:AccumulatedTranslationAdjustmentMembersrt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2017-12-310000914208us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMembersrt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2017-12-310000914208ivz:EquityMethodInvestmentAdjustmentMembersrt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2017-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMembersrt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2017-12-310000914208us-gaap:AccumulatedTranslationAdjustmentMembersrt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMember2017-12-310000914208srt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2017-12-310000914208srt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMemberivz:EquityMethodInvestmentAdjustmentMember2017-12-310000914208us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMembersrt:CumulativeEffectPeriodOfAdoptionAdjustedBalanceMember2017-12-31iso4217:EUR0000914208us-gaap:DesignatedAsHedgingInstrumentMember2020-12-310000914208us-gaap:DesignatedAsHedgingInstrumentMember2019-12-31ivz:award0000914208us-gaap:PerformanceSharesMemberivz:AwardDateFebruary2018Membersrt:MinimumMember2020-01-012020-12-310000914208us-gaap:PerformanceSharesMembersrt:MaximumMemberivz:AwardDateFebruary2018Member2020-01-012020-12-310000914208us-gaap:PerformanceSharesMembersrt:MinimumMemberivz:AwardDateFebruary2019Member2020-01-012020-12-310000914208us-gaap:PerformanceSharesMemberivz:AwardDateFebruary2020Membersrt:MinimumMember2020-01-012020-12-310000914208us-gaap:PerformanceSharesMembersrt:MaximumMemberivz:AwardDateFebruary2019Member2020-01-012020-12-310000914208us-gaap:PerformanceSharesMembersrt:MaximumMemberivz:AwardDateFebruary2020Member2020-01-012020-12-310000914208ivz:GlobalEquityIncentivePlan2016Member2016-05-310000914208ivz:GlobalEquityIncentivePlan2010Member2010-05-310000914208ivz:TimeVestedNYSEMember2019-12-310000914208us-gaap:PerformanceSharesMember2019-12-310000914208ivz:TimeVestedNYSEMember2018-12-310000914208us-gaap:PerformanceSharesMember2018-12-310000914208ivz:TimeVestedNYSEMember2017-12-310000914208us-gaap:PerformanceSharesMember2017-12-310000914208ivz:TimeVestedNYSEMember2020-01-012020-12-310000914208us-gaap:PerformanceSharesMember2020-01-012020-12-310000914208ivz:TimeVestedNYSEMember2019-01-012019-12-310000914208us-gaap:PerformanceSharesMember2019-01-012019-12-310000914208ivz:TimeVestedNYSEMember2018-01-012018-12-310000914208us-gaap:PerformanceSharesMember2018-01-012018-12-310000914208ivz:TimeVestedNYSEMember2020-12-310000914208us-gaap:PerformanceSharesMember2020-12-310000914208us-gaap:RestrictedStockMemberivz:OppenheimerFundsMember2019-05-242019-05-240000914208us-gaap:PensionPlansDefinedBenefitMember2020-01-012020-12-310000914208us-gaap:PensionPlansDefinedBenefitMember2019-01-012019-12-310000914208us-gaap:PensionPlansDefinedBenefitMember2018-01-012018-12-310000914208us-gaap:PensionPlansDefinedBenefitMember2020-12-310000914208us-gaap:PensionPlansDefinedBenefitMember2019-12-310000914208us-gaap:PensionPlansDefinedBenefitMember2018-12-310000914208us-gaap:DefinedBenefitPlanCashAndCashEquivalentsMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000914208ivz:FundInvestmentsMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000914208us-gaap:PensionPlansDefinedBenefitMemberus-gaap:DefinedBenefitPlanEquitySecuritiesMember2020-12-310000914208ivz:GovernmentDebtSecuritiesMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000914208ivz:GuaranteedInvestmentsContractsMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000914208us-gaap:OtherAssetsMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000914208us-gaap:DefinedBenefitPlanCashAndCashEquivalentsMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000914208ivz:FundInvestmentsMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000914208us-gaap:PensionPlansDefinedBenefitMemberus-gaap:DefinedBenefitPlanEquitySecuritiesMember2019-12-310000914208ivz:GovernmentDebtSecuritiesMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000914208ivz:GuaranteedInvestmentsContractsMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000914208us-gaap:OtherAssetsMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000914208srt:MinimumMember2020-12-310000914208srt:MaximumMember2020-12-310000914208us-gaap:EmployeeSeveranceMember2020-12-310000914208us-gaap:EmployeeSeveranceMember2020-06-300000914208us-gaap:OtherRestructuringMember2020-06-300000914208us-gaap:EmployeeSeveranceMember2020-07-012020-09-300000914208us-gaap:OtherRestructuringMember2020-07-012020-09-3000009142082020-07-012020-09-300000914208us-gaap:EmployeeSeveranceMember2020-09-300000914208us-gaap:OtherRestructuringMember2020-09-3000009142082020-09-300000914208us-gaap:EmployeeSeveranceMember2020-10-012020-12-310000914208us-gaap:OtherRestructuringMember2020-10-012020-12-3100009142082020-10-012020-12-310000914208us-gaap:OtherRestructuringMember2020-12-310000914208us-gaap:EmployeeSeveranceMember2020-01-012020-12-310000914208us-gaap:OtherRestructuringMember2020-01-012020-12-31ivz:lease_renewal_option0000914208us-gaap:OtherAssetsMember2020-12-310000914208us-gaap:StateAndLocalJurisdictionMember2020-12-310000914208us-gaap:StateAndLocalJurisdictionMember2019-12-310000914208ivz:FederalAndForeignTaxAuthorityMember2020-12-310000914208ivz:FederalAndForeignTaxAuthorityMember2019-12-310000914208country:CA2020-01-012020-12-310000914208us-gaap:TaxYear2020Member2020-12-310000914208us-gaap:TaxYear2019Member2019-12-310000914208us-gaap:TaxYear2018Member2018-12-310000914208us-gaap:PerformanceSharesMember2020-01-012020-12-310000914208us-gaap:PerformanceSharesMember2019-01-012019-12-310000914208ivz:TimeVestedNYSEMember2019-01-012019-12-310000914208ivz:TimeVestedNYSEMember2020-01-012020-12-310000914208ivz:TimeVestedNYSEMember2018-01-012018-12-31ivz:segment0000914208srt:AmericasMember2020-01-012020-12-310000914208country:GB2020-01-012020-12-310000914208ivz:EMEAExcludingUnitedKingdomMember2020-01-012020-12-310000914208srt:AsiaMember2020-01-012020-12-310000914208srt:AmericasMember2020-12-310000914208country:GB2020-12-310000914208ivz:EMEAExcludingUnitedKingdomMember2020-12-310000914208srt:AsiaMember2020-12-310000914208srt:AmericasMember2019-01-012019-12-310000914208country:GB2019-01-012019-12-310000914208ivz:EMEAExcludingUnitedKingdomMember2019-01-012019-12-310000914208srt:AsiaMember2019-01-012019-12-310000914208srt:AmericasMember2019-12-310000914208country:GB2019-12-310000914208ivz:EMEAExcludingUnitedKingdomMember2019-12-310000914208srt:AsiaMember2019-12-310000914208srt:AmericasMember2018-01-012018-12-310000914208country:GB2018-01-012018-12-310000914208ivz:EMEAExcludingUnitedKingdomMember2018-01-012018-12-310000914208srt:AsiaMember2018-01-012018-12-310000914208srt:AmericasMember2018-12-310000914208country:GB2018-12-310000914208ivz:EMEAExcludingUnitedKingdomMember2018-12-310000914208srt:AsiaMember2018-12-3100009142082018-10-1800009142082018-10-182018-10-180000914208ivz:SeedCapitalSubjecttoMassmutualRedemptionAgreementMember2020-12-310000914208ivz:OppenheimerFundsAcquisitionrelatedMatterMember2020-12-310000914208ivz:OppenheimerFundsAcquisitionrelatedMatterMember2020-01-012020-12-31ivz:fund0000914208ivz:RebalancingCorrectionMatterMember2020-04-012020-06-300000914208ivz:RebalancingCorrectionMatterMember2020-01-012020-12-310000914208us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2020-01-012020-12-310000914208us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2019-01-012019-12-310000914208us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2018-01-012018-12-310000914208us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2020-12-310000914208us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMember2019-12-31ivz:entity0000914208us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2020-12-310000914208ivz:VotingRightsEntityPrimaryBeneficiaryMember2020-12-310000914208us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2019-12-310000914208ivz:VotingRightsEntityPrimaryBeneficiaryMember2019-12-310000914208ivz:VotingRightsEntityNotPrimaryBeneficiaryMember2020-12-310000914208ivz:VotingRightsEntityNotPrimaryBeneficiaryMember2019-12-310000914208us-gaap:BankLoanObligationsMember2020-12-310000914208us-gaap:FairValueInputsLevel1Memberus-gaap:BankLoanObligationsMember2020-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:BankLoanObligationsMember2020-12-310000914208us-gaap:FairValueInputsLevel3Memberus-gaap:BankLoanObligationsMember2020-12-310000914208us-gaap:BankLoanObligationsMemberus-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2020-12-310000914208us-gaap:CorporateBondSecuritiesMember2020-12-310000914208us-gaap:FairValueInputsLevel1Memberus-gaap:CorporateBondSecuritiesMember2020-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateBondSecuritiesMember2020-12-310000914208us-gaap:CorporateBondSecuritiesMemberus-gaap:FairValueInputsLevel3Member2020-12-310000914208us-gaap:CorporateBondSecuritiesMemberus-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2020-12-310000914208us-gaap:EquitySecuritiesMember2020-12-310000914208us-gaap:FairValueInputsLevel1Memberus-gaap:EquitySecuritiesMember2020-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:EquitySecuritiesMember2020-12-310000914208us-gaap:FairValueInputsLevel3Memberus-gaap:EquitySecuritiesMember2020-12-310000914208us-gaap:PortionAtOtherThanFairValueFairValueDisclosureMemberus-gaap:EquitySecuritiesMember2020-12-310000914208ivz:EquityandFixedincomeMutualFundsMember2020-12-310000914208ivz:EquityandFixedincomeMutualFundsMemberus-gaap:FairValueInputsLevel1Member2020-12-310000914208ivz:EquityandFixedincomeMutualFundsMemberus-gaap:FairValueInputsLevel2Member2020-12-310000914208ivz:EquityandFixedincomeMutualFundsMemberus-gaap:FairValueInputsLevel3Member2020-12-310000914208ivz:EquityandFixedincomeMutualFundsMemberus-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2020-12-310000914208us-gaap:PrivateEquityFundsMember2020-12-310000914208us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel1Member2020-12-310000914208us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel2Member2020-12-310000914208us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel3Member2020-12-310000914208us-gaap:PrivateEquityFundsMemberus-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2020-12-310000914208us-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2020-12-310000914208us-gaap:BankLoanObligationsMember2019-12-310000914208us-gaap:FairValueInputsLevel1Memberus-gaap:BankLoanObligationsMember2019-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:BankLoanObligationsMember2019-12-310000914208us-gaap:FairValueInputsLevel3Memberus-gaap:BankLoanObligationsMember2019-12-310000914208us-gaap:BankLoanObligationsMemberus-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2019-12-310000914208us-gaap:CorporateBondSecuritiesMember2019-12-310000914208us-gaap:FairValueInputsLevel1Memberus-gaap:CorporateBondSecuritiesMember2019-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateBondSecuritiesMember2019-12-310000914208us-gaap:CorporateBondSecuritiesMemberus-gaap:FairValueInputsLevel3Member2019-12-310000914208us-gaap:CorporateBondSecuritiesMemberus-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2019-12-310000914208us-gaap:EquitySecuritiesMember2019-12-310000914208us-gaap:FairValueInputsLevel1Memberus-gaap:EquitySecuritiesMember2019-12-310000914208us-gaap:FairValueInputsLevel2Memberus-gaap:EquitySecuritiesMember2019-12-310000914208us-gaap:FairValueInputsLevel3Memberus-gaap:EquitySecuritiesMember2019-12-310000914208us-gaap:PortionAtOtherThanFairValueFairValueDisclosureMemberus-gaap:EquitySecuritiesMember2019-12-310000914208ivz:EquityandFixedincomeMutualFundsMember2019-12-310000914208ivz:EquityandFixedincomeMutualFundsMemberus-gaap:FairValueInputsLevel1Member2019-12-310000914208ivz:EquityandFixedincomeMutualFundsMemberus-gaap:FairValueInputsLevel2Member2019-12-310000914208ivz:EquityandFixedincomeMutualFundsMemberus-gaap:FairValueInputsLevel3Member2019-12-310000914208ivz:EquityandFixedincomeMutualFundsMemberus-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2019-12-310000914208us-gaap:PrivateEquityFundsMember2019-12-310000914208us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel1Member2019-12-310000914208us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel2Member2019-12-310000914208us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel3Member2019-12-310000914208us-gaap:PrivateEquityFundsMemberus-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2019-12-310000914208us-gaap:PortionAtOtherThanFairValueFairValueDisclosureMember2019-12-310000914208us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:FairValueInputsLevel3Member2020-01-012020-12-310000914208us-gaap:VariableInterestEntityNotPrimaryBeneficiaryMemberus-gaap:FairValueInputsLevel3Member2019-01-012019-12-310000914208ivz:SeniorSecuredBankLoansAndBondsMember2020-12-310000914208ivz:SeniorSecuredBankLoansAndBondsMember2019-12-310000914208us-gaap:PrivateEquityFundsMember2020-12-310000914208us-gaap:PrivateEquityFundsMember2020-01-012020-12-310000914208us-gaap:PrivateEquityFundsMember2019-12-310000914208us-gaap:PrivateEquityFundsMember2019-01-012019-12-310000914208us-gaap:PreferredStockMemberivz:MassMutualMemberivz:OppenheimerFundsMember2020-12-310000914208us-gaap:PreferredStockMemberivz:OppenheimerFundsMember2020-01-012020-12-310000914208srt:AffiliatedEntityMemberus-gaap:InvestmentAdviceMember2020-01-012020-12-310000914208srt:AffiliatedEntityMemberus-gaap:InvestmentAdviceMember2019-01-012019-12-310000914208srt:AffiliatedEntityMemberus-gaap:InvestmentAdviceMember2018-01-012018-12-310000914208srt:AffiliatedEntityMemberus-gaap:DistributionAndShareholderServiceMember2020-01-012020-12-310000914208srt:AffiliatedEntityMemberus-gaap:DistributionAndShareholderServiceMember2019-01-012019-12-310000914208srt:AffiliatedEntityMemberus-gaap:DistributionAndShareholderServiceMember2018-01-012018-12-310000914208srt:AffiliatedEntityMemberus-gaap:InvestmentPerformanceMember2020-01-012020-12-310000914208srt:AffiliatedEntityMemberus-gaap:InvestmentPerformanceMember2019-01-012019-12-310000914208srt:AffiliatedEntityMemberus-gaap:InvestmentPerformanceMember2018-01-012018-12-310000914208srt:AffiliatedEntityMemberus-gaap:FinancialServiceOtherMember2020-01-012020-12-310000914208srt:AffiliatedEntityMemberus-gaap:FinancialServiceOtherMember2019-01-012019-12-310000914208srt:AffiliatedEntityMemberus-gaap:FinancialServiceOtherMember2018-01-012018-12-310000914208srt:AffiliatedEntityMember2020-01-012020-12-310000914208srt:AffiliatedEntityMember2019-01-012019-12-310000914208srt:AffiliatedEntityMember2018-01-012018-12-310000914208srt:AffiliatedEntityMember2020-12-310000914208srt:AffiliatedEntityMember2019-12-310000914208us-gaap:SubsequentEventMember2021-01-262021-01-26

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| | | | | | | | |

| ☑ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2020

OR

| | | | | | | | |

| ☐ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-13908

Invesco Ltd.

(Exact Name of Registrant as Specified in Its Charter)

| | | | | | | | | | | | | | | | | |

| Bermuda | | 98-0557567 |

| (State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| | | | | |

| 1555 Peachtree Street, N.E., | Suite 1800, | Atlanta, | GA | | 30309 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (404) 892-0896

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common stock, $0.20 par value | IVZ | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known, seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☑ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | | | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes ☐ No ☑

At June 30, 2020, the aggregate market value of the voting stock held by non-affiliates was $4.9 billion, based on the closing price of the registrant's Common Shares, par value U.S. $0.20 per share, on the New York Stock Exchange. At January 31, 2021, the most recent practicable date, the number of Common Shares outstanding was 459,072,262.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant will incorporate by reference information required in response to Part III, Items 10-14 in its definitive Proxy Statement for its annual meeting of shareholders, to be filed with the Securities and Exchange Commission within 120 days after December 31, 2020.

TABLE OF CONTENTS

We include cross references to captions elsewhere in this Annual Report on Form 10-K, which we refer to as this “Report,” where you can find related additional information. The following table of contents tells you where to find these captions.

SPECIAL CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report, other public filings and oral and written statements by us and our management, may include statements that constitute “forward-looking statements” within the meaning of the United States securities laws. These statements are based on the beliefs and assumptions of our management and on information available to us at the time such statements are made. Forward-looking statements include information concerning future results of our operations, expenses, earnings, liquidity, cash flows and capital expenditures, industry or market conditions, assets under management, acquisitions and divestitures, debt and our ability to obtain additional financing or make payments, regulatory developments, demand for and pricing of our products, the prospects for certain legal contingencies, and other aspects of our business or general economic conditions. In addition, when used in this Report or such other documents or statements, words such as “believes,” “expects,” “anticipates,” “intends,” “plans,” “estimates,” “projects,” “forecasts,” and future or conditional verbs such as “will,” “may,” “could,” “should,” and “would,” and any other statement that necessarily depends on future events, are intended to identify forward-looking statements.

Forward-looking statements are not guarantees and they involve risks, uncertainties and assumptions. Although we make such statements based on assumptions that we believe to be reasonable, there can be no assurance that actual results will not differ materially from our expectations. In most cases, such assumptions will not be expressly stated. We caution investors not to rely unduly on any forward-looking statements.

The following important factors, and other factors described elsewhere in this Report or contained in our other filings with the U.S. Securities and Exchange Commission (SEC), among others, could cause our results to differ materially from any results described in any forward-looking statements:

•significant fluctuations in the performance of capital and credit markets worldwide;

•adverse changes in the global economy;

•the performance of our investment products;

•significant changes in net asset flows into or out of the accounts we manage or declines in market value of the assets in, or redemptions or other withdrawals from, those accounts;

•pandemics or other widespread health crises and governmental responses to the same;

•competitive pressures in the investment management business, including consolidation, which may force us to reduce fees we earn;

•any inability to adjust our expenses quickly enough to match significant deterioration in markets;

•the effect of fluctuations in interest rates, liquidity and credit markets in the U.S. or globally, including regulatory reform of benchmarks, such as LIBOR;

•our ability to acquire and integrate other companies into our operations successfully and the extent to which we can realize anticipated product sales, cost savings or synergies from such acquisitions;

•the occurrence of breaches and errors in the conduct of our business, including any failure to properly safeguard confidential and sensitive information, cyber-attacks or acts of fraud;

•our ability to attract and retain key personnel, including investment management professionals;

•limitations or restrictions on access to distribution channels for our products;

•our ability to develop, introduce and support new investment products and services;

•our ability to comply with client contractual requirements and/or investment guidelines despite preventative compliance procedures and controls;

•variations in demand for our investment products or services, including termination or non-renewal of our investment management agreements;

•harm to our reputation;

•our ability to maintain our credit ratings and access the capital markets in a timely manner;

•our debt and the limitations imposed by our credit facility;

•exchange rate fluctuations, especially as against the U.S. Dollar;

•the effect of political, economic or social instability in or involving countries in which we invest or do business (including the effect of terrorist attacks, war and other hostilities);

•the effect of failures or delays in support systems or customer service functions, and other interruptions of our operations;

•the effect of non-performance by our counterparties, third party service providers and other key vendors to fulfill their obligations;

•impairment of goodwill and other intangible assets;

•adverse results in litigation and any other regulatory or other proceedings, governmental investigations, and enforcement actions; and

•enactment of adverse federal, state or foreign legislation or changes in government policy or regulation (including accounting standards) affecting our operations, our capital requirements or the way in which our profits are taxed.

Other factors and assumptions not identified above were also involved in the derivation of these forward-looking statements, and the failure of such other assumptions to be realized may also cause actual results to differ materially from those projected. For more discussion of the risks affecting us, please refer to Item 1A, “Risk Factors.”

You should consider the areas of risk described above in connection with any forward-looking statements that may be made by us and our businesses generally. We expressly disclaim any obligation to update any of the information in this or any other public report if any forward-looking statement later turns out to be inaccurate, whether as a result of new information, future events or otherwise. For all forward-looking statements, we claim the “safe harbor” provided by Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

PART I

Item 1. Business

Introduction

Invesco Ltd. (Invesco or the company) is an independent investment management firm dedicated to delivering an investment experience that helps people get more out of life. Our comprehensive range of active, passive and alternative investment capabilities has been constructed over many years to help clients achieve their investment objectives. We draw on this comprehensive range of capabilities to provide customized solutions designed to deliver key outcomes aligned to client needs.

With more than 8,000 employees and an on-the-ground presence in over 20 countries, Invesco is well positioned to meet the needs of investors across the globe. We have specialized investment teams managing investments across a broad range of asset classes, investment styles and geographies. For decades, individuals and institutions have viewed our organization as a trusted partner for a broad range of investment needs. We have a significant presence in the retail and institutional markets within the investment management industry in North America, EMEA (Europe, Middle East and Africa) and Asia-Pacific, serving clients in more than 120 countries. As of December 31, 2020, the firm managed approximately $1.35 trillion in assets for investors around the world.

The key drivers of success for Invesco are long-term investment performance, competitive pricing which we achieve through scaling our business, high-quality client service and effective distribution relationships, delivered across a diverse spectrum of investment management capabilities, distribution channels, geographic areas and market exposures. By achieving success in these areas, we seek to deliver better outcomes for clients and generate competitive investment results, positive net flows, increased assets under management (AUM) and associated revenues.

We are affected significantly by market movements, which are beyond our control; however, we endeavor to mitigate the impact of market movements for the firm and for clients by maintaining broad diversification across asset classes, investment vehicles, client domiciles and geographies. We measure relative investment performance by comparing our investment capabilities to competitors' products, industry benchmarks and client investment objectives. Generally, distributors, investment advisors and consultants take into consideration longer-term investment performance (e.g., three-year and five-year performance) in their selection of investment products and manager recommendations to their clients, although shorter-term performance may also be an important consideration. Third-party ratings may also influence client investment decisions. We monitor quality of client service in a variety of ways, including periodic client satisfaction surveys, analysis of response times and redemption rates, competitive benchmarking of services and feedback from investment consultants.

Invesco Ltd. is organized under the laws of Bermuda. Our common shares are listed and traded on the New York Stock Exchange under the symbol “IVZ.” We maintain a website at www.invesco.com/corporate. (Information contained on our website shall not be deemed to be part of, or be incorporated into, this document).

Strategy

The company focuses on four key long-term strategic objectives that are designed to sharpen our focus on client needs, further strengthen our business over time and help ensure our long-term success:

•Achieve strong, long-term investment performance across distinct investment capabilities with clearly articulated investment philosophies and processes, aligned with client needs;

•Be instrumental to our clients' success by delivering our distinctive investment capabilities worldwide to meet their needs;

•Harness the power of our global platform by continuously improving execution effectiveness to enhance quality and productivity, and allocating our resources to the opportunities that will best benefit clients and our business; and

•Perpetuate a high-performance organization by driving greater transparency, accountability, diversity of thought, fact-based decision making and execution at all levels.

As an integrated global investment manager, we are keenly focused on meeting clients' needs and operating effectively and efficiently. We take a unified approach to our business and present our financial statements and other disclosures under the single operating segment “investment management.”

We believe one of Invesco's greatest strengths is our separate, distinct investment teams in multiple markets across the globe. A key focus of our business is fostering a strong investment culture and providing the support that enables our investment teams to maintain well-performing investment capabilities. We believe the ability to leverage the capabilities of our investment teams to help clients across the globe achieve their investment objectives is a significant differentiator for our firm.

Industry Trends

Trends around the world continue to transform the investment management industry and underscore the need to be well diversified with broad capabilities globally and across asset classes:

•Distribution partners are becoming more selective and are moving towards developing fewer relationships and partners, reducing the number of investment managers with whom they work. Invesco provides a robust set of capabilities and creates investment solutions that delivers key outcomes aligned to their investment objectives. Invesco delivers competitive pricing, investor education, thought leadership, digital platforms and other value-added services that enhance the client experience.

•Clients are also demanding more from investment managers. While investment performance remains paramount, competitive pricing, client engagement and value-added services (including portfolio analytics and providing consultative solutions) increasingly differentiate managers. Invesco is working to enhance the client's user experience through digital marketing (web, mobile, social) and improved service.

•Investors continue to demand alternative, passive and smart beta strategies. As a consequence, the industry is seeing client demand for core equities portfolios decline as a share of global flows. Invesco is the #3 provider of smart beta AUM in the US and has 76 ETFs with greater than $500 million in assets. Invesco also has a strong lineup of alternative and multi-asset strategies supported by ongoing product development.

•We are seeing increased pressure on net revenue yield within the asset management industry, arising from increased use of low fee passive products and further concentration within our channel distribution partners (which increases their ability to negotiate pricing).

•Regulatory activity remains at increased levels and is influencing competitive dynamics. Increased regulatory scrutiny of managers has focused on many areas including transparency/unbundling of fees, inducements, conflicts of interest, capital, liquidity, solvency, leverage, operational risk management, controls and compensation. Invesco continues to work proactively with regulators around the world. Efforts to further modernize and strengthen our global platform will enhance our ability to compete effectively across markets while complying with the variety of applicable regulatory regimes. This is a key differentiator for large, scaled firms such as Invesco, and smaller firms may struggle to make the necessary investment to stay current and comply with the increased regulation we are seeing globally.

•Although the developed markets in the U.S. and Europe are currently the two largest markets for financial assets by a wide margin, other key emerging markets in the world, such as China and India, are growing faster and positioned for greater future growth over the long term. As these population-heavy markets mature, we believe investment managers that are truly global will be in the best position to capture this growth. Additionally, population age differences between emerging and developed markets will result in differing investment needs and horizons among countries. Asset allocation and retirement savings schemes also differ substantially among countries. We believe firms such as Invesco, with experience in key markets, and diversified investment capabilities and product types, are best positioned to meet clients' needs in this global competitive landscape. Invesco has a meaningful market presence in many of the world's most attractive regions, including North America, EMEA and Asia-Pacific. We believe our strong and growing presence in established and emerging markets provides significant long-term growth potential for our business.

•Technology advances are impacting core elements of the investment management industry, which lags other industries in its use of technology. Clients increasingly seek to interact digitally with their investment portfolios. This is leading to established managers investing in and/or acquiring technology platforms. As the investment management business becomes more complex, automation will become increasingly important to serve clients effectively and efficiently. Invesco is leveraging technology across its business and exploring opportunities to work with third-party technology firms to enhance our clients' investment experience. Over the past few years, we have made strategic acquisitions to strengthen our digital wealth platform. These acquisitions and others have strengthened our ability to offer competitive digital wealth capabilities and position us ahead of the evolving client needs.

As a result of the trends discussed above, clients are seeking to work with a smaller number of asset managers who can deliver a comprehensive set of products and value-added services. They want money managers who can provide a robust set of capabilities and create investment solutions that deliver key outcomes aligned to their investment objectives. They also want greater value for their money, which means competitive pricing, investor education, thought leadership, digital platforms and other value-added services that enhance the client experience. These dynamics are driving fundamental changes within our industry and we believe will drive increasing consolidation. We believe the steps we have taken over the past decade and throughout 2020 strengthened our ability to meet client needs and will help ensure Invesco is well-positioned to compete and win within our industry over the long term.

Investment Management Capabilities

We believe that the proven strength of our distinct and globally located investment teams and their well-defined investment disciplines and risk management approach provide us with a robust competitive advantage. There are few independent investment managers with teams as globally diverse as Invesco's and with the same breadth and depth of investment capabilities and vehicles. We offer multiple investment objectives within the various asset classes and products that we manage. Our asset classes, broadly defined, include money market, balanced, equity, fixed income and alternatives.

The following sets forth our managed investment objectives by asset class:

| | | | | | | | | | | | | | |

Money Market | Balanced | Equity | Fixed Income | Alternatives |

| ●Custom Solutions | ●Custom Solutions | ●Custom Solutions | ●Custom Solutions | ●Custom Solutions |

| ●Environmental, Social and Governance | ●Environmental, Social and Governance | ●Environmental, Social and Governance | ●Environmental, Social and Governance | ●Environmental, Social and Governance |

| ●Cash Plus | ●Balanced Risk | ●Economic Sectors | ●Buy and Hold | ●Absolute Return |

| ●Government/Treasury | ●Global/Regional | ●Emerging Markets | ●Convertibles | ●Commodities |

| ●Prime | ● Single Country | ●International/Global | ●Core/Core Plus | ●Currencies |

| ●Taxable | ●Target Date | ●Large Cap Core | ●Emerging Markets | ●Financial Structures |

| ●Tax-Free | ●Target Risk | ●Large Cap Growth | ●Government Bonds | ●Global Macro |

| ●Traditional Balanced | ●Large Cap Value | ●High-Yield Bonds | ●Infrastructure and MLPs |

| | ●Low Volatility/Defensive | ●International/Global | ●Long/Short Equity |

| | ●Mid Cap Core | ●Investment Grade Credit | ●Managed Futures |

| | ●Mid Cap Growth | ●Multi-Sector | ●Multi-Alternatives |

| | ●Mid Cap Value | ●Municipal Bonds | ●Private and Distressed Debt |

| | ●Passive/Enhanced | ●Passive/Enhanced | ●Private Real Estate |

| | ●Regional/Single Country | ●Regional/Single Country | ●Public Real Estate Securities |

| | ●Small Cap Core | ●Short/Ultra-Short Duration | ●Senior Secured Loans |

| | ●Small Cap Growth | ●Stable Value | |

| | ●Small Cap Value | ●Structured Securities | |

| | ●Smart Beta/Factor-based | ●Smart Beta/Factor-based | |

| | | | |

Distribution Channels

Retail AUM originates from clients investing into funds available to the public in the form of shares or units. Institutional AUM originates from entities such as individual corporate clients, insurance companies, endowments, foundations, government authorities, universities or charities. AUM disclosure by distribution channel represents consolidated AUM distributed by type of sales team (the company's internal distribution channels). AUM amounts disclosed as retail channel AUM represents AUM distributed by the company's retail sales team; whereas AUM amounts disclosed as institutional channel AUM represents AUM distributed by the company's institutional sales team.

The company operates as an integrated global investment manager, presenting itself as a single firm to clients around the world. Dedicated sales forces deliver our investment strategies through a variety of vehicles that meet the needs of retail and institutional clients. Note that not all products sold in the disclosed retail distribution channel are in "retail" vehicles, and not all products sold in the disclosed institutional channel are in "institutional" vehicles, as described in the table below. This aggregation, however, is viewed as a proxy for presenting AUM in the retail and institutional markets in which we operate.

The following lists our primary investment vehicles by distribution channel:

| | | | | | | | | | | |

Retail | | Institutional | |

| ● Closed-end Mutual Funds | | ● Collective Trust Funds | |

| ● Exchange-traded Funds (ETF) | | ● Exchange-traded Funds (ETF) | |

| ● Individual Savings Accounts (ISA) | | ● Institutional Separate Accounts | |

| ● Investment Companies with Variable Capital (ICVC) | | ● Open-end Mutual Funds | |

| ● Investment Trusts | | ● Private Capital Funds | |

| ● Open-end Mutual Funds | | | |

| ● Separately Managed Accounts (SMA) | | | |

| ● Société d'investissement à Capital Variable (SICAV) | | | |

| ● Unit Investment Trusts (UIT) | | | |

| ● Variable Insurance Funds | | | |

Retail

Retail AUM were $947.1 billion at December 31, 2020. We offer retail products within all of the major asset classes. Our retail products are primarily distributed through third-party financial intermediaries, including major wire houses, fund supermarkets, regional broker-dealers, insurance companies, banks and financial planners in North America, and independent brokers and financial advisors, banks and supermarket platforms in EMEA and Asia-Pacific.

The Americas, UK and EMEA ex-UK retail operations rank among the largest by AUM in their respective markets. As of December 31, 2020, Invesco holds a leading position amongst retail fund providers in the UK; Invesco's U.S. retail business, including our ETF franchise, is a top 10 asset manager in the U.S. by long-term assets, and Invesco in EMEA ex-UK is among the largest non-proprietary investment managers in the retail channel. Invesco Great Wall was one of the largest Sino-foreign managers of equity products in China, with total AUM of approximately $66.6 billion as of December 31, 2020. We provide our retail clients with one of the industry's most robust and comprehensive product lines.

Institutional

Institutional AUM were $402.8 billion in AUM as of December 31, 2020. We offer a broad suite of domestic and global strategies, including traditional and quantitative equities, fixed income (including money market funds for institutional clients), real estate, financial structures and absolute return strategies. Regional sales forces distribute our products and provide services to clients and intermediaries around the world. We have a diversified client base that includes major public entities, corporations, unions, non-profit organizations, endowments, foundations, pension funds, financial institutions and sovereign wealth funds. Invesco's institutional money market funds serve some of the largest financial institutions, government entities and corporations in the world.

AUM Diversification

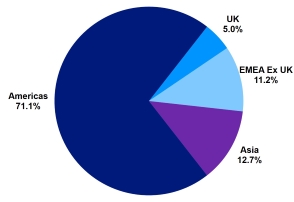

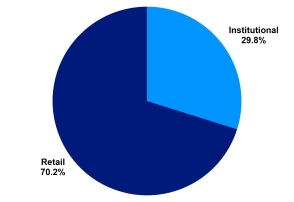

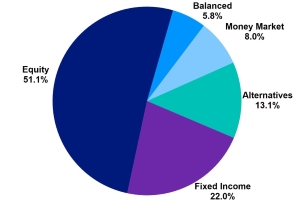

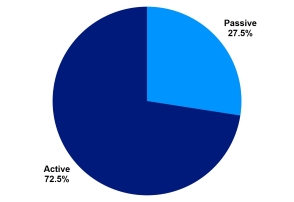

One of Invesco's greatest competitive strengths is the diversification in its AUM by client domicile, distribution channel and asset class. Our distribution network has attracted assets of 70% retail and 30% institutional as of December 31, 2020. By client domicile, 29% of client AUM are outside the U.S., and we serve clients in more than 120 countries. The following tables present a breakdown of AUM by client domicile, distribution channel and asset class as of December 31, 2020. Additionally, the fourth table below illustrates the split of our AUM as Passive and Active. Passive AUM include index-based ETFs, unit investment trusts (UITs), non-management fee earning AUM and other passive mandates. Active AUM is total AUM less Passive AUM. See the company's disclosures regarding the changes in AUM years ended December 31, 2020 in Part II, Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations - Assets Under Management” section for additional information regarding the changes in AUM.

| | | | | | | | | | | | | | |

| By Client Domicile | | | |

| ($ in billions) | Total | | 1-Yr Change |

c Americas | 959.9 | | | 9.1 | % |

c UK | 66.9 | | | (10.1) | % |

c EMEA Ex UK | 151.8 | | | 5.6 | % |

c Asia | 171.3 | | | 33.2 | % |

| Total | 1,349.9 | | | |

| | | |

| | | |

| | | |

| | | |

| | | | | | | | | | | | | | |

| | | | |

| By Distribution Channel | |

| ($ in billions) | Total | | 1-Yr Change |

c Retail | 947.1 | | | 7.8 | % |

c Institutional | 402.8 | | | 15.7 | % |

| Total | 1,349.9 | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | | | | | | | | | | | |

| By Asset Class | | | | |

| ($ in billions) | Total | | 1-Yr Change |

c Equity | 689.6 | | | 15.2 | % |

c Fixed Income | 296.4 | | | 4.6 | % |

c Balanced | 78.9 | | | 17.2 | % |

c Money Market | 108.5 | | | 18.7 | % |

c Alternatives | 176.5 | | | (4.7) | % |

| Total | 1,349.9 | | | |

| | | |

| | | |

| | | |

| | | | | | | | | | | | | | |

| Active vs. Passive | | | | |

| ($ in billions) | Total | | 1-Yr Change |

c Active | 979.3 | | | 5.4 | % |

c Passive | 370.6 | | | 24.8 | % |

| Total | 1,349.9 | | | |

| | | |

| | | |

| | | |

| | | |

Human Capital

Invesco’s long-term success depends on our ability to attract, develop and retain talent. Invesco invests significantly in talent development, health and welfare programs, technology and other resources that support our employees in developing their full potential both personally and professionally. We believe that an employee community that is diverse and inclusive; engaged in community involvement and invested in employee well-being will drive positive outcomes for our clients and shareholders.

During 2020, the COVID-19 pandemic created an unprecedented worldwide public health and business phenomenon. Our top priority in 2020 was the health and well-being of our worldwide employees. In addition to other actions taken, we continue to assess the general well-being of our employees, their ability to stay well, stay productive and stay connected.

In addition, we regularly survey our employees in a confidential survey to gauge their sentiment across a variety of engagement categories, including questions related to compensation, benefits, work/life balance, career development, inclusion, teamwork, and leadership, and more recently our focus on social justice.

We believe that diversity and inclusion are both moral and business imperatives. We are committed to improving diversity at all levels and in all functions across our global business as evidenced by our CEO and senior managing directors all including diversity and inclusion goals as part of their annual performance goals. Increasing representation of women and other underrepresented employees remains a focus for Invesco, as does building an inclusive environment. At the end of 2020, our global workforce was 39% female and 61% male, with 33% of senior managers worldwide being women. Unconscious bias training is required of all managers and is being expanded to the entire employee population. Our employees are also encouraged to participate in any of our nine Business Resource Groups where employees with diverse backgrounds, experiences and perspectives can connect. These Business Resource Groups are sponsored by senior leaders and are designed by employees, for employees.

As of December 31, 2020, the company had 8,512 employees with an on-the-ground presence in over 20 countries (December 31, 2019: 8,821). None of our employees are covered under collective bargaining agreements.

Competition

The investment management business is highly competitive, with points of differentiation including investment performance, the level of fees, the range of products offered, brand recognition, business reputation, financial strength, the depth and continuity of relationships and quality of service. We compete with a large number of investment management firms, commercial banks, investment banks, broker dealers, hedge funds, insurance companies and other financial institutions. We believe the quality and diversity of our investment capabilities, product types and channels of distribution enable us to compete effectively in the global investment management business. We also believe being an independent investment manager is a competitive advantage, as our business model avoids conflicts that are inherent within institutions that both manage and distribute and/or service those products. Lastly, we believe continued execution against our strategic objectives will further strengthen our long-term competitive position.

Management Contracts

We derive substantially all of our revenues from investment management contracts with funds and other clients. Fees vary with the type of assets being managed, with higher fees earned on actively managed equity and balanced accounts, along with real estate and other alternative asset products, and lower fees earned on fixed income, money market and stable value accounts, as well as certain ETFs. Investment management contracts are generally terminable upon thirty or fewer days' notice. Typically, retail investors may withdraw their funds at any time without prior notice. Institutional clients typically may elect to terminate their relationship with us or reduce the aggregate amount of assets under management with very short notice periods.

Risk Management

Invesco is committed to continually strengthening and evolving our risk management activities to ensure they keep pace with business change and client expectations. We believe a key factor in our ability to manage through challenging market conditions and significant business change is our integrated and global approach to risk management. Risk management is embedded in our day-to-day decision-making as well as our strategic planning process while our global risk management framework enables consistent and meaningful risk dialogue up, down and across the company.

Our framework leverages two governance structures: (i) our Global Performance and Risk Committee oversees the management of core investment risks; and (ii) our Corporate Risk Management Committee oversees the management of all other business and strategy related risks. A network of regional, business unit and specific risk management committees, with oversight of the Corporate Risk Management Committee, provides ongoing identification, assessment, management and monitoring of risk that ensures both broad as well as in-depth, multi-layered coverage of the risks existing and emerging in the various domains of our business.

Available Information

The SEC maintains a website that contains reports, proxy and information statements and other information regarding issuers with the SEC, at www.sec.gov. We make available free of charge on our website, www.invesco.com/corporate, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC.

Item 1A. Risk Factors

Risks Related to the Coronavirus (COVID-19) Pandemic

As a result of the global market reactions to the COVID-19 pandemic, our assets under management (AUM) and revenues have been negatively impacted and we face various potential operational challenges due to the pandemic.

As a result of the global market reactions to the COVID-19 pandemic, our assets under management (AUM) and revenues declined significantly during the early phases of the pandemic as governments enacted social containment measures and central banks and governments sought to enact economic relief measures. While many global markets have improved materially since the early stages of the pandemic, further negative market reactions may occur as a result of failures to limit infections or deaths to the COVID-19 virus, delays in developing and/or delivering effective treatments for the virus, and reduced support or positive impact of central banks and government economic relief measures. Additional negative market reactions could further negatively impact our AUM and revenues. The volatility in the global markets has also adversely affected the liquidity of certain managed investment products in which client and company assets are invested.

Our efforts to mitigate the impact of the COVID-19 pandemic have required, and will continue to require, a significant investment of time and resources across our business. In response to mandated precautions where applicable and to ensure the safety of our employees, the significant majority of our employees are working remotely at this time. While our teams have been successful in working remotely, operational challenges may arise in the future. Many of the key service providers we rely on have also transitioned to working remotely. If we or they were to experience material disruptions in the ability for our or their employees to work remotely (e.g., disruption in Internet-based communications systems or networks or the availability of essential goods and services), our ability to operate our business in the ordinary course could be materially adversely disrupted. To date our own employees and, we believe, the employees of our key service providers, have not experienced any material degree of illness due to the COVID-19 virus. If our or their workforces, or key components thereof, were to experience significant illness levels, our ability to operate our business could be materially adversely disrupted. Further if our cyber security diligence and efforts to offset the increased risks associated with greater reliance on mobile, collaborative and remote technologies during the COVID-19 pandemic, as well as the increased frequency and sophistication of external threat actors are not effective or successful, we may be at increased risk for data privacy or other cyber security incidents. Any such material adverse disruptions to our business operations or loss of information could have a material adverse impact on our results of operation or financial condition.

The extent to which our business, results of operations, AUM and financial results are further affected by the COVID‐19 pandemic will largely depend on future developments, which cannot be accurately predicted and are uncertain, including the duration and severity of the pandemic, length of time it will take for the financial markets and economy to recover and for our employees to safely return to the workplace, along with potentially more permanent impacts on how we operate and serve our clients. In addition, many of the risk factors described below may be heightened by the effects of the COVID‐19 pandemic and related economic conditions.

Risks Related to Market Dynamics and Volatility

Volatility and disruption in world capital and credit markets, as well as adverse changes in the global economy, can negatively affect Invesco's revenues, operations, financial condition and liquidity.

In recent years, capital and credit markets have experienced substantial volatility. In this regard:

•In the event of extreme circumstances, including economic, political, or business crises, such as a widespread systemic failure or disruptions in the global financial system or failures of firms that have significant obligations as counterparties on financial instruments, we may suffer significant declines in AUM and severe liquidity or valuation issues in managed investment products in which client and company assets are invested, all of which would adversely affect our operating results, financial condition, liquidity, credit ratings, ability to access capital markets, and ability to retain and attract key employees. Additionally, these factors could impact our ability to realize the carrying value of our goodwill and other intangible assets.

•Illiquidity and/or volatility of the global fixed income and/or equity markets could negatively affect our ability to manage client inflows and outflows or to timely meet client redemption requests.

•Uncertainties regarding geopolitical developments, such as Brexit, can produce volatility in global financial markets. This may impact the levels and composition of our AUM and also negatively impact investor sentiment, which could result in reduced or negative flows. The longer term relationship between the UK and the EU is still uncertain following the departure of the UK from the EU. Because the UK Pound Sterling is the functional currency

for certain of our subsidiaries, any weakening of the UK Pound Sterling relative to the U.S. Dollar could negatively impact our reported financial results.

•Changes to United States tax, tariff and import/export regulations may have a negative effect on global economic conditions, financial markets and our business. Any changes with respect to trade policies, treaties, taxes, government regulations and tariffs or the perception that any of these changes could occur, may have a material adverse effect on global economic conditions and the stability of global financial markets, and may significantly reduce global trade and, in particular, trade between other nations and the United States. Given our strong position in Asia Pacific and EMEA, we could be more adversely affected than others by such market uncertainties.

Our revenues and profitability would be adversely affected by any reduction in AUM as a result of either a decline in market value of such assets or net outflows, which would reduce the investment management fees we earn.

We derive substantially all our revenues from investment management contracts with clients. Under these contracts, the investment management fees paid to us are typically based on the market value of AUM. AUM may decline for various reasons. For any period in which revenues decline, our income and operating margin likely would decline by a greater proportion because a majority of our expenses remain fixed. Factors that could decrease AUM (and therefore revenues) include the following:

Declines in the market value of AUM in client portfolios. Our AUM as of January 31, 2021 were $1,367.1 billion. We cannot predict whether volatility in the markets will result in substantial or sustained declines in the securities markets generally or result in price declines in market segments in which our AUM are concentrated. Any of the foregoing could negatively impact the market value of our AUM, our revenues, income and operating margin.