Exhibit 10.60

LEASE AGREEMENT

STATE OF TEXAS, COUNTY OF EL PASO

THIS LEASE AGREEMENT, made and entered into as of the Effective Date (as defined in Paragraph 25(g)), by and between EastGroup Properties, L.P., a Delaware limited partnership, hereinafter referred to as “Landlord”, and UFP Technologies Inc., a Delaware corporation, hereinafter referred to as “Tenant”;

WITNESSETH:

Preamble

Landlord is currently the lessee of the real estate located at a portion of Lot 8, Block 12, Butterfield Trail Industrial Park, Unit 1, El Paso, Texas (the “Land”) under the Ground Lease dated December 1, 1997, (the “Ground Lease”), with the City of El Paso (the “Ground Lessor”), a copy of which has been provided to Tenant and by this reference is incorporated for the premises described herein. All the obligations contained in the Ground Lease conferred and imposed upon Landlord (as lessee therein), except for the payment of ground rental and other charges payable pursuant thereto and except as specifically modified further and amended by this Lease, are hereby conferred and imposed upon Tenant with respect to the Premises (as hereinafter described). Any duty or obligation in the Ground Lease required to be performed for the benefit of the Ground Lessor or any right in the Ground Lease granted for the benefit of the Ground Lessor shall be deemed to be for the benefit of Ground Lessor and Landlord.

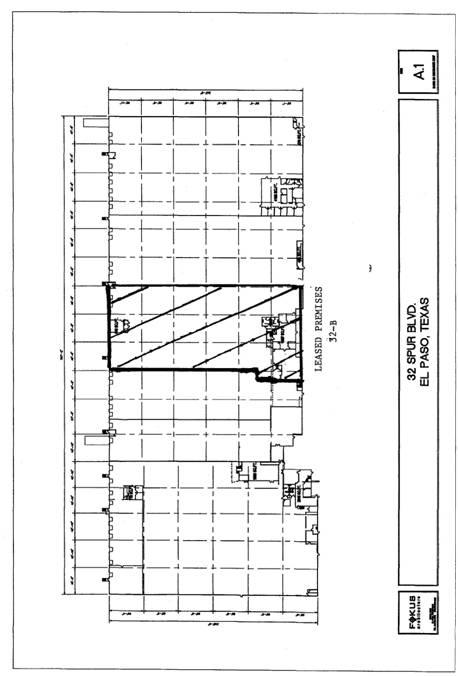

1. PREMISES AND TERM. In consideration of the obligation of Tenant to pay Rent as herein provided, and in consideration of the other terms, provisions and covenants hereof, Landlord hereby demises and leases to Tenant, and Tenant hereby takes from Landlord, approximately 48,325 square feet of that certain building located at 32-B Spur Drive, El Paso, Texas 79906, County of El Paso, State of Texas, the real property of which is more particularly described on Exhibit “A” attached hereto and incorporated herein by reference, together with all rights, privileges, easements, appurtenances and immunities belonging to or in any way pertaining thereto and together with the building and other improvements situated or to be situated thereon (the said portion of the project’s real property, building and improvements being hereinafter referred to as the “Premises”).

Landlord and Tenant acknowledge that the Premises is part of a multi-tenant project (the “Project”). Expenses covering the buildings in the Project for property taxes and assessments, insurance, common area utilities and maintenance, and management fees shall be prorated on a square foot basis. The Premises proportionate share of these expenses is 48,325 SF/ 260,500 SF or 18.55 %.

TO HAVE AND TO HOLD the same for a term commencing on the “Commencement Date”, as hereinafter defined, and ending sixty (60) months thereafter (the “Term”), provided, however, that in the event the Commencement Date is a date other than the first day of a calendar month, said Term shall extend for said number of months in addition to the remainder of the calendar month following the Commencement Date.

The “Commencement Date” shall be the date on which the Premises and other improvements to be erected in accordance with the plans and specifications described on Exhibit “B” attached hereto (the “Plans”) have been substantially completed. As used herein, the term “substantially completed” shall mean, that in the reasonable opinion of the architect or space planner that prepared the Plans, such improvements have been completed in accordance with the Plans and the Premises are in good and satisfactory condition, subject only to completion of minor punch list items. Landlord shall notify Tenant ten (10) days prior to the occurrence of the Commencement Date.

Landlord shall deliver the Premises to Tenant broom clean and free of debris on the Commencement Date and warrants to Tenant that the existing plumbing, electrical systems, fire sprinkler system, lighting, air conditioning and heating systems and loading doors, if any, in the Premises, other than those constructed or installed by Tenant, shall be in good operating condition on the Commencement Date. If a non-compliance with said warranty exists as of the Commencement Date, Landlord shall, except as otherwise provided in this Lease, promptly after receipt of written notice from Tenant setting forth with specificity the nature and extent of such non-compliance, rectify the same at Landlord’s expense. If Tenant does not give Landlord written notice of a non-compliance with this warranty within sixty (60) days after the Commencement Date (except as to the air conditioning system which shall be governed by Paragraph 5(b) below), correction of that non-compliance shall be the obligation of Tenant at Tenant’s sole cost and expense.

Landlord shall notify Tenant in writing of the Commencement Date as soon as such improvements to said Premises have been substantially completed and ready for occupancy as aforesaid. Within ten (10) days thereafter,

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

Tenant shall submit to Landlord in writing a punch list of items needing completion or correction. Landlord shall use reasonable efforts to complete such items within thirty (30) days after receipt of such notice. In the event Tenant, its employees, agents or contractors cause construction of such improvements to be delayed, the Commencement Date shall be deemed to be the date that, in the opinion of the architect or space planner that prepared the Plans, substantial completion would have occurred if such delays had not taken place. Subject to the paragraph next above and other specific provisions of this Lease, the taking of possession by Tenant shall be deemed conclusively to establish that the buildings and other improvements had been completed in accordance with the Plans, that the Premises are in good and satisfactory condition as of when possession was so taken, and that Tenant has accepted the Premises without representation or warranty from Landlord, except as stated in this Lease. After such Commencement Date, Tenant shall, upon demand, execute and deliver to Landlord a Letter of Acceptance of delivery of the Premises.

Landlord and Tenant further agree that Tenant’s obligations, privileges, covenants and agreements contained in this Lease shall be operative and effective regardless of whether the Premises are ever occupied by Tenant. If Tenant fails to occupy the Premises for any reason (other than a default hereunder by Landlord) after substantial completion of any building or improvements constructed in accordance with the Plans, or if Tenant whether constructively or actively prevents or hinders Landlord from constructing the improvements contemplated herein in accordance with the Plans, this Lease shall be deemed to have commenced automatically and the Commencement Date shall be deemed to be the date on which the improvements would have been completed in Landlord’s sole, but reasonable judgment, but for such hindrance or prevention by Tenant.

2. RENT AND SECURITY DEPOSIT.

(a) As part of the consideration for the execution of this Lease, and for the Lease and use of the Premises, Tenant covenants and agrees and promises to pay as net rental to Landlord, or Landlord’s assignees, $0.00 per month during the months 1 through 4 in the Term hereof, $11,880.00 per month during the months 5 through 12 during the Term hereof, $12,887.00 per month during the months 13 through 24 during the Term hereof, $13,289.00 per month during the months 25 through 36 during the Term hereof, $13,692.00 per month during the months 37 through 48 during the Term hereof, and $14,095.00 per month during the months 49 through 60 during the Term hereof (collectively, “Base Rent”). One such monthly installment of $11,880.00, plus the other monthly charges set forth in Paragraph 2(c) below (initially $3,423.00) per month, shall be due and payable on the date hereof and shall be applied in satisfaction of Tenant’s obligation to pay rent as defined in Paragraph 2(c) below for month 5 of the Term, and subsequent monthly installments for an amount as indicated in Paragraph 2(a), herein, shall be due and payable in advance, without demand, deduction or set off, on or before the first day of each succeeding calendar month succeeding the Commencement Date, except that all payments due hereunder for any fractional calendar month shall be prorated.

(b) In addition, Tenant agrees to deposit with Landlord the sum of $16,591.60, which shall be held by Landlord, without obligation for interest, as security for the performance of Tenant’s covenants and obligations under this Lease, it being expressly understood and agreed that such deposit is not an advance rental deposit or a measure of Landlord’s damages in case of Tenant’s default. Upon each occurrence of an event of default by Tenant, Landlord may, from time to time, without prejudice to any other remedy provided herein or provided by law, use such fund to the extent necessary to make good any arrears of Rent or other payments due Landlord hereunder, and any other damage, injury, expense or liability caused by such event of default. On demand, Tenant shall pay to Landlord the amount that will restore the security deposit to its original amount. Although the security deposit shall be deemed the property of the Landlord, any remaining balance of such deposit shall be returned by Landlord to Tenant within thirty (30) days after termination of this Lease, provided that all of Tenant’s obligations under this Lease have been fulfilled.

(c) Tenant agrees to pay to Landlord, as additional rental, beginning on the first day of the fifth (5th) month of the Term, its proportionate share (as defined in Paragraph 1 herein) of Operating Expenses in each calendar year. Operating Expenses include (i) Taxes (hereinafter defined) pursuant to Paragraph 4(a) below, (ii) the cost of all insurance relating to the building or buildings of which the Premises are a part, (iii) the cost of utilities payable by Landlord pursuant to Paragraph 9 below, and the cost of any common area charges payable by Landlord in accordance with Paragraph 5 below, (iv) the cost of management services and (v) any other costs related to the ownership, operation, repair and maintenance of the Project. Operating Expenses shall not include depreciation or amortization of the Project or equipment in the Project except as provided herein, loan principal payments, costs of alterations of tenants’ premises, leasing commissions, advertising and promotional costs; principal or interest payments on any mortgages or other financing arrangements; legal fees; expenses incurred in connection with negotiating and enforcing leases with tenants in the Project; build out allowances, moving expenses, and other concessions incurred in connection with leasing spacing in the Project; the cost of any item or service to the extent Landlord is reimbursed by tenants, third parties or insurance; cost of any service or material provided by a related party to the extent that the cost of such service or material exceeds the competitive cost of such service or material absent such relationship; fines or penalties (unless such fines or penalties were the result of the acts or omissions of Tenant); and, except as included in the cost of

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

management services, wages, salaries, or other compensation paid to any executive employees of Landlord above the grade of Property Manager.

Base Rent, Operating Expenses and any other costs which Landlord is entitled to collect under this Lease are hereinafter referred to collectively as “Rent”. The amount of the initial monthly Base Rent and the initial monthly Operating Expense escrow payments are as follows:

|

1.) |

|

Initial Base Rent as set forth in Paragraph 2 (a) |

|

$ |

11,880.00 |

|

|

2.) |

|

Operating Expense escrow |

|

$ |

3,423.00 |

|

|

|

|

|

|

|

| |

|

TOTAL INITIAL MONTHLY RENTAL PAYMENT |

|

$ |

15,303.00 |

| ||

Beginning on the first day of the fifth (5th) month of the Term, and continuing during each month of the Term thereafter, on the same day that Base Rent is due hereunder, Tenant shall escrow with Landlord an amount equal to 1/12 of the estimated annual cost of its proportionate share of such Operating Expenses. The monthly escrow payments shall be adjusted annually to reflect the then current projected cost of all Operating Expenses. Landlord shall annually reconcile Tenant’s proportionate share of Operating Expenses against Tenant’s total annual escrow payments. If Tenant’s total annual escrow payments were insufficient to cover Tenant’s share of the actual annual Operating Expenses, Tenant shall pay the difference to Landlord within ten (10) days after demand. If Tenant’s annual escrow payments were excessive, Landlord shall retain such excess and credit it against Tenant’s future liabilities for Operating Expenses.

In implementation of the foregoing, within a reasonable time after the end of each whole or partial calendar year during the Lease Term, Landlord shall render to Tenant a statement, prepared according to generally accepted accounting principles consistently applied, showing in reasonable detail the Landlord’s Operating Expenses for the preceding calendar year or fraction thereof, as the case may be. Such statement shall be binding upon Landlord and Tenant, subject to the provisions of this Paragraph . Tenant shall have the right, at its expense and upon written notice given to Landlord no later than forty-five (45) days after receipt of the annual reconciliation statement from Landlord, to make an audit of all of Landlord’s bills and records relating to Operating Expenses for the immediately preceding calendar year. Upon such written request of Tenant, Landlord shall make available to Tenant, during normal business hours, at the location where Landlord’s books and records are kept, such information as Tenant shall reasonably request. Landlord shall cooperate reasonably with Tenant in its explanation of its bills and records. Tenant agrees that it will treat such information confidentially and shall not divulge such information obtained from Landlord to any other person, firm, corporation, business organization, entity, tenant or occupant at any time. Tenant shall have the right to retain the services of an independent certified public accountant or lease audit firm for such audit; provided, however, Tenant shall not retain any such auditor or audit firm on a contingency fee basis. Tenant shall complete any such audit of Operating Expenses within sixty (60) days after the date of Tenant’s audit notice and shall deliver to Landlord the written results of such audit within ten (10) days after Tenant receives the same. If such audit discloses an overpayment by Tenant in excess of five percent (5%) of the amount Tenant should have paid, Landlord shall credit such amount against Tenant’s future obligations for Operating Expenses. If such audit discloses additional amounts due from Tenant in excess of five percent (5%) of the amount Tenant should have paid, Tenant shall pay such amounts within ten (10) days of completion of such audit.

3. USE. The Premises shall be used only for normal manufacturing and assembly with related office and warehouse use and for such other lawful and permitted purposes as may be incidental thereto, and in compliance with applicable city and local codes and the Rules of the Premises attached hereto as Exhibit “C”. Tenant shall, at its own cost and expense, obtain any and all licenses and permits necessary for such use, shall at all times maintain the Premises in a clean, healthful and safe condition and comply with all governmental laws, codes, ordinances, regulations or any other applicable authorities with regard to the use, condition or occupancy of the Premises, including, without limitation, all requirements of the Ground Lease and regulations issued under the provisions of the Texas Architectural Barriers Act, TX Govt. Code Chap. 469, and the Americans with Disabilities Act, 42 U.S.C. 12101 et seq. Tenant shall be responsible, at Tenant’s sole expense, for the correction, prevention and abatement of nuisances in or upon, or connected with the Premises. Tenant shall not permit any objectionable or unpleasant odors, smoke, dust, gas, noise or vibrations, or pest infestations to emanate from the Premises, nor take any other action that would constitute a nuisance or would disturb, unreasonably interfere with, or endanger Landlord or any other tenants of the building or Project of which the Premises are a part. Landlord covenants and warrants to Tenant that the Premises shall, as of the Commencement Date be in compliance with all applicable governmental laws, codes, ordinances, regulations or any other applicable authorities with regard to the condition of the Premises and its use and occupancy for general office and warehouse uses, including, without limitation, all requirements of the Ground Lease and regulations issued under the provisions of the Texas Architectural Barriers Act, TX Govt. Code Chap. 469, and the Americans with Disabilities Act, 42 U.S.C. 12101 et seq. Notwithstanding the foregoing, Landlord and Tenant agree that the Premises and/or the Project may not comply in all respects with current codes, ordinances or regulations, and Landlord shall not be required

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

to comply with such current codes, ordinances or regulations if (i) compliance is waived or otherwise not required by the provisions thereof or (ii) the Premises and/or the Project is considered grandfathered or non-conforming but permissible under any such code or regulation.

Without Landlord’s prior written consent, Tenant shall not receive, store or otherwise handle any product, material or merchandise which is explosive or highly inflammable. Tenant will not permit the Premises to be used for any purpose which would render the property or liability insurance thereon void or the insurance risk more hazardous or cause the State Board of Insurance or other insurance authority to disallow any sprinkler credits.

Tenant and its employees, agents, customers, invitees, and/or licensees shall have the use of sixty (60) parking spaces in the parking area located in front of the Premises. Landlord reserves the right, in its reasonable discretion, to determine whether such parking facilities are becoming crowded, and in such event, to allocate parking spaces among Tenant and other tenants in the Project. In the event Landlord elects to allocate parking spaces, Landlord shall allocate no fewer than sixty (60) spaces to Tenant. Landlord shall not be responsible for enforcing Tenant’s parking rights against any third parties.

4. TAXES AND OTHER ASSESSMENTS.

(a) Landlord agrees to pay all taxes, assessments or governmental charges of any kind and nature whatsoever (hereinafter collectively referred to as “Taxes”), levied or assessed against the Premises, and/or the land and/or improvements of which the Premises are a part, and all taxes of whatsoever nature that are imposed in substitution for or in lieu of any such taxes, assessments, or governmental charges, and Tenant shall be liable for its proportionate share of the same.

(b) If at any time during the Term of this Lease, there shall be levied, assessed or imposed on Landlord a capital levy or other tax directly on the rents received therefrom and/or a margin tax or franchise tax, assessment, levy or charge measured by or based, in whole or in part, upon such rents for the Premises and/or the land and/or improvements of which the Premises are a part, including, but not limited to, any franchise tax imposed under Chapter 171 of the Texas Tax Code, then all such taxes, assessments, levies or charges, or the part thereof so measured or based, shall be deemed to be included within the term “Taxes” for the purposes hereof.

(c) The Landlord shall have the right to employ a tax consulting firm to attempt to assure a fair tax burden on the Premises within the applicable taxing jurisdictions. Tenant agrees to pay its proportionate share of the cost of such consultant as additional rental. Landlord agrees to make commercially reasonable efforts, in the exercise of Landlord’s reasonable business judgment, to minimize taxes assessed against the Premises, including, without limitation, the timely filing of a protest regarding the annual appraisal of the Premises as appropriate.

(d) Tenant shall be liable for all taxes levied or assessed against any personal property or fixtures placed in the Premises. If any such taxes are levied or assessed against Landlord or Landlord’s property and (i) Landlord pays the same or (ii) the assessed value of Landlord’s property is increased by inclusion of such personal property and fixtures and Landlord pays the increased taxes, then, upon demand Tenant shall pay to Landlord such taxes.

(e) To the extent permitted by applicable law, Tenant hereby waives the provisions of §41.413 of the Texas Property Tax Code, or any successor thereto.

5. MAINTENANCE AND REPAIRS.

(a) Tenant, at its own cost and expense, shall (i) maintain all parts of the Premises in good condition, (ii) promptly make all necessary repairs and replacements, including, but not limited to, windows, glass and plate glass, exterior doors, interior walls and finish work, interior doors and floor covering, utility connections, downspouts, gutters, heating and air conditioning systems (subject to the provisions of paragraph (b) below), light bulbs and ballasts, truck doors, dock bumpers, dock lights, dock levelers, paving, plumbing work and fixtures, termite and pest extermination, regular removal of trash and debris, and dedicated sewer lines, and (iii) keep the parking areas, driveways, truck aprons, and grounds surrounding the Premises in a clean and sanitary condition.

(b) Tenant shall, at its own cost and expense, enter into a regularly scheduled preventive maintenance/service contract with a maintenance contractor for servicing all hot water, heating and air conditioning systems and equipment within the Premises (which contractor and contract must be approved by Landlord, which approval shall not be unreasonably withheld or delayed). The service contract must include all services outlined in Paragraph 31B below and must become effective (and a copy thereof delivered to Landlord) within thirty (30) days of the date Tenant takes possession of the Premises. Prior to entering the Premises, Tenant’s maintenance contractor shall provide evidence of liability insurance naming Landlord, its directors, officers, employees, agents and affiliates as additional insureds and

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

workers compensation insurance including an endorsement waiving subrogation against Landlord, its directors, officers, employees, agents and affiliates, in amounts acceptable to Landlord. Landlord shall, at its cost, make any repairs or replacements necessary to place the heating and air conditioning units serving the Premises in good working order as of the date of initial startup of such units. Provided Tenant complies with the requirements of this Paragraph 5 and of Paragraph 31B regarding Tenant’s maintenance obligations, and except to the extent necessitated by the negligence or willful misconduct of Tenant, its employees or agents, if during the period beginning on the date of initial startup of such units and ending on September 30, 2012, (i) any heating or cooling unit provided by Landlord cannot be repaired and requires replacement, Landlord shall provide such replacement at Landlord’s sole cost, and (ii) any heating or cooling unit provided by Landlord shall require repair in excess of $600 per unit per repair, Landlord shall perform such repair at its sole cost. The cost of the regularly scheduled preventive maintenance/service contract and the cost of routine maintenance items such as filters and belts shall not be considered repair or replacement costs for purposes of determining Landlord’s repair or replacement obligations under this Paragraph 5(b).

(c) Landlord shall (i) maintain the roof, foundation and the structural soundness of the exterior walls of the building of which the Premises are a part in good repair, reasonable wear and tear excepted, (ii) perform the repair, replacement and maintenance of access ways, driveways, parking areas and landscaping, and (iii) perform all exterior painting, common water and sewage line plumbing, and any other common maintenance items, and Tenant shall be liable for its proportionate share of the cost and expense of such repair, replacement, and maintenance. Landlord agrees that such costs shall not include any capital costs for roof, foundation, building structural, or parking lot replacement or work occasioned by fire, windstorm or other casualty to the extent of net insurance proceeds received by Landlord with respect thereto. Notwithstanding the foregoing, however, to the extent any repair or replacement is necessitated by the acts or omissions of Tenant, its officers, directors, employees, agents, licensees, assignees or subtenants, Tenant shall be liable for the entire cost of such repair or replacement.

6. TENANT’S ALTERATIONS, ADDITIONS, INSTALLATIONS.

The Tenant shall not make any alterations or additions to or installations at the Premises except as provided in this Section 6.

(a) Tenant’s Improvements and Installations. Subject to the provisions of paragraph 6(b) below, Tenant, at its own expense (a) shall, prior to commencing its business operations at the Premises, install a water submeter as described in Paragraph 9 below, (b) may, after the Commencement Date, at Tenant’s election and at Tenant’s sole expense, perform the installations and alterations listed on Exhibit F attached hereto and incorporated herein, which installations and alterations are conceptually acceptable to Landlord, subject to reasonable adjustments to be agreed upon after submittal and review of Tenant’s plans pursuant to paragraph (b) below (“Tenant’s Initial Installations”), and (c) may make further installations, improvements or alterations to the interior of the Premises during the Term of this Lease, provided that Tenant shall comply with the provisions of paragraph (b) below in each such instance. Should Tenant desire to make additional installations during the Term of the Lease, Tenant may request, in connection with Tenant’s request for Landlord’s approval, that such installations be added to Exhibit F, and Landlord shall not unreasonably withhold consent to the addition of said items.

(b) Tenant’s Work. Tenant shall procure at Tenant’s sole expense all necessary permits and licenses before undertaking any work on the Premises; do all such work in a good and workmanlike manner employing materials of good quality and so as to conform with all applicable zoning, building, environmental, fire, health and other codes, regulations, ordinances and laws; furnish to Landlord for Landlord’s review and approval prior to the commencement of any such work reasonably detailed plans and specifications. Landlord hereby agrees not to unreasonably withhold or delay approval of such plans and/or specifications; provided that Landlord shall not be deemed unreasonable for refusing to approve any construction, alterations, or additions requested by Tenant which would render the Premises or any material part thereof unsuitable for its current use and which would require unusual expense to readapt the Premises substantially to such use on lease termination or would materially increase the cost of insurance or taxes on the Building, unless Tenant first provides security reasonably acceptable to Landlord assuring that such readaptation will be made prior to such termination without expense to Landlord or Tenant agrees to pay such increased cost of insurance. Any work requiring penetration of, or alterations to, the roof of the Premises shall be performed by Landlord’s approved roofing contractor. All equipment or structures placed on the roof of the building in which the Premises is located shall be screened from view so as not to be visible from the street and shall be located no closer than thirty feet (30’) from any edge of the roof. The location and manner of attachment of any equipment or structures placed on the roof by Tenant or its contractors shall be subject to Landlord’s prior review and approval. Landlord and Landlord’s consultants shall have the right at any time and from time to time to inspect the Premises during the construction of Tenant’s Initial Installations to ensure compliance with the terms hereof, and in the event that Landlord or Landlord’s consultant gives notice to the Tenant of non-compliance of such construction, Tenant shall promptly undertake to correct such deficiencies in order to bring the construction of Tenant’s Initial Installations into compliance with the terms and conditions of this Lease and all applicable laws, ordinances, rules, regulations and/or code

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

requirements. Tenant agrees to pay promptly when due the entire cost of any work on the Premises undertaken by Tenant so that the Premises shall at all times be free of liens for labor and materials; to employ for such work one or more responsible contractors reasonably satisfactory to Landlord; to require such contractors employed by Tenant to carry (i) worker’s compensation insurance in accordance with statutory requirements including an endorsement waiving subrogation against Landlord, its directors, officers, employees, agents and affiliates, and (ii) commercial public liability insurance naming Landlord as an additional insured and covering such contractors on or about the Premises in amounts reasonably satisfactory to Landlord, and to submit certificates evidencing such coverage to Landlord prior to the commencement of such work; and to save Landlord harmless and indemnified from all injury, loss, claims or damage to any person or property occasioned by or growing out of such work. Tenant may also from time to time, with prior notice to Landlord and without the necessity of providing plans to or receiving approval from Landlord, at its own cost and expense and in a good workmanlike manner, make minor alterations, additions or improvements to the interior of the Premises, or erect, remove or alter such shelves, bins, machinery and trade fixtures as Tenant may deem advisable, without altering the basic character of the building or improvements and without overloading or damaging such building or improvements.

(c) Restoration. Tenant’s Initial Installations shall be and remain the property of Tenant, and upon the termination of this Lease, Tenant shall quit and surrender the Premises having first removed Tenant’s Initial Installations and such of its other alterations, installations and additions as Landlord may designate (unless otherwise agreed at the time the same were approved by Landlord) and having restored the Premises substantially to the condition in which they now exist and repaired all damage occasioned by the removal of Tenant’s installations, alterations and improvements in a good and workmanlike manner. All such removals and restoration shall be accomplished in good workmanlike manner so as not to damage the primary structure or structural qualities of the Building and other improvements situated on the Premises.

7. SIGNS. Tenant shall have the right to install a sign upon the exterior of the building only when first approved in writing by Landlord and subject to any applicable governmental laws, ordinances, regulations, deed restrictions and architectural standards reasonably set forth by Landlord, and so long as such signs comply with the requirements set forth in Exhibit C attached hereto. Tenant shall not (i) make any changes to the exterior of the Premises, (ii) install any exterior lights, decorations, balloons, flags, pennants, banners or painting, or (iii) erect or install any signs, window or door lettering, placards, decorations or advertising media of any type which can be viewed from the exterior of the Premises without Landlord’s prior written consent, which shall not be unreasonably withheld. All signs, decorations, advertising media, blinds, draperies, and other window treatment or bars or other security installations visible from outside the Premises shall conform in all respects to the criteria established by Landlord and by the Ground Lease. Tenant shall remove all such signs upon the termination of this Lease. Such installations and removals shall be made in such manner as to avoid injury to or defacement of the building and other improvements. Tenant shall repair any injury or defacement, including without limitation discoloration, caused by such installation and/or removal, if so required by Landlord.

8. INSPECTION. Landlord and Landlord’s agents and representatives shall have the right to enter and inspect the Premises at any reasonable time during business hours after prior notice to Tenant (provided, however, that no notice shall be required in the event of emergency) for the purpose of ascertaining the condition of the Premises, determining if Tenant is performing its obligations hereunder, performing the repairs that Landlord is obligated or elects to perform hereunder, making repairs to adjoining space, or curing any Defaults of Tenant hereunder that Landlord elects to cure. Commencing six (6) months prior to the end of the Term hereof, Landlord and Landlord’s agents and representatives shall have the right to enter the Premises at any reasonable time during business hours for the purpose of showing the Premises and shall have the right to erect on the Premises a suitable sign indicating that the Premises are available. Any such entry by Landlord and its agents, representatives and contractors (and, in particular, any activities involving repairs to adjoining space or construction of a demising wall separating such space from the Premises) shall be made at such times and conducted in such manner as to reasonably minimize any interference with Tenant’s use of the Premises for the conduct of its business.

Tenant shall give written notice to Landlord at least thirty (30) days prior to vacating the Premises and shall arrange to meet with Landlord for a joint inspection of the Premises prior to vacating. In the event of Tenant’s failure to give such notice or arrange such joint inspection, if Landlord is aware of Tenant’s pending departure from the Premises, Landlord shall use reasonable efforts to contact Tenant to arrange such joint inspection. If Tenant fails to respond to Landlord’s contact, then Landlord’s inspection at or after Tenant’s vacating the Premises shall be conclusively deemed correct for purposes of determining Tenant’s responsibility for repairs and restoration.

9. UTILITIES. Upon the Commencement Date, Landlord agrees to provide normal water, sewer and electricity service connections to the Premises and normal gas and telephone service connections to the demarcation point in the building, which connections shall hereafter be maintained by Tenant. Tenant shall pay for all water, gas, heat, light, power, telephone, sewer, sprinkler charges and other utilities and services used on or at the Premises, and any

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

maintenance or inspection charges for utilities. Tenant shall pay its proportional share of all charges for jointly metered and common area utilities. Landlord shall not be liable for any interruption or failure of utility services on the Premises.

Landlord shall furnish the Premises with water and sewer for normal domestic restroom and kitchen usage, and Tenant agrees to reimburse Landlord for the common water and sewer service as a component of additional rental under Paragraph 2(c) above. Furthermore, Tenant agrees, at its own expense prior to commencement of business operations in the Premises, to install a submeter to measure Tenant’s water usage in connection with its manufacturing use and thereafter to promptly upon demand reimburse Landlord for the cost of such submetered water (and additional sewer costs, if any) as additional rent. The location and manner of installation of such submeter shall be subject to Landlord’s prior review and approval.

10. ASSIGNMENT AND SUBLETTING. Tenant shall not have the right to assign this Lease or to sublet the whole or any part of the Premises without the prior written consent of the Landlord. Upon the occurrence of an “event of default” as hereinafter defined, if the Premises or any part thereof are then assigned or sublet, Landlord, in addition to any other remedies herein provided or provided by law, may at its option collect directly from such assignee or subtenant all rents becoming due to Tenant under such assignment or sublease and apply such rent against any sums due to Landlord from Tenant hereunder, and no such collection shall be construed to constitute a novation or a release of Tenant from the further performance of Tenant’s obligations hereunder.

Notwithstanding any of the above provisions of this Paragraph 10 to the contrary, Tenant may assign this Lease or sublet the Premises or any portion thereof, upon notice to Landlord but without Landlord’s written consent, but subject to all other provisions of this Lease, to any corporation or other entity which controls, is controlled by, or is under common control with Tenant, or to any corporation or other entity resulting from a merger or consolidation of Tenant (collectively, an “Affiliate”), provided that (i) the Affiliate assumes in writing all of Tenant’s obligations under this Lease, and (ii) such transfer is not a subterfuge by Tenant to avoid its obligations under this Lease or the restrictions on assignment and subletting under this Paragraph 10. Notwithstanding any assignment or subletting, Tenant shall at all times remain directly, primarily and fully responsible and liable for the payment of the Rent herein specified and for compliance with all of Tenant’s other obligations under the terms, provisions and covenants of this Lease.

11. INSURANCE: FIRE AND CASUALTY DAMAGE

(a) Tenant agrees to reimburse Landlord for its proportionate share of the cost to maintain property insurance covering the Premises in an amount equal to the full replacement cost thereof, insuring against the perils of Fire, Lightning, Extended Coverage, Vandalism and Malicious Mischief, extended by Special Extended Coverage Endorsement to insure against all other risks of direct physical loss, such coverages and endorsements to be as defined, provided and limited in the standard bureau forms prescribed by the insurance regulatory authority for the State of Texas for use by insurance companies admitted in Texas for the writing of such insurance on risks located within Texas. Such insurance shall cover those risks of loss that a reasonable and prudent property owner of a like or similar building located in El Paso, Texas would insure against, including liability and loss of rents coverage. Subject to the provisions of subparagraphs 11(b), 11(d) and 11(e) below, such insurance shall be for the sole benefit of Landlord.

(b) If the Premises should be damaged or destroyed by any peril covered by the insurance to be provided by Landlord under subparagraph 11(a) above, Tenant shall give immediate notice thereof to Landlord and Landlord shall at its sole cost and expense thereupon proceed with reasonable diligence to rebuild and repair the Premises to substantially the condition in which they existed prior to such damage or destruction, except that Landlord shall not be required to rebuild, repair or replace any part of the partitions, fixtures, additions and other improvements which may have been placed in, on or about the Premises by Tenant. Unless the damage or destruction is due to the negligence or fault of Landlord, Tenant shall pay to Landlord upon demand Tenant’s proportionate share of any applicable deductible amounts specified under such insurance. The Rent payable hereunder shall abate or be reduced by reason of the damage or destruction, but only in the proportion that the damage or destruction prevents or materially interferes, in Landlord’s reasonable determination, with Tenant’s use of the Premises for the intended purpose hereunder.

(c) If the Premises should be damaged or destroyed by a casualty other than a peril covered by the insurance to be provided under subparagraph 11(a) above, and the casualty or loss was the result of an action or failure to act by Tenant or Tenant’s employees, agents, guests, customers, representatives or invitees, Tenant shall be responsible for the reasonable cost to rebuild and repair the Premises to substantially the condition in which they existed prior to such damage or destruction.

(d) Other than the improvements and build-out performed by Landlord as a condition to Tenant’s occupancy of the Premises, Tenant covenants and agrees to maintain insurance on all alterations, additions, partitions and improvements erected by, or on behalf of, Tenant, and all other property of Tenant located in, on or about the Premises

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

in an amount equal to the full replacement cost thereof. Such insurance shall insure against the perils and be in form, including stipulated endorsements, as provided in subparagraph 11(a) hereof. Such insurance shall be for the sole benefit of Tenant and under its sole control. All such policies shall be procured by Tenant from responsible insurance companies satisfactory to Landlord. Certificates of Insurance for each such policy of such insurance, together with receipt evidencing payment of the premiums therefore, shall be delivered to Landlord prior to the Commencement Date of this Lease. Not less than fifteen (15) days prior to the expiration date of any such policies, new Certificates of Insurance (bearing notations evidencing the payment of renewal premiums) shall be delivered to Landlord. Such policies shall further provide that not less than thirty (30) days written notice shall be given to Landlord before such policy may be canceled or changed to reduce insurance provided thereby. If requested by the holder of any indebtedness secured by a mortgage or Deed of Trust covering the Premises, certified copies of the insurance policies will need to be furnished in lieu of the certificates of insurance.

(e) Notwithstanding anything herein to the contrary, in the event the holder of any indebtedness secured by a mortgage or Deed of Trust covering the Premises requires that the insurance proceeds be applied to such indebtedness as a result of total loss or constructive total loss of the Premises, then the Landlord shall have the right to terminate this Lease by delivering written notice of termination to Tenant within fifteen (15) days after such requirement is made by any such holder whereupon all rights and obligations hereunder shall cease and terminate. The insurance proceeds arising out of any loss which is not a total loss or a constructive total loss shall be applied by Landlord in the manner prescribed in subparagraph 11(b) above.

(f) Notwithstanding any provision to the contrary contained herein, each party hereto hereby releases any and every claim which arises or may arise in its favor and against the other party hereto and/or such party’s agents, directors, officers, shareholders, partners, employees and affiliates during the Lease Term or any extension or renewal thereof for any and all injury, loss or damage to persons or property (regardless of whether such injury, loss or damage is the result of or caused by the negligent acts or omissions of the released party or any strict liability) arising from any cause that (a) would be insured against under the terms of any property or workers compensation insurance required to be carried hereunder; or (b) is insured against under the terms of any property or workers compensation insurance actually carried, regardless of whether it is required hereunder. Said waivers shall be in addition to, and not in limitation or derogation of, any other waiver or release contained in this Lease with respect to any injury, loss or damage to persons or property of the parties hereto. Each party hereto hereby agrees immediately to give to each insurance company which has issued to it policies of property or workers compensation insurance written notice of the terms of said mutual waivers, if necessary, and to have said insurance policies properly endorsed, if necessary, to prevent the invalidation of said insurance coverages by reason of said waivers.

12. LIABILITY. Unless caused by Landlord’s gross negligence or willful misconduct, Landlord shall not be liable to Tenant or to Tenant’s officers, directors, employees, agents, licensees, or visitors, or to any other person whomsoever, for any injury, loss or damage (regardless of whether such injury, loss or damage is caused by or arises out of Landlord’s negligence or the negligence of any employee or agent of Landlord or any strict liability) to person or property (i) due to the building or the land or any part thereof becoming out of repair or by defect in or failure of pipes or wiring, or by the backing up of drains or by the bursting or leaking of pipes, faucets and plumbing fixtures or by gas, water, steam, electricity or oil leaking, escaping or flowing into the Premises, or (ii) that may be occasioned by or through the acts or omissions of other tenants in the building or of any other persons whatsoever, or (iii) that may be occasioned by theft, fire, act of God, public enemy, injunction, riot, insurrection, war, court order, requisition or order of governmental authority, or any other matter beyond the control of Landlord. Tenant agrees that all Tenant’s property shall be at the risk of Tenant only, and that Landlord and Ground Lessor shall not be liable for any loss or damage thereto or theft thereof (regardless of whether such loss, damage or theft is caused by or arises out of Landlord’s negligence or the negligence of any employee or agent of Landlord or any strict liability), except where caused by the gross negligence or willful misconduct of Landlord. Tenant agrees to indemnify Landlord, its agents, directors, officers, shareholders, partners, employees and affiliates and Ground Lessor, and hold them harmless from any loss, expense or claims including attorneys’ fees, arising out of any damage or injury to the extent caused by the acts or omissions of Tenant, its employees, agents, contractors, invitees and subtenants. Tenant’s obligations pursuant to the foregoing indemnity shall survive the expiration or earlier termination of this Lease. Tenant shall procure and maintain throughout the Term of this Lease a general liability policy or policies of insurance, at its sole cost and expense, insuring Landlord and Ground Lessor (as additional insureds) and Tenant against all claims, demands, or actions arising out of or in connection with: (i) the Premises; (ii) the condition of the Premises; and (iii) Tenant’s operations in and maintenance and use of the Premises, and which coverage shall be primary. Such policy or policies shall afford protection with respect to bodily injury, death or property damage (including loss of use) of not less than Two Million Dollars ($2,000,000) each occurrence/Three Million Dollars ($3,000,000) aggregate, and shall include contractual liability coverage which insures contractual liability under the indemnification of Landlord and Ground Lessor by Tenant set forth in this Lease. Tenant shall also procure and maintain throughout the Term of this Lease a worker’s compensation insurance policy with applicable statutory limits. All such policies shall be procured by Tenant from responsible insurance companies satisfactory to Landlord. Certificates of Insurance for each such policies,

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

together with receipts evidencing payment of premiums therefor, shall be delivered to Landlord prior to the Commencement Date of this Lease, and not less than fifteen (15) days prior to the expiration date of any such policies, new Certificates of Insurance (bearing notations evidencing the payment of renewal premiums) shall be delivered to Landlord. Such policies shall further provide that not less than thirty (30) days written notice shall be given to Landlord before such policy may be canceled or changed to reduce insurance provided thereby. If requested by the holder of any indebtedness secured by a mortgage or deed of trust covering the Premises, certified copies of the insurance policies will need to be furnished in lieu of the Certificates of Insurance. If Tenant fails to comply with the foregoing requirements relating to insurance, Landlord may, following ten (10) days written notice to Tenant, obtain such insurance and Tenant shall pay to Landlord within thirty (30) days of receipt of an invoice the premium cost thereof.

Any and all covenants of Landlord contained in this Lease shall be binding upon Landlord and its successors only with respect to breaches occurring during its or their respective periods of ownership of the Landlord’s interest hereunder. Notwithstanding anything to the contrary contained herein, the liability of Landlord to Tenant for any default by Landlord under the terms of this Lease shall be limited to Landlord’s interest in the Project, and Tenant agrees to look solely to Landlord’s interest in the Project, of which the Premises is a part, for the recovery of any judgment against Landlord, it being intended that Landlord shall not be personally liable for any judgment or deficiency. Notwithstanding anything to the contrary contained herein, in no event shall Landlord be liable for special, incidental, consequential, exemplary or punitive damages. Before filing suit for an alleged default by Landlord, Tenant shall give Landlord, and any mortgagee of the building of whom Tenant has been notified, notice and reasonable time to cure the default.

13. CONDEMNATION.

(a) If the whole or any substantial part of the Premises, in Landlord’s reasonable opinion, should be taken for any public or quasi-public use under governmental law, ordinance or regulation, or by right of eminent domain, or by private purchase in lieu thereof, and the taking would prevent or materially interfere with the use of the Premises for the purpose for which they are being used, this Lease shall terminate and the Rent shall be abated during the unexpired portion of this Lease, effective when the physical taking of said Premises shall occur.

(b) If less than a substantial part of the Premises, in Landlord’s reasonable opinion, shall be taken for any public or quasi-public use under any governmental law, ordinance or regulation, or by right of Eminent Domain, or by private purchase in lieu thereof, this Lease shall not terminate, but the Rent payable hereunder during the unexpired portion of this Lease shall be reduced by an amount proportional to the amount of square footage taken.

(c) All compensation awarded in connection with or as a result of any of the foregoing proceedings shall be the property of Landlord and Tenant hereby assigns any interest in any such award to Landlord; provided, however, Landlord shall have no interest in any separate award made to Tenant for loss of business or goodwill or for the taking of Tenant’s fixtures and improvements, if a separate award for such items is made to Tenant.

14. HOLDING OVER. At the termination of this Lease by expiration or otherwise, Tenant shall remove all of Tenant’s trade fixtures and other items of personal property from the Premises and shall deliver possession to Landlord with all repairs and maintenance required herein to be performed by Tenant completed. If Tenant does not remove its property prior to termination, then, in addition to its other remedies at law or in equity, Landlord shall have the right to consider the property abandoned and such property may be removed by Landlord, at Tenant’s expense, or at Landlord’s option become Landlord’s property, and Tenant shall have no further rights relating thereto or for reimbursement therefor. If, for any reason, Tenant retains possession of the Premises after the expiration or termination of this Lease, unless the parties hereto otherwise agree in writing, such possession shall be subject to termination by either Landlord or Tenant at any time upon not less than ten (10) days advance written notice, and all of the other terms and provisions of this Lease shall be applicable during such period, except that Tenant shall pay Landlord from time to time, upon demand, as rental for the period of any hold over, an amount equal to double the Rent in effect on the expiration or termination date, computed on a daily basis for each day of the hold over period. No holding over by Tenant, whether with or without consent of Landlord, shall operate to extend this Lease except as otherwise expressly provided. The preceding provisions of this Paragraph 14 shall not be construed as Landlord’s consent for Tenant to hold over.

15. QUIET ENJOYMENT. Landlord covenants that it now has, or will acquire before Tenant takes possession of the Premises, good title to the Premises, free and clear, of all liens and encumbrances, excepting only the lien for current taxes not yet due, such mortgage or mortgages as are permitted by the terms of this Lease, zoning ordinances and other building and fire ordinances and governmental regulations relating to the use of such property, the provisions of the Ground Lease and easements, restrictions and other conditions of record. Landlord represents and warrants that it has full right and authority to enter into this Lease and that Tenant upon paying the Rent herein set forth and performing its other covenants and agreements herein set forth, shall peaceably and quietly enjoy the Premises for the

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

Term hereof without hindrance or molestation from Landlord or anyone claiming by or under Landlord, subject to the terms and provisions of this Lease.

16. EVENTS OF DEFAULT. The following events shall be deemed to be events of default by Tenant under this Lease:

(a) Tenant shall fail to pay any installment of the Rent hereby reserved when due, or any other payment or reimbursement to Landlord required herein, and such failure shall continue for a period of five (5) days from the date Landlord gives Tenant written notice that such amount is due; provided, however, Tenant shall not be entitled to more than one (1) such notice during any twelve (12) month period, and if after such notice any Rent or other payment due hereunder is not paid within five (5) days of when due, an event of default will be considered to have occurred without notice.

(b) Tenant shall become insolvent, or shall make a transfer in fraud of creditors, or shall make an assignment for the benefit of creditors.

(c) Tenant shall file a petition in bankruptcy or under any similar law or statute of the United States or any State thereof, or Tenant shall be adjudged bankrupt, or insolvent in proceedings filed against Tenant thereunder.

(d) A receiver or trustee shall be appointed for all or substantially all of the assets of Tenant.

(e) Tenant shall desert or vacate any substantial portion of the Premises.

(f) Tenant shall fail to comply with any term, provision or covenant of this Lease (other than the foregoing in this Paragraph 16) within the time period in which such term, provision or covenant is required to be performed by the terms of this Lease, or, if no time period is specified for performance, within thirty (30) days after written notice of such failure to Tenant (plus such additional time as may be reasonably necessary provided Tenant commences such cure within thirty (30) days and diligently pursues same to completion).

17. REMEDIES. Upon the occurrence of an event of default described in Paragraph 16 hereof, Landlord shall have the option to pursue any one or more of the following remedies without any notice or demand:

(a) Terminate this Lease, in which event Tenant shall immediately surrender the Premises to Landlord, and if Tenant fails so to do, Landlord may, without prejudice to any other remedy which it may have for possession or arrearages in Rent, enter upon and take possession of the Premises and expel or remove Tenant or any other person who may be occupying such Premises or any part thereof, without being liable for prosecution or any claim of damages therefor; and Tenant agrees to pay to Landlord on demand the amount of any loss and damage which Landlord may suffer by reason of such termination, whether through inability to relet the Premises on satisfactory terms or otherwise.

(b) Enter upon and take possession of the Premises without termination of this Lease and expel or remove Tenant and any other person who may be occupying such Premises or any part thereof, without being liable for prosecution or any claim of damages therefor; and relet the Premises and receive the rent therefor; and Tenant agrees to pay to the Landlord on demand any deficiency that may arise by reason of such reletting. In the event Landlord is successful in reletting the Premises at a rental in excess of that agreed to be paid by Tenant pursuant to the terms of this Lease, Landlord and Tenant each mutually agree that Tenant shall not be entitled, under any circumstances, to such excess rental, and Tenant does hereby specifically waive any claim to such excess rental.

(c) Terminate this Lease and treat the event of default as an entire breach of this Lease and Tenant immediately shall become liable to Landlord for damages for the entire breach in the amount equal to the amount of additional Rent which would be payable by Tenant during the unexpired balance of the Term of this Lease and all other payments due for the balance of the Term, adjusted to present value. In the event Landlord elects to so accelerate the Rent due hereunder, Landlord shall use reasonable efforts to relet the Premises, and if Landlord is successful in reletting the Premises during the unexpired balance of the Term of the Lease, Landlord shall offset the rent received by Landlord for such unexpired portion of the Term as a result of any reletting against the amount of additional Rent owed by Tenant. Landlord and Tenant each mutually agree that Tenant shall not be entitled, under any circumstances, to any excess rental obtained by Landlord as a result of any reletting, and Tenant does hereby specifically waive any claim to such excess rental. Such amount shall be due and payable upon Landlord’s notice to Tenant of termination of the Lease and shall bear interest until paid at the maximum annual rate permitted by law.

(d) Enter upon the Premises, without being liable for prosecution or any claim of damages therefor, and do whatever Tenant is obligated to do under the terms of this Lease; and Tenant agrees to reimburse Landlord on demand for any expenses which Landlord may incur in thus effecting compliance with Tenant’s obligations under this Lease,

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

and Tenant further agrees that Landlord shall not be liable for any damages resulting to the Tenant from such action, whether caused by the negligence of Landlord or otherwise.

(e) Alter locks and other security devices at the Premises without being liable for prosecution or any claim of damages therefor, and such alteration of locks and security devices shall not be deemed unauthorized or constitute a conversion.

(f) Receive payment from Tenant, in addition to any sum provided to be paid above, for any and all of the following expenses for which Tenant shall be considered liable:

1. Broker’s fees incurred by Landlord in connection with reletting the whole or any part of the Premises;

2. The cost of removing and storing Tenant’s or other occupant’s property;

3. The cost of repairing, altering, remodeling or otherwise putting the Premises into the condition in which they were required to be put upon termination of this Lease, plus a reasonable charge to cover Landlord’s overhead; and

4. All reasonable expenses incurred by Landlord in enforcing Landlord’s remedies.

In the event Tenant fails to pay any installment of Rent hereunder within five (5) days after such installment is due, to help defray the additional cost to Landlord for processing such late payments Tenant shall pay to Landlord on demand a late charge in an amount equal to five percent (5%) of such installment; and the failure to pay such late charges within ten (10) days after demand therefor shall be an event of default hereunder. The provision for such late charge shall be in addition to all of Landlord’s other rights and remedies hereunder or at law and shall not be construed as liquidated damages or as limiting Landlord’s remedies in any manner.

Pursuit of any of the foregoing remedies shall not preclude pursuit of any of the other remedies herein provided or any other remedies provided by law, nor shall pursuit of any remedy herein provided constitute a forfeiture or waiver of any Rent due to Landlord hereunder or of any damages accruing to Landlord by reason of the violation of any of the terms, provisions and covenants herein contained. No act or thing done by the Landlord or its agents during the Term hereby granted shall be deemed a termination of this Lease or an acceptance of the surrender of the Premises, and no agreement to terminate this Lease or to accept a surrender of said Premises shall be valid unless in writing and signed by Landlord, no waiver by Landlord of any violation or breach of any of the terms, provisions and covenants herein contained shall be deemed or construed to constitute a waiver of any other violation or breach of any of the other terms, provisions and covenants herein contained. Landlord’s acceptance of the payment of rental or other payments hereunder after the occurrence of an event of default shall not be construed as a waiver of such default, unless Landlord so notifies Tenant in writing. Forbearance by Landlord to enforce one or more of the remedies herein provided upon an event of default shall not be deemed or construed to constitute a waiver of such default or of any subsequent default. If, on account of any breach or default by Tenant in Tenant’s obligations under the terms and conditions of this Lease, it shall become necessary or appropriate for Landlord to employ or consult with an attorney concerning any of Landlord’s rights or remedies hereunder or to enforce or defend any of the Landlord’s rights or remedies hereunder, Tenant agrees to pay any reasonable attorneys fees so incurred.

18. LANDLORD’S LIEN. [Intentionally omitted].

19. MORTGAGES AND GROUND LEASES. This Lease shall be subordinate to the Ground Lease and to any deed of trust, mortgage, or other security instrument (a “Mortgage”) that hereafter covers all or any part of the Premises or the Project. The mortgagee under any Mortgage is referred to herein as “Landlord’s Mortgagee”. Landlord shall use commercially reasonable efforts to obtain a recognition and non-disturbance agreement in commercially reasonable form from any future Landlord’s Mortgagee whereby such Landlord’s Mortgagee agrees not to disturb the possession of Tenant and to recognize Tenant’s rights under this Lease in the event such Landlord’s Mortgagee obtains possession of the Premises or Project through foreclosure or otherwise for so long as Tenant is not in default hereunder.

Tenant shall attorn to any party succeeding to Landlord’s interest in the Premises, whether by purchase, foreclosure, deed in lieu of foreclosure, power of sale, termination of lease, or otherwise, upon such party’s request, and shall execute such agreements confirming such attornment as such party may reasonably request. In the event of such request and upon Tenant’s attornment as aforesaid, Tenant will automatically become the tenant of the successor to Landlord’s interest without change in the terms or provisions of this Lease; provided, however, that such successor to Landlord’s interest shall not be bound by (a) an payment of Rent for more than one month in advance (except prepayments for security deposits, if any), (b) any amendments or modifications of this Lease made without the prior

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

written consent of Landlord’s Mortgagee if Tenant was advised on the interest of the same, or (c) any credits, offsets, defenses or claims which Tenant may have against Landlord.

Tenant shall not seek to enforce any remedy it may have for any default on the part of the Landlord without first giving written notice by certified mail, return receipt requested, specifying the default in reasonable detail, to any Landlord’s Mortgagee, whose address has been given to Tenant, and affording such Landlord’s Mortgagee a reasonable opportunity to perform Landlord’s obligations hereunder. Subject to the provisions of Paragraph 12 hereof, Landlord reserves the right, without notice to or consent of the Tenant, to assign this Lease and/or any and all Rent hereunder as security for the payment of any Mortgage.

Tenant agrees at any time and from time to time during the Term to execute, acknowledge and deliver to Landlord and/or Landlord’s designee within seven (7) days of any request by Landlord, a statement or statements, in writing, certifying (if such be true) that a copy of this Lease and any amendments hereto are true and correct copies, this Lease is unmodified and in good standing (or if modified, then in good standing as modified, stating the modification), the date to which all Rent and other charges hereunder have been paid in advance, and any other items reasonably requested of Tenant. From time to time, Tenant shall furnish to any Landlord’s Mortgagee, within ten (10) days after a request therefor, such estoppel certificates, non-disturbance and attornment agreements, or other certificates as Landlord’s Mortgagee may reasonably request.

20. LANDLORD’S DEFAULT.

(a) In the event Landlord should default in any of its obligations hereunder, Tenant shall simultaneously give Landlord and Landlord’s Mortgagee (if Landlord has given Tenant written advance notice of such mortgagee’s interest and address) written notice specifying such default and Landlord shall thereupon have thirty (30) days (plus an additional reasonable period as may be required in the exercise by Landlord of due diligence) in which to cure any such default. In addition, Landlord’s Mortgagee shall have the right (but not the obligation) to cure or remedy such default during the period that is permitted to Landlord hereunder, plus an additional period of thirty (30) days, and Tenant will accept such curative or remedial action taken by Landlord’s Mortgagee with the same effect as if such action had been taken by Landlord,

(b) Upon the failure of Landlord or Landlord’s Mortgagee to cure such default in accordance with the provisions of Paragraph 20(a) hereof, Tenant shall be authorized and empowered to perform the obligations which Landlord failed to perform, and the reasonable costs incurred by Tenant in so doing, together with any interest or penalty required to be paid in connection therewith, shall be payable on demand by Landlord to Tenant. Tenant’s exclusive remedy shall be self-help as set forth herein and an action for damages against Landlord, and Tenant hereby waives the benefit of any laws granting Tenant a lien upon the property of Landlord and/or upon Rent due Landlord.

21. ASSIGNMENT BY LANDLORD. Landlord shall have the right to assign or transfer, in whole or in part every feature of its rights and obligations hereunder and the Premises provided such assignee or transferee recognizes and agrees to be bound by the terms of this Lease. Such assignments or transfers may be made to a corporation, trust, trust company, individual or group of individuals, and howsoever made shall be in all things respected and recognized by Tenant.

22. DISCLAIMER. This Lease and the obligation of Tenant to pay Rent hereunder and perform all of the other covenants and agreements hereunder on the part of the Tenant to be performed shall not be affected, impaired or excused because Landlord is unable to fulfill any of its covenants and obligations under this Lease, expressly or impliedly to be performed by Landlord, if Landlord is prevented or delayed from doing so by reason of strikes, labor troubles, accident, adjustment of insurance, or by any reason or cause whatsoever reasonably beyond Landlord’s control. Reasons beyond Landlord’s control shall include, but not be limited to, laws, governmental preemption in connection with a National Emergency or by any reason of any rule, order or regulation of any governmental agency, federal, state, county or municipal authority or any department or subdivision thereof, or by reason of the conditions of supply and demand which have been or are affected by war or other emergency.

23. MECHANIC’S LIENS. Tenant shall have no authority, express or implied, to create or place any lien or encumbrance, of any kind or nature whatsoever, upon, or in any manner to bind, the interest of Landlord in the Premises for any claim in favor of any person dealing with Tenant, including those who may furnish materials or perform labor for any construction or repairs, and each such claim shall affect and each such lien shall attach to, if at all, only the leasehold interest granted to Tenant by this instrument. Tenant covenants and agrees that it will pay or cause to be paid all sums legally due and payable by it on account of any labor performed or materials furnished in connection with any work performed on the Premises on which any lien is or can be validly and legally asserted against its leasehold interest in the Premises or the improvements thereon, and that it will save and hold Landlord harmless from any and all loss, cost or expense based on or arising out of asserted claims or liens against the leasehold estate, or

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

against the right, title and interest of the Landlord in the Premises or under the terms of this Lease. In the event any such lien is attached to the Premises or any portion thereof, Tenant shall cause the same to be discharged of record within twenty (20) days after filing of same.

24. NOTICES. Each provision of this instrument or of any applicable governmental laws, ordinances, regulations and other requirements with reference to the sending, mailing or delivery of any notice or the making of any payment by Landlord to Tenant or with reference to the sending, mailing or delivery of any notice or the making of any payment by Tenant to Landlord shall be deemed to be complied with when and if the following steps are taken:

(a) All Rent and other payments required to be made by Tenant to Landlord hereunder shall be payable to Landlord at the address hereinbelow set forth or at such other address as Landlord may specify from time to time by written notice delivered in accordance herewith. Tenant’ s obligation to pay Rent and any other amounts to Landlord under the terms of this Lease shall not be deemed satisfied until Rent and other amounts have been actually received by Landlord.

(b) All payments required to be made by Landlord to Tenant hereunder shall be payable to Tenant at the address hereinbelow set forth, or at such other address within the continental United States as Tenant may specify from time to time by written notice delivered in accordance herewith.

(c) Any notice or document required or permitted to be delivered hereunder may be personally delivered, sent via nationally recognized overnight courier or placed in the United States mail, postage prepaid, registered or certified mail, return receipt requested, addressed in each case to the parties hereto at the respective addresses set out below, or at such other address as the parties have theretofore specified by written notice delivered in accordance herewith. A notice shall be deemed to be effective (a) when delivered personally, (b) if sent by registered or certified mail or overnight delivery service, at the time the delivery is indicated on the duly completed United States Postal Service return receipt, or (c) the time of package delivery as indicated on the records of or certificates provided by the overnight delivery service:

|

LANDLORD: |

|

TENANT: |

|

|

|

|

|

|

|

EastGroup Properties, L.P. |

|

UFP Technologies Inc., |

|

|

c/o NDH Property Management |

|

172 East Main Street |

|

|

7400 Viscount, Suite 112 |

|

Georgetown, MA 01833 |

|

|

El Paso, Texas 79925 |

|

Attention: Ron Lataille |

|

|

Attention: Nancy De Haro |

|

|

|

|

|

|

|

|

|

With copy to: |

|

With copy to: |

|

|

EastGroup Properties, L.P. |

|

Owen B. Lynch, Esq. |

|

|

4220 World Houston Parkway, Suite 170 |

|

Lynch, Brewer, Hoffman & Fink, LLP |

|

|

Houston, Texas 77032 |

|

75 Federal Street, Floor 7 |

|

|

Attention: Asset Manager |

|

Boston, MA 02110 |

|

If and when included within the term “Landlord”, as used in this instrument, there are more than one person, firm or corporation, all shall jointly arrange among themselves for their joint execution of such a notice specifying some individual at some specific address for the receipt of notices and payments to Landlord; if and when included within the term “Tenant”, as used in this instrument, there are more than one person, firm or corporation, all shall jointly arrange among themselves for their joint execution of such a notice specifying some individual at some specific address within the continental United States for the receipt of notices and payments to Tenant. All parties included within the terms “Landlord” and “Tenant”, respectively, shall be bound by notices given in accordance with the provisions of this Paragraph to the same effect as if each had received such notice.

25. MISCELLANEOUS.

(a) Words of any gender used in this Lease shall be held and construed to include any other gender and words in the singular number shall be held to include the plural, unless the context otherwise requires.

(b) The terms, provisions, covenants and conditions contained in this Lease shall apply to, inure to the benefit of, and be binding upon, the parties hereto and upon their respective heirs, legal representatives, successors and permitted assigns except as otherwise herein expressly provided.

(c) Because the Premises are on the open market and are presently being shown, this Lease shall be treated as an offer with the Premises being subject to prior lease and such offer subject to withdrawal or non-acceptance by Landlord

|

Initials: |

/s/ KS |

|

/s/ RL |

|

|

Landlord |

|

Tenant |

or to other use of the Premises without notice, and this Lease shall not be valid or binding unless and until accepted by Landlord in writing and a fully executed copy delivered to both parties.

(d) The captions inserted in this Lease are for convenience only and in no way define, limit or otherwise describe the scope or intent of this Lease, or any provision hereof, or in any way affect the interpretation of this Lease.

(e) All obligations of Tenant hereunder not fully performed upon the expiration or earlier termination of the Term of this Lease shall survive the expiration or earlier termination of the Term hereof, including, without limitation, all payment obligations with respect to taxes and insurance and all obligations concerning the condition of the Premises. Upon the expiration or termination of the Term hereof, and prior to Tenant vacating the Premises, Tenant shall put the Premises, including, without limitation, all heating and air conditioning systems and equipment therein, in good condition and repair, reasonable wear and tear excepted, including, but not limited to, removal of Tenant’s Initial Installations and other alterations and restoration of the Premises as set forth in Paragraph 6(c) above, and shall pay to Landlord the amount, if any, as reasonably estimated by Landlord, of Tenant’s proportionate share of Taxes and insurance premiums for the pro-rata portion of the year in which the Lease expires or terminates. All such amounts shall be used and held by Landlord for payment of such obligations of Tenant hereunder, with Tenant being liable for any additional costs therefor upon demand by Landlord, or with any excess to be returned to Tenant after all such obligations have been determined and satisfied, as the case may be. Any security deposit held by Landlord shall be credited against the amount payable by Tenant under this Paragraph 25(e).

(f) If any clause or provision of this Lease is illegal, invalid or unenforceable under present or future laws effective during the Term of this Lease, then and in that event, it is the intention of the parties hereto that the remainder of this Lease shall not be affected thereby, and it is also the intention of the parties to this Lease that, in lieu of each clause or provision of this Lease that is illegal, invalid or unenforceable, there be added as a part of this Lease contract a clause or provision as similar in terms to such illegal, invalid or unenforceable clause or provision as may be possible and be legal, valid and enforceable.

(g) The Effective Date of this Lease shall be the date on which the last of Landlord or Tenant has executed this Lease. All references in this Lease to “the date hereof” or similar references shall be deemed to refer to the Effective Date.