SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

|

o |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

o |

SHELL COMPANY REPORT PURSUANT TO SECTION 23 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number: 001-12440

|

ENERSIS S.A. |

|

(Exact name of Registrant as specified in its charter) |

|

|

|

ENERSIS S.A. |

|

(Translation of Registrant’s name into English) |

|

|

|

CHILE |

|

(Jurisdiction of incorporation or organization) |

|

|

|

SANTA ROSA 76, SANTIAGO, CHILE |

|

(Address of principal executive offices) |

|

|

|

Nicolás Billikopf, phone: (56-2) 353-4639, fax: (56-2) 378-4789, nbe@enersis.cl, Santa Rosa 76, Piso 15, Santiago, Chile |

|

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

|

|

American Depositary Shares representing Common Stock |

|

New York Stock Exchange |

|

|

|

Common Stock, no par value * |

|

New York Stock Exchange |

|

|

|

$ 249,734,000 7.40% Notes due December 1, 2016 |

|

New York Stock Exchange |

|

|

|

$ 858,000 6.60% Notes due December 1, 2026 |

|

New York Stock Exchange |

|

*Listed, not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

$ 350,000,000 7.375% Notes due January 15, 2014

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

|

Shares of Common Stock: |

32,651,166,465 |

|

|

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act:

x Yes o No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934:

o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days:

x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

o Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act:

|

Large accelerated filer x |

Accelerated filer o |

Non-accelerated filer o |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP o |

International Financial Reporting Standards as issued |

Other o |

Indicate by check mark which financial statement item the registrant has elected to follow:

o Item 17 x Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act):

o Yes x No

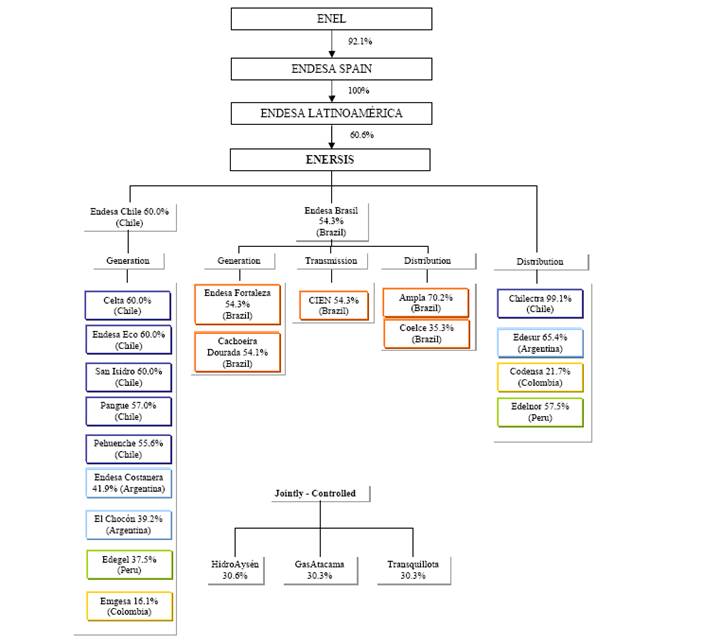

“Enersis’ Simplified Organizational Structure” (1)

As of December 31, 2011

(1) Only principal operating subsidiaries are presented here. The percentages listed for each of our subsidiaries represents Enersis’ economic interest in such subsidiary.

|

|

|

|

Page | |

|

|

|

|

| |

|

|

|

4 | ||

|

|

|

8 | ||

|

|

8 | |||

|

|

9 | |||

|

|

9 | |||

|

|

9 | |||

|

|

|

10 | ||

|

|

10 | |||

|

|

10 | |||

|

|

10 | |||

|

|

22 | |||

|

|

96 | |||

|

|

97 | |||

|

|

126 | |||

|

|

135 | |||

|

|

137 | |||

|

|

139 | |||

|

|

141 | |||

|

|

154 | |||

|

|

158 | |||

|

|

|

159 | ||

|

|

159 | |||

|

Material Modifications to the Rights of Security Holders and Use of Proceeds |

|

159 | ||

|

|

159 | |||

|

|

160 | |||

|

|

160 | |||

|

|

161 | |||

|

|

162 | |||

|

Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

|

162 | ||

|

|

162 | |||

|

|

162 | |||

|

|

|

163 | ||

|

|

163 | |||

|

|

163 | |||

|

|

163 | |||

|

Acciona |

|

Acciona, S.A. |

|

Spanish construction holding company. Together with Enel, Acciona held a controlling interest in Endesa Spain until June 25, 2009. |

|

|

|

|

|

|

|

AFP |

|

Administradora de Fondos de Pensiones |

|

A legal entity that manages a Chilean pension fund. |

|

|

|

|

|

|

|

Ampla |

|

Ampla Energia e Serviços S.A. |

|

Brazilian distribution company operating in Rio de Janeiro, owned by Endesa Brasil, a subsidiary of Enersis. |

|

|

|

|

|

|

|

ANEEL |

|

Agéncia Nacional de Energia Elétrica |

|

Brazilian governmental agency for electric energy. |

|

|

|

|

|

|

|

Betania |

|

Central Hidroeléctrica de Betania S.A. E.S.P. |

|

A former Endesa Chile’s Colombian subsidiary which merged with Emgesa, another Endesa Chile subsidiary, in 2007. |

|

|

|

|

|

|

|

Cachoeira Dourada |

|

Centrais Elétricas Cachoeira Dourada S.A. |

|

Brazilian generation company owned by Endesa Brasil, a subsidiary of Enersis. |

|

|

|

|

|

|

|

CAM |

|

Compañía Americana de Multiservicios Ltda. |

|

A former Enersis’ subsidiary engaged in the electrical parts procurement business. |

|

|

|

|

|

|

|

CAMMESA |

|

Compañía Administradora del Mercado Mayorista Eléctrico S.A. |

|

Argentine autonomous entity in charge of the operation of the Mercado Eléctrico Mayorista (Wholesale Electricity Market), or MEM. CAMMESA’s stockholders are generation, transmission and distribution companies, large users and the Secretariat of Energy. |

|

|

|

|

|

|

|

CDEC |

|

Centro de Despacho Económico de Carga |

|

Autonomous entity in two Chilean electric systems in charge of coordinating the efficient operation and dispatch of generation units to satisfy demand. |

|

|

|

|

|

|

|

Celta |

|

Compañía Eléctrica Tarapacá S.A. |

|

Endesa Chile’s subsidiary that operates in the SING with thermal plants. |

|

|

|

|

|

|

|

Cemsa |

|

Endesa Cemsa S.A. |

|

Energy trading company with operations in Argentina, a subsidiary of Endesa Chile. |

|

|

|

|

|

|

|

Chilectra |

|

Chilectra S.A. |

|

Chilean electricity distribution company operating in the Santiago metropolitan area, a subsidiary of Enersis. |

|

|

|

|

|

|

|

CIEN |

|

Companhia de Interconexão Energética S.A. |

|

Brazilian transmission company, wholly-owned by Endesa Brasil, a subsidiary of Enersis. |

|

|

|

|

|

|

|

CNE |

|

Comisión Nacional de Energía |

|

Chilean National Energy Commission, governmental entity with responsibilities under the Chilean regulatory framework. |

|

|

|

|

|

|

|

Codensa |

|

Codensa S.A. E.S.P. |

|

Colombian distribution company that operates mainly in Bogotá, and is a subsidiary of Enersis. |

|

|

|

|

|

|

|

Coelce |

|

Companhia Energética do Ceará S.A. |

|

Brazilian distribution company operating in the state of Ceará. Coelce is controlled by Endesa Brasil, a subsidiary of Enersis. |

|

COES |

|

Comité de Operación Económica del Sistema |

|

Peruvian entity in charge of coordinating the efficient operation and dispatch of generation units to satisfy demand. |

|

|

|

|

|

|

|

CREG |

|

Comisión de Regulación de Energía y Gas |

|

Colombian Commission for the Regulation of Energy and Gas. |

|

|

|

|

|

|

|

CTM |

|

Compañía de Transmisión del Mercosur S.A. |

|

Endesa Brasil’s subsidiary transmission company with operations in Argentina. |

|

|

|

|

|

|

|

DECSA |

|

Distribuidora Eléctrica de Cundinamarca S.A. |

|

Colombian distribution company, subsidiary of Codensa. |

|

|

|

|

|

|

|

Edegel |

|

Edegel S.A.A. |

|

Peruvian generation company, subsidiary of Endesa Chile. |

|

|

|

|

|

|

|

Edelnor |

|

Empresa de Distribución Eléctrica de Lima Norte S.A.A. |

|

Peruvian distribution company with a concession area in the northern part of Lima, and a subsidiary of Enersis. |

|

|

|

|

|

|

|

Edesur |

|

Empresa Distribuidora Sur S.A. |

|

Argentine distribution company with concession area in the south of the Buenos Aires greater metropolitan area, and a subsidiary of Enersis. |

|

|

|

|

|

|

|

EEB |

|

Empresa de Energía de Bogotá S.A. |

|

Colombian stated-owned financial and energy holding company, with investments in the electricity generation, transmission, trading and distribution sectors; and in the natural gas transmission, distribution and trading sectors. |

|

|

|

|

|

|

|

EEC |

|

Empresa de Energía de Cundinamarca S.A. |

|

Colombian electricity distribution company, subsidiary of DECSA. |

|

|

|

|

|

|

|

El Chocón |

|

Hidroeléctrica El Chocón S.A. |

|

Endesa Chile’s Argentine generation subsidiary with two hydroelectric plants, El Chocón and Arroyito, both located in the Limay River, Argentina. |

|

|

|

|

|

|

|

Elesur |

|

Elesur S.A. |

|

A former Chilean subsidiary of Enersis that absorbed Chilectra, and later changed its name to Chilectra. |

|

|

|

|

|

|

|

Emgesa |

|

Emgesa S.A. E.S.P. |

|

Colombian generation company controlled by Endesa Chile. |

|

|

|

|

|

|

|

Endesa Brasil |

|

Endesa Brasil S.A. |

|

Brazilian holding company, a subsidiary of Enersis. |

|

|

|

|

|

|

|

Endesa Chile |

|

Empresa Nacional de Electricidad S.A. |

|

Our generation subsidiary with consolidated operations in four countries in South America. |

|

|

|

|

|

|

|

Endesa Costanera |

|

Endesa Costanera S.A. |

|

Argentine generation company controlled by Endesa Chile. |

|

|

|

|

|

|

|

Endesa Eco |

|

Endesa Eco S.A. |

|

Chilean electricity company, owner of Central Eólica Canela S.A. and Ojos de Agua mini hydro plant. Endesa Eco is an Endesa Chile subsidiary. |

|

|

|

|

|

|

|

Endesa Fortaleza |

|

Central Geradora Termelétrica Fortaleza S.A. |

|

Operates a combined cycle generating plant, located in the state of Ceará. Endesa Fortaleza is wholly-owned by our subsidiary Endesa Brasil. |

|

|

|

|

|

|

|

Endesa Latinoamérica |

|

Endesa Latinoamérica, S.A.U. |

|

A subsidiary of Endesa Spain and our direct controller, formerly known as Endesa Internacional, S.A.U. |

|

Endesa Spain |

|

Endesa, S.A. |

|

A Spanish electricity generation and distribution company with a 60.6% beneficial interest in Enersis. |

|

|

|

|

|

|

|

Enel |

|

Enel S.p.A. |

|

Italian power company, with a 92.1% controlling ownership of Endesa Spain. |

|

|

|

|

|

|

|

Enersis |

|

Enersis S.A. |

|

Our company, a publicly held limited liability stock company incorporated under the laws of the Republic of Chile, with subsidiaries engaged primarily in the generation, transmission and distribution of electricity in Chile, Argentina, Brazil, Colombia and Peru. Registrant of this Report. |

|

|

|

|

|

|

|

ENRE |

|

Ente Nacional Regulador de la Electricidad |

|

Argentine national regulatory authority for the energy sector. |

|

|

|

|

|

|

|

ESM |

|

Extraordinary Shareholders Meeting |

|

Extraordinary Shareholders Meeting |

|

|

|

|

|

|

|

Etevensa |

|

Empresa de Generación Termoeléctrica Ventanilla S.A. |

|

Peruvian generation company that merged with Edegel in 2006. |

|

|

|

|

|

|

|

FONINVEMEM |

|

Fondo para Inversiones Necesarias que permitan Incrementar la Oferta de Energía Eléctrica en el Mercado Eléctrico Mayorista |

|

Argentine fund created to increase electricity supply in the MEM. |

|

|

|

|

|

|

|

GasAtacama |

|

GasAtacama S.A. |

|

Company involved in gas transportation and electricity generation in northern Chile that is 50% owned by Endesa Chile. |

|

|

|

|

|

|

|

Gener |

|

AES Gener S.A. |

|

Chilean generation company that competes with the Company in Chile, Argentina and Colombia. |

|

|

|

|

|

|

|

GNLQ |

|

GNL Quintero S.A. |

|

Company created to develop, build, finance, own and operate a LNG regasification facility at Quintero Bay (Chile) in which LNG is unloaded, stored and regasified. |

|

|

|

|

|

|

|

IDR |

|

Issuer Default Rating |

|

Reflects the relative vulnerability of an entity to default on its financial obligations. |

|

|

|

|

|

|

|

IFRS |

|

International Financial Reporting Standards |

|

Accounting standards adopted by the Company on January 1, 2009. |

|

|

|

|

|

|

|

IMV |

|

Inmobiliaria Manso de Velasco Ltda. |

|

Enersis’ wholly-owned subsidiary engaged in the real estate business. |

|

|

|

|

|

|

|

LNG |

|

Liquefied Natural Gas. |

|

Liquefied natural gas. |

|

|

|

|

|

|

|

MEM |

|

Mercado Eléctrico Mayorista |

|

Wholesale Electricity Market in Argentina. |

|

|

|

|

|

|

|

MME |

|

Ministério de Minas e Energia |

|

Brazilian Ministry of Mines and Energy. |

|

|

|

|

|

|

|

NCRE |

|

Non Conventional Renewable Energy |

|

Energy sources which are continuously replenished by natural processes, such as wind, biomass, mini-hydro, geothermal, wave or tidal energy. |

|

|

|

|

|

|

|

NIS |

|

Sistema Interconectado Nacional |

|

National interconnected electric system. There are such systems in Chile, Argentina, Brazil and Colombia. |

|

ONS |

|

Operador Nacional do Sistema Elétrico |

|

Electric System National Operator. Brazilian non-profit private entity responsible for the planning and coordination of operations in interconnected systems. |

|

|

|

|

|

|

|

Osinergmin |

|

Organismo Supervisor de la Inversión en Energía y Minería |

|

Energy and Mining Investment Supervisor Authority, the Peruvian regulatory electricity authority. |

|

|

|

|

|

|

|

OSM |

|

Ordinary Shareholders Meeting |

|

Ordinary Shareholders Meeting |

|

|

|

|

|

|

|

Pangue |

|

Empresa Eléctrica Pangue S.A. |

|

Chilean electricity company, owner of the Pangue power station. Pangue is an Endesa Chile subsidiary. |

|

|

|

|

|

|

|

Pehuenche |

|

Empresa Eléctrica Pehuenche S.A. |

|

Chilean electricity company, owner of three power stations in the Maule River basin. Pehuenche is an Endesa Chile subsidiary. |

|

|

|

|

|

|

|

San Isidro |

|

Compañía Eléctrica San Isidro S.A. |

|

Chilean electricity company, owner of a thermal power station. San Isidro is wholly-owned by Endesa Chile. |

|

|

|

|

|

|

|

SEF |

|

Superintendencia de Electricidad y Combustible |

|

Chilean Superintendency of Electricity and Fuels, a Governmental entity in charge of supervising the Chilean electricity industry. |

|

|

|

|

|

|

|

SEIN |

|

Sistema Eléctrico Interconectado Nacional |

|

Peruvian interconnected electric system. |

|

|

|

|

|

|

|

SIC |

|

Sistema Interconectado Central |

|

Chilean central interconnected electric system covering all of Chile except the north and the extreme south. |

|

|

|

|

|

|

|

SING |

|

Sistema Interconectado del Norte Grande |

|

Electric interconnected system operating in northern Chile. |

|

|

|

|

|

|

|

SVS |

|

Superintendencia de Valores y Seguros |

|

Chilean authority in charge of supervising public companies, securities and the insurance business. |

|

|

|

|

|

|

|

TESA |

|

Transportadora del Energía de Mercosur S.A. |

|

Endesa Brasil’s transmission company subsidiary with operations in Argentina. |

|

|

|

|

|

|

|

UF |

|

Unidad de Fomento |

|

Chilean inflation-indexed, peso-denominated monetary unit. |

|

|

|

|

|

|

|

UTA |

|

Unidad Tributaria Anual |

|

Chilean annual tax unit. One UTA equals 12 UTM. |

|

|

|

|

|

|

|

UTM |

|

Unidad Tributaria Mensual |

|

Chilean inflation-indexed monthly tax unit used to define fines, among other purposes. |

|

|

|

|

|

|

|

VAD |

|

Valor Agregado de Distribución |

|

Value added from distribution of electricity. |

|

|

|

|

|

|

|

VNR |

|

Valor Nuevo de Reemplazo |

|

The net replacement value of electricity assets. |

As used in this Report on Form 20-F, first person personal pronouns such as “we,” “us” or “our” refer to Enersis S.A. (Enersis or the Company) and our consolidated subsidiaries unless the context indicates otherwise. Unless otherwise noted, our interest in our principal subsidiaries, jointly —controlled entities and associates is expressed in terms of our economic interest as of December 31, 2011.

We are a Chilean company engaged through our subsidiaries and jointly-controlled entities in the electricity generation, transmission and distribution businesses in Chile, Argentina, Brazil, Colombia and Peru. As of the date of this Report, we own 60.0% of Empresa Nacional de Electricidad S.A. (Endesa Chile, a Chilean electricity generation company) and 99.1% of Chilectra S.A. (Chilectra, a Chilean electricity distribution company). As of the same date, Endesa, S.A. (Endesa Spain), a Spanish electricity generation and distribution company, owns 60.6% of Enersis. Enel S.p.A. (Enel), an Italian generation and distribution company, owns 92.1% of Endesa Spain through a wholly-owned subsidiary.

In this Report on Form 20-F, unless otherwise specified, references to “dollars” or “$,” are to dollars of the United States of America; references to “pesos” or “Ch$” are to Chilean pesos, the legal currency of Chile; references to “Ar$” or “Argentine pesos” are to the legal currency of Argentina; references to “R$” or “reais” are to Brazilian reals, the legal currency of Brazil; references to “soles” are to Peruvian Nuevo Sol, the legal currency of Peru; references to “CPs” or “Colombian pesos” are to the legal currency of Colombia; references to “€” or “Euros” are to the legal currency of the European Union; and references to “UF” are to Unidades de Fomento.

The Unidad de Fomento is a Chilean inflation-indexed, peso-denominated monetary unit. The UF rate is set daily in advance based on changes in the previous month’s inflation rate. As of December 31, 2011, UF 1 was equivalent to Ch$ 22,294.03. The dollar equivalent of UF 1 was $ 42.94 as of December 31, 2011, using the Observed Exchange Rate reported by the Banco Central de Chile (the “Chilean Central Bank,” or the “Central Bank”) as of December 31, 2011 of Ch$ 519.20 per $ 1.00. As of March 31, 2012, UF 1 was equivalent to Ch$ 22,533.51. The dollar equivalent of UF 1 was $ 46.01 at March 31, 2012, using the observed Exchange Rate reported by the Central Bank as of such date of Ch$ 489.76 per $ 1.00.

Our Consolidated Financial Statements and, unless otherwise indicated, other financial information concerning Enersis included in this Report are presented in pesos. Until the year ended December 31, 2008, Enersis prepared its financial statements in accordance with generally accepted accounting principles in Chile (Chilean GAAP). Since January 1, 2009, Enersis has prepared its financial statements in accordance with International Financial Reporting Standards (IFRS), as issued by the International Accounting Standard Board (IASB).

The subsidiaries are consolidated and all their assets, liabilities, income, expenses and cash flows are included in the consolidated financial statements after making the adjustments and eliminations related to intra-Group transactions.

Jointly-controlled entities, which are those that do not have a controlling shareholder but are governed by a joint management agreement, are consolidated by the proportional consolidation method. Enersis recognizes, line by line, its share of the assets, liabilities, income, expenses and cash flow of such entities, subject to accounting eliminations.

Investments in associates in which the Company has significant influence, are recorded in our Consolidated Financial Statements under the equity method.

For detailed information regarding subsidiaries, jointly-controlled entities and associates, see Appendix No. 1 and No. 3 to the Consolidated Financial Statements.

For the convenience of the reader, this Report contains translations of certain peso amounts into dollars at specified rates. Unless otherwise indicated, the dollar equivalent for information in pesos is based on the Observed Exchange Rate as of December 31, 2011, as defined in “Item 3. Key Information — A. Selected Financial Data — Exchange Rates” The Federal Reserve Bank of New York does not report a noon buying rate for pesos. No representation is made that the peso or dollar amounts shown in this Report could have been or could be converted into dollars or pesos, as the case may be, at such rate or at any other rate (See “Item 3. Key Information — A. Selected Financial Data — Exchange Rates”).

References to “GW” and “GWh” are to gigawatts and gigawatt hours, respectively; references to “MW” and “MWh” are to megawatts and megawatt hours, respectively; references to “kW” and “kWh” are to kilowatts and kilowatt hours, respectively; references to “kV” are to kilovolts, and references to “MVA” are to megavolt amperes. Unless otherwise indicated, statistics provided in this Report with respect to the installed capacity of electricity generation facilities are expressed in MW. One TW = 1,000 GW, one GW = 1,000 MW, and one MW = 1,000 kW.

Statistics relating to aggregate annual electricity production are expressed in GWh and based on a year of 8,760 hours, except for leap years (such as 2008), which are based on 8,784 hours. Statistics relating to installed capacity and production of the electricity industry do not include electricity of self-generators. Statistics relating to our production do not include electricity consumed by us by our own generation units.

Energy losses experienced by generation companies during transmission are calculated by subtracting the number of GWh of energy sold from the number of GWh of energy generated (excluding its own energy consumption and losses on the part of the power plant), within a given period. Losses are expressed as a percentage of total energy generated.

Energy losses during distribution are calculated as the difference between total energy purchased (GWh of physical demand, including own generation) and the energy sold (also measured in GWh), within a given period. Losses are expressed as a percentage of total energy purchased. Losses in distribution arise from illegally tapped energy as well as technical losses.

Calculation of Economic Interest

References are made in this Report to the “economic interest” of Enersis in its related companies. In circumstances where we do not directly own an interest in a related company, our economic interest in such ultimate related company is calculated by multiplying the percentage of economic interest in a directly held related company by the percentage of economic interest of any entity in the ownership chain of such related company. For example, if we own 60% of a directly held subsidiary and that subsidiary owns 40% of an associate, our economic interest in such associate would be 60% times 40%, or 24%.

This Report contains statements that are or may constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements appear throughout this Report and include statements regarding our intent, belief or current expectations, including but not limited to any statements concerning:

· our capital investment program;

· trends affecting our financial condition or results from operations;

· our dividend policy;

· the future impact of competition and regulation;

· political and economic conditions in the countries in which we or our related companies operate or may operate in the future;

· any statements preceded by, followed by or that include the words “believes,” “expects,” “predicts,” “anticipates,” “intends,” “estimates,” “should,” “may” or similar expressions; and

· other statements contained or incorporated by reference in this Report regarding matters that are not historical facts.

Because such statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to:

· changes in the regulatory framework of the electricity industry in one or more of the countries in which we operate;

· our ability to implement proposed capital expenditures, including our ability to arrange financing where required;

· the nature and extent of future competition in our principal markets;

· political, economic and demographic developments in the emerging market countries of South America where we conduct our business; and

· the factors discussed below under “Risk Factors.”

You should not place undue reliance on such statements, which speak only as of the date that they were made. Our independent public accountants have not examined or compiled the forward-looking statements, and, accordingly, do not provide any assurance with respect to such statements. You should consider these cautionary statements together with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to release publicly any revisions to forward-looking statements contained in this Report to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

For all these forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

A. Selected Financial Data

The following summary of consolidated financial data should be read in conjunction with our audited Consolidated Financial Statements, included in this Report. Our audited Consolidated Financial Statements as of and for the years ended December 31, 2011, 2010 and 2009 are prepared in accordance with International Financial Reporting Standards (IFRS), as issued by the IASB. The financial data as of and for each of the four years ended December 31, 2011 in the table below are presented in pesos.

Amounts are expressed in millions except for ratios, operating data, shares and ADS (American Depositary Shares) data. For the convenience of the reader, all data presented in dollars in the following summary, as of and for the year ended December 31, 2011, are translated at the Observed Exchange Rate for that date of Ch$ 519.20 per $ 1.00. No representation is made that the peso or dollar amounts shown in this Report could have been or could be converted into dollars or pesos, at such rate or at any other rate. For more information concerning historical exchange rates, see “Exchange Rates” below.

The following tables set forth the selected consolidated financial data of Enersis in accordance with IFRS for the periods indicated and the operating data of subsidiaries:

|

|

|

As of and for the year ended December 31, |

| ||||||||

|

|

|

2008 |

|

2009 |

|

2010 |

|

2011 |

|

2011 (1) |

|

|

|

|

Ch$ Million |

|

Million of $ |

| ||||||

|

Consolidated Income Statement Data |

|

|

|

|

|

|

|

|

|

|

|

|

Revenues |

|

6,579,945 |

|

6,472,056 |

|

6,563,581 |

|

6,534,880 |

|

12,586 |

|

|

Operating Expense (2) |

|

(4,716,294 |

) |

(4,544,611 |

) |

(4,859,280 |

) |

(4,968,569 |

) |

(9,570 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income |

|

1,863,651 |

|

1,927,445 |

|

1,704,301 |

|

1,566,311 |

|

3,016 |

|

|

Financial Income (Expense), Net |

|

(419,366 |

) |

(309,256 |

) |

(270,605 |

) |

(236,585 |

) |

(456 |

) |

|

Total gain (loss) on sale of non-current assets not held for sale |

|

2,503 |

|

50,502 |

|

11,711 |

|

(5,853 |

) |

(11 |

) |

|

Other non-operating income |

|

3,297 |

|

2,374 |

|

1,288 |

|

9,504 |

|

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income Before Tax |

|

1,450,085 |

|

1,671,065 |

|

1,446,695 |

|

1,333,377 |

|

2,567 |

|

|

Income tax |

|

(415,903 |

) |

(359,737 |

) |

(346,007 |

) |

(460,837 |

) |

(888 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income |

|

1,034,182 |

|

1,311,328 |

|

1,100,688 |

|

872,540 |

|

1,679 |

|

|

Net income attributable to: Owners of parent |

|

507,590 |

|

660,231 |

|

486,227 |

|

375,471 |

|

723 |

|

|

Net income attributable to: Non-controlling interests |

|

526,592 |

|

651,097 |

|

614,461 |

|

497,069 |

|

957 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income (loss) from continuing operations per Share (Ch$ / $) |

|

15.55 |

|

20.22 |

|

14.89 |

|

11.50 |

|

0.0222 |

|

|

Net Income (loss) from continuing operations per ADS (Ch$ / $) |

|

777.29 |

|

1,011.04 |

|

744.58 |

|

574.97 |

|

1.1074 |

|

|

Net income (loss) per Share (Ch$/$ per share) |

|

15.55 |

|

20.22 |

|

14.89 |

|

11.50 |

|

0.0222 |

|

|

Net income (loss) per ADS (Ch$/$ per ADS) |

|

777.29 |

|

1,011.04 |

|

744.58 |

|

574.97 |

|

1.1074 |

|

|

Cash Dividends per Share (Ch$/$ per share) |

|

4.95 |

|

7.02 |

|

4.64 |

|

7.45 |

|

0.0143 |

|

|

Cash Dividends per ADS (Ch$/$ per ADS) |

|

247.50 |

|

351.00 |

|

232.00 |

|

372.50 |

|

0.7174 |

|

|

Capital Stock |

|

2,824,883 |

|

2,824,883 |

|

2,824,883 |

|

2,824,883 |

|

5,441 |

|

|

Number of shares of common stock (thousands) |

|

32,651,166 |

|

32,651,166 |

|

32,651,166 |

|

32,651,166 |

|

32,651,166 |

|

|

Number of ADS (thousands) |

|

71,267 |

|

81,303 |

|

82,320 |

|

82,456 |

|

82,456 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Consolidated Balance Sheet Data |

|

|

|

|

|

|

|

|

|

|

|

|

Total Assets |

|

13,781,176 |

|

13,210,140 |

|

13,005,845 |

|

13,733,871 |

|

26,452 |

|

|

Non-Current Liabilities |

|

5,049,265 |

|

4,637,749 |

|

4,084,540 |

|

4,377,183 |

|

8,431 |

|

|

Equity Attributable to Owners of parent |

|

3,091,315 |

|

3,518,480 |

|

3,735,545 |

|

3,895,729 |

|

7,503 |

|

|

Equity Attributable to Non-controlling interests |

|

2,937,816 |

|

2,858,524 |

|

2,778,483 |

|

3,000,425 |

|

5,779 |

|

|

Capital Stock (3) |

|

2,983,642 |

|

2,983,642 |

|

2,983,642 |

|

2,983,642 |

|

5,747 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Consolidated Financial Data |

|

|

|

|

|

|

|

|

|

|

|

|

Capital Expenditures (Capex)(4) |

|

781,542 |

|

736,474 |

|

701,341 |

|

686,006 |

|

1,321 |

|

|

Depreciation, amortization and impairment losses |

|

438,064 |

|

539,655 |

|

557,391 |

|

561,057 |

|

1,081 |

|

(1) Solely for the convenience of the reader, peso amounts have been translated into dollars at the exchange rate of Ch$ 519.20 per dollar, the Observed Exchange Rate as of December 31, 2011.

(2) Operating Expense include Selling and Administration Expense.

(3) Includes share premium.

(4) Capex figures represent actual payments for each year. These figures do not coincide with those presented in “Item 4A.— Investments, Capital Expenditures and Divestitures,” where accrued investments for each year are presented.

|

|

|

As of and for the year ended December 31, |

| ||||||||

|

|

|

2007 |

|

2008 |

|

2009 |

|

2010 |

|

2011 |

|

|

OPERATING DATA OF SUBSIDIARIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Chilectra (Chile) |

|

|

|

|

|

|

|

|

|

|

|

|

Electricity Sold (GWh) |

|

12,923 |

|

12,535 |

|

12,585 |

|

13,098 |

|

13,697 |

|

|

Number of Customers (thousands) |

|

1,483 |

|

1,534 |

|

1,579 |

|

1,610 |

|

1,638 |

|

|

Total Energy Losses (%)(1) |

|

5.9 |

% |

5.9 |

% |

6.1 |

% |

5.8 |

% |

5.5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Edesur (Argentina) |

|

|

|

|

|

|

|

|

|

|

|

|

Electricity Sold (GWh) |

|

15,833 |

|

16,160 |

|

16,026 |

|

16,759 |

|

17,233 |

|

|

Number of Customers (thousands) |

|

2,228 |

|

2,262 |

|

2,305 |

|

2,353 |

|

2,389 |

|

|

Total Energy Losses (%)(1) |

|

10.7 |

% |

10.6 |

% |

10.5 |

% |

10.5 |

% |

10.5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ampla (Brazil) |

|

|

|

|

|

|

|

|

|

|

|

|

Electricity Sold (GWh) |

|

8,985 |

|

9,119 |

|

9,394 |

|

9,927 |

|

10,223 |

|

|

Number of Customers (thousands) |

|

2,379 |

|

2,466 |

|

2,522 |

|

2,571 |

|

2,643 |

|

|

Total Energy Losses (%)(1) |

|

21.4 |

% |

20.2 |

% |

21.2 |

% |

20.5 |

% |

19.7 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Coelce (Brazil) |

|

|

|

|

|

|

|

|

|

|

|

|

Electricity Sold (GWh) |

|

7,227 |

|

7,571 |

|

7,860 |

|

8,850 |

|

8,970 |

|

|

Number of Customers (thousands) |

|

2,689 |

|

2,842 |

|

2,965 |

|

3,095 |

|

3,224 |

|

|

Total Energy Losses (%)(1) |

|

12.5 |

% |

11.7 |

% |

11.6 |

% |

12.1 |

% |

11.9 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Codensa (Colombia)(2) |

|

|

|

|

|

|

|

|

|

|

|

|

Electricity Sold (GWh) |

|

11,441 |

|

11,822 |

|

11,837 |

|

12,141 |

|

12,552 |

|

|

Number of Customers (thousands) |

|

2,209 |

|

2,285 |

|

2,361 |

|

2,429 |

|

2,495 |

|

|

Total Energy Losses (%)(1) |

|

8.7 |

% |

8.1 |

% |

8.2 |

% |

8.2 |

% |

7.8 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EEC (Colombia) (3) |

|

|

|

|

|

|

|

|

|

|

|

|

Electricity Sold (GWh) |

|

n.a. |

|

n.a. |

|

277 |

|

373 |

|

305 |

|

|

Number of Customers (thousands) |

|

n.a. |

|

n.a. |

|

115 |

|

117 |

|

121 |

|

|

Total Energy Losses (%)(1) |

|

n.a. |

|

n.a. |

|

15.2 |

% |

17.7 |

% |

20.2 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Edelnor (Peru) |

|

|

|

|

|

|

|

|

|

|

|

|

Electricity Sold (GWh) |

|

5,201 |

|

5,599 |

|

5,716 |

|

6,126 |

|

6,572 |

|

|

Number of Customers (thousands) |

|

986 |

|

1,028 |

|

1,061 |

|

1,098 |

|

1,144 |

|

|

Total Energy Losses (%)(1) |

|

8.1 |

% |

8.2 |

% |

8.1 |

% |

8.3 |

% |

8.2 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Endesa Chile |

|

|

|

|

|

|

|

|

|

|

|

|

Installed capacity in Chile (MW) |

|

4,779 |

|

5,283 |

|

5,650 |

|

5,611 |

|

5,611 |

|

|

Installed capacity in Argentina (MW) |

|

3,644 |

|

3,652 |

|

3,652 |

|

3,652 |

|

3,652 |

|

|

Installed capacity in Colombia (MW) |

|

2,829 |

|

2,895 |

|

2,895 |

|

2,914 |

|

2,914 |

|

|

Installed capacity in Peru (MW) |

|

1,468 |

|

1,467 |

|

1,667 |

|

1,668 |

|

1,668 |

|

|

Production in Chile (GWh)(4) |

|

18,773 |

|

21,267 |

|

22,239 |

|

20,914 |

|

20,722 |

|

|

Production in Argentina (GWh)(4) |

|

12,117 |

|

10,480 |

|

11,955 |

|

10,940 |

|

10,801 |

|

|

Production in Colombia (GWh)(4) |

|

11,942 |

|

12,905 |

|

12,674 |

|

11,283 |

|

12,090 |

|

|

Production in Peru (GWh)(4) |

|

7,654 |

|

8,102 |

|

8,163 |

|

8,466 |

|

9,153 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Endesa Brasil |

|

|

|

|

|

|

|

|

|

|

|

|

Installed capacity in Brazil (MW) |

|

987 |

|

987 |

|

987 |

|

987 |

|

987 |

|

|

Production in Brazil (GWh)(4) |

|

3,954 |

|

3,379 |

|

3,319 |

|

5,095 |

|

4,155 |

|

(1) Energy losses are calculated as the difference between total energy purchased (GWh of physical demand, including own generation) and the energy sold (GWh), within a given period. Losses are expressed as a percentage of total energy purchased. Losses in distribution arise from illegally tapped energy as well as technical failures.

(2) In February 2009, Codensa, our Colombian distribution subsidiary, acquired approximately 49% of DECSA. On March 13, 2009, DECSA acquired 82.3% of EEC. Beginning in 2010, we started separately presenting the information concerning EEC, a jointly-controlled company of Codensa.

(3) The results for 2009 include the period of April through December.

(4) Energy production is defined as total generation minus energy consumption and technical losses within our own power plants.

Exchange Rates

Fluctuations in the exchange rate between the peso and the dollar will affect the dollar equivalent of the peso price of our shares of common stock, without par value (the Shares or the Common Stock), on the Bolsa de Comercio de Santiago (the Santiago Stock Exchange), the Bolsa Electrónica de Chile (the Chilean Electronic Exchange) and the Bolsa de Corredores de Valparaíso (the Valparaíso Stock Exchange) (collectively, the Chilean Exchanges). These exchange rate fluctuations will likely affect the price of the Company’s ADS and the conversion of cash dividends relating to the Shares represented by ADS from pesos to dollars. In addition, to the extent that significant financial liabilities of the Company are denominated in foreign currencies, exchange rate fluctuations may have a significant impact on earnings.

The Ley Orgánica del Banco Central de Chile 18,840 (the Central Bank Act), provides that the Central Bank may require that certain purchases and sales of foreign currency be carried out in the Mercado Cambiario Formal (the Formal Exchange Market), a market comprised of banks and other entities explicitly authorized by the Central Bank. Purchases and sales of foreign currency,

which can take place outside the Formal Exchange Market, can be carried out in the Mercado Cambiario Informal (the Informal Exchange Market), which is a recognized currency market in Chile. Free market forces drive both the Formal and Informal Exchange Markets. Foreign currency for payments and distributions with respect to the ADS may be purchased in either the Formal or the Informal Exchange Market, but such payments and distributions must be remitted through the Formal Exchange Market. The Central Bank publishes the dólar observado (the Observed Exchange Rate) daily, and it is computed by taking the weighted average of the previous business day’s transactions in the Formal Exchange Market.

Unless otherwise indicated in this Report, amounts translated to dollars have been calculated based on the exchange rates prevailing as of December 31, 2011.

The following table sets forth, for the periods and dates indicated, certain information concerning the Observed Exchange Rate reported by the Central Bank.

|

|

|

Observed Exchange Rate |

| ||||||

|

Year |

|

Low |

|

High |

|

Average(1) |

|

Period- |

|

|

2007 |

|

493.14 |

|

548.67 |

|

521.06 |

|

496.89 |

|

|

2008 |

|

431.22 |

|

676.75 |

|

530.48 |

|

636.45 |

|

|

2009 |

|

491.09 |

|

643.87 |

|

554.22 |

|

507.10 |

|

|

2010 |

|

468.01 |

|

549.17 |

|

510.38 |

|

468.01 |

|

|

2011 |

|

455.91 |

|

533.74 |

|

483.45 |

|

519.20 |

|

|

|

|

Monthly Observed Exchange Rate(1) |

| ||||||

|

Last six months |

|

Low |

|

High |

|

Average (1) |

|

Period- |

|

|

2011 |

|

|

|

|

|

|

|

|

|

|

October |

|

490.29 |

|

533.74 |

|

— |

|

490.29 |

|

|

November |

|

494.08 |

|

526.83 |

|

— |

|

517.37 |

|

|

December |

|

508.67 |

|

522.62 |

|

— |

|

519.20 |

|

|

2012 |

|

|

|

|

|

|

|

|

|

|

January |

|

485.35 |

|

518.20 |

|

— |

|

488.75 |

|

|

February |

|

475.29 |

|

487.73 |

|

— |

|

476.27 |

|

|

March |

|

480.62 |

|

491.57 |

|

— |

|

487.44 |

|

Source: Chilean Central Bank.

(1) The average of the exchange rates on the last day of each month during the yearly period. This is not applicable to monthly data.

Calculation of the appreciation or devaluation of the Chilean peso against the U.S. dollar in any given period is made by determining the percent change between the reciprocals of the Chilean peso equivalent of $1.00 at the end of the preceding period and the end of the period for which the calculation is being made. For example, to calculate the devaluation of the year-end Chilean peso in 2011, one determines the percent change between the reciprocal of Ch$ 468.01 (the value of one dollar as of December 31, 2010) and the reciprocal of Ch$ 519.20 (the value of one dollar as of December 31, 2011). In this example, the percentage change between 0.002137 (the reciprocal of 468.01) and 0.001926 (the reciprocal of 519.20) is (9.9)%, which represents the 2011 year-end devaluation of the Chilean peso against the 2010 year-end dollar. A positive percentage change means that the Chilean peso appreciated against the dollar, while a negative percentage change means that the peso devaluated against the dollar.

The following table sets forth the period-end rates for U.S. dollars for the years ended December 31, 2007 through December 31, 2011 and through the date indicated in the table below, based on information published by the Chilean Central Bank.

|

|

|

Period |

|

Appreciation |

|

|

Chilean Peso Equivalent of $ 1 |

|

|

|

|

|

|

Year Ended: |

|

|

|

|

|

|

December 31, 2007 |

|

496.89 |

|

7.1 |

% |

|

December 31, 2008 |

|

636.45 |

|

(21.9 |

)% |

|

December 31, 2009 |

|

507.10 |

|

25.5 |

% |

|

December 31, 2010 |

|

468.01 |

|

8.4 |

% |

|

December 31, 2011 |

|

519.20 |

|

(9.9 |

)% |

Source: Chilean Central Bank.

(1) Calculated based on the variation of period-end exchange rates.

B. Capitalization and Indebtedness.

Not applicable.

C. Reasons for the Offer and Use of Proceeds.

Not applicable.

D. Risk Factors.

A financial crisis in any region worldwide can have a significant impact in the countries in which we operate, and consequently, may adversely affect our operations, as well as our liquidity.

The five countries in which we operate are vulnerable to external shocks, which could cause significant economic difficulties and affect their growth. In case any of these economies experience a lower economic growth or a recession, it is likely that our customers will demand less electricity, which could affect our results of operations and financial condition adversely. Furthermore, some of our customers may experience difficulties in paying their electricity bills, and an increase in uncollectible accounts would also affect our results adversely.

In addition, a financial crisis and its disruptive effect on the financial industry can have an adverse impact on our ability to obtain new bank loans under normal terms and conditions. Our ability to tap the capital markets in the five countries where we operate, as well as the international capital markets for other sources of liquidity, may also be diminished, or such financing may be available only at higher interest levels. Reduced liquidity could, in turn, affect our capital expenditures, our long-term investments and acquisitions, our growth prospects, and our dividend payout policy.

A financial crisis in the European Community or a European sovereign debt crisis may have an adverse effect on our liquidity.

At the time of filing this Report, the crisis in the euro zone is threatening a recession in Europe and defaults by certain governments. There is also a risk of a run on deposits of banks short of cash, a significant increase in the yields of European governments’ bonds, a corporate credit crunch, tighter fiscal policies, and a significant decrease in investor confidence in the euro zone. Among the countries that are particularly at risk are Spain and Italy, home of our parent companies, Endesa Spain and Enel, respectively.

We carry out a significant portion of our bank financings and derivative hedges with European banks. Our European counterparty risk takes into account loans and derivatives accounted for either in the parent bank entities headquartered in Europe or in any of their subsidiaries or agencies outside Europe. In general terms, European banks who act through their foreign subsidiaries, agencies and representative offices also take an aggregated group risk to counterparty exposure, both theirs and ours. If any of the European banks with which we have significant relationships were to encounter severe financial difficulties, our access to bank loans would be significantly curtailed, and would probably lead to an increase in our interest expense.

As of December 31, 2011, $ 560 million of our outstanding bank debt and $ 1,550 million of the notional amount of our derivative hedges are with bank groups whose parent companies are headquartered in Europe. The derivative hedges deal with both currency swaps and interest rates swaps, though the most significant component is the currency hedge for the inflation-indexed Chilean peso (the UF) against the dollar. As of December 31, 2011, these derivative hedges had a mark to market value of $ 358 million against us, but there is always the possibility that the position could be in our favor in the future. Of the amounts mentioned here, 97% of our bank debt and 74% of the notional amount of our derivatives have been contracted with Spanish banks. A severe

financial disruption affecting these Spanish banks could therefore have an adverse effect on us, especially regarding our bank lenders. (See “Item 5. Operating and Financial Review and Prospects. — B. Liquidity & Capital Resources” and “Item 11. Quantitative and Qualitative Disclosures about Market Risk.”)

South American economic fluctuations are likely to affect our results from operations and financial condition, as well as the value of our securities.

All of our operations are located in five South American countries. Accordingly, our consolidated revenues are sensitive to the performance of South American economies as a whole. If local, regional or worldwide economic trends adversely affect the economy of any of the five countries in which we have investments or operations, our financial condition and results from operations could be adversely affected. Moreover, we have investments in relatively risky countries such as Argentina. Generation and distribution of cash from subsidiaries located in Argentina have been lower than expected.

A substantial portion of our operations are located in Chile and Brazil and more than 70% of our operating revenues in 2011 were derived from our operations in these countries, making our financial condition and results of operations particularly dependent on the performance of Chile and Brazil. In 2011, Chilean GDP increased by 6.2% compared to a 5.2% increase in 2010. The latest estimate from the Chilean Central Bank forecasts growth for 2012 in the 3.75%-4.75% range. In 2011, Brazilian GDP increased by 3.8% compared to a 7.5% increase in 2010. The consensus forecast according to the Brazilian Central Bank is a growth of 4.5% in 2012. However, such growth may not be achieved and the growth trend may not be sustainable in the future in one or both of these countries. Future developments in the Chilean and Brazilian economies may impair our ability to proceed with our strategic plans and adversely impact our financial condition or results of operations.

In addition, the South American financial and securities markets are, to varying degrees, influenced by economic and market conditions in other countries. Although economic conditions are different in each country, investor reaction to developments in one country may have a significant contagion effect on the securities of issuers in other countries, including Chile and Brazil. Chilean and Brazilian financial and securities markets may be adversely affected by events in other countries and such effects may affect the value of our securities.

Certain South American economies have been characterized by frequent and occasionally drastic intervention by governmental authorities, which may adversely affect our business and financial results.

Governmental authorities have changed monetary, credit, tariff, tax and other policies to influence the course of the economies of Argentina, Brazil, Colombia and Peru. To a lesser extent, the Chilean government has also exercised and continues to exercise a substantial influence over many aspects of the private sector, which may result in changes to economic or other policies. These governmental actions, intended to control inflation and affect other policies, have often involved wage, price and tariff rate controls as well as other interventionist measures. For example, Argentina froze bank accounts and imposed capital restrictions in 2001, nationalized the private sector pension funds in 2008, used Central Bank reserves of the Argentine Treasury in order to pay down indebtedness maturing in 2010, and according to a survey by Torcuato di Tella University, the government has intervened the national statistics office since 2007 in order to underreport inflation. In 2010, Colombia imposed an equity tax to finance the reconstruction to repair damages caused by severe flooding, which resulted in an accrual booked in January 2011 for tax payable in 2011-2014. For additional information please see “Item 5. Operating and Financial Review and Prospects — A. Operating Results — 2. Enersis’ Results from Operations for the Years ended December 31, 2010 and December 31, 2011 — Operating Costs”).

Changes in the policies of these governmental authorities with respect to tariff rates, exchange controls, regulations and taxation could adversely affect our business and financial results, reducing our profitability, as could inflation, devaluation, social instability and other political, economic or diplomatic developments, including the response by governments in the region to these circumstances.

Our electricity business is subject to risks arising from natural disasters, catastrophic accidents and acts of terrorism, which could adversely affect our operations, earnings and cash flow.

Our primary facilities include power plants, transmission and distribution assets, pipelines, LNG terminals and re-gasification plants, storage and chartered LNG tankers. Our facilities may be damaged by earthquakes, flooding, fires, other catastrophic disasters arising from natural or accidental human causes, as well as acts of terrorism. We could experience severe business disruptions, significant decreases in revenues based on lower demand arising from catastrophic events, or significant additional costs to us not otherwise covered by business interruption insurance clauses. There may be an important time lag between a major accident or catastrophic event and the final reimbursement from our insurance policies, which typically carry non-recoverable deductible amounts, and in any event are subject to caps per event. For further detail, please see “Item 4 D. Property, Plants and Equipment.”

As an example, on February 27, 2010, Chile experienced a major earthquake, with a magnitude of 8.8 on the Richter scale, in the Bío-Bío Region, followed by a tsunami. Our thermal generation plants Bocamina and Bocamina II, which are located near the epicenter, sustained damages as a result of the earthquake.

A material breach of penal law by our senior management or employees may lead to adverse consequences.

In each of the countries where we operate, our senior management or employees could become involved in fraudulent practices such as intentional manipulation of financial statements, misappropriation of assets, inappropriate traffic of influence, insider trading, bribery, kickbacks, receipt of gratuities, unauthorized intercompany transactions, deliberate release of misleading information or rumors, and other forms of corruption or breach of penal law. Depending on the materiality of such fraudulent acts, we could be exposed to regulatory fines, litigation, loss of operating licenses or concessions, and even insolvency or bankruptcy. For further discussion, please see “Item 6 Directors, Senior Management and Employees — c. Board Practices” and “Item 16.B Code of Ethics.”

We are subject to financing risks, such as those associated with funding our new projects and capital expenditures, risk related to refinancing our maturing debt and we are also subject to debt covenant compliance, all of which could adversely affect our liquidity.

As of December 31, 2011, the principal amount of our outstanding debt in financial terms was $ 7,330 million while, for accounting purposes, it totaled $ 7,581 million. These amounts differ since financial debt, unlike accounting debt, does not include accrued interest.

Our financial debt had the following maturity timetable:

· $ 1,099 million in 2012;

· $ 910 million in 2013;

· $ 2,755 million in the 2014-2016 period; and

· $ 2,566 million thereafter.

Set forth below is a breakdown by country for financial debt maturing in 2012:

· $ 109 million — Chile;

· $ 171 million — Argentina;

· $ 529 million — Brazil;

· $ 174 million — Colombia; and

· $ 116 million — Peru.

Some of our debt agreements are subject to financial covenants. They also contain affirmative and negative covenants, events of default or mandatory prepayments for contractual breaches, including certain changes of control, and for material mergers and divestments, among other provisions. A significant portion of our financial indebtedness is subject to cross default provisions, with different definitions, criteria, materiality thresholds, and applicability as to the subsidiaries that could give rise to such a cross default.

In the event that we or our subsidiaries breach any of these material contractual provisions, our creditors and bond holders may demand immediate repayment, and a significant portion of our indebtedness could become due and payable.

We may be unable to refinance our indebtedness or obtain such refinancing on terms acceptable to us. In the absence of such refinancing, we could be forced to dispose of assets in order to make up for any shortfall in the payments due on our indebtedness under circumstances that might not be favorable to obtaining the best price for such assets. Furthermore, assets may not be sold quickly enough, or for amounts sufficient to enable us to make such payments.

We may also be unable to raise funds required to finish our projects under development or under construction. Market conditions prevailing at the moment we require these funds or other unforeseen project costs can compromise our ability to finance these projects and expenditures.

As of the date of this Report, Argentina continues to be the country with the highest refinancing risk. As of December 31, 2011, the third-party financial debt of our Argentine subsidiaries amounted to $ 389 million. As a matter of policy for all of our Argentine subsidiaries as long as fundamental issues concerning the electricity sector remain unresolved, we intend to roll over our outstanding Argentine debt to the extent we are able to do so. If our creditors do not continue to accept rolling over debt when it becomes due, and we are unable to refinance such obligations, we may default on such indebtedness. Our Argentine subsidiary, Endesa Costanera, did not make an installment payment due on March 30, 2012 of $ 17.6 million (which includes $ 4.3 million in interest expense) under the terms of a supplier credit agreement with Mitsubishi Corporation (“MC”) originally entered into in 1996. The aggregate amount accrued under the supplier credit agreement as of March 30, 2012, including capitalized interest, was $ 141 million. Endesa Costanera has experienced difficulties in making timely payments under its agreement with MC on a recurring basis since the Argentine crisis of 2002, but has in the past received waivers expressing the willingness to renegotiate payments. Such missed payments have been carried out on mutually agreed terms. As of the date of this Report, Endesa Costanera has not received a waiver for the payment past due. The relevant terms of the supplier credit provide for a 180-day grace period for payment. There can be no assurance that Endesa Costanera will receive a waiver or payment extension prior to the expiration of the 180-day grace period for payment. (See “Item 4. Information on the Company. B. Business Overview. Electricity Industry Regulatory Framework. Argentina. Regulatory Developments: the industry after the Public Emergency Law” and “Item 5. Operating and Financial Review and Prospects - B. Liquidity and Capital Resources”). For more information on covenants, cross default

and relevant provisions of our credit facilities, see “Item 5. Operating and Financial Review and Prospects — B. Liquidity and Capital Resources.”

Since our generation business depends heavily on hydrological conditions, drought conditions may hurt our profitability.

Approximately 58% of our consolidated installed generation capacity in 2011 was hydroelectric. Accordingly, extreme hydrological conditions may affect our business and may have an adverse effect on our results. In the last few years, regional hydrology has been affected by two climactic phenomena — El Niño and La Niña — that influence rainfall regularity and may lead to droughts. The effects of El Niño or La Niña can unevenly affect the hydrology of the countries where we operate.

During periods of drought, thermal plants, such as ours that use natural gas, fuel oil or coal as a fuel, are dispatched more frequently. Operating costs of thermal plants might be considerably higher than those of hydroelectric plants. Our operating expenses increase during these periods, and depending on our commercial obligations, we may have to buy electricity from the spot market in order to comply with our contractual supply obligations. The cost of these electricity purchases may exceed the price at which we sell contracted electricity, thus producing losses from those contracts. For further information on hydrology please refer to “Item 5. Operating and Financial Review and Prospects — A. Operating Results — 1. Discussion of Main Factors Affecting Operating Results — a. Hydrological Conditions: Generation Business.”

Governmental regulations may adversely affect our business and have already done so in Argentina.

We are subject to extensive regulation of tariffs and other aspects of our business in the five countries in which we operate, and these regulations may adversely affect our profitability. For example, the Chilean government can impose electricity rationing during drought conditions or prolonged failures in power facilities. If, during rationing, we are unable to generate enough electricity to comply with our contractual obligations, we may be forced to buy electricity in the pool market at the spot price, since even a severe drought does not constitute a force majeure event. The spot price may be significantly higher than our costs to generate the electricity and can be as high as the “cost of failure” set by the National Energy Commission, or the CNE. This “cost of failure,” which is updated semiannually by the CNE, is a measurement of how much final users would pay for one extra MWh under rationing conditions. If we are unable to buy enough electricity in the pool market to comply with all of our contractual obligations, then we would have to compensate our regulated customers for the electricity we failed to provide at the rationed price. If material rationing policies are imposed by regulatory authorities in any of the countries in which we operate, our business, financial condition and results from operations may be affected adversely in a material way. Rationing periods may occur in the future, and consequently our generation subsidiaries may be required to pay regulatory penalties if such subsidiaries fail to provide adequate service under such conditions.

Governmental authorities may also delay the distribution tariff review process, or tariff adjustments determined by governmental authorities may not be sufficient to pass through our costs (as has been the case with Edesur, our Argentine distribution subsidiary). Similarly, the regulatory framework for the electricity sector in a jurisdiction may affect the ability of our generation companies (such as Endesa Costanera, our electricity generation company) to collect revenues sufficient to offset our costs.

The inability of any company in the Enersis Group to collect revenues sufficient to cover operating costs may affect the ability of the affected company to operate as a going concern and may otherwise have an adverse effect on our business, assets, financial results and operations. For additional information on Edesur and Endesa Costanera, see “Item 5. Operating and Financial Review and Prospects — A. Operating Results — 2. Enersis’ Results from Operations for the Years ended December 31, 2010 and December 31, 2011.”

In addition, changes in the regulatory framework, including changes that if adopted would significantly affect our operations, are often submitted to the legislators and administrative authorities in the countries in which we operate and, if approved, could have a material adverse impact on our business. For instance, in 2005 there was a change in the water rights’ law in Chile that requires us to pay for unused water rights. (See “Item 4. Information on the Company. — B. Business Overview. — Electricity Industry Regulatory Framework. — Chile — Water Rights).”

Regulatory authorities may impose fines on our subsidiaries.

Our electricity businesses may be subject to regulatory fines for any breach of current regulations, including energy supply failure, in the five countries in which we operate. In Chile, such fines may range from 1 Unidad Tributaria Mensual (UTM), or $ 75, to 10,000 Unidades Tributarias Anuales (UTA), or $ 9.0 million, in each case using the UTM, UTA and foreign exchange rate as of December 31, 2011. In Peru, fines can reach a maximum of 1,300 Unidad Impositiva Tributaria (UIT) or $ 1.7 million as of December 31, 2011; in Colombia fines may range from $ 2,900 to $ 0.6 million; in Argentina, there is no maximum limit for the fines and in Brazil fines may be imposed for up to 2.0% of the concessionaire’s revenues.

Our electricity subsidiaries, supervised by their local regulatory entities, may be subject to these fines in cases where, in the opinion of the regulatory entity, operational failures that affect the regular energy supply to the system are the fault of the company; for instance, when the agents are not coordinated with the system operation. Also, our subsidiaries may be required to pay fines or to compensate customers if those subsidiaries are unable to deliver electricity to them even if such failure is due to forces outside of our control.

For example, in January 2011, ENRE imposed fines on Edesur in the amount of $ 16.2 million due to a blackout that occurred in Buenos Aires during the last days of December 2010, including the compensation to end users with respect to the blackout. In September 2011 SEF imposed fines totaling 2,782 UTA, or $ 2.5 million, on Endesa Chile, Pehuenche and Chilectra due to a blackout that occurred in the Metropolitan Region in March 2010. For further information on fines please refer to “Item 4. Information on the Company. — B. Business Overview. — Electricity Industry Regulatory Framework.”

We depend in part on payments from our subsidiaries, jointly-controlled entities and associates to meet our payment obligations.

We have no significant assets other than the stock of our subsidiaries. Our ability to pay our obligations depends on cash from dividends, loans, interest payments, capital reductions and other distributions from our subsidiaries and equity affiliates. The ability of our subsidiaries and equity affiliates to pay dividends, interest payments, loans and other distributions to us is subject to legal constraints such as dividend restrictions, fiduciary duties, contractual limitations and foreign exchange controls that may be imposed in any of the five countries where they operate.

Historically, we have been able to access the cash flows of our Chilean subsidiaries, but we have not been similarly able to access at all times the cash flows of our non-Chilean operating subsidiaries due to government regulations, strategic considerations, economic conditions and credit restrictions.