UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2020

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number 1-475

(Exact name of registrant as specified in its charter)

(State of Incorporation)

(Address of Principal Executive Office)

(I.R.S. Employer Identification No.)

(Zip Code)

(414 ) 359-4000

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Shares of Stock Outstanding January 29, 2021 | Name of Each Exchange on Which Registered | ||||||||||||

| Class A Common Stock (par value $5.00 per share) | Not listed | |||||||||||||

(par value $1.00 per share) | ||||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ¨ No.

Indicate by check mark whether the registrant has submitted every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | Emerging growth company | ||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2of the Act.) ☐ Yes ☒ No

The aggregate market value of voting stock held by non-affiliates of the registrant was $42,461,387 for Class A Common Stock and $6,241,019,639 for Common Stock as of June 30, 2020.

DOCUMENTS INCORPORATED BY REFERENCE

| 1. | Portions of the company’s definitive Proxy Statement for the 2021 Annual Meeting of Stockholders (to be filed with the Securities and Exchange Commission under Regulation 14A within 120 days after the end of the registrant’s fiscal year and, upon such filing, to be incorporated by reference in Part III). | ||||

1

A. O. Smith Corporation

Index to Form 10-K

Year Ended December 31, 2020

| Page | ||||||||

2

PART 1

ITEM 1 – BUSINESS

Our company is comprised of two reporting segments: North America and Rest of World. Our Rest of World segment is primarily comprised of China, Europe and India. Both segments manufacture and market comprehensive lines of residential and commercial gas and electric water heaters, boilers, tanks and water treatment products. Both segments primarily manufacture and market in their respective regions of the world.

NORTH AMERICA

We serve residential and commercial end markets in North America with a broad range of products including:

Water heaters. Our residential and commercial water heaters come in sizes ranging from 2.5 gallon (point-of-use) models to 2,500 gallon products with varying efficiency ranges. We offer electric, natural gas and liquid propane tank-type models as well as tankless (gas and electric), heat pump and solar tank units. Typical applications for our water heaters include residences, restaurants, hotels and motels, office buildings, laundries, car washes, schools and small businesses.

Boilers. Our residential and commercial boilers range in size from 45,000 British Thermal Units (BTUs) to 6.0 million BTUs. Our boilers are primarily used in space heating applications for residences, hospitals, schools, hotels and other large commercial buildings.

Water treatment products. With the acquisition of Aquasana, Inc. (Aquasana) in 2016 we entered the water treatment market. We expanded our product offerings with the acquisitions of Hague Quality Water International (Hague) in 2017 and Water-Right, Inc. (Water-Right) in 2019. Our water treatment products range from point-of-entry water softeners, solutions for problem well water, and whole-home water filtration products to on-the-go filtration bottles and point-of-use carbon and reverse osmosis products. We also offer a complete line of food and beverage filtration products. Typical applications for our water treatment products include residences, restaurants, hotels and offices.

Other. In our North America segment, we also manufacture expansion tanks, commercial solar water heating systems, swimming pool and spa heaters, related products and parts.

A significant portion of our North America sales is derived from the replacement of existing products.

We believe we are the largest manufacturer and marketer of water heaters in North America with a leading share in both the residential and commercial portions of the market. In the commercial portions of the market for both water heating and space heating, we believe our comprehensive product lines and our high-efficiency products give us a competitive advantage. Our wholesale distribution channel, where we sell our products primarily under the A. O. Smith and State brands, includes more than 1,200 independent wholesale plumbing distributors serving residential and commercial end markets. We also sell our residential water heaters through the retail and maintenance, repair and operations (MRO) channels. In the retail channel, our customers include four of the six largest national hardware and home center chains, including a long-standing exclusive relationship with Lowe’s where we sell A. O. Smith branded products.

Our Lochinvar brand is one of the leading residential and commercial boiler brands in the U.S. Approximately 40 percent of Lochinvar branded sales consist of residential and commercial water heaters while the remaining 60 percent of Lochinvar branded sales consist primarily of boilers and related parts. Our commercial boiler distribution channel is primarily comprised of manufacturer representative firms, the remainder of our Lochinvar branded products are distributed through wholesale channels.

We sell our Aquasana branded products primarily directly to consumers through e-commerce as well as on-line retailers including Amazon and through other retail chains. Our water softener branded products and problem well water solutions, which include Hague, WaterBoss, Water-Right, WaterCare, and Evolve, are sold through water quality dealers. Our water softener products are also sold through home center retail chains. Our A. O. Smith branded water treatment products are sold through Lowe’s, Amazon, and our wholesale distribution channels.

Our energy-efficient product offerings continue to be a sales driver for our business. Our commercial water heaters and our condensing boilers continue to be an option for commercial customers looking for high-efficiency water and space heating with a short payback period through energy savings. We offer residential heat pump, condensing tank-type and tankless water heaters in North America, as well as other higher efficiency water heating solutions to round out our energy-efficient product offerings.

We sell our products in highly competitive markets. We compete in each of our targeted market segments based on product design, reliability, quality of products and services, advanced technologies, energy efficiency, maintenance costs and price.

3

Our principal water heating and boiler competitors in North America include Rheem, Bradford White, Rinnai, Aerco and Navien. Numerous other manufacturing companies also compete. Our principal water treatment competitors in the U.S. are Culligan, Kinetico, Pentair and Ecowater as well as numerous regional assemblers.

REST OF WORLD

We have operated in China for more than 25 years. In that time, we have established A. O. Smith brand recognition in the residential and commercial markets. The Chinese water heater market is predominantly comprised of electric wall-hung, gas tankless, combi-boiler, heat pump and solar water heaters. We believe we are one of the leading suppliers of water heaters to the residential market in China in dollar terms. We manufacture and market water treatment products, primarily residential reverse osmosis products. We also manufacture and market air purification products as well as design and market range hoods and cooktops in China.

We sell our products in over 13,000 points of sale in China, approximately 6,400 are retail outlets in tier one and tier two cities of which over 2,000 exclusively sell our products. We also sell our products through e-commerce channels.

In 2008, we established a sales office in India and began importing products specifically designed for India. We began manufacturing water heaters in India in 2010 and water treatment products in 2015.

Our primary competitors in China in the water heater market segment are Haier and Midea, which are Chinese companies, as well as Rinnai. Our principal competitors in the water treatment market are Angel, Midea, Truliva, and Xiaomi. In India, we compete with Racold, Bajaj and Havells in the water heater market and Eureka Forbes, Kent and Hindustan Unilever in the water treatment market.

In addition, we sell water heaters in the European and Middle Eastern markets and water treatment products in Hong Kong, Turkey and Vietnam, all of which combined comprised less than 13 percent of total Rest of World sales in 2020.

RAW MATERIALS

Raw materials for our manufacturing operations, primarily consisting of steel, are generally available in adequate quantities, however the current COVID-19 pandemic has periodically stressed the availability of certain raw materials. A portion of our customers are contractually obligated to accept price changes based on fluctuations in steel prices. There has been volatility in steel costs over the last several years, including an increase in steel costs in the second half of 2020.

RESEARCH AND DEVELOPMENT

To improve our competitiveness by generating new products and processes, we conduct research and development at our Corporate Technology Center in Milwaukee, Wisconsin, our Global Engineering Center in Nanjing, China, and our operating locations. Our total expenditures for research and development in 2020, 2019 and 2018 were $80.7 million, $87.9 million and $94.0 million, respectively.

PATENTS AND TRADEMARKS

We own and use in our businesses various trademarks, trade names, patents, trade secrets and licenses. We do not believe that our business as a whole is materially dependent upon any such trademark, trade name, patent, trade secret or license. However, our trade name is important with respect to our products, particularly in China, India and the U.S.

HUMAN CAPITAL

We employed approximately 13,900 employees as of December 31, 2020, primarily non-union. We have a set of values for conducting our business and interacting with our employees as outlined in the A. O. Smith Corporation Guiding Principles. These principles help to shape how we hire, train and treat our employees. We believe that the critical elements of the effort to retain and develop talent are employee engagement, talent development, a focus on employee safety, and market competitive compensation.

We conduct a Global Employee Engagement Survey on a biannual basis. This third-party-managed survey measures employees' level of engagement against external norms and provides us with actionable feedback that drives improvement priorities. Survey participation in 2020 was 96 percent, which we believe indicates our employees' willingness to share their perspectives and a commitment to continuous improvement.

We provide all employees with a wide range of professional development experiences, both formal and informal. Some of the formal development programs that employees have access to include early-career leadership development programs, continuous improvement skill-building programs, and tuition reimbursement for degree programs or trade schools.

4

It is expected that managers work closely with their employees to ensure performance feedback and development discussions take place on a regular basis.

The safety of our people is always at the forefront of what we do. We provide safety training in our production facilities, designed to empower our employees with the knowledge and tools they need to make safe choices and mitigate risks. In addition to traditional training, we use standardized signage and visual management throughout our facilities. Since 1954, we have awarded annually the Lloyd B. Smith President's Safety Award, which acknowledges an A. O. Smith facility that demonstrates the most improvement over one year in the area of workplace safety. Specific to the COVID-19 pandemic, we have undertaken numerous and meaningful steps to protect our employees, suppliers, and customers. See Item 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations," of this Annual Report on Form 10-K for additional information.

We provide what we believe is a robust total compensation program designed to be market-competitive and internally equitable to attract, retain, motivate and reward a high-performance workforce. Regular internal and external analysis is performed to ensure this market alignment. In addition to salaries, these programs, which vary by country, can include annual bonuses, stock-based compensation awards, retirement plans with employee matching opportunities, and other benefits.

BACKLOG

Due to the short-cycle nature of our businesses, none of our operations sustain significant backlogs.

GOVERNMENT REGULATIONS AND ENVIRONMENTAL MATTERS

Our operations, including the manufacture, packaging, labeling, storage, distribution, advertising and sale of our products, are subject to various federal, state, local and foreign laws and regulations. In the U.S., many of our products are regulated by the Department of Energy, the Consumer Product Safety Commission, and the Federal Trade Commission. State and local governments, through laws, regulations, and building codes, also regulate our water heating and water treatment products. Whether at the federal, state, or local level, these laws are intended to improve energy efficiency and product safety, and protect public health and the environment. Similar laws and regulations have been adopted by government authorities in other countries in which we manufacture, distribute, and sell our products.

In addition, our operations are subject to federal, state and local environmental laws. We are subject to regulations of the U.S. Environmental Protection Agency and the Occupational Health and Safety Administration and their counterpart state agencies. Compliance with government regulations and environmental laws has not had and is not expected to have a material effect upon the capital expenditures, earnings, or competitive position of our company. See Item 3.

AVAILABLE INFORMATION

We maintain a website with the address www.aosmith.com. The information contained on our website is not included as a part of, or incorporated by reference into, this Annual Report on Form 10-K. Other than an investor’s own internet access charges, we make available free of charge through our website our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports as soon as reasonably practical after we have electronically filed such material with, or furnished such material to, the Securities and Exchange Commission (SEC). All reports we file with the SEC are also available free of charge via EDGAR through the SEC’s website at www.sec.gov.

We are committed to sound corporate governance and have documented our corporate governance practices by adopting the A. O. Smith Corporate Governance Guidelines. The Corporate Governance Guidelines, Criteria for Selection of Directors, Financial Code of Ethics, the A. O. Smith Guiding Principles, as well as the charters for the Audit, Personnel and Compensation, Nominating and Governance and the Investment Policy Committees of the Board of Directors and other corporate governance materials, may be viewed on the company’s website. Any waiver of or amendments to the Financial Code of Conduct or the A. O. Smith Guiding Principles also would be posted on this website; to date there have been none. Copies of these documents will be sent to stockholders free of charge upon written request of the corporate secretary at the address shown on the cover page of this Annual Report on Form 10-K.

We are also committed to growing our business in a sustainable and socially responsible manner consistent with our Guiding Principles. This commitment has driven us to design, engineer, and manufacture highly innovative and efficient products in an environmentally responsible manner that help reduce energy consumption, conserve water, and improve drinking water quality and public health. Consistent with this commitment, we issued our 2020 Corporate Responsibility & Sustainability (CRS) report detailing our company’s historical and current CRS efforts. Our CRS report is available on our website. The report is not included as part of, or incorporated by reference into, this Annual Report on Form 10-K.

5

ITEM 1A – RISK FACTORS

In the ordinary course of our business, we face various strategic, operating, compliance and financial risks. These risks could have an impact on our business, financial condition, operating results and cash flows. The risks set forth below are not an exhaustive list of potential risks but reflect those that we believe to be material. You should carefully consider the risk factors set forth below and all other information contained in this Annual Report on Form 10-K, including the documents incorporated by reference, before making an investment decision regarding our common stock. If any of the events contemplated by the following risks were to actually occur, then our business, financial condition, or results of operations could be materially adversely affected. As a result, the trading price of our common stock could decline, and you may lose all or part of your investment.

Economic and Industry Risks

■The global coronavirus (COVID-19) pandemic, or other global public health pandemics, could have a material adverse effect on our business, results of operations and financial condition

Our business, results of operations and financial condition may be adversely affected if a global public health pandemic, including the current COVID-19 pandemic, interferes with the ability of our employees, suppliers, and customers to perform our and their respective responsibilities and obligations relative to the conduct of our business and operations. The COVID-19 pandemic has significantly impacted economic activity and markets around the world, and it could have a material negative impact on our business and operations in numerous ways, including but not limited to those outlined below:

•The risk that we, or our employees, suppliers or customers may be prevented from conducting business activities for an indefinite period of time, including shutdowns that may be requested or mandated by governmental authorities.

•Restrictions on shipping products from certain jurisdictions where they are produced or into certain jurisdictions where customers are located.

•Inability to meet our customers’ needs and achieve cost targets due to increased logistics costs, longer shipment times, and disruptions in our manufacturing and supply arrangements caused by the loss or disruption of essential manufacturing and supply elements, such as raw materials or other finished product components, transportation, workforce or other manufacturing and distribution capability.

•Failure of third parties on which we rely, including our suppliers, distributors, contractors and commercial banks, to meet their obligations to us, or significant disruptions in their ability to do so, which may be caused by their own financial or operational difficulties, or mandated shutdowns by governmental authorities, may adversely impact our operations.

•Significant reductions in demand, particularly for our commercial products, or significant volatility in demand and a global economic recession that could further reduce demand for our products, resulting from actions taken by governments, businesses, and/or the general public in an effort to limit exposure to and spreading of such infectious diseases, such as travel restrictions, quarantines, and business shutdowns or slowdowns. In addition, there is risk that the commercial sector, such as the restaurant and hospitality industries in which we have customers, will experience long-term shifts in consumer behavior which could negatively impact demand or capacity and may not return to pre-pandemic levels.

•Manufacturing plant inefficiencies due to safety and preventative health measures that we have implemented in our plants to prevent the spread of COVID-19.

•Deterioration of worldwide capital, credit, and financial markets that could limit our ability to obtain external financing to fund our operations and capital expenditures.

The extent to which the COVID-19 pandemic, or other outbreaks of disease or similar public health threats, materially and adversely impacts our business, results of operations and financial condition is highly uncertain and will depend on future developments. Such developments may include the geographic spread and duration of the virus, the severity of the virus and the actions that may be taken by various governmental authorities and other third parties in response to the outbreak. In addition, we cannot predict how quickly, and to what extent, normal economic and operating conditions can resume, and the resumption of normal business operations may be delayed or constrained by lingering effects of the COVID-19 pandemic on our suppliers, third-party service providers, and/or customers.

■The effects of a global economic downturn could have a material adverse effect on our business

Global economic growth remains volatile and could stall or reverse course. A continuation or deepening of the global economic downturn could adversely affect consumer confidence and spending patterns which could result in decreased demand for the products we sell, a delay in purchases, increased price competition, or slower adoption of energy-efficient water heaters and boilers, or high-quality water treatment products, which could negatively impact our profitability and cash flows. In addition, a deterioration in current economic conditions due to many factors or fears including public health crises

6

or political instability, could negatively impact our vendors and customers, which could result in an increase in bad debt expense, customer and vendor bankruptcies, interruption or delay in supply of materials, or increased material prices, which could negatively impact our ability to distribute, market and sell our products and our financial condition, results of operations and cash flows.

■Because approximately 24 percent of our net sales in 2020 were attributable to China, adverse economic conditions or changes in consumer behavior in China could impact our business

Our sales in China decreased in 2020 compared to 2019. We believe the decrease was due to business closures and restrictions associated with the COVID-19 pandemic, weaker end-market demand, a higher sales mix of mid-price products versus premium price products and further reductions to previously elevated channel inventory levels. We derive a substantial portion of our sales in China from premium-tier products. Changes in consumer preferences and purchasing behaviors including preferences for e-commerce, weakening consumer confidence and sentiment as well as economic uncertainty, socio-political risks, increased competition from Chinese based companies, and the potential future impact of the COVID-19 pandemic, may prompt Chinese consumers to postpone purchases, choose lower-priced products or different alternatives, or lengthen the cycle of replacement purchases. Further deterioration in the Chinese economy may adversely affect our financial condition, results of operations and cash flows.

■Because we participate in markets that are highly competitive, our revenues and earnings could decline as we respond to competition

We sell all of our products in highly competitive and evolving markets. We compete in each of our targeted markets based on product design, reliability, quality of products and services, advanced technologies, product performance, maintenance costs and price. Some of our competitors may have greater financial, marketing, manufacturing, research and development and distribution resources than we have; others may invest little in technology or product development but compete on price and the rapid replication of features, benefits, and technologies, and some are increasingly expanding beyond their existing manufacturing or geographic footprints. In North America, the gas tankless portion of the water heating market has for many years increased as a percentage of the overall market. While we have many gas tankless products, our market share for gas tankless products is lower than our market share for the remainder of the water heating market. Further expansion of the gas tankless portion of the North America market, which we believe was approximately ten percent of the residential market segment in 2020, could have an impact on our operating results. We cannot assure that our products will continue to compete successfully with those of our competitors. There could be new market participants that change the dynamics of those markets and it is possible that we will not be able to retain our customer base or improve or maintain our profit margins on sales to our customers, all of which could materially and adversely affect our financial condition, results of operations and cash flows.

■Our business could be adversely impacted by changes in consumer purchasing behavior, consumer preferences and technological changes

Consumer preferences for products and the methods in which they purchase products are constantly changing based on, among other factors, cost, convenience, environmental and social concerns and perceptions. Consumer purchasing behavior may shift the product mix in the markets we participate in or result in a shift to new distribution channels, including e-commerce, which continues to expand. For example, consumer preferences may shift toward more efficient gas products or electric powered products due to the increased attention on the impact of greenhouse gas emissions on the environment in response to utility incentive programs, or the emergence of state or federal incentives. In addition, technologies are ever changing. Our ability to timely develop and successfully market new products and to develop, acquire, and retain necessary intellectual property rights is essential to our continued success, but cannot reasonably be assured. It is possible that we will not be able to develop new technologies, products or distribution channels to align with consumer purchasing behavior and consumer preferences, which could materially and adversely affect our financial condition, results of operations and cash flows.

■The occurrence or threat of extraordinary events, including natural disasters, political disruptions, terrorist attacks, public health issues, and acts of war, could significantly disrupt production, or impact consumer spending

As a global company with a large international footprint, we are subject to increased risk of damage or disruption to us and our employees, facilities, suppliers, distributors, or customers. Extraordinary events, including natural disasters, political disruptions, terrorist attacks, public health issues, such as the current COVID-19 pandemic, and acts of war may disrupt our business and operations and impact our supply chain and access to necessary raw materials or could adversely affect the economy generally, resulting in a loss of sales and customers. One of our manufacturing plants is located within a floodplain that has experienced past flooding events. We also have other manufacturing facilities located in hurricane and earthquake zones. Any of these disruptions or other extraordinary events outside of our control that impact our operations or the operations of our suppliers and key distributors could affect our business negatively, harming operating results. In addition,

7

these types of events also could negatively impact consumer spending in the impacted regions or depending on the severity, globally, which could materially and adversely affect our financial condition, results of operations and cash flows.

Business, Operational, and Strategic Risks

■We sell our products and operate outside the U.S., and to a lesser extent, rely on imports and exports, which may present additional risks to our business

Approximately 33 percent of our net sales in 2020 were attributable to products sold outside of the U.S., primarily in China and Canada, and to a lesser extent in Europe and India. We also have operations and business relationships outside the U.S. that comprise a portion of our manufacturing, supply, and distribution. Approximately 7,500 of our 13,900 employees as of December 31, 2020 were located in China. At December 31, 2020, approximately $524 million of cash and marketable securities were held by our foreign subsidiaries, substantially all of which were located in China. International operations generally are subject to various risks, including: political, religious, and economic instability; local labor market conditions; new or increased tariffs or other trade restrictions, or changes to trade agreements; the impact of foreign government regulations, actions or policies; the effects of income taxes; governmental expropriation; the imposition or increases in withholding and other taxes on remittances and other payments by foreign subsidiaries; labor relations problems; the imposition of environmental or employment laws, or other restrictions or actions by foreign governments; and differences in business practices. Unfavorable changes in the political, regulatory, or trade climate, diplomatic relations, or government policies, particularly in relation to countries where we have a presence, including Canada, China, India and Mexico, could have a material adverse effect on our financial condition, results of operations and cash flows or our ability to repatriate funds to the U.S.

■A material loss, cancellation, reduction, or delay in purchases by one or more of our largest customers could harm our business

Net sales to our five largest customers represented approximately 43 percent of our sales in 2020. We expect that our customer concentration will continue for the foreseeable future. Our concentration of sales to a relatively small number of customers makes our relationships with each of these customers important to our business. We cannot assure that we will be able to retain our largest customers. Some of our customers may shift their purchases to our competitors in the future. Other customers may experience financial instability. Further, a customer may be acquired by a customer of a competitor which could result in our loss of that customer. The loss of one or more of our largest customers, any material reduction or delay in sales to these customers, or our inability to successfully develop relationships with additional customers could have a material adverse effect on our financial position, results of operations and cash flows.

■A portion of our business could be adversely affected by a decline in North American new residential construction further decline in commercial construction or a decline in replacement related volume of water heaters and boilers

Residential new construction activity in North America and industry-wide replacement-related volume of water heaters have shown growth which could decline in the future. Commercial construction activity in North America declined in 2020 after growing modestly in 2019. We believe that the significant majority of the markets we serve are for replacement of existing products, and residential water heater replacement volume was strong in 2020. Changes in the replacement volume and in the construction market in North America could negatively affect us.

■Our operations could be adversely impacted by material and component price volatility and availability, as well as supplier concentration

The market prices for certain materials and components we purchase, primarily steel, have been volatile. In addition, some components are subject to long lead times. We engage in ongoing communications with our suppliers to identify and mitigate risk of potential disruptions and to manage inventory levels. Significant increases in the cost of any of the key materials and components we purchase could increase our cost of doing business and ultimately could lead to lower operating earnings if we are not able to recover these cost increases through price increases to our customers. Historically, there has been a lag in our ability to recover increased material costs from customers, and that lag could negatively impact our profitability. Limited component availability and long lead times could make it difficult for us to meet customer demand. In some cases, we are dependent on a limited number of suppliers for some of the raw materials and components we require in the manufacturing of our products. A significant disruption or termination of the supply from one of these suppliers could delay sales or increase costs which could result in a material adverse effect on our financial condition, results of operations and cash flows.

8

■An inability to adequately maintain our information systems and their security, as well as to protect data and other confidential information, could adversely affect our business and reputation

In the ordinary course of business, we utilize information systems for day-to-day operations, to collect and store sensitive data and information, including our proprietary and regulated business information and personally identifiable information of our customers, suppliers and business partners, as well as personally identifiable information about our employees. Our information systems, like those of other companies, are susceptible to outages due to system failures, cybersecurity threats, failures on the part of third-party information system providers, natural disasters, power loss, telecommunications failures, viruses, fraud, theft, malicious actors or breaches of security. We have a response plan in place in the event of a data breach and we continue to take steps to maintain and improve data security and address these risks and uncertainties by implementing and improving internal controls, security technologies, insurance programs, network and data center resiliency and recovery processes. However, any operations failure or breach of security which are occurring with increasing frequency from increasingly sophisticated cyber threats could lead to disruptions of our business activities, the loss or disclosure of both our and our customers’ financial, product and other confidential information and could result in regulatory actions, litigation and have a material adverse effect on our financial condition, results of operations and cash flows and our reputation.

■Our international operations are subject to risks related to foreign currencies

We have a significant presence outside of the U.S., primarily in China and Canada and to a lesser extent Europe, Mexico, and India, and therefore, hold assets, including $385 million of cash and marketable securities denominated in Chinese renminbi, incur liabilities, earn revenues and pay expenses in a variety of currencies other than the U.S. dollar. The financial statements of our foreign subsidiaries are translated into U.S. dollars in our consolidated financial statements. Furthermore, typically our products are priced in foreign countries in local currencies. As a result, we are subject to risks associated with operating in foreign countries including fluctuations in currency exchange rates and interest rates, hyperinflation in some foreign countries or global exchange rate instability or volatility that strengthens the U.S. dollar against foreign currencies. As a result, an increase in the value of the U.S. dollar relative to the local currencies of our foreign markets has had and could have a negative effect on our profitability. In addition to currency translation risks, we incur a currency transaction risk whenever one of our subsidiaries enters into either a purchase or sale transaction using a currency different from the operating subsidiaries’ functional currency. The majority of our foreign currency transaction risk results from sales of our products in Canada which we manufacture in the U.S, and to a lesser extent from component purchases in Europe and payroll in Mexico. These risks may hurt our reported sales and profits in the future or negatively impact revenues and earnings translated from foreign currencies into U.S. dollars.

■Our business may be adversely impacted by product defects

Product defects can occur through our own product development, design and manufacturing processes or through our reliance on third parties for component design and manufacturing activities. We may incur various expenses related to product defects, including product warranty costs, product liability and recall or retrofit costs. While we maintain a reserve for product warranty costs based on certain estimates and our knowledge of current events and actions, our actual warranty costs may exceed our reserve, resulting in current period expenses and a need to increase our reserves for warranty charges. In addition, product defects and recalls may diminish the reputation of our brand. Further, our inability to cure a product defect could result in the failure of a product line or the temporary or permanent withdrawal from a product or market. Any of these events may have a material adverse impact on our financial condition, results of operations and cash flows.

■Potential acquisitions could use a significant portion of our capital and we may not successfully integrate future acquisitions or operate them profitably or achieve strategic objectives

We will continue to evaluate potential acquisitions, and we could use a significant portion of our available capital to fund future acquisitions. If we complete any future acquisitions, we may not be able to successfully integrate the acquired businesses or operate them profitably or accomplish our strategic objectives for those acquisitions. If we complete any future acquisitions in new geographies, our unfamiliarity with local regulations and market customs may impact our ability to operate them profitably or achieve our strategic objectives for those acquisitions. Our level of indebtedness may increase in the future if we finance acquisitions with debt, which would cause us to incur additional interest expense and could increase our vulnerability to general adverse economic and industry conditions and limit our ability to service our debt or obtain additional financing. The impact of future acquisitions may have a material adverse effect on our financial condition, results of operations and cash flows.

Legal, Regulatory, and Governance Risks

■Changes in regulations or standards could adversely affect our business

Our products are subject to a wide variety of statutory, regulatory and industry standards and requirements related to, among other items, energy and water efficiency, environmental emissions, labeling and safety. While we believe our products are

9

currently efficient, safe and environment-friendly, federal, foreign, state and local governments are adopting laws, regulations and codes that will require a transition to non-fossil fuel based sources of energy production as well as significantly reducing or eliminating the on-site combustion of fossil fuels in the building sector, such as limiting or prohibiting the delivery of natural gas in new construction. A significant change to regulatory requirements that promote a transition to alternative energy sources as a replacement for gas, or a significant shift in industry standards, could substantially increase manufacturing costs, impact the size and timing of demand for our products, affect the types of products we are able to offer or put us at a competitive disadvantage, any of which could harm our business and have a material adverse effect on our financial condition, results of operations and cash flow.

■We are subject to U.S. and global laws and regulations covering our domestic and international operations that could adversely affect our business and results of operations

Due to our global operations, we are subject to many laws governing international relations, including those that prohibit improper payments to government officials and restrict where we can do business, what information or products we can supply to certain countries and what information we can provide to a non-U.S. government, including but not limited to the Foreign Corrupt Practices Act and the U.S. Export Administration Act. Violations of these laws may result in criminal penalties or sanctions that could have a material adverse effect on our financial condition, results of operations and cash flows.

■Our results of operations may be negatively impacted by product liability lawsuits and claims

Our products expose us to potential product liability risks that are inherent in the design, manufacture, sale and use of our products. While we currently maintain what we believe to be suitable product liability insurance, we cannot be certain that we will be able to maintain this insurance on acceptable terms, that this insurance will provide adequate protection against potential liabilities or that our insurance providers will be able to ultimately pay all insured losses. In addition, we self-insure a portion of product liability claims. A series of successful claims against us could materially and adversely affect our reputation and our financial condition, results of operations and cash flows.

■We have significant goodwill and indefinite-lived intangible assets and an impairment of our goodwill or indefinite-lived intangible assets could cause a decline in our net worth

Our total assets include significant goodwill and indefinite-lived intangible assets. Our goodwill results from our acquisitions, representing the excess of the purchase prices we paid over the fair value of the net tangible and intangible assets we acquired. We assess whether there have been impairments in the value of our goodwill or indefinite-lived intangible assets during the fourth quarter of each calendar year or sooner if triggering events warrant. If future operating performance at our businesses does not meet expectations, we may be required to reflect non-cash charges to operating results for goodwill or indefinite-lived intangible asset impairments. The recognition of an impairment of a significant portion of goodwill or indefinite-lived intangible assets would negatively affect our results of operations and total capitalization, the effect of which could be material. A significant reduction in our stockholders’ equity due to an impairment of goodwill or indefinite-lived intangible assets may affect our ability to maintain the debt-to-capital ratio required under our existing debt arrangements. We have identified the valuation of goodwill and indefinite-lived intangible assets as a critical accounting policy. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Critical Accounting Policies—Goodwill and Indefinite-lived Intangible Assets” included in Item 7 of this Annual Report on Form 10-K.

■Our pension plans may require future pension contributions which could limit our flexibility in managing our company

The projected benefit obligation liability of our defined benefit pension plans of $870 million exceeded the fair value of the plan assets of $859 million by approximately $11 million at December 31, 2020. U.S. employees hired after January 1, 2010 have not participated in our defined benefit plan, and benefit accruals for the majority of current salaried and hourly employees ended on December 31, 2014. We forecast that we will not be required to make a contribution to the plan in 2021, and we do not plan to make any voluntary contributions. However, we cannot provide any assurance that contributions will not be required in the future. Among the key assumptions inherent in our actuarially calculated pension plan obligation and pension plan expense are the discount rate and the expected rate of return on plan assets. If interest rates and actual rates of return on invested plan assets were to decrease significantly, our pension plan obligations could increase materially. The size of future required pension contributions could result in us dedicating a significant portion of our cash flows from operations to making contributions which could negatively impact our flexibility in managing our company.

■Certain members of the founding family of our company and trusts for their benefit have the ability to influence all matters requiring stockholder approval

We have two classes of common equity: our Common Stock and our Class A Common Stock. The holders of Common Stock currently are entitled, as a class, to elect only one-third of our board of directors. The holders of Class A Common Stock are entitled, as a class, to elect the remaining directors. Certain members of the founding family of our company and trusts for

10

their benefit (Smith Family) have entered into a voting trust agreement with respect to shares of our Class A Common Stock and shares of our Common Stock they own. As of December 31, 2020, through the voting trust, these members of the Smith Family own approximately 63.8 percent of the total voting power of our outstanding shares of Class A Common Stock and Common Stock, taken together as a single class, and approximately 96.6 percent of the voting power of the outstanding shares of our Class A Common Stock, as a separate class. Due to the differences in the voting rights between shares of our Common Stock (one-tenth of one vote per share) and shares of our Class A Common Stock (one vote per share), the Smith Family voting trust is in a position to control to a large extent the outcome of matters requiring a stockholder vote, including the adoption of amendments to our certificate of incorporation or bylaws or approval of transactions involving a change of control. This ownership position may increase if other members of the Smith Family enter into the voting trust agreement, and the voting power relating to this ownership position may increase if shares of our Class A Common Stock held by stockholders who are not parties to the voting trust agreement are converted into shares of our Common Stock. The voting trust agreement provides that, in the event one of the parties to the voting trust agreement wants to withdraw from the trust or transfer any of its shares of our Class A Common Stock, such shares of our Class A Common Stock are automatically exchanged for shares of our Common Stock held by the trust to the extent available in the trust. In addition, the trust will have the right to purchase the shares of our Class A Common Stock and our Common Stock proposed to be withdrawn or transferred from the trust. As a result, the Smith Family members that are parties to the voting trust agreement have the ability to maintain their collective voting rights in our company even if certain members of the Smith Family decide to transfer their shares.

ITEM 1B – UNRESOLVED STAFF COMMENTS

None.

ITEM 2 – PROPERTIES

Properties utilized by us at December 31, 2020 were as follows:

North America

In this segment, we have 16 manufacturing plants located in eight states and two non-U.S. countries, of which 14 are owned directly by us or our subsidiaries and two are leased from outside parties. The terms of leases in effect at December 31, 2020 expire between 2021 and 2025.

Rest of World

In this segment, we have six manufacturing plants located in four non-U.S. countries, of which four are owned directly by us or our subsidiaries and two are leased from outside parties. The terms of leases in effect at December 31, 2020 expire between 2022 and 2025.

Corporate and General

We consider our plants and other physical properties to be suitable, adequate, and of sufficient productive capacity to meet the requirements of our business. The manufacturing plants operate at varying levels of utilization depending on the type of operation and market conditions. The executive offices of the company, which are leased, are located in Milwaukee, Wisconsin.

ITEM 3 – LEGAL PROCEEDINGS

We are involved in various unresolved legal actions, administrative proceedings and claims in the ordinary course of our business involving product liability, property damage, insurance coverage, exposure to asbestos and other substances, patents and environmental matters, including the disposal of hazardous waste. Although it is not possible to predict with certainty the outcome of these unresolved legal actions or the range of possible loss or recovery, we believe, based on past experience, adequate reserves and insurance availability, that these unresolved legal actions will not have a material effect on our financial position or results of operations. A more detailed discussion of certain of these matters appears in Note 16 of Notes to Consolidated Financial Statements.

On May 28, 2019, a putative securities class action lawsuit was filed in the U.S. District Court for the Eastern District of Wisconsin against the Company and certain of its current or former officers. Subsequently, on November 22, 2019, a consolidated amended complaint was filed by the lead plaintiff. This action, captioned as City of Birmingham Retirement and Relief System v. A. O. Smith Corporation, et al., asserted securities fraud claims under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 (“Exchange Act”), and sought damages and other relief based upon the allegations in the complaint. On January 24, 2020, A. O. Smith and the other defendants moved to dismiss the consolidated amended complaint

11

for failure to state a claim. On June 24, 2020, the U.S. District Court granted defendants’ motion to dismiss in its entirety. Based on its June 24, 2020 order, on August 3, 2020, the District Court entered final judgement for the defendants and dismissed the lawsuit.

A shareholder derivative lawsuit, captioned as Pierce v. A. O. Smith Corporation, et al. and based on similar allegations as the putative class action, was filed on August 20, 2019, also in the U.S. District Court for the Eastern District of Wisconsin. On November 6, 2019, the plaintiff in the derivative action moved to dismiss his lawsuit, and the plaintiff re-filed it in the U.S. District Court for the District of Delaware on November 12, 2019. The derivative action asserted claims under Sections 14(a) and 20(a) of the Exchange Act, as well as for breach of fiduciary duty, unjust enrichment, and waste of corporate assets, and sought damages and other relief based upon the allegations in the complaint. On February 12, 2020, the parties filed a stipulation seeking to stay the derivative lawsuit pending resolution of the City of Birmingham lawsuit. On February 13, 2020, a second shareholder derivative suit, captioned as Jarozewski v. A. O. Smith Corporation, et al., was filed in the U.S. District Court for the District of Delaware, to assert claims under Sections 10(b), 14(a) and 20(a) of the Exchange Act, as well as for breach of fiduciary duty, unjust enrichment, and insider trading, and sought damages and other relief based upon the allegations in the complaint. On April 1, 2020, the U.S. District Court for the District of Delaware, upon a joint stipulation filed by the parties, consolidated both the Pierce and Jarozewski derivative lawsuits and stayed the consolidated actions pending resolution of the City of Birmingham lawsuit. On October 7, 2020, following dismissal of the City of Birmingham lawsuit and upon a joint stipulation filed by the parties, the District Court dismissed the consolidated derivative lawsuits. A. O. Smith and the other defendants paid no settlement consideration to achieve these dismissals.

ITEM 4 – MINE SAFETY DISCLOSURES

Not applicable.

12

EXECUTIVE OFFICERS OF THE COMPANY

Pursuant to General Instruction of G(3) of Form 10-K, the following is a list of our executive officers which is included as an unnumbered Item in Part I of this report in lieu of being included in our Proxy Statement for our 2021 Annual Meeting of Stockholders.

Name (Age) | Positions Held | Period Position Was Held | ||||||||||||

| Patricia K. Ackerman (60) | Senior Vice President – Investor Relations, Treasurer and Corporate Responsibility and Sustainability | 2019 to Present | ||||||||||||

| Vice President – Investor Relations & Treasurer | 2008 to 2018 | |||||||||||||

| Vice President and Treasurer | 2006 to 2008 | |||||||||||||

| Assistant Treasurer | 1995 to 2006 | |||||||||||||

| Paul R. Dana (58) | Senior Vice President – Global Operations | 2019 to Present | ||||||||||||

| Senior Vice President – Global Manufacturing | 2016 to 2018 | |||||||||||||

| Vice President – Global Manufacturing | 2015 | |||||||||||||

| President – APCOM, a division of State Industries, LLC, a subsidiary of the Company | 2011 to 2017 | |||||||||||||

| Vice President – Product Engineering | 2006 to 2010 | |||||||||||||

| Plant Manager – Productos de Agua, S. de R.L. de C.V. | 1998 to 2005 | |||||||||||||

| Anindadeb V. DasGupta (55) | Senior Vice President | 2018 to Present | ||||||||||||

| President – A. O. Smith Holdings (Barbados) SRL | 2018 to Present | |||||||||||||

Vice President, Global Head Strategic Marketing; Global Head e-commerce; Global GM Flex & Signage Business Lines – OSRAM GmbH, Munich and Hong Kong (lighting manufacturer) | 2014 to 2018 | |||||||||||||

| Wallace E. Goodwin (65) | Senior Vice President | 2018 to Present | ||||||||||||

| President and General Manager – Lochinvar, LLC | 2018 to Present | |||||||||||||

| Senior Vice President and General Manager – Lochinvar, LLC | 2011 to 2017 | |||||||||||||

| President – APCOM, a division of State Industries, LLC | 1999 to 2011 | |||||||||||||

| Robert J. Heideman (54) | Senior Vice President – Chief Technology Officer | 2013 to Present | ||||||||||||

| Senior Vice President – Engineering & Technology | 2011 to 2012 | |||||||||||||

| Senior Vice President – Corporate Technology | 2010 to 2011 | |||||||||||||

| Vice President – Corporate Technology | 2007 to 2010 | |||||||||||||

| Director – Materials | 2005 to 2007 | |||||||||||||

| Section Manager | 2002 to 2005 | |||||||||||||

| D. Samuel Karge (46) | Senior Vice President | 2018 to Present | ||||||||||||

| President – North America Water Treatment | 2018 to Present | |||||||||||||

| Vice President, Sales and Marketing – Zurn Industries (water solutions manufacturer) | 2016 to 2018 | |||||||||||||

| Vice President & Platform Leader – Pentair Residential Filtration (water solutions manufacturer) | 2012 to 2016 | |||||||||||||

| Daniel L. Kempken (48) | Senior Vice President – Strategy and Corporate Development | 2019 to Present | ||||||||||||

| Vice President and Controller | 2011 to 2019 | |||||||||||||

13

Name (Age) | Positions Held | Period Position Was Held | ||||||||||||

| Charles T. Lauber (58) | Executive Vice President and Chief Financial Officer | 2019 to Present | ||||||||||||

| Senior Vice President, Strategy and Corporate Development | 2013 to 2019 | |||||||||||||

| Senior Vice President – Chief Financial Officer – A. O. Smith Water Products Company | 2006 to 2012 | |||||||||||||

| Vice President – Global Finance – A. O. Smith Electrical Products Company | 2004 to 2006 | |||||||||||||

| Vice President and Controller – A. O. Smith Electrical Products Company | 2001 to 2004 | |||||||||||||

| Director of Audit and Tax | 1999 to 2001 | |||||||||||||

| Mark A. Petrarca (57) | Senior Vice President – Human Resources and Public Affairs | 2006 to Present | ||||||||||||

| Vice President – Human Resources and Public Affairs | 2005 to 2006 | |||||||||||||

| Vice President – Human Resources – A. O. Smith Water Products Company | 1999 to 2004 | |||||||||||||

| Jack Qiu (48) | Senior Vice President - A. O. Smith China | 2020 to Present | ||||||||||||

| Vice President - A. O. Smith China | 2012 to 2020 | |||||||||||||

| General Manager of Residential Gas SBU - A. O. Smith China | 2008 to 2012 | |||||||||||||

| Deputy General Manager, Engineering - A. O. Smith China | 2003 to 2008 | |||||||||||||

| Engineering Manager - York (Guangzhou) Air Conditioner and Refrigeration Equipment, Co., Ltd. | 2000 to 2003 | |||||||||||||

| S. Melissa Scheppele (58) | Senior Vice President - Chief Information Officer | 2020 to Present | ||||||||||||

| Vice President and Chief Information Officer - Triumph Group (aerospace and defense business) | 2016 to 2020 | |||||||||||||

| Vice President and Chief Information Officer - Ascend Performance Materials (specialty chemical manufacturer) | 2013 to 2016 | |||||||||||||

| James F. Stern (58) | Executive Vice President, General Counsel and Secretary | 2007 to Present | ||||||||||||

| Partner – Foley & Lardner LLP | 1997 to 2007 | |||||||||||||

| David R. Warren (57) | Senior Vice President | 2017 to Present | ||||||||||||

| President and General Manager – North America Water Heating | 2017 to Present | |||||||||||||

| Vice President – International | 2008 to 2017 | |||||||||||||

| Managing Director – A.O. Smith Water Products Company B.V. | 2004 to 2008 | |||||||||||||

| Director, Reliance Sales | 2002 to 2004 | |||||||||||||

| Regional Sales Manager | 1999 to 2002 | |||||||||||||

| District Sales Manager | 1990 to 1996 | |||||||||||||

| Sales Coordinator | 1989 to 1990 | |||||||||||||

14

Name (Age) | Positions Held | Period Position Was Held | ||||||||||||

| Kevin J. Wheeler (61) | Chairman | 2020 to Present | ||||||||||||

| President and Chief Executive Officer | 2018 to Present | |||||||||||||

| President and Chief Operating Officer | 2017 to 2018 | |||||||||||||

| Senior Vice President | 2013 to 2017 | |||||||||||||

| President and General Manager – North America, India and Europe Water Heating | 2013 to 2017 | |||||||||||||

| Senior Vice President and General Manager – North America, India and Europe – A. O. Smith Water Products Company | 2011 to 2012 | |||||||||||||

| Senior Vice President and General Manager – U.S. Retail – A. O. Smith Water Products Company | 2007 to 2011 | |||||||||||||

| Vice President – International – A. O. Smith Water Products Company | 2004 to 2007 | |||||||||||||

| Managing Director – A. O. Smith Water Products Company B.V. | 1999 to 2004 | |||||||||||||

15

PART II

ITEM 5 – MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

(a)Market Information. Our Common Stock is listed on the New York Stock Exchange under the symbol AOS. Our Class A Common Stock is not listed. EQ Shareowner Services, P.O. Box 64874, St. Paul, Minnesota, 55164-0874 serves as the registrar, stock transfer agent and the dividend reinvestment agent for our Common Stock and Class A Common Stock.

(b)Holders. As of January 29, 2021, the approximate number of stockholders of record of Common Stock and Class A Common Stock were 568 and 155, respectively. The actual number of stockholders is greater than this number of holders of record, and includes stockholders who are beneficial owners, but whose shares are held in street name by brokers and other nominees. This number of stockholders of record also does not include stockholders whose shares may be held in trust by other entities.

(c)Dividends. Dividends declared on the common stock are shown in Note 18 of Notes to Consolidated Financial Statements appearing elsewhere herein.

(d)Stock Repurchases. In the second quarter of 2019, our Board of Directors approved adding 3,000,000 shares of Common Stock to an existing discretionary share repurchase authority. Under the share repurchase program, the Common Stock may be purchased through a combination of Rule 10b5-1 automatic trading plan and discretionary purchases in accordance with applicable securities laws. The number of shares purchased and the timing of the purchases will depend on a number of factors, including share price, trading volume and general market conditions, as well as working capital requirements, general business conditions and other factors, including alternative investment opportunities. The stock repurchase authorization remains effective until terminated by our Board of Directors which may occur at any time, subject to the parameters of any Rule 10b5-1 automatic trading plan that we may then have in effect. Due to the uncertainty surrounding the impact of the global COVID-19 pandemic, we suspended our share repurchases on March 18, 2020. In 2020, we repurchased 1,348,391 shares at an average price of $42.02 per share and at a total cost of $56.7 million. As of December 31, 2020, there were 1,613,824 shares remaining on the existing repurchase authorization. On January 27, 2021, the Board of Directors approved adding 7,000,000 shares of common stock to the existing discretionary share repurchase authority. Including the additional shares, we have approximately 8.6 million shares available for repurchase. We currently intend to spend approximately $400 million to repurchase common stock in 2021 through a combination of 10b5-1 plans and open market purchases.

(e)Performance Graph. The following information in this Item 5 of this Annual Report on Form 10-K is not deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to the liabilities of Section 18 of the Securities Exchange Act of 1934, and will not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate it by reference into such a filing.

16

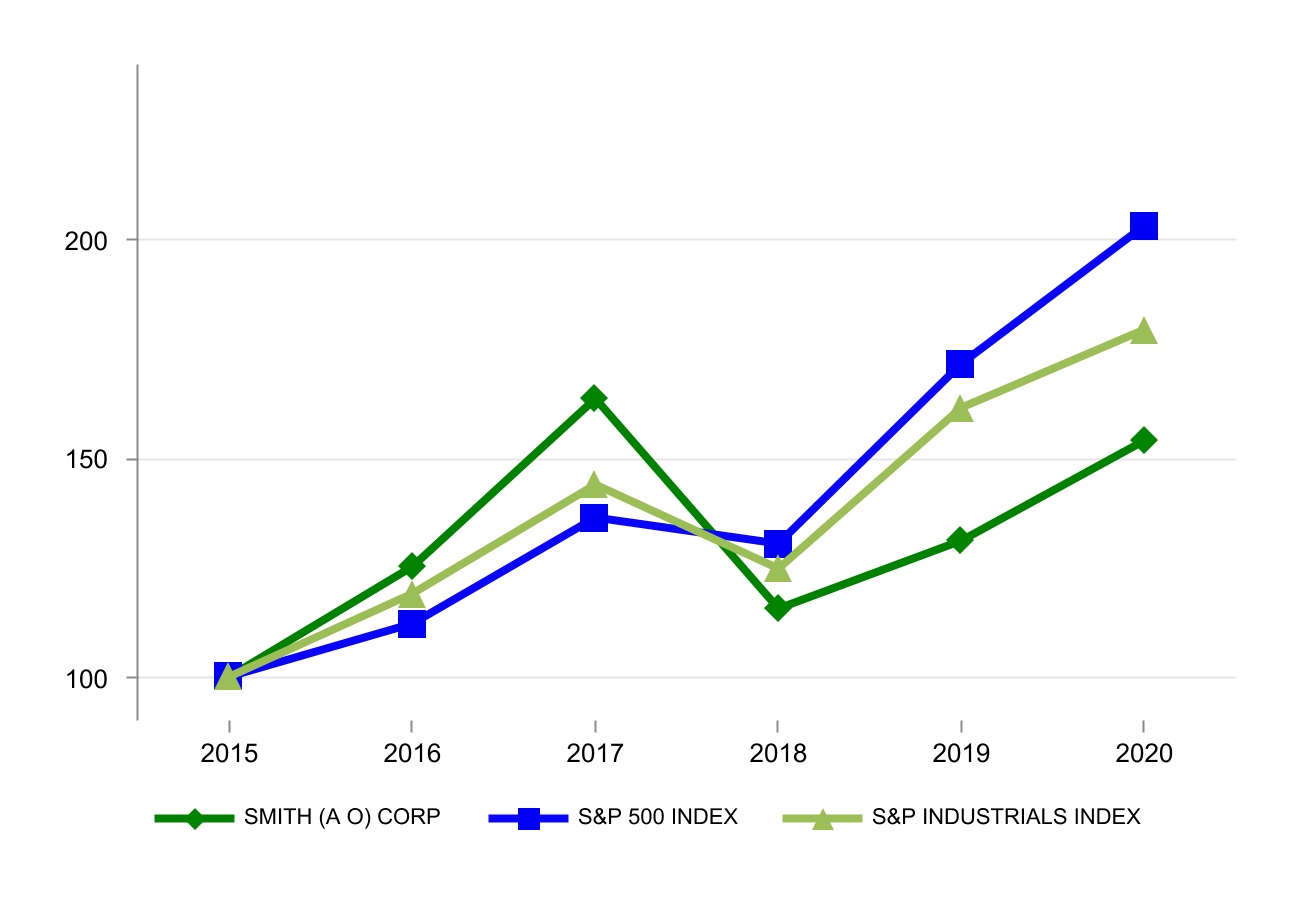

The graph below shows a five-year comparison of the cumulative shareholder return on our Common Stock with the cumulative total return of the Standard & Poor’s (S&P) 500 Index, S&P 500 Select Industrials Index, which are published indices.

Comparison of Five-Year Cumulative Total Return

From December 31, 2015 to December 31, 2020

Assumes $100 Invested with Reinvestment of Dividends

| Base Period | Indexed Returns | ||||||||||||||||||||||||||||||||||

| Company/Index | 12/31/15 | 12/31/16 | 12/31/17 | 12/31/18 | 12/31/19 | 12/31/20 | |||||||||||||||||||||||||||||

| A. O. Smith Corporation | 100.0 | 125.0 | 163.5 | 115.4 | 131.1 | 154.0 | |||||||||||||||||||||||||||||

| S&P 500 Index | 100.0 | 112.0 | 136.4 | 130.4 | 171.5 | 203.1 | |||||||||||||||||||||||||||||

| S&P 500 Select Industrial Index | 100.0 | 118.9 | 143.9 | 124.7 | 161.4 | 179.2 | |||||||||||||||||||||||||||||

17

ITEM 6 – SELECTED FINANCIAL DATA

| (dollars in millions, except per share amounts) | |||||||||||||||||||||||||||||

| Years ended December 31, | |||||||||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017(1) | 2016(2) | |||||||||||||||||||||||||

| Net sales | $ | 2,895.3 | $ | 2,992.7 | $ | 3,187.9 | $ | 2,996.7 | $ | 2,685.9 | |||||||||||||||||||

Net earnings(1) | $ | 344.9 | $ | 370.0 | $ | 444.2 | $ | 296.5 | $ | 326.5 | |||||||||||||||||||

Basic earnings per share of common stock(1,2) | |||||||||||||||||||||||||||||

| Net earnings | $ | 2.13 | $ | 2.24 | $ | 2.60 | $ | 1.72 | $ | 1.87 | |||||||||||||||||||

Diluted earnings per share of common stock(1,2) | |||||||||||||||||||||||||||||

| Net earnings | $ | 2.12 | $ | 2.22 | $ | 2.58 | $ | 1.70 | $ | 1.85 | |||||||||||||||||||

Cash dividends per common share(2) | $ | 0.98 | $ | 0.90 | $ | 0.76 | $ | 0.56 | $ | 0.48 | |||||||||||||||||||

| Years ended December 31, | |||||||||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | |||||||||||||||||||||||||

| Total assets | $ | 3,160.7 | $ | 3,058.0 | $ | 3,071.5 | $ | 3,197.4 | $ | 2,891.0 | |||||||||||||||||||

Long-term debt(3) | 106.4 | 277.2 | 221.4 | 402.9 | 316.4 | ||||||||||||||||||||||||

| Total stockholders’ equity | 1,848.3 | 1,666.8 | 1,717.0 | 1,644.9 | 1,511.4 | ||||||||||||||||||||||||

(1)Due to the enactment of the U.S. Tax Cuts & Jobs Act in December 2017, we recorded a one-time charge of $81.8 million in 2017, our estimate of the costs primarily associated with the repatriation of undistributed foreign earnings. These charges reduced 2017 earnings per share by $0.47.

(2)In September 2016, we declared a 100 percent stock dividend to holders of Common Stock and Class A Common Stock which is not included in cash dividends. Basic and diluted earnings per share are calculated using the weighted average shares outstanding which were restated for all periods presented to reflect the stock dividend.

(3)Excludes the current portion of long-term debt.

18

ITEM 7 – MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

OVERVIEW

Our company is comprised of two reporting segments: North America and Rest of World. Our Rest of World segment is primarily comprised of China, Europe and India. Both segments manufacture and market comprehensive lines of residential and commercial gas and electric water heaters, boilers, tanks, and water treatment products. Both segments primarily manufacture and market in their respective region of the world.

In January 2020, an outbreak of a novel coronavirus (COVID-19) surfaced in Wuhan, China. As a result of the outbreak, the Chinese government required businesses to close and restricted certain travel within the country. In cooperation with the government authorities, our operations in China closed for approximately four weeks before resuming production before the end of the first quarter. In March 2020, COVID-19 was declared a global pandemic and we experienced impacts to our business and other markets worldwide. To date, our global manufacturing operations of essential water heating and water treatment products continue without material disruption to our operations. As a result of the COVID-19 pandemic and in support of continuing our manufacturing efforts, we have undertaken numerous and meaningful steps to protect our employees, suppliers, and customers. These important steps, which in certain cases reduce efficiency, include continuous communication and training to our employees on living and working safely in a COVID-19 environment, plant accommodations and reconfigurations to maintain social distancing, masks for all employees, implementation of sanitizing stations, temperature taking and regular, proactive deep cleaning and sanitization of our facilities, among others. As we receive guidance from governmental authorities, we adjust our safety measures to meet or exceed those guidelines. The majority of our customers in the U.S. are also deemed essential under Cybersecurity and Infrastructure Security Agency (CISA) guidance and are operating their businesses under varying state and local governmental guidance.

Our global supply chain management team continues to monitor and manage our ability to operate effectively during the COVID-19 pandemic. To date, we have not seen any material disruptions to our supply chain, although we have seen an increase in logistics costs and shipment times as a result of pandemic-related capacity reductions. Ongoing communications with our suppliers to identify and mitigate risk of potential disruptions and to manage inventory levels continue. Our U.S. water heater manufacturing lead times, which were extended in the second and third quarters due to self-quarantine absenteeism mandated by our COVID-19 prevention measures, stabilized in the fourth quarter of 2020 as a result of adding manufacturing shifts, hiring temporary workers and shifting some production.

While we believe our balance sheet and capital position are strong, proactive management of discretionary spending and cost structure will continue. On May 1, 2020, the members of our Board of Directors voluntarily reduced the cash component of their board compensation by 25 percent and our chairman and chief executive officer (CEO) voluntarily reduced his base salary by 25 percent. Our CEO’s staff, which includes our other named executive officers, also volunteered a 15 percent reduction in base salary. Full compensation of our Board of Directors, our CEO and our CEO’s staff was reinstated on October 1, 2020.

We estimate that between 80 to 85 percent of our water heater and boiler units sold in the U.S. relate to replacement business. While we expect that our replacement business in both water heating and boilers will provide a buffer in any economic downturn resulting from COVID-19 in a similar manner to what we have seen historically, the impacts of the pandemic on consumer spending are difficult to predict.

In our North America segment, we expect industry residential water heater volumes will be down approximately two percent in 2021 compared with 2020, which is driven by our belief that customers may have added inventory in 2020 due to industry extended lead times. We believe that some de-stocking by our customers will occur in early 2021 as our lead times have improved and continue to improve. We believe that commercial water heater industry volumes will further decline approximately four percent in 2021 as COVID-19 pandemic-impacted businesses delay or defer new construction and discretionary replacement installations. We expect to see a mid-single digit increase to our boiler sales in 2021 compared to 2020 due to industry growth of three to four percent driven by pandemic-related pent up demand as well as our new product introductions. We expect sales of our North America water treatment products to increase by 13 to 14 percent in 2021, compared to 2020, primarily driven by consumer demand for our point of use and point of entry water treatment systems.

In our Rest of World segment, we expect China sales in 2021 to increase 14 to 15 percent in local currency compared with 2020 due to increased consumer demand. We assume China currency rates will stay at current levels and which would add approximately $47 million and $3 million to sales and earnings in 2021, respectively. In addition, we project that our mix of products sold in China is shifting to more mid-price range products from our historical mix of higher priced products. We also continue to focus on aligning our cost structure in China through headcount reductions, store closures, cuts in advertising

19

and other cost saving measures. Our 2020 headcount reductions and restructuring actions we took were largely completed as of the end of the third quarter of 2020.

Combining all of these factors, we expect our consolidated sales to increase approximately ten percent in 2021. Our guidance excludes the potential impacts from future acquisitions and assumes the conditions of our business environment and that of our suppliers and customers are similar in 2021 to what we are experienced in recent months and does not deteriorate as a result of further restrictions or shutdowns due to the COVID-19 pandemic.

Our stated acquisition strategy includes a number of our water-related strategic initiatives. We will seek to continue to grow our core residential and commercial water heating, boiler and water treatment businesses throughout the world. We will also continue to look for opportunities to add to our existing operations in high growth regions demonstrated by our introduction of water treatment products in India and Vietnam and range hoods and cooktops in China.

RESULTS OF OPERATIONS

Our sales in 2020 were $2,895 million, a decline of 3.3 percent compared to our 2019 sales of $2,993 million. Compared to 2019, our sales decline in 2020 was primarily driven by lower sales in China and lower commercial water heater volumes, and reduced boiler sales in North America. The decreased sales in 2020 compared to the prior year more than offset higher water treatment volumes including incremental sales of $16 million from Water-Right, acquired on April 8, 2019 and higher residential water heater volumes in North America. In addition, our sales in China were favorably impacted by currency translation of approximately $9 million in 2020 compared to 2019, due to the appreciation of the Chinese currency compared to the U.S. dollar. Our sales in 2019 were $2,993 million, a decline of 6.1 percent compared to our 2018 sales of $3,188 million. The decrease in 2019 sales was primarily due to a 23 percent decline in China sales in U.S. dollar terms, which was largely a result of weaker end-market demand in the region, year over year channel inventory shifts, and a higher mix of sales of mid-price products versus premium price products than in the prior year. Excluding the unfavorable impact from currency translation, China sales declined 19 percent in 2019. The sales reduction in China in 2019 compared to 2018, more than offset the benefits of higher sales in North America, which were primarily a result of higher sales of water treatment products, including incremental sales from our Water-Right acquisition, and water heater pricing actions related to steel and freight cost increases. The increase in North America sales in 2019 compared to 2018, was partially offset by lower residential water heater volumes.

Our gross profit margin in 2020 of 38.3 percent declined compared to our gross profit margin of 39.5 percent in 2019 primarily due to the lower sales volumes. Our gross profit margin in 2019 of 39.5 percent declined compared to our gross profit margin of 41.0 percent in 2018, primarily due to the lower sales volumes in China and a higher mix of mid-price products, which have lower margins, in that region.

Selling, general, and administrative (SG&A) expenses were $660.3 million in 2020 or $55.3 million lower than 2019. SG&A expenses were $715.6 million in 2019 or $38.2 million lower than in 2018. The decrease in SG&A expenses in both 2020 and 2019 was primarily due to lower selling and advertising expenses in China.

To align our business to current market conditions, we recognized $7.7 million of pre-tax severance and restructuring expenses in 2020. Charges recognized were comprised of $6.8 million severance costs and $0.9 million of other restructuring expenses. On March 21, 2018, we announced a plan to transfer water heater, boiler and storage tank production from our Renton, Washington plant to our other U.S. plants. The majority of the consolidation of operations occurred in the second quarter of 2018. As a result of the relocation of production, we incurred pre-tax restructuring and impairment expenses of $6.7 million in the first quarter of 2018, primarily related to employee severance, building lease exit costs, and the impairment of assets. These activities are reflected in "severance, restructuring, and impairment expenses" in the accompanying financial statements.

We provide non-U.S. Generally Accepted Accounting Principles (GAAP) measures (adjusted earnings, adjusted earnings per share, and adjusted segment earnings) that exclude severance, restructuring, and impairment expenses. Reconciliations to measures on a GAAP basis are provided later in this section. We believe that the measures of adjusted earnings, adjusted EPS, and adjusted segment earnings provide useful information to investors about our performance and allow management and our investors to better understand our performance between periods without regard to items we do not consider to be a component of our core operating performance.