UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

(Mark

One)

|

[X]

|

QUARTERLY

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

|

For the

quarterly period ended December 31, 2017

or

|

[ ]

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

|

For the

transition period from ___________ to __________

Commission

file number: 001-15543

________________________

PALATIN TECHNOLOGIES, INC.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

|

95-4078884

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

|

(I.R.S.

Employer Identification No.)

|

|

|

|

|

|

4B Cedar Brook Drive

Cranbury, New Jersey

|

|

08512

|

|

(Address

of principal executive offices)

|

|

(Zip

Code)

|

(609) 495-2200

(Registrant's

telephone number, including area code)

Indicate

by check mark whether the registrant (1) has filed all reports

required to be filed by Section 13 or 15(d) of the Securities

Exchange Act of 1934 during the preceding 12 months (or for such

shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirements for

the past 90 days.

Yes

☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically

and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405

of Regulation S-T (§232.405 of this chapter) during the

preceding 12 months (or for such shorter period that the registrant

was required to submit and post such

files). Yes ☒ No

☐

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the definitions of

“large accelerated filer,” “accelerated

filer,” “smaller reporting company,” and

“emerging growth company” in Rule 12b-2 of the Exchange

Act.

|

Large

accelerated

filer

☐

|

Accelerated

filer

☐

|

|

Non-accelerated

filer

☐ (Do not check if a

smaller reporting company)

|

Smaller

reporting company ☒

|

|

|

Emerging

growth company ☐

|

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 13(a) for the Exchange Act.

☐

Indicate

by check mark whether the registrant is a shell company (as defined

in Rule 12b-2 of the Exchange Act). Yes ☐ No

☒

As of

February 9, 2018, 195,373,239 shares of the registrant’s

common stock, par value $0.01 per share, were

outstanding.

Table of Contents

|

|

Page

|

|

PART I – FINANCIAL INFORMATION

|

|

|

Item 1. Financial Statements (Unaudited)

|

|

|

Consolidated

Balance Sheets as of December 31, 2017 and June 30,

2017

|

3

|

|

Consolidated

Statements of Operations for the Three and Six Months Ended

December 31, 2017 and 2016

|

4

|

|

Consolidated

Statements of Comprehensive Income (Loss) for the Three and Six

Months Ended December 31, 2017 and 2016

|

5

|

|

Consolidated

Statements of Cash Flows for the Three and Six Months Ended

December 31, 2017 and 2016

|

6

|

|

Notes

to Consolidated Financial Statements

|

7

|

|

Item 2. Management’s Discussion and Analysis of Financial

Condition and Results of Operations

|

19

|

|

Item 3. Quantitative and Qualitative Disclosures About Market

Risk

|

22

|

|

Item 4. Controls and Procedures

|

22

|

|

PART

II – OTHER INFORMATION

|

|

|

|

|

|

Item 1. Legal Proceedings

|

23

|

|

Item 1A. Risk Factors

|

23

|

|

Item 2. Unregistered Sales of Equity Securities and Use of

Proceeds

|

23

|

|

Item 3. Defaults Upon Senior Securities

|

23

|

|

Item 4. Mine Safety Disclosures

|

23

|

|

Item 5. Other Information

|

23

|

|

Item 6. Exhibits

|

23

|

|

Signatures

|

24

|

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

In this

Quarterly Report on Form 10-Q, references to “we”,

“our”, “us” or “Palatin” means

Palatin Technologies, Inc. and its subsidiary.

Statements

in this Quarterly Report on Form 10-Q, as well as oral statements

that may be made by us or by our officers, directors, or employees

acting on our behalf, that are not historical facts constitute

“forward-looking statements”, which are made pursuant

to the safe harbor provisions of Section 21E of the Securities

Exchange Act of 1934, as amended (the “Exchange Act”).

The forward-looking statements in this Quarterly Report on Form

10-Q do not constitute guarantees of future performance. Investors

are cautioned that statements that are not strictly historical

statements contained in this Quarterly Report on Form 10-Q,

including, without limitation, the following are forward looking

statements:

●

estimates of our

expenses, future revenue and capital requirements;

●

our ability to

obtain additional financing on terms acceptable to us, or at

all;

●

our ability to

advance product candidates into, and successfully complete,

clinical trials;

●

the initiation,

timing, progress and results of future preclinical studies and

clinical trials, and our research and development

programs;

●

the timing or

likelihood of regulatory filings and approvals;

●

our expectations

regarding completion of required clinical trials and studies and

validation of methods and controls used to manufacture

bremelanotide for the treatment of premenopausal women with

hypoactive sexual desire disorder (“HSDD”), which is a

type of female sexual dysfunction (“FSD”);

●

our expectation

regarding the timing of our regulatory submissions for approval of

bremelanotide for HSDD in the United States and in certain other

jurisdictions outside the United States;

●

our expectation

regarding performance of our exclusive licensees of bremelanotide,

including;

o

AMAG

Pharmaceuticals, Inc. (“AMAG”) for North

America,

o

Shanghai Fosun

Pharmaceutical Industrial Development Co. Ltd.

(“Fosun”), a subsidiary of Shanghai Fosun

Pharmaceutical (Group) Co., Ltd. for the territories of mainland

China, Taiwan, Hong Kong S.A.R. and Macau S.A.R., and

o

Kwangdong

Pharmaceutical Co., Ltd. (“Kwangdong”) for the Republic

of Korea;

●

the potential for

commercialization of bremelanotide for HSDD in North America by

AMAG and other product candidates, if approved, by us;

●

our expectations

regarding the potential market size and market acceptance for

bremelanotide for HSDD and our other product candidates, if

approved for commercial use;

●

our ability to

compete with other products and technologies similar to our product

candidates;

●

the ability of our

third-party collaborators to timely carry out their duties under

their agreements with us;

●

the ability of our

contract manufacturers to perform their manufacturing activities

for us in compliance with applicable regulations;

●

our ability to

recognize the potential value of our licensing arrangements with

third parties;

●

the potential to

achieve revenues from the sale of our product

candidates;

●

our ability to

obtain adequate reimbursement from Medicare, Medicaid, private

insurers and other healthcare payers;

●

our ability to

maintain product liability insurance at a reasonable cost or in

sufficient amounts, if at all;

●

the retention of

key management, employees and third-party contractors;

●

the scope of

protection we are able to establish and maintain for intellectual

property rights covering our product candidates and

technology;

●

our compliance with

federal and state laws and regulations;

●

the timing and

costs associated with obtaining regulatory approval for our product

candidates;

●

the impact of

fluctuations in foreign exchange rates;

●

the impact of

legislative or regulatory healthcare reforms in the United

States;

●

our ability to

adapt to changes in global economic conditions; and

●

our ability to

remain listed on the NYSE American stock exchange.

1

Such

forward-looking statements involve risks, uncertainties and other

factors that could cause our actual results to be materially

different from historical results or from any results expressed or

implied by such forward-looking statements. Our future operating

results are subject to risks and uncertainties and are dependent

upon many factors, including, without limitation, the risks

identified in this report, in our Annual Report on Form 10-K for

the year ended June 30, 2017, and in our other Securities and

Exchange Commission (“SEC”) filings.

We

expect to incur losses in the future as a result of spending on our

planned development programs and results may fluctuate

significantly from quarter to quarter.

Palatin

Technologies® is a registered trademark of Palatin

Technologies, Inc.

2

PART I - FINANCIAL INFORMATION

Item 1. Financial

Statements

|

PALATIN TECHNOLOGIES, INC.

|

|||

|

and Subsidiary

|

|||

|

Consolidated Balance Sheets

|

|||

|

(unaudited)

|

|

|

December

31,

2017

|

June

30,

2017

|

|

ASSETS

|

|

|

|

Current

assets:

|

|

|

|

Cash and cash

equivalents

|

$34,958,048

|

$40,200,324

|

|

Available-for-sale

investments

|

-

|

249,837

|

|

Accounts

receivable

|

-

|

15,116,822

|

|

Prepaid expenses

and other current assets

|

1,288,504

|

1,011,221

|

|

Total current

assets

|

36,246,552

|

56,578,204

|

|

|

|

|

|

Property and

equipment, net

|

178,767

|

198,153

|

|

Other

assets

|

556,916

|

56,916

|

|

Total

assets

|

$36,982,235

|

$56,833,273

|

|

|

|

|

|

LIABILITIES

AND STOCKHOLDERS’ EQUITY (DEFICIENCY)

|

|

|

|

Current

liabilities:

|

|

|

|

Accounts

payable

|

$703,767

|

$1,551,367

|

|

Accrued

expenses

|

5,527,776

|

10,521,098

|

|

Notes payable, net

of discount and debt issuance costs

|

7,889,152

|

7,824,935

|

|

Capital lease

obligations

|

-

|

14,324

|

|

Deferred

revenue

|

9,548,228

|

35,050,572

|

|

Total current

liabilities

|

23,668,923

|

54,962,296

|

|

|

|

|

|

Notes payable, net

of discount and debt issuance costs

|

2,321,124

|

6,281,660

|

|

Deferred

revenue

|

500,000

|

-

|

|

Other non-current

liabilities

|

866,135

|

753,961

|

|

Total

liabilities

|

27,356,182

|

61,997,917

|

|

|

|

|

|

Stockholders’

equity (deficiency):

|

|

|

|

Preferred stock of

$0.01 par value – authorized 10,000,000 shares:

|

|

|

|

Series A

Convertible: issued and outstanding 4,030 shares as of December 31,

2017 and June 30, 2017

|

40

|

40

|

|

Common stock of

$0.01 par value – authorized 300,000,000 shares:

|

|

|

|

issued and

outstanding 195,373,239 shares as of December 31, 2017 and

160,515,361 shares as of June 30, 2017, respectively

|

1,953,732

|

1,605,153

|

|

Additional paid-in

capital

|

350,787,078

|

349,974,538

|

|

Accumulated other

comprehensive loss

|

-

|

(590)

|

|

Accumulated

deficit

|

(343,114,797)

|

(356,743,785)

|

|

Total

stockholders’ equity (deficiency)

|

9,626,053

|

(5,164,644)

|

|

Total liabilities

and stockholders’ equity (deficiency)

|

$36,982,235

|

$56,833,273

|

The

accompanying notes are an integral part of these consolidated

financial statements.

3

|

PALATIN TECHNOLOGIES, INC.

|

||||

|

and Subsidiary

|

||||

|

Consolidated Statements of Operations

|

||||

|

(unaudited)

|

||||

|

|

|

|

|

|

|

|

Three Months Ended

December 31,

|

Six Months Ended

December 31,

|

||

|

|

2017

|

2016

|

2017

|

2016

|

|

|

|

|

|

|

|

REVENUES:

|

|

|

|

|

|

License

and contract revenue

|

$10,612,153

|

$-

|

$37,553,661

|

$-

|

|

|

|

|

|

|

|

OPERATING

EXPENSES:

|

|

|

|

|

|

Research

and development

|

6,045,884

|

8,134,575

|

20,208,981

|

19,360,659

|

|

General

and administrative

|

1,625,189

|

1,306,300

|

3,169,764

|

2,515,646

|

|

Total

operating expenses

|

7,671,073

|

9,440,875

|

23,378,745

|

21,876,305

|

|

|

|

|

|

|

|

Income

(Loss) from operations

|

2,941,080

|

(9,440,875)

|

14,174,916

|

(21,876,305)

|

|

|

|

|

|

|

|

OTHER

INCOME (EXPENSE):

|

|

|

|

|

|

Interest

income

|

81,356

|

5,991

|

133,082

|

12,636

|

|

Interest

expense

|

(391,363)

|

(594,535)

|

(848,040)

|

(1,218,520)

|

|

Total

other expense, net

|

(310,007)

|

(588,544)

|

(714,958)

|

(1,205,884)

|

|

|

|

|

|

|

|

Income

(Loss) before income taxes

|

2,631,073

|

(10,029,419)

|

13,459,958

|

(23,082,189)

|

|

Income

tax benefit, net

|

399,120

|

-

|

173,865

|

-

|

|

|

|

|

|

|

|

NET

INCOME (LOSS)

|

$3,030,193

|

$(10,029,419)

|

$13,633,823

|

$(23,082,189)

|

|

|

|

|

|

|

|

Basic

net income (loss) per common share

|

$0.02

|

$(0.06)

|

$0.07

|

$(0.13)

|

|

|

|

|

|

|

|

Diluted

net income (loss) per common share

|

$0.01

|

$(0.06)

|

$0.07

|

$(0.13)

|

|

|

|

|

|

|

|

Weighted

average number of common shares outstanding used in computing basic

net income (loss) per common share

|

197,238,056

|

177,798,511

|

197,175,316

|

171,823,390

|

|

|

|

|

|

|

|

Weighted

average number of common shares outstanding used in computing

diluted net income (loss) per common share

|

202,711,616

|

177,798,511

|

200,430,824

|

171,823,390

|

The

accompanying notes are an integral part of these consolidated

financial statements.

4

|

PALATIN

TECHNOLOGIES, INC.

|

||||

|

and

Subsidiary

|

||||

|

Consolidated

Statements of Comprehensive Income (Loss)

|

||||

|

(unaudited)

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three Months

Ended

December

31,

|

Six Months

Ended

December

31,

|

||

|

|

2017

|

2016

|

2017

|

2016

|

|

|

|

|

|

|

|

Net income

(loss)

|

$3,030,193

|

$(10,029,419)

|

$13,633,823

|

$(23,082,189)

|

|

|

|

|

|

|

|

Other comprehensive

income (loss):

|

|

|

|

|

|

Unrealized gain

(loss) on available-for-sale investments

|

153

|

515

|

590

|

(62)

|

|

|

|

|

|

|

|

Total comprehensive

income (loss)

|

$3,030,346

|

$(10,028,904)

|

$13,634,413

|

$(23,082,251)

|

The

accompanying notes are an integral part of these consolidated

financial statements.

5

|

PALATIN

TECHNOLOGIES, INC.

|

||

|

and

Subsidiary

|

||

|

Consolidated

Statements of Cash Flows

|

||

|

(unaudited)

|

||

|

|

|

|

|

|

Six Months

Ended

December

31,

|

|

|

|

2017

|

2016

|

|

CASH FLOWS FROM

OPERATING ACTIVITIES:

|

|

|

|

Net

income (loss)

|

$13,633,823

|

$(23,082,189)

|

|

Adjustments

to reconcile net income (loss) to net cash

|

|

|

|

used

in operating activities:

|

|

|

|

Depreciation and

amortization

|

28,886

|

15,261

|

|

Non-cash interest

expense

|

104,108

|

160,711

|

|

Stock-based

compensation

|

1,041,900

|

853,241

|

|

Deferred income tax

benefit

|

(500,000)

|

-

|

|

Changes in

operating assets and liabilities:

|

|

|

|

Accounts

receivable

|

15,116,822

|

-

|

|

Prepaid expenses

and other assets

|

(277,283)

|

481,877

|

|

Accounts

payable

|

(847,600)

|

3,992,124

|

|

Accrued

expenses

|

(4,968,942)

|

(320,908)

|

|

Deferred

revenue

|

(25,002,344)

|

-

|

|

Other non-current

liabilities

|

112,174

|

168,358

|

|

Net cash used in

operating activities

|

(1,558,456)

|

(17,731,525)

|

|

|

|

|

|

CASH FLOWS FROM

INVESTING ACTIVITIES:

|

|

|

|

Proceeds from

matured investments

|

250,000

|

-

|

|

Purchases of

property and equipment

|

(9,500)

|

-

|

|

Net cash provided

by investing activities

|

240,500

|

-

|

|

|

|

|

|

CASH FLOWS FROM

FINANCING ACTIVITIES:

|

|

|

|

Payments on capital

lease obligations

|

(14,324)

|

(13,534)

|

|

Payment of

withholding taxes related to restricted

|

|

|

|

stock

units

|

(24,380)

|

-

|

|

Payment on notes

payable obligations

|

(4,000,000)

|

(2,000,000)

|

|

Proceeds from the

exercise of warrants

|

114,384

|

-

|

|

Proceeds from the

sale of common stock and

|

|

|

|

warrants, net of

costs

|

-

|

23,856,972

|

|

Net cash (used in)

provided by financing activities

|

(3,924,320)

|

21,843,438

|

|

|

|

|

|

NET (DECREASE)

INCREASE IN CASH AND CASH EQUIVALENTS

|

(5,242,276)

|

4,111,913

|

|

|

|

|

|

CASH AND CASH

EQUIVALENTS, beginning of period

|

40,200,324

|

8,002,668

|

|

|

|

|

|

CASH AND CASH

EQUIVALENTS, end of period

|

$34,958,048

|

$12,114,581

|

|

|

|

|

|

SUPPLEMENTAL CASH

FLOW INFORMATION:

|

|

|

|

Cash paid for

interest

|

$632,185

|

$891,717

|

|

Unrealized gain

(loss) on available-for-sale investments

|

590

|

(62)

|

|

Non-cash equity

financing costs in accrued expenses

|

-

|

50,861

|

The

accompanying notes are an integral part of these consolidated

financial statements.

6

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

(1)

ORGANIZATION:

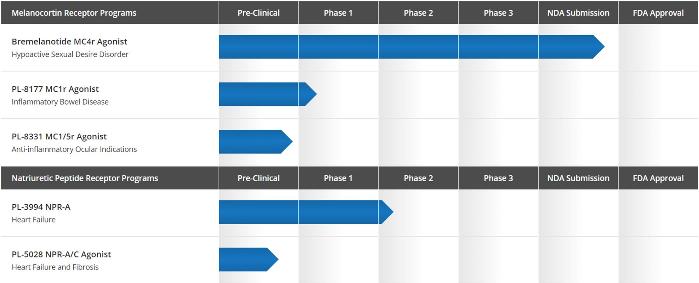

Nature of Business – Palatin Technologies, Inc.

(“Palatin” or the “Company”) is a

biopharmaceutical company developing targeted, receptor-specific

peptide therapeutics for the treatment of diseases with significant

unmet medical need and commercial potential. Palatin’s

programs are based on molecules that modulate the activity of the

melanocortin and natriuretic peptide receptor systems. The

melanocortin system is involved in a large and diverse number of

physiologic functions, and therapeutic agents modulating this

system may have the potential to treat a variety of conditions and

diseases, including sexual dysfunction and inflammation-related

diseases. The natriuretic peptide receptor system has numerous

cardiovascular functions, and therapeutic agents modulating this

system may be useful in treatment of heart failure and other

cardiovascular diseases.

The

Company’s primary product in development is bremelanotide for

the treatment of hypoactive sexual desire disorder

(“HSDD”), which is a type of female sexual dysfunction

(“FSD”). The Company also has drug candidates or

development programs for cardiovascular diseases, including heart

failure and fibrosis, and inflammatory diseases, including

inflammatory bowel disease and ocular indications.

Key

elements of the Company’s business strategy include using its

technology and expertise to develop and commercialize therapeutic

products; entering into alliances and partnerships with

pharmaceutical companies to facilitate the development,

manufacture, marketing, sale and distribution of product candidates

that the Company is developing; and partially funding its product

candidate development programs with the cash flow generated from

its relationships with third parties.

Business Risk and Liquidity – Since inception, the

Company has incurred negative cash flows from operations, and has

expended, and expects to continue to expend, substantial funds to

complete its planned product development efforts. As shown in the

accompanying consolidated financial statements, the Company had an

accumulated deficit as of December 31, 2017 of $343,614,797 and had

net income for the three and six months ended December 31, 2017 of

$2,530,193 and $13,133,823, respectively. The Company anticipates

incurring losses in the future as a result of spending on its

development programs and will require substantial additional

financing to continue to fund its planned developmental activities.

To achieve sustained profitability, if ever, the Company, alone or

with others, must successfully develop and commercialize its

technologies and proposed products, conduct successful preclinical

studies and clinical trials, obtain required regulatory approvals

and successfully manufacture and market such technologies and

proposed products. The time required to reach sustained

profitability is highly uncertain, and the Company may never be

able to achieve profitability on a sustained basis, if at

all.

On

November 21, 2017, the Company entered into a license agreement

with Kwangdong for exclusive rights to develop and commercialize

bremelanotide in the Republic of Korea. (“License Agreement

with Kwangdong”) (Note 7).

As of

December 31, 2017, the Company’s cash and cash equivalents

were $34,958,048 and current liabilities were $14,120,695, net of

deferred revenue of $9,548,228. The Company intends to utilize

existing capital resources for general corporate purposes and

working capital, including the preparation of and filing a New Drug

Application (“NDA”) on bremelanotide for HSDD with the

U.S. Food and Drug Administration (“FDA”), and

preclinical and clinical development of the Company’s other

product candidates and programs, including natriuretic peptide

receptor and melanocortin receptor programs.

Management

believes that its existing capital resources will be sufficient to

fund its planned operations through at least one year after the

date that these financial statements are issued. The Company will

need additional funding to complete required clinical trials for

its other product candidates and, assuming those clinical trials

are successful, as to which there can be no assurance, to complete

submission of required applications to the FDA. If the Company is

unable to obtain approval or otherwise advance in the FDA approval

process, the Company’s ability to sustain its operations

would be materially adversely affected.

The

Company may seek the additional capital necessary to fund its

operations through public or private equity offerings,

collaboration agreements, debt financings or licensing

arrangements. Additional capital that is required by the Company

may not be available on reasonable terms, or at all.

Concentrations – Concentrations in the Company’s

assets and operations subject it to certain related risks.

Financial instruments that subject the Company to concentrations of

credit risk primarily consist of cash and cash equivalents,

accounts receivable and investments. The Company’s cash and

cash equivalents are primarily invested in one money market account

sponsored by a large financial institution. For the three and six

months ended December 31, 2017, the Company reported $10,612,153

and $32,553,661, respectively, in license and contract revenue

related to a license agreement with AMAG for bremelanotide for

North America (“License Agreement with AMAG”) (Note 5).

In addition, for the six months ended December 31, 2017, the

Company reported $5,000,000 in license revenue related to a license

agreement with Fosun for bremelanotide for China and certain other

Asian territories (“License Agreement with Fosun”)

(Note 6). The Company did not generate any revenue for the three

and six months ended December 31, 2016.

7

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

(2)

BASIS

OF PRESENTATION:

The

accompanying unaudited consolidated financial statements have been

prepared in accordance with accounting principles generally

accepted in the United States of America (“U.S. GAAP”)

for interim financial information and with the instructions to Form

10-Q. Accordingly, they do not include all of the information and

footnote disclosures required to be presented for complete

financial statements. In the opinion of management, these

consolidated financial statements contain all adjustments

(consisting of normal recurring adjustments) considered necessary

for fair presentation. The results of operations for the three and

six months ended December 31, 2017 may not necessarily be

indicative of the results of operations expected for the full

year.

The

accompanying consolidated financial statements should be read in

conjunction with the audited consolidated financial statements and

notes thereto included in the Company’s Annual Report on Form

10-K for the year ended June 30, 2017, filed with the SEC, which

includes consolidated financial statements as of June 30, 2017 and

2016 and for each of the fiscal years in the three-year period

ended June 30, 2017.

(3)

SUMMARY

OF SIGNIFICANT ACCOUNTING POLICIES:

Principles of Consolidation – The consolidated

financial statements include the accounts of Palatin and its

wholly-owned inactive subsidiary. All intercompany accounts and

transactions have been eliminated in consolidation.

Use of Estimates – The preparation of consolidated

financial statements in conformity with U.S. GAAP requires

management to make estimates and assumptions that affect the

reported amount of assets and liabilities and disclosure of

contingent assets and liabilities at the date of the consolidated

financial statements and the reported amounts of revenues and

expenses during the reporting period. Actual results could differ

from those estimates.

Cash and Cash Equivalents – Cash and cash equivalents

include cash on hand, cash in banks and all highly liquid

investments with a purchased maturity of less than three months.

Cash equivalents consist of $34,769,696 and $40,019,336 in a money

market account as of December 31, 2017 and June 30, 2017,

respectively.

Investments – The Company determines the appropriate

classification of its investments in debt and equity securities at

the time of purchase and reevaluates such determinations at each

balance sheet date. Debt securities are classified as

held-to-maturity when the Company has the intent and ability to

hold the securities to maturity. Debt securities for which the

Company does not have the intent or ability to hold to maturity are

classified as available-for-sale. Held-to-maturity securities are

recorded as either short-term or long-term on the balance sheet,

based on the contractual maturity date and are stated at amortized

cost. Marketable securities that are bought and held principally

for the purpose of selling them in the near term are classified as

trading securities and are reported at fair value, with unrealized

gains and losses recognized in earnings. Debt and marketable equity

securities not classified as held-to-maturity or as trading are

classified as available-for-sale and are carried at fair market

value, with the unrealized gains and losses, net of tax, included

in the determination of other comprehensive income

(loss).

The

fair value of substantially all securities is determined by quoted

market prices. The estimated fair value of securities for which

there are no quoted market prices is based on similar types of

securities that are traded in the market.

Fair Value of Financial Instruments – The

Company’s financial instruments consist primarily of cash

equivalents, accounts receivable, accounts payable and notes

payable. Management believes that the carrying values of cash

equivalents, accounts receivable, available-for-sale investments

and accounts payable are representative of their respective fair

values based on the short-term nature of these instruments.

Management believes that the carrying amount of its notes payable

approximates fair value based on the terms of the

notes.

Credit Risk – Financial instruments which potentially

subject the Company to concentrations of credit risk consist

principally of cash and cash equivalents. Total cash and cash

equivalent balances have exceeded balances insured by the Federal

Depository Insurance Company.

Property and Equipment – Property and equipment

consists of office and laboratory equipment, office furniture and

leasehold improvements and includes assets acquired under capital

leases. Property and equipment are recorded at cost. Depreciation

is recognized using the straight-line method over the estimated

useful lives of the related assets, generally five years for

laboratory and computer equipment, seven years for office furniture

and equipment and the lesser of the term of the lease or the useful

life for leasehold improvements. Amortization of assets acquired

under capital leases is included in depreciation expense.

Maintenance and repairs are expensed as incurred while expenditures

that extend the useful life of an asset are capitalized.

Accumulated depreciation and amortization was $2,310,875 and

$2,281,989 as of December 31, 2017 and June 30, 2017,

respectively.

8

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

Impairment of Long-Lived Assets – The Company reviews

its long-lived assets for impairment whenever events or changes in

circumstances indicate that the carrying amount of the assets may

not be fully recoverable. To determine recoverability of a

long-lived asset, management evaluates whether the estimated future

undiscounted net cash flows from the asset are less than its

carrying amount. If impairment is indicated, the long-lived asset

would be written down to fair value. Fair value is determined by an

evaluation of available price information at which assets could be

bought or sold, including quoted market prices, if available, or

the present value of the estimated future cash flows based on

reasonable and supportable assumptions.

Revenue Recognition – The Company has generated

revenue solely through license and collaboration agreements. The

Company recognizes revenue in accordance with Financial Accounting

Standards Board (“FASB”) Accounting Standards

Codification (“ASC”) Topic 605-25, Revenue Recognition for Arrangements with

Multiple Elements, which addresses the determination of

whether an arrangement involving multiple deliverables contains

more than one unit of accounting. A delivered item within an

arrangement is considered a separate unit of accounting only if

both of the following criteria are met:

●

the delivered item

has value to the customer on a stand-alone basis; and

●

if the arrangement

includes a general right of return relative to the delivered item,

delivery or performance of the undelivered item is considered

probable and substantially in control of the vendor.

Under

FASB ASC Topic 605-25, if both of the criteria above are not met,

then separate accounting for the individual deliverables is not

appropriate.

The

Company has determined that it is appropriate to recognize the

consideration received under its License Agreement with AMAG as

revenue using the input-based proportional method during the period

of the Palatin Development Obligation as defined in the License

Agreement with AMAG. Refer to Note 5 for additional information on

this topic.

Under

its License Agreement with Fosun (Note 6), the Company received

consideration in the form of an upfront license fee payment and

determined that it was appropriate to recognize such consideration

as revenue in the first quarter of 2018, which was the quarter in

which the license was granted, since the license has stand-alone

value and the upfront payment received by the Company is

non-refundable.

Under

its License Agreement with Kwangdong (Note 7), the Company received

consideration in the form of an upfront license fee payment and has

currently determined that it is appropriate to record such

consideration as non-current deferred revenue because the upfront

payment received by the Company is subject to certain refund

provisions.

Revenue

resulting from the achievement of development milestones is

recorded in accordance with the accounting guidance for the

milestone method of revenue recognition.

Amounts

received prior to satisfying the revenue recognition criteria are

recorded as deferred revenue on the Company’s consolidated

balance sheet. Amounts expected to be recognized as revenue in the

next 12 months following the balance sheet date are classified as

current liabilities.

Research and Development Costs – The costs of research

and development activities are charged to expense as incurred,

including the cost of equipment for which there is no alternative

future use.

Accrued Expenses – Third parties perform a significant

portion of the Company’s development activities. The Company

reviews the activities performed under all contracts each quarter

and accrue expenses and the amount of any reimbursement to be

received from collaborators based upon the estimated amount of work

completed. Estimating the value or stage of completion of certain

services requires judgment based on available information. If the

Company does not identify services performed but not billed by the

service-provider, or if the Company underestimates or overestimates

the value of services performed as of a given date, reported

expenses will be understated or overstated.

Stock-Based Compensation – The Company charges to

expense the fair value of stock options and other equity awards

granted. The Company determines the value of stock options

utilizing the Black-Scholes option pricing model. Compensation

costs for share-based awards with pro-rata vesting are determined

using the quoted market price of the Company’s common stock

on the date of grant and allocated to periods on a straight-line

basis, while awards containing a market condition and performance

conditions are valued using multifactor Monte Carlo

simulations.

9

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

Income Taxes – The Company and its subsidiary file

consolidated federal and separate-company state income tax returns.

Income taxes are accounted for under the asset and liability

method. Deferred tax assets and liabilities are recognized for the

future tax consequences attributable to differences between the

financial statement carrying amounts of assets and liabilities and

their respective tax basis and operating loss and tax credit

carryforwards. Deferred tax assets and liabilities are measured

using enacted tax rates expected to apply to taxable income in the

years in which those temporary differences or operating loss and

tax credit carryforwards are expected to be recovered or settled.

The effect on deferred tax assets and liabilities of a change in

tax rates is recognized in the period that includes the enactment

date. The Company has recorded a valuation allowance against its

deferred tax assets based on the history of losses

incurred.

Pursuant

to the License Agreement with Fosun (Note 6) and the License

Agreement with Kwangdong (Note 7), $500,000 and $82,500,

respectively, was withheld in accordance with tax withholding

requirements in China and the Republic of Korea, respectively, and

will be recorded as an expense during the fiscal year ending June

30, 2018. For the three and six months ended December 31, 2017, the

Company incurred $100,880 and $326,135, respectively, in income tax

expense and the remaining balance of $256,365 was included in

prepaid expenses and other current assets at December 31, 2017. Any

potential credit to be received by the Company on its United States

tax returns is currently offset by the Company’s valuation

allowance.

On

December 22, 2017, the U.S. government enacted wide-ranging tax

legislation, the Tax Cuts and Jobs Act (the "2017 Tax Act"). The

2017 Tax Act significantly revises U.S. tax law by, among other

provisions, (a) lowering the applicable U.S. federal statutory

corporate income tax rate from 35% to 21%, (b) eliminating or

reducing certain income tax deductions, such as deductions for

interest expense, executive compensation expenses and certain

employee expenses, and (c) repealing the federal alternative

minimum tax ("AMT") and providing for the refund of existing AMT

credits.

As a

result of the 2017 tax Act, during the quarter ended December 31,

2017, the Company recorded a tax benefit of $500,000 related to the

release of a valuation allowance against an AMT credit; accordingly

$500,000 is included in Other long-term assets at December 31,

2017. In addition, as a

result of the enactment of the new corporate income tax rate, the

Company remeasured certain deferred tax assets and liabilities

based on the rates at which they are expected to reverse and with

the exception of the AMT credit, the Company continues to maintain

a full valuation allowance against its net deferred tax

assets.

Net Income (Loss) per Common Share – Basic and diluted

earnings per common share (“EPS”) are calculated in

accordance with the provisions of FASB ASC Topic 260,

“Earnings per

Share,” which includes guidance pertaining to the

warrants issued in connection with the July 3, 2012, December 23,

2014, and July 2, 2015 private placement offerings and the August

4, 2016 underwritten offering, that were exercisable for nominal

consideration and, therefore, to the extent not yet exercised are

considered in the computation of basic and diluted net loss per

common share. As of December 31, 2017, all warrants exercisable for

nominal value have been converted into common stock.

The

following table is a reconciliation of net income (loss) and the

shares used in calculating basic and diluted net income (loss) per

common share for the three and six months ended December 30, 2017

and 2016:

10

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

|

|

Three Months Ended December 31,

|

Six Months Ended December 31,

|

||

|

|

2017

|

2016

|

2017

|

2016

|

|

|

|

|

|

|

|

Net

income (loss)

|

$3,030,193

|

$(10,029,419)

|

$13,633,823

|

$(23,082,189)

|

|

|

|

|

|

|

|

Denominator:

|

|

|

|

|

|

Weighted

average common shares outstanding - Basic

|

197,238,056

|

177,798,511

|

197,175,316

|

171,823,390

|

|

|

|

|

|

|

|

Effect

of dilutive shares:

|

|

|

|

|

|

Common

stock equivalents arising from stock options,

|

|

|

|

|

|

warrants

and conversion of preferred stock

|

3,525,013

|

-

|

1,792,803

|

-

|

|

Restricted

stock units

|

1,948,547

|

-

|

1,462,705

|

-

|

|

Weighted

average common shares outstanding - Diluted

|

202,711,616

|

177,798,511

|

200,430,824

|

171,823,390

|

|

|

|

|

|

|

|

Net

income (loss) per common share:

|

|

|

|

|

|

Basic

|

$0.02

|

$(0.06)

|

$0.07

|

$(0.13)

|

|

Diluted

|

$0.01

|

$(0.06)

|

$0.07

|

$(0.13)

|

For the

three and six months ended December 31, 2017 and 2016, common

shares issuable upon conversion of Series A Convertible Preferred

Stock, the exercise of outstanding options and warrants (excluding

the Series A 2012, Series B 2012, Series C 2014, Series E 2015 and

Series I 2016 warrants issued in connection with the July 3, 2012,

December 23, 2014, and July 2, 2015 private placement offerings and

the August 4, 2016 underwritten offering as such warrants, to the

extent not yet exercised, are already included in the weighted

average number of common shares outstanding used in computing basic

net income (loss) per common share since they are exercisable for

nominal consideration), and the vesting of restricted stock units

amounted to an aggregate of 46,966,803 and 57,174,473 shares,

respectively, and are excluded from the weighted average number of

common shares outstanding used in computing basic net income (loss)

per common share. For the three and six months ended December 31,

2017, an additional 5,473,560 and 3,255,508 of common shares,

respectively, have been included in the computation of diluted EPS

using the treasury stock and if-converted methods. However, for the

three and six months ended December 31, 2016, no additional common

shares were added in the computation of diluted EPS because to do

so would have been anti-dilutive.

(4)

NEW

AND RECENTLY ADOPTED ACCOUNTING PRONOUNCEMENTS:

In May

2017, the FASB issued ASU No. 2017-09, Compensation-Stock Compensation (Topic 718):

Scope of Modification Accounting, which clarifies when to

account for a change to the terms or conditions of a share-based

payment award as a modification. Under the new guidance,

modification accounting is required only if the fair value, the

vesting conditions, or the classification of the award (as equity

or liability) changes as a result of the change in terms or

conditions. It is effective prospectively for the annual period

ending June 30, 2019 and interim periods within that annual period.

Early adoption is permitted. The Company is currently evaluating

the effect that ASU No. 2017-09 will have on its consolidated

financial statements and related disclosures.

In June

2016, the FASB issued ASU No. 2016-13, Financial Instruments Credit Losses:

Measurement of Credit Losses on Financial Instruments, which

requires measurement and recognition of expected credit losses for

financial assets held at the reporting date based on historical

experience, current conditions, and reasonable and supportable

forecasts. This is different from the current guidance as this will

require immediate recognition of estimated credit losses expected

to occur over the remaining life of many financial assets. The new

guidance will be effective for the Company on July 1, 2020. Early

adoption will be available on July 1, 2019. The Company is

currently evaluating the effect that ASU No. 2016-13 will have on

its consolidated financial statements and related

disclosures.

In

March 2016, the FASB issued ASU No. 2016-09, Compensation – Improvements to Employee

Share-Based Payment Accounting, which amends the current

guidance related to stock compensation. The updated guidance

changes how companies account for certain aspects of share-based

payment awards to employees, including the accounting for income

taxes, forfeitures, and statutory tax withholding requirements, as

well as classification in the statement of cash flows. Under this guidance, on a prospective basis,

companies will no longer be able to record excess tax benefits and

certain tax deficiencies as additional paid-in capital. Instead,

companies will record all excess tax benefits and tax deficiencies

as income tax expense or benefit in the income statement. In

addition, the guidance eliminates the requirement that excess tax

benefits be realized before companies can recognize them. The ASU

requires a cumulative-effect adjustment for previously unrecognized

excess tax benefits in opening retained earnings in the period of

adoption. Effective July 1, 2017, the Company adopted this updated

guidance and elected to recognize forfeitures when they occur using

a modified retrospective approach. The adoption of ASU No. 2016-09

did not have a material impact on the Company’s consolidated

financial statements.

11

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

In

February 2016, the FASB issued ASU No. 2016-02, Leases, related to the recognition of

lease assets and lease liabilities. The new guidance requires

lessees to recognize almost all leases on their balance sheet as a

right-of-use asset and a lease liability, other than leases that

meet the definition of a short term lease, and requires

expanded disclosures about leasing arrangements. The recognition,

measurement, and presentation of expenses and cash flows arising

from a lease have not significantly changed from the current

guidance. Lessor accounting is similar to the current guidance, but

updated to align with certain changes to the lessee model and the

new revenue recognition standard. The new guidance is effective for

the Company on July 1, 2019, with early adoption permitted. The

Company is evaluating the impact that ASU No. 2016-02 will have on

its consolidated financial statements and related

disclosures.

In

January 2016, the FASB issued ASU No. 2016-01, Financial Instruments: Recognition and

Measurement of Financial Assets and Financial Liabilities.

The new guidance relates to the recognition and measurement of

financial assets and liabilities. The new guidance makes targeted

improvements to U.S. GAAP impacting equity investments (other than

those accounted for under the equity method or consolidated),

financial liabilities accounted for under the fair value election,

and presentation and disclosure requirements for financial

instruments, among other changes. The new guidance is effective for

the Company on July 1, 2018, with early adoption prohibited other

than for certain provisions. The Company is evaluating the impact

that ASU No. 2016-01 will have on its consolidated financial

statements and related disclosures.

In November 2015, the FASB issued ASU No. 2015-17,

Income Taxes:

Balance Sheet Classification of Deferred Taxes, which simplifies the balance sheet classification

of deferred taxes. The new guidance requires that deferred tax

liabilities and assets be classified as noncurrent in a classified

statement of financial position. The current requirement that

deferred tax liabilities and assets of a tax-paying component of an

entity be offset and presented as a single amount is not affected

by the new guidance. Effective July 1, 2017, the Company adopted

this updated guidance, which did not have a material impact on the

Company’s financial position or results of operations because

its net deferred tax assets were fully offset by a valuation

allowance based on the history of losses

incurred.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with

Customers, which requires an

entity to recognize the amount of revenue to which it expects to be

entitled for the transfer of promised goods or services to

customers. The ASU will replace most existing revenue recognition

guidance in U.S. GAAP when it becomes effective. In July 2015, the

FASB voted to defer the effective date of the new standard until

fiscal years beginning after December 15, 2017 with early

application permitted for fiscal years beginning after December 15,

2016. With the deferral, the new standard is effective for the

Company on July 1, 2018. In addition, in April 2016 the FASB

issued ASU No. 2016-10, Identifying Performance Obligations and

Licensing, which addresses various issues associated with

identifying performance obligations, licensing of intellectual

property, royalty considerations, and other matters. ASU No.

2016-10 is effective in connection with ASU No. 2014-09.

The two permitted transition methods

under ASU 2014-09 are the full retrospective method, in which case

the new standard would be applied to each prior period presented

and the cumulative effect of applying the standard would be

recognized as of the earliest period reported, or the modified

retrospective method, in which case the cumulative effect of

applying the new standard would be recognized as of the date of

initial application. The Company is currently evaluating the impact

that the implementation of this standard will have on the

Company’s consolidated financial statements, including

performing an assessment of the impact of the new standard on its

collaboration arrangements with third parties.

(5)

AGREEMENT

WITH AMAG:

On

January 8, 2017, the Company entered into the License Agreement

with AMAG. Under the terms of the License Agreement with AMAG, the

Company granted to AMAG (i) an exclusive license in all countries

of North America (the “Territory”), with the right to

grant sub-licenses, to research, develop and commercialize products

containing bremelanotide (each a “Product,” and

collectively, “Products”), (ii) a non-exclusive license

in the Territory, with the right to grant sub-licenses, to

manufacture Products, and (iii) a non-exclusive license in all

countries outside the Territory, with the right to grant

sub-licenses, to research, develop and manufacture (but not

commercialize) the Products.

Following

the satisfaction of certain conditions to closing, the License

Agreement with AMAG became effective on February 2, 2017. On that

date, AMAG paid the Company $60,000,000 as a one-time initial

payment. Pursuant to the terms of and subject to the conditions in

the License Agreement with AMAG, AMAG is required to reimburse the

Company up to an aggregate amount of $25,000,000 for reasonable,

documented, direct out-of-pocket expenses incurred by the Company

following February 2, 2017, in connection with the development and

regulatory activities necessary to file an NDA for bremelanotide

for HSDD in the United States related to Palatin’s

development obligations.

12

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

The

Company has determined there is no stand-alone value for the

license, and that the license and the reimbursable direct

out-of-pocket expenses, pursuant to the terms of the License

Agreement with AMAG, represent a combined unit of accounting which

totals $85,000,000. The Company is recognizing revenue of the

combined unit of accounting over the arrangement using the

input-based proportional method as the Company completes its

development obligations. For the three and six months ended

December 31, 2017, the Company recognized $10,612,153 and

$32,553,661, respectively, as license and contract revenue related

to this transaction. As of December 31, 2017 and June 30, 2017,

there was $9,548,228 and $35,050,572, respectively, of current

deferred revenue on the consolidated balance sheet related to this

transaction.

In

addition, pursuant to the terms of and subject to the conditions in

the License Agreement with AMAG, the Company is eligible to receive

from AMAG: (i) up to $80,000,000 in specified regulatory

payments upon achievement of certain regulatory milestones, and

(ii) up to $300,000,000 in sales milestone payments based on

achievement of annual net sales amounts for all Products in the

Territory.

AMAG is

also obligated to pay the Company tiered royalties on annual net

sales of Products, on a product-by-product basis, in the Territory

ranging from the high single-digits to the low double-digits. The

royalties will expire on a product-by-product and

country-by-country basis until the latest to occur of (i) the

earliest date on which there are no valid claims of the

Company’s patent rights covering such Product in such

country, (ii) the expiration of the regulatory exclusivity period

for such Product in such country and (iii) ten years following the

first commercial sale of such Product in such country. Such

royalties are subject to reductions in the event that:

(a) AMAG must license additional third party intellectual

property in order to develop, manufacture or commercialize a

Product, or (b) generic competition occurs with respect to a

Product in a given country, subject to an aggregate cap on such

deductions of royalties otherwise payable to the Company. After the

expiration of the applicable royalties for any Product in a given

country, the license for such Product in such country will become a

fully paid-up, royalty-free, perpetual and irrevocable

license.

The

Company engaged Greenhill & Co. LLC (“Greenhill”)

as the Company’s sole financial advisor in connection with a

potential transaction with respect to bremelanotide. Under the

engagement agreement with Greenhill, the Company was obligated to

pay Greenhill a fee equal to 2% of all proceeds and consideration

paid to the Company by AMAG in connection with the License

Agreement with AMAG, subject to a minimum fee of $2,500,000. The

minimum fee of $2,500,000, less credit of $50,000 for an advisory

fee previously paid by the Company, was paid to Greenhill upon the

closing of the licensing transaction. This amount will be credited

toward amounts that become due to Greenhill in the future, provided

that the aggregate fee payable to Greenhill will not be less than

2% of all proceeds and consideration paid to the Company by AMAG in

connection with the License Agreement with AMAG. The Company will

pay Greenhill an aggregate total of 2% of all proceeds and

consideration paid to the Company by AMAG in connection with the

License Agreement with AMAG, including future milestone and royalty

payments, after crediting the $2,500,000 that was paid to Greenhill

upon entering into the License Agreement with AMAG. The Company

also reimbursed Greenhill $7,263 for certain expenses incurred in

connection with its advisory services.

Pursuant

to the License Agreement with AMAG, the Company has assigned to

AMAG the Company’s manufacturing and supply agreements with

Catalent Belgium S.A. to perform fill, finish and packaging of

bremelanotide.

(6)

AGREEMENT

WITH FOSUN:

On

September 6, 2017, the Company entered into the License Agreement

with Fosun for exclusive rights to commercialize bremelanotide in

the territories of mainland China, Taiwan, Hong Kong S.A.R. and

Macau S.A.R.

Under the terms of the agreement, the Company received

$4,500,000 in October 2017, which consisted of an upfront payment

of $5,000,000 less $500,000 which was withheld in accordance with

tax withholding requirements in China and will be recorded as an

expense during the fiscal year ending June 30, 2018. For the three

and six months ended December 31, 2017, the Company incurred

$54,712 and $279,967, respectively, in income tax expense utilizing

an estimated effective annual income tax rate applied to income for

the three and six months ended December 31, 2017 and the remaining

balance of $220,033 was included in prepaid expenses and other

current assets at December 31, 2017. The Company will receive a

$7,500,000 milestone payment when regulatory approval in China is

obtained, provided that a commercial supply agreement for

bremelanotide has been entered into. Palatin has the potential to

receive up to $92,500,000 in additional sales related milestone

payments and high single-digit to low double-digit royalties on net

sales in the licensed territory. All development, regulatory,

sales, marketing, and commercial activities and associated costs in

the licensed territory will be the sole responsibility of

Fosun.

(7)

AGREEMENT

WITH KWANGDONG:

On

November 21, 2017, the Company entered into the License Agreement

with Kwangdong for exclusive rights to commercialize bremelanotide

in the Republic of Korea.

13

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

Under

the terms of the agreement, the Company received $417,500 in

December 2017, consisting of an upfront payment of $500,000, less

$82,500, which was withheld in accordance with tax withholding

requirements in Korea and will be recorded as an expense during the

fiscal year ending June 30, 2018. Based upon certain refund

provisions, the upfront payment has been recorded as non-current

deferred revenue at December 31, 2017. For the three and six months

ended December 31, 2017, the Company incurred $46,168 in income tax

expense utilizing an estimated effective annual income tax rate

applied to income for the three and six months ended December 31,

2017 and the remaining balance of $36,332 was included in prepaid

expenses and other current assets at December 31, 2017. The Company

will receive a $3,000,000 milestone payment based on the first

commercial sale in Korea. Palatin has the potential to receive up

to $37,500,000 in additional sales related milestone payments and

mid-single-digit to low double-digit royalties on net sales in the

licensed territory. All development, regulatory, sales, marketing,

and commercial activities and associated costs in the licensed

territory will be the sole responsibility of

Kwangdong.

(8)

PREPAID EXPENSES AND OTHER CURRENT

ASSETS:

Prepaid

expenses and other current assets consist of the

following:

|

|

December

31,

2017

|

June

30,

2017

|

|

Clinical

costs

|

$753,614

|

$657,069

|

|

Insurance

premiums

|

53,886

|

182,966

|

|

Foreign withholding

tax (Notes 6 & 7)

|

256,365

|

-

|

|

Other

|

224,639

|

171,186

|

|

|

$1,288,504

|

$1,011,221

|

(9)

INVESTMENTS:

The

following summarizes the carrying value of the Company’s

available-for-sale investments, which consist of corporate debt

securities:

|

|

December

31,

2017

|

June

30,

2017

|

|

Cost

|

$-

|

$262,023

|

|

Amortization of

premium

|

-

|

(11,596)

|

|

Gross unrealized

loss

|

-

|

(590)

|

|

Fair

value

|

$-

|

$249,837

|

(10)

FAIR

VALUE MEASUREMENTS:

The

fair value of cash equivalents and investments is classified using

a hierarchy prioritized based on inputs. Level 1 inputs are quoted

prices (unadjusted) in active markets for identical assets or

liabilities. Level 2 inputs are quoted prices for similar assets

and liabilities in active markets or inputs that are observable for

the asset or liability, either directly or indirectly through

market corroboration, for substantially the full term of the

financial instrument. Level 3 inputs are unobservable inputs based

on management’s own assumptions used to measure assets and

liabilities at fair value. A financial asset or liability’s

classification within the hierarchy is determined based on the

lowest level input that is significant to the fair value

measurement.

14

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

The

following table provides the assets carried at fair value measured

on a recurring basis:

|

|

Carrying

Value

|

Quoted prices

in active markets

(Level

1)

|

Other

quoted/observable inputs

(Level

2)

|

Significant

unobservable inputs

(Level

3)

|

|

December 31,

2017:

|

|

|

|

|

|

Money market

account

|

$34,769,696

|

$34,769,696

|

$-

|

$-

|

|

TOTAL

|

$34,769,696

|

$34,769,696

|

$-

|

$-

|

|

June 30,

2017:

|

|

|

|

|

|

Money market

account

|

$40,019,336

|

$40,019,336

|

$-

|

$-

|

|

Corporate debt

securities

|

249,837

|

249,837

|

-

|

-

|

|

TOTAL

|

$40,269,173

|

$40,269,173

|

$-

|

$-

|

(11)

ACCRUED EXPENSES:

Accrued

expenses consist of the following:

|

|

December

31,

2017

|

June

30,

2017

|

|

Clinical

costs

|

$5,055,378

|

$9,138,827

|

|

Other research

related expenses

|

180,820

|

217,307

|

|

Professional

services

|

51,732

|

434,768

|

|

Other

|

239,846

|

730,196

|

|

|

$5,527,776

|

$10,521,098

|

(12)

NOTES PAYABLE:

Notes

payable consist of the following:

|

|

December

31,

2017

|

June

30,

2017

|

|

Notes payable under

venture loan

|

$10,333,334

|

$14,333,334

|

|

Unamortized related

debt discount

|

(78,564)

|

(143,524)

|

|

Unamortized debt

issuance costs

|

(44,494)

|

(83,215)

|

|

Notes

payable

|

10,210,276

|

14,106,595

|

|

|

|

|

|

Less: current

portion

|

7,889,152

|

7,824,935

|

|

|

|

|

|

Long-term

portion

|

$2,321,124

|

$6,281,660

|

On

December 23, 2014, the Company closed on a $10,000,000 venture loan

which was led by Horizon Technology Finance Corporation

(“Horizon”). The debt facility is a four year senior

secured term loan that bears interest at a floating coupon rate of

one-month LIBOR (floor of 0.50%) plus 8.50%, and provides for

interest-only payments for the first eighteen months followed by

monthly payments of principal of $333,333 plus accrued interest

through January 1, 2019. The lenders also received five-year

immediately exercisable Series D 2014 warrants to purchase 666,666

shares of common stock exercisable at an exercise price of $0.75

per share. The Company recorded a debt discount of $267,820 equal

to the fair value of these warrants at issuance, which is being

amortized to interest expense over the term of the related debt.

This debt discount is offset against the note payable balance and

included in additional paid-in capital on the Company’s

balance sheet at December 31, 2017 and June 30, 2017. In addition,

a final incremental payment of $500,000 is due on January 1, 2019,

or upon early repayment of the loan. This final incremental payment

is being accreted to interest expense over the term of the related

debt. The Company incurred $209,367 of costs in connection with the

loan. These costs were capitalized as deferred financing costs and

are offset against the note payable balance. These debt issuance

costs are being amortized to interest expense over the term of the

related debt.

15

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

On July

2, 2015, the Company closed on a $10,000,000 venture loan led

by Horizon. The debt

facility is a four-year senior secured term loan that bears

interest at a floating coupon rate of one-month LIBOR (floor of

0.50%) plus 8.50% and provides for interest-only payments for the

first eighteen months followed by monthly payments of principal of

$333,333 plus accrued interest through August 1, 2019. The lenders

also received five-year immediately exercisable Series G warrants

to purchase 549,450 shares of the Company’s common stock

exercisable at an exercise price of $0.91 per share. The Company

has recorded a debt discount of $305,196 equal to the fair value of

these warrants at issuance, which is being amortized to interest

expense over the term of the related debt. This debt discount is

offset against the note payable balance and is included in

additional paid-in capital on the Company’s balance sheet at

December 31, 2017 and June 30, 2017. In addition, a final

incremental payment of $500,000 is due on August 1, 2019, or upon

early repayment of the loan. This final incremental payment is

being accreted to interest expense over the term of the related

debt. The Company incurred $146,115 of costs in connection with the

loan agreement. These costs were capitalized as deferred financing

costs and are offset against the note payable balance. These debt

issuance costs are being amortized to interest expense over the

term of the related debt.

The

Company’s obligations under the 2015 amended and restated

loan agreement, which includes both the 2014 venture loan and the

2015 venture loan, are secured by a first priority security

interest in substantially all of its assets other than its

intellectual property. The Company also has agreed to specified

limitations on pledging or otherwise encumbering its intellectual

property assets. The 2015 amended and restated loan agreement

include customary affirmative and restrictive covenants, but does

not include any covenants to attain or maintain specified financial

metrics. The loan agreement includes customary events of default,

including payment defaults, breaches of covenants, change of

control and a material adverse change default. Upon the occurrence

of an event of default and following any applicable cure periods, a

default interest rate of an additional 5% may be applied to the

outstanding loan balances, and the lenders may declare all

outstanding obligations immediately due and payable and take such

other actions as set forth in the loan agreement. As of December

31, 2017, the Company was in compliance with all of its loan

covenants.

(13)

STOCKHOLDERS’

EQUITY (DEFICIENCY):

Financing Transactions – On December 6, 2016, the

Company closed on an underwritten public offering of units, with

each unit consisting of a share of common stock and a Series J

warrant to purchase 0.50 of a share of common stock. Gross proceeds

were $16,500,000, with net proceeds to the Company, after deducting

underwriting discounts and commissions and offering expenses, of

$15,386,075. The Company issued 25,384,616 shares of common stock

and Series J warrants to purchase 12,692,310 shares of common stock

at an initial exercise price of $0.80 per share, which warrants are

exercisable immediately upon issuance and expire on the fifth

anniversary of the date of issuance. The Series J warrants are subject to

limitation on exercise if the holder and its affiliates would

beneficially own more than 9.99%, or 4.99% for certain holders, of

the total number of the Company’s shares of common stock

outstanding following such exercise.

On