UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark one)

For the fiscal year ended

For the transition period from to

Commission File Number:

(exact name of registrant as specified in its charter)

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, Including Area Code: (

Securities registered pursuant to Section 12 (b) of the Act:

Title of each class: | Trading Symbol | Name of each exchange on which registered: |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days:

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Non-accelerated filer ☐ | Accelerated filer ☐ Smaller reporting company Emerging growth company | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.

Yes

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was $

Shares of no par value Common Stock outstanding as of February 26, 2024:

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the Registrant’s Annual Meeting of Shareholders to be held on April 24, 2024 have been incorporated by reference into Items 10, 11, 12, 13 and 14 of Part III of this report.

WINMARK CORPORATION AND SUBSIDIARIES

INDEX TO ANNUAL REPORT ON FORM 10-K

FORWARD LOOKING STATEMENTS OR INFORMATION

The statements contained in this Form 10-K Item 1 “Business”, Item 1A “Risk Factors”, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and in Item 8 “Financial Statements and Supplemental Data” that are not strictly historical fact, including without limitation, the Company’s statements relating to growth opportunities, its ability to open new franchises, its ability to manage costs in the future, the number of franchises it believes will open, performance of its lease portfolio, its future cash requirements, its future effective tax rate and its belief that it will have adequate capital and reserves to meet its current and contingent obligations and operating needs, as well as its disclosures regarding market rate risk, and other statements in which we use words or phrases such as “will,” “may,” “should,” “could,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “intends,” and similar words are all forward looking statements made under the safe harbor provision of the Private Securities Litigation Reform Act. Such statements are based on management’s current expectations as of the date of this report but involve risks, uncertainties and other factors which may cause actual results to differ materially from those contemplated by such forward looking statements. Investors are cautioned to consider these forward looking statements in light of important factors which may result in material variations between results contemplated by such forward looking statements and actual results and conditions including, but not limited to, the risk factors discussed in Section 1A of this report. You should not place undue reliance on these forward-looking statements, which speak only as of the date they were made. The Company undertakes no obligation to revise or update publicly any forward-looking statement for any reason.

Winmark qualifies as a “Smaller Reporting Company” under Item 10(f)(1) of Regulation S-K. Winmark has elected to voluntarily include certain disclosures not required by a Smaller Reporting Company.

PART I

ITEM 1: BUSINESS

Background

Winmark – the Resale Company® (Winmark Corporation, Winmark or the Company), is a nationally recognized franchisor focused on sustainability and small business formation. We champion and guide entrepreneurs interested in operating one of our award winning resale franchises: Plato’s Closet®, Once Upon A Child®, Play It Again Sports®, Style Encore® and Music Go Round®. At December 30, 2023, there were 1,319 franchises in operation in the United States and Canada and over 2,800 available territories. Our mission is to provide Resale for Everyone™.

Each of our resale brands emphasizes consumer value by offering high-quality used merchandise at substantial savings from the price of new merchandise and by purchasing customers’ used goods that have been outgrown or are no longer used. Our concepts also offer a limited amount of new merchandise to customers. For over 30 years, we have offered a sustainable solution for consumers to recycle their gently used clothing, toys, sporting goods and musical instruments. We estimate that, since 2010, stores in our resale brands have extended the lives of over 1.7 billion items. We continue to enhance our franchise model and provide our franchisees with the technology, tools and training to profitably expand their operations and evolve towards being a multi-channel retailer.

Our significant assets are located within the United States, and we generate the majority of revenues from United States operations. Revenues from Canadian franchisees in 2023, 2022 and 2021 were approximately $6.8 million, $6.4 million and $4.9 million, respectively. For additional financial information, please see Item 8 — Financial Statements and Supplementary Data. We were incorporated in Minnesota in 1988.

1

Operations

We currently franchise five brands:

Plato’s Closet

We began franchising the Plato’s Closet brand in 1999. Plato’s Closet franchisees buy and sell gently used clothing and accessories geared toward the teenage and young adult market. Customers have the opportunity to sell their used items to Plato’s Closet stores and to purchase quality used clothing and accessories at prices lower than new merchandise.

Once Upon A Child

We began franchising the Once Upon A Child brand in 1993. Once Upon A Child franchisees buy and sell gently used and, to a lesser extent, new children’s clothing, toys, furniture, equipment and accessories. This brand primarily targets parents of children ages infant to 12 years. These customers have the opportunity to sell their used children’s items to a Once Upon A Child store when outgrown and to purchase quality used children’s clothing, toys, furniture and equipment at prices lower than new merchandise.

Play It Again Sports

We began franchising the Play It Again Sports brand in 1988. Play It Again Sports franchisees buy, sell and trade gently used and new sporting goods, equipment and accessories for a variety of athletic activities including team sports (baseball/softball, hockey, football, lacrosse, soccer), fitness, ski/snowboard and golf among others. The stores offer a flexible mix of merchandise that is adjusted to adapt to seasonal and regional differences.

Style Encore

We began franchising the Style Encore brand in 2013. Style Encore franchisees buy and sell gently used women’s (and to a lesser extent, men’s) apparel, shoes and accessories. Customers have the opportunity to sell their used items to Style Encore stores and to purchase quality used clothing, shoes and accessories at prices lower than new merchandise.

Music Go Round

We began franchising the Music Go Round brand in 1994. Music Go Round franchisees buy, sell and trade gently used and, to a lesser extent, new musical instruments, speakers, amplifiers, music-related electronics and related accessories.

The following table presents system-wide sales, which we define as estimated revenues generated by all franchise locations through both in-store and e-commerce sales, for each of the past three years.

System-Wide Sales | |||||||||

(in millions) | |||||||||

| 2021 |

| 2022 |

| 2023 | ||||

Plato’s Closet | $ | 594.4 | $ | 638.8 | $ | 647.6 | |||

Once Upon A Child |

| 420.3 |

| 466.2 |

| 504.8 | |||

Play It Again Sports |

| 300.7 |

| 324.1 |

| 328.2 | |||

Style Encore |

| 49.4 |

| 58.1 |

| 59.2 | |||

Music Go Round |

| 41.8 |

| 47.1 |

| 49.2 | |||

$ | 1,406.6 | $ | 1,534.3 | $ | 1,589.0 | ||||

We have developed an e-commerce platform that allows franchisees of our Music Go Round, Play It Again Sports and Style Encore brands to market and sell in-store product inventory online. Consumers that visit musicgoround.com, playitagainsports.com or style-encore.com can find all product listed by participating stores in one convenient location. All product listings are available for in-store pickup, and certain products may be available for shipment. Our e-commerce platform assists our franchisees in marketing, increasing brand awareness, and driving consumers to local stores, which provides further opportunities for our stores to purchase product from consumers. Additionally, our franchisees use other vehicles to drive non-store sales including social media platforms (Facebook and Instagram) as well as third-party e-commerce platforms (Shopify) and marketplaces (eBay).

2

The following table presents the royalties and franchise fees contributed by each of our brands for the past three years and the corresponding percentage of consolidated revenues for each such year:

Total Royalties and Franchise Fees |

| |||||||||||||||

(in millions) | % of Consolidated Revenue |

| ||||||||||||||

| 2021 |

| 2022 |

| 2023 |

| 2021 |

| 2022 |

| 2023 |

| ||||

Plato’s Closet | $ | 26.8 | $ | 29.4 | $ | 30.2 |

| 34.3 | % | 36.2 | % | 36.3 | % | |||

Once Upon A Child |

| 18.9 |

| 21.1 |

| 23.1 |

| 24.1 | 25.9 | 27.7 | ||||||

Play It Again Sports |

| 12.6 |

| 13.6 |

| 13.8 |

| 16.1 | 16.7 | 16.6 | ||||||

Style Encore |

| 2.7 |

| 3.1 |

| 3.1 |

| 3.4 | 3.8 | 3.8 | ||||||

Music Go Round |

| 1.3 |

| 1.5 |

| 1.5 |

| 1.7 | 1.8 | 1.8 | ||||||

$ | 62.3 | $ | 68.7 | $ | 71.7 |

| 79.6 | % | 84.4 | % | 86.2 | % | ||||

The following table presents a summary of our net store growth and renewal activity for the fiscal year ended December 30, 2023:

AVAILABLE | |||||||||||||||

TOTAL | TOTAL | FOR | COMPLETED |

| |||||||||||

| 12/31/2022 |

| OPENED |

| CLOSED |

| 12/30/2023 |

| RENEWAL |

| RENEWALS |

| % RENEWED |

| |

Plato’s Closet |

| 500 |

| 11 |

| (5) |

| 506 | 65 | 65 | 100 | % | |||

Once Upon A Child |

| 406 |

| 11 |

| (1) |

| 416 | 54 | 54 | 100 | % | |||

Play It Again Sports |

| 281 |

| 17 |

| (4) | 294 | 34 | 34 | 100 | % | ||||

Style Encore |

| 71 |

| — |

| (5) |

| 66 | 18 | 17 | 94 | % | |||

Music Go Round |

| 37 |

| — |

| — |

| 37 | 6 | 6 | 100 | % | |||

Total Franchised Stores(1) |

| 1,295 |

| 39 |

| (15) |

| 1,319 |

| 177 | 176 |

| 99 | % |

| (1) | All stores are owned and operated by franchisees. Winmark does not own or operate any corporate stores. |

Of the 1,319 total franchised stores as of December 30, 2023, 149 were located in Canada.

Sustainability

As a leader in the circular economy, we have been at the forefront of the sustainability movement for over 30 years. Our franchise brands offer customers a better way to keep their clothes, sporting goods and music equipment out of landfills and in use for a fuller, longer product lifespan. In 2023 alone, stores across our five resale brands extended the lives of over 182 million items of clothing, toys, books, musical instruments and sports equipment. Our high-quality franchised stores give consumers an easier way to buy and sell used goods within their local communities without placing demands on wasteful production. In turn, this means less water and energy consumption, giving consumers a way to help cut down on pollution and greenhouse gas emissions.

Franchising Business Model

We use franchising as a business method of distributing goods and services through our retail brands to consumers. We, as franchisor, own a retail business brand, represented by a service mark or similar right, and an operating system for the franchised business. We then enter into franchise agreements with franchisees and grant the franchisee the right to use our business brand, service marks and operating system to manage a retail business. Franchisees are required to operate their retail businesses according to the systems, specifications, standards and formats we develop for the business brand. We train the franchisees how to operate the franchised business. We also provide continuing support and service to our franchisees.

We have developed value-oriented retail brands based on a mix of gently used and, to a lesser extent, new merchandise. We franchise rights to franchisees who open franchised locations under such brands. The key elements of our franchise strategy include:

| ● | franchising the rights to operate retail stores offering value-oriented merchandise; |

| ● | attracting new, qualified franchisees; and |

| ● | providing initial and continuing support to franchisees. |

3

Offering Value-Oriented Merchandise

Our retail brands provide value to consumers by purchasing and reselling gently used merchandise that consumers have outgrown or no longer use at substantial savings from the price of new merchandise. By offering a combination of high-quality used and value-priced new merchandise, we benefit from consumer demand for value-oriented retailing. In addition, we believe that among national retail operations our brands provide a unique source of value to consumers by purchasing used merchandise. We also believe that the strategy of buying used merchandise increases consumer awareness of our retail brands.

Franchisee Qualification

We seek to attract prospective franchisees with experience in management and operations and an interest in being the owner and operator of their own business. We seek franchisees who:

| ● | have a sufficient net worth; |

| ● | have prior business experience; and |

| ● | intend to be integrally involved with the management of the business. |

At December 30, 2023, we had 71 signed franchise agreements, of which the majority are expected to open in 2024.

Franchise Support

As a franchisor, our success depends upon our ability to develop and support competitive and successful franchise owners. We emphasize the following areas of franchise support and assistance.

Training

Each franchisee must attend our training program regardless of prior experience. Soon after signing a franchise agreement, the franchisee is required to attend new owner orientation training. This course covers basic management issues, such as preparing a business plan, lease evaluation, evaluating insurance needs and obtaining financing. Our training staff assists each franchisee in developing a business plan for their retail store with financial and cash flow projections. The second training session is centered on store operations. It covers, among other things, point-of-sale computer training, inventory selection and acquisition, sales, marketing and other topics. We provide the franchisee with operations manuals that we periodically update.

Operations Support

We provide operational support and guidance to assist the franchisee in the opening of a new business. We also have an ongoing support program designed to assist franchisees in operating their retail stores. Our franchise support personnel visit each store periodically (in person or virtually) and, in most cases, a business assessment is made to determine whether the franchisee is operating in accordance with our standards. The visit is also designed to assist franchisees with operational issues.

Purchasing

During training each franchisee is taught how to evaluate, purchase and price used goods directly from customers. We have developed specialized computer point-of-sale systems for our brands that provide the franchisee with standardized pricing information to assist in the purchasing of used items.

We provide centralized buying services, which on a limited basis include credit and billing for the Play It Again Sports franchisees. Our Play It Again Sports franchise system uses several major vendors for new product including Bowflex, Wilson Sporting Goods, Champro Sports, Rawlings/Easton, CCM Hockey and Bauer Hockey. The loss of any of the above vendors would change the vendor mix, but not significantly change our products offered.

To provide the franchisees of our Play It Again Sports, Once Upon A Child and Music Go Round systems a source of affordable new product, we have developed relationships with our significant vendors and negotiated prices for our franchisees to take advantage of the buying power a franchise system brings.

4

Our typical Once Upon A Child franchised store purchases approximately 30% of its new product from Rachel’s Ribbons, Wild Side Accessories, Melissa & Doug and Nuby. The loss of any of the above vendors would change the vendor mix, but not significantly change our products offered.

Our typical Music Go Round franchised store purchases approximately 50% of its new product from KMC/Musicorp, RapcoHorizon Company, D’Addario, GHS Corporation and Ernie Ball. The loss of any of the above vendors would change the vendor mix, but not significantly change our products offered.

There are no significant vendors of new products to our typical Plato’s Closet and Style Encore franchised stores as new product is an extremely low percentage of sales for these brands.

Retail Advertising and Marketing

We encourage our franchisees to implement a marketing program that includes the following: television, radio, point-of-purchase materials, in-store signage and local store marketing programs as well as email marketing promotions, website promotions and participation in social and digital media. Franchisees of the respective brands are required to spend a minimum of 5% of their gross sales on approved advertising and marketing. Franchisees may be required to participate in regional cooperative advertising groups.

Computerized Point-Of-Sale Systems

We require our franchisees to use a retail information management computer system in each store, which has evolved with the development of new technology. This computerized point-of-sale system is designed specifically for use in our franchise retail stores. The current system includes our proprietary Data Recycling System software, a dedicated server, two or more work station registers with touch screen monitors, receipt printers, label printers and bar code scanners, together with software modules for inventory management, cash management and customer information management. Our franchisees purchase the computer hardware from us. The Data Recycling System software is designed to accommodate buying of used merchandise. This system provides franchisees with an important management tool that reduces errors, increases efficiencies and enhances inventory control. We provide point-of-sale system support through our Computer Support Center located at our Company headquarters.

The Franchise Agreement

We enter into franchise agreements with our franchisees. The following is a summary of certain key provisions of our current standard brand franchise agreement. Except as noted, the franchise agreements used for each of our brands, whether for locations in the United States or Canada, are generally the same.

Each franchisee must execute our franchise agreement and pay an initial franchise fee. At December 30, 2023, the franchise fee for all brands was $25,000 for an initial store in the U.S. and $34,000CAD for an initial store in Canada. Once a franchisee opens its initial store, it can open additional stores, in any brand, by paying a $15,000 franchise fee for a store in the U.S. and $20,500CAD for a store in Canada, provided an acceptable territory is available and the franchisee meets the brand’s additional store standards. The franchise fee for our initial store and additional store in Canada is based upon the exchange rate applied to the United States franchise fee on the last business day of the preceding fiscal year. The franchise fee in March 2024 for an initial store in Canada will be $33,200CAD, and an additional store in Canada will be $20,000CAD. Typically, the franchisee’s initial store is open for business approximately 10 to 14 months from the date the franchise agreement is signed. The franchise agreement has an initial term of 10 years, with subsequent 10-year renewal periods, and grants the franchisee an exclusive geographic area, which will vary in size depending upon population, demographics and other factors. Under current franchise agreements, franchisees of the respective brands are required to pay us weekly continuing fees (royalties) equal to the percentage of gross sales outlined in their Franchise Agreements, generally ranging from 4% to 5% for all of our brands.

Each Franchisee is currently required to pay us an annual marketing fee of $1,500, and is required to spend 5% of its gross sales for advertising and promoting its franchised store. We have the option to increase the minimum advertising expenditure requirement from 5% to 6% of the franchisee’s gross sales, of which up to 2% would be paid to us as an advertising fee for deposit into an advertising fund. This fund, if initiated, would be managed by us and would be used for advertising and promotion of the franchise system.

During the term of a franchise agreement, franchisees agree not to operate directly or indirectly any competitive business. In addition, franchisees agree that after the end of the term or termination of the franchise agreement, franchisees will not operate any competitive business for a period of two years and within a reasonable geographic area.

5

Although our franchise agreements contain provisions designed to assure the quality of a franchisee’s operations, we have less control over a franchisee’s operations than we would if we owned and operated a retail store. Under the franchise agreement, we have a right of first refusal on the sale of any franchised store, but we are not obligated to repurchase any franchised store.

Renewal of the Franchise Relationship

At the end of the 10-year term of each franchise agreement, each franchisee has the option to “renew” the franchise relationship by signing a new 10-year franchise agreement. If a franchisee chooses not to sign a new franchise agreement, a franchisee must comply with all post termination obligations including the franchisee’s noncompetition clause discussed above. We may choose not to renew the franchise relationship only when permitted by the franchise agreement and applicable state law.

We believe that renewing a significant number of these franchise relationships is important to the success of the Company. During the past three years, we renewed over 99% of franchise agreements up for renewal.

Competition

Retailing, including the sale of apparel, sporting goods and musical instruments, is highly competitive. Many retailers have substantially greater financial and other resources than we do. Our franchisees compete with established, locally owned retail stores, discount chains and traditional retail stores for sales of new merchandise. Full line retailers generally carry little or no used merchandise. Resale, thrift and consignment shops and garage and rummage sales offer competition to our franchisees for the sale of used merchandise. Also, our franchisees increasingly compete with online used and new goods marketplaces such as eBay, craigslist, facebook Marketplace, Poshmark, thredUP, Amazon and many others. More recently, retail and consumer apparel brands themselves have been participating (mostly through e-commerce) in developing platforms to sell previously used items. These have been done on their own or in connection with a technology partner.

Our Plato’s Closet franchise stores primarily compete with specialty apparel stores such as American Eagle, Gap, Abercrombie & Fitch, Old Navy, Hollister and Forever 21. We compete with other franchisors in the teenage resale clothing retail market.

Our Once Upon A Child franchisees compete primarily with large retailers such as Walmart, Target and various specialty children’s retail stores such as Carter’s and Gap Kids. We compete with other franchisors in the specialty children’s resale retail market.

Our Play It Again Sports franchisees compete with large retailers such as Dick’s Sporting Goods, Academy Sports & Outdoors as well as regional and local sporting goods stores. We also compete with Target and Walmart.

Our Style Encore franchise stores compete with a wide range of women’s apparel stores. We also compete with other franchisors in the women’s resale clothing retail market.

Our Music Go Round franchise stores compete with large musical instrument retailers such as Guitar Center as well as local independent musical instrument stores.

Our franchises may face additional competition in the future. This could include additional competitors that may enter the used merchandise market. We believe that our franchisees will continue to be able to compete with other retailers based on the strength of our value-oriented brands and the name recognition associated with our service marks.

We also face competition in connection with the sale of franchises. Our prospective franchisees frequently evaluate other franchise opportunities before purchasing a franchise from us. We compete with other franchise companies for franchisees based on the following factors, among others: amount of initial investment, franchise fee, royalty rate, profitability, franchisor services and industry. We believe that our franchise brands are competitive with other franchises based on the fees we charge, our franchise support services and the performance of our existing franchise brands.

6

Equipment Leasing Operations

Our leasing operations consist of a middle-market leasing business through Winmark Capital Corporation, which is a wholly-owned subsidiary.

Our middle-market leasing business began operations in 2004. In May 2021, we made the decision to no longer solicit new leasing customers and pursue an orderly run-off of this leasing portfolio. Given this decision, we anticipate that leasing revenues, expenses, contribution and cash flows will continue to decrease throughout the run-off period. For additional information on our leasing business, please see Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Item 8 “Financial Statements and Supplementary Data.”

Government Regulation

Fourteen states, the Federal Trade Commission and six Canadian Provinces impose pre-sale franchise registration and/or disclosure requirements on franchisors. In addition, a number of states have statutes which regulate substantive aspects of the franchisor-franchisee relationship such as termination, nonrenewal, transfer, discrimination among franchisees and competition with franchisees.

Additional legislation, both at the federal and state levels, could expand pre-sale disclosure requirements, further regulate substantive aspects of the franchise relationship and require us to file our Franchise Disclosure Documents with additional states. We cannot predict the effect of future franchise legislation, but do not believe there is any imminent legislation currently under consideration which would have a material adverse impact on our operations.

We believe that we are currently in compliance with all material statutes and regulations that are applicable to our business. We do not currently incur any material costs or effects of compliance with the environmental laws (federal, state and local).

Trademarks and Service Marks

We have various trademark registrations and pending trademark applications for registration, including Plato’s Closet®, Once Upon A Child®, Play It Again Sports®, Style Encore®, Music Go Round®, Winmark®, Winmark – the Resale Company®, and Resale for Everyone®, among others. These marks are of considerable value to our business. We intend to protect our service marks by appropriate legal action where and when necessary. Each service mark registration must be renewed every 10 years. We have taken, and intend to continue to take, all steps necessary to renew the registration of all our material service marks.

Seasonality

Our Plato’s Closet and Once Upon A Child franchise brands have experienced higher than average sales volumes during the spring months and during the back-to-school season. Our Play It Again Sports franchise brand has experienced higher than average sales volumes during the winter season. Overall, the different seasonal trends of our brands partially offset each other and do not result in significant seasonality trends on a Company-wide basis.

Human Capital Resources

Human capital resources are an integral and essential component of our business. As of December 30, 2023, we employed 83 employees. None of these employees are covered by a collective bargaining agreement. Our franchisees are independent business owners, therefore, they and their employees are not included in our employee count and are not employees of Winmark Corporation.

Our employees are our most valuable resource. We recognize that employee development is a critical element of maintaining an engaged and inclusive work environment. Investing in our employees supports employee retention, morale and enhances the quality of work. We provide mentorship opportunities, leadership succession planning and encourage promoting from within to further strengthen our commitment to each employee. Our compensation programs are designed to support not only the financial, but the physical and mental well-being of our employees. In addition to our competitive salaries, our programs include, among other things, robust health and welfare benefits, a 401(k) plan with matching contribution, profit-sharing, generous paid leave policies, and an employee assistance program. We have in the past and will continue to place a strong emphasis on our employee’s welfare, health, and safety.

We recognize the benefits of and are committed to a culture of diversity and inclusion, where each individual is valued for their own unique perspective and experiences. As of December 30, 2023, 55% of our overall employee count and 53% of our management team identify as female. Additionally, we provide training to our management team and

7

employees regarding diversity and inclusion and we continue to actively work to increase representation among underrepresented demographic groups within our employee base.

Available Information

We maintain a Web site at www.winmarkcorporation.com, the contents of which are not part of or incorporated by reference into this Annual Report on Form 10-K. We make our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K (and amendments to those reports) available on our Web site via a link to the U.S. Securities and Exchange Commission (SEC) Web site, free of charge, as soon as reasonably practicable after such reports have been filed with or furnished to the SEC.

ITEM 1A: RISK FACTORS

Our business, results of operations, financial condition, cash flows and the market value of our common stock can be adversely affected by pandemics, epidemics or other public health emergencies, such as the outbreak of COVID-19.

Our business, results of operations, financial condition, cash flows and the market value of our common stock can be adversely affected by pandemics, epidemics or other public health emergencies, such as the outbreak of COVID-19.

The extent to which pandemics, epidemics or other public health emergencies may adversely impact our business depends on future developments, which are highly uncertain and unpredictable, depending upon the severity and duration of any such outbreak and the effectiveness of actions taken globally, nationally and locally to contain or mitigate its effects. Any resulting financial impact cannot be estimated reasonably at this time, but may materially adversely affect our business, results of operations, financial condition and cash flows. Even after any pandemic, epidemic or other public health emergency has subsided, we may experience materially adverse effects to our business due to any resulting economic recession or depression. Additionally, concerns over the economic affect of any pandemic, epidemic or other public health emergency may cause extreme volatility in financial and other capital markets which may adversely impact the market value of our common stock and our ability to access capital markets and debt capital. To the extent any pandemic, epidemic or other public health emergency adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this Annual Report.

We are dependent on franchise renewals.

Each of our franchise agreements is 10 years long. At the end of the term of each franchise agreement, each franchisee may, if certain conditions are met, “renew” the franchise relationship by signing a new 10-year franchise agreement. As of December 30, 2023 each of our five brands have the following number of franchise agreements that will expire over the next three years:

| 2024 |

| 2025 |

| 2026 |

| |

Plato’s Closet |

| 56 |

| 44 |

| 40 | |

Once Upon A Child |

| 51 |

| 44 |

| 50 | |

Play It Again Sports |

| 22 |

| 20 |

| 14 | |

Music Go Round |

| 2 |

| 4 |

| 6 | |

Style Encore |

| 15 |

| 8 |

| 6 | |

| 146 |

| 120 |

| 116 |

We believe that renewing a significant number of these franchise relationships is important to our continued success. If a significant number of franchise relationships are not renewed, our financial performance would be materially and adversely impacted.

We are dependent on new franchisees.

Our ability to generate increased revenue and achieve higher levels of profitability depends in part on increasing the number of franchises open. Unfavorable macro-economic conditions may affect the ability of potential franchisees to obtain external financing and/or impact their net worth, both of which could lead to a lower level of openings than we have historically experienced. There can be no assurance that we will sustain our current level of franchise openings.

We may make additional investments outside of our core businesses.

From time to time, we have and may continue to make investments both inside and outside of our current businesses. To the extent that we make additional investments that are not successful, such investments could have a material adverse impact on our financial results.

8

We may sell franchises for a territory, but the franchisee may not open.

We believe that a substantial majority of franchises awarded but not opened will open within the time period permitted by the applicable franchise agreement or we will be able to resell the territories for most of the terminated or expired franchises. However, there can be no assurance that substantially all of the currently sold but unopened franchises will open and commence paying royalties to us.

Our franchisees are dependent on supply of used merchandise.

Our retail brands are based on offering customers a mix of used and new merchandise. As a result, the ability of our franchisees to obtain continuing supplies of high quality used merchandise is important to the success of our brands. Supply of used merchandise comes from the general public and may not be regular or highly reliable. In addition, adherence to federal and state product safety and other requirements may limit the amount of used merchandise available to our franchisees. In addition to laws and regulations that apply to businesses generally, our franchised retail stores may be subject to state or local statutes or ordinances that govern secondhand dealers. There can be no assurance that our franchisees will avoid supply problems with respect to used merchandise.

We may be unable to collect accounts receivable from franchisees.

In the event that our ability to collect accounts receivable significantly declines from current rates, we may incur additional charges that would affect earnings. If we are unable to collect payments due from our franchisees, it would materially adversely impact our results of operations and financial condition.

We operate in an extremely competitive industry.

Retailing, including the sale of apparel, sporting goods and musical instruments, is highly competitive. Many retailers and online marketplaces have significantly greater financial and other resources than us and our franchisees. Individual franchisees face competition in their markets from retailers of new merchandise and, in certain instances, resale, thrift and other stores that sell used merchandise. We may face additional competition as our franchise systems expand and if additional competitors enter the used merchandise market.

We currently, and may in the future, have assets held at financial institutions that may exceed the insurance coverage offered by the Federal Deposit Insurance Corporation, the loss of such assets would have a severe negative affect on our operations and liquidity.

We may maintain our cash assets at certain financial institutions in the U.S. in amounts that may be in excess of the Federal Deposit Insurance Corporation (“FDIC”) insurance limit of $250,000. In the event of a failure of any financial institutions where we maintain our deposits or other assets, we may incur a loss to the extent such loss exceeds the FDIC insurance limitation, which could have a material adverse effect upon our liquidity, financial condition and our results of operations.

We are subject to restrictions in our line of credit/term loan and note facilities. Additionally, we are subject to counter party risk in our line of credit facility.

The terms of our line of credit/term loan and note facilities impose certain operating and financial restrictions on us and require us to meet certain financial tests including tests related to minimum levels of debt service coverage and maximum levels of leverage. As of December 30, 2023, we were in compliance with all of our financial covenants under these facilities; however, failure to comply with these covenants in the future may result in default under one or both of these sources of capital and could result in acceleration of the related indebtedness. Any such acceleration of indebtedness would have an adverse impact on our business activities and financial condition.

Sustained credit market deterioration could jeopardize the counterparty obligations of the bank participating in our line of credit facility, which could have an adverse impact on our business if we are not able to replace such credit facility or find other sources of liquidity on acceptable terms.

9

We have indebtedness.

We have existing indebtedness in the form of notes payable and term loans (see Note 7 — “Debt”). We expect to generate the cash necessary to pay our expenses and to pay the principal and interest on all of our outstanding debt from cash flows provided by operating activities and by opportunistically using other means to repay or refinance our obligations as we determine appropriate. Our ability to pay our expenses and meet our debt service obligations depends on our future performance, which may be affected by financial, business, economic, and other factors. If we do not have enough money to pay our debt service obligations, we may be required to refinance all or part of our existing debt, sell assets, borrow more money or raise equity. In such an event, we may not be able to refinance our debt, sell assets, borrow more money or raise equity on terms acceptable to us or at all. Also, our ability to carry out any of these activities on favorable terms, if at all, may be further impacted by any financial or credit crisis which may limit access to the credit markets and increase our cost of capital.

We are subject to government regulation.

As a franchisor, we are subject to various federal and state franchise laws and regulations. Fourteen states, the Federal Trade Commission and six Canadian Provinces impose pre-sale franchise registration and/or disclosure requirements on franchisors. In addition, a number of states have statutes which regulate substantive aspects of the franchisor-franchisee relationship such as termination, nonrenewal, transfer, discrimination among franchisees and competition with franchisees.

Additional legislation, both at the federal and state levels, could expand pre-sale disclosure requirements, further regulate substantive aspects of the franchise relationship and require us to file our franchise offering circulars with additional states. Future franchise legislation could impose costs or other burdens on us that could have a material adverse impact on our operations. In addition, evolving labor and employment laws, rules and regulations could result in potential claims against us as a franchisor for labor and employment related liabilities that have historically been borne by franchisees.

We may be unable to protect against data security risks.

We have implemented security systems with the intent of maintaining the physical security of our facilities and protecting our employees, franchisees, lessees, customers’, clients’ and suppliers’ confidential information and information related to identifiable individuals against unauthorized access through our information systems or by other electronic transmission or through the misdirection, theft or loss of physical media. These include, for example, the appropriate encryption of information. Despite such efforts, we are subject to potential breach of security systems which may result in unauthorized access to our facilities or the information we are trying to protect. Because the techniques used to obtain unauthorized access are constantly changing and becoming increasingly more sophisticated and often are not recognized until launched against a target, we may be unable to anticipate these techniques or implement sufficient preventative measures. If unauthorized parties gain physical access to one of our facilities or electronic access to our information systems or such information is misdirected, lost or stolen during transmission or transport, any theft or misuse of such information could result in, among other things, unfavorable publicity, governmental inquiry and oversight, difficulty in marketing our services, allegations by our customers and clients that we have not performed our contractual obligations, litigation by affected parties and possible financial obligations for damages related to the theft or misuse of such information, any of which could have a material adverse effect on our business.

Our stock price will fluctuate, and at times these fluctuations may be volatile.

The prices of markets and individual equities tend to fluctuate. These fluctuations commonly reflect events, many of which may be fully or partially outside of our control, that may change investor's perception of our future earnings growth prospects, including changes in economic conditions, ability to execute business strategy, the impacts of public policy, investor sentiment, competitive dynamics, and many other factors. While the sources of stock price fluctuation can be common across companies, the magnitude of these fluctuations can vary for different companies.

10

ITEM 1B: UNRESOLVED STAFF COMMENTS

None.

ITEM 1C: CYBERSECURITY

We deploy several processes for assessing, identifying and managing material risks from cybersecurity threats. These processes include, but are not limited to, security assessments, physical access restrictions, internal and external penetration testing, endpoint detection and response, and employee security awareness programs and training.

Our cybersecurity processes have been integrated into our overall risk management processes, and we engage assistance from third parties as we deem necessary or appropriate. We believe that we have processes in place to oversee and identify risks from cybersecurity threats associated with our use of third-party services providers to our business. See Item 1A: Risk Factors for further discussion regarding data security risks.

Our Information Technology team, under the direction of the Chief Financial Officer and with the assistance of industry-leading third parties with over 20 years of expertise, is tasked with monitoring cybersecurity and operational risks related to information security and system disruption. They have many years of experience in various technology-related functions including security, auditing, compliance and systems. Our Executive Leadership team is briefed regularly on information security, including discussion of processes such as those listed above to monitor the prevention, detection, mitigation and remediation of cybersecurity incidents.

Our Board of Directors is charged with providing oversight of our risk management process. Specifically, the Audit Committee is primarily responsible for overseeing the risk management function, including risks from cybersecurity threats. Periodically, the Audit Committee reviews risk assessments, including cybersecurity risks, prepared by management and/or third-party providers.

There have been no previous cybersecurity incidents which have materially affected us to date, including our business strategy, results of operations or financial condition. However, any future potential risks from cybersecurity threats, including but not limited to exploitation of vulnerabilities, ransomware, denial of service, or other similar threats may materially affect us, including our execution of business strategy, reputation, results of operations and/or financial condition.

ITEM 2: PROPERTIES

We lease 41,016 square feet at our headquarters facility in Minneapolis, Minnesota. We are obligated to pay rent monthly under the lease, and will pay an average of $840,500 annually over the remaining term that expires in 2029. We are also obligated to pay estimated taxes and operating expenses as described in the lease, which change annually. The total rentals, taxes and operating expenses paid may increase if we exercise any of our rights to acquire additional space described in the lease. Our facilities are sufficient to meet our current and immediate future needs.

ITEM 3: LEGAL PROCEEDINGS

We are not a party to any material litigation and are not aware of any threatened litigation that would have a material adverse effect on our business.

ITEM 4: MINE SAFETY DISCLOSURES

Not applicable.

11

PART II

ITEM 5: MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information, Holders, Dividends

Winmark Corporation’s common stock trades on the NASDAQ Global Market under the symbol “WINA”. For dividend information see Note 6 – “Shareholders’ Equity (Deficit).”

At February 26, 2024, there were approximately 52 shareholders of record of our common stock.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

Total Number of | Maximum Number | |||||||||

Shares Purchased as | of Shares that may |

| ||||||||

Total Number of | Average Price | Part of a Publicly | yet be Purchased |

| ||||||

Period |

| Shares Purchased |

| Paid Per Share |

| Announced Plan(1) |

| Under the Plan |

| |

October 1, 2023 to November 4, 2023 |

| — | $ | — |

| — |

| 78,600 | ||

November 5, 2023 to December 2, 2023 |

| — | $ | — |

| — |

| 78,600 | ||

December 3, 2023 to December 30, 2023 |

| — | $ | — |

| — |

| 78,600 | ||

| (1) | The Board of Directors’ authorization for the repurchase of shares of the Company’s common stock was originally approved in 1995 with no expiration date. The total shares approved for repurchase has been increased by additional Board of Directors’ approvals and as of December 30, 2023 was limited to 5,400,000 shares, of which 78,600 may still be repurchased. |

The table set forth in Part III, Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholders Matter” of this Annual Report is also incorporated herein by reference.

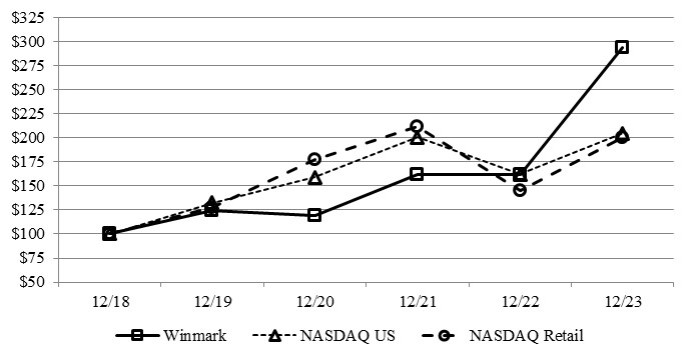

Performance Graph

In accordance with the rules of the SEC, the following graph compares the performance of our common stock on the NASDAQ stock market to the NASDAQ US Benchmark TR composite index and to the NASDAQ US Benchmark Retail TR industry index, of which we are a component. The graph compares on an annual basis the cumulative total shareholder return on $100 invested on December 29, 2018 though our fiscal year ended December 30, 2023 and assumes reinvestment of all dividends. The performance graph is not necessarily indicative of future investment performance.

12

ITEM 6: [RESERVED]

None.

ITEM 7: MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following is management’s discussion and analysis of certain significant factors which have affected our financial position and operating results during the periods included in the accompanying consolidated financial statements and should be read in conjunction with those consolidated financial statements. This section of this 10-K generally discusses 2023 and 2022 items and year-to-year comparisons between 2023 and 2022. Discussions of 2021 items and year-to-date comparisons between 2022 and 2021 that are not included in this Form 10-K, can be found in ‘Management’s Discussion and Analysis of Financial Condition and Results of Operations’ in Part II, Item 7 of our Annual Report on Form 10-K for the fiscal year ended December 31, 2022.

Overview

Winmark – the Resale Company is focused on sustainability and small business formation. As of December 30, 2023, we had 1,319 franchises operating under the Plato’s Closet, Once Upon A Child, Play It Again Sports, Style Encore and Music Go Round brands. Our business is not capital intensive and is designed to generate consistent, recurring revenue and strong operating margins.

The financial criteria that management closely tracks to evaluate current business operations and future prospects include royalties and selling, general and administrative expenses.

Our most significant source of franchising revenue is royalties received from our franchisees. During 2023, our royalties increased $3.1 million or 4.6% compared to 2022.

Management continually monitors the level and timing of selling, general and administrative expenses. The major components of selling, general and administrative expenses include salaries, wages and benefits, advertising, travel, occupancy, legal and professional fees. During 2023, selling, general and administrative expense increased $2.0 million, or 8.4%, compared to the same period last year.

Management also monitors several nonfinancial factors in evaluating the current business operations and future prospects including franchise openings and closings and franchise renewals. The following is a summary of our net store growth and renewal activity for the fiscal year ended December 30, 2023:

AVAILABLE | |||||||||||||||

TOTAL | TOTAL | FOR | COMPLETED |

| |||||||||||

| 12/31/2022 | OPENED | CLOSED | 12/30/2023 |

| RENEWAL | RENEWALS | % RENEWED | |||||||

Plato’s Closet |

| 500 |

| 11 |

| (5) |

| 506 |

| 65 |

| 65 |

| 100 | % |

Once Upon A Child |

| 406 |

| 11 |

| (1) |

| 416 |

| 54 | 54 |

| 100 | % | |

Play It Again Sports |

| 281 |

| 17 |

| (4) |

| 294 |

| 34 | 34 |

| 100 | % | |

Style Encore |

| 71 |

| — |

| (5) |

| 66 |

| 18 |

| 17 |

| 94 | % |

Music Go Round |

| 37 |

| — |

| — |

| 37 |

| 6 |

| 6 |

| 100 | % |

Total Franchised Stores(1) |

| 1,295 |

| 39 |

| (15) |

| 1,319 |

| 177 |

| 176 |

| 99 | % |

| (1) | All stores are owned and operated by franchisees. Winmark does not own or operate any corporate stores. |

Renewal activity is a key focus area for management. Our franchisees sign 10-year agreements with us. The renewal of existing franchise agreements as they approach their expiration is an indicator that management monitors to determine the health of our business and the preservation of future royalties. In 2023, we renewed 99% of franchise agreements up for renewal. This percentage of renewal has ranged between 99% and 100% during the last three years.

Our ability to grow our operating income is dependent on our ability to: (i) effectively support our franchise partners so that they produce higher revenues, (ii) open new franchises, and (iii) control our selling, general and administrative expenses. A detailed description of the risks to our business along with other risk factors can be found in Item 1A “Risk Factors”.

13

In May 2021, we made the decision to no longer solicit new leasing customers and will pursue an orderly run-off of our middle-market leasing portfolio. Leasing income net of leasing expense for the fiscal year of 2023 was $4.4 million compared to $6.0 million in 2022. Our leasing portfolio (net investment in leases – current and long-term), was $0.1 million at December 30, 2023 compared to $0.3 million at December 31, 2022. Given the decision to run-off the portfolio, we anticipate that leasing income net of leasing expense and the size of the leasing portfolio will continue to decrease through the run-off period. See Note 3 – “Investment in Leasing Operations” for information regarding the lease portfolio, including future minimum lease payments receivable under lease contracts and the amortization of unearned lease income.

Results of Operations

The following table sets forth selected information from our Consolidated Statements of Operations expressed as a percentage of total revenue and the percentage change in the dollar amounts from the prior period:

Fiscal Year Ended | Fiscal 2023 | |||||

December 30, | December 31, | over (under) | ||||

2023 |

| 2022 |

| 2022 |

| |

Revenue: | ||||||

Royalties | 84.4 | % | 82.5 | % | 4.6 | % |

Leasing income | 5.7 | 8.5 | (31.3) | |||

Merchandise sales | 5.7 | 4.8 | 21.4 | |||

Franchise fees | 1.8 | 1.9 | (4.0) | |||

Other | 2.4 | 2.3 | 8.0 | |||

Total revenue | 100.0 | 100.0 | 2.3 | |||

Cost of merchandise sold | (5.3) | (4.6) | 20.2 | |||

Leasing expense | (0.5) | (1.2) | (59.5) | |||

Provision for credit losses | - | 0.1 | (90.3) | |||

Selling, general and administrative expenses | (30.2) | (28.4) | 8.4 | |||

Income from operations | 64.0 | 65.9 | (0.6) | |||

Interest expense | (3.7) | (3.6) | 6.0 | |||

Interest and other income | 1.4 | 0.1 | 1,269.3 | |||

Income before income taxes | 61.7 | 62.4 | 1.1 | |||

Provision for income taxes | (13.4) | (14.0) | (1.5) | |||

Net income | 48.3 | % | 48.4 | % | 1.9 | % |

Revenue

Revenues for the year ended December 30, 2023 totaled $83.2 million compared to $81.4 million in 2022.

Royalties and Franchise Fees

Royalties increased to $70.2 million for 2023 from $67.1 million for the same period in 2022, a 4.6% increase. The increase is primarily due to higher franchisee retail sales and from having additional franchise stores in 2023 compared to 2022. Fiscal 2023 was a 52-week year compared to a 53-week year in fiscal 2022, which also impacted the comparability of royalty revenue.

Franchise fees of $1.5 million for 2023 were comparable to $1.6 million for 2022. Franchise fees include initial franchise fees from the sale of new franchises and transfer fees related to the transfer of existing franchises. Franchise fee revenue is recognized over the estimated life of the franchise, beginning when the franchise opens. An overview of retail brand franchise fees is presented in the Operations subsection of the Business section (Item 1).

Leasing Income

Leasing income decreased to $4.8 million in 2023 compared to $6.9 million for the same period in 2022. The decrease is primarily due to a decrease in selling profit on the commencement of sales type leases and lower levels of equipment sales to customers, partially offset by an increase in operating lease income when compared to last year.

14

Merchandise Sales

Merchandise sales include the sale of product to franchisees either through our Computer Support Center or through the Play It Again Sports buying group (together, “Direct Franchisee Sales”). Direct Franchisee Sales increased to $4.8 million in 2023 from $3.9 million in 2022. The increase is due to an increase in technology and buying group purchases by our franchisees.

Cost of Merchandise Sold

Cost of merchandise sold includes in-bound freight and the cost of merchandise associated with Direct Franchisee Sales. Cost of merchandise sold increased to $4.5 million in 2023 from $3.7 million in 2022. The increase was due to an increase in Direct Franchisee Sales discussed above. Cost of merchandise sold as a percentage of Direct Franchisee Sales for 2023 and 2022 was 93.7% and 94.7%, respectively.

Leasing Expense

Leasing expense decreased to $0.4 million in 2023 compared to $1.0 million in 2022. The decrease was primarily due to a decrease in depreciation on operating leases and a decrease in the associated cost of equipment sales to customers noted above.

Selling, General and Administrative Expenses

Selling, general and administrative expenses increased 8.4% to $25.1 million in 2023 from $23.2 million in 2022. The increase was primarily due to an increase in conference expenses, as we returned to holding an in-person conference for our apparel brands for the first time since the Covid-19 outbreak, advertising related expenses, outside services and amortization expense.

Interest Expense

Interest expense was $3.1 million in 2023 compared to $2.9 million in 2022. The increase is primarily due to higher average corporate borrowings when compared to last year.

Income Taxes

The provision for income taxes was calculated at an effective rate of 21.8% and 22.4% for 2023 and 2022, respectively. The decrease is primarily due to higher tax benefits on the exercise of non-qualified stock options.

Segment Comparison of Fiscal Years 2023 and 2022

As of December 30, 2023, we have one reportable operating segment, franchising, and one non-reportable operating segment. The franchising segment franchises value-oriented retail store concepts that buy, sell and trade merchandise. The non-reportable operating segment includes our equipment leasing business. Segment reporting is intended to give financial statement users a better view of how we manage and evaluate our businesses. Our internal management reporting is the basis for the information disclosed for our operating segments. The following tables summarize financial information by segment and provide a reconciliation of segment contribution to income from operations:

Year Ended |

| ||||||

| December 30, 2023 |

| December 31, 2022 |

| |||

Revenue: | |||||||

Franchising | $ | 78,477,300 | $ | 74,473,100 | |||

Other |

| 4,766,200 |

| 6,937,700 | |||

Total revenue | $ | 83,243,500 | $ | 81,410,800 | |||

Reconciliation to income from operations: | |||||||

Franchising segment contribution | $ | 49,375,900 | $ | 49,007,900 | |||

Other operating segment contribution |

| 3,904,700 |

| 4,604,900 | |||

Total income from operations | $ | 53,280,600 | $ | 53,612,800 | |||

Revenues are all generated from United States operations other than franchising revenue from Canadian operations of $6.8 million and $6.4 million in each of fiscal 2023 and 2022, respectively.

15

Franchising Segment Operating Income

The franchising segment’s 2023 operating income increased by $0.4 million, or 0.8%, to $49.4 million from $49.0 million for 2022. The increase in segment contribution was primarily due to increased royalty revenues, partially offset by an increase in selling, general and administrative expenses.

Other Segment Operating Income

The other segment operating income for 2023 decreased by $0.7 million, or 15.2%, to $3.9 million from $4.6 million for 2022. The decrease in segment contribution was due to a decrease in leasing income net of leasing expense, partially offset by a decrease in selling, general and administrative expenses.

Liquidity and Capital Resources

Our primary sources of liquidity have historically been cash flow from operations and borrowings. The components of the Consolidated Statements of Operations that reduce our net income but do not affect our liquidity include non-cash items for depreciation and amortization and compensation expense related to stock options.

We ended 2023 with $13.4 million in cash, cash equivalents and restricted cash compared to $13.7 million in cash, cash equivalents and restricted cash at the end of 2022.

Operating activities provided $44.0 million of cash during 2023 compared to $43.8 million provided during 2022.

Investing activities used $0.4 million of cash during 2023 compared to $3.7 million used during 2022.

Financing activities used $43.9 million of cash during 2023 compared to $37.9 million used during 2022. Our most significant financing activities over the past two years have consisted of net borrowings/payments on our debt facilities, the payment of dividends, repurchase of common stock, and net proceeds received from the exercise of stock options. During 2023, we paid $43.7 million in cash dividends (including a $9.40 per share special cash dividend; the “2023 Special Dividend”), and paid $4.3 million on notes payable; partially offset by $4.0 million of proceeds from the exercise of stock options. (See Note 6 — “Shareholders’ Equity (Deficit)” and Note 7 — “Debt”).

We have debt obligations and future operating lease commitments for our corporate headquarters. As of December 30, 2023, we had no other material outstanding commitments. (See Note 12 — “Commitments and Contingencies”). The following table summarizes our significant future contractual obligations at December 30, 2023:

Payments due by period |

| |||||||||||||||

Less than 1 | More than 5 | |||||||||||||||

| Total |

| year |

| 1-3 years |

| 3-5 years |

| years |

| ||||||

Contractual Obligations | ||||||||||||||||

Line of Credit/Term loan(1)(3) | $ | 37,372,900 | $ | 1,395,500 | $ | 2,791,000 | $ | 2,791,000 | $ | 30,395,400 | ||||||

Notes Payable(2)(3) |

| 44,413,700 | 5,604,800 | 6,178,000 | 32,630,900 | — | ||||||||||

Operating Lease Obligations |

| 5,042,900 | 784,400 | 1,634,200 | 1,725,700 | 898,600 | ||||||||||

Total Contractual Obligations | $ | 86,829,500 | $ | 7,784,700 | $ | 10,603,200 | $ | 37,147,600 | $ | 31,294,000 | ||||||

| (1) | Includes interest payable monthly at rates ranging from 4.60% to 4.75%. |

| (2) | Includes interest payable quarterly at rates ranging from 3.18% to 5.50% assuming principal payments in accordance with amortizing schedules. |

| (3) | Refer to Part II, Item 8 in this report under Note 7 — “Debt” for additional information regarding long-term debt. |

Our debt facilities include a Line of Credit with CIBC Bank USA and a Note Agreement and Shelf Agreement with Prudential. These facilities have been and will continue to be used for general corporate purposes, are secured by a lien against substantially all of our assets, contain customary financial conditions and covenants, and require maintenance of minimum levels of debt service coverage and maximum levels of leverage (all as defined within the agreements governing the facilities). As of December 30, 2023, we were in compliance with all of the financial covenants under the Line of Credit, the Note Agreement and the Shelf Agreement.

16

The Line of Credit provides for up to $20.0 million in revolving loans and $30.0 million in delayed draw term loans. As of December 30, 2023, we had no revolving loans outstanding, and had delayed draw term loan borrowings totaling $30.0 million that mature in 2029.

The Shelf Agreement allows us to offer privately negotiated senior notes to Prudential in an aggregate principal amount up to (i) $100.0 million, less (ii) the aggregate principal amount of notes outstanding at such point (including notes outstanding under the Note Agreement, which at December 30, 2023 was $39.2 million). As of December 30, 2023, we had not issued any notes under the Shelf Agreement. Of the $39.2 million of principal outstanding under the Note Agreement, $9.2 million amortizes over 2024 through 2027, and $30.0 million matures in 2028.

See Part II, Item 8, Note 7 – “Debt” for more information regarding the Line of Credit, Note Agreement and Shelf Agreement.

We expect to generate the cash necessary to pay our expenses and to pay the principal and interest on our outstanding debt from cash flows provided by operating activities and by opportunistically using other means to repay or refinance our obligations as we determine appropriate. Our ability to pay our expenses and meet our debt service obligations depends on our future performance, which may be affected by financial, business, economic, and other factors including the risk factors described under Item 1A of this report. If we do not have enough money to pay our debt service obligations, we may be required to refinance all or part of our existing debt, sell assets, borrow more money or raise equity. In such an event, we may not be able to refinance our debt, sell assets, borrow more money or raise equity on terms acceptable to us or at all. Also, our ability to carry out any of these activities on favorable terms, if at all, may be further impacted by any financial or credit crisis which may limit access to the credit markets and increase our cost of capital.

As of the date of this report we believe that the combination of our cash on hand, the cash generated from our franchising and leasing businesses, our Line of Credit and our Shelf Agreement will be adequate to fund our planned operations through 2024.

Critical Accounting Policies

The Company prepares the consolidated financial statements of Winmark Corporation and Subsidiaries in conformity with accounting principles generally accepted in the United States of America. As such, the Company is required to make certain estimates, judgments and assumptions that it believes are reasonable based on information available. These estimates and assumptions affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the periods presented. There can be no assurance that actual results will not differ from these estimates. The critical accounting policies that the Company believes are most important to aid in fully understanding and evaluating the reported financial results include the following:

Revenue Recognition — Royalty Revenue and Franchise Fees

The Company collects royalties from each retail franchise based on a percentage of retail store gross sales. The Company recognizes royalties as revenue when earned. At the end of each accounting period, royalty amounts due are based on franchisee sales information. As of December 30, 2023, the Company’s royalty receivable was $1,110,500.

The Company collects initial franchise fees when franchise agreements are signed and recognizes the initial franchise fees as revenue over the estimated life of the franchise, beginning when the franchise is opened. Franchise fees collected from franchisees but not yet recognized as income are recorded as deferred revenue in the liability section of the consolidated balance sheet. As of December 30, 2023, deferred franchise fee revenue was $7,088,700.

Recent Accounting Pronouncements

See Note 2, “Significant Accounting Policies — Recently Issued Accounting Pronouncements”.

17

ITEM 7A: QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

The Company incurs financial markets risk in the form of interest rate risk. Risk can be quantified by measuring the financial impact of a near-term adverse increase in short-term interest rates. At December 30, 2023, the Company’s line of credit with CIBC Bank USA included a commitment for revolving loans of $20.0 million. The interest rates applicable to revolving loans are based on either the bank’s base rate or SOFR for short-term borrowings (twelve months or less). The Company had no revolving loans outstanding at December 30, 2023 under this line of credit. The Company’s earnings would be affected by changes in short-term interest rates only in the event that it were to borrow amounts under this facility. With the Company’s borrowings at December 30, 2023, a one percent increase in short-term rates would have no impact on annual pretax earnings. The Company had no interest rate derivatives in place at December 30, 2023.

None of the Company’s cash and cash equivalents at December 30, 2023 was invested in money market mutual funds, which are subject to the effects of market fluctuations in interest rates.

Foreign currency transaction gains and losses were not material to the Company’s results of operations for the year ended December 30, 2023, as approximately 8% of the Company’s total revenues and less than 1% of expenses were denominated in a foreign currency. Based upon these revenues and expenses, a 10% increase or decrease in the foreign currency exchange rates would impact annual pretax earnings by approximately $670,000. To date, the Company has not entered into any foreign currency forward exchange contracts or other derivative financial instruments to hedge the effects of adverse fluctuations in foreign currency exchange rates.

ITEM 8: FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

Winmark Corporation and Subsidiaries

Index to Consolidated Financial Statements

Page 19 | |

Page 20 | |

Page 21 | |

Page 22 | |

Page 23 | |

Reports of Independent Registered Public Accounting Firm (PCAOB ID: | Page 39 |

18

WINMARK CORPORATION AND SUBSIDIARIES

Consolidated Balance Sheets

| December 30, 2023 |

| December 31, 2022 | |||

ASSETS | ||||||

Current Assets: | ||||||

Cash and cash equivalents | $ | | $ | | ||

Restricted cash |

| |

| | ||

Receivables, less allowance for credit losses of $ |

| |

| | ||

Net investment in leases - current |

| |

| | ||

Income tax receivable |

| |

| | ||

Inventories |

| |

| | ||

Prepaid expenses |

| |

| | ||

Total current assets |

| |

| | ||

Net investment in leases — long-term |

| — |

| | ||

Property and equipment: | ||||||

Furniture and equipment |

| |

| | ||

Building and building improvements |

| |

| | ||

Less - accumulated depreciation and amortization |

| ( |

| ( | ||

Property and equipment, net |

| |

| | ||

Operating lease right of use asset | | | ||||

Intangible assets, net | | | ||||

Goodwill |

| |

| | ||

Other assets | | | ||||

Deferred income taxes | | | ||||

$ | | $ | | |||

LIABILITIES AND SHAREHOLDERS' EQUITY (DEFICIT) | ||||||

Current Liabilities: | ||||||

Notes payable, net of unamortized debt issuance costs of $ | $ | | $ | | ||

Accounts payable |

| |

| | ||

Accrued liabilities |

| |

| | ||

Deferred revenue |

| |

| | ||

Total current liabilities |

| |

| | ||

Long-term Liabilities: | ||||||

Line of credit/Term loan | | | ||||

Notes payable, net of unamortized debt issuance costs of $ | | | ||||

Deferred revenue |

| |

| | ||

Operating lease liabilities | | | ||||

Other liabilities |

| |

| | ||

Total long-term liabilities |

| |

| | ||

Commitments and Contingencies (Note 12) |

|

| ||||

Shareholders’ Equity (Deficit): | ||||||

Common stock, |

| |

| | ||

Retained earnings (accumulated deficit) |

| ( |

| ( | ||

Total shareholders' equity (deficit) |

| ( |

| ( | ||

$ | | $ | | |||

The accompanying notes are an integral part of these consolidated financial statements.

19

WINMARK CORPORATION AND SUBSIDIARIES

Consolidated Statements of Operations

Fiscal Year Ended |

| |||||||||

| December 30, 2023 |

| December 31, 2022 |

| December 25, 2021 |

| ||||

Revenue: | ||||||||||

Royalties | $ | | $ | | $ | | ||||

Leasing income |

| |

| |

| | ||||

Merchandise sales |

| |

| |

| | ||||

Franchise fees |

| |

| |

| | ||||

Other |

| |

| |

| | ||||

Total revenue |

| |

| |

| | ||||

Cost of merchandise sold |

| |

| |

| | ||||

Leasing expense |

| |

| |

| | ||||

Provision for credit losses |

| ( |

| ( |

| ( | ||||

Selling, general and administrative expenses |

| |

| |

| | ||||

Income from operations |

| |

| |

| | ||||

Interest expense |

| ( |

| ( |

| ( | ||||

Interest and other income (expense) |

| |

| |

| ( | ||||

Income before income taxes |

| |

| |

| | ||||

Provision for income taxes |

| ( |

| ( |

| ( | ||||

Net income | $ | | $ | | $ | | ||||

Earnings per share - basic | $ | $ | $ | |||||||

Earnings per share - diluted | $ | | $ | | $ | | ||||

Weighted average shares outstanding - basic |

| |

| |

| | ||||

Weighted average shares outstanding - diluted |

| |

| |

| | ||||

The accompanying notes are an integral part of these consolidated financial statements.

20

WINMARK CORPORATION AND SUBSIDIARIES

Consolidated Statements of Shareholders’ Equity (Deficit)

Fiscal years ended December 30, 2023, December 31, 2022 and December 25, 2021

Retained |

| |||||||||||

Earnings |

| |||||||||||

Common Stock | (Accumulated |

| ||||||||||

| Shares |

| Amount |

| Deficit) |

| Total |

| ||||

BALANCE, December 26, 2020 | | $ | $ | ( | $ | ( | ||||||

Repurchase of common stock |

| ( | ( | ( | ( | |||||||

Stock options exercised |

| | | — | | |||||||

Compensation expense relating to stock options |

| — | | — | | |||||||

Cash dividends |

| — | — | ( | ( | |||||||

Comprehensive income (Net income) |

| — | — | | | |||||||

BALANCE, December 25, 2021 |

| | — | ( | ( | |||||||

Repurchase of common stock |