Explanatory Note

The Registrant is filing this amendment to its Form N-CSR for the period ended December 31, 2017, originally filed with the Securities and Exchange Commission on March 8, 2018 (Accession Number 0000277751-18-000031). The sole purpose of this filing is to replace the Independent Auditor's Report that was previously filed.

United States Securities and Exchange Commission

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report

of Registered Management Investment Companies

Investment Company Act file number 811-07736

Janus

Aspen Series

(Exact name of registrant as specified in charter)

151 Detroit Street, Denver,

Colorado 80206

(Address of principal executive offices) (Zip code)

Kathryn L. Santoro, 151

Detroit Street, Denver, Colorado 80206

(Name and address of agent for service)

Registrant's telephone number, including area code: 303-333-3863

Date of fiscal year end: 12/31

Date of reporting period:

12/31/17

Item 1 - Reports to Shareholders

ANNUAL REPORT December 31, 2017 | |||

Janus Henderson VIT Balanced Portfolio (formerly named Janus Aspen Balanced Portfolio) | |||

Janus Aspen Series | |||

| |||

HIGHLIGHTS · Portfolio management perspective · Investment strategy behind your portfolio · Portfolio performance, characteristics | |||

|

Table of Contents

Janus Henderson VIT Balanced Portfolio

Janus Henderson VIT Balanced Portfolio (unaudited)

PERFORMANCE SUMMARY

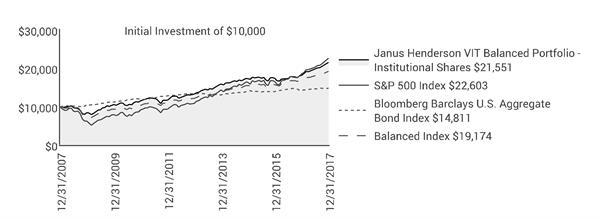

Janus Henderson VIT Balanced Portfolio’s Institutional Shares and Service Shares returned 18.43% and 18.13%, respectively, for the 12-month period ended December 31, 2017, compared with 13.29% for the Balanced Index, an internally calculated benchmark that combines the total returns from the S&P 500® Index (55%) and the Bloomberg Barclays U.S. Aggregate Bond Index (45%). The S&P 500 Index returned 21.83% and the Bloomberg Barclays U.S. Aggregate Bond Index returned 3.54%.

INVESTMENT ENVIRONMENT

Stocks rallied over the course of the year fueled by a combination of strong corporate fundamentals and the expectation that the Trump administration would champion a pro-growth agenda. For their part, corporations delivered as both revenue and earnings results consistently exceeded consensus expectations. On the policy front, after early missteps and failure to pass health care reform, a tax deal was signed into law by the end of the period. Economic data reinforced the notion that conditions remained favorable for risk assets. Changes in non-farm payrolls averaged 172,000 for reports released during the period. After sliding from 1.8% to 1.3%, year-over-year core inflation rebounded to 1.5% by period end. The Federal Reserve (Fed) raised interest rates three times throughout the year and began normalizing its balance sheet late in the period. Investors were reassured that the central bank’s methodical cadence in unwinding accommodative monetary policy would continue under Jerome Powell, the nominee for the next Fed chairman. On a sector basis, within the S&P 500 Index, technology outpaced the broader market. Only energy and telecommunications failed to deliver positive returns.

Investment-grade corporate credit was the strongest-performing asset class in the Bloomberg Barclays U.S. Aggregate Bond Index, while asset-backed securities lagged. Spreads on investment-grade corporate credit reached post crisis tights amid investors’ risk-on mindset. High-yield spreads also tightened. The Treasury curve flattened over the year. Fed-driven volatility pushed shorter-dated yields higher, the 10-year note ended 2017 near where it began, and the yield on the 30-year bond fell amid investors’ reach for yield. The 10-year Treasury note yield closed December at 2.41%, compared with 2.44% one year ago.

PERFORMANCE DISCUSSION

The Portfolio, which seeks to provide more consistent returns over time by allocating across the spectrum of fixed income and equity securities, outperformed the Balanced Index, a blended benchmark of the S&P 500 Index (55%) and the Bloomberg Barclays U.S. Aggregate Bond Index (45%). The Portfolio underperformed its primary benchmark, the S&P 500 Index, and outperformed its secondary benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index.

Compared to the Balanced Index, the Portfolio remains overweight equities, with a 62% allocation to stocks, approximately 37% in fixed income and a small portion in cash. Our year-end allocation reflects our view that on a risk-adjusted basis, equities present more attractive opportunities relative to fixed income. The equity weighting may vary based on market conditions.

The Portfolio’s equity sleeve outperformed its benchmark, the S&P 500 Index. Growth equities performed well during the period, creating a tailwind for our growth tilt. At the sector level, stock selection in industrials and information technology aided relative returns. Our limited exposure to the poor-performing energy and telecommunications sectors also contributed to performance. Stock selection in the health care, consumer discretionary and financials sectors weighed on relative results.

Aerospace company Boeing was the top equity contributor to performance. Boeing benefited from

Janus Aspen Series | 1 |

Janus Henderson VIT Balanced Portfolio (unaudited)

continued strength in global air traffic and strong demand for its 737 and 787 planes, as well as from optimism around its newly integrated services business, which combined its defense and commercial servicing facilities. We like Boeing’s ability to generate free cash flow, which management often returns to shareholders. We also appreciate the multiple dividend increases throughout the period.

Microsoft also aided results. Our investment thesis in the technology company continues to play out as momentum in its cloud-based businesses, Azure and Office 365, led to strong earnings results. Microsoft continues to return cash to shareholders by way of dividends and share repurchases, and we believe tax reform will allow them to bring back much of their offshore cash balance. While the stock’s valuation is now toward the higher end of its historic range, we continue to like the company’s position as the second-largest provider of cloud-based IT services, and believe its strategic partnerships with clients provide a competitive advantage relative to peers.

Financial services firm Mastercard was another strong contributor. Our investment theme for Mastercard continues to play out, as the company has benefited from consumers and businesses switching from cash and check to plastic and electronic payments. The company continues to take market share, particularly outside of the U.S. where many markets have a lower penetration of electronic payments and are experiencing significantly faster growth in electronic purchase volume.

While pleased with the performance of our equity sleeve during the period, some holdings disappointed. Global pharmaceutical company Allergan was the largest equity detractor from performance. Patent disputes – which ultimately resulted in the invalidation of Allergan’s patent – concerning Restasis, the firm’s blockbuster medicine for dry eye, weighed on the stock. The arrival of a new competitor to the company’s popular wrinkle treatment Botox created further negative sentiment. Given our concerns around these issues, we are reviewing our position.

Mattel was another detractor. The toy manufacturer faced excess inventory issues which resulted from a slowdown in toy sales during the 2016 holiday season. The company also cut its dividend over the period, which was negatively received by investors. More bad news impacted the stock when Toys “R” Us, a major customer, filed for bankruptcy late in the period.

Kroger, an American grocery retailer, also detracted, primarily due to increased competition within the grocery store industry. Amazon’s acquisition of Whole Foods and the subsequent reduction of in-store prices created noise for all grocers over the period. German grocer Lidl also began expanding into the U.S. despite increased competition, we continue to have a favorable view of the company. The company should benefit from the passage of U.S. tax reform given its high effective tax rate. Kroger also continues to benefit from capital investments made to existing stores as well as its online “Clicklist” ordering platform that should allow it to remain on the leading edge of any potential online grocery transition.

The Portfolio’s fixed income sleeve outperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index. We spent the year emphasizing corporate issuers in traditionally defensive sectors, issuers with higher-quality business models, consistent free cash flow and management teams committed to sound balance sheets. We have been particularly concerned with the general complacency prevalent across markets, wary that any shift in sentiment would likely come with increased volatility. We are also mindful of how far spreads have tightened amid the extended innings of the credit cycle. While we are more constructive on both the economic outlook and corporate earnings growth in 2018, it is difficult to say how much optimism markets are already pricing in. Further, we anticipate spread tightening will be limited in the months ahead and carry (a measure of excess income) the primary driver of returns. As such, we continue to emphasize managing idiosyncratic risk and maintaining a diversified portfolio. While we anticipate the Fed’s path to both rate and balance sheet normalization to remain gradual, moderately higher yields are likely. In light of our cautious stance on rates, we lowered duration in the fixed income sleeve over the latter half of the period, ending December at 94% of the benchmark.

Our positioning in Treasury securities was the leading contributor to relative outperformance. We remain biased to the 30-year bond to help balance our corporate credit exposure. This positioning aided performance as long-term yields rallied. With yields rising across the front end of the Treasury curve, our significant underweight allocation to Treasuries further supported results.

Our corporate credit allocation was also accretive. As spreads tightened, our overweight allocation to investment-grade corporates contributed positively to relative outperformance. Our emphasis on owning securities in the lowest tier of investment-grade ratings

2 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio (unaudited)

was particularly beneficial, as “riskier” assets generally performed well during the period. For similar reasons, our out-of-index allocation to high yield was another leading contributor. Our focus on securities that can provide greater spread carry than the index supported results in both investment grade and high yield. However, our limited exposure to the duration of longer-dated corporate credit held back performance, while many benchmark constituents benefited from the decline in long-term rates.

At the credit sector level, banking and brokerage, asset managers and exchanges were among the largest relative contributors. Financials generally performed well throughout the period, benefiting from improved fundamentals, rising interest rates – which help pad net interest income – and the prospect of a more relaxed regulatory environment under the Trump administration. Security selection and our overweight allocations in both sectors aided relative results. At the individual issuer level, Neuberger Berman contributed positively to performance. The asset manager benefited from increased liquidity after the company issued a bond early in 2017. Although we continue to like the company’s conservative management team and its commitment to reducing leverage, our target valuation was realized and we trimmed our position.

Financial services company Raymond James was another leading corporate credit contributor. Raymond James received credit ratings upgrades by both Standard & Poor’s and Moody’s over the period, creating positive investor sentiment. Further, the company continues to demonstrate its ability to attract advisors and assets and to strengthen its business for the long term. We like the stability of the company’s business model and appreciate the management team’s conservative approach to the balance sheet.

Electric utilities led relative sector detractors; our limited exposure to longer-dated securities held back results. We shifted our positioning in independent energy and ended the period with a zero weight allocation, which was a factor in that sector detracting from relative performance. Energy-related issuers generally benefited from climbing oil prices in the latter half of the year.

Broadcom was the leading corporate credit detractor on a relative basis. Our overweight position weighed on results as the semiconductor company made an unexpected bid for Qualcomm late in the period. Spreads widened under the assumption that much of the acquisition would be financed with debt. We believe the diversification will ultimately be positive for Broadcom. We also appreciate management’s commitment to investment-grade ratings and the company’s track record of rapid deleveraging after prior acquisitions.

At the asset class level, our out-of-index allocation to bank loans failed to keep pace with corporate bonds and weighed on relative results. Also detracting was our exposure to U.S. mortgage-backed securities, which lagged the performance of index constituents. Negligible exposure to government-related debt also held back performance. Government-related securities include government agency debt as well as debt issued by state-owned firms, including many emerging market issuers. Emerging markets generally performed well amid investors’ risk-on appetite during the period.

OUTLOOK

We believe equities will continue to present more attractive risk-adjusted opportunities relative to fixed income as we start the new year. Barring a shock to the market, we expect the equity market to continue grinding higher. The predicted gradual pace of monetary normalization by Mr. Powell and the Fed should continue to foster a benign rate environment, which bodes well for stocks. Modest economic growth around the world adds to the favorable environment for equities, and a number of our holdings stand to benefit from tax reform. We remain focused on companies with strong growth prospects and those that are innovating through the use of technology to improve the efficiency and quality of product offerings.

We expect range-bound but moderately higher Treasury yields and a flatter curve, and within the fixed income sleeve, we intend to maintain duration modestly below that of the benchmark. However, we will continue in our tactical approach to yield curve positioning with a focus on capital preservation. While both the economic and corporate earnings outlooks remain constructive and supported by tax reform, we expect a lower return environment for corporate credit in 2018 compared with the previous two calendar years. Spread tightening will be moderate, in our view, and carry will be the primary driver of returns. Given rich valuations and the asymmetric risk profile of credit investing, security avoidance will be critical. As we balance our constructive fundamental outlook with the current valuation environment, we remain opportunistic, seeking to identify and capitalize on spread movements that create the potential for attractive returns. As always, our goal is to participate in spread tightening

Janus Aspen Series | 3 |

Janus Henderson VIT Balanced Portfolio (unaudited)

while keeping capital preservation and strong risk-adjusted returns at the forefront.

Thank you for your investment in Janus Henderson VIT Balanced Portfolio.

4 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio (unaudited)

Portfolio At A Glance

December 31, 2017

5 Top Performers - Holdings |

|

|

| 5 Bottom Performers - Holdings |

| |

Contribution | Contribution | |||||

Boeing Co | 3.48% | Allergan PLC | -0.55% | |||

Microsoft Corp | 2.09% | Mattel Inc | -0.32% | |||

Mastercard Inc | 1.93% | Kroger Co | -0.22% | |||

Adobe Systems Inc | 1.66% | Colony NorthStar Inc | -0.13% | |||

Alphabet Inc - Class C | 1.17% | Outfront Media Inc | -0.03% | |||

5 Top Performers - Sectors* |

|

|

|

|

| |

Portfolio | Portfolio Weighting | S&P 500 Index | ||||

Contribution | (Average % of Equity) | Weighting | ||||

Industrials | 4.00% | 13.80% | 10.15% | |||

Energy | 1.88% | 1.08% | 6.26% | |||

Information Technology | 1.13% | 23.10% | 22.79% | |||

Telecom Services | 0.61% | 0.00% | 2.21% | |||

Utilities | 0.33% | 0.00% | 3.17% | |||

5 Bottom Performers - Sectors* |

|

|

|

|

| |

Portfolio | Portfolio Weighting | S&P 500 Index | ||||

Contribution | (Average % of Equity) | Weighting | ||||

Health Care | -0.53% | 11.95% | 14.12% | |||

Consumer Discretionary | -0.44% | 17.73% | 12.16% | |||

Financials | -0.39% | 12.16% | 14.47% | |||

Other** | -0.24% | 1.04% | 0.00% | |||

Consumer Staples | 0.06% | 11.48% | 8.85% | |||

Security contribution to performance is measured by using an algorithm that multiplies the daily performance of each security with the previous day’s ending weight in the portfolio and is gross of advisory fees. Fixed income securities and certain equity securities, such as private placements and some share classes of equity securities, are excluded. | ||||||

* | Based on sector classification according to the Global Industry Classification Standard (“GICS”) codes, which are the exclusive property and a service mark of MSCI Inc. and Standard & Poor’s. | |||||

** | Not a GICS classified sector. | |||||

Janus Aspen Series | 5 |

Janus Henderson VIT Balanced Portfolio (unaudited)

Portfolio At A Glance

December 31, 2017

5 Largest Equity Holdings - (% of Net Assets) | |

Microsoft Corp | |

Software | 3.5% |

Mastercard Inc | |

Information Technology Services | 2.7% |

Boeing Co | |

Aerospace & Defense | 2.6% |

Alphabet Inc - Class C | |

Internet Software & Services | 2.3% |

Altria Group Inc | |

Tobacco | 2.1% |

13.2% | |

Asset Allocation - (% of Net Assets) | |||||

Common Stocks | 62.0% | ||||

Corporate Bonds | 16.0% | ||||

Mortgage-Backed Securities | 9.1% | ||||

United States Treasury Notes/Bonds | 8.0% | ||||

Investment Companies | 3.0% | ||||

Asset-Backed/Commercial Mortgage-Backed Securities | 2.9% | ||||

Bank Loans and Mezzanine Loans | 1.1% | ||||

Other | (2.1)% | ||||

100.0% | |||||

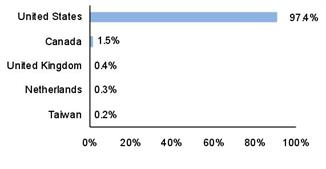

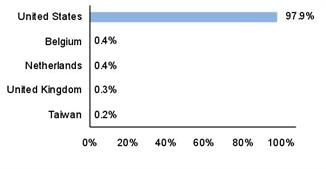

Top Country Allocations - Long Positions - (% of Investment Securities) | |

As of December 31, 2017

| As of December 31, 2016

|

6 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio (unaudited)

Performance

See important disclosures on the next page. |

| Expense Ratios - | ||||||||

Average Annual Total Return - for the periods ended December 31, 2017 |

|

| per the May 1, 2017 prospectuses | ||||||

|

| One

| Five

| Ten | Since |

|

| Total

Annual Fund | |

Institutional Shares |

| 18.43% | 10.20% | 7.98% | 9.94% |

|

| 0.64% | |

Service Shares |

| 18.13% | 9.92% | 7.71% | 9.77% |

|

| 0.89% | |

S&P 500 Index |

| 21.83% | 15.79% | 8.50% | 9.63% |

|

|

| |

Bloomberg Barclays U.S. Aggregate Bond Index |

| 3.54% | 2.10% | 4.01% | 5.22% |

|

|

| |

Balanced Index |

| 13.29% | 9.57% | 6.73% | 7.89% |

|

|

| |

Morningstar Quartile - Institutional Shares |

| 1st | 1st | 1st | 1st |

|

|

| |

Morningstar Ranking - based on total returns for Allocation - 50% to 70% Equity Funds |

| 26/842 | 79/771 | 13/626 | 9/222 |

|

|

| |

Returns quoted are past performance and do not guarantee future results; current performance may be lower or higher. Investment returns and principal value will vary; there may be a gain or loss when shares are sold. For the most recent month-end performance call 800.668.0434 or visit janushenderson.com/VITperformance.

Performance may be affected by risks that include those associated with non-diversification, portfolio turnover, short sales, potential conflicts of interest, foreign and emerging markets, initial public offerings (IPOs), high-yield and high-risk securities, undervalued, overlooked and smaller capitalization companies, real estate related securities including Real Estate Investment Trusts (REITs), derivatives, and commodity-linked investments. Each product has different risks. Please see the prospectus for more information about risks, holdings and other details.

Returns shown do not represent actual returns since they do not include insurance charges. Returns shown would have been lower had they included insurance charges.

Returns include reinvestment of all dividends and distributions and do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or redemptions of Portfolio shares. The returns do not include adjustments in accordance with generally accepted accounting principles required at the period end for financial reporting purposes.

See Financial Highlights for actual expense ratios during the reporting period.

Performance for Service Shares prior to December 31, 1999 reflects the performance of Institutional Shares, adjusted to reflect the expenses of Service Shares.

Ranking is for the share class shown only; other classes may have different performance characteristics.

© 2017 Morningstar, Inc. All Rights Reserved.

There is no assurance that the investment process will consistently lead to successful investing.

Janus Aspen Series | 7 |

Janus Henderson VIT Balanced Portfolio (unaudited)

Performance

See Notes to Schedule of Investments and Other Information and Other Information for index definitions..

Index performance does not reflect the expenses of managing a portfolio as an index is unmanaged and not available for direct investment.

See “Useful Information About Your Portfolio Report.”

*The Portfolio’s inception date – September 13, 1993

8 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio (unaudited)

Expense Examples

As a shareholder of the Portfolio, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; 12b-1 distribution and shareholder servicing fees (applicable to Service Shares only); transfer agent fees and expenses payable pursuant to the Transfer Agency Agreement; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. The example is based upon an investment of $1,000 invested at the beginning of the period and held for the six-months indicated, unless noted otherwise in the table and footnotes below.

Actual Expenses

The information in the table under the heading “Actual” provides information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the appropriate column for your share class under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based upon the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Additionally, for an analysis of the fees associated with an investment in either share class or other similar funds, please visit www.finra.org/fundanalyzer.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as any charges at the separate account level or contract level. These fees are fully described in the Portfolio’s prospectuses. Therefore, the hypothetical examples are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Actual | Hypothetical | |||||||||

| Beginning | Ending | Expenses |

| Beginning | Ending | Expenses | Net Annualized | ||

Institutional Shares | $1,000.00 | $1,091.60 | $3.32 |

| $1,000.00 | $1,022.03 | $3.21 | 0.63% | ||

Service Shares | $1,000.00 | $1,090.30 | $4.58 |

| $1,000.00 | $1,020.82 | $4.43 | 0.87% | ||

† | Expenses Paid During Period are equal to the Net Annualized Expense Ratio multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). Expenses in the examples include the effect of applicable fee waivers and/or expense reimbursements, if any. Had such waivers and/or reimbursements not been in effect, your expenses would have been higher. Please refer to the Notes to Financial Statements or the Portfolio’s prospectuses for more information regarding waivers and/or reimbursements. | |||||||||

Janus Aspen Series | 9 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Asset-Backed/Commercial Mortgage-Backed Securities – 2.9% | |||||||

AmeriCredit Automobile Receivables 2016-1, 3.5900%, 2/8/22 | $1,718,000 | $1,745,603 | |||||

AmeriCredit Automobile Receivables Trust 2015-2, 3.0000%, 6/8/21 | 1,180,000 | 1,191,727 | |||||

AmeriCredit Automobile Receivables Trust 2016-2, 3.6500%, 5/9/22 | 1,165,000 | 1,185,070 | |||||

Applebee's Funding LLC / IHOP Funding LLC, 4.2770%, 9/5/44 (144A) | 6,035,873 | 5,872,146 | |||||

BAMLL Commercial Mortgage Securities Trust 2013-WBRK, | |||||||

3.5343%, 3/10/37 (144A)‡ | 2,000,000 | 2,032,314 | |||||

BAMLL Commercial Mortgage Securities Trust 2014-FL1, | |||||||

ICE LIBOR USD 1 Month + 4.0000%, 5.4770%, 12/15/31 (144A) | 198,000 | 192,712 | |||||

BAMLL Commercial Mortgage Securities Trust 2014-FL1, | |||||||

ICE LIBOR USD 1 Month + 5.5000%, 6.9770%, 12/15/31 (144A) | 824,955 | 784,408 | |||||

BBCMS Trust 2015-SRCH, 4.1970%, 8/10/35 (144A) | 2,486,000 | 2,680,694 | |||||

BXP Trust 2017-GM, 3.3790%, 6/13/39 (144A) | 1,105,000 | 1,128,134 | |||||

Caesars Palace Las Vegas Trust 2017-VICI, 4.1384%, 10/15/34 (144A) | 1,596,000 | 1,639,125 | |||||

Caesars Palace Las Vegas Trust 2017-VICI, 4.3540%, 10/15/34 (144A)‡ | 2,263,000 | 2,197,245 | |||||

Caesars Palace Las Vegas Trust 2017-VICI, 4.3540%, 10/15/34 (144A)‡ | 1,700,000 | 1,734,556 | |||||

CGMS Commercial Mortgage Trust 2017-MDDR, | |||||||

ICE LIBOR USD 1 Month + 1.7500%, 3.2270%, 7/15/30 (144A) | 934,000 | 934,392 | |||||

CGMS Commercial Mortgage Trust 2017-MDDR, | |||||||

ICE LIBOR USD 1 Month + 2.5000%, 3.9770%, 7/15/30 (144A) | 589,000 | 589,242 | |||||

CKE Restaurant Holdings Inc, 4.4740%, 3/20/43 (144A) | 3,013,221 | 3,019,111 | |||||

Coinstar Funding LLC Series 2017-1, 5.2160%, 4/25/47 (144A) | 790,030 | 820,282 | |||||

DB Master Finance LLC, 3.6290%, 11/20/47 (144A) | 901,000 | 906,875 | |||||

DB Master Finance LLC, 4.0300%, 11/20/47 (144A) | 1,063,000 | 1,085,961 | |||||

Domino's Pizza Master Issuer LLC, 3.4840%, 10/25/45 (144A) | 3,085,020 | 3,095,756 | |||||

Domino's Pizza Master Issuer LLC, 3.0820%, 7/25/47 (144A) | 450,870 | 445,919 | |||||

Domino's Pizza Master Issuer LLC, 4.1180%, 7/25/47 (144A) | 2,314,200 | 2,364,372 | |||||

Fannie Mae Connecticut Avenue Securities, | |||||||

ICE LIBOR USD 1 Month + 3.0000%, 4.5521%, 7/25/24 | 2,577,672 | 2,755,287 | |||||

Fannie Mae Connecticut Avenue Securities, | |||||||

ICE LIBOR USD 1 Month + 4.9000%, 6.4521%, 11/25/24 | 1,407,411 | 1,610,302 | |||||

Fannie Mae Connecticut Avenue Securities, | |||||||

ICE LIBOR USD 1 Month + 4.0000%, 5.5521%, 5/25/25 | 524,048 | 569,385 | |||||

Freddie Mac Structured Agency Credit Risk Debt Notes, | |||||||

ICE LIBOR USD 1 Month + 4.5000%, 6.0521%, 2/25/24 | 3,675,000 | 4,292,961 | |||||

Freddie Mac Structured Agency Credit Risk Debt Notes, | |||||||

ICE LIBOR USD 1 Month + 3.6000%, 5.1521%, 4/25/24 | 2,525,620 | 2,817,523 | |||||

FREMF 2010 K-SCT Mortgage Trust, 2.0000%, 1/25/20 (144A)§ | 1,042,523 | 979,433 | |||||

GS Mortgage Securities Corp II, 3.5911%, 9/10/37 (144A)‡ | 1,433,000 | 1,459,325 | |||||

GS Mortgage Securities Trust 2014-GSFL, | |||||||

ICE LIBOR USD 1 Month + 5.9500%, 7.4270%, 7/15/31 (144A) | 992,000 | 994,833 | |||||

GSCCRE Commercial Mortgage Trust 2015-HULA, | |||||||

ICE LIBOR USD 1 Month + 4.4000%, 5.8770%, 8/15/32 (144A) | 1,558,000 | 1,562,890 | |||||

Houston Galleria Mall Trust 2015-HGLR, 3.0866%, 3/5/37 (144A) | 795,000 | 786,970 | |||||

Jimmy Johns Funding LLC, 4.8460%, 7/30/47 (144A) | 1,746,623 | 1,749,679 | |||||

JP Morgan Chase Commercial Mortgage Securities Trust 2010-C2, | |||||||

5.6616%, 11/15/43 (144A)‡ | 933,000 | 935,402 | |||||

JP Morgan Chase Commercial Mortgage Securities Trust 2015-UES, | |||||||

3.6210%, 9/5/32 (144A)‡ | 1,084,000 | 1,081,171 | |||||

JP Morgan Chase Commercial Mortgage Securities Trust 2016-WIKI, | |||||||

3.5537%, 10/5/31 (144A) | 336,000 | 337,900 | |||||

JP Morgan Chase Commercial Mortgage Securities Trust 2016-WIKI, | |||||||

4.0090%, 10/5/31 (144A)‡ | 513,000 | 515,353 | |||||

LB-UBS Commercial Mortgage Trust 2006-C1, 5.2760%, 2/15/41‡ | 2,850 | 2,851 | |||||

LB-UBS Commercial Mortgage Trust 2008-C1, 6.3193%, 4/15/41‡ | 1,162,000 | 1,154,625 | |||||

loanDepot Station Place Agency Securitization Trust 2017-1, | |||||||

ICE LIBOR USD 1 Month + 0.8000%, 2.3521%, 11/25/50 (144A)§ | 3,088,000 | 3,088,000 | |||||

loanDepot Station Place Agency Securitization Trust 2017-1, | |||||||

ICE LIBOR USD 1 Month + 1.0000%, 2.5521%, 11/25/50 (144A)§ | 772,000 | 772,000 | |||||

MAD Mortgage Trust 2017-330M, 3.2944%, 8/15/34 (144A)‡ | 839,000 | 843,973 | |||||

MSSG Trust 2017-237P, 3.3970%, 9/13/39 (144A) | 1,870,000 | 1,893,297 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

10 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Asset-Backed/Commercial Mortgage-Backed Securities – (continued) | |||||||

MSSG Trust 2017-237P, 3.6900%, 9/13/39 (144A) | $327,000 | $330,643 | |||||

OSCAR US Funding Trust V, 2.7300%, 12/15/20 (144A) | 570,000 | 568,944 | |||||

OSCAR US Funding Trust V, 2.9900%, 12/15/23 (144A) | 806,000 | 802,661 | |||||

Santander Drive Auto Receivables Trust 2013-4, 4.6700%, 1/15/20 (144A) | 2,189,000 | 2,193,671 | |||||

Santander Drive Auto Receivables Trust 2013-A, 4.7100%, 1/15/21 (144A) | 1,166,000 | 1,173,910 | |||||

Santander Drive Auto Receivables Trust 2015-1, 3.2400%, 4/15/21 | 1,237,000 | 1,249,912 | |||||

Santander Drive Auto Receivables Trust 2015-4, 3.5300%, 8/16/21 | 2,120,000 | 2,156,500 | |||||

Shops at Crystals Trust 2016-CSTL, 3.1255%, 7/5/36 (144A) | 1,424,000 | 1,398,979 | |||||

Starwood Retail Property Trust 2014-STAR, | |||||||

ICE LIBOR USD 1 Month + 2.5000%, 3.9770%, 11/15/27 (144A) | 654,000 | 633,513 | |||||

Starwood Retail Property Trust 2014-STAR, | |||||||

ICE LIBOR USD 1 Month + 3.2500%, 4.7270%, 11/15/27 (144A) | 1,997,000 | 1,889,638 | |||||

Starwood Retail Property Trust 2014-STAR, | |||||||

ICE LIBOR USD 1 Month + 4.1500%, 5.6270%, 11/15/27 (144A) | 1,059,000 | 976,187 | |||||

Station Place Securitization Trust 2017-3, | |||||||

ICE LIBOR USD 1 Month + 1.0000%, 2.2942%, 7/24/18 (144A)§ | 3,142,000 | 3,142,521 | |||||

Taco Bell Funding LLC, 3.8320%, 5/25/46 (144A) | 2,263,350 | 2,294,064 | |||||

Wachovia Bank Commercial Mortgage Trust Series 2007-C30, 5.4130%, 12/15/43‡ | 1,239,935 | 1,264,784 | |||||

Wachovia Bank Commercial Mortgage Trust Series 2007-C31, 5.6600%, 4/15/47‡ | 1,635,799 | 1,660,810 | |||||

Wachovia Bank Commercial Mortgage Trust Series 2007-C34, 6.0841%, 5/15/46‡ | 650,736 | 667,286 | |||||

Wendys Funding LLC 2015-1, 3.3710%, 6/15/45 (144A) | 3,705,703 | 3,715,634 | |||||

Wendys Funding LLC 2018-1, 3.5730%, 3/15/48 (144A) | 892,000 | 891,722 | |||||

Wendys Funding LLC 2018-1, 3.8840%, 3/15/48 (144A) | 1,267,000 | 1,267,891 | |||||

Worldwide Plaza Trust 2017-WWP, 3.5263%, 11/10/36 (144A) | 1,332,000 | 1,367,579 | |||||

Total Asset-Backed/Commercial Mortgage-Backed Securities (cost $95,664,237) | 95,495,653 | ||||||

Bank Loans and Mezzanine Loans – 1.1% | |||||||

Banking – 0% | |||||||

Vantiv LLC, ICE LIBOR USD + 2.0000%, 0%, 3/31/25 | 141,000 | 141,588 | |||||

Basic Industry – 0.2% | |||||||

Axalta Coating Systems US Holdings Inc, | |||||||

ICE LIBOR USD + 2.0000%, 3.6934%, 6/1/24 | 5,228,300 | 5,244,874 | |||||

Capital Goods – 0.1% | |||||||

Reynolds Group Holdings Inc, ICE LIBOR USD + 2.7500%, 4.0998%, 2/5/23 | 3,827,008 | 3,842,890 | |||||

Communications – 0.3% | |||||||

Mission Broadcasting Inc, ICE LIBOR USD + 2.5000%, 3.8607%, 1/17/24 | 224,553 | 225,033 | |||||

Nexstar Broadcasting Inc, ICE LIBOR USD + 2.5000%, 3.8607%, 1/17/24 | 1,778,282 | 1,782,088 | |||||

Nielsen Finance LLC, ICE LIBOR USD + 2.0000%, 3.4319%, 10/4/23 | 2,204,483 | 2,212,749 | |||||

Sinclair Television Group Inc, ICE LIBOR USD + 2.5000%, 0%, 12/12/24(a) | 2,660,000 | 2,655,026 | |||||

Zayo Group LLC, ICE LIBOR USD + 2.0000%, 3.5521%, 1/19/21 | 205,448 | 205,887 | |||||

Zayo Group LLC, ICE LIBOR USD + 2.2500%, 3.8021%, 1/19/24 | 1,881,066 | 1,886,804 | |||||

8,967,587 | |||||||

Consumer Cyclical – 0.4% | |||||||

Aramark Services Inc, ICE LIBOR USD + 2.0000%, 3.5690%, 3/28/24 | 2,148,180 | 2,159,587 | |||||

Golden Nugget Inc/NV, ICE LIBOR USD + 3.2500%, 4.7699%, 10/4/23 | 2,441,049 | 2,457,843 | |||||

Hilton Worldwide Finance LLC, ICE LIBOR USD + 2.0000%, 3.5521%, 10/25/23 | 5,398,590 | 5,423,531 | |||||

KFC Holding Co, ICE LIBOR USD + 2.0000%, 3.4908%, 6/16/23 | 5,023,321 | 5,049,493 | |||||

15,090,454 | |||||||

Consumer Non-Cyclical – 0% | |||||||

Post Holdings Inc, ICE LIBOR USD + 2.2500%, 3.8200%, 5/24/24 | 600,980 | 602,807 | |||||

Quintiles IMS Inc, ICE LIBOR USD + 2.0000%, 3.6934%, 3/7/24 | 927,738 | 931,050 | |||||

1,533,857 | |||||||

Technology – 0.1% | |||||||

CommScope Inc, ICE LIBOR USD + 2.5000%, 3.3833%, 12/29/22 | 2,501,567 | 2,513,025 | |||||

Total Bank Loans and Mezzanine Loans (cost $37,344,508) | 37,334,275 | ||||||

Corporate Bonds – 16.0% | |||||||

Asset-Backed Securities – 0.1% | |||||||

American Tower Trust #1, 1.5510%, 3/15/18 (144A) | 2,658,000 | 2,654,395 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

Janus Aspen Series | 11 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares or | Value | |||||||

Corporate Bonds – (continued) | ||||||||

Banking – 3.1% | ||||||||

Ally Financial Inc, 3.2500%, 11/5/18 | $1,453,000 | $1,456,632 | ||||||

Ally Financial Inc, 8.0000%, 12/31/18 | 844,000 | 884,090 | ||||||

Bank of America Corp, 2.5030%, 10/21/22† | 6,364,000 | 6,295,430 | ||||||

Bank of America Corp, ICE LIBOR USD 3 Month + 1.0900%, 3.0930%, 10/1/25 | 1,560,000 | 1,556,063 | ||||||

Bank of America Corp, 4.1830%, 11/25/27 | 3,075,000 | 3,210,243 | ||||||

Bank of America Corp, ICE LIBOR USD 3 Month + 1.8140%, 4.2440%, 4/24/38 | 3,096,000 | 3,355,204 | ||||||

Bank of New York Mellon Corp, 2.4500%, 8/17/26 | 505,000 | 479,481 | ||||||

Bank of New York Mellon Corp, 3.2500%, 5/16/27 | 4,014,000 | 4,056,014 | ||||||

Capital One Financial Corp, 3.3000%, 10/30/24 | 4,550,000 | 4,532,488 | ||||||

Citigroup Inc, ICE LIBOR USD 3 Month + 1.4300%, 2.9106%, 9/1/23 | 3,119,000 | 3,210,458 | ||||||

Citigroup Inc, 3.2000%, 10/21/26 | 1,916,000 | 1,900,498 | ||||||

Citigroup Inc, ICE LIBOR USD 3 Month + 1.5630%, 3.8870%, 1/10/28 | 5,465,000 | 5,655,143 | ||||||

Citizens Bank NA/Providence RI, 2.6500%, 5/26/22 | 1,287,000 | 1,275,069 | ||||||

Citizens Financial Group Inc, 3.7500%, 7/1/24 | 785,000 | 784,327 | ||||||

Citizens Financial Group Inc, 4.3500%, 8/1/25 | 613,000 | 637,460 | ||||||

Citizens Financial Group Inc, 4.3000%, 12/3/25 | 3,426,000 | 3,592,595 | ||||||

Discover Financial Services, 3.9500%, 11/6/24 | 1,494,000 | 1,525,776 | ||||||

Discover Financial Services, 3.7500%, 3/4/25 | 766,000 | 770,885 | ||||||

First Republic Bank/CA, 4.6250%, 2/13/47 | 1,158,000 | 1,237,324 | ||||||

Goldman Sachs Capital I, 6.3450%, 2/15/34 | 3,843,000 | 4,833,830 | ||||||

Goldman Sachs Group Inc, ICE LIBOR USD 3 Month + 1.2010%, 3.2720%, 9/29/25 | 4,031,000 | 4,013,838 | ||||||

Goldman Sachs Group Inc, 3.7500%, 2/25/26 | 1,236,000 | 1,267,930 | ||||||

Goldman Sachs Group Inc, 3.5000%, 11/16/26 | 5,508,000 | 5,538,850 | ||||||

JPMorgan Chase & Co, 2.2950%, 8/15/21 | 3,316,000 | 3,285,957 | ||||||

JPMorgan Chase & Co, 3.3750%, 5/1/23 | 4,252,000 | 4,321,354 | ||||||

JPMorgan Chase & Co, 3.8750%, 9/10/24 | 986,000 | 1,028,297 | ||||||

JPMorgan Chase & Co, ICE LIBOR USD 3 Month + 1.3370%, 3.7820%, 2/1/28 | 4,366,000 | 4,522,993 | ||||||

Morgan Stanley, ICE LIBOR USD 3 Month + 1.3400%, 3.5910%, 7/22/28 | 5,758,000 | 5,809,278 | ||||||

Santander UK PLC, 5.0000%, 11/7/23 (144A) | 3,833,000 | 4,095,787 | ||||||

SVB Financial Group, 5.3750%, 9/15/20 | 2,429,000 | 2,595,873 | ||||||

Synchrony Financial, 4.5000%, 7/23/25 | 3,093,000 | 3,231,459 | ||||||

Synchrony Financial, 3.7000%, 8/4/26 | 3,473,000 | 3,423,187 | ||||||

Wells Fargo & Co, 3.0000%, 4/22/26 | 1,013,000 | 993,587 | ||||||

Wells Fargo & Co, 4.1000%, 6/3/26 | 3,276,000 | 3,434,386 | ||||||

Wells Fargo & Co, 4.3000%, 7/22/27 | 2,869,000 | 3,054,043 | ||||||

101,865,829 | ||||||||

Basic Industry – 0.8% | ||||||||

CF Industries Inc, 4.5000%, 12/1/26 (144A) | 2,557,000 | 2,664,730 | ||||||

Freeport-McMoRan Inc, 3.1000%, 3/15/20 | 885,000 | 879,469 | ||||||

Georgia-Pacific LLC, 3.1630%, 11/15/21 (144A) | 4,027,000 | 4,098,387 | ||||||

Georgia-Pacific LLC, 3.6000%, 3/1/25 (144A) | 2,166,000 | 2,225,550 | ||||||

Reliance Steel & Aluminum Co, 4.5000%, 4/15/23 | 2,039,000 | 2,148,999 | ||||||

Sherwin-Williams Co, 2.7500%, 6/1/22 | 912,000 | 908,345 | ||||||

Sherwin-Williams Co, 3.1250%, 6/1/24 | 1,057,000 | 1,062,598 | ||||||

Sherwin-Williams Co, 3.4500%, 6/1/27 | 2,960,000 | 3,006,483 | ||||||

Sherwin-Williams Co, 4.5000%, 6/1/47 | 767,000 | 837,817 | ||||||

Steel Dynamics Inc, 4.1250%, 9/15/25 (144A) | 2,199,000 | 2,215,492 | ||||||

Steel Dynamics Inc, 5.0000%, 12/15/26 | 1,027,000 | 1,086,052 | ||||||

Teck Resources Ltd, 4.5000%, 1/15/21 | 919,000 | 947,673 | ||||||

Teck Resources Ltd, 4.7500%, 1/15/22 | 1,328,000 | 1,386,166 | ||||||

Teck Resources Ltd, 8.5000%, 6/1/24 (144A) | 2,184,000 | 2,467,920 | ||||||

25,935,681 | ||||||||

Brokerage – 0.7% | ||||||||

Cboe Global Markets Inc, 3.6500%, 1/12/27 | 3,023,000 | 3,112,753 | ||||||

Charles Schwab Corp, 3.0000%, 3/10/25 | 930,000 | 926,699 | ||||||

Charles Schwab Corp, 3.2000%, 1/25/28 | 1,880,000 | 1,882,373 | ||||||

E*TRADE Financial Corp, 2.9500%, 8/24/22 | 3,047,000 | 3,020,880 | ||||||

E*TRADE Financial Corp, 3.8000%, 8/24/27 | 2,680,000 | 2,670,487 | ||||||

Lazard Group LLC, 4.2500%, 11/14/20 | 1,625,000 | 1,692,443 | ||||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

12 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares or | Value | |||||||

Corporate Bonds – (continued) | ||||||||

Brokerage – (continued) | ||||||||

Neuberger Berman Group LLC / Neuberger Berman Finance Corp, | ||||||||

4.8750%, 4/15/45 (144A) | $562,000 | $572,605 | ||||||

Raymond James Financial Inc, 5.6250%, 4/1/24 | 1,545,000 | 1,751,255 | ||||||

Raymond James Financial Inc, 3.6250%, 9/15/26 | 1,409,000 | 1,415,225 | ||||||

Raymond James Financial Inc, 4.9500%, 7/15/46 | 2,747,000 | 3,102,865 | ||||||

TD Ameritrade Holding Corp, 2.9500%, 4/1/22 | 1,355,000 | 1,371,067 | ||||||

TD Ameritrade Holding Corp, 3.6250%, 4/1/25 | 1,752,000 | 1,813,338 | ||||||

23,331,990 | ||||||||

Capital Goods – 0.8% | ||||||||

Ball Corp, 4.3750%, 12/15/20 | 1,565,000 | 1,619,775 | ||||||

CNH Industrial Capital LLC, 3.6250%, 4/15/18 | 2,969,000 | 2,984,379 | ||||||

Huntington Ingalls Industries Inc, 5.0000%, 11/15/25 (144A) | 698,000 | 746,860 | ||||||

Martin Marietta Materials Inc, 4.2500%, 7/2/24 | 1,531,000 | 1,610,086 | ||||||

Northrop Grumman Corp, 2.5500%, 10/15/22 | 3,184,000 | 3,160,880 | ||||||

Northrop Grumman Corp, 2.9300%, 1/15/25 | 2,741,000 | 2,724,058 | ||||||

Northrop Grumman Corp, 3.2500%, 1/15/28 | 3,368,000 | 3,371,865 | ||||||

Northrop Grumman Corp, 4.0300%, 10/15/47 | 2,154,000 | 2,248,975 | ||||||

Owens Corning, 4.2000%, 12/1/24 | 1,411,000 | 1,477,938 | ||||||

Owens Corning, 3.4000%, 8/15/26 | 678,000 | 665,301 | ||||||

Rockwell Collins Inc, 3.2000%, 3/15/24 | 1,356,000 | 1,366,112 | ||||||

Rockwell Collins Inc, 3.5000%, 3/15/27 | 2,319,000 | 2,360,487 | ||||||

Vulcan Materials Co, 7.5000%, 6/15/21 | 1,083,000 | 1,253,148 | ||||||

Vulcan Materials Co, 4.5000%, 4/1/25 | 2,597,000 | 2,766,765 | ||||||

28,356,629 | ||||||||

Communications – 2.1% | ||||||||

American Tower Corp, 3.3000%, 2/15/21 | 2,413,000 | 2,457,028 | ||||||

American Tower Corp, 3.4500%, 9/15/21 | 249,000 | 254,473 | ||||||

American Tower Corp, 3.5000%, 1/31/23 | 443,000 | 452,904 | ||||||

American Tower Corp, 4.4000%, 2/15/26 | 1,580,000 | 1,661,098 | ||||||

American Tower Corp, 3.3750%, 10/15/26 | 2,919,000 | 2,867,077 | ||||||

AT&T Inc, 3.4000%, 8/14/24 | 2,139,000 | 2,149,510 | ||||||

AT&T Inc, 4.2500%, 3/1/27 | 993,000 | 1,012,006 | ||||||

AT&T Inc, 3.9000%, 8/14/27 | 1,774,000 | 1,785,342 | ||||||

AT&T Inc, 4.1000%, 2/15/28 (144A) | 3,030,000 | 3,039,124 | ||||||

AT&T Inc, 5.2500%, 3/1/37 | 875,000 | 924,801 | ||||||

AT&T Inc, 5.1500%, 2/14/50 | 1,233,000 | 1,239,152 | ||||||

AT&T Inc, 5.3000%, 8/14/58 | 2,790,000 | 2,796,570 | ||||||

CCO Holdings LLC / CCO Holdings Capital Corp, 5.2500%, 3/15/21 | 2,252,000 | 2,290,002 | ||||||

CCO Holdings LLC / CCO Holdings Capital Corp, 5.1250%, 5/1/27 (144A) | 810,000 | 797,850 | ||||||

CCO Holdings LLC / CCO Holdings Capital Corp, 5.0000%, 2/1/28 (144A) | 3,954,000 | 3,845,265 | ||||||

Charter Communications Operating LLC / Charter Communications Operating Capital, | ||||||||

4.9080%, 7/23/25 | 3,939,000 | 4,186,940 | ||||||

Charter Communications Operating LLC / Charter Communications Operating Capital, | ||||||||

3.7500%, 2/15/28 | 942,000 | 901,666 | ||||||

Charter Communications Operating LLC / Charter Communications Operating Capital, | ||||||||

4.2000%, 3/15/28 | 1,989,000 | 1,968,794 | ||||||

Charter Communications Operating LLC / Charter Communications Operating Capital, | ||||||||

5.3750%, 5/1/47 | 1,026,000 | 1,051,145 | ||||||

Comcast Corp, 2.3500%, 1/15/27 | 1,917,000 | 1,809,873 | ||||||

Comcast Corp, 3.3000%, 2/1/27 | 1,371,000 | 1,398,305 | ||||||

Comcast Corp, 3.4000%, 7/15/46 | 332,000 | 313,812 | ||||||

Cox Communications Inc, 3.1500%, 8/15/24 (144A) | 2,250,000 | 2,215,489 | ||||||

Cox Communications Inc, 3.3500%, 9/15/26 (144A) | 3,038,000 | 2,968,054 | ||||||

Cox Communications Inc, 3.5000%, 8/15/27 (144A) | 2,041,000 | 2,012,544 | ||||||

Crown Castle International Corp, 5.2500%, 1/15/23 | 1,968,000 | 2,154,559 | ||||||

Crown Castle International Corp, 3.2000%, 9/1/24 | 2,028,000 | 2,006,516 | ||||||

Crown Castle International Corp, 3.6500%, 9/1/27 | 3,680,000 | 3,669,899 | ||||||

NBCUniversal Media LLC, 4.4500%, 1/15/43 | 603,000 | 657,437 | ||||||

Time Warner Inc, 3.6000%, 7/15/25 | 1,929,000 | 1,932,863 | ||||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

Janus Aspen Series | 13 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares or | Value | |||||||

Corporate Bonds – (continued) | ||||||||

Communications – (continued) | ||||||||

UBM PLC, 5.7500%, 11/3/20 (144A) | $3,166,000 | $3,286,917 | ||||||

Verizon Communications Inc, 2.6250%, 8/15/26 | 6,068,000 | 5,713,784 | ||||||

Verizon Communications Inc, 4.1250%, 3/16/27 | 1,618,000 | 1,686,635 | ||||||

Verizon Communications Inc, 4.1250%, 8/15/46 | 2,241,000 | 2,068,380 | ||||||

Verizon Communications Inc, 4.8620%, 8/21/46 | 1,206,000 | 1,255,104 | ||||||

70,830,918 | ||||||||

Consumer Cyclical – 1.6% | ||||||||

1011778 BC ULC / New Red Finance Inc, 4.6250%, 1/15/22 (144A) | 3,214,000 | 3,290,332 | ||||||

1011778 BC ULC / New Red Finance Inc, 4.2500%, 5/15/24 (144A) | 2,992,000 | 2,984,520 | ||||||

Amazon.com Inc, 2.8000%, 8/22/24 (144A) | 1,501,000 | 1,496,094 | ||||||

Amazon.com Inc, 3.1500%, 8/22/27 (144A) | 4,781,000 | 4,786,784 | ||||||

Amazon.com Inc, 4.0500%, 8/22/47 (144A) | 1,780,000 | 1,916,468 | ||||||

CVS Health Corp, 2.8000%, 7/20/20 | 2,660,000 | 2,670,909 | ||||||

CVS Health Corp, 4.7500%, 12/1/22 | 1,198,000 | 1,283,048 | ||||||

DR Horton Inc, 3.7500%, 3/1/19 | 1,856,000 | 1,880,833 | ||||||

General Motors Co, 4.8750%, 10/2/23 | 2,289,000 | 2,476,713 | ||||||

General Motors Financial Co Inc, 3.9500%, 4/13/24† | 6,217,000 | 6,399,017 | ||||||

IHO Verwaltungs GmbH, 4.1250%, 9/15/21 (144A) | 515,000 | 524,012 | ||||||

IHO Verwaltungs GmbH, 4.5000%, 9/15/23 (144A) | 376,000 | 383,287 | ||||||

IHS Markit Ltd, 5.0000%, 11/1/22 (144A) | 1,496,000 | 1,621,963 | ||||||

IHS Markit Ltd, 4.7500%, 2/15/25 (144A) | 1,997,000 | 2,106,835 | ||||||

IHS Markit Ltd, 4.0000%, 3/1/26 (144A) | 3,421,000 | 3,416,724 | ||||||

McDonald's Corp, 3.5000%, 3/1/27 | 5,025,000 | 5,166,387 | ||||||

McDonald's Corp, 4.8750%, 12/9/45 | 1,719,000 | 1,989,603 | ||||||

MDC Holdings Inc, 5.5000%, 1/15/24 | 2,138,000 | 2,255,590 | ||||||

MGM Growth Properties Operating Partnership LP / MGP Finance Co-Issuer Inc, | ||||||||

5.6250%, 5/1/24 | 1,246,000 | 1,326,990 | ||||||

Tapestry Inc, 3.0000%, 7/15/22 | 986,000 | 982,390 | ||||||

Tapestry Inc, 4.1250%, 7/15/27 | 986,000 | 993,219 | ||||||

Toll Brothers Finance Corp, 4.0000%, 12/31/18 | 837,000 | 850,601 | ||||||

Toll Brothers Finance Corp, 5.8750%, 2/15/22 | 764,000 | 832,760 | ||||||

Toll Brothers Finance Corp, 4.3750%, 4/15/23 | 404,000 | 419,150 | ||||||

52,054,229 | ||||||||

Consumer Non-Cyclical – 1.8% | ||||||||

Abbott Laboratories, 3.8750%, 9/15/25 | 474,000 | 490,153 | ||||||

Abbott Laboratories, 3.7500%, 11/30/26 | 766,000 | 786,366 | ||||||

Anheuser-Busch InBev Finance Inc, 2.6500%, 2/1/21 | 831,000 | 835,097 | ||||||

Anheuser-Busch InBev Finance Inc, 3.3000%, 2/1/23 | 3,808,000 | 3,896,162 | ||||||

Becton Dickinson and Co, 2.8940%, 6/6/22 | 1,516,000 | 1,506,327 | ||||||

Becton Dickinson and Co, 3.3630%, 6/6/24 | 3,373,000 | 3,381,700 | ||||||

Becton Dickinson and Co, 3.7000%, 6/6/27 | 2,393,000 | 2,410,765 | ||||||

Celgene Corp, 2.7500%, 2/15/23 | 1,848,000 | 1,832,480 | ||||||

Constellation Brands Inc, 4.7500%, 12/1/25 | 333,000 | 365,762 | ||||||

Constellation Brands, Inc., 4.2500%, 5/1/23 | 2,885,000 | 3,051,481 | ||||||

Danone SA, 2.0770%, 11/2/21 (144A) | 2,758,000 | 2,697,576 | ||||||

Danone SA, 2.5890%, 11/2/23 (144A) | 1,891,000 | 1,843,813 | ||||||

Express Scripts Holding Co, 3.5000%, 6/15/24 | 1,165,000 | 1,175,065 | ||||||

Express Scripts Holding Co, 3.4000%, 3/1/27 | 1,333,000 | 1,307,716 | ||||||

HCA Inc, 3.7500%, 3/15/19 | 1,542,000 | 1,555,492 | ||||||

HCA Inc, 5.0000%, 3/15/24 | 1,908,000 | 1,984,320 | ||||||

HCA Inc, 5.2500%, 6/15/26 | 1,708,000 | 1,810,480 | ||||||

HCA Inc, 4.5000%, 2/15/27 | 2,001,000 | 2,011,005 | ||||||

LifePoint Health Inc, 5.5000%, 12/1/21 | 200,000 | 204,000 | ||||||

McCormick & Co Inc/MD, 3.1500%, 8/15/24 | 2,729,000 | 2,742,852 | ||||||

McCormick & Co Inc/MD, 3.4000%, 8/15/27 | 2,080,000 | 2,106,621 | ||||||

Molson Coors Brewing Co, 3.0000%, 7/15/26 | 3,899,000 | 3,815,217 | ||||||

Post Holdings Inc, 5.7500%, 3/1/27 (144A) | 1,238,000 | 1,259,665 | ||||||

Post Holdings Inc, 5.6250%, 1/15/28 (144A) | 658,000 | 660,467 | ||||||

Reckitt Benckiser Treasury Services PLC, 2.7500%, 6/26/24 (144A) | 1,891,000 | 1,849,605 | ||||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

14 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Corporate Bonds – (continued) | |||||||

Consumer Non-Cyclical – (continued) | |||||||

Shire Acquisitions Investments Ireland DAC, 2.4000%, 9/23/21 | $1,837,000 | $1,807,892 | |||||

Shire Acquisitions Investments Ireland DAC, 3.2000%, 9/23/26 | 2,493,000 | 2,436,862 | |||||

Sysco Corp, 2.5000%, 7/15/21 | 630,000 | 628,232 | |||||

Sysco Corp, 3.3000%, 7/15/26 | 1,390,000 | 1,398,348 | |||||

Sysco Corp, 3.2500%, 7/15/27 | 1,121,000 | 1,116,893 | |||||

Universal Health Services Inc, 4.7500%, 8/1/22 (144A) | 1,894,000 | 1,929,512 | |||||

Wm Wrigley Jr Co, 2.4000%, 10/21/18 (144A) | 3,916,000 | 3,926,943 | |||||

58,824,869 | |||||||

Electric – 0.7% | |||||||

Dominion Energy Inc, 2.0000%, 8/15/21 | 366,000 | 357,616 | |||||

Dominion Energy Inc, 2.8500%, 8/15/26 | 506,000 | 488,529 | |||||

Duke Energy Corp, 1.8000%, 9/1/21 | 915,000 | 889,882 | |||||

Duke Energy Corp, 2.4000%, 8/15/22 | 1,332,000 | 1,308,507 | |||||

Duke Energy Corp, 2.6500%, 9/1/26 | 2,633,000 | 2,522,145 | |||||

Duke Energy Corp, 3.1500%, 8/15/27 | 2,042,000 | 2,026,624 | |||||

NextEra Energy Operating Partners LP, 4.2500%, 9/15/24 (144A) | 405,000 | 412,087 | |||||

NextEra Energy Operating Partners LP, 4.5000%, 9/15/27 (144A) | 850,000 | 845,750 | |||||

PPL Capital Funding Inc, 3.1000%, 5/15/26 | 3,249,000 | 3,179,059 | |||||

PPL WEM Ltd / Western Power Distribution Ltd, 5.3750%, 5/1/21 (144A) | 2,176,000 | 2,331,878 | |||||

Southern Co, 2.3500%, 7/1/21 | 2,835,000 | 2,817,892 | |||||

Southern Co, 2.9500%, 7/1/23 | 1,784,000 | 1,784,599 | |||||

Southern Co, 3.2500%, 7/1/26 | 2,850,000 | 2,794,305 | |||||

21,758,873 | |||||||

Energy – 1.0% | |||||||

Andeavor Logistics LP / Tesoro Logistics Finance Corp, 5.2500%, 1/15/25 | 811,000 | 852,929 | |||||

Columbia Pipeline Group Inc, 4.5000%, 6/1/25 | 998,000 | 1,062,372 | |||||

Enbridge Energy Partners LP, 5.8750%, 10/15/25 | 1,467,000 | 1,661,183 | |||||

Energy Transfer Equity LP, 4.2500%, 3/15/23 | 1,711,000 | 1,698,167 | |||||

Energy Transfer Equity LP, 5.8750%, 1/15/24 | 1,604,000 | 1,688,210 | |||||

Energy Transfer LP, 4.1500%, 10/1/20 | 1,412,000 | 1,458,000 | |||||

Kinder Morgan Energy Partners LP, 5.0000%, 10/1/21 | 1,294,000 | 1,379,081 | |||||

Kinder Morgan Energy Partners LP, 3.9500%, 9/1/22 | 1,383,000 | 1,427,113 | |||||

Kinder Morgan Inc/DE, 6.5000%, 9/15/20 | 134,000 | 146,511 | |||||

Motiva Enterprises LLC, 5.7500%, 1/15/20 (144A) | 1,765,000 | 1,863,936 | |||||

NGPL PipeCo LLC, 4.3750%, 8/15/22 (144A) | 388,000 | 394,547 | |||||

NGPL PipeCo LLC, 4.8750%, 8/15/27 (144A) | 996,000 | 1,033,350 | |||||

NuStar Logistics LP, 5.6250%, 4/28/27 | 2,174,000 | 2,212,045 | |||||

Oceaneering International Inc, 4.6500%, 11/15/24 | 1,240,000 | 1,206,163 | |||||

Phillips 66 Partners LP, 3.6050%, 2/15/25 | 1,548,000 | 1,559,265 | |||||

Phillips 66 Partners LP, 3.7500%, 3/1/28 | 619,000 | 619,092 | |||||

Phillips 66 Partners LP, 4.6800%, 2/15/45 | 551,000 | 565,468 | |||||

Plains All American Pipeline LP / PAA Finance Corp, 4.6500%, 10/15/25 | 741,000 | 763,417 | |||||

Plains All American Pipeline LP / PAA Finance Corp, 4.5000%, 12/15/26 | 718,000 | 727,645 | |||||

Regency Energy Partners LP / Regency Energy Finance Corp, 5.8750%, 3/1/22 | 1,788,000 | 1,954,531 | |||||

Sabine Pass Liquefaction LLC, 5.0000%, 3/15/27 | 2,769,000 | 2,970,574 | |||||

TC PipeLines LP, 3.9000%, 5/25/27 | 2,107,000 | 2,116,932 | |||||

Williams Cos Inc, 3.7000%, 1/15/23 | 894,000 | 889,530 | |||||

Williams Partners LP, 3.7500%, 6/15/27 | 3,544,000 | 3,550,358 | |||||

Williams Partners LP / ACMP Finance Corp, 4.8750%, 3/15/24 | 1,098,000 | 1,147,410 | |||||

34,947,829 | |||||||

Finance Companies – 0.1% | |||||||

Quicken Loans Inc, 5.2500%, 1/15/28 (144A) | 3,209,000 | 3,167,925 | |||||

Financial Institutions – 0.4% | |||||||

Jones Lang LaSalle Inc, 4.4000%, 11/15/22 | 2,686,000 | 2,829,508 | |||||

Kennedy-Wilson Inc, 5.8750%, 4/1/24 | 5,195,000 | 5,363,837 | |||||

LeasePlan Corp NV, 2.5000%, 5/16/18 (144A) | 4,744,000 | 4,744,543 | |||||

12,937,888 | |||||||

Industrial – 0% | |||||||

Cintas Corp No 2, 4.3000%, 6/1/21 | 1,143,000 | 1,205,019 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

Janus Aspen Series | 15 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Corporate Bonds – (continued) | |||||||

Insurance – 0.4% | |||||||

Aetna Inc, 2.8000%, 6/15/23 | $1,264,000 | $1,243,814 | |||||

Centene Corp, 4.7500%, 5/15/22 | 183,000 | 189,863 | |||||

Centene Corp, 6.1250%, 2/15/24 | 559,000 | 591,142 | |||||

Centene Corp, 4.7500%, 1/15/25 | 794,000 | 807,895 | |||||

UnitedHealth Group Inc, 2.3750%, 10/15/22 | 1,138,000 | 1,126,841 | |||||

UnitedHealth Group Inc, 3.7500%, 7/15/25 | 2,171,000 | 2,287,735 | |||||

UnitedHealth Group Inc, 3.1000%, 3/15/26 | 1,134,000 | 1,142,078 | |||||

UnitedHealth Group Inc, 3.4500%, 1/15/27 | 833,000 | 861,463 | |||||

UnitedHealth Group Inc, 3.3750%, 4/15/27 | 612,000 | 628,707 | |||||

UnitedHealth Group Inc, 2.9500%, 10/15/27 | 2,202,000 | 2,194,895 | |||||

WellCare Health Plans Inc, 5.2500%, 4/1/25 | 2,183,000 | 2,303,065 | |||||

13,377,498 | |||||||

Real Estate Investment Trusts (REITs) – 0.5% | |||||||

Alexandria Real Estate Equities Inc, 2.7500%, 1/15/20 | 1,328,000 | 1,333,526 | |||||

Alexandria Real Estate Equities Inc, 4.6000%, 4/1/22 | 3,339,000 | 3,545,221 | |||||

Alexandria Real Estate Equities Inc, 4.5000%, 7/30/29 | 1,809,000 | 1,916,983 | |||||

Digital Realty Trust LP, 3.7000%, 8/15/27 | 1,193,000 | 1,201,327 | |||||

Senior Housing Properties Trust, 6.7500%, 4/15/20 | 756,000 | 802,890 | |||||

Senior Housing Properties Trust, 6.7500%, 12/15/21 | 840,000 | 929,431 | |||||

SL Green Realty Corp, 5.0000%, 8/15/18 | 1,894,000 | 1,917,199 | |||||

SL Green Realty Corp, 7.7500%, 3/15/20 | 3,720,000 | 4,092,870 | |||||

15,739,447 | |||||||

Technology – 1.8% | |||||||

Broadcom Corp / Broadcom Cayman Finance Ltd, 3.6250%, 1/15/24 (144A) | 2,112,000 | 2,099,710 | |||||

Broadcom Corp / Broadcom Cayman Finance Ltd, 3.8750%, 1/15/27 (144A)† | 8,579,000 | 8,439,789 | |||||

Cadence Design Systems Inc, 4.3750%, 10/15/24 | 4,174,000 | 4,427,365 | |||||

Equifax Inc, 2.3000%, 6/1/21 | 727,000 | 709,557 | |||||

Equifax Inc, 3.3000%, 12/15/22 | 2,536,000 | 2,519,189 | |||||

First Data Corp, 7.0000%, 12/1/23 (144A) | 2,991,000 | 3,162,982 | |||||

Iron Mountain Inc, 4.8750%, 9/15/27 (144A) | 3,574,000 | 3,574,000 | |||||

Iron Mountain Inc, 5.2500%, 3/15/28 (144A) | 2,885,000 | 2,870,575 | |||||

NXP BV / NXP Funding LLC, 4.1250%, 6/15/20 (144A) | 902,000 | 923,675 | |||||

NXP BV / NXP Funding LLC, 4.1250%, 6/1/21 (144A) | 687,000 | 700,740 | |||||

NXP BV / NXP Funding LLC, 3.8750%, 9/1/22 (144A) | 2,613,000 | 2,642,396 | |||||

NXP BV / NXP Funding LLC, 4.6250%, 6/1/23 (144A) | 1,500,000 | 1,569,000 | |||||

Total System Services Inc, 3.8000%, 4/1/21 | 1,610,000 | 1,650,045 | |||||

Total System Services Inc, 4.8000%, 4/1/26 | 2,865,000 | 3,098,865 | |||||

Trimble Inc, 4.7500%, 12/1/24† | 5,305,000 | 5,724,098 | |||||

TSMC Global Ltd, 1.6250%, 4/3/18 (144A) | 6,525,000 | 6,513,392 | |||||

Verisk Analytics Inc, 4.8750%, 1/15/19 | 1,750,000 | 1,791,869 | |||||

Verisk Analytics Inc, 5.8000%, 5/1/21 | 2,601,000 | 2,829,940 | |||||

Verisk Analytics Inc, 4.1250%, 9/12/22 | 1,574,000 | 1,643,020 | |||||

Verisk Analytics Inc, 5.5000%, 6/15/45 | 1,854,000 | 2,158,292 | |||||

VMware Inc, 3.9000%, 8/21/27 | 1,175,000 | 1,185,801 | |||||

60,234,300 | |||||||

Transportation – 0.1% | |||||||

Penske Truck Leasing Co Lp / PTL Finance Corp, 3.3750%, 3/15/18 (144A) | 2,579,000 | 2,586,656 | |||||

Total Corporate Bonds (cost $523,741,092) | 529,809,975 | ||||||

Mortgage-Backed Securities – 9.1% | |||||||

Fannie Mae Pool: | |||||||

6.0000%, 10/1/35 | 607,044 | 688,050 | |||||

6.0000%, 12/1/35 | 710,144 | 806,518 | |||||

6.0000%, 2/1/37 | 122,624 | 141,002 | |||||

6.0000%, 10/1/38 | 448,240 | 505,345 | |||||

5.5000%, 12/1/39 | 974,790 | 1,075,109 | |||||

5.5000%, 3/1/40 | 853,420 | 953,810 | |||||

5.5000%, 4/1/40 | 1,871,034 | 2,058,482 | |||||

5.5000%, 2/1/41 | 497,824 | 556,417 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

16 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Mortgage-Backed Securities – (continued) | |||||||

Fannie Mae Pool – (continued) | |||||||

5.0000%, 5/1/41 | $1,006,260 | $1,086,466 | |||||

5.5000%, 5/1/41 | 661,419 | 728,965 | |||||

5.5000%, 6/1/41 | 1,118,766 | 1,231,998 | |||||

5.5000%, 6/1/41 | 949,158 | 1,059,106 | |||||

5.5000%, 7/1/41 | 111,696 | 123,000 | |||||

5.5000%, 12/1/41 | 893,170 | 984,968 | |||||

5.5000%, 2/1/42 | 3,861,885 | 4,252,403 | |||||

4.5000%, 6/1/42 | 294,265 | 314,606 | |||||

4.5000%, 11/1/42 | 482,380 | 520,588 | |||||

3.5000%, 2/1/43 | 3,520,937 | 3,630,829 | |||||

3.5000%, 2/1/43 | 840,976 | 867,265 | |||||

3.5000%, 4/1/44 | 1,623,579 | 1,681,658 | |||||

5.5000%, 5/1/44 | 877,299 | 966,086 | |||||

5.0000%, 7/1/44 | 110,074 | 120,865 | |||||

4.5000%, 10/1/44 | 1,146,939 | 1,244,057 | |||||

3.5000%, 2/1/45 | 3,421,209 | 3,528,480 | |||||

4.5000%, 3/1/45 | 1,906,542 | 2,068,208 | |||||

4.5000%, 6/1/45 | 1,094,169 | 1,171,412 | |||||

4.5000%, 9/1/45 | 662,259 | 718,429 | |||||

3.0000%, 10/1/45 | 831,793 | 832,415 | |||||

3.0000%, 10/1/45 | 529,679 | 530,054 | |||||

3.5000%, 12/1/45 | 1,064,074 | 1,101,999 | |||||

3.0000%, 1/1/46 | 107,607 | 107,691 | |||||

3.5000%, 1/1/46 | 2,989,651 | 3,096,206 | |||||

3.5000%, 1/1/46 | 2,592,328 | 2,684,722 | |||||

3.0000%, 3/1/46 | 3,581,220 | 3,583,755 | |||||

3.0000%, 3/1/46 | 2,409,912 | 2,411,618 | |||||

4.0000%, 5/31/46 | 57,918,000 | 60,599,603 | |||||

3.5000%, 7/1/46 | 1,912,203 | 1,976,469 | |||||

3.5000%, 7/1/46 | 1,878,666 | 1,943,431 | |||||

4.5000%, 7/1/46 | 1,312,394 | 1,415,218 | |||||

3.5000%, 8/1/46 | 1,134,896 | 1,169,912 | |||||

4.0000%, 8/1/46 | 140,059 | 148,251 | |||||

4.0000%, 8/1/46 | 119,502 | 126,492 | |||||

4.0000%, 8/1/46 | 90,696 | 96,001 | |||||

4.0000%, 10/1/46 | 1,304,568 | 1,379,761 | |||||

3.0000%, 11/1/46 | 570,206 | 571,725 | |||||

3.0000%, 11/1/46 | 536,032 | 537,463 | |||||

4.5000%, 11/1/46 | 519,766 | 561,809 | |||||

3.5000%, 12/1/46 | 187,884 | 193,609 | |||||

3.5000%, 12/1/46 | 43,747 | 45,080 | |||||

4.5000%, 12/1/46 | 1,139,539 | 1,225,062 | |||||

3.5000%, 1/1/47 | 703,052 | 724,475 | |||||

3.5000%, 1/1/47 | 126,068 | 129,909 | |||||

3.5000%, 1/1/47 | 84,988 | 87,578 | |||||

3.0000%, 2/1/47 | 4,600,073 | 4,628,590 | |||||

4.5000%, 2/1/47 | 2,072,211 | 2,235,204 | |||||

4.0000%, 3/1/47 | 188,070 | 199,002 | |||||

4.0000%, 3/1/47 | 50,483 | 53,413 | |||||

4.0000%, 3/1/47 | 49,099 | 51,938 | |||||

4.0000%, 4/1/47 | 245,230 | 259,031 | |||||

4.0000%, 4/1/47 | 196,461 | 207,862 | |||||

4.0000%, 4/1/47 | 173,896 | 183,682 | |||||

4.0000%, 5/1/47 | 17,116,692 | 18,102,020 | |||||

4.0000%, 5/1/47 | 702,660 | 735,688 | |||||

4.0000%, 5/1/47 | 260,874 | 275,555 | |||||

4.0000%, 5/1/47 | 205,131 | 217,035 | |||||

4.0000%, 5/1/47 | 161,408 | 170,775 | |||||

4.0000%, 5/1/47 | 67,198 | 71,144 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

Janus Aspen Series | 17 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Mortgage-Backed Securities – (continued) | |||||||

Fannie Mae Pool – (continued) | |||||||

4.5000%, 5/1/47 | $342,595 | $370,901 | |||||

4.5000%, 5/1/47 | 282,107 | 304,391 | |||||

4.5000%, 5/1/47 | 276,870 | 298,334 | |||||

4.5000%, 5/1/47 | 208,517 | 225,828 | |||||

4.5000%, 5/1/47 | 194,023 | 209,064 | |||||

4.5000%, 5/1/47 | 169,769 | 183,705 | |||||

4.5000%, 5/1/47 | 95,555 | 103,257 | |||||

4.5000%, 5/1/47 | 69,065 | 74,808 | |||||

4.5000%, 5/1/47 | 62,530 | 67,658 | |||||

3.0000%, 5/31/47 | 1,317,000 | 1,315,463 | |||||

3.5000%, 5/31/47 | 12,877,000 | 13,207,416 | |||||

3.5000%, 6/1/47 | 134,722 | 138,862 | |||||

4.0000%, 6/1/47 | 757,670 | 800,308 | |||||

4.0000%, 6/1/47 | 416,242 | 436,714 | |||||

4.0000%, 6/1/47 | 372,301 | 393,735 | |||||

4.0000%, 6/1/47 | 361,797 | 382,793 | |||||

4.0000%, 6/1/47 | 356,559 | 374,647 | |||||

4.0000%, 6/1/47 | 291,818 | 309,182 | |||||

4.0000%, 6/1/47 | 176,158 | 184,823 | |||||

4.0000%, 6/1/47 | 169,054 | 177,369 | |||||

4.0000%, 6/1/47 | 133,488 | 141,381 | |||||

4.0000%, 6/1/47 | 110,163 | 116,345 | |||||

4.0000%, 6/1/47 | 80,141 | 83,926 | |||||

4.0000%, 6/1/47 | 48,009 | 51,008 | |||||

4.5000%, 6/1/47 | 1,284,099 | 1,383,646 | |||||

4.5000%, 6/1/47 | 119,517 | 129,454 | |||||

3.5000%, 7/1/47 | 264,946 | 273,235 | |||||

3.5000%, 7/1/47 | 159,546 | 164,615 | |||||

3.5000%, 7/1/47 | 118,404 | 122,417 | |||||

3.5000%, 7/1/47 | 72,213 | 74,583 | |||||

3.5000%, 7/1/47 | 71,539 | 74,018 | |||||

4.0000%, 7/1/47 | 3,114,793 | 3,295,990 | |||||

4.0000%, 7/1/47 | 777,501 | 821,255 | |||||

4.0000%, 7/1/47 | 598,492 | 632,173 | |||||

4.0000%, 7/1/47 | 559,273 | 591,472 | |||||

4.0000%, 7/1/47 | 307,225 | 324,436 | |||||

4.0000%, 7/1/47 | 299,500 | 317,091 | |||||

4.0000%, 7/1/47 | 230,261 | 243,876 | |||||

4.0000%, 7/1/47 | 165,312 | 175,021 | |||||

4.0000%, 7/1/47 | 143,812 | 150,886 | |||||

4.0000%, 7/1/47 | 142,897 | 151,290 | |||||

4.0000%, 7/1/47 | 91,691 | 96,342 | |||||

4.0000%, 7/1/47 | 81,130 | 85,478 | |||||

4.5000%, 7/1/47 | 912,604 | 983,352 | |||||

4.5000%, 7/1/47 | 814,580 | 877,729 | |||||

4.5000%, 7/1/47 | 788,518 | 849,650 | |||||

3.5000%, 8/1/47 | 985,567 | 1,013,013 | |||||

3.5000%, 8/1/47 | 623,072 | 642,332 | |||||

3.5000%, 8/1/47 | 569,732 | 587,833 | |||||

3.5000%, 8/1/47 | 137,688 | 142,003 | |||||

3.5000%, 8/1/47 | 119,462 | 123,257 | |||||

4.0000%, 8/1/47 | 1,641,064 | 1,718,654 | |||||

4.0000%, 8/1/47 | 1,352,162 | 1,416,094 | |||||

4.0000%, 8/1/47 | 1,303,807 | 1,377,180 | |||||

4.0000%, 8/1/47 | 1,280,292 | 1,352,341 | |||||

4.0000%, 8/1/47 | 794,010 | 838,693 | |||||

4.0000%, 8/1/47 | 592,576 | 626,872 | |||||

4.0000%, 8/1/47 | 557,718 | 586,010 | |||||

4.0000%, 8/1/47 | 343,681 | 362,004 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

18 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Mortgage-Backed Securities – (continued) | |||||||

Fannie Mae Pool – (continued) | |||||||

4.0000%, 8/1/47 | $244,692 | $259,161 | |||||

4.0000%, 8/1/47 | 148,450 | 155,477 | |||||

4.5000%, 8/1/47 | 1,110,684 | 1,196,793 | |||||

4.5000%, 8/1/47 | 211,510 | 227,907 | |||||

3.5000%, 9/1/47 | 3,685,976 | 3,788,811 | |||||

3.5000%, 9/1/47 | 579,820 | 599,506 | |||||

4.0000%, 9/1/47 | 1,462,408 | 1,544,708 | |||||

4.0000%, 9/1/47 | 938,584 | 991,405 | |||||

4.0000%, 9/1/47 | 153,063 | 161,677 | |||||

4.0000%, 9/1/47 | 85,744 | 90,753 | |||||

4.5000%, 9/1/47 | 5,382,493 | 5,733,395 | |||||

4.5000%, 9/1/47 | 1,106,210 | 1,191,975 | |||||

4.5000%, 9/1/47 | 826,667 | 890,756 | |||||

4.5000%, 9/1/47 | 724,531 | 780,703 | |||||

3.5000%, 10/1/47 | 5,921,599 | 6,086,959 | |||||

3.5000%, 10/1/47 | 2,413,032 | 2,480,414 | |||||

3.5000%, 10/1/47 | 203,414 | 210,014 | |||||

3.5000%, 10/1/47 | 180,434 | 186,560 | |||||

3.5000%, 10/1/47 | 144,581 | 149,312 | |||||

3.5000%, 10/1/47 | 84,754 | 87,835 | |||||

4.0000%, 10/1/47 | 1,383,693 | 1,454,254 | |||||

4.0000%, 10/1/47 | 644,136 | 680,385 | |||||

4.0000%, 10/1/47 | 632,158 | 669,289 | |||||

4.0000%, 10/1/47 | 619,358 | 654,214 | |||||

4.0000%, 10/1/47 | 415,046 | 438,403 | |||||

4.0000%, 10/1/47 | 327,117 | 346,331 | |||||

4.5000%, 10/1/47 | 171,659 | 184,968 | |||||

4.5000%, 10/1/47 | 79,622 | 85,795 | |||||

3.0000%, 11/1/47 | 1,402,820 | 1,403,813 | |||||

3.5000%, 11/1/47 | 388,861 | 402,426 | |||||

3.5000%, 11/1/47 | 243,346 | 251,844 | |||||

4.0000%, 11/1/47 | 935,046 | 982,481 | |||||

4.0000%, 11/1/47 | 290,302 | 306,995 | |||||

4.0000%, 11/1/47 | 151,465 | 160,456 | |||||

4.5000%, 11/1/47 | 850,406 | 916,335 | |||||

3.0000%, 12/1/47 | 608,000 | 608,430 | |||||

3.0000%, 12/1/47 | 295,000 | 295,209 | |||||

3.5000%, 12/1/47 | 812,000 | 838,947 | |||||

3.5000%, 12/1/47 | 167,000 | 172,542 | |||||

3.5000%, 5/1/56 | 4,534,004 | 4,665,753 | |||||

232,644,573 | |||||||

Freddie Mac Gold Pool: | |||||||

5.5000%, 10/1/36 | 400,212 | 447,739 | |||||

6.0000%, 4/1/40 | 2,098,685 | 2,415,846 | |||||

5.5000%, 8/1/41 | 2,058,086 | 2,330,874 | |||||

5.5000%, 8/1/41 | 1,318,904 | 1,476,704 | |||||

5.5000%, 9/1/41 | 284,678 | 311,697 | |||||

5.0000%, 3/1/42 | 1,017,338 | 1,116,037 | |||||

3.5000%, 2/1/44 | 1,316,059 | 1,356,516 | |||||

4.5000%, 5/1/44 | 52,144 | 56,132 | |||||

3.0000%, 1/1/45 | 1,198,481 | 1,200,480 | |||||

4.5000%, 6/1/46 | 2,783,025 | 2,997,950 | |||||

3.5000%, 7/1/46 | 3,717,617 | 3,852,388 | |||||

3.0000%, 10/1/46 | 4,512,070 | 4,522,223 | |||||

3.0000%, 12/1/46 | 4,556,636 | 4,566,897 | |||||

4.0000%, 6/1/47 | 2,954,822 | 3,123,904 | |||||

4.0000%, 8/1/47 | 2,904,237 | 3,041,149 | |||||

3.5000%, 9/1/47 | 3,535,392 | 3,648,280 | |||||

3.5000%, 9/1/47 | 2,571,010 | 2,645,459 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

Janus Aspen Series | 19 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Mortgage-Backed Securities – (continued) | |||||||

Freddie Mac Gold Pool – (continued) | |||||||

3.5000%, 9/1/47 | $1,473,707 | $1,516,379 | |||||

3.5000%, 9/1/47 | 1,168,345 | 1,202,178 | |||||

3.5000%, 9/1/47 | 1,137,665 | 1,176,190 | |||||

4.0000%, 9/1/47 | 1,329,011 | 1,390,437 | |||||

3.5000%, 10/1/47 | 3,138,219 | 3,229,091 | |||||

3.5000%, 10/1/47 | 1,808,364 | 1,860,729 | |||||

3.5000%, 12/1/47 | 4,733,766 | 4,892,610 | |||||

54,377,889 | |||||||

Ginnie Mae I Pool: | |||||||

4.0000%, 1/15/45 | 4,112,713 | 4,319,794 | |||||

4.5000%, 8/15/46 | 4,782,838 | 5,150,843 | |||||

4.0000%, 7/15/47 | 3,706,110 | 3,888,237 | |||||

4.0000%, 8/15/47 | 746,728 | 783,481 | |||||

14,142,355 | |||||||

Ginnie Mae II Pool: | |||||||

4.5000%, 10/20/41 | 1,200,851 | 1,261,498 | |||||

4.0000%, 8/20/47 | 391,534 | 411,254 | |||||

4.0000%, 8/20/47 | 184,469 | 193,760 | |||||

4.0000%, 8/20/47 | 93,490 | 98,199 | |||||

1,964,711 | |||||||

Total Mortgage-Backed Securities (cost $304,885,842) | 303,129,528 | ||||||

United States Treasury Notes/Bonds – 8.0% | |||||||

1.2500%, 6/30/19 | 1,308,000 | 1,296,304 | |||||

1.3750%, 7/31/19 | 320,000 | 317,561 | |||||

1.2500%, 8/31/19 | 12,278,000 | 12,151,703 | |||||

1.3750%, 9/30/19 | 17,675,000 | 17,520,645 | |||||

1.5000%, 10/31/19 | 16,104,000 | 15,991,351 | |||||

1.7500%, 11/30/19 | 56,812,000 | 56,666,419 | |||||

1.6250%, 10/15/20 | 4,349,000 | 4,310,040 | |||||

1.7500%, 11/15/20 | 18,167,000 | 18,061,149 | |||||

1.8750%, 9/30/22 | 5,452,000 | 5,372,333 | |||||

2.0000%, 11/30/22 | 1,779,000 | 1,762,558 | |||||

2.0000%, 5/31/24 | 8,050,000 | 7,897,888 | |||||

2.1250%, 9/30/24 | 1,619,000 | 1,598,255 | |||||

2.2500%, 2/15/27 | 2,845,000 | 2,806,816 | |||||

2.2500%, 8/15/27 | 7,629,000 | 7,519,343 | |||||

2.2500%, 11/15/27 | 53,707,000 | 52,932,535 | |||||

2.2500%, 8/15/46 | 16,454,000 | 14,825,437 | |||||

3.0000%, 2/15/47 | 1,105,000 | 1,160,827 | |||||

3.0000%, 5/15/47 | 5,919,000 | 6,216,185 | |||||

2.7500%, 8/15/47 | 13,781,000 | 13,782,737 | |||||

2.7500%, 11/15/47 | 22,867,000 | 22,878,777 | |||||

Total United States Treasury Notes/Bonds (cost $264,287,955) | 265,068,863 | ||||||

Common Stocks – 62.0% | |||||||

Aerospace & Defense – 4.4% | |||||||

Boeing Co | 289,690 | 85,432,478 | |||||

General Dynamics Corp† | 144,086 | 29,314,297 | |||||

Northrop Grumman Corp | 101,335 | 31,100,725 | |||||

145,847,500 | |||||||

Air Freight & Logistics – 0.6% | |||||||

United Parcel Service Inc | 178,897 | 21,315,578 | |||||

Automobiles – 1.0% | |||||||

General Motors Co | 812,944 | 33,322,575 | |||||

Banks – 1.9% | |||||||

US Bancorp | 1,146,685 | 61,439,382 | |||||

Beverages – 0.6% | |||||||

Dr Pepper Snapple Group Inc | 207,075 | 20,098,699 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

20 | DECEMBER 31, 2017 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Common Stocks – (continued) | |||||||

Biotechnology – 1.9% | |||||||

AbbVie Inc | 80,197 | $7,755,852 | |||||

Amgen Inc | 321,831 | 55,966,411 | |||||

63,722,263 | |||||||

Capital Markets – 3.9% | |||||||

Blackstone Group LP | 632,543 | 20,254,027 | |||||

CME Group Inc | 447,600 | 65,371,980 | |||||

Morgan Stanley | 216,067 | 11,337,035 | |||||

TD Ameritrade Holding Corp | 645,301 | 32,994,240 | |||||

129,957,282 | |||||||

Chemicals – 1.9% | |||||||

LyondellBasell Industries NV | 576,948 | 63,648,903 | |||||

Consumer Finance – 1.6% | |||||||

American Express Co | 174,729 | 17,352,337 | |||||

Synchrony Financial | 948,449 | 36,619,616 | |||||

53,971,953 | |||||||

Equity Real Estate Investment Trusts (REITs) – 1.6% | |||||||

Colony NorthStar Inc | 1,216,682 | 13,882,342 | |||||

Crown Castle International Corp | 140,945 | 15,646,304 | |||||

Invitation Homes Inc | 167,730 | 3,953,396 | |||||

MGM Growth Properties LLC | 331,181 | 9,653,926 | |||||

Outfront Media Inc | 461,539 | 10,707,705 | |||||

53,843,673 | |||||||

Food & Staples Retailing – 3.1% | |||||||

Costco Wholesale Corp | 265,431 | 49,402,018 | |||||

Kroger Co† | 757,339 | 20,788,956 | |||||

Sysco Corp | 518,606 | 31,494,942 | |||||

101,685,916 | |||||||

Food Products – 0.7% | |||||||

Hershey Co | 193,025 | 21,910,268 | |||||

Health Care Equipment & Supplies – 2.3% | |||||||

Abbott Laboratories | 560,904 | 32,010,791 | |||||

Medtronic PLC | 529,995 | 42,797,096 | |||||

74,807,887 | |||||||

Health Care Providers & Services – 0.8% | |||||||

Aetna Inc | 153,095 | 27,616,807 | |||||

Hotels, Restaurants & Leisure – 2.0% | |||||||

McDonald's Corp | 123,127 | 21,192,619 | |||||

Norwegian Cruise Line Holdings Ltd* | 191,941 | 10,220,858 | |||||

Six Flags Entertainment Corp | 200,378 | 13,339,163 | |||||

Starbucks Corp | 363,596 | 20,881,318 | |||||

65,633,958 | |||||||

Household Products – 0.3% | |||||||

Kimberly-Clark Corp | 73,033 | 8,812,162 | |||||

Industrial Conglomerates – 1.8% | |||||||

Honeywell International Inc | 379,502 | 58,200,427 | |||||

Information Technology Services – 3.9% | |||||||

Accenture PLC | 204,401 | 31,291,749 | |||||

Automatic Data Processing Inc | 73,938 | 8,664,794 | |||||

Mastercard Inc | 597,490 | 90,436,086 | |||||

130,392,629 | |||||||

Insurance – 0.6% | |||||||

Progressive Corp | 323,761 | 18,234,220 | |||||

Internet & Direct Marketing Retail – 1.3% | |||||||

Priceline Group Inc* | 25,280 | 43,930,067 | |||||

Internet Software & Services – 2.3% | |||||||

Alphabet Inc - Class C* | 73,222 | 76,619,501 | |||||

Leisure Products – 0.6% | |||||||

Hasbro Inc | 167,700 | 15,242,253 | |||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

Janus Aspen Series | 21 |

Janus Henderson VIT Balanced Portfolio

Schedule of Investments

December 31, 2017

Shares

or | Value | ||||||

Common Stocks – (continued) | |||||||

Leisure Products – (continued) | |||||||

Mattel Inc | 290,043 | $4,460,861 | |||||

19,703,114 | |||||||

Machinery – 0.4% | |||||||

Deere & Co | 90,881 | 14,223,785 | |||||

Media – 1.8% | |||||||

Comcast Corp | 1,291,420 | 51,721,371 | |||||

Madison Square Garden Co* | 32,179 | 6,784,942 | |||||

58,506,313 | |||||||

Oil, Gas & Consumable Fuels – 1.1% | |||||||

Suncor Energy Inc | 568,972 | 20,892,652 | |||||

Suncor Energy Inc¤ | 468,279 | 17,195,318 | |||||

38,087,970 | |||||||

Personal Products – 0.8% | |||||||

Estee Lauder Cos Inc | 196,469 | 24,998,716 | |||||

Pharmaceuticals – 2.1% | |||||||

Allergan PLC | 164,263 | 26,870,142 | |||||

Bristol-Myers Squibb Co | 259,444 | 15,898,728 | |||||

Eli Lilly & Co | 221,733 | 18,727,569 | |||||

Merck & Co Inc | 163,289 | 9,188,272 | |||||

70,684,711 | |||||||

Real Estate Investment Trusts (REITs) – 0% | |||||||

Colony American Homes III (144A)¢,§ | 639,963 | 41,108 | |||||

Real Estate Management & Development – 0.8% | |||||||

CBRE Group Inc* | 649,991 | 28,151,110 | |||||

Road & Rail – 1.4% | |||||||

CSX Corp | 823,966 | 45,326,370 | |||||

Semiconductor & Semiconductor Equipment – 2.1% | |||||||

Intel Corp | 922,077 | 42,563,074 | |||||

Lam Research Corp | 151,611 | 27,907,037 | |||||

70,470,111 | |||||||

Software – 5.6% | |||||||

Activision Blizzard Inc | 120,144 | 7,607,518 | |||||

Adobe Systems Inc* | 303,516 | 53,188,144 | |||||

Microsoft Corp | 1,363,891 | 116,667,237 | |||||

salesforce.com Inc* | 96,027 | 9,816,840 | |||||

187,279,739 | |||||||

Specialty Retail – 1.9% | |||||||

Home Depot Inc | 332,968 | 63,107,425 | |||||

Technology Hardware, Storage & Peripherals – 1.8% | |||||||

Apple Inc | 353,697 | 59,856,143 | |||||

Textiles, Apparel & Luxury Goods – 1.0% | |||||||