UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________________________________________

FORM 10-K

_____________________________________________________________

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-12378

_________________________________________________

NVR, Inc.

(Exact Name of Registrant as Specified in its Charter)

_____________________________________________________________

Virginia | 54-1394360 | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification Number) | |

11700 Plaza America Drive, Suite 500 Reston, Virginia | 20190 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (703) 956-4000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common stock, par value $0.01 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

_____________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☒ | Accelerated filer | ☐ | |

Non-accelerated filer | ☐ | (Do not check if a smaller reporting company) | Smaller reporting company | ☐ |

Emerging growth company | ☐ | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting stock held by non-affiliates of NVR, Inc. on June 30, 2017, the last business day of NVR, Inc.’s most recently completed second fiscal quarter, was approximately $8,443,210,000.

As of February 12, 2018 there were 3,683,093 total shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement of NVR, Inc. to be filed with the Securities and Exchange Commission pursuant to Regulation 14A of the Securities Exchange Act of 1934 on or prior to April 30, 2018 are incorporated by reference into Part III of this report.

NVR, Inc.

Form 10-K

TABLE OF CONTENTS

Page | ||

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

PART I

Item 1. Business.

General

NVR, Inc., a Virginia corporation, was formed in 1980 as NVHomes, Inc. Our primary business is the construction and sale of single-family detached homes, townhomes and condominium buildings, all of which are primarily constructed on a pre-sold basis. To more fully serve customers of our homebuilding operations, we also operate a mortgage banking and title services business. We conduct our homebuilding activities directly. Our mortgage banking operations are operated primarily through a wholly owned subsidiary, NVR Mortgage Finance, Inc. (“NVRM”). Unless the context otherwise requires, references to “NVR”, “we”, “us” or “our” include NVR, Inc. and its consolidated subsidiaries.

We are one of the largest homebuilders in the United States. We operate in multiple locations in fourteen states, which are primarily in the eastern part of the country, and in Washington, D.C. During 2017, approximately 23% and 9% of our home settlements occurred in the Washington, D.C. and Baltimore, MD metropolitan areas, respectively, which accounted for approximately 30% and 11%, respectively, of our 2017 homebuilding revenues. Our homebuilding operations include the construction and sale of single-family detached homes, townhomes and condominium buildings under three trade names: Ryan Homes, NVHomes and Heartland Homes. Our Ryan Homes product is marketed primarily to first-time and first-time move-up buyers. Ryan Homes operates in twenty-nine metropolitan areas located in Maryland, Virginia, Washington, D.C., West Virginia, Pennsylvania, New York, North Carolina, South Carolina, Florida, Ohio, New Jersey, Delaware, Indiana, Illinois and Tennessee. Our NVHomes and Heartland Homes products are marketed primarily to move-up and luxury buyers. NVHomes operates in Delaware and the Washington, D.C., Baltimore, MD, Philadelphia, PA and Raleigh, NC metropolitan areas. Heartland Homes operates in the Pittsburgh, PA metropolitan area.

We generally do not engage in land development (see discussion below of our land development activities). Instead, we typically acquire finished building lots at market prices from various third party land developers pursuant to fixed price finished lot purchase agreements (“Lot Purchase Agreements”) that require deposits that may be forfeited if we fail to perform under the Lot Purchase Agreements. The deposits required under the Lot Purchase Agreements are in the form of cash or letters of credit in varying amounts and typically range up to 10% of the aggregate purchase price of the finished lots.

We believe that our lot acquisition strategy avoids the financial requirements and risks associated with direct land ownership and land development. We may, at our option, choose for any reason and at any time not to perform under these Lot Purchase Agreements by delivering notice of our intent not to acquire the finished lots under contract. Our sole legal obligation and economic loss for failure to perform under these Lot Purchase Agreements is limited to the amount of the deposit pursuant to the liquidated damage provision contained within the Lot Purchase Agreements. We do not have any financial guarantees or completion obligations and we typically do not guarantee lot purchases on a specific performance basis under these Lot Purchase Agreements. None of the creditors of any of the development entities with which we have entered these Lot Purchase Agreements have recourse to our general credit. We generally seek to maintain control over a supply of lots believed to be suitable to meet our five-year business plan.

In addition to constructing homes primarily on a pre-sold basis and utilizing what we believe is a conservative lot acquisition strategy, we focus on obtaining and maintaining a leading market position in each market we serve. This strategy allows us to gain valuable efficiencies and competitive advantages in our markets, which we believe contributes to minimizing the adverse effects of regional economic cycles and provides growth opportunities within these markets. Our continued success is contingent upon our ability to control an adequate supply of finished lots on which to build. As a result, in certain specific strategic circumstances we deviate from our historical lot acquisition strategy and engage in joint venture arrangements with land developers or directly acquire raw ground already zoned for its intended use for development. Once we acquire control of raw ground, we determine whether to sell the raw parcel to a developer and enter into a Lot Purchase Agreement with the developer to purchase the finished lots or hire a developer to develop the land on our behalf. While joint venture arrangements and direct land development activity are not our preferred method of acquiring finished building lots, we may enter into additional transactions in the future on a limited basis where there exists a compelling strategic or prudent financial reason to do so. We expect, however, to continue to acquire substantially all of our finished lot inventory using Lot Purchase Agreements with forfeitable deposits. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of this Form 10-K for additional discussion of lots controlled. In addition, see Notes 3, 4 and 5 in the accompanying consolidated financial statements included herein for additional information regarding Lot Purchase Agreements, joint ventures and land under development, respectively.

In addition to building and selling homes, we provide a number of mortgage-related services through our mortgage banking operations. Through operations in each of our homebuilding markets, NVRM originates mortgage loans almost exclusively for our homebuyers. NVRM generates revenues primarily from origination fees, gains on sales of loans and title fees. NVRM sells all of the mortgage loans it closes into the secondary markets on a servicing released basis.

Segment information for our homebuilding and mortgage banking businesses is included in Note 2 in the accompanying consolidated financial statements.

1

Current Business Environment

During 2017, we continued to experience improving new home demand as a result of favorable market conditions, including low mortgage interest rates, low unemployment and improved consumer confidence. However, new home prices continued to be constrained due to the competitive market environment. We believe that a continuation of the housing market recovery is dependent upon sustained economic growth, driven by continued improvements in job and wage growth and household formation. For additional information and analysis of recent trends in our operations and financial condition, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of this Form 10-K.

Homebuilding

Products

We offer single-family detached homes, townhomes and condominium buildings with many different basic home designs. These home designs have a variety of elevations and numerous other options. Our homes combine traditional, transitional, cottage or urban exterior designs with contemporary interior designs and amenities, generally include two to four bedrooms and range from approximately 1,000 to 9,500 finished square feet. During 2017, the prices at which we settled homes ranged from approximately $130,000 to $2.0 million and averaged approximately $386,900. During 2016, our average price of homes settled was approximately $381,200.

Markets

Our four reportable homebuilding segments operate in the following geographic regions:

Mid Atlantic: | Maryland, Virginia, West Virginia, Delaware and Washington, D.C. | |

North East: | New Jersey and Eastern Pennsylvania | |

Mid East: | New York, Ohio, Western Pennsylvania, Indiana and Illinois | |

South East: | North Carolina, South Carolina, Florida and Tennessee | |

Backlog

Backlog, which represents homes sold but not yet settled with the customer, totaled 8,531 units and approximately $3.3 billion at December 31, 2017 compared to 6,884 units and approximately $2.7 billion at December 31, 2016. Backlog may be impacted by customer cancellations for various reasons that are beyond our control, such as the customer’s failure to obtain mortgage financing, inability to sell an existing home, job loss or a variety of other reasons. In any period, a portion of the cancellations that we experience are related to new sales that occurred during the same period, and a portion are related to sales that occurred in prior periods and therefore appeared in the opening backlog for the current period. Expressed as the total of all cancellations during the period as a percentage of gross sales during the period, our cancellation rate was approximately 14% in 2017 and 15% in both 2016 and 2015. Additionally, during each of 2017, 2016 and 2015, approximately 6% of a reporting quarter’s opening backlog balance cancelled during the quarter. We can provide no assurance that our historical cancellation rates are indicative of the actual cancellation rate that may occur in future periods. Other than those units that are cancelled, we expect to settle substantially all of our December 31, 2017 backlog during 2018. See “Risk Factors” in Item 1A and “Seasonality” in Item 7 of this Form 10-K.

Further discussion of settlements, new orders and backlog activity by our homebuilding reportable segment for each of the last three years can be found in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of this Form 10-K.

Construction

We utilize independent subcontractors under fixed price contracts to perform construction work on our homes. We use several independent subcontractors in our various markets and we are not dependent on any single subcontractor or on a small number of subcontractors.

Sales and Marketing

Our preferred marketing method is for customers to visit a furnished model home featuring many built-in options and a landscaped lot. The garages of these model homes are usually converted into temporary sales centers where alternative facades and floor plans are displayed and designs for other models are available for review. Sales representatives are compensated predominantly on a commission basis.

Regulation

We and our subcontractors must comply with various federal, state and local zoning, building, environmental, advertising and consumer credit statutes, rules and regulations, as well as other regulations and requirements in connection with our construction and sales activities. All of these regulations have increased the cost to produce and market our products, and in some instances, have delayed our developers’ ability to deliver finished lots to us. Counties and cities in which we build homes have at times declared moratoriums on the issuance of building permits and imposed other restrictions in the areas in which sewage treatment facilities and

2

other public facilities do not reach minimum standards. In addition, our homebuilding operations are regulated in certain areas by restrictive zoning and density requirements that limit the number of homes that can be built within the boundaries of a particular area. To date, restrictive zoning laws and the imposition of moratoriums have not had a material adverse effect on our construction activities.

Competition and Market Factors

The housing industry is highly competitive. We compete with numerous homebuilders of varying size, ranging from local to national in scope, some of which have greater financial resources than we do. We also face competition from the home resale market. Our homebuilding operations compete primarily on the basis of price, location, design, quality, service and reputation. Historically, we have been one of the market leaders in each of the markets where we build homes.

The housing industry is cyclical and is affected by consumer confidence levels, prevailing economic conditions and interest rates. Other factors that affect the housing industry and the demand for new homes include: the availability and the cost of land, labor and materials; changes in consumer preferences; demographic trends; and the availability of mortgage finance programs. See “Risk Factors” in Item 1A of this Form 10-K for additional information regarding these risks.

We are dependent upon building material suppliers for a continuous flow of raw materials. Whenever possible, we utilize standard products available from multiple sources. In the past, such raw materials have been generally available to us in adequate supply.

Mortgage Banking

We provide a number of mortgage related services to our homebuilding customers through our mortgage banking operations. Our mortgage banking operations also include separate subsidiaries that broker title insurance and perform title searches in connection with mortgage loan closings for which they receive commissions and fees. Because NVRM originates mortgage loans almost exclusively for our homebuilding customers, NVRM is dependent on our homebuilding segment. In 2017, NVRM closed approximately 13,100 loans with an aggregate principal amount of approximately $4.2 billion as compared to approximately 12,300 loans with an aggregate principal amount of approximately $4.0 billion in 2016.

NVRM sells all of the mortgage loans it closes to investors in the secondary markets on a servicing released basis, typically within 30 days from the loan closing. NVRM is an approved seller/servicer for Fannie Mae (“FNMA”) and Freddie Mac ("FHLMC") mortgage loans and an approved seller/issuer of Ginnie Mae (“GNMA”), Department of Veterans Affairs (“VA”) and Federal Housing Administration (“FHA”) mortgage loans.

Regulation

NVRM is subject to the rules and regulations of FNMA, GNMA, FHLMC, VA and FHA. These rules and regulations restrict certain activities of NVRM. NVRM is currently eligible and expects to remain eligible to participate in such programs. In addition, NVRM is subject to regulation at the state and federal level, including regulations issued by the Consumer Financial Protection Bureau (the “CFPB”) with respect to specific origination, selling and servicing practices.

Competition and Market Factors

NVRM’s main competition comes from national, regional, and local mortgage bankers, mortgage brokers, credit unions and banks in each of these markets. NVRM competes primarily on the basis of customer service, variety of products offered, interest rates offered, prices of ancillary services and relative financing availability and costs.

Pipeline

NVRM’s mortgage loans in process that had not closed at December 31, 2017 and 2016 had an aggregate principal balance of approximately $2.2 billion and $1.8 billion, respectively. NVRM’s cancellation rate was approximately 31%, 34% and 29% in 2017, 2016 and 2015, respectively. We can provide no assurance that our historical loan cancellation rates are indicative of the actual loan cancellation rate that may occur in future periods. See “Risk Factors” in Item 1A in this Form 10-K for additional information about factors that could increase our cancellation rate.

Employees

At December 31, 2017, we employed approximately 5,200 full-time persons. None of our employees are subject to a collective bargaining agreement and we have never experienced a work stoppage. We believe that our employee relations are good.

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission (the “SEC”). These filings are available to the public over the internet at the SEC’s website at http://www.sec.gov. All of the documents we file with the SEC may also be read and copied at the SEC’s Public Reference Room located at 100 F Street, NE, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the Public Reference Room.

3

Our principal internet website can be found at http://www.nvrinc.com. We make available free of charge on or through our website, access to our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after such material is electronically filed, or furnished, to the SEC.

Our website also includes a corporate governance section which contains our Corporate Governance Guidelines (which includes our Directors’ Independence Standards), Code of Ethics, Board Committee Charters, Policies and Procedures for the Consideration of Board of Director Candidates, and Policies and Procedures Regarding Communications with the NVR, Inc. Board of Directors, the Independent Lead Director and the Non-Management Directors as a Group. Additionally, amendments to and waivers from a provision of the Code of Ethics that apply to our principal executive officer, principal financial officer, principal accounting officer or persons performing similar functions will be disclosed on our website.

Forward-Looking Statements

Some of the statements in this Form 10-K, as well as statements made by us in periodic press releases or other public communications, constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Certain, but not necessarily all, of such forward-looking statements can be identified by the use of forward-looking terminology, such as “believes,” “expects,” “may,” “will,” “should,” or “anticipates” or the negative thereof or other comparable terminology. All statements other than of historical facts are forward looking statements. Forward-looking statements contained in this document include those regarding market trends, NVR’s financial position, business strategy, the outcome of pending litigation, investigations or similar contingencies, projected plans and objectives of management for future operations. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results or performance of NVR to be materially different from future results, performance or achievements expressed or implied by the forward-looking statements. Such risk factors include, but are not limited to the following: general economic and business conditions (on both a national and regional level); interest rate changes; access to suitable financing by NVR and NVR’s customers; increased regulation in the mortgage banking industry; the ability of our mortgage banking subsidiary to sell loans it originates into the secondary market; competition; the availability and cost of land and other raw materials used by NVR in its homebuilding operations; shortages of labor; weather related slow-downs; building moratoriums; governmental regulation; fluctuation and volatility of stock and other financial markets; mortgage financing availability; and other factors over which NVR has little or no control. NVR undertakes no obligation to update such forward-looking statements except as required by law.

Item 1A. Risk Factors.

Our business is affected by the risks generally incident to the residential construction business, including, but not limited to:

• | actual and expected direction of interest rates, which affect our costs, the availability of construction financing, and long-term financing for potential purchasers of homes; |

• | the availability of mortgage financing; |

• | the availability of adequate land in desirable locations on favorable terms; |

• | unexpected changes in customer preferences; and |

• | changes in the national economy and in the local economies of the markets in which we operate. |

All of these risks are discussed in detail below.

An economic downturn or decline in economic conditions could adversely affect our business and our results of operations.

Demand for new homes is sensitive to economic changes driven by conditions such as employment levels, job growth, consumer confidence and interest rates. If the housing industry suffers a downturn, our sales may decline which could have a material adverse effect on our profitability, stock performance, ability to service our debt obligations and future cash flows.

Interest rate movements, inflation and other economic factors can negatively impact our business.

High rates of inflation generally affect the homebuilding industry adversely because of their adverse impact on interest rates. High interest rates not only increase the cost of borrowed funds to homebuilders but also have a significant adverse effect on housing demand and on the affordability of permanent mortgage financing to prospective purchasers. We are also subject to potential volatility in the price of commodities that impact costs of materials used in our homebuilding business. Increases in prevailing interest rates could have a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

Our financial results also are affected by the risks generally incident to our mortgage banking business, including interest rate levels, the impact of government regulation on mortgage loan originations and servicing and the need to issue forward commitments to fund and sell mortgage loans. Our homebuilding customers account for almost all of our mortgage banking business. The volume of our continuing homebuilding operations therefore affects our mortgage banking business.

4

Our mortgage banking business also is affected by interest rate fluctuations. We also may experience marketing losses resulting from daily increases in interest rates to the extent we are unable to match interest rates and amounts on loans we have committed to originate with forward commitments from third parties to purchase such loans. Increases in interest rates may have a material adverse effect on our mortgage banking revenue, profitability, stock performance, ability to service our debt obligations and future cash flows.

Our operations may also be adversely affected by other economic factors within our markets such as negative changes in employment levels, job growth, wage growth, consumer confidence and household formation and availability of mortgage financing, one or all of which could result in reduced demand or price depression from current levels. Such negative trends could have a material adverse effect on homebuilding operations.

These factors and thus, the homebuilding and mortgage banking businesses, have at times in the past been cyclical in nature. Any downturn in the national economy or the local economies of the markets in which we operate could have a material adverse effect on our sales, profitability, stock performance and ability to service our debt obligations. In particular, during 2017, approximately 23% and 9% of our home settlements occurred in the Washington, D.C. and Baltimore, MD metropolitan areas, respectively, which accounted for approximately 30% and 11%, respectively, of our 2017 homebuilding revenues. Thus, we are dependent to a significant extent on the economy and demand for housing in those areas.

Because almost all of our customers require mortgage financing, the availability of suitable mortgage financing could impair the affordability of our homes, lower demand for our products, and limit our ability to fully deliver our backlog.

Our business and earnings depend on the ability of our potential customers to obtain mortgages for the purchase of our homes. In addition, many of our potential customers must sell their existing homes in order to buy a home from us. The tightening of credit standards and the availability of suitable mortgage financing could prevent customers from buying our homes and could prevent buyers of our customers’ homes from obtaining mortgages they need to complete that purchase, either of which could result in potential customers’ inability to buy a home from us. If potential customers or the buyers of our customers’ current homes are not able to obtain suitable financing, the result could have a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

If our ability to sell mortgages to investors is impaired, we may be required to fund these commitments ourselves, or we may not be able to originate loans at all.

Our mortgage banking business sells all of the loans it originates into the secondary market, usually within 30 days from the date of closing, and has up to $150 million available under a repurchase agreement to fund mortgage closings. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources” in Item 7 of this Form 10-K for more information about the repurchase agreement. In the event that disruptions to the secondary markets tighten or eliminate the available liquidity within the secondary markets for mortgage loans, or the underwriting requirements by our secondary market investors continue to become more stringent, our ability to sell future mortgages could decline and we could be required, among other things, to fund our commitments to our buyers with our own financial resources, which is limited, or require our home buyers to find another source of financing. The result of such secondary market disruption could have a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

If the market value of our inventory or controlled lot position declines, our profit could decrease and we may incur losses.

Inventory risk can be substantial for homebuilders. The market value of building lots and housing inventories can fluctuate significantly as a result of changing market conditions. In addition, inventory carrying costs can be significant and can result in losses in a poorly performing project or market. We must continuously seek and make acquisitions of lots for expansion into new markets as well as for replacement and expansion within our current markets, which we generally accomplish by entering into Lot Purchase Agreements and paying forfeitable deposits under the Lot Purchase Agreements to developers for the contractual right to acquire the lots. In the event of adverse changes in economic, market or project conditions, we may cease further building activities in certain communities or restructure existing Lot Purchase Agreements, resulting in forfeiture of some or all of any remaining land contract deposit paid to the developer. We may also have significant impairments of land under development. The forfeiture of land contract deposits or inventory impairments may result in a loss that could have a material adverse effect on our profitability, stock performance, ability to service our debt obligations and future cash flows.

If the underwriting quality of our mortgage originations is found to be deficient, our profit could decrease and we may incur losses.

We originate several different loan products to our customers to finance the purchase of their home. We sell all of the loans we originate into the secondary mortgage market generally within 30 days from the date of closing. All of the loans that we originate are underwritten to the standards and specifications of the ultimate investor. Insofar as we underwrite our originated loans to those standards, we bear no increased concentration of credit risk from the issuance of loans, except in certain limited instances where early payment default occurs. In the event that a substantial number of the loans that we have originated fall into default and the investors to whom we sold the loans determine that we did not underwrite the loans in accordance with their requirements, we could be required to repurchase the loans from the investor or indemnify the investor for any losses incurred. Any resulting losses could have a material adverse effect on our profitability, stock performance, ability to service our debt obligations and future cash flows.

5

We may be subject to claims on mortgage loans sold to third parties.

Our mortgage banking operations may be responsible for losses associated with mortgage loans originated and sold to investors in the event of errors or omissions relating to certain representations and warranties that the loans sold meet certain requirements, including representations as to underwriting standards, the type of collateral, the existence of primary mortgage insurance, and the validity of certain borrower representations in connection with the loan. The resolution of claims related to alleged breaches of these representations and warranties and repurchase claims could have a material adverse effect on our financial condition, cash flows and results of operations and could result in losses that exceed existing estimates and accruals. Because of the uncertainties inherent in estimating these matters, there can be no assurance that any amounts reserved will be adequate or that any potential inadequacies will not have a material adverse effect on our results of operations.

Our inability to secure and control an adequate inventory of lots could adversely impact our operations.

The results of our homebuilding operations depend upon our continuing ability to control an adequate number of homebuilding lots in desirable locations. There can be no assurance that an adequate supply of building lots will continue to be available to us on terms similar to those available in the past, or that we will not be required to devote a greater amount of capital to controlling building lots than we have historically. An insufficient supply of building lots in one or more of our markets, an inability of our developers to deliver finished lots in a timely fashion due to their inability to secure financing to fund development activities or for other reasons, or our inability to purchase or finance building lots on reasonable terms could have a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

Volatility in the credit and capital markets may impact our ability to access necessary financing.

If we require working capital greater than that provided by our operations and our credit facility, we may be required to seek to increase the amount available under the facility or seek alternative financing, which might not be available on terms that are favorable or acceptable. If we are required to seek financing to fund our working capital requirements, volatility in credit or capital markets may restrict our flexibility to access financing. If we are at any time unsuccessful in obtaining sufficient capital to fund our planned homebuilding expenditures, we may experience a substantial delay in the completion of homes then under construction, or we may be unable to control or purchase finished building lots. Any delay could result in cost increases and could have a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

Our mortgage banking operations depend in part on the availability, cost and other terms of mortgage financing facilities, and may be adversely affected by any shortage or increased cost of such financing. Additional or replacement financing might not be available on terms that are favorable or acceptable. Our mortgage banking operations are also dependent upon the securitization market for mortgage-backed securities, and could be materially adversely affected by any fluctuation or downturn in such market.

Our current indebtedness may impact our future operations.

Our existing indebtedness contains restrictive covenants and any future indebtedness may also contain such covenants. These covenants include, or could include, restrictions on our ability to create, incur, assume or guarantee secured debt, enter into sale and leaseback transactions and conditions related to mergers and/or the sale of assets. Substantial losses by us or other action or inaction by us or our subsidiaries could result in the violation of one or more of these covenants, which could result in decreased liquidity or a default on our current or future indebtedness, thereby having a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

Government regulations and environmental matters could negatively affect our operations.

We are subject to various local, state and federal statutes, ordinances, rules and regulations concerning zoning, building design, construction and similar matters, including local regulations that impose restrictive zoning and density requirements in order to limit the number of homes that can eventually be built within the boundaries of a particular area. These regulations may further increase the cost to produce and market our products. In addition, we have from time to time been subject to, and may also be subject in the future to, periodic delays in our homebuilding projects due to building moratoriums in the areas in which we operate or delays in receiving the necessary governmental approvals. Changes in regulations that restrict homebuilding activities in one or more of our principal markets could have a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

In addition, new housing developments are often subject to various assessments or impact fees for schools, parks, streets, highways and other public improvements. The cost of these assessments is subject to substantial change and could cause increases in the construction cost of our homes, which, in turn, could reduce our profitability.

We are also subject to a variety of local, state and federal statutes, ordinances, rules and regulations concerning the protection of health and the environment. We are subject to a variety of environmental conditions that can affect our business and our homebuilding projects. The particular environmental laws that apply to any given homebuilding site vary greatly according to the location and environmental condition of the site and the present and former uses of the site and adjoining properties. Environmental laws and conditions may result in delays, cause us to incur substantial compliance and other costs, or prohibit or severely restrict

6

homebuilding activity in certain environmentally sensitive regions or areas, thereby adversely affecting our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

Increased regulation of the mortgage industry could harm our future sales and earnings.

The mortgage industry remains under intense scrutiny and continues to face increasing regulation at the federal, state and local level. Potential changes to federal laws and regulations could have the effect of limiting the activities of FNMA and FHLMC, the entities that provide liquidity to the secondary mortgage market, which could lead to increases in mortgage interest rates. Tighter underwriting requirements and fee restrictions and the increasingly complex regulatory environment may negatively impact our mortgage loan origination business in the form of lower demand, decreased revenue and increased operating costs.

We are an approved seller/servicer of FNMA and FHLMC mortgage loans and an approved seller/issuer of GNMA, VA and FHA mortgage loans, and are subject to all of those agencies’ rules and regulations. Any significant impairment of our eligibility to sell/service these loans could have a material adverse impact on our mortgage operations. In addition, we are subject to regulation at the state and federal level with respect to specific origination, selling and servicing practices including the Real Estate Settlement and Protection Act. Adverse changes in governmental regulation may have a negative impact on our mortgage loan origination business.

We face competition in our homebuilding and mortgage banking operations.

The homebuilding industry is highly competitive. We compete with numerous homebuilders of varying size, ranging from local to national in scope, some of whom have greater financial resources than we do. We face competition:

• | for suitable and desirable lots at acceptable prices; |

• | from selling incentives offered by competing builders within and across developments; and |

• | from the existing home resale market. |

Our homebuilding operations compete primarily on the basis of price, location, design, quality, service and reputation.

The mortgage banking industry is also competitive. Our main competition comes from national, regional and local mortgage bankers, credit unions, banks and mortgage brokers in each of these markets. Our mortgage banking operations compete primarily on the basis of customer service, variety of products offered, interest rates offered, prices of ancillary services and relative financing availability and costs.

We might not be able to continue to compete successfully in our homebuilding or mortgage banking operations. An inability to effectively compete may have an adverse impact on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

A shortage of building materials or labor, or increases in materials or labor costs may adversely impact our operations.

The homebuilding business has from time to time experienced building material and labor shortages, including fluctuating lumber prices and supply. In addition, strong construction market conditions could restrict the labor force available to our subcontractors and us in one or more of our markets. Significant increases in costs resulting from these shortages, or delays in construction of homes, could have a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

We rely on subcontractors to construct our homes. The failure of our subcontractors to properly construct our homes may be costly.

We engage subcontractors to perform the actual construction of our homes. Despite our quality control efforts, we may discover that our subcontractors have engaged in improper construction practices. The occurrence of such events could require us to repair the homes in accordance with our standards and as required by law. The cost of satisfying our legal obligations in these instances may be significant, and we may be unable to recover the cost of repair from subcontractors, suppliers and insurers.

Product liability litigation and warranty claims may adversely impact our operations.

Construction defect and home warranty claims are common and can represent a substantial risk for the homebuilding industry. The cost of insuring against construction defect and product liability claims, as well as the claims themselves, can be high. In addition, insurance companies limit coverage offered to protect against these claims. Further restrictions on coverage availability, or significant increases in premium costs or claims, could have a material adverse effect on our financial results.

We are subject to litigation proceedings that could harm our business if an unfavorable ruling were to occur.

From time to time, we are involved in litigation and other legal proceedings relating to claims arising from our operations in the normal course of business. As described in, but not limited to, Item 3, “Legal Proceedings” of this Form 10-K, we are currently subject to certain legal proceedings. Litigation is subject to inherent uncertainties, and unfavorable rulings may occur. These or other litigation or legal proceedings could materially affect our ability to conduct our business in the manner that we expect or otherwise adversely affect us should an unfavorable ruling occur.

7

Our failure to maintain the security of our electronic and other confidential information could expose us to liability and materially adversely affect our financial condition and results of operations.

Privacy, security, and compliance concerns have continued to increase as technology has evolved. As part of our normal business activities, we collect and store certain confidential information, including personal information of homebuyers/borrowers and information about employees, vendors and suppliers. This information is entitled to protection under a number of federal and state laws. We may share some of this information with vendors who assist us with certain aspects of our business, particularly our mortgage and title businesses. We have implemented systems and processes intended to secure our information technology systems and prevent unauthorized access to or loss of sensitive, confidential and personal data, including through the use of encryption and authentication technologies. Additionally, we have increased our monitoring capabilities to enhance early detection and rapid response to potential security anomalies. These security measures may not be sufficient for all possible occurrences and may be vulnerable to hacking, employee error, malfeasance, system error, faulty password management or other irregularities. Further, development and maintenance of these measures are costly and require ongoing monitoring and updating as technologies change and efforts to overcome security measures become increasingly sophisticated. Our failure to maintain the security of the data we are required to protect, including via the penetration of our network security and the misappropriation of confidential and personal information, could result in business disruption, damage to our reputation, financial obligations to third parties, fines, penalties, regulatory proceedings and private litigation with potentially large costs, and also in deterioration in customers’ confidence in us and other competitive disadvantages, and thus could have a material adverse effect on our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

Weather-related and other events beyond our control may adversely impact our operations.

Extreme weather or other events, such as significant snowfalls, hurricanes, tornadoes, earthquakes, forest fires, floods, terrorist attacks or war may affect our markets, our operations and our profitability. These events may impact our physical facilities or those of our suppliers or subcontractors and our housing inventories, causing us material increases in costs, or delays in construction of homes, which could have a material adverse effect upon our sales, profitability, stock performance, ability to service our debt obligations and future cash flows.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

Our corporate offices are located in Reston, Virginia, where we currently lease approximately 61,000 square feet of office space. The current corporate office lease expires in April 2026.

In connection with the operation of the homebuilding segment, we lease production facilities in the following six locations: Thurmont, Maryland; Burlington County, New Jersey; Farmington, New York; Kings Mountain, North Carolina; Darlington, Pennsylvania; and Portland, Tennessee. These facilities range in size from approximately 40,000 square feet to 400,000 square feet and total approximately one million square feet. Each of these leases contains various options for extensions of the lease and for the purchase of the facility. These leases currently expire between 2019 and 2025. In addition, we own a production facility of approximately 100,000 square feet in Dayton, Ohio. Our plant utilization was 47% and 43% of total capacity in 2017 and 2016, respectively.

In connection with both our homebuilding and mortgage banking businesses, we also lease office space in multiple locations for homebuilding divisional offices and mortgage banking and title services branches under leases expiring at various times through 2025, none of which are individually material to our business.

We anticipate that, upon expiration of existing production facility and office leases, we will be able to renew them or obtain comparable facilities on terms acceptable to us.

Item 3. Legal Proceedings.

We are involved in various litigation matters arising in the ordinary course of business. In the opinion of management, and based on advice of legal counsel, these matters are not expected to have a material adverse effect on our financial position, results of operations or cash flows. Legal costs incurred in connection with outstanding litigation matters are expensed as incurred.

Item 4. Mine Safety Disclosures.

Not applicable.

8

Executive Officers of the Registrant

Name | Age | Positions | ||

Paul C. Saville | 62 | President and Chief Executive Officer of NVR | ||

Daniel D. Malzahn | 48 | Senior Vice President, Chief Financial Officer and Treasurer of NVR | ||

Jeffrey D. Martchek | 52 | President of Homebuilding Operations of NVR | ||

Robert W. Henley | 51 | President of NVRM | ||

Eugene J. Bredow | 48 | Vice President, Chief Accounting Officer and Controller of NVR | ||

Paul C. Saville was named President and Chief Executive Officer of NVR effective July 1, 2005. Mr. Saville has been employed by NVR since 1981.

Daniel D. Malzahn was named Senior Vice President in February 2016, and continues to serve as Chief Financial Officer and Treasurer of NVR, roles he has occupied since February 20, 2013. From February 1, 2004 through February 20, 2013, Mr. Malzahn was Vice President of Planning and Investor Relations of NVR. Mr. Malzahn has been employed by NVR since 1994.

Jeffrey D. Martchek was named President of Homebuilding Operations of NVR effective January 1, 2016. From February 2011 through January 1, 2016, Mr. Martchek was Area President for the Maryland and Virginia homebuilding operations. Mr. Martchek has been employed by NVR since 1988.

Robert W. Henley was named President of NVRM effective October 1, 2012. Mr. Henley served as interim acting President of NVRM from June 1, 2012 until October 1, 2012. Mr. Henley has been employed by NVR since 1994.

Eugene J. Bredow was named Chief Accounting Officer in February 2016, and continues to serve as Vice President and Controller of NVR, roles he has occupied since June 1, 2012. Mr. Bredow has been employed by NVR since 2004.

9

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our shares of common stock are listed and principally traded on the New York Stock Exchange under the ticker symbol “NVR.” The following table sets forth the high and low prices per share for our common stock for each quarter during the years ended December 31, 2017 and 2016:

High | Low | |||||||

Prices per share: | ||||||||

2017 | ||||||||

Fourth Quarter | $ | 3,536.97 | $ | 2,828.00 | ||||

Third Quarter | $ | 2,891.43 | $ | 2,393.82 | ||||

Second Quarter | $ | 2,510.76 | $ | 2,028.99 | ||||

First Quarter | $ | 2,115.00 | $ | 1,631.78 | ||||

2016 | ||||||||

Fourth Quarter | $ | 1,695.41 | $ | 1,478.04 | ||||

Third Quarter | $ | 1,845.37 | $ | 1,633.00 | ||||

Second Quarter | $ | 1,801.94 | $ | 1,606.75 | ||||

First Quarter | $ | 1,820.00 | $ | 1,462.02 | ||||

As of the close of business on February 12, 2018, there were 241 shareholders of record.

We have never paid a cash dividend on our shares of common stock and have no current intention to do so in the future.

We had two share repurchase authorizations outstanding during the quarter ended December 31, 2017. On February 15, 2017 and December 12, 2017, we publicly announced the Board of Directors’ approval to repurchase our outstanding common stock in one or more open market and/or privately negotiated transactions, up to an aggregate of $300 million per authorization. The repurchase authorizations do not have expiration dates. The following table provides information regarding common stock repurchases during the quarter ended December 31, 2017:

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number (or Approximate Dollar Value) of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||

October 1 - 31, 2017 | — | $ | — | — | $ | 253,660 | ||||||||

November 1 - 30, 2017 | 6,000 | $ | 3,333.05 | 6,000 | $ | 233,662 | ||||||||

December 1 - 31, 2017 | 50,128 | $ | 3,430.60 | 50,128 | $ | 361,693 | ||||||||

Total | 56,128 | $ | 3,420.17 | 56,128 | ||||||||||

On February 14, 2018, the Board of Directors approved a repurchase authorization providing us authorization to repurchase up to an aggregate of $300 million of our common stock in one or more open market and/or privately negotiated transactions.

10

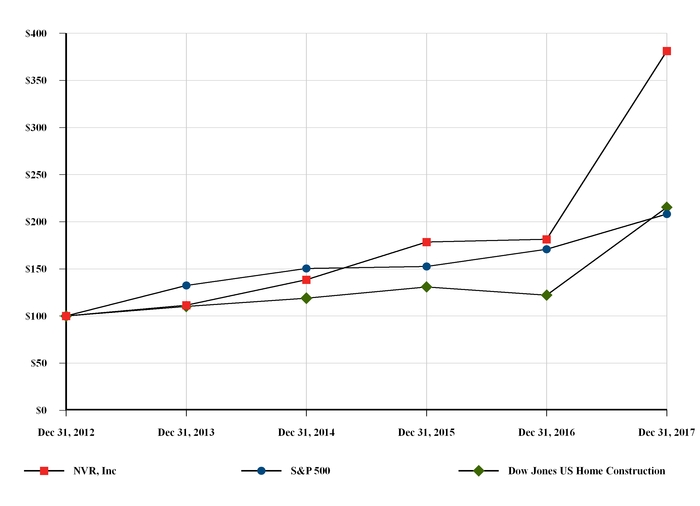

STOCK PERFORMANCE GRAPH

The following graph compares the cumulative total return to holders of our common stock since December 31, 2012 with the Dow Jones US Home Construction Index and the S&P 500 Index for that same period, assuming that $100 was invested in NVR stock and the indices on December 31, 2012.

For the Year Ended December 31, | ||||||||||||||||||||||||

Comparison of 5 Year Cumulative Total Return | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | ||||||||||||||||||

NVR, Inc. | $ | 100 | $ | 112 | $ | 139 | $ | 179 | $ | 181 | $ | 381 | ||||||||||||

S&P 500 | $ | 100 | $ | 132 | $ | 151 | $ | 153 | $ | 171 | $ | 208 | ||||||||||||

Dow Jones US Home Construction | $ | 100 | $ | 110 | $ | 119 | $ | 131 | $ | 122 | $ | 215 | ||||||||||||

11

Item 6. Selected Financial Data.

(in thousands, except per share amounts)

The following tables set forth selected consolidated financial data. The selected income statement and balance sheet data have been derived from our consolidated financial statements for each of the periods presented and are not necessarily indicative of results of future operations. The selected financial data should be read in conjunction with, and are qualified in their entirety by, the accompanying consolidated financial statements and related notes included herein.

Year Ended December 31, | ||||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

Consolidated income statement data: | ||||||||||||||||||||

Homebuilding data: | ||||||||||||||||||||

Revenues | $ | 6,175,521 | $ | 5,709,223 | $ | 5,065,200 | $ | 4,375,059 | $ | 4,134,481 | ||||||||||

Gross profit | $ | 1,185,143 | $ | 1,001,362 | $ | 946,418 | $ | 806,473 | $ | 710,277 | ||||||||||

Homebuilding income | $ | 776,370 | $ | 601,102 | $ | 555,329 | $ | 427,884 | $ | 379,370 | ||||||||||

Mortgage Banking data: | ||||||||||||||||||||

Mortgage banking fees | $ | 130,319 | $ | 113,321 | $ | 93,808 | $ | 69,509 | $ | 76,786 | ||||||||||

Mortgage banking income | $ | 70,541 | $ | 60,595 | $ | 47,883 | $ | 25,662 | $ | 39,326 | ||||||||||

Consolidated data: | ||||||||||||||||||||

Net income | $ | 537,521 | $ | 425,262 | $ | 382,927 | $ | 281,630 | $ | 266,477 | ||||||||||

Earnings per share: | ||||||||||||||||||||

Basic | $ | 144.00 | $ | 110.53 | $ | 95.21 | $ | 65.83 | $ | 56.25 | ||||||||||

Diluted | $ | 126.77 | $ | 103.61 | $ | 89.99 | $ | 63.50 | $ | 54.81 | ||||||||||

Weighted average number of shares outstanding: | ||||||||||||||||||||

Basic | 3,733 | 3,847 | 4,022 | 4,278 | 4,737 | |||||||||||||||

Diluted | 4,240 | 4,104 | 4,255 | 4,435 | 4,862 | |||||||||||||||

December 31, | ||||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

Consolidated balance sheet data: | ||||||||||||||||||||

Homebuilding inventory | $ | 1,246,199 | $ | 1,092,100 | $ | 1,006,526 | $ | 869,486 | $ | 738,565 | ||||||||||

Contract land deposits, net | $ | 370,429 | $ | 379,844 | $ | 343,295 | $ | 294,676 | $ | 236,885 | ||||||||||

Total assets | $ | 2,989,279 | $ | 2,643,943 | $ | 2,511,718 | $ | 2,347,413 | $ | 2,481,718 | ||||||||||

Notes and loans payable (1) | $ | 597,066 | $ | 596,455 | $ | 595,847 | $ | 595,244 | $ | 594,760 | ||||||||||

Shareholders’ equity | $ | 1,605,492 | $ | 1,304,441 | $ | 1,239,165 | $ | 1,124,255 | $ | 1,261,352 | ||||||||||

Cash dividends per share | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||

____________________________

(1) | Balance does not include non-recourse debt related to the consolidated variable interest entity. |

12

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

(dollars in thousands, except per share data)

Results of Operations for the Years Ended December 31, 2017, 2016 and 2015

Overview

Business

Our primary business is the construction and sale of single-family detached homes, townhomes and condominium buildings, all of which are primarily constructed on a pre-sold basis. To fully serve customers of our homebuilding operations, we also operate a mortgage banking and title services business. We primarily conduct our operations in mature markets. Additionally, we generally grow our business through market share gains in our existing markets and by expanding into markets contiguous to our current active markets. Our four homebuilding reportable segments consist of the following regions:

Mid Atlantic: | Maryland, Virginia, West Virginia, Delaware and Washington, D.C. | |

North East: | New Jersey and Eastern Pennsylvania | |

Mid East: | New York, Ohio, Western Pennsylvania, Indiana and Illinois | |

South East: | North Carolina, South Carolina, Florida and Tennessee | |

Our lot acquisition strategy is predicated upon avoiding the financial requirements and risks associated with direct land ownership and development. We generally do not engage in land development (see discussion below of our land development activities). Instead, we typically acquire finished lots at market prices from various third party land developers pursuant to Lot Purchase Agreements. These Lot Purchase Agreements require deposits, typically ranging up to 10% of the aggregate purchase price of the finished lots, in the form of cash or letters of credit that may be forfeited if we fail to perform under the Lot Purchase Agreement. This strategy has allowed us to maximize inventory turnover, which we believe enables us to minimize market risk and to operate with less capital, thereby enhancing rates of return on equity and total capital.

In addition to constructing homes primarily on a pre-sold basis and utilizing what we believe is a conservative lot acquisition strategy, we focus on obtaining and maintaining a leading market position in each market we serve. This strategy allows us to gain valuable efficiencies and competitive advantages in our markets, which we believe contributes to minimizing the adverse effects of regional economic cycles and provides growth opportunities within these markets. Our continued success is contingent upon our ability to control an adequate supply of finished lots on which to build.

In certain specific strategic circumstances, we deviate from our historical lot acquisition strategy and engage in joint venture arrangements with land developers or directly acquire raw ground already zoned for its intended use for development. Once we acquire control of raw ground, we determine whether to sell the raw parcel to a developer and enter into a Lot Purchase Agreement with the developer to purchase the finished lots or to hire a developer to develop the land on our behalf. While joint venture arrangements and direct land development activity are not our preferred method of acquiring finished building lots, we may enter into additional transactions in the future on a limited basis where there exists a compelling strategic or prudent financial reason to do so. We expect, however, to continue to acquire substantially all of our finished lot inventory using Lot Purchase Agreements with forfeitable deposits.

As of December 31, 2017, we controlled lots as described below.

Lot Purchase Agreements

We controlled approximately 84,300 lots under Lot Purchase Agreements with third parties through deposits in cash and letters of credit totaling approximately $393,900 and $1,900, respectively. Included in the number of controlled lots are approximately 4,600 lots for which we have recorded a contract land deposit impairment reserve of approximately $30,000 as of December 31, 2017.

Joint Venture Limited Liability Corporations (“JVs”)

We had an aggregate investment totaling approximately $45,500 in six JVs, expected to produce approximately 7,300 lots. Of the lots to be produced by the JVs, approximately 3,900 lots were controlled by us and approximately 3,400 lots were either under contract with unrelated parties or currently not under contract.

Land Under Development

We directly owned four separate raw land parcels, zoned for their intended use, with a current cost basis, including development costs, of approximately $34,200 that we intend to develop into approximately 500 finished lots. We had additional funding commitments of approximately $7,900 under a joint development agreement related to one parcel, a portion of which we expect will be offset by development credits of approximately $4,700.

See Notes 3, 4 and 5 to the consolidated financial statements included herein for additional information regarding Lot Purchase Agreements, JVs and land under development, respectively.

13

Raw Land Purchase Agreements

In addition to the lots we currently control as discussed above, we have certain properties under contract with land owners that are expected to yield approximately 10,700 lots. Some of these properties may require rezoning or other approvals to achieve the expected yield. These properties are controlled with cash deposits and letters of credit totaling approximately $6,600 and $100, respectively, as of December 31, 2017, of which approximately $5,800 is refundable if we do not perform under the contract. We generally expect to assign the raw land contracts to a land developer and simultaneously enter into a Lot Purchase Agreement with the assignee if the project is determined to be feasible.

Current Business Environment and Key Financial Results

During 2017, we continued to experience improving new home demand as a result of favorable market conditions, including low mortgage interest rates, low unemployment and improved consumer confidence. However, new home prices continued to be constrained due to the competitive market environment.

Our consolidated revenues for the year ended December 31, 2017 totaled $6,305,840, an increase of 8% from $5,822,544 in 2016. Our net income for 2017 was $537,521, or $126.77 per diluted share, increases of 26% and 22% compared to 2016 net income and diluted earnings per share, respectively. Our homebuilding gross profit margin percentage increased to 19.2% in 2017 from 17.5% in 2016. New orders, net of cancellations (“New Orders”) during 2017 increased 13% from 2016 while our average New Order sales price decreased 1% to $383.2 in 2017. Our backlog of homes sold but not yet settled with the customer as of December 31, 2017 increased on a unit basis by 24% to 8,531 units and increased on a dollar basis by 21% to $3,277,888 when compared to December 31, 2016.

We believe that a continuation of the housing market recovery is dependent upon sustained economic growth, driven by continued improvements in job and wage growth and household formation. We expect to continue to face gross profit margin pressure which will be impacted by modest pricing power and our ability to manage land and construction costs. We also expect to face pressure on mortgage banking profit due to the competitive pricing pressures in the mortgage market. We believe that we are well positioned to take advantage of opportunities that may arise from future economic and homebuilding market volatility due to the strength of our balance sheet.

Homebuilding Operations

The following table summarizes the results of our consolidated homebuilding operations and certain operating activity for each of the last three years:

Year Ended December 31, | ||||||||||||

2017 | 2016 | 2015 | ||||||||||

Financial data: | ||||||||||||

Revenues | $ | 6,175,521 | $ | 5,709,223 | $ | 5,065,200 | ||||||

Cost of sales | $ | 4,990,378 | $ | 4,707,861 | $ | 4,118,782 | ||||||

Gross profit margin percentage | 19.2 | % | 17.5 | % | 18.7 | % | ||||||

Selling, general and administrative expenses | $ | 392,272 | $ | 382,459 | $ | 371,127 | ||||||

Operating data: | ||||||||||||

New orders (units) | 17,608 | 15,583 | 14,080 | |||||||||

Average new order price | $ | 383.2 | $ | 386.4 | $ | 378.7 | ||||||

Settlements (units) | 15,961 | 14,928 | 13,326 | |||||||||

Average settlement price | $ | 386.9 | $ | 381.2 | $ | 379.9 | ||||||

Backlog (units) | 8,531 | 6,884 | 6,229 | |||||||||

Average backlog price | $ | 384.2 | $ | 392.8 | $ | 381.3 | ||||||

New order cancellation rate | 14.0 | % | 15.5 | % | 14.5 | % | ||||||

Consolidated Homebuilding

2017 versus 2016

Homebuilding revenues increased 8% in 2017 compared to 2016, primarily as a result of a 7% increase in the number of units settled year over year. The increase in the number of units settled was primarily attributable to an 11% higher backlog unit balance entering 2017 compared to the backlog unit balance entering 2016, offset partially by a lower backlog turnover rate year over year.

Gross profit margin percentage in 2017 increased to 19.2% from 17.5% in 2016, due primarily to modest improvement in pricing, moderating construction costs and the increase in the number of units settled, which allowed us to better leverage certain operating costs.

14

The number of New Orders increased 13% while the average sales price of New Orders decreased 1% in 2017 when compared to 2016. New Orders increased in each of our market segments due to more favorable market conditions in 2017 compared to 2016, which led to higher community absorption rates year over year.

Selling, general and administrative ("SG&A") expenses in 2017 increased by 3% compared to 2016, but as a percentage of revenue decreased to 6.4% in 2017 from 6.7% in 2016. SG&A expenses as a percentage of revenue were favorably impacted by the 8% increase in revenues.

Backlog units and dollars were 8,531 units and $3,277,888, respectively, as of December 31, 2017 compared to 6,884 units and $2,704,277, respectively, as of December 31, 2016. The 24% increase in backlog units was primarily attributable to a 19% increase in New Orders for the six-month period ended December 31, 2017 compared to the same period in 2016. Backlog dollars were favorably impacted by the increase in backlog units.

Backlog may be impacted by customer cancellations for various reasons that are beyond our control, such as failure to obtain mortgage financing, inability to sell an existing home, job loss, or a variety of other reasons. In any period, a portion of the cancellations that we experience are related to new sales that occurred during the same period, and a portion are related to sales that occurred in prior periods and therefore appeared in the beginning backlog for the current period. Expressed as the total of all cancellations during the period as a percentage of gross sales during the period, our cancellation rate was approximately 14% in 2017 and approximately 15% in both 2016 and 2015. Additionally, during each of 2017, 2016 and 2015, approximately 6% of a reporting quarter’s opening backlog cancelled during the quarter. We can provide no assurance that our historical cancellation rates are indicative of the actual cancellation rate that may occur in future years. Other than those units that are cancelled, we expect to settle substantially all of our December 31, 2017 backlog during 2018. See “Risk Factors” in Item 1A of this Form 10-K.

The backlog turnover rate is impacted by various factors, including, but not limited to, changes in New Order activity, internal production capacity, external subcontractor capacity and other external factors over which we do not exercise control.

2016 versus 2015

Homebuilding revenues increased 13% in 2016 compared to 2015, primarily as a result of a 12% increase in the number of units settled year over year. The increase in the number of units settled was attributable to a 14% higher backlog unit balance entering 2016 compared to backlog entering 2015. In addition, the number of units settled was favorably impacted by a 10% increase in New Orders for the first six months of 2016 compared to the same period in 2015.

The number of New Orders and the average sales price of New Orders increased 11% and 2%, respectively, in 2016 compared to 2015. New Orders and the average sales price of New Orders increased in each of our market segments due to more favorable market conditions in 2016 compared to 2015, which led to a higher sales absorption rate year over year. Additionally, New Orders were favorably impacted by a 3% increase in the average number of active communities year over year.

Gross profit margin percentage in 2016 decreased to 17.5% from 18.7% in 2015, due to higher construction and selling related costs year over year.

SG&A expenses in 2016 increased approximately $11,300, or 3% compared to 2015, but as a percentage of revenue decreased to 6.7% from 7.3% year over year. SG&A expenses increased primarily due to an approximate $10,500 increase in marketing costs attributable to the 3% increase in the number of active communities year over year and higher spending levels.

Backlog units and dollars were 6,884 units and $2,704,277, respectively, as of December 31, 2016 compared to 6,229 units and $2,375,182, respectively, as of December 31, 2015. The 11% increase in backlog units was primarily attributable to a 12% increase in New Orders for the six month period ended December 31, 2016 compared to the same period in 2015. The 14% increase in backlog dollars was attributable to the increase in backlog units coupled with a 3% increase in the average New Order sales price for the six month period ended December 31, 2016 compared to the same period in 2015.

Reportable Homebuilding Segments

Homebuilding profit before tax includes all revenues and income generated from the sale of homes, less the cost of homes sold, SG&A expenses, and a corporate capital allocation charge determined by corporate management. The corporate capital allocation charge eliminates in consolidation and is based on the segment’s average net assets employed. The corporate capital allocation charged to the operating segment allows the Chief Operating Decision Maker to determine whether the operating segment’s results are providing the desired rate of return after covering our cost of capital.

We record charges on contract land deposits when we determine that it is probable that recovery of the deposit is impaired. For segment reporting purposes, impairments on contract land deposits are generally charged to the operating segment upon the determination to terminate a Lot Purchase Agreement with the developer or to restructure a Lot Purchase Agreement resulting in the forfeiture of the deposit. For presentation purposes below, the contract land deposit reserve at December 31, 2017 and 2016 has been allocated to the reportable segments for the respective years to show contract land deposits on a net basis. The net contract land

15

deposit balances below also include approximately $2,000 and $2,400 at December 31, 2017 and 2016, respectively, of letters of credit issued as deposits in lieu of cash.

The following tables summarize certain homebuilding operating activity by reportable segment for each of the last three years:

Selected Segment Financial Data:

Year Ended December 31, | ||||||||||||

2017 | 2016 | 2015 | ||||||||||

Revenues: | ||||||||||||

Mid Atlantic | $ | 3,543,687 | $ | 3,319,776 | $ | 3,022,789 | ||||||

North East | 517,141 | 462,385 | 432,145 | |||||||||

Mid East | 1,250,165 | 1,192,472 | 1,014,920 | |||||||||

South East | 864,528 | 734,590 | 595,346 | |||||||||

Year Ended December 31, | ||||||||||||

2017 | 2016 | 2015 | ||||||||||

Gross profit margin: | ||||||||||||

Mid Atlantic | $ | 663,650 | $ | 561,857 | $ | 563,299 | ||||||

North East | 104,501 | 68,808 | 79,588 | |||||||||

Mid East | 244,832 | 215,335 | 178,508 | |||||||||

South East | 173,961 | 137,787 | 113,210 | |||||||||

Year Ended December 31, | |||||||||

2017 | 2016 | 2015 | |||||||

Gross profit margin percentage: | |||||||||

Mid Atlantic | 18.7 | % | 16.9 | % | 18.6 | % | |||

North East | 20.2 | % | 14.9 | % | 18.4 | % | |||

Mid East | 19.6 | % | 18.1 | % | 17.6 | % | |||

South East | 20.1 | % | 18.8 | % | 19.0 | % | |||

Year Ended December 31, | ||||||||||||

2017 | 2016 | 2015 | ||||||||||

Segment profit: | ||||||||||||

Mid Atlantic | $ | 398,494 | $ | 301,173 | $ | 322,829 | ||||||

North East | 60,218 | 21,947 | 37,914 | |||||||||

Mid East | 149,639 | 121,166 | 86,336 | |||||||||

South East | 95,826 | 71,098 | 57,384 | |||||||||

16

Segment Operating Activity:

Year Ended December 31, | |||||||||||||||||||||

2017 | 2016 | 2015 | |||||||||||||||||||

Units | Average Price | Units | Average Price | Units | Average Price | ||||||||||||||||

New orders, net of cancellations: | |||||||||||||||||||||

Mid Atlantic | 8,654 | $ | 438.9 | 7,916 | $ | 443.1 | 7,070 | $ | 439.5 | ||||||||||||

North East | 1,362 | $ | 409.7 | 1,314 | $ | 387.1 | 1,173 | $ | 365.9 | ||||||||||||

Mid East | 4,171 | $ | 332.7 | 3,659 | $ | 329.2 | 3,485 | $ | 321.4 | ||||||||||||

South East | 3,421 | $ | 293.5 | 2,694 | $ | 296.9 | 2,352 | $ | 287.3 | ||||||||||||

Total | 17,608 | $ | 383.2 | 15,583 | $ | 386.4 | 14,080 | $ | 378.7 | ||||||||||||

Year Ended December 31, | |||||||||||||||||||||

2017 | 2016 | 2015 | |||||||||||||||||||

Units | Average Price | Units | Average Price | Units | Average Price | ||||||||||||||||

Settlements: | |||||||||||||||||||||

Mid Atlantic | 7,971 | $ | 444.5 | 7,512 | $ | 439.6 | 6,879 | $ | 439.2 | ||||||||||||

North East | 1,288 | $ | 401.5 | 1,246 | $ | 371.1 | 1,221 | $ | 353.9 | ||||||||||||

Mid East | 3,772 | $ | 331.4 | 3,658 | $ | 325.7 | 3,137 | $ | 323.5 | ||||||||||||

South East | 2,930 | $ | 295.1 | 2,512 | $ | 292.4 | 2,089 | $ | 284.9 | ||||||||||||

Total | 15,961 | $ | 386.9 | 14,928 | $ | 381.2 | 13,326 | $ | 379.9 | ||||||||||||

Year Ended December 31, | |||||||||||||||||||||

2017 | 2016 | 2015 | |||||||||||||||||||

Units | Average Price | Units | Average Price | Units | Average Price | ||||||||||||||||

Backlog: | |||||||||||||||||||||

Mid Atlantic | 4,224 | $ | 432.2 | 3,541 | $ | 443.4 | 3,137 | $ | 435.3 | ||||||||||||

North East | 682 | $ | 424.3 | 608 | $ | 408.7 | 540 | $ | 374.7 | ||||||||||||

Mid East | 1,898 | $ | 341.2 | 1,499 | $ | 340.1 | 1,498 | $ | 331.7 | ||||||||||||

South East | 1,727 | $ | 298.4 | 1,236 | $ | 304.1 | 1,054 | $ | 294.6 | ||||||||||||

Total | 8,531 | $ | 384.2 | 6,884 | $ | 392.8 | 6,229 | $ | 381.3 | ||||||||||||

Operating Data:

Year Ended December 31, | |||||||||

2017 | 2016 | 2015 | |||||||

New order cancellation rate: | |||||||||

Mid Atlantic | 15.2 | % | 15.7 | % | 15.2 | % | |||

North East | 13.3 | % | 15.1 | % | 14.3 | % | |||

Mid East | 11.5 | % | 14.4 | % | 13.4 | % | |||

South East | 14.3 | % | 16.5 | % | 14.2 | % | |||

Year Ended December 31, | |||||||||

2017 | 2016 | 2015 | |||||||

Average active communities: | |||||||||

Mid Atlantic | 238 | 239 | 233 | ||||||

North East | 42 | 42 | 38 | ||||||

Mid East | 121 | 128 | 130 | ||||||

South East | 84 | 76 | 71 | ||||||

Total | 485 | 485 | 472 | ||||||

17

Homebuilding Inventory:

As of December 31, | ||||||||

2017 | 2016 | |||||||

Sold inventory: | ||||||||

Mid Atlantic | $ | 617,471 | $ | 544,840 | ||||

North East | 96,412 | 79,751 | ||||||

Mid East | 173,572 | 141,033 | ||||||

South East | 151,219 | 107,967 | ||||||

Total (1) | $ | 1,038,674 | $ | 873,591 | ||||

As of December 31, | ||||||||

2017 | 2016 | |||||||

Unsold lots and housing units inventory: | ||||||||

Mid Atlantic | $ | 118,209 | $ | 117,920 | ||||

North East | 6,666 | 6,370 | ||||||

Mid East | 7,112 | 7,218 | ||||||

South East | 13,511 | 10,872 | ||||||

Total (1) | $ | 145,498 | $ | 142,380 | ||||

(1) | Total segment inventory differs from consolidated inventory due to certain consolidation adjustments necessary to convert the reportable segments’ results, which are predominantly maintained on a cash basis, to a full accrual basis for external financial statement presentation purposes. These consolidation adjustments are not allocated to our operating segments. |

Lots Controlled and Land Deposits:

As of December 31, | ||||||

2017 | 2016 | |||||

Total lots controlled: | ||||||