UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K |

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 28, 2017

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 001-16435

Chico’s FAS, Inc. (Exact name of registrant as specified in charter) |

Florida | 59-2389435 | |

(State or other jurisdiction of incorporation) | (IRS Employer Identification No.) | |

11215 Metro Parkway, Fort Myers, Florida | 33966 | |

(Address of principal executive offices) | (Zip code) | |

(239) 277-6200

(Registrant’s telephone number)

Securities registered pursuant to Section 12(b) of the Act:

Title of Class | Name of Exchange on Which Registered | |

Common Stock, Par Value $0.01 Per Share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K ¨.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ý | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ (do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

State the aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant:

Approximately $1,557,000,000 as of July 30, 2016, based upon the closing stock price on July 29, 2016 as reported by the NYSE.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date:

Common Stock, par value $0.01 per share – 128,031,928 shares as of February 24, 2017.

Documents incorporated by reference:

Part III Definitive Proxy Statement for the Company’s Annual Meeting of Stockholders presently scheduled for June 22, 2017.

CHICO’S FAS, INC.

ANNUAL REPORT ON FORM 10-K

FOR THE

YEAR ENDED JANUARY 28, 2017

TABLE OF CONTENTS

Item 1. | |||

Item 1A. | |||

Item 1B. | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Item 5. | |||

Item 6. | |||

Item 7. | |||

Item 7A. | |||

Item 8. | |||

Item 9. | |||

Item 9A. | |||

Item 9B. | |||

Item 10. | |||

Item 11. | |||

Item 12. | |||

Item 13. | |||

Item 14. | |||

Item 15. | |||

PART I

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, and are subject to risks, uncertainties, and other factors which could cause actual results to differ materially from those expressed or implied by such forward-looking statements. See “Item 1A. Risk Factors.”

ITEM 1. | BUSINESS |

Overview

Chico’s FAS, Inc.1, is a collection of distinct lifestyle brands serving the needs of fashion-savvy women 35 years and older. The Company’s portfolio currently consists of three brands: Chico’s, White House Black Market (“WHBM”) and Soma. Our omni-channel brands are specialty retailers of private label women’s apparel, accessories and related products. Our product is available to customers in our domestic and international retail stores, through our optimized e-commerce websites, via telephone through our call centers and through an unaffiliated franchise partner in Mexico. As of January 28, 2017, we operated 1,501 stores across 48 states, Puerto Rico, the U.S. Virgin Islands and Canada, and sold merchandise through 91 franchise locations in Mexico.

Since 1983, we have grown by offering high quality and unique merchandise, supported by compelling marketing and outstanding personalized customer service. While each of our brands has a distinct customer base, the overall portfolio caters to a broad age and economic demographic, with household incomes ranging from $50,000 to well over $100,000.

Our Brands

Chico’s

The Chico’s brand, which began operations in 1983, primarily sells exclusively designed, private branded clothing focusing on women 45 and older with a moderate to high income level. The style sensibility is unique with an individual expression created to illuminate the women wearing the brand. Chico's apparel, including the Black Label, Zenergy and Travelers collections, emphasizes a style that has a comfortable and relaxed fit. Accessories and jewelry are designed to elevate the clothing assortment, allowing our customer to individualize her personal style. Chico's is vertically integrated, controlling almost all aspects of the apparel design process, including choices of pattern, print, construction, design specifications, fabric, finishes and color through in-house designers, purchased designs and independent suppliers.

The distinctive nature of Chico’s clothing is also reflected in its sizing, which is comprised of sizes 000, 00 (size 0-2), 0 (size 4-6), 1 (size 8-10), 2 (size 12-14), 3 (size 16-18) and 4 (size 20-22). Chico’s will occasionally offer half-sizes (up to 4.5), one-size-fits-all, petite sizes, short and tall inseams, and small, medium and large sizing for some items. The relaxed fit allows us to utilize this kind of sizing and thus offer a wide selection of clothing without investing in a large number of sizes within a single style.

White House Black Market

The WHBM brand, which began operations in 1985 and we acquired in September 2003, is dedicated to being a go-to style destination and authority on wardrobe building. WHBM primarily sells exclusively designed, private branded clothing focusing on women 35 and older with a moderate to high income level. WHBM offers a modern collection for the way women live now, selling stylish and versatile clothing and accessory items, including everyday basics, wear-to-work, denim and elegant occasion. Historically known for its black and white color palette, WHBM's collection reflects on-trend colors and patterns. The accessories at WHBM, such as shoes, belts, scarves, handbags and jewelry, are specifically designed to coordinate with each collection, allowing customers to easily individualize their wardrobe selections. WHBM is vertically integrated, controlling almost all aspects of the apparel design process, including choices of patterns, prints, construction, design specifications, fabric, finishes and color through in-house designers, purchased designs and independent suppliers.

___________________________

1 | As used in this report, all references to “we,” “us,” “our,” and “the Company,” refer to Chico’s FAS, Inc., a Florida corporation, and all of its wholly-owned subsidiaries. |

2

WHBM uses American sizes in the 00-14 range (with online sizes up to 16), including petite sizing, as well as short and long inseams, and small, medium and large sizing for some items. The fit of the WHBM clothing is tailored to complement the figure of a body-conscious woman, while still remaining comfortable.

Soma

The Soma brand, which began operations in 2004, primarily sells exclusively designed, private branded lingerie, sleepwear, loungewear, activewear, and beauty products focusing on women 35 and older with a moderate to high income level. The lingerie category includes bras, panties, shapewear and swimwear while the loungewear category includes tops, bottoms and dresses. Bras range in size from 32A-46HH. The sleepwear and loungewear offerings range from extra small to extra-extra large sizing. The beauty category consists of the Memorable, Enticing and Oh My Gorgeous lines of fine fragrance. The Soma team develops product offerings by working closely with a small number of independent suppliers to design proprietary products in-house and, in some cases, designs provided by its independent suppliers under labels other than the Soma brand.

Our Business Strategy

Our overall business strategy is focused on building a collection of distinct high-performing retail brands serving the fashion needs of women 35 and older. We seek to accomplish this strategy through our four focus areas: (1) evolving the customer experience, (2) strengthening our brands' positions, (3) leveraging actionable retail science, and (4) sharpening our financial principles. Over the long term, we may build our brand portfolio by organic development or acquisition of other specialty retail concepts if research indicates that the opportunity complements our current brands and is appropriate and in the best interest of the shareholders.

We pursue improving the performance of our brands by building our omni-channel capabilities, which includes managing our store base and growing our online presence, by executing marketing plans, by effectively leveraging expenses and by optimizing the merchandise offerings of each of our three brands. We continue to invest heavily in our omni-channel capabilities in order to allow customers to fully experience our brands through more than one channel. In essence, we view our various sales channels as a single, integrated process rather than as separate sales channels operating independently. To that end, we often refer to our brands' respective websites as "our largest store" within the brand.

Under this integrated, omni-channel approach, we encourage our customers to take advantage of each of our sales channels in whatever way best fits their needs. Customers may shop our products through one channel and consummate the purchase through a different channel. Our domestic customers have the option of returning merchandise to a store or to our distribution center, regardless of the channel used for purchase. We believe this omni-channel approach meets our customers’ expectations, enhances the customer experience, contributes to the overall success of our brands, reflects that our customers do not differentiate between channels, and is consistent with how we plan and manage our business. As a result, we maintain a shared inventory platform for our operations, allowing us to fulfill orders for all channels from our distribution center in Winder, Georgia. We also fulfill in-store orders directly from other stores or our distribution center.

We seek to acquire and retain omni-channel customers by leveraging existing customer-specific data and through targeted marketing, including e-marketing, television, catalogs and mailers. We seek to optimize the potential of our brands with improved product offerings, which includes potential new merchandise opportunities and brand extensions that enhance the current offerings, as well as our continued emphasis on our “Most Amazing Personal Service” standard.

In 2016, we announced and began implementing cost reduction and operating efficiency initiatives, including realigning marketing and digital commerce, improving supply chain efficiency, reducing non-merchandise expenses, and optimizing marketing spend. Actions taken as part of these initiatives are expected to continue to reduce expenses and complexity, standardize processes and improve the Company's ability to respond to changes in customer demand for merchandise.

Our Customer Service Model

Our customers deserve outstanding and personalized customer service, which we strive to achieve through our trademark “Most Amazing Personal Service” standard. We believe this service model is one of our competitive advantages and a key to the success of our omni-channel approach. An important aspect of our successful implementation of this model involves the specialized training we give sales associates to help meet their customers’ fashion and wardrobe needs, including clothing and accessory style, color selection, coordination of complete outfits, and suggestions on different ways in which to wear the clothing and accessories. Our sales associates are encouraged to develop long-term relationships with their customers, to know their customers’ preferences, and to assist those customers in selecting merchandise best suited to their tastes and wardrobe needs. In 2016, all of our brands began utilizing tablets in stores to access customer purchase history and style preferences as a clienteling tool that enhances the shopping experience in a personalized and efficient manner.

3

We also serve our customers’ needs and build customer loyalty through our customer rewards programs. Our programs are designed to reward our loyal customers by leveraging the rich data our customers share with us to deliver a relevant and engaging experience with our brands. The benefits provided are continuously evaluated in conjunction with our overall customer relationship management and marketing activities to ensure they remain a compelling reason for customers to shop at our brands.

• | Chico’s. A Chico’s customer can join the “Passport” program at no cost and receive additional benefits after spending a fixed amount. Features of the program include a 5% discount, exclusive offers, special promotions, free shipping, invitations to private sale events and advance notice regarding new arrivals. |

• | WHBM. With “WHBM Rewards”, a customer can join at no cost for tier-based discounts, a 5% discount after spending a fixed amount, free shipping, special promotions, and invitations to private sales based on annual spend. |

• | Soma. A Soma customer can join “Love Soma Rewards” at no cost and earns points based on purchases. Features of the program include reward coupons at specified loyalty point levels, exclusive promotions and free shipping. |

Our Boutiques and Outlet Stores

Our boutiques are located in upscale indoor shopping malls, outdoor shopping areas, and standalone street-front locations. Boutique locations are determined on the basis of various factors, including, but not limited to: geographic and demographic characteristics of the market, nearby competitors, our own network of existing boutiques, the location of the shopping venue, including the site within the shopping center, proposed lease terms, anchor or other co-tenants, parking accommodations and convenience. Our merchandise is also sold through franchise locations in Mexico, including boutique locations as well as shop-in-shop formats within a department store environment.

Our outlet stores are primarily located in quality outlet centers. The Chico’s and WHBM brand outlets contain a mixture of made-for-outlet and clearance merchandise. The made-for-outlet product carries a higher margin than the clearance items from our boutique stores. Soma outlets contain a mix of boutique and clearance merchandise. We also sell clearance merchandise on our websites. We regularly review the appropriate ratio of made-for-outlet and clearance merchandise sold at our outlets and adjust that ratio as appropriate.

4

As of January 28, 2017, we operated 1,501 retail stores in 48 states, Puerto Rico, the U.S. Virgin Islands, and Canada. As of January 28, 2017, our merchandise was also sold through 91 franchise locations in Mexico. The following tables set forth information concerning our retail stores during the past five fiscal years:

Fiscal Year1 | ||||||||||||||

Stores | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||

Stores at beginning of year | 1,518 | 1,547 | 1,472 | 1,357 | 1,256 | |||||||||

Opened | 17 | 40 | 109 | 135 | 125 | |||||||||

Closed | (34 | ) | (69 | ) | (34 | ) | (20 | ) | (24 | ) | ||||

Total Stores | 1,501 | 1,518 | 1,547 | 1,472 | 1,357 | |||||||||

Fiscal Year End | ||||||||||||||

Stores by Brand | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||

Chico’s frontline boutiques | 587 | 604 | 613 | 611 | 606 | |||||||||

Chico’s outlets | 116 | 117 | 118 | 110 | 99 | |||||||||

Chico's Canada | 4 | 4 | 3 | — | — | |||||||||

Chico’s total | 707 | 725 | 734 | 721 | 705 | |||||||||

WHBM frontline boutiques | 423 | 429 | 441 | 436 | 398 | |||||||||

WHBM outlets | 71 | 71 | 68 | 59 | 45 | |||||||||

WHBM Canada | 6 | 6 | 5 | 3 | — | |||||||||

WHBM total | 500 | 506 | 514 | 498 | 443 | |||||||||

Soma frontline boutiques | 275 | 269 | 263 | 232 | 193 | |||||||||

Soma outlets | 19 | 18 | 17 | 17 | 16 | |||||||||

Soma total | 294 | 287 | 280 | 249 | 209 | |||||||||

Boston Proper boutiques | — | — | 19 | 4 | — | |||||||||

Total Stores | 1,501 | 1,518 | 1,547 | 1,472 | 1,357 | |||||||||

________________________

1Our fiscal years end on the Saturday closest to January 30th and are designated by the calendar year in which the fiscal year commences. The periods presented in these financial statements are the fiscal years ended January 28, 2017 (“fiscal 2016”, “2016”, or “current period”), January 30, 2016 (“fiscal 2015”, “2015”, or “prior period”), January 31, 2015 (“fiscal 2014”, or “2014”), February 1, 2014 (“fiscal 2013”, or “2013”), and February 2, 2013 (“fiscal 2012”, or “2012”). Each of these periods had 52 weeks, except for fiscal 2012, which consisted of 53 weeks.

In fiscal 2017, we anticipate opening approximately 10 stores while closing 50 stores in our efforts to continue our capital allocation and cost reduction initiatives. We expect 14-18 net closures of Chico's stores, 14-18 net closures of WHBM stores, and 6-10 net closures of Soma stores. We continuously evaluate the appropriate new store growth rate and closures in light of economic conditions and may adjust the growth rate and closures as conditions require or as opportunities arise. Our unaffiliated franchisee expects to continue opening franchise locations in Mexico.

Digital Commerce

Each of our brands has a digital flagship: www.chicos.com, www.whbm.com and www.soma.com, which provide customers the ability to browse and order merchandise, locate our stores, and engage with content to enhance the shopping experience. Our websites are designed to complement the in-store experience and play a vital role in both our omni-channel strategy and the customer experience. Some products are available exclusively online including extended sizes, additional style and color choices, premier partner brands and clearance items. Online merchandise is also available for order through our call centers and in our stores through our clienteling applications. Domestic customers may return product directly to our distribution center or in our store locations regardless of the channel in which the merchandise was purchased.

5

We continue to focus our efforts to better align with shifts in customer traffic and consumers' consumption of media and content. As a result of significant increases in mobile traffic, in 2016 we implemented a responsive website design for Chico's and WHBM to ensure a consistent and seamless customer experience across devices. In fiscal 2017, we will complete the responsive website design conversion for Soma. We will maintain focus on our omni-channel approach by enhancing all brand websites through new features, functionality, search engine optimization and content designed to improve and evolve the customer's experience.

Marketing and Advertising

Driven by our industry-leading transactional data, our brands continue to develop targeted and effective marketing strategies. We continue to optimize and shift advertising from traditional to digital media with a focus on attracting new customers and using predictive modeling and advanced segmentation to drive retention and reactivation.

Our marketing programs currently consists of the following media mix to engage current and prospective customers:

• | Loyalty and rewards programs; |

• | Direct marketing: catalogs, postcards, email and calling campaigns; |

• | Digital marketing: mobile paid search, product listing ads, display banner advertising and remarketing, affiliate programs; |

• | Social marketing: organic and paid efforts across social platforms; |

• | National and local print and broadcast advertising; |

• | Editorial content; |

• | Public relations; and |

• | Charitable giving and outreach programs. |

In 2017, our marketing efforts will continue to focus on attracting customers to our iconic brands' differentiated positioning by leveraging retail science.

Information Technology

We are committed to having information systems that enable us to obtain, analyze and act upon information on a timely basis and to maintain effective financial and operational controls. This effort includes testing of new products and applications so that we are able to take advantage of technological developments to support and enhance our processes across all areas of our business.

Merchandise Distribution

The distribution functions for all brands are handled from our Distribution Center (“DC”) in Winder, Georgia. New merchandise is generally received daily at the DC. Imported merchandise is shipped from the country of export by sea, air, truck or rail, as circumstances require. Domestic merchandise is primarily shipped by truck or rail. Upon arriving at the DC, merchandise is sorted and packaged for shipment to individual stores or is held for future store replenishment or direct shipment to customers. Merchandise is generally pre-ticketed with price and related informational tags at the point of manufacture.

Our DC has been granted Foreign Trade Zone status from the Department of Commerce and U.S. Customs and Border Protection. This status facilitates international expansion and allows us to move certain merchandise to the DC without paying U.S. Customs duty until the merchandise is shipped to domestic stores or online customers.

Product Sourcing

Our sourcing activities are performed by one shared service team focused on identifying cost-effective opportunities to improve production speed and flexibility while maintaining our quality standards. In fiscal 2010, China sources accounted for approximately 63% of our merchandise cost, compared to approximately 55% for fiscal 2016. We take ownership in the foreign country, at a designated point of entry into the United States, or at our DC, depending on the specific terms of sale.

We purchase the majority of our merchandise through key suppliers with whom we have established strategic collaborations; these key suppliers represented 57% of our purchases in fiscal 2016 with our largest supplier accounting for 23% of the total. Currently, we believe our product is appropriately distributed among suppliers and across countries of manufacture taking into consideration product quality execution, flexibility and speed at an acceptable cost and level of risk.

6

Competition

The women’s retail apparel and intimate apparel business is highly competitive and includes local, national and international department stores, specialty stores, boutique stores, catalog companies, and online retailers. We believe that our distinctively designed merchandise offerings and emphasis on customer service distinguish us from our competitors.

Trademarks and Service Marks

We are the owner of certain registered and common law trademarks and service marks (collectively referred to as “Marks”).

Our Marks include, but are not limited to: CHICO’S, CHICO'S PASSPORT, ZENERGY, SO SLIMMING, WHITE HOUSE BLACK MARKET, WHBM REWARDS, WORK KIT, SOMA, SOMA INTIMATES, ENTICING, COOL NIGHTS, EMBRACEABLE, VANISHING BACK, VANISHING EDGE, and LOVE SOMA REWARDS. We have registered or are seeking to register a number of these Marks in the United States, Canada, Mexico and other foreign countries.

In the opinion of management, our rights in the Marks are important to our business. Accordingly, we intend to maintain our Marks and the related registrations and applications. We are not aware of any material claims of infringement or other challenges to our rights to use any registered Marks in the United States.

Available Information

Through our investor relations website, www.chicosfas.com, we make available free of charge our Securities and Exchange Commission (“SEC”) filings, including our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, as soon as reasonably practicable after those reports are electronically filed with the SEC and are available at www.sec.gov. This website also includes recent press releases, corporate governance information, beneficial ownership reports, institutional presentations, quarterly and institutional conference calls and other quarterly financial data, including historical store square footage.

Our Code of Ethics, which is applicable to all of our employees, including the principal executive officer, the principal financial officer, and the Board of Directors ("Board"), is posted on our investor relations website. Any amendments to or waivers from our Code of Ethics are also available on this website. Charters of each of the Audit Committee, Human Resources, Compensation and Benefits Committee, Corporate Governance and Nominating Committee and Executive Committee as well as the Corporate Governance Guidelines, Insider Trading Policy, Terms of Commitment to Ethical Sourcing, and Stock Ownership Guidelines are available on this website or upon written request by any shareholder.

Employees

As of January 28, 2017, we employed approximately 21,000 people, approximately 30% of whom were full-time employees and the balance of whom were part-time employees. The number of part-time employees fluctuates during peak selling periods. As of the above date, approximately 90% of our employees worked in our boutique and outlet stores. We have no collective bargaining agreements covering any of our employees, have never experienced any material labor disruption, and are unaware of any efforts or plans to organize our employees. We currently contribute a significant portion of the cost of medical, dental and life and disability insurance coverage for eligible employees. We also offer a qualified 401(k) retirement plan with an employer matching contribution percentage and an employee stock purchase plan to full-time employees and to part-time employees working twenty hours or more, as well as a deferred compensation plan to highly compensated employees. All employees are also eligible to receive substantial discounts on our merchandise. We consider the overall relations with our employees to be good.

7

ITEM 1A. | RISK FACTORS |

An investment in our common stock involves certain risks. The risks and uncertainties described below are not the only risks that may have a material adverse effect on the Company and the risks described herein are not listed in order of the likelihood that the risk might occur or the severity of the impact if the risk should occur. There can be no assurance that we have identified, assessed and appropriately addressed all risks affecting our business operations. Additional risks and uncertainties could adversely affect our business and our results. If any of the following risks actually occur, our business, consolidated financial condition or results of operations could be negatively affected, and the market price for our shares could decline. Further, to the extent that any of the information contained in this Annual Report on Form 10-K constitutes forward-looking statements, the risk factors set forth below are cautionary statements, identifying important factors that could cause the Company’s actual results to differ materially from those expressed in any forward-looking statements made by or on behalf of the Company. There can also be no assurance that the actual future results, performance, benefits, or achievements that we expect from our strategies, systems, initiatives, or products will occur.

Business Strategy

If we cannot successfully execute our business strategy, our consolidated financial condition and results of operations could be materially adversely impacted. There are numerous risks associated with this strategy including, but not limited to, the following:

Risk | Description | |

1. Failure to implement and manage our business strategy | Our long-term omni-channel business strategy is dependent upon a number of factors, including anticipating and quickly responding to changing customer preferences, shopping habits (such as online versus in-store) and fashion trends, identifying and developing new brand extensions and new markets, effectively using our marketing resources to communicate with existing and potential customers, effectively managing our store base, including management of store productivity and negotiating acceptable lease terms, having the appropriate corporate resources to support our business strategies, sourcing levels of inventory in line with expected sales and then managing its disposition, hiring, training and retaining qualified employees, generating sufficient operating cash flows to fund our business strategies, maintaining brand-specific websites that offer the system functionality, service and security customers expect, and implementing and maintaining appropriate technology to support our business strategies. | |

2. Competition | The women's specialty retail industry is highly competitive. We compete with local, national and international department stores, specialty and discount stores, catalogs and internet businesses offering similar categories of merchandise. Many of our competitors have advantages over us, including substantially greater financial, marketing and other resources. Increased levels of promotional activity by our competitors, some of whom may be able to adopt more aggressive pricing policies than we can, both online and in stores, may negatively impact our sales and profitability. There is no assurance that we can compete successfully with these companies in the future. In addition to competing for sales, we compete for favorable store locations, lease terms and qualified associates. The growth of fast fashion and value fashion retailers and expansion of off-price retailers has shifted shopper expectations to more affordable pricing of well-known brands and continued promotional pressure. The rise of these retailers as well as the shift in shopping preferences from brick-and-mortar stores to online e-commerce channels has increased the difficulty of maintaining and gaining market share. Increased competition in any of these areas may result in higher costs or otherwise reduce our sales or operating margins. |

8

3. Risks of expanding internationally | Our current growth strategy includes potential expansion of our operations and presence internationally. As part of that strategy, we may face significant costs and challenges including setting up foreign offices, hiring experienced management or franchising partners, maintaining good relations with associates, obtaining prime locations for stores, introducing and marketing our brands, and others. We may be unable to successfully grow our international business, or we may face operational issues that delay our intended pace of international growth, such as an inability to identify suitable franchising partners, identify markets and sites for store locations, address the different operational characteristics present in a new country, negotiate acceptable lease terms, hire, train and retain store personnel, localize our online brand experience and e-commerce capabilities, find vendors that can meet our international merchandise needs, achieve acceptable operating margins, compete with local competitors or adapt to potential different consumer demand and behavior. Any challenges that we encounter may divert financial, operational and managerial resources from our existing operations. In addition, we are subject to certain U.S. laws that may impact our international operations or expansion, including the Foreign Corrupt Practices Act, as well as the laws of the foreign countries in which we operate. Violations of these laws could subject us to sanctions or other penalties that could negatively affect our reputation, business and operating results. |

General Economic Conditions

Numerous economic conditions, all of which are outside of our control, could negatively affect the level of our customers' spending or our costs of operations. If these economic conditions persist for a sustained period, our consolidated financial condition and results of operations could be materially adversely impacted. These economic conditions include, but are not limited to, the following:

Risk | Description |

4. Declines in consumer spending | Consumer spending may decline as a result of: threatened or actual government shut downs, higher unemployment levels, low levels of consumer credit, declines in consumer confidence, inflation, changes in interest rates, recessionary pressures, increasing gas and other energy costs, increased taxes, changes in housing prices, higher durable and other consumer spending, volatility in the financial markets and changes in the political climate or conditions. |

5. Fluctuating costs | Fluctuations in the price, availability and quality of fabrics and other raw materials used to manufacture our products, as well as the price for labor and transportation, may contribute to ongoing pricing pressures throughout our supply chain. The price and availability of such inputs to the manufacturing process may fluctuate significantly, depending on several factors, including commodity costs (such as higher cotton prices), energy costs (such as fuel), shipping costs, inflationary pressures from emerging markets, increased labor costs, weather conditions and currency fluctuations. |

6. Impairment charges | Significant negative industry or general economic trends, changes in customer demand for our product, disruptions to our business and unexpected significant changes or planned changes in our operating results or use of long-lived assets (such as boutique relocations or discontinuing use of certain boutique fixtures) may result in impairments to goodwill, intangible assets and other long-lived assets. |

9

7. Fluctuating comparable sales and operating results | Our comparable sales and overall operating results have fluctuated in the past and are expected to continue to fluctuate in the future. In addition to other factors discussed in this Item 1A., a variety of factors affect comparable sales and operating results, including changes in fashion trends, change in our merchandise mix, customer acceptance of merchandise offerings, the timing of marketing activities, calendar shifts of holiday periods, the periodic impact of a fifty-three week fiscal year, weather conditions and general economic conditions. In addition, our ability to address the current challenges of sustained declining store traffic combined with a highly promotional retail environment may impact our comparable sales, operating results and ability to maintain or gain market share. Past comparable sales or operating results are not an indicator of future results. |

Omni-Channel Operations

Our omni-channel operations (including our websites and catalogs), are a critical part of our customers’ overall experience with our brands and will be a significant contributor to our future business growth and profitability. Our inability or failure to successfully manage and maintain those operations could materially and adversely impact our results of operations. Specific risks include, but are not limited to, the following:

Risk | Description |

8. Reliance on technology | Our brands’ websites are heavily dependent on technology, which creates numerous risks including unanticipated operating problems, system failures, rapid technological change, failure of systems to operate the websites as anticipated, reliance on third party computer hardware and software providers, computer viruses, telecommunication failures, liability for online content, systems and data breaches, denial of service attacks, spamming, phishing attacks, computer hackers and other similar disruptions. Our failure to successfully assess and respond to these risks could negatively impact sales, increase costs and damage the reputation of our brands. |

9. Reliance on the U.S. Postal Service and other shipping vendors | Postal rate increases or a reduction or delay in service could affect the cost of our order fulfillment and catalog and promotional mailings. We use the Postal Service to mail millions of catalogs each year to educate our customers about our products, acquire new customers, drive customers to our boutiques and websites and promote catalog sales. We rely on discounts from the basic postal rate structure, such as discounts for bulk mailings and sorting. We utilize additional shipping vendors, including Federal Express, to support our online operations. Any significant and unanticipated increase in shipping costs, reduction in service, or slow-down in delivery could impair our ability to deliver merchandise in a timely or economically efficient manner. |

Information Technology Systems

In addition to the dependence of our retail websites on technology as discussed above, we also rely on various information technology systems to manage our overall operations, and failure of those systems to operate as expected or a significant interruption in service could materially adversely impact our consolidated financial condition and results of operations. Risks include, but are not limited to, the following:

Risk | Description |

10. Disruptions in current systems or difficulties in integrating new systems | We regularly maintain, upgrade, enhance or replace our information technology systems to support our business strategies and provide business continuity. Replacing legacy systems with successor systems, making changes to existing systems or acquiring new systems with new functionality have inherent risks including disruptions, delays, gaps in functionality, user acceptance, adequate user training, or other difficulties that may impair the effectiveness of our information technology systems. |

10

11. Cybersecurity | We are subject to cybersecurity risks. Cybersecurity refers to the combination of technologies, processes and procedures established to protect information technology systems and data from unauthorized access, attack, exfiltration, loss or damage. Our business involves the storage and/or transmission of customers’ personal information, shipping preferences and credit card information, as well as confidential information regarding our business, employees and third parties. In addition, as part of our acceptance of customers’ debit and credit cards as forms of payment, we are required to comply with the Payment Card Industry Data Security Standards (“PCI”). While we have implemented measures reasonably designed to prevent security breaches and cyber incidents, and while we have taken steps to comply with PCI, those measures may not be effective. A breach or cyber incident could result in the loss or misuse of data and could result in fines, penalties, damages, loss of business, reputational damage or loss of our ability to accept debit and credit cards as forms for payment. In addition, changes in laws or regulations, or in the PCI standards, could result in cost increases due to system or administrative charges. |

Sourcing and Distribution Strategies

Our sourcing and distribution strategies are subject to numerous risks that could materially adversely impact our consolidated financial condition and results of operations. These risks include, but are not limited to, the following:

Risk | Description |

12. Reliance on foreign sources of production | The majority of the merchandise we sell is produced outside the United States. As a result, our business remains subject to the various risks of doing business in foreign markets and importing merchandise from abroad, such as: geo-political instability; non-compliance with the Foreign Corrupt Practices Act and other anti-corruption laws and regulations; potential changes to the North American Free Trade Agreement; imposition of new legislation relating to import quotas; imposition of new or increased duties, taxes, or other charges on imports, such as the proposed Border Adjustment Tax; foreign exchange rate challenges and pressures presented by implementation of U.S. monetary policy; challenges from local business practices or political issues; transportation disruptions; our shift to a predominantly FOB (free on board) shipping structure rather than predominantly DDP (delivered duty paid); natural disasters; delays in the delivery of cargo due to port security considerations or government funding; seizure or detention of goods by U.S. Customs authorities; or a reduction in the availability of shipping sources caused by industry consolidation or other reasons. We continue to source a substantial portion of our merchandise from Asia, including China. A change in exchange rates, labor laws or policies affecting the costs of goods in Asia could negatively impact our merchandise costs. Furthermore, delays in production or shipping product, whether due to work slow-downs, work stoppages, strikes, port congestion, labor disputes, product regulations and customs inspections or other factors, could have a negative impact. We cannot predict whether or not any of the foreign countries in which our clothing and accessories are produced will be subject to import restrictions or taxes by the United States government. Trade restrictions, including increased tariffs, or more restrictive quotas, including safeguard quotas, or anything similar, applicable to apparel items could affect the importation of apparel generally and, in that event, could increase the cost, or reduce the supply, of apparel available to us. |

13. Our suppliers’ inability to provide quality goods in a timely manner | We are subject to risk because we do not own or operate any manufacturing facilities and depend on independent third parties to manufacture our merchandise. A key supplier may become unable to address our merchandising needs for a variety of reasons. If we were unexpectedly required to change suppliers or if a key supplier were unable to supply acceptable merchandise in sufficient quantities on acceptable terms, we could experience a significant impact to the supply or cost of merchandise. |

11

14. Reliance upon one supplier | Approximately 23% of total purchases in fiscal 2016 and 23% of total purchases in 2015 were made from one supplier, and we cannot guarantee that this relationship will be maintained in the future or that the supplier will continue to be available to supply merchandise. However, we have no material long-term or exclusive contract with any apparel or accessory manufacturer or supplier. Our business depends on our network of suppliers and our continued good relations with them. |

15. Our suppliers’ failure to implement acceptable labor practices | Although we have adopted our Terms of Commitment to Ethical Sourcing and use the services of third party audit firms to monitor compliance with these terms, some of our independent suppliers may not be in complete compliance with our guidelines at all times. The violation of labor or other laws by any of our key independent suppliers or the divergence of an independent supplier’s labor practices from those generally accepted by us as ethical could interrupt or otherwise disrupt the shipment of finished merchandise or damage our reputation. |

16. Reliance on one location to distribute goods for our brands | The distribution functions for all of our brands are handled from our DC in Winder, Georgia and a significant interruption in the operation of that facility due to natural disasters, severe weather, accidents, system failures or other unforeseen causes could delay or impair our ability to distribute merchandise to our stores and/or fulfill online or catalog orders. |

Other Risks Factors

Our business is subject to numerous other risks that could materially adversely impact our consolidated financial condition and results of operations. These risks include, but are not limited to, the following:

Risk | Description |

17. Failure to comply with applicable laws and regulations | Our policies, procedures and internal controls are designed to help us comply with all applicable foreign and domestic laws, accounting and reporting requirements, regulations and tax requirements, including those imposed by the Sarbanes-Oxley Act of 2002, the Dodd-Frank Wall Street Reform and Consumer Protection Act, the Foreign Corrupt Practices Act, The Patient Protection and Affordable Care Act, the SEC and the New York Stock Exchange (“NYSE”), as well as applicable employment laws. We could be subject to legal or regulatory action in the event of our failure to comply, which could be expensive to defend and resolve and be disruptive to our business. Any changes in regulations, the imposition of additional regulations or the enactment of any new legislation that affects us may increase the complexity of the legal and regulatory environment in which we operate and the related costs of compliance. |

18. Adverse outcomes of litigation matters | We are involved in litigation and other claims against our business. These matters arise primarily in the ordinary course of business but could raise complex factual and legal issues, presenting multiple risks and uncertainties and requiring significant management time. At this time, we believe that our current litigation matters will not have a material adverse effect on the consolidated results of operations or financial condition. However, our assessment could change in light of the discovery of facts with respect to pending or potential legal actions against us, not presently known to us, or determinations by judges, juries or other finders of fact which are inconsistent with our evaluation of the possible liability or outcome of such litigation. In addition, we may be subject to litigation which has not yet been filed. |

19. Our inability to retain or recruit key personnel | Our success and ability to properly manage our business depends to a significant extent upon our ability to attract, develop and retain qualified employees, including executive and senior management and talented merchants. Competition for talented employees within our industry is intense. Failure to recruit and retain such personnel and implement appropriate succession planning, including the transition of new executives, particularly at the CEO and executive level, could jeopardize our continued and sustained success. |

12

20. Our inability to achieve the results of our restructuring program | During the fourth quarter of fiscal 2014, we initiated a multi-year restructuring program, including the acceleration of domestic store closures and an organizational realignment, to ensure that resources align with long-term growth initiatives. The Company has substantially completed this restructuring program; however, the benefits associated with the restructuring program may vary materially from estimates as a result of various factors including: the timing and success in execution of the restructuring program, outcome of negotiations with landlords and other third parties, inventory levels, and changes in management’s assumptions and projections. As a result of these events and circumstances, delays and unexpected costs may occur, which could result in our not realizing some of the anticipated benefits of the restructuring program. |

21. Our inability to achieve the results of our strategic initiatives | During the first quarter of fiscal 2016, we announced significant initiatives designed to further align the organizational structure for long-term growth and to reduce COGS and SG&A. These initiatives require substantial internal change and effort, including reductions and changes in personnel and significant adjustments in how we design and source product and how we ultimately present it to our customers. While we are confident that these initiatives are appropriate for the long-term viability and success of our business, they may not deliver all of the results we expect. Moreover, the process of implementing them places significant stress on the Company and could result in unexpected short-term disruptions or negative impacts to our business, including, by way of example: • Unintended loss of key personnel or unexpected delay in the hiring of personnel whose expertise is needed for the successful implementation of the initiatives. • Disruption to our current business processes as we migrate to the new processes, or failure to successfully migrate to those new processes, which could negatively impact product flow, product quality or inventory levels. • Inadvertent lapses or failures in our process, compliance or financial controls as we implement the new initiatives. In addition, there is no assurance that we can complete the implementation of all of these initiatives in the manner or in the time-frame planned, or that, once implemented, they will result in the expected increases in the efficiency or productivity of our business. |

22. Our inability to operate our business within our financial covenants or to replace our credit facility | Our revolving credit agreement and term loan contain various affirmative and negative covenants that may restrict the ability of the Company to incur indebtedness, grant liens, engage in mergers, make certain investments, pay dividends or distributions on our common stock or enter into sales-leaseback transactions. The agreement also contains financial covenants that require the Company to maintain certain financial ratios. The ability of the Company to comply with these provisions may be affected by events beyond our control. Failure to comply with these covenants could result in an event of default which, if not cured or waived, could accelerate the Company's repayment obligations. Also, the inability to obtain credit on commercially reasonable terms in the future when this facility expires could adversely impact our liquidity and results of operations. In addition, market conditions could potentially impact the size and terms of a replacement facility or facilities. |

23. War, terrorism or other catastrophes | In the event of war, acts of terrorism or the threat of terrorist attacks, public health crises, or weather catastrophes, consumer spending could significantly decrease for a sustained period. In addition, local authorities or shopping center management could close in response to any immediate security concern, public health concern or weather catastrophe such as hurricanes, earthquakes, or tornadoes. Similarly, war, acts of terrorism, threats of terrorist attacks, or a weather catastrophe could severely and adversely affect our National Store Support Center (“NSSC”) campus, our Distribution Center, or our entire supply chain. |

13

24. Our inability to protect our brands’ reputation | Our ability to protect our brands’ reputation is an integral part of our general success strategy and is critical to the overall value of the brands. If we fail to maintain high standards for merchandise quality and integrity in our business conduct or fail to address other risk factors, such failures could jeopardize our brands' reputations. Consumers value readily available information from social media and other sources concerning retailers and their goods and services and many times act on such information without further investigation in regards to its accuracy. Any negative publicity, whether true or not, may affect our reputation and brand and, consequently, reduce demand for our merchandise, decrease customer and investor loyalty, and affect our vendor relationships. |

25. Our inability to protect our intellectual property | While we devote significant resources to the protection of our intellectual property, others may still attempt to imitate our products or infringe upon our intellectual property rights. Other parties may also claim that some of our products infringe on their trademarks, copyrights, or other intellectual property rights. In addition, the intellectual property laws and enforcement practices in many foreign countries can be substantially different from those in the United States. There are also inherent challenges with enforcing intellectual property rights on third party e-commerce websites, especially those based in foreign jurisdictions. We have taken steps to protect and enforce our intellectual property rights in these arenas, but cannot guarantee that such rights are not infringed. |

26. Stock price volatility | The market price of our common stock has fluctuated substantially in the past and may continue to do so in the future. Future announcements or management discussions concerning us or our competitors, sales and profitability results, quarterly variations in operating results or comparable sales, changes in earnings estimates by analysts or the failure of investors or analysts to understand our business strategies or fundamental changes in our business or sector, among other factors, could cause the market price of the common stock to fluctuate substantially. In addition, stock markets, in general, have experienced extreme price and volume volatility in recent years. This volatility has had a substantial effect on the market prices of securities of many public companies for reasons frequently unrelated to the operating performance of the specific companies. |

27. Our business could be impacted as a result of actions by activist shareholders or others | From time to time, we may be subject to legal and business challenges in the operation of our Company due to proxy contests, shareholder proposals, media campaigns and other such actions instituted by activist shareholders or others. Responding to such actions is costly and time-consuming, disrupts our operations, may not align with our business strategies and may divert the attention of our Board of Directors and senior management from the pursuit of current business strategies. Perceived uncertainties as to our future direction or changes to the composition of our Board of Directors as a result of shareholder activism may lead to the perception of instability in the organization and its future and may make it more difficult to attract and retain qualified personnel and business partners. |

28. Disadvantageous lease obligations and commercial retail consolidation | We have, and will continue to have, significant lease obligations. If an existing or future store is not profitable, and we decide to close it, we may nonetheless be committed to fulfill our obligations under the applicable lease including paying the base rent for the balance of the lease term. Additionally, continued consolidation in the commercial retail real estate market could affect our ability to successfully negotiate favorable rental terms for our stores in the future and could concentrate our leases with fewer landlords who may then be in a position to dictate unfavorable terms to us due to their significant negotiating leverage. If we are unable to enter into new leases or renew existing leases on terms acceptable to us or be released from our obligations under leases for stores that we close this could affect our ability to profitably operate our stores. |

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

14

ITEM 2. | PROPERTIES |

Stores

At fiscal year-end for 2016, 2015 and 2014 our total consolidated selling square feet was 3.6 million, 3.7 million and 3.7 million, respectively. For a general description of our leases, see Note 1 to our financial statements under the heading "Operating Leases." As of January 28, 2017, our 1,501 stores were located in 48 states, the U.S. Virgin Islands, Puerto Rico and Canada, as follows:

Alabama | 20 | Maine | 4 | Oklahoma | 15 | |||||

Arizona | 34 | Maryland | 40 | Oregon | 17 | |||||

Arkansas | 12 | Massachusetts | 34 | Pennsylvania | 70 | |||||

California | 150 | Michigan | 36 | Rhode Island | 5 | |||||

Colorado | 24 | Minnesota | 28 | South Carolina | 35 | |||||

Connecticut | 23 | Mississippi | 12 | South Dakota | 4 | |||||

Delaware | 8 | Missouri | 30 | Tennessee | 34 | |||||

Florida | 127 | Montana | 6 | Texas | 136 | |||||

Georgia | 56 | Nebraska | 10 | Utah | 11 | |||||

Hawaii | 1 | Nevada | 21 | Vermont | 1 | |||||

Idaho | 6 | New Hampshire | 6 | Virginia | 48 | |||||

Illinois | 64 | New Jersey | 51 | Washington | 29 | |||||

Indiana | 24 | New Mexico | 8 | West Virginia | 4 | |||||

Iowa | 7 | New York | 62 | Wisconsin | 18 | |||||

Kansas | 14 | North Carolina | 48 | U.S. Virgin Islands | 1 | |||||

Kentucky | 17 | North Dakota | 5 | Puerto Rico | 8 | |||||

Louisiana | 21 | Ohio | 46 | Ontario, Canada | 10 | |||||

NSSC and Distribution Centers

Our NSSC is located on approximately 65 acres in Fort Myers, Florida and consists of approximately 504,000 square feet of office space. Our distribution center is located on approximately 110 acres in Winder, Georgia and consists of approximately 583,000 square feet of distribution, fulfillment, call center and office space.

ITEM 3. | LEGAL PROCEEDINGS |

In July 2015, the Company was named as a defendant in Altman v. White House Black Market, Inc., a putative class action filed in the United States District Court for the Northern District of Georgia. The Complaint alleges that the Company, in violation of federal law, published more than the last five digits of a credit or debit card number or an expiration date on customers' receipts. The Company denies the material allegations of the complaint. Its motion to dismiss was denied on July 13, 2016, but the Company continues to believe that the case is without merit and is not appropriate for class treatment. It will continue to vigorously defend the matter. At this time, it is not possible to predict whether the proceeding will be permitted to proceed as a class or the size of the putative class, and no assurance can be given that the Company will be successful in its defense on the merits or otherwise. No specific dollar amount in damages or other relief is specified in the Complaint, and the Company is unable to estimate any potential loss or range of loss. However, if the case were to proceed as a class action and the Company were to be unsuccessful in its defense on the merits, the ultimate resolution of the case could have a material adverse effect on the Company’s consolidated financial condition.

In June 2015, the Company was named as a defendant in Ackerman v. Chico’s FAS, Inc., a putative representative Private Attorney General action filed in the Superior Court of California, County of Los Angeles. The Complaint alleges numerous violations of California law related to wages, meal periods, rest periods, wage statements and failure to reimburse business expenses, among other things. Plaintiff subsequently amended her complaint to make the same allegations on a class action basis. In June 2016, the parties submitted a proposed settlement of the matter to the court, and the court granted preliminary approval on August 26, 2016, and settlement notices have been distributed. If finally approved, the proposed settlement will not have a material adverse effect on the Company’s consolidated financial condition or results of operations.

15

In March 2016, the Company was named as a defendant in Cunningham v. Chico’s FAS, Inc., a putative class action filed in the Superior Court of California, County of San Diego. The Complaint alleged many of the same Labor Code violations as Ackerman, described above. Given the overlap with the Ackerman case, the Court stayed the matter pending final approval of the Ackerman proposed settlement. In October 2016, the parties agreed to lift the stay and to resolve the matter as an individual action. The Court has since dismissed the case. The settlement amount was immaterial.

In June 2016, the Company was named as a defendant in Rodems v. Chico’s FAS, Inc., a putative class action filed in the Superior Court of California, County of Fresno. The Complaint alleged many of the same Labor Code violations as Ackerman, described above. Given the overlap with the Ackerman case, the court stayed the matter pending final approval of the Ackerman proposed settlement. The Company and the plaintiff subsequently agreed to a lifting of the stay and a filing of an amended complaint in early November. The Company removed the case to the United States District Court for the Eastern District of California on November 9, 2016. In the First Amended Complaint, the plaintiffs make similar claims, but only on behalf of three individuals, and they do not seek class status. The Company disputes the allegations of the First Amended Complaint and, as the matter is no longer a putative class action, is confident that this case will not have a material adverse effect on the Company’s consolidated financial condition or results of operation.

In July 2016, the Company was named as a defendant in Calleros v. Chico’s FAS, Inc., a putative class action filed in the Superior Court of California, County of Santa Barbara. Plaintiff alleges that the Company failed to comply with California law requiring it to provide consumers cash for gift cards with a stored value of less than $10.00. Following voluntary mediation of the matter in November of 2016, the parties entered into a settlement agreement, which is subject to court review and approval. If finally approved, the settlement will not have a material adverse effect on the Company’s consolidated financial condition or results of operation.

Other than as noted above, we are not currently a party to any legal proceedings, other than various claims and lawsuits arising in the normal course of business, none of which we believe should have a material adverse effect on our consolidated financial condition or results of operations.

ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

16

PART II

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our Common Stock trades on the NYSE under the symbol “CHS”. On February 24, 2017, the last reported sale price of the Common Stock on the NYSE was $14.75 per share. The number of holders of record of common stock on February 24, 2017 was 1,218.

The following table sets forth, for the periods indicated, the range of high and low sale prices for the Common Stock, as reported on the NYSE:

For the Fiscal Year Ended January 28, 2017 | |||||||

High | Low | ||||||

Fourth Quarter (October 30, 2016 – January 28, 2017) | $ | 16.70 | $ | 11.28 | |||

Third Quarter (July 30, 2016 – October 29, 2016) | 12.68 | 11.23 | |||||

Second Quarter (May 1, 2016 – July 30, 2016) | 12.72 | 10.15 | |||||

First Quarter (January 31, 2016 - April 30, 2016) | 13.27 | 9.73 | |||||

For the Fiscal Year Ended January 30, 2016 | |||||||

High | Low | ||||||

Fourth Quarter (November 1, 2015 – January 30, 2016) | $ | 13.77 | $ | 9.69 | |||

Third Quarter (August 2, 2015 – October 31, 2015) | 17.00 | 13.68 | |||||

Second Quarter (May 3, 2015 – August 1, 2015) | 17.29 | 14.97 | |||||

First Quarter (February 1, 2015 - May 2, 2015) | 18.38 | 16.60 | |||||

In fiscal 2016, we declared four quarterly dividends of $0.08 per share, resulting in an annualized dividend of $0.32 per share. In fiscal 2015, we declared four quarterly dividends of $0.0775 per share, resulting in an annualized dividend of $0.31 per share.

On February 22, 2017, we announced that our Board of Directors declared a quarterly dividend of $0.0825 per share on our common stock. The dividend will be payable on March 27, 2017 to shareholders of record at the close of business on March 13, 2017.

In fiscal 2015, we executed accelerated share repurchase agreements ( the “ASR Agreements”) and purchased $250 million of the Company's common stock under our $300 million share repurchase authorization announced in December 2013. In November 2015, we announced a new $300 million share repurchase authorization for the Company's common stock and canceled the remainder of the December 2013 authorization, which had $40 million remaining. During the fourth quarter of fiscal 2016, we repurchased 1.6 million shares of the Company's common stock, for a total fiscal 2016 repurchase of 8.1 million shares at approximately $96.4 million. There was approximately $163.6 million remaining under the program at the end of fiscal 2016. The repurchase program has no specific termination date and will expire when we have repurchased all securities authorized for repurchase thereunder, unless terminated earlier by our Board of Directors.

17

In fiscal 2016, we repurchased 430,499 restricted shares in connection with employee tax withholding obligations under employee compensation plans, of which 35,447 were repurchased in the fourth quarter and are included in the following chart (amounts in thousands except share and per share amounts):

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Publicly Announced Plans | |||||||||

October 30, 2016 – November 26, 2016 | 1,184,607 | $ | 12.18 | 1,180,341 | $ | 169,292 | |||||||

November 27, 2016 – December 31, 2016 | 299,002 | $ | 14.93 | 268,858 | $ | 165,289 | |||||||

January 1, 2017 – January 28, 2017 | 115,807 | $ | 14.36 | 114,770 | $ | 163,642 | |||||||

Total | 1,599,416 | $ | 12.85 | 1,563,969 | |||||||||

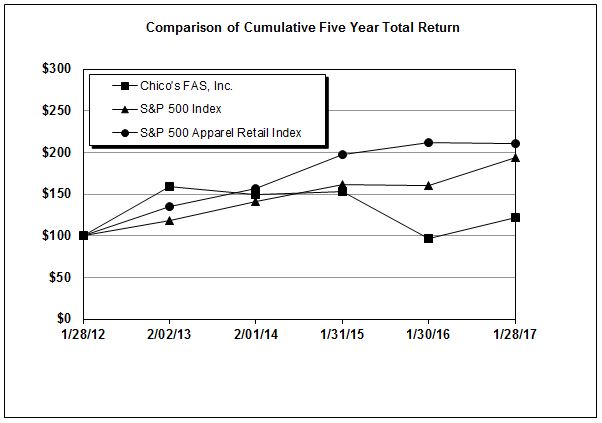

Five Year Performance Graph

The following graph compares the cumulative total return on our common stock with the cumulative total return of the companies in the Standard & Poor’s (“S&P”) 500 Index and the Standard & Poor’s 500 Apparel Retail Index. Cumulative total return for each of the periods shown in the Performance Graph is measured assuming an initial investment of $100 on January 28, 2012 and the reinvestment of dividends.

01/28/12 | 02/02/13 | 02/01/14 | 01/31/15 | 01/30/16 | 01/28/17 | ||||||||||||||||||

Chico’s FAS, Inc. | $ | 100 | $ | 159 | $ | 149 | $ | 153 | $ | 97 | $ | 122 | |||||||||||

S&P 500 Index | $ | 100 | $ | 118 | $ | 141 | $ | 162 | $ | 161 | $ | 194 | |||||||||||

S&P 500 Apparel Retail Index | $ | 100 | $ | 135 | $ | 156 | $ | 197 | $ | 212 | $ | 211 | |||||||||||

18

ITEM 6. | SELECTED FINANCIAL DATA |

Selected Financial Data at the dates and for the periods indicated should be read in conjunction with, and is qualified in its entirety by reference to the consolidated financial statements and the notes thereto referenced in this Annual Report on Form 10-K. Amounts in the following tables are in thousands, except per share data, and number of stores data.

Fiscal Year | |||||||||||||||||||

2016 (52 weeks) | 2015 (52 weeks) | 2014 (52 weeks) | 2013 (52 weeks) | 2012 (53 weeks) | |||||||||||||||

(dollars in thousands) | |||||||||||||||||||

Summary of operations:1 | |||||||||||||||||||

Net sales | $ | 2,476,410 | $ | 2,660,635 | $ | 2,693,929 | $ | 2,604,411 | $ | 2,590,024 | |||||||||

Gross margin | 946,836 | 1,026,871 | 1,034,238 | 1,049,353 | 1,124,060 | ||||||||||||||

Gross margin as a percent of net sales | 38.2 | % | 38.6 | % | 38.4 | % | 40.3 | % | 43.4 | % | |||||||||

Income from operations | 140,702 | (13,084 | ) | 116,343 | 141,183 | 287,538 | |||||||||||||

Income from operations as a percent of net sales | 5.7 | % | (0.5 | )% | 4.3 | % | 5.5 | % | 11.1 | % | |||||||||

Net income | 91,229 | 1,946 | 64,641 | 65,883 | 180,219 | ||||||||||||||

Net income as a percent of net sales | 3.7 | % | 0.1 | % | 2.4 | % | 2.5 | % | 6.9 | % | |||||||||

Per share data: | |||||||||||||||||||

Net income per common share-basic | $ | 0.69 | $ | 0.01 | $ | 0.42 | $ | 0.41 | $ | 1.09 | |||||||||

Net income per common and common equivalent share–diluted | $ | 0.69 | $ | 0.01 | $ | 0.42 | $ | 0.41 | $ | 1.08 | |||||||||

Weighted average common shares outstanding–basic | 128,995 | 138,366 | 148,622 | 155,048 | 162,989 | ||||||||||||||

Weighted average common and common equivalent shares outstanding–diluted | 129,237 | 138,741 | 149,126 | 155,995 | 164,119 | ||||||||||||||

Cash dividends per share | $ | 0.32 | $ | 0.31 | $ | 0.30 | $ | 0.24 | $ | 0.21 | |||||||||

Balance sheet data (at year end): | |||||||||||||||||||

Cash and marketable securities | $ | 192,505 | $ | 140,145 | $ | 259,912 | $ | 152,446 | $ | 329,358 | |||||||||

Total assets | 1,108,994 | 1,166,052 | 1,438,581 | 1,371,191 | 1,580,628 | ||||||||||||||

Working capital | 174,766 | 167,190 | 255,405 | 167,568 | 282,913 | ||||||||||||||

Long-term debt | 68,535 | 82,219 | — | — | — | ||||||||||||||

Stockholders’ equity | 609,173 | 639,788 | 943,621 | 909,103 | 1,093,199 | ||||||||||||||

Other selected operating data: | |||||||||||||||||||

Percentage (decrease) increase in comparable sales | (3.7 | )% | (1.5 | )% | 0.0 | % | (1.8 | )% | 7.2 | % | |||||||||

Purchases of property and equipment, net | $ | 47,836 | $ | 84,841 | $ | 119,817 | $ | 138,510 | $ | 164,690 | |||||||||

Total depreciation and amortization | 109,251 | 118,800 | 122,269 | 118,303 | 108,471 | ||||||||||||||

Goodwill and trade name impairment, pre-tax charges | — | 112,455 | 30,100 | 72,466 | — | ||||||||||||||

Restructuring and strategic charges, pre-tax | 31,027 | 48,801 | 16,745 | — | — | ||||||||||||||

Total stores at year end | 1,501 | 1,518 | 1,547 | 1,472 | 1,357 | ||||||||||||||

Total selling square feet (in thousands) | 3,612 | 3,652 | 3,706 | 3,547 | 3,271 | ||||||||||||||

____________________________

1 | Five-year table includes the operating results of Boston Proper through fiscal 2015. |

19

ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following discussion and analysis should be read in conjunction with the consolidated financial statements and notes thereto. References herein to “Notes” refer to the Notes to our consolidated financial statements.

EXECUTIVE OVERVIEW

We are a leading omni-channel specialty retailer of women’s private branded, sophisticated, casual-to-dressy clothing, intimates and complementary accessories, operating under the Chico’s, White House Black Market (“WHBM”) and Soma brand names. We earn revenues and generate cash through the sale of merchandise in our domestic and international retail stores, our various websites and our call center, which takes orders for all of our brands, and through an unaffiliated franchise partner in Mexico.

We utilize an integrated, omni-channel approach to managing our business. We want our customers to experience our brands, not limited to a channel within our brands, and view our various sales channels as a single, integrated process rather than as separate sales channels operating independently. This approach allows our customers to browse, purchase, return, or exchange our merchandise through whatever sales channel and at whatever time is most convenient. As a result, we track total sales and comparable sales on a combined basis.

2016 Financial Highlights |

• Earnings per share of $0.69 compared to $0.01 last year |

• $138.7 million returned to shareholders, consisting of $96.4 million in share repurchases and $42.3 million in dividends |

• Reduction in SG&A of 180 basis points as a percent of sales |

• Decrease in inventory, reflecting improved management |

• Generated approximately $30 million savings from cost reduction and operating efficiency initiatives |

Income from Operations and Select Charges

The following table depicts income from operations and select charges for fiscal 2016, 2015, and 2014:

Fiscal 2016 | Fiscal 2015 | Fiscal 2014 | |||||||||

(dollars in millions) | |||||||||||

Income from operations | $ | 140.7 | $ | (13.1 | ) | $ | 116.3 | ||||

Restructuring and strategic charges | $ | 31.0 | $ | 48.8 | $ | 16.7 | |||||

Goodwill and intangible impairment charges | $ | — | $ | 112.5 | $ | 30.1 | |||||

Earnings per diluted share for fiscal 2016 was $0.69 compared to $0.01 in fiscal 2015. The change in earnings per share reflects the increase in net income and the impact of share repurchases in fiscal 2016.

Key Initiatives |

The initiatives announced in fiscal 2016 included: |

• realigning marketing and digital commerce functions, placing the decision makers directly into the Company's three brands |

• completing an organizational redesign, including transition of key executive leadership |

• improving supply chain efficiency, reducing non-merchandise expenses and optimizing marketing spend |

20

Future Outlook |

For the full year of fiscal 2017, the Company is anticipating: |

• a low single-digit percentage decline in comparable sales |

• gross margin and SG&A leverage |

• approximately 10 store openings and 50 store closings |

• $50 million savings from cost reduction and operating efficiency initiatives |

RESULTS OF OPERATIONS

Net Sales

The following table depicts net sales by Chico’s, WHBM, Soma and Boston Proper in dollars and as a percentage of total net sales for fiscal 2016, 2015, and 2014:

Net sales: | Fiscal 2016 | % | Fiscal 2015 | % | Fiscal 2014 | % | ||||||||||||||

(dollars in millions) | ||||||||||||||||||||

Chico’s | $ | 1,286 | 51.9 | % | $ | 1,364 | 51.3 | % | $ | 1,385 | 51.4 | % | ||||||||

WHBM | 846 | 34.2 | % | 875 | 32.9 | % | 892 | 33.1 | % | |||||||||||

Soma | 344 | 13.9 | % | 335 | 12.6 | % | 314 | 11.6 | % | |||||||||||

Boston Proper1 | — | — | 87 | 3.2 | % | 103 | 3.9 | % | ||||||||||||

Total net sales | $ | 2,476 | 100.0 | % | $ | 2,661 | 100.0 | % | $ | 2,694 | 100.0 | % | ||||||||

1We completed the sale of the Boston Proper direct-to-consumer business and closed all Boston Proper stores in fiscal 2015.

For fiscal 2016, net sales were $2.5 billion compared to $2.7 billion in fiscal 2015. This decrease of 6.9% included $87.0 million related to Boston Proper last year. When excluding Boston Proper from fiscal 2015, net sales decreased 3.8%, primarily reflecting a decline in comparable sales of 3.7%, comprised of reduced transaction count and lower average dollar sale. Comparable sales is defined as sales from stores open for the preceding twelve months, including stores that have been expanded, remodeled, or relocated within the same general market and includes online and catalog sales. International and Boston Proper sales are excluded from comparable sales calculations.

Net sales decreased 1.2% in fiscal 2015 to $2.7 billion from $2.7 billion in fiscal 2014, primarily reflecting a 1.5% decrease in comparable sales, partially offset by the full year benefit of 2014 new store openings. The 2015 comparable sales reflected a decrease in average dollar sale and flat transaction count.

The following table depicts comparable sales percentages for Chico's, WHBM and Soma for fiscal 2016, 2015 and 2014:

Fiscal 2016 | Fiscal 2015 | Fiscal 2014 | ||||||

Chico's | (5.3 | )% | (2.0 | )% | (0.5 | )% | ||

WHBM | (2.8 | )% | (2.5 | )% | (1.7 | )% | ||

Soma | 0.5 | % | 3.1 | % | 8.0 | % | ||

Total Company | (3.7 | )% | (1.5 | )% | 0.0 | % | ||

21

Cost of Goods Sold/Gross Margin

The following table depicts cost of goods sold and gross margin in dollars and gross margin as a percentage of net sales for fiscal 2016, 2015 and 2014:

Fiscal 2016 | Fiscal 2015 | Fiscal 2014 | |||||||||

(dollars in millions) | |||||||||||

Cost of goods sold | $ | 1,530 | $ | 1,634 | $ | 1,660 | |||||

Gross margin | $ | 947 | $ | 1,027 | $ | 1,034 | |||||

Gross margin percentage | 38.2 | % | 38.6 | % | 38.4 | % | |||||

For fiscal 2016, gross margin was $947 million, or 38.2%, compared to $1,027 million, or 38.6%, in fiscal 2015. When excluding Boston Proper from fiscal 2015, gross margin decreased 60 basis points in fiscal 2016 compared to gross margin of $1,000 million, or 38.8%, last year. This 60 basis point decrease from the 2015 adjusted gross margin rate primarily reflects deleverage of occupancy costs and incentive compensation, partially offset by an improvement in merchandise margin.

For fiscal 2015, gross margin was $1,027 million compared to $1,034 million in fiscal 2014. As a percentage of net sales, gross margin was 38.6%, a 20 basis point increase from fiscal 2014, primarily reflecting a decrease in promotional activity in response to improved inventory management in fiscal 2015. When excluding Boston Proper in fiscal 2015 and fiscal 2014, gross margin was $1,000 million and $997 million, or 38.8% and 38.5% of net sales, respectively.

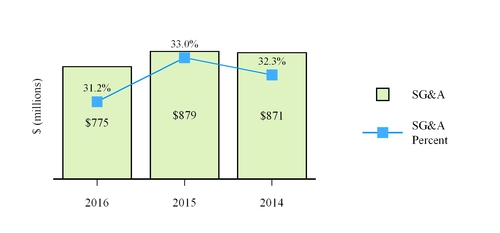

Selling, General and Administrative Expenses