As filed with the Securities and Exchange Commission on November 25, 2020

Registration No. 333-[●]

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

FORM S-3

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

____________________________

DPW HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 3679 | 94-1721931 | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

201 Shipyard Way, Suite E

Newport Beach, CA 92663

(949) 444-5464

(Address, including zip code, and telephone number,

including area code, of principal executive offices)

Milton C. Ault III

Chairman and Chief Executive Officer

DPW Holdings, Inc.

201 Shipyard Way, Suite E

Newport Beach, CA 92663

(949) 444-5464

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to:

|

Henry Nisser, Esq. Executive Vice President and General Counsel DPW Holdings, Inc. 100 Park Ave., Suite 1658A New York, NY 10017 (646) 650-5044 |

Kenneth Schlesinger, Esq. Olshan Frome Wolosky LLP 1325 Avenue of the Americas, 15th Floor New York, NY 10019 (212) 451-2300 |

Approximate date of commencement of proposed sale to the public: As soon as practicable on or after the effective date of this registration statement.

If the only securities being registered on this form are being offered pursuant to dividend or interest reinvestment plans, please check the following box ¨

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in connection with dividend or interest reinvestment plans, check the following box. x

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a registration statement pursuant to General Instruction I.D. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ¨

If this form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.D. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer x | Smaller reporting company x |

| Emerging growth company ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ¨

CALCULATION OF REGISTRATION FEE

| Amount to be | Proposed maximum | Amount of | ||||||||||

| Title of each class of securities to be registered | registered(1) | aggregate offering price (2) | registration fee | |||||||||

| Common Stock underlying Convertible Note | 155,660 | $ | 314,433 | $ | 34.30 | |||||||

| Common Stock underlying Warrants | 4,905,629 | $ | 9,909,371 | $ | 1,081.11 | |||||||

| TOTAL | 5,061,289 | $ | 10,223,804 | $ | 1,115.41 | |||||||

(1) Pursuant to Rule 416 under the Securities Act of 1933, as amended (the “Securities Act”), the shares of common stock offered hereby also include an indeterminate number of additional shares of common stock as may from time to time become issuable by reason of stock splits, stock dividends, recapitalizations or other similar transactions.

(2) With respect to the shares of common stock offered by the selling stockholders named herein, the offering price has been estimated at $2.02 per share, the average of the high and low prices as reported on the NYSE American on November 20, 2020, for the purpose of calculating the registration fee in accordance with Rule 457(c) under the Securities Act.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the Securities and Exchange Commission declares our registration statement effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED NOVEMBER 25, 2020

PRELIMINARY PROSPECTUS

DPW HOLDINGS, INC.

Up to 5,061,289 Shares of Common Stock

Consisting of

Up to 155,660 Shares of Common Stock Issuable upon Conversion of a Note

Up to 4,905,629 Shares of Common Stock Issuable upon Exercise of Warrants

This prospectus relates to the resale or other disposition from time to time of up to 5,061,289 shares of our common stock to be offered by the persons and entities listed as selling stockholders in this prospectus, consisting of: (i) 155,660 shares of common stock issuable upon the conversion of a convertible note (the “Conversion Shares”) and (ii) 4,905,629 shares of common stock (the “Warrant Shares”) issuable upon the exercise of warrants, as described in the following transactions.

• On February 10, 2020, we entered into a Master Exchange Agreement (the “Exchange Agreement”) with Esousa Holdings, LLC (“Esousa”) pursuant to which, among other items, it acquired approximately $4.2 million in certain promissory notes, including accrued but unpaid interest, that had been previously issued by us to other entities. Pursuant to the Exchange Agreement, we issued Esousa a warrant to purchase 1,832,597 shares of common stock (the “MEA Warrant”).

• Beginning on February 27, 2020 and ending on July 24, 2020, we issued certain promissory notes (the “Esousa Term Notes”) to Esousa. In connection with the issuance of the Esousa Term Notes, we agreed to issue to Esousa, upon approval of the NYSE American, LLC (the “NYSE American”), warrants to purchase an aggregate of 1,536,655 shares of common stock (the “Esousa Term Warrants”).

• On April 14, 2020, we issued to Jess Mogul (i) a convertible promissory note in the principal amount of $100,000 and (ii) a warrant to purchase up to 45,242 shares of common stock (the “Mogul Warrant”).

• On May 28, 2020, we entered into a securities purchase and exchange agreement with Cavalry Fund I LP providing for the (i) the exchange of an outstanding secured promissory note, (ii) the issuance of a promissory note, and (iii) a warrant to purchase 400,000 shares of common stock (the “Cavalry Warrant”).

• On June 26, 2020, we issued to several institutional investors promissory notes (the “EMF Notes”) in the aggregate principal face amount of $800,000. In connection therewith, we delivered to the investors warrants (the “EMF Warrants”) to purchase an aggregate of up to 361,991 shares of common stock at an exercise price of $2.43. The EMF Warrants may be exercised via cashless exercise at the option of the Investors. If the Investors elect to exercise the EMF Warrants on a cashless basis, then we would be required to issue up to an aggregate of 1,091,135 shares of common stock.

• On August 21, 2020, we issued to JLA Realty Associates, LLC a convertible promissory note in the principal amount of $330,000 (the “JLA Note”) convertible into 155,660 shares of common stock.

The selling stockholders may, from time to time, sell, transfer or otherwise dispose of any or all of their shares of our common stock on any stock exchange, market or trading facility on which the shares are traded or in private transactions. These dispositions may be at fixed prices, at prevailing market prices at the time of sale, at prices related to the prevailing market price, at varying prices determined at the time of sale, or at negotiated prices. See “Plan of Distribution” on page 34.

We are not offering any shares of our common stock for sale under this prospectus. We will not receive any of the proceeds from the sale of common stock by the selling stockholders, though we will receive proceeds in the event of any warrant exercise for cash. We will pay all the expenses, estimated to be approximately $17,115, in connection with this offering, other than underwriting commissions and discounts and counsel fees and expenses of the selling stockholders. The shares of our common stock are being registered to satisfy contractual obligations owed by us to the selling stockholders pursuant to their respective transaction documents.

Our common stock is traded on NYSE American under the symbol “DPW.” The last reported sale price for the common stock on the NYSE American on November 23, 2020 was $7.19 per share.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read the entire prospectus and any amendments or supplements carefully before you make your investment decision.

An investment in our common stock involves a high degree of risk. You should review carefully the risks and uncertainties described under the heading “Risk Factors” contained herein on page 8 and in our Annual Report on Form 10-K/A for the year ended December 31, 2019, as well as our subsequently filed periodic and current reports, which we file with the Securities and Exchange Commission and which are incorporated by reference into the registration statement of which this prospectus is a part. You should read the entire prospectus carefully before you make your investment decision.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is _______ __, 2020.

TABLE OF CONTENTS

|

Page

| ||

| About this Prospectus | 1 | |

| Disclosure Regarding Forward-Looking Statements | 2 | |

| About the Company | 3 | |

| Risk Factors | 8 | |

| Use of Proceeds | 32 | |

| Selling Stockholders | 32 | |

| Plan of Distribution | 34 | |

| Description of Our Securities | 36 | |

| Legal Matters | 40 | |

| Experts | 40 | |

| Where you can find more Information | 40 | |

| Incorporation of Documents by Reference | 40 |

| i |

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-3 that we filed with the Securities and Exchange Commission (the “SEC” or the “Commission”).

You should read this prospectus and the information and documents incorporated by reference carefully. Such documents contain important information you should consider when making your investment decision. See “Where You Can Find More Information” and “Documents Incorporated by Reference” in this prospectus.

This prospectus may be supplemented from time to time to add, to update or change information in this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will be deemed not to constitute a part of this prospectus. You should rely only on the information contained or incorporated by reference in this prospectus, any applicable prospectus supplement or any related free writing prospectus. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement, as well as information we have filed with the SEC that is incorporated by reference, is accurate as of the date on the front of those documents only, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

No person is authorized in connection with this prospectus to give any information or to make any representations about us, the securities offered hereby or any matter discussed in this prospectus, other than the information and representations contained in this prospectus. If any other information or representation is given or made, such information or representation may not be relied upon as having been authorized by us.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

For investors outside the United States: Neither we nor any Underwriter has done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

Unless otherwise stated or the context requires otherwise, references to “DPW,” the “Company,” “we,” “us” or “our” are to DPW Holdings, Inc. and its subsidiaries.

| - 1 - |

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus and the documents incorporated by reference in it contain forward-looking statements regarding future events and our future results that are subject to the safe harbors created under the Securities Act of 1933 and the Securities Exchange Act of 1934. All statements other than statements of historical facts are statements that could be deemed forward-looking statements. These statements are based on our expectations, beliefs, forecasts, intentions and future strategies and are signified by the words “expects,” “anticipates,” “intends,” “believes” or similar language. In addition, any statements that refer to projections of our future financial performance, our anticipated growth, trends in our business and other characterizations of future events or circumstances are forward-looking statements. These forward-looking statements are only predictions and are subject to risks, uncertainties and assumptions that are difficult to predict, including those identified above, under “Risk Factors” and elsewhere in this prospectus. Therefore, actual results may differ materially and adversely from those expressed in any forward-looking statements. All forward-looking statements included in this prospectus are based on information available to us on the date of this prospectus and speak only as of the date hereof.

We disclaim any current intention to update our “forward-looking statements,” and the estimates and assumptions within them, at any time or for any reason. In particular, the following factors, among others, could cause actual results to differ materially from those described in the “forward-looking statements”:

| ● | our continued operating and net losses in the future; |

| ● | our need for additional capital for our operations and to fulfill our business plans; |

| ● | the effect of COVID-19; |

| ● | dependency on our ability, and the ability of our contract manufacturers, to timely procure electronic components; |

| ● | the potential ineffectiveness of our strategic focus on power supply solution competencies; |

| ● | dependency on developer partners for the development of some of our custom design products; |

| ● | dependency on sales of our legacy products for a meaningful portion of our revenues; |

| ● | the possible failure of our custom product development efforts to result in products which meet customers’ needs or such customers’ failure to accept such new products; |

| ● | our ability to attract, retain and motivate key personnel; |

| ● | dependence on a few major customers; |

| ● | dependence on the electronic equipment industry; |

| ● | reliance on third-party subcontract manufacturers to manufacture certain aspects of the products sold by us; |

| ● | reduced profitability as a result of increased competition, price erosion and product obsolescence within the industry; |

| ● | our ability to establish, maintain and expand its OEM relationships and other distribution channels; |

| ● | our inability to procure necessary key components for its products, or the purchase of excess or the wrong inventory; |

| ● | variations in operating results from quarter to quarter; |

| ● | dependence on international sales and the impact of certain governmental regulatory restrictions on such international sales and operations; and |

| ● | the risk factors included in our most recent filings with the SEC, including, but not limited to, our Forms 10-K and 10-Q. All filings are also available on our website at www.dpwholdings.com. |

| - 2 - |

ABOUT THE COMPANY

This summary highlights selected information contained in other parts of this prospectus. Because it is a summary, it does not contain all of the information that you should consider in making your investment decision. Before investing in our securities, you should read the entire prospectus carefully, including the information set forth under the heading “Risk Factors.”

Company Overview

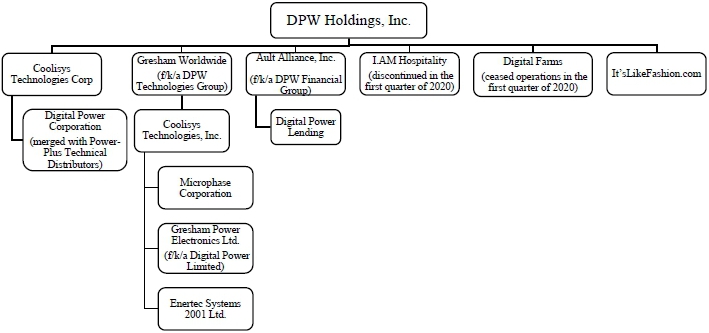

DPW Holdings, Inc. is a diversified holding company that owns operating subsidiaries and divisions engaged in a number of diversified business operations including the defense, aerospace, commercial, health/medical, finance and commercial lending sectors. Our largest subsidiary is Gresham Worldwide, which provides advanced bespoke military and commercial applications. We began implementing our strategy in late 2016 led by our Chairman and CEO Milton “Todd” Ault, III and Vice Chairman and President William B. Horne. DPW is presently led by an Executive Committee, the members of which are Messrs. Ault and Horne and Henry Nisser, our Executive Vice President and General Counsel.

We operate as a holding company with operations conducted primarily through our subsidiaries. We conduct our activities in a manner so as not to be deemed an investment company under the Investment Company Act of 1940, as amended (the “Investment Company Act”). Generally, this means that we do not invest or intend to invest in securities as our primary business and that no more than 40% of our total assets will be invested in investment securities as such term is defined in the Investment Company Act. Pursuant to the Investment Company Act, companies such as our subsidiary Digital Power Lending, LLC (“DP Lending”) are excluded from the definition of an investment company since its business consists of making small loans and industrial banking. We also maintain a large investment in Avalanche International, Corp., which does business as MTIX International.

Originally, we were primarily a solution-driven organization that designed, developed, manufactured and sold high-grade customized and flexible power system solutions for the medical, military, telecom and industrial markets. Although we are actively seeking growth through acquisitions, we will continue to focus on high-grade and custom product designs for the commercial, medical and military/defense markets, where customers demand high density, high efficiency and ruggedized products to meet the harshest and/or military mission critical operating conditions.

We have operations located in Europe through our wholly-owned subsidiary, Gresham Power Electronics (formerly Digital Power Limited) (“Gresham Power”), Salisbury, England. Gresham Power designs, manufactures and sells power products and system solutions mainly for the European marketplace, including power conversion, power distribution equipment, DC/AC (direct current/active current) inverters and UPS (uninterrupted power supply) products. Our European defense business is specialized in the field of naval power distribution products.

| - 3 - |

Recent Events

Reorganization of Our Corporate Structure

Commencing in October and continuing through July 2020, we reorganized our corporate structure pursuant to a series of transactions among our company and our directly and indirectly-owned subsidiaries. The purpose of the reorganization was to align our various businesses by the products and services that constitute the majority of each subsidiaries’ revenues. As a result of the foregoing transactions, our corporate structure is as follows:

On January 7, 2020, we formed Coolisys Technologies Corp. (“CTC”) in order to hold Digital Power Corporation. Coolisys is presently owned by GWW and owns Microphase Corporation, Gresham Power Electronics and Enertec Systems. We may dispose of Coolisys in the future, leaving GWW as the direct owner of the three foregoing subsidiaries.

I. AM’s operations were discontinued in the first quarter of 2020. On November 2, 2020, I.AM, Inc. filed a voluntary petition for bankruptcy under Chapter 7 in the United States Bankruptcy Court in the Central District of California, Santa Ana Division, case number 8:20-bk-13076.

Other Matters

In January 2018, we formed Super Crypto Mining, Inc., a wholly-owned subsidiary, which recently changed its name to Digital Farms, Inc. (“DFI”). DFI was established to operate our newly formed cryptocurrency business, which mined a variety of digital currency for our own account. These cryptocurrencies include Bitcoin, Litecoin and Ethereum. We made the decision to discontinue DFI’s operations in the first quarter of 2020.

On May 23, 2018, DP Lending entered into and closed a securities purchase agreement with I. AM, Inc. (“I. AM”). I. AM’s operations were discontinued in the first quarter of 2020.

On October 2, 2020, we entered into an At-The-Market Issuance Sales Agreement (the “2020 ACM Sales Agreement”) with Ascendiant Capital Markets, LLC to sell shares of common stock having an aggregate offering price of up to $8,975,000 from time to time, through an “at the market offering” program (the “2020 ACM ATM Offering”). The offer and sale of shares of common stock from the 2020 ACM ATM Offering was made pursuant to our effective “shelf” registration statement on Form S-3 and an accompanying base prospectus contained therein (Registration Statement No. 333-222132) which became effective on January 11, 2018. Through November 20, 2020, we had received gross proceeds of $8,953,354 through the sale of 4,906,340 shares of common stock from the 2020 ACM ATM Offering.

On August 5, 2020, we received $2,000,000 from Esousa and on October 22, 2020, we issued to Esousa a promissory note in the principal face amount of $2,000,000, with an interest rate of 13%. The outstanding principal face amount, plus any accrued and unpaid interest, is due by November 3, 2020, or as otherwise provided in accordance with the terms set forth therein. In connection therewith, we delivered to Esousa a warrant to purchase 729,927 shares of common stock at an exercise price of $3.01. The exercise of the warrant is subject to approval of the NYSE American.

On October 27, 2020, we issued to Esousa two unsecured promissory notes in the aggregate principal face amount of $1,200,000, of which $850,000 was received prior to September 30, 2020. The principal amount of $850,000 of the first note dated October 27, 2020, together with all accrued unpaid interest at an annual rate of 14%, is due and payable on December 28, 2020. The principal amount of $350,000 of the second note dated October 27, 2020, together with all accrued unpaid interest at an annual rate of 14%, is due and payable on January 7, 2021. In connection with the two promissory notes, we delivered to the Esousa (i) a warrant dated October 27, 2020, to purchase 425,000 shares of common stock at an exercise price of $2.20, and (ii) a warrant dated October 27, 2020, to purchase 148,936 shares of common stock at an exercise price of $2.59. The exercise of the warrants is subject to approval of the NYSE American.

| - 4 - |

On November 9, 2020, our wholly-owned subsidiary Gresham Worldwide, Inc. (“GWW”) entered into a stock purchase agreement with Tabard Holdings Inc., a Delaware corporation and wholly owned subsidiary of GWW (“Tabard”), the legal and beneficial owners (the “Sellers”) of 100% of the issued shares in the capital of Relec Electronics Ltd., a corporation organized under the laws of England and Wales (“Relec”), and Peter Lappin, in his capacity as the representative of the Sellers. Upon the terms and subject to the conditions set forth in the stock purchase agreement, Tabard agreed to acquire Relec pursuant to the stock purchase agreement whereby the Sellers will sell to Tabard (i) 100% of the issued shares of Relec. The purchase price is approximately £3,000,000 plus an amount equal to Relec’s cash balance immediately prior to closing of the acquisition. Tabard has paid the sum of $500,000 to an escrow as a deposit toward payment of the purchase price.

On November 19, 2020, we issued to Esousa and two other institutional investors unsecured promissory notes in the aggregate principal face amount of $2,250,000, with an interest rate of 12%. The outstanding principal face amount, plus any accrued and unpaid interest, is due by February 18, 2021, or as otherwise provided in accordance with the terms set forth therein. In connection therewith, we delivered warrants to purchase an aggregate of 1,323,531 shares of common stock at an exercise price of $1.87, subject to adjustments. Exercise of the warrants is subject to approval of the NYSE American.

Settlement of Derivative Litigation

On February 24, 2020, we entered into a definitive settlement agreement (the “Settlement Agreement”) intended to settle the previously disclosed derivative litigation captioned Ethan Young and Greg Young, Derivatively on Behalf of Nominal Defendant, DPW Holdings, Inc. v. Milton C. Ault, III, Amos Kohn, William B. Horne, Jeff Bentz, Mordechai Rosenberg, Robert O. Smith, and Kristine Ault and DPW Holdings, Inc., as the nominal defendant (Case No. 18-cv-6587) (as amended on March 11, 2019, the “Amended Complaint”) against us and certain of our officers and directors pending in the United States District Court for the Central District of California (the “Court”). As previously disclosed, the Amended Complaint alleges violations including breaches of fiduciary duties and unjust enrichment claims based on the previously pled transactions.

On April 15, 2020, the Court issued an Order (the “Order”) approving a Motion for Preliminary Approval of Settlement in the Derivative Action. On July 16, 2020, the Court issued an Order (the “Final Order”) approving a Motion for Final Approval of Settlement in the Derivative Action filed against DPW as a Nominal Defendant and its directors who served on its board of directors on July 31, 2018 who were not dismissed from the action as a result of the Court’s partial grant of the Motion.

In accordance with the terms of the Final Order, the Board has adopted certain resolutions and amendments to our committee charters and/or bylaws, to ensure adherence to certain corporate governance policies (collectively, the “Reforms”). The Final Order further provides that such Reforms shall remain in effect for a period of no less than five (5) years and shall be subject to any of the following: (a) a determination by a majority of the independent directors that the Reforms are no longer in our best interest, including, but not limited to, due to circumstances making the Reforms no longer applicable, feasible, or available on commercially reasonable terms, or (b) modifications which we reasonably believe are required by applicable law or regulation.

In connection with the Settlement Agreement, the parties have agreed upon a payment of attorneys’ fees in the amount of $600,000, which sum shall be payable by our directors & officers liability insurance. The Settlement Agreement contains no admission of wrongdoing.

We have always maintained and continue to believe that neither we nor our current or former directors engaged in any wrongdoing or otherwise committed any violation of federal or state securities laws or any other laws or regulations.

Impact of Coronavirus on Our Operations

On March 16, 2020, to try and mitigate the spread of the novel coronavirus, San Diego County health officials issued orders mandating that all restaurants must end dine-in services. As a result of these temporary closures by the San Diego County health officials and the deteriorating business conditions at both our cryptocurrency mining and restaurant businesses, management concluded that discontinuing these operations was ultimately in our best interest. Although we have ceased operations at Digital Farms, since the assets and operations have not yet been abandoned, sold or distributed, these assets do not yet meet the requirement for presentation as discontinued operations. However, management determined that the permanent closing of the restaurant operations met the criteria for presentation as discontinued operations.

In March 2020, the World Health Organization declared the outbreak of a novel coronavirus (“COVID-19”) as a pandemic which continues to spread throughout the United States and the World. We are monitoring the outbreak of COVID-19 and the related business and travel restrictions and changes to behavior intended to reduce its spread, and its impact on operations, financial position, cash flows, inventory, supply chains, customer purchasing trends, customer payments, and the industry in general, in addition to the impact on our employees. Due to the rapid development and fluidity of this situation, the magnitude and duration of the pandemic and its impact on our operations and liquidity is uncertain as of the date of this prospectus.

| - 5 - |

However, our business has been disrupted and materially adversely affected by the recent outbreak of COVID-19. We are still assessing our business operations and system supports and the impact COVID-19 may have on our results and financial condition, but there can be no assurance that this analysis will enable us to avoid part or all of any impact from the spread of COVID-19 or its consequences, including downturns in business sentiment generally or in our sectors in particular.

Our operations are located in Alameda County, CA, Orange County, CA, Fairfield County, CT, the United Kingdom, Israel and members of our senior management work in Seattle, WA and New York, NY. We have been following the recommendations of local health authorities to minimize exposure risk for our employees, including the temporary closures of our offices and having employees work remotely to the extent possible, which has to an extent adversely affected their efficiency. For more information, see “Risk Factors – We face business disruption and related risks resulting from the recent outbreak of the novel coronavirus . . . .”

Corporate Information

Our corporate name is DPW Holdings, Inc. for both legal and commercial purposes. Our principal address is 201 Shipyard Way, Suite E, Newport Beach, CA 92663. Our phone number is (949) 444-5464. Our website is www.dpwholdings.com. The information on our website does not constitute part of this prospectus. We have included our website address as a factual reference and do not intend it to be an active link to our website.

| - 6 - |

The Offering

The following summary is provided solely for your convenience and is not intended to be complete. You should read the full text and more specific details contained elsewhere in this prospectus. For a more detailed description of our common stock, see “Description of Our Securities.”

| Securities Offered by us: | 5,061,289 shares of our common stock, consisting of up to 155,660 shares of common stock issuable upon conversion of the JLA Note and up to 4,905,629 shares of common stock issuable upon exercise of Warrants | |

| Common Stock outstanding before this offering: |

18,487,902 shares | |

| Common Stock to be outstanding after this offering (assuming full exercise and conversion): |

23,549,191 shares | |

| Use of Proceeds: | We will not receive any of the proceeds from the sale of common stock by the selling stockholders, though we will receive proceeds in the event of any warrant exercise for cash. See “Use of Proceeds.” | |

| Plan of Distribution: | The shares may be offered and sold from time to time by the selling stockholder named herein through public or private transactions at fixed prices, at prevailing market prices at the time of sale, at prices related to the prevailing market price, at varying prices determined at the time of sale, or at negotiated prices. See “Plan of Distribution.” | |

| NYSE American Symbol | DPW | |

| Risk Factors: | Investing in our securities is highly speculative and involves a significant degree of risk. See “Risk Factors” and other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our securities. |

The number of shares of common stock that will be outstanding after this offering set forth above is based on 18,487,902 shares of common stock outstanding as of November 23, 2020, and excludes the following:

| · | 695,004 shares of common stock issuable upon the conversion of outstanding convertible debt instruments at conversion prices of between $1.28 per share and $8.80 per share; |

| · | 4,235,168 shares of common stock issuable upon the exercise of outstanding warrants at an exercise prices of between $0.00 per share and $2,000 per share; |

| · | 950 shares of common stock issuable upon the exercise of stock options at a weighted average exercise prices of $578 per share, all of which were issued under the 2016 Stock Incentive Plan or the 2017 Stock Incentive Plan; and |

| · | 3,125 shares of common stock reserved for issuance under our Amended and Restated 2018 Stock Incentive Plan. |

Unless otherwise specifically stated, all information in this prospectus assumes no exercise of the outstanding options or warrants described above.

| - 7 - |

RISK FACTORS

An investment in our securities is speculative and involves a high degree of risk. Our business, financial condition or results of operations could be adversely affected by any of these risks. You should carefully consider the risks described below and those risks set forth in the reports that we file with the SEC and that we incorporate by reference into this prospectus, before deciding to invest in our securities. The risks and uncertainties we have described are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also affect our operations. Past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results or trends in future periods. If any of these risks actually occurs, our business, business prospects, financial condition or results of operations could be seriously harmed. This could cause the trading price of our shares of common stock to decline, resulting in a loss of all or part of your investment. Please also read carefully the section above entitled “Disclosure Regarding Forward-Looking Statements.”

Risks Related to Our Company

We have historically incurred significant losses and our financial situation creates doubt whether we will continue as a going concern.

We have historically experienced operating and net losses and anticipate continuing to experience such losses in the future. For the years ended December 31, 2019 and 2018, we had an operating loss of $26,941,797 and $19,605,456 and net losses of $32,913,412 and $32,233,881, respectively. As of December 31, 2019 and 2018, we had a working capital deficiency of $19,150,075 and $18,445,302, respectively. There are no assurances that we will be able to achieve a level of revenues adequate to generate sufficient cash flow from operations or obtain additional financing through private placements, public offerings and/or bank financing necessary to support our working capital requirements. To the extent that funds generated from any private placements, public offerings and/or bank financing are insufficient, we will have to raise additional working capital. No assurance can be given that additional financing will be available, or if available, will be on acceptable terms. These conditions raise substantial doubt about our ability to continue as a going concern. If adequate working capital is not available we may be forced to discontinue operations, which would cause investors to lose their entire investment.

We expect to continue to incur losses for the foreseeable future and need to raise additional capital to continue business development initiatives and to support our working capital requirements. However, if we are unable to raise additional capital, we may be required to curtail operations and take additional measures to reduce costs, including reducing our workforce, eliminating outside consultants and reducing legal fees in order to conserve cash in amounts sufficient to sustain operations and meet our obligations. As a result of these financing uncertainties, during the year ended December 31, 2019, we recognized that our dependence on ongoing capital requirements to fund our operations raise substantial doubt about our ability to continue as a going concern. Our ongoing capital requirements have only increased since then, meaning that substantial doubt about our ability to continue as a going concern remains and will likely do so for the foreseeable future.

We will need to raise additional capital to fund our operations in furtherance of our business plan.

Until we are profitable, we will need to quickly raise additional capital in order to fund our operations in furtherance of our business plan. The proposed financing may include shares of common stock, shares of preferred stock, warrants to purchase shares of common stock or preferred stock, debt securities, units consisting of the foregoing securities, equity investments from strategic development partners or some combination of each. Any additional equity financings may be financially dilutive to, and will be dilutive from an ownership perspective to our stockholders, and such dilution may be significant based upon the size of such financing. Additionally, we cannot assure that such funding will be available on a timely basis, in needed quantities, or on terms favorable to us, if at all.

We have substantial amounts of indebtedness. This indebtedness and the covenants contained in our loan documents with senior creditors substantially limit our financial and operating flexibility.

We have entered into a number of loan documents, including security and similar agreements, with senior lenders (the “Senior Lenders”). These loan documents (the “Senior Loan Documents”) grant priority security interests in all of our assets to the Senior Lenders. Such Senior Loan Documents contain restrictions that substantially limit our financial flexibility. These Senior Loan Documents place limits on our ability to (i) incur additional indebtedness even if such indebtedness is subordinated to the debt instruments issued to the Senior Lenders, and (ii) grant security to third persons, among other matters. These restrictions limit the Company’s ability to finance its future operations and capital needs. Absent the consent of the Senior Lenders, we would be unable to, among other things, obtain additional debt to raise additional capital, implement our business strategy, establish corporate infrastructure and in any other way fund the development of its business. In addition, our substantial indebtedness could require us to dedicate a substantial portion of our cash flow from the anticipated operations to making payments on our indebtedness and other liabilities, which would limit the availability of funds for working capital and other general corporate purposes; limit our flexibility in reacting to changes in the various industries in which we or any of our subsidiaries operates or in our competitive environment; place us at a competitive disadvantage compared to those of our competitors who have less debt than we do, and limit our ability to borrow additional funds and increase the costs of any such additional borrowings. If we are unable to pay our debts, we would become insolvent.

| - 8 - |

Servicing our debt will require a significant amount of cash, and we may not have sufficient cash flow from our business to pay our debt. We have defaulted on certain prior repayment obligations.

Our ability to make scheduled payments of the principal of, to pay interest on or to refinance our indebtedness, including the DPW Notes, depends on our future performance, which is subject to economic, financial, competitive and other factors beyond our control. In addition, we have defaulted on certain prior repayment obligations as set forth below:

| ● | On March 23, 2018, we entered into a securities purchase agreement pursuant to which we issued a note in the amount of $1,000,000 to an investor. Pursuant to the terms of the note, we were required to pay interest on a monthly basis. The maturity date of this note was June 22, 2018. We did not pay the interest on a timely basis or pay the note in full on the maturity date. On July 3, 2019, we reached an agreement with the investor to repay the note under renegotiated terms with a maturity date of January 22, 2020. This note was subsequently acquired by Esousa. As of the filing date of this prospectus, the current principal amount outstanding on the note is $632,000. |

| ● | On September 21, 2018, we entered into a securities purchase agreement pursuant to which we issued a note in the amount of $526,316 to an investor. The maturity date of this note was December 31, 2018. We did not pay the principal or accrued interest in full on the maturity date. On July 2, 2019, we entered into an exchange agreement with the investor pursuant to which, in exchange for the note issued by us to the investor, we sold to the investor a new convertible promissory note in the principal amount of $783,031 with an interest rate of 12% per annum and a maturity date of December 31, 2019. On September 26, 2019, principal and interest on the 12% Convertible Note was exchanged for a convertible promissory note in the principal amount of $815,218 with an interest rate of 12% per annum and a maturity date of December 31, 2019. Further, on February 5, 2020, we entered into an exchange agreement with the investor pursuant to which, in exchange for the September 26, 2019 note issued by us to the investor, we sold to the investor a new convertible promissory note in the principal amount of $295,000 and a new promissory note in the principal amount of $585,919. Both of these notes have an interest rate of 12% per annum and a maturity date of December 31, 2019. We issued 203,448 shares of our common stock on February 25, 2020 in satisfaction of the February 5, 2020 convertible promissory note. |

| ● | During 2018, we received funding as a result of entering into multiple Agreements for the Purchase and Sale of Future Receipts (collectively, the “Agreements on Future Receipts”) pursuant to which we sold in the aggregate $5,632,400 in future receipts for a purchase price in the amount of $4,100,000. Pursuant to the terms of the Agreements on Future Receipts, we were required to make payments on a daily basis until the balance of the amount sold was fully repaid. We did not make these daily payments on a timely basis. We reached an agreement with the investor to repay the Agreements on Future Receipts under renegotiated terms. As of the filing date of this prospectus, the amount outstanding on the Agreements on Future Receipts is $1,588,563. |

| ● | On November 28, 2018, Blockchain Mining Supply and Services, Ltd, a vendor who sold computers to our subsidiary Digital Farms, Inc. (t/k/a Super Crypto Mining, Inc.), filed in the United States District Court for the Southern District of New York against us and our subsidiary (Case No. 18-cv-11099). The Complaint asserted claims for breach of contract and promissory estoppel against us and our subsidiary arising from the subsidiary’s failure to satisfy a purchase agreement. The Complaint seeks damages in the amount of $1,388,495, which approximates the amount of the reserve that we have established. To date, the Court has not set a briefing schedule in connection with our anticipated motion to dismiss. |

Our business may not generate cash flow from operations in the future sufficient to service our debt and make necessary capital expenditures. If we are unable to generate such cash flow, we may be required to adopt one or more alternatives, such as selling assets, restructuring debt or obtaining additional equity capital on terms that may be onerous or highly dilutive. Our ability to refinance our indebtedness will depend on the capital markets and our financial condition at such time. We may not be able to engage in any of these activities or engage in these activities on desirable terms, which could result in a default on our debt obligations.

| - 9 - |

If we default on secured debt instruments, we may be required to repay the principal and accrued unpaid interest due thereon, together with additional penalties.

If we do not timely cure an event of default under the secured debt instruments, whether or not convertible, the holder(s) may accelerate all of our repayment obligations and take control of our pledged assets, potentially requiring us to renegotiate the secured debt instruments on terms less favorable to us or to immediately cease operations. Further, if we are liquidated, the holders’ rights to repayment would be senior to the rights of the holders of our common stock to receive any proceeds from the liquidation. Any declaration by the holders of an event of default could significantly harm our business and prospects and could cause the price of our common stock to decline. If we raise any additional debt financing, the terms of such additional debt could further restrict our operating and financial flexibility.

We face business disruption and related risks resulting from the continuing impact of the novel coronavirus (“COVID-19”), which could have a material adverse effect on our business and results of operations and curtail our ability to raise financing.

Our business has been disrupted and materially adversely affected by the recent outbreak of COVID-19. As a result of measures imposed by the governments in affected regions, businesses and schools have been suspended due to quarantines intended to contain this outbreak and many people have been forced to work from home in those areas. The spread of COVID-19 from China to other countries has resulted in the Director General of the World Health Organization declaring the outbreak of COVID-19 as a Public Health Emergency of International Concern, based on the advice of the Emergency Committee under the International Health Regulations (2005), and the Centers for Disease Control and Prevention in the U.S. issued a warning on February 25, 2020 regarding the likely spread of COVID-19 to the U.S. While the COVID-19 outbreak is still in its early stages, international stock markets have begun to reflect the uncertainty associated with the slow-down in the American, Israeli and UK economies and the reduced levels of international travel experienced since the beginning of January and the significant decline in the Dow Industrial Average at the end of February 2020 was largely attributed to the effects of COVID-19. We are still assessing our business operations and system supports and the impact COVID-19 may have on our results and financial condition, but there can be no assurance that this analysis will enable us to avoid part or all of any impact from the spread of COVID-19 or its consequences, including downturns in business sentiment generally or in our sectors in particular.

Our operations are located in Alameda County, CA, Orange County, CA, Fairfield County, CT, the United Kingdom, Israel and members of our senior management work in Seattle, WA and New York, NY, which is also the location of the offices of the Company’s independent auditor. We have been following the recommendations of local health authorities to minimize exposure risk for its employees for the past several weeks, including the temporary closures of our offices and having employees work remotely to the extent possible, which has to an extent adversely affected their efficiency.

Updates by business unit are as follows:

| · | DPW Holdings’ corporate headquarters, located in Newport Beach, CA, has begun working remotely, based on the occupancy and social distancing order from the Orange County Health Officer (http://www.ochealthinfo.com/phs/about/epidasmt/epi/dip/prevention/novel_coronavirus). The headquarters staff has tested the secure remote access systems and technology infrastructure to adjust working arrangements for its employees and believes it has adequate internal communications system and can remain operational with a remote staff. |

| · | Coolisys Technologies Corp., currently located in Milpitas, CA, decreased the number of its employees working at its prior site in Fremont, CA for 14 weeks as a result of the Alameda County Public Health Department’s order to cease all activities at facilities located within the County. |

| · | Microphase Corporation, located in Shelton, CT, has developed an emergency plan to ensure that its mission critical manufacturing and logistical functions are up and running. Microphase has implemented additional steps to ensure a higher level of cleanliness in its facility. Employees at greater risk of major health issues from COVID-19 are not required to work on site. The crisis management team meets regularly to monitor the situation, and modifies and communicates the plan as the need arises. Once the COVID-19 crisis has passed, the team will work on transitioning Microphase back to normal operations. |

| · | Gresham Power Electronics Limited, located in Salisbury, UK, suspended production operations on March 19, 2020 until June of 2020 and recently suspended such operations in November of 2020. |

| - 10 - |

| · | Enertec Systems 2001 Ltd., located in Karmiel, Israel, has been granted a waiver by the Israeli government to remain open to complete key projects that impact national security. Approximately 50% of the Enertec workforce is working remotely. |

Due to the unprecedented market conditions domestically and internationally, and the effect COVID-19 has had and will continue to have on the Company’s operations and financial performance, the extent of which is not currently known, the Company is temporarily suspending guidance for 2020. We will monitor the situation rigorously and provide business updates as circumstances warrant and resume providing guidance on our business when management believes that such information would be both reliable and substantively informative.

The duration and extent of the impact from the COVID-19 pandemic depends on future developments that cannot be accurately predicted at this time, such as the severity and transmission rate of the virus, the extent and effectiveness of containment actions and the impact of these and other factors on our employees, customers, partners and vendors. If we are not able to respond to and manage the impact of such events effectively, our business will be harmed.

As noted above, we rely to a great extent on external financing to fund our operations. The outbreak of COVD-19 has had a materially adverse impact on our ability to raise financing for our operations. Unless investors’ outlook improves dramatically in the near future, it will further inhibit our ability to raise the funds we need to sustain our operations. No assurance can be given that additional financing will be available, or if available, will be on acceptable terms.

Our limited operating history makes it difficult to evaluate our future business prospects and to make decisions based on our historical performance.

Although our executive officers have been engaged in the industries in which we operate for varying degrees of time, we did not begin operations of our current business until recently. We have a very limited operating history in our current form, which makes it difficult to evaluate our business on the basis of historical operations. As a consequence, it is difficult, if not impossible, to forecast our future results based upon our historical data. Reliance on our historical results may not be representative of the results we will achieve, and for certain areas in which we operate, principally those unrelated to defense contracting, will not be indicative at all. Because of the uncertainties related to our lack of historical operations, we may be hindered in our ability to anticipate and timely adapt to increases or decreases in sales, product costs or expenses. If we make poor budgetary decisions as a result of unreliable historical data, we could be less profitable or incur losses, which may result in a decline in our stock price.

We have an evolving business model, which increases the complexity of our business.

Our business model has evolved in the past and continues to do so. In prior years we have added additional types of services and product offerings and in some cases we have modified or discontinued those offerings. We intend to continue to try to offer additional types of products or services, and we do not know whether any of them will be successful. From time to time we have also modified aspects of our business model relating to our product mix. We do not know whether these or any other modifications will be successful. The additions and modifications to our business have increased the complexity of our business and placed significant strain on our management, personnel, operations, systems, technical performance, financial resources, and internal financial control and reporting functions. Future additions to or modifications of our business are likely to have similar effects. Further, any new business or website we launch that is not favorably received by the market could damage our reputation or our brand. The occurrence of any of the foregoing could have a material adverse effect on our business.

We are a holding company whose subsidiaries are given certain degree of independence and our failure to integrate our subsidiaries may adversely affect our financial condition.

We have given our subsidiary companies and their executives a certain degree of independence in decision-making. On the one hand, this independence may increase the sense of ownership at all levels, on the other hand it has also increased the difficulty of the integration of operation and management, which has resulted in increased difficulty of management integration. In the event we are not able to successfully manage our subsidiaries this will result in operating difficulties and have a negative impact on our business.

The Company and our independent auditors have expressed doubt about our ability to continue as a going concern. If we do not continue as a going concern, investors will lose their entire investment.

In its report on our financial statements included in our Annual Report for the fiscal year ended December 31, 2019, our independent auditors have expressed doubt about our ability to continue as a going concern. Our ability to continue as a going concern is an issue raised as a result of ongoing operating losses and a lack of financing commitments then in place to meet expected cash requirements. Our ability to continue as a going concern is subject to our ability to generate a profit and/or obtain necessary funding from outside sources, including obtaining additional funding from the sale of our securities, increasing sales or obtaining loans and grants from various financial institutions where possible. If we do not continue as a going concern, investors will lose their entire investment.

| - 11 - |

We received an order and a subpoena from the SEC in the investigation now known as “In the Matter of DPW Holdings, Inc.,” the consequences of which are unknown.

We received an order and related subpoena from the SEC that stated that the staff of the SEC is conducting an investigation now known as “In the Matter of DPW Holdings, Inc.,” and that the subpoena was issued as part of an investigation as to whether we and certain of our officers, directors, employees, partners, subsidiaries and/or affiliates, and/or other persons or entities, directly or indirectly, violated certain provisions of the Securities Act and the Exchange Act, in connection with the offer and sale of our securities. Although the order states that the SEC may have information relating to such alleged violations, the subpoena expressly provides that the inquiry is not to be construed as an indication by the SEC or its staff that any violations of the federal securities laws have occurred. We have produced documents in response to the subpoena. The SEC may in the future require us to produce additional documents or information, or seek testimony from other members of our management team.

We are unaware of the scope or timing of the SEC’s investigation. As a result, we do not know how the SEC’s investigation is proceeding, when the investigation will be concluded. We also are unable to predict what action, if any, might be taken in the future by the SEC or its staff as a result of the matters that are the subject to its investigation or what impact, if any, the cost of continuing to respond to subpoenas might have on our financial position, results of operations, or cash flows. We have not established any provision for losses in respect of this matter In addition, complying with any such future requests by the SEC for documents or testimony could distract the time and attention of our officers and directors or divert our resources away from ongoing business matters. This investigation could result in significant legal expenses, the diversion of management’s attention from our business, damage to our business and reputation, and could subject us to a wide range of remedies, including an enforcement action by the SEC. There can be no assurance that any final resolution of this and any similar matters will not have a material adverse effect on our financial condition or results of operations.

Our inability to successfully integrate new acquisitions could adversely affect our combined business; our operations are widely disbursed.

Our growth strategy through acquisitions is subject to various risks. On June 2, 2017, we acquired a majority interest in Microphase and on May 23, 2018 we acquired Enertec Systems 2001 Ltd. (“Enertec”). Further, we have announced the entry into an agreement whereby Gresham Worldwide will acquire Relec Electronics Ltd. from its present shareholders; however, we cannot presently assure you that this transaction will be consummated. Our strategy and business plan are dependent on our ability to successfully integrate Microphase’s, Enertec’s and our other acquired entities’ operations. In addition, while we are based in Newport Beach, CA, Microphase’s operations are located in Shelton, Connecticut, Enertec’s operations are located in Karmiel, Israel and Gresham Power’s operations are located in Salisbury, England. These distant locations and others that we may become involved with in the future will stretch our resources and management time. Further, failure to quickly and adequately integrate all of these operations and personnel could adversely affect our combined business and our ability to achieve our objectives and strategy. No assurance can be given that we will realize synergies in the areas we currently operate.

If we make any additional acquisitions, they may disrupt or have a negative impact on our business.

We have plans to eventually make additional acquisitions beyond Microphase and Enertec. Whenever we make acquisitions, we could have difficulty integrating the acquired companies’ personnel and operations with our own. In addition, the key personnel of the acquired business may not be willing to work for us. We cannot predict the effect expansion may have on our core business. Regardless of whether we are successful in making an acquisition, the negotiations could disrupt our ongoing business, distract our management and employees and increase our expenses. In addition to the risks described above, acquisitions are accompanied by a number of inherent risks, including, without limitation, the following:

| · | difficulty of integrating acquired products, services or operations; |

| · | potential disruption of the ongoing businesses and distraction of our management and the management of acquired companies; |

| · | difficulty of incorporating acquired rights or products into our existing business; |

| · | difficulties in disposing of the excess or idle facilities of an acquired company or business and expenses in maintaining such facilities; |

| · | difficulties in maintaining uniform standards, controls, procedures and policies; |

| · | potential impairment of relationships with employees and customers as a result of any integration of new management personnel; |

| - 12 - |

| · | potential inability or failure to achieve additional sales and enhance our customer base through cross-marketing of the products to new and existing customers; |

| · | effect of any government regulations which relate to the business acquired; and |

| · | potential unknown liabilities associated with acquired businesses or product lines, or the need to spend significant amounts to retool, reposition or modify the marketing and sales of acquired products or the defense of any litigation, whether or not successful, resulting from actions of the acquired company prior to our acquisition. |

Our business could be severely impaired if and to the extent that we are unable to succeed in addressing any of these risks or other problems encountered in connection with these acquisitions, many of which cannot be presently identified, these risks and problems could disrupt our ongoing business, distract our management and employees, increase our expenses and adversely affect our results of operations.

No assurance can be given as to the successful expansion of our operations.

Our significant increase in the scope and the scale of our operations, including the hiring of additional personnel, has resulted in significantly higher operating expenses. We anticipate that our operating expenses will continue to increase. Expansion of our operations may also make significant demands on our management, finances and other resources. Our ability to manage the anticipated future growth, should it occur, will depend upon a significant expansion of our accounting and other internal management systems and the implementation and subsequent improvement of a variety of systems, procedures and controls. We cannot assure that significant problems in these areas will not occur. Failure to expand these areas and implement and improve such systems, procedures and controls in an efficient manner at a pace consistent with our business could have a material adverse effect on our business, financial condition and results of operations. We cannot assure that attempts to expand our marketing, sales, manufacturing and customer support efforts will succeed or generate additional sales or profits in any future period. As a result of the expansion of our operations and the anticipated increase in our operating expenses, along with the difficulty in forecasting revenue levels, we expect to continue to experience significant fluctuations in its results of operations.

We may be unable to successfully expand our production capacity, which could result in material delays, quality issues, increased costs and loss of business opportunities, which may negatively impact our product margins and profitability.

Part of our future growth strategy is to increase our production capacity to meet increasing demand for our goods. Assuming we obtain sufficient funding to increase our production capacity, any projects to increase such capacity may not be constructed on the anticipated timetable or within budget. We may also experience quality control issues as we implement any production upgrades. Any material delay in completing these projects, or any substantial cost increases or quality issues in connection with these projects could materially delay our ability to bring our products to market and adversely affect our business, reduce our revenue, income and available cash, all of which could harm our financial condition.

If we fail to establish and maintain an effective system of internal control over financial reporting, we may not be able to report our financial results accurately or prevent fraud. Any inability to report and file our financial results accurately and timely could harm our reputation and adversely impact the trading price of our common stock.

Effective internal control over financial reporting is necessary for us to provide reliable financial reports and prevent fraud. If we cannot provide reliable financial reports or prevent fraud, we may not be able to manage our business as effectively as we would if an effective control environment existed, and our business and reputation with investors may be harmed. As a result, our small size and any current internal control deficiencies may adversely affect our financial condition, results of operations and access to capital. We have carried out an evaluation under the supervision and with the participation of our management, including our principal executive officer and principal financial officer, of the effectiveness of the design and operation of our disclosure controls and procedures as of the end of the most recent period covered by this report. Based on the foregoing, our principal executive officer and principal financial officer concluded that our disclosure controls and procedures were not effective at the reasonable assurance level due to the material weaknesses described below.

A material weakness is a deficiency, or a combination of deficiencies, within the meaning of Public Company Accounting Oversight Board (“PCAOB”) Audit Standard No. 5, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our annual or interim financial statements will not be prevented or detected on a timely basis. Management has identified the following material weaknesses which have caused management to conclude that as of December 31, 2019, our internal control over financial reporting (“ICFR”) was not effective at the reasonable assurance level:

| 1. | We do not have sufficient resources in our accounting function, which restricts our ability to gather, analyze and properly review information related to financial reporting, including fair value estimates, in a timely manner. In addition, due to our size and nature, segregation of all conflicting duties may not always be possible and may not be economically feasible. However, to the extent possible, the initiation of transactions, the custody of assets and the recording of transactions should be performed by separate individuals. Management evaluated the impact of our failure to have segregation of duties during our assessment of our disclosure controls and procedures and concluded that the control deficiency that resulted represented a material weakness. |

| - 13 - |

| 2. |

We have inadequate controls to ensure that information necessary to properly record transactions is adequately communicated on a timely basis from non-financial personnel to those responsible for financial reporting. Management evaluated the impact of the lack of timely communication between non–financial and financial personnel on our assessment of our reporting controls and procedures and has concluded that the control deficiency represented a material weakness. |

| 3. |

We did not design or maintain effective general information technology (“IT”) controls over certain information systems that are relevant to the mitigation of the risk pertaining to the misappropriation of assets. Specifically, we did not design and implement program change management controls for certain financially relevant systems to ensure that IT program and data changes affecting the Company’s (i) financial IT applications, (ii) digital currency mining equipment, (iii) digital currency hardware wallets, and (iv) underlying accounting records, are identified, tested, authorized and implemented appropriately. |

Planned Remediation

Management, in coordination with the input, oversight and support of our Board of Directors, has identified the measures below to strengthen our control environment and internal control over financial reporting.

In January 2018, we hired a new Chief Financial Officer and engaged the services of a financial accounting advisory firm. In September 2018, we hired a Chief Accounting Officer and in January 2019, we hired a Senior Vice President of Finance. Finally, in May 2019, we hired an Executive Vice President and General Counsel. We have tasked these individuals with expanding and monitoring the Company’s internal controls, to provide an additional level of review of complex financial issues and to assist with financial reporting. On October 7, 2019, we created an Executive Committee comprised of our Chief Executive Officer, President and Executive Vice President and General Counsel. The Executive Committee meets on a daily basis to address the Company’s critical needs and provide a forum to approve transactions. Further, as we continue to expand our internal accounting department, the Chairman of the Audit Committee will:

| · | assist with documentation and implementation of policies and procedures and monitoring of controls; and |

| · | review all anticipated transactions that are not considered in the ordinary course of business to assist in the early identification of accounting issues and ensure that appropriate disclosures are made in our financial statements. |

We are currently working to improve and simplify our internal processes and implement enhanced controls, as discussed above, to address the material weaknesses in our internal control over financial reporting and to remedy the ineffectiveness of our disclosure controls and procedures. These material weaknesses will not be considered to be remediated until the applicable remediated controls are operating for a sufficient period of time and management has concluded, through testing, that these controls are operating effectively.

If our accounting controls and procedures are circumvented or otherwise fail to achieve their intended purposes, our business could be seriously harmed.

We evaluate our disclosure controls and procedures as of the end of each fiscal quarter, and are annually reviewing and evaluating our internal control over financial reporting in order to comply with the SEC’s rules relating to internal control over financial reporting adopted pursuant to the Sarbanes-Oxley Act of 2002. Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. If we fail to maintain effective internal control over financial reporting or our management does not timely assess the adequacy of such internal control, we may be subject to regulatory sanctions, and our reputation may decline.

We face significant competition, including changes in pricing.

The markets for our products are both competitive and price sensitive. Many competitors have significant financial, operations, sales and marketing resources, plus experience in research and development, and compete with us by offering lower prices. Competitors could develop new technologies that compete with our products to achieve a lower unit price. If a competitor develops lower cost superior technology or cost-effective alternatives to our products and services, our business could be seriously harmed.

| - 14 - |

The markets for some of our products are also subject to specific competitive risks because these markets are highly price competitive. Our competitors have competed in the past by lowering prices on certain products. If they do so again, we may be forced to respond by lowering our prices. This would reduce sales revenues and increase losses. Failure to anticipate and respond to price competition may also impact sales and aggravate losses.

Many of our competitors are larger and have greater financial and other resources than we do.

Our products compete and will compete with similar if not identical products produced by our competitors. These competitive products could be marketed by well-established, successful companies that possess greater financial, marketing, distribution personnel, and other resources than we do. Using said resources, these companies can implement extensive advertising and promotional campaigns, both generally and in response to specific marketing efforts by competitors. They can introduce new products to new markets more rapidly. In certain instances, competitors with greater financial resources may be able to enter a market in direct competition with us, offering attractive marketing tools to encourage the sale of products that compete with our products or present cost features that consumers may find attractive.

Our growth strategy is subject to a significant degree of risk.

Our growth strategy through acquisitions involves a significant degree of risk. Some of the companies that we have identified as acquisition targets or make a significant investment in may not have a developed business or are experiencing inefficiencies and incur losses. Therefore, we may lose our investment in the event that these companies’ businesses do not develop as planned or that we are unable to achieve the cost efficiencies or reduction of losses as anticipated.

Further, in order to implement our growth plan, we have hired additional staff and consultants to review potential investments and implement our plan. As a result, we have substantially increased our infrastructure and costs. If we fail to quickly find new companies that provide revenue to offset our costs, we will continue to experience losses. No assurance can be given that our product development and investments will produce sufficient revenues to offset these increases in expenditures.

Our business and operations are growing rapidly. If we fail to effectively manage our growth, our business and operating results could be harmed.

We have experienced, and may continue to experience, rapid growth in our operations. This has placed, and may continue to place, significant demands on our management, operational and financial infrastructure. If we do not manage our growth effectively, the quality of our products and services could suffer, which could negatively affect our operating results. To effectively manage our growth, we must continue to improve our operational, financial and management controls and reporting systems and procedures. These systems improvements may require significant capital expenditures and management resources. Failure to implement these improvements could hurt our ability to manage our growth and our financial position.

We are heavily dependent on our senior management, and a loss of a member of our senior management team could cause our stock price to suffer.