UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended December 31, 2020

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE EXCHANGE ACT OF 1934 | |||||

For the transition period from _________ to _________

Commission file number 001-33365

_______________________________________________________________

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||||||||

(610 ) 989-0340

_______________________________________________________________

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name Of Each Exchange On Which Registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☑ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

As of January 29, 2021 there were 65,285,674 outstanding shares of Common Stock, no par value.

USA TECHNOLOGIES, INC.

TABLE OF CONTENTS

Part I. Financial Information

Item 1. Consolidated Financial Statements

USA Technologies, Inc.

Condensed Consolidated Balance Sheets

(Unaudited)

| ($ in thousands, except share data) | December 31, 2020 | June 30, 2020 | ||||||||||||

| Assets | ||||||||||||||

| Current assets: | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Accounts receivable, net | ||||||||||||||

| Finance receivables, net | ||||||||||||||

| Inventory, net | ||||||||||||||

| Prepaid expenses and other current assets | ||||||||||||||

| Total current assets | ||||||||||||||

| Non-current assets: | ||||||||||||||

| Finance receivables due after one year | ||||||||||||||

| Property and equipment, net | ||||||||||||||

| Operating lease right-of-use assets | ||||||||||||||

| Intangibles, net | ||||||||||||||

| Goodwill | ||||||||||||||

| Other assets | ||||||||||||||

| Total non-current assets | ||||||||||||||

| Total assets | $ | $ | ||||||||||||

| Liabilities, convertible preferred stock and shareholders’ equity | ||||||||||||||

| Current liabilities: | ||||||||||||||

| Accounts payable | $ | $ | ||||||||||||

| Accrued expenses | ||||||||||||||

| Current obligations under long-term debt | ||||||||||||||

| Deferred revenue | ||||||||||||||

| Total current liabilities | ||||||||||||||

| Long-term liabilities: | ||||||||||||||

| Deferred income taxes | ||||||||||||||

| Long-term debt, less current portion | ||||||||||||||

| Operating lease liabilities, non-current | ||||||||||||||

| Total long-term liabilities | ||||||||||||||

| Total liabilities | ||||||||||||||

Commitments and contingencies (Note 13) | ||||||||||||||

| Convertible preferred stock: | ||||||||||||||

Series A convertible preferred stock, | ||||||||||||||

| Shareholders’ equity: | ||||||||||||||

Preferred stock, | ||||||||||||||

Common stock, | ||||||||||||||

| Accumulated deficit | ( | ( | ||||||||||||

| Total shareholders’ equity | ||||||||||||||

| Total liabilities, convertible preferred stock and shareholders’ equity | $ | $ | ||||||||||||

See accompanying notes.

3

USA Technologies, Inc.

Condensed Consolidated Statements of Operations

(Unaudited)

| Three months ended | Six months ended | |||||||||||||||||||||||||

| December 31, | December 31, | |||||||||||||||||||||||||

| ($ in thousands, except per share data) | 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||||

| Revenue: | ||||||||||||||||||||||||||

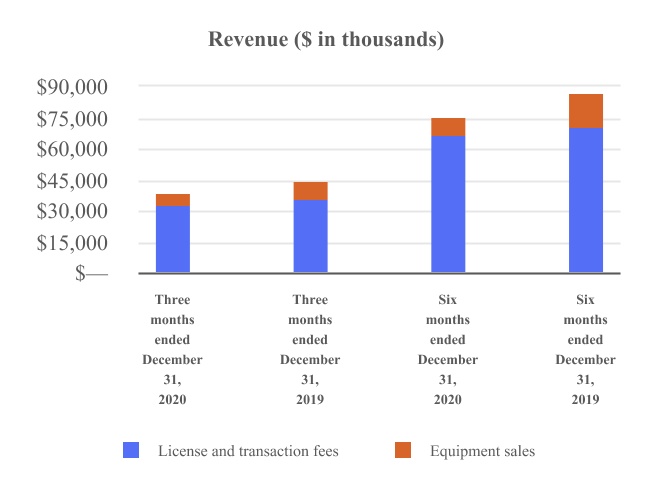

| License and transaction fees | $ | $ | $ | $ | ||||||||||||||||||||||

| Equipment sales | ||||||||||||||||||||||||||

| Total revenue | ||||||||||||||||||||||||||

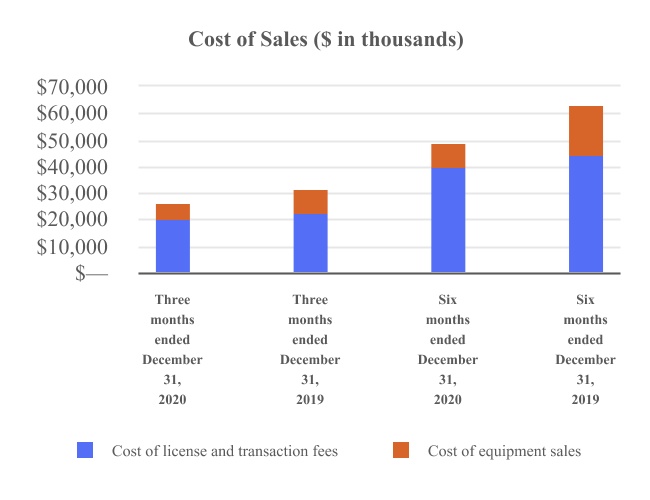

| Cost of sales: | ||||||||||||||||||||||||||

| Cost of license and transaction fees | ||||||||||||||||||||||||||

| Cost of equipment sales | ||||||||||||||||||||||||||

| Total cost of sales | ||||||||||||||||||||||||||

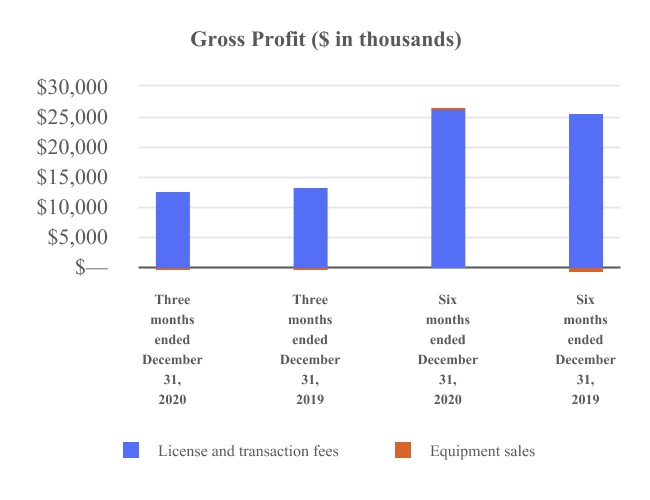

| Gross profit | ||||||||||||||||||||||||||

| Operating expenses: | ||||||||||||||||||||||||||

| Selling, general and administrative | ||||||||||||||||||||||||||

| Investigation, proxy solicitation and restatement expenses | ||||||||||||||||||||||||||

| Depreciation and amortization | ||||||||||||||||||||||||||

| Total operating expenses | ||||||||||||||||||||||||||

| Operating loss | ( | ( | ( | ( | ||||||||||||||||||||||

| Other income (expense): | ||||||||||||||||||||||||||

| Interest income | ||||||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | ||||||||||||||||||||||

| Total other income (expense), net | ( | ( | ( | ( | ||||||||||||||||||||||

| Loss before income taxes | ( | ( | ( | ( | ||||||||||||||||||||||

| Provision for income taxes | ( | ( | ( | ( | ||||||||||||||||||||||

| Net loss | ( | ( | ( | ( | ||||||||||||||||||||||

| Preferred dividends | ( | ( | ||||||||||||||||||||||||

| Net loss applicable to common shares | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Net loss per common share | ||||||||||||||||||||||||||

| Basic | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Diluted | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Weighted average number of common shares outstanding | ||||||||||||||||||||||||||

| Basic | ||||||||||||||||||||||||||

| Diluted | ||||||||||||||||||||||||||

See accompanying notes.

4

USA Technologies, Inc.

Condensed Consolidated Statements of Shareholders’ Equity

(Unaudited)

Six Month Period Ended December 31, 2020

| Common Stock | Accumulated Deficit | Total | ||||||||||||||||||||||||

| ($ in thousands, except share data) | Shares | Amount | ||||||||||||||||||||||||

| Balance, June 30, 2020 | $ | $ | ( | $ | ||||||||||||||||||||||

| — | — | |||||||||||||||||||||||||

| Stock based compensation | — | |||||||||||||||||||||||||

| Net loss | — | — | ( | ( | ||||||||||||||||||||||

| Balance, September 30, 2020 | ( | |||||||||||||||||||||||||

| Stock based compensation | — | |||||||||||||||||||||||||

| Net loss | — | — | ( | ( | ||||||||||||||||||||||

| Balance, December 31, 2020 | $ | $ | ( | $ | ||||||||||||||||||||||

Six Month Period Ended December 31, 2019

| Common Stock | Accumulated Deficit | Total | ||||||||||||||||||||||||

| ($ in thousands, except share data) | Shares | Amount | ||||||||||||||||||||||||

| Balance, June 30, 2019 | $ | $ | ( | $ | ||||||||||||||||||||||

| Stock based compensation | — | — | ||||||||||||||||||||||||

| Net loss | — | — | ( | ( | ||||||||||||||||||||||

| Balance, September 30, 2019 | ( | |||||||||||||||||||||||||

Issuance of common stock in relation to private placement, net of offering costs incurred of $ | — | |||||||||||||||||||||||||

| Stock based compensation | — | |||||||||||||||||||||||||

| Net loss | — | — | ( | ( | ||||||||||||||||||||||

| Balance, December 31, 2019 | $ | $ | ( | $ | ||||||||||||||||||||||

See accompanying notes.

5

USA Technologies, Inc.

Condensed Consolidated Statements of Cash Flows

(Unaudited)

| Six months ended | ||||||||||||||

| December 31, | ||||||||||||||

| ($ in thousands) | 2020 | 2019 | ||||||||||||

| OPERATING ACTIVITIES: | ||||||||||||||

| Net loss | $ | ( | $ | ( | ||||||||||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||||||||

| Stock based compensation | ||||||||||||||

| Amortization of debt discount and issuance costs | ||||||||||||||

| Provision for expected losses | ||||||||||||||

| Provision for inventory reserve | ||||||||||||||

| Depreciation and amortization included in operating expenses | ||||||||||||||

| Depreciation included in cost of sales for rental equipment | ||||||||||||||

| Other | ||||||||||||||

| Changes in operating assets and liabilities: | ||||||||||||||

| Accounts receivable | ( | |||||||||||||

| Finance receivables | ( | |||||||||||||

| Inventory | ( | ( | ||||||||||||

| Prepaid expenses and other assets | ( | |||||||||||||

| Accounts payable and accrued expenses | ||||||||||||||

| Operating lease liabilities | ( | ( | ||||||||||||

| Deferred revenue | ( | ( | ||||||||||||

| Net cash provided by operating activities | ( | ( | ||||||||||||

| INVESTING ACTIVITIES: | ||||||||||||||

| Purchase of property and equipment | ( | ( | ||||||||||||

| Proceeds from sale of property and equipment | ||||||||||||||

| Net cash used in investing activities | ( | ( | ||||||||||||

| FINANCING ACTIVITIES: | ||||||||||||||

| Proceeds from long-term debt issuance by Antara, net of issuance costs paid to Antara | ||||||||||||||

| Proceeds from equity issuance by Antara, net of issuance costs paid to Antara | ||||||||||||||

| Payment of third-party debt issuance costs | ( | |||||||||||||

| Repayment of 2018 JPMorgan Revolving Credit Facility | ( | |||||||||||||

| Proceeds from 2021 JPMorgan Revolving Credit Facility | ||||||||||||||

| Repayment of 2021 JPMorgan Revolving Credit Facility | ( | |||||||||||||

| Proceeds from long-term debt issuance by JPMorgan Chase Bank, N.A., net of debt issuance costs | ||||||||||||||

| Repayment of long-term debt | ( | ( | ||||||||||||

| Proceeds from exercise of common stock options | ||||||||||||||

| Payment of Antara prepayment penalty and commitment termination fee | ( | |||||||||||||

| Net cash used in (provided by) financing activities | ( | |||||||||||||

| Net (decrease) increase in cash and cash equivalents | ( | |||||||||||||

| Cash and cash equivalents at beginning of year | ||||||||||||||

| Cash and cash equivalents at end of period | $ | $ | ||||||||||||

Supplemental disclosures of cash flow information: | ||||||||||||||

| Interest paid in cash | $ | $ | ||||||||||||

| Supplemental disclosures of noncash financing activities: | ||||||||||||||

| Third-party debt issuance costs related to Antara financing, incurred during the six months ended December 31, 2019 and paid the nine months ended March 31, 2020 | $ | $ | ||||||||||||

| Registration termination fee related to Antara financing, incurred during the six months ended December 31, 2019 and paid during the nine months ended March 31, 2020 | $ | $ | ||||||||||||

See accompanying notes.

6

USA Technologies, Inc.

Condensed Notes to Consolidated Financial Statements

(Unaudited)

1. BUSINESS

USA Technologies, Inc. (“USAT” or the “Company”) was incorporated in the Commonwealth of Pennsylvania in January 1992. We are a provider of technology-enabled solutions and value-added services that facilitate electronic payment transactions and consumer engagement services primarily within the unattended Point of Sale (“POS”) market. We are a leading provider in the small ticket, beverage and food vending industry in the United States and are expanding our solutions and services to other unattended market segments, such as gas and car charging stations, laundromats, kiosks, amusements and more. Since our founding, we have designed and marketed systems and solutions that facilitate electronic payment options, as well as telemetry and Internet of Things services, which include the ability to remotely monitor, control, and report on the results of distributed assets containing our electronic payment solutions. Historically, these distributed assets have relied on cash for payment in the form of coins or bills, whereas, our systems allow them to accept cashless payments such as through the use of credit or debit cards or other emerging contactless forms, such as mobile payment. The ePort Connect platform also enables consumer loyalty programs, national rewards programs and digital content, including advertisements and product information to be delivered at the point of sale.

We have evolved from unlocking the potential of cashless payments in vending to transforming into the first platform as a service (PaaS) to power unattended retail operations, from hardware to software for a variety of brands. Today, the unattended retail experience is constantly expanding into new markets and enables brands and merchants to work in new ways. USAT’s mission is to deliver a superior operational and payments platform for unattended retail, that is quick to implement, easy to integrate, flexible to operate, cost effective and provides valuable, real-time customer knowledge. The Company’s PaaS is transforming the unattended retail community by offering one cohesive, integrated solution for payments processing, logistics, and back-office management. It is intended to increase consumer engagement and sales revenue through contactless payments, digital advertising and customer loyalty programs, while providing retailers with control and visibility over their operations and inventory.

Impact of COVID-19

The coronavirus (COVID-19) was first identified in China in December 2019, and subsequently declared a global pandemic in March 2020 by the World Health Organization. COVID-19 containment measures began in parts of the United States in March 2020 resulting in forced closure of non-essential businesses and social distancing protocols. As a result, COVID-19 has impacted our business, significantly reducing foot traffic to distributed assets containing our electronic payment solutions and reducing discretionary spending by consumers. The Company did not observe meaningful reductions in processing volume until mid-March, when average daily processing volume decreased approximately 40 %. By mid-April, processing volumes began to recover and had steadily improved through September 2020. As of September 30, 2020, our average daily processing volume had increased 53 % from the lows in April. During the second half of the current quarter, we have experienced an approximately 7 % decrease in volumes driven by an increase in COVID-19 cases across the country and seasonality of the business. Continued COVID-19 recurrences could result in further reductions in foot traffic to distributed assets containing our electronic payment solutions and reduced discretionary spending by consumers. In addition, the length of time required for an effective vaccine or therapy to become widely available is uncertain. At this time, we are unable to reasonably estimate the length of time that containment measures will be needed in the United States. Furthermore, even after containment measures are lifted there can be no assurance as to the time required to regain operations and sales at levels prior to the pandemic.

In response to the outbreak and business disruption, first and foremost, we prioritized the health and safety of our employees while continuing to diligently serve our customers. An internal task force was created at the start of the pandemic to develop measures to protect the business in light of the volatility and uncertainty caused by the COVID-19 pandemic. This included such aspects as ensuring the safety of our employees and our community by implementing work from home policies, conserving liquidity, evaluating cost saving actions, partnering with customers to position USAT for renewed growth post crisis, and temporarily pausing plans for international expansion. The liquidity conservation and cost savings initiatives included: a 20 % salary reduction for the senior leadership team through December 2020; deferral of all cash-based director fees until calendar year 2021; a temporary furlough of approximately 10 % of our employee base; negotiations with and concessions from vendors in regard to cost reductions and/or payment deferrals; an increased collection effort to reduce outstanding accounts receivables; and various supply chain/inventory improvements. During the summer of 2020 as restrictions lifted, our offices were opened with strict guidelines for social distancing and with adherence to state and local mandates. As a result of an increase in COVID-19 cases during the current quarter and additional lockdowns mandated by state officials, most of our employees continue to work remotely as of December 31, 2020. All of our furloughed employees returned to work, primarily remotely, by June 26, 2020. To date, our supply chain network has not been significantly disrupted and we are continuously

7

monitoring for the impact from COVID-19. In addition, the Company received loan proceeds from the Paycheck Protection Program in the fourth quarter of fiscal year 2020. See Note 8 for additional information.

We continue to monitor the continuously evolving situation and follow guidance from federal, state and local public health authorities. As such, given the dynamic nature of this situation, the Company cannot, at this time, reasonably estimate the longer-term repercussions of COVID-19 on our financial condition, results of operations or cash flows in the future. However, based on current trends and if the pandemic is not substantially contained in the near future, COVID-19 may have a material adverse impact on our revenue growth as well as our overall profitability in fiscal year 2021, and may lead to higher sales-related, inventory-related, and operating reserves. As of December 31, 2020, we have evaluated the potential impact of the COVID-19 outbreak on our financial statements, including, but not limited to, the impairment of goodwill and intangible assets, impairment of long-lived assets including operating lease right-of-use assets, property and equipment and allowance for doubtful accounts for accounts and finance receivables. We have concluded that there are no material impairments as a result of our evaluation. Where applicable, we have incorporated judgments and estimates of the expected impact of COVID-19 in the preparation of the financial statements based on information currently available. These judgments and estimates may change, as new events develop and additional information is obtained, and are recognized in the consolidated financial statements as soon as they become known.

BASIS OF PRESENTATION AND PREPARATION

The accompanying unaudited condensed consolidated financial statements of the Company have been prepared in accordance with U.S. generally accepted accounting principles for interim financial information and with the instructions to Form 10-Q. Accordingly, they do not include all of the information and footnotes required by U.S. generally accepted accounting principles for complete financial statements and therefore should be read in conjunction with the Company’s June 30, 2020 Annual Report on Form 10-K. In the opinion of management, all adjustments considered necessary for a fair presentation, consisting of normal recurring adjustments, have been included. Operating results for the three and six months ended December 31, 2020 are not necessarily indicative of the results that may be expected for the full fiscal year ending June 30, 2021. Actual results could differ from estimates. The balance sheet at June 30, 2020 has been derived from the audited consolidated financial statements at that date, but does not include all disclosures required by accounting principles generally accepted in the United States of America.

The Company operates as one operating segment because its chief operating decision maker, who is the Chief Executive Officer, reviews its financial information on a consolidated basis for purposes of making decisions regarding allocating resources and assessing performance.

As previously disclosed in the Company’s June 30, 2020 Annual Report on Form 10-K and the September 30, 2020 Quarterly Report on Form 10-Q, during the fourth quarter of fiscal year 2020, the Company reclassified certain operating expenses previously reported in the first three quarters of fiscal year 2020 as Selling, general and administrative expenses to Investigation, proxy solicitation and restatement expenses. The reclassifications resulted from management’s conclusion that those operating expenses related to non-recurring professional services fees to assist the Company with accounting and compliance activities following the filing of the 2019 Form 10-K, as well as the proxy solicitation costs incurred in fiscal year 2020. These reclassifications did not affect Total operating expenses or Net loss.

8

Operating expenses for each quarter of fiscal year 2020 and other reporting periods before and after the revision discussed above are as follows:

| Three months ended | Other reporting periods | |||||||||||||||||||||||||||||||||||||||||||

| ($ in thousands) | September 30, 2019 | December 31, 2019 | March 31, 2020 | June 30, 2020 | Year ended June 30, 2020 | Six months ended December 31, 2019 | Nine months ended March 31, 2020 | |||||||||||||||||||||||||||||||||||||

Selling, general and administrative, before revision (a) (b) | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

Investigation, proxy solicitation and restatement expenses, before revision (a) (b) | ||||||||||||||||||||||||||||||||||||||||||||

| Additional amounts reclassified from (to) Selling, general and administrative to (from) Investigation, proxy solicitation and restatement expenses | ( | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||

Selling, general and administrative, after revision (c) | ||||||||||||||||||||||||||||||||||||||||||||

Investigation, proxy solicitation and restatement expenses, after revision (c) | ||||||||||||||||||||||||||||||||||||||||||||

Depreciation and amortization, no change (a) (b) (d) | ||||||||||||||||||||||||||||||||||||||||||||

Total operating expenses, no change (a) (b) (d) | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

(a) The amounts for the three months ended September 30, 2019, December 31, 2019, March 31, 2020 and full year ended June 30, 2020 were presented in the Company’s June 30, 2020 Annual Report on Form 10-K.

(b) The amounts for the three months ended September 30, 2019 were presented in the Company’s September 30, 2020 Quarterly Report on Form 10-Q.

(c) The revised amounts for the three and six months ended December 2019 are presented in the Condensed Consolidated Statements of Operations.

(d) No changes noted for these amounts. The amounts for the three and six months ended December 2019 are presented in the Condensed Consolidated Statements of Operations.

2. ACCOUNTING POLICIES

RECENT ACCOUNTING PRONOUNCEMENTS

Accounting pronouncements adopted

ASC Topic 326 - Credit Losses

On July 1, 2020, we adopted Topic 326, Financial Instruments-Credit Losses, which was primarily introduced under Accounting Standards Update (“ASU”) No. 2016-13, “Financial Instruments – Measurement of Credit Losses on Financial Instruments”. Topic 326 introduces a new credit loss impairment methodology for financial assets measured at amortized cost, requiring recognition of the full lifetime expected credit losses upon initial recognition of the financial asset and each reporting period, replacing current GAAP, which generally requires that a loss be incurred before it is recognized. The expected credit loss model is based on historical experience, current conditions, and reasonable and supportable economic forecasts of collectability.

The Company adopted Topic 326 using the modified retrospective approach through an adjustment to retained earnings, and began calculating our allowance for accounts and finance receivables under an expected loss model rather than an incurred loss model.

We estimate our allowances using an aging analysis of the receivables balances, primarily based on historical loss experience, as there have been no significant changes in the mix or risk characteristics of the receivable revenue streams used to calculate historical loss rates. We also take into consideration that receivables for monthly service fees that are collected as part of the flow of funds from our transaction processing service have a lower risk profile than receivables for equipment and service fees billed under the Company’s standard payment terms of 30 to 60 days from invoice issuance, and adjust our aging analysis to incorporate those risk assessments. Current conditions are analyzed at each measurement date as we reassess whether our receivables continue to exhibit similar risk characteristics as the prior measurement date, and determine if the reserve calculation needs to be adjusted for new developments, such as a customer’s inability to meet its financial obligations. Lastly, we also factor reasonable and supportable economic expectations into our allowance estimate for the asset’s entire expected life, which is generally less than one year for accounts receivable and five years for finance receivables.

The adoption of this pronouncement on July 1, 2020 resulted in a net increase of $0.3

9

The following table represents a rollforward of the allowance for doubtful accounts for accounts and finance receivables for the six months ending December 31, 2020:

| Six months ended December 31, 2020 | ||||||||||||||

| ($ in thousands) | Accounts receivable | Finance receivable | ||||||||||||

| Beginning balance of allowance at June 30, 2020, prior to adopting ASC 326 | $ | $ | ||||||||||||

| Impact of adoption of ASC 326 | ( | |||||||||||||

| Provision for expected losses | ||||||||||||||

| Balance at September 30, 2020 | ||||||||||||||

| Provision for expected losses | ||||||||||||||

| Balance at December 31, 2020 | $ | $ | ||||||||||||

ASU 2018-15 - Intangibles—Goodwill and Other (Topic 350): Internal-Use Software

In August 2018, the FASB issued ASU No. 2018-15, “Intangibles—Goodwill and Other (Topic 350): Internal-Use Software.” This standard aligns the requirements for capitalizing implementation costs incurred in a cloud computing arrangement that is a service contract with the requirements for capitalizing implementation costs incurred to develop or obtain internal-use software. The adoption of this ASU on July 1, 2020 did not have a material impact on our condensed consolidated financial statements.

Accounting pronouncements to be adopted

The Company is evaluating whether the effects of the following recent accounting pronouncements, or any other recently issued but not yet effective accounting standards, will have a material effect on the Company’s condensed consolidated financial position, results of operations or cash flows.

ASU 2019-12 - Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes

In December 2019, the FASB issued ASU No. 2019-12, “Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes.” ASU 2019-12 is intended to simplify accounting for income taxes by removing certain exceptions to the general principles in Topic 740 and amends existing guidance to improve consistent application. ASU 2019-12 is effective for fiscal years beginning after December 15, 2020 and interim periods within those fiscal years. The Company does not expect the changes to have a material impact on its financial statements.

ASU 2020-04, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting

In March 2020, the FASB issued ASU No. 2020-04, “Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting.” This standard provides practical expedients for contract modifications with the transition from reference rates, such as LIBOR, that are expected to be discontinued. This guidance is applicable for the Company's revolving credit facility and secured term facility with JPMorgan Chase Bank, N.A., which uses LIBOR as a reference rate. In addition, the facility provides for an alternative rate of interest if LIBOR is discontinued. The Company will continue to evaluate ASU 2020-04 to determine the timing and extent to which we will apply the provided accounting relief.

ASU 2020-10, Codification Improvements

In October 2020, the FASB issued ASU 2020-10, “Codification Improvements.” The purpose of the ASU is to update a variety of ASC Topics to make conforming amendments, clarifications to guidance, simplifications to wording or structure of guidance, and other minor improvements. The ASU is effective for fiscal years beginning after December 15, 2020 with early application permitted. The Company does not expect the changes to have a material impact on its financial statements.

3. LEASES

Lessee Accounting

The Company determines if an arrangement is a lease at inception. The Company has operating leases for office space, warehouses, automobiles and office equipment. USAT’s leases have lease terms of one year to eight years and some include

10

options to extend and/or terminate the lease. The exercise of lease renewal options is at the Company’s sole discretion. When deemed reasonably certain of exercise, the renewal options are included in the determination of the lease term. The Company’s lease agreements do not contain any material variable lease payments, material residual value guarantees or any material restrictive covenants.

Right-of-Use (“ROU”) assets represent the Company’s right to use an underlying asset for the lease term and lease liabilities represent the obligation to make lease payments arising from the lease. ROU assets and liabilities are recognized at commencement date of the lease based on the present value of lease payments over the lease term. As most of our leases do not provide an implicit rate, we use our incremental borrowing rate, which is the collateralized rate of interest that we would pay to borrow over a similar term an amount equal to the lease payments, based on the information available at commencement date in determining the present value of lease payments. The operating lease ROU asset also includes any lease payments made and excludes lease incentives received. USAT has lease agreements with lease and non-lease components. The Company elected the practical expedient related to treating lease and non-lease components as a single lease component for all leases as well as electing a policy exclusion permitting leases with an original lease term of less than one year to be excluded from the ROU assets and lease liabilities. Lease expense for operating lease payments is recognized on a straight-line basis over the lease term.

At December 31, 2020, the Company has the following balances recorded in the balance sheet related to its lease arrangements:

| ($ in thousands) | Classification | As of December 31, 2020 | ||||||||||||

| Assets | Operating lease right-of-use assets | $ | ||||||||||||

| Liabilities | ||||||||||||||

| Current | Accrued expenses | |||||||||||||

| Long-term | Operating lease liabilities, non-current | $ | ||||||||||||

Components of lease cost are as follows:

| ($ in thousands) | Three months ended December 31, 2020 | Three months ended December 31, 2019 | |||||||||

| Operating lease costs* | |||||||||||

| ($ in thousands) | Six months ended December 31, 2020 | Six months ended December 31, 2019 | |||||||||

| Operating lease costs* | |||||||||||

* Includes short-term lease and variable lease costs, which are not material.

Supplemental cash flow information and non-cash activity related to our leases are as follows:

| ($ in thousands) | Six months ended December 31, 2020 | Six months ended December 31, 2019 | |||||||||

| Supplemental cash flow information: | |||||||||||

| Cash paid for amounts included in the measurement of operating lease liabilities | $ | $ | |||||||||

| Non-cash activity | |||||||||||

| Right-of-use assets obtained in exchange for lease obligations: | |||||||||||

| Operating lease liabilities | $ | $ | |||||||||

11

Weighted-average remaining lease term and discount rate for our leases are as follows:

| Six months ended December 31, 2020 | |||||||||||

| Weighted-average remaining lease term (years) | |||||||||||

| Operating leases | |||||||||||

| Weighted-average discount rate | |||||||||||

| Operating leases | % | ||||||||||

Maturities of lease liabilities by fiscal year for our leases are as follows:

| ($ in thousands) | Operating Leases | ||||

| Remainder of 2021 | $ | ||||

| 2022 | |||||

| 2023 | |||||

| 2024 | |||||

| 2025 | |||||

| Thereafter | |||||

| Total lease payments | $ | ||||

| Less: Imputed interest | ( | ||||

| Present value of lease liabilities | $ | ||||

Lessor Accounting

The Company offers its customers financing for the lease of our POS electronic payment devices. We account for these transactions as sales-type leases. Our sales-type leases generally have a non-cancellable term of 60 months. Certain leases contain an end-of-term purchase option that is generally insignificant and is reasonably certain to be exercised by the lessee. Leases that do not meet the criteria for sales-type lease accounting are accounted for as operating leases, which are typically our JumpStart program leases, which are agreements for renting POS electronic payment devices. JumpStart terms are typically 36 months and are cancellable with 30 to 60 days' written notice.

The Company treats lease and non-lease components as a single component for those leases where the timing and pattern of transfer for the non-lease component and associated lease component are the same and the stand-alone lease component would be classified as an operating lease if accounted for separately. The combined component is then accounted for under Topic 606, Revenue from Contracts with Customers or Topic 842 depending on the predominant characteristic of the combined component, which was Topic 606 for the Company's operating leases. All QuickStart leases are sales-type and do not qualify for the election.

Lessor consideration is allocated between lease components and the non-lease components using the requirements under Topic 606. Revenue from sales-type leases is recognized upon shipment to the customer and the interest portion is deferred and recognized as earned. The revenues related to the sales-type leases are included in Equipment sales in the Condensed Consolidated Statements of Operations and a portion of the lease payments as interest income. Revenue from operating leases is recognized ratably over the applicable service period with service fee revenue related to the leases included in License and transaction fees in the Condensed Consolidated Statements of Operations.

Property and equipment used for the operating lease rental program consisted of the following:

| ($ in thousands) | December 31, 2020 | June 30, 2020 | ||||||||||||

| Cost | $ | |||||||||||||

| Accumulated depreciation | ( | ( | ||||||||||||

| Net | $ | $ | ||||||||||||

12

4. REVENUE

Disaggregated Revenue

Based on similar operational and economic characteristics, the Company’s revenue from contracts with customers is disaggregated by License and transaction fees and Equipment sales, as reported in the Company’s Condensed Consolidated Statements of Operations. The Company believes these revenue categories depict how the nature, amount, timing, and uncertainty of its revenue and cash flows are influenced by economic factors, and also represent the level at which management makes operating decisions and assesses financial performance.

Transaction Price Allocated to Future Performance Obligations

In determining the transaction price allocated to unsatisfied performance obligations, we do not include non-recurring charges. Further, we apply the practical expedient to not consider arrangements with an original expected duration of one year or less, which are primarily month to month rental agreements. The majority of our contracts have a contractual term of between 36 and 60 months based on implied and explicit termination penalties. These amounts will be converted into revenue in future periods as work is performed, primarily based on the services provided or at delivery and acceptance of products, depending on the applicable accounting method for the services or products being delivered.

The following table reflects the estimated fees to be recognized in the future related to performance obligations that are unsatisfied at the end of the period:

| ($ in thousands) | As of December 31, 2020 | ||||

| Remainder of 2021 | $ | ||||

| 2022 | |||||

| 2023 | |||||

| 2024 | |||||

| 2025 and thereafter | |||||

| Total | $ | ||||

Contract Liabilities

The Company’s contract liability (i.e., deferred revenue) balances are as follows:

| Three months ended December 31, | Three months ended December 31, | |||||||||||||

| ($ in thousands) | 2020 | 2019 | ||||||||||||

| Deferred revenue, beginning of the period | $ | $ | ||||||||||||

| Deferred revenue, end of the period | ||||||||||||||

| Revenue recognized in the period from amounts included in deferred revenue at the beginning of the period | $ | $ | ||||||||||||

| Six months ended December 31, | Six months ended December 31, | |||||||||||||

| ($ in thousands) | 2020 | 2019 | ||||||||||||

| Deferred revenue, beginning of the period | $ | $ | ||||||||||||

| Deferred revenue, end of the period | ||||||||||||||

| Revenue recognized in the period from amounts included in deferred revenue at the beginning of the period | $ | $ | ||||||||||||

The change in the contract liability balances period-over-period is primarily the result of timing difference between the Company’s satisfaction of a performance obligation and payment from the customer.

13

Contract Costs

At December 31, 2020 and June 30, 2020, the Company had net capitalized costs to obtain contracts of $0.4 million included in Prepaid expenses and other current assets and $1.8 million included in Other noncurrent assets on the Condensed Consolidated Balance Sheet. None of these capitalized contract costs were impaired. During the three and six months ended December 31, 2020, amortization of capitalized contract costs was $0.1 million and $0.3 million. During the three and six months ended December 31, 2019, amortization of capitalized contract costs was $0.1 million and $0.2 million.

5. FINANCE RECEIVABLES

The Company's finance receivables consist of financed devices under the Quickstart program and devices contractually associated with the Seed platform. Predominately all of the Company’s finance receivables agreements are classified as non-cancellable sixty month sales-type leases. As of December 31, 2020 and June 30, 2020, finance receivables consist of the following:

| ($ in thousands) | December 31, 2020 | June 30, 2020 | ||||||||||||

| Current finance receivables, net | $ | |||||||||||||

| Finance receivables due after one year, net | ||||||||||||||

Total finance receivables, net of allowance of $ | $ | $ | ||||||||||||

We collect lease payments from customers primarily as part of the flow of funds from our transaction processing service. Balances are considered past due if customers do not have sufficient transaction revenue to cover the monthly lease payment by the end of the monthly billing period. The Company routinely monitors customer payment performance and uses prior payment performance as a measure to assess the capability of the customer to repay contractual obligations of the lease agreements as scheduled. On an as-needed basis, qualitative information may be taken into consideration if new information arises related to the customer’s ability to repay the lease.

Credit risk for these receivables is continuously monitored by management and reflected within the allowance for finance receivables by aggregating leases with similar risk characteristics into pools that are collectively assessed. Because the Company’s lease contracts generally have similar terms, customer characteristics around transaction processing volume and sales were used to disaggregate the leases. Our key credit quality indicator is the amount of transaction revenue we process for each customer relative to their lease payment due, as we consider this customer characteristic to be the strongest predictor of the risk of customer default. Customers with low processing volume or with transaction sales that are insufficient to cover the lease payment are considered to be at a higher risk of customer default.

Customers are pooled based on their ratio of gross sales to required monthly lease obligations. We categorize outstanding receivables into two categories: high ratio customers (customers who have adequate transaction processing volumes to cover monthly fees) and low ratio customers (customers that do not consistently have adequate transaction processing volumes to cover monthly fees). Using these two categories, we performed an analysis of historical write-offs to calculate reserve percentages by aging buckets for each category of customer.

At December 31, 2020, the gross lease receivable by current payment performance on a contractual basis and year of origination consisted of the following:

| Leases by Origination | ||||||||||||||||||||||||||||||||||||||||||||

| ($ in thousands) | Up to 1 Year Ago | Between 1 and 2 Years Ago | Between 2 and 3 Years Ago | Between 3 and 4 Years Ago | Between 4 and 5 Years Ago | More than 5 Years Ago | Total | |||||||||||||||||||||||||||||||||||||

| Current | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| 30 days and under | ||||||||||||||||||||||||||||||||||||||||||||

| 31-60 days | ||||||||||||||||||||||||||||||||||||||||||||

| 61-90 days | ||||||||||||||||||||||||||||||||||||||||||||

| Greater than 90 days | ||||||||||||||||||||||||||||||||||||||||||||

| Total finance receivables | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

14

At June 30, 2020, the gross lease receivable by current payment performance on a contractual basis and year of origination consisted of the following:

| Leases by Origination | ||||||||||||||||||||||||||||||||||||||||||||

| ($ in thousands) | Up to 1 Year Ago | Between 1 and 2 Years Ago | Between 2 and 3 Years Ago | Between 3 and 4 Years Ago | Between 4 and 5 Years Ago | More than 5 Years Ago | Total | |||||||||||||||||||||||||||||||||||||

| Current | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| 30 days and under | ||||||||||||||||||||||||||||||||||||||||||||

| 31-60 days | ||||||||||||||||||||||||||||||||||||||||||||

| 61-90 days | ||||||||||||||||||||||||||||||||||||||||||||

| Greater than 90 days | ||||||||||||||||||||||||||||||||||||||||||||

| Total finance receivables | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

At December 31, 2020, credit quality indicators by year of origination consisted of the following:

| Leases by Origination | ||||||||||||||||||||||||||||||||||||||||||||

| ($ in thousands) | Up to 1 Year Ago | Between 1 and 2 Years Ago | Between 2 and 3 Years Ago | Between 3 and 4 Years Ago | Between 4 and 5 Years Ago | More than 5 Years Ago | Total | |||||||||||||||||||||||||||||||||||||

| High ratio customers | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| Low ratio customers | ||||||||||||||||||||||||||||||||||||||||||||

| Total finance receivables | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

The following table represents a rollforward of the allowance for finance receivables for the six months ending December 31, 2020 and 2019:

| Six months ended December 31, | Six months ended December 31, | |||||||||||||

| ($ in thousands) | 2020 | 2019 | ||||||||||||

| Balance at June 30 | $ | $ | ||||||||||||

| Impact of ASC 326 * | — | |||||||||||||

| Provision for expected losses | ||||||||||||||

| Balance at September 30 | ||||||||||||||

| Provision for expected losses | ||||||||||||||

| Write-offs | ( | |||||||||||||

| Balance at December 31 | $ | $ | ||||||||||||

* The Company adopted ASC 326 on July 1, 2020.

15

Cash to be collected on our performing finance receivables due for each of the fiscal years are as follows:

| ($ in thousands) | |||||

| 2021 | $ | ||||

| 2022 | |||||

| 2023 | |||||

| 2024 | |||||

| 2025 | |||||

| Thereafter | |||||

| Total amounts to be collected | |||||

| Less: interest | ( | ||||

| Less: allowance for receivables | ( | ||||

| Total finance receivables | $ | ||||

6. LOSS PER SHARE

The calculation of basic and diluted loss per share are presented below:

| Three months ended December 31, | ||||||||||||||

| ($ in thousands, except per share data) | 2020 | 2019 | ||||||||||||

| Numerator for basic and diluted loss per share | ||||||||||||||

| Net loss applicable to common shareholders | $ | ( | $ | ( | ||||||||||

Denominator for basic loss per share - Weighted average shares outstanding | ||||||||||||||

| Effect of dilutive potential common shares | ||||||||||||||

Denominator for diluted loss per share - Adjusted weighted average shares outstanding | ||||||||||||||

| Basic loss per share | $ | ( | $ | ( | ||||||||||

| Diluted loss per share | $ | ( | $ | ( | ||||||||||

| Six months ended December 31, | ||||||||||||||

| ($ in thousands, except per share data) | 2020 | 2019 | ||||||||||||

| Numerator for basic and diluted loss per share | ||||||||||||||

| Net loss applicable to common shareholders | $ | ( | $ | ( | ||||||||||

Denominator for basic loss per share - Weighted average shares outstanding | ||||||||||||||

| Effect of dilutive potential common shares | ||||||||||||||

Denominator for diluted loss per share - Adjusted weighted average shares outstanding | ||||||||||||||

| Basic loss per share | $ | ( | $ | ( | ||||||||||

| Diluted loss per share | $ | ( | $ | ( | ||||||||||

16

7. GOODWILL AND INTANGIBLES

Intangible asset balances and goodwill consisted of the following:

| As of December 31, 2020 | ||||||||||||||||||||||||||

| ($ in thousands) | Gross | Accumulated Amortization | Net | Amortization Period | ||||||||||||||||||||||

| Intangible assets: | ||||||||||||||||||||||||||

| Brand and tradenames | $ | $ | ( | $ | ||||||||||||||||||||||

| Developed technology | ( | |||||||||||||||||||||||||

| Customer relationships | ( | |||||||||||||||||||||||||

| Total intangible assets | $ | $ | ( | $ | ||||||||||||||||||||||

| Goodwill | — | Indefinite | ||||||||||||||||||||||||

| As of June 30, 2020 | ||||||||||||||||||||||||||

| ($ in thousands) | Gross | Accumulated Amortization | Net | Amortization Period | ||||||||||||||||||||||

| Intangible assets: | ||||||||||||||||||||||||||

| Brand and tradenames | ( | |||||||||||||||||||||||||

| Developed technology | ( | |||||||||||||||||||||||||

| Customer relationships | ( | |||||||||||||||||||||||||

| Total intangible assets | $ | $ | ( | $ | ||||||||||||||||||||||

| Goodwill | — | Indefinite | ||||||||||||||||||||||||

For the three and six months ended December 31, 2020 and 2019, there was $0.8 million and $1.6 million in amortization expense related to intangible assets, respectively, that was recognized.

The Company performs an annual goodwill impairment test on April 1 and more frequently if events and circumstances indicate that the asset might be impaired. The Company has determined that there is a single reporting unit for purposes of testing goodwill for impairment. During the three and six months ended December 31, 2020, the Company did not recognize any impairment charges related to goodwill.

8. DEBT AND OTHER FINANCING ARRANGEMENTS

The Company's debt and other financing arrangements as of December 31, 2020 and June 30, 2020 consisted of the following:

| As of December 31, | As of June 30, | |||||||||||||

| ($ in thousands) | 2020 | 2020 | ||||||||||||

| 2020 Antara Term Facility | $ | $ | ||||||||||||

| 2021 JPMorgan Credit Facility | ||||||||||||||

| PPP and other loans | ||||||||||||||

| Less: unamortized issuance costs and debt discount | ( | ( | ||||||||||||

| Total | ||||||||||||||

| Less: debt and other financing arrangements, current | ( | ( | ||||||||||||

| Debt and other financing arrangements, noncurrent | $ | $ | ||||||||||||

17

Details of interest expense presented on the Condensed Consolidated Statements of Operations are as follows:

| Three months ended | Six months ended | |||||||||||||||||||||||||

| December 31, | December 31, | |||||||||||||||||||||||||

| ($ in thousands) | 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||||

| 2020 Antara Term Facility | $ | $ | $ | $ | ||||||||||||||||||||||

| 2021 JPMorgan Credit Facility | ||||||||||||||||||||||||||

| 2018 JPMorgan Revolving Credit Facility | ||||||||||||||||||||||||||

| 2018 JPMorgan Term Loan | ||||||||||||||||||||||||||

| Other interest expense | ||||||||||||||||||||||||||

| Total interest expense | $ | $ | $ | $ | ||||||||||||||||||||||

JPMorgan Chase Bank Credit Agreement

On August 14, 2020, the Company repaid all amounts outstanding under the $30.0 million senior secured term loan facility (“2020 Antara Term Facility”) with Antara Capital Master Fund LP (“Antara”) and entered into a credit agreement with JPMorgan Chase Bank, N.A.

The 2021 JPMorgan Credit Agreement provides for a $5 million secured revolving credit facility (the “2021 JPMorgan Revolving Facility”) and a $15 million secured term facility (the “2021 JPMorgan Secured Term Facility” and together with the 2021 JPMorgan Revolving Facility, the “2021 JPMorgan Credit Facility”), which includes an uncommitted expansion feature that allows the Company to increase the total revolving commitments and/or add new tranches of term loans in an aggregate amount not to exceed $5 million. In connection with the consummation of the 2021 JPMorgan Credit Agreement, the Company repaid all amounts outstanding under the 2020 Antara Term Facility. The Company recognized $2.8 million of interest expense related to the 2020 Antara Term Facility during the fiscal quarter ended September 30, 2020, including the recognition of $2.6 million of unamortized issuance costs and debt discount as interest expense, reflecting the difference between the carrying value of the 2020 Antara Term Facility and the amount due upon repayment.

The 2021 JPMorgan Credit Facility has a three year maturity, with interest determined, at the Company’s option, on a base rate of LIBOR or Prime Rate plus an applicable margin tied to the Company’s total leverage ratio and having ranges between 2.75 % and 3.75 % for Prime rate loans and between 3.75 % and 4.75 % for LIBOR rate loans. In the event of default, the interest rate may be increased by 2.00 %. The 2021 JPMorgan Credit Facility will also carry a commitment fee of 0.50 % per annum on the unused portion. Through December 31, 2021, the applicable interest rate was Prime Rate plus 3.75 %. Principal payments are due in quarterly installments of $187,500 beginning December 31, 2020 through September 30, 2022 for a total annual repayment of $750,000 and total repayment over the period of $1,500,000 . Beginning December 31, 2022 through June 30, 2023, principal payments are due in quarterly installments of $375,000 for a total repayment over the period of $1,125,000 . The remaining unpaid principal amounts are due at the maturity date of the 2021 JPMorgan Credit Facility.

The Company’s obligations under the 2021 JPMorgan Credit Facility are secured by first priority security interests in substantially all of the assets of the Company. The 2021 JPMorgan Credit Agreement includes customary representations, warranties and covenants, and acceleration, indemnity and events of default provisions, including a financial covenant requiring the Company to maintain an adjusted quick ratio of not less than 2.00 to 1.00 through and including September 30, 2020, not less than 2.50 to 1.00 beginning October 1, 2020, not less than 2.75 to 1.00 beginning January 1, 2021 and not less than 3.00 to 1.00 beginning April 1, 2021, and a financial covenant requiring the Company to maintain, as of the end of each of its fiscal quarters commencing with the fiscal quarter ended December 31, 2021, a total leverage ratio of not greater than 3.00 to 1.00. The Company was in compliance with its financial covenants as of December 31, 2020.

Term Facility with Antara

On October 9, 2019, the Company entered into a commitment letter with Antara, pursuant to which Antara committed to extend to the Company a $30.0 million senior secured term loan facility. On October 31, 2019, the Company entered into a Financing Agreement with Antara to draw $15.0 million on the 2020 Antara Term Facility and agreed to draw an additional $15.0 million at any time between July 31, 2020 and April 30, 2021, subject to the terms of the Financing Agreement. If the Company failed to make the subsequent draw on the 2020 Antara Term Facility by April 30, 2021, the Company would pay Antara a commitment termination fee equal to 3 % of the subsequent draw commitment. The outstanding amount of the draws under the 2020 Antara Term Facility bore interest at 9.75 % per annum, payable monthly in arrears. The proceeds of the initial draw were

18

used to repay the outstanding balance of the 2018 JPMorgan Revolving Credit Facility (as defined below) due to JPMorgan in the amount of $10.1 million, including accrued interest, and to pay transaction expenses. The Company would also incur a prepayment premium of 5 % of the principal balance if prepaid on or prior to December 31, 2020.

On October 9, 2019, the Company also sold shares of the Company’s common stock to Antara at a price below market value. Since the 2020 Antara Term Facility and equity issuance were negotiated in contemplation of each other and executed within a short period of time, the Company evaluated the debt and equity financing as a combined arrangement, and estimated the fair values of the debt and equity components to allocate the proceeds, net of the registration rights agreement liability on a relative fair value basis between the debt and equity components. The non-lender fees incurred to establish the debt and equity financing arrangement were allocated to the debt and equity components on a relative fair value basis and capitalized on the Company’s balance sheet. $0.9 million was allocated to debt issuance costs and $0.1 million was allocated to debt commitment fees. The 2020 Antara Term Facility agreement also contained a mandatory prepayment feature that was determined to be an embedded derivative, requiring bifurcation and fair value recognition for the derivative liability. The allocation of the proceeds to the debt component and the bifurcation of the embedded derivative liability resulted in a $2.1 million debt discount, which was de-recognized during the three months ended September 30, 2020.

On August 14, 2020, the Company repaid all amounts outstanding under the 2020 Antara Term Facility and entered into the 2021 JPMorgan Credit Agreement. The Company recorded a liability for the commitment termination fee and prepayment premium for $1.2 million as of June 30, 2020, which was paid during the three months ended September 30, 2020.

Revolving Credit Facility and Term Loan with JPMorgan Chase

On November 9, 2017, in connection with the acquisition of Cantaloupe, the Company entered into a five year credit agreement among the Company, as the borrower, its subsidiaries, as guarantors, and JPMorgan, as the lender and administrative agent for the lender (the “Lender”), pursuant to which the Lender (i) made a $25 million term loan (“2018 JPMorgan Term Loan”) to the Company and (ii) provided the Company with a line of credit (“2018 JPMorgan Revolving Credit Facility”) under which the Company may borrow revolving credit loans in an aggregate principal amount not to exceed $12.5 million at any time. All advances under the 2018 JPMorgan Revolving Credit Facility and all other obligations were required to be paid in full at maturity on November 9, 2022. The applicable interest rate on the loans for the year to date ended October 31, 2019 was LIBOR plus 4 %. On September 30, 2019, the Company prepaid the remaining principal balance of the 2018 JPMorgan Term Loan, and on October 31, 2019, the Company repaid the outstanding balance on the 2018 JPMorgan Revolving Credit Facility.

Other Borrowings

In the fourth quarter of fiscal year 2020, we received loan proceeds of approximately $3.1 million (the “PPP Loan”) pursuant to the Paycheck Protection Program under the Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”) administered by the U.S. Small Business Administration (the “SBA”). We used the PPP Loan in accordance with the provisions of the CARES Act. The loan bears a fixed interest rate of 1% over a two year term from the approval date of April 28, 2020. The application for these funds required the Company to, in good faith, certify that the economic uncertainty caused by COVID-19 made the loan request necessary to support the ongoing operations of the Company. This certification further required the Company to take into account our current business activity and our ability to access other sources of liquidity sufficient to support ongoing operations in a manner that is not significantly detrimental to the business. The receipt of these funds, and the forgiveness of the loan attendant to these funds, is dependent on the Company having initially qualified for the loan and qualifying for the forgiveness of such loan based on our future adherence to the forgiveness criteria. The Company anticipates filing for the forgiveness of the loan in the quarter ended March 31, 2021.

19

9. ACCRUED EXPENSES

Accrued expenses consisted of the following as of December 31, 2020 and June 30, 2020:

| As of December 31, | As of June 30, | |||||||||||||

| ($ in thousands) | 2020 | 2020 | ||||||||||||

| Accrued sales tax | $ | $ | ||||||||||||

| Accrued compensation and related sales commissions | ||||||||||||||

| Operating lease liabilities, current | ||||||||||||||

| Accrued professional fees | ||||||||||||||

| Income taxes payable | ||||||||||||||

| Accrued other taxes and filing fees | ||||||||||||||

| Accrued other, including settlement of shareholder class action lawsuit | ||||||||||||||

| Total accrued expenses | $ | $ | ||||||||||||

10. FAIR VALUE MEASUREMENTS

The accounting guidance for fair value provides a framework for measuring fair value, clarifies the definition of fair value and expands disclosures regarding fair value measurements. Fair value is defined as the price that would be received in the sale of an asset or paid to transfer a liability (an exit price) in an orderly transaction between market participants at the reporting date. The accounting guidance establishes a three-tiered hierarchy, which prioritizes the inputs used in the valuation methodologies in measuring fair value as follows:

Level 1 ‑ Inputs are unadjusted quoted prices in active markets for identical assets or liabilities that the Company has the ability to access at the measurement date.

Level 2 ‑ Inputs are other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly. Level 2 inputs include quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the asset or liability (i.e., interest rates, yield curves, etc.), and inputs that are derived principally from or corroborated by observable market data by correlation or other means (market corroborated inputs).

Level 3 ‑ Inputs are unobservable and reflect the Company’s assumptions that market participants would use in pricing the asset or liability. The Company develops these inputs based on the best information available.

Financial assets and liabilities are initially recorded at fair value. The carrying amounts of certain of the Company’s financial instruments, including cash equivalents, accounts receivable, accounts payable and accrued expenses, are carried at cost which approximates fair value due to the short-term maturity of these instruments and are Level 1 assets or liabilities of the fair value hierarchy. We have not identified material impacts from COVID-19 on the fair value of our financial assets and liabilities.

The Company’s obligations under its long-term debt agreements are carried at amortized cost, which approximates their fair value as of December 31, 2020. The fair value of the Company’s obligations under its long-term debt agreements with JPMorgan Chase were considered Level 2 liabilities of the fair value hierarchy because these instruments have interest rates that reset frequently. The fair value of the Company's obligations under its long-term debt agreements with Antara as of June 30, 2020 was approximately $15.8 million and considered a Level 3 liability of the fair value hierarchy because this instrument used significant unobservable inputs consistent with those used in determining the embedded derivative liability values, as discussed below.

As discussed in Note 8, the Company’s 2020 Antara Term Facility agreement contained a mandatory prepayment feature that was determined to be an embedded derivative, requiring bifurcation and fair value recognition. At June 30, 2020, the Company’s embedded derivative liability was measured at fair value using a probability-weighted discounted cash flow model including assumptions for (1) management's estimates of the probability and timing of future cash flows and related events; (2) the Company's risk-adjusted discount rate that includes a company-specific risk premium; and (3) the Company's cost of debt; and was classified as a Level 3 liability of the fair value hierarchy and included as a component of Accrued expenses on the

20

11. INCOME TAXES

On December 21, 2020, Congress approved the Consolidated Appropriations Act, 2021 (the “Appropriations Act”), which was signed into law by the President on December 27, 2020. The Appropriations Act funds the federal government to the end of the fiscal year and provides further COVID-19 economic relief. Some of the business provisions included in the Appropriations Act are additional Paycheck Protection Program (PPP) loans, clarification of the deductibility of business expenses that were paid for with PPP funds, expansion of the employee retention credit, and temporary full deduction for business expenses for food and beverages provided by a restaurant. The Appropriations Act did not have a material impact on the Company’s income taxes. The Company will continue to monitor for additional legislation related to COVID-19 and its impact on our results of operations.

For the three months ended December 31, 2020, the Company recorded an income tax provision of $49 thousand. For the six months ended December 31, 2020, the Company recorded an income tax provision of $89 thousand. As of December 31, 2020, the Company reviewed the existing deferred tax assets and continues to record a full valuation against its deferred tax assets. The income tax provisions primarily relate to the Company's uncertain tax positions, as well as state income and franchise taxes. As of December 31, 2020, the Company had a total unrecognized income tax benefit of $0.2 million. The provision is based upon actual loss before income taxes for the six months ended December 31, 2020, as the use of an estimated annual effective income tax rate does not provide a reliable estimate of the income tax provision. The Company will continue to monitor the status of the COVID-19 pandemic and its impact on our results of operations.

For the three months ended December 31, 2019, the Company recorded an income tax provision of $72 thousand. For the six months ended December 31, 2019, an income tax provision of $131 thousand was recorded. As of December 31, 2019, the Company continued to record a full valuation against its deferred tax assets. The income tax provision primarily relates to the Company’s uncertain tax positions, as well as state income and franchise taxes. As of December 31, 2019, the Company had a total unrecognized income tax benefit of $0.3 million. The provision is based upon actual loss before income taxes for the six months ended December 31, 2019, as the use of an estimated annual effective income tax rate does not provide a reliable estimate of the income tax provision.

12. EQUITY

WARRANTS

The Company had 23,978 5.00

STOCK OPTIONS

The Company estimates the grant date fair value of the stock options it grants using a Black-Scholes valuation model. The Company’s assumption for expected volatility is based on its historical volatility data related to market trading of its own common stock. The Company uses the simplified method to determine expected term, as the Company does not have adequate historical exercise and forfeiture behavior on which to base the expected life assumption. The dividend yield assumption is based on dividends expected to be paid over the expected life of the stock option. The risk-free interest rate assumption is determined by using the U.S. Treasury rates of the same period as the expected option term of each stock option.

During the three and six months ended December 31, 2020, the Company granted stock options to certain employees which vest each year over a three-year period. Certain of those stock options are also subject to the achievement of goals to be established by the Company for each fiscal year. Because the performance conditions of those stock options granted had not yet been established as of December 31, 2020, a measurement date under ASC 718, Compensation - Stock Compensation, has not yet been established for those stock options and compensation cost will not be measured and recorded until the date on which those specific performance terms are established and mutually understood with the awardee. In January 2021, the Compensation Committee of the Board of Directors established and approved the performance metrics applicable to the above mentioned stock options.

21

The fair value of all options granted during the six months ended December 31, 2020 and 2019 was determined using the following assumptions and includes only options with an established measurement date under ASC 718:

| Six months ended December 31, | ||||||||||||||

| 2020 | 2019 | |||||||||||||

| Expected volatility (percent) | ||||||||||||||

| Weighted average expected life (years) | ||||||||||||||

| Dividend yield (percent) | % | % | ||||||||||||

| Risk-free interest rate (percent) | ||||||||||||||

| Number of options granted | ||||||||||||||

| Weighted average exercise price | $ | $ | ||||||||||||

| Weighted average grant date fair value | $ | $ | ||||||||||||

Stock based compensation related to stock options for the three and six months ended December 31, 2020 was $1.4 million and $2.5 million, respectively, and for the three and six months ended December 31, 2019 was $1.1 million and $1.4 million, respectively.

COMMON STOCK

There were no significant new common stock awards granted during the three and six months ended December 31, 2020.

The total expense recognized for all common stock awards for the three and six months ended December 31, 2020 was $0.3 million and $0.7 million, respectively, and for the three and six months ended December 31, 2019 was $0.5

13. COMMITMENTS AND CONTINGENCIES

Litigation

We are a party to litigation and other proceedings that arise in the ordinary course of our business. These types of matters could result in fines, penalties, compensatory or treble damages or non-monetary sanctions or relief. In accordance with the accounting guidance for contingencies, we reserve for litigation claims and assessments asserted or threatened against us when a loss is probable and the amount of the loss can be reasonably estimated. We cannot predict the outcome of legal or other proceedings with certainty.

Eastern District of Pennsylvania Consolidated Shareholder Class Actions

As previously reported, on September 11, 2018, Stéphane Gouet filed a putative class action complaint against the Company, Stephen P. Herbert, the then-current Chief Executive Officer, and Priyanka Singh, the then-current Chief Financial Officer, in the United States District Court for the District of New Jersey. The class was defined as purchasers of the Company’s securities from November 9, 2017 through September 11, 2018. The complaint alleged that the Company disclosed on September 11, 2018 that it was unable to timely file its Annual Report on Form 10-K for the fiscal year ended June 30, 2018 (the “2018 Form 10-K”), and that the Audit Committee of the Company’s Board of Directors was in the process of conducting an internal investigation of current and prior period matters relating to certain of the Company’s contractual arrangements, including the accounting treatment, financial reporting and internal controls related to such arrangements. The complaint alleged that the defendants disseminated false statements and failed to disclose material facts and engaged in practices that operated as a fraud or deceit upon Gouet and others similarly situated in connection with their purchases of the Company’s securities during the proposed class period. The complaint alleged violations of Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 (the “1934 Act”) and Rule 10b-5 promulgated thereunder.

Two additional class action complaints, containing substantially the same factual allegations and legal claims, were filed against the Company, Herbert and Singh in the United States District Court for the District of New Jersey. On September 13, 2018, David Gray filed a putative class action complaint, and on October 3, 2018, Anthony E. Phillips filed a putative class action complaint. Subsequently, multiple shareholders moved to be appointed lead plaintiff, and on December 19, 2018, the Court consolidated the three actions, appointed a lead plaintiff (the “Lead Plaintiff”), and appointed lead counsel for the consolidated actions (the “Consolidated Action”).

22

On February 28, 2019, the Court approved a Stipulation agreed to by the parties in the Consolidated Action for the filing of an amended complaint within fourteen days after the Company filed its 2018 Form 10-K. On January 22, 2019, the Company and Herbert filed a motion to transfer the Consolidated Action to the United States District Court for the Eastern District of Pennsylvania. On February 5, 2019, the Lead Plaintiff filed its opposition to the Motion to Transfer. On August 12, 2019, the University of Puerto Rico Retirement System (“UPR”) filed a putative class action complaint in the United States District Court for the District of New Jersey against the Company, Herbert, Singh, the Company’s Directors at the relevant time (Steven D. Barnhart, Joel Books, Robert L. Metzger, Albin F. Moschner, William J. Reilly and William J. Schoch) (the “Independent Directors”), and the investment banking firms who acted as underwriters for the May 2018 follow-on public offering of the Company (the “Public Offering”): William Blair & Company; LLC; Craig-Hallum Capital Group, LLC; Northland Securities, Inc.; and Barrington Research Associates, Inc. (the “Underwriters”). The class was defined as purchasers of the Company’s shares pursuant to the registration statement and prospectus issued in connection with the Public Offering. Plaintiff sought to recover damages caused by Defendants’ alleged violations of the Securities Act of 1933 (as amended, the “1933 Act”), and specifically Sections 11, 12 and 15 thereof. The complaint generally sought compensatory damages, rescissory damages and attorneys’ fees and costs. The UPR complaint was consolidated into the Consolidated Action and the UPR docket was closed.

On September 30, 2019, the Court granted the motion to transfer and transferred the Consolidated Action to the United States District Court for the Eastern District of Pennsylvania, Docket No. 19-cv-04565. On November 20, 2019, Plaintiff filed an amended complaint that asserted claims under both the 1933 Act and the 1934 Act. Defendants filed motions to dismiss on February 3, 2020. Before briefing on the motions was completed, the parties participated in a private mediation on February 27, 2020, which ultimately resulted in a settlement. On May 29, 2020, the plaintiffs filed documents with the Court seeking preliminary approval of the settlement, with the defendants supporting approval of the settlement. On June 9, 2020, the Court granted preliminary approval of the settlement and issued a scheduling order for further action on the settlement. The settlement provides for a payment of $15.3 million which includes all administrative costs and plaintiffs’ attorneys’ fees and expenses. The Company’s insurance carriers paid approximately $12.7 million towards the settlement and the Company paid approximately $2.6 million towards the settlement. The settlement payments were deposited into an escrow account in July 2020. Only one putative class member submitted an objection to the settlement. On October 30, 2020, the Court held a hearing on the motion for final settlement approval and granted approval. Under the settlement, payment of plaintiffs’ counsel’s fees and expenses may be distributed within three business days of approval (subject to being returned if the settlement is reversed based on any appeal). The deadline for filing an appeal has now passed, so final settlement approval order is no longer at risk of being reversed or revised on appeal and this action is completed.

Chester County, Pennsylvania Class Action

As previously reported, a putative shareholder class action complaint was filed against the Company, its chief executive officer and chief financial officer at the relevant time, its directors at the relevant time, and the Underwriters, in the Court of Common Pleas, Chester County, Pennsylvania, Docket No. 2019-04821-MJ. The complaint alleged violations of the 1933 Act. As also previously reported, on September 20, 2019 the Court granted the defendants’ Petition for Stay and stayed the Chester County action until the Consolidated Action reaches a final disposition. On October 18, 2019, plaintiff filed an appeal to the Pennsylvania Superior Court from the Order granting defendants’ Petition for Stay, Docket No. 3100 EDA 2019. On December 6, 2019, the Pennsylvania Superior Court issued an Order stating that the Stay Order does not appear to be final or otherwise appealable and directed plaintiff to show cause as to the basis of the Pennsylvania Superior Court’s jurisdiction. The plaintiff filed a Response to the Order to Show Cause on December 16, 2019, and the defendants filed an Application to Quash Appeal on December 26, 2019. On February 20, 2020, the Pennsylvania Superior Court quashed the appeal. This action has remained stayed pending final disposition of the Consolidated Action. The Company expects that this action will be dismissed, but there can be no guarantee as to the outcome.

Department of Justice Subpoena

As previously reported, in the third quarter of fiscal year 2020, the Company responded to a subpoena received from the U.S. Department of Justice that sought records regarding Company activities that occurred during prior financial reporting periods, including restatements. The Company is cooperating fully with the agency’s queries.

Other Shareholder Demand Letters