As filed with the Securities and Exchange Commission on July 21, 2022

Registration No. 333-255805

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 9

TO

FORM

REGISTRATION STATEMENT

Under

THE SECURITIES ACT OF 1933

___________________

(Exact Name of Registrant as Specified in its Charter) |

0-21320 | ||||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

+86 (

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jun Wang

Chief Executive Officer

Yubo International Biotech Limited

Room 105, Building 5, 31 Xishiku Avenue

Xicheng District, Beijing, China

+86 (010) 6615-5141

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all correspondence to:

Lina Liu |

| Barbara A. Jones, Esq. |

Chief Financial Officer Yubo International Biotech Limited Room 105, Building 5, 31 Xishiku Avenue Xicheng District, Beijing, China +86 (010) 6615-5141 |

| Greenberg Traurig, LLP 1840 Century Park East, Suite 1900 Los Angeles, California 90067 +1 (310) 586-7700 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

Emerging growth company | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the SEC, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. Neither we nor the selling stockholders may sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell these securities, nor a solicitation of an offer to buy these securities, in any jurisdiction where the offer, solicitation, or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 21, 2022

PRELIMINARY PROSPECTUS

YUBO INTERNATIONAL BIOTECH LIMITED

5,000,000 Shares of Class A Common Stock Offered by the Company

12,251,100 Shares of Class A Common Stock Offered by the Selling Stockholders

We are offering, on a “best efforts” basis, up to an aggregate of 5,000,000 shares of our Class A common stock, par value 0.001 per share, at a fixed price of $0.50 per share. Our shares of Class A common stock are quoted on the OTC Marketplace under the symbol “YBGJ.” On July 19, 2022, the last reported sale price of our Class A common stock on the OTC Marketplace was $0.13 per share.

Additionally, the selling stockholders are offering an additional 12,251,100 shares of Class A common stock, par value 0.001 per share, at a fixed price of $0.50 per share. The selling stockholders include: (i) Focus Draw Group Limited (“Focus”), which is selling up to 4,728,000 shares of our Class A common stock held by Focus (the “Focus Shares”), (ii) Dragoncloud Technology Limited (“Dragoncloud”), which is selling up to 5,768,100 shares of our Class A common stock held by Dragoncloud (the “Dragoncloud Shares”), and (iii) Cheung Ho Shun (“Cheung”), who is selling up to 1,755,000 shares of our Class A common stock held by Cheung (the “Cheung Shares”). The Focus Shares, the Dragoncloud Shares and the Cheung Shares are referred to collectively as the “Resale Securities.”

We are offering the shares on a self-underwritten basis which means our officers and directors will attempt to sell the shares in reliance on the safe harbor from broker-dealer registration under Rule 3a4-1 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All funds that we raise from the offering will be immediately available for our use and will not be returned to investors. We do not have any arrangements to place the funds received from the sale of shares in the offering in an escrow, trust or similar account.

The offering will end on December 31, 2022, unless all of the shares are sold before that date, we extend the offering another 30 days or we otherwise decide to terminate the offering early or cancel it, in each case in our sole discretion. If we extend the offering, we will provide that information in an amendment to this prospectus. If we close the offering early or cancel it, including during any extended offering period, we may do so without notice to investors, although if we cancel the offering we will promptly return any funds investors may already have paid. We will bear the expenses relating to the registration of the shares. The selling stockholder will sell the Resale Securities at a fixed price of $0.50 per share.

We are a U.S. holding company primarily operating through our wholly owned subsidiary, Platinum International Biotech Co., Ltd., a company organized under the laws of the Cayman Islands (“Platinum”). Platinum is not a Chinese operating company but a Cayman Islands holding company which in turn operates in China through its subsidiaries and contractual arrangements with a variable interest entity (the “VIE”), Yubo International Biotech (Beijing) Limited, a company organized under the laws of the People’s Republic of China and, through contractual arrangements with us, the Chinese operating company (“Yubo Beijing”). None of our Company, Platinum, or Platinum International Biotech (Hong Kong) Limited, a wholly owned subsidiary of Platinum (“Platinum HK”), each as a holding company, conducts any day-to-day business operations in China. Yubo Beijing conducts the day-to-day business operations of our Company in China through contractual relationships with us and our subsidiaries. We do not own any equity interest in Yubo Beijing. Investors in our Class A common stock are not purchasing, and may never hold, any equity interests, directly or indirectly, in Yubo Beijing through participation in this offering. As a result of our contractual relationships with Yubo Beijing, we consolidate Yubo Beijing’s financial results in our consolidated financial statements and are the primary beneficiary of Yubo Beijing for accounting purposes only.

Our corporate structure involving the VIE provides investors with contractual exposure to foreign investment in China-based companies where PRC laws prohibit direct foreign investment in Chinese operating companies in certain industries, such as Yubo Beijing. This structure involves unique risks to investors and is subject to risks relating to our contractual arrangements with Yubo Beijing and its shareholders. Our contractual arrangements with Yubo Beijing have not been tested in a court of law. If the PRC government finds these contractual arrangements non-compliant with the restrictions on direct foreign investment in the relevant industries, or if the relevant PRC laws, regulations, and rules or the interpretation thereof change in the future, we could be subject to severe penalties or be forced to relinquish our interests in Yubo Beijing or forfeit our rights under the contractual arrangements. Further, the Chinese regulatory authorities could disallow our contractual arrangements with Yubo Beijing, which would likely result in a material adverse change in our operations, and, given the resulting inability to consolidate Yubo Beijing’s financial results in our consolidated financial statements, in the value of our Class A common stock, which could significantly decline or become worthless. We and investors in our Class A common stock face uncertainty about potential future actions by the PRC government, which could affect the enforceability of our contractual arrangements with Yubo Beijing and, consequently, significantly affect our financial condition and results of operations. See “Risk Factors—Risks Related to Our Corporate Structure.”

We and Yubo Beijing face various legal and operational risks and uncertainties relating to doing business in China. We operate our business primarily in China through Yubo Beijing, which is subject to complex and evolving PRC laws and regulations. Therefore, investors of our Class A common stock face potential uncertainty from the PRC government. Changes in China’s economic, political or social conditions or government policies could materially adversely affect Yubo Beijing’s business and results of operations. Furthermore, the PRC government has significant authority to intervene or influence the China operations of an offshore holding company, such as ours, at any time. Recently, the PRC government is enhancing supervision over companies seeking listings overseas and some specific business or activities such as the use of variable interest entities and data security or anti-monopoly. Yubo Beijing has obtained all the required licenses and approvals to conduct its operations in China and, to date, no application for any such licenses and approvals has been denied. We believe we and our PRC subsidiaries, as well as Yubo Beijing, are not subject to permission requirements from the China Securities Regulatory Commission (the “CSRC”), the Cyberspace Administration of China (the “CAC”) or other governmental agency that is required for this offering. We did not retain any PRC legal counsel for purposes of this offering, and as such, we did not rely on the advice of PRC legal counsel. Our understanding with regards to the permission requirements from the CSRC, the CAC, or other PRC governmental agency is based on a risk-based analysis of the currently effective PRC laws, regulations and rules, as well as the local market practice as of the date of this prospectus. We cannot assure you that our understanding is correct, or consistent with the opinion of PRC legal counsel if one were retained to opine on such permission requirements. However, the PRC government may adopt new measures that may affect Yubo Beijing’s operations, or exert more oversight and control over offerings conducted outside of China and foreign investment in China-based companies, and we may be subject to challenges brought by these new laws, regulations and policies. These legal and operational risks, together with uncertainties in the PRC legal system and the interpretation and enforcement of PRC laws, regulations and policies, could hinder our ability to offer or continue to offer securities to investors, result in a material adverse change to Yubo Beijing’s business operations, and damage Yubo Beijing’s reputation, each of which could cause our Class A common stock to significantly decline in value or become worthless. See “Risk Factors—Risks Related to Doing Business in China.”

In addition, as more stringent criteria have been imposed by the SEC and the Public Company Accounting Oversight Board, or the PCAOB, recently, our securities may be prohibited from trading if our auditor cannot be fully inspected. As of the date of this prospectus, our auditor, Michael T. Studer CPA P.C., an independent registered public accounting firm headquartered in the United States, was not included in the determinations made by the PCAOB, on December 16, 2021. Our auditor is currently subject to PCAOB inspections and has been inspected by the PCAOB on a regular basis. In the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor because of a position taken by an authority in a foreign jurisdiction, then such lack of inspection could cause trading in our securities to be delisted from the stock exchange. Furthermore, although we believe that the Holding Foreign Companies Accountable Act and the related regulations do not currently affect us, we cannot assure you that there will not be any further implementations and interpretations of the Holding Foreign Companies Accountable Act or the related regulations, which might pose regulatory risks to and impose restrictions on us because of our operations in mainland China. See “Risk Factors—Risks Related to Doing Business in China.”

As a holding company, we may rely on dividends and other distributions on equity paid by our subsidiaries for our cash and financing requirements. See “Prospectus Summary—Dividends and Other Distributions” for a detailed diagram illustrating how cash is transferred among our main subsidiaries, the WFOE and the VIE. As of the date of this prospectus, except as disclosed below, no transfers of cash or other types of assets, dividends, or distributions have been made between our New York holding company, any of our subsidiaries, and Yubo Beijing. As of the date of this prospectus, neither we nor any of our subsidiaries have ever paid dividends or made distributions to U.S. investors. There has been no capital flow from the WFOE, Yubo Chengdu, to the VIE, Yubo Beijing. On May 15, 2021, Yubo Beijing received $500,000 from Yubo Global in the form of a loan to fund Yubo Beijing’s operations. On September 15, 2021, Yubo Global received a loan of $1,538 from Yubo Beijing to supplement Yubo Global’s general working capital. These loans are non-interest bearing and payable on demand. See Note 10: Due to Related Parties to our audited consolidated financial statements for the years ended December 31, 2021 and 2020 and our unaudited consolidated financial statements for the three months ended March 31, 2022 and 2021 included elsewhere in this prospectus. As an early-stage company, we do not intend to distribute earnings or settle amount owed under the VIE agreements, if any, in the near future. There were no intercompany revenues or expenses and no intercompany payables or receivables between Yubo Beijing and the WOFE, Yubo Chengdu, under our contractual arrangements with Yubo Beijing for the years ended December 31, 2021 and 2020 and the three months ended March 31, 2022. See the unaudited condensed consolidating balance sheets for our Company, our subsidiaries, and Yubo Beijing as of December 31, 2021 and 2020, and the unaudited condensed consolidating statements of operations for such entities for the years ended December 31, 2021 and 2020, set forth on Exhibit 99.2 to the registration statement to which this prospectus forms a part.

Investing in our securities involves a high degree of risk. You should review carefully the risks and uncertainties described under the heading “Risk Factors” beginning on page 13 of this prospectus, and under similar headings in any amendments or supplements to this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

| Per share of Common Stock |

|

| Total (100%) |

|

|

| 75% |

|

| 50% |

|

| 25% | |||||

Public offering price |

| $ | 0.50 |

|

| $ | 2,500,000.00 |

|

| $ | 1,857,000.00 |

|

| $ | 1,250,000.00 |

|

| $ | 625,000.00 |

|

Proceeds to us, before expenses |

| $ | 0.50 |

|

| $ | 2,415,058.95 |

|

| $ | 1,790,058.95 |

|

| $ | 1,165,058.95 |

|

| $ | 540,058.95 |

|

Because there is no minimum offering amount required as a condition to closing in this offering, the actual public offering amount and proceeds to us, if any, are not presently determinable and may be substantially less than the total maximum offering amounts set forth above.

The date of this prospectus is , 2022

TABLE OF CONTENTS

|

| PAGE |

| |

|

|

|

| |

|

| 1 |

| |

|

| 12 |

| |

|

| 13 |

| |

|

| 41 |

| |

|

| 42 |

| |

|

| 43 |

| |

|

| 44 |

| |

|

| 45 |

| |

|

| 46 |

| |

|

| 48 |

| |

|

| 50 |

| |

|

| 72 |

| |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

| 74 |

|

|

| 81 |

| |

|

| 84 |

| |

|

| 85 |

| |

Certain Relationships and Related Transactions and Director Independence |

|

| 88 |

|

|

| 91 |

| |

|

| 91 | ||

|

| 91 |

| |

|

| 92 |

| |

| F-1 |

| ||

You should rely only on the information contained in this prospectus. Neither we nor the selling stockholders have authorized any other person to provide you with information that is different from that contained in this prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. Neither we nor the selling stockholders take any responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. You should assume that the information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our securities. Our business, financial condition, results of operations and prospects may have changed since that date.

i |

| Table of Contents |

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all the information that you should consider before investing in our securities. You should carefully read the entire prospectus including “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our financial statements contained elsewhere in this prospectus, before making an investment decision.

In this prospectus, unless otherwise specified, the terms “we,” “our,” “us,” the “Company,” or the “Registrant” refer to Yubo International Biotech Limited, a U.S. holding company and New York corporation formerly known as Magna-Lab, Inc., and its wholly owned subsidiaries, including without limitation, Platinum International Biotech Co., Ltd., a company organized under the laws of the Cayman Islands, and Yubo International Biotech (Chengdu) Limited, a company organized under the laws of the People’s Republic of China (“Yubo Chengdu” or the “WFOE”). The term “Yubo Beijing” refers to Yubo International Biotech (Beijing) Limited, a variable interest entity organized under the laws of the People’s Republic of China, and, through contractual arrangements with us, the Chinese operating company.

Corporate Overview

We are a U.S. holding company primarily operating through our wholly owned subsidiary, Platinum. Platinum is not a Chinese operating company but a Cayman Islands holding company which in turn operates in China through its subsidiaries and contractual arrangements with Yubo Beijing, the Chinese operating company. None of our Company, Platinum, or Platinum HK, each as a holding company, conducts any day-to-day business operations in China.

Yubo Beijing conducts the day-to-day business operations of our Company in China through contractual relationships with us and our subsidiaries. Yubo Beijing is a technology company focused on the research and development and application of endometrial stem cells. Yubo Beijing is committed to building the first public endometrial stem cell repository in the world. Yubo Beijing offers its products and services under the brand “VIVCELL.” Yubo Beijing’s product offerings include healthcare products for respiratory system, skincare products, hair care products, healthy beverages and male and female personal care products. Yubo Beijing also offers stem cell related services including cell testing and health management consulting services.

Name Change

Effective December 4, 2020, we changed our corporate name from Magna-Lab, Inc. to Yubo International Biotech Limited under the stock symbol “YBGJ.”

Reverse Merger with Platinum International Biotech Co., Ltd.

On January 14, 2021 (the “Closing Date”), we entered into a voluntary share exchange transaction with Platinum International Biotech Co., Ltd., a company organized under the laws of the Cayman Islands (“Platinum”), pursuant to that certain Agreement and Plan of Share Exchange, dated January 14, 2021 (the “Exchange Agreement”), by and among us, Platinum, Yubo Beijing, and certain selling stockholders named therein.

In accordance with the terms of the Exchange Agreement, on the Closing Date, we issued a total of 117,000,000 shares of our Class A common stock to the then stockholders of Platinum (the “Selling Stockholders”), in exchange for 100% of the issued and outstanding capital stock of Platinum (the “Exchange Transaction”). As a result of the Exchange Transaction, the Selling Stockholders acquired more than 99% of our issued and outstanding capital stock, Platinum became our wholly-owned subsidiary, and we acquired the business and operations of Platinum and Yubo Beijing.

Platinum was incorporated on April 7, 2020 under the laws of the Cayman Islands as a holding company.

| 1 |

| Table of Contents |

Immediately prior to the Exchange Transaction, we had 117,875,323 shares of Class A common stock and 4,447 shares of Class B common stock issued and outstanding. Immediately after the Exchange Transaction and the surrender and cancellation of 116,697,438 shares of Class A common stock previously held by Lina Liu, and as of the date hereof, our authorized capital stock consists of 120,000,000 shares of common stock, par value $.001 per share, of which 118,177,885 Class A common plus 4,447 Class B common) are issued and outstanding, and 5,000,000 shares of Preferred Stock, $0.001 par value, none of which shares are issued or outstanding. Each share of Class A common stock is entitled to one vote with respect to all matters to be acted on by the stockholders; and each share of Class B common stock is entitled to five votes per share, and is convertible into one share of Class A common stock.

The VIE and China Operations

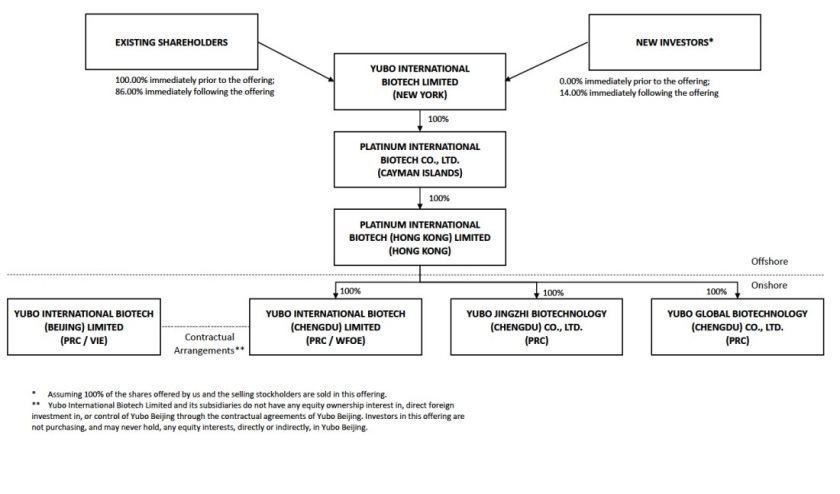

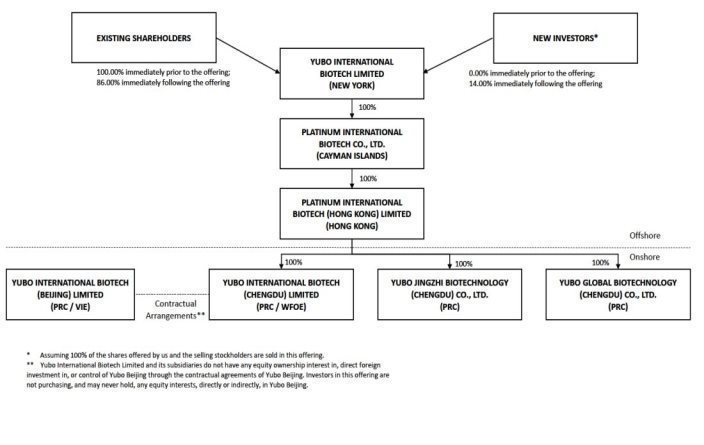

As a result of the Exchange Transaction, we became a U.S. holding company primarily operating through our wholly owned subsidiary, Platinum. Platinum is not a Chinese operating company but a Cayman Islands holding company which in turn operates in China through (i) its Hong Kong and PRC subsidiaries, including Yubo Global Biotechnology (Chengdu) Co., Ltd. (“Yubo Global”) and Yubo Chengdu, each a company organized under the laws of the PRC, in each of which we hold equity ownership interests, and (ii) Yubo Beijing, the VIE and the Chinese operating company that conducts the day-to-day business operations of our Company in China through contractual relationships with us and our subsidiaries as described in this prospectus, including Yubo Jingzhi Biotechnology (Chengdu) Co. Ltd., a company organized under the laws of the PRC (“Yubo Jingzhi”) and a wholly owned subsidiary of Yubo Beijing. We do not own any equity interest in Yubo Beijing or Yubo Jingzhi.

On September 11, 2020, the WFOE entered into a series of contractual arrangements with Yubo Beijing and its shareholders, allowing us, for accounting purposes only, to consolidate the financial results of Yubo Beijing in our consolidated financial statements. These agreements include:

| · | Exclusive Consulting Services Agreement. Pursuant to the Exclusive Consulting Services Agreement, the WFOE agrees to provide, and Yubo Beijing agrees to accept, exclusive management services provided by the WFOE. The Exclusive Consulting Services Agreement was amended in March 2022 for the sole purpose of clarifying the fee structure under such agreement. Pursuant to the amendment, Yubo Beijing agreed to compensate the WFOE, Yubo Chengdu, for its services on an annual basis. Under the amendment, the WFOE is entitled to receive 90% of the after-tax profit from Yubo Beijing annually following the closing of Yubo Beijing’s annual accounts. In light of such arrangement, the WFOE is considered a primary beneficiary of benefits that are otherwise potentially significant to Yubo Beijing. The amendment did not change the contractual relationships that we have with Yubo Beijing. Since Yubo Beijing has not generated any after-tax profit to date, Yubo Beijing has not paid any fee to the WFOE to date. |

| · | Exclusive Option Agreement. Pursuant the Exclusive Option Agreement, the shareholders of Yubo Beijing granted the WFOE an irrevocable and exclusive purchase option to acquire Yubo Beijing’s equity and/or assets at a nominal consideration. The WFOE may exercise the purchase option at any time. |

| · | Equity Pledge Agreement. Pursuant to the Equity Pledge Agreement, the shareholders of Yubo Beijing pledged all of their equity interests in Yubo Beijing, including the proceeds thereof, to guarantee all of the WFOE’s rights and benefits under the Exclusive Consulting Services Agreement and the Exclusive Option Agreement. |

Neither we nor the investors of our Class A common stock have any equity ownership interest in, direct foreign investment in, or control through such contractual agreements of the VIE. Investors in our Class A common stock are not purchasing, and may never hold, any equity interests, directly or indirectly, in Yubo Beijing through participation in this offering. As a result of our contractual relationships with Yubo Beijing, we consolidate Yubo Beijing’s financial results in our consolidated financial statements and are the primary beneficiary of Yubo Beijing for accounting purposes only. Our corporate structure involving the VIE provides investors with contractual exposure to foreign investment in China-based companies where PRC laws prohibit direct foreign investment in Chinese operating companies in certain industries, such as Yubo Beijing. This structure involves unique risks to investors. For example, management through these contractual arrangements may be less effective than direct ownership, and we could face heightened risks and costs in enforcing these contractual arrangements, because there are substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations, and rules relating to these contractual arrangements. Our contractual arrangements with Yubo Beijing have not been tested in a court of law. If the PRC government finds such agreements non-compliant with relevant PRC laws, regulations, and rules, or if these laws, regulations, and rules or the interpretation thereof change in the future, we could be subject to severe penalties or be forced to relinquish our interests in Yubo Beijing or forfeit our rights under the contractual arrangements. Further, the Chinese regulatory authorities could disallow our contractual arrangements with Yubo Beijing, which would likely result in a material adverse change in our operations, and, given the resulting inability to consolidate Yubo Beijing’s financial results in our consolidated financial statements, in the value of our Class A common stock, which could significantly decline or become worthless. See “Risk Factors—Risks Related to Our Corporate Structure.” See the unaudited condensed consolidating balance sheets for our Company, our subsidiaries, and Yubo Beijing as of December 31, 2021 and 2020, and the unaudited condensed consolidating statements of operations for such entities for the years ended December 31, 2021 and 2020, set forth on Exhibit 99.2 to the registration statement to which this prospectus forms a part. There were no intercompany revenues or expenses and no intercompany payables or receivables between Yubo Beijing and the WOFE under our contractual arrangements with Yubo Beijing for the years ended December 31, 2021 and 2020 and the three months ended March 31, 2022.

| 2 |

| Table of Contents |

The following diagram illustrates our corporate structure, including the VIE, Yubo Beijing, as of the date of this prospectus:

Common Stock

Our authorized common stock is divided into Class A common stock and Class B common stock. Holders of Class A common stock are entitled to one vote per share, while holders of Class B common stock are entitled to five votes per share. Each share of Class B is convertible into one share of Class A common stock upon notice of the holder, while Class A common stock is not convertible into Class B common stock under any circumstances. As of the date of this prospectus, we have authorized (i) 1,000,000,000 shares of Class A common stock, of which 118,177,885 shares were issued and outstanding, and (ii) 3,750,000 shares of Class B common stock, of which 4,447 shares were issued and outstanding. See “Description of Securities—Common Stock.”

| 3 |

| Table of Contents |

Summary Risk Factors

Investing in our Class A common stock involves significant risks. You should carefully consider all of the information in this prospectus before making an investment in our common stock. Below please find a summary of the principal risks we face, organized under relevant headings. These risks are discussed more fully in the section titled “Risk Factors” beginning on page 13 of this prospectus.

Risks Related to our Corporate Structure

Our corporate structure is subject to risks relating to our contractual arrangements with Yubo Beijing and its shareholders. If the PRC government finds these contractual arrangements non-compliant with the restrictions on direct foreign investment in the relevant industries, or if the relevant PRC laws, regulations, and rules or the interpretation thereof change in the future, we could be subject to severe penalties or be forced to relinquish our interests in Yubo Beijing or forfeit our rights under the contractual arrangements. We and investors in our Class A common stock face uncertainty about potential future actions by the PRC government, which could affect the enforceability of our contractual arrangements with Yubo Beijing and, consequently, significantly affect our financial condition and results of operations. If we are unable to consolidate the financial results of Yubo Beijing in our financial statements, our Class A common stock may decline in value or become worthless. See “Risk Factors—Risks Related to Our Corporate Structure” beginning on page 13 of this prospectus.

| ·

| There are substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations, and rules relating to the agreements that establish the VIE structure for our operations in China, including potential future actions by the PRC government, which could affect the enforceability of our contractual arrangements with Yubo Beijing and, consequently, significantly affect our financial condition and results of operations. If the PRC government finds that the contractual arrangements that establish the structure for operating our business in China do not comply with PRC laws and regulations, or if these regulations or their interpretations change in the future, we could be subjected to severe consequences, including the nullification of such agreements and the relinquishment of our interest in the VIE. See page 13 of this prospectus. |

| · | We currently conduct our business primarily through contractual arrangements with the PRC operating entity, and our management of the day-to-day operations of such PRC entity pursuant to contracts, to comply with Chinese law, may not be as effective as conducting business through direct equity ownership of such PRC entity due to uncertainties with respect to the PRC legal system which could materially and adversely affect our results of operations. See page 15 of this prospectus. |

| · | Our contractual arrangements with Yubo Beijing and its shareholders will not provide any direct ownership of or control over Yubo Beijing. See page 16 of this prospectus. |

| · | Transactions among our affiliates are subject to scrutiny by the PRC tax authorities and a finding that we or any of our consolidated entities owe additional taxes could have a material adverse impact on our net income and the value of an investment in our common stock. See page 16 of this prospectus. |

Risks related to Doing Business in China

We and Yubo Beijing face various legal and operational risks and uncertainties relating to doing business in China. We operate our business in China through Yubo Beijing, which is subject to complex and evolving PRC laws and regulations. Therefore, investors of our Class A common stock face potential uncertainty from the PRC government. Changes in China’s economic, political or social conditions or government policies could materially adversely affect Yubo Beijing’s business and results of operations. For example, Yubo Beijing faces risks relating to regulatory approvals on the business operations and oversight on cybersecurity and data privacy. These risks could result in a material change in Yubo Beijing’s operations and/or the value of our Class A common stock or could cause the value of such securities to significantly decline or be worthless. See “Risk Factors—Risks Related to Doing Business in China” beginning on page 16 of this prospectus.

| 4 |

| Table of Contents |

| · | The PRC government has significant authority to exert influence on the China operations of an offshore holding company, such as us. Therefore, investors in our Class A common stock and Yubo Beijing’s business face potential uncertainty from the PRC government’s policy. Changes in China’s economic, political or social conditions, or government policies could materially and adversely affect our or Yubo Beijing’s business, financial condition, and results of operations. See page 16 of this prospectus. |

| · | Yubo Beijing is subject to extensive and evolving legal development, non-compliance with which, or changes in which, may materially and adversely affect its business and prospects, and may result in a material change in its operations and/or the value of our Class A common stock or could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless. See page 17 of this prospectus. |

| · | Yubo Beijing’s business might be subject to various evolving PRC laws and regulations regarding data privacy and security. Failure of data privacy and security compliance could subject Yubo Beijing to penalties, damage its reputation and brand and harm its business and results of operations. See page 18 of this prospectus. |

| · | The medical industry in China is highly regulated and such regulations are subject to change which may affect approval and commercialization of Yubo Beijing’s products and services. See page 19 of this prospectus. |

| · | You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions in China against us or our management named in this prospectus based on foreign laws. See page 19 of this prospectus. |

| · | Although our audit report is prepared by U.S. auditors who are currently inspected by the PCAOB, there is no guarantee that future audit reports will be prepared by auditors that are completely inspected by the PCAOB and, as such, future investors may be deprived of such inspections, which could result in limitations or restrictions to our access of the U.S. capital markets. Furthermore, trading in our securities may be prohibited under the Holding Foreign Companies Accountable Act or the Accelerating Holding Foreign Companies Accountable Act if the SEC subsequently determines our audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely or the SEC identifies us as a Commission-Identified Issuer, and as a result, U.S. national securities exchanges, such as the Nasdaq, may decide to delist our securities. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if passed by the U.S. House of Representatives and signed into law, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years, instead of three as currently provided by the HFCAA. See page 21 of this prospectus. |

| · | The approval of the CSRC or other PRC government authorities may be required in connection with this offering under PRC law, and, if so required, we cannot predict whether or for how long Yubo Beijing will be able to obtain such approval. Any failure to obtain or delay in obtaining such approval for this offering would subject Yubo Beijing to sanctions imposed by the CSRC or other PRC government authorities. See page 27 of this prospectus. We did not retain any PRC legal counsel for purposes of this offering, and as such, we did not rely on the advice of PRC legal counsel with respect to the permission requirements from the CSRC or other PRC government authorities. |

| 5 |

| Table of Contents |

Risks Related to Shares of our Common Stock and this Offering (beginning on page 29 of this prospectus)

| · | You will experience immediate and substantial dilution in the book value per share of the common stock you purchase. See page 29 of this prospectus. |

| · | Shares of our common stock that have not been registered under the Securities Act of 1933, as amended (the “Securities Act”), regardless of whether such shares are restricted or unrestricted, are subject to resale restrictions imposed by Rule 144, including those set forth in Rule 144(i) which apply to a “shell company.” See page 29 of this prospectus. |

| · | The relative lack of public company experience of our management team may put us at a competitive disadvantage. See page 30 of this prospectus. |

| · | Our common stock is not listed on any stock exchange and there is a limited market for shares of our common stock. Even if a market for our common stock develops, our common stock could be subject to wide fluctuations. See page 30 of this prospectus. |

| · | Because we became public by means of a “reverse merger,” we may not be able to attract the attention of major brokerage firm or investors in general. See page 31 of this prospectus. |

| · | Our common stock may be subject to penny stock rules, which may make it more difficult for our stockholders to sell their common stock. See page 31 of this prospectus. |

| · | FINRA sales practice requirements may also limit a stockholder’s ability to buy and sell our stock. See page 31 of this prospectus. |

| · | We do not anticipate paying any cash dividends. See page 31 of this prospectus. |

| · | We may need additional capital, and the sale of additional shares or other equity securities, including our Class B common stock, could result in additional dilution to our stockholders. See page 32 of this prospectus. |

| · | Our principal stockholders and management own a significant percentage of our stock and will be able to exert significant control over matters subject to stockholder approval. See page 32 of this prospectus. |

| · | We have a substantial number of authorized common shares available for future issuance that could cause dilution of our stockholders’ interest and adversely impact the rights of holders of our common stock. See page 32 of this prospectus. |

Risks Related to Yubo Beijing’s Business and Industry (beginning on page 33 of this prospectus)

| · | The commercial success of Yubo Beijing’s products depends upon the degree of their market acceptance among the medical community. If Yubo Beijing’s products do not attain market acceptance among the medical community, its operations and profitability would be adversely affected. See page 33 of this prospectus. |

| · | We have a history of losses and may continue to incur losses in the future, which raises substantial doubt about our ability to continue as a going concern. See page 33 of this prospectus. |

| · | Yubo Beijing’s proprietary, next-generation stem cell derived technologies, approach for stem cell storage facilities and manufacturing platform for its stem cell-based product candidates, represent emerging approaches to medical treatments that face significant challenges and hurdles. See page 34 of this prospectus. |

| · | Yubo Beijing may not be able to successfully create its own manufacturing infrastructure and stem cell storage facilities for supply and maintenance of its requirements of programmed stem cell products for use in clinical trials and for commercial sale. See page 34 of this prospectus. |

| · | Yubo Beijing may not be able to timely identify or otherwise effectively respond to changing customer preferences, and Yubo Beijing may fail to optimize its product offering and inventory position. See page 35 of this prospectus. |

| · | Yubo Beijing faces significant competition, and if Yubo Beijing does not compete successfully against existing and new competitors, its revenue and profitability would be materially and adversely affected. See page 35 of this prospectus. |

| · | Yubo Beijing relies on third-party manufacturers to supply its products. See page 36 of this prospectus. |

| · | Yubo Beijing depends on a limited number of customers and the loss of one or more of these customers could have a material adverse effect on its business, financial condition and results of operations. See page 36 of this prospectus. Yubo Beijing’s certificates, permits, and licenses related to its business are subject to governmental control and renewal and failure to obtain renewal will cause all or part of Yubo Beijing’s operations to be terminated. See page 37 of this prospectus. |

| · | If Yubo Beijing is unable to protect its intellectual property from infringement, its business and prospects may be harmed. See page 37 of this prospectus. |

| 6 |

| Table of Contents |

Regulatory Developments

Implication of the Holding Foreign Companies Accountable Act

The Holding Foreign Companies Accountable Act, or the HFCA Act, was enacted on December 18, 2020. The HFCA Act states that if the SEC determines that an issuer’s audit reports issued by a registered public accounting firm have not been subject to inspection by the PCAOB for three consecutive years beginning in 2021, the SEC shall prohibit such issuer’s securities from being traded on a national securities exchange or in the over-the-counter trading market in the United States. As of the date of this prospectus, our auditor, Michael T. Studer CPA P.C., an independent registered public accounting firm headquartered in the United States, is currently subject to PCAOB inspections and has been inspected by the PCAOB on a regular basis, and our auditor was not included in the determinations made by the PCAOB, on December 16, 2021. However, in the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor because of a position taken by an authority in a foreign jurisdiction, then such lack of inspection could cause trading in our securities to be delisted from the stock exchange in the U.S pursuant to the HFCA Act. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if passed by the U.S. House of Representatives and signed into law, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three. See “Risk Factors—Although our audit report is prepared by U.S. auditors who are currently inspected by the PCAOB, there is no guarantee that future audit reports will be prepared by auditors that are completely inspected by the PCAOB and, as such, future investors may be deprived of such inspections, which could result in limitations or restrictions to our access of the U.S. capital markets. Furthermore, trading in our securities may be prohibited under the Holding Foreign Companies Accountable Act or the Accelerating Holding Foreign Companies Accountable Act if the SEC subsequently determines our audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely or the SEC identifies us as a Commission-Identified Issuer (as defined in the final rules), and as a result, U.S. national securities exchanges, such as the Nasdaq, may decide to delist our securities. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if passed by the U.S. House of Representatives and signed into law, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years, instead of three as currently provided by the HFCAA.”

Cybersecurity Review Measures

On December 28, 2021, the CAC published the revised Cybersecurity Review Measures (“CRM”), which further restates and expands the applicable scope of the cybersecurity review. The revised CRM took effect on February 15, 2022. Pursuant to the revised CRM, if a network platform operator holding personal information of over one million users seeks for “foreign” listing, it must apply for the cybersecurity review. In addition, operators of critical information infrastructure purchasing network products and services are also obligated to apply for the cybersecurity review for such purchasing activities. Although the CRM provides no further explanation on the extent of “network platform operator” and “foreign” listing, we do not believe we are obligated to apply for a cybersecurity review pursuant to the revised CRM, considering that (i) we are not in possession of or otherwise holding personal information of over one million users and it is also very unlikely that we will reach such threshold in the near future; (ii) as of the date of this this prospectus, we have not received any notice or determination from applicable PRC governmental authorities identifying it as a critical information infrastructure operator or requiring us to go through cybersecurity review or similar government reviews. In light of the foregoing, which are consistent with the local market practice, we did not retain any PRC legal counsel for purposes of this offering, and as such, we did not rely on the advice of PRC legal counsel with respect to such matters. Our understanding with regards to the permission requirements under the revised CRM is based on a risk-based analysis of the currently effective PRC laws, regulations and rules, as well as the local market practice as of the date of this prospectus. We cannot assure you that our understanding is correct, or consistent with the opinion of PRC legal counsel if one were retained to opine on such permission requirements.

That being said, the revised CRM empowers the cybersecurity review office to initiate cybersecurity review when they believe any particular data processing activities “affect or may affect national security.” In addition, on 14 November 2021, the CAC promulgated the Regulations on the Administration of Cyber Data Security (Draft for Comments) (the “Draft CAC Regulations”), and according to the Draft CAC Regulations, any data processors shall, in accordance with relevant state provisions, apply for a cybersecurity review when carrying out, among other things, “other data processing activities that affect or may affect national security.” However, neither the revised CRM nor the Draft CAC Regulations provides for any further explanation or interpretation over what constitutes activities that “affect or may affect national security.” Therefore, if any competent government authorities deem that Yubo Beijing’s data processing activities may affect national security or if the competent government authorities, including the CAC, adopt new laws, regulations or rules related to the revised CRM, we may be subject to cybersecurity review, and in that scenario, we may be required to suspend our operations or experience other disruptions to our operations. Cybersecurity review could also result in negative publicity with respect to our Company and diversion of our managerial and financial resources, which could materially and adversely affect our business, financial condition, and results of operations. Failure to pass such cybersecurity review and/or to comply with the data privacy and data security requirements raised during a cybersecurity review could subject Yubo Beijing to penalties, damage its reputation and brand, and harm its business and results of operations. See “Risk Factors—Yubo Beijing’s business might be subject to various evolving PRC laws and regulations regarding cybersecurity, data privacy and data security. Failure of cybersecurity, data privacy and data security compliance could subject Yubo Beijing to penalties, damage its reputation and brand and harm its business and results of operations.”

| 7 |

| Table of Contents |

On August 20, 2021, the Standing Committee of the National People’s Congress promulgated the PRC Personal Information Protection Law, which took effect in November 2021. The Personal Information Protection Law provides that any entity involving processing of personal information (“Personal Information Processer”) shall take various measures to prevent the disclosure, modification or losing of the personal information processed by such entity, including, but not limited to, formulating a related internal management system and standard of operation, conducting classified management of personal information, taking safety technology measures to encrypt and de-identify the processed personal information, providing regular safety training and education for staff and formulating a personal information safety emergency accident plan. The Personal Information Protection Law further provides that a Personal Information Processer shall conduct a prior evaluation of the impact of personal information protection before the occurrence of various situations, including, but not limited to, processing of sensitive personal information (personal information that, once leaked or illegally used, may lead to discrimination against an individual or serious harm to an individual’s personal or property safety, including information on an individual’s ethnicity, religious beliefs, personal biological characteristics, medical health, financial accounts, personal whereabouts), using personal information to make automated decisions and providing personal information to any overseas entity. Yubo Beijing’s business involves the processing of personal information of customers using Yubo Beijing’s healthcare products and receiving Yubo Beijing’s services, which may be deemed as sensitive personal information. If Yubo Beijing does not take measures to review and improve its mechanisms in protecting personal information after the new Personal Information Protection Law takes effect, failure of personal information protection compliance could subject Yubo Beijing to penalties, damage its reputation and brand and harm its business and results of operations. See “Risk Factors—Yubo Beijing’s business might be subject to various evolving PRC laws and regulations regarding data privacy and security. Failure of data privacy and security compliance could subject Yubo Beijing to penalties, damage its reputation and brand and harm its business and results of operations.”

Potential CSRC Approval Required for This Offering

On December 24, 2021, the CSRC published the Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Enterprises (Draft for Comments) and the Administrative Measures for the Filing of Overseas Securities Offering and Listing by Domestic Enterprises (Draft for Comments) (collectively, “CSRC Draft Rules”). Pursuant to the CSRC Draft Rules, for any “indirect offering and listing” of Chinese enterprises, the issuer shall designate a Chinese operating entity to complete the filing with the CSRC, and the “indirect offering and listing” refers to such securities offering and listing in an overseas stock exchanges made in the name of an offshore/non-Chinese issuer and based on the underlying equity, assets, earnings, or other similar interest of Chinese operating entities. The CSRC Draft Rules proposes two criteria, the satisfaction of which will give rise to the CSRC’s determination of “indirect overseas offering and listing”: (i) the financial criteria: the total assets, net assets, revenues or profits of the issuer’s Chinese operation entities in the immediately preceding financial year account for more than 50% of the issuer’s audited and consolidated financial result in the same period; (ii) the management and operation criteria: a majority of the issuer’s senior management in charge of business operation are Chinese citizens or having Chinese residence, the issuer’s primary site of business is located, or its principal business activities occur in China.

| 8 |

| Table of Contents |

For an initial public offering and listing, the issuer shall, within three workings days after the overseas submission of the application document for initial public offering and listing, provide the CSRC with filing materials, including but not limited to (1) a filing report and relevant commitments; (2) a regulatory opinion, filing, or approval and other documents issued by the competent authorities of the industry (if applicable); (3) an opinion of security assessment and review issued by relevant departments (if applicable); (4) a Chinese legal opinion; and (5) a prospectus. For each offering of foreign-listed securities after an initial overseas listing, the issuer shall provide the CSRC with filing materials, including but not limited to (a) a filing report and relevant commitments; and (b) a Chinese legal opinion. If the filing materials are complete and requirements are fulfilled, the CSRC will issue the letter accepting the filing within 20 working days and publish the information for filing on website. In case of any of the following significant events after the initial overseas listing, the issuer shall report the details to the CSRC within 3 working days from the occurrence of relevant events: (x) changes in control; (y) investigations, penalties and other measures taken by overseas securities administrative authorities or relevant competent authorities; (z) voluntary termination of the listing or mandatory termination of the listing. Pursuant to the CSRC Draft Rules, an overseas offering and listing of China-based companies will be prohibited in a certain number of specified circumstances, including, inter alia, as determined by competent authorities, the overseas offering and listing will threat or jeopardize national security. If the CSRC suspects of any of such circumstances during their review of the filing materials, the CSRC may consult with other government authorities which consultation may prolong the review process, and if any of such circumstances are found to exist, the issuer may be ordered to suspend or cancel the securities offering.

On December 27, 2021, the NDRC and MOFCOM issued the Special Administrative Measures for Access of Foreign Investment (Negative List) (2021 Edition) (the “Negative List 2021”), which came into effect on January 1, 2022. According to Negative List 2021, PRC entities which engage in any prohibited sectors by the Negative List 2021 for access to foreign investment must be approved by the competent PRC authorities when they seek listing offshore, and foreign investors are not permitted to participate in operation and management. In addition, the shareholding ratio must be in compliance with PRC laws.

We believe this offering is not subject to the approval of the CSRC or other equivalent PRC government authorities, as (i) both the CSRC rules are in draft form and have not come into effect to date; and (ii) no provisions under the currently effective PRC laws, regulations, and rules explicitly require an indirect listing through contractual arrangements such as ours to obtain approvals from PRC authorities. In light of the foregoing, which are consistent with the local market practice, we did not retain any PRC legal counsel for purposes of this offering, and as such, we did not rely on the advice of PRC legal counsel with respect to such matters. Our understanding with regards to the permission requirements from the CSRC or other PRC governmental agency is based on a risk-based analysis of the currently effective PRC laws, regulations and rules, as well as the local market practice as of the date of this prospectus. We cannot assure you that our understanding is correct, or consistent with the opinion of PRC legal counsel if one were retained to opine on such permission requirements.

According to the information released by the CSRC officials upon the publication of the CSRC rules, the CSRC will adhere to the principle of non-retroactive application of the law. Therefore, new initial public offerings and follow-on financings by existing overseas-listed Chinese companies will be required to go through the filing process, and existing overseas-listed companies will be given a transition period in which to comply. This means that, if we complete this offering before the effectiveness of such CSRC rules, we could be subject to the filing requirements with the CSRC in connection with any future offerings, and/or be granted a transition period to complete the filing procedure with respect to this offering as an existing overseas-listed company. We and our investors would be adversely affected if (i) we or our subsidiaries, including the Yubo Beijing were required to receive or maintain such permissions or approvals from the CSRC, CAC, or other PRC regulatory agencies and did not do so, (ii) if we inadvertently concluded that such approvals are not required, or (iii) if applicable laws, regulations, or interpretations change and we become required to obtain approval in the future. See “Risk Factors—The approval of the CSRC or other PRC government authorities may be required in connection with this offering under PRC law, and, if so required, we cannot predict whether or for how long Yubo Beijing will be able to obtain such approval. Any failure to obtain or delay in obtaining such approval for this offering would subject Yubo Beijing to sanctions imposed by the CSRC or other PRC government authorities.”

| 9 |

| Table of Contents |

Other

To operate its general business activities in China, Yubo Beijing is required to obtain the following licenses and approvals. Yubo Beijing has obtained such licenses and approvals, and, to date, no application for any such licenses and approvals has been denied.

Licenses and Approvals |

| PRC Regulatory Authority |

|

|

|

Food Operation License Permit |

| Xicheng District Market Supervision and Administration Office of Beijing Municipality |

|

|

|

Medical License Distribution Enterprise Filing Certificate |

| Xicheng District Market Supervision and Administration Office of Beijing Municipality |

Corporate Information

Our principal executive offices are located at Room 105, Building 5, 31 Xishiku Avenue, Xicheng District, Beijing, PRC. Our telephone number is +86 (010) 6615-5141. Our website address is http://www.yubogroup.com/. The information contained in, or that can be accessed through, our website is not incorporated by reference into, and is not a part of, this prospectus. You should not consider any information on our website to be part of this prospectus or in decides whether to purchase our securities. We have included our website address in this prospectus solely for informational purposes.

Dividends and Other Distributions

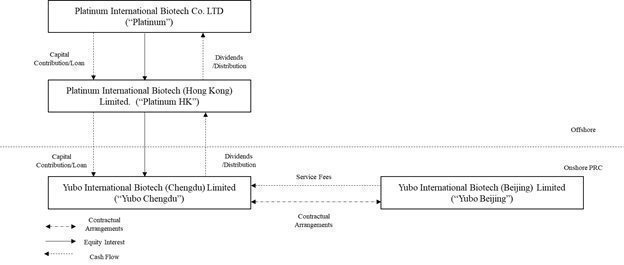

We are a holding company, and we may rely on dividends and other distributions on equity paid by our subsidiaries for our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our shareholders or holders of our Class A common stock or to service any debt we may incur. The following diagram illustrates the typical cash flow among our main subsidiaries, the WFOE and Yubo Beijing, the VIE.

| 10 |

| Table of Contents |

As of the date of this prospectus, except as disclosed below, no transfers of cash or other types of assets, dividends, or distributions have been made between our New York holding company, any of our subsidiaries, and Yubo Beijing. As of the date of this prospectus, neither we nor any of our subsidiaries have ever paid dividends or made distributions to U.S. investors. There has been no capital flow from the WFOE, Yubo Chengdu, to the VIE, Yubo Beijing. On May 15, 2021, Yubo Beijing received $500,000 from Yubo Global in the form of a loan to fund Yubo Beijing’s operations. On September 15, 2021, Yubo Global received a loan of $1,538 from Yubo Beijing to supplement Yubo Global’s general working capital. See Note 10: Due to Related Parties to our audited consolidated financial statements for the years ended December 31, 2021 and 2020 and our unaudited consolidated financial statements for the three months ended March 31, 2022 and 2021 included elsewhere in this prospectus. These loans are non-interest bearing and payable on demand. While we have not to date adopted a formal cash management policy in writing, we carefully monitor the cash positions of and the fund flows between our New York holding company and each of our subsidiaries, including Yubo Chengdu, and Yubo Beijing. All such fund flows are reviewed regularly by our Chief Executive Officer and Chief Financial Officer and are subject to approval by our board.

In the future, cash proceeds raised from our financing activities may be transferred by us to our Chinese subsidiaries via capital contribution or shareholder loans, as the case may be. We intend to use the net proceeds from this offering to expand Yubo Beijing’s operations in the PRC and fund the operations of its stem cell storage facilities in the form of capital contributions or loans. See “Use of Proceeds.” As an early-stage company, we do not intend to distribute earnings or settle amount owed under the VIE agreements, if any, in the near future.

According to the Foreign Investment Law of the People’s Republic of China and its implementing rules, which jointly established the legal framework for the administration of foreign-invested companies, a foreign investor may, in accordance with other applicable laws, freely transfer into or out of China its contributions, profits, capital earnings, income from asset disposal, intellectual property rights, royalties acquired, compensation or indemnity legally obtained, and income from liquidation, made or derived within the territory of China in RMB or any foreign currency, and any entity or individual shall not illegally restrict such transfer in terms of the currency, amount and frequency. According to the Company Law of the People’s Republic of China and other Chinese laws and regulations, our Chinese subsidiaries may pay dividends only out of their respective accumulated profits as determined in accordance with Chinese accounting standards and regulations. In addition, each of our Chinese subsidiaries, namely Yubo Chengdu and Yubo Global, and Yubo Beijing and its wholly owned subsidiary, Yubo Jingzhi, is required to set aside at least 10% of its accumulated after-tax profits, if any, each year to fund a certain statutory reserve fund, until the aggregate amount of such fund reaches 50% of its registered capital. Where the statutory reserve fund is insufficient to cover any loss the Chinese subsidiary incurred in the previous financial year, its current financial year’s accumulated after-tax profits shall first be used to cover the loss before any statutory reserve fund is drawn therefrom. Such statutory reserve funds and the accumulated after-tax profits that are used for covering the loss cannot be distributed to us as dividends. At their discretion, our Chinese subsidiaries may allocate a portion of their after-tax profits based on Chinese accounting standards to a discretionary reserve fund.

Currently, the RMB cannot be freely converted into any foreign currency. The PRC government imposes controls on the convertibility of RMB into foreign currencies and, in certain cases, the remittance of currency out of China. Our income is received in RMB and shortages in foreign currencies may restrict our ability to pay dividends or other payments, or otherwise satisfy our foreign currency denominated obligations, if any. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade-related transactions, can be made in foreign currencies without prior approval from the PRC State Administration of Foreign Exchange, or SAFE, by complying with certain procedural requirements. However, for most capital account items, approval from or registration with appropriate government authorities is required where RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of bank loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay dividends in foreign currencies to our shareholders, including holders of the Class A common stock. See “Risk Factors—Restrictions on foreign exchange and the ability to transfer cash between entities, across borders and to U.S. investors may affect the value of your investment.”

Our cash dividends, if any, will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax. See “Risk Factors—If we are classified as a “resident enterprise” of China under the PRC Enterprise Income Tax Law, we and our non-PRC shareholders could be subject to unfavorable tax consequences, and our business, financial condition and results of operations could be materially and adversely affected.”

| 11 |

| Table of Contents |

INCORPORATION BY REFERENCE

The SEC allows us to “incorporate by reference” into this prospectus the information in other documents that we file with it, including at a subsequent date. The information incorporated by reference is considered to be a part of this prospectus, and information in documents that we file later with the SEC will automatically update and supersede information contained in documents filed earlier with the SEC or contained in this prospectus. In addition to documents referenced as incorporated by reference elsewhere in this prospectus, we incorporate by reference herein all documents subsequently filed by us with the SEC pursuant to Sections 13(a), 13(c), 14 or 15(d) of the Exchange Act, prior to the termination of the offering; provided, however, that we are not incorporating, in each case, any documents or information deemed to have been furnished and not filed in accordance with SEC rules.

| 12 |

| Table of Contents |

RISK FACTORS

Any investment in our securities involves a high degree of risk. Investors should carefully consider the risks described below and all of the information contained in this prospectus before deciding whether to purchase our securities. Our business, financial condition or results of operations could be materially adversely affected by these risks if any of them actually occur. Our common stock is quoted on the OTC Marketplace under the symbol “YBGJ.” This market is extremely limited and the prices quoted are not a reliable indication of the value of our common stock. As of the date of this prospectus, there has been very limited trading of shares of our common stock. If and when our common stock is traded, the trading price could decline due to any of these risks, and an investor may lose all or part of his or her investment. Some of these factors have affected our financial condition and operating results in the past or are currently affecting us. This prospectus also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks described below and elsewhere in this prospectus.

Risks Related to our Corporate Structure

There are substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations, and rules relating to the agreements that establish the VIE structure for our operations in China, including potential future actions by the PRC government, which could affect the enforceability of our contractual arrangements with Yubo Beijing and, consequently, significantly affect our financial condition and results of operations. If the PRC government finds that the contractual arrangements that establish the structure for operating our business in China do not comply with PRC laws and regulations, or if these regulations or their interpretations change in the future, we could be subjected to severe consequences, including the nullification of such agreements and the relinquishment of our interest in the VIE.

Current PRC laws and regulations impose certain restrictions or prohibitions on foreign ownership of companies that engage in medical institutions which our stem cell bank relates to, and in the development and application of technologies for diagnosis and treatment of human stem cells and genes, which our stem cell bank and endometrial stem cell bank business relates to. Pursuant to the Special Administrative Measures (Negative List) issued by the NDRC and MOFCOM on December 27, 2021, which came into force on January 1, 2022, foreign investment are allowed in PRC medical institutions only through joint venture entities, and the foreign shareholding in these entities is limited to 70.0%, which percentage was stipulated in the Interim Administrative Measures on Sino-Foreign Equity Medical Institutions and Sino-Foreign Cooperative Medical Institutions, or the JV Interim Measures. Additionally, certain industries are specifically prohibited for foreign investment, including the development and application of technologies for diagnosis and treatment of human stem cells and genes.

Considering the foreign investment restrictions that may be applicable to our business, we conduct our stem cell bank and endometrial stem cell bank business in China through the VIE. The VIE structure through contractual arrangements has been adopted by many PRC-based companies, including us, such that if our businesses are determined to be subject to the foreign investment restrictions, we can obtain necessary license, for example, the Practice License of Medical Institutions, in the industry currently subject to foreign investment restrictions in China.

On March 15, 2019, the Foreign Investment Law was formally passed by the thirteenth National People’s Congress and it became effective on January 1, 2020. The Foreign Investment Law replaced the Law on Sino-Foreign Equity Joint Ventures, the Law on Sino-Foreign Cooperative Joint Ventures and the Law on Foreign-Capital Enterprises and became the legal foundation for foreign investment in the PRC. The Foreign Investment Law stipulates certain forms of foreign investment and defines enterprises incorporated within PRC with complete or partial foreign investment as foreign-invested enterprises or “FIEs.” However, the Foreign Investment Law does not explicitly stipulate contractual arrangements such as those we rely on as a form of foreign investment.

The 2019 PRC Foreign Investment Law further specifies that foreign investments shall be conducted in line with the "negative list" to be issued by or approved to be issued by the State Council. This means that an FIE would not be allowed to make investments in prohibited industries in the "negative list," while the FIE must satisfy certain conditions stipulated in the "negative list" for investment in restricted industries. As pursuant to the negative list issued by the NDRC and MOFCOM taking effect on January 1, 2022, medical services is a restricted industry and foreign investment are allowed in PRC medical institutions only through joint venture entities, i.e., an FIE in which foreign ownership is limited to 70.0%. Additionally, certain industries are specifically prohibited for foreign investment, including the development and application of technologies for diagnosis and treatment of human stem cells and genes, which means, pursuant to the Foreign Investment Law, FIEs are prohibited from practicing such businesses in China.

| 13 |

| Table of Contents |

Considering the above, Yubo International Biotech Limited, Platinum and Platinum HK are considered as foreign investors under the 2019 PRC Foreign Investment Law, Yubo WOFE is deemed as an FIE. Accordingly, none of such entities are eligible to provide such restricted services related to our businesses, such as medical services. As a result, we will conduct such business activities through the VIE and Chinese operating company, Yubo Beijing. Since Yubo Beijing is not an FIE, Yubo Beijing will be able to apply and hold license as medical institution as other PRC companies and provide medical services which are otherwise restricted to FIEs.

Notwithstanding the above, the Foreign Investment Law stipulates that foreign investment includes “foreign investors investing through any other methods under laws, administrative regulations or provisions prescribed by the State Council.” Future laws, administrative regulations or provisions prescribed by the State Council may possibly regard contractual arrangements as a form of foreign investment. If this happens, it is uncertain whether our contractual arrangements with Yubo Beijing, its subsidiaries and shareholders would be recognized as foreign investment, or whether our contractual arrangements would be deemed to be in violation of the foreign investment access requirements. Therefore, there is no guarantee that our contractual arrangements, or Yubo Beijing’s business will not be adversely affected.

To comply with PRC laws and regulations, we conduct our stem cell bank and endometrial stem cell bank business in China through the VIE, Yubo Beijing. We, through the WFOE, our wholly owned subsidiary in China, entered into a series of contractual arrangements with the VIE and its ultimate shareholders, in order to (i) consolidate the financial results of the VIE in our consolidated financial statements, (ii) receive substantially all of the economic benefits of the VIE, and (iii) have an exclusive option to purchase all or part of the equity interests in the VIE when and to the extent permitted by PRC law. As a result of these contractual arrangements, we are deemed, for accounting purpose only, the primary beneficiary of the VIE and hence consolidate its financial results under GAAP. Although the structure we have adopted is consistent with long-standing practice in certain industries, is also adopted by some of our peers in China, and our contractual agreements with Yubo Beijing have not been tested in a court of law, the PRC government may not agree that these arrangements comply with PRC license, registration or other regulatory requirements, with existing policies, or with requirements or policies that may be adopted in the future, or could disallow our contractual arrangements with Yubo Beijing, which would likely result in a material adverse change in our operations, and, given the resulting inability to consolidate Yubo Beijing's financial results in our consolidated financial statements, in the value of our Class A common stock, which could significantly decline or become worthless. The VIE hold the licenses, approvals and key assets that are essential for the operations and we, as a U.S. holding company, do not have any direct busines operations in China, nor do we have any title to or ownership interest in such licenses, approvals and key assets.