SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

for the transition period from to

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number 001-12518

BANCO SANTANDER, S.A.

(Exact name of Registrant as specified in its charter)

Kingdom of Spain

(Jurisdiction of incorporation)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid), Spain

(address of principal executive offices)

José Antonio Álvarez

Banco Santander, S.A.

Ciudad Grupo Santander

28660 Boadilla del Monte

Madrid, Spain

Tel: +34 91 289 32 80

Fax: +34 91 257 12 82

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered, pursuant to Section 12(b) of the Act

| Title of each class |

Name of each exchange on which registered | |

| American Depositary Shares, each representing the right to receive one Share of Capital Stock of Banco Santander, S.A., par value Euro 0.50 each |

New York Stock Exchange | |

| Shares of Capital Stock of Banco Santander, S.A., par value Euro 0.50 each |

New York Stock Exchange * | |

| Guarantee of Non-cumulative Guaranteed Preferred Stock of Santander Finance Preferred, S.A. Unipersonal, Series 1,4,5, 6, 10 and 11 |

New York Stock Exchange ** |

| * | Banco Santander Shares are not listed for trading, but are only listed in connection with the registration of the American Depositary Shares, pursuant to requirements of the New York Stock Exchange. |

| ** | The guarantee is not listed for trading, but is listed only in connection with the registration of the corresponding Non-cumulative Guaranteed Preferred Stock of Santander Finance Preferred, S.A. Unipersonal (a wholly owned subsidiary of Banco Santander, S.A.) |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None.

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act

None.

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

US GAAP ¨ International Financial Reporting Standards as issued by the International Accounting Standards Board x Other ¨

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

Indicate the number of outstanding shares of each of the issuer’s classes of capital stock or common stock as of the close

of business covered by the annual report.

9,076,853,400 shares

BANCO SANTANDER, S.A.

| Page | ||||

| 4 | ||||

| 5 | ||||

| ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

7 | |||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 12 | ||||

| 12 | ||||

| 12 | ||||

| 22 | ||||

| 22 | ||||

| 37 | ||||

| 100 | ||||

| 100 | ||||

| 100 | ||||

| 100 | ||||

| 107 | ||||

| 139 | ||||

| 140 | ||||

| 140 | ||||

| 141 | ||||

| 142 | ||||

| 143 | ||||

| 145 | ||||

| 145 | ||||

| 152 | ||||

| 177 | ||||

| 185 | ||||

| 187 | ||||

| 188 | ||||

| 188 | ||||

| 189 | ||||

| 189 | ||||

| 190 | ||||

| 190 | ||||

| 200 | ||||

| 201 | ||||

| 201 | ||||

| 203 | ||||

| 203 | ||||

| 208 | ||||

| 208 | ||||

| 208 | ||||

| 208 | ||||

| 208 | ||||

| 208 | ||||

| 217 | ||||

| 217 | ||||

| 218 | ||||

| 222 | ||||

| 223 | ||||

| 223 | ||||

| 223 | ||||

| ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

224 | |||

| 224 | ||||

| Part 1. Corporate principles of risk management, control and risk appetite |

224 | |||

| 230 | ||||

| 232 | ||||

| 234 | ||||

| 267 | ||||

| 272 | ||||

| 275 | ||||

| 277 | ||||

| 280 | ||||

| 280 | ||||

| ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES |

307 | |||

| 307 | ||||

| 307 | ||||

| 307 | ||||

| 307 | ||||

| 309 | ||||

| ITEM 14. MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

309 | |||

| 309 | ||||

| 312 | ||||

| 312 | ||||

| 312 | ||||

| 313 | ||||

| D. Exemptions from the Listing Standards for Audit Committees |

314 | |||

| E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

314 | |||

| 314 | ||||

| 314 | ||||

| 317 | ||||

| 318 | ||||

| 318 | ||||

| 318 | ||||

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Accounting Principles

Under Regulation (EC) No. 1606/2002 of the European Parliament and of the Council of July 19, 2002, all companies governed by the law of an EU Member State and whose securities are admitted to trading on a regulated market of any Member State must prepare their consolidated financial statements in conformity with the International Financial Reporting Standards previously adopted by the European Union (“EU-IFRS”). The Bank of Spain Circular 4/2004 of December 22, 2004 on Public and Confidential Financial Reporting Rules and Formats (“Circular 4/2004”) requires Spanish credit institutions to adapt their accounting systems to the principles derived from the adoption by the European Union of International Financial Reporting Standards. Therefore, Grupo Santander (“the Group” or “Santander”) is required to prepare its consolidated financial statements for the year ended December 31, 2011 in conformity with the EU-IFRS and Bank of Spain’s Circular 4/2004. Differences between EU-IFRS, Bank of Spain’s Circular 4/2004 and International Financial Reporting Standards as issued by the International Accounting Standard Board (IFRS-IASB) are not material. Therefore, we assert that the financial information contained in this annual report on Form 20-F complies with IFRS-IASB.

We have formatted our financial information according to the classification format for banks used in Spain. We have not reclassified the line items to comply with Article 9 of Regulation S-X. Article 9 is a regulation of the US Securities and Exchange Commission that contains formatting requirements for bank holding company financial statements.

Our auditors, Deloitte, S.L., an independent registered public accounting firm, have audited our consolidated financial statements in respect of the three years ended December 31, 2011, 2010 and 2009 in accordance with IFRS-IASB. See page F-1 to our consolidated financial statements for the 2011, 2010 and 2009 report prepared by Deloitte, S.L.

General Information

Our consolidated financial statements are in Euros, which are denoted “euro”, “euros”, “EUR” or “€” throughout this annual report. Also, throughout this annual report, when we refer to:

| • | “dollars”, “US$” or “$”, we mean United States dollars; |

| • | “pounds” or “£”, we mean United Kingdom pounds; and |

| • | “one billion”, we mean 1,000 million. |

When we refer to “average balances” for a particular period, we mean the average of the month-end balances for that period, unless otherwise noted. We do not believe that monthly averages present trends that are materially different from trends that daily averages would show. In calculating our interest income, we include any interest payments we received on non-accruing loans if they were received in the period when due. We have not reflected consolidation adjustments in any financial information about our subsidiaries or other business units.

When we refer to “loans”, we mean loans, leases, discounted bills and accounts receivable, unless otherwise noted. The loan to value “LTV” ratios disclosed in this report refer to LTV ratios upon origination unless otherwise noted. Additionally, if a debt is approaching a doubtful status, we update the appraisals which are then used to estimate allowances for loan losses.

When we refer to “impaired balances” or “non-performing balances”, we mean impaired or non-performing loans and contingent liabilities (“NPL”), securities and other assets to collect.

When we refer to “allowances for credit losses”, we mean the specific allowances for credit losses, and unless otherwise noted, the collectively assessed allowance for credit losses and any allowances for country-risk. See “Item 4. Information on the Company—B. Business Overview—Classified Assets—Allowances for Credit Losses and Country-Risk Requirements”.

Where a translation of foreign exchange is given for any financial data, we use the exchange rates of the relevant period (as of the end of such period for balance sheet data and the average exchange rate of such period for income statement data) as published by the European Central Bank, unless otherwise noted.

4

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains statements that constitute “forward-looking statements” within the meaning of the US Private Securities Litigation Reform Act of 1995. Forward-looking statements include, but are not limited to, information regarding:

| • | exposure to various types of market risks; |

| • | management strategy; |

| • | capital expenditures; |

| • | earnings and other targets; and |

| • | asset portfolios. |

Forward-looking statements may be identified by words such as “expect,” “project,” “anticipate,” “should,” “intend,” “probability,” “risk,” “VaR,” “RORAC,” “target,” “goal,” “objective,” “estimate,” “future” and similar expressions. We include forward-looking statements in the “Operating and Financial Review and Prospects,” “Information on the Company,” and “Quantitative and Qualitative Disclosures About Market Risk” sections. Forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those in the forward-looking statements.

You should understand that adverse changes in the following important factors, in addition to those discussed in “Key Information—Risk Factors”, “Operating and Financial Review and Prospects,” “Information on the Company” and elsewhere in this annual report, could affect our future results and could cause those results or other outcomes to differ materially from those anticipated in any forward-looking statement:

Economic and Industry Conditions

| • | exposure to various types of market risks, principally including interest rate risk, foreign exchange rate risk and equity price risk; |

| • | general economic or industry conditions in Spain, the United Kingdom, the United States, other European countries, Brazil, other Latin American countries and the other areas in which we have significant business activities or investments; |

| • | a default on, or a ratings downgrade of, the sovereign debt of Spain, and the other countries where we operate; |

| • | a worsening of the economic environment in the United Kingdom, other European countries, Brazil, other Latin American countries, and the United States, and an increase of the volatility in the capital markets; |

| • | a further deterioration of the Spanish economy; |

| • | the effects of a continued decline in real estate prices, particularly in Spain, the UK and the US; |

| • | monetary and interest rate policies of the European Central Bank and various central banks; |

| • | inflation or deflation; |

| • | the effects of non-linear market behavior that cannot be captured by linear statistical models, such as the VaR model we use; |

| • | changes in competition and pricing environments; |

| • | the inability to hedge some risks economically; |

| • | the adequacy of loss reserves; |

| • | acquisitions or restructurings of businesses that may not perform in accordance with our expectations; |

| • | changes in demographics, consumer spending, investment or saving habits; and |

| • | changes in competition and pricing environments as a result of the progressive adoption of the internet for conducting financial services and/or other factors. |

5

Political and Governmental Factors

| • | political stability in Spain, the United Kingdom, other European countries, Latin America and the US; |

| • | changes in Spanish, UK, EU, Latin American, US or other jurisdictions’ laws, regulations or taxes; and |

| • | increased regulation in light of the global financial crisis. |

Transaction and Commercial Factors

| • | damage to our reputation; |

| • | our ability to integrate successfully our acquisitions and the challenges inherent in diverting management’s focus and resources from other strategic opportunities and from operational matters while we integrate these acquisitions; and |

| • | the outcome of our negotiations with business partners and governments. |

Operating Factors

| • | potential losses associated with an increase in the level of substandard loans or non-performance by counterparties to other types of financial instruments. |

| • | technical difficulties and the development and use of new technologies by us and our competitors; |

| • | the occurrence of force majeure, such as natural disasters, that impact our operations or impair the asset quality of our loan portfolio; and |

| • | the impact of changes in the composition of our balance sheet on future net interest income. |

The forward-looking statements contained in this annual report speak only as of the date of this annual report. We do not undertake to update any forward-looking statement to reflect events or circumstances after that date or to reflect the occurrence of unanticipated events.

6

Item 1. Identity of Directors, Senior Management and Advisers

A. Directors and Senior Management

Not applicable.

B. Advisers

Not applicable.

C. Auditor

Not applicable.

Item 2. Offer Statistics and Expected Timetable

A. Offer Statistics

Not applicable.

B. Method and Expected Timetable

Not applicable.

Selected Consolidated Financial Information

We have selected the following financial information from our consolidated financial statements. You should read this information in connection with, and it is qualified in its entirety by reference to, our consolidated financial statements.

In the F-pages of this Form 20-F, the audited financial statements for the years 2011, 2010 and 2009 are presented. The audited financial statements for 2008 and 2007 are not included in this document, but they can be found in our previous annual reports on Form 20-F.

Under IFRS-IASB, revenues and expenses of discontinued businesses must be reclassified from each income statement line item to “Profit from discontinued operations”. Revenues and expenses from prior years are also required to be reclassified for comparison purposes to present the same businesses as discontinued operations. This change in presentation does not affect “Consolidated profit for the year” (see Note 37 to our consolidated financial statements).

In addition, the income statement for the year ended December, 31, 2011 reflects the impact of the consolidation of Bank Zachodni WBK, S.A. and the income statement for the year ended December, 31, 2009 reflects the impact of the consolidation of Banco Real, Alliance & Leicester, Bradford & Bingley’s branch network and retail deposits, Sovereign and other consumer businesses.

7

| Year ended December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| (in millions of euros, except percentages and per share data) | ||||||||||||||||||||

| Interest and similar income |

60,856 | 52,907 | 53,173 | 55,044 | 45,512 | |||||||||||||||

| Interest expense and similar charges |

(30,035 | ) | (23,683 | ) | (26,874 | ) | (37,506 | ) | (31,069 | ) | ||||||||||

| Interest income / (charges) |

30,821 | 29,224 | 26,299 | 17,538 | 14,443 | |||||||||||||||

| Income from equity instruments |

394 | 362 | 436 | 553 | 420 | |||||||||||||||

| Income from companies accounted for using the equity method |

57 | 17 | (1 | ) | 792 | 438 | ||||||||||||||

| Fee and commission income |

12,749 | 11,681 | 10,726 | 9,741 | 9,290 | |||||||||||||||

| Fee and commission expense |

(2,277 | ) | (1,946 | ) | (1,646 | ) | (1,475 | ) | (1,422 | ) | ||||||||||

| Gains/losses on financial assets and liabilities (net) |

2,838 | 2,164 | 3,802 | 2,892 | 2,306 | |||||||||||||||

| Exchange differences (net) |

(522 | ) | 441 | 444 | 582 | 649 | ||||||||||||||

| Other operating income |

8,050 | 8,195 | 7,929 | 9,436 | 6,740 | |||||||||||||||

| Other operating expenses |

(8,032 | ) | (8,089 | ) | (7,785 | ) | (9,163 | ) | (6,449 | ) | ||||||||||

| Total income |

44,078 | 42,049 | 40,204 | 30,896 | 26,415 | |||||||||||||||

| Administrative expenses |

(17,781 | ) | (16,255 | ) | (14,825 | ) | (11,666 | ) | (10,777 | ) | ||||||||||

| Personnel expenses |

(10,326 | ) | (9,329 | ) | (8,451 | ) | (6,813 | ) | (6,435 | ) | ||||||||||

| Other general administrative expenses |

(7,455 | ) | (6,926 | ) | (6,374 | ) | (4,853 | ) | (4,342 | ) | ||||||||||

| Depreciation and amortization |

(2,109 | ) | (1,940 | ) | (1,596 | ) | (1,240 | ) | (1,247 | ) | ||||||||||

| Provisions (net) |

(2,601 | ) | (1,133 | ) | (1,792 | ) | (1,641 | ) | (896 | ) | ||||||||||

| Impairment losses on financial assets (net) |

(11,868 | ) | (10,443 | ) | (11,578 | ) | (6,283 | ) | (3,430 | ) | ||||||||||

| Impairment losses on other assets (net) |

(1,517 | ) | (286 | ) | (165 | ) | (1,049 | ) | (1,548 | ) | ||||||||||

| Gains/(losses) on disposal of assets not classified as non-current assets held for sale |

1,846 | 350 | 1,565 | 101 | 1,810 | |||||||||||||||

| Gains/(losses) on non-current assets held for sale not classified as discontinued operations |

(2,109 | ) | (290 | ) | (1,225 | ) | 1,731 | 643 | ||||||||||||

| Operating profit/(loss) before tax |

7,939 | 12,052 | 10,588 | 10,849 | 10,970 | |||||||||||||||

| Income tax |

(1,776 | ) | (2,923 | ) | (1,207 | ) | (1,836 | ) | (2,322 | ) | ||||||||||

| Profit from continuing operations |

6,163 | 9,129 | 9,381 | 9,013 | 8,648 | |||||||||||||||

| Profit/(loss) from discontinued operations (net) |

(24 | ) | (27 | ) | 31 | 319 | 988 | |||||||||||||

| Consolidated profit for the year |

6,139 | 9,102 | 9,412 | 9,332 | 9,636 | |||||||||||||||

| Profit attributable to the Parent |

5,351 | 8,181 | 8,942 | 8,876 | 9,060 | |||||||||||||||

| Profit attributable to non-controlling interest |

788 | 921 | 470 | 456 | 576 | |||||||||||||||

| Per share information: |

||||||||||||||||||||

| Average number of shares (thousands) (1) |

8,892,033 | 8,686,522 | 8,554,224 | 7,271,470 | 6,801,899 | |||||||||||||||

| Basic earnings per share (euros) |

0.60 | 0.94 | 1.05 | 1.22 | 1.33 | |||||||||||||||

| Basic earnings per share continuing operation (euros) |

0.60 | 0.94 | 1.04 | 1.18 | 1.20 | |||||||||||||||

| Diluted earnings per share (euros) |

0.60 | 0.94 | 1.04 | 1.21 | 1.32 | |||||||||||||||

| Diluted earnings per share continuing operation (euros) |

0.60 | 0.94 | 1.04 | 1.17 | 1.19 | |||||||||||||||

| Remuneration paid (euros) (2) |

0.60 | 0.60 | 0.60 | 0.63 | 0.61 | |||||||||||||||

| Remuneration paid (US$) (2) |

0.78 | 0.80 | 0.86 | 0.88 | 0.89 | |||||||||||||||

8

| Year ended December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| (in millions of euros, except percentages and per share data) | ||||||||||||||||||||

| Total assets |

1,251,526 | 1,217,501 | 1,110,529 | 1,049,632 | 912,915 | |||||||||||||||

| Loans and advances to credit institutions (net) (3) |

51,726 | 79,855 | 79,837 | 78,792 | 57,643 | |||||||||||||||

| Loans and advances to customers (net) (3) |

750,100 | 724,153 | 682,551 | 626,888 | 571,099 | |||||||||||||||

| Investment securities (net) (4) |

154,015 | 174,258 | 173,990 | 124,673 | 132,035 | |||||||||||||||

| Investments: Associates and joint venture |

4,155 | 273 | 164 | 1,323 | 15,689 | |||||||||||||||

| Contingent liabilities (net) |

48,042 | 59,795 | 59,256 | 65,323 | 76,217 | |||||||||||||||

| Liabilities |

||||||||||||||||||||

| Deposits from central banks and credit institutions (5) |

143,138 | 140,112 | 142,091 | 129,877 | 112,897 | |||||||||||||||

| Customer deposits (5) |

632,533 | 616,376 | 506,975 | 420,229 | 355,407 | |||||||||||||||

| Debt securities (5) |

197,372 | 192,873 | 211,963 | 236,403 | 233,287 | |||||||||||||||

| Capitalization |

||||||||||||||||||||

| Guaranteed subordinated debt excluding preferred securities and preferred shares (6) |

6,619 | 10,934 | 13,867 | 15,748 | 16,742 | |||||||||||||||

| Other subordinated debt |

10,477 | 12,189 | 15,193 | 14,452 | 11,667 | |||||||||||||||

| Preferred securities (6) |

5,447 | 6,917 | 7,315 | 7,622 | 7,261 | |||||||||||||||

| Preferred shares (6) |

449 | 435 | 430 | 1,051 | 523 | |||||||||||||||

| Non-controlling interest (including net income of the period) |

6,445 | 5,897 | 5,203 | 2,415 | 2,358 | |||||||||||||||

| Stockholders’ equity (7) |

76,414 | 75,018 | 68,667 | 57,587 | 55,200 | |||||||||||||||

| Total capitalization |

105,851 | 111,390 | 110,675 | 98,875 | 93,751 | |||||||||||||||

| Stockholders’ equity per share (7) |

8.59 | 8.64 | 8.03 | 7.92 | 8.12 | |||||||||||||||

| Other managed funds |

||||||||||||||||||||

| Mutual funds |

102,611 | 113,510 | 105,216 | 90,306 | 119,211 | |||||||||||||||

| Pension funds |

9,645 | 10,965 | 11,310 | 11,128 | 11,952 | |||||||||||||||

| Managed portfolio |

19,200 | 20,314 | 18,364 | 17,289 | 19,814 | |||||||||||||||

| Total other managed funds |

131,456 | 144,789 | 134,890 | 118,723 | 150,977 | |||||||||||||||

| Consolidated ratios |

||||||||||||||||||||

| Profitability ratios: |

||||||||||||||||||||

| Net yield (8) |

2.74 | % | 2.68 | % | 2.62 | % | 2.05 | % | 1.80 | % | ||||||||||

| Return on average total assets (ROA) |

0.50 | % | 0.76 | % | 0.86 | % | 1.00 | % | 1.10 | % | ||||||||||

| Return on average stockholders’ equity (ROE) |

7.14 | % | 11.80 | % | 13.90 | % | 17.07 | % | 21.91 | % | ||||||||||

| Capital ratio: |

||||||||||||||||||||

| Average stockholders’ equity to average total assets |

6.10 | % | 5.82 | % | 5.85 | % | 5.55 | % | 4.71 | % | ||||||||||

| Ratio of earnings to fixed charges (9) |

||||||||||||||||||||

| Excluding interest on deposits |

1.63 | % | 2.28 | % | 2.01 | % | 1.57 | % | 1.67 | % | ||||||||||

| Including interest on deposits |

1.27 | % | 1.52 | % | 1.40 | % | 1.27 | % | 1.35 | % | ||||||||||

| Credit quality data |

||||||||||||||||||||

| Loans and advances to customers |

||||||||||||||||||||

| Allowances for impaired balances including country risk and excluding contingent liabilities as a percentage of total gross loans |

2.46 | % | 2.65 | % | 2.55 | % | 1.95 | % | 1.50 | % | ||||||||||

| Impaired balances as a percentage of total gross loans |

4.07 | % | 3.75 | % | 3.43 | % | 2.19 | % | 1.05 | % | ||||||||||

| Allowances for impaired balances as a percentage of impaired balances |

60.52 | % | 70.58 | % | 74.32 | % | 89.08 | % | 143.24 | % | ||||||||||

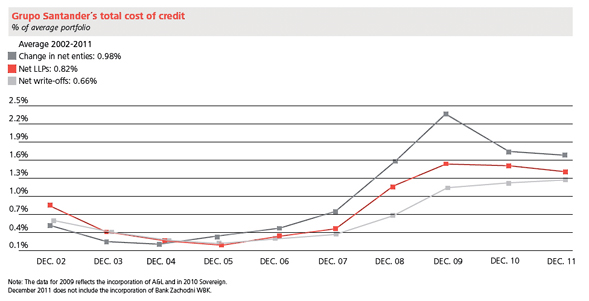

| Net loan charge-offs as a percentage of total gross loans |

1.38 | % | 1.31 | % | 1.27 | % | 0.60 | % | 0.46 | % | ||||||||||

| Ratios adding contingent liabilities to loans and advances to customers and excluding country risk (*) |

||||||||||||||||||||

| Allowances for impaired balances (**) as a percentage of total loans and contingent liabilities |

2.39 | % | 2.58 | % | 2.44 | % | 1.83 | % | 1.42 | % | ||||||||||

| Impaired balances (**) (10) as a percentage of total loans and contingent liabilities |

3.89 | % | 3.55 | % | 3.24 | % | 2.02 | % | 0.94 | % | ||||||||||

| Allowances for impaired balances (**) as a percentage of impaired balances (**) |

61.37 | % | 72.74 | % | 75.33 | % | 90.64 | % | 150.55 | % | ||||||||||

| Net loan and contingent liabilities charge-offs as a percentage of total loans and contingent liabilities |

1.29 | % | 1.21 | % | 1.17 | % | 0.55 | % | 0.41 | % | ||||||||||

| (*) | We disclose these ratios because our credit risk exposure comprises loans and advances to customers as well as contingent liabilities, all of which are subject to impairment and, therefore, allowances are taken in respect thereof. |

| (**) | Impaired or non-performing loans and contingent liabilities, securities and other assets to collect. |

9

| (1) | Average number of shares has been calculated on the basis of the weighted average number of shares outstanding in the relevant year, net of treasury stock. |

| (2) | The shareholders at the annual shareholders’ meeting held on June 19, 2009 approved a dividend of €0.6508 per share to be paid out of our profits for 2008. In accordance with IAS 33, for comparative purposes, dividends per share paid, as disclosed in the table above, take into account the adjustment arising from the capital increase with pre-emptive subscription rights carried out in December 2008. As a result of this adjustment, the dividend per share for 2008 amounts to €0.6325. The shareholders also approved a new remuneration scheme (scrip dividend), whereby the Bank offered the shareholders the possibility to opt to receive an amount equivalent to the second interim dividend on account of the 2009 financial year in cash or new shares. In light of the acceptance of this remuneration program (81% of the capital opted to receive shares instead of cash), at the general shareholders’ meetings held in June 2010 and 2011, the shareholders approved to offer again this option to the shareholders as payment for the second and third interim dividends on account of 2010 and 2011. The remuneration per share for 2009, 2010 and 2011 disclosed above, €0.60, is calculated assuming that the four dividends for these years were paid in cash. In 2010 and 2011, 85% and 80% of the capital, respectively, opted to receive the second and third interim dividends in the form of shares instead of cash. Additionally, at its meeting on December 19, 2011, the board of directors resolved to apply the scrip dividend program on the dates on which the fourth interim dividend is traditionally paid, and offered shareholders the option of receiving an amount equal to this dividend of €0.220 per share, to be paid in shares or cash. This resolution was approved by the annual general shareholders’ meeting held on March 30, 2012. |

| (3) | Equals the sum of the amounts included under the headings “Financial assets held for trading”, “Other financial assets at fair value through profit or loss” and “Loans and receivables” as stated in our consolidated financial statements. |

| (4) | Equals the amounts included as “Debt instruments” and “Equity instruments” under the headings “Financial assets held for trading”, “Other financial assets at fair value through profit or loss”, “Available-for-sale financial assets” and “Loans and receivables” as stated in our consolidated financial statements. |

| (5) | Equals the sum of the amounts included under the headings “Financial liabilities held for trading”, “Other financial liabilities at fair value through profit or loss” and “Financial liabilities at amortized cost” included in Notes 20, 21 and 22 to our consolidated financial statements. |

| (6) | In our consolidated financial statements, preferred securities and preferred shares are included under “Subordinated liabilities”. |

| (7) | Equals the sum of the amounts included at the end of each year as “Own funds” and “Valuation adjustments” as stated in our consolidated financial statements. We have deducted the book value of treasury stock from stockholders’ equity. |

| (8) | Net yield is the total of net interest income (including dividends on equity securities) divided by average earning assets. See “Item 4. Information on the Company—B. Business Overview—Selected Statistical Information—Assets—Earning Assets—Yield Spread”. |

| (9) | For the purpose of calculating the ratio of earnings to fixed charges, earnings consist of pre-tax income from continuing operations before adjustment for income or loss from equity investees plus fixed charges. Fixed charges consist of total interest expense (including or excluding interest on deposits as appropriate) and the interest expense portion of rental expense. |

| (10) | Impaired loans reflect Bank of Spain classifications. These classifications differ from the classifications applied by U.S. banks in reporting loans as non-accrual, past due, restructured and potential problem loans. See “Item 4. Information on the Company—B. Business Overview—Classified Assets—Bank of Spain Classification Requirements”. |

10

Set forth below is a table showing our allowances for impaired balances broken down by various categories as disclosed and discussed throughout this annual report on Form 20-F:

| IFRS-IASB | ||||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| Allowances refers to: |

(in millions of euros) | |||||||||||||||||||

| Allowances for impaired balances (*) (excluding country risk) |

19,661 | 20,748 | 18,497 | 12,863 | 9,302 | |||||||||||||||

| Allowances for contingent liabilities and commitments (excluding country risk) |

(648 | ) | (1,011 | ) | (623 | ) | (622 | ) | (587 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Allowances for impaired balances of loans (excluding country risk): |

19,013 | 19,737 | 17,874 | 12,241 | 8,715 | |||||||||||||||

| Allowances referred to country risk and other |

210 | 121 | 192 | 660 | 173 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Allowances for impaired balances (excluding contingent liabilities) |

19,223 | 19,858 | 18,066 | 12,901 | 8,888 | |||||||||||||||

| Of which: |

||||||||||||||||||||

| Allowances for Loans and receivables: |

18,988 | 19,739 | 17,899 | 12,720 | 8,796 | |||||||||||||||

| Allowances for Customers |

18,936 | 19,697 | 17,873 | 12,466 | 8,695 | |||||||||||||||

| Allowances for Credit institutions and other financial assets |

36 | 17 | 26 | 254 | 101 | |||||||||||||||

| Allowances for Debt Instruments |

16 | 25 | 0 | 0 | 0 | |||||||||||||||

| Allowances for Debt Instruments available for sale |

235 | 119 | 167 | 181 | 92 | |||||||||||||||

| (*) | Impaired or non-performing loans and contingent liabilities, securities and other assets to collect. |

Exchange Rates

Fluctuations in the exchange rate between euros and dollars have affected the dollar equivalent of the share prices on Spanish stock exchanges and, as a result, are likely to affect the dollar market price of our American Depositary Shares, or ADSs, in the United States. In addition, dividends paid to the depositary of the ADSs are denominated in euros and fluctuations in the exchange rate affect the dollar conversion by the depositary of dividends paid on the shares to the holders of the ADSs. Fluctuations in the exchange rate of euros against other currencies may also affect the euro value of our non-euro denominated assets, liabilities, earnings and expenses.

The following tables set forth, for the periods and dates indicated, certain information concerning the exchange rate for euros and dollars (expressed in dollars per euro), based on the Noon Buying Rate as announced by the Federal Reserve Bank of New York for the dates and periods indicated.

The New York Federal Reserve Bank announced its decision to discontinue the publication of foreign exchange rates on December 31, 2008. From that date, the exchange rates shown are those published by the European Central Bank (“ECB”), and are based on the daily consultation procedures between central banks within and outside the European System of Central Banks, which normally takes place at 14:15 p.m. ECB time.

| Rate During Period | ||||||||

| Calendar Period | Period End ($) |

Average Rate ($) |

||||||

| 2007 |

1.46 | 1.38 | ||||||

| 2008 |

1.39 | 1.47 | ||||||

| 2009 |

1.44 | 1.39 | ||||||

| 2010 |

1.34 | 1.33 | ||||||

| 2011 |

1.29 | 1.39 | ||||||

11

| Rate During Period | ||||||||

| Last six months | High $ | Low $ | ||||||

| 2011 |

||||||||

| October |

1.42 | 1.32 | ||||||

| November |

1.38 | 1.32 | ||||||

| December |

1.35 | 1.29 | ||||||

| 2012 |

||||||||

| January |

1.32 | 1.27 | ||||||

| February |

1.35 | 1.30 | ||||||

| March |

1.34 | 1.31 | ||||||

| April (through April 26) |

1.33 | 1.30 | ||||||

On April 26, 2012, the exchange rate for euros and dollars (expressed in dollars per euro), as published by the ECB, was $1.32.

For a discussion of the accounting principles used in translation of foreign currency-denominated assets and liabilities to euros, see Note 2 (a) of our consolidated financial statements.

B. Capitalization and indebtedness.

Not Applicable.

C. Reasons for the offer and use of proceeds.

Not Applicable.

Because our loan portfolio is concentrated in Continental Europe, the United Kingdom and Latin America, adverse changes affecting the economies of Continental Europe, the United Kingdom or certain Latin American countries could adversely affect our financial condition.

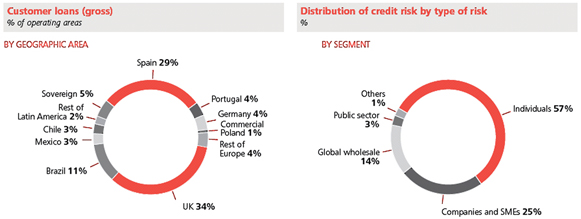

Our loan portfolio is concentrated in Continental Europe (in particular, Spain), the United Kingdom and Latin America. At December 31, 2011, Continental Europe accounted for 42% of our total loan portfolio (Spain accounted for 29% of our total loan portfolio), while the United Kingdom and Latin America accounted for 34% and 19%, respectively. Continued recessionary economic conditions in the economies of Continental Europe (in particular, Spain), or a return to recessionary conditions in the United Kingdom or the Latin American countries in which we operate, would likely have a significant adverse impact on our loan portfolio and, as a result, on our financial condition, cash flows and results of operations. See “Item 4. Information on the Company—B. Business Overview.”

Some of our business is cyclical and our income may decrease when demand for certain products or services is in a down cycle.

The level of income we derive from certain of our products and services depends on the strength of the economies in the regions where we operate and market trends prevailing in those regions. Customer loans and deposits, which collectively account for most of our earnings, are particularly sensitive to economic conditions. In 2011, Continental Europe, the United Kingdom, Latin America and Sovereign (US) represented 31%, 12%, 51% and 6%, respectively, of the profit attributable to the Group’s operating areas for the year. However, many of the economies of Continental Europe, including Spain and Portugal, are forecast to have flat or weakening economies in 2012. If the business environment in any of our geographic segments does not improve or worsens, our results of operations could be materially adversely affected.

Our business could be affected if our capital is not managed effectively or if changes limiting our ability to manage our capital position are adopted.

Effective management of our capital position is important to our ability to operate our business, to continue to grow organically and to pursue our business strategy. However, in response to the recent financial crisis, a number of changes to the regulatory capital framework have been adopted or are being considered. For example, on December 16, 2010 and January 13, 2011, the Basel Committee on Banking Supervision issued its final guidance on a number of regulatory reforms to the regulatory capital framework in order to strengthen minimum capital requirements, including the phasing out of Innovative Tier 1 Capital instruments with incentives to redeem and implementing a leverage ratio on institutions in addition to current risk-based regulatory requirements. As these and other changes are implemented or future changes are considered or adopted that limit our ability to manage our balance sheet and capital resources effectively or to access funding on commercially acceptable terms, we may experience a material adverse effect on our financial condition and regulatory capital position.

12

Reduced access to financing or increases in our cost of funding could have an adverse effect on our liquidity and results of operations.

Historically, our principal source of funds has been customer deposits (demand, time and notice deposits). Total time deposits (including repurchase agreements) represented 52.5%, 53.0% and 46.8% of total customer deposits at the end of 2011, 2010 and 2009, respectively. Large-denomination time deposits may be a less stable source of deposits than other type of deposits and, at December 31, 2011, 21.5% of total customer deposits were time deposits in amounts greater than $100,000. The ongoing availability of deposits as a source of funding is sensitive to a variety of factors outside our control, such as general economic conditions and the confidence of retail depositors in the economy and the financial services industry, in general, and in our creditworthiness, in particular, and the availability and extent of deposit guarantees, as well as competition between banks for deposits. In the event deposit levels decrease, we may be forced to raise the rates we pay on deposits, with a view to attracting more customers, and/or to increase our reliance on capital markets financing, which may be more expensive or unavailable.

We also fund our operations through the capital markets by issuing long-term debt, by issuing promissory notes and commercial paper or by obtaining bank loans or lines of credit. The cost and availability of capital markets financing generally are dependent on our short-term and long-term credit ratings and the market’s perception of the risks inherent in European banks and Spain. Factors that are important to the determination of our credit ratings include the level and quality of our earnings, capital adequacy, liquidity, risk appetite and management, asset quality, business mix and actual and perceived levels of government support. Banco Santander S.A.’s rating, together with that of the other main Spanish banks, was downgraded by all three rating agencies in October 2011 and by Standard & Poor’s and Fitch in February 2012. Any further downgrade in our ratings would likely increase our borrowing costs and could limit our access to capital markets and adversely affect our commercial business. See “—Credit, market and liquidity risks may have an adverse effect on our credit ratings and our cost of funds. Any reduction in our credit rating would likely increase our cost of funding, require us to post additional collateral or take other actions under some of our derivative contracts and adversely affect our interest margins and results of operations.”

The effects of the widespread crisis in investor confidence and resulting liquidity crisis experienced in 2008 and early 2009, and to some extent in 2011, have resulted in increased costs of funding and limited access to some of our traditional sources of liquidity, such as domestic and international capital markets and the interbank market, which has adversely affected our results of operations and financial condition. Further or continued reductions in our access to financing or increases in our cost of funding may make it harder and more expensive to obtain funding for our businesses. If our available funding is limited or we are forced to fund our operations at a higher cost, we may experience further adverse effects on our results of operations and financial condition.

The possibility of the moderate economic recovery returning to recessionary conditions or of turmoil or volatility in the financial markets would likely have an adverse effect on our business, financial position and results of operations.

In 2011, the global economy began to recover from the severe recessionary conditions of mid-2009, and certain regions (such as Latin America, the US and the UK) experienced a moderate economic recovery. However, the sustainability of this partial recovery has been dependent on a number of factors that are not within our control, such as a return of job growth and investment in the private sector, strengthening of housing sales and construction and timing of the exit from government credit easing policies. In addition, the modest economic recovery that had been experienced in Continental Europe has been tempered by adverse financial conditions in Europe, triggered by high sovereign budget deficits, austerity measures and rising sovereign debt levels in Greece, Ireland, Italy and Portugal, and is projected to slow or, in some cases, reverse in 2012. We continue to face risks resulting from the aftermath of the severe recession and the uneven and fragile recovery. A slowing or failing of the economic recovery or a deterioration in the economy of Continental Europe, especially in Spain, could result in a return of some or all of the adverse effects of the earlier recessionary conditions.

Since the middle of 2007, there has been disruption and turmoil in financial markets around the world. Throughout many of our largest markets, including Spain, there have been dramatic declines in the housing market, with falling home prices and increasing foreclosures, high levels of unemployment and underemployment, and reduced earnings, or, in some cases, losses, for businesses across many industries, with reduced investments in growth.

13

This overall environment resulted in significant stress for the financial services industry, led to distress in credit markets, reduced liquidity for many types of financial assets, including loans and securities and caused concerns regarding the financial strength and adequacy of the capitalization of financial institutions. Some financial institutions around the world have failed, some have needed significant additional capital, and others have been forced to seek acquisition partners.

Concerned about the stability of the financial markets generally, the strength of counterparties and about their own capital and liquidity positions, many lenders and institutional investors reduced or ceased providing funding to borrowers. The resulting economic pressure on consumers and businesses and the lack of confidence in the financial markets exacerbated the state of economic distress and hampered, and to some extent continues to hamper, efforts to bring about sustained economic recovery. While certain segments of the global economy are currently experiencing a moderate recovery, we expect these conditions to continue to have an ongoing negative impact on our business and results of operations. A slowing or failing of the economic recovery would likely aggravate the adverse effects of these difficult economic and market conditions on us and on others in the financial services industry.

In an attempt to prevent the failure of the financial system, Spain, the United States and other European governments intervened on an unprecedented scale. In Spain, the government increased consumer deposit guarantees, made available a program to guarantee the debt of certain financial institutions, created a fund to purchase assets from financial institutions and the Spanish Ministry of Economy and Finance was authorized, on an exceptional basis and until December 31, 2009, to acquire, at the request of credit institutions resident in Spain, shares and other capital instruments (including preferred shares) issued by such institutions. Additionally, in 2009 the Spanish government created the Orderly Banking Restructuring Fund (FROB) to manage the restructuring processes of credit institutions and reinforce the equity of institutions undergoing integration. In the United States, the federal government took equity stakes in several financial institutions, implemented a program to guarantee the short-term and certain medium-term debt of financial institutions, increased consumer deposit guarantees, and brokered the acquisitions of certain struggling financial institutions, among other measures. In the United Kingdom, the government effectively nationalized some of the country’s largest banks, provided a preferred equity program open to all financial institutions and a program to guarantee short-term and certain medium-term debt of financial institutions, among other measures. For more information on recent regulatory changes, see “—Changes in the regulatory framework in the jurisdictions where we operate could adversely affect our business.”

Despite the extent of the aforementioned intervention, global investor confidence remains cautious. The economies of the United States, United Kingdom, Brazil and other Latin American countries grew during 2011, although, in most cases, still at a slow pace. Spain, however, continued to suffer from a recession. In addition, recent downgrades of the sovereign debt of Ireland, Greece, Portugal, Italy and Spain have caused volatility in the capital markets. Our exposure to the sovereign debt of Greece, Portugal, Italy and Spain as of December 31, 2011 was €0.1, €1.8, €0.7 and €39.3 billion, respectively, and we had no exposure to the sovereign debt of Ireland.

Risks and ongoing concerns about the debt crisis in Europe could have a detrimental impact on the global economic recovery, sovereign and non-sovereign debt in these countries and the financial condition of European financial institutions, including us, and international financial institutions with exposure to the region. Market and economic disruptions have affected, and may continue to affect, consumer confidence levels and spending, personal bankruptcy rates, levels of incurrence and default on consumer debt and residential mortgages, and housing prices, among other factors. There can be no assurance that the market disruptions in Europe, including the increased cost of funding for certain governments and financial institutions, will not continue, nor can there be any assurance that future assistance packages will be available or, even if provided, will be sufficient to stabilize the affected countries and markets in Europe or elsewhere. To the extent uncertainty regarding the European economic recovery continues to negatively impact consumer confidence and consumer credit factors, or should the EU enter a deep recession, our business and results of operations could be materially adversely affected.

Continued or worsening disruption and volatility in the global financial markets could have a material adverse effect on our ability to access capital and liquidity on financial terms acceptable to us, if at all. If capital markets financing ceases to become available, or becomes excessively expensive, we may be forced to raise the rates we pay on deposits to attract more customers. Any such increase in capital markets funding costs or deposit rates would entail a repricing of loans, which would result in a reduction of volume, and may also have an adverse effect on our interest margins.

14

Risks concerning borrower credit quality and general economic conditions are inherent in our business.

Risks arising from changes in credit quality and the recoverability of loans and amounts due from counterparties are inherent in a wide range of our businesses. Adverse changes in the credit quality of our borrowers and counterparties or a general deterioration in Spanish, United Kingdom, Latin American, United States or global economic conditions, or arising from systemic risks in the financial systems, could reduce the recoverability and value of our assets and require an increase in our level of allowances for credit losses. Deterioration in the economies in which we operate could reduce the profit margins for our banking and financial services businesses.

The financial problems faced by our customers could adversely affect us.

Market turmoil and economic recession, especially in Spain, the United Kingdom, the United States and certain Latin American countries, could materially and adversely affect the liquidity, businesses and/or financial conditions of our borrowers, which could in turn increase our non-performing loan (“NPL”) ratios, impair our loan and other financial assets and result in decreased demand for borrowings in general. The uneven global recovery from the recent market turmoil and economic recession and the possibility of renewed economic contraction in Continental Europe, combined with continued high unemployment and low consumer spending, could cause the value of assets collateralizing our secured loans, including homes and other real estate, to decline significantly, which could result in the impairment of the value of our loan assets. Accordingly, in 2011 we experienced an increase in our non-performing ratios and a deterioration in asset quality as compared to 2010. In addition, our customers may further significantly decrease their risk tolerance to non-deposit investments such as stocks, bonds and mutual funds, which would adversely affect our fee and commission income. Any of the conditions described above could have a material adverse effect on our business, financial condition and results of operations.

We are exposed to risks faced by other financial institutions.

We routinely transact with counterparties in the financial services industry, including brokers and dealers, commercial banks, investment banks, mutual funds, hedge funds and other institutional clients. Defaults by, and even rumors or questions about the solvency of, certain financial institutions and the financial services industry generally have led to market-wide liquidity problems and could lead to losses or defaults by other institutions. Many of the routine transactions we enter into expose us to significant credit risk in the event of default by one of our significant counterparties. In 2011, the financial health of a number of European governments was shaken by the European sovereign debt crisis, contributing to volatility of the capital and credit markets, and the risk of contagion throughout and beyond the Eurozone remains, as a significant number of financial institutions throughout Europe have substantial exposures to sovereign debt issued by nations which are under considerable financial pressure. These liquidity concerns have had, and may continue to have, an adverse effect on interbank financial transactions in general. Should any of those nations default on their debt, or experience a significant widening of credit spreads, major financial institutions and banking systems throughout Europe could be destabilized. A default by a significant financial counterparty, or liquidity problems in the financial services industry generally, could have a material adverse effect on our business, financial condition and results of operations.

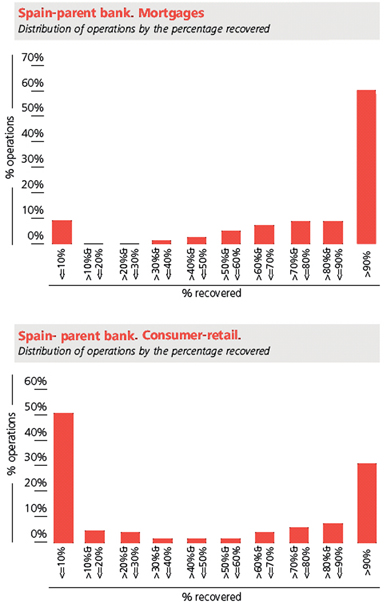

Our exposure to Spanish and UK real estate markets makes us more vulnerable to adverse developments in these markets.

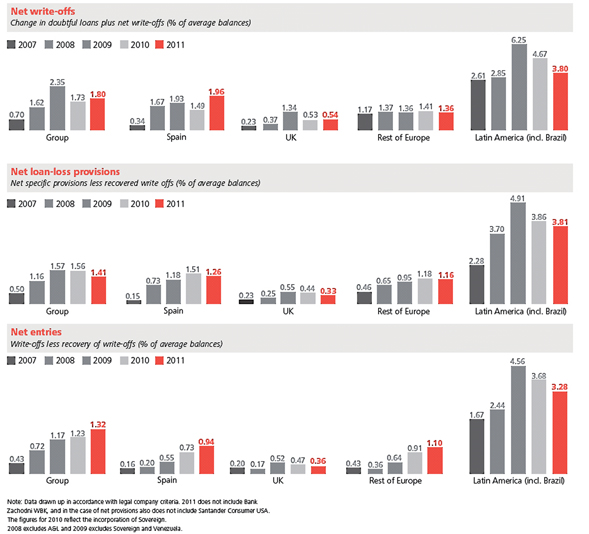

Mortgage loans are one of our principal assets, comprising 52% of our loan portfolio as of December 31, 2011. As a result, we are highly exposed to developments in real estate markets, especially in Spain and the United Kingdom. In addition, we have exposure to a number of large real estate developers in Spain. From 2002 to 2007, demand for housing and mortgage financing in Spain increased significantly driven by, among other things, economic growth, declining unemployment rates, demographic and social trends, the desirability of Spain as a vacation destination and historically low interest rates in the Eurozone. The United Kingdom experienced an increase in housing and mortgage demand driven by, among other things, economic growth, declining unemployment rates, demographic trends and the increasing prominence of London as an international financial center. During late 2007, the housing market began to adjust in Spain and the United Kingdom as a result of excess supply (particularly in Spain) and higher interest rates. Since 2008, as economic growth stalled in Spain and the United Kingdom, persistent housing oversupply, decreased housing demand, rising unemployment, subdued earnings growth, greater pressure on disposable income, a decline in the availability of mortgage finance and the continued effect of global market volatility have caused home prices to decline, while mortgage delinquencies increased. As a result, our NPL ratio increased from 0.94% at December 31, 2007, to 2.02% at December 31, 2008, to 3.24% at December 31, 2009 and to 3.55% at December 31, 2010. At December 31, 2011, our NPL ratio was 3.89%. These trends, especially higher unemployment rates coupled with declining real estate prices, could have a material adverse impact on our mortgage payment delinquency rates, which in turn could have a material adverse effect on our business, financial condition and results of operations.

15

Portions of our loan portfolio are subject to risks relating to force majeure events and any such event could materially adversely affect our operating results.

Our financial and operating performance may be adversely affected by force majeure events, such as natural disasters, particularly in locations where a significant portion of our loan portfolio is composed of real estate loans. Natural disasters such as earthquakes and floods may cause widespread damage which could impair the asset quality of our loan portfolio and could have an adverse impact on the economy of the affected region.

We may generate lower revenues from brokerage and other commission—and fee—based businesses.

Market downturns have lead, and are likely to continue to lead, to a decline in the volume of transactions that we execute for our customers and, therefore, to a decline in our non-interest revenue. In addition, because the fees that we charge for managing our clients’ portfolios are in many cases based on the value or performance of those portfolios, a market downturn that reduces the value of our clients’ portfolios or increases the amount of withdrawals would reduce the revenues we receive from our asset management, private banking and custody businesses and adversely affect our results of operations.

Even in the absence of a market downturn, below-market performance by our mutual funds may result in increased withdrawals and reduced inflows, which would reduce the revenue we receive from our asset management business and adversely affect our results of operations.

Market risks associated with fluctuations in bond and equity prices and other market factors are inherent in our business. Protracted market declines can reduce liquidity in the markets, making it harder to sell assets and leading to material losses.

The performance of financial markets may cause changes in the value of our investment and trading portfolios. In some of our businesses, protracted adverse market movements, particularly asset price declines, can reduce the level of activity in the market, reducing market liquidity. These developments can lead to material losses if we cannot close out deteriorating positions in a timely way. This risk is especially great for assets with normally less liquid markets. Assets that are not traded on stock exchanges or other public trading markets, such as derivative contracts between banks, may have values that we calculate using models other than publicly quoted prices. Monitoring the deterioration of prices of assets like these is difficult and could lead to losses that we did not anticipate.

The volatility of world equity markets due to the continued economic uncertainty and sovereign debt crisis has had a particularly strong impact on the financial sector. Continued volatility may affect the value of our investments in entities in this sector and, depending on their fair value and future recovery expectations, could become a permanent impairment which would be subject to write-offs against our results.

Volatility in interest rates may negatively affect our net interest income and increase our non-performing loan portfolio.

Changes in market interest rates could affect the interest rates charged on our interest-earning assets differently than the interest rates paid on our interest-bearing liabilities. This difference could result in an increase in interest expense relative to interest income leading to a reduction in our net interest income. Income from treasury operations is particularly vulnerable to interest rate volatility. Because the majority of our loan portfolio reprices in less than one year, rising interest rates may also lead to an increasing non-performing loan portfolio. Interest rates are highly sensitive to many factors beyond our control, including deregulation of the financial sector, monetary policies, domestic and international economic and political conditions and other factors.

As of December 31, 2011, our interest rate risk measured in daily Value at Risk (“VaRD”) terms amounted to €328.5 million.

Foreign exchange rate fluctuations may negatively affect our earnings and the value of our assets and shares.

Fluctuations in the exchange rate between the euro and the US dollar will affect the US dollar equivalent of the price of our securities on the stock exchanges in which our shares and ADSs are traded. These fluctuations will also affect the conversion to US dollars of cash dividends paid in euros on our ADSs.

In the ordinary course of our business, we have a percentage of our assets and liabilities denominated in currencies other than the euro. Fluctuations in the value of the euro against other currencies may adversely affect our profitability. For example, the appreciation of the euro against some Latin American currencies and the US dollar will depress earnings from our Latin American and US operations, and the appreciation of the euro against the sterling will depress earnings from our UK operations. Additionally, while most of the governments of the countries in which we operate have not imposed material prohibitions on the repatriation of dividends, capital investment or other distributions, no assurance can be given that these governments will not institute restrictive exchange control policies in the future. Moreover, fluctuations among the currencies in which our shares and ADSs trade could reduce the value of your investment.

16

As of December 31, 2011, our largest exposures on temporary positions (with a potential impact on the income statement) were concentrated on, in descending order, the pound sterling, the Mexican peso, the Chilean peso the Polish zloty (PLN) and the US dollar. At December 31, 2011, our largest exposures on permanent positions (with a potential impact on equity) were concentrated on, in descending order, the Brazilian real, the pound sterling, the US dollar, the Mexican peso, and the Polish zloty.

Despite our risk management policies, procedures and methods, we may nonetheless be exposed to unidentified or unanticipated risks.

Our risk management techniques and strategies may not be fully effective in mitigating our risk exposure in all economic market environments or against all types of risk, including risks that we fail to identify or anticipate. Some of our qualitative tools and metrics for managing risk are based upon our use of observed historical market behavior. We apply statistical and other tools to these observations to arrive at quantifications of our risk exposures. These qualitative tools and metrics may fail to predict future risk exposures. These risk exposures could, for example, arise from factors we did not anticipate or correctly evaluate in our statistical models. This would limit our ability to manage our risks. Our losses thus could be significantly greater than the historical measures indicate. In addition, our quantified modeling does not take all risks into account. Our more qualitative approach to managing those risks could prove insufficient, exposing us to material unanticipated losses. If existing or potential customers believe our risk management is inadequate, they could take their business elsewhere. This could harm our reputation as well as our revenues and profits.

Our recent and future acquisitions may not be successful and may be disruptive to our business.

We have acquired controlling interests in various companies and have engaged in other strategic partnerships. See “Item 4. Information on the Company—A. History and development of the Company.” Additionally, we may consider other strategic acquisitions and partnerships from time to time. While we are optimistic about the acquisitions we have made, there can be no assurances that we will be successful in our plans regarding the operation of these or other acquisitions and strategic partnerships.

We can give no assurance that our recent and any future acquisition and partnership activities will perform in accordance with our expectations. We base our assessment of potential acquisitions and partnerships on limited and potentially inexact information and on assumptions with respect to operations, profitability and other matters that may prove to be incorrect. We can give no assurances that our expectations with regards to integration and synergies will materialize.

Increased competition in the countries where we operate may adversely affect our growth prospects and operations.

Most of the financial systems in which we operate are highly competitive. Financial sector reforms in the markets in which we operate have increased competition among both local and foreign financial institutions, and we believe that this trend will continue. In particular, price competition in Europe, Latin America and the US has increased recently. Our success in the European, Latin American and US markets will depend on our ability to remain competitive with other financial institutions. In addition, there has been a trend towards consolidation in the banking industry, which has created larger and stronger banks with which we must now compete. There can be no assurance that this increased competition will not adversely affect our growth prospects, and therefore our operations. We also face competition from non-bank competitors, such as brokerage companies, department stores (for some credit products), leasing and factoring companies, mutual fund and pension fund management companies and insurance companies.

Changes in the regulatory framework in the jurisdictions where we operate could adversely affect our business.

Extensive legislation affecting the financial services industry has recently been adopted in Spain, the United States, the European Union and other jurisdictions, and regulations are in the process of being implemented. In Spain, the Bank of Spain issued Circular 9/2010 on December 22, 2010, which amends certain rules in order to establish more restrictive conditions regarding capital requirements for credit risk, credit risk mitigation techniques, securitization and treatment of counterparty and trading book risk. This Circular has not had and it is not expected that it will have a quantifiable material impact on our business. The Circular was issued following the passage of two EU Directives on risk management (Directive 2009/27/CE and Directive 2009/83/CE).

17

The European Union has created a European Systemic Risk Board to monitor financial stability and has implemented rules that will increase capital requirements for certain trading instruments or exposures and impose compensation limits on certain employees located in affected countries. In addition, the European Union Commission is considering a wide array of other initiatives, including new legislation that will affect derivatives trading, impose surcharges on “globally” systemically important firms and possibly impose new levies on bank balance sheets.

In the United States, the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) that was adopted in 2010 will result in significant structural reforms affecting the financial services industry. This legislation provides for, among other things: the establishment of a Consumer Financial Protection Bureau which will have broad authority to regulate the credit, savings, payment and other consumer financial products and services that we offer; the creation of a structure to regulate systemically important financial companies; more comprehensive regulation of the over-the-counter derivatives market; prohibitions on our engaging in certain proprietary trading activities and restricting our ownership of, investment in or sponsorship of, hedge funds and private equity funds; restrictions on the interchange fees that we earn on debit card transactions; and a requirement that bank regulators phase out the treatment of trust preferred capital debt securities as Tier 1 capital for regulatory capital purposes.

Regulators in the UK have produced a range of proposals for future legislative and regulatory changes, which could force us to comply with certain operational restrictions or take steps to raise further capital, or could increase our expenses or otherwise adversely affect our results of operations and financial condition. These proposals include: (i) the introduction of recovery and resolution planning requirements (popularly known as ‘living wills’) for banks and other financial institutions as contingency planning for the failure of a financial institution that may affect the stability of the financial system; (ii) the implementation of the Financial Services Act 2010, which enhances the FSA’s disciplinary and enforcement powers; (iii) the introduction of more regular and detailed reporting obligations; and (iv) a requirement for large UK retail banks to hold a minimum Core Tier 1 to risk-weighted assets ratio of at least 10%, which is approximately 3% higher than the minimum capital levels required under Basel III.

In December 2010, the Basel Committee on Banking Supervision announced revisions to its Capital Accord, which will require higher capital ratio requirements for banks, narrow the definition of capital, and introduce short term liquidity and term funding standards, among other things. The Basel Committee is also proposing to consider the imposition of a bank surcharge on institutions that are determined to be “globally significant financial institutions,” a liquidity coverage ratio and a net stable funding ratio. Compliance with these requirements could increase our funding and operational costs.

During the last few months of 2011 the European Banking Authority (EBA) established new requirements to strengthen capital ratios. These requirements are part of a series of measures adopted by the European Council in the second half of 2011, which aim to restore stability and confidence in the European markets. These capital requirements are expected to be exceptional and temporary.

The selected banks are required to have a core capital Tier 1 ratio of at least 9% by June 30, 2012, in accordance with the EBA’s rules. Each bank was required to present by January 20, 2012 their capitalization plan to reach the requirement by June 30, 2012. In the beginning of December 2011, the EBA disclosed its capital requirements for the main European banks. According to the EBA, our additional capital needs amounted to €15,302 million.

During the last few months of 2011 we have carried out a series of measures which allowed us, at the beginning of 2012, to achieve a core capital ratio of 9% ahead of the EBA deadline of June 30, 2012.

On February 3, 2012 the Ministry of Economy and Competitiveness approved the Royal Decree-Law 2/2012 on the clean-up of the financial sector (see Item 4. Information on the Company—A. History and Development of the Company – Recent Events)

These and any additional legislative or regulatory actions in Spain, the European Union, the United States, the UK or other countries, and any required changes to our business operations resulting from such legislation and regulations, could result in significant loss of revenue, limit our ability to pursue business opportunities in which we might otherwise consider engaging, affect the value of assets that we hold, require us to increase our prices and therefore reduce demand for our products, impose additional costs on us or otherwise adversely affect our businesses. Accordingly, we cannot provide assurance that any such new legislation or regulations would not have an adverse effect on our business, results of operations or financial condition in the future.

18

We may also face increased compliance costs and limitations on our ability to pursue certain business opportunities and provide certain products and services. As some of the banking laws and regulations have been recently adopted, the manner in which those laws and related regulations are applied to the operations of financial institutions is still evolving. Moreover, to the extent these recently adopted regulations are implemented inconsistently in the various jurisdictions in which we operate, we may face higher compliance costs. No assurance can be given generally that laws or regulations will be adopted, enforced or interpreted in a manner that will not have material adverse effect on our business and results of operations.

Operational risks are inherent in our business.

Our businesses depend on the ability to process a large number of transactions efficiently and accurately, and on our ability to rely on our digital technologies, computer and email services, software and networks, as well as on the secure processing, storage and transmission of confidential and other information in our computer systems and networks. Losses can result from inadequate personnel, inadequate or failed internal control processes and systems or from external events that interrupt normal business operations. We also face the risk that the design of our controls and procedures prove to be inadequate or are circumvented. Although we work with our clients, vendors, service providers, counterparties and other third parties to develop secure transmission capabilities and prevent against cyber attacks, we routinely exchange personal, confidential and proprietary information by electronic means, and we may be the target of attempted cyber attacks. We take protective measures and continuously monitor and develop our systems to protect our technology infrastructure and data from misappropriation or corruption, but our systems, software and networks nevertheless may be vulnerable to unauthorized access, misuse, computer viruses or other malicious code and other events that could have a security impact. An interception, misuse or mishandling of personal, confidential or proprietary information sent to or received from a client, vendor, service provider, counterparty or third party could result in legal liability, regulatory action and reputational harm. Although we have not experienced any material losses to date relating to cyber attacks or other such security breaches, we have suffered losses from operational risk in the past, and there can be no assurance that we will not suffer material losses from operational risk in the future. Further, as cyber attacks continue to evolve, we may incur significant costs in our attempt to modify or enhance our protective measures or investigate or remediate any vulnerabilities.

In addition, there have been a number of highly publicized cases around the world involving actual or alleged fraud or other misconduct by employees in the financial services industry in recent years and we run the risk that employee misconduct could occur. This misconduct has included and may include in the future the theft of proprietary information, including proprietary software. It is not always possible to deter or prevent employee misconduct and the precautions we take to prevent and detect this activity have not been and may not be effective in all cases.

We rely on recruiting, retaining and developing appropriate senior management and skilled personnel.

Our continued success depends in part on the continued service of key members of our management team. The ability to continue to attract, train, motivate and retain highly qualified professionals is a key element of our strategy. The successful implementation of our growth strategy depends on the availability of skilled management, both at our head office and at each of our business units. If we or one of our business units or other functions fails to staff our operations appropriately or loses one or more of our key senior executives and fails to replace them in a satisfactory and timely manner, our business, results of operations and financial condition, including control and operational risks, may be adversely affected.

In addition, the financial industry has and may continue to experience more stringent regulation of employee compensation, which could have an adverse effect on our ability to hire or retain the most qualified employees. If we fail or are unable to attract and appropriately train, motivate and retain qualified professionals, our business may also be adversely affected.

Damage to our reputation could cause harm to our business prospects.

Maintaining a positive reputation is critical to our attracting and maintaining customers, investors and employees. Damage to our reputation can therefore cause significant harm to our business and prospects. Harm to our reputation can arise from numerous sources, including, among others, employee misconduct, litigation or regulatory outcomes, failure to deliver minimum standards of service and quality, compliance failures, unethical behavior, and the activities of customers and counterparties. Further, negative publicity regarding us, whether or not true, may harm our business prospects.

Actions by the financial services industry generally or by certain members of, or individuals in, the industry can also affect our reputation. For example, the role played by financial services firms in the financial crisis and the seeming shift toward increasing regulatory supervision and enforcement has caused public perception of us and others in the financial services industry to decline.

19

We could suffer significant reputational harm if we fail to properly identify and manage potential conflicts of interest. Management of potential conflicts of interest has become increasingly complex as we expand our business activities through more numerous transactions, obligations and interests with and among our clients. The failure to adequately address, or the perceived failure to adequately address, conflicts of interest could affect the willingness of clients to deal with us, or give rise to litigation or enforcement actions against us. Therefore, there can be no assurance that conflicts of interest will not arise in the future that could cause material harm to us.

Different disclosure and accounting principles between Spain and the US may provide you with different or less information about us than you expect.