Management's Discussion and Analysis for the Year Ended December 31, 2010

Exhibit 99.2

Management’s Discussion & Analysis

|

|

|

| INDEX |

|

|

| 8 Overview of the

Business 10 Our Strategy

12 How We Analyze Our Business

13 Financial Highlights

13 Production Summary

15 Results of Operations

21 Liquidity and Capital Resources

27 Risk Factors and Risk Management |

|

35 Critical Accounting

Estimates 37 Anticipated Changes to Canadian Generally Accepted Accounting

Principles 45 Supplemental Non-GAAP Measures

46 Quarterly Financial Data (Unaudited)

46 Selected Annual Information

46 Controls and Procedures

47 Forward-Looking Statements |

This Management’s Discussion and Analysis is dated March 24, 2011 and should be read in conjunction with our consolidated financial statements and the

accompanying notes for the year ended December 31, 2010. Our consolidated financial statements are prepared in accordance with Canadian generally accepted accounting principles (Canadian GAAP). We use the United States dollar as our reporting

currency. Except where otherwise noted, all dollar amounts are stated in United States dollars.

Canadian GAAP differs in some respects from

accounting principles generally accepted in the United States (US GAAP). Significant differences between Canadian GAAP and US GAAP are described in note 20 to our consolidated financial statements. The Canadian Accounting Standards Board

confirmed January 1, 2011 as the changeover date for Canadian publicly accountable enterprises to start using International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). Accordingly, we

will issue our first interim consolidated financial statements in accordance with IFRS beginning with the first quarter ending March 31, 2011 with comparative financial results for 2010 (refer to the Anticipated Changes to Canadian Generally Accepted Accounting Principles section on page 37 for more information).

At March 18, 2011 we had 92,715,072 common shares issued and outstanding and stock options exercisable for 3,987,749 additional common shares.

Additional information relating to Methanex, including our Annual Information Form, is available on the Canadian Securities Administrators’ SEDAR website at

www.sedar.com and on the United States Securities and Exchange Commission’s EDGAR website at www.sec.gov.

OVERVIEW OF THE

BUSINESS

Methanol is a clear liquid commodity chemical that is predominantly produced from natural gas and also, particularly in China, from coal.

Approximately two-thirds of all methanol demand is used to produce traditional chemical derivatives including formaldehyde, acetic acid and a variety of other chemicals that form the basis of a large number of chemical derivatives for which demand

is influenced by levels of global economic activity. The remaining one-third of methanol demand comes from the energy sector. There has been strong demand growth for methanol in energy-related applications such as direct methanol blending into

gasoline and dimethyl ether (DME), which can be blended with liquefied petroleum gas for use in household cooking and heating, and also as a substitute for diesel. Methanol is also used to produce biodiesel and methyl tertiary butyl ether (MTBE), a

gasoline component.

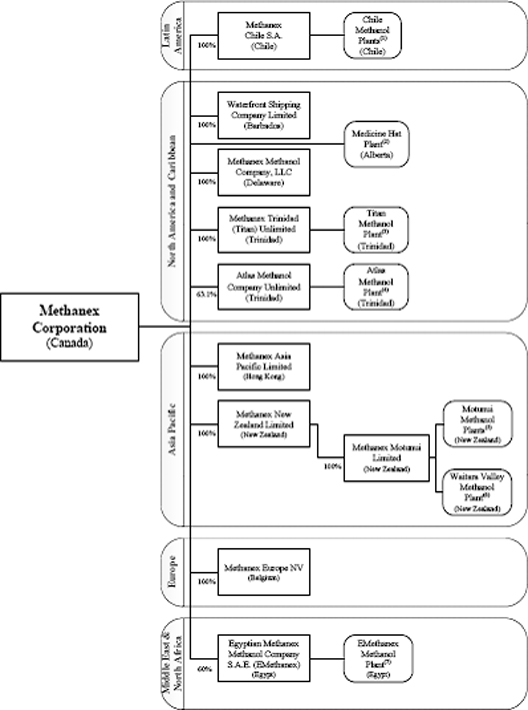

We are the world’s largest supplier of methanol to the major international markets of Asia Pacific, North America, Europe and

Latin America. Our total annual production capacity, including equity interests in jointly owned plants, is approximately 7.93 million tonnes and is located in Chile, Trinidad, New Zealand, Egypt and Canada (refer to the Production Summary section on page 13 for more information). We have marketing rights for 100% of the production from our jointly owned plants in Trinidad

and Egypt and this provides us with an additional 1.17 million tonnes per year of methanol offtake supply. In addition to the methanol produced at our sites, we purchase methanol produced by others under methanol

|

|

|

| |

|

| |

|

8 METHANEX

Annual Report 2010 Management’s Discussion & Analysis |

offtake contracts and on the spot market. This gives us flexibility in managing our supply chain while continuing to meet customer needs and support our marketing efforts.

2010 Industry Overview & Outlook

Methanol is a global commodity and our earnings are significantly affected by fluctuations in the price of methanol, which is directly impacted by the balance of

methanol supply and demand. Demand for methanol is driven primarily by levels of industrial production, energy prices and the strength of the global economy.

During 2010, the methanol industry experienced strong demand growth with total demand of approximately 45 million tonnes, representing a 13% increase over 2009. The increase in demand was driven primarily by

demand for both traditional and energy-related derivatives in Asia, particularly China. There were also increases in demand for traditional methanol derivatives in other regions, including Europe, Latin America and North America.

Energy-related derivatives currently represent approximately one-third of global methanol demand, and over the last few years high energy prices have driven strong

demand growth for methanol into energy applications such as gasoline blending and DME in China. During 2010, methanol blending into gasoline in China was particularly strong and continues to be supported by standards introduced by national and

provincial governments. There are a number of provincially sponsored programs for methanol fuel blending and more are under development. In 2009, national standards were introduced for the use of M85 and M100 (85 percent and 100 percent methanol

blends) and we expect the Government of China to introduce an M15 national standard in 2011, which should be a further catalyst to grow methanol fuel blending in China. China is currently the largest energy and automobile market in the world and, as

a developing country, the per capita use of automobiles and the demand for transportation fuels is expected to grow significantly over time. DME demand in China in 2010 was also strong and ended the year at record levels.

The methanol industry conditions were balanced to tight in 2010, underpinned by strong global methanol demand growth and supply constraints. While three new

world-scale plants (in Brunei, Oman and Venezuela) with combined capacity totalling 2.8 million tonnes per year started up in 2010, there were also some shut-ins of higher cost capacity and a number of planned and unplanned plant outages across

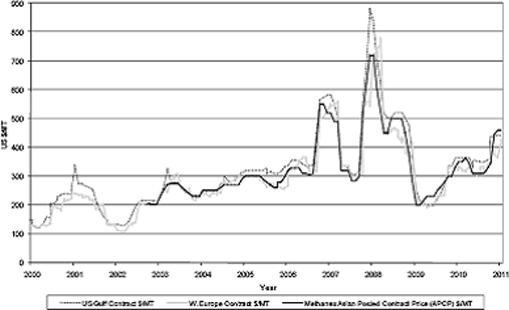

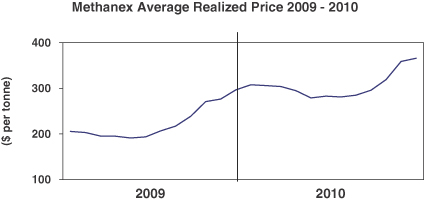

the industry. These factors, combined with the continuing higher energy price environment, led to balanced to tight market conditions and a strong methanol pricing environment throughout 2010. Our average non-discounted price in 2010 was $356 per

tonne compared with $252 per tonne in 2009, and our average realized price for 2010 was $306 per tonne compared with $225 per tonne in 2009.

Going

forward, with China continuing to demonstrate the success of methanol for use in energy, other countries are also considering the use of methanol in energy applications. Australia, Iran, Pakistan and Malaysia are currently studying the use of

methanol in gasoline, and we are involved in a project to test methanol fuel blending in Trinidad. We are also working with several producers of renewable methanol to help develop markets that recognize the unique characteristics of methanol

produced from renewable feedstock. Finally, there is also potential for growth in the DME industry outside China, with Indonesia, Japan, Sweden, Iran, Egypt and India all studying or developing DME projects.

Another recent development that is also being led by China is the use of methanol to produce olefins, with the first commercial methanol-to-olefins plant starting

up in Baotou in 2010. Historically, we have viewed these projects as fully integrated and therefore having little impact on the merchant methanol market. However, some projects are now being considered that require the purchase of merchant methanol.

These methanol-to-olefin projects consume a significant amount of methanol and there are a number of projects under development in several countries. This industry could therefore have a significant impact on future demand for merchant methanol.

We anticipate a significant increase in our production capacity in 2011 from the 1.26 million tonne per year Egypt plant and the restart of our

0.47 million tonne per year Medicine Hat facility. We also are focused on accessing natural gas to increase production at our existing sites in Chile and New Zealand over the next few years (refer to the Production Summary section on page 13 for more information). Beyond our own capacity additions, there are few global methanol capacity additions outside

China expected over the next few years. There is a 0.85 million tonne plant in Beaumont, Texas and a 0.7 million tonne plant in Azerbaijan and we anticipate that product from both of these plants will enter the market over the 2012-2013

period.

|

|

|

| |

|

| Management’s Discussion & Analysis Annual Report 2010 METHANEX 9

|

|

|

Global methanol demand continues to be strong, supported by continuing growth of methanol into energy applications,

and further recovery of global economies should lead to increased demand for traditional methanol derivatives. With few capacity additions expected to enter the market over the next few years, we believe we are well positioned with anticipated

production increases from our existing sites. As production from these sites comes on line, we believe our leadership position in the industry will be strengthened, the overall cost position of our assets will be improved and we will have

significant upside potential to our cash flows and earnings.

The methanol price will ultimately depend on the strength of the economic recovery,

industry operating rates, global energy prices, the rate of industry restructuring and the strength of global demand. We believe that our financial position and financial flexibility, outstanding global supply network and competitive cost position

will provide a sound basis for Methanex to continue to be the leader in the methanol industry and to invest to grow the Company.

OUR

STRATEGY

Our primary objective is to create value by maintaining and enhancing our leadership in the global production, marketing and delivery of

methanol to our customers. Our simple, clearly defined strategy – global leadership, low cost and operational excellence – has helped us achieve this objective.

Global Leadership

Global Leadership is a key element of our strategy, with a focus on

maintaining and enhancing our position as the major supplier to the global methanol industry, enhancing our ability to cost-effectively deliver methanol supply to our customers and supporting global methanol demand growth for both traditional and

energy-related methanol derivatives.

We are the leading supplier of methanol to the major international markets of North America, Asia Pacific, Europe

and Latin America. Our sales volumes in 2010 represented approximately 15% of total global methanol demand and we grew sales volumes by 16% from 5.95 million tonnes in 2009 to 6.93 million tonnes in 2010. Our leadership position has

enabled us to play an important role in the industry, which includes publishing Methanex reference prices that are generally used in each major market as the basis of pricing for most of our customer contracts and which we believe enhances market

transparency.

The geographically diverse location of our production sites allows us to deliver methanol cost-effectively to customers in all major

global markets, while our global distribution and supply infrastructure, which includes a dedicated fleet of ocean-going vessels and terminal capacity within all major international markets, enables us to enhance value to customers by providing

reliable and secure supply.

A key component of our Global Leadership strategy is a focus on strengthening our asset position and increasing production

at our sites. We expect increased production in 2011 with the start-up of production from the 1.26 million tonne per year methanol plant in Egypt and the restart of our 0.47 million tonne per year Medicine Hat, Alberta plant. Both of these

sites are well located and will provide additional security of supply for our customers. Our methanol facilities in Chile represent 3.8 million tonnes of annual production capacity and since mid-2007 we have operated the site significantly

below capacity. This is primarily due to curtailments of natural gas supply from Argentina (refer to the Production Summary – Chile section

on page 14). Our goal is to progressively increase production at our Chile site with natural gas from suppliers in Chile by supporting the acceleration of natural gas development in southern Chile. We are also focused on accessing additional

natural gas supply to increase production in New Zealand, where we currently have approximately 1.35 million tonnes of annual idled production capacity.

Another key component of our Global Leadership strategy is our ability to supplement our methanol production with methanol purchases from others to give us flexibility in our supply chain and continue to meet

customer commitments. We purchase through a combination of methanol offtake contracts and spot purchases. We manage the cost of purchased methanol by taking advantage of our global supply chain infrastructure, which allows us to purchase methanol in

the most cost-effective region while still maintaining overall security of supply. We grew our sales and purchasing levels in 2010 in anticipation of increased production from the Egypt plant. However, we expect purchased methanol will represent a

lower proportion of our overall sales volumes with increased production in Egypt and Canada in 2011.

|

|

|

| |

|

| |

|

10 METHANEX

Annual Report 2010 Management’s Discussion & Analysis |

The Asia Pacific region continues to lead global methanol demand growth and we have invested in and developed our

presence in this important region. We have storage capacity in China and Korea that allows us to cost-effectively manage supply to customers in this region. We have offices in Hong Kong, Shanghai, Beijing, Korea and Japan to enhance customer service

and industry positioning in the region. This also enables us to participate in and improve our knowledge of the rapidly evolving and high growth methanol market in China and other Asian countries. Our expanding presence in Asia has also helped us

identify several opportunities to support the development of applications for methanol in the energy sector.

With China continuing to demonstrate the

success of methanol for use in energy markets, other countries are also considering the use of methanol in energy applications and we are involved in a project to test methanol fuel blending in Trinidad. We are also working with several producers of

renewable methanol to help develop markets that recognize the unique characteristics of methanol produced from renewable feedstock. We also continued to advance our joint venture DME project in Egypt.

Low Cost

A low cost structure is an

important element of competitive advantage in a commodity industry and is a key element of our strategy. Our approach to major business decisions is guided by our drive to improve our cost structure, expand margins and return value to shareholders.

The most significant components of our costs are natural gas for feedstock and distribution costs associated with delivering methanol to customers.

Our

production facilities in Trinidad represent 2.05 million tonnes per year of competitive cost production capacity. These facilities are well located to supply markets in North America and Europe and are underpinned by take-or-pay natural gas

purchase agreements where the gas price varies with methanol prices.

As described above, we expect an increase in our production capability in 2011 from

the new methanol plant in Egypt and the restart of our Medicine Hat, Alberta plant. We also are focused on accessing natural gas to increase production at our existing sites in Chile and New Zealand. We believe these initiatives will further enhance

our competitive cost structure and our ability to cost-effectively deliver methanol to customers (refer to the Production Summary section on

page 13 for more information on all of our production sites).

The cost to distribute methanol from production facilities to customers is also a

significant component of our operating costs. These include costs for ocean shipping, in-market storage facilities and in-market distribution. We are focused on identifying initiatives to reduce these costs, including optimizing the use of our

shipping fleet to reduce costs and taking advantage of prevailing conditions in the shipping market by varying the type and length of term of ocean vessel contracts. We are continuously investigating opportunities to further improve the efficiency

and cost-effectiveness of distributing methanol from our production facilities to customers. We also look for opportunities to leverage our global asset position by entering into product exchanges with other methanol producers to reduce distribution

costs.

Operational Excellence

We maintain a focus on operational excellence in all aspects of our business. This includes excellence in our manufacturing and supply chain processes, marketing

and sales, human resources, corporate governance practices and financial management.

To differentiate ourselves from our competitors, we strive to be

the best operator in all aspects of our business and to be the preferred supplier to customers. We believe that reliability of supply is critical to the success of our customers’ businesses and our goal is to deliver methanol reliably and

cost-effectively. We have a commitment to Responsible Care (a risk-minimization approach developed by the Chemistry Industry Association of Canada) and we use it as the umbrella under which we manage issues related to health, safety, the

environment, community involvement, social responsibility, security and emergency preparedness at each of our facilities and locations. We believe our commitment to Responsible Care helps us reduce the likelihood of unplanned shutdowns and safety

incidents and achieve an excellent overall environmental record. In 2010 we experienced no employee recordable injuries across the organization as well as improvement in contractor safety performance, resulting in overall safety performance that

exceeds the Canadian industry average for comparable companies.

|

|

|

| |

|

| Management’s Discussion & Analysis Annual Report 2010 METHANEX 11

|

|

|

Product stewardship is a vital component of our Responsible Care culture and guides our actions through the complete

life cycle of our product. We aim for the highest safety standards to minimize risk to our employees, customers and suppliers as well as to the environment and the communities in which we do business. We promote the proper use and safe handling of

methanol at all times through a variety of internal and external health, safety and environmental initiatives, and we work with industry colleagues to improve safety standards and regulatory compliance. We readily share our technical and safety

expertise with key stakeholders, including customers, end-users, suppliers, logistics providers and industry associations in the methanol and methanol applications marketplace through active participation in local and international industry seminars

and conferences, and online education initiatives.

As a natural extension of our Responsible Care ethic, we have a Social Responsibility policy that

aligns our corporate governance, employee engagement and development, community involvement and social investment strategies with our core values and corporate strategy.

Our strategy of operational excellence includes the financial management of the Company. We operate in a highly competitive commodity industry. Accordingly, we believe it is important to maintain financial

flexibility and we have adopted a prudent approach to financial management. At December 31, 2010, we had a strong balance sheet with a cash balance of $194 million, a $200 million undrawn credit facility and no re-financing requirements until

mid-2012. We believe we are well positioned to meet our financial commitments and continue investing to grow our business.

HOW WE

ANALYZE OUR BUSINESS

Our operations consist of a single operating segment – the production and sale of methanol. We review our results of

operations by analyzing changes in the components of our adjusted earnings before interest, taxes, depreciation and amortization (Adjusted EBITDA) (refer to the Supplemental Non-GAAP

Measures section on page 45 for a reconciliation to the most comparable GAAP measure), depreciation and amortization, interest expense, interest and other income, and income taxes. In addition

to the methanol that we produce at our facilities (“Methanex-produced methanol”), we also purchase and re-sell methanol produced by others (“purchased methanol”) and we sell methanol on a commission basis. We analyze the results

of all methanol sales together. The key drivers of change in our Adjusted EBITDA are average realized price, cash costs and sales volume.

The price,

cash cost and volume variances included in our Adjusted EBITDA analysis are defined and calculated as follows:

|

|

|

| PRICE |

|

The change in Adjusted EBITDA as a result of changes in average realized price is calculated as the difference from

period to period in the selling price of methanol multiplied by the current period total methanol sales volume excluding commission sales volume plus the difference from period to period in commission revenue. |

| CASH COST |

|

The change in our Adjusted EBITDA as a result of changes in cash costs is calculated as the difference from period to period in cash costs per tonne

multiplied by the current period total methanol sales volume excluding commission sales volume in the current period. The cash costs per tonne is the weighted average of the cash cost per tonne of Methanex-produced methanol and the cash cost per

tonne of purchased methanol. The cash cost per tonne of Methanex-produced methanol includes absorbed fixed cash costs per tonne and variable cash costs per tonne. The cash cost per tonne of purchased methanol consists principally of the cost of

methanol itself. In addition, the change in our Adjusted EBITDA as a result of changes in cash costs includes the changes from period to period in unabsorbed fixed production costs, consolidated selling, general and administrative expenses and fixed

storage and handling costs. |

| VOLUME |

|

The change in Adjusted EBITDA as a result of changes in sales volume is calculated as the difference from period to period in total methanol sales

volume excluding commission sales volumes multiplied by the margin per tonne for the prior period. The margin per tonne for the prior period is the weighted average margin per tonne of Methanex-produced methanol and margin per tonne of purchased

methanol. The margin per tonne for Methanex-produced methanol is calculated as the selling price per tonne of methanol less absorbed fixed cash costs per tonne and variable cash costs per tonne. The margin per tonne for purchased methanol is

calculated as the selling price per tonne of methanol less the cost of purchased methanol per tonne. |

|

|

|

| |

|

| |

|

12 METHANEX

Annual Report 2010 Management’s Discussion & Analysis |

We also sell methanol on a commission basis. Commission sales represent volumes marketed on a commission basis related

to the 36.9% of the Atlas methanol facility in Trinidad that we do not own.

FINANCIAL HIGHLIGHTS

|

|

|

|

|

|

|

|

|

| ($ MILLIONS, EXCEPT WHERE NOTED) |

|

2010 |

|

|

2009 |

|

| Production (thousands of tonnes): |

|

|

3,540 |

|

|

|

3,543 |

|

| Sales volumes (thousands of tonnes): |

|

|

|

|

|

|

|

|

| Produced methanol |

|

|

3,540 |

|

|

|

3,764 |

|

| Purchased methanol |

|

|

2,880 |

|

|

|

1,546 |

|

| Commission

sales1 |

|

|

509 |

|

|

|

638 |

|

| Total sale volumes |

|

|

6,929 |

|

|

|

5,948 |

|

| Methanex average non-discounted posted price ($ per

tonne)2 |

|

|

356 |

|

|

|

252 |

|

| Average realized price ($ per tonne)3 |

|

|

306 |

|

|

|

225 |

|

| Revenue |

|

|

1,967 |

|

|

|

1,198 |

|

| Adjusted EBITDA4 |

|

|

267 |

|

|

|

142 |

|

| Cash flows from operating activities |

|

|

153 |

|

|

|

110 |

|

| Cash flows from operating activities before changes in non-cash working capital |

|

|

252 |

|

|

|

129 |

|

| Net income |

|

|

102 |

|

|

|

1 |

|

| Net income before unusual items4 |

|

|

80 |

|

|

|

1 |

|

| Basic net income per common share ($ per share) |

|

|

1.10 |

|

|

|

0.01 |

|

| Diluted net income per common share ($ per share) |

|

|

1.09 |

|

|

|

0.01 |

|

| Diluted net income per common share before unusual item ($ per

share)4 |

|

|

0.85 |

|

|

|

0.01 |

|

| Common share information (millions of shares): |

|

|

|

|

|

|

|

|

| Weighted average number of common shares outstanding |

|

|

92 |

|

|

|

92 |

|

| Diluted weighted average number of common shares outstanding |

|

|

94 |

|

|

|

93 |

|

| Number of common shares outstanding |

|

|

93 |

|

|

|

92 |

|

| 1 |

Commission sales represent volumes marketed on a commission basis. Commission income is included in revenue when earned. |

| 2 |

Methanex average non-discounted posted price represents the average of our non-discounted posted prices in North America, Europe and Asia Pacific weighted by

sales volume. Current and historical pricing information is available on our website at www.methanex.com. |

| 3 |

Average realized price is calculated as revenue, net of commission income, divided by total sales volumes of produced and purchased methanol.

|

| 4 |

These items are non-GAAP measures that do not have any standardized meaning prescribed by Canadian Generally Accepted Accounting Principles (GAAP) and therefore

are unlikely to be comparable to similar measures presented by other companies. Refer to the Supplemental Non-GAAP Measures section on page 45 for a description of each non-GAAP measure and a reconciliation to the most comparable GAAP measure.

|

PRODUCTION SUMMARY

The following table details the annual production capacity and actual production of our facilities that operated in 2010 and 2009:

|

|

|

|

|

|

|

|

|

|

|

|

|

| (THOUSANDS OF TONNES) |

|

ANNUAL

PRODUCTION

CAPACITY1 |

|

|

2010 |

|

|

2009 |

|

| Chile I, II, III and IV |

|

|

3,800 |

|

|

|

935 |

|

|

|

942 |

|

| Atlas (Trinidad) (63.1% interest) |

|

|

1,150 |

|

|

|

884 |

|

|

|

1,015 |

|

| Titan (Trinidad) |

|

|

900 |

|

|

|

891 |

|

|

|

764 |

|

| New Zealand2 |

|

|

850 |

|

|

|

830 |

|

|

|

822 |

|

| Egypt (60% interest)3 |

|

|

760 |

|

|

|

– |

|

|

|

– |

|

| Medicine

Hat3 |

|

|

470 |

|

|

|

– |

|

|

|

– |

|

| |

|

|

7,930 |

|

|

|

3,540 |

|

|

|

3,543 |

|

| 1 |

The annual production capacity of our production facilities may be higher than original nameplate capacity as, over time, these figures have been adjusted to

reflect ongoing operating efficiencies at these facilities. |

| 2 |

The annual production capacity of New Zealand represents only our 0.85 million tonne per year Motunui facility that we restarted in late 2008. Practical

operating capacity will depend partially on the composition of natural gas feedstock and may differ from the stated capacity above. We also have additional potential production capacity that is currently idled in New Zealand (refer to the New Zealand section on page 14 for more information). |

| 3 |

These two plants are anticipated to commence production in 2011. The Egypt methanol facility produced first methanol in January 2011 and we are nearing

completion of the restart of our Medicine Hat, Alberta facility (refer to the Egypt and

Medicine Hat sections on page 15 for more information). |

|

|

|

| |

|

| Management’s Discussion & Analysis Annual Report 2010 METHANEX 13

|

|

|

Chile

Our methanol facilities in Chile produced 0.94 million tonnes of methanol in 2010 and 2009. Since 2007, we have operated our methanol facilities in Chile significantly below site capacity primarily due to

curtailments of natural gas supply from Argentina. In June 2007, our natural gas suppliers from Argentina curtailed all gas supply to our plants in Chile in response to various actions by the Argentinean government, including imposing a large

increase to the duty on natural gas exports. Under the current circumstances, we do not expect to receive any further natural gas supply from Argentina. As a result of the Argentinean natural gas supply issues, all of the methanol production at our

Chile facilities since June 2007 has been produced with natural gas from Chile.

Our goal is to progressively increase production at our Chile site with

natural gas from suppliers in Chile. We are pursuing investment opportunities with the state-owned energy company Empresa Nacional del Petroleo (ENAP), GeoPark Chile Limited (GeoPark) and others to help accelerate natural gas exploration and

development in southern Chile. We are working with ENAP to develop natural gas in the Dorado Riquelme block in southern Chile. Under the arrangement, we fund a 50% participation in the block and, as at December 31, 2010, we had contributed

approximately $86 million. Over the past few years, we have also provided $57 million in financing to GeoPark (of which approximately $32 million had been repaid at December 31, 2010) to support and accelerate GeoPark’s natural gas

exploration and development activities in southern Chile. GeoPark has agreed to supply us with all natural gas sourced from the Fell block in southern Chile under a ten-year exclusive supply arrangement that commenced in 2008. Approximately 60% of

total production at our Chilean facilities is currently being produced with natural gas supplied from the Fell and Dorado Riquelme blocks.

Other

investment activities are also supporting the acceleration of natural gas exploration and development in areas of southern Chile. In late 2007, the Government of Chile completed an international bidding round to assign oil and natural gas

exploration areas that lie close to our production facilities and announced the participation of several international oil and gas companies. The terms of the agreements from the bidding round require minimum investment commitments. To date, two

companies that participated in the bidding round have advised of gas discoveries and we expect first deliveries of gas from these new finds in 2011. We are participating in a consortium for two exploration blocks under this bidding round – the

Tranquilo and Otway blocks. The consortium includes Wintershall, GeoPark and Pluspetrol each having 25% participation and International Finance Corporation, member of the World Bank Group, and Methanex each having 12.5% participation. GeoPark is the

operator of both blocks.

Our methanol facilities in Chile produced 0.94 million tonnes of methanol in both 2010 and 2009. During 2010, natural gas

deliveries from ENAP were lower than 2009 primarily as a result of declines in deliverability from existing wells and this was offset by increased natural gas deliveries from the Dorado Riquelme block in 2010 compared with 2009. As we entered 2011,

we were operating one plant at approximately 65% capacity at our Chile site and the short-term outlook for gas supply in Chile continues to be challenging. While significant investments have been made in the last few years for natural gas

exploration and development in southern Chile, the timelines for a significant increase in gas deliveries to our plants are much longer than we originally anticipated. As a result, we expect there to be short-term pressure on gas supply in southern

Chile that could impact the operating rate of our Chile site, particularly in the southern hemisphere winter months when residential energy demand is at its peak.

Refer to the Risk Factors and Risk Management – Chile section on page 27 for more information.

Trinidad

Our equity ownership

of methanol facilities in Trinidad represents approximately 2.05 million tonnes of competitive cost annual capacity. The Titan and Atlas facilities in Trinidad are well located to supply markets in North America and Europe and are underpinned

by take-or-pay natural gas purchase agreements that expire in 2014 and 2024, respectively, where the gas price varies with methanol prices. These facilities produced a total of 1.78 million tonnes in both 2010 and 2009. For both 2010 and 2009,

we operated these facilities at below operating capacity due to planned and unplanned maintenance activities. During 2010, we experienced an outage at our Atlas facility that lasted approximately 60 days.

New Zealand

Our New Zealand facilities

provide competitive cost capacity and are underpinned by shorter term natural gas supply contracts. For both 2010 and 2009, we produced 0.83 million tonnes from one 0.85 million tonne per year plant at our Motunui facility in New Zealand.

We have natural gas contracts with a number of gas suppliers that will allow us to

|

|

|

| |

|

| |

|

14 METHANEX

Annual Report 2010 Management’s Discussion & Analysis |

continue to operate the 0.85 million tonne per year Motunui plant through 2012. We also have an additional 1.38 million tonnes per year of idled capacity in New Zealand, including a second

0.85 million tonne per year Motunui plant and a 0.53 million tonne per year plant at our nearby site in Waitara Valley. These facilities provide the potential to increase production in New Zealand depending on the methanol supply and demand

dynamics and the availability of economically priced natural gas feedstock.

We believe there has been continued improvement in the natural gas supply

outlook in New Zealand and we are focused on accessing additional natural gas supply to increase production in New Zealand. We continue to pursue opportunities to obtain economically priced natural gas with suppliers in New Zealand to underpin a

restart of a second plant. We are also pursuing natural gas exploration and development opportunities in the area close to our plants with the objective of obtaining long-term competitively priced supply. During 2010, we entered into an agreement

with Kea Exploration (Kea), an oil and gas exploration and development company, to explore areas of the Taranaki basin in New Zealand close to our plants. Under the agreement, funding will be shared 50% by both parties, and we will be entitled to

all natural gas deliveries from our participation at a price that is competitive to our other locations in Trinidad, Chile and Egypt. During 2010, we spent approximately $10 million on exploration activities with Kea. Under the agreement, there are

no minimum investment commitments and future contributions will be agreed by the parties on an ongoing basis.

Egypt

The new 1.26 million tonne per year methanol plant in Egypt is in the commissioning phase and produced first methanol in January 2011. The start-up coincided

with widespread anti-government protests and civil unrest in Egypt. For the safety and security of our employees, we took the decision to temporarily close our Cairo office and curtail the commissioning activities at the plant in Damietta, Egypt. As

conditions stabilized, we reopened our Cairo office and our plant in Damietta resumed operations to continue the start-up and commissioning process.

We

have a 60% interest in the facility and have marketing rights for 100% of the production. This facility is underpinned by a 25-year take-or-pay natural gas purchase agreement where the gas price varies with methanol prices. We believe this methanol

facility will further enhance our cost structure and our market position and it is well located to supply the European market.

Medicine Hat

In September 2010, we made the

decision to restart the 0.47 million tonne per year idled facility in Medicine Hat, Alberta, Canada. In support of the restart, we commenced a program to purchase natural gas on the Alberta gas market, and by the end of 2010 we had contracted

sufficient volumes of natural gas to meet approximately 80% of our requirements when operating at capacity for the period from start-up to October 2012. We are nearing completion of this restart project with production expected to commence in the

second quarter of 2011.

RESULTS OF OPERATIONS

|

|

|

|

|

|

|

|

|

| ($ MILLIONS) |

|

2010 |

|

|

2009 |

|

| Consolidated statements of income: |

|

|

|

|

|

|

|

|

| Revenue |

|

$ |

1,967 |

|

|

$ |

1,198 |

|

| Cost of sales and operating expenses |

|

|

(1,700 |

) |

|

|

(1,056 |

) |

| Adjusted EBITDA1 |

|

|

267 |

|

|

|

142 |

|

| Gain on sale of Kitimat assets |

|

|

22 |

|

|

|

– |

|

| Depreciation and amortization |

|

|

(131 |

) |

|

|

(118 |

) |

| Operating income1 |

|

|

158 |

|

|

|

24 |

|

| Interest expense |

|

|

(24 |

) |

|

|

(27 |

) |

| Interest and other income |

|

|

2 |

|

|

|

– |

|

| Income tax recovery (expense) |

|

|

(34 |

) |

|

|

4 |

|

| Net income |

|

$ |

102 |

|

|

$ |

1 |

|

| 1 |

These items are non-GAAP measures that do not have any standardized meaning prescribed by Canadian GAAP and therefore are unlikely to be comparable to similar

measures presented by other companies. Refer to the Supplemental Non-GAAP Measures section on page 45 for a description of each non-GAAP

measure and a reconciliation to the most comparable GAAP measure. |

|

|

|

| |

|

| Management’s Discussion & Analysis Annual Report 2010 METHANEX 15

|

|

|

For the year ended December 31, 2010, we recorded Adjusted EBITDA of $267 million and net income of $102 million

($1.09 per share on a diluted basis) and net income of $80 million ($0.85 per share on a diluted basis) before an after-tax gain of $22 million related to the sale of land and terminal facilities in Kitimat, Canada. This compares with Adjusted

EBITDA of $142 million and net income of $1 million ($0.01 per share on a diluted basis) for the year ended December 31, 2009.

The following

discussion on pages 16 – 20 provides a description of changes in revenue, Adjusted EBITDA, depreciation and amortization, interest expense, interest and other income, and income taxes for 2010 compared with 2009.

Revenue

There are many factors that impact

our global and regional revenue levels. The methanol business is a global commodity industry affected by supply and demand fundamentals. Due to the diversity of the end products in which methanol is used, demand for methanol largely depends upon

levels of industrial production, the value of energy and changes in general economic conditions, which can vary across the major international methanol markets.

Revenue for 2010 was $2.0 billion compared with $1.2 billion in 2009. The increase in revenue was primarily due to higher methanol

pricing and increased sales volumes in 2010 compared with 2009.

Entering 2010, global methanol demand had recovered to pre-recession levels. During

2010, global methanol demand was 45 million tonnes, a 13% increase over 2009. This was primarily driven by demand growth for both traditional and energy-related derivatives in Asia (particularly China). There were also increases in demand for

traditional methanol derivatives in other regions, including Europe, Latin America and North America. In anticipation of the start-up of the new methanol plant in Egypt, we grew our total sales volumes by approximately 16%, from 5.95 million

tonnes in 2009 to 6.93 million tonnes in 2010, and this increased our revenues by approximately $0.2 billion.

Methanol industry conditions were

balanced to tight in 2010, underpinned by strong global demand growth and supply constraints. While three new world-scale plants (in Brunei, Oman and Venezuela) with combined capacity totalling 2.8 million tonnes per year started up in 2010,

there were also some shut-ins of higher cost capacity and a number of planned and unplanned plant outages across the industry. These factors, combined with the continuing higher energy price environment, led to tight market conditions and a strong

methanol pricing environment throughout 2010. Our average realized price in 2010 was $306 per tonne compared with $225 per tonne in 2009, and this increased our revenues by approximately $0.6 billion.

The methanol industry is highly competitive and prices are affected by supply and demand fundamentals. We publish non-discounted reference prices for each major

methanol market and offer discounts to customers based on various factors. Our average non-discounted published reference price for 2010 was $356 per tonne compared with $252 per tonne in 2009. Our average realized price was approximately 14% and

11% lower than our average non-discounted published reference price for 2010 and 2009, respectively.

We have entered into long-term contracts for a

portion of our production volume with certain global customers where prices are either fixed or linked to costs plus a margin. Sales under these contracts represented approximately 8% of our total sales volumes in 2010 compared with 19% of our total

sales volumes in 2009. The difference between our average non-discounted published reference price and our average realized price is expected to narrow during periods of lower pricing.

|

|

|

| |

|

| |

|

16 METHANEX

Annual Report 2010 Management’s Discussion & Analysis |

Distribution of Revenue

The distribution of revenue for 2010 and 2009 is as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ($ MILLIONS, EXCEPT WHERE NOTED) |

|

2010 |

|

|

2009 |

|

| Canada |

|

$ |

142 |

|

|

|

7 |

% |

|

$ |

106 |

|

|

|

9 |

% |

| United States |

|

|

470 |

|

|

|

24 |

% |

|

|

355 |

|

|

|

30 |

% |

| Europe |

|

|

454 |

|

|

|

23 |

% |

|

|

198 |

|

|

|

17 |

% |

| China |

|

|

351 |

|

|

|

18 |

% |

|

|

195 |

|

|

|

16 |

% |

| Korea |

|

|

216 |

|

|

|

11 |

% |

|

|

136 |

|

|

|

11 |

% |

| Other Asia |

|

|

127 |

|

|

|

6 |

% |

|

|

83 |

|

|

|

7 |

% |

| Latin America |

|

|

207 |

|

|

|

11 |

% |

|

|

125 |

|

|

|

10 |

% |

| |

|

$ |

1,967 |

|

|

|

100 |

% |

|

$ |

1,198 |

|

|

|

100 |

% |

The primary changes in

the distribution of our revenue in 2010 compared with 2009 were an increase in the proportion of revenues earned in Europe and Asia and a decrease in the proportion of revenues earned in North America. This is primarily due to growth in sales

volumes in Europe and China, with sales volumes remaining relatively flat in North America in 2010 compared with 2009. Revenue in Europe increased as a proportion of our total revenue in 2010 compared with 2009 by 6%, primarily as a result of our

initiative to grow sales in this region in anticipation of the start-up of the 1.26 million tonne per year methanol facility in Egypt. We also grew sales volumes in China, resulting in a 2% increase in the proportion of total revenue earned in

China in 2010 compared with 2009. China continues to play an important role in the methanol industry as a substantial producer and consumer. A key part of our global leadership strategy is to increase our presence in China and the Asia Pacific

region.

Adjusted EBITDA

We

review our results of operations by analyzing changes in the components of Adjusted EBITDA. In addition to the methanol that we produce at our facilities, we also purchase and re-sell methanol produced by others and we sell methanol on a commission

basis. We analyze the results of all methanol sales together. The key drivers of change in our Adjusted EBITDA are average realized price, sales volume and cash costs (refer to the How We Analyze

Our Business section on page 12 for more information).

2010 Adjusted EBITDA was $267 million

compared with $142 million in 2009. The increase in Adjusted EBITDA of $125 million resulted from changes in the following:

|

|

|

|

|

| ($ MILLIONS) |

|

2010 VS. 2009 |

|

| Average realized price |

|

$ |

520 |

|

| Sales volume |

|

|

62 |

|

| Total cash

costs1 |

|

|

(457 |

) |

| Increase in Adjusted EBITDA |

|

$ |

125 |

|

| 1 |

Includes cash costs related to both Methanex-produced methanol and purchased methanol, as well as consolidated selling, general and administrative expenses and

fixed storage and handling costs. |

Average Realized Price

Our average realized price for the year ended December 31, 2010 was $306 per tonne compared with $225 per tonne for 2009, and this increased our revenues by

$520 million (refer to the Revenue section on page 16 for more information).

Sales Volumes

Total methanol sales volumes, excluding commission sales volumes, for the year

ended December 31, 2010 were 1.11 million tonnes higher than in 2009, which resulted in higher Adjusted EBITDA of $62 million.

Total Cash Costs

The primary driver of

changes in our total cash costs are changes in the cost of methanol we produce at our facilities and changes in the cost of methanol we purchase from others. Our production facilities are underpinned by natural gas purchase agreements with pricing

terms that include base and variable price components. We supplement our production with methanol produced by others through methanol offtake contracts and purchases on the spot market to meet

|

|

|

| |

|

| Management’s Discussion & Analysis Annual Report 2010 METHANEX 17

|

|

|

customer needs and support our marketing efforts within the major global markets. We have adopted the first-in, first-out method of accounting for inventories and it generally takes between 30

and 60 days to sell the methanol we produce or purchase. Accordingly, the changes in Adjusted EBITDA as a result of changes in natural gas costs and purchased methanol costs will depend on changes in methanol pricing and the timing of inventory

flows.

Cash costs for produced methanol and purchased methanol were $457 million higher in 2010 than in 2009. The primary changes in cash costs were as

follows:

|

|

|

|

|

| ($ MILLIONS) |

|

2010 VS. 2009 |

|

| Natural gas costs on sales of produced methanol |

|

$ |

98 |

|

| Purchased methanol costs |

|

|

223 |

|

| Proportion of purchased methanol sales |

|

|

90 |

|

| Stock-based compensation |

|

|

19 |

|

| Other, net |

|

|

27 |

|

| Increase in total cash costs |

|

$ |

457 |

|

Natural gas costs on sales of produced methanol

Natural gas is the primary feedstock at our

methanol production facilities and is the most significant component of our cost structure. The natural gas supply contracts for our production facilities in Chile, Trinidad and New Zealand include base and variable price components to reduce our

commodity price risk exposure. The variable price component of each gas contract is adjusted by a formula related to methanol prices above a certain level. We believe this pricing relationship enables these facilities to be competitive throughout

the methanol price cycle. The higher average methanol prices in 2010 increased our natural gas costs per tonne for produced methanol and this increased cash costs by approximately $98 million compared with 2009. For additional information regarding

our natural gas agreements refer to the Summary of Contractual Obligations and Commercial Commitments section on page 24.

Purchased methanol costs

A key element of

our corporate strategy is global leadership, and as such we have built a leading market position in each of the major global markets where methanol is sold. We supplement our production with purchased methanol through methanol offtake contracts and

on the spot market to meet customer needs and support our marketing efforts within the major global markets. In structuring offtake agreements, we look for opportunities that provide synergies with our existing supply chain and market position. Our

strong global supply chain allows us to take advantage of unique opportunities to add value through logistics cost savings and purchase methanol in the lowest-cost region. The cost of purchased methanol consists principally of the cost of the

methanol itself, which is directly related to the price of methanol at the time of purchase. The higher average methanol prices in 2010 increased the cost of purchased methanol per tonne and this increased cash costs by approximately $223 million

compared with 2009.

Proportion of purchased methanol sales

The cost of purchased methanol is directly linked to the selling price for methanol at the time of purchase and the cost of purchased methanol is generally higher than the cost of produced methanol. Accordingly, an

increase in the proportion of purchased methanol sales results in an increase in our overall cost structure for a given period. The proportion of purchased methanol sales for the year ended December 31, 2010 was higher compared with 2009 and

this increased cash costs by $89 million. The increase in the proportion of purchased methanol sales in 2010 compared with 2009 was primarily due to the increase in sales volumes in anticipation of the start-up of the Egypt methanol facility. When

the Egypt and Medicine Hat methanol facilities commence production in 2011, we expect the proportion of purchased methanol to decrease.

Stock-based compensation

We grant

stock-based awards as an element of compensation. Stock-based awards granted include stock options, share appreciation rights or tandem share appreciation rights, deferred share units, restricted share units and performance share units.

|

|

|

| |

|

| |

|

18 METHANEX

Annual Report 2010 Management’s Discussion & Analysis |

For stock options, the cost is measured based on an estimate of the fair value at the date of grant and this

grant-date fair value is recognized as compensation expense over the related service period. Accordingly, stock-based compensation expense associated with stock options will not vary significantly from period to period. Commencing in 2010, we

granted share appreciation rights (SARs) and tandem share appreciation rights (TSARs) to replace grants of stock options as a result of our initiative to reduce dilution to shareholders. SARs and TSARs are units that grant the holder the right to

receive a cash payment upon exercise for the difference between the market price of the Company’s common shares and the exercise price, which is determined at the date of grant. SARs and TSARs are measured based on the intrinsic value, which is

defined as the amount by which the market value of common shares exceeds the exercise price.

Deferred, restricted and performance share units are grants

of notional common shares that are redeemable for cash upon vesting based on the market value of the Company’s common shares and are non-dilutive to shareholders. Performance share units have an additional feature where the ultimate number of

units that vest will be determined by the Company’s total shareholder return in relation to a predetermined target over the period to vesting. The number of units that will ultimately vest will be in the range of 50% to 120% of the original

grant. For deferred, restricted and performance share units, the fair value is initially measured at the grant date and subsequently remeasured based on the market value of common shares.

For all the stock-based awards with the exception of stock options, the initial value and any subsequent change in value due to changes in the market value of

common shares is recognized in earnings over the related service period for the proportion of the service that has been rendered at each reporting date. Accordingly, stock-based compensation associated with these stock-based awards may vary

significantly from period to period as a result of changes in the share price.

Stock-based compensation expense for the year ended December 31,

2010 was $31 million compared with $12 million for 2009. The increase in stock-based compensation of $19 million during 2010 was primarily due to the impact of the increase in the share price during the year from $19.49 per share to $30.40 per

share. This resulted in a higher charge of approximately $13 million from an increase in the fair value of deferred, restricted and performance share units and a higher charge of approximately $3 million related to the value of SARs and TSARs.

Additionally, the increase in share price resulted in a higher charge of approximately $3 million due to an increase in the estimated number of performance share units that will ultimately vest.

Other, net

Our investment in global

distribution and supply infrastructure includes a dedicated fleet of ocean-going vessels. We utilize these vessels to enhance value to customers by providing reliable and secure supply and to optimize supply chain costs overall. Due to the

significant reduction of production levels in Chile since mid-2007, we have had excess shipping capacity that is subject to fixed time charter costs. We have been successful in mitigating some of these costs by entering into sub-charters and

third-party backhaul arrangements. However, excess capacity in the global tanker market over the last two years has made it more difficult to mitigate these costs. For the year ended December 31, 2010 compared with 2009, ocean freight and other

logistics costs were higher by $16 million primarily as a result of lower backhaul cost recoveries and higher bunker fuel costs.

Selling, general and

administrative expenses were higher by $11 million in 2010 compared with 2009 as a result of higher costs associated with employee training, travel and other initiatives combined with the negative impact of the weakening US dollar in 2010 on costs

incurred in other currencies. Selling, general and administrative costs returned to more normalized levels in 2010 following spending deferrals and reductions in 2009 as a result of economic recession.

Depreciation and Amortization

Depreciation

and amortization was $131 million for the year ended December 31, 2010 compared with $118 million for 2009. The increase in depreciation and amortization expense for 2010 compared with 2009 was primarily due to the inclusion of depletion

charges associated with our oil and gas investment in Chile. Upon receipt of final approval from the Government of Chile in late 2009, we adopted the full cost methodology for accounting for oil and gas exploration costs associated with our 50%

participation in the Dorado Riquelme block in southern Chile (refer to the Production Summary section on page 13 for more information). Under

these accounting standards, cash investments in the block are initially capitalized and are recorded to earnings through non-cash depletion charges as natural gas is produced from the block.

|

|

|

| |

|

| Management’s Discussion & Analysis Annual Report 2010 METHANEX 19

|

|

|

Interest Expense

|

|

|

|

|

|

|

|

|

| ($ MILLIONS) |

|

2010 |

|

|

2009 |

|

| Interest expense before capitalized interest |

|

$ |

62 |

|

|

$ |

60 |

|

| Less capitalized interest related to Egypt plant under construction |

|

|

(38 |

) |

|

|

(33 |

) |

| Interest expense |

|

$ |

24 |

|

|

$ |

27 |

|

Interest expense

before capitalized interest in 2010 was $62 million compared with $60 million in 2009. Interest expense before capitalized interest was higher in 2010 primarily as a result of higher debt balances related to our methanol project in Egypt. We have

limited recourse debt facilities of $530 million for this 1.26 million tonne per year methanol facility that we are developing with partners. Interest costs related to the project are capitalized.

Interest and Other Income

Interest and

other income for the year ended December 31, 2010 was $2 million compared with nil for 2009. The increase in interest and other income during 2010 compared with 2009 was primarily due to the impact of changes in foreign exchange rates.

Income Taxes

We recorded an

income tax expense of $34 million for the year ended December 31, 2010 compared with an income tax recovery of $4 million for 2009. The effective tax rate for the year ended December 31, 2010 was approximately 25%. Included in income

before tax for 2010 was a before and after-tax gain of $22.2 million on the sale of our land and terminal assets in Kitimat, Canada. Excluding this item, the effective tax rate for 2010 was approximately 30%.

The statutory tax rate in Chile and Trinidad, where we earn a substantial portion of pre-tax earnings, is 35%. Our Atlas facility in Trinidad has partial relief

from corporate income tax until 2014. In Chile, the tax rate consists of a first tier tax that is payable when income is earned and a second tier tax that is due when earnings are distributed from Chile. The second category tax is initially recorded

as future income tax expense and is subsequently reclassified to current income tax expense when earnings are distributed. Accordingly, the ratio of current income tax expense to total income tax expense is highly dependent on the level of cash

distributed from Chile.

For additional information regarding income taxes, refer to note 13 of our 2010 consolidated financial statements.

|

|

|

| |

|

| |

|

20 METHANEX

Annual Report 2010 Management’s Discussion & Analysis |

LIQUIDITY AND CAPITAL RESOURCES

|

|

|

|

|

|

|

|

|

| ($ MILLIONS) |

|

2010 |

|

|

2009 |

|

| Cash flows from operating activities: |

|

|

|

|

|

|

|

|

| Cash flows from operating activities1 |

|

$ |

252 |

|

|

$ |

128 |

|

| Changes in non-cash working capital |

|

|

(99 |

) |

|

|

(18 |

) |

|

|

|

153 |

|

|

|

110 |

|

| Cash flows from investing activities: |

|

|

|

|

|

|

|

|

| Property, plant and equipment |

|

|

(58 |

) |

|

|

(61 |

) |

| Egypt plant under construction |

|

|

(86 |

) |

|

|

(262 |

) |

| Oil and gas assets |

|

|

(24 |

) |

|

|

(23 |

) |

| GeoPark financing, net |

|

|

20 |

|

|

|

(9 |

) |

| Proceeds on sale of assets |

|

|

32 |

|

|

|

– |

|

| Other, net |

|

|

(1 |

) |

|

|

3 |

|

| Changes in non-cash working capital |

|

|

(2 |

) |

|

|

(28 |

) |

|

|

|

(119 |

) |

|

|

(380 |

) |

| Cash flows from financing activities: |

|

|

|

|

|

|

|

|

| Dividend payments |

|

|

(57 |

) |

|

|

(57 |

) |

| Proceeds from limited recourse debt |

|

|

68 |

|

|

|

151 |

|

| Equity contributions by non-controlling interest |

|

|

23 |

|

|

|

45 |

|

| Repayment of limited recourse debt |

|

|

(31 |

) |

|

|

(15 |

) |

| Settlements on interest rate swap contracts |

|

|

(16 |

) |

|

|

(6 |

) |

| Proceeds on issue of shares on exercise of stock options |

|

|

9 |

|

|

|

– |

|

| Other, net |

|

|

(6 |

) |

|

|

(6 |

) |

| |

|

|

(10 |

) |

|

|

112 |

|

| Increase (decrease) in cash and cash equivalents |

|

|

24 |

|

|

|

(158 |

) |

| Cash and cash equivalents, end of year |

|

$ |

194 |

|

|

$ |

170 |

|

| 1 |

Before changes in non-cash working capital. |

Cash Flow Highlights

Cash Flows from Operating Activities

Cash flows from operating activities for the year ended December 31, 2010 were $153 million compared with $110 million for 2009. The change in cash flows from

operating activities is explained by changes in Adjusted EBITDA after excluding non-cash expenses such as stock-based compensation expense and other items (net of any related cash payments), and changes in interest expense, interest and other

income, current taxes and non-cash working capital. The following table provides a summary of these items for 2010 and 2009.

|

|

|

|

|

|

|

|

|

| ($ MILLIONS) |

|

2010 |

|

|

2009 |

|

| Adjusted EBITDA |

|

$ |

267 |

|

|

$ |

142 |

|

| Stock-based compensation expense |

|

|

31 |

|

|

|

12 |

|

| Other non-cash items (net of cash payments) |

|

|

2 |

|

|

|

(4 |

) |

| Interest expense |

|

|

(24 |

) |

|

|

(27 |

) |

| Interest and other income |

|

|

3 |

|

|

|

– |

|

| Current taxes |

|

|

(27 |

) |

|

|

6 |

|

|

|

|

252 |

|

|

|

129 |

|

| Changes in non-cash working capital: |

|

|

|

|

|

|

|

|

| Receivables |

|

|

(62 |

) |

|

|

(43 |

) |

| Inventories |

|

|

(55 |

) |

|

|

5 |

|

| Prepaid expenses |

|

|

(3 |

) |

|

|

(7 |

) |

| Accounts payable and accrued liabilities |

|

|

21 |

|

|

|

26 |

|

| |

|

|

(99 |

) |

|

|

(19 |

) |

| Cash flows from operating activities |

|

$ |

153 |

|

|

$ |

110 |

|

Cash flows from

operating activities before changes in non-cash working capital for the year ended December 31, 2010 were $252 million compared with $129 million for 2009. Adjusted EBITDA was higher by $125 million for the year ended

|

|

|

| |

|

| Management’s Discussion & Analysis Annual Report 2010 METHANEX 21

|

|

|

December 31, 2010 compared with 2009 and this was the primary driver of the increase in cash flows from operating activities before changes in non-cash working capital (refer to the Adjusted EBITDA section on page 17 for a discussion of changes in Adjusted EBITDA). Non-cash stock-based compensation expense included in Adjusted EBITDA for

the year ended December 31, 2010 was higher compared with 2009 by $19 million primarily due to the impact of the increase in our share price during 2010 (refer to the Stock-based

Compensation section on page 18 for more information). Cash flows from operating activities were lower by $33 million for the year ended December 31, 2010 compared with 2009 due to higher

current taxes as a result of higher income levels in 2010.

For the year ended December 31, 2010, non-cash working capital increased by $99 million,

resulting in a decrease in cash flows from operating activities. The primary changes in non-cash working capital for 2010 were increases in receivables and inventories of $62 million and $55 million, respectively, offset by an increase in accounts

payable and accrued liabilities of $21 million. The increase in receivables was primarily due to the impact of higher methanol pricing and higher sales volumes on trade receivables at December 31, 2010 compared with December 31, 2009. The

increase in inventories was also primarily due to the impact of higher methanol pricing on both produced and purchased ending inventory as well as higher ending inventory volumes at December 31, 2010 compared with December 31, 2009. During

2010, we grew total sales volumes by approximately 16% from 5.95 million tonnes in 2009 to 6.93 million tonnes in 2010, and as a result we had a higher volume of trade receivables and higher ending inventory at December 31, 2010

compared with December 31, 2009 to support these sales. The increase in accounts payable and accrued liabilities at December 31, 2010 compared with December 31, 2009 was primarily as a result of the impact of higher methanol pricing

on natural gas payables and the timing of other payments.

Cash Flows from Investing Activities

In 2010, our priorities for allocating capital were funding the completion of the methanol project in Egypt, supporting natural gas development in Chile and

investing to maintain the reliability of our existing plants.

During 2010, additions to property, plant and equipment, which include turnarounds,

catalyst and other capital expenditures, were $58 million. This includes approximately $12 million associated with major maintenance activities at our Trinidad facilities with the remaining capital expenditure of approximately $27 million relating

primarily to maintenance costs at our plants in Chile and New Zealand. In 2010, approximately $10 million was also incurred for the restart of our Medicine Hat, Alberta plant. Included in additions to property, plant and equipment for 2010 is $9

million for the acquisition of an ocean-going vessel that we acquired through a 50% interest in a joint venture.

During 2010, total capital expenditures

were $86 million for the development and construction of the 1.26 million tonne per year methanol plant in Egypt.

We have an agreement with ENAP to

invest in natural gas exploration and development in the Dorado Riquelme exploration block in southern Chile. Under the arrangement, we fund a 50% participation in the block and receive 100% of the natural gas produced in the block. In 2010, we

contributed $24 million and to December 31, 2010, we had made total contributions of approximately $86 million.

We also have agreements with

GeoPark under which we have provided $57 million in financing to support and accelerate GeoPark’s natural gas exploration and development activities in southern Chile. During 2010, GeoPark repaid approximately $20 million of this

financing, $15 million of which was funded through proceeds of a debt financing, bringing cumulative repayments for this financing to $32 million as at December 31, 2010. We have no further obligations to provide funding to GeoPark.

During 2010, we sold our land and terminal facilities at the Kitimat, Canada site and received proceeds from this sale of $32 million.

We are pursuing natural gas exploration and development opportunities in New Zealand. During 2010, we entered into an agreement with Kea to explore areas of the

Taranaki basin in New Zealand close to our plants. Under the agreement, funding will be shared 50% by both parties, and we will be entitled to all natural gas deliveries from our participation at a price that is competitive to our other locations in

Trinidad, Chile and Egypt. During 2010, we spent approximately $10 million on exploration activities with Kea.

|

|

|

| |

|

| |

|

22 METHANEX

Annual Report 2010 Management’s Discussion & Analysis |

During 2010, we sold our 20% equity interest in Xinneng (Zhangjiagang) Energy Co. Ltd, a company that owns a DME

production facility in China, for approximately $10 million to the ENN Group with no gain or loss on sale. Under the arrangement, we continue to supply all of the methanol requirements for the DME facility under an exclusive supply arrangement.

Cash Flows from Financing Activities

During 2010, we paid our regular quarterly dividend of $0.155 per share and made total dividend payments of $57 million, the same amount as in 2009.

We own 60% of the 1.26 million tonne per year Egypt methanol facility and we account for this investment using consolidation accounting, which results in 100% of the assets and liabilities being included in

our financial statements with the other investors’ interest in the project being presented as “non-controlling interest”. We have limited recourse debt facilities totalling $530 million for the methanol facility in Egypt. During 2010,

a total of $58 million of this limited recourse debt was drawn for construction activities and a total of $23 million was funded by equity contributions from our partners in the project. At December 31, 2010, the full amount of $530 million had

been drawn under these facilities. The remaining proceeds on limited recourse debt of $10 million relates to debt facilities obtained on the acquisition of an ocean-going vessel during 2010.

We repaid $15 million in principal on our Atlas and other limited recourse debt facilities in each of 2010 and 2009. On September 30, 2010, we also made the first debt principal payment of $16 million on the

Egypt limited recourse debt facilities.

The Egypt limited recourse debt facilities bear interest at LIBOR plus a spread. We have entered into interest

rate swap contracts to swap the LIBOR-based interest payments for an average aggregated fixed rate of 4.8% plus a spread on approximately 75% of the Egypt limited recourse debt facilities for the period to March 31, 2015 (refer to the Financial Instruments section on page 26 for more information). The cash settlements associated with these interest rate swap contracts during 2010 and 2009

were approximately $16 million and $6 million, respectively.

During 2010, we received proceeds of $9 million on the issue of 0.5 million common

shares on the exercise of stock options.

Liquidity and Capitalization

We maintain conservative financial policies and focus on maintaining our financial strength and flexibility through prudent financial management. Our objectives in managing liquidity and capital are to provide

financial capacity and flexibility to meet our strategic objectives, to provide an adequate return to shareholders commensurate with the level of risk and to return excess cash through a combination of dividends and share repurchases.

The following table provides information on our liquidity and capitalization position as at December 31, 2010 and December 31, 2009, respectively:

|

|

|

|

|

|

|

|

|

| ($ MILLIONS, EXCEPT WHERE NOTED) |

|

2010 |

|

|

2009 |

|

| Liquidity: |

|

|

|

|

|

|

|

|

| Cash and cash equivalents |

|

$ |

194 |

|

|

$ |

170 |

|

| Undrawn Egypt limited recourse debt facilities |

|

|

– |

|

|

|

58 |

|

| Undrawn credit facilities |

|

|

200 |

|

|

|

200 |

|

| Total liquidity |

|

$ |

394 |

|

|

$ |

428 |

|

| Capitalization: |

|

|

|

|

|

|

|

|

| Unsecured notes |

|

$ |

348 |

|

|

$ |

347 |

|

| Limited recourse debt facilities, including current portion |

|

|

599 |

|

|

|

567 |

|

| Total debt |

|

|

947 |

|

|

|

914 |

|

| Non-controlling interest |

|

|

146 |

|

|

|

133 |

|

| Shareholders’ equity |

|

|

1,277 |

|

|

|

1,236 |