UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________________________________________________________________________

FORM 10-K

_____________________________________________________________________________________________

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Fiscal Year Ended December 31 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to .

Commission File No. 001-33093

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: (858 ) 550-7500

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered | ||||||

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☒ | Accelerated Filer | ☐ | Non-accelerated Filer | ☐ | Smaller reporting company | Emerging growth company | ||||||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the Registrant’s voting and non-voting stock held by non-affiliates was approximately $0.9 billion based on the last sales price of the Registrant’s Common Stock on the Nasdaq Global Market of the Nasdaq Stock Market LLC on June 30, 2023. For purposes of this calculation, shares of Common Stock held by directors, officers and 10% stockholders known to the Registrant have been deemed to be owned by affiliates which should not be construed to indicate that any such person possesses the power, direct or indirect, to direct or cause the direction of the management or policies of the Registrant or that such person is controlled by or under common control with the Registrant.

As of February 26, 2024, the Registrant had 17,705,287 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Registrant’s 2024 Annual Meeting of Stockholders to be filed with the Commission within 120 days of December 31, 2023 are incorporated by reference in Part III of this Annual Report on Form 10-K. With the exception of those portions that are specifically incorporated by reference in this Annual Report on Form 10-K, such Proxy Statement shall not be deemed filed as part of this Report or incorporated by reference herein.

Table of Contents

| Part I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 1C. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Part II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| Part III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Part IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

| GLOSSARY OF TERMS AND ABBREVIATIONS | |||||

| Abbreviation | Definition | ||||

| 2023 Notes | $750.0 million aggregate principal amount of convertible senior unsecured notes due 2023 | ||||

| Aldeyra | Aldeyra Therapeutics, Inc. | ||||

| Amgen | Amgen, Inc. | ||||

| ASC | Accounting Standards Codification | ||||

| ASU | Accounting Standards Update | ||||

| Aziyo | Aziyo Med, LLC | ||||

| Baxter | Baxter International, Inc. | ||||

| BeiGene | BeiGene, Ltd. | ||||

| BendaRx | BendaRx Corp. | ||||

| BLA | Biologics license application | ||||

| CASI | CASI Pharmaceuticals, Inc. | ||||

| cGMP | Current Good Manufacturing Practice | ||||

| Company | Ligand Pharmaceuticals Incorporated, including subsidiaries | ||||

| Convertible Note | Senior Convertible Promissory Note | ||||

| COPD | Chronic obstructive pulmonary disease | ||||

| Cormatrix | Cormatrix Cardiovascular, Inc. | ||||

| Corvus | Corvus Pharmaceuticals, Inc. | ||||

| Credit Agreement | Credit Agreement, dated as of October 12, 2023, among Ligand Pharmaceuticals Incorporated, certain of its subsidiaries, as Guarantors (as defined therein), the Lenders (as defined therein), and Citibank, N.A., as Administrative Agent, Swingline Lender and L/C Issuer. | ||||

| CVR | Contingent value right | ||||

| CyDex | CyDex Pharmaceuticals, Inc. | ||||

| Daiichi Sankyo | Daiichi Sankyo Company, Ltd. | ||||

| Dianomi | Dianomi Therapeutics, Inc. | ||||

| DMF | Drug Master File | ||||

| ESG | Environmental, Social and Governance | ||||

| ECM | Extracellular matrix | ||||

| Eisai | Eisai Inc. | ||||

| Elutia | Elutia Inc. | ||||

| EPA | Environmental Protection Agency | ||||

| ESPP | Employee Stock Purchase Plan, as amended and restated | ||||

| EU | European Union | ||||

| Exelixis | Exelixis, Inc. | ||||

| FASB | Financial Accounting Standards Board | ||||

| FDA | U.S. Food and Drug Administration | ||||

| FSGS | Focal segmental glomerulosclerosis | ||||

| FY 2023 | The Company's fiscal year ended December 31, 2023 | ||||

| FY 2022 | The Company's fiscal year ended December 31, 2022 | ||||

| FY 2021 | The Company's fiscal year ended December 31, 2021 | ||||

| GAAP | Generally accepted accounting principles in the United States | ||||

| GCSF | Granulocyte-colony stimulating factor | ||||

| Gilead | Gilead Sciences, Inc. | ||||

| HBV | Hepatitis B Virus | ||||

| Hikma | Hikma Pharmaceuticals PLC | ||||

| Hovione | Hovione FarmCiencia, S.A. | ||||

| IM | Intramuscular | ||||

| IND | Investigational New Drug | ||||

| IRS | Internal Revenue Service | ||||

| IV | Intravenous | ||||

| Jazz | Jazz Pharmaceuticals, Inc. | ||||

| Ligand | Ligand Pharmaceuticals Incorporated, including subsidiaries | ||||

| LTP | Liver targeting prodrug | ||||

| Marinus | Marinus Pharmaceuticals, Inc. | ||||

| Melinta | Melinta Therapeutics, Inc. | ||||

| Merck | Merck & Co., Inc. | ||||

| Metabasis | Metabasis Therapeutics, Inc. | ||||

| NDA | New Drug Application | ||||

| NOLs | Net Operating Losses | ||||

| Novan | Novan, Inc. (n/k/a NVN Liquidation, Inc.) | ||||

| Novartis | Novartis AG | ||||

| Nucorion | Nucorion Pharmaceuticals, Inc. | ||||

| OmniAb | OmniAb Operations, Inc. (f/k/a OmniAb, Inc.) | ||||

| Ono | Ono Pharmaceutical Co., Ltd. | ||||

| Opthea | Opthea Limited | ||||

| Orange Book | Publication identifying drug products approved by the FDA based on safety and effectiveness | ||||

| Palvella | Palvella Therapeutics, Inc. | ||||

| PDUFA | Prescription Drug User Fee Act | ||||

| Pfenex | Pfenex Inc. | ||||

| Pfizer | Pfizer, Inc. | ||||

| Phoenix Tissue | Phoenix Tissue Repair | ||||

| PSU | Performance stock unit | ||||

| R&D | Research and Development | ||||

| Revolving Credit Facility | The revolving credit facility under the Credit Agreement | ||||

| RSU | Restricted stock unit | ||||

| Sage | Sage Therapeutics, Inc. | ||||

| Sanofi | Sanofi SA | ||||

| SARM | Selective Androgen Receptor Modulator | ||||

| SEC | Securities and Exchange Commission | ||||

| Sedor | Sedor Pharmaceuticals, Inc., or RODES, Inc. | ||||

| Seelos | Seelos Therapeutics, Inc. | ||||

| Selexis | Selexis, SA | ||||

| Sermonix | Sermonix Pharmaceuticals, LLC | ||||

| SII | Serum Institute of India | ||||

| SQ Innovation | SQ Innovation, Inc. | ||||

| Sunshine Lake Pharma | Sunshine Lake Pharma Co., Ltd. | ||||

| Takeda | Takeda Pharmaceuticals Company Limited | ||||

| Tax Act | The Tax Cuts and Jobs Act | ||||

| Teva | Teva Pharmaceuticals USA, Inc., Teva Pharmaceutical Industries Ltd. and Actavis, LLC | ||||

| Travere | Travere Inc. | ||||

| TR-Beta | Thyroid hormone receptor beta | ||||

| Vernalis | Vernalis plc | ||||

| Verona | Verona Pharma plc | ||||

| Viking | Viking Therapeutics | ||||

| Xi'an Xintong | Xi'an Xintong Medicine Research | ||||

| Zydus Cadila | Zydus Cadila Healthcare, Ltd | ||||

PART I

1

Cautionary Note Regarding Forward-Looking Statements:

You should read the following report together with the more detailed information regarding our company, our common stock and our financial statements and notes to those statements appearing elsewhere in this document.

This report contains forward-looking statements that involve a number of risks and uncertainties. Although our forward-looking statements reflect the good faith judgment of our management, these statements can only be based on facts and factors currently known by us. Consequently, these forward-looking statements are inherently subject to risks and uncertainties, and actual results and outcomes may differ materially from results and outcomes discussed in the forward-looking statements.

Forward-looking statements can be identified by the use of forward-looking words such as “believes,” “expects,” “may,” “will,” “plan,” “intends,” “estimates,” “would,” “continue,” “seeks,” “pro forma,” or “anticipates,” or other similar words (including their use in the negative), or by discussions of future matters such as those related to our future results of operations and financial position, royalties and milestones under license agreements, Captisol material sales, product development, and product regulatory filings and approvals, and the timing thereof, Ligand's status as a high-growth company, as well as other statements that are not historical. You should be aware that the occurrence of any of the events discussed under the caption “Risk Factors” could negatively affect our results of operations and financial condition and the trading price of our stock.

The cautionary statements made in this report are intended to be applicable to all related forward-looking statements wherever they may appear in this report. We urge you not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. Except as required by law, we assume no obligation to update our forward-looking statements, even if new information becomes available in the future. This caution is made under the safe harbor provisions of Section 21E of the Securities Exchange Act of 1934, as amended.

References to “Ligand Pharmaceuticals Incorporated,” “Ligand,” the “Company,” “we,” “our” and “us” include Ligand Pharmaceuticals Incorporated and our wholly-owned subsidiaries.

Partner Information

Information regarding partnered products and programs comes from information publicly released by our partners and licensees.

Trademarks

This Annual Report on Form 10-K includes trademarks, trade names and service marks owned by us. Ligand®, BEPro™, Captisol®, CyDex®, LTP®, LTP Technology®, NITRICILTM, and ZELSUVMITM are protected under applicable intellectual property laws and are our property. All other trademarks, trade names and service marks including, but not limited to Pelican Expression Technology®, PeliCRM®, Pfenex Expression Technology®, OmniAb® Kyprolis®, Evomela®, Veklury®, Livogiva®, Bonteo®, Zulresso®, Rylaze®, VAXNEUVANCE™, Pneumosil®, Minnebro®, Baxdela®, Nexterone®, Noxafil®, Duavee®, FILSPARI® and are the property of their respective owners. Solely for convenience, trademarks, trade names and service marks referred to in this report may appear without the ®, ™ or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to such trademarks, trade names and service marks. Use or display by us of other parties’ trademarks, trade dress or products is not intended to and does not imply a relationship with, or endorsement or sponsorship of, us by the trademark or trade dress owners.

2

| Item 1. | Business | ||||

Overview

We are a biopharmaceutical company enabling scientific advancement through supporting the clinical development of high-value medicines. Ligand does this by providing financing, licensing our technologies or both. Our business model seeks to generate value for stockholders by creating a diversified portfolio of biopharmaceutical product revenue streams that are supported by an efficient and low corporate cost structure. Our goal is to offer investors an opportunity to participate in the promise of the biotech industry in a profitable and diversified manner. Our business model focuses on funding programs in mid- to late-stage drug development in return for economic rights, purchasing royalty rights in development stage or commercial biopharmaceutical products and licensing our technology to help partners discover and develop medicines. We partner with other pharmaceutical companies to leverage what they do best (late-stage development, regulatory management and commercialization) in order to generate our revenue. Our Captisol platform technology is a chemically modified cyclodextrin with a structure designed to optimize the solubility and stability of drugs. We have established multiple alliances, licenses and other business relationships with the world’s leading biopharmaceutical companies including Amgen, Merck, Pfizer, Jazz, Takeda, Gilead Sciences and Baxter International.

Our revenue consists of three primary elements: royalties from commercialized products, sales of our Captisol material to partners, and contract revenue from license fees and milestones payments.

Strategy and Execution

We are a biopharmaceutical royalty aggregator, focused on investing in differentiated late-stage assets and operating royalty-generating, infrastructure-light platform technologies. Since our transition to this business model in 2007, we have deployed over $1 billion of capital to build our diverse portfolio. Following the spin-offs of our OmniAb antibody discovery business in November 2022 and the Pelican Expression Technology subsidiary in September 2023, our strategy is to continue to expand our pipeline by aggregating royalty rights in mid- to late-stage development and commercial biopharma products, while maintaining a lean infrastructure and high-margin business.

Our business model is highly differentiated from a traditional biotechnology company in several key ways. First, we have limited infrastructure requirements, enabling us to maintain relative high operating margins. Second, we can enable development over a broad range of therapeutic areas and can be strategic and balanced about the size of our investments to achieve a highly diversified portfolio. Third, our business model mitigates the high volatility associated with building a business around a single or small number of assets. With this approach, we have the ability to mitigate the impact of binary clinical outcomes in the biopharmaceutical industry, thereby facilitating cash flows that are more predictable. Finally, we can target the size of our investments to achieve appropriate risk management across the portfolio.

As an organization, we bring a highly experienced team and financial strength to execute on our strategy. There is high demand for capital and low availability of structured capital in the segment of the biopharmaceutical market in which we operate, creating significant deal flow opportunity for Ligand. Unlike open-market equity investing, many of our investments take place under Confidential Disclosure Agreements (CDAs), allowing us access to in-depth, advantageous diligence materials. Our flexible investment structures are designed to mitigate risks, and also help accommodate different transaction structures based on our partners' goals. We believe our business model is highly scalable and has significant growth potential. We have assembled a talented, long-tenured team with deep industry relationships, investment experience and industry knowledge.

From a more tactical perspective, we execute our strategy using four key approaches: royalty monetization, M&A, project finance, and platform investments. With royalty monetization, we purchase rights on existing royalty contracts that are owned by inventors, academic institutions or companies. There are advantages of royalty investing as a model since royalties 1) have minimal infrastructure, 2) are non-dilutive and 3) their cash flows are often protected in bankruptcy. In M&A investments, we acquire companies with valuable assets or partnerships and realize the value of those assets by restructuring operations and/or partnering the assets. Ligand has a history of doing this successfully with deals such as:

•Pharmacopeia acquisition in 2008 which yielded Travere’s Filspari

•Metabasis acquisition in 2010 which contributed to the creation of Viking Therapeutics

•Vernalis acquisition in 2018 which yielded Verona’s ensifentrine

•Pfenex acquisition in 2020 which yielded four of our major commercial programs – Vaxneuvance, Rylaze, Pneumosil, and Teriparatide as well as our equity interest in Primrose Bio

•Novan acquisition in 2023 which yielded Zelsuvmi

3

Project finance involves the provision of development capital to fund late-stage clinical programs in return for royalty contracts that we negotiate, creating royalties on the future sales of those products. Finally, with platform technology acquisitions, we look for platforms with high operating margins and existing licensing contracts and acquire these targets. The ideal platform will provide new royalties by operating those platforms, and it will be scalable and have broad applicability. Our Captisol business is an excellent example of a successful platform technology investment.

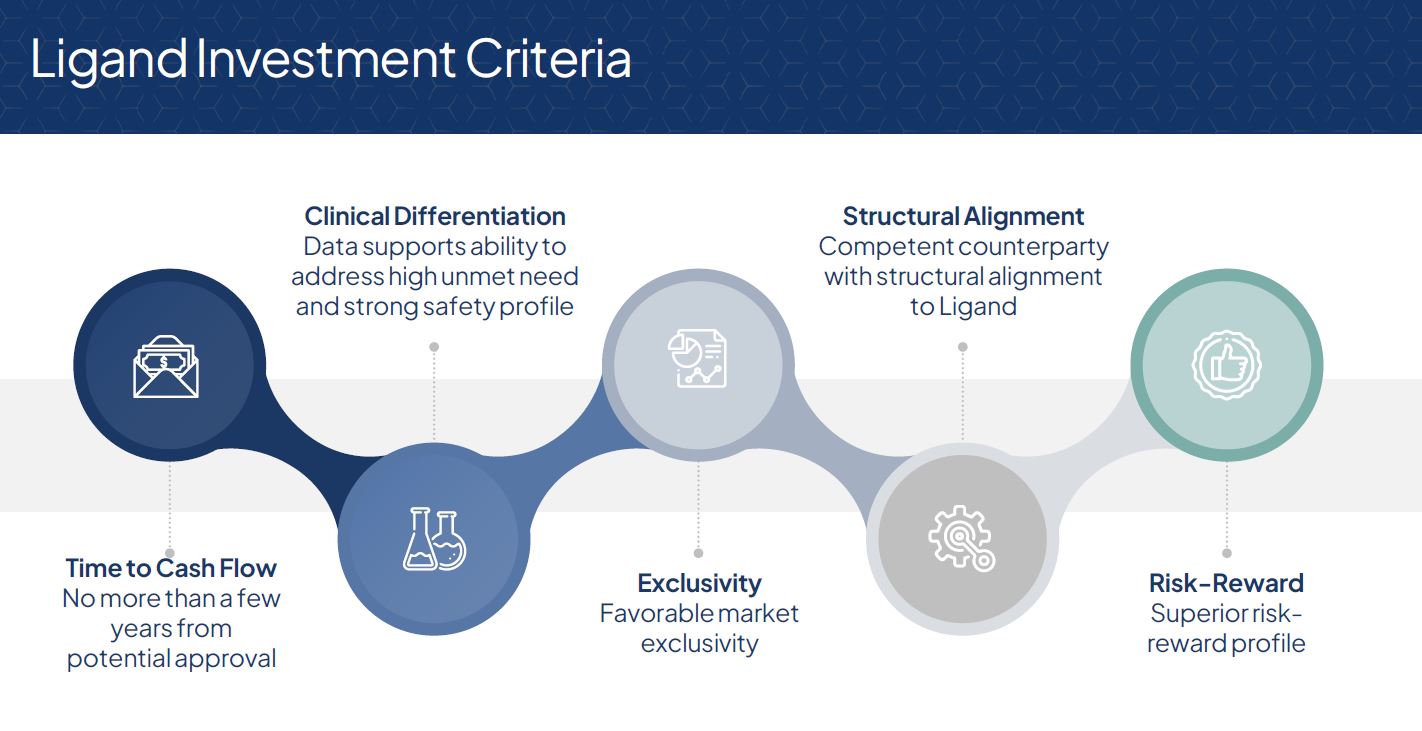

We have a specific set of criteria we use to assess potential investments. The first criteria is time to cash flow, as we seek products that are within a few years of regulatory approval and commercialization. Typically, this means we invest in Phase 3 assets, although we also evaluate opportunities to invest in Phase 2 assets. In terms of an asset's clinical profile, we are looking for strong data supporting both efficacy and safety, and products which will ultimately deliver significant value to patients and to the healthcare system. We also look for strong market exclusivity, which can be achieved through intellectual property and/or regulatory protections. Structural alignment with our counterparty and the marketer is also a key criteria of the investments we make. Ultimately, we look for assets with favorable risk-reward profiles, which have above average probability of technical and regulatory success and can be commercialized effectively.

4

Technologies

Through a combination of research and acquisitions, we have created a partnered portfolio with a wide variety of underlying technologies. This diversification provides the added benefits of exposure to a wider breadth of scientific innovation, more licensing opportunities and lower impact of individual patent expiry.

Captisol Technology

Captisol is a patent-protected, chemically modified cyclodextrin with a structure designed to optimize the solubility and stability of drugs. This unique technology has enabled several FDA-approved products, including Gilead’s Veklury, Amgen’s Kyprolis, Baxter International’s Nexterone, Acrotech Biopharma’s and CASI Pharmaceuticals’ Evomela, Melinta Therapeutics’ Baxdela and Sage Therapeutics’ Zulresso. There are many Captisol-enabled products currently in various stages of development. We maintain a broad global patent portfolio for Captisol with the latest expiration date in 2035. Other patent applications covering methods of making Captisol, if issued, extend to 2041.

In addition to solid Captisol powder, we offer our partners access to cGMP manufactured aqueous Captisol concentrate. This product offering was established in 2017 to reduce cycle time and increase Captisol production capacity for large-volume drug products. We maintain both Type IV and Type V drug master files (DMFs) with the FDA. These DMFs contain manufacturing and safety information relating to Captisol that our licensees can reference when developing Captisol-enabled drugs. We also have active DMFs in Japan, China and Canada. In 2023, royalties on commercial products using Captisol comprised over half of our total royalty revenue.

HepDirect, LTP and BEPro Technology Platform

The HepDirect and LTP platforms are our proprietary liver-targeting prodrug technologies that can deliver many different chemical classes of drugs to the liver by using a chemical modification that renders an active pharmaceutical ingredient (API) biologically inactive until cleaved by a liver-specific enzyme. These technologies may improve the efficacy and/or safety of certain drugs and can be applied to marketed or new drug products to treat liver diseases or diseases caused by hemostasis imbalance of circulating molecules controlled by the liver.

The BEPro technology platform is a next generation prodrug technology distinct from HepDirect and LTP prodrug technologies, expanding use to non-liver related diseases. BEPro is specifically applicable to nucleotides and nucleotide analogs for the development of compounds with improved product profiles. Ligand has demonstrated benefits in cell penetration and oral, intravenous and inhaled pharmacokinetics with BEPro-enabled nucleotide analogs.

SUREtechnology Platform (owned by Selexis)

5

We acquired economic rights to various SUREtechnology Platform programs from Selexis. The SUREtechnology Platform, developed and owned by Selexis, is a novel technology that improves the way that cells are utilized in the development and manufacturing of recombinant proteins and drugs.

Pelican Expression Technology (owned by Primrose Bio, of which Ligand owns 49.9%)

The Pelican Expression Technology platform is a robust, validated, cost-effective and scalable platform for recombinant protein production, and is especially well suited for complex, large-scale proteins. Global manufacturers have demonstrated consistent success with the platform and the technology is currently outlicensed for multiple commercial and development-stage programs. The versatility of the platform has been demonstrated in the production of enzymes, peptides, antibody derivatives and engineered non-natural proteins. The platform contributes significant value to biopharmaceutical development programs by shortening timelines and reducing costs associated with research and development through commercial manufacturing of therapeutics and vaccines. Given pharmaceutical industry trends toward large molecules with increased structural complexities, the Pelican Expression Technology platform is well positioned to meet these growing needs as one of the most comprehensive and broadly available, commercially validated protein production platforms in the industry.

2023 Investment Highlights

In September 2023, we announced the sale of our Pelican business, inclusive of the Pelican Expression Technology platform, and a merger of Pelican with Primordial Genetics to form a new company, Primrose Bio. As part of the investment, Ligand retained the existing commercial royalties related to the Pelican Expression Technology platform and owns 49.9% of Primrose Bio. We also entered into a purchase and sale agreement with Primrose, whereby we invested $15 million in exchange for a portion of the economic rights from the two existing contracts of Primordial Genetics and an economic interest in potential future revenues generated from the Pelican business. Ligand retains the pre-spin royalty rights from the Pelican Expression Technology, including economic rights to Jazz’s RYLAZE, Merck’s VAXNEUVANCE and V116 vaccines, Alvogen’s Teriparatide, Serum Institute of India’s Pneumosil and MenFive vaccines, among others. We had originally acquired the Pelican business through the acquisition of Pfenex in 2020. After incubating this technology for three years, we now have five commercial royalty streams from the platform, and with the spinoff and merger, we retain a significant equity stake. We consider the acquisition of Pfenex and spin-off of Pelican Technology Holdings, Inc. to be a very successful transaction and expect these assets will continue to generate significant revenues for the Company.

In October 2023, we announced an investment of $30 million to acquire a 13% portion of the royalties and milestones owed to Ovid Therapeutics related to the potential approval and commercialization of soticlestat. Soticlestat is a Phase 3, first-in-class, novel mechanism of action molecule being studied by Takeda in two rare pediatric epilepsies: Lennox-Gastaut syndrome (LGS) and Dravet syndrome. Takeda is one of the world's leading pharmaceutical companies in neurology and rare diseases. LGS and Dravet are two very difficult treat conditions, with high unmet clinical needs despite having a few products that have been recently approved. Takeda has stated it anticipates regulatory filings for soticlestat in its fiscal year 2024. If regulatory approval is granted, commercialization and royalties to Ligand could begin a year later.

In November 2023, we closed a $20 million acquisition of Tolerance Therapeutics, a holding company owned by the inventors of TZIELD (teplizumab). TZIELD is the first disease-modifying therapy approved to treat patients with type-1 diabetes (T1D). It is a CD3-directed antibody indicated to delay the onset of stage-3 T1D in adults and in children aged eight years and older with stage-2 T1D. TZIELD was granted breakthrough therapy designation by the FDA in 2019 and was approved by the FDA in November 2022. TZIELD is marketed by Sanofi following its $2.9 billion acquisition of Provention Bio in 2023. Sanofi recently announced new data from the TZIELD PROTECT Phase 3 trial, which showed TZIELD’s potential to slow the progression of stage 3 T1D in newly diagnosed children and adolescents. These findings were published in the New England Journal of Medicine. Sanofi has a robust history in the diabetes space. Sanofi has been featuring TZIELD as one of their key launches with significant blockbuster potential. Ligand is owed a royalty of less than 1% on worldwide net sales of TZIELD.

Novan Acquisition

In September 2023, the bankruptcy court approved a $12.2 million bid from Ligand to purchase certain assets of Novan, Inc., including berdazimer gel, all assets related to the NITRICIL™ technology platform and the rights to one commercial stage asset. Prior to Novan's bankruptcy, we had a royalty interest in berdazimer topical gel, 10.3%. Berdazimer topical gel, 10.3% was approved by the FDA in January 2024, with a brand name of ZELSUVMI.

ZELSUVMI™ (berdazimer) topical gel, 10.3% is a first-in-class topical medication for the treatment of molluscum contagiosum in adults and pediatric patients one year of age or older. The FDA approved ZELSUVMI as the novel drug for the treatment of molluscum infections. ZELSUVMI is the first and only topical prescription medication that can be applied by patients, parents, or caregivers at home, outside of a physician's office, or other medical setting to treat this highly contagious viral skin infection.

6

As we incubate this newly acquired business, the Novan team is actively preparing for commercialization. Consistent with our business model, we are engaging with potential commercial partners to maximize the value for Ligand shareholders through a strategic transaction.

Commercial and Clinical Stage Partnered Portfolio

We have a large portfolio of assets currently generating royalties and future potential revenue-generating programs, including over 85 fully-funded by our partners.

Royalties on Commercial Products

The following table provides an overview of our current portfolio of royalties:

| Product | Partner | Therapeutic Area | Royalty Rate | 2023 Royalty Revenue (in millions) | Estimated 2023 Product Revenue (in millions) | ||||||||||||

| Kyprolis | Amgen/Ono/Beigene | Cancer | 1.5% - 3.0% | $35.6 | $1,503.1 | ||||||||||||

| Rylaze | Jazz | Cancer | Low single digit | $13.5 | $397.5 | ||||||||||||

| Teriparatide | Alvogen | Women's Health | 25%-40%¹ | $11.1 | $37.2 | ||||||||||||

| Evomela | Acrotech/CASI | Cancer | 20% | $10.2 | $51.0 | ||||||||||||

| Vaxneuvance | Merck | Infectious Disease | Low single digit | $4.1 | $653.9 | ||||||||||||

| Pneumosil | Serum Institute | Infectious Disease | Low single digit | $4.5 | $198.5 | ||||||||||||

| Filspari | Travere | IgA Nephropathy | 9% | $2.7 | $29.5 | ||||||||||||

| Nexterone | Baxter | Cardiovascular | Low single digit | $1.5 | $50.9 | ||||||||||||

| Other | Various | Various | Various | $0.7 | $23.6 | ||||||||||||

(1) We receive tiered profit sharing of 25% on quarterly profits less than $3.75 million, 35% on quarterly profits greater than $3.75 million but less than $7.5 million and 40% on quarterly profits greater than $7.5 million. If therapeutic equivalence is achieved, quarterly profit changes to 50% of quarterly profits.

Key Partnered Commercial Programs

The following programs represent important revenue-generating components of our current portfolio. For information about the royalties owed to us for certain of these programs, see “Royalties” later in this business section.

Kyprolis (Amgen, Ono, BeiGene)

We supply Captisol to Amgen for use with Kyprolis (carfilzomib) and granted Amgen an exclusive product-specific license under our patent rights with respect to Captisol. Kyprolis is formulated with Ligand’s Captisol technology and is approved in the United States for the following:

•In combination with dexamethasone, lenalidomide plus dexamethasone, daratumumab plus dexamethasone, or daratumumab and hyaluronidase-fihj and dexamethasone, or isatuximab and dexamethasone for the treatment of patients with relapsed or refractory multiple myeloma who have received one to three lines of therapy.

•As a single agent for the treatment of patients with relapsed or refractory multiple myeloma who have received one or more lines of therapy.

Our agreement with Amgen may be terminated by either party in the event of material breach or bankruptcy, or unilaterally by Amgen with prior written notice, subject to certain surviving obligations. Absent early termination, the agreement will terminate upon expiration of the obligation to pay royalties. Under this agreement, we are entitled to receive revenue from clinical and commercial Captisol material sales and royalties on annual net sales of Kyprolis based on our patents and applications relating to the Captisol component of Kyprolis which are not expected to expire until 2033.

Rylaze (Jazz Pharmaceuticals)

In July 2021, Jazz announced the U.S. launch of RYLAZE (asparaginase erwinia chrysanthemi (recombinant)-rywn), previously referred to as JZP458. RYLAZE, which was approved by the FDA in June 2021, is a recombinant erwinia

7

asparaginase used as a component of a multi-agent chemotherapeutic regimen for the treatment of acute lymphoblastic leukemia (ALL) and lymphoblastic lymphoma (LBL) in adult and pediatric patients one month or older who have developed hypersensitivity to E. coli-derived asparaginase. In September 2023, Jazz announced that the European Commission (EC) had granted marketing authorization for RYLAZE, to be marketed as Enrylaze®. Jazz began a rolling launch in the second half of 2023. Additionally, Jazz is utilizing our technology for the development of PF745 (JZP341), a long-acting Erwinia asparaginase for the treatment of ALL and other hematological malignancies. Jazz has worldwide rights to develop and commercialize PF745.

Ligand is eligible to receive up to $152 million in milestone payments and tiered low-single digit royalties based on worldwide net sales of any products resulting from this collaboration, including Rylaze.

Filspari (Travere)

In early 2012, Ligand licensed the world-wide rights to sparsentan to Travere Therapeutics. Travere recently received FDA accelerated approval for FILSPARI (sparsentan) for the treatment of immunoglobulin A nephropathy (IgAN). FILSPARI is the first and only dual endothelin and angiotensin II receptor antagonist in development for rare kidney diseases and is the first non-immunosuppressive treatment indicated for IgAN. Travere anticipates a review opinion by the Committee for Medicinal Products for Human Use (CHMP) on the potential approval for sparsentan for the treatment of IgAN in Europe in the first quarter of 2024. Additionally, Travere is on track to submit a supplemental New Drug Application (sNDA) for the conversion of the existing U.S. accelerated approval in IgAN to full approval.

Travere also completed regulatory engagement on focal segmental glomerulosclerosis (FSGS) in which the FDA communicated that the Phase 3 DUPLEX study results alone are not sufficient to support an sNDA submission for an FSGS indication for sparsentan. As a result, Travere plans to conduct additional analyses of FSGS data with plans to re-engage the FDA in 2024, and implemented a strategic reorganization in the fourth quarter of 2023 to focus near-term resources on the ongoing FILSPARI launch in IgAN.

Under our license agreement with Travere, we are entitled to receive over $50 million in potential milestone payments, as well as a 9% royalty on any future worldwide sales.

Teriparatide Injection Product (PF708) (Alvogen/Adalvo)

We acquired the teriparatide injection product with the acquisition of Pfenex in October 2020. Teriparatide injection is a drug indicated for various uses including the treatment of osteoporosis in certain patients at high risk for fracture. Teriparatide injection was developed using our Pelican Expression Technology and was approved by the FDA in 2019 in accordance with the 505(b)(2) regulatory pathway, with FORTEO as the reference product. Our commercialization partner, Alvogen, launched the product in June 2020 in the United States.

Our partner, Alvogen, has exclusively licensed the rights to commercialize and manufacture the teriparatide injection product in the United States, while Adalvo has the rights to commercialize in the EU, certain countries in the Middle East and North Africa (MENA), and the rest of world (ROW) territories (the latter defined as all countries outside of the EU, U.S. and MENA, excluding Mainland China, Hong Kong, Singapore, Malaysia and Thailand). In August 2020, marketing authorization throughout the EU was received under the trade name Livogiva and in December 2020 in Saudi Arabia under the name Bonteo. In December of 2022, we terminated a license agreement with Beijing Kangchen Biological Technology Co., Ltd. (Kangchen) thereby regaining the right to commercialize PF708 in Mainland China, Hong Kong, Singapore, Malaysia and Thailand along with a non-exclusive right to conduct development activities in such countries with respect to PF708.

In accordance with our agreements with Alvogen, we are eligible to receive tiered gross profit sharing of between 25% and 40% of quarterly profits prior to an “A” therapeutic equivalence designation, which increases to a flat 50% if an “A” rating is achieved.

In accordance with our EU, MENA and ROW agreements with Adalvo, we may be eligible to receive additional upfront and milestone payments of $1.5 million and may also be eligible to receive up to 60% of gross profit derived from product sales and regional license fees, if approved, depending on geography, cost of goods sold and sublicense fees.

Evomela (Acrotech and CASI)

We supply Captisol to, and receive royalties from, Acrotech Biopharma for sales of Evomela in the U.S., and CASI Pharmaceuticals for sales in China. Evomela received marketing approval by the NMPA in August of 2019. It is the only approved and commercially available melphalan product in China. Evomela is a Captisol-enabled melphalan IV formulation which is approved by the FDA for use in two indications:

•a high-dose conditioning treatment prior to autologous stem cell transplantation (ASCT) in patients with multiple myeloma; and

•for the palliative treatment of patients with multiple myeloma for whom oral therapy is not appropriate.

8

Evomela has been granted Orphan Designation by the FDA for use as a high-dose conditioning regimen for patients with multiple myeloma undergoing ASCT. The Evomela formulation avoids the use of propylene glycol, which has been reported to cause renal and cardiac side-effects that limit the ability to deliver higher quantities of therapeutic compounds. The use of the Captisol technology to reformulate melphalan is anticipated to allow for longer administration durations and slower infusion rates, potentially enabling clinicians to safely achieve a higher dose intensity of pre-transplant chemotherapy.

Under the terms of the license agreement, Acrotech Biopharma has marketing rights worldwide excluding China and CASI Pharmaceuticals has rights to market in China. We are eligible to receive over $50 million in potential milestone payments, royalties on global net sales of the Captisol-enabled melphalan product and revenue from Captisol material sales. Acrotech and CASI’s obligation to pay royalties will expire at the end of the life of the relevant patents or when a competing product is launched, whichever is earlier, but in no event before ten years after the commercial launch. Our patents and applications relating to the Captisol component of melphalan are not expected to expire until 2033. As described herein, we have entered into a settlement agreement with Teva and Acrotech Biopharma (the holder of the NDA for Evomela) which will allow Teva to market a generic version of Evomela in the United States in 2026, or earlier under certain circumstances. Absent early termination, the agreement will terminate upon expiration of the obligation to pay royalties. The agreement may be terminated by either party for an uncured material breach or unilaterally by Acrotech and CASI by prior written notice.

VAXNEUVANCE (Merck)

VAXNEUVANCE, a 15-valent pneumococcal conjugate vaccine, also known as V114, was approved in the U.S. in July of 2021 for the prevention of invasive disease caused by Streptococcus pneumoniae serotypes 1, 3, 4, 5, 6A, 6B, 7F, 9V, 14, 18C, 19A, 19F, 22F, 23F and 33F in adults 18 years of age and older, and subsequently in children 6 weeks through 17 years of age in June of 2022. VAXNEUVANCE was also approved in Europe in October 2022 for the prevention of invasive disease and pneumonia caused by Streptococcus pneumoniae in individuals 18 years and older and in infants, children and adolescents from 6 weeks to less than 18 years of age. VAXNEUVANCE utilizes CRM197 vaccine carrier protein, which is produced using the patent-protected Pelican Expression Technology™ platform. We are entitled to low single digit royalties derived from net sales of Vaxneuvance.

In December 2023, Merck announced the FDA accepted for priority review a new BLA for V116, Merck's investigational 21-valent pneumococcal conjugate vaccine specifically designed to help prevent invasive pneumococcal disease and pneumococcal pneumonia in adults. The FDA grants priority review to medicines and vaccines that, if approved, would provide a significant improvement in the safety or effectiveness of the treatment or prevention of a serious condition. The FDA has set a PDUFA date, or target action date, of June 17, 2024. If approved, Ligand is entitled to a royalty on worldwide net sales.

Pneumosil (Serum Institute of India, SII)

SII began commercialization of its 10-valent pneumococcal conjugate vaccine, Pneumosil, which is produced using CRM197 made in the Pelican Expression Technology platform, in the second quarter of 2020. Pneumosil is designed primarily to help fight against pneumococcal pneumonia among children, with an advantage of targeting the most prevalent serotypes of the bacterium causing serious illness in developing countries. Pneumosil achieved WHO Prequalification in December 2019, allowing the product to be procured by United Nations agencies and Gavi, the Vaccine Alliance, and subsequently achieved Indian Marketing Authorization in July 2020, and SII announced commercial launch of the product in India in December 2020.

TZIELD (Sanofi)

We acquired a royalty of less than 1% on net sales of TZIELD through our acquisition of Tolerance Therapeutics in the fourth quarter of 2023. TZIELD is the first disease-modifying therapy to be approved in type 1 diabetes (“T1D”). It is a CD3-directed antibody indicated to delay the onset of Stage 3 T1D in adults and children aged 8 years and older with Stage 2 T1D. TZIELD was granted Breakthrough Therapy Designation in 2019 and was approved by the FDA in November 2022. TZIELD is marketed by Sanofi, following its acquisition of Provention Bio, Inc., the developer of TZIELD, in 2023 for $2.9 billion. Sanofi recently announced new data from TZIELD’s PROTECT Phase 3 trial which showed TZIELD’s potential to slow the progression of Stage 3 T1D in newly diagnosed children and adolescents. TZIELD met the study’s primary endpoint, significantly slowing the decline of C-peptide levels, compared to placebo. Under our agreement with Tolerance, we are entitled to receive royalties through December 1, 2032.

Nexterone (Baxter)

We have a license agreement with Baxter, related to Baxter's Nexterone, a Captisol-enabled formulation of amiodarone, which is marketed in the United States and Canada. We supply Captisol to Baxter for use in accordance with the terms of the license agreement under a separate supply agreement. Under the terms of the license agreement, we will continue to earn milestone payments, royalties, and revenue from Captisol material sales. We will earn royalties on net sales of Nexterone through early 2033.

Veklury (Gilead)

9

We supply Captisol to Gilead for sales of Veklury (remdesivir). Gilead received marketing approval from the FDA in October 2020. Veklury is an antiviral treatment for COVID-19. The product has regulatory approvals for the treatment of moderate or severe COVID-19 in over 70 countries. We are supplying Captisol to Gilead under a 10-year supply agreement. We are also supplying Captisol to Gilead’s voluntary licensing generic partners who are manufacturing remdesivir for 127 low- and middle-income countries. We receive our commercial compensation for this program through the sale of Captisol.

Zulresso (Sage)

We have a license agreement with Sage, related to Sage's Zulresso, a Captisol-enabled formulation of brexanolone for the treatment of postpartum depression (PPD). Under the terms of the agreement, we receive royalties and revenue from Captisol material sales.

Noxafil-IV (Merck)

We have a supply agreement with Merck related to Merck’s NOXAFIL-IV, a Captisol-enabled formulation of posaconazole for IV use. NOXAFIL-IV is marketed in the United States, EU, Japan and Canada. We receive our commercial compensation for this program through the sale of Captisol.

Duavee or Duavive (Pfizer)

Pfizer is responsible for the marketing of bazedoxifene, a synthetic drug specifically designed to reduce the risk of osteoporotic fractures while also protecting uterine tissue. Pfizer has combined bazedoxifene with the active ingredient in Premarin to create a combination therapy for the treatment of post-menopausal symptoms in women. Pfizer is marketing the combination treatment under the brand names Duavee and Duavive in various territories. Net royalties on annual net sales of Duavee/Duavive are payable to us through the life of the relevant patent or ten years from the first commercial sale, whichever is longer, on a country-by-country basis.

Exemptia, Vivitra, Bryxta and Zybev (Zydus Cadila)

Zydus Cadila’s Exemptia (adalimumab biosimilar) is marketed in India for autoimmune diseases. Zydus Cadila uses the Selexis technology platform for Exemptia. We earn royalties on sales by Zydus Cadila for ten years following approval.

Zydus Cadila’s Vivitra (trastuzumab biosimilar) is marketed in India for breast cancer. Zydus Cadila uses the Selexis technology platform for Vivitra. We are entitled to earn royalties on sales by Zydus Cadila for ten years following approval.

Zydus Cadila’s Bryxta and Zybev (bevacizumab biosimilar) is marketed in India for various indications. Zydus Cadila uses the Selexis technology platform for Bryxta and Zybev. We earn royalties on sales by Zydus Cadila for ten years following approval.

FYCOMPA IV (Eisai)

Our partner, Eisai, is developing an intravenous Fycompa® (perampanel), formulated with Captisol, as a substitute in Japan for oral tablets as an adjunctive therapy in patients with partial onset seizures (including secondarily generalized seizures) or primary generalized tonic-clonic seizures. In January of 2023, Eisai announced that it obtained marketing authorization approval from the Japanese Ministry of Health, Labour and Welfare for the injection formulation of its in-house discovered antiepileptic drug (AED) Fycompa in Japan as an alternative therapy when oral administration is temporarily not possible. We are entitled to revenue from Captisol material sales and tiered royalties on potential future sales.

Key Partnered Pipeline Programs

We have a highly diversified partnered pipeline of development stage assets that either have or are nearing regulatory approval, or given the area of research or value of the license terms, we consider particularly noteworthy. We are eligible to receive milestone payments and royalties on these programs. This list does not include all of our partnered programs. In the case of Captisol-related programs, we are also eligible to receive revenue for the sale of Captisol material supply. The following table represents development-stage assets with disclosed royalty rates:

10

| Development stage assets with disclosed royalties | ||||||||

| Program | Licensee | Royalty Rate | ||||||

| Ciforadenant | Corvus | Mid-single digit to low-teen royalty | ||||||

| DGAT-1 | Viking | 3.0% - 7.0% | ||||||

| Ensifentrine (RPL554) | Verona | Low single digit royalty | ||||||

| FBPase Inhibitor (VK0612) | Viking | 7.5% - 9.5% | ||||||

| Lasofoxifene | Sermonix | 6.0% - 10.0% | ||||||

| MB07133 | Xi'an Xintong | 6% | ||||||

| ME-344 | MEI Pharma | Low single digit royalty | ||||||

| Oral EPO | Viking | 4.5% - 8.5% | ||||||

| Pradefovir | Xi'an Xintong | 9% | ||||||

| PTX-022 | Palvella | 8.0% - 9.8% | ||||||

| SARM (VK5211) | Viking | 7.25% - 9.25% | ||||||

| TR Beta (VK2809 and VK0214) | Viking | 3.5% - 7.5% | ||||||

| Various | Nucorion | 4.0% - 9.0% | ||||||

| Various | Seelos | 4.0% - 10.0% | ||||||

TR-Beta - VK2809 and VK0214 (Viking)

Our partner, Viking, is developing VK2809, a novel selective thyroid hormone receptor beta (TR-beta) agonist with potential in multiple indications, including hypercholesterolemia, dyslipidemia and non-alcoholic steatohepatitis (NASH). VK2809 is currently in a Phase 2b clinical trial (the VOYAGE study) in patients with biopsy-confirmed NASH. VK0214, another novel, orally available, TR-beta agonist, is in development for the potential treatment of X-linked adrenoleukodystrophy (X-ALD). VK0214 is currently being evaluated in a Phase 1b clinical trial in patients with the adrenomyeloneuropathy (AMN) form of X-ALD. Under the terms of the agreement with Viking, we may be entitled to up to $375 million of development, regulatory and commercial milestones and tiered royalties on potential future sales. Our TR Beta programs partnered with Viking are subject to CVR sharing and a portion of the cash received will be paid out to CVR holders.

In November 2023, Viking presented new results from the ongoing Phase 2b clinical trial of VK2809, a novel liver-selective thyroid hormone receptor beta agonist, in patients with biopsy-confirmed NASH. The latest findings from the VOYAGE study were featured in a late breaking poster presentation at the Liver Meeting® 2023, the annual meeting of the American Association for the Study of Liver Diseases. The newly reported findings demonstrated robust and comparable liver fat reductions in patients with or without Type 2 diabetes, as well as patients with either F2 or F3 fibrosis.

Ensifentrine – RPL554 (Verona)

Ensifentrine is a first-in-class, selective, dual inhibitor of phosphodiesterase 3 and 4 enzymes combining bronchodilator and non-steroidal anti-inflammatory activities in one compound. Ligand obtained the rights to ensifentrine in 2018 in the acquisition of Vernalis. Our partner, Verona Pharma, recently completed the Phase 3 ENHANCE-21 and ENHANCE-12 trials evaluating nebulized ensifentrine for the maintenance treatment of chronic obstructive pulmonary disease (COPD) and the NDA was accepted by the U.S. FDA in September 2023. The PDUFA date for ensifentrine is June 26, 2024. Under the terms of our agreement with Verona, we are entitled to development and regulatory milestones, including a £5.0 million payment upon the first approval by any regulatory authority, and low single digit royalties on potential future sales.

Verona recently announced that it has entered into a debt financing facility providing the company with access to up to $400 million from funds managed by Oxford Finance LLC and Hercules Capital, Inc. The debt facility provides non-dilutive capital and further financial flexibility to support Verona Pharma’s continued growth, including the planned commercial launch of ensifentrine.. The debt facility replaces the existing facility of up to $150 million with an affiliate of Oxford.

Soticlestat (Takeda)

In the fourth quarter of 2023, we entered into an agreement with Ovid Therapeutics for a 13% interest in soticlestat royalties. Ovid sold its rights in soticlestat to Takeda in 2021. Under the terms of its agreement with Takeda, Ovid is eligible to receive regulatory and commercial milestone payments of up to $660 million, as well as tiered royalties on net sales of soticlestat at percentages ranging from the low-double-digits up to 20%, if soticlestat is approved and successfully commercialized. Takeda is currently studying soticlestat in two pivotal Phase 3 trials in people with Lennox-Gastaut syndrome (LGS) and Dravet

11

syndrome (DS) and announced that it anticipates regulatory filings for soticlestat in its fiscal year 2024. Ovid has no ongoing obligations or costs associated with the development of soticlestat.

Soticlestat is a potent, highly selective, first-in-class inhibitor of the enzyme cholesterol 24-hydroxylase (CH24H), with the potential to reduce seizure susceptibility and improve seizure control. CH24H is predominantly expressed in the brain, where it converts cholesterol into 24S-hydroxycholesterol (24HC) to adjust the homeostatic balance of brain cholesterol. 24HC is a positive allosteric modulator of the NMDA receptor and modulates glutamatergic signaling associated with epilepsy. Glutamate is one of the main neurotransmitters in the brain and has been shown to play a role in the initiation and spread of seizure activity. Recent literature indicates that CH24H is involved in over-activation of the glutamatergic pathway through modulation of the NMDA channel and that increased expression of CH24H can disrupt the reuptake of glutamate by astrocytes, resulting in epileptogenesis and neurotoxicity. Inhibition of CH24H by soticlestat reduces the neuronal levels of 24HC and may improve excitatory/inhibitory balance of NMDA channel activity.

Under the terms of our agreement with Ovid, we are entitled to receive regulatory and sales-based milestones of up to $85.8 million as well as 13% of royalties received by Ovid.

Ganaxalone IV (Marinus)

Our partner, Marinus, is conducting Phase 3 clinical trials with Captisol-enabled ganaxolone IV in patients with refractory status epilepticus. Marinus has exclusive worldwide rights to Captisol-enabled ganaxolone, a GABAA receptor modulator, for use in humans. We are entitled to development and regulatory milestones, revenue from Captisol material sales, and royalties on potential future sales.

Ciforadenant – CPI-444 (Corvus)

Our partner, Corvus, is conducting a Phase 1b/2 clinical trial evaluating ciforadenant as a potential first line therapy for metastatic renal cell cancer (RCC) in combination with ipilimumab (anti-CTLA-4) and nivolumab (anti-PD-1). The Phase 1b/2 study is being conducted by the Kidney Cancer Research Consortium (KCRC) and is led by The University of Texas MD Anderson Cancer Center. Under the terms of our agreement with Corvus, we are entitled to development and regulatory milestones and tiered royalties on potential future sales. The aggregate potential milestone payments from Corvus are approximately $220 million for all indications.

QTORIN (Palvella)

We acquired the economic rights to QTORIN™ 3.9% rapamycin anhydrous gel (QTORIN™ rapamycin, formerly PTX-022) from Palvella in December 2018. QTORIN™ rapamycin is a novel, topical formulation of high-strength rapamycin currently in development for the treatment of Microcystic Lymphatic Malformations (Microcystic LM). In November 2023, Palvella announced that the FDA granted Breakthrough Therapy Designation to QTORIN rapamycin for the treatment of microcystic LMs. Microcystic LMs is a chronically debilitating and lifelong genetic disease affecting an estimated more than 30,000 patients in the U.S. There are currently no FDA-approved treatments for microcystic LMs.

Lasofoxifene (Sermonix)

Lasofoxifene is a selective estrogen receptor modulator for osteoporosis treatment and other diseases, discovered through the research collaboration between Pfizer and Ligand. Our partner, Sermonix has a license for the development of oral lasofoxifene, its lead investigational drug, for the United States and additional territories. Sermonix is currently conducting the Phase 3 ELAINE-3 clinical trial to assess the efficacy of lasofoxifene in combination with Eli Lilly and Company’s CDK4/6 inhibitor abemaciclib (Verzenio®) compared to fulvestrant and abemaciclib in pre- and post-menopausal subjects with locally advanced or metastatic ER+/HER2- breast cancer with an ESR1 mutation. Under the terms of the agreement, we are entitled to receive over $45 million in potential regulatory and commercial milestone payments as well as royalties on potential future net sales.

In January 2024, Sermonix announced it entered into a strategic collaboration and exclusive license agreement with Henlius for the rights to develop, manufacture and commercialize lasofoxifene in China. Under the terms of the agreement, Henlius will receive exclusive rights and sublicenses to lasofoxifene for at least two estrogen receptor-positive (ER+)/HER2- breast cancer indications in the territory, with Sermonix retaining all other global rights. Sermonix plans to work with Henlius to accelerate the clinical development of the Phase 3 ELAINE-3 multi-regional clinical trial in China, making lasofoxifene available to Chinese patients as soon as possible. In December 2023, Sermonix activated and began enrollment for ELAINE-3 in the United States.

Pradefovir (Xi'an Xintong)

Our Chinese licensee, Xi'an Xintong Medicine Research (following its acquisition of Chiva Pharmaceuticals), is developing pradefovir, an oral liver-targeting prodrug of the HBV DNA polymerase/reverse transcriptase inhibitor adefovir, for the potential treatment of HBV infection. Pradefovir was developed using Ligand’s HepDirect technology. Xi'an Xintong

12

submitted the pradefovir NDA in May 2023, and it is under priority review by the Chinese FDA (NMPA). We are entitled to an annual licensing maintenance fee and royalties on potential future sales.

MB07133 (Xi'an Xintong)

Chinese licensee Xi'an Xintong Medicine Research is also developing MB07133, a liver specific, HepDirect prodrug of cytarabine monophosphate, for the potential treatment of hepatocellular carcinoma and intrahepatic cholangiocarcinoma. MB07133 is currently in Phase 2 in China. We are entitled to an annual licensing maintenance fee and royalties on potential future sales.

Milestone Payments

Our programs under license with our partners may generate milestone payments to us if our partners reach certain development, regulatory and commercial milestones. The following table represents the maximum value of our milestone payment pipeline by technology, development stage and partner (in millions):

| Technology* | Stage* | Partner* | |||||||||||||||||||||

| Pelican | >$195.0 | Preclinical | > $1.0 | Viking | $950.0 | ||||||||||||||||||

| Captisol | > $170.0 | Clinical | > $80.0 | Jazz | $150.0 | ||||||||||||||||||

| LTP/Hep Direct/BEPro | > $330.0 | Regulatory | > $800.0 | Travere | $50.0 | ||||||||||||||||||

| NCE/Other | > $1,200.0 | Commercial | > $900.0 | Other | >$750.0 | ||||||||||||||||||

| Total | >$1,900.0 | Total | >$1,900.0 | Total | >$1,900.0 | ||||||||||||||||||

*All tables exclude any annual access fees and collaboration revenue for development work.

Full Portfolio Details

We have assembled one of the largest portfolios of biopharmaceutical assets in the industry which provides investors the opportunity to participate in the biotech industry while mitigating the industry’s usual inherent clinical binary risks. Our portfolio consists of assets which currently generate revenue through royalties on commercial products as well as Captisol sales on commercial products. In addition to these assets, we have a substantial pipeline of development stage assets that currently generate contractual payments through milestone and license fees with future potential for royalties and Captisol material sales for those programs under our Captisol technology.

| Approved | ||||||||

| Partner Name | Program | Therapeutic Area | ||||||

| Acrotech/CASI | Evomela | Cancer | ||||||

| Alvogen/Adalvo | Teriparatide | Women's Health | ||||||

| Alvogen/Hikma/Nanjing King-Friend | Voriconazole | Infectious Disease | ||||||

| Amgen/Beigene/Ono | Kyprolis | Cancer | ||||||

| Baxter | Nexterone | Cardiovascular | ||||||

| Biocad | Teberif | Inflammatory/Metabolic | ||||||

| Eisai | FYCOMPA | Central Nervous System | ||||||

| Elutia | ECM portfolio | Medical device/Cardiology | ||||||

| Exelixis/Daiichi-Sankyo | Minnebro | Cardiovascular | ||||||

| Gilead | Veklury | Infectious Disease | ||||||

| Ingenus | ML-141 | Cancer | ||||||

| Jazz | Rylaze | Cancer | ||||||

| Melinta | Baxdela | Infectious Disease | ||||||

| Menarini | Frovatriptan | Central Nervous System | ||||||

| Fareva | Noxafil-IV | Infectious Disease | ||||||

| Merck | Vaxneuvance | Infectious Disease | ||||||

| Novan | SB206 | Infectious Disease | ||||||

13

| Novartis | Mekinist | Cancer | ||||||

| Par | Posaconazole | Infectious Disease | ||||||

| Pfizer | Duavee | Inflammatory/Metabolic | ||||||

| Pfizer | Vfend-IV | Infectious Disease | ||||||

| Sage | Zulresso | Central Nervous System | ||||||

| Sanofi | Tzield | Metabolic | ||||||

| Sedor/Lupin | Sesquient | Central Nervous System | ||||||

| Serum Institute of India | Pneumosil | Infectious Disease | ||||||

| Serum Institute of India | Meningococcal | Infectious Disease | ||||||

| Travere | Filspari | Metabolic | ||||||

| Zydus Cadila | Vivitra | Cancer | ||||||

| Zydus Cadila | Bryxta/ZyBev | Cancer | ||||||

| Zydus Cadila | Maropitant | Central Nervous System | ||||||

| Zydus Cadila | Exemptia | Inflammatory/Metabolic | ||||||

| Zydus Cadila | Vortuxi | Inflammatory/Metabolic | ||||||

| Phase 3/Pivotal or Regulatory Submission Stage | ||||||||

| Partner Name | Program | Therapeutic Area | ||||||

| Aldeyra | Reproxalap | Other/Undisclosed | ||||||

| BendaRx | Bendamustine | Oncology | ||||||

| Marinus | Ganaxalone IV | Central Nervous System | ||||||

| Merck | V116 | Pneumococcal adult | ||||||

| Ohara Pharmaceuticals | JPH203 | Cancer | ||||||

| Opthea | OPT-302 | Ophthalmology | ||||||

| Outlook Therapeutics | ONS-5010 | Other/Undisclosed | ||||||

| Palvella | PTX-022 | Other/Undisclosed | ||||||

| Sermonix | Lasofoxifene | Cancer | ||||||

| SQ Innovation | CE-Furosemide | Cardiovascular disease | ||||||

| Sunshine Lake | Vilazodone | Central Nervous System | ||||||

| Takeda | Soticlestat | Central Nervous System | ||||||

| Verona | Ensifentrine (RPL554) | Respiratory Disease | ||||||

| Xi'an Xintong | Pradefovir | Infectious Disease | ||||||

| Phase 2 | ||||||||

| Partner Name | Program | Therapeutic Area | ||||||

| Acrivon | ACR-368 | Cancer | ||||||

| Anebulo | ANEB-001 | Central Nervous System | ||||||

| Corvus | Ciforadenant | Cancer | ||||||

| CurX | CE-Topiramate | Central Nervous System | ||||||

| Phoenix Tissue | PTR-01 | Genetic Disease | ||||||

| Oncternal | Zilovertamab | Cancer | ||||||

| Sato | SB206 (Japan) | Infectious Disease | ||||||

14

| Takeda | TAK-981 | Cancer | ||||||

| Takeda | TAK-925 | Central Nervous System | ||||||

| Verona | Ensifentrine | Asthma | ||||||

| Verona | Ensifentrine | Cystic Fibrosis | ||||||

| Viking | VK5211 | Inflammatory/Metabolic | ||||||

| Viking | VK2809 | Inflammatory/Metabolic | ||||||

| Xi'an Xintong | MB07133 | Cancer | ||||||

| Phase 1 | ||||||||

| Partner Name | Program | Therapeutic Area | ||||||

| Apotex | Meloxicam | Migraine | ||||||

| Arcellx | ACLX-001 | Cancer | ||||||

| Arcellx | ACLX-002 | Cancer | ||||||

| China Resources Double Crane | CX2101A | COVID 19 | ||||||

| CSL | CSL-324 | Immunology | ||||||

| Jazz | JZP-341 | Long Acting Erwinia Asparaginase | ||||||

| Jupiter Biomedical Research | Viright | Cancer | ||||||

| MEI Pharma | ME-344 | Cancer | ||||||

| Merck | V117 | Pneumococcal | ||||||

| Novartis | MIK-665 | Cancer | ||||||

| Nucorion | NUC-1010 | Infectious disease | ||||||

| Revision Therapeutics | Rev0100 | Ophthalmology | ||||||

| Sage | SAGE-689 | Central Nervous System | ||||||

| Takeda | TAK-243 | Cancer | ||||||

| Vaxxas | Nanopatch | Infectious Disease | ||||||

| Viking | VK-0214 | Genetic Disease | ||||||

Summary of selected programs available for license

In addition to Zelsuvmi, discussed above, we have a number of unpartnered programs focused on a wide-range of potential indications or diseases with the potential for further development or licensing:

| Program | Development Stage | Targeted Indication or Disease | ||||||||||||

| CE-Iohexol | Phase 2 | Diagnostics | ||||||||||||

| Luminespib/Hsp90 Inhibitor | Phase 2 | Oncology | ||||||||||||

| CE-Sertraline, Oral Concentrate | Phase 1 | Depression | ||||||||||||

| CCR1 Antagonist | Preclinical | Oncology | ||||||||||||

| CE-Busulfan | Preclinical | Oncology | ||||||||||||

| CE-Cetirizine Injection | Preclinical | Allergy | ||||||||||||

| CE-Silymarin for Topical formulation | Preclinical | Sun damage | ||||||||||||

| FLT3 Kinase Inhibitors | Preclinical | Oncology | ||||||||||||

| GCSF Receptor Agonist | Preclinical | Blood disorders | ||||||||||||

15

Manufacturing

We contract with a third-party manufacturer, Hovione, for Captisol production. Hovione operates FDA-inspected sites in the United States, Macau, Ireland and Portugal. Manufacturing operations for Captisol are performed primarily at Hovione's Portugal and Ireland facilities. We believe we maintain adequate inventory of Captisol to meet our current partner needs and that our Captisol capacity will be sufficient to meet future partner needs.

In the event of a Captisol supply interruption, we are permitted to designate and, with Hovione’s assistance, qualify one or more alternate suppliers. If the supply interruption continues beyond a designated period, we may terminate the agreement. In addition, if Hovione cannot supply our requirements of Captisol due to an uncured force majeure event, we may also obtain Captisol from a third party and have previously identified such parties.

The current term of the agreement with Hovione is through December 2024. The agreement will automatically renew for successive two-year renewal terms unless either party gives written notice of its intention to terminate the agreement no less than two years prior to the expiration of the initial term or renewal term. In addition, either party may terminate the agreement for the uncured material breach or bankruptcy of the other party or an extended force majeure event. We may terminate the agreement for extended supply interruption, regulatory action related to Captisol or other specified events. We have ongoing minimum purchase commitments under the agreement.

Competition

Some of the drugs we and our licensees and partners are developing may compete with existing therapies or other drugs in development by other companies. Furthermore, academic institutions, government agencies and other public and private organizations conducting research may seek patent protection with respect to potentially competing products or technologies and may establish collaborative arrangements with our competitors.

Our Captisol business may face competition from other suppliers of similar cyclodextrin excipients or other technologies that are aimed to increase solubility or stability of APIs.

Our competitive position also depends upon our ability to obtain patent protection or otherwise develop proprietary products or processes. For a discussion of the risks associated with competition, see below under “Item 1A. Risk Factors.”

Corporate and Governance Highlights

We are committed to policies and practices focused on environmental sustainability, positively impacting our social community and maintaining and cultivating good corporate governance. By focusing on such ESG policies and practices, we believe we can affect a meaningful and positive change in our community and maintain our open, collaborative corporate culture. We will continue our proactive shareholder and employee engagement in 2024. See www.ligand.com for information about our ESG policies and practices. However, note that the information contained on our website is not intended to be part of this filing.

Environmental, Health and Safety (EHS)

We are committed to providing a safe and healthy workplace, promoting environmental excellence in our communities, and complying with all relevant regulations and industry standards. We establish and monitor programs to reduce pollution, prevent injuries, and maintain compliance with applicable regulations. By focusing on such practices, we believe we can affect a meaningful, positive change in our community and maintain a healthy and safe environment. During 2023, we progressed our $2.5 million solar investment at Kansas University Innovation Park; made Environmental, Social and Governance (ESG) related charitable donations; and evolved numerous programs from our ESG-focused outreach committees. We expect to continue our effort and to refine our EHS policies and practices in 2024. More information on our EHS policies and initiatives is available on our website at www.ligand.com. However, note that the information contained on our website is not intended to be part of this filing.

Government Regulation

The research and development, manufacturing and marketing of pharmaceutical products are subject to regulation by numerous governmental authorities in the United States and other countries. We and our partners, depending on specific activities performed, are subject to these regulations. In the United States, pharmaceuticals are subject to regulation by both federal and various state authorities, including the FDA. The Federal Food, Drug and Cosmetic Act and the Public Health Service Act govern the research and development, testing, manufacture, quality, safety, efficacy, labeling, storage, record keeping, approval, advertising and promotion of pharmaceutical products. These activities are subject to additional regulations that apply at the state level. There are similar regulations in other countries as well. For both currently marketed products and products in development, failure to comply with applicable regulatory requirements at any time during the product development process, approval process or after approval, can, among other things, result in delays, the suspension of regulatory approvals, regulatory enforcement

16

actions, as well as possible civil and criminal sanctions. In addition, changes in existing regulations could have a material adverse effect on us or our partners.

In particular, FDA approval is required before a drug or biological product may be marketed in the United States and they are also subject to other federal, state, and local statutes and regulations. The process required by the FDA before pharmaceutical products may be marketed in the United States generally involves the following:

•completion of extensive preclinical laboratory tests and preclinical animal studies, certain of which must performed in accordance with Good Laboratory Practice regulations and other applicable requirements ;

•submission to the FDA of an IND application, which must become effective before human clinical studies may begin;

•approval by an independent institutional review board or ethics committee at each clinical site before each clinical study may be initiated;

•performance of adequate and well-controlled human clinical studies in accordance with Good Clinical Practice (GCP) requirements to establish the safety and efficacy, or with respect to biologics, the safety, purity and potency of the product candidate for each proposed indication;

•preparation of and submission to the FDA of an NDA or BLA after completion of all pivotal clinical studies that include substantial evidence of safety, purity, and potency of the drug from analytical studies and from results of nonclinical testing and clinical trials;

•satisfactory completion of an FDA advisory committee review, where appropriate and if applicable;

•a determination by the FDA within 60 days of its receipt of an NDA or BLA to file the application for review;

•satisfactory completion of an FDA inspection of the manufacturing facility or facilities where the proposed product is produced to assess compliance with cGMP, and potential FDA inspection of nonclinical study and clinical trial sites that generated the data in support of the NDA or BLA to ensure compliance with GCP; and

•FDA review and approval of an NDA or BLA prior to any commercial marketing or sale of the drug in the United States.

Any products manufactured or distributed pursuant to FDA approvals are subject to pervasive and continuing regulation by the FDA, including, among other things, requirements relating to record-keeping, reporting of adverse experiences, periodic reporting, product sampling and distribution, and advertising and promotion of the product. There also are continuing user fee requirements, under which the FDA assesses an annual program fee for each product identified in an approved NDA or BLA. Drug and biologic manufacturers and their subcontractors are required to register their establishments with the FDA and some state agencies, and are subject to periodic unannounced inspections by the FDA and some state agencies for compliance with cGMPs, which among other things, impose certain procedural and documentation requirements upon BLA or NDA holders and any third-party manufacturers. FDA regulations also require investigation and correction of any deviations from cGMPs and impose reporting requirements upon manufacturers and their subcontractors. Accordingly, manufacturers must continue to expend time, money and effort in the area of production and quality control to maintain compliance with cGMPs and other aspects of regulatory compliance.

The FDA closely regulates the marketing, labeling, advertising and promotion of drug products and biologics. A company can make only those claims relating to safety and efficacy, purity and potency that are approved by the FDA and in accordance with the provisions of the approved label. The FDA and other agencies actively enforce the laws and regulations prohibiting the promotion of off-label uses. Failure to comply with these requirements can result in, among other things, adverse publicity, warning letters, corrective advertising and potential civil and criminal penalties

The FDA may withdraw approval if compliance with regulatory requirements and standards is not maintained or if problems occur after the product reaches the market. Later discovery of previously unknown problems with a product, including adverse events of unanticipated severity or frequency, or with manufacturing processes, or failure to comply with regulatory requirements, may result in revisions to the approved labeling to add new safety information; imposition of post-market studies or clinical studies to assess new safety risks; or imposition of distribution restrictions or other restrictions under a REMS program. Other potential consequences for non-compliance include, among other things:

•restrictions on the marketing or manufacturing of a product, complete withdrawal of the product from the market or product recalls;

•fines, warning letters or holds on post-approval clinical studies;

17

•refusal of the FDA to approve pending applications or supplements to approved applications, or suspension or revocation of existing product approvals;

•product seizure or detention, or refusal of the FDA to permit the import or export of products;

•consent decrees, corporate integrity agreements, debarment or exclusion from federal healthcare programs;

•mandated modification of promotional materials and labeling and the issuance of corrective information;

•the issuance of safety alerts, Dear Healthcare Provider letters, press releases and other communications containing warnings or other safety information about the product; or

•injunctions or the imposition of civil or criminal penalties.

For a discussion of the risks associated with government regulations, see below under “Item 1A. Risk Factors.”

Patents and Proprietary Rights

We believe that patents and other proprietary rights are important to our business. Our policy is to file patent applications to protect technology, inventions and improvements to our inventions that are considered important to the development of our business. We also rely upon trade secrets, know-how, continuing technological innovations and licensing opportunities to develop and maintain our competitive position.

Patents are issued or pending for the following key products or product families. The scope and type of patent protection provided by each patent family is defined by the claims in the various patents. Patent term may vary by jurisdiction and depend on a number of factors including potential patent term adjustments, patent term extensions, and terminal disclaimers. For each product or product family, the patents and/or applications referred to are in force in at least the United States, and for most products and product families, the patents and/or applications are also in force in European jurisdictions, Japan and other jurisdictions.

Captisol