Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06629

Western Asset Managed Municipals Fund Inc.

Exact name of registrant as specified in charter)

620 Eighth Avenue, 49th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 777-0102

Date of fiscal year end: May 31

Date of reporting period: May 31, 2017

Table of Contents

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

Table of Contents

| Annual Report | May 31, 2017 |

WESTERN ASSET

MANAGED MUNICIPALS FUND INC. (MMU)

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Table of Contents

Fund objective

The Fund seeks to maximize current income exempt from federal income tax* as is consistent with preservation of principal.

The Fund seeks to achieve its objective by investing primarily in long-term investment grade municipal debt securities issued by state and local governments, political subdivisions, agencies and public authorities (municipal obligations). Under normal market conditions, the Fund will invest at least 80% of its total assets in municipal obligations rated investment grade at the time of investment.

Dear Shareholder,

We are pleased to provide the annual report of Western Asset Managed Municipals Fund Inc. for the twelve-month reporting period ended May 31, 2017. Please read on for a detailed look at prevailing economic and market conditions during the Fund’s reporting period and to learn how those conditions have affected Fund performance.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.lmcef.com. Here you can gain immediate access to market and investment information, including:

| • | Fund prices and performance, |

| • | Market insights and commentaries from our portfolio managers, and |

| • | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

Chairman, President and Chief Executive Officer

June 30, 2017

| * | Certain investors may be subject to the federal alternative minimum tax (“AMT”), and state and local taxes will apply. Capital gains, if any, are fully taxable. Please consult your personal tax or legal adviser. |

| II | Western Asset Managed Municipals Fund Inc. |

Table of Contents

Economic review

The pace of U.S. economic activity fluctuated during the twelve months ended May 31, 2017 (the “reporting period”). Looking back, the U.S. Department of Commerce reported that second quarter 2016 U.S. gross domestic product (“GDP”)i growth was 1.4%. GDP growth for the third quarter of 2016 was 3.5%, the strongest reading in two years. However, fourth quarter 2016 GDP growth then moderated to 2.1%. Finally, the U.S. Department of Commerce’s final reading for first quarter 2017 GDP growth — released after the reporting period ended — was 1.4%. The deceleration in growth reflected downturns in private inventory investment and personal consumption expenditures, along with more modest state and local government spending.

Job growth in the U.S. was solid overall and a tailwind for the economy during the reporting period. When the reporting period ended on May 31, 2017, the unemployment rate was 4.3%, as reported by the U.S. Department of Labor. This was the lowest unemployment rate since May 2001. The percentage of longer-term unemployed also declined over the period. In May 2017, 24.0% of Americans looking for a job had been out of work for more than six months, versus 25.8% when the period began.

Looking back, after an extended period of maintaining the federal funds rateii at a historically low range between zero and 0.25%, the Federal Reserve Board (the “Fed”)iii increased the rate at its meeting on December 16, 2015. This marked the first rate hike since 2006. In particular, the U.S. central bank raised the federal funds rate to a range between 0.25% and 0.50%. The Fed then kept rates on hold at each meeting prior to its meeting in mid-December 2016. On December 14, 2016, the Fed raised rates to a range between 0.50% and 0.75%.

After holding rates steady at its meeting that concluded on February 1, 2017, the Fed raised rates to a range between 0.75% and 1.00% at its meeting that ended on March 15, 2017. Finally, at its meeting that concluded on June 14, 2017 — after the reporting period ended — the Fed raised rates to a range between 1.00% and 1.25%. The Fed also said that it planned to reduce its balance sheet, saying, “The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee currently expects to begin implementing a balance sheet normalization program this year, provided that the economy evolves broadly as anticipated.”

As always, thank you for your confidence in our stewardship of your assets.

Sincerely,

Jane Trust, CFA

Chairman, President and Chief Executive Officer

June 30, 2017

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results.

| Western Asset Managed Municipals Fund Inc. | III |

Table of Contents

Investment commentary (cont’d)

| i | Gross domestic product (“GDP”) is the market value of all final goods and services produced within a country in a given period of time. |

| ii | The federal funds rate is the rate charged by one depository institution on an overnight sale of immediately available funds (balances at the Federal Reserve) to another depository institution; the rate may vary from depository institution to depository institution and from day to day. |

| iii | The Federal Reserve Board (the “Fed”) is responsible for the formulation of U.S. policies designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments. |

| IV | Western Asset Managed Municipals Fund Inc. |

Table of Contents

Q. What is the Fund’s investment strategy?

A. The Fund seeks to maximize current income exempt from federal income tax as is consistent with preservation of principal. We select securities primarily by identifying undervalued sectors and individual securities, while also selecting securities that we believe will benefit from changes in market conditions.

Under normal market conditions, the Fund invests primarily in investment grade municipal bonds, but it can also invest up to 20% of its total assets in municipal bonds rated below investment grade by a nationally recognized statistical rating organization or, if unrated, determined to be of equivalent quality. The Fund may also use a variety of derivative instruments for investment purposes, as well as for hedging or risk-management purposes.

At Western Asset Management Company (“Western Asset”), the Fund’s subadviser, we utilize a fixed-income team approach, with decisions derived from interaction among various investment management

sector specialists. The sector teams are comprised of Western Asset’s senior portfolio management personnel, research analysts and an in-house economist. Under this team approach, management of client fixed-income portfolios will reflect a consensus of interdisciplinary views within the Western Asset organization. Effective August 1, 2016, the individuals responsible for development of investment strategy, day-to-day portfolio management, oversight and coordination of the Fund are S. Kenneth Leech, Robert E. Amodeo and David T. Fare.

Q. What were the overall market conditions during the Fund’s reporting period?

A. The overall fixed income market experienced periods of volatility and generated a modest gain over the twelve-month reporting period ended May 31, 2017. The spread sectors (non-Treasuries) generally rallied from June 2016 through September 2016, as concerns over global growth moderated, energy prices stabilized and the Federal Reserve Board’s (the “Fed”)i monetary policy remained accommodative. This rally occurred even as the market overcame several headwinds, including questions related to global monetary policy, implications of the U.K.’s referendum to leave the European Union (“Brexit”) and a number of geopolitical issues. U.S. Treasury yields then moved sharply higher and most segments of the fixed income market posted weak results from October 2016 through the end of December 2016 (yields and prices move in the opposite direction). This turnaround was triggered by expectations for improving economic growth and higher inflation due to potential fiscal stimulus from President Donald Trump’s administration. In addition, for the first time in a year the Fed raised rates in December 2016. The U.S. central bank also indicated that it may institute more rate hikes in 2017 than it had previously projected. However, the spread sectors then regained their footing over the last five months of the period, as Treasury yields generally edged lower, even though the Fed again raised rates in March 2017.

Both short- and long-term Treasury yields moved higher during the reporting period as a whole. The yields for the two-year Treasury began the reporting period at 0.87% and

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 1 |

Table of Contents

Fund overview (cont’d)

ended the period at 1.28%. Their peak of 1.40% occurred on both March 13 and March 14, 2017, and they were as low as 0.56% on July 5, 2016. The yields for the ten-year Treasury were 1.84% at the beginning of the period and ended the period at 2.21%. Their peak of 2.62% was on March 13, 2017, and their low of 1.37% occurred on both July 5 and July 8, 2016.

The municipal bond market modestly underperformed its taxable bond counterpart during the twelve-month reporting period. Over that time, the Bloomberg Barclays Municipal Bond Indexii and the Bloomberg Barclays U.S. Aggregate Indexiii returned 1.46% and 1.58%, respectively. After posting positive returns over the first three months of the reporting period, the municipal market declined from September through November 2016. This turnaround occurred as yields moved higher, municipal supply increased and investor demand weakened. The municipal market then generally rallied over the last six months of the period as long-term yields stabilized and then edged lower, supply moderated and investor demand improved.

Q. How did we respond to these changing market conditions?

A. A number of adjustments were made to the Fund during the reporting period. Our allocation to the Health Care sector declined during the reporting period, as several securities were pre-refundediv. As a byproduct of this, the Fund’s Pre-Refunded securities exposure increased during the period. The Fund’s exposure to State General Obligation bonds increased as we identified several individual securities that we felt were attractively valued. Finally, post the U.S. presidential election, we modestly increased the Fund’s durationv. This adjustment was consistent with our view that relatively “safe haven” assets (U.S. Treasuries and municipals) were oversold and the prices of risky assets were vulnerable. In our view, the long end of the municipal market continues to be attractive relative to Treasuries.

We employed the use of U.S. Treasury futures during the reporting period to manage duration. This strategy contributed to the Fund’s performance.

During the reporting period, we utilized leverage in the Fund. We generally maintained liabilities as a percentage of gross assets of approximately 29% during the period. The use of leverage was additive for results given the positive performance of the municipal bond market over the twelve months ended May 31, 2017.

Performance review

For the twelve months ended May 31, 2017, Western Asset Managed Municipals Fund Inc. returned 1.16% based on its net asset value (“NAV”)vi and -1.31% based on its New York Stock Exchange (“NYSE”) market price per share. The Fund’s unmanaged benchmark, the Bloomberg Barclays Municipal Bond Index, returned 1.46% for the same period. The Lipper General & Insured Municipal Debt (Leveraged) Closed-End Funds Category Averagevii returned 0.93% over the same time frame. Please note that Lipper performance returns are based on each fund’s NAV.

Certain investors may be subject to the federal alternative minimum tax, and state and local taxes will apply. Capital gains, if any, are fully taxable. Please consult your personal tax or legal adviser.

| * | For the tax character of distributions paid during the fiscal year ended May 31, 2017, please refer to page 36 of this report. |

| 2 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

During the twelve-month period, the Fund made distributions to shareholders totaling $0.77 per share.* The performance table shows the Fund’s twelve-month total return based on its NAV and market price as of May 31, 2017. Past performance is no guarantee of future results.

| Performance Snapshot as of May 31, 2017 | ||||

| Price Per Share | 12-Month Total Return† |

|||

| $13.99 (NAV) | 1.16 | %‡ | ||

| $13.84 (Market Price) | -1.31 | %‡‡ | ||

All figures represent past performance and are not a guarantee of future results.

† Total returns are based on changes in NAV or market price, respectively. Returns reflect the deduction of all Fund expenses, including management fees, operating expenses, and other Fund expenses. Returns do not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the sale of shares.

‡ Total return assumes the reinvestment of all distributions at NAV.

‡‡ Total return assumes the reinvestment of all distributions in additional shares in accordance with the Fund’s Dividend Reinvestment Plan.

Q. What were the leading contributors to performance?

A. The largest contributor to the Fund’s relative performance during the reporting period was its duration positioning. We tactically adjusted the Fund’s duration given the changing market environment.

Our positioning in a number of sectors was beneficial for performance. In particular, security selection within and overweights to the Industrial Revenue and Transportation sectors were additive for results, as was security selection in the Education sector. Elsewhere, our Pre-Refunded securities holdings were positive for performance.

The Fund’s quality biases overall also contributed to results. Overweights to municipal securities rated A and BBB, along with underweights to municipal securities rated AAA and AA, were rewarded, as lower-rated, higher yielding securities generally outperformed their higher-rated counterparts over the reporting period.

Q. What were the leading detractors from performance?

A. The largest detractor from the Fund’s relative performance during the reporting period was its security selection of debt issued by the U.S. Virgin Islands. In particular, the Fund was negatively impacted by having a small overweight position relative to the benchmark in the U.S. Virgin Island’s debt backed by U.S. rum sales. These bonds were downgraded due to the U.S. Virgin Islands’ weak fiscal condition and structural budget imbalances. The ratings agencies also changed their methodology in rating U.S. territory debt to reflect the risks associated with a Puerto Rico Oversight, Management, and Economic Stability Act (“PROMESA”) type legislation. This change in methodology could provide a legal framework to restructure any territory debt in the event of insolvency. The governor of the U.S. Virgin Islands recently crafted a five-year plan and the senate enacted several tax increases and proposed spending cuts equal to 10% of its budget.

Elsewhere, security selection in the Leasing sectors and our State General Obligation bonds were headwinds for results during the reporting period. Finally, an overweight to municipal securities rated BB was a drag on performance.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 3 |

Table of Contents

Fund overview (cont’d)

Looking for additional information?

The Fund is traded under the symbol “MMU” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available on-line under the symbol “XMMUX” on most financial websites. Barron’s and the Wall Street Journal’s Monday edition both carry closed-end fund tables that provide additional information. In addition, the Fund issues a quarterly press release that can be found on most major financial websites as well as www.lmcef.com (click on the name of the Fund.)

In a continuing effort to provide information concerning the Fund, shareholders may call 1-888-777-0102 (toll free), Monday through Friday from 8:00 a.m. to 5:30 p.m. Eastern Time, for the Fund’s current NAV, market price and other information.

Thank you for your investment in Western Asset Managed Municipals Fund Inc. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Western Asset Management Company

June 20, 2017

RISKS: The Fund is a non-diversified, closed-end management investment company designed primarily as a long-term investment and not as a trading vehicle. The Fund is not intended to be a complete investment program and, due to the uncertainty inherent in all investments, there can be no assurance that the Fund will achieve its investment objective. The Fund’s common stock is traded on the New York Stock Exchange. Similar to stocks, the Fund’s share price will fluctuate with market conditions and, at the time of sale, may be worth more or less than the original investment. Shares of closed-end funds often trade at a discount to their net asset value. Because the Fund is non-diversified, it may be more susceptible to economic, political or regulatory events than a diversified fund. The Fund’s investments are subject to a number of risks such as interest rate risk, credit risk, leveraging risk and management risk. As interest rates rise, the price of fixed- income investments declines. Lower rated, higher-yielding bonds, known as “high yield” or “junk” bonds, are subject to greater liquidity and credit risk than higher-rated investment grade securities. Municipal securities purchased by the Fund may be adversely affected by changes in the financial condition of municipal issuers and insurers, regulatory and political developments, uncertainties and public perceptions, and other factors. The Fund may make significant investments in derivative instruments. Derivative instruments can be illiquid, may disproportionately increase losses and could have a potentially large impact on Fund performance. Investing in securities issued by other investment companies, including exchange-traded funds (“ETFs”) that invest primarily in municipal securities, involves risks similar to those of investing directly in the securities in which those investment companies invest. To the extent the Fund invests in securities of other investment companies, Fund stock holders will indirectly pay a portion of the operating costs of such companies, in addition to the expenses that the Fund bears directly in connection with its own operation. Leverage may result in greater volatility of NAV and market price of common shares and may increase a shareholder’s risk of loss.

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or

sell any securities. The information provided

| 4 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. Portfolio holdings are subject to change at any time and may not be representative of the portfolio managers’ current or future investments. The Fund’s portfolio composition is subject to change at any time.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

| i | The Federal Reserve Board (the “Fed”) is responsible for the formulation of U.S. policies designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| ii | The Bloomberg Barclays Municipal Bond Index is a market value weighted index of investment grade municipal bonds with maturities of one year or more. |

| iii | The Bloomberg Barclays U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| iv | A pre-refunded bond is a bond in which the original security has been replaced by an escrow, usually consisting of treasuries or agencies, which has been structured to pay principal and interest and any call premium, either to a call date (in the case of a pre-refunded bond), or to maturity (in the case of an escrowed to maturity bond). |

| v | Duration is the measure of the price sensitivity of a fixed- income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

| vi | Net asset value (“NAV”) is calculated by subtracting total liabilities, including liabilities associated with financial leverage (if any), from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is the Fund’s market price as determined by supply of and demand for the Fund’s shares. |

| vii | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the twelve-month period ended May 31, 2017, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 64 funds in the Fund’s Lipper category. |

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 5 |

Table of Contents

Investment breakdown (%) as a percent of total investments

| † | The bar graph above represents the composition of the Fund’s investments as of May 31, 2017 and May 31, 2016 and does not include derivatives, such as futures contracts. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time. |

| 6 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

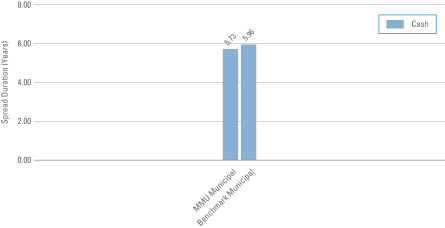

Economic exposure — May 31, 2017

| Total Spread Duration | ||

| MMU | — 5.73 | |

| Benchmark | — 5.96 | |

Spread duration measures the sensitivity to changes in spreads. The spread over Treasuries is the annual risk-premium demanded by investors to hold non-Treasury securities. Spread duration is quantified as the % change in price resulting from a 100 basis points change in spreads. For a security with positive spread duration, an increase in spreads would result in a price decline and a decline in spreads would result in a price increase. This chart highlights the market sector exposure of the Fund’s portfolio and the exposure relative to the selected benchmark as of the end of the reporting period.

| Benchmark | — Bloomberg Barclays Municipal Bond Index | |

| MMU | — Western Asset Managed Municipals Fund Inc. |

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 7 |

Table of Contents

Effective duration (unaudited)

Interest rate exposure — May 31, 2017

| Total Effective Duration | ||

| MMU | — 6.00 years | |

| Benchmark | — 6.10 years | |

Effective duration measures the sensitivity to changes in relevant interest rates. Effective duration is quantified as the % change in price resulting from a 100 basis points change in interest rates. For a security with positive effective duration, an increase in interest rates would result in a price decline and a decline in interest rates would result in a price increase. This chart highlights the interest rate exposure of the Fund’s sectors relative to the selected benchmark sectors as of the end of the reporting period.

| Benchmark | — Bloomberg Barclays Municipal Bond Index | |

| MMU | — Western Asset Managed Municipals Fund Inc. |

| 8 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

May 31, 2017

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| Municipal Bonds — 140.0% | ||||||||||||||||

| Alabama — 6.1% |

||||||||||||||||

| Jefferson County, AL, Sewer Revenue: |

||||||||||||||||

| AGM |

5.500 | % | 10/1/53 | $ | 1,400,000 | $ | 1,605,828 | |||||||||

| Convertible CAB, Subordinated Lien |

0.000 | % | 10/1/50 | 11,580,000 | 9,216,985 | (a) | ||||||||||

| Subordinated Lien Warrants |

6.000 | % | 10/1/42 | 9,230,000 | 10,684,833 | |||||||||||

| Subordinated Lien Warrants |

6.500 | % | 10/1/53 | 6,900,000 | 8,162,079 | |||||||||||

| Lower Alabama Gas District, Gas Project Revenue |

5.000 | % | 9/1/46 | 6,000,000 | 7,448,160 | |||||||||||

| Total Alabama |

37,117,885 | |||||||||||||||

| Arizona — 4.6% |

||||||||||||||||

| Navajo Nation, AZ, Revenue |

5.500 | % | 12/1/30 | 950,000 | 1,049,550 | (b) | ||||||||||

| Phoenix, AZ, Civic Improvement Corp. Airport Revenue |

5.000 | % | 7/1/40 | 5,000,000 | 5,507,600 | |||||||||||

| Salt Verde, AZ, Financial Corp. Senior Gas Revenue |

5.250 | % | 12/1/28 | 2,000,000 | 2,423,740 | |||||||||||

| Salt Verde, AZ, Financial Corp. Senior Gas Revenue |

5.000 | % | 12/1/32 | 10,000,000 | 11,967,800 | |||||||||||

| Salt Verde, AZ, Financial Corp. Senior Gas Revenue |

5.000 | % | 12/1/37 | 5,500,000 | 6,645,045 | |||||||||||

| Total Arizona |

27,593,735 | |||||||||||||||

| California — 21.5% |

||||||||||||||||

| Alameda, CA, Corridor Transportation Authority Revenue, Second Subordinated Lien |

5.000 | % | 10/1/34 | 1,750,000 | 1,985,480 | |||||||||||

| Anaheim, CA, Public Financing Authority Lease Revenue |

5.000 | % | 5/1/46 | 2,000,000 | 2,271,800 | |||||||||||

| Bay Area Toll Authority, CA, Toll Bridge Revenue: |

||||||||||||||||

| San Francisco Bay Area |

1.880 | % | 4/1/24 | 5,500,000 | 5,678,750 | (a)(c) | ||||||||||

| San Francisco Bay Area |

5.125 | % | 4/1/39 | 19,200,000 | 20,666,304 | (d) | ||||||||||

| California Health Facilities Financing Authority Revenue, Stanford Hospital & Clinics |

5.150 | % | 11/15/40 | 2,000,000 | 2,214,300 | |||||||||||

| California Housing Finance Agency Revenue, Home Mortgage |

4.700 | % | 8/1/24 | 2,110,000 | 2,115,634 | (e) | ||||||||||

| California State Health Facilities Financing Authority Revenue, Kaiser Permanente |

4.000 | % | 11/1/38 | 1,750,000 | 1,830,378 | |||||||||||

| California State PCFA, Water Furnishing Revenue |

5.000 | % | 11/21/45 | 12,500,000 | 13,376,125 | (b)(e) | ||||||||||

| California State PCFA, Water Furnishing Revenue |

5.000 | % | 11/21/45 | 5,000,000 | 5,005,200 | (b) | ||||||||||

| California Statewide CDA Revenue, Methodist Hospital Project, FHA |

6.625 | % | 8/1/29 | 5,235,000 | 5,870,895 | (d) | ||||||||||

| California Statewide CDA, Student Housing Revenue, Provident Group-Pomona Properties LLC |

5.750 | % | 1/15/45 | 1,770,000 | 1,924,220 | |||||||||||

| Imperial Irrigation District, CA, Electric Revenue |

5.500 | % | 11/1/41 | 2,750,000 | 3,159,310 | (d) | ||||||||||

| Inland Valley, CA, Development Agency, Successor Agency Tax Allocation Revenue |

5.000 | % | 9/1/44 | 2,405,000 | 2,673,133 | |||||||||||

| Los Angeles County, CA, Public Works Financing Authority, Lease Revenue: |

||||||||||||||||

| Multiple Capital Project II |

5.000 | % | 8/1/32 | 3,000,000 | 3,441,900 | |||||||||||

| Multiple Capital Project II |

5.000 | % | 8/1/37 | 1,000,000 | 1,135,740 | |||||||||||

See Notes to Financial Statements.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 9 |

Table of Contents

Schedule of investments (cont’d)

May 31, 2017

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| California — continued |

||||||||||||||||

| Los Angeles, CA, Convention & Exhibition Center Authority, Lease Revenue |

5.125 | % | 8/15/22 | $ | 8,000,000 | $ | 8,407,440 | (d) | ||||||||

| Los Angeles, CA, Department of Water & Power Revenue: |

||||||||||||||||

| Power System |

5.000 | % | 7/1/38 | 2,000,000 | 2,380,120 | |||||||||||

| Power System |

5.000 | % | 7/1/47 | 4,000,000 | 4,712,280 | |||||||||||

| M-S-R Energy Authority, CA, Gas Revenue |

7.000 | % | 11/1/34 | 3,430,000 | 4,945,237 | |||||||||||

| M-S-R Energy Authority, CA, Gas Revenue |

6.500 | % | 11/1/39 | 8,000,000 | 11,437,520 | |||||||||||

| Modesto, CA, Irrigation District COP: |

||||||||||||||||

| Capital Improvement |

6.000 | % | 10/1/39 | 4,595,000 | 4,979,096 | |||||||||||

| Capital Improvement |

6.000 | % | 10/1/39 | 1,905,000 | 2,078,717 | (d) | ||||||||||

| River Islands, CA, Public Financing Authority Special Tax, Community Facilities District No. 2003-1 |

5.500 | % | 9/1/45 | 2,000,000 | 2,147,280 | |||||||||||

| Riverside County, CA, Transportation Commission Sales Tax Revenue, Limited Tax |

5.250 | % | 6/1/39 | 900,000 | 1,064,313 | |||||||||||

| Riverside County, CA, Transportation Commission Toll Revenue: |

||||||||||||||||

| Senior Lien |

5.750 | % | 6/1/44 | 200,000 | 225,042 | |||||||||||

| Senior Lien |

5.750 | % | 6/1/48 | 600,000 | 671,682 | |||||||||||

| San Bernardino County, CA, COP, Arrowhead Project |

5.125 | % | 8/1/24 | 5,185,000 | 5,600,526 | |||||||||||

| Shafter Wasco Irrigation District Revenue, CA, COP |

5.000 | % | 11/1/40 | 5,000,000 | 5,538,400 | |||||||||||

| University of California, CA, Medical Center Pooled Revenue |

5.000 | % | 5/15/32 | 1,750,000 | 2,072,507 | |||||||||||

| Total California |

129,609,329 | |||||||||||||||

| Colorado — 10.9% |

||||||||||||||||

| Base Village Metropolitan District #2 Co., GO |

5.750 | % | 12/1/46 | 500,000 | 512,825 | |||||||||||

| Colorado State Educational & Cultural Facilities Authority Revenue, University of Denver Project |

5.000 | % | 3/1/47 | 1,600,000 | 1,846,640 | (f) | ||||||||||

| Colorado State Health Facilities Authority Revenue: |

||||||||||||||||

| Catholic Health Initiatives |

5.000 | % | 9/1/41 | 4,000,000 | 4,009,880 | |||||||||||

| Sisters Leavenworth |

5.000 | % | 1/1/35 | 6,000,000 | 6,463,140 | |||||||||||

| Denver, CO, City & County Airport Revenue |

6.125 | % | 11/15/25 | 24,575,000 | 27,620,241 | (e)(g) | ||||||||||

| Public Authority for Colorado Energy, Natural Gas Purchase Revenue |

6.500 | % | 11/15/38 | 18,000,000 | 25,651,080 | |||||||||||

| Total Colorado |

66,103,806 | |||||||||||||||

| District of Columbia — 2.3% |

||||||||||||||||

| District of Columbia, Hospital Revenue, Children’s Hospital Obligation, AGM |

5.450 | % | 7/15/35 | 13,570,000 | 14,147,946 | (d) | ||||||||||

| Florida — 10.1% |

||||||||||||||||

| Florida State Development Finance Corp., Educational Facilities Revenue, Renaissance Charter School Inc. Project |

6.125 | % | 6/15/46 | 555,000 | 574,708 | (b) | ||||||||||

See Notes to Financial Statements.

| 10 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| Florida — continued |

||||||||||||||||

| Florida State Development Finance Corp., Senior Living Revenue, Tuscan Isle Champions Gate Project |

6.375 | % | 6/1/46 | $ | 750,000 | $ | 748,515 | (b) | ||||||||

| Florida State Mid-Bay Bridge Authority Revenue |

5.000 | % | 10/1/30 | 2,410,000 | 2,764,463 | |||||||||||

| Miami-Dade County, FL, Aviation Revenue |

5.000 | % | 10/1/30 | 3,000,000 | 3,417,990 | (e) | ||||||||||

| Miami-Dade County, FL, Aviation Revenue |

5.500 | % | 10/1/41 | 10,000,000 | 10,861,400 | |||||||||||

| Miami-Dade County, FL, Aviation Revenue, Miami International Airport |

5.375 | % | 10/1/35 | 10,705,000 | 12,029,423 | |||||||||||

| Miami-Dade County, FL, Expressway Authority Toll System Revenue |

5.000 | % | 7/1/40 | 9,000,000 | 9,820,170 | |||||||||||

| Miami-Dade County, FL, Health Facilities Authority Hospital Revenue, Nicklaus Children’s Hospital |

5.000 | % | 8/1/42 | 1,250,000 | 1,421,637 | |||||||||||

| Orange County, FL, Health Facilities Authority Revenue: |

||||||||||||||||

| Balance Hospital-Orlando Regional Healthcare, AGM |

5.000 | % | 11/1/35 | 2,670,000 | 2,782,327 | |||||||||||

| Hospital-Orlando Regional Healthcare, AGM |

5.000 | % | 11/1/35 | 1,875,000 | 1,982,119 | (d) | ||||||||||

| Presbyterian Retirement Communities |

5.000 | % | 8/1/47 | 750,000 | 812,895 | |||||||||||

| Orange County, FL, School Board, COP, AGC |

5.500 | % | 8/1/34 | 8,000,000 | 8,771,120 | (d) | ||||||||||

| Orlando, FL, State Sales Tax Payments Revenue |

5.000 | % | 8/1/32 | 5,000,000 | 5,135,650 | (d) | ||||||||||

| Total Florida |

61,122,417 | |||||||||||||||

| Georgia — 4.3% |

||||||||||||||||

| Atlanta, GA, Water & Wastewater Revenue |

6.250 | % | 11/1/39 | 13,000,000 | 14,638,000 | (d) | ||||||||||

| DeKalb, Newton & Gwinnett Counties, GA, Joint Development Authority Revenue, GGC Foundation LLC Project |

6.125 | % | 7/1/40 | 6,220,000 | 6,876,148 | (d) | ||||||||||

| Main Street Natural Gas Inc., GA, Gas Project Revenue |

5.000 | % | 3/15/22 | 4,000,000 | 4,501,320 | |||||||||||

| Total Georgia |

26,015,468 | |||||||||||||||

| Hawaii — 1.3% |

||||||||||||||||

| Hawaii State Airports System Revenue |

5.000 | % | 7/1/39 | 7,000,000 | 7,730,660 | |||||||||||

| Illinois — 11.3% |

||||||||||||||||

| Chicago, IL, GO |

5.000 | % | 1/1/25 | 3,000,000 | 3,043,320 | |||||||||||

| Chicago, IL, GO |

5.500 | % | 1/1/32 | 3,300,000 | 3,348,807 | |||||||||||

| Chicago, IL, GO |

5.500 | % | 1/1/34 | 10,000 | 10,123 | |||||||||||

| Chicago, IL, GO |

5.500 | % | 1/1/37 | 220,000 | 222,295 | |||||||||||

| Chicago, IL, GO |

6.000 | % | 1/1/38 | 1,500,000 | 1,560,825 | |||||||||||

| Chicago, IL, O’Hare International Airport Revenue |

5.000 | % | 1/1/31 | 1,000,000 | 1,135,280 | (e) | ||||||||||

| Chicago, IL, O’Hare International Airport Revenue |

5.000 | % | 1/1/35 | 7,000,000 | 7,826,210 | (e) | ||||||||||

| Chicago, IL, O’Hare International Airport Revenue |

5.625 | % | 1/1/35 | 6,415,000 | 7,231,694 | |||||||||||

| Chicago, IL, O’Hare International Airport Revenue |

5.750 | % | 1/1/39 | 6,000,000 | 6,789,600 | |||||||||||

| Chicago, IL, O’Hare International Airport Revenue, General, Senior Lien |

5.000 | % | 1/1/41 | 1,000,000 | 1,135,600 | |||||||||||

| Chicago, IL, Wastewater Transmission Revenue, Second Lien |

5.000 | % | 1/1/44 | 1,000,000 | 1,060,820 | |||||||||||

See Notes to Financial Statements.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 11 |

Table of Contents

Schedule of investments (cont’d)

May 31, 2017

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| Illinois — continued |

||||||||||||||||

| Illinois State Finance Authority Revenue: |

||||||||||||||||

| Advocate Health Care & Hospitals Corp. Network |

6.250 | % | 11/1/28 | $ | 2,445,000 | $ | 2,627,275 | (d) | ||||||||

| Depaul University |

6.125 | % | 10/1/40 | 5,000,000 | 5,917,150 | (d) | ||||||||||

| Memorial Health System |

5.500 | % | 4/1/39 | 7,000,000 | 7,455,560 | |||||||||||

| Illinois State, GO |

5.000 | % | 2/1/28 | 2,840,000 | 2,981,829 | |||||||||||

| Illinois State, GO |

5.000 | % | 2/1/29 | 1,660,000 | 1,728,292 | |||||||||||

| Illinois State, GO |

5.000 | % | 1/1/33 | 1,500,000 | 1,536,720 | |||||||||||

| Metropolitan Pier & Exposition Authority, IL, Dedicated State Tax Revenue, McCormick Project, State Appropriations |

5.250 | % | 6/15/50 | 12,000,000 | 12,116,640 | |||||||||||

| Metropolitan Pier & Exposition Authority, IL, Revenue, CAB-McCormick Place Expansion Project |

0.000 | % | 12/15/52 | 3,100,000 | 451,019 | |||||||||||

| Total Illinois |

68,179,059 | |||||||||||||||

| Indiana — 3.8% |

||||||||||||||||

| Indiana Finance Authority, Wastewater Utility Revenue, CWA Authority |

5.000 | % | 10/1/41 | 5,000,000 | 5,556,600 | |||||||||||

| Indiana State Finance Authority Revenue, Private Activity-Ohio River Bridges East End Crossing Project |

5.000 | % | 7/1/44 | 5,000,000 | 5,401,250 | (e) | ||||||||||

| Indianapolis, IN, Thermal Energy System Revenue, AGC |

5.000 | % | 10/1/25 | 5,000,000 | 5,269,450 | (d) | ||||||||||

| Richmond, IN, Hospital Authority Revenue, Reid Hospital & Health Care Services Inc. Project |

6.625 | % | 1/1/39 | 5,000,000 | 5,432,650 | (d) | ||||||||||

| Valparaiso, IN, Exempt Facilities Revenue, Pratt Paper LLC Project |

7.000 | % | 1/1/44 | 1,000,000 | 1,190,930 | (e) | ||||||||||

| Total Indiana |

22,850,880 | |||||||||||||||

| Louisiana — 0.9% |

||||||||||||||||

| St. Charles Parish, LA, Gulf Zone Opportunity Zone Revenue, Valero Refining-New Orleans LLC |

4.000 | % | 6/1/22 | 5,000,000 | 5,329,400 | (a)(c) | ||||||||||

| Massachusetts — 6.1% |

||||||||||||||||

| Massachusetts State DFA Revenue: |

||||||||||||||||

| Boston University |

5.000 | % | 10/1/29 | 3,000,000 | 3,275,460 | (d) | ||||||||||

| Broad Institute Inc. |

5.250 | % | 4/1/37 | 8,000,000 | 9,033,840 | |||||||||||

| Milford Regional Medical Center |

5.750 | % | 7/15/43 | 500,000 | 557,320 | |||||||||||

| Partners Healthcare System |

5.000 | % | 7/1/47 | 5,750,000 | 6,472,430 | |||||||||||

| Suffolk University |

5.750 | % | 7/1/39 | 5,320,000 | 5,840,402 | (d) | ||||||||||

| Suffolk University |

5.750 | % | 7/1/39 | 2,680,000 | 2,894,909 | |||||||||||

| Umass Boston Student Housing Project |

5.000 | % | 10/1/48 | 750,000 | 815,753 | |||||||||||

| Massachusetts State Housing Finance Agency, Housing Revenue |

7.000 | % | 12/1/38 | 4,575,000 | 4,814,501 | |||||||||||

| Massachusetts State School Building Authority, Sales Tax Revenue |

5.000 | % | 5/15/43 | 3,000,000 | 3,417,180 | |||||||||||

| Total Massachusetts |

37,121,795 | |||||||||||||||

See Notes to Financial Statements.

| 12 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| Michigan — 4.6% |

||||||||||||||||

| Great Lakes, MI, Water Authority Water Supply System Revenue: |

||||||||||||||||

| Senior Lien |

5.000 | % | 7/1/35 | $ | 500,000 | $ | 570,370 | |||||||||

| Senior Lien |

5.000 | % | 7/1/46 | 5,500,000 | 6,172,760 | |||||||||||

| Lansing, MI, Board of Water & Light Utility System Revenue |

5.000 | % | 7/1/37 | 7,000,000 | 7,826,000 | |||||||||||

| Michigan State Building Authority Revenue, Facilities Program |

5.250 | % | 10/15/47 | 650,000 | 739,336 | |||||||||||

| Michigan State Finance Authority Limited Obligation Revenue, Higher Education, Thomas M Cooley Law School Project |

6.750 | % | 7/1/44 | 1,600,000 | 1,616,960 | (b) | ||||||||||

| Michigan State Finance Authority Revenue: |

||||||||||||||||

| Local Government Loan Program, Detroit Water & Sewer Department |

5.000 | % | 7/1/33 | 625,000 | 689,031 | |||||||||||

| Local Government Loan Program, Detroit Water & Sewer Department |

5.000 | % | 7/1/34 | 250,000 | 274,508 | |||||||||||

| Senior Lien Detroit Water & Sewer |

5.000 | % | 7/1/33 | 1,270,000 | 1,424,724 | |||||||||||

| Senior Lien Detroit Water & Sewer |

5.000 | % | 7/1/44 | 1,320,000 | 1,418,881 | |||||||||||

| Royal Oak, MI, Hospital Finance Authority Revenue: |

||||||||||||||||

| William Beaumont Hospital |

5.000 | % | 9/1/39 | 2,500,000 | 2,772,325 | |||||||||||

| William Beaumont Hospital |

8.250 | % | 9/1/39 | 4,000,000 | 4,359,200 | (d) | ||||||||||

| Total Michigan |

27,864,095 | |||||||||||||||

| Minnesota — 0.3% |

||||||||||||||||

| Western Minnesota Municipal Power Agency Revenue |

5.000 | % | 1/1/46 | 1,530,000 | 1,715,145 | |||||||||||

| Missouri — 2.7% |

||||||||||||||||

| Kansas City, MO, IDA, Senior Living Facilities Revenue, Kansas City United Methodist Retirement Home Inc. |

6.000 | % | 11/15/51 | 900,000 | 878,220 | (b) | ||||||||||

| Kansas City, MO, Water Revenue |

5.250 | % | 12/1/32 | 1,000,000 | 1,062,040 | |||||||||||

| Missouri State HEFA Revenue: |

||||||||||||||||

| Children’s Mercy Hospital |

5.625 | % | 5/15/39 | 4,980,000 | 5,422,423 | (d) | ||||||||||

| Children’s Mercy Hospital |

5.625 | % | 5/15/39 | 1,020,000 | 1,099,101 | |||||||||||

| Lutheran Senior Services |

5.000 | % | 2/1/44 | 2,710,000 | 2,894,605 | |||||||||||

| Platte County, MO, IDA Revenue, Improvement Zona Rosa Retail Project, GTD |

5.000 | % | 12/1/32 | 5,000,000 | 5,093,050 | |||||||||||

| Total Missouri |

16,449,439 | |||||||||||||||

| Nevada — 2.2% |

||||||||||||||||

| Reno, NV, Hospital Revenue: |

||||||||||||||||

| Washoe Medical Center, AGM |

5.500 | % | 6/1/33 | 11,565,000 | 12,091,092 | (d) | ||||||||||

| Washoe Medical Center, AGM |

5.500 | % | 6/1/33 | 1,185,000 | 1,228,489 | |||||||||||

| Total Nevada |

13,319,581 | |||||||||||||||

| New Jersey — 9.3% |

||||||||||||||||

| New Jersey Institute of Technology Revenue |

5.000 | % | 7/1/45 | 750,000 | 847,058 | |||||||||||

See Notes to Financial Statements.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 13 |

Table of Contents

Schedule of investments (cont’d)

May 31, 2017

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| New Jersey — continued |

||||||||||||||||

| New Jersey State EDA Revenue |

5.000 | % | 6/15/26 | $ | 2,500,000 | $ | 2,703,825 | |||||||||

| New Jersey State EDA Revenue: |

||||||||||||||||

| Continental Airlines Inc. Project |

4.875 | % | 9/15/19 | 1,440,000 | 1,488,384 | (e) | ||||||||||

| Continental Airlines Inc. Project |

5.125 | % | 9/15/23 | 2,000,000 | 2,168,980 | (e) | ||||||||||

| Continental Airlines Inc. Project |

5.250 | % | 9/15/29 | 3,000,000 | 3,288,630 | (e) | ||||||||||

| Private Activity-The Goethals Bridge Replacement Project, AGM |

5.125 | % | 7/1/42 | 2,500,000 | 2,786,275 | (e) | ||||||||||

| School Facilities Construction, SIFMA |

2.380 | % | 3/1/28 | 15,000,000 | 14,050,200 | (a) | ||||||||||

| New Jersey State Health Care Facilities Financing Authority Revenue: |

||||||||||||||||

| Hackensack Meridian Health |

5.000 | % | 7/1/38 | 400,000 | 460,452 | |||||||||||

| RWJ Barnabas Health Obligation Group |

5.000 | % | 7/1/43 | 1,200,000 | 1,358,784 | |||||||||||

| New Jersey State Higher Education Assistance Authority, Student Loan Revenue |

5.625 | % | 6/1/30 | 12,320,000 | 13,234,021 | |||||||||||

| New Jersey State Higher Education Assistance Authority, Student Loan Revenue, AGC |

6.125 | % | 6/1/30 | 6,075,000 | 6,274,867 | (e) | ||||||||||

| New Jersey State Housing & Mortgage Finance Agency Revenue |

6.375 | % | 10/1/28 | 225,000 | 226,483 | |||||||||||

| New Jersey State Transportation Trust Fund Authority Revenue, Capital Appreciation Transportation System, NATL |

0.000 | % | 12/15/31 | 9,000,000 | 4,878,540 | |||||||||||

| New Jersey State Turnpike Authority Revenue |

1.460 | % | 1/1/18 | 2,500,000 | 2,500,675 | (a)(c) | ||||||||||

| Total New Jersey |

56,267,174 | |||||||||||||||

| New Mexico — 0.9% |

||||||||||||||||

| New Mexico State Hospital Equipment Loan Council, Hospital Revenue, Presbyterian Healthcare Services |

6.125 | % | 8/1/28 | 5,000,000 | 5,294,800 | (d) | ||||||||||

| New York — 14.3% |

||||||||||||||||

| Hudson, NY, Yards Infrastructure Corp. Revenue |

5.000 | % | 2/15/42 | 3,500,000 | 4,088,105 | |||||||||||

| Liberty, NY, Development Corp. Revenue: |

||||||||||||||||

| Goldman Sachs Headquarters |

5.250 | % | 10/1/35 | 3,045,000 | 3,846,718 | |||||||||||

| Goldman Sachs Headquarters |

5.500 | % | 10/1/37 | 1,485,000 | 1,929,550 | |||||||||||

| Long Island Power Authority, NY, Electric System Revenue |

6.000 | % | 5/1/33 | 24,570,000 | 26,922,086 | (d) | ||||||||||

| MTA Hudson Rail Yards Trust Obligations Revenue |

5.000 | % | 11/15/56 | 2,750,000 | 3,024,367 | |||||||||||

| MTA, NY, Dedicated Tax Fund Revenue, Green Bonds |

5.000 | % | 11/15/47 | 1,500,000 | 1,756,275 | |||||||||||

| MTA, NY, Revenue |

5.250 | % | 11/15/40 | 5,000,000 | 5,603,800 | |||||||||||

| New York City, NY, Municipal Water Finance Authority, Water & Sewer System Revenue, Second General Resolution Fiscal 2013 |

5.000 | % | 6/15/47 | 5,000,000 | 5,647,600 | (h) | ||||||||||

| New York City, NY, TFA, Building Aid Revenue |

5.000 | % | 1/15/32 | 4,000,000 | 4,241,120 | |||||||||||

| New York State Liberty Development Corp., Liberty Revenue: |

||||||||||||||||

| 3 World Trade Center LLC Project |

5.000 | % | 11/15/44 | 1,750,000 | 1,882,668 | (b) | ||||||||||

See Notes to Financial Statements.

| 14 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| New York — continued |

||||||||||||||||

| 4 World Trade Center LLC Project |

5.750 | % | 11/15/51 | $ | 5,000,000 | $ | 5,747,550 | |||||||||

| Second Priority, Bank of America Tower |

5.125 | % | 1/15/44 | 1,000,000 | 1,089,240 | |||||||||||

| New York State Transportation Development Corp., Special Facilities Revenue: |

||||||||||||||||

| LaGuardia Airport Terminal B Redevelopment Project |

5.000 | % | 7/1/41 | 8,000,000 | 8,745,840 | (e) | ||||||||||

| LaGuardia Airport Terminal B Redevelopment Project |

5.000 | % | 7/1/46 | 1,500,000 | 1,635,915 | (e) | ||||||||||

| Port Authority of New York & New Jersey Revenue |

5.000 | % | 1/15/41 | 2,750,000 | 3,049,145 | |||||||||||

| Port Authority of New York & New Jersey Revenue |

5.000 | % | 10/15/41 | 6,400,000 | 7,417,024 | |||||||||||

| Total New York |

86,627,003 | |||||||||||||||

| North Carolina — 0.5% |

||||||||||||||||

| North Carolina State Turnpike Authority Monroe Expressway Toll Revenue |

5.000 | % | 7/1/47 | 750,000 | 815,498 | |||||||||||

| North Carolina State Turnpike Authority Monroe Expressway Toll Revenue |

5.000 | % | 7/1/51 | 1,500,000 | 1,623,825 | |||||||||||

| North Carolina State Turnpike Authority Revenue, Senior Lien |

5.000 | % | 1/1/30 | 300,000 | 349,866 | |||||||||||

| Total North Carolina |

2,789,189 | |||||||||||||||

| Ohio — 2.0% |

||||||||||||||||

| JobsOhio Beverage System Statewide Liquor Profits Revenue |

5.000 | % | 1/1/38 | 8,000,000 | 8,963,440 | |||||||||||

| Ohio State Water Development Authority, Environmental Improvement Revenue, U.S. Steel Corp. Project |

6.600 | % | 5/1/29 | 3,000,000 | 3,002,010 | |||||||||||

| Total Ohio |

11,965,450 | |||||||||||||||

| Oklahoma — 0.1% |

||||||||||||||||

| Payne County, OK, EDA Revenue, Epworth Living at The Ranch |

6.875 | % | 11/1/46 | 575,000 | 575,541 | |||||||||||

| Oregon — 0.5% |

||||||||||||||||

| Oregon State Facilities Authority Revenue, Legacy Health Project |

5.000 | % | 6/1/46 | 2,000,000 | 2,255,960 | |||||||||||

| Umatilla County, OR, Hospital Facility Authority Revenue, Catholic Health Initiatives |

5.000 | % | 5/1/32 | 510,000 | 511,428 | |||||||||||

| Total Oregon |

2,767,388 | |||||||||||||||

| Pennsylvania — 2.6% |

||||||||||||||||

| Cumberland County, PA, Municipal Authority Revenue, Diakon Lutheran Social Ministries Project |

5.000 | % | 1/1/30 | 2,375,000 | 2,635,110 | |||||||||||

| East Hempfield Township, PA, IDA Revenue, Student Services Inc.-Student Housing Project-Millersville University |

5.000 | % | 7/1/47 | 550,000 | 565,422 | |||||||||||

| Pennsylvania State Turnpike Commission Revenue |

5.250 | % | 12/1/41 | 6,000,000 | 6,745,320 | |||||||||||

| Philadelphia, PA, School District, GO |

5.000 | % | 9/1/33 | 1,755,000 | 1,931,360 | |||||||||||

| Philadelphia, PA, Water & Wastewater Revenue |

5.000 | % | 7/1/45 | 1,000,000 | 1,123,190 | |||||||||||

| State Public School Building Authority PA, Lease Revenue: |

||||||||||||||||

| Philadelphia School District Project, AGM |

5.000 | % | 6/1/31 | 600,000 | 688,308 | |||||||||||

| Philadelphia School District Project, AGM |

5.000 | % | 6/1/33 | 1,780,000 | 2,020,140 | |||||||||||

| Total Pennsylvania |

15,708,850 | |||||||||||||||

See Notes to Financial Statements.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 15 |

Table of Contents

Schedule of investments (cont’d)

May 31, 2017

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| Rhode Island — 0.9% |

||||||||||||||||

| Rhode Island State Health & Educational Building Corp. Revenue, Hospital Financing |

7.000 | % | 5/15/39 | $ | 5,000,000 | $ | 5,581,400 | (d) | ||||||||

| South Carolina — 0.5% |

||||||||||||||||

| South Carolina State Ports Authority Revenue |

5.250 | % | 7/1/40 | 2,500,000 | 2,758,200 | |||||||||||

| Tennessee — 0.0% |

||||||||||||||||

| Hardeman County, TN, Correctional Facilities Corp., Correctional Facilities Revenue |

7.750 | % | 8/1/17 | 140,000 | 140,241 | |||||||||||

| Texas — 13.1% |

||||||||||||||||

| Alamo, TX, Regional Mobility Authority Revenue, Senior Lien |

5.000 | % | 6/15/46 | 1,300,000 | 1,486,251 | |||||||||||

| Dallas-Fort Worth, TX, International Airport Revenue, Joint Improvement |

5.000 | % | 11/1/45 | 8,500,000 | 9,394,455 | |||||||||||

| Grand Parkway Transportation Corp., TX, System Toll Revenue, Convertible CAB, Step Bond |

0.000 | % | 10/1/36 | 4,000,000 | 3,641,000 | (a) | ||||||||||

| Harris County, TX, Health Facilities Development Corp. Revenue, School Health Care System Revenue |

5.750 | % | 7/1/27 | 1,000,000 | 1,252,150 | (g) | ||||||||||

| Houston, TX, Airport Systems Revenue, United Airlines Inc. |

5.000 | % | 7/15/30 | 5,500,000 | 5,960,790 | (e) | ||||||||||

| Houston, TX, Utility System Revenue, Combined First Lien |

5.000 | % | 11/15/44 | 1,000,000 | 1,140,400 | |||||||||||

| Love Field Airport Modernization Corp., TX, Special Facilities Revenue, Southwest Airlines Co. Project |

5.250 | % | 11/1/40 | 14,500,000 | 15,697,410 | |||||||||||

| Love Field, TX, Airport Modernization Corp., General Airport Revenue |

5.000 | % | 11/1/32 | 120,000 | 139,967 | (e) | ||||||||||

| Love Field, TX, Airport Modernization Corp., General Airport Revenue |

5.000 | % | 11/1/33 | 120,000 | 138,899 | (e) | ||||||||||

| Love Field, TX, Airport Modernization Corp., General Airport Revenue |

5.000 | % | 11/1/35 | 130,000 | 149,214 | (e) | ||||||||||

| Love Field, TX, Airport Modernization Corp., General Airport Revenue |

5.000 | % | 11/1/36 | 120,000 | 137,316 | (e) | ||||||||||

| New Hope Cultural Education Facilities Finance Corp., TX, Student Housing Revenue: |

||||||||||||||||

| Collegiate Housing College Station LLC, Texas A&M University Project, AGM |

5.000 | % | 4/1/46 | 750,000 | 828,735 | |||||||||||

| NCCD-College Station Properties LLC |

5.000 | % | 7/1/47 | 2,200,000 | 2,327,050 | |||||||||||

| North Texas Tollway Authority Revenue |

5.000 | % | 1/1/39 | 825,000 | 942,851 | |||||||||||

| North Texas Tollway Authority Revenue |

5.000 | % | 1/1/40 | 2,000,000 | 2,234,260 | |||||||||||

| North Texas Tollway Authority Revenue |

5.000 | % | 1/1/45 | 2,105,000 | 2,377,597 | |||||||||||

| North Texas Tollway Authority Revenue: |

||||||||||||||||

| System-First Tier |

5.750 | % | 1/1/40 | 7,490,000 | 7,697,698 | (d) | ||||||||||

| System-First Tier |

5.750 | % | 1/1/40 | 1,845,000 | 1,891,309 | |||||||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp., Retirement Facility Revenue, Buckner Senior Living Ventana Project |

6.625 | % | 11/15/37 | 610,000 | 625,348 | (f) | ||||||||||

See Notes to Financial Statements.

| 16 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| Texas — continued |

||||||||||||||||

| Texas State Municipal Gas Acquisition & Supply Corp. I, Gas Supply Revenue |

5.625 | % | 12/15/17 | $ | 405,000 | $ | 410,630 | |||||||||

| Texas State Municipal Gas Acquisition & Supply Corp. III, Gas Supply Revenue |

5.000 | % | 12/15/27 | 8,550,000 | 9,595,494 | |||||||||||

| Texas State Private Activity Bond Surface Transportation Corp. Revenue: |

||||||||||||||||

| LBJ Infrastructure Group LLC |

7.000 | % | 6/30/40 | 7,000,000 | 7,951,650 | |||||||||||

| Senior Lien, Blueridge Transportation Group LLC |

5.000 | % | 12/31/45 | 1,600,000 | 1,749,104 | (e) | ||||||||||

| Woodloch Health Facilities Development Corp., TX, Senior Housing Revenue: |

||||||||||||||||

| Inspired Living Lewsville Project |

6.750 | % | 12/1/51 | 1,000,000 | 1,002,420 | (b) | ||||||||||

| Inspired Living Lewsville Project |

10.000 | % | 12/1/51 | 150,000 | 137,805 | |||||||||||

| Total Texas |

78,909,803 | |||||||||||||||

| U.S. Virgin Islands — 0.5% |

||||||||||||||||

| Virgin Islands Public Finance Authority Revenue: |

||||||||||||||||

| Matching Fund Loan |

6.750 | % | 10/1/37 | 2,320,000 | 1,890,800 | |||||||||||

| Matching Fund Loan |

6.000 | % | 10/1/39 | 1,475,000 | 1,109,937 | |||||||||||

| Total U.S. Virgin Islands |

3,000,737 | |||||||||||||||

| Utah — 0.2% |

||||||||||||||||

| Utah State Charter School Finance Authority, Charter School Revenue, Syracuse Arts Academy Project, UT CSCE |

5.000 | % | 4/15/47 | 1,000,000 | 1,108,570 | |||||||||||

| Virginia — 1.4% |

||||||||||||||||

| Virginia State Port Authority Port Facility Revenue |

5.000 | % | 7/1/41 | 1,100,000 | 1,248,324 | (e) | ||||||||||

| Virginia State Port Authority Port Facility Revenue |

5.000 | % | 7/1/45 | 1,500,000 | 1,695,975 | (e) | ||||||||||

| Virginia State Small Business Financing Authority Revenue: |

||||||||||||||||

| Elizabeth River Crossings OpCo LLC Project |

5.250 | % | 1/1/32 | 3,000,000 | 3,285,750 | (e) | ||||||||||

| Elizabeth River Crossings OpCo LLC Project |

5.500 | % | 1/1/42 | 2,000,000 | 2,200,960 | (e) | ||||||||||

| Total Virginia |

8,431,009 | |||||||||||||||

| Washington — 0.1% |

||||||||||||||||

| Washington State HFC Revenue: |

||||||||||||||||

| Heron’s Key |

6.500 | % | 7/1/30 | 350,000 | 351,064 | (b) | ||||||||||

| Heron’s Key |

6.750 | % | 7/1/35 | 370,000 | 366,171 | (b) | ||||||||||

| Total Washington |

717,235 | |||||||||||||||

| Wisconsin — 0.1% |

||||||||||||||||

| Public Finance Authority, WI, Education Revenue, North Carolina Charter Educational Foundation Project |

5.000 | % | 6/15/46 | 500,000 | 464,630 | (b) | ||||||||||

| Total Investments before Short-Term Investments (Cost — $764,793,188) |

|

845,377,860 | ||||||||||||||

See Notes to Financial Statements.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 17 |

Table of Contents

Schedule of investments (cont’d)

May 31, 2017

Western Asset Managed Municipals Fund Inc.

| Security | Rate | Maturity Date |

Face Amount |

Value | ||||||||||||

| Short-Term Investments — 0.2% | ||||||||||||||||

| New York — 0.2% |

||||||||||||||||

| New York City, NY, GO, AGM, SPA-Dexia Credit Local |

0.980 | % | 11/1/26 | $ | 50,000 | $ | 50,000 | (i)(j) | ||||||||

| New York City, NY, Municipal Water Finance Authority, Water & Sewer System Revenue: |

||||||||||||||||

| Second General Resolution, SPA-Dexia Credit Local |

0.960 | % | 6/15/32 | 900,000 | 900,000 | (i)(j) | ||||||||||

| Second General Resolution, SPA-Dexia Credit Local |

0.980 | % | 6/15/32 | 300,000 | 300,000 | (i)(j) | ||||||||||

| Total Short-Term Investments (Cost — $1,250,000) |

1,250,000 | |||||||||||||||

| Total Investments — 140.2% (Cost — $766,043,188#) |

846,627,860 | |||||||||||||||

| Auction Rate Cumulative Preferred Stock, at Liquidation Value — (5.3)% |

|

(32,075,000 | ) | |||||||||||||

| Variable Rate Demand Preferred Stock, at Liquidation Value — (36.0)% |

|

(217,575,000 | ) | |||||||||||||

| Other Assets in Excess of Liabilities — 1.1% |

7,023,000 | |||||||||||||||

| Total Net Assets Applicable to Common Shareholders — 100.0% |

|

$ | 604,000,860 | |||||||||||||

| (a) | Variable rate security. Interest rate disclosed is as of the most recent information available. |

| (b) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors, unless otherwise noted. |

| (c) | Maturity date shown represents the mandatory tender date. |

| (d) | Pre-Refunded bonds are escrowed with U.S. government obligations and/or U.S. government agency securities and are considered by the manager to be triple-A rated even if issuer has not applied for new ratings. |

| (e) | Income from this issue is considered a preference item for purposes of calculating the alternative minimum tax (“AMT”). |

| (f) | Security is purchased on a when-issued basis. |

| (g) | Bonds are escrowed to maturity by government securities and/or U.S. government agency securities and are considered by the manager to be triple-A rated even if issuer has not applied for new ratings. |

| (h) | All or a portion of this security is held at the broker as collateral for open futures contracts. |

| (i) | Variable rate demand obligations have a demand feature under which the Fund can tender them back to the issuer or liquidity provider on no more than 7 days notice. |

| (j) | Maturity date shown is the final maturity date. The security may be sold back to the issuer before final maturity. |

| # | Aggregate cost for federal income tax purposes is $764,956,845. |

| Abbreviations used in this schedule: | ||

| AGC | — Assured Guaranty Corporation — Insured Bonds | |

| AGM | — Assured Guaranty Municipal Corporation — Insured Bonds | |

| CAB | — Capital Appreciation Bonds | |

| CDA | — Communities Development Authority | |

| COP | — Certificates of Participation | |

| CSCE | — Charter School Credit Enhancement | |

| DFA | — Development Finance Agency | |

| EDA | — Economic Development Authority | |

| FHA | — Federal Housing Administration | |

See Notes to Financial Statements.

| 18 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

Western Asset Managed Municipals Fund Inc.

| Abbreviations used in this schedule (cont’d): | ||

| GO | — General Obligation | |

| GTD | — Guaranteed | |

| HEFA | — Health & Educational Facilities Authority | |

| HFC | — Housing Finance Commission | |

| IDA | — Industrial Development Authority | |

| MTA | — Metropolitan Transportation Authority | |

| NATL | — National Public Finance Guarantee Corporation — Insured Bonds | |

| PCFA | — Pollution Control Financing Authority | |

| SIFMA | — Securities Industry and Financial Markets Association | |

| SPA | — Standby Bond Purchase Agreement — Insured Bonds | |

| TFA | — Transitional Finance Authority | |

| Ratings Table* (unaudited) | ||||

| Standard & Poor’s/Moody’s/Fitch** | ||||

| AAA/Aaa | 1.2 | % | ||

| AA/Aa | 32.9 | |||

| A | 36.5 | |||

| BBB/Baa | 20.2 | |||

| BB/Ba | 1.9 | |||

| B/B | 0.4 | |||

| CCC/Caa | 0.1 | |||

| A-1/VMIG 1 | 0.2 | |||

| NR*** | 6.6 | |||

| 100.0 | % | |||

| * | As a percentage of total investments. |

| ** | The ratings shown are based on each portfolio security’s rating as determined by Standard & Poor’s, Moody’s or Fitch, each a Nationally Recognized Statistical Rating Organization (“NRSRO”). These ratings are the opinions of the NRSRO and are not measures of quality or guarantees of performance. Securities may be rated by other NRSROs, and these ratings may be higher or lower. In the event that a security is rated by multiple NRSROs and receives different ratings, the Fund will treat the security as being rated in the highest rating category received from a NRSRO. |

| *** | The credit quality of unrated investments is evaluated based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. |

At May 31, 2017, the Fund had the following open futures contracts:

| Number of Contracts |

Expiration Date |

Notional Amount |

Market Value |

Unrealized Appreciation |

||||||||||||||||

| Contracts to Buy: | ||||||||||||||||||||

| U.S. Treasury Long-Term Bonds | 132 | 9/17 | $ | 20,071,239 | $ | 20,303,250 | $ | 232,011 | ||||||||||||

See Notes to Financial Statements.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 19 |

Table of Contents

Statement of assets and liabilities

May 31, 2017

| Assets: | ||||

| Investments, at value (Cost — $766,043,188) |

$ | 846,627,860 | ||

| Interest receivable |

10,977,914 | |||

| Receivable from broker — variation margin on open futures contracts |

66,000 | |||

| Prepaid expenses |

36,283 | |||

| Total Assets |

857,708,057 | |||

| Liabilities: | ||||

| Variable Rate Demand Preferred Stock ($25,000 liquidation value per share; 8,703 shares issued and outstanding) (net of deferred offering costs of $1,535,907) (Note 5) |

216,039,093 | |||

| Distributions payable to Common Shareholders |

2,470,266 | |||

| Payable for securities purchased |

2,430,485 | |||

| Investment management fee payable |

396,183 | |||

| Due to custodian |

114,539 | |||

| Directors’ fees payable |

10,025 | |||

| Distributions payable to Variable Rate Demand Preferred Stockholders |

7,668 | |||

| Distributions payable to Auction Rate Cumulative Preferred Stockholders |

5,259 | |||

| Accrued expenses |

158,679 | |||

| Total Liabilities |

221,632,197 | |||

| Series M, T, W, Th and F Auction Rate Cumulative Preferred Stock (1,283 shares authorized and issued at $25,000 for each share) (Note 6) |

32,075,000 | |||

| Total Net Assets Applicable to Common Shareholders | $ | 604,000,860 | ||

| Net Assets Applicable to Common Shareholders: | ||||

| Common stock par value ($0.001 par value, 43,166,488 shares issued and outstanding; 500,000,000 common shares authorized) |

$ | 43,166 | ||

| Paid-in capital in excess of par value |

531,311,774 | |||

| Undistributed net investment income |

12,610,588 | |||

| Accumulated net realized loss on investments and futures contracts |

(20,781,351) | |||

| Net unrealized appreciation on investments and futures contracts |

80,816,683 | |||

| Total Net Assets Applicable to Common Shareholders | $ | 604,000,860 | ||

| Common Shares Outstanding | 43,166,488 | |||

| Net Asset Value Per Common Share | $13.99 | |||

See Notes to Financial Statements.

| 20 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

For the Year Ended May 31, 2017

| Investment Income: | ||||

| Interest |

$ | 39,764,270 | ||

| Expenses: | ||||

| Investment management fee (Note 2) |

4,729,914 | |||

| Liquidity fees (Note 5) |

1,685,085 | |||

| Distributions to Variable Rate Demand Preferred Stockholders (Notes 1 and 5) |

1,664,896 | |||

| Remarketing fees (Note 5) |

220,599 | |||

| Directors’ fees |

141,418 | |||

| Legal fees |

102,171 | |||

| Audit and tax fees |

69,500 | |||

| Fund accounting fees |

62,005 | |||

| Transfer agent fees |

57,754 | |||

| Amortization of Variable Rate Demand Preferred Stock offering costs (Note 5) |

55,290 | |||

| Auction agent fees |

52,636 | |||

| Rating agency fees |

35,526 | |||

| Stock exchange listing fees |

33,514 | |||

| Shareholder reports |

32,504 | |||

| Auction participation fees (Note 6) |

16,018 | |||

| Custody fees |

11,476 | |||

| Insurance |

9,700 | |||

| Miscellaneous expenses |

24,592 | |||

| Total Expenses |

9,004,598 | |||

| Net Investment Income | 30,759,672 | |||

| Realized and Unrealized Gain (Loss) on Investments and Futures Contracts (Notes 1, 3 and 4): | ||||

| Net Realized Gain (Loss) From: |

| |||

| Investment transactions |

614,379 | |||

| Futures contracts |

(151,218) | |||

| Net Realized Gain |

463,161 | |||

| Change in Net Unrealized Appreciation (Depreciation) From: |

| |||

| Investments |

(24,026,350) | |||

| Futures contracts |

250,656 | |||

| Change in Net Unrealized Appreciation (Depreciation) |

(23,775,694) | |||

| Net Loss on Investments and Futures Contracts | (23,312,533) | |||

| Distributions Paid to Auction Rate Cumulative Preferred Stockholders From Net Investment Income (Notes 1 and 6) |

(347,598) | |||

| Increase in Net Assets Applicable to Common Shareholders From Operations | $ | 7,099,541 | ||

See Notes to Financial Statements.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 21 |

Table of Contents

Statements of changes in net assets

| For the Years Ended May 31, | 2017 | 2016 | ||||||

| Operations: | ||||||||

| Net investment income |

$ | 30,759,672 | $ | 31,558,203 | ||||

| Net realized gain (loss) |

463,161 | (7,999,095) | ||||||

| Change in net unrealized appreciation (depreciation) |

(23,775,694) | 18,568,624 | ||||||

| Distributions paid to Auction Rate Cumulative Preferred Stockholders from net investment income |

(347,598) | (90,619) | ||||||

| Increase in Net Assets Applicable to Common Shareholders From Operations |

7,099,541 | 42,037,113 | ||||||

| Distributions to Common Shareholders From (Note 1): | ||||||||

| Net investment income |

(33,067,764) | (33,445,504) | ||||||

| Decrease in Net Assets From Distributions to Common Shareholders |

(33,067,764) | (33,445,504) | ||||||

| Fund Share Transactions: | ||||||||

| Net increase from tender and repurchase of Auction Rate Cumulative Preferred Shares (Note 6) |

— | 35,000 | ||||||

| Reinvestment of distributions (195,380 and 129,634 shares issued, respectively) |

2,718,345 | 1,833,971 | ||||||

| Increase in Net Assets From Fund Share Transactions |

2,718,345 | 1,868,971 | ||||||

| Increase (Decrease) in Net Assets Applicable to Common Shareholders |

(23,249,878) | 10,460,580 | ||||||

| Net Assets Applicable to Common Shareholders: | ||||||||

| Beginning of year |

627,250,738 | 616,790,158 | ||||||

| End of year* |

$ | 604,000,860 | $ | 627,250,738 | ||||

| *Includes undistributed net investment income of: |

$12,610,588 | $15,379,619 | ||||||

See Notes to Financial Statements.

| 22 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

For the Year Ended May 31, 2017

| Increase (Decrease) in Cash: | ||||

| Cash Provided (Used) by Operating Activities: | ||||

| Net increase in net assets applicable to common shareholders resulting from operations |

$ | 7,447,139 | ||

| Adjustments to reconcile net increase in net assets resulting from operations to net cash provided (used) by operating activities: |

||||

| Purchases of portfolio securities |

(101,044,736) | |||

| Sales of portfolio securities |

99,615,313 | |||

| Net purchases, sales and maturities of short-term investments |

9,650,000 | |||

| Net amortization of premium (accretion of discount) |

60,733 | |||

| Decrease in receivable for securities sold |

55,000 | |||

| Increase in interest receivable |

(304,367) | |||

| Increase in receivable from broker — variation margin on open futures contracts |

(66,000) | |||

| Decrease in prepaid expenses |

26,242 | |||

| Decrease in payable for securities purchased |

(10,747,392) | |||

| Decrease in investment management fee payable |

(12,657) | |||

| Decrease in Directors’ fees payable |

(4,020) | |||

| Decrease in accrued expenses |

(7,149) | |||

| Increase in distributions payable to Variable Rate Demand Preferred Stockholders |

2,392 | |||

| Decrease in payable to broker — variation margin on open futures contracts |

(22,125) | |||

| Net realized gain on investments |

(614,379) | |||

| Change in net unrealized appreciation(depreciation) of investments |

24,026,350 | |||

| Net Cash Provided by Operating Activities |

28,060,344 | |||

| Cash Flows From Financing Activities: | ||||

| Distributions paid on common stock |

(27,879,603) | |||

| Distributions paid on Auction Rate Cumulative Preferred Stock |

(344,490) | |||

| Decrease in deferred preferred stock offering costs |

55,291 | |||

| Increase in due to custodian |

108,458 | |||

| Net Cash Used in Financing Activities |

(28,060,344) | |||

| Cash at Beginning of Year | — | |||

| Cash at End of Year | — | |||

| Non-Cash Financing Activities: | ||||

| Proceeds from reinvestment of distributions |

$2,718,345 | |||

See Notes to Financial Statements.

| Western Asset Managed Municipals Fund Inc. 2017 Annual Report | 23 |

Table of Contents

| For a common share of capital stock outstanding throughout each year ended May 31: | ||||||||||||||||||||

| 20171 | 20161 | 20151 | 20141 | 20131 | ||||||||||||||||

| Net asset value, beginning of year | $14.60 | $14.40 | $13.80 | $14.12 | $13.98 | |||||||||||||||

| Income (loss) from operations: | ||||||||||||||||||||

| Net investment income |

0.71 | 0.74 | 0.78 | 0.79 | 0.81 | |||||||||||||||

| Net realized and unrealized gain (loss) |

(0.54) | 0.24 | 0.09 | (0.32) | 0.12 | |||||||||||||||

| Distributions paid to Auction Rate Cumulative Preferred Stockholders from net investment income |

(0.01) | (0.00) | 2 | (0.00) | 2 | (0.01) | (0.01) | |||||||||||||

| Total income from operations |

0.16 | 0.98 | 0.87 | 0.46 | 0.92 | |||||||||||||||

| Less distributions to common shareholders from: | ||||||||||||||||||||

| Net investment income |

(0.77) | (0.78) | (0.78) | (0.78) | (0.78) | |||||||||||||||

| Total distributions to common shareholders |

(0.77) | (0.78) | (0.78) | (0.78) | (0.78) | |||||||||||||||

| Net increase from tender and repurchase of Auction Rate Cumulative Preferred Shares | — | 0.00 | 2 | 0.51 | — | — | ||||||||||||||

| Net asset value, end of year | $13.99 | $14.60 | $14.40 | $13.80 | $14.12 | |||||||||||||||

| Market price, end of year | $13.84 | $14.82 | $13.96 | $13.17 | $13.37 | |||||||||||||||

| Total return, based on NAV3,4 |

1.16 | % | 7.05 | % | 10.26 | %5 | 3.78 | % | 6.66 | % | ||||||||||

| Total return, based on Market Price6 |

(1.31) | % | 12.19 | % | 12.26 | % | 4.82 | % | 1.90 | % | ||||||||||

| Net assets applicable to common shareholders, end of year (000s) | $604,001 | $627,251 | $616,790 | $591,184 | $603,935 | |||||||||||||||

| Ratios to average net assets:7 | ||||||||||||||||||||

| Gross expenses |

1.48 | % | 1.28 | % | 0.99 | % | 0.92 | % | 0.88 | % | ||||||||||

| Net expenses |

1.48 | 1.28 | 0.99 | 0.92 | 0.88 | |||||||||||||||

| Net investment income |

5.04 | 5.13 | 5.49 | 6.10 | 5.65 | |||||||||||||||

| Portfolio turnover rate | 12 | % | 5 | % | 4 | % | 1 | % | 19 | % | ||||||||||

| Supplemental data: | ||||||||||||||||||||

| Auction Rate Cumulative Preferred Stock at Liquidation Value, End of Year (000s) |

$32,075 | $32,075 | $32,425 | $250,000 | $250,000 | |||||||||||||||

| Variable Rate Demand Preferred Stock at Liquidation Value, End of Year (000s) |

$217,575 | $217,575 | $217,575 | — | — | |||||||||||||||

| Asset Coverage Ratio for Auction Rate Cumulative Preferred Stock and Variable Rate Demand Preferred Stock8 |

342 | % | 351 | % | 347 | % | 336 | %9 | 342 | %9 | ||||||||||

| Asset Coverage, per $25,000 Liquidation Value per Share of Auction Rate Cumulative Preferred Stock and Variable Rate Demand Preferred Stock8 |

$85,485 | $87,813 | $86,679 | $84,118 | $85,393 | |||||||||||||||

See Notes to Financial Statements.

| 24 | Western Asset Managed Municipals Fund Inc. 2017 Annual Report |

Table of Contents

| 1 | Per share amounts have been calculated using the average shares method. |

| 2 | Amount represents less than $0.005 per share. |

| 3 | Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 4 | The total return calculation assumes that distributions are reinvested at NAV. Past performance is no guarantee of future results. |