UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

x

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the quarterly period ended June 30, 2013

|

|

|

Or

|

|

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the transition period from _________ to _________

|

Commission File Number: 000-20936

GULF RESOURCES, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

13-3637458

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

|

Level 11,Vegetable Building, Industrial Park of the East City,

Shouguang City, Shandong,

|

262700

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: +86 (536) 567 0008

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every, Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

|

Non-accelerated filer (Do not check if a smaller reporting company) o

|

Smaller reporting company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

As of August 8, 2013, the registrant had outstanding 38,368,505 shares of common stock.

|

Part I – Financial Information

|

|

|

1

|

|

|

20

|

|

|

39

|

|

|

40

|

|

|

Part II – Other Information

|

|

|

40

|

|

|

41

|

|

|

41

|

|

|

41

|

|

|

41

|

|

|

41

|

|

|

41

|

|

|

42

|

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements

|

GULF RESOURCES, INC.

|

|

AND SUBSIDIARIES

|

|

CONDENSED CONSOLIDATED BALANCE SHEETS

|

|

(Expressed in U.S. dollars)

|

|

(UNAUDITED)

|

|

June 30, 2013

Unaudited

|

December 31, 2012

Audited

|

|||||||

|

Current Assets

|

||||||||

|

Cash

|

$

|

86,422,512

|

$

|

65,241,035

|

||||

|

Accounts receivable

|

39,163,206

|

35,969,900

|

||||||

|

Inventories

|

5,371,214

|

5,993,598

|

||||||

|

Prepayments and deposits

|

18,750

|

-

|

||||||

|

Prepaid land leases

|

459,774

|

47,307

|

||||||

|

Deferred tax assets

|

7,094

|

6,973

|

||||||

|

Total Current Assets

|

131,442,550

|

107,258,813

|

||||||

|

Non-Current Assets

|

||||||||

|

Property, plant and equipment, net

|

155,117,858

|

165,942,542

|

||||||

|

Property, plant and equipment under capital leases, net

|

1,898,683

|

1,996,478

|

||||||

|

Prepaid land leases, net of current portion

|

752,697

|

748,502

|

||||||

|

Deferred tax assets

|

2,285,533

|

2,246,699

|

||||||

|

Total non-current assets

|

160,054,771

|

170,934,221

|

||||||

|

Total Assets

|

$

|

291,497,321

|

$

|

278,193,034

|

||||

|

Liabilities and Stockholders’ Equity

|

||||||||

|

Current Liabilities

|

||||||||

|

Accounts payable and accrued expenses

|

$

|

6,330,644

|

$

|

6,533,236

|

||||

|

Retention payable

|

385,360

|

1,432,690

|

||||||

|

Capital lease obligation, current portion

|

99,011

|

193,164

|

||||||

|

Taxes payable

|

4,715,553

|

2,856,658

|

||||||

|

Total Current Liabilities

|

11,530,568

|

11,015,748

|

||||||

|

Non-Current Liabilities

|

||||||||

|

Capital lease obligation, net of current portion

|

2,904,931

|

2,952,902

|

||||||

|

Total Liabilities

|

$

|

14,435,499

|

$

|

13,968,650

|

||||

|

|

||||||||

|

Stockholders’ Equity

|

||||||||

|

PREFERRED STOCK; $0.001 par value; 1,000,000 shares authorized; none outstanding

|

$

|

$

|

||||||

|

COMMON STOCK; $0.0005 par value; 400,000,000 shares authorized as of June 30, 2013 and December 31, 2012; 38,552,070 and 38,552,070 shares issued; and 38,367,471 and 38,367,471 shares outstanding as of June 30,

2013 and December 31, 2012, respectively

|

19,276

|

19,276

|

||||||

|

Treasury stock; 184,599 shares as of June 30, 2013 and December 31, 2012 at cost

|

(500,000

|

)

|

(500,000

|

)

|

||||

|

Additional paid-in capital

|

80,021,488

|

79,489,188

|

||||||

|

Retained earnings unappropriated

|

153,572,726

|

146,745,754

|

||||||

|

Retained earnings appropriated

|

16,385,779

|

15,973,887

|

||||||

|

Cumulative translation adjustment

|

27,562,553

|

22,496,279

|

||||||

|

Total Stockholders’ Equity

|

277,061,822

|

264,224,384

|

||||||

|

Total Liabilities and Stockholders’ Equity

|

$

|

291,497,321

|

$

|

278,193,034

|

||||

See accompanying notes to the condensed consolidated financial statements.

GULF RESOURCES, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(Expressed in U.S. dollars)

(UNAUDITED)

|

Three-Month Period Ended June 30,

|

Six-Month Period Ended June 30,

|

|||||||||||||||

|

2013

|

2012

|

2013

|

2012

|

|||||||||||||

|

NET REVENUE

|

||||||||||||||||

|

Net revenue

|

$

|

32,853,896

|

$

|

31,314,846

|

$

|

55,356,476

|

$

|

55,123,520

|

||||||||

|

OPERATING INCOME (EXPENSES)

|

||||||||||||||||

|

Cost of net revenue

|

(23,260,201

|

)

|

(21,389,651

|

)

|

(41,245,673

|

)

|

(38,505,533

|

)

|

||||||||

|

Sales, marketing and other operating expenses

|

(25,115

|

)

|

(22,709

|

)

|

(45,418

|

)

|

(40,473

|

)

|

||||||||

|

Research and development cost

|

(54,480

|

)

|

(62,526

|

)

|

(72,182

|

)

|

(105,324

|

)

|

||||||||

|

Write-off/Impairment on property, plant and equipment

|

-

|

(911,995

|

)

|

-

|

(911,995

|

)

|

||||||||||

|

General and administrative expenses

|

(2,422,452

|

)

|

(1,370,866

|

)

|

(4,391,669

|

)

|

(3,483,071

|

)

|

||||||||

|

Other operating income

|

287,127

|

76,104

|

382,689

|

133,178

|

||||||||||||

|

(25,475,121

|

)

|

(23,681,643

|

)

|

(45,372,253

|

)

|

(42,913,218

|

)

|

|||||||||

|

INCOME FROM OPERATIONS

|

7,378,775

|

7,633,203

|

9,984,223

|

12,210,302

|

||||||||||||

|

OTHER INCOME (EXPENSE)

|

||||||||||||||||

|

Interest expense

|

(53,583

|

)

|

(54,255

|

)

|

(106,589

|

)

|

(108,667

|

)

|

||||||||

|

Interest income

|

79,429

|

84,915

|

152,272

|

183,805

|

||||||||||||

|

INCOME BEFORE TAXES

|

7,404,621

|

7,663,863

|

10,029,906

|

12,285,440

|

||||||||||||

|

INCOME TAXES

|

(2,048,722

|

)

|

(1,975,189

|

)

|

(2,791,042

|

)

|

(3,309,659

|

)

|

||||||||

|

NET INCOME

|

$

|

5,355,899

|

$

|

5,688,674

|

$

|

7,238,864

|

$

|

8,975,781

|

||||||||

|

COMPREHENSIVE INCOME:

|

||||||||||||||||

|

NET INCOME

|

$

|

5,355,899

|

$

|

5,688,674

|

$

|

7,238,864

|

$

|

8,975,781

|

||||||||

|

OTHER COMPREHENSIVE INCOME (LOSS)

|

||||||||||||||||

|

- Foreign currency translation adjustments

|

4,298,508

|

(1,316,002

|

)

|

5,066,274

|

(1,038,104

|

)

|

||||||||||

|

COMPREHENSIVE INCOME

|

$

|

9,654,407

|

$

|

4,372,672

|

$

|

12,305,138

|

$

|

7,937,677

|

||||||||

|

EARNINGS PER SHARE:

|

||||||||||||||||

|

BASIC

|

$

|

0.14

|

$

|

0.16

|

$

|

0.19

|

$

|

0.26

|

||||||||

|

DILUTED

|

$

|

0.14

|

$

|

0.16

|

$

|

0.19

|

$

|

0.26

|

||||||||

|

WEIGHTED AVERAGE NUMBER OF SHARES:

|

||||||||||||||||

|

BASIC

|

38,367,471

|

34,560,743

|

38,367,471

|

34,560,743

|

||||||||||||

|

DILUTED

|

38,591,127

|

34,560,743

|

38,546,042

|

34,561,394

|

||||||||||||

See accompanying notes to the condensed consolidated financial statements.

|

GULF RESOURCES, INC.

|

|

AND SUBSIDIARIES

|

|

CONDENSED CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

|

|

SIX-MONTH PERIOD ENDED JUNE 30, 2013

|

|

(Expressed in U.S. dollars)

|

|

(UNAUDITED)

|

|

Common stock

|

||||||||||||||||||||||||||||||||||||||||

|

Number

|

Number

|

Number

|

Additional

|

Statutory

|

Cumulative

|

|||||||||||||||||||||||||||||||||||

|

of shares

|

of shares

|

of treasury

|

Treasury

|

paid-in

|

common

|

Retained

|

translation

|

|||||||||||||||||||||||||||||||||

|

issued

|

outstanding

|

stock

|

Amount

|

stock

|

capital

|

reserve

|

earnings

|

adjustment

|

Total

|

|||||||||||||||||||||||||||||||

|

$

|

$

|

$

|

$

|

$

|

$

|

$

|

||||||||||||||||||||||||||||||||||

|

BALANCE AT DECEMBER 31, 2012

|

38,552,070 | 38,367,471 | 184,599 | 19,276 | (500,000 | ) | 79,489,188 | 15,973,887 | 146,745,754 | 22,496,279 | 264,224,384 | |||||||||||||||||||||||||||||

|

Translation adjustment

|

-

|

- | - |

-

|

-

|

-

|

-

|

5,066,274 | 5,066,274 | |||||||||||||||||||||||||||||||

|

Issuance of stock options to employees

|

- | - | - | - | - | 532,300 | - | - | - | 532,300 | ||||||||||||||||||||||||||||||

|

Net income for six-month period ended June 30, 2013

|

-

|

- | - |

-

|

- |

-

|

-

|

7,238,864 |

-

|

7,238,864 | ||||||||||||||||||||||||||||||

|

Transfer to statutory common reserve fund

|

- | - | - | - | - | - | 411,892 | (411,892 | ) | - | - | |||||||||||||||||||||||||||||

|

BALANCE AT JUNE 30, 2013

|

38,552,070 | 38,367,471 | 184,599 | 19,276 | (500,000 | ) | 80,021,488 | 16,385,779 | 153,572,726 | 27,562,553 | 277,061,822 | |||||||||||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

|

GULF RESOURCES, INC.

|

|

AND SUBSIDIARIES

|

|

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

|

|

(Expressed in U.S. dollars)

|

|

(UNAUDITED)

|

|

Six-Month Period Ended June 30,

|

||||||||

|

2013

|

2012

|

|||||||

|

|

|

|||||||

|

CASH FLOWS FROM OPERATING ACTIVITIES

|

|

|

||||||

|

Net income

|

$

|

7,238,864

|

$

|

8,975,781

|

||||

|

Adjustments to reconcile net income to net cash provided by operating activities:

|

||||||||

|

Interest on capital lease obligation

|

106,206

|

108,044

|

||||||

|

Amortization of prepaid land leases

|

189,918

|

105,051

|

||||||

|

Depreciation and amortization

|

13,685,539

|

11,290,588

|

||||||

|

Write-off/Impairment loss on property, plant and equipment

|

-

|

911,995

|

||||||

|

Exchange (gain) loss on inter-company balances

|

431,147

|

(92,057

|

)

|

|||||

|

Stock-based compensation expense

|

532,300

|

26,300

|

||||||

|

Deferred tax asset

|

-

|

160,826

|

||||||

|

Changes in assets and liabilities:

|

||||||||

|

Accounts receivable

|

(2,621,905

|

)

|

(19,514,217

|

)

|

||||

|

Inventories

|

715,714

|

467,279

|

||||||

|

Prepayments and deposits

|

(18,750

|

)

|

(38,610

|

)

|

||||

|

Accounts payable and accrued expenses

|

(296,268

|

)

|

206,207

|

|||||

|

Retention payable

|

(1,055,003

|

)

|

(457,813

|

)

|

||||

|

Taxes payable

|

1,797,837

|

189,434

|

||||||

|

Net cash provided by operating activities

|

20,705,599

|

2,338,808

|

||||||

|

CASH FLOWS USED IN INVESTING ACTIVITIES

|

||||||||

|

Additions of prepaid land leases

|

(588,830

|

)

|

(422,877

|

)

|

||||

|

Increase in construction in progress

|

-

|

(7,871,130

|

)

|

|||||

|

Net cash used in investing activities

|

(588,830

|

)

|

(8,294,007

|

)

|

||||

|

CASH FLOWS USED IN FINANCING ACTIVITIES

|

||||||||

|

Repayment of capital lease obligation

|

(302,498

|

)

|

(297,598

|

)

|

||||

|

Net cash used in financing activities

|

(302,498

|

)

|

(297,598

|

)

|

||||

|

EFFECTS OF EXCHANGE RATE CHANGES ON CASH AND CASH EQUIVALENTS

|

1,367,206

|

(278,492

|

)

|

|||||

|

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS

|

21,181,477

|

(6,531,289

|

)

|

|||||

|

CASH AND CASH EQUIVALENTS - BEGINNING OF PERIOD

|

65,241,035

|

78,576,060

|

||||||

|

CASH AND CASH EQUIVALENTS - END OF PERIOD

|

$

|

86,422,512

|

$

|

72,044,771

|

||||

|

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION

|

||||||||

|

Cash paid during the period for:

|

||||||||

|

Income taxes

|

$

|

1,287,273

|

$

|

2,945,542

|

||||

See accompanying notes to the condensed consolidated financial statements.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 1 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of Presentation and Consolidation

The accompanying condensed financial statements have been prepared by Gulf Resources, Inc. a Delaware corporation and its subsidiaries (collectively, the “Company”), without audit, in accordance with the instructions to Form 10-Q and, therefore, do not necessarily include all information and footnotes necessary for a fair statement of its financial position, results of operations and cash flows in accordance with accounting principles generally accepted in the United States (“US GAAP”). The balance sheet at December 31, 2012 is derived from the audited balance sheet but does not include all disclosures required by US GAAP. In connection with the consolidated financial statements and notes included in this report, reference is made to the consolidated financial statements and notes contained in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2012 (the “2012 Form 10-K”).

In the opinion of management, the unaudited financial information for the three and six months ended June 30, 2013 presented reflects all adjustments, which are only normal and recurring, necessary for a fair statement of results of operations, financial position and cash flows. These condensed financial statements should be read in conjunction with the financial statements included in the Company’s 2012 Form 10-K. Operating results for the interim periods are not necessarily indicative of operating results for an entire fiscal year.

The preparation of financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the amounts that are reported in the financial statements and accompanying disclosures. Although these estimates are based on management’s best knowledge of current events and actions that the Company may undertake in the future, actual results may be different from the estimates. The Company also exercises judgments in the preparation of these condensed financial statements in the areas including classification of leases and related party transactions.

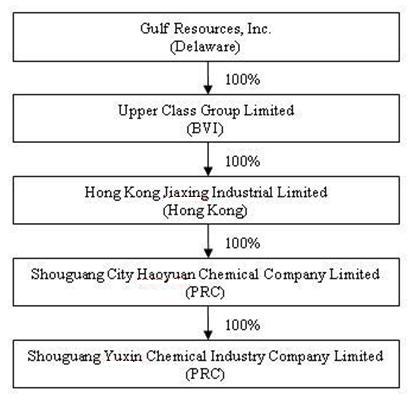

The consolidated financial statements include the accounts of Gulf Resources, Inc. and its wholly-owned subsidiary, Upper Class Group Limited, a company incorporated in the British Virgin Islands, which owns 100% of Hong Kong Jiaxing Industrial Limited, a company incorporated in Hong Kong (“HKJI”). HKJI owns 100% of Shouguang City Haoyuan Chemical Company Limited ("SCHC") which owns 100% of Shouguang Yuxin Chemical Industry Co., Limited (“SYCI”). All material intercompany transactions have been eliminated on consolidation.

(b) Nature of the Business

The Company manufactures and trades bromine and crude salt through its wholly-owned subsidiary, Shouguang City Haoyuan Chemical Company Limited ("SCHC"), and manufactures chemical products for use in the oil industry and paper manufacturing industry through its wholly-owned subsidiary, Shouguang Yuxin Chemical Industry Co., Limited ("SYCI") in The People’s Republic of China (“PRC”).

(c) Allowance for Doubtful Accounts

As of June 30, 2013 and December 31, 2012, allowances for doubtful accounts were nil. No allowances for doubtful accounts were charged to the income statement for the three-month and six-month periods ended June 30, 2013 and 2012.

(d) Concentration of Credit Risk

The Company is exposed to credit risk in the normal course of business, primarily related to accounts receivable and cash and cash equivalents. Substantially all of the Company’s cash and cash equivalents are maintained with financial institutions in the PRC, namely, Industrial and Commercial Bank of China Limited and China Merchants Bank Company Limited, which are not insured or otherwise protected. The Company placed $86,422,512 and $65,241,035 with these institutions as of June 30, 2013 and December 31, 2012, respectively. The Company has not experienced any losses in such accounts in the PRC.

Concentrations of credit risk with respect to accounts receivable exists as the Company sells a substantial portion of its products to a limited number of customers. However, such concentrations of credit risks are limited since the Company performs ongoing credit evaluations of its customers’ financial condition and due to the generally short payment terms. About 89.5% and 100% of the balances of accounts receivable as of June 30, 2013 and December 31, 2012, respectively, are outstanding for less than three months. For the balances of accounts receivable aged more than 90 days as of June 30, 2013, all was settled in July 2013.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 1 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

(e) Property, Plant and Equipment

Property, plant and equipment are stated at cost less accumulated depreciation and any impairment losses. Expenditures for new facilities or equipment, and major expenditures for betterment of existing facilities or equipment are capitalized and depreciated using the straight-line method at rates sufficient to depreciate such costs over the estimated productive lives. All other ordinary repair and maintenance costs are expensed as incurred.

Mineral rights are recorded at cost less accumulated depreciation and any impairment losses. Mineral rights are amortized ratably over the term of the lease, or the equivalent term under the units of production method, whichever is shorter.

Construction in progress primarily represents direct costs of construction of plant, machinery and equipment. Costs incurred are capitalized and transferred to property and equipment upon completion, at which time depreciation commences.

The Company’s depreciation and amortization policies on property, plant and equipment, other than mineral rights and construction in progress, are as follows:

|

Useful life

(in years)

|

||

|

Buildings (including salt pans)

|

8 - 20

|

|

|

Plant and machinery (including protective shells, transmission channels and ducts)

|

5 - 8

|

|

|

Motor vehicles

|

5

|

|

|

Furniture, fixtures and equipment

|

8

|

Property, plant and equipment under capital leases are depreciated over their expected useful lives on the same basis as owned assets, or where shorter, the term of the lease, which is 20 years.

(f) Retirement Benefits

Pursuant to the relevant laws and regulations in the PRC, the Company participates in a defined contribution retirement plan for its employees arranged by a governmental organization. The Company makes contributions to the retirement scheme at the applicable rate based on the employees’ salaries. The required contributions under the retirement plans are charged to the consolidated income statement on an accrual basis when they are due. The Company’s contributions totaled $124,158 and $112,275 for the three-month periods ended June 30, 2013 and 2012, respectively, and totaled $243,913 and $242,393 for the six-month periods ended June 30, 2013 and 2012, respectively.

(g) Revenue Recognition

The Company recognizes revenue, net of value-added tax, when persuasive evidence of an arrangement exists, delivery of the goods has occurred, customer acceptance has been obtained, which means the significant risks and ownership have been transferred to the customer, the price is fixed or determinable and collectability is reasonably assured.

(h) Shipping and Handling Fees and Costs

The Company does not charge its customers for shipping and handling as all customers arrange their own transportation of finished goods. The Company classifies shipping and handling costs for purchase of raw materials as part of the cost of net revenue, which amounted to $0 and $80,607 for the six-month periods ended June 30, 2013 and 2012, respectively. There is no such shipping and handling costs for the three-month period ended June 30, 2013 and 2012 as they are borne by the suppliers since April 2012.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 1 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

(i) Recoverability of Long-lived Assets

In accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 360-10-35 “Impairment or Disposal of Long-lived Assets” , long-lived assets to be held and used are analyzed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be fully recoverable or that the useful lives of those assets are no longer appropriate. The Company evaluates at each balance sheet date whether events and circumstances have occurred that indicate possible impairment.

The Company determines the existence of such impairment by measuring the expected future cash flows (undiscounted and without interest charges) and comparing such amount to the carrying amount of the assets. An impairment loss, if one exists, is then measured as the amount by which the carrying amount of the asset exceeds the discounted estimated future cash flows. Assets to be disposed of are reported at the lower of the carrying amount or fair value of such assets less costs to sell. Asset impairment charges are recorded to reduce the carrying amount of the long-lived asset that will be sold or disposed of to their estimated fair values. Charges for the asset impairment reduce the carrying amount of the long-lived assets to their estimated salvage value in connection with the decision to dispose of such assets.

For the three-month periods ended June 30, 2012, Certain eroded protective shells for transmission channels and ducts, with net book values of $911,995, were replaced during the second phase enhancement project, write-offs of the same amounts, were made in this quarter and included in write-off/impairment on property, plant and equipment.

For the three-month and six-month periods ended June 30, 2013, the Company determined that there are no events or circumstances indicating possible impairment of its long-lived assets.

(j) Basic and Diluted Net Income per Share of Common Stock

Basic earnings per common share are based on the weighted average number of shares outstanding during the periods presented. Diluted earnings per share are computed using weighted average number of common shares plus dilutive common share equivalents outstanding during the period. Potential common shares that would have the effect of increasing diluted earnings per share are considered to be anti-dilutive, i.e. the exercise prices of the outstanding stock options were greater than the market price of the common stock. Anti-dilutive common stock equivalents which were excluded from the calculation of number of dilutive common stock equivalents amounted to 5,282,849 and 2,906,971 shares for the three-month periods ended June 30, 2013 and 2012, respectively, and amounted to 5,189,462 and 2,175,548 shares for the six-month periods ended June 30, 2013 and 2012, respectively. These awards could be dilutive in the future if the market price of the common stock increases and is greater than the exercise price of these awards.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 1 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

(j) Basic and Diluted Net Income per Share of Common Stock – Continued

The following table sets forth the computation of basic and diluted earnings per share:

|

|

Three-Month Period Ended June 30,

|

Six-Month Period Ended June 30,

|

||||||||||||||

|

2013

|

2012

|

2013

|

2012

|

|||||||||||||

|

Numerator

|

||||||||||||||||

|

Net income

|

$

|

5,355,899

|

$

|

5,688,674

|

$

|

7,238,864

|

$

|

8,975,781

|

||||||||

|

Denominator

|

||||||||||||||||

|

Basic: Weighted-average common shares outstanding during the period

|

38,367,471

|

34,560,743

|

38,367,471

|

34,560,743

|

||||||||||||

|

Add: Dilutive effect of stock options

|

223,656

|

-

|

178,571

|

651

|

||||||||||||

|

Diluted

|

38,591,127

|

34,560,743

|

38,546,042

|

34,561,394

|

||||||||||||

|

Net income per share

|

||||||||||||||||

|

Basic

|

$

|

0.14

|

$

|

0.16

|

$

|

0.19

|

$

|

0.26

|

||||||||

|

Diluted

|

$

|

0.14

|

$

|

0.16

|

$

|

0.19

|

$

|

0.26

|

||||||||

(k) Reporting Currency and Translation

The financial statements of the Company’s foreign subsidiaries are measured using the local currency, Renminbi (“RMB”), as the functional currency; whereas the functional currency and reporting currency of the Company is the United States dollar (“USD” or “$”).

As such, the Company uses the “current rate method” to translate its PRC operations from RMB into USD, as required under ASC 830 “Foreign Currency Matters”. The assets and liabilities of its PRC operations are translated into USD using the rate of exchange prevailing at the balance sheet date. The capital accounts are translated at the historical rate. Adjustments resulting from the translation of the balance sheets of the Company’s PRC subsidiaries are recorded in stockholders’ equity as part of accumulated comprehensive income. The statement of income and comprehensive income is translated at average rates during the reporting period. Gains or losses resulting from transactions in currencies other than the functional currencies are recognized in net income for the reporting periods as part of general and administrative expense. The statement of cash flows is translated at average rates during the reporting period, with the exception of issuance of shares and payment of dividends which are translated at historical rates.

(l) Foreign Operations

All of the Company’s operations and assets are located in PRC. The Company may be adversely affected by possible political or economic events in this country. The effect of these factors cannot be accurately predicted.

(m) New Accounting Pronouncements

No accounting standards and guidance with an effective date during the three-month and six-month periods ended June 30, 2013 or issued during 2013 had or are expected to have a significant impact on the Company’s condensed consolidated financial statements.

NOTE 2 – ASSET ACQUISITIONS

On November 26, 2012, the Company acquired substantially all of the assets owned by Chengyong Zhao in Guantai Village located Shouguang City Yangkou Township area (the “Chengyong Zhao Property” or “Factory No. 11”). The Chengyong Zhao Property includes a 20-year land lease covering approximately 1,727 acres of real property, with the related production facility, wells, pipelines, other production equipment, and the buildings located on the property. The total purchase price for the acquired assets was RMB 62 million (approximately $9.80 million), consisting of RMB 31 million (approximately $4.93million) in cash and 3,806,728 shares of the Company’s Common Stock valued at approximately $4.87 million (fair value). The production line of Factory No. 11 was resumed in March 2013 after certain repair and adjustments.

The Factory No. 11 described above was not in operation when the Company acquired the assets. Production of Factory No. 11 had previously been halted by the government since the owners of the bromine factories did not hold the proper license for the exploration and production of bromine. The Factories No.11 had not been in operation for more than six months at the time of the acquisition. The Company recorded the above transactions as a purchase of assets.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 3 – INVENTORIES

Inventories consist of:

|

June 30,

2013

|

December 31,

2012

|

|||||||

|

Raw materials

|

$

|

692,551

|

$

|

773,453

|

||||

|

Finished goods

|

4,707,039

|

5,248,039

|

||||||

|

Allowance for obsolete and slow-moving inventory

|

(28,376

|

)

|

(27,894

|

)

|

||||

|

$

|

5,371,214

|

$

|

5,993,598

|

|||||

NOTE 4 – PREPAID LAND LEASES

The Company prepaid for land leases with lease terms for periods ranging from one to fifty years to use the land on which the office premises, production facilities and warehouses of the Company are situated. The prepaid land lease is amortized on a straight line basis.

During the three-month periods ended June 30, 2013 and 2012, amortization of prepaid land lease totaled $91,703 and $50,180, respectively, which were recorded as cost of net revenue. During the six-month periods ended June 30, 2013 and 2012, amortization of prepaid land lease totaled $189,918 and $105,051, respectively, which were recorded as cost of net revenue.

The Company has the rights to use certain parcels of land located in Shouguang, the PRC, through lease agreements signed with local townships. Such parcels of land are collectively owned by local townships and accordingly, the Company could not obtain land use rights certificates on these parcels of land. The parcels of land that the Company could not obtain land use rights certificates cover a total of approximately 59.39 square kilometers with an aggregate carrying value of $1,169,534 and approximately 59.39 square kilometers with an aggregate carrying value of $753,086 as at June 30, 2013 and December 31, 2012, respectively.

NOTE 5 – PROPERTY, PLANT AND EQUIPMENT, NET

Property, plant and equipment, net consist of the following:

|

June 30,

2013

|

December 31,

2012

|

|||||||

|

At cost:

|

||||||||

|

Mineral rights

|

$

|

6,443,763

|

$

|

6,334,277

|

||||

|

Buildings

|

51,785,222

|

50,905,337

|

||||||

|

Plant and machinery

|

168,992,691

|

166,121,329

|

||||||

|

Motor vehicles

|

9,298

|

9,140

|

||||||

|

Furniture, fixtures and office equipment

|

4,859,614

|

4,777,044

|

||||||

|

Total

|

232,090,588

|

228,147,127

|

||||||

|

Less: Accumulated depreciation and amortization

|

(76,972,730

|

)

|

(62,204,585

|

)

|

||||

|

Net book value

|

$

|

155,117,858

|

$

|

165,942,542

|

||||

The Company has certain buildings and salt pans erected on parcels of land located in Shouguang, PRC, and such parcels of land are collectively owned by local townships. The Company has not been able to obtain property ownership certificates over these buildings and salt pans as the Company could not obtain land use rights certificates on the underlying parcels of land. The aggregate carrying values of these properties situated on parcels of the land are $39,179,525 and $39,563,438 as at June 30, 2013 and December 31, 2012, respectively.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 5 – PROPERTY, PLANT AND EQUIPMENT, NET – Continued

During the three-month period ended June 30, 2013, depreciation and amortization expense totaled $6,812,181, of which $6,504,164 and $308,017 were recorded as cost of net revenue and administrative expenses, respectively. During the three-month period ended June 30, 2012, depreciation and amortization expense totaled $5,521,178, of which $5,403,370 and $117,808 were recorded as cost of net revenue and administrative expenses, respectively. During the six-month period ended June 30, 2013, depreciation and amortization expense totaled $13,554,571, of which $12,758,306 and $796,264 were recorded as cost of sales and administrative expenses respectively. During the six-month period ended June 30, 2012, depreciation and amortization expense totaled $11,118,099, of which $10,645,703 and $472,396 were recorded as cost of sales and administrative expenses respectively.

NOTE 6 – PROPERTY, PLANT AND EQUIPMENT UNDER CAPITAL LEASES, NET

Property, plant and equipment under capital leases, net consist of the following:

|

June 30,

2013

|

December 31,

2012

|

|||||||

|

At cost:

|

||||||||

|

Buildings

|

$

|

133,190

|

$

|

130,925

|

||||

|

Plant and machinery

|

2,503,566

|

2,461,028

|

||||||

|

Total

|

2,636,756

|

2,591,953

|

||||||

|

Less: Accumulated depreciation and amortization

|

(738,073

|

)

|

(595,475

|

)

|

||||

|

Net book value

|

$

|

1,898,683

|

$

|

1,996,478

|

||||

The above buildings erected on parcels of land located in Shouguang, PRC, are collectively owned by local townships. The Company has not been able to obtain property ownership certificates over these buildings as the Company could not obtain land use rights certificates on the underlying parcels of land.

During the three-month periods ended June 30, 2013 and 2012, depreciation and amortization expense totaled $65,870 and $86,247, respectively, which was recorded as cost of net revenue. During the six-month periods ended June 30, 2013 and 2012, depreciation and amortization expense totaled $130,968 and $172,489, respectively, which was recorded as cost of net revenue.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 7 – ACCOUNTS PAYABLE AND ACCRUED EXPENSES

Accounts payable and accrued expenses consist of the following:

|

June 30,

|

December 31,

|

|||||||

|

2013

|

2012

|

|||||||

|

Accounts payable

|

$

|

5,173,565

|

$

|

3,797,552

|

||||

|

Salary payable

|

202,317

|

190,926

|

||||||

|

Social security insurance contribution payable

|

56,643

|

52,399

|

||||||

|

Price adjustment funds

|

395,936

|

1,758,828

|

||||||

|

Other payables

|

502,183

|

733,531

|

||||||

|

Total

|

$

|

6,330,644

|

$

|

6,533,236

|

||||

NOTE 8 – RELATED PARTY TRANSACTIONS

During the three-month and six-month periods ended June 30, 2013, the Company borrowed $99,000 and $420,449, respectively, and fully repaid later during the same period, from Jiaxing Lighting Appliance Company Limited (Jiaxing Lighting”), in which Mr. Ming Yang, a shareholder and the Chairman of the Company, had a 100% equity interest in Jiaxing Lighting. The amounts due to Jiaxing Lighting were unsecured, interest free and repayable on demand.

NOTE 9 – TAXES PAYABLE

|

Taxes payable consists of the following:

|

|

June 30,

|

December 31,

|

|||||||

|

2013

|

2012

|

|||||||

|

Income tax payable

|

$

|

2,129,332

|

$

|

606,190

|

||||

|

Mineral resource compensation fee payable

|

366,583

|

239,776

|

||||||

|

Value added tax payable

|

1,065,876

|

771,673

|

||||||

|

Land use tax payable

|

940,364

|

888,349

|

||||||

|

Other tax payables

|

213,398

|

350,670

|

||||||

|

Total

|

$

|

4,715,553

|

$

|

2,856,658

|

||||

NOTE 10 – CAPITAL LEASE OBLIGATIONS

The components of capital lease obligations are as follows:

|

Imputed

|

June 30,

|

December 31,

|

|||||||

|

Interest rate

|

2013

|

2012

|

|||||||

|

Total capital lease obligations

|

6.7%

|

$

|

3,003,942

|

$

|

3,146,066

|

||||

|

Less: Current portion

|

(99,011

|

)

|

(193,164

|

)

|

|||||

|

Capital lease obligations, net of current portion

|

$

|

2,904,931

|

$

|

2,952,902

|

|||||

Interest expenses from capital lease obligations amounted to $53,416 and $54,024 for the three-month periods ended June 30, 2013 and 2012, respectively, which were charged to the income statements. Interest expenses from capital lease obligations amounted to $106,206 and $108,044 for the six-month periods ended June 30, 2013 and 2012, respectively, which were charged to the income statements.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 11 ––EQUITY

|

(a)

|

Authorized shares

|

During the annual general meeting held on June 18, 2013, the shareholders of the Company approved the amendment to the Certificate of Incorporation to decrease the number of the authorized shares of the Company’s comment stocks to 80,000,000. The Company is in the process of filing the amendment and restatement of the Certificate of Incorporation with the Secretary of the State of Delaware to decrease the number of authorized shares of the Company’s common stock.

|

(b)

|

Retained Earnings - Appropriated

|

In accordance with the relevant PRC regulations and the PRC subsidiaries’ Articles of Association, the Company’s PRC subsidiaries are required to allocate its profit after tax to the following reserve:

Statutory Common Reserve Funds

SCHC and SYCI are required each year to transfer at least 10% of the profit after tax as reported under the PRC statutory financial statements to the Statutory Common Reserve Funds until the balance reaches 50% of the registered share capital. This reserve can be used to make up any loss incurred or to increase share capital. Except for the reduction of losses incurred, any other application should not result in this reserve balance falling below 25% of the registered capital. The Statutory Common Reserve Fund as of June 30, 2013 for SCHC and SYCI is 35% and 50% of its registered capital respectively.

NOTE 12 – STOCK-BASED COMPENSATION

Pursuant to the Company’s Amended and Restated 2007 Equity Incentive Plan, the aggregate number shares of the Company’s common stock available for grant of stock options and issuance is 4,341,989 shares.

The fair value of each option award below is estimated on the date of grant using the Black-Scholes option-pricing model. The risk free rate is based on the yield-to-maturity in continuous compounding of the US Government Bonds with the time-to-maturity similar to the expected tenor of the option granted, volatility is based on the annualized historical stock price volatility of the Company, and the expected life is based on the estimated average of the life of options using the “simplified” method, as prescribed in FASB ASC 718, due to insufficient historical exercise activity during recent years as a basis from which to estimate future exercise patterns.

In early March 2013, the Company granted to an independent director an option to purchase 12,500 shares of the Company’s common stock at an exercise price of $1.12 per share and the options vested immediately. The options were valued at $4,900 fair value, with assumed 74.73% volatility, a three-year expiration term with expected tenor of 1.49 years, a risk free rate of 0.19% and no dividend yield. For the three-month period ended March 31, 2013, $4,900 was recognized as general and administrative expenses.

On May 30, 2013, the Company granted to 3 executive officers and 17 management staff options to purchase 600,000 shares and 203,000 shares of the Company’s common stock, respectively, at an exercise price of $0.952 per share and the options vested immediately. The options to executive officers and management staff were valued at $394,100 and $133,300 fair value, respectively, both with assumed 80.76% volatility, a four-year expiration term with expected tenor of 2 years, a risk free rate of 0.29% and no dividend yield.

The following table summarizes all Company stock option transactions between January 1, 2013 and June 30, 2013.

|

Number of Option

and Warrants

Outstanding

|

Number of Option

and Warrants

Vested

|

Range of

Exercise Price per Common Share

|

|||||||||

|

Balance, January 1, 2013

|

1,974,471

|

1,974,471

|

$0.95 - $12.60

|

||||||||

|

Granted and vested during the six-month period ended June 30, 2013

|

815,500

|

815,500

|

$0.95 - $1.12

|

||||||||

|

Balance, June 30, 2013

|

2,789,971

|

2,789,971

|

$0.95 - $12.60

|

||||||||

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 12 – STOCK-BASED COMPENSATION – Continued

|

Stock and Warrants Options Exercisable and Outstanding

|

||||||||

|

Weighted Average

|

Weighted Average

|

|||||||

|

Remaining

|

Exercise Price of

|

|||||||

|

Outstanding at June 30, 2013

|

Range of

Exercise Prices

|

Contractual Life

(Years)

|

Options Currently

Outstanding

|

|||||

|

Exercisable and outstanding

|

2,789,971

|

$0.95 - $12.60

|

2.75

|

$ 3.11

|

||||

The weighted average grant-date fair values as at June 30, 2013 and December 31, 2012 were $3.64 and $4.62, respectively.

NOTE 13 – INCOME TAXES

The Company utilizes the asset and liability method of accounting for income taxes in accordance with FASB ASC 740-10.

(a) United States

Gulf Resources, Inc. is subject to the United States of America Tax law at a tax rate of 34%. No provision for the US federal income taxes has been made as the Company had no US taxable income for the three-month and six-month periods ended June 30, 2013 and 2012, and management believes that its earnings are permanently invested in the PRC.

(b) BVI

Upper Class Group Limited, a subsidiary of Gulf Resources, Inc., was incorporated in the BVI and, under the current laws of the BVI, it is not subject to tax on income or capital gain in the BVI. Upper Class Group Limited did not generate assessable profit for the three-month and six-month periods ended June 30, 2013 and 2012.

(c) Hong Kong

Hong Kong Jiaxing Industrial Limited, a subsidiary of Upper Class Group Limited, was incorporated in Hong Kong and is subject to Hong Kong profits tax. The Company is subject to Hong Kong taxation on its activities conducted in Hong Kong and income arising in or derived from Hong Kong. No provision for profits tax has been made as the Company has no assessable income for the three-month and six-month periods ended June 30, 2013 and 2012. The applicable statutory tax rates for the three-month and six-month periods ended June 30, 2013 and 2012 are 16.5%.

(d) PRC

Enterprise income tax (“EIT”) for SCHC and SYCI in the PRC is charged at 25% of the assessable profits.

The operating subsidiaries SCHC and SYCI are wholly foreign-owned enterprises (“FIE”) incorporated in the PRC and are subject to PRC Foreign Enterprise Income Tax Law.

On February 22, 2008, the Ministry of Finance (“MOF”) and the State Administration of Taxation (“SAT”) jointly issued Cai Shui [2008] Circular 1 (“Circular 1”). According to Article 4 of Circular 1, distributions of accumulated profits earned by a FIE prior to January 1, 2008 to foreign investor(s) in 2008 will be exempted from withholding tax (“WHT”) while distribution of the profit earned by an FIE after January 1, 2008 to its foreign investor(s) shall be subject to WHT at 5% effective tax rate.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2012

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 13 – INCOME TAXES – Continued

As of June 30, 2013 and December 31, 2012, the accumulated distributable earnings under the Generally Accepted Accounting Principles (GAAP”) of PRC are $208,469,568 and $197,042,047, respectively. Since the Company intends to reinvest its earnings to further expand its businesses in mainland China, its foreign invested enterprises do not intend to declare dividends to their immediate foreign holding companies in the foreseeable future. Accordingly, as of June 30, 2013 and December 31, 2012, the Company has not recorded any WHT on the cumulative amount of distributable retained earnings of its foreign invested enterprises in China. As of June 30, 2013 and December 31, 2012, the unrecognized WHT are $9,321,132 and $8,768,486, respectively.

The components of the provision for income taxes from continuing operations are:

|

Three-Month Period Ended June 30,

|

Six-Month Period Ended June 30,

|

||||||||||||||

|

2013

|

2012

|

2013

|

2012

|

||||||||||||

|

Current taxes – PRC

|

$ | 2,048,722 | $ | 1,892,567 | $ | 2,791,042 | $ | 3,148,833 | |||||||

|

Deferred taxes – PRC

|

- | 82,622 | - | 160,826 | |||||||||||

| $ | 2,048,722 | $ | 1,975,189 | $ | 2,791,042 | $ | 3,309,659 | ||||||||

The effective income tax expenses differ from the PRC statutory income tax rate of 25% from continuing operations in the PRC as follows:

|

Three-Month Period Ended June 30,

|

Six-Month Period Ended June 30,

|

|||||||||||||||

|

Reconciliations

|

2013

|

2012

|

2013

|

2012

|

||||||||||||

|

Statutory income tax rate

|

25

|

%

|

25

|

%

|

25

|

%

|

25

|

%

|

||||||||

|

Non-deductible expenses

|

1

|

%

|

0

|

%

|

1

|

%

|

0

|

%

|

||||||||

|

US federal net operating loss

|

2

|

%

|

1

|

%

|

2

|

%

|

2

|

%

|

||||||||

|

Effective tax rate

|

28

|

%

|

26

|

%

|

28

|

%

|

27

|

%

|

||||||||

Significant components of the Company’s deferred tax assets and liabilities at June 30, 2013 and December 31, 2012 are as follows:

|

June 30,

|

December 31,

|

|||||||

|

2013

|

2012

|

|||||||

|

Deferred tax liabilities

|

$

|

-

|

$

|

-

|

||||

|

Deferred tax assets:

|

||||||||

|

Allowance for obsolete and slow-moving inventories

|

$

|

7,094

|

$

|

6,973

|

||||

|

Impairment on property, plant and equipment

|

472,812

|

464,778

|

||||||

|

Exploration costs

|

1,812,721

|

1,781,921

|

||||||

|

Compensation costs of unexercised stock options

|

1,990,360

|

1,809,378

|

||||||

|

US federal net operating loss

|

8,876,646

|

8,809,935

|

||||||

|

Total deferred tax assets

|

13,159,633

|

12,872,985

|

||||||

|

Valuation allowance

|

(10,867,006

|

)

|

(10,619,313

|

)

|

||||

|

Net deferred tax asset

|

$

|

2,292,627

|

$

|

2,253,672

|

||||

|

Current deferred tax asset

|

$

|

7,094

|

$

|

6,973

|

||||

|

Long-term deferred tax asset

|

$

|

2,285,533

|

$

|

2,246,699

|

||||

The increase in valuation allowance for each of the three-month periods ended June 30, 2013 and 2012 is $148,308 and $106,382, respectively, and six-month periods ended June 30, 2013 and 2012 is $247,693 and $330,313, respectively.

There were no unrecognized tax benefits and accrual for uncertain tax positions as of June 30, 2013 and December 31, 2012.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 14 – BUSINESS SEGMENTS

The Company has three reportable segments: bromine, crude salt and chemical products. The reportable segments are consistent with how management views the markets served by the Company and the financial information that is reviewed by its chief operating decision maker.

An operating segment’s performance is primarily evaluated based on segment operating income, which excludes share-based compensation expense, certain corporate costs and other income not associated with the operations of the segment. These corporate costs (income) are separately stated below and also include costs that are related to functional areas such as accounting, treasury, information technology, legal, human resources, and internal audit. The Company believes that segment operating income, as defined above, is an appropriate measure for evaluating the operating performance of its segments. All the customers are located in PRC.

|

Three-Month Period Ended June 30, 2013

|

Bromine*

|

Crude

Salt*

|

Chemical

Products

|

Segment

Total

|

Corporate

|

Total

|

||||||||||||||||||

|

Net revenue

(external customers)

|

$

|

17,473,276

|

$

|

3,629,976

|

$

|

11,750,644

|

$

|

32,853,896

|

$

|

-

|

$

|

32,853,896

|

||||||||||||

|

Net revenue

(intersegment)

|

777,746

|

-

|

-

|

777,746

|

-

|

777,746

|

||||||||||||||||||

|

Income (loss) from operations before taxes

|

3,882,612

|

728,638

|

3,572,036

|

8,183,286

|

(804,511

|

)

|

7,378,775

|

|||||||||||||||||

|

Income taxes

|

941,322

|

209,755

|

897,645

|

2,048,722

|

-

|

2,048,722

|

||||||||||||||||||

|

Income (loss) from operations after taxes

|

2,941,290

|

518,883

|

2,674,391

|

6,134,564

|

(804,511

|

)

|

5,330,053

|

|||||||||||||||||

|

Total assets

|

174,524,258

|

56,693,091

|

60,193,635

|

291,410,984

|

86,337

|

291,497,321

|

||||||||||||||||||

|

Depreciation and amortization

|

4,309,920

|

1,687,487

|

880,645

|

6,878,052

|

-

|

6,878,052

|

||||||||||||||||||

|

Capital expenditures

|

-

|

-

|

-

|

-

|

-

|

-

|

||||||||||||||||||

|

Write-off / Impairment

|

-

|

-

|

-

|

-

|

-

|

-

|

||||||||||||||||||

|

Three-Month Period Ended June 30, 2012

|

Bromine*

|

Crude

Salt*

|

Chemical

Products

|

Segment

Total

|

Corporate

|

Total

|

||||||||||||||||||

|

Net revenue

(external customers)

|

$

|

17,539,429

|

$

|

3,779,658

|

$

|

9,995,759

|

$

|

31,314,846

|

$

|

-

|

$

|

31,314,846

|

||||||||||||

|

Net revenue

(intersegment)

|

808,596

|

-

|

-

|

808,596

|

-

|

808,596

|

||||||||||||||||||

|

Income (loss) from operations before taxes

|

3,933,561

|

888,555

|

3,007,381

|

7,829,497

|

(196,294

|

)

|

7,633,203

|

|||||||||||||||||

|

Income taxes

|

1,018,311

|

198,783

|

758,095

|

1,975,189

|

-

|

1,975,189

|

||||||||||||||||||

|

Income (loss) from operations after taxes

|

2,915,250

|

689,772

|

2,249,286

|

5,854,308

|

(196,294

|

)

|

5,658,014

|

|||||||||||||||||

|

Total assets

|

158,305,734

|

56,621,811

|

50,634,822

|

265,562,367

|

425,477

|

265,987,844

|

||||||||||||||||||

|

Depreciation and amortization

|

3,509,790

|

1,442,179

|

655,456

|

5,607,425

|

-

|

5,607,425

|

||||||||||||||||||

|

Capital expenditures

|

6,567,296

|

1,281,991

|

-

|

7,849,287

|

-

|

7,849,287

|

||||||||||||||||||

|

Write-off / Impairment

|

763,043

|

148,952

|

-

|

911,995

|

-

|

911,995

|

||||||||||||||||||

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2012

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 14 – BUSINESS SEGMENTS – Continued

|

Six-Month Period Ended June 30, 2013

|

Bromine*

|

Crude

Salt*

|

Chemical

Products

|

Segment

Total

|

Corporate

|

Total | ||||||||||||||||||

|

Net revenue

(external customers)

|

$

|

29,207,643

|

$

|

6,080,762

|

$

|

20,068,071

|

$

|

55,356,476

|

$

|

-

|

$

|

55,356,476

|

||||||||||||

|

Net revenue

(intersegment)

|

1,392,476

|

-

|

-

|

1,392,476

|

-

|

1,392,476

|

||||||||||||||||||

|

Income (loss) from operations before taxes

|

4,210,425

|

1,266,858

|

5,668,715

|

11,145,998

|

(1,161,775

|

)

|

9,984,223

|

|||||||||||||||||

|

Income taxes

|

1,121,955

|

243,020

|

1,426,067

|

2,791,042

|

-

|

2,791,042

|

||||||||||||||||||

|

Income (loss) from operations after taxes

|

3,088,471

|

1,023,837

|

4,242,648

|

8,354,956

|

(1,161,775

|

)

|

7,193,181

|

|||||||||||||||||

|

Total assets

|

174,524,258

|

56,693,091

|

60,193,635

|

291,410,984

|

86,337

|

291,497,321

|

||||||||||||||||||

|

Depreciation and amortization

|

8,687,891

|

3,246,686

|

1,750,962

|

13,685,539

|

-

|

13,685,539

|

||||||||||||||||||

|

Capital expenditures

|

-

|

-

|

-

|

-

|

-

|

-

|

||||||||||||||||||

|

Write-off / Impairment

|

-

|

-

|

-

|

-

|

-

|

-

|

||||||||||||||||||

|

Six-Month Period Ended June 30, 2012

|

Bromine*

|

Crude

Salt*

|

Chemical

Products

|

Segment

Total

|

Corporate

|

Total

|

||||||||||||||||||

|

Net revenue

(external customers)

|

$

|

30,993,311

|

$

|

6,054,582

|

$

|

18,075,627

|

$

|

55,123,520

|

$

|

-

|

$

|

55,123,520

|

||||||||||||

|

Net revenue

(intersegment)

|

1,563,153

|

-

|

-

|

1,563,153

|

-

|

1,563,153

|

||||||||||||||||||

|

Income (loss) from operations before taxes

|

6,401,865

|

1,437,005

|

5,250,276

|

13,089,146

|

(878,844

|

)

|

12,210,302

|

|||||||||||||||||

|

Income taxes

|

1,681,209

|

302,649

|

1,325,801

|

3,309,659

|

-

|

3,309,659

|

||||||||||||||||||

|

Income (loss) from operations after taxes

|

4,720,656

|

1,134,356

|

3,924,475

|

9,779,487

|

(878,844

|

)

|

8,900,643

|

|||||||||||||||||

|

Total assets

|

158,305,734

|

56,621,811

|

50,634,822

|

265,562,367

|

425,477

|

265,987,844

|

||||||||||||||||||

|

Depreciation and amortization

|

7,174,033

|

2,805,685

|

1,310,870

|

11,290,588

|

-

|

11,290,588

|

||||||||||||||||||

|

Capital expenditures

|

6,567,296

|

1,281,991

|

-

|

7,849,287

|

-

|

7,849,287

|

||||||||||||||||||

|

Write-off / Impairment

|

763,043

|

148,952

|

-

|

911,995

|

-

|

911,995

|

||||||||||||||||||

* Certain common production overheads, operating and administrative expenses and asset items (mainly cash and certain office equipment) of bromine and crude salt segments in SCHC were split by reference to the average selling price and production volume of respective segment.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2013

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 14 – BUSINESS SEGMENTS – Continued

|

Three-Month Period Ended June 30,

|

Six-Month Period Ended June 30,

|

|||||||||||||||

|

Reconciliations

|

2013

|

2012

|

2013

|

2012

|

||||||||||||

|

Total segment operating income

|

$

|

8,183,286

|

$

|

7,829,497

|

$

|

11,145,998

|

$

|

13,089,146

|

||||||||

|

Corporate costs

|

(804,511

|

)

|

(196,294

|

)

|

(1,161,775

|

)

|

(878,844

|

)

|

||||||||

|

Income from operations

|

7,378,775

|

7,633,203

|

9,984,223

|

12,210,302

|

||||||||||||

|

Other income (expense)

|

25,846

|

30,660

|

45,683

|

75,138

|

||||||||||||

|

Income before taxes

|

$

|

7,404,621

|

$

|

7,663,863

|

$

|

10,029,906

|

$

|

12,285,440

|

||||||||

The following table shows the major customer(s) (10% or more) for the three-month period ended June 30, 2013.

|

Number

|

Customer

|

Bromine

(000’s)

|

Crude Salt

(000’s)

|

Chemical Products

(000’s)

|

Total

Revenue

(000’s)

|

Percentage of

Total

Revenue (%)

|

|||||||||||||||||

| 1 |

Shandong Morui Chemical Company Limited

|

$ | 2,166 | $ | 751 | $ | 1,125 | $ | 4,042 | 12.3 | % | ||||||||||||

|

TOTAL

|

$ | 2,166 | $ | 751 | $ | 1,125 | $ | 4,042 | 12.3 | % | |||||||||||||

The following table shows the major customer(s) (10% or more) for the six-month period ended June 30, 2013.

|

Number

|

Customer

|

Bromine

(000’s)

|

Crude Salt

(000’s)

|

Chemical Products

(000’s)

|

Total

Revenue

(000’s)

|

Percentage of

Total

Revenue (%)

|

|||||||||||||||||

| 1 |

Shandong Morui Chemical Company Limited

|

$ | 3,347 | $ | 1,494 | $ | 2,055 | $ | 6,896 | 12.5 | % | ||||||||||||

|

TOTAL

|

$ | 3,347 | $ | 1,494 | $ | 2,055 | $ | 6,896 | 12.5 | % | |||||||||||||

The following table shows the major customer(s) (10% or more) for the three-month period ended June 30, 2012.

|

Number

|

Customer

|

Bromine

(000’s)

|

Crude Salt

(000’s)

|

Chemical Products

(000’s)

|

Total

Revenue

(000’s)

|

Percentage of

Total Revenue (%)

|

|||||||||||||||||

| 1 |

Shandong Morui Chemical Company Limited

|

$

|

1,904

|

$

|

727

|

$

|

1,109

|

$

|

3,740

|

11.9%

|

|||||||||||||

| 2 |

Shouguang City Rongyuan Chemical Company Limited

|

$

|

2,257

|

$

|

898

|

$

|

-

|

$

|

3,155

|

10.1%

|

|||||||||||||

|

TOTAL

|

$

|

4,161

|

$

|

1,625

|

$

|

1,109

|

$

|

6,895

|

22.0%

|

||||||||||||||

The following table shows the major customer(s) (10% or more) for the six-month period ended June 30, 2012.

|

Number

|

Customer

|

Bromine

(000’s)

|

Crude Salt

(000’s)

|

Chemical Products

(000’s)

|

Total

Revenue

(000’s)

|

Percentage of

Total Revenue (%)

|

|||||||||||||||||

| 1 |

Shandong Morui Chemical Company Limited

|

$

|

3,634

|

$

|

1,113

|

$

|

2,107

|

$

|

6,854

|

12.4%

|

|||||||||||||

| 2 |

Shouguang City Rongyuan Chemical Company Limited

|

$

|

4,278

|

$

|

1,346

|

$

|

-

|

$

|

5,624

|

10.2%

|

|||||||||||||

|

TOTAL

|

$

|

7,912

|

$

|

2,459

|

$

|

2,107

|

$

|

12,478

|

22.6%

|

||||||||||||||

NOTE 15 – MAJOR SUPPLIERS

During the three-month and six-month periods ended June 30, 2013, the Company purchased 83.4% and 82.6% of its raw materials from its top five suppliers, respectively. As of June 30, 2013, amounts due to those suppliers included in accounts payable were $4,289,947. During the three-month and six-month periods ended June 30, 2012, the Company purchased 85.7% and 83.5% of its raw materials from its top five suppliers, respectively. As of June 30, 2012, amounts due to those suppliers included in accounts payable were $3,305,237. This concentration makes the Company vulnerable to a near-term severe impact, should the relationships be terminated.

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2012

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 16 – CUSTOMER CONCENTRATION

The Company sells a substantial portion of its products to a limited number of customers. During the three-month and six-month periods ended June 30, 2013, the Company sold 40.0% and 40.3% of its products to its top five customers, respectively. As of June 30, 2013, amounts due from these customers were $16,955,022. During the three-month and six-month periods ended June 30, 2012, the Company sold 42.8% and 43.4% of its products to its top five customers, respectively. As of June 30, 2012, amounts due from these customers were $19,888,840. This concentration makes the Company vulnerable to a near-term severe impact, should the relationships be terminated.

NOTE 17 – FAIR VALUE OF FINANCIAL INSTRUMENTS

The carrying values of financial instruments, which consist of cash, accounts receivable and accounts payable and other payables, approximate their fair values due to the short-term nature of these instruments. There were no material unrecognized financial assets and liabilities as of June 30, 2013 and December 31, 2012.

NOTE 18 – RESEARCH AND DEVELOPMENT EXPENSES