UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

For the Fiscal Year Ended January 28 , 2023

For the Transition Period from ____________ to ____________

Commission File Number: 001-12951

THE BUCKLE, INC .

(Exact name of Registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: (308 ) 236-8491

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for a shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

þ Large accelerated filer ; o Accelerated filer; o Non-accelerated filer; o Smaller Reporting Company; o Emerging Growth Company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. þ

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

The aggregate market value (based on the closing price of the New York Stock Exchange) of the common stock of the registrant held by non-affiliates of the registrant was $896,564,521 on July 30, 2022. For purposes of this response, executive officers and directors are deemed to be the affiliates of the Registrant and the holdings by non-affiliates was computed as 29,687,567 shares.

The number of shares outstanding of the Registrant's Common Stock, as of March 28, 2023, was 50,456,196 .

DOCUMENTS INCORPORATED BY REFERENCE

THE BUCKLE, INC.

FORM 10-K

January 28, 2023

Table of Contents

| Pages | ||||||||

| Part I | ||||||||

| Part II | ||||||||

| Part III | ||||||||

| Part IV | ||||||||

3

PART I

ITEM 1 - BUSINESS

The Buckle, Inc. (the "Company") is a retailer of medium to better-priced casual apparel, footwear, and accessories for fashion-conscious young men and women. As of January 28, 2023, the Company operated 441 retail stores in 42 states throughout the United States under the names "Buckle" and "Buckle Youth." The Company markets a wide selection of mostly brand name casual apparel including denims, other casual bottoms, tops, sportswear, outerwear, accessories, and footwear. The Company emphasizes personalized attention to its customers and provides customer services such as free hemming, free gift-packaging, easy layaways, the Buckle private label credit card, and a guest loyalty program. Most stores are located in regional shopping malls and lifestyle centers. In recent years, however, the Company has successfully relocated several of its stores in smaller and middle markets from enclosed malls into power center locations, with continued plans for pursuing more such relocation opportunities in the future. The majority of the Company's central office functions, including purchasing, pricing, accounting, advertising, and distribution, are controlled from its corporate offices and distribution center in Kearney, Nebraska. The Company’s men’s buying team is located in Overland Park, Kansas.

Incorporated in Nebraska in 1948, the Company commenced business under the name Mills Clothing, Inc., a conventional men's clothing store with only one location. In 1967, a second store, under the trade name Brass Buckle, was purchased. In the early 1970s, the store image changed to that of a jeans store with a wide selection of denims and shirts. The first branch store was opened in Columbus, Nebraska, in 1976. In 1977, the Company began selling young women's apparel and opened its first mall store. The Company changed its corporate name to The Buckle, Inc. on April 23, 1991 and has experienced significant growth since that time, operating 441 stores in 42 states at the end of fiscal 2022. All references herein to fiscal 2022 refer to the 52-week period ended January 28, 2023. Fiscal 2021 refers to the 52-week period ended January 29, 2022 and fiscal 2020 refers to the 52-week period ended January 30, 2021. All references herein to the “Company”, “Buckle”, “we”, “us”, or similar terms refer to The Buckle, Inc. and its subsidiary.

The Company's principal executive offices are located at 2407 West 24th Street, Kearney, Nebraska 68845. The Company's telephone number is (308) 236-8491. The Company publishes its corporate web site at www.buckle.com.

Available Information

The Company’s annual reports on Form 10-K, along with all other reports and amendments filed with or furnished to the Securities and Exchange Commission, are publicly available free of charge on the Investor Information section of the Company’s website at www.buckle.com as soon as reasonably practicable after the Company files such materials with, or furnishes them to, the Securities and Exchange Commission. The Company’s corporate governance policies, ethics code, and Board of Directors’ committee charters are also posted within this section of the website. The information on the Company’s website is not part of this or any other report The Buckle, Inc. files with, or furnishes to, the Securities and Exchange Commission.

Special Note Regarding Forward-Looking Statements

Certain statements herein, including anticipated store openings, trends in or expectations regarding the Company’s revenue and net earnings growth, comparable store sales growth, cash flow requirements, and capital expenditures, all constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are based on currently available operating, financial, and competitive information and are subject to various risks and uncertainties. Actual future results and trends may differ materially depending on a variety of factors, including, but not limited to, changes in product mix, changes in fashion trends and/or pricing, competitive factors, general economic conditions, economic conditions in the retail apparel industry, successful execution of internal performance and expansion plans, and other risks detailed herein and in the Company’s other filings with the Securities and Exchange Commission.

A forward-looking statement is neither a prediction nor a guarantee of future events or circumstances, and those future events or circumstances may not occur. Users should not place undue reliance on the forward-looking statements, which are accurate only as of the date of this report. The Company is under no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

4

Merchandising

The Company's merchandising strategy is designed to create loyalty by offering a wide selection of key brand name and private label merchandise and providing a broad range of value-added services. The Company believes it provides a unique specialty apparel store experience with merchandise designed to appeal to the fashion-conscious 15 to 30-year old. The merchandise mix includes denims, casual bottoms, tops, sportswear, outerwear, accessories, and footwear. Denim is a significant contributor to total sales (39.3% of fiscal 2022 net sales) and is a key to the Company's merchandising strategy. The Company believes it attracts guests with its wide selection of branded and private label denim and a wide variety of fits, finishes, and styles. Tops are also significant contributors to total sales (29.7% of fiscal 2022 net sales). The Company strives to provide a continually changing selection of the latest casual fashions.

The percentage of net sales over the past three fiscal years of the Company's major product lines are set forth in the following table:

| Fiscal Years Ended | |||||||||||||||||

| Merchandise Group | January 28, 2023 | January 29, 2022 | January 30, 2021 | ||||||||||||||

| Denims | 39.3 | % | 39.6 | % | 40.1 | % | |||||||||||

| Tops (including sweaters) | 29.7 | 30.2 | 30.1 | ||||||||||||||

| Accessories | 10.0 | 9.3 | 9.0 | ||||||||||||||

| Footwear | 9.2 | 9.7 | 10.2 | ||||||||||||||

| Sportswear/fashions | 5.5 | 5.9 | 5.8 | ||||||||||||||

| Outerwear | 2.1 | 1.9 | 1.9 | ||||||||||||||

| Casual bottoms | 1.1 | 0.9 | 0.9 | ||||||||||||||

| Youth | 3.1 | 2.5 | 2.0 | ||||||||||||||

| Total | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||

Brand name merchandise accounted for approximately 56% of the Company's net sales during fiscal 2022. The remaining balance is comprised of private label merchandise from exclusive brands including BKE, Buckle Black, Salvage, Red by BKE, Daytrip, Gimmicks, Gilded Intent, FITZ + EDDI, Willow & Root, Outpost Makers, Departwest, Sterling & Stitch, Reclaim, BKE Vintage, Nova Industries, J.B. Holt, Modish Rebel, and Veece. The Company's merchandisers continually work with manufacturers and vendors to produce brand name merchandise, the majority of which they believe is exclusive in terms of color, style, and fit. While the brands offered by the Company change to meet current customer preferences, the Company currently offers denims from brands such as Miss Me, Rock Revival, KanCan, Hidden, Flying Monkey, Levi's, Preme, Smoke Rise, Ariat, Good American, and Wrangler. Other key brands include Hurley, Billabong, Affliction, American Fighter, Sullen, Howitzer, Oakley, Fox, RVCA, 7 Diamonds, Nixon, Free People, Z Supply, Salt Life, White Crow, Brew City, Reef, Stance, Versace Cologne, American Highway, Eight X, Pendelton, Hooey, Goorin Bros., Old Row, Timberland, Teva, Kimes Ranch, SOREL, Hey Dude, Steve Madden, Dolce Vita, SAXX, Ray-Ban, Wanakome, Guess, Fossil, Brixton, Dr. Martens, Very G, Birkenstock, Bed Stu, Palladium, Mia, K-Swiss, Myra, STS, and G-Shock. The Company expects that brand name merchandise will continue to constitute the majority of sales.

Management believes the Company provides a unique store environment by maintaining a high level of personalized service and by offering a wide selection of fashionable, quality merchandise. The Company believes it is essential to create an enjoyable shopping environment and, in order to fulfill this mission, it employs highly motivated employees who provide personal attention to customers. Each salesperson is educated to help create a complete look for the customer by helping them find the best fits and showing merchandise as coordinating outfits. The Company also incorporates specialized services such as free hemming, free gift-packaging, layaways, a guest loyalty program, the Buckle private label credit card, personalized stylist services, and a special order system that allows stores to obtain specifically requested merchandise from other Company stores or from the Company's online order fulfillment center.

5

Merchandising and pricing decisions are made centrally; however, the Company's distribution system allows for variation in the mix of merchandise distributed to each store. This allows individual store inventories to be tailored to reflect differences in customer buying patterns at various locations. In addition, to ensure a continually fresh look in its stores, the Company ships new merchandise daily to most stores. The Company also has a transfer program that shifts certain merchandise to locations where it is selling best. This distribution and transfer system helps to maintain customer satisfaction by providing in-stock popular items and reducing the need to markdown slow-moving merchandise at a particular location. The Company believes the reduced markdowns justify the incremental distribution costs associated with the transfer system. The Company does not hold store-wide off-price sales at any time.

The Company continually evaluates its store design as part of the overall shopping experience and feels its current design continues to be well received by both guests and developers. This store design contains warm wood fixtures and floors, real brick finishes, and an appealing ceiling and lighting layout that creates a comfortable environment for the guest to shop. The signature Buckle-B icon is used throughout the store on fixtures, graphic images, and print materials to reinforce the brand identity. To enhance selling and product presentation, the Company continually updates the fixtures in its stores. The Company has been able to modify the store design for specialized venues including lifestyle centers and larger mall fronts. Over the past several fiscal years, the Company has also developed updated storefront designs that enhance the exterior visibility for stores relocating from enclosed mall locations to outdoor power centers and lifestyle centers.

Marketing and Advertising

In fiscal 2022, the Company spent $19.2 million, or 1.4% of net sales, on targeted seasonal marketing campaigns, digital marketing efforts, and in-store point-of-sale materials. A coordinated effort to amplify value and relevance through brand image, voice, and experience is presented through store window displays, seasonal and product-level signage throughout the store, and on digital commerce and experience platforms. Promotions such as special, seasonal events combined with gift-with-purchase offers are offered to enhance the guest’s shopping experience. Seasonal guides, featuring current fashion trends and product selection, are distributed in the stores, at special events, and in new markets. Additionally, Buckle partners with key merchandise vendors on joint advertising and promotional opportunities that expand the marketing reach and position Buckle as the first-choice for these specialty branded fashions.

The Company also offers programs to build and strengthen its relationship with loyal guests. In October 2020, the Company combined its multi-tender loyalty program (Buckle Guest Loyalty) and private label credit card rewards program (B-Rewards) into one, all-inclusive program (Buckle Rewards). The Buckle Rewards incentive program rewards loyal guests and cardholders with real-time rewards after 300 points have been earned. There are three tiers in the program, providing guests with opportunities to earn additional points and exclusive benefits. The base tier is available for all guests who enroll, while the top two tiers are exclusive to holders of a Buckle private label credit card. In addition to the stated benefits, the Company also extends other exclusive offers to Buckle Rewards members such as special bonus points opportunities, targeted mailings, and other exclusive offers. The Company provides a special Buckle Premier+ tier for its most loyal cardholders. Buckle Premier+ cardholders must purchase at least $1,000 annually using their Buckle credit card to qualify, and these guests enjoy additional benefits including free ground shipping on online purchases and special orders. The Buckle credit card marketing program is partially funded by Comenity Bank, a third-party bank that owns the credit card accounts.

The Company supports a corporate web site at www.buckle.com. The Company’s web site serves as a portal to enhance, influence, and help its valued guests through their decision journey, reaching a growing online audience. Buckle.com provides an interactive, informative, and brand building environment where guests can shop, discover, learn, engage, and seek information, as well as search for career opportunities and read the Company’s latest financial news. The Company also maintains an opt-in email database. Targeted email campaigns are deployed informing guests of the latest styles and promotions. Paid-search, organic-search, and affiliate marketing programs are individually managed to increase online and in-store traffic. The Company continually invests in enhancements to the site's features and functionality, helping improve the overall digital guest experience and facilitate the growth in online traffic.

Store Operations

The Company has an Executive Vice President of Stores, a Senior Vice President of Sales, 3 Vice Presidents of Sales, 4 Regional Managers, 32 District Managers, and 68 Area Managers. Certain district managers and all area managers also serve as manager of their home base store. In general, each store has 1 manager, 1 or 2 assistant managers, 1 to 3 additional full-time salespeople, and up to 20 part-time salespeople. Most stores have peak levels of staff during the back-to-school and holiday seasons. Almost every location also employs an alterations person.

6

The Company has established a comprehensive program stressing the prevention and control of shrinkage losses. Steps taken to reduce shrinkage include monitoring returns, cash refunds, voids, inappropriate discounts, and employee sales. The Company also has electronic article surveillance systems in all of the Company’s stores as well as surveillance camera systems in approximately 99% of the stores. As a result, the Company achieved a merchandise shrinkage rate of 0.4% of net sales in fiscal 2022, 0.3% of net sales in fiscal 2021, and 0.4% of net sales in fiscal 2020.

The average store is approximately 5,300 square feet (of which the Company estimates an average of approximately 80% is selling space), and stores range in size from 1,937 square feet to 9,935 square feet.

Purchasing and Distribution

The Company has an experienced buying team. The experience and leadership within the buying team contributes significantly to the Company’s success by enabling the buying team to react quickly to changes in fashion and by providing extensive knowledge of sources for both branded and private label goods.

The Company purchases products from manufacturers within the United States as well as from agents who source goods from foreign manufacturers. The Company's merchandising team shops and monitors fashion to stay abreast of the latest trends. The Company continually monitors styles, quality, and delivery schedules. The Company has not experienced any material difficulties with merchandise manufactured in foreign countries. The Company does not have long-term or exclusive contracts with any brand name manufacturer, private label manufacturer, or supplier. The Company plans its private label production with private label vendors three to six months in advance of product delivery. The Company requires its vendors to sign and adhere to its Buckle Responsible Sourcing Standards & Code of Conduct, which addresses adherence to legal requirements regarding employment practices and health, safety, and environmental regulations.

In fiscal 2022, Axis Denim (which produces private label denim for the Company) accounted for 15.2% of net sales and Rock Revival/Miss Me accounted for 10.7% of the Company’s net sales. No other vendor accounted for more than 10% of the Company’s net sales.

Buckle stores generally carry the same merchandise, with quantity and seasonal variations based upon historical sales data, climate, and perceived local customer demand. The Company uses a centralized receiving and distribution center located in Kearney, Nebraska. Merchandise is received daily in Kearney where it is sorted, tagged with bar-coded tickets (unless the vendor UPC code is used or the merchandise is pre-ticketed), and packaged for distribution to individual stores primarily via FedEx. The Company's goal is to ship the majority of its merchandise out to the stores within one to two business days of receipt. This system allows stores to receive new merchandise almost daily, creating excitement within the store and providing customers with a reason to shop often.

The Company has developed an effective system for tracking merchandise from the time it is checked in at the Company's distribution center until it arrives at the stores and is sold to a customer. The system's function is to ensure that store shipments are delivered accurately and promptly, to account for inventory, and to assist in allocating merchandise among stores. Management can track, on a daily basis, which merchandise is selling at specific locations and direct transfers of merchandise from one store to another as necessary. This allows stores to carry a reduced inventory while at the same time satisfying customer demand.

To reduce inter-store shipping costs and provide timely restocking of in-season merchandise, the Company warehouses a portion of initial shipments for later distribution. Sales data is then analyzed to replenish, on a basis of one to three times each week, those stores that are experiencing the greatest success selling specific styles, colors, and sizes of merchandise. This system is also designed to prevent an over-crowded look in the stores at the beginning of a season.

During fiscal 2010, the Company completed construction of a 240,000 square foot distribution center in Kearney, Nebraska, which currently serves as the Company’s only store distribution center. The Company also owns two additional facilities as part of its home office campus in Kearney, Nebraska (one of which was completed during the first quarter of fiscal 2015). These facilities serve as the Company's corporate headquarters and house its online fulfillment and customer service center.

7

Store Locations and Expansion Strategies

As of January 28, 2023, the Company operated 441 stores in 42 states. The existing stores are in 3 downtown locations, 50 strip centers, 54 lifestyle centers, and 334 shopping malls. The Company anticipates opening 6 new stores in fiscal 2023. The following table lists the location of existing stores as of January 28, 2023:

| Location of Stores | ||||||||||||||||||||||||||||||||

| State | Number of Stores | State | Number of Stores | State | Number of Stores | |||||||||||||||||||||||||||

| Alabama | 8 | Maryland | 1 | Oregon | 6 | |||||||||||||||||||||||||||

| Alaska | 1 | Michigan | 17 | Pennsylvania | 9 | |||||||||||||||||||||||||||

| Arizona | 12 | Minnesota | 11 | South Carolina | 4 | |||||||||||||||||||||||||||

| Arkansas | 7 | Mississippi | 6 | South Dakota | 3 | |||||||||||||||||||||||||||

| California | 13 | Missouri | 14 | Tennessee | 11 | |||||||||||||||||||||||||||

| Colorado | 15 | Montana | 5 | Texas | 54 | |||||||||||||||||||||||||||

| Florida | 20 | Nebraska | 13 | Utah | 12 | |||||||||||||||||||||||||||

| Georgia | 10 | Nevada | 5 | Virginia | 4 | |||||||||||||||||||||||||||

| Idaho | 9 | New Jersey | 1 | Washington | 14 | |||||||||||||||||||||||||||

| Illinois | 15 | New Mexico | 5 | West Virginia | 6 | |||||||||||||||||||||||||||

| Indiana | 15 | New York | 4 | Wisconsin | 11 | |||||||||||||||||||||||||||

| Iowa | 16 | North Carolina | 12 | Wyoming | 2 | |||||||||||||||||||||||||||

| Kansas | 16 | North Dakota | 4 | Total | 441 | |||||||||||||||||||||||||||

| Kentucky | 6 | Ohio | 22 | |||||||||||||||||||||||||||||

| Louisiana | 11 | Oklahoma | 11 | |||||||||||||||||||||||||||||

Over the past ten years, Buckle has opened a total of 55 new stores and closed 54, with the number of openings and closings in a given year being based on local economic conditions and available opportunities. The Company intends to open new stores only when management believes there is a reasonable expectation of satisfactory results.

The following table sets forth information regarding store openings and closings from the beginning of fiscal 2013 through the end of fiscal 2022:

| Total Number of Stores Per Year | ||||||||||||||||||||||||||

| Fiscal Year | Open at start of year | Opened in Current Year | Closed in Current Year | Open at end of year | ||||||||||||||||||||||

| 2013 | 440 | 13 | 3 | 450 | ||||||||||||||||||||||

| 2014 | 450 | 16 | 6 | 460 | ||||||||||||||||||||||

| 2015 | 460 | 9 | 1 | 468 | ||||||||||||||||||||||

| 2016 | 468 | 5 | 6 | 467 | ||||||||||||||||||||||

| 2017 | 467 | 2 | 12 | 457 | ||||||||||||||||||||||

| 2018 | 457 | — | 7 | 450 | ||||||||||||||||||||||

| 2019 | 450 | 2 | 4 | 448 | ||||||||||||||||||||||

| 2020 | 448 | 3 | 8 | 443 | ||||||||||||||||||||||

| 2021 | 443 | 1 | 4 | 440 | ||||||||||||||||||||||

| 2022 | 440 | 4 | 3 | 441 | ||||||||||||||||||||||

8

The Company's criteria used when considering a particular location for expansion include:

•Market area, including proximity to existing markets to capitalize on name recognition;

•Trade area population (number, average age, and college population);

•Economic vitality of market area;

•Location, anchor tenants, tenant mix, and average sales per square foot;

•Available location, square footage, storefront width, and facility of using the current store design;

•Availability of experienced management personnel for the market;

•Cost of rent, including minimum rent, common area, and extra charges; and

•Estimated construction costs, including landlord charge backs and tenant allowances.

The Company generally seeks sites of 4,250 to 5,000 square feet for its stores. The projected cost of opening a store is approximately $1.2 million, including construction costs of approximately $1.0 million (prior to any construction allowance received) and inventory costs of approximately $0.2 million, net of accounts payable.

The Company anticipates opening 6 new stores during fiscal 2023 and expects to complete approximately 12-17 full remodels. Year-to-date through March 28, 2023, the Company has closed 3 stores in fiscal 2023, with no other specific store closings currently planned for the remainder of the year. The construction costs for a full remodel are comparable to those of a new store. The Company also plans to complete several smaller store remodeling projects during fiscal 2023. The Company anticipates capital spending of approximately $24.0 to $30.0 million during fiscal 2023, which includes primarily planned store projects and technology investments.

The Company's ability to expand in the future will depend, in part, on general business conditions, the ability to find suitable locations with acceptable sites on satisfactory terms, and the readiness of trained store managers. There can be no assurance that the Company's future expansion plans will be fulfilled in whole or in part, or that leases for potential new sites will be obtained on terms favorable to the Company.

Information Technology

The Company's information technology systems consist of a full range of retail, financial, and merchandising platforms, including purchasing, inventory distribution and control, financial reporting, accounts payable, and merchandise management.

The system includes PC based point-of-sale ("POS") registers in each store. The registers trickle transactions to a central server using a virtual private network ("VPN") for collection of comprehensive data, including complete item-level sales information. The transactions are then swept into the central database (IBM iSeries). Price updates are sent daily for the price lookup (“PLU”) file maintained within the POS registers.

Twice a week, the Company initiates an electronic "sweep" of the individual store bank accounts to the Company's primary concentration account. This allows the Company to meet its obligations and invest cash on a timely basis.

Management monitors the performance of each of its stores on a continual basis. Daily information is used to evaluate inventory, determine markdowns, analyze profitability, and assist management in the scheduling and compensation of employees.

The PLU system allows management to control merchandise pricing centrally, permitting faster and more accurate processing of sales at the store and the monitoring of specific inventory items to confirm that centralized pricing decisions are carried out in each of the stores. Management is able to direct all price changes, including promotional, clearance, and markdowns on a central basis and estimate the financial impact of such changes.

The VPN for communication with the stores also supports the Company’s intranet site. The intranet allows stores to view various types of information from the corporate office. Stores also have access to a variety of tools such as a product search with pictures, product availability, special order functions, inventory management, scheduling, performance tracking, printable forms, links to transmit various requests and information to the corporate office, training videos, email, and information/guidelines from each of the departments at the corporate office. The Company’s network is also structured so that it can support additional functionality such as digital video monitoring and digital music content programming at each store location.

9

The Company is committed to the ongoing review of its technology systems to maintain productive, timely information and effective controls. This review includes testing of new products and systems to ensure that the Company is aware of technological developments. Most important, continual feedback is sought from every level of the Company to ensure that information provided is pertinent to all aspects of the Company's operations.

Employees and Human Capital

The Company’s employees, which we refer to as our “teammates,” are critical to carrying out Buckle’s mission statement, “to create the most enjoyable shopping experience possible for our guests.” The Company’s success is highly dependent on the continued contributions of all teammates, including those in the Company’s stores, distribution center, and corporate offices. As a result, the Company seeks to recruit and retain talented teammates through competitive pay and benefits offerings, along with an entrepreneurial culture that emphasizes education, training, and advancement.

Teammate Demographics. As of January 28, 2023, the Company had approximately 9,100 teammates, of which approximately 3,100 were full-time. Of the total number of teammates, approximately 830 were employed at the corporate offices and in the distribution center. The Company has an experienced management team and most of the management team, from store managers through senior management, began work for the Company on the sales floor. The Company experiences high turnover of store and distribution center teammates, primarily due to the number of part-time teammates. However, the Company has not experienced significant difficulty in hiring qualified personnel.

Teammate Compensation. Buckle's entrepreneurial culture is vital to our continued success. As such, we seek to offer competitive base pay and benefits to our teammates, as well as incentive compensation tied to both individual and overall Company performance. As teammates advance, a larger share of their compensation generally becomes performance-based. For example, the majority of store teammates are compensated with a base plus commission structure. Store managers receive compensation in the form of a base salary and incentive bonuses based on the individual performance of their store. District and area managers receive incentives based upon the performance of the stores in their district/area. We believe our incentive-based compensation structure creates a sense of ownership amongst our teammates. This aligns with our entrepreneurial culture, motivating our teammates to constantly seek improvements in the service we provide to our guests.

Training and Advancement. The Company invests heavily in the education, training, and leadership development of its teammates. Store managers perform sales training for new teammates at the store level, utilizing training videos and educational programs developed by sales leadership. As teammates progress, leadership development opportunities are provided through the Company's Leadership Academy, which is designed to prepare potential future leaders for store management opportunities. Additionally, the Company hosts manager meetings three times per year to provide continuing education and leadership development opportunities for our store managers. At the corporate offices, teammates are afforded professional growth opportunities aligned with their area of responsibility, including internal trainings, industry seminars and conferences, and experiential opportunities. Mentoring is also an important training and development tool utilized at all levels of the Company.

Competition

The men's and women's apparel industries are highly competitive with fashion, selection, quality, price, location, store environment, and service being the principal competitive factors. While the Company believes it is able to compete favorably with other merchandisers, including department stores and specialty retailers, with respect to each of these factors, the Company believes it competes mainly on the basis of customer service and merchandise selection.

In the men's merchandise area, the Company competes primarily with specialty retailers such as Abercrombie & Fitch, American Eagle Outfitters, Boot Barn, Express, Gap, Hollister, PacSun, Scheels, and Tilly’s. The men's market also competes with certain department stores, such as Dillards, Macy’s, Nordstrom, and certain local or regional department stores and small specialty stores, as well as with direct-to-consumer brands and online retailers.

In the women's merchandise area, the Company competes primarily with specialty retailers such as Abercrombie & Fitch, Altar'd State, American Eagle Outfitters, Anthropologie, Boot Barn, Express, Forever 21, Francesca's, Free People, H&M, Hollister, Journey's, Lulus, Madewell, Maurices, PacSun, Revolve, Scheels, Tilly's, Urban Outfitters, Zara, and Zumiez. The women's market also competes with department stores, such as Dillards, Macy’s, Nordstrom, and certain local or regional department stores, and small specialty boutiques, as well as with direct-to-consumer brands and online retailers.

Many of the Company's competitors are considerably larger and have substantially greater financial, marketing, and other resources than the Company, and there is no assurance that the Company will be able to compete successfully with them in the future. Furthermore, while the Company believes it competes effectively for favorable site locations and lease terms, competition for prime locations is intense.

10

Seasonality

The Company's business is seasonal, with the holiday season (from approximately November 15 to December 30) and the back-to-school season (from approximately July 15 to September 1) historically contributing the greatest volume of net sales. For fiscal years 2022, 2021, and 2020, the holiday and back-to-school seasons accounted for approximately 35% of the Company's fiscal year net sales.

Trademarks

“BUCKLE”, “THE BUCKLE”, “BUCKLE BLACK”, “BKE”, “BKE BOUTIQUE”, “BKE SOLE”, “DAYTRIP”, “RECLAIM”, “B BELIEVES”, “GIMMICKS”, "BKE RED", "BEST BRANDS. FAVORITE JEANS.", "BKE SPORT", "BKE RESERVE", "BUCKLE BELIEVES", "FADE BY BKE", "SOLELY BLACK BY BKE", "FITZ + EDDI", "BUCKLE SELECT", "IN THESE BLUES", "POETIC REBEL", "UNTAMED SOUL", "WILLOW & ROOT", "TWINE & STARK", "INDIE SPIRIT DESIGNS", "BKE CORE", "GILDED INTENT", "#BUCKLEDOUT", "QUINN & COPPER", "LEGACY COLLECTION BY BKE", "SWEET HARMONY BY BUCKLE", "DAYTRIP REFINED", "WHEREVER YOU WANDER BY BUCKLE", "RED BY BKE", "#INTHESEBLUES", "J.B. HOLT", "OUTPOST MAKERS", "DEPARTWEST", "STONE REFINERY", "stylized G", "DEPARTWEST logo", "GREHY", "NOVA INDUSTRIES", "SAY YOU WILL", "BRILL BOUTIQUE", "BUCKLE B", "BUCKLE REWARDS", "BKE ESSENTIALS" and “B” icon are federally registered trademarks of the Company. The Company also owns trademarks for certain product designs. The Company believes the strength of its trademarks is of considerable value to its business, and its trademarks are important to its marketing efforts. The Company intends to protect and promote its trademarks as management deems appropriate.

Regulation

The Company and the merchandise it sells are subject to regulation by various federal, state, local, and foreign regulatory authorities. In addition, because some of the merchandise the Company sells is manufactured by foreign suppliers and imported by the Company, the Company’s operations are subject to a variety of trade laws, customs regulations, and international trade agreements. Compliance with these laws, rules, and regulations has not had, and at the present time is not expected to have, a material effect on the Company’s capital expenditures, results of operations, or competitive position. See “ITEM 1A – Risk Factors – Reliance on Foreign Sources of Production” for additional information.

Executive Officers of the Company

The Executive Officers of the Company are listed below, together with brief accounts of their experience and certain other information.

Daniel J. Hirschfeld, age 81. Mr. Hirschfeld is Chairman of the Board of the Company. He has served as Chairman of the Board since April 19, 1991. Prior to that time, Mr. Hirschfeld served as President and Chief Executive Officer. Mr. Hirschfeld has been involved in all aspects of the Company's business, including the development of the Company's management information systems.

Dennis H. Nelson, age 73. Mr. Nelson is President and Chief Executive Officer and a Director of the Company. He has held the titles of President and Director since April 19, 1991. Mr. Nelson was elected Chief Executive Officer on March 17, 1997. Mr. Nelson began his career with the Company in 1970 as a part-time salesperson while he was attending Kearney State College (now the University of Nebraska - Kearney). While attending college, he became involved in merchandising and sales supervision for the Company. Upon graduation from college in 1973, Mr. Nelson became a full-time employee of the Company and he has worked in all phases of the Company's operations since that date. Prior to his election as President and Chief Operating Officer on April 19, 1991, Mr. Nelson performed all of the functions normally associated with those positions.

Thomas B. Heacock, age 45. Mr. Heacock is Senior Vice President of Finance, Treasurer, Chief Financial Officer, and a Director of the Company. He was elected a Director on December 4, 2017. Mr. Heacock was appointed Senior Vice President of Finance, Treasurer, and Chief Financial Officer effective February 4, 2018, after having served as Vice President of Finance, Treasurer, and Chief Financial Officer upon his appointment as Chief Financial Officer on July 20, 2017. He has been employed by the Company since October 2003 and served as Vice President of Finance, Treasurer, and Corporate Controller prior to his appointment as Chief Financial Officer. Prior to joining the Company, he was employed by Ernst & Young, LLP. Mr. Heacock is the son-in-law of Dennis H. Nelson, who serves as President and Chief Executive Officer and a Director of The Buckle, Inc.

11

Kari G. Smith, age 59. Ms. Smith is Executive Vice President of Stores and a Director of the Company. She was elected a Director effective February 4, 2018 and was appointed Executive Vice President of Stores on February 13, 2014, after having served as Vice President of Sales since May 2001. Ms. Smith joined the Company in May 1978 as a part-time salesperson. Later she became store manager in Great Bend, Kansas and then began working with other stores as an area manager. Ms. Smith has continued to develop her involvement with the sales management team, helping with manager meetings and the development of new store managers, as well as providing support for store managers, area managers, and district managers.

Brett P. Milkie, age 63. Mr. Milkie is Senior Vice President of Leasing. He was appointed to this position on March 6, 2014, after having served as Vice President of Leasing since May 1996. Mr. Milkie was a leasing agent for a national retail mall developer for 6 years prior to joining the Company in January 1992 as Director of Leasing.

Michelle M. Hoffman, age 61. Ms. Hoffman is Senior Vice President of Sales. She was appointed to this position on February 22, 2022, after having served as Vice President of Sales since March 2014. Ms. Hoffman has been employed by the Company since 1979 and has served in various roles of increasing responsibility on the sales team since that time; including salesperson, Store Manager, District Manager, and Regional Manager.

Kelli D. Molczyk, age 44. Ms. Molczyk is Senior Vice President of Women's Merchandising. She was appointed to this position on February 22, 2022, after having served as Vice President of Women's Merchandising since December 2014. Ms. Molczyk has been employed by the Company since 1999 and has served in various roles on the women's merchandising team since that time, including Divisional Merchandise Manager.

Brady M. Fritz, age 43. Ms. Fritz is Senior Vice President, General Counsel, and Corporate Secretary. She was appointed to this position on February 22, 2022, after having served as Vice President, General Counsel, and Corporate Secretary since March 2021. Ms. Fritz was hired by the Company on December 10, 2018 and has served as General Counsel and Corporate Secretary since that time. Prior to joining the Company, she served Cargill Incorporated for over 10 years in several roles of increasing responsibility, including most recently as Global Legal Operations Leader and Senior Attorney. Prior to joining Cargill Incorporated, Ms. Fritz began her career at Scudder Law Firm in Lincoln, Nebraska.

ITEM 1A - RISK FACTORS

In management’s judgment, the following are material risk factors that might make an investment in the Company speculative or risky:

Business and Industry Risks:

Dependence on Merchandising/Fashion Sensitivity. The Company’s success is largely dependent upon its ability to gauge the fashion tastes of its customers and to provide merchandise that satisfies customer demand in a timely manner. The Company’s failure to anticipate, identify, or react appropriately and timely to changes in fashion trends would reduce the Company’s net sales and profitability. Misjudgments or unanticipated fashion changes could have a negative impact on the Company’s image with its customers, which would also reduce the Company’s net sales and profitability.

Dependence on Private Label Merchandise. Sales from private label merchandise accounted for approximately 44% of net sales for fiscal 2022 and 43% for fiscal 2021. The Company may increase or decrease the percentage of net sales from private label merchandise in the future. The Company’s private label products generally earn a higher margin than branded products. Thus, reductions in the private label mix would decrease the Company’s merchandise margins and, as a result, reduce net earnings.

Fluctuations in Comparable Store Net Sales Results. The Company’s comparable store net sales results have fluctuated in the past and are expected to continue to fluctuate in the future. A variety of factors affect comparable store sales results, including changes in fashion trends, changes in the Company’s merchandise mix, calendar shifts of holiday periods, actions by competitors, weather conditions, and general economic conditions. As a result of these or other factors, the Company’s future comparable store sales could decrease, reducing overall net sales and profitability.

12

Ability to Continue Expansion and Management of Growth. The Company’s growth depends on its ability to open and operate stores on a profitable basis and management’s ability to manage planned expansion. During fiscal 2023, the Company plans to open 6 new stores. Potential future expansion is dependent upon factors such as the ability to locate and obtain favorable store sites, negotiate acceptable lease terms, obtain necessary merchandise, and hire and train qualified management and other employees. There may be factors outside of the Company’s control that affect the ability to expand, including general economic conditions. There is no assurance that the Company will be able to achieve its planned expansion or that future expansion will be profitable. If the Company fails to achieve store growth, there would be less growth in the Company’s net sales from new stores and less growth in profitability. If the Company opens unprofitable store locations, there could be a reduction in net earnings, even with the resulting growth in the Company’s net sales.

Ability to Adjust to Changes in Shopping Center Traffic and Consumer Trends Related to E-Commerce Shopping. Shopping patterns have been evolving rapidly, along with consumers’ ability to shop whenever and wherever they choose. These changing dynamics and increased competition from online retailers have adversely impacted shopping center traffic in many malls. The Company’s ability to compete effectively in the future is dependent on its ability to continue to profitably manage both its in-store and e-commerce businesses. The Company considers its unique merchandise selection and its outstanding customer service to be key differentiators. The Company continues to invest in its e-commerce website and other digital initiatives to drive traffic to both its stores and buckle.com. The Company also continues to expand its omni-channel capabilities to satisfy its guests however they choose to shop. There can, however, be no assurance that the Company will be able to successfully integrate both channels and compete successfully with other retailers. The Company’s inability to profitably adapt to changing consumer preferences would cause a decrease in the Company’s net sales and net earnings.

Reliance on Key Personnel. The continued success of the Company is dependent to a significant degree on the continued service of key personnel, including senior management. The loss of a member of senior management could create additional expense in covering their position as well as cause a reduction in net sales, thus reducing net earnings. The Company’s success in the future will also be dependent upon the Company’s ability to attract and retain qualified personnel. The Company’s failure to attract and retain qualified personnel could negatively impact net sales, could create additional operating expenses, and could reduce overall profitability for the Company.

Dependence on a Single Distribution Facility and Third-Party Carriers. The distribution function for all of the Company’s stores is handled from a single facility in Kearney, Nebraska. Any significant interruption in the operation of the distribution facility due to natural disasters, system failures, or other unforeseen causes would impede the distribution of merchandise to the stores, causing a decline in store inventory, a reduction in store sales, and a reduction in Company profitability. Interruptions in service by common carriers could also delay shipment of goods to Company store locations. Additionally, there can be no assurance that the current facilities will be adequate to support future growth.

Reliance on Foreign Sources of Production. The Company purchases a portion of its private label merchandise through sourcing agents in foreign markets. In addition, some of the Company’s domestic vendors manufacture goods overseas. The Company does not have any long-term merchandise supply contracts and its imports are subject to existing or potential duties, tariffs, and quotas. The Company faces a variety of risks associated with doing business overseas including competition for facilities and quotas, political instability, possible new legislation relating to imports that could limit the quantity of merchandise that may be imported, imposition of tariffs, duties, taxes, and other charges on imports, and local business practice and political issues which may result in adverse publicity. The Company’s inability to rely on foreign sources of production due to these or other causes could reduce the amount of inventory the Company is able to purchase, hold up the timing on the receipt of new merchandise, and reduce merchandise margins if comparable inventory is purchased from branded sources. Any or all of these changes would cause a decrease in the Company’s net sales and net earnings.

13

Dependence upon Maintaining Sales and Profit Growth in the Highly Competitive Retail Apparel Industry. The specialty retail industry is highly competitive. The Company competes primarily on the basis of fashion, selection, quality, price, location, service, and store environment. The Company faces a variety of competitive challenges, including:

•Anticipating and responding timely to changing customer demands and preferences;

•Effectively marketing both branded and private label merchandise to consumers in several diverse market segments and maintaining favorable brand recognition;

•Providing unique, high-quality merchandise in styles, colors, and sizes that appeal to consumers;

•Sourcing merchandise efficiently;

•Competitively pricing merchandise and creating customer perception of value; and

•Monitoring increased labor costs, including increases in health care benefits and worker’s compensation and unemployment insurance costs.

There is no assurance that the Company will be able to compete successfully in the future.

Reliance on Consumer Spending Trends. The continued success of the Company depends, in part, upon numerous factors that impact the levels of individual disposable income and thus, consumer spending. Factors include the political environment, the threat or outbreak of war (including, the ongoing conflict in Ukraine), terrorism, civil unrest, economic conditions, employment, consumer debt, interest rates, inflation, and consumer confidence. A decline in consumer spending, for any reason, could have an adverse effect on the Company’s net sales, gross profits, and results from operations.

Operational Risks:

Fluctuations in Tax Obligations and Effective Tax Rate. The Company records tax expense based on its estimates of future payments. At any one time, multiple tax years are subject to audit by various taxing authorities. There can be no assurance as to the outcome of any current or potential future audits and their impact on the tax owed by the Company. In addition, the Company's effective tax rate may be materially impacted by changes in tax laws and regulations in the jurisdictions where it operates. Future tax law changes could materially impact the Company's effective tax rate and, therefore, its net earnings.

Evolving Regulations and Expectations with Respect to Environmental, Social, and Governance Matters. There has been increasing stakeholder and regulatory focus on environmental, social, and governance ("ESG") initiatives and related disclosures affecting public companies. The Company anticipates that expectations and requirements in these areas will continue to evolve. To the extent the Company is unable to meet or is perceived to be unable to meet these expectations and requirements, the Company's reputation, business, and financial performance could be adversely affected.

Modifications and/or Upgrades to Information Technology Systems May Disrupt Operations. The Company relies upon its various information systems to manage its operations and regularly evaluates its information technology in order for management to identify investment opportunities for maintaining, modifying, upgrading, or replacing these systems. There are inherent risks associated with replacing or changing these systems. Any delays, errors in capturing data, or difficulties in transitioning to these or other new systems, or in integrating these systems with the Company’s current systems, or any other disruptions affecting the Company’s information systems, could have a material adverse impact on the Company’s business.

Reliance on Increasingly Complex Information Systems for Management of Distribution, Sales, and Other Functions. If the Company’s information systems fail to perform these functions adequately or if the Company experiences an interruption in their operation, including a breach in cyber-security, its business and results of operations could suffer. All of the Company’s major operations, including distribution, sales, and accounting, are dependent upon the Company’s complex information systems. The Company’s information systems are vulnerable to damage or interruption from:

•Earthquake, fire, flood, tornado, and other natural disasters;

•Power loss, computer systems failure, internet and telecommunications or data network failure;

•Hackers, computer viruses, software bugs, or glitches.

Any damage or significant disruption in the operation of such systems, or the failure of the Company’s information systems to perform as expected, could disrupt the Company’s business, result in decreased sales, increased overhead costs, excess inventory, or product shortages and otherwise adversely affect the Company’s operations, financial performance, and financial condition.

14

Unauthorized Access to, or Accidental Disclosure of, Consumer Personally-Identifiable Information that the Company Collects May Result in Significant Expenses and Negatively Impact the Company's Reputation and Business. As part of the Company's normal operations, it receives and maintains confidential information about customers, employees, and other third parties. The Company employs systems and websites that allow for the secure storage and transmission of proprietary or confidential information regarding customers, employees, job applicants, and others, including credit card information and personally-identifiable information. Despite safeguards and security processes and protections, the Company’s computer systems may be susceptible to electronic or physical computer break-ins, viruses, and other disruptions and security breaches. Additionally, the Company may not have the resources or technical sophistication to anticipate or prevent rapidly evolving types of cyber-attacks. Attacks may be targeted at the Company, its customers, or others who have entrusted the Company with information. Actual or anticipated attacks may cause the Company to incur increasing costs, including costs to deploy additional personnel and protection technologies, train employees, and engage third-party experts and consultants. Advances in computer capabilities, new technological discoveries, or other developments may result in the technology used to protect transaction or other data being breached or compromised. In addition, data and security breaches can also occur as a result of non-technical issues, including intentional or inadvertent breach by employees or by persons with whom the Company has commercial relationships that result in the unauthorized release of personal or confidential information. Any perceived or actual unauthorized disclosure of personally-identifiable information regarding visitors to the Company’s websites or otherwise, whether through a breach of the Company’s network by an unauthorized party, employee theft, misuse, or error, or otherwise, could harm the Company’s reputation, impair the Company’s ability to attract and retain customers, or subject the Company to claims or litigation arising from damages suffered by consumers, and adversely affect the Company’s operations, financial performance, and financial condition.

Interest Rate Risk. The Company is exposed to market risk related to interest rate risk on the cash and investments in interest-bearing securities. These investments have carrying values that are subject to interest rate changes that could impact earnings to the extent that the Company did not hold the investments to maturity. If there are changes in interest rates, those changes would also affect the investment income the Company earns on its cash and investments. For each one-quarter percent decline in the interest/dividend rate earned on cash and investments, the Company’s net income would decrease approximately $0.5 million or less than $0.01 per share. This amount could vary based upon the number of shares of the Company’s stock outstanding and the level of cash and investments held by the Company.

Operations of the Company Could be Adversely Affected by Events Beyond the Company's Control. The Company's operations, our suppliers, and the spending patterns of our guests could be negatively impacted by various events beyond the Company's control. Such events include, but are not limited to, natural disasters, such as hurricanes, tornadoes, floods, wildfires, and other extreme weather conditions; unforeseen public health crises, such as pandemics and epidemics; negative climate conditions; or other catastrophic events or disasters occurring in or impacting the areas in which the Company's stores, distribution center, corporate offices, or suppliers' facilities are located. Such events have the potential to adversely affect the Company's operations and financial results.

Impact to the Operations of the Company's Facilities and Retail Stores Resulting from the Novel Coronavirus ("COVID-19") or Other Global Pandemics. The Company currently has a concentration of facilities in Kearney, Nebraska, including its corporate office, distribution center, and online fulfillment center. The Company also has an office in Overland Park, Kansas for its men's buying team. The Company is dependent on the successful operation of these facilities to sustain its operations, including the operation of its online business at buckle.com and its 441 stores in 42 states across the United States.

While the Company has effectively managed the risks posed to its teammates and guests as a result of the COVID-19 global pandemic, there can be no assurances that it will be able to continue to do so as the result of further spread of COVID-19, any variants thereof, or the outbreak of infectious diseases in the future. The operation of all of the Company's facilities is critically dependent on the employees who staff these locations. In addition, federal and state governments have, and may again, imposed restrictions ranging from limitations on public interaction to stay-at-home orders in affected areas. Any events that threaten the operation of the Company's facilities or retail stores, including the outbreak of COVID-19, could have a material adverse effect on the Company's business. This coupled with the potential reduction in consumer spending could materially impact the Company's financial condition and results of operations. Further, these events may also limit the ability of the Company's vendors/manufacturers to operate, which would limit or delay the receipt of new merchandise.

15

General Risks:

Forward-Looking Statements. The Company cautions that the risk factors described above could cause actual results to vary materially from those anticipated in any forward-looking statements made by or on behalf of the Company. Management cannot assess the impact of each factor on the Company’s business or the extent to which any factor, or combination of factors, may cause actual results to vary from those contained in forward-looking statements.

ITEM 1B - UNRESOLVED STAFF COMMENTS

None.

ITEM 2 - PROPERTIES

All of the store locations operated by the Company are leased facilities. Most of the Company's stores have lease terms of approximately ten years. In the past, the Company has not experienced problems renewing its leases, although no assurance can be given that the Company can renew existing leases on favorable terms. The Company seeks to negotiate extensions on leases for stores undergoing remodeling to provide terms of approximately ten years after completion of remodeling. Consent of the landlord generally is required to remodel or change the name under which the Company does business. The Company has not experienced problems in obtaining such consent in the past. Most leases provide for a fixed minimum rental cost plus an additional rental cost based upon a set percentage of sales beyond a specified breakpoint, plus common area and other charges. The current terms of the Company's leases for stores open as of January 28, 2023, including automatic renewal options, expiring on or before January 31 of each year is as follows:

| Year | Number of Expiring Leases | |||||||

| 2024 | 145 | |||||||

| 2025 | 104 | |||||||

| 2026 | 53 | |||||||

| 2027 | 42 | |||||||

| 2028 | 38 | |||||||

| 2029 | 10 | |||||||

| 2030 | 4 | |||||||

| 2031 and later | 45 | |||||||

| Total | 441 | |||||||

The corporate headquarters and online fulfillment center for the Company are located within a facility purchased by the Company in 1988, which is located in Kearney, Nebraska. The building currently provides approximately 261,200 square feet of space, which includes approximately 82,200 square feet related to the Company’s 2005 addition. During fiscal 2010, the Company completed construction of a 240,000 square foot distribution center in Kearney, Nebraska, which currently serves as the Company’s only store distribution center. In fiscal 2015, the Company completed construction of a new office building as a part of its home office campus in Kearney, Nebraska, which provides 80,000 square feet of office space.

ITEM 3 - LEGAL PROCEEDINGS

From time to time, the Company is involved in litigation relating to claims arising out of its operations in the normal course of business. As of the date of this Form 10-K, the Company was not engaged in legal proceedings that are expected, individually or in the aggregate, to have a material effect on the Company.

ITEM 4 - MINE SAFETY DISCLOSURES

Not applicable.

16

PART II

ITEM 5 - MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

The Company’s common stock trades on the New York Stock Exchange under the symbol BKE.

Dividend Payments

During fiscal 2020, the Company's Board of Directors suspended the Company's quarterly cash dividends during the first two quarters of the fiscal year as a result of the global COVID-19 pandemic. Upon resuming the Company's quarterly cash dividends, the Company paid cash dividends of $0.30 per share in both the third and fourth quarters. The Company also paid a special cash dividend of $2.00 per share in the fourth quarter of fiscal 2020. During fiscal 2021, the Company paid cash dividends of $0.33 per share in each of the first three quarters and $0.35 per share in the fourth quarter. The Company also paid a special cash dividend of $5.65 per share in the fourth quarter of fiscal 2021. During fiscal 2022, the Company paid cash dividends of $0.35 per share in each of the four quarters. The Company also paid a special cash dividend of $2.65 per share in the fourth quarter of fiscal 2022.

Issuer Purchases of Equity Securities

The following table sets forth information concerning purchases made by the Company of its common stock for each of the months in the fiscal quarter ended January 28, 2023:

| Total Number of Shares Purchased | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans | Approximate Number of Shares Yet To Be Purchased Under Publicly Announced Plans | ||||||||||||||||||||

| Oct. 30, 2022 to Nov. 26, 2022 | — | — | — | 410,655 | |||||||||||||||||||

| Nov. 27, 2022 to Dec. 31, 2022 | — | — | — | 410,655 | |||||||||||||||||||

| Jan. 1, 2023 to Jan. 28, 2023 | — | — | — | 410,655 | |||||||||||||||||||

| Total | — | — | — | ||||||||||||||||||||

The Board of Directors authorized a 1,000,000 share repurchase plan on November 20, 2008. The Company has 410,655 shares remaining to complete this authorization.

17

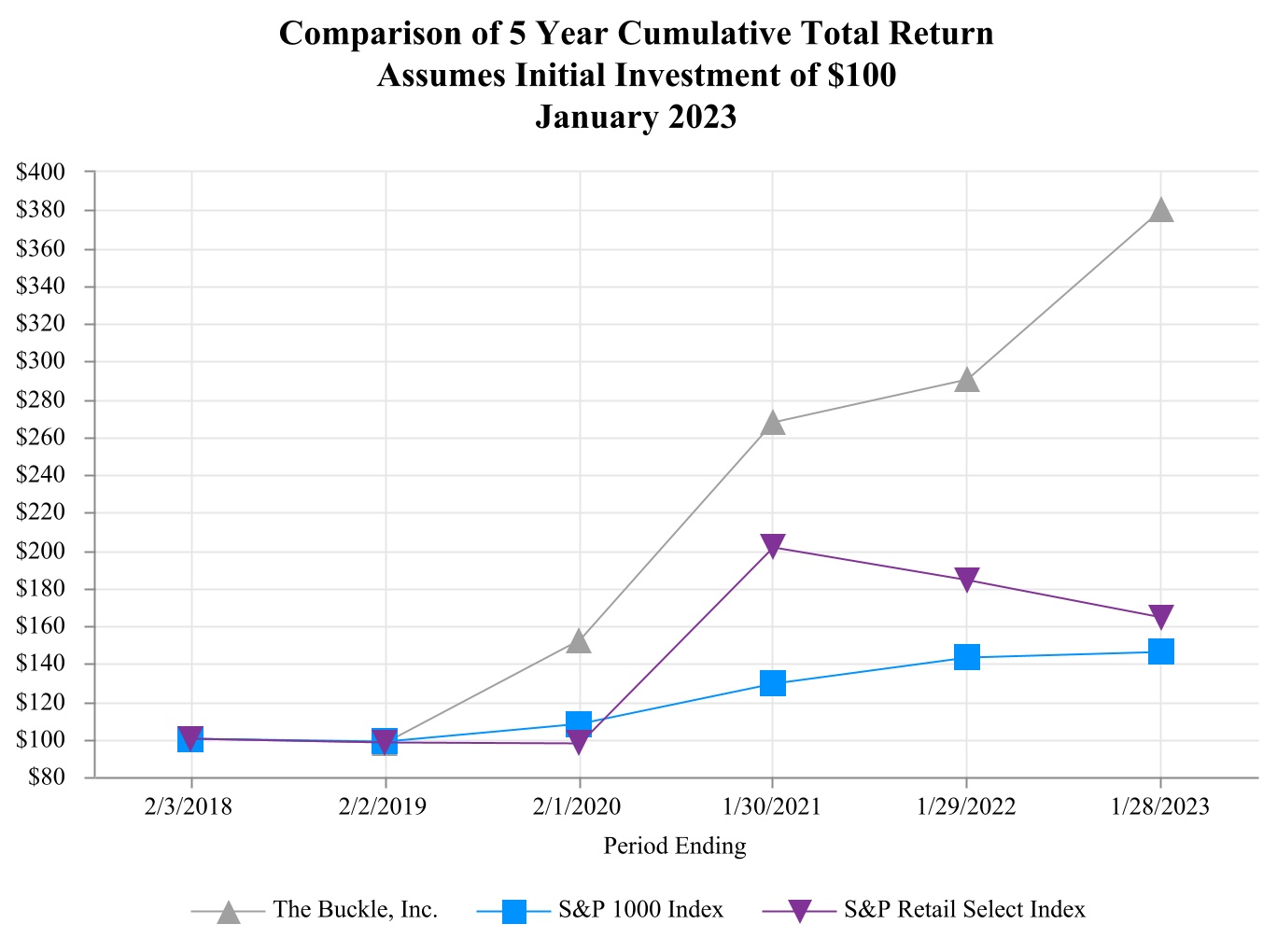

Stock Price Performance Graph

The graph below compares the cumulative total return on common shares of the Company for the last five fiscal years with the cumulative total return on the S&P 1000 Index and the S&P Retail Select Industry Index:

| Total Return Analysis | 2/3/2018 | 2/2/2019 | 2/1/2020 | 1/30/2021 | 1/29/2022 | 1/28/2023 | |||||||||||||||||||||||||||||

| The Buckle, Inc. | $ | 100.00 | $ | 98.05 | $ | 152.18 | $ | 267.26 | $ | 290.34 | $ | 380.09 | |||||||||||||||||||||||

| S&P 1000 Index | 100.00 | 98.43 | 107.86 | 129.33 | 142.98 | 146.16 | |||||||||||||||||||||||||||||

| S&P Retail Select Industry Index | 100.00 | 97.81 | 97.47 | 201.40 | 183.74 | 164.01 | |||||||||||||||||||||||||||||

18

The following table lists the Company’s quarterly market range for fiscal years 2022, 2021, and 2020, as reported by the New York Stock Exchange:

| Fiscal Years Ended | |||||||||||||||||||||||||||||||||||

| January 28, 2023 | January 29, 2022 | January 30, 2021 | |||||||||||||||||||||||||||||||||

| Quarter | High | Low | High | Low | High | Low | |||||||||||||||||||||||||||||

| First | $ | 40.07 | $ | 30.30 | $ | 45.53 | $ | 35.77 | $ | 26.77 | $ | 11.76 | |||||||||||||||||||||||

| Second | 33.94 | 26.50 | 50.79 | 38.45 | 19.03 | 12.76 | |||||||||||||||||||||||||||||

| Third | 40.54 | 29.55 | 46.80 | 38.11 | 25.08 | 15.02 | |||||||||||||||||||||||||||||

| Fourth | 50.35 | 37.20 | 57.10 | 32.26 | 42.36 | 23.98 | |||||||||||||||||||||||||||||

The number of record holders of the Company’s common stock as of March 28, 2023 was 470. Based upon information from the principal market makers, the Company believes there are more than 30,000 beneficial owners. The closing price of the Company’s common stock on March 28, 2023 was $34.44.

Additional information required by this item appears in the Notes to Consolidated Financial Statements contained herein under Footnote K "Stock-Based Compensation" and is incorporated by reference.

ITEM 6 - RESERVED

ITEM 7 - MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in conjunction with the consolidated financial statements and notes thereto of the Company included in this Form 10-K. The following is management’s discussion and analysis of certain significant factors which have affected the Company’s financial condition and results of operations during the periods included in the accompanying consolidated financial statements included in this Form 10-K.

EXECUTIVE OVERVIEW

Company management considers the following items to be key performance indicators in evaluating Company performance.

Comparable Store Sales – Stores are deemed to be comparable stores if they were open in the prior year on the first day of the fiscal period being presented. Stores which have been remodeled, expanded, and/or relocated, but would otherwise be included as comparable stores, are not excluded from the comparable store sales calculation. Online sales are included in comparable store sales. Management considers comparable store sales to be an important indicator of current Company performance, helping leverage certain fixed costs when results are positive. Negative comparable store sales results could reduce net sales and have a negative impact on operating leverage, thus reducing net earnings.

Net Merchandise Margins – Management evaluates the components of merchandise margin including initial markup and the amount of markdowns during a period. Any inability to obtain acceptable levels of initial markups or any significant increase in the Company’s use of markdowns could have an adverse effect on the Company’s gross margin and results of operations.

Operating Margin – Operating margin is a good indicator for management of the Company’s success. Operating margin can be positively or negatively affected by comparable store sales, merchandise margins, occupancy costs, and the Company’s ability to control operating costs.

Cash Flow and Liquidity (working capital) – Management reviews current cash and short-term investments along with cash flow from operating, investing, and financing activities to determine the Company’s short-term cash needs for operations and expansion. The Company believes that existing cash, short-term investments, and cash flow from operations will be sufficient to fund current and long-term anticipated capital expenditures and working capital requirements for the next several years.

19

RESULTS OF OPERATIONS

The following table sets forth certain financial data expressed as a percentage of net sales and the percentage change in the dollar amount of such items compared to the prior period:

| Percentage of Net Sales | Percentage Increase | ||||||||||||||||||||||||||||

| For Fiscal Years Ended | (Decrease) | ||||||||||||||||||||||||||||

| January 28, 2023 | January 29, 2022 | January 30, 2021 | Fiscal Year 2021 to 2022 | Fiscal Year 2020 to 2021 | |||||||||||||||||||||||||

| Net sales | 100.0 | % | 100.0 | % | 100.0 | % | 3.9 | % | 43.6 | % | |||||||||||||||||||

Cost of sales (including buying, distribution, and occupancy costs) | 49.7 | % | 49.6 | % | 55.5 | % | 4.3 | % | 28.2 | % | |||||||||||||||||||

| Gross profit | 50.3 | % | 50.4 | % | 44.5 | % | 3.5 | % | 63.0 | % | |||||||||||||||||||

| Selling expenses | 21.9 | % | 20.6 | % | 21.2 | % | 10.3 | % | 39.4 | % | |||||||||||||||||||

General and administrative expenses | 4.0 | % | 3.9 | % | 4.6 | % | 5.7 | % | 23.1 | % | |||||||||||||||||||

| Income from operations | 24.4 | % | 25.9 | % | 18.7 | % | (2.2) | % | 99.7 | % | |||||||||||||||||||

| Other income, net | 0.5 | % | 0.2 | % | 0.3 | % | 206.8 | % | (22.9) | % | |||||||||||||||||||

Income before income taxes | 24.9 | % | 26.1 | % | 19.0 | % | (0.8) | % | 97.6 | % | |||||||||||||||||||

| Income tax expense | 6.0 | % | 6.4 | % | 4.6 | % | (3.0) | % | 103.2 | % | |||||||||||||||||||

| Net income | 18.9 | % | 19.7 | % | 14.4 | % | (0.1) | % | 95.8 | % | |||||||||||||||||||

Fiscal 2022 Compared to Fiscal 2021

Net sales for the 52-week fiscal year ended January 28, 2023, increased 3.9% to $1.345 billion from net sales of $1.295 billion for the 52-week fiscal year ended January 29, 2022. Comparable store net sales for the 52-week fiscal year increased 3.3% from comparable store net sales for the prior year 52-week period ended January 29, 2022. Total sales growth for the year was the result of a 4.6% increase in the average unit retail and a 0.1% increase in the number of transactions, partially offset by a a 0.8% decrease in the average number of units sold per transaction. Online sales for the fiscal year increased 4.3% to $230.4 million for the 52-week fiscal year ended January 28, 2023 compared to $220.8 million for the 52-week fiscal year ended January 29, 2022.

The Company’s average retail price per piece of merchandise sold increased $2.13, or 4.6%, during fiscal 2022 compared to fiscal 2021. This $2.13 increase was primarily attributable to the following changes (with their corresponding effect on the overall average price per piece): a 5.2% increase in average denim price points ($0.95), a 3.0% increase in average knit shirt price points ($0.32), a 5.9% increase in average accessory price points ($0.27), a 6.9% increase in average woven shirt price points ($0.18), a 7.3% increase in average sportswear price points ($0.16), and an increase in average price points for certain other merchandise categories ($0.43); which were partially offset by a shift in the merchandise mix (-$0.18). These changes are primarily a reflection of merchandise shifts in terms of brands and product styles, fabrics, details, and finishes.

Gross profit after buying, distribution, and occupancy costs increased from $653.0 million in fiscal 2021 to $676.0 million in fiscal 2022. As a percentage of net sales, gross profit was 50.3% in fiscal 2022 compared to 50.4% in fiscal 2021. The gross margin decrease was the result of a decline in merchandise margins (0.45%, as a percentage of net sales), partially offset by leveraged occupancy, buying, and distribution expenses (0.35%, as a percentage of net sales). Merchandise shrinkage was 0.4% of net sales for fiscal 2022 compared to 0.3% of net sales for fiscal 2021.

Selling expenses increased from $266.4 million in fiscal 2021 to $293.9 million in fiscal 2022. As a percentage of net sales, selling expenses increased from 20.6% in fiscal 2021 to 21.9% in fiscal 2022.

General and administrative expenses increased from $51.1 million in fiscal 2021 to $54.0 million in fiscal 2022. As a percentage of net sales, general and administrative expenses increased from 3.9% in fiscal 2021 to 4.0% in fiscal 2022.

20

In total, selling, general, and administrative expenses were 25.9% of net sales for fiscal 2022 compared to 24.5% of net sales for fiscal 2021. The increase was the result of increases in store labor-related expenses (1.00%, as a percentage of net sales) and certain other expense categories (0.80%, as a percentage of net sales), which were partially offset by a decrease in expense related to incentive compensation accruals (0.40%, as a percentage of net sales).

As a result of the above changes, the Company’s income from operations decreased from $335.5 million for fiscal 2021 to $328.1 million for fiscal 2022. Income from operations was 24.4% as a percentage of net sales in fiscal 2022 compared to 25.9% as a percentage of net sales in fiscal 2021.

Other income was $6.9 million in fiscal 2022 compared to $2.3 million in fiscal 2021. The Company’s other income is derived primarily from investment income related to the Company’s cash and investments.

Income tax expense as a percentage of pre-tax income was 24.0% in fiscal 2022 and 24.6% in fiscal 2021, bringing net income to $254.6 million in fiscal 2022 versus $254.8 million in fiscal 2021.

Fiscal 2021 Compared to Fiscal 2020

A discussion of fiscal 2020 and year-over-year comparisons between fiscal 2021 and fiscal 2020 can be found in PART II, ITEM 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report on Form 10-K for the fiscal year ended January 29, 2022, filed with the United States Securities and Exchange Commission on March 30, 2022.

LIQUIDITY AND CAPITAL RESOURCES

As of January 28, 2023, the Company had working capital of $197.3 million, including $252.1 million of cash and cash equivalents and $21.0 million of short-term investments. The Company’s cash receipts are generated from retail sales and from investment income, and the Company's primary ongoing cash requirements are for inventory, payroll, occupancy costs, dividend payments, new store expansion, remodeling, and other capital expenditures. Historically, the Company’s primary source of working capital has been cash flow from operations. During fiscal 2022, 2021, and 2020 the Company's cash flow from operations was $242.4 million, $311.8 million, and $227.4 million, respectively. Changes in operating cash flow between each of the three years is primarily a function of changes in net income, along with changes in inventory and accounts payable based on the timing and amount of merchandise purchased in each respective period. Operating cash flow is also impacted by the timing of certain other payments, including rent, income taxes, and annual incentive bonuses. The reduction in operating cash flow for fiscal 2022 compared to fiscal 2021 is primarily attributable to changes in inventory and accounts payable as the Company built its inventory back to more normalized levels, as well as the payment of incentive bonuses in the first quarter of fiscal 2022 based on the Company's strong financial results in fiscal 2021. These factors also had a significant impact on operating cash flow compared to fiscal 2020, but were offset by strong increases in both net sales and net income for both fiscal 2022 and fiscal 2021 compared to fiscal 2020.

During fiscal 2022, 2021, and 2020, the Company invested $29.5 million, $18.3 million, and $5.5 million, respectively, in new store construction, store renovation, and store technology upgrades. The Company spent $0.9 million, $0.8 million, and $2.2 million in fiscal 2022, 2021, and 2020, respectively, in capital expenditures for the corporate offices and distribution facility.