UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

FOR THE FISCAL YEAR ENDED SEPTEMBER 30 , 2023

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ________ to ________

Commission file number 1-11071

(Exact name of registrant as specified in its charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of Principal Executive Offices) (Zip Code)

(610 ) 337-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class: | Trading Symbol(s): | Name of each exchange on which registered: | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☑ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | |||||||||||||||||||

| Smaller reporting company | Emerging growth company | ||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of UGI Corporation Common Stock held by non-affiliates of the registrant on March 31, 2023 was $7,252,195,251 .

At November 10, 2023, there were 210,899,583 shares of UGI Corporation Common Stock issued and outstanding.

TABLE OF CONTENTS

| Page | |||||

F-2 | |||||

1

GLOSSARY OF TERMS AND ABBREVIATIONS

Terms and abbreviations used in this Form 10-K are defined below:

UGI Corporation and Related Entities

AmeriGas Finance Corp. - A wholly owned subsidiary of AmeriGas Partners

AmeriGas OLP - AmeriGas Propane, L.P., the principal operating subsidiary of AmeriGas Partners

AmeriGas Partners - AmeriGas Partners, L.P., an indirect wholly owned subsidiary of UGI; also referred to, together with its consolidated subsidiaries, as the “Partnership”

AmeriGas Propane - Reportable segment comprising AmeriGas Propane, Inc. and its subsidiaries, including AmeriGas Partners and AmeriGas OLP

AmeriGas Propane, Inc. - A wholly owned second-tier subsidiary of UGI and the general partner of AmeriGas Partners; also referred to as the “General Partner”

AvantiGas - AvantiGas Limited, an indirect wholly owned subsidiary of UGI International, LLC

Company - UGI and its consolidated subsidiaries collectively

DVEP - DVEP Investeringen B.V., an indirect wholly owned subsidiary of UGI International, LLC

Electric Utility - UGI Utilities’ regulated electric distribution utility

Energy Services - UGI Energy Services, LLC, a wholly owned subsidiary of Enterprises

Enterprises - UGI Enterprises, LLC, a wholly owned subsidiary of UGI

ESFC - Energy Services Funding Corporation, a wholly owned subsidiary of Energy Services

Flaga - Flaga GmbH, an indirect wholly owned subsidiary of UGI International, LLC

Gas Utility - UGI’s regulated natural gas businesses, inclusive of PA Gas Utility and WV Gas Utility

General Partner - AmeriGas Propane, Inc., the general partner of AmeriGas Partners

GHI - GHI Energy, LLC, a Houston-based renewable natural gas company and indirect wholly owned subsidiary of Energy Services

MBL Bioenergy - MBL Bioenergy, LLC

Midstream & Marketing - Reportable segment comprising Energy Services and UGID

Mountaineer - Mountaineer Gas Company, a natural gas distribution company in West Virginia and a wholly owned subsidiary of Mountaintop Energy Holdings, LLC

Mountaintop Energy Holdings, LLC - Parent company of Mountaineer and wholly owned subsidiary of UGI, acquired on September 1, 2021

PA Gas Utility - UGI Utilities’ regulated natural gas distribution business, primarily located in Pennsylvania

Partnership - AmeriGas Partners and its consolidated subsidiaries, including AmeriGas OLP; also referred to as “AmeriGas Partners”

Pennant - Pennant Midstream, LLC, an indirect wholly owned subsidiary of Energy Services

2

PennEast - PennEast Pipeline Company, LLC

Pine Run - Pine Run Gathering, LLC

Stonehenge - Stonehenge Appalachia, LLC, a midstream natural gas gathering business

UGI - UGI Corporation or, collectively, UGI Corporation and its consolidated subsidiaries

UGI Appalachia - UGI Appalachia, LLC, a wholly owned subsidiary of Energy Services

UGI France - UGI France SAS (a Société par actions simplifiée), an indirect wholly owned subsidiary of UGI International, LLC

UGI International - Reportable segment principally comprising UGI’s foreign operations

UGI International, LLC - UGI International, LLC, a wholly owned subsidiary of Enterprises

UGI Moraine East - UGI Moraine East Gathering LLC, a wholly owned subsidiary comprising the assets acquired in the Stonehenge Acquisition

UGI Pine Run, LLC - A wholly owned subsidiary of Energy Services that holds a 49% membership interest in Pine Run

Utilities - Reportable segment comprising UGI Utilities and Mountaintop Energy Holdings, LLC

UGI Utilities - UGI Utilities, Inc., a wholly owned subsidiary of UGI comprising PA Gas Utility and Electric Utility

UGID - UGI Development Company, a wholly owned subsidiary of Energy Services

UniverGas - UniverGas Italia S.r.l, an indirect wholly owned subsidiary of UGI International, LLC

WV Gas Utility - Mountaineer’s regulated natural gas distribution business, located in West Virginia

Other Terms and Abbreviations

2013 OICP - UGI Corporation 2013 Omnibus Incentive Compensation Plan

5.625% Senior Notes - An underwritten public offering of $675 million aggregate principal amount of notes due May 2024, issued by AmeriGas Partners. Pursuant to the tender offer, dated May 22, 2023, AmeriGas Partners, in June 2023, redeemed all outstanding 5.625% Senior Notes due May 2024 and in so doing was released from the obligations with respect to the indenture for the 5.625% Senior Notes

9.375% Senior Notes - An underwritten private offering of $500 million aggregate principal amount of notes due May 2028, co-issued by AmeriGas Partners and AmeriGas Finance Corp.

2021 IAP - UGI Corporation 2021 Incentive Award Plan

2022 AmeriGas OLP Credit Agreement - Entered into by AmeriGas OLP providing for borrowings of up to $600 million, with the option to increase to a maximum principal amount of $900 million assuming certain conditions are met, including a letter of credit subfacility of up to $100 million, scheduled to expire in September 2026. On November 15, 2023, the Company amended the 2022 AmeriGas OLP Credit agreement reducing the revolver to $400 million

2024 Purchase Contract - A forward stock purchase contract issued by the Company as a part of the issuance of Equity Units which obligates holders to purchase a number of shares of UGI Common Stock from the Company on June 1, 2024

ABO - Accumulated Benefit Obligation

ACE - AmeriGas Cylinder Exchange

3

AFUDC - Allowance for Funds Used During Construction

AmeriGas OLP Credit Agreement - The second amended and restated credit agreement entered into by AmeriGas OLP providing for borrowings of up to $600 million, including a letter of credit subfacility of up to $150 million, was paid in full and terminated concurrently with the execution of the 2022 AmeriGas OLP Credit Agreement

AOCI - Accumulated Other Comprehensive Income (Loss)

ASC - Accounting Standards Codification

ASC 606 - ASC 606, “Revenue from Contracts with Customers”

ASC 820 - ASC 820, “Fair Value Measurement”

ASC 980 - ASC 980, “Regulated Operations”

ASU - Accounting Standards Update

Bcf - Billions of cubic feet

Board of Directors - The board of directors of UGI

Btu - British thermal unit

CERCLA - Comprehensive Environmental Response, Compensation and Liability Act

CFTC - Commodity Futures Trading Commission

COA - Consent Order and Agreement

CODM - Chief Operating Decision Maker as defined in ASC 280, “Segment Reporting”

Common Stock - Shares of UGI common stock

Common Units - Limited partnership ownership interests in AmeriGas Partners

Convertible Preferred Stock - Preferred stock of UGI titled 0.125% series A cumulative perpetual convertible preferred stock without par value and having a liquidation preference of $1,000 per share

Core market - Comprises (1) firm residential, commercial and industrial customers to whom Utilities has a statutory obligation to provide service who purchase their natural gas or electricity from Utilities; and (2) residential, commercial and industrial customers to whom Utilities has a statutory obligation to provide service who purchase their natural gas or electricity from others

DOT - U.S. Department of Transportation

DSIC - Distribution System Improvement Charge

Energy Services Amended Term Loan Credit Agreement - The first amendment to the Energy Services Term Loan Credit Agreement, entered into on February 23, 2023, comprising an $800 million variable-rate term loan with a final maturity of February 2030

Energy Services Term Loan Credit Agreement - A seven-year $700 million variable rate senior secured term loan agreement entered into on August 13, 2019 by Energy Services and amended on February 23, 2023

EPACT 2005 - Energy Policy Act of 2005

4

ERISA - Employee Retirement Income Security Act of 1974

ERO - Electric Reliability Organization

EU - European Union

Equity Unit Agreements - Collection of agreements governing the rights, privileges and obligations of the holders of the Equity Units and UGI as issuer of the Equity Units, which were filed with the SEC on Form 8-K on May 25, 2021

Equity Unit - A corporate unit consisting of a 2024 Purchase Contract and 1/10th or 10% undivided interest in one share of Convertible Preferred Stock

Exchange Act - Securities Exchange Act of 1934, as amended

FDIC - Federal Deposit Insurance Corporation

FERC - Federal Energy Regulatory Commission

FIFO - First-in, first-out inventory valuation method

Fiscal 2020 - The fiscal year ended September 30, 2020

Fiscal 2021 - The fiscal year ended September 30, 2021

Fiscal 2022 - The fiscal year ended September 30, 2022

Fiscal 2023 - The fiscal year ended September 30, 2023

Fiscal 2024 - The fiscal year ending September 30, 2024

Fiscal 2025 - The fiscal year ending September 30, 2025

Fiscal 2026 - The fiscal year ending September 30, 2026

Fiscal 2027 - The fiscal year ending September 30, 2027

Fiscal 2028 - The fiscal year ending September 30, 2028

GAAP - U.S. generally accepted accounting principles

GDPR - General Data Protection Regulation

GHG - Greenhouse gas

GILTI - Global Intangible Low Taxed Income

Gwh - Millions of kilowatt hours

Hunlock - Hunlock Creek Energy Center located near Wilkes-Barre, Pennsylvania, a 174-megawatt natural gas-fueled electricity generating station

ICE - Intercontinental Exchange

IRC - Internal Revenue Code

IREP - Infrastructure Replacement and Expansion Plan

IRPA - Interest rate protection agreement

5

IRS - Internal Revenue Service

IT - Information technology

LIBOR - London Inter-bank Offered Rate

LNG - Liquefied natural gas

LPG - Liquefied petroleum gas

LTIIP - Long-term infrastructure improvement plans

MD&A - Management’s Discussion and Analysis of Financial Condition and Results of Operations

MDPSC - Maryland Public Service Commission

MGP - Manufactured gas plant

Mountaineer Acquisition - Acquisition of Mountaintop Energy Holdings LLC, which closed on September 1, 2021

Mountaineer 2023 Credit Agreement - Third amendment to the third amended and restated credit agreement entered into by Mountaineer, as borrower, providing for borrowings up to $150 million, with the option to increase to a maximum principal amount of $250 million assuming certain conditions are met, including a letter or credit subfacility of up to $20 million, scheduled to expire in November 2024, with an option to extend the maturity date

NAV - Net asset value

NOAA - National Oceanic and Atmospheric Administration

NOL - Net operating loss

NPNS - Normal purchase and normal sale

NTSB - National Transportation Safety Board

NYDEC - New York State Department of Environmental Conservation

NYMEX - New York Mercantile Exchange

OSHA - Occupational Safety and Health Act

PADEP - Pennsylvania Department of Environmental Protection

PAPUC - Pennsylvania Public Utility Commission

Partnership Agreement - Fourth amended and restated agreement of Limited Partnership of AmeriGas Partners, L.P. dated as of July 27, 2009, as amended

PBO - Projected benefit obligation

Pennant Acquisition - Energy Services’ Fiscal 2022 acquisition of the remaining 53% equity interest in Pennant

PennEnergy - PennEnergy Resources, LLC

PGA - Purchased gas adjustment

PGC - Purchased gas costs

PJM - PJM Interconnection, LLC

6

PRP - Potentially responsible party

PUHCA 2005 - Public Utility Holding Company Act of 2005

Receivables Facility - A receivables purchase facility of Energy Services with an issuer of receivables-backed commercial paper

Retail core-market - Comprises firm residential, commercial and industrial customers to whom Utilities has a statutory obligation to provide service that purchase their natural gas from Utilities

RNG - Renewable natural gas

ROU - Right-of-use

ROD - Record of Decision

SEC - U.S. Securities and Exchange Commission

Series B preferred stock - Preferred stock of UGI titled 0.125% series B cumulative perpetual preferred stock with terms substantially identical to the Convertible Preferred Stock, except that it will not be convertible

Stonehenge - Stonehenge Energy Resources III, LLC, a portfolio company of Energy Spectrum Partners VIII, L.P.

Stonehenge Acquisition - Acquisition of Stonehenge Appalachia, LLC, which closed January 27, 2022

Stock Unit - Unit awards that entitle the grantee to shares of UGI Common Stock or cash subject to service conditions

TCJA - Tax Cuts and Jobs Act

Term SOFR - Secured Overnight Financing Rate

TSR - Total Shareholder Return

U.K. - United Kingdom

U.S. - United States of America

UGI comparator group - The Russell Midcap Utility Index, excluding telecommunications companies, and beginning in Fiscal 2021, a custom UGI performance peer group

UGI Corporation Credit Facility Agreement - An amended and restated unsecured senior credit facilities agreement entered into by UGI Corporation on May 4, 2021 (the “2021 UGI Corporation Senior Credit Facility”), comprising (1) a $250 million term loan facility maturing in August 2024, (2) a $300 million term loan facility maturing in May 2025, (3) a $300 million delayed draw term loan facility maturing in May 2025, and (4) a $300 million revolving credit facility maturing in August 2024 (including a $10 million sublimit for letters of credit). On May 12, 2023, the Company entered into the second amendment to the UGI Corporation Credit Agreement to replace the reference rate from LIBOR with Term SOFR. On September 20, 2023, the Company entered into the third amendment that, among other things, extended the maturity date of (1) the $250 million term loan facility and (2) the $300 million revolving credit facility to May 2025.

UGI Energy Services Credit Agreement - A five-year senior secured revolving credit agreement entered into by Energy Services on March 6, 2020, providing for borrowings up to $260 million, including a letter of credit subfacility of up to $50 million, scheduled to expire in March 2025. On May 12, 2023, Energy Services entered into the second amendment to the UGI Energy Services Credit Agreement to replace the reference rate from LIBOR with Term SOFR.

UGI International 2023 Credit Facilities Agreement - A five-year unsecured senior facilities agreement entered into in March 2023 comprising a €300 million variable-rate term loan facility and a €500 million multicurrency revolving credit facility scheduled to expire in March 2028.

7

UGI International 3.25% Senior Notes - An underwritten private placement of €350 million principal amount of senior unsecured notes originally due November 1, 2025, issued by UGI International, LLC. The UGI International 3.25% Senior Notes were repaid in December 2021.

UGI International Credit Facilities Agreement - A five-year unsecured senior facilities agreement entered into in October 2018, by UGI International, LLC comprising a €300 million term loan facility and a €300 million revolving credit facility, scheduled to expire in October 2023, repaid in full and terminated concurrently with the execution of the UGI International 2023 Credit Facilities Agreement.

UGI Performance Units - Unit awards that entitle the grantee to shares of UGI Common Stock or cash subject to service and market performance conditions

UGI Utilities 2023 Credit Agreement - An unsecured revolving credit agreement entered into by UGI Utilities on November 9, 2023, providing for borrowings up to $375 million, including a letter of credit subfacility of up to $50 million and a $38 million sublimit for swingline loans, set to mature November 2024, including an automatic extension to November 9, 2028 upon receipt of authorization from the PAPUC

UGI Utilities Credit Agreement - A five-year unsecured revolving credit agreement entered into by UGI Utilities on June 27, 2019, providing for borrowings up to $350 million, including a letter of credit subfacility of up to $100 million, scheduled to expire in June 2024. On December 13, 2022, UGI Utilities entered into an amendment to UGI Utilities Credit Agreement, providing for borrowings up to $425 million and to replace the reference rate from LIBOR with Term SOFR, repaid in full and terminated concurrently with the execution of the UGI Utilities 2023 Credit Agreement

USD - U.S. dollar

U.S. Pension Plans - Consists of (1) a defined benefit pension plan for employees hired prior to January 1, 2009 of UGI, UGI Utilities and certain of UGI’s other domestic wholly owned subsidiaries; and (2) a defined benefit pension plan for employees of Mountaineer hired prior to January 1, 2023.

VEBA - Voluntary Employees’ Beneficiary Association

WVPSC - Public Service Commission of West Virginia

8

FORWARD-LOOKING INFORMATION

Information contained in this Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such statements use forward-looking words such as “believe,” “plan,” “anticipate,” “continue,” “estimate,” “expect,” “may,” or other similar words and terms of similar meaning, although not all forward-looking statements contain such words. These statements discuss plans, strategies, events or developments that we expect or anticipate will or may occur in the future. All forward-looking statements made in this Report rely upon the safe harbor protections provided under the Private Securities Litigation Reform Act of 1995.

A forward-looking statement may include a statement of the assumptions or bases underlying the forward-looking statement. We believe that we have chosen these assumptions or bases in good faith and that they are reasonable. However, we caution you against relying on any forward-looking statement as these statements are subject to risks and uncertainties that may cause actual results to vary from assumed facts or bases, and the differences between actual results and assumed facts or bases can be material, depending on the circumstances. When considering forward-looking statements, you should keep in mind our Risk Factors included in Item 1A herein and the following important factors that could affect our future results and could cause those results to differ materially from those expressed in our forward-looking statements: (1) weather conditions, including increasingly uncertain weather patterns due to climate change, resulting in reduced demand, the seasonal nature of our business, and disruptions in our operations and supply chain; (2) cost volatility and availability of energy products, including propane and other LPG, electricity, and natural gas, as well as the availability of LPG cylinders, and the capacity to transport product to our customers; (3) changes in domestic and foreign laws and regulations, including safety, health, tax, transportation, consumer protection, data privacy, accounting, and environmental matters, such as regulatory responses to climate change; (4) inability to timely recover costs through utility rate proceedings; (5) the impact of pending and future legal or regulatory proceedings, inquiries or investigations; (6) competitive pressures from the same and alternative energy sources; (7) failure to acquire new customers or retain current customers thereby reducing or limiting any increase in revenues; (8) liability for environmental claims; (9) increased customer conservation measures due to high energy prices and improvements in energy efficiency and technology resulting in reduced demand; (10) adverse labor relations and our ability to address existing or potential workforce shortages; (11) customer, counterparty, supplier, or vendor defaults; (12) liability for uninsured claims and for claims in excess of insurance coverage, including those for personal injury and property damage arising from explosions, acts of war, terrorism, natural disasters, pandemics, and other catastrophic events that may result from operating hazards and risks incidental to generating and distributing electricity and transporting, storing and distributing natural gas and LPG in all forms; (13) transmission or distribution system service interruptions; (14) political, regulatory and economic conditions in the United States, Europe and other foreign countries, including uncertainties related to the war between Russia and Ukraine, the conflict in the Middle East, the European energy crisis, and foreign currency exchange rate fluctuations, particularly the euro; (15) credit and capital market conditions, including reduced access to capital markets and interest rate fluctuations; (16) changes in commodity market prices resulting in significantly higher cash collateral requirements; (17) impacts of our indebtedness and the restrictive covenants in our debt agreements; (18) reduced distributions from subsidiaries impacting the ability to pay dividends or service debt; (19) changes in Marcellus and Utica Shale gas production; (20) the success of our strategic initiatives and investments that are intended to advance our business strategy; (21) our ability to successfully integrate acquired businesses and achieve anticipated synergies; (22) the interruption, disruption, failure, malfunction, or breach of our information technology systems, and those of our third-party vendors or service providers, including due to cyber attack; (23) the inability to complete pending or future energy infrastructure projects; (24) our ability to attract, develop, retain and engage key employees; (25) uncertainties related to global pandemics; (26) the impact of a material impairment of our assets; (27) the impact of proposed or future tax legislation; (28) the impact of declines in the stock market or bond market, and a low interest rate environment, on our pension liability; (29) our ability to protect our intellectual property; (30) our ability to overcome supply chain issues that may result in delays or shortages in, as well as increased costs of, equipment, materials or other resources that are critical to our business operations; and (31) our ability to control operating costs and realize cost savings.

These factors are not necessarily all of the important factors that could cause actual results to differ materially from those expressed in any of our forward-looking statements. Other unknown or unpredictable factors could also have material adverse effects on future results. Any forward-looking statement speaks only as of the date on which such statement is made. We undertake no obligation (and expressly disclaim any obligation) to update publicly any forward-looking statement whether as a result of new information or future events except as required by the federal securities laws.

PART I:

ITEMS 1. AND 2. BUSINESS AND PROPERTIES

CORPORATE OVERVIEW

UGI Corporation is a holding company that, through subsidiaries and affiliates, distributes, stores, transports and markets energy products and related services. In the U.S., we own and operate (1) a retail propane marketing and distribution business, (2) natural gas and electric distribution utilities, and (3) energy marketing (including RNG), midstream infrastructure, storage, natural gas gathering and processing, natural gas production, electricity generation and energy services businesses. In Europe,

9

we market and distribute propane and other LPG, and market other energy products and services. Our subsidiaries and affiliates operate principally in the following four business segments:

•AmeriGas Propane

•UGI International

•Midstream & Marketing

•Utilities

The AmeriGas Propane segment consists of the propane distribution business of AmeriGas Partners, an indirect wholly owned subsidiary of UGI. The Partnership conducts its domestic propane distribution business through its principal operating subsidiary, AmeriGas OLP, and is the nation’s largest retail propane distributor based on the volume of propane gallons distributed annually. The general partner of AmeriGas Partners is our wholly owned subsidiary, AmeriGas Propane, Inc.

The UGI International segment consists of LPG distribution businesses conducted by our subsidiaries and affiliates in Austria, Belgium, the Czech Republic, Denmark, Finland, France, Hungary, Italy, Luxembourg, the Netherlands, Norway, Poland, Romania, Slovakia, Sweden, Switzerland and the United Kingdom. Based on reported market volumes for 2022, which is the most recent information available, UGI International believes that it is the largest distributor of LPG in France, Austria, Belgium, Denmark and Luxembourg and one of the largest distributors of LPG in Norway, Poland, the Czech Republic, Slovakia, the Netherlands, Sweden and Switzerland. During Fiscal 2023, we made significant progress on our strategic decision to exit the energy marketing business at UGI International. In Fiscal 2023, we divested of our energy marketing business in the United Kingdom and Belgium. On October 1, 2023, we divested substantially all of our energy marketing business in France. We also continue to make significant progress on the wind-down of our energy marketing business in the Netherlands. See Note 5 for additional information regarding the UGI International energy marketing businesses.

The Midstream & Marketing segment consists of energy-related businesses conducted by our indirect, wholly owned subsidiary, Energy Services. These businesses (i) conduct energy marketing, including RNG, in the Mid-Atlantic region of the United States and California, (ii) own and operate natural gas liquefaction, storage and vaporization facilities and propane-air mixing assets, (iii) manage natural gas pipeline and storage contracts, (iv) develop, own and operate pipelines, gathering infrastructure and gas storage facilities in the Marcellus and Utica Shale regions of Pennsylvania, eastern Ohio, and the panhandle of West Virginia, (v) own electricity generation facilities, and (vi) develop, own and operate RNG production facilities. Energy Services and its subsidiaries’ storage, LNG and portions of its midstream transmission operations are subject to regulation by the FERC.

The Utilities segment consists of the regulated natural gas (PA Gas Utility) and electric (Electric Utility) distribution businesses of our wholly owned subsidiary, UGI Utilities, and the regulated natural gas distribution business of our indirect, wholly owned subsidiary, Mountaineer. PA Gas Utility serves customers in eastern and central Pennsylvania and in portions of one Maryland county, and Mountaineer serves customers in West Virginia. Electric Utility serves customers in portions of Luzerne and Wyoming counties in northeastern Pennsylvania. PA Gas Utility is subject to regulation by the PAPUC and FERC and, with respect to its customers in Maryland, the MDPSC. Mountaineer is subject to regulation by the WVPSC and FERC. Electric Utility is subject to regulation by the PAPUC and FERC.

Business Strategy

Our business strategy is to grow the Company by focusing on our core competencies of distributing, storing, transporting and marketing energy products and services. We utilize our core competencies from our existing diversified businesses and our international experience, extensive asset base and access to customers to accelerate both organic growth and growth through acquisitions in our existing businesses, as well as in related and complementary businesses.

In August 2023, the Company announced the commencement of a strategic review with a focus on our LPG businesses to unlock and maximize shareholder value. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for additional information. We continue to focus on advancing our strategy of: (1) providing reliable earnings growth; (2) rebalancing our portfolio, with an emphasis on natural gas and renewable energy solutions; and (3) investing in renewable energy solutions. The following discussion highlights some of our key accomplishments in these areas during Fiscal 2023.

Reliable Earnings Growth

We are committed to consistently growing our earnings and plan to continue this growth through robust investments in our regulated utilities businesses, generating significant fee-based income in our Midstream and Marketing operations, optimizing our cost structure and effectively managing our global LPG businesses, which generate significant free cash flow. We strive to

10

be the preferred provider in all markets we serve and remain focused on making continuous improvements and focusing on growth across our businesses.

At our Utilities segment, we continue to deliver attractive earnings growth through capital investments and customer additions, while taking actions to reduce earnings volatility. In Fiscal 2023, PA Gas Utility connected more than 1,460 new commercial and industrial customers and added more than 11,100 residential heating customers. Beginning on November 1, 2022, PA Gas Utility was authorized to implement a weather normalization adjustment rider as a five-year pilot program which we expect to result in reduced earnings volatility and stabilize our customers’ distribution charges. In September 2023, our Electric Utility received PAPUC approval for an $8.5 million annual base distribution rate increase beginning in October 2023. On October 6, 2023, Mountaineer filed a joint stipulation and agreement for settlement of the base rate case proceeding that Mountaineer had initiated in March of 2023 with the WVPSC. The settlement is subject to approval by the WVPSC and is expected to result in a net revenue increase of approximately $13.9 million and an overall increase in total revenues of 4.16% for Mountaineer. See Note 9 to Consolidated Financial Statements for additional information.

Our Midstream and Marketing business continues to provide stable earnings, which is underpinned by fee-based contracts from customers. This fee-based income is derived from fixed-fee peaking, storage and gathering, and fixed rate, variable volume gathering and marketing transactions. In Fiscal 2023, over 85% of Midstream and Marketing’s total margin was fee-based. In addition, Midstream and Marketing continued expanding in the renewable energy space, which we believe will contribute to our future earnings growth. For more information on these transactions, see “Investment in Renewable Energy” below.

During Fiscal 2023, we made technology and other investments to promote the safety of our employees and the communities we serve. For example, we continued (i) installing cameras in our delivery and service vehicles to facilitate in-cab coaching capabilities, among other functionality, and (ii) installing fall protection towers on rail terminals that are designed to prevent employees from falling during the process of offloading propane into bulk storage.

During Fiscal 2023, we made significant progress on our strategic decision to exit the energy marketing business at UGI International. We divested of our energy marketing businesses in the United Kingdom and Belgium during Fiscal 2023 and divested substantially all of our energy marketing business in France on October 1, 2023. In addition, we continue to make progress on the wind-down of our energy marketing business in the Netherlands.

Rebalancing Our Portfolio

We are committed to rebalancing our portfolio through both organic growth and investment in natural gas and renewable energy solutions.

In Fiscal 2023, we executed our rebalancing strategy by prioritizing our capital investment in the natural gas businesses. At the Utilities, we continued to execute our infrastructure replacement and system betterment program, with record capital expenditures in Fiscal 2023 and additional expenditures expected in the coming years. Our PA Gas Utility remains on schedule to achieve its goal of replacing the cast iron portions of its gas mains by March 2027 and the bare steel portion of its gas mains by September 2041. We believe that the replacement of aging infrastructure results in increased contributions to rate base growth and also reduces emissions while improving operational efficiency and distribution system integrity.

Investment in Renewable Energy

We are pursuing investments in several renewable energy areas, including RNG, bio-LPG and renewable dimethyl ether. Our natural gas businesses are exploring RNG opportunities involving both distribution and RNG feedstock infrastructure, and our LPG businesses are developing bio-LPG sources to augment our existing bio-LPG source in Sweden. We believe that UGI is well-positioned to develop investment opportunities in these emerging markets due to our competencies in project development, project execution, gas transportation and storage, and energy marketing.

We expect to utilize our existing natural gas and LPG distribution infrastructure to deliver RNG and bio-LPG to the customers we serve. In most cases, these renewable solutions can be delivered to our customers with no additional local infrastructure, incremental investments by our customers, or community disruption related to infrastructure buildout.

In Fiscal 2023, we completed the following transactions:

•In November 2022, Energy Services announced a project that will modify an existing anaerobic biogas facility to generate RNG. The project is expected to be completed in the second half of 2024 and, once completed, is expected to produce approximately 35 million cubic feet of RNG annually.

•In January 2023, Energy Services announced that it entered into an agreement to invest $150 million in two RNG projects currently under development in South Dakota. One project is expected to generate approximately 300 million cubic feet of RNG annually once completed in calendar year 2024 and the other project is expected to generate approximately 225 million cubic feet of RNG annually once completed in calendar year 2024.

11

•In February 2023, Energy Services entered into a joint venture to develop an RNG project at the Commonwealth Environmental Systems landfill in Pennsylvania. Once complete, the project is expected to have the capacity to produce approximately 5,000 MMBtu per day of pipeline-quality RNG.

These projects provide a range of benefits, including reducing our carbon footprint while also addressing increased customer demand for low carbon energy sources.

Environmental Strategy

We believe that corporate sustainability is critical to our overall business success and we are committed to growing the Company in an environmentally responsible way. UGI’s environmental strategy is focused on three main areas: reducing our emissions; reducing our customers’ emissions affordably, reliably, and responsibly; and investing in renewable solutions. To support our strategy, we have made the following environmental commitments discussed below while also committing to continue to grow our earnings per share and dividends.

•Scope 1 Emissions Reduction Commitment – Reduce Scope 1 GHG emissions by 55% by 2025 (using Fiscal 2020 as a baseline). Our Scope 1 emissions reduction target does not include emissions from the Mountaineer Acquisition, which closed in September 2021. The target also excluded the Stonehenge Acquisition and only accounts for our ownership interest in Pennant at the time we set the target. The emissions from the Pine Run acquisition were included in the baseline 2020 number as this investment contributed to our goal. The 2020 base number also takes a five year emissions average from the Hunlock generation facility to account for year-over-year differences in run time.

•Methane Emissions Reduction Commitment – 92% reduction by 2030, and 95% reduction by 2040.

•Pipeline Replacement and Betterment Commitment – Replace all cast iron pipelines by 2027 and all bare steel by 2041. Our pipeline replacement and betterment activities better enable us to achieve our emissions reductions goals.

We report our progress on the environmental goals and commitments annually in our Sustainability Reports, including our Scope 1, 2 and 3 emissions, air quality impact, and water management efforts. Our Scope 3 emissions stem primarily from the extraction (upstream) and combustion (downstream) of the molecules we distribute, and from our supply chain. Our Sustainability Reports may be accessed on our website under “ESG - Resources - Sustainability Reports.” Information published in our Sustainability Reports is not incorporated by reference in this Report.

In formulating our environmental strategy, our management and Board of Directors consider certain risks and uncertainties that may materially impact our financial condition and results of operations. For more information on these risks and uncertainties, see “Risk Factors - The potential effects of climate change may affect our business, operations, supply chain and customers, which could adversely impact our financial condition and results of operations.”

Corporate Information

UGI was incorporated in Pennsylvania in 1991. The Company is not subject to regulation by the PAPUC but, following completion of the Mountaineer Acquisition, is a regulated “holding company” under PUHCA 2005. PUHCA 2005 and the implementing regulations of FERC give FERC access to certain holding company books and records and impose certain accounting, record-keeping, and reporting requirements on holding companies. PUHCA 2005 also provides state utility regulatory commissions with access to holding company books and records in certain circumstances.

Our executive offices are located at 500 North Gulph Road, King of Prussia, Pennsylvania 19406, and our telephone number is (610) 337-1000. In this Report, the terms “Company” and “UGI,” as well as the terms “our,” “we,” “us,” and “its” are sometimes used as abbreviated references to UGI Corporation or, collectively, UGI Corporation and its consolidated subsidiaries. For further information on the meaning of certain terms used in this Report, see “Glossary of Terms and Abbreviations.”

The Company’s corporate website can be found at www.ugicorp.com. Information on our website, including the information published in our Sustainability Reports, is not incorporated by reference in this Report. The Company makes available free of charge at this website (under the “Investors - Financial Reports - SEC Filings and Proxies” caption) copies of its reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, including its Annual Reports on Form 10-K, its Quarterly Reports on Form 10-Q, and its Current Reports on Form 8-K. The Company’s Principles of Corporate Governance, Code of Business Conduct and Ethics, and Supplier Code of Business Conduct and Ethics are available on the Company’s website under the caption “Company - Leadership and Governance - Governance Documents.” The charters of the Audit, Corporate Governance, Compensation and Management Development, and Safety, Environmental and Regulatory Compliance Committees of the Board of Directors are available on the Company’s website under the caption “Company - Leadership and Governance - Committees & Charters.” All of these documents are also available free of charge by writing to Director,

12

Investor Relations, UGI Corporation, P.O. Box 858, Valley Forge, PA 19482.

AMERIGAS PROPANE

Products, Services and Marketing

Our domestic propane distribution business is conducted through AmeriGas Propane. AmeriGas Propane serves nearly 1.2 million customers in all 50 states from approximately 1,380 propane distribution locations. Typically, propane distribution locations are in suburban and rural areas where natural gas is not readily available. Our local offices generally consist of operations facilities and propane storage. As part of its overall transportation and distribution infrastructure, AmeriGas Propane operates as an interstate carrier in all states throughout the continental U.S.

AmeriGas Propane sells propane primarily to residential, commercial/industrial, motor fuel, agricultural and wholesale customers. AmeriGas Propane distributed approximately 940 million gallons of propane in Fiscal 2023. Approximately 88% of AmeriGas Propane’s Fiscal 2023 sales (based on gallons sold) was to retail accounts and approximately 12% was to wholesale accounts. Sales to residential customers in Fiscal 2023 represented approximately 30% of retail gallons sold; commercial/industrial customers 41%; motor fuel customers 21%; and agricultural customers 3%. Transport gallons, which are large-scale deliveries to retail customers other than residential, accounted for approximately 5% of Fiscal 2023 retail gallons. With the exception of one customer representing 5.1% of AmeriGas Propane’s consolidated revenues, no other single customer represents more than 5% of AmeriGas Propane’s consolidated revenues.

The ACE program continued to be an important element of AmeriGas Propane’s business in Fiscal 2023. At September 30, 2023, ACE cylinders were available at over 48,000 retail locations throughout the U.S. Sales of our ACE cylinders to retailers are included in commercial/industrial sales. The ACE program enables consumers to purchase or exchange propane cylinders at various retail locations such as home centers, gas stations, mass merchandisers and grocery and convenience stores. In addition, our Cynch propane home delivery service was available in 24 cities as of September 30, 2023. We also supply retailers with large propane tanks to enable them to replenish customers’ propane cylinders directly at the retailers’ locations.

Residential and commercial customers use propane primarily for home heating, water heating and cooking purposes. Commercial users include hotels, restaurants, churches, warehouses and retail stores. Industrial customers use propane to fire furnaces, as a cutting gas and in other process applications. Other industrial customers are large-scale heating accounts and local gas utility customers that use propane as a supplemental fuel to meet peak load deliverability requirements. As a motor fuel, propane is burned in internal combustion engines that power school buses and other over-the-road vehicles, forklifts and stationary engines. Agricultural uses include tobacco curing, chicken brooding, crop drying and orchard heating. In its wholesale operations, AmeriGas Propane principally sells propane to large industrial end-users and other propane distributors.

Retail deliveries of propane are usually made to customers by means of bobtail and rack trucks. Propane is pumped from the bobtail truck, which generally holds 2,400 to 3,000 gallons of propane, into a stationary storage tank on the customer’s premises. AmeriGas Propane owns most of these storage tanks and leases them to its customers. The capacity of these tanks ranges from approximately 120 gallons to approximately 1,200 gallons. AmeriGas Propane also delivers propane in portable cylinders, including ACE and motor fuel cylinders. Some of these deliveries are made to the customer’s location where cylinders are either picked up or replenished in place.

During Fiscal 2023, we made technology and other investments to promote the safety of our employees and the communities we serve. For example, we continued (i) installing cameras in our delivery and service vehicles to facilitate in-cab coaching capabilities, among other functionality, and (ii) installing fall protection towers on rail terminals that are designed to prevent employees from falling during the process of offloading propane into bulk storage.

Propane Supply and Storage

The U.S. propane market has approximately 190 domestic and international sources of supply, including the spot market. Supplies of propane from AmeriGas Propane’s sources historically have been readily available. In recent years, certain geographies experienced varying levels of reduced propane availability as a result of transportation issues within the supply chain. In response to these supply and transportation challenges, AmeriGas Propane utilized a combination of increased regional storage as well as rail and transport supply from different origins to offset localized supply/demand imbalances.

In addition to these factors, the availability and pricing of propane supply has historically been dependent upon, among other things, the severity of winter weather, the price and availability of competing fuels such as natural gas and crude oil, and the

13

amount and availability of exported supply and, to a much lesser extent, imported supply. For more information on risks relating to our supply chain, see “Risk Factors - Risks Relating to Our Supply Chain and Our Ability to Obtain Adequate Quantities of LPG.”

During Fiscal 2023, approximately 97% of AmeriGas Propane’s propane supply was purchased under supply agreements with terms of one to three years. Although no assurance can be given that supplies of propane will be readily available in the future, management currently expects to be able to secure adequate supplies during Fiscal 2024. If supply from major sources were interrupted, however, the cost of procuring replacement supplies and transporting those supplies from alternative locations might be materially higher and, at least on a short-term basis, margins could be adversely affected. In Fiscal 2023, AmeriGas Propane derived approximately 14% of its propane supply from Enterprise Products Operating LLC and approximately 11% of its propane supply from Targa Liquids Marketing and Trade LLC. No other single supplier provided more than 10% of AmeriGas Propane’s total propane supply in Fiscal 2023. In certain geographic areas, however, a single supplier provides more than 50% of AmeriGas Propane’s requirements. Disruptions in supply in these areas could also have an adverse impact on AmeriGas Propane’s margins.

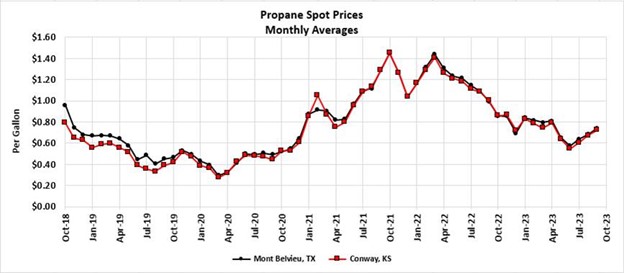

AmeriGas Propane’s supply contracts typically provide for pricing based upon (i) index formulas using the current prices established at a major storage point such as Mont Belvieu, Texas, or Conway, Kansas, or (ii) posted prices at the time of delivery. In addition, some agreements provide maximum and minimum seasonal purchase volume guidelines. The percentage of contract purchases, and the amount of supply contracted for at fixed prices, will vary from year to year. AmeriGas Propane uses a number of interstate pipelines, as well as railroad tank cars, delivery trucks and barges, to transport propane from suppliers to storage and distribution facilities. AmeriGas Propane stores propane at various storage facilities and terminals located in strategic areas across the U.S.

Because AmeriGas Propane’s profitability is sensitive to changes in wholesale propane costs, AmeriGas Propane generally seeks to pass on increases in the cost of propane to customers. There is no assurance, however, that AmeriGas Propane will always be able to pass on product cost increases fully, or keep pace with such increases, particularly when product costs rise rapidly. Product cost increases can be triggered by periods of severe cold weather, supply interruptions, increases in the prices of base commodities, such as crude oil and natural gas, or other unforeseen events. AmeriGas Propane has supply acquisition and product cost risk management practices to reduce the effect of volatility on selling prices. These practices currently include the use of summer storage, forward purchases and derivative commodity instruments, such as propane price swaps. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Market Risk Disclosures.”

The following graph shows the average prices of propane on the propane spot market during the last five fiscal years at Mont Belvieu, Texas, and Conway, Kansas, both major storage areas.

Average Propane Spot Market Prices

14

General Industry Information

Propane is separated from crude oil during the refining process and also extracted from natural gas or oil wellhead gas at processing plants. Propane is normally transported and stored in a liquid state under moderate pressure or refrigeration for economy and ease of handling in shipping and distribution. When the pressure is released or the temperature is increased, it is usable as a flammable gas. Propane is colorless and odorless; an odorant is added to allow for its detection. Propane is considered a clean alternative fuel under the Clean Air Act Amendments of 1990.

Competition

Propane competes with other sources of energy, some of which are less costly for equivalent energy value. Propane distributors compete for customers with suppliers of electricity, fuel oil and natural gas, principally on the basis of price, service, availability and portability. Electricity is generally more expensive than propane on a Btu equivalent basis, but the convenience and efficiency of electricity make it an attractive energy source for consumers and developers of new homes. Fuel oil, which is also a major competitor of propane, is a less environmentally attractive energy source. Furnaces and appliances that burn propane will not operate on fuel oil, and vice versa, and, therefore, a conversion from one fuel to the other requires the installation of new equipment. Propane serves as an alternative to natural gas in rural and suburban areas where natural gas is unavailable or portability of product is required. Natural gas is generally a significantly less expensive source of energy than propane, although in areas where natural gas is available, propane is used for certain industrial and commercial applications and as a standby fuel during interruptions in natural gas service. The gradual expansion of the nation’s natural gas distribution systems has resulted in the availability of natural gas in some areas that previously depended upon propane. However, natural gas pipelines are not present in many areas of the country where propane is sold for heating and cooking purposes.

For motor fuel customers, propane competes with gasoline, diesel fuel, electric batteries, fuel cells and, in certain applications, LNG and compressed natural gas. Wholesale propane distribution is a highly competitive, low margin business. Propane sales to other retail distributors and large-volume, direct-shipment industrial end-users are price sensitive and frequently involve a competitive bidding process.

Retail propane industry volumes have been flat for several years and no or modest growth in total demand is foreseen in the next several years. Therefore, AmeriGas Propane’s ability to grow within the industry is dependent on the success of its sales and marketing programs designed to attract and retain customers, the success of business transformation initiatives, its ability to achieve internal growth, which includes the continuation of ACE, Cynch and National Accounts (through which multi-location propane users enter into a single AmeriGas Propane supply agreement rather than agreements with multiple suppliers), and its ability to acquire other retail distributors. The failure of AmeriGas Propane to retain and grow its customer base would have an adverse effect on its long-term results.

The domestic propane retail distribution business is highly competitive. AmeriGas Propane competes in this business with other large propane marketers, including other full-service marketers, and thousands of small independent operators. Some farm cooperatives, rural electric cooperatives and fuel oil distributors include propane distribution in their businesses and AmeriGas Propane competes with them as well. The ability to compete effectively depends on providing high quality customer service, maintaining competitive retail prices and controlling operating expenses. AmeriGas Propane also offers customers various payment and service options, including guaranteed price programs, fixed price arrangements and pricing arrangements based on published propane prices at specified terminals.

In Fiscal 2023, AmeriGas Propane’s retail propane sales totaled approximately 820 million gallons. Based on the most recent annual survey by the Propane Education & Research Council, 2022 domestic retail propane sales (annual sales for other than chemical uses) in the U.S. totaled approximately 9.8 billion gallons. Based on LP-GAS magazine rankings, 2022 sales volume of the ten largest propane distribution companies (including AmeriGas Propane) represented approximately 32% of domestic retail propane sales.

Properties

As of September 30, 2023, AmeriGas Propane owned approximately 87% of its nearly 525 local offices throughout the country. The transportation of propane requires specialized equipment. The trucks and railroad tank cars utilized for this purpose carry specialized steel tanks that maintain the propane in a liquefied state. As of September 30, 2023, the Partnership operated a transportation fleet with the following assets:

15

| Approximate Quantity & Equipment Type | % Owned | % Leased | |||||||||

| 850 | Trailers | 66% | 34% | ||||||||

| 320 | Tractors | 1% | 99% | ||||||||

| 650 | Railroad tank cars | 0% | 100% | ||||||||

| 2,460 | Bobtail trucks | 4% | 96% | ||||||||

| 285 | Rack trucks | 9% | 91% | ||||||||

| 2,910 | Service and delivery trucks | 11% | 89% | ||||||||

Other assets owned at September 30, 2023 included approximately 909,000 stationary storage tanks with typical capacities of more than 120 gallons, approximately 4.7 million portable propane cylinders with typical capacities of 1 to 120 gallons, 21 terminals and 11 transflow units.

Trade Names, Trade and Service Marks

AmeriGas Propane markets propane and other services principally under the “AmeriGas®,” “America’s Propane Company®,” and “Cynch®” trade names and related service marks. AmeriGas Propane owns, directly or indirectly, all the right, title and interest in the “AmeriGas” name and related trade and service marks. AmeriGas Polska Sp. z.o.o. has an exclusive, royalty-free license from AmeriGas Propane to use the “AmeriGas®” name and related service marks in Poland and Germany and with respect thereto on the Internet. The term of the license is in perpetuity.

Seasonality

Because many customers use propane for heating purposes, AmeriGas Propane’s retail sales volume is seasonal. During Fiscal 2023, approximately 63% of the Partnership’s retail sales volume occurred, and substantially all of AmeriGas Propane’s operating income was earned, during the peak heating season from October through March. As a result of this seasonality, revenues are typically higher in AmeriGas Propane’s first and second fiscal quarters (October 1 through March 31). Cash receipts are generally greatest during the second and third fiscal quarters when customers pay for propane purchased during the winter heating season. For more information on the risks associated with the seasonality of our business, see “Risk Factors - Our business is seasonal and decreases in the demand for our energy products and services because of warmer-than-normal heating season weather or unfavorable weather conditions may adversely affect our results of operations.”

Sales volume for AmeriGas Propane traditionally fluctuates from year-to-year in response to variations in weather, prices, competition, customer mix and other factors, such as conservation efforts and general economic conditions. For information on national weather statistics, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Government Regulation

AmeriGas Propane is subject to various federal, state and local environmental, health, data privacy, safety and transportation laws and regulations governing the storage, distribution and transportation of propane and the operation of bulk storage propane terminals.

Environmental

Generally, applicable environmental laws impose limitations on the discharge of pollutants, establish standards for the handling of solid and hazardous substances, and require the investigation and cleanup of environmental contamination. These laws include, among others, the Resource Conservation and Recovery Act, CERCLA, the Clean Air Act, the Clean Water Act, the Homeland Security Act of 2002, the Emergency Planning and Community Right-to-Know Act, comparable state statutes and any applicable amendments. The Partnership incurs expenses associated with compliance with its obligations under federal and state environmental laws and regulations, and we believe that the Partnership is in material compliance with its obligations. The Partnership maintains various permits that are necessary to operate its facilities, some of which may be material to its operations. AmeriGas Propane continually monitors its operations with respect to potential environmental issues, including changes in legal requirements.

AmeriGas Propane is investigating and remediating contamination at a number of present and former operating sites in the U.S., including sites where its predecessor entities operated MGPs. CERCLA and similar state laws impose joint and several liability on certain classes of persons considered to have contributed to the release or threatened release of a “hazardous substance” into the environment without regard to fault or the legality of the original conduct. Propane is not a hazardous substance within the meaning of CERCLA.

16

Health and Safety

AmeriGas Propane is subject to the requirements of OSHA and comparable state laws that regulate the protection of the health and safety of our workers. These laws require the Partnership, among other things, to maintain information about materials utilized, stored, transported, or sold, in accordance with OSHA’s Hazard Communications Standard. Certain portions of this information must be provided to employees, federal and state and local governmental authorities, emergency responders, commercial and industrial customers and local citizens in accordance with the Environmental Protection Agency’s Emergency Planning and Community Right-to-Know Act requirements.

All states in which AmeriGas Propane operates have adopted fire and life safety codes that regulate the storage, distribution, and use of propane. In some states, these laws are administered by state agencies, and in others they are administered on a municipal level. AmeriGas Propane conducts training programs to help ensure that its operations comply with applicable governmental regulations. With respect to general operations, AmeriGas Propane is subject in all jurisdictions in which it operates to rules and procedures governing the safe handling of propane, including those established by National Fire Protection Association (“NFPA”) in the Liquefied Petroleum Gas Code (NFPA 58) and National Fuel Gas Code (NFPA 54), the International Code Council’s International Fuel Gas Code and International Fire Code, as well as various state and local codes. Management believes that the policies and procedures currently in effect at all of its facilities for the handling, storage, distribution and use of propane are consistent with industry standards and are in compliance, in all material respects, with applicable laws and regulations.

With respect to the transportation of propane, AmeriGas Propane is subject to regulations promulgated under federal legislation, including the Federal Motor Carrier Safety Regulations and Pipeline Hazardous Materials Regulations which fall under the enforcement and supervision of the DOT, Pipeline Hazardous Materials Safety Administration, Federal Railroad Administration, Federal Motor Carrier Safety Administration, and the Federal Aviation Administration. AmeriGas Propane facilities and containers are equally regulated by these agencies regarding security standards as well as the Cybersecurity and Infrastructure Security Agency’s Chemical Facility Anti-Terrorism Standards. AmeriGas Propane’s programs related to the transportation and security of hazardous materials are regularly inspected and meet all applicable standards and regulations.

AmeriGas Propane maintains jurisdictional pipeline systems as defined by the Transportation of Natural and Other Gas by Pipeline: Minimum Federal Safety Standards as regulated by the Pipeline Hazardous Materials Safety Administration and multiple State Public Utility Commissions under the authority and authorization of the Pipeline Hazardous Materials Safety Administration. These pipeline safety regulations apply to, among other things, propane gas systems that supplies 10 or more residential customers or two or more commercial customers from a single source and to a propane gas system any portion of which is located in a public place. The DOT’s pipeline safety regulations require operators of all gas systems to provide operator qualification standards and training and written instructions for employees and third-party contractors working on covered pipelines and facilities, establish written procedures to minimize the hazards resulting from gas pipeline emergencies, and conduct and keep records of inspections and testing. Operators are subject to the Pipeline Safety Improvement Act of 2002. Management believes that the procedures currently in effect at all of AmeriGas Propane’s facilities for the handling, storage, transportation and distribution of propane are consistent with industry standards and are in compliance, in all material respects, with applicable laws and regulations.

Climate Change

There continues to be increased legislative and regulatory activity related to climate change and the contribution of GHG emissions, most notably carbon dioxide, to global warming. Because propane is considered a clean alternative fuel under the federal Clean Air Act Amendments of 1990, the Partnership believes this provides it with a competitive advantage over other sources of energy, such as fuel oil and coal. At the same time, however, increasing regulations of GHG emissions, especially in the transportation and building sectors, could restrict the use of fossil fuels and could impose significant additional costs on AmeriGas Propane, its suppliers, its vendors and its customers. There has been an increase in state initiatives aimed at regulating GHG emissions, including the California Low Carbon Fuel Standard, the Washington Cap and Invest Program and the New York Climate Leadership and Community Protection Act. Compliance with these types of regulations may increase our operating costs if we are unable to pass on these costs to our customers.

Employees

The Partnership does not directly employ any persons responsible for managing or operating the Partnership. The General Partner provides these services and is reimbursed for its direct and indirect costs and expenses, including all compensation and benefit costs. At September 30, 2023, the General Partner had approximately 5,160 employees, including more than 100 part-time, seasonal and temporary employees, working on behalf of the Partnership. UGI also performs, and is reimbursed for, certain financial and administrative services on behalf of the Partnership and AmeriGas OLP.

17

UGI INTERNATIONAL

UGI International, through its subsidiaries and affiliates, conducts an LPG distribution business in 17 countries throughout Europe (Austria, Belgium, the Czech Republic, Denmark, Finland, France, Hungary, Italy, Luxembourg, the Netherlands, Norway, Poland, Romania, Slovakia, Sweden, Switzerland and the United Kingdom). Based on reported market volumes for 2022, which is the most recent information available, UGI International believes that it is the largest distributor of LPG in France, Austria, Belgium, Denmark and Luxembourg and one of the largest distributors of LPG in Norway, Poland, the Czech Republic, Slovakia, the Netherlands, Sweden and Switzerland.

During Fiscal 2023, we made significant progress on our strategic decision to exit the energy marketing business at UGI International. In Fiscal 2023, we divested of our energy marketing business in the United Kingdom and Belgium. On October 1, 2023, we divested substantially all of our energy marketing business in France. We also continue to make significant progress on the wind-down of our energy marketing business in the Netherlands.

Products, Services and Marketing

LPG Distribution Business

During Fiscal 2023, UGI International sold approximately 900 million gallons of LPG throughout Europe. UGI International operates under six distinct LPG brands, and its customer base primarily consists of residential, commercial, industrial, agricultural, wholesale and automobile fuel (“autogas”) customers that use LPG for space heating, cooking, water heating, motor fuel, leisure activities, crop drying, irrigation, construction, power generation, manufacturing and as an aerosol propellant. For Fiscal 2023, approximately 50% of UGI International’s LPG volume was sold to commercial and industrial customers, 15% was sold to residential, 9% was sold to agricultural and 26% was sold to wholesale and other customers (including autogas). UGI International supplies LPG to its customers in small, medium and large bulk tanks at their locations. In addition to bulk sales, UGI International sells LPG in cylinders through retail outlets, such as supermarkets, individually owned stores and gas stations and directly to businesses that operate LPG-powered forklifts. Sales of LPG are also made to service stations to fuel vehicles that run on LPG. UGI International’s Fiscal 2023 LPG sales were attributed to bulk, cylinder, wholesale and autogas. For Fiscal 2023, no single customer represented more than 5% of UGI International’s revenues.

Bulk

Approximately 62% of UGI International’s Fiscal 2023 LPG sales (based on volumes) were attributed to bulk customers. UGI International classifies its bulk customers as small, medium or large bulk, depending upon volume consumed annually at the customer locations. Based on volumes consumed, small bulk customers are primarily residential and small business users, such as restaurants, that use LPG mainly for heating and cooking. Medium bulk customers consist mainly of large residential housing developments, hospitals, hotels, municipalities, medium-sized industrial enterprises and poultry brooders. Large bulk customers include agricultural customers (including crop drying) and companies that use LPG in their industrial processes. UGI International had approximately 492,000 bulk LPG customers and sold 557 million gallons of bulk LPG during Fiscal 2023.

Cylinder

Approximately 15% of UGI International’s Fiscal 2023 LPG sales (based on volumes) were attributed to cylinder customers. UGI International sells LPG in both steel and composite cylinders and typically owns the cylinders in which the LPG is sold. The principal end-users of cylinders are residential customers who use LPG for domestic applications, such as cooking and heating. Non-residential uses include fuel for forklift trucks, road construction and welding. At September 30, 2023, UGI International had more than 20 million cylinders in circulation and sold approximately 137 million gallons of LPG in cylinders during Fiscal 2023. UGI International also delivers LPG to wholesale and retail customers in cylinders, including through the use of vending machines.

Wholesale, Autogas and Other Services

Approximately 19% of UGI International’s Fiscal 2023 LPG sales (based on volumes) were to wholesale customers (including small competitors and large industrial customers), and approximately 4% of Fiscal 2023 LPG sales (based on volumes) were to autogas customers. UGI International also provides logistics, storage and other services to third-party LPG distributors.

Energy Marketing Business

UGI sold its energy marketing business in the United Kingdom, France and Belgium and continues to make progress on the wind-down of its energy marketing business in the Netherlands. For further information, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Executive Overview – Recent Developments.”

18

LPG Supply, Storage and Transportation

UGI International is typically party to term contracts, with approximately 45 different suppliers, including producers and international oil and gas trading companies, to meet LPG supply requirements throughout Europe. LPG supply is transported via rail and sea, and by road for shorter distances. Agreements are generally one-year terms with pricing based on internationally quoted market prices. Additionally, LPG is purchased on the European spot markets to manage supply needs. In certain geographic areas, such as the U.K. and Italy, a single supplier may provide nearly 50% or more of UGI International’s requirements. Because UGI International’s profitability is sensitive to changes in wholesale LPG costs, UGI International generally seeks to pass on increases in the cost of LPG to its customers. There can be no assurance, however, that UGI International will always be able to pass on product cost increases fully, or keep pace with such increases, particularly when product costs rise rapidly. Product cost increases can be triggered by periods of severe cold weather, supply interruptions, increases in the prices of base commodities such as crude oil and natural gas, or other unforeseen events.

The significant increase in European natural gas prices have resulted in refineries substituting a portion of their natural gas refinery fuels with LPG, leading to a decrease in some areas in the availability of LPG. In addition, gas processing plants supplying the United Kingdom and Norway markets are injecting LPG into the natural gas grid, decreasing the overall supply of LPG from the gas processing plants.

UGI International stores LPG at various storage facilities and terminals located across Europe and has interests in both primary storage facilities and secondary storage facilities. LPG stored in primary storage facilities is transported by rail and road to secondary storage facilities where LPG is loaded into cylinders or trucks equipped with tanks and then is delivered to customers. UGI International also manages an extensive logistics and transportation network and has access to seaborne import facilities.

UGI International transports LPG to customers primarily through outsourced transportation providers to serve both bulk and cylinder markets. UGI International has long-term relationships with many providers of logistics and transportation services in most of its markets, and is not dependent on the services of any single transportation provider.

Trade Names, Trade and Service Marks

UGI International protects its intellectual property rights through tradenames, trade and service marks and foreign intellectual property laws. UGI International and its subsidiaries utilize a variety of tradenames, including, but not limited to, AmeriGas (Poland), Antargaz, AvantiGas, FLAGA, Kosan Gas and UniverGas, and related service marks to market its LPG products and services and energy marketing services. UGI International and its subsidiaries currently have tradenames, trade and service marks registered in various countries. UGI International’s trademarks, tradenames and other proprietary rights are valuable assets and we believe that they have significant value in the marketing of our products and services.

Competition and Seasonality

The LPG markets in western and northern Europe are mature, with modest declines in total demand due to competition with other fossil fuels and other energy sources, conservation and macroeconomic conditions. Sales volumes are affected principally by the severity of the weather and customer migration to alternative energy forms, including natural gas, electricity, heating oil and wood. High LPG prices also may result in slower than expected growth due to customer conservation and customers seeking less expensive alternative energy sources. Conversely, high natural gas prices versus LPG prices over a period of time will result in customers seeking to migrate to LPG. In addition, government policies and incentives that favor alternative energy sources, such as heat pumps as well as wind and solar sources, can result in customers migrating to energy sources other than LPG. In addition to price, UGI International competes for customers in its various markets based on contract terms. UGI International competes locally as well as regionally in many of its service territories. Additionally, particularly in France, although UGI International supplies certain supermarket chains, it also competes with some of these supermarket chains that affiliate with LPG distributors to offer their own brands of cylinders. UGI International seeks to increase demand for its LPG cylinders through marketing and product innovations, such as the use of automatic vending machines.

Because many of UGI International’s customers use LPG for heating, sales volumes are affected principally by the severity of the temperatures during the heating season months and traditionally fluctuates from year-to-year in response to variations in weather, prices and other factors, such as conservation efforts and the economic environment. During Fiscal 2023, approximately 60% of UGI International’s retail sales volumes occurred during the peak heating season from October through March. As a result of this seasonality, revenues are typically higher in UGI International’s first and second fiscal quarters (October 1 through March 31). For historical information on weather statistics for UGI International, see ‘‘Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

19

Government Regulation

UGI International’s business is subject to various laws and regulations at the country and local levels, as well as at the EU level, with respect to matters such as protection of the environment, the storage, transportation and handling of hazardous materials and flammable substances (including the Seveso II Directive), regulations specific to bulk tanks, cylinders and piped networks, competition, pricing, regulation of contract terms, anti-corruption (including the U.S. Foreign Corrupt Practices Act, Sapin II and the U.K. Bribery Act), data privacy and protection, and the safety of persons and property.

Environmental