UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

Preliminary Proxy Statement |

|

|

|

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

|

☒ |

|

Definitive Proxy Statement |

|

|

|

|

|

|

|

Definitive Additional Materials |

|

|

|

|

|

|

|

Soliciting Material Pursuant to §240.14a-12 |

|

|

|

|

QUICKLOGIC CORPORATION

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

|

|

|

|

|

|

|

☒ |

No fee required. |

|

|

|

|

|

|

|

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

|

|

|

|

|

|

|

(1) |

Title of each class of securities to which transaction applies: N/A |

|

|

|

|

(2) |

Aggregate number of securities to which transaction applies: N/A |

|

|

|

|

(3) |

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): N/A |

|

|

|

|

(4) |

Proposed maximum aggregate value of transaction: N/A |

|

|

|

|

(5) |

Total fee paid: N/A |

|

|

|

|

|

|

|

|

|

|

|

Fee paid previously with preliminary materials. |

|

|

|

|

|

|

|

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

|

|

|

|

|

|

|

(1) |

Amount Previously Paid: N/A |

|

|

|

|

(2) |

Form, Schedule or Registration Statement No.: N/A |

|

|

|

|

(3) |

Filing Party: N/A |

|

(4) |

Date Filed: N/A |

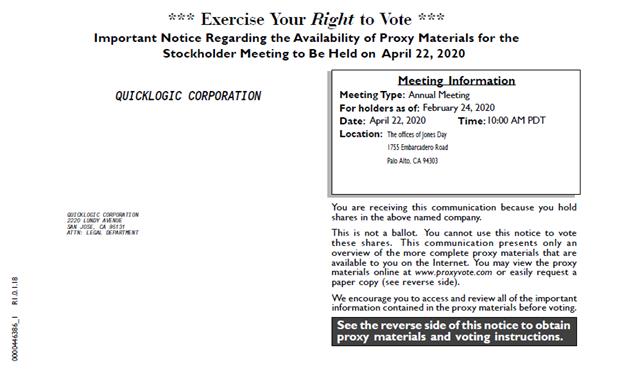

QUICKLOGIC CORPORATION

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON WEDNESDAY, APRIL 22, 2020

The Annual Meeting of Stockholders of QUICKLOGIC CORPORATION, a Delaware corporation (“QuickLogic” or the Company), will be held at the offices of Jones Day, located at 1755 Embarcadero Road, Palo Alto, California 94303, on Wednesday, April 22, 2020, at 10:00 a.m., local time, for the following purposes:

|

1 |

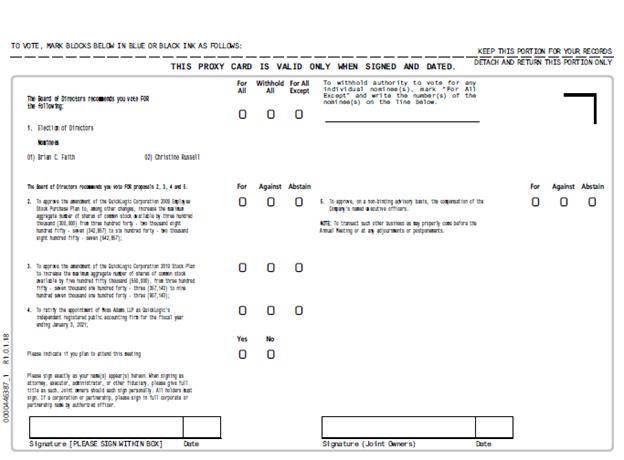

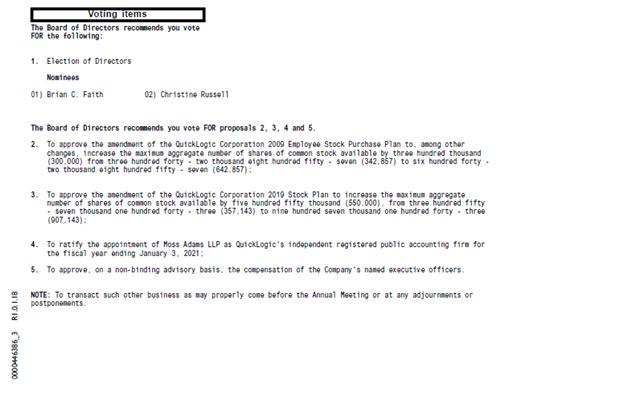

To elect two Class III directors to serve for a term of three years expiring on the date on which our Annual Meeting of Stockholders is held in 2023; |

|

4 |

To ratify the appointment of Moss Adams LLP as QuickLogic’s independent registered public accounting firm for the fiscal year ending January 3, 2021; |

|

5 |

To approve, on a non-binding advisory basis, the compensation of QuickLogic’s named executive officers; |

and

|

6 |

To transact such other business as may properly come before the Annual Meeting, or at any and all adjournments or postponements. |

The foregoing items of business are more fully described in the Proxy Statement accompanying this Notice. Only stockholders of record at the close of business on February 24, 2020 are entitled to notice of and to vote at the Annual Meeting and any adjournments or postponements thereof.

Again this year, we are using the U.S. Securities and Exchange Commission rule that allows companies to furnish their proxy materials over the Internet. This allows us to mail our stockholders a notice instead of a paper copy of the Proxy Statement and our 2019 Annual Report on Form 10-K. The notice contains instructions on how our stockholders may access our Proxy Statement and Annual Report over the Internet and how our stockholders can receive a paper copy of our proxy materials, including the Proxy Statement, our 2019 Annual Report and a proxy card. Stockholders who do not receive a notice, including stockholders who have previously requested to receive paper copies of proxy materials, will receive a paper copy of the proxy materials by mail unless they have previously requested delivery of proxy materials electronically. Employing this distribution process will help us to conserve natural resources and reduce the costs of printing and distributing our proxy materials. The Proxy Statement and form of proxy are being distributed and made available on or about March 13, 2020.

All stockholders are cordially invited to attend the Annual Meeting in person.

|

For the Board of Directors, |

San Jose, California

March 13, 2020

YOUR VOTE IS IMPORTANT

WHETHER OR NOT YOU PLAN TO ATTEND THE ANNUAL MEETING, WE HOPE YOU WILL VOTE AS SOON AS POSSIBLE. YOU MAY VOTE BY PROXY OVER THE INTERNET OR BY TELEPHONE, OR, IF YOU RECEIVED PAPER COPIES OF THE PROXY MATERIALS BY MAIL, BY FOLLOWING THE INSTRUCTIONS ON THE PROXY CARD OR VOTING INSTRUCTION CARD. VOTING OVER THE INTERNET, BY TELEPHONE OR BY WRITTEN PROXY OR VOTING INSTRUCTION CARD WILL ENSURE YOUR REPRESENTATION AT THE ANNUAL MEETING REGARDLESS OF WHETHER YOU ATTEND IN PERSON.

2

|

|

|

|

|

|

|

|

Page |

|

|

|

|

1 |

|

|

4 |

|

|

9 |

|

|

Proposal Two- Approve the Amendment to the 2009 Employee Stock Purchase Plan |

17 |

|

Proposal Three – Approve the Amendment to the 2019 Stock Plan |

22 |

|

Proposal Four - Ratification of Appointment of Independent Registered Public Accounting Firm |

30 |

|

32 |

|

|

33 |

|

|

35 |

|

|

42 |

|

|

43 |

|

|

44 |

|

|

46 |

|

|

46 |

|

|

46 |

|

|

50 |

|

|

51 |

|

|

52 |

|

|

53 |

|

|

|

|

3

QUICKLOGIC CORPORATION

PROXY STATEMENT

FOR ANNUAL MEETING OF STOCKHOLDERS

ABOUT THE ANNUAL GENERAL MEETING

General

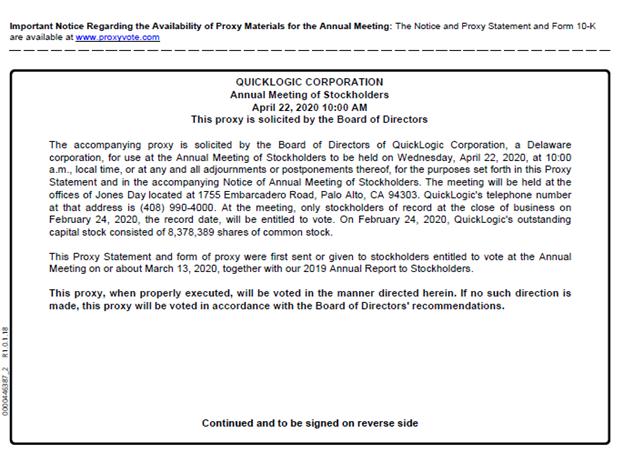

The accompanying proxy is solicited by the Board of Directors of QuickLogic Corporation, a Delaware corporation (“QuickLogic” or the “Company”), for use at the Annual Meeting of Stockholders to be held on Wednesday, April 22, 2020, at 10:00 a.m., local time, and at any and all adjournments or postponements thereof (the “Annual Meeting”), for the purposes set forth in this Proxy Statement and in the accompanying Notice of Annual Meeting of Stockholders. The Annual Meeting will be held at the offices of Jones Day, located at 1755 Embarcadero Road, Palo Alto, California 94303. QuickLogic’s telephone number at that address is (408) 990-4000. At the Annual Meeting, only stockholders of record at the close of business on February 24, 2020, the record date, will be entitled to vote. On February 24, 2020, QuickLogic’s outstanding capital stock consisted of 8,378,389 shares of common stock.

At the Annual Meeting, the stockholders will be asked:

|

|

1 |

To elect two Class III directors to serve for a term of three years expiring on the date on which our Annual Meeting of Stockholders is held in 2023; |

|

|

4 |

To ratify the appointment of Moss Adams LLP as QuickLogic’s independent registered public accounting firm for the fiscal year ending January 3, 2021; |

|

|

5 |

To approve, on a non-binding advisory basis, the compensation of QuickLogic’s named executive officers; and |

|

|

6 |

To transact such other business as may properly come before the Annual Meeting or at any and all adjustments or postponements thereof. |

This Proxy Statement and form of proxy were first provided to stockholders entitled to vote at the Annual Meeting on or about March 13, 2020, together with our 2019 Annual Report to Stockholders.

Board’s Recommendation

Our Board of Directors recommends that you vote:

|

1 |

“ FOR ” the election of the two nominated Class III directors; |

|

2 |

“ FOR ” the approval of the amendment to the QuickLogic Corporation 2009 Employee Stock Purchase Plan; |

|

4 |

“ FOR ” the ratification of the appointment of Moss Adams LLP as the Company’s independent registered public accounting firm for the fiscal year ending January 3, 2021; and |

|

5 |

“ FOR ” the approval, on a non-binding advisory basis, of the compensation of QuickLogic’s named executive officers; |

4

Our management does not intend to present other items of business and knows of no items of business that are likely to be brought before the Annual Meeting, except those described in this Proxy Statement. However, if any other matters should properly come before the Annual Meeting, the proxy holders will have discretionary authority to vote the shares represented by proxies in accordance with their best judgment on the matters.

Voting

Each stockholder is entitled to one vote for each share of common stock held on all matters presented at the Annual Meeting. Stockholders do not have the right to cumulate votes in the election of directors. Voting instructions are included on the notice of availability of proxy materials or voting instruction card.

Properly executed proxies received prior to the meeting, and subsequently not revoked, will be voted in accordance with the instructions on the proxy. Where no instructions are given, proxies will be voted "FOR" the election of the director nominees described herein, “FOR” the approval of the amendment of the 2009 Employee Stock Purchase Plan, “FOR” the approval of the amendment of the 2019 Stock Plan, “FOR” the ratification of the independent registered public accounting firm, and “FOR” the approval, on a non-binding advisory basis, of the compensation of the our named executive officers,.

What’s required to approve each item?

Proposal 1: Election of Directors. Directors of the Company are elected by a plurality of the votes cast in contested and uncontested elections. The election at the Annual Meeting will be uncontested. “Plurality” means that the two individuals who receive the highest number of “FOR” votes will be elected as directors. You may vote either “FOR” or “WITHHOLD” your vote from any one or more of the nominees. Proxy cards specifying that votes should be withheld with respect to one or more nominees will result in those nominees receiving fewer votes but will not count as a vote against the nominees. If you do not instruct your broker how to vote with respect to this item, your broker may not vote your shares with respect to the election of directors. Any shares not voted by a stockholder will be treated as broker non-votes, and broker non-votes will have no effect on the results of the election of directors.

Proposal 2: Approval of Amendment of the Company's 2009 Employee Stock Purchase Plan. The affirmative vote of a majority of shares of common stock present (in person or by proxy) at the Annual Meeting and entitled to vote is required for the approval of the amendment of the Company's 2009 Employee Stock Purchase Plan to, among other changes, increase the maximum aggregate number of shares of common stock available by three hundred thousand (300,000), from three hundred forty-two thousand eight hundred fifty-seven (342,857) to six hundred forty-two thousand eight hundred fifty-seven (642,857). Abstentions will have the effect of a vote against the proposal and broker non-votes will have no effect.

Proposal 3: Approval of Amendment of the Company's 2019 Stock Plan. The affirmative vote of a majority of shares of common stock present (in person or by proxy) at the Annual Meeting and entitled to vote is required for the approval of the amendment of the Company's 2019 Stock Plan to increase the maximum aggregate number of shares of common stock available by five hundred fifty thousand (550,000), from three hundred fifty-seven thousand one hundred forty-three (357,143) to nine hundred seven thousand one hundred forty-three (907,143). Abstentions will have the effect of a vote against the proposal and broker non-votes will have no effect.

Proposal 4: Ratification of Appointment of Independent Registered Public Accounting Firm . Ratification of the appointment of Moss Adams LLP (“Moss Adams”) as the Company’s independent registered public accounting firm for the fiscal year ending January 3, 2021 will require the affirmative vote of a majority of shares of common stock present (in person or by proxy) at the Annual Meeting and entitled to vote on the proposal. An abstention will have the effect of a vote against the ratification. Brokers will have discretionary authority to vote on Proposal 4 and, accordingly, there will be no broker non-votes for this proposal.

Proposal 5: Advisory Vote on Executive Compensation. The affirmative vote of a majority of shares of common stock present (in person or by proxy) at the Annual Meeting and entitled to vote is required for the advisory vote on the compensation of the Company’s named executive officers. Because your vote on this proposal is advisory, it will not be binding on the Board of Directors or the Company. However, the Board of Directors will

5

review the voting results and take them into consideration when making future decisions regarding executive compensation. An abstention will not be counted toward the approval of executive compensation, and the effect of an abstention is the same as a vote against the approval. Broker non-votes will have no effect on the outcome.

Will my shares be voted if I do not provide my proxy?

Under applicable rules, if you hold your shares through a brokerage firm, bank or other nominee, and do not give instructions to that entity, it will still be able to vote your shares with respect to “discretionary” items, but it will not be allowed to vote your shares with respect to “non-discretionary” items. The ratification of Moss Adams as our independent registered public accounting firm (Proposal 4) is considered to be a discretionary item under applicable rules and your brokerage firm, bank or other nominee will be able to vote on that item even if it does not receive instructions from you, so long as it holds your shares in its name. The remaining items of business at the Annual Meeting are “non-discretionary” and if you do not instruct your broker, bank or other nominee how to vote with respect to such proposals, it may not vote with respect to these proposals and those shares will be counted as “broker non-votes.” “Broker non-votes” are shares that are held in “street name” by a brokerage firm, bank or other nominee that indicates on its proxy that it does not have or did not exercise discretionary authority to vote on a particular matter. Please see “What’s required to approve each item?” for information regarding the vote required to approve the matters being considered at the Annual Meeting and the treatment of broker non-votes.

If you hold your shares through our transfer agent, American Stock Transfer and Trust Company, they will not be voted if you do not provide a proxy.

If your shares are held in street name, you must bring an account statement or letter from your bank or brokerage firm showing that you are the beneficial owner of the shares as of the record date in order to be admitted to the Annual Meeting. To be able to vote your shares held in street name at the Annual Meeting, you will need to obtain a legal proxy card from the holder of record.

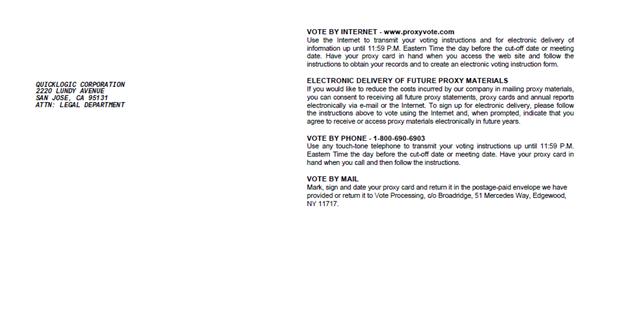

Voting Electronically via the Internet, by Telephone or by Mail

There are three ways to vote by proxy:

By Internet —Stockholders who have received a notice of the availability of the proxy materials by mail may submit proxies over the Internet by following the instructions on the notice. Stockholders who have received the notice of the availability of the proxy materials by e-mail may submit proxies over the Internet by following the instructions included in the e-mail. Stockholders who have received a paper copy of a proxy card or voting instruction card by mail may submit proxies over the Internet by following the instructions on the proxy card or voting instruction card.

By Telephone —Stockholders of record who live in the United States or Canada may submit proxies by telephone by calling 1-800-690-6903 and following the instructions. Stockholders of record who have received a notice of availability of the proxy materials by mail must have the control number that appears on their notice available when voting. Stockholders of record who received notice of the availability of the proxy materials by e-mail must have the control number included in the e-mail available when voting. Stockholders of record who have received a proxy card by mail must have the control number that appears on their proxy card available when voting. Most of the stockholders, who are beneficial owners of their shares living in the United States or Canada and who have received a voting instruction card by mail may vote by phone by calling the number specified on the voting instruction card provided by their broker, trustee or nominee. Those stockholders should check the voting instruction card for telephone voting availability.

By Mail —Stockholders who have received a paper copy of a proxy card or voting instruction card by mail may submit proxies by completing, signing and dating their proxy card or voting instruction card and mailing it in the accompanying pre-addressed envelope.

Important Notice Regarding the Availability of Proxy Materials for the Shareholders Meeting To Be Held on April 22, 2020.

Our proxy materials including our Proxy Statement, Annual Report on Form 10-K and proxy card are available on the Internet and may be viewed free of charge and printed at www.proxydocs.com/QUIK.

6

We have engaged The Proxy Advisory Group, LLC, to assist in the solicitation of proxies and provide related advice and informational support, for a services fee, plus customary disbursements, which are not expected to exceed $15,000 in total. We will also reimburse brokerage firms and other custodians, nominees and fiduciaries for their expenses in forwarding proxy and solicitation materials to stockholders.

Revocability of Proxies

Any proxy given pursuant to this solicitation may be revoked by the person giving it at any time before its use by delivering to our Secretary a written notice of revocation or a duly executed proxy bearing a later date, or by attending the meeting and voting in person. Your presence at the Annual Meeting in and of itself is not sufficient to revoke your proxy. For shares you hold in street name, you may revoke your prior proxy by submitting new voting instructions to your broker or nominee.

Neither Delaware law nor our amended and restated certificate of incorporation provide for appraisal or other similar rights for dissenting stockholders in connection with any of the proposals to be voted upon at the Annual Meeting. Accordingly, our stockholders will have no right to dissent and obtain payment for their shares.

Quorum; Abstentions; Broker Non-Votes

The presence at the Annual Meeting, in person or by proxy, of the holders of at least one-third of the voting power of our stock outstanding on the record date will constitute a quorum. As of the close of business on the record date, there were 8,378,389 shares of our common stock outstanding. Both abstentions and broker non-votes are counted for the purpose of determining the presence of a quorum. For the purpose of determining whether the stockholders have approved matters other than the election of directors (Proposal 1), abstentions are treated as shares present or represented and voting, so abstaining has the same effect as a negative vote. Directors are elected based on a plurality of the votes cast. Shares held by brokers who do not have discretionary authority to vote on a particular matter and who have not received voting instructions from their customers are counted for determining the presence or absence of a quorum for conducting business but are not counted or deemed to be present or represented for the purpose of determining whether stockholders have approved that matter.

Stockholder Nominations and Proposals for Candidates to the Board of Directors

The Nominating and Corporate Governance Committee of our Board of Directors has established policies and procedures, available on our website at http://www.quicklogic.com/corporate/about-us/management, to consider recommendations for candidates to the Board of Directors from stockholders holding either (i) shares of the outstanding voting securities of the Company in an amount equal to at least $2,000 in market value or (ii) 1% of the Company’s outstanding voting securities continuously for at least one-year prior to the date of the submission of the recommendation. Recommendations received after the date that is 120 days prior to the one-year anniversary of the mailing of the previous year’s proxy statement will likely not be considered timely for consideration at that year’s annual meeting.

A stockholder that desires to recommend a candidate for election to the Board of Directors must direct the recommendation in writing to the Nominating and Corporate Governance Committee, care of the Chief Financial Officer, 2220 Lundy Avenue, San Jose, California 95131, and must include the candidate’s name, home and business contact information, detailed biographical data and qualifications and an explanation of the reasons why the stockholder believes this candidate is qualified for service on the Company’s Board of Directors. The stockholder must also provide such other information about the candidate that would be required by the Securities and Exchange Commission (“SEC”) rules to be included in a proxy statement. In addition, the stockholder must include the consent of the candidate and describe any arrangements or undertakings between the stockholder and the candidate regarding the nomination. The stockholder must submit proof of ownership of the requisite number of Company voting securities.

A stockholder that instead desires to nominate a person directly for election to the Board of Directors must meet the deadlines and other requirements set forth in Section 2.4 of the Company’s Bylaws and the rules and regulations of the SEC.

7

Deadlines for Submission of Other Stockholder Proposals

Stockholders are entitled to present proposals for consideration at the next annual meeting of stockholders provided that they comply with the proxy rules promulgated by the SEC and our Bylaws.

Stockholders wishing to present a proposal for inclusion in the proxy statement relating to our 2021 Annual Meeting of Stockholders must submit such proposal to us by the date that is 120 days prior to the one-year anniversary of the date on which this proxy is first mailed, in order to be considered timely for stockholder proposals or nominations to be included in such proxy statement, which date is November 14, 2020. Proposals received after this date will likely not be considered timely for consideration at that year’s annual meeting.

Householding

Householding is a cost-saving procedure used by us and approved by the SEC. Under the householding procedure, we send only one Annual Report and Proxy Statement to stockholders of record who share the same address and last name, unless one of those stockholders notifies us that the stockholder would like a separate Annual Report and Proxy Statement. A stockholder may notify us that the stockholder would like a separate Annual Report and Proxy Statement by telephone at (408) 990-4000 or at the following mailing address: 2220 Lundy Avenue, San Jose, California 95131, Attention: Investor Relations. If we receive such notification that the stockholder wishes to receive a separate Annual Report and Proxy Statement, we will promptly deliver such Annual Report and Proxy Statement. A separate proxy card is included in the materials for each stockholder of record. If you wish to update your participation in householding, beneficial owners should contact their broker and registered shareholders should contact our transfer agent American Stock Transfer & Trust Company or AST at 1 (800) 937-5449.

8

ELECTION OF DIRECTORS

QuickLogic’s Board of Directors (the “Board”) is currently comprised of seven members, divided into three classes with overlapping three-year terms. As a result, a portion of our Board of Directors will be elected each year. Christine Russell, E. Thomas Hart (deceased) and Brian C. Faith have been designated as Class III directors whose terms expire at the 2020 Annual Meeting of Stockholders. Michael R. Farese, Andrew J. Pease, and Daniel A. Rabinovitsj have been designated as Class I directors whose terms expire at the 2021 Annual Meeting of Stockholders, and Arturo Krueger and Gary H. Tauss have been designated as Class II directors whose terms expire at the 2022 Annual Meeting of Stockholders. Any additional directorships resulting from an increase in the number of directors will be distributed among the three classes so that, as nearly as possible, each class will consist of an equal number of directors. There are no family relationships between any of our directors or executive officers.

Nominees for Class III Directors

Two Class III directors are to be elected at this Annual Meeting of Stockholders for a three-year term ending in 2023. Pursuant to action by the Nominating and Corporate Governance Committee, the Board of Directors has nominated Christine Russell and Brian C. Faith. No new director has been nominated to replace E. Thomas Hart, who passed away in December 2019. Unless otherwise instructed, the persons named in the enclosed proxy intend to vote proxies received by them for the election of Christine Russell and Brian C. Faith. QuickLogic expects that Christine Russell and Brian C. Faith will serve if elected. In the event that any nominee is unable or declines to serve as a director at the time of the Annual Meeting, proxies will be voted for a substitute nominee or nominees designated by the Nominating and Corporate Governance Committee of the Board of Directors. The term of office of each person elected as director will continue until such director’s term expires in 2023 or until such director’s successor has been elected and qualified or until such director’s earlier death, resignation or removal.

Required Vote

The two nominees receiving a plurality, or the highest number of affirmative votes of the shares present or represented and entitled to be voted for them, shall be elected directors. Votes withheld from any director are counted for purposes of determining the presence or absence of a quorum for the transaction of business, but have no other legal effect in the election of directors under Delaware law.

Recommendation of the Board of Directors

QUICKLOGIC’S BOARD OF DIRECTORS UNANIMOUSLY RECOMMENDS A

VOTE “FOR” THE CLASS III DIRECTOR NOMINEES LISTED ABOVE.

Directors and Nominees for Director

The following table sets forth information concerning the nominees for Class III director.

Nominees for Class III Director

|

Name |

|

Age |

|

Position |

|

Christine Russell |

|

70 |

|

Director |

|

Brian C. Faith |

|

45 |

|

Director |

Christine Russell has been serving as a member of our Board of Directors since June 2005. On December 23, 2019, Ms. Russell was elected as member of the Board of Directors of AXT, Inc. In July 2018, Ms. Russell was appointed as Chief Financial Officer at PDF Solutions, which offers yield process improvement and manufacturing efficiencies to the semiconductor industry and their supply chain using proprietary AI and data mining software technology. In February 2017, she became a member of the Board of Directors of eGain Corporation, a Nasdaq traded SaaS company providing software for call center and customer support organizations. From May 2015 through March 2018, she served as Chief Financial Officer at UniPixel, Inc., a precision engineered film company whose products include touch-screen films. From May 2014 to March 2015, Ms. Russell served as Chief Financial

9

Officer of Vendavo, Inc., a pricing optimization enterprise software company, which was sold in late 2014 to a private equity firm. From May 2009 to October 2013, Ms. Russell was Chief Financial Officer of Evans Analytical Group (EAG), a leading international provider of materials characterization and microelectronic failure analysis and “release to production” services. From June 2006 to April 2009, Ms. Russell was at Virage Logic Corporation, a provider of advanced intellectual property for the design of integrated circuits, where she served as Executive Vice President of Business Development from September 2008 and as Vice President and Chief Financial Officer from June 2006 to September 2008. Ms. Russell served as Senior Vice President and Chief Financial Officer of OuterBay Technologies, Inc., a privately held software company enabling information lifecycle management for enterprise applications, from May 2005 until February 2006, when OuterBay was acquired by Hewlett-Packard Company. From October 2003 to May 2005, Ms. Russell served as the Chief Financial Officer of Ceva, Inc., a company specializing in semiconductor intellectual property offering digital signal processing cores and application software. Prior to 2005, Ms. Russell served as Chief Financial Officer and in various senior financial management positions with a number of technology companies for a period of more than twenty years. Ms. Russell holds a B.A. degree and an M.B.A. degree from the University of Santa Clara.

Ms. Russell’s extensive executive experience in corporate finance, accounting and operations, and her involvement in governance issues for boards of directors in her role as Chairman Emeritus of the SVDX (Silicon Valley Directors Exchange), an organization that fosters excellence in corporate governance for directors in affiliation with Stanford University and past service as President of the NACD, Silicon Valley Chapter, make her an important asset to the Company. In addition, her career background in semiconductor intellectual property companies provides her with specific industry knowledge.

Brian C. Faith was promoted to Chief Executive Officer and was elected as a director in June 2016 after having served as Vice President of Worldwide Marketing and Vice President of Worldwide Sales & Marketing between 2008 and 2016. Mr. Faith has been with QuickLogic since 1996, and during the last 20 years has held a variety of managerial and executive leadership positions in engineering, product line management, marketing and sales. Mr. Faith has also served as the Chairman of the Marketing Committee for the CE-ATA Organization. He holds a B.S. degree in Computer Engineering from Santa Clara University and was an Adjunct Lecturer at Santa Clara University for Programmable Logic courses.

Mr. Faith’s vast understanding of the semiconductor industry coupled with his in-depth knowledge of the day-to-day operation and strategic direction of the Company makes him an invaluable resource and contributor to the Board.

Incumbent Class I Directors Whose Terms Expire in 2021

|

Name |

|

Age |

|

|

Position |

|

|

Michael R. Farese |

|

|

73 |

|

|

Director |

|

Andrew J. Pease |

|

|

69 |

|

|

Director |

|

Daniel A. Rabinovitsj |

|

|

55 |

|

|

Director |

Michael R. Farese (Ph.D.) has been serving as a member of our Board of Directors since April 2008, and as our Chairman since December 6, 2019. In January 2015, Dr. Farese joined Antenna79, a consumer electronics company creating advanced antenna technology for wireless devices, where he held the position of Chief Scientist until December 2016 when Antenna79 was acquired. From June 2010 to December 2014, Dr. Farese served as Chief Technology Officer and Senior Vice President of Global Engineering at Entropic Communications Inc., a fabless semiconductor company that designs, develops and markets system solutions to enable connected home entertainment. From September 2007 to May 2010, he was President and Chief Executive Officer and member of the Board of Directors of BitWave Semiconductor, Inc., a fabless semiconductor company and innovator of programmable radio frequency ICs. From September 2005 to September 2007, Dr. Farese was Senior Vice President, Engineering, of Palm, Inc., a leading mobile products company. Dr. Farese also served as President and Chief Executive Officer of WJ Communications, a radio frequency (RF) semiconductor company, from March 2002 to July 2005 and President and CEO of Tropian Inc., a developer of high efficiency RF ASICs for 2.5 and 3G cellular phones, from October 1999 to March 2002. Prior to that time, Dr. Farese held senior management positions at Motorola Corp., Ericsson Inc., Nokia Corp. and ITT Corp. Dr. Farese also held management positions at AT&T

10

Corp. and Bell Laboratories, Inc. and has been in the telecommunications and semiconductor industry for more than 40 years. Dr. Farese also served on the board of PMC-Sierra, Inc., an Internet infrastructure semiconductor solution provider, from May 2006 until its acquisition in January 2016 by Microsemi Corp. Dr. Farese holds a B.S. degree and a Ph.D. in Electrical Engineering from Rensselaer Polytechnic Institute. He also received his M.S. degree in Engineering from Princeton University.

Dr. Farese has extensive executive experience and knowledge of the wireless industry, cellular handsets and wireless devices, and the use of semiconductors for the wireless industry. His business acumen and strong technical and strategic planning skills bring an invaluable perspective to the Board.

Andrew J. Pease has been serving as a member of our Board of Directors since April 2011. He joined QuickLogic in November 2006 and served as our President and Chief Executive Officer from January 2011 to his retirement in June 2016, and as our President from March 2009 to his retirement in June 2016. From November 2006 to March 2009, Mr. Pease served as our Vice President of Worldwide Sales. From July 2003 to June 2006, Mr. Pease was Senior Vice President of Worldwide Sales at Broadcom Corporation, a global leader in semiconductors for wired and wireless communications. From March 2000 to July 2003, Mr. Pease was Vice President of Sales at Syntricity, Inc., a company providing software and services to better manage semiconductor production yields and improve design-to-production processes. From 1984 to 1996, Mr. Pease served in a number of sales positions at Advanced Micro Devices, or AMD, a global semiconductor manufacturer, where his last assignment was Group Director, Worldwide Headquarters Sales and Operations. Mr. Pease previously held Vice President of Sales positions at Integrated Systems Inc., an embedded software manufacturer (1996-1997), and Vantis Corporation, a programmable logic subsidiary of AMD (1997-1999). Mr. Pease holds a B.S. degree from the United States Naval Academy and an M.S. in computer science from the Naval Postgraduate School in Monterey, California.

Mr. Pease has many years of executive experience in the semiconductor industry, primarily in sales and operations. His vast understanding of the semiconductor industry coupled with his in-depth knowledge of the day-to-day operation and strategic direction of the Company makes him an invaluable resource and contributor to the Board.

Daniel A. Rabinovitsj has been serving as a member of our Board of Directors since October 2014. In August 2018, Mr. Rabinovitsj joined Facebook, a social networking company. From April 2018, he has been serving as board member in NanoSemi, Inc. a startup company, which develops intellectual property based upon machine learning to improve communication and other systems. Mr. Rabinovitsj served as Chief Operating Officer of Ruckus Wireless, Inc., a global supplier of advanced wireless systems for the mobile Internet infrastructure market, from October 2014 until its acquisition by ARRIS International plc in December 2017. Mr. Rabinovitsj served as President of ARRIS International plc. From 2011 to September 2014, Mr. Rabinovitsj served as Senior Vice President of Qualcomm Atheros, Inc.’s wired and wireless networking and small cell infrastructure business. Prior to Qualcomm Atheros, Mr. Rabinovitsj served in a number of executive management positions at companies including Atheros Communications, NXP Semiconductors, ST Ericsson, and Silicon Labs. Mr. Rabinovitsj received an M.A. in Asian Studies and a B.A. in Philosophy from the University of Texas at Austin.

Mr. Rabinovitsj has over twenty-five years of experience in the semiconductor industry where he has spent considerable time focusing on communications and networking. Drawing from his extensive background, he is able to provide invaluable insights into the mobile market, the Company’s focused market. These insights coupled with his international business experience make Mr. Rabinovitsj a significant and respected contributor to the Board.

Incumbent Class II Directors Whose Terms Expire in 2022

|

Name |

|

Age |

|

|

Position |

|

|

Arturo Krueger |

|

|

80 |

|

|

Director |

|

Gary Tauss |

|

|

65 |

|

|

Director |

Arturo Krueger has been as a member of our Board of Directors since September 2004. Mr. Krueger has more than 40 years of experience in systems architecture, semiconductor design and development, operations and marketing, as well as general management. Since February 2001, Mr. Krueger has been a consultant to automobile

11

manufacturers and to semiconductor companies serving the automotive and telecommunication markets. Mr. Krueger was Corporate Vice President and General Manager of Motorola’s Semiconductor Products Sector for Europe, the Middle East and Africa from January 1998 until February 2001. Mr. Krueger was the Strategic and Technology/Systems advisor to the President of Motorola’s Semiconductor Products Sector from 1996 until January 1998. In addition, Mr. Krueger was the Director of the Advanced Architectural and Design Automation Lab at Motorola. Mr. Krueger served as a director of Marvell Technology Group Ltd., a semiconductor provider of high-performance analog, mixed-signal, digital signal processing and embedded microprocessor integrated circuits, from August 2005 to January 1, 2017. He holds an M.S. degree in Electrical Engineering from the Institute of Technology in Switzerland, and has studied Advanced Computer Science at the University of Minnesota.

Mr. Krueger’s extensive executive experience in and knowledge of multiple facets of the semiconductor industry give him insights into the challenges facing the Company and his knowledge of the European market provides the Board with a global perspective.

Gary H. Tauss has been serving as a member of our Board of Directors since June 2002. Mr. Tauss has also been serving as a board member for Hootsuite Inc., a social media dashboard company, since January 2010. In January 2017, Mr. Tauss joined the board of NetForecast, Inc., an auditing firm which audits ISP data usage meter systems. From January 2010 to March 2014, Mr. Tauss served as the Executive Director and Chief Executive Officer of BizTech, a not-for-profit technology-focused business incubator. From October 2006 until February 2008, Mr. Tauss served as President and Chief Executive Officer of Mobidia Technology, Inc., a provider of performance management software that enables wireless operators to provide users with high-quality mobile content. From May 2005 until the sale of its assets to Transaction Network Services, Inc. in March 2006, Mr. Tauss served as President, Chief Executive Officer and director of InfiniRoute Networks Inc., a provider of software peering services for wireline and wireless carriers. From October 2002 until April 2005, Mr. Tauss served as President and Chief Executive Officer of LongBoard, Inc., a company specializing in fixed-to-mobile convergence application software for leading carriers and service providers. From August 1998 until June 2002, Mr. Tauss was President, Chief Executive Officer and a director of TollBridge Technologies, Inc., a developer of voice-over-broadband products. Prior to co-founding TollBridge, Mr. Tauss was Vice President and General Manager of Ramp Networks, Inc., a provider of Internet security and broadband access products, with responsibility for engineering, customer support and marketing. Mr. Tauss earned both a B.S. and an M.B.A. degree from the University of Illinois.

Mr. Tauss has a strong executive background with technology companies providing products for the mobile market. His in-depth understanding of the important attributes of products for the mobile market make him an invaluable resource as QuickLogic develops and markets devices for the mobile market.

Board Leadership Structure; Lead Independent Director

The Board of Directors does not currently have a policy on whether the roles of Chief Executive Officer and Chairman may be filled by one individual. This allows the Board flexibility to better address the leadership needs of the Company from time to time as it deems appropriate. We currently separate the positions of Chief Executive Officer and Chairman of the Board. Mr. Brian C. Faith is our President and Chief Executive Officer and Dr. Farese was elected as our non-employee Chairman of the Board on December 6, 2019 to replace Mr. E. Thomas Hart, who passed away on December 3, 2019.

Dr. Farese has served as the Chairman of the Nominating and Corporate Governance Committee of our Board since August 2014 and as our Lead Independent Director since January 2015. The responsibilities of the Lead Independent Director include presiding at all meetings of the Board at which the Chairman is not present; calling and presiding at all executive sessions of the independent directors; approving the agenda and materials for meetings of the independent directors; consulting with the Chairman regarding Board meeting agendas, materials, and proposed meeting calendars and schedules; collaborating with the Chairman and acting as liaison between the Chairman and the independent directors; and serving as the Board’s liaison for consultation and communication with stockholders as appropriate, including at the request of major stockholders.

Board’s Oversight of Risk Management

The Board has an active role, as a whole and also at the committee level, in overseeing management of the Company’s risks. The Board regularly reviews information regarding the Company’s credit, liquidity, operations,

12

and enterprise risks. The Company’s Compensation Committee is responsible for overseeing the management of risks relating to the Company’s executive compensation plans and arrangements. The Audit Committee oversees management of financial, accounting and internal control risks. The Nominating and Corporate Governance Committee manages risks associated with the independence of the Board of Directors and potential conflicts of interest. While each committee is responsible for evaluating certain risks and overseeing the management of such risks, the entire Board of Directors is regularly informed through committee reports about such risks. The Board and its committees are committed to ensuring effective risk management oversight and work with management to ensure that effective risk management strategies are incorporated into the Company’s culture and day-to-day business operations.

Board Meetings, Committees and Corporate Governance

The Board of Directors has determined that the Company’s current directors, with the exception of Messrs. Pease and Faith, meet the independence requirements of the Nasdaq Capital Market. No director qualifies as independent unless the Board of Directors determines that the director has no direct or indirect material relationship with the Company. In making the determination that a particular director is independent, the Board considers the relationships that such director has with the Company and all other facts and circumstances deemed relevant in determining their independence, including information requested from and provided by each director concerning his or her background, employment and affiliations, including family relationships and other information received through annual directors’ questionnaires.

It is the policy of the Board of Directors to have a separate meeting time for independent directors. During the last fiscal year, five sessions of the independent directors were held.

The standing committees of the Board of Directors include an Audit Committee, a Compensation Committee, and a Nominating and Corporate Governance Committee.

We have written charters for the Audit Committee, the Compensation Committee, and the Nominating and Corporate Governance Committee, copies of which are available on our website, free of charge, at http://www.quicklogic.com/corporate/about-us/management. You can also obtain copies of the charters, free of charge, by writing to us at 2220 Lundy Avenue, San Jose, California 95131, Attention: Finance Department.

In accordance with applicable SEC requirements and Nasdaq Capital Market listing standards, all the standing committees are comprised solely of non-employee, independent directors. The table below shows current membership for each of the standing committees.

|

Audit Committee |

|

Nominating and Corporate Governance Committee |

|

Compensation Committee |

|

Christine Russell (1)(2) |

|

Michael R. Farese (1)(3) |

|

Gary H. Tauss (1) |

|

Michael R. Farese |

|

Arturo Krueger |

|

Michael R. Farese |

|

Arturo Krueger |

|

Daniel A. Rabinovitsj |

|

Daniel A. Rabinovitsj |

|

|

|

Christine Russell |

|

Christine Russell |

|

|

|

Gary H. Tauss |

|

|

|

(1) |

Committee Chairman |

|

(2) |

Audit Committee Financial Expert |

|

(3) |

Lead Independent Director |

Audit Committee

The Audit Committee held four meetings in 2019. Ms. Russell has served as Chairman of the Audit Committee since April 2006. Dr. Farese and Mr. Krueger have served as members of the Audit Committee since February 2010. Each member meets the independence requirements of the SEC and the Nasdaq Capital Market. The Board of Directors has determined that Ms. Russell is an Audit Committee Financial Expert as defined by Item 407(d)(5) of Regulation S-K.

The Audit Committee has sole and direct authority to select, evaluate and compensate our independent registered public accounting firm, and it reviews and approves in advance all audit, audit related and non-audit

13

services, and the related fees, provided by the independent registered public accounting firm (to the extent those services are permitted by the Securities Exchange Act of 1934, as amended). The Audit Committee meets with our management and appropriate financial personnel regularly to consider the adequacy of our internal controls and financial reporting process and the reliability of our financial reports to the public. The Audit Committee also meets with the independent registered public accounting firm regarding these matters. The Audit Committee has established a Financial Information Integrity Policy, pursuant to which QuickLogic can receive, retain and treat employee complaints concerning questionable accounting, internal control or auditing matters, or the reporting of fraudulent financial information. The Audit Committee examines the independence and performance of our independent registered public accounting firm. In addition, among its other responsibilities, the Audit Committee reviews our critical accounting policies, our annual and quarterly reports on Forms 10-K and 10-Q, and our earnings releases before they are published. The Audit Committee has a written charter, a copy of which is available on our website, free of charge, at http://www.quicklogic.com/corporate/about-us/management.

Compensation Committee

The Compensation Committee held three meetings in 2019 and acted by unanimous written consent two times during the year. Mr. Tauss has served as Chairman of the Compensation Committee since September 2004. Ms. Russell, Dr. Farese and Mr. Rabinovitsj have served as members of the Compensation Committee since February 2010, August 2014, and January 2015, respectively. Each member of the Compensation Committee meets the independence requirements of the SEC and the Nasdaq Capital Market. The purpose of the Compensation Committee is to: (i) discharge the responsibilities of the Board of Directors relating to compensation of the Company’s directors, Chief Executive Officer, and executive officers; (ii) review and recommend to the Board of Directors compensation plans, policies and benefit programs, as well as approve individual executive officer compensation packages; and (iii) review and discuss the Compensation Discussion and Analysis with management and prepare the Compensation Committee Report to be included in the Company’s Proxy Statement and Annual Report on Form 10-K. The Compensation Committee’s duties also include administering QuickLogic’s stock option plans and employee stock purchase plans.

The Compensation Committee has the authority to retain and meet privately with independent advisors and compensation and benefits specialists as needed, and may request the assistance of any director, officer or employee of the Company whose advice and counsel are sought by the Compensation Committee. The Compensation Committee, after reviewing management’s recommendations, determines the equity and non-equity compensation of the Company’s executive officers and directors. Management generally provides internal compensation information, compensation survey information for similarly sized technology companies, and other information to the Compensation Committee, and the Chief Executive Officer recommends compensation amounts for the executive officers other than the Chief Executive Officer. Under the guidance of the Compensation Committee, the Chief Executive Officer or an executive officer of the Company makes recommendations to the Compensation Committee regarding the executive incentive compensation plan, including plan objectives and payments earned based on performance to those objectives. The Compensation Committee may delegate its responsibilities to subcommittees when appropriate. The Compensation Committee has a written charter, which is available on our website, free of charge, at http://www.quicklogic.com/corporate/about-us/management.

Nominating and Corporate Governance Committee

The Nominating and Corporate Governance Committee held one meeting in 2019. Dr. Farese has served as Chairman of the Nominating and Corporate Governance Committee since August 2014. Each of the directors on the Nominating and Corporate Governance Committee meets the independence requirements of the SEC and the Nasdaq Capital Market. The purpose of the Nominating and Corporate Governance Committee is to: (i) assist the Board of Directors by identifying, evaluating and recommending to the Board of Directors, or approving as appropriate, individuals qualified to be directors of QuickLogic for either appointment to the Board of Directors or to stand for election at a meeting of the stockholders; (ii) review the composition and evaluate the performance of the Board of Directors; (iii) review the composition and evaluate the performance of the committees of the Board of Directors; (iv) recommend persons to be members of the committees of the Board of Directors; (v) review conflicts of interest of members of the Board of Directors and executive officers; and (vi) review and recommend corporate governance principles to the Board of Directors. Other duties of the Nominating and Corporate Governance Committee include overseeing the evaluation of management, succession planning, and reviewing and monitoring

14

the Company’s Code of Conduct and Ethics. The Nominating and Corporate Governance Committee adopted our Corporate Governance Guidelines in December 2004. A copy of the Guidelines and a copy of the written charter of the Nominating and Corporate Governance Committee are available on our website, free of charge, at http://www.quicklogic.com/corporate/about-us/management.

The Nominating and Corporate Governance Committee regularly reviews the size and composition of the full Board of Directors and considers the recommendations properly presented by qualified stockholders as well as recommendations from management, other directors and search firms to attract top candidates to serve on the Board of Directors. Except as may be required by rules promulgated by the SEC and the Nasdaq Capital Market, there are no specific, minimum qualifications that must be met by each candidate for the Board of Directors, nor are there specific qualities or skills that are necessary for one or more of the members of the Board of Directors to possess. In evaluating the qualifications of the candidates, the Nominating and Corporate Governance Committee considers many factors, including character, judgment, independence, expertise, length of service and other commitments, among others. Although the Nominating and Corporate Governance Committee does not have a formal policy with respect to diversity, the Nominating and Corporate Governance Committee does consider diversity when identifying director candidates and nominees with respect to differences of viewpoints, professional experiences, race, gender, and other individual qualities and attributes that contribute to heterogeneity on the Board. The Committee evaluates such factors and does not assign any particular weight or priority to any of these factors. While the Nominating and Corporate Governance Committee has not established specific minimum qualifications for director candidates, the Nominating and Corporate Governance Committee believes that candidates and nominees must reflect a Board of Directors that is predominantly independent and is comprised of directors who (i) are of high integrity, (ii) have qualifications that will increase the overall effectiveness of the Board of Directors, and (iii) meet other requirements as may be required by applicable rules, such as financial literacy or financial expertise with respect to Audit Committee members.

It is the policy of the Nominating and Corporate Governance Committee to consider recommendations for candidates to the Board of Directors from stockholders holding, continuously for at least one year prior to the date of the submission of the recommendation, either (i) shares of the outstanding voting securities of the Company in an amount equal to at least $2,000 in market value or (ii) 1% of the Company’s outstanding voting securities. Recommendations received after the date that is 120 days prior to the one year anniversary of the mailing of the previous year’s proxy statement, will likely not be considered timely for consideration at that year’s annual meeting. Stockholders may suggest qualified candidates for director by writing to the Nominating and Corporate Governance Committee, care of the Chief Financial Officer, 2220 Lundy Avenue, San Jose, California 95131 and must include the candidate’s name, home and business contact information, detailed biographical data and qualifications and an explanation of the reasons why the stockholder believes this candidate is qualified for service on QuickLogic’s Board of Directors. The stockholder must also provide such other information about the candidate that would be required by the SEC rules to be included in a proxy statement. In addition, the stockholder must include the consent of the candidate and describe any arrangements or undertakings between the stockholder and the candidate regarding the nomination. The Nominating and Corporate Governance Committee will evaluate all director nominations that are timely and properly submitted by stockholders on the same basis as any other candidate. Our Nominating and Corporate Governance Committee’s Policies and Procedures for Director Candidates is posted on our website at http://www.quicklogic.com/corporate/about-us/management.

During 2019, activities of the Nominating and Corporate Governance Committee included reviewing and approving any actual or potential conflicts of interest, assessing the structure and performance of the Board and the committees of the Board, and reviewing our Code of Conduct and Ethics and our Policy for Stockholder Communications with Directors. The Nominating and Corporate Governance Committee also assessed the independence and qualifications of our directors, reviewed the performance of the CEO and his assessment of our executive officers, and ensured our directors adhered to our Corporate Governance Guidelines, including reviewing, monitoring and, where appropriate, approving fundamental financial and business strategies and major corporate actions. A copy of the Code of Conduct and Ethics and a copy of the Policy for Stockholder Communications with Directors are posted on our website at http://www.quicklogic.com/corporate/about-us/management.

Non-Standing Committees and Participation

The Board of Directors has delegated to the Equity Incentive Committee, which currently consists of Brian C. Faith, our President and Chief Executive Officer and Suping (Sue) Cheung, our Chief Financial Officer, the authority to: (i) approve the grant of options to purchase Company stock to employees other than executive officers

15

and certain other individuals, up to a limit of 40,000 shares per option grant; (ii) approve the award of restricted stock units (RSUs) based on dollar value maximums in accordance with guidelines established by Radford Consulting up to a maximum dollar value of $100,000 for the top non-executive job level; (iii) grant refresh options or RSUs to employees other than executive officers and certain other individuals, subject to the approval of the total number of such refresh options or RSUs by the Board of Directors or the Compensation Committee; and (iv) amend options as authorized by the Board of Directors.

The Board of Directors held a total of five meetings and acted by unanimous written consent two times during 2019. During 2019, no incumbent director attended fewer than 75% of the aggregate of (i) the total number of meetings of the Board of Directors held during his or her term as a director and (ii) the total number of meetings held by all committees of the Board of Directors on which such director served during his or her term on such committee.

QuickLogic expects its directors to attend its annual meetings absent a valid reason. All then-current directors attended the April 24, 2019 Annual Meeting of Stockholders.

Stockholder Communications with the Board of Directors

The Nominating and Corporate Governance Committee has established a policy for stockholder communication with our Board of Directors. This policy, which is available on the investor relations portion of our website, provides a process for stockholders to send communications to the Board of Directors. Stockholders may contact QuickLogic’s Board of Directors or any individual thereof, by writing, whether by mail or express mail, to: QuickLogic Corporation Board of Directors, 2220 Lundy Avenue, San Jose, California 95131. Communications received in writing are reviewed internally by management and then distributed to the Chairman, Lead Independent Director or other members of the Board, as appropriate. Stockholders who wish to contact the Board of Directors or any member of the Audit Committee to report questionable accounting or auditing matters may do so by using this address and designating the communication as “Compliance Confidential.”

Code of Conduct and Ethics

QuickLogic adopted a Code of Conduct and Ethics applicable to all directors, officers and employees on February 12, 2004. The Code of Conduct and Ethics covers topics including, but not limited to, financial reporting, conflicts of interest, confidentiality of information, compliance with laws and regulations and the code of ethics for our Chief Executive Officer, Chief Financial Officer and controllers. A copy of the Code of Conduct and Ethics, as amended, is posted on our website at http://www.quicklogic.com/corporate/management. To date, there have been no waivers under our Code of Conduct and Ethics. We will post any waivers, if and when granted, on our website at http://www.quicklogic.com/corporate/about-us/management.

Compensation Committee Interlocks and Insider Participation

During fiscal year 2019, the following directors were members of QuickLogic’s Compensation Committee: Gary H. Tauss (Chairman), Michael R. Farese, Daniel A. Rabinovitsj, and Christine Russell. None of the Compensation Committee’s members has at any time been an officer or employee of QuickLogic.

None of QuickLogic’s named executive officers serve, or in the past fiscal year have served, as a member of the board of directors or compensation committee of any entity that has one or more of its executive officers serving on QuickLogic’s Board or Compensation Committee and none have engaged in any transaction with related persons, promotors or certain control persons requiring disclosure under Item 404 of Regulation S-K.

16

APPROVAL OF AMENDMENT OF THE COMPANY’S 2009 EMPLOYEE STOCK PURCHASE PLAN

Summary

Our Board is requesting that our stockholders approve certain amendments (the “ESPP Amendment”) to our 2009 Employee Stock Purchase Plan (the “2009 ESPP”), adopted by the Board on March 6, 2019 and March 9, 2020, subject to stockholder approval. The ESPP Amendment (i) extends the term of the 2009 ESPP by ten (10) years until March 5, 2029 and (ii) increases the number of shares reserved for issuance under the 2009 ESPP by 300,000 shares, from 342,857 to 642,857 shares.

As of February 24, 2020, there were 62,335 shares available for use in connection with future awards under our 2009 ESPP. If the stockholders approve the ESPP Amendment, it will be effective as of the date of the Annual Meeting. In the event stockholders do not approve the proposed ESPP Amendment, the 2009 ESPP will terminate and no more shares will be available for purchase under the 2009 ESPP. However, this could limit our ability to successfully attract and retain highly skilled personnel. The Board has determined that it is in the best interests of the Company and its stockholders to have our 2009 ESPP amended by the ESPP Amendment and is asking the Company’s stockholders to approve the ESPP Amendment.

The Company’s executive officers have an interest in this proposal.

Reasons for Voting for Amendment to 2009 ESPP

ESPP is Valuable for Attracting and Retaining Talented Employees. The 2009 ESPP allows our employees to buy our shares at a discount through payroll deductions. In the highly competitive technology industry in which we compete for talent, we believe that offering an employee stock purchase program is critical to our ability to be competitive. If the proposed ESPP Amendment is not approved by the Company’s stockholders, we may be restricted in our ability to offer competitive compensation to existing employees and qualified candidates, and our business could be adversely affected.

Key Considerations for Requesting Additional Shares. In determining the increase to the share reserve under the 2009 ESPP, the Board reviewed the number of shares currently available for grant. As of February 24, 2020, there were 62,335 shares available for use in connection with future awards under our 2009 ESPP. We believe that the number of shares remaining available for issuance under the 2009 ESPP will not be sufficient for the expected levels of participation in the 2009 ESPP, and therefore may not meet the goals of our compensation structure and strategy.

The approval of the ESPP Amendment requires the affirmative vote of a majority of the shares of QuickLogic common stock present in person or represented by proxy and entitled to vote on the proposal at the Annual Meeting.

Recommendation of the Board of Directors

THE BOARD OF DIRECTORS UNANIMOUSLY RECOMMENDS THAT STOCKHOLDERS VOTE "FOR" THE AMENDMENT OF THE QUICKLOGIC CORPORATION 2009 EMPLOYEE STOCK PURCHASE PLAN.

Summary of the 2009 Employee Stock Purchase Plan

The following is a summary of the principal features of the 2009 ESPP and its operation. The summary is qualified in its entirety by reference to the 2009 ESPP as set forth in Appendix A.

17

General. The 2009 ESPP was adopted in 2009. The purpose of the 2009 ESPP is to provide eligible employees of the Company and its designated subsidiaries with an opportunity to purchase shares of the Company’s common stock through payroll deductions, to enhance the employees’ sense of participation in the Company and its participating subsidiaries, and to provide an incentive for continued employment.

Shares Authorized for Issuance. The maximum number of shares of Common Stock that have been authorized for purchases under the 2009 ESPP is 342,857, which will be increased to 642,857 if Proposal Two is approved.

Administration. The 2009 ESPP is administered by the Board or a committee of the Board appointed by the Board (in either case, the “Administrator”). Subject to the provisions of the 2009 ESPP, all questions of interpretation or application of the 2009 ESPP are determined by the Administrator and its decisions are final and binding upon all participants.

Eligibility. Each of the Company’s (or the Company’s participating subsidiaries) employees who are common law employees of the Company or a participating subsidiary on the first trading day of the applicable offering period and whose customary employment with the Company or one of the Company’s participating subsidiaries is at least 20 hours per week and more than 5 months in a calendar year is eligible to participate in the 2009 ESPP with respect to such offering period; except that no employee will be granted an option to purchase stock under the 2009 ESPP (i) to the extent that, immediately after the grant, such employee would own 5% or more of the total combined voting power of all classes of the Company’s capital stock or the capital stock of any Company parent or subsidiary, or (ii) to the extent that his or her rights to purchase stock under all of the Company’s employee stock purchase plans accrues at a rate which exceeds $25,000 worth of stock (determined at the fair market value of the shares at the time such option is granted) for each calendar year in which such option is outstanding. As of February 28, 2020, because there were no offerings outstanding under the 2009 ESPP, none of the employees were participating in the 2009 ESPP as of such date.

Offering Period. Each offering period under the 2009 ESPP will have a duration of approximately 6 months, commencing on the first trading day on or after May 15 and November 15 of each year and terminating on the last trading day of the applicable period ending 6 months later. During each offering period, shares of Common Stock may be purchased on behalf of the participant in accordance with the terms of the 2009 ESPP.

Eligible employees may participate in the 2009 ESPP by (i) delivering a subscription agreement in a form determined by the Administrator, or (ii) following an electronic or other enrollment procedure prior to the first trading day of each offering period (the “enrollment date”) authorizing payroll deductions pursuant to the 2009 ESPP. Such payroll deductions may not exceed 20% of the compensation a participant receives on each pay day during the offering period. For purposes of the 2009 ESPP, “compensation” means an employee’s base straight time gross earnings, overtime and incentive/variable compensation, but exclusive of bonuses and other compensation. Once an employee becomes a participant in the 2009 ESPP, the employee automatically will participate in each successive offering period at the same rate of contribution until the employee withdraws from the 2009 ESPP or the employee’s employment with the Company or one of the Company’s participating subsidiaries terminates. On the first trading day of each offering period (the “enrollment date”), each participant automatically is granted an option to purchase shares of Common Stock. The option is exercised on the last trading day of an offering period to the extent of the payroll deductions accumulated during such offering period.

Purchase Price. The Administrator has the discretion to implement one of two types of offering periods to determine the purchase price: (i) an offering period with a purchase price equal to 85% of the fair market value of the Common Stock on the last day of the offering period (a “Purchase Date Offering Period”) or (ii) an offering period with a purchase price equal to 85% of the fair market value of the Common Stock on (x) the enrollment date, or (y) the last day of the offering period, whichever is lower (a “Look-Back Offering Period”). The purchase price for subsequent offering periods may be determined by the Administrator, subject to compliance with the Code and the terms of the 2009 ESPP.

Payment of Purchase Price. The purchase price of the shares is accumulated by payroll deductions made during each offering period. The number of whole shares that a participant may purchase in each offering period will be determined by dividing the total amount of payroll deductions withheld from the participant’s compensation

18

during that offering period by the purchase price; provided, however, that in no event will a participant be permitted to purchase during each offering period more than 1,428 shares, subject to automatic adjustment upon certain changes in capitalization. No fractional shares will be purchased under the 2009 ESPP and any payroll deductions accumulated in a participant’s account which are not sufficient to purchase a full share will be retained in a participant’s account for the subsequent offering period.

Payroll Deductions. All payroll deductions made for a participant are credited to the participant’s account under the 2009 ESPP, are withheld in whole percentages only, and are included with the Company’s general funds. Funds received by the Company pursuant to exercises under the 2009 ESPP may be used for general corporate purposes. A participant may not make any additional payments into his or her account under the 2009 ESPP other than through payroll deductions.

Withdrawal. A participant may withdraw all but not less than all of his or her payroll deductions from an offering period prior to the end of such offering period by (i) delivering a written notice of withdrawal to the Company’s payroll office on a form provided by the Company for such purpose or (ii) following an electronic or other withdrawal procedures. A participant’s withdrawal from the 2009 ESPP will not affect his or her eligibility to participate in future offering periods. Once a participant withdraws from a particular offering period, however, that participant may not participate again in the same offering period. To participate in a subsequent offering period, the participant must re-enroll in the 2009 ESPP in accordance with the 2009 ESPP enrollment procedures; payroll deductions will not resume at the beginning of the succeeding offering period unless the employee re-enrolls in the 2009 ESPP.

Termination of Employment. Upon termination of a participant’s employment for any reason, his or her participation in the 2009 ESPP will immediately terminate and the payroll deductions credited to the participant’s account will be returned to him or her and such participant’s option will automatically terminate.

Changes in Capitalization. In the event any dividend or other distribution (whether in the form of cash, shares, or other securities or other property), recapitalization, stock split, reverse stock split, reorganization, merger, consolidation, split-up, spin-off, combination, repurchase, or exchange of shares or other securities of the Company, or other similar change in the corporate structure of the Company affecting the shares occurs, the number and class of shares of Common Stock deliverable under the 2009 ESPP, the purchase price per share and the number of shares covered by each option under the 2009 ESPP which has not been exercised, and the numerical limits under the 2009 ESPP will be proportionately and automatically adjusted.

Dissolution or Liquidation. In the event of the Company’s proposed dissolution or liquidation, the offering period will be shortened by setting a new exercise date and the 2009 ESPP will terminate immediately prior to such proposed dissolution or liquidation, unless otherwise provided by the Board. The Board will notify each participant in writing at least 10 business days prior to the new exercise date that the purchase date for the participant’s option has been changed to the new exercise date and that the participant’s option will be exercised automatically on the new exercise date unless the participant withdraws from the 2009 ESPP prior to such date.

Merger or Asset Sale. In the event of a proposed sale of all or substantially all of the assets of the Company, or the merger of the Company with or into another corporation, each outstanding option under the 2009 ESPP will be assumed or an equivalent option will be substituted by the successor corporation or a parent or subsidiary of such successor corporation. In the event the successor corporation refuses to assume or substitute for the options, any offering period then in progress will be shortened by setting a new exercise date on which such offering period will end. The new exercise date will be prior to the proposed sale or merger. The Board will notify each participant in writing at least 10 business days prior to the new exercise date that the purchase date for the participant’s option has been changed to the new exercise date and that the participant’s option will be exercised automatically on the new exercise date unless the participant withdraws from the 2009 ESPP prior to such date.

Amendment and Termination of the 2009 ESPP. The Board may amend, terminate or suspend the 2009 ESPP at any time and for any reason. If the 2009 ESPP is terminated, the Board, in its sole discretion, may elect to terminate all outstanding offering periods either immediately or upon completion of the purchase of shares on the next exercise date (which may be sooner than originally scheduled, if determined by the Board in its discretion) or may elect to permit offering periods to expire in accordance with their terms. If the offering periods are terminated

19

prior to expiration, all amounts then-credited to participants’ accounts which have not been used to purchase shares will be returned to participants as soon as administratively practicable.

Without stockholder consent, the Administrator is entitled to change the offering periods, limit the frequency and/or number of changes in the amount withheld during an offering period, establish the exchange ratio applicable to amounts withheld in a currency other than U.S. dollars, permit payroll withholding in excess of the amount designated by a participant in order to adjust for delays or mistakes in the Company’s processing of properly completed withholding elections, establish reasonable waiting and adjustment periods and/or accounting and crediting procedures to ensure that amounts applied toward the purchase of shares for each participant properly correspond with amounts withheld from the participant’s compensation, and establish such other limitations or procedures as the Administrator determines in its sole discretion advisable which are consistent with the 2009 ESPP.

The 2009 ESPP will continue until the earlier to occur of (i) the termination of the 2009 ESPP by the Board, or (ii) March 5, 2029 (the date which is 10 years from the adoption of the latest amendment to the 2009 ESPP by the Board).

Number of Shares Purchased by Employees

Participation in the 2009 ESPP is voluntary and is dependent on each eligible employee’s election to participate and his or her determination as to the level of payroll deductions. Accordingly, future purchases under the 2009 ESPP are not determinable. Non-employee directors are not eligible to participate in the 2009 ESPP. The following table sets forth the number of shares of our Common Stock that were purchased under the 2009 ESPP since its adoption.

|

Name of Individual or Group |

|

Number of shares purchased |

|

|

|

Brian C. Faith (CEO) |

|

|

- |

|

|

Sue Cheung (CFO) |

|

|

2,167 |

|

|

Timothy Saxe (CTO) |

|

|

7,285 |

|

|

All executive officers, as a group |

|

|

9,452 |

|

|

All non-executive directors, as a group (1) |

|

|

2,294 |

|

|

|

|

268,777 |

|

|

_________________

|

1) |

Thomas Hart, former Chairman and Director purchased 2,294 shares when he was chief executive officer. |

Certain U.S. Federal Income Tax Information